Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - FRANKLIN ELECTRIC CO INC | a20161231ex991.htm |

| EX-32.2 - EXHIBIT 32.2 - FRANKLIN ELECTRIC CO INC | a20161231ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - FRANKLIN ELECTRIC CO INC | a20161231ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - FRANKLIN ELECTRIC CO INC | a20161231ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - FRANKLIN ELECTRIC CO INC | a20161231ex311.htm |

| EX-23.1 - EXHIBIT 23.1 - FRANKLIN ELECTRIC CO INC | a20161231ex231.htm |

| EX-21 - EXHIBIT 21 - FRANKLIN ELECTRIC CO INC | a20161231ex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________

FORM 10-K

_________

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____

Commission file number 0-362

FRANKLIN ELECTRIC CO., INC.

(Exact name of registrant as specified in its charter)

Indiana | 35-0827455 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

9255 Coverdale Road | ||

Fort Wayne, Indiana | 46809 | |

(Address of principal executive offices) | (Zip Code) | |

(260) 824-2900

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.10 par value | NASDAQ Global Select Market | |

(Title of each class) | (Name of each exchange on which registered) | |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of each class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES o | NO x |

1

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

YES o | NO x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

YES x | NO o |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

YES x | NO o |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer x | Accelerated Filer o | Non-Accelerated Filer o | Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

YES o | NO x |

The aggregate market value of the registrant's common stock held by non-affiliates of the registrant at July 1, 2016 (the last business day of the registrant’s most recently completed second quarter) was $1,527,181,567. The stock price used in this computation was the last sales price on that date, as reported by NASDAQ Global Select Market. For purposes of this calculation, the registrant has excluded shares held by executive officers and directors of the registrant, including restricted shares and except for shares owned by the executive officers through the registrant's 401(k) Plan. Determination of stock ownership by non-affiliates was made solely for the purpose of responding to this requirement and the registrant is not bound by this determination for any other purpose.

Number of shares of common stock outstanding at February 15, 2017:

46,382,586 shares

DOCUMENTS INCORPORATED BY REFERENCE

A portion of the Proxy Statement for the Annual Meeting of Shareholders to be held on May 5, 2017 (Part III).

2

FRANKLIN ELECTRIC CO., INC.

TABLE OF CONTENTS

Page | |||

PART I. | Number | ||

Item 1. | |||

Item 1A. | |||

Item 1B. | |||

Item 2. | |||

PART II. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A. | |||

Item 8. | |||

Item 9. | |||

Item 9A. | |||

Item 9B. | |||

PART III. | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

PART IV. | |||

Item 15. | |||

3

PART I

ITEM 1. BUSINESS

Description of the Business

Franklin Electric Co., Inc. (“Franklin Electric” or the “Company”) is an Indiana corporation founded in 1944 and incorporated in 1946. Named after America’s pioneer electrical engineer, Benjamin Franklin, Franklin Electric manufactured the first water-lubricated submersible motor for water systems, and the first submersible motor for fueling systems. With 2016 revenue of $949.9 million and approximately 5,200 employees, today the Company designs, manufactures and distributes water and fuel pumping systems, composed primarily of submersible motors, pumps, electronic controls and related parts and equipment.

The Company’s water pumping systems move fresh and waste water for the housing, agriculture, and other industrial end markets. With a growing global footprint, the Company has also evolved into being a top supplier of submersible fueling systems at gas stations, making pumps, pipes, electronic controls, and monitoring devices. Fuel pumping systems account for the balance of the Company’s revenues.

The Company's products are sold worldwide by its employee sales force and independent manufacturing representatives. The Company offers normal and customary trade terms to its customers, no significant part of which is of an extended nature. Special inventory requirements are not necessary, and customer merchandise return rights do not extend beyond normal warranty provisions.

Franklin Electric’s Key Factors for Success

While maintaining a culture of safety and lean principals, Franklin Electric promises to deliver quality, availability, service, innovation, and value in every encounter the Company has with stakeholders, including direct or indirect customers, employees, shareholders, and suppliers. These key factors for success are a roadmap to ensure the Company consistently offers the best value to its customer.

Markets and Applications

The Company's business consists of two reporting segments based on the principal end market served: the Water Systems segment and the Fueling Systems segment. The Company includes unallocated corporate expenses in an “Other” segment that, together with the Water Systems and Fueling Systems segments, represent the Company. Segment and geographic information appears in Note 16, “Segment and Geographic Information” to the consolidated financial statements.

The market for the Company's products is highly competitive and includes diversified accounts by size and type. The Company's Water Systems and Fueling Systems products and related equipment are sold to specialty distributors and some original equipment manufacturers (“OEMs”), as well as industrial and petroleum equipment distributors and major oil and utility companies.

Water Systems Segment

Water Systems is a global leader in the production and marketing of water pumping systems and is a technical leader in submersible motors, pumps, drives, electronic controls, and monitoring devices. The Water Systems segment designs, manufactures and sells motors, pumps, electronic controls and related parts and equipment primarily for use in groundwater, wastewater, and fuel transfer applications.

Water Systems motors and pumps are used principally for pumping clean water and wastewater in a variety of residential, agricultural, and industrial applications. Water Systems also manufactures electronic drives and controls for the motors which control functionality and provide protection from various hazards, such as electric surges, over-heating, or dry wells or tanks.

The Water Systems business has grown from a domestic submersible motor manufacturer to a global manufacturer of systems and components for the movement of water and automotive fuels. Founded in the 1940s, the Company made submersible motors for pumps for much of its history. About 10 years ago, it entered the pump business, and has since grown through acquisitions. Highlights of the Water Systems business transformation, from its origins to the present, are as follows:

• | 1950s - Domestic submersible motor manufacturer |

• | 1990s - Global manufacturer of submersible motors, electronic drives and controls selling to pump OEMs |

• | 2004 - Began to change the business model to include pumps and sell directly to wholesale distributors |

• | 2006 - Added adjacent pumping systems, acquired Little Giant Pump Company, United States |

• | 2007 - Expanded globally, acquired Pump Brands (Pty) Limited, South Africa |

4

• | 2008 - Continued global expansion, acquired Industrias Schneider SA, Brazil |

• | 2009 - International acquisition, Vertical, S.p.A., Italy |

• | 2011 - International acquisition, Impo Motor Pompa Sanayi ve Ticaret A.S., Turkey |

• | 2012 - Acquired majority interest, 70.5%, in mobile pumping systems company, Pioneer Pump Holdings, Inc. ("PPH"), a United States company with subsidiaries in the United Kingdom and South Africa |

• | 2014 - International acquisitions, Bombas Leao S.A., Brazil and majority interest, 70%, of Pluga Pumps and Motors Private Limited, India |

• | 2015 - Acquired remaining 29.5% noncontrolling interest of PPH |

Water Systems products are sold in highly competitive markets. Water-pumping systems contribute about 75 to 80 percent of revenue. Significant portions of segment revenue come from selling groundwater and surface pumps to residential and commercial buildings, as well as agricultural sales which are more seasonal and subject to commodity price changes. The Water segment generates 40 percent of its revenue in developing markets, which often lack municipal water systems. As those countries bring systems up to date, the Company views those markets as an opportunity. The Company has had 15 to 20 percent compounded annual sales growth in those regions in recent years. Water Systems competes in each of its targeted markets based on product design, quality of products and services, performance, availability, and price. The Company's principal competitors in the specialty water products industry are Grundfos Management A/S, Pentair, Inc., and Xylem, Inc.

2016 Water Systems research and development expenditures were primarily related to the following activities:

• | Electronic drives and controls for submersible pumping, above-ground pumping, and HVAC applications |

• | Solar pumping technology, including new models and new accessories for the Fhoton™ Solar Pumping Systems |

• | Submersible and surface pumps for agricultural and municipal applications |

• | Gray water pumping equipment, including the redesigned PowerSewer™ Systems and the IGPDS series dual seal grinder pumps |

• | Condensate removal pumps, including the VCC-20-P designed for use in plenum applications |

• | Submersible motor technology and motor protection, including ultra-efficient permanent magnet motors |

• | Artificial Lift systems for gas well dewatering and oil pumping, including new pump shrouds, abrasion resistant pump geometries, pumps for improved oil handling, and drives for deeper set pumps |

Fueling Systems Segment

Fueling Systems is a global leader in the production and marketing of fuel pumping systems, fuel containment systems, and monitoring and control systems. The Fueling Systems segment designs, manufactures and sells pumps, pipe, sumps, fittings, vapor recovery components, electronic controls, monitoring devices and related parts and equipment primarily for use in submersible fueling system applications.

Fueling Systems has expanded its product offerings through internal development and acquisitions. Highlights of the Fueling Systems history are as follows:

• | 1990s - Domestic manufacturer of submersible turbine pumping systems |

• | 2000 - Acquired Advanced Polymer Technology, Inc., a manufacturer of underground pipe for fueling applications, and EBW, Inc., a manufacturer and distributor of fueling hardware components |

• | 2006 - Acquired Healy Systems, Inc., a manufacturer of fueling nozzles and vapor recovery systems |

• | 2010 - Acquired PetroTechnik Limited, a United Kingdom distributor that designs and sources flexible and lightweight underground pipe |

• | 2012 - Acquired Flexing, Inc., a manufacturer of fueling equipment including stainless steel flexible hose connectors |

• | 2014 - Acquired majority interest, 65%, in Wadcorpp India Private Limited, India, a distributor of fueling equipment |

Fueling Systems products are sold in highly competitive markets. Rising car use is leading to more investment in gas stations which, in turn, leads to increased demand for the Company’s Fueling Systems products. The Company believes there is growth opportunity in developing markets and, accordingly, acquired an investment in India in 2014. Fueling Systems competes in each of its targeted markets based on product design, quality of products and services, performance, availability, and price. The Company's principal competitors in the petroleum equipment industry are Danaher Corporation and Dover Corporation.

2016 Fueling Systems research and development expenditures were primarily related to the following activities:

• | Development of a new automatic tank gauge platform |

• | Development of a pumping system for alternative fuels |

5

• | Development of new fuel dispensing nozzles |

• | Software enhancements to automatic tank gauges |

Information Regarding All Reportable Segments

Research and Development

The Company incurred research and development expense as follows:

(In millions) | 2016 | 2015 | 2014 | ||||||||

Research and development expense | $ | 21.5 | $ | 18.4 | $ | 19.3 | |||||

Expenses incurred were for activities related to the development of new products, improvement of existing products and manufacturing methods, and other applied research and development.

The Company owns a number of patents, trademarks, and licenses. In the aggregate, these patents are of material importance to the operation of the business; however, the Company believes that its operations are not dependent on any single patent or group of patents.

Raw Materials

The principal raw materials used in the manufacture of the Company’s products are coil and bar steel, stainless steel, copper wire, and aluminum ingot. Major components are electric motors, capacitors, motor protectors, forgings, gray iron castings, plastic resins, and bearings. Most of these raw materials are available from multiple sources in the United States and world markets. Generally, the Company believes that adequate alternative sources are available for the majority of its key raw material and purchased component needs; however, the Company is dependent on a single or limited number of suppliers for certain materials or components. Availability of fuel and energy is adequate to satisfy current and projected overall operations unless interrupted by government direction or allocation.

Major Customers

No single customer accounted for over 10 percent of net sales in 2016, 2015, or 2014. No single customer accounted for over 10 percent of gross accounts receivable in 2016 and 2015.

Backlog

The dollar amount of backlog by segment was as follows:

(In millions) | February 15, 2017 | February 17, 2016 | |||||

Water Systems | $ | 39.4 | $ | 44.4 | |||

Fueling Systems | 25.2 | 15.0 | |||||

Consolidated | $ | 64.6 | $ | 59.4 | |||

The backlog is composed of written orders at prices adjustable on a price-at-the-time-of-shipment basis for products, primarily standard catalog items. All backlog orders are expected to be filled in fiscal 2017. The Company’s sales in the first quarter are generally less than its sales in other quarters due to generally less water well drilling and overall product sales during the winter months in the Northern hemisphere. Beyond that, there is no seasonal pattern to the backlog and the backlog has not proven to be a significant indicator of future sales.

Environmental Matters

The Company believes that it is in compliance with all applicable federal, state, and local laws concerning the discharge of material into the environment, or otherwise relating to the protection of the environment. The Company has not experienced any material costs in connection with environmental compliance, and does not believe that such compliance will have any material effect upon the financial position, results of operations, cash flows, or competitive position of the Company.

Available Information

The Company’s website address is www.franklin-electric.com. The Company makes available free of charge on or through its website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports, as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and

6

Exchange Commission. Additionally, the Company’s website includes the Company’s corporate governance guidelines, its Board committee charters, and the Company’s code of business conduct and ethics. Information contained on the Company’s website is not part of this annual report on Form 10-K.

ITEM 1A. RISK FACTORS

The following describes the principal risks affecting the Company and its business. Additional risks and uncertainties, not presently known to the Company, could negatively impact the Company’s results of operations or financial condition in the future.

Risks Related to the Industry

Reduced housing starts adversely affect demand for the Company’s products, thereby reducing revenues and earnings. Demand for certain Company products is affected by housing starts. Variation in housing starts due to economic volatility both within the United States and globally could adversely impact gross margins and operating results.

The Company's results may be adversely affected by global macroeconomic supply and demand conditions related to the energy and mining industries. The energy and mining industries are users of the Company's products, including the coal, iron ore, gold, copper, oil, and natural gas industries. Decisions to purchase the Company's products are dependent upon the performance of the industries in which our customers operate. If demand or output in these industries increases, the demand for our products will generally increase. Likewise, if demand or output in these industries declines, the demand for our products will generally decrease. The energy and mining industries' demand and output are impacted by the prices of commodities in these industries which are frequently volatile and change in response to general economic conditions, economic growth, commodity inventories, and any disruptions in production or distribution. Changes in these conditions could adversely impact sales, gross margin, and operating results.

Risks Related to the Business

The Company is exposed to political, economic and other risks that arise from operating a multinational business. The Company has significant operations outside the United States, including Europe, South Africa, Brazil, Mexico, India, China, and Turkey. Further, the Company obtains raw materials and finished goods from foreign suppliers. Accordingly, the Company’s business is subject to political, economic, and other risks that are inherent in operating a multinational business. These risks include, but are not limited to, the following:

• | Difficulty in enforcing agreements and collecting receivables through foreign legal systems |

• | Trade protection measures and import or export licensing requirements |

• | Inability to obtain raw materials and finished goods in a timely manner from foreign suppliers |

• | Imposition of tariffs, exchange controls or other restrictions |

• | Difficulty in staffing and managing widespread operations and the application of foreign labor regulations |

• | Compliance with foreign laws and regulations |

• | Changes in general economic and political conditions in countries where the Company operates |

Additionally, the Company’s operations outside the United States could be negatively impacted by changes in treaties, agreements, policies, and laws implemented by the United States.

If the Company does not anticipate and effectively manage these risks, these factors may have a material adverse impact on its international operations or on the business as a whole.

The Company’s acquisition strategy entails expense, integration risks, and other risks that could affect the Company’s earnings and financial condition. One of the Company’s continuing strategies is to increase revenues and expand market share through acquisitions that will provide complementary Water and Fueling Systems products, add to the Company's global reach, or both. The Company spends significant time and effort expanding existing businesses through identifying, pursuing, completing, and integrating acquisitions, which generate expense whether or not the acquisitions are actually completed. Competition for acquisition candidates may limit the number of opportunities and may result in higher acquisition prices. There is uncertainty related to successfully acquiring, integrating and profitably managing additional businesses without substantial costs, delays or other problems. There can also be no assurance that acquired companies will achieve revenues, profitability or cash flows that justify the investment in them. Failure to manage or mitigate these risks could adversely affect the Company’s results of operations and financial condition.

7

The Company’s products are sold in highly competitive markets, by numerous competitors whose actions could negatively impact sales volume, pricing and profitability. The Company is a global leader in the production and marketing of groundwater and fuel pumping systems. End user demand, distribution relationships, industry consolidation, new product capabilities of the Company’s competitors or new competitors, and many other factors contribute to a highly competitive environment. Additionally, some of the Company’s competitors have substantially greater financial resources than the Company. Although the Company believes that consistency of product quality, timeliness of delivery, service, and continued product innovation, as well as price, are principal factors considered by customers in selecting suppliers, competitive factors previously described may lead to declines in sales or in the prices of the Company’s products which could have an adverse impact on its results of operations and financial condition.

The Company's products are sold to numerous distribution outlets based on market performance. The Company may, from time to time, change distribution outlets in certain markets based on market share and growth. These changes could adversely impact sales and operating results.

Increases in the prices of raw materials, components, finished goods and other commodities could adversely affect operations. The Company purchases most of the raw materials for its products on the open market and relies on third parties for the sourcing of certain finished goods. Accordingly, the cost of its products may be affected by changes in the market price of raw materials, sourced components, or finished goods. The Company and its suppliers also use natural gas and electricity in manufacturing products and natural gas and electricity prices have historically been volatile. The Company does not generally engage in commodity hedging for raw materials and energy. Significant increases in the prices of commodities, sourced components, finished goods, energy or other commodities could cause product prices to increase, which may reduce demand for products or make the Company more susceptible to competition. Furthermore, in the event the Company is unable to pass along increases in operating costs to its customers, margins and profitability may be adversely affected.

Transferring operations of the Company to lower cost regions may not result in the intended cost benefits. The Company is continuing its rationalization of manufacturing capacity between all existing manufacturing facilities and the manufacturing complexes in lower cost regions. To implement this strategy, the Company must complete the transfer of assets and intellectual property between operations. Each of these transfers involves the risk of disruption to the Company’s manufacturing capability, supply chain, and, ultimately, to the Company’s ability to service customers and generate revenues and profits and may include significant severance amounts.

The Company has significant investments in foreign entities and has significant sales and purchases in foreign denominated currencies creating exposure to foreign currency exchange rate fluctuations. The Company has significant investments outside the United States, including Europe, South Africa, Brazil, Mexico, India, China, and Turkey. Further, the Company has sales and makes purchases of raw materials and finished goods in foreign denominated currencies. Accordingly, the Company has exposure to fluctuations in foreign currency exchange rates relative to the U.S. dollar. Foreign currency exchange rate risk is partially mitigated through several means: maintenance of local production facilities in the markets served, invoicing of customers in the same currency as the source of the products, prompt settlement of inter-company balances, limited use of foreign currency denominated debt, and application of derivative instruments when appropriate. To the extent that these mitigating strategies are not successful, foreign currency rate fluctuations can have a material adverse impact on the Company's international operations or on the business as a whole.

Delays in introducing new products or the inability to achieve or maintain market acceptance with existing or new products may cause the Company’s revenues to decrease. The industries to which the Company belongs are characterized by intense competition, changes in end-user requirements, and evolving product offerings and introductions. The Company believes future success will depend, in part, on the ability to anticipate and adapt to these factors and offer, on a timely basis, products that meet customer demands. Failure to successfully develop new and innovative products or to enhance existing products could result in the loss of existing customers to competitors or the inability to attract new business, either of which may adversely affect the Company’s revenues.

Certain Company products are subject to regulation and government performance requirements in addition to the warranties provided by the Company. The Company’s product lines have expanded significantly and certain products are subject to government regulations and standards for manufacture, assembly, and performance in addition to the warranties provided by the Company. The Company’s failure to meet all such standards or perform in accordance with warranties could result in significant warranty or repair costs, lost sales and profits, damage to the Company’s reputation, fines or penalties from governmental organizations, and increased litigation exposure. Changes to these regulations or standards may require the Company to modify its business objectives and incur additional costs to comply, and any liabilities or penalties actually incurred could have a material adverse effect on the Company's earnings and operating results.

8

The growth of municipal water systems and increased government restrictions on groundwater pumping could reduce demand for private water wells and the Company’s products, thereby reducing revenues and earnings. Demand for certain Company products is affected by rural communities shifting from private and individual water well systems to city or municipal water systems. Many economic and other factors outside the Company’s control, including Federal and State regulations on water quality, and tax credits and incentives, could adversely impact the demand for private and individual water wells. A decline in private and individual water well systems in the United States or other economies in the international markets the Company serves could reduce demand for the Company’s products and adversely impact sales, gross margins, and operating results.

Demand for Fueling Systems products is impacted by environmental legislation which may cause significant fluctuations in costs and revenues after meeting compliance requirements. Environmental legislation related to air quality and fueling containment may create demand for certain Fueling Systems products which must be supplied in a relatively short time frame to meet the governmental mandate. During periods of increased demand the Company’s revenues and profitability could increase significantly, although the Company can also be at risk of not having capacity to meet demand or cost overruns due to inefficiencies during ramp up to the higher production levels. After the Company’s customers have met the compliance requirements, the Company’s revenues and profitability may decrease significantly as the demand for certain products declines substantially. The risk of not reducing production costs in relation to the decreased demand and reduced revenues could have a material adverse impact on gross margins and the Company's results of operations.

Changes in tax legislation regarding the Company's foreign earnings could materially affect future results. Since the Company operates in different countries and is subject to taxation in different jurisdictions, the Company’s future effective tax rates could be impacted by changes in such countries’ tax laws or their interpretations. Both domestic and international tax laws are subject to change as a result of changes in fiscal policy, legislation, evolution of regulation and court rulings. The application of these tax laws and related regulations is subject to legal and factual interpretation, judgment, and uncertainty. Changes to the U.S. international tax laws could limit U.S. deductions for expenses related to un-repatriated foreign-source income and modify the U.S. foreign tax credit and “check-the-box” rules. The Company cannot predict whether any proposed changes in U.S. tax laws will be enacted into law or what, if any, changes may be made to any such proposals prior to their being enacted into law. If the U.S. tax laws change in a manner that increases the Company’s tax obligation, it could have a material adverse impact on the Company’s results of operations and financial condition.

The Company has significant goodwill and intangible assets and future impairment of the value of these assets may adversely affect operating results and financial condition. The Company's total assets reflect substantial intangible assets, primarily goodwill. Goodwill results from the Company's acquisitions, representing the excess of the purchase price paid over the fair value of the net assets acquired. Goodwill and indefinite-lived intangible assets are tested annually for impairment during the fourth quarter or as warranted by triggering events. If future operating performance at one or more of the Company's operating segments were to decline significantly below current levels, the Company could incur a non-cash charge to operating earnings for an impairment. Any future determination requiring the recognition of an impairment of a significant portion of the Company's goodwill or intangible assets could have a material adverse impact on the Company's results of operations and financial condition.

The Company's business may be adversely affected by the seasonality of sales and weather conditions. The Company experiences seasonal demand in a number of markets within the Water Systems segment. End-user demand in primary markets follows warm weather trends and is at seasonal highs from April to August in the Northern Hemisphere. Demand for residential and agricultural water systems are also affected by weather-related disasters including heavy flooding and drought. Changes in these patterns could reduce demand for the Company's products and adversely impact sales, gross margins, and operating results.

The Company depends on certain key suppliers, and any loss of those suppliers or their failure to meet commitments may adversely affect business and results of operations. The Company is dependent on a single or limited number of suppliers for some materials or components required in the manufacture of its products. If any of those suppliers fail to meet their commitments to the Company in terms of delivery or quality, the Company may experience supply shortages that could result in its inability to meet customer requirements, or could otherwise experience an interruption in operations that could negatively impact the Company's business and results of operations.

The Company's operations are dependent on information technology infrastructure and failures could significantly affect its business. The Company depends on information technology infrastructure in order to achieve business objectives. If the Company experiences a problem that impairs this infrastructure, such as a computer virus, a problem with the functioning of an important IT application, or an intentional disruption of IT systems by a third party, the resulting disruptions could impede the

9

Company's ability to record or process orders, manufacture and ship products in a timely manner, or otherwise carry on business in the ordinary course. Any such events could cause the loss of customers or revenue and could cause significant expense to be incurred to eliminate these problems and address related security concerns. The Company is also in the process of updating its global Enterprise Resource Planning ("ERP") system that will redesign and deploy a common information system over a period of several years. The process of implementation can be costly and can divert the attention of management from the day-to-day operations of the business. As the Company implements the ERP system, the new system may not perform as expected, which could have an adverse effect on the Company's business.

Additional Risks to the Company. The Company is subject to various risks in the normal course of business. Exhibit 99.1 sets forth risks and other factors that may affect future results, including those identified above, and is incorporated herein by reference.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Franklin Electric serves customers worldwide with over 125 manufacturing and distribution facilities located in over 20 countries. The Global Headquarters is located in Fort Wayne, Indiana, United States and houses sales, marketing, and administrative offices along with a state of the art research and engineering facility. Besides the owned corporate facility, the Company considers the following to be principal properties:

Location / Segment | Purpose | Own/Lease |

Santa Catarina, Brazil / Both | Manufacturing/Distribution/Sales | Own |

Sao Paulo, Brazil / Both | Manufacturing/Distribution/Sales | Own |

Jiangsu Province, China / Both | Manufacturing | Own |

Brno, Czech Republic / Water | Manufacturing | Own |

Dueville, Italy / Water | Manufacturing | Own |

Nuevo Leon, Mexico / Both | Manufacturing | Own |

Edenvale, South Africa / Water | Manufacturing | Own |

Izmir, Turkey / Water | Manufacturing/Distribution/Sales/R&D | Own |

Indiana, United States / Both | Manufacturing/Distribution/Sales/R&D | Own |

Oklahoma, United States / Water | Manufacturing | Own |

Wisconsin, United States / Fueling | Manufacturing/Distribution/Sales/R&D | Lease |

The Company also owns and leases other small facilities which serve as manufacturing locations and distribution warehouses. The Company does not consider these facilities to be principal to the business or operations. In the Company’s opinion, its facilities are suitable for their intended use, adequate for the Company’s business needs, all currently utilized, and in good condition.

10

EXECUTIVE OFFICERS OF THE REGISTRANT

Current executive officers of the Company, their ages, current position, and business experience during at least the past five years as of December 31, 2016, are as follows:

Name | Age | Position Held | Period Holding Position |

Gregg C. Sengstack | 58 | Chairman of the Board and Chief Executive Officer | 2015 - present |

President and Chief Executive Officer | 2014 - 2015 | ||

President and Chief Operating Officer | 2011 - 2014 | ||

Robert J. Stone | 52 | Senior Vice President and President, International Water Systems | 2012 - present |

Senior Vice President and President, Americas Water Systems Group | 2007 - 2012 | ||

Daniel J. Crose | 69 | Vice President, Global Water Product Supply | 2011 - present |

DeLancey W. Davis | 51 | Vice President and President, North America Water Systems | 2012 - present |

Donald P. Kenney | 56 | Vice President and President, Energy Systems | 2014 - present |

President, Energy Systems | 2013 - 2014 | ||

President, Fueling Systems | 1991 - 2013 | ||

John J. Haines | 53 | Vice President, Chief Financial Officer | 2008 - present |

Julie S. Freigang | 49 | Vice President, Chief Information Officer | 2015 - present |

Chief Information Officer | 2014 - 2015 | ||

Vice President, Information Technologies - Eaton Corporation | 2011 - 2014 | ||

Steven W. Aikman | 57 | Vice President, Global Water Systems Engineering | 2010 - present |

Jonathan M. Grandon | 41 | Vice President, Chief Administrative Officer, General Counsel and Secretary | 2016 - present |

Vice President, Integration - Zimmer Biomet | 2015 - 2016 | ||

Senior Vice President and General Counsel - Biomet | 2014 - 2015 | ||

Vice President and Division General Counsel, Associate General Counsel, Corporate - Biomet | 2013 - 2014 | ||

Partner - Ropes & Gray LLP | 2008 - 2013 | ||

All executive officers are elected annually by the Board of Directors at the Board meeting held in conjunction with the annual meeting of shareholders. All executive officers hold office until their successors are duly elected or until their death, resignation, or removal by the Board.

11

PART II

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

The number of shareholders of record as of February 15, 2017 was 762. The Company's stock is traded on the NASDAQ Global Select Market under the symbol FELE.

Dividends paid and the price range per common share as quoted by the NASDAQ Global Select Market for 2016 and 2015 were as follows:

Dividends per Share | Price per Share | ||||||||||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||||||||||

Low | High | Low | High | ||||||||||||||||||||

1st Quarter | $ | .0975 | $ | .0900 | $ | 23.93 | $ | 32.71 | $ | 33.45 | $ | 39.12 | |||||||||||

2nd Quarter | .1000 | .0975 | 30.58 | 35.37 | 32.13 | 39.56 | |||||||||||||||||

3rd Quarter | .1000 | .0975 | 32.65 | 40.71 | 26.75 | 31.67 | |||||||||||||||||

4th Quarter | .1000 | .0975 | 34.90 | 44.50 | 26.91 | 35.11 | |||||||||||||||||

The Company has increased dividend payments on an annual basis for 24 consecutive periods. The payment of dividends in the future will be determined by the Board of Directors and will depend on business conditions, earnings, and other factors.

Issuer Purchases of Equity Securities

In April 2007, the Company’s Board of Directors unanimously approved a plan to increase the number of shares remaining for

repurchase from 628,692 to 2,300,000 shares. There is no expiration date for this plan. On August 3, 2015, the Company's Board of Directors approved a plan to increase the number of shares remaining for repurchase by an additional 3,000,000 shares. The authorization was in addition to the 535,107 shares that remained available for repurchase as of July 31, 2015. The Company did not repurchase any shares under this plan during the fourth quarter of 2016. The maximum number of shares that may still be purchased under this plan as of December 31, 2016 is 2,156,362.

12

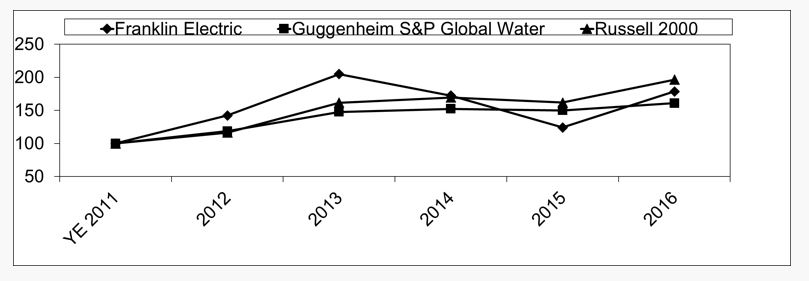

Stock Performance Graph

The following graph compares the Company's cumulative total shareholder return (Common Stock price appreciation plus dividends, on a reinvested basis) over the last five fiscal years with the Guggenheim S&P Global Water Index and the Russell 2000 Index.

Hypothetical $100 invested on December 31, 2011 (fiscal year-end 2011) in Franklin Electric common stock (FELE), Guggenheim S&P Global Water Index, and Russell 2000 Index, assuming reinvestment of dividends:

YE 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |||||||||||||||||||

FELE | $ | 100 | $ | 142 | $ | 205 | $ | 172 | $ | 124 | $ | 179 | ||||||||||||

Guggenheim S&P Global Water | 100 | 119 | 148 | 152 | 150 | 161 | ||||||||||||||||||

Russell 2000 | 100 | 116 | 162 | 169 | 162 | 196 | ||||||||||||||||||

13

ITEM 6. SELECTED FINANCIAL DATA

The following selected financial data should be read in conjunction with the Company’s consolidated financial statements. The information set forth below is not necessarily indicative of future operations.

Five Year Financial Summary

(In thousands, except per share amounts and ratios) | 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||

(c) | (d) | ||||||||||||||||||

Operations: | |||||||||||||||||||

Net sales | $ | 949,856 | $ | 924,923 | $ | 1,047,777 | $ | 965,462 | $ | 891,345 | |||||||||

Gross profit | 331,406 | 297,608 | 344,410 | 331,514 | 301,664 | ||||||||||||||

Interest expense | 8,732 | 10,039 | 10,735 | 10,597 | 10,208 | ||||||||||||||

Income tax expense | 24,798 | 12,625 | 18,851 | 28,851 | 32,250 | ||||||||||||||

Net income attributable to Franklin Electric Co., Inc. | 78,745 | 72,945 | 69,806 | 81,958 | 82,864 | ||||||||||||||

Depreciation and amortization | 35,534 | 35,476 | 37,210 | 31,356 | 28,335 | ||||||||||||||

Capital expenditures | 37,624 | 25,933 | 42,396 | 67,206 | 42,062 | ||||||||||||||

Balance sheet: | |||||||||||||||||||

Working capital (a)(b)(e) | 326,058 | 293,450 | 268,434 | 333,880 | 283,278 | ||||||||||||||

Property, plant, and equipment, net | 196,137 | 190,039 | 209,786 | 208,596 | 171,975 | ||||||||||||||

Total assets (a) | 1,039,905 | 996,111 | 1,075,797 | 1,051,770 | 976,283 | ||||||||||||||

Long-term debt (a) | 156,544 | 187,806 | 143,605 | 174,063 | 150,633 | ||||||||||||||

Shareholders’ equity | 613,445 | 557,700 | 596,840 | 595,707 | 514,406 | ||||||||||||||

Other data: | |||||||||||||||||||

Net income attributable to Franklin Electric Co., Inc., to sales | 8.3 | % | 7.9 | % | 6.7 | % | 8.5 | % | 9.3 | % | |||||||||

Net income attributable to Franklin Electric Co., Inc., to average total assets | 7.7 | % | 7.0 | % | 6.6 | % | 8.1 | % | 9.2 | % | |||||||||

Current ratio (b)(f) | 3.1 | 3.0 | 2.3 | 3.4 | 2.9 | ||||||||||||||

Number of common shares outstanding | 46,376 | 46,219 | 47,594 | 47,715 | 47,132 | ||||||||||||||

Per share: | |||||||||||||||||||

Market price range | |||||||||||||||||||

High | $ | 44.50 | $ | 39.56 | $ | 45.42 | $ | 45.62 | $ | 30.98 | |||||||||

Low | $ | 23.93 | $ | 26.75 | $ | 33.93 | $ | 29.95 | $ | 22.77 | |||||||||

Net income attributable to Franklin Electric Co., Inc., per weighted average common share | $ | 1.67 | $ | 1.52 | $ | 1.43 | $ | 1.70 | $ | 1.76 | |||||||||

Net income attributable to Franklin Electric Co., Inc., per weighted average common share, assuming dilution | $ | 1.65 | $ | 1.50 | $ | 1.41 | $ | 1.68 | $ | 1.73 | |||||||||

Book value (g) | $ | 13.12 | $ | 11.73 | $ | 12.38 | $ | 12.38 | $ | 10.78 | |||||||||

Dividends per common share | $ | 0.3975 | $ | 0.3825 | $ | 0.3475 | $ | 0.3050 | $ | 0.2850 | |||||||||

(a) | In 2016, the Company adopted Financial Accounting Standard Board ("FASB") Accounting Standard Update ("ASU") 2015-03, Interest - Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs. This ASU required retrospective adoption; therefore, years 2015, 2014, 2013, and 2012 were restated above to reflect the adoption of the ASU. See Note 2 for additional information regarding this ASU. |

(b) | Balances as of year-end 2014, 2013, 2012, and 2011 were not retrospectively adjusted for the adoption of ASU 2015-17, Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes, which related to the presentation of deferred taxes. |

14

(c) | Includes the results of operations of the Company's 100% wholly owned subsidiary, Bombas Leao S.A., since its acquisition in the second quarter of 2014, and 90% of the Company's owned subsidiary, Impo Motor Pompa Sanayi ve Ticaret A.S., since the Company's acquisition of an additional 10% in the second quarter of 2014. |

(d) | Includes the results of operations of the Company's 70.5% owned subsidiary, Pioneer Pump Holdings, Inc., since the Company's acquisition of an additional 39.5% in the first quarter of 2012, 100% of the wholly owned subsidiary, Cerus Industrial Corporation, since its acquisition in the third quarter of 2012, and 100% of the wholly owned subsidiary, Flexing, Incorporated, since the Company's acquisition in the fourth quarter of 2012. |

(e) | Working capital = Current assets minus current liabilities. |

(f) | Current ratio = Current assets divided by current liabilities. |

(g) | Book value = Shareholders’ equity divided by weighted average common shares, assuming full dilution. |

15

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

2016 vs. 2015

OVERVIEW

Sales in 2016 increased from the prior year. Net sales in 2016 were $949.9 million, an increase of about 3 percent compared to 2015 sales of $924.9 million. The sales increase was attributable to both volume and price increases partially offset by the impact of foreign currency translation as the US dollar strengthened against certain foreign currencies. The Company's consolidated gross profit was $331.4 million for 2016, an increase of $33.8 million or about 11 percent from 2015. The gross profit as a percent of net sales increased 270 basis points to 34.9 percent in 2016 from 32.2 percent in 2015. The gross profit margin change was due primarily to favorable pricing, lower direct material costs and lower fixed cost on higher sales. For 2016, diluted earnings per share were $1.65, an increase of 10 percent compared to 2015 diluted earnings per share of $1.50. Adjusted earnings per share were $1.66, an increase of 13 percent versus the $1.47 adjusted earnings per share in 2015 (see the table below for a reconciliation of the GAAP EPS to the adjusted EPS).

RESULTS OF OPERATIONS

Net Sales

Net sales in 2016 were $949.9 million, an increase of $25.0 million or about 3 percent compared to 2015 sales of $924.9 million. The incremental impact of sales from acquired businesses was $0.7 million. Sales revenue decreased by $23.2 million or about 2 percent in 2016 due to foreign currency translation. The sales change in 2016, excluding acquisitions and foreign currency translation, was an increase of $47.5 million or about 5 percent.

Net Sales | |||||||||||

(In millions) | 2016 | 2015 | 2016 v 2015 | ||||||||

Water Systems | $ | 723.2 | $ | 707.6 | $ | 15.6 | |||||

Fueling Systems | 226.7 | 217.3 | 9.4 | ||||||||

Consolidated | $ | 949.9 | $ | 924.9 | $ | 25.0 | |||||

Net Sales-Water Systems

Water Systems sales were $723.2 million in 2016, an increase of $15.6 million or 2 percent versus 2015. The incremental impact of sales from acquired businesses was $0.7 million. Foreign currency translation rate changes decreased sales $21.4 million, or about 3 percent, compared to sales in 2015. The sales change in 2016, excluding acquisitions and foreign currency translation, was an increase of $36.3 million or about 5 percent.

Water Systems sales in the U.S. and Canada were 36 percent of consolidated sales and increased by about 5 percent in 2016 compared to the prior year. Sales revenue decreased by $2.1 million or less than 1 percent in 2016 due to foreign currency translation. The sales change in 2016, excluding acquisitions and foreign currency translation, was an increase of $16.4 million or about 5 percent. In 2016, sales of groundwater pumping equipment increased by about 9 percent. The growth in groundwater equipment sales was led by a 12 percent increase in sales of products for both residential and agricultural applications. Sales of Pioneer branded mobile dewatering equipment declined by about 12 percent. The decline in mobile dewatering equipment is primarily attributed to reduced demand in the oil and gas end markets.

Water Systems sales in Europe, Middle East and Africa were about 17 percent of consolidated sales and declined by about 4 percent compared to 2015. Water Systems in Europe, the Middle East and Africa were reduced by $10.5 million or about 6 percent due to foreign currency translation. Excluding the impact of foreign currency translation, sales were up in 2016 by about 2 percent compared to 2015. The growth was driven by strong sales of groundwater pumping equipment in Turkey.

In local currency sales in Turkey grew; however, this growth was offset by sales declines in other parts of the region due to political and economic turmoil and the lower price of oil which reduced investment by the public sector, particularly in Saudi Arabia.

Water Systems sales in Latin America were about 14 percent of consolidated sales for 2016 and declined by about 1 percent compared to 2015. Sales revenue decreased by $8.5 million or about 7 percent in 2016 due to foreign currency translation. The sales change in 2016, excluding foreign currency translation, was an increase of $7.4 million or about 6 percent. The growth in sales was led by increased sales in Mexico and Brazil, in local currency. This sales growth is a result of increasing demand for

16

Franklin submersible pumps and motors, customer acceptance of the many product line upgrades that have been implemented over the past two years, and general market conditions.

Water Systems sales in the Asia Pacific region were 9 percent of consolidated sales and grew by about 12 percent compared to the prior year. Foreign currency translation rate changes decreased sales in 2016 in the Asia Pacific region by less than a percent. The Asia Pacific region experienced strong year over year growth in Southeast Asia and Australia.

Net Sales-Fueling Systems

Fueling Systems sales which represented 24 percent of consolidated sales were $226.7 million in 2016, an increase of $9.4 million or about 4 percent versus 2015. Foreign currency translation rate changes decreased sales $1.8 million or about 1 percent compared to sales in 2015. The sales change in 2016, excluding acquisitions and foreign currency translation, was an increase of $11.2 million or about 5 percent.

Fueling Systems sales in the U.S. and Canada grew by about 8 percent in 2016 compared to the prior year with sales growth coming from most product lines, most significantly our pumping and fuel management systems. Fueling Systems sales in the rest of the world were down about 2 percent year over year. In 2016, Fueling Systems revenues increased in the Asia Pacific regions by about 14 percent, driven by higher sales in India. This growth in Asia was more than offset by a sales decline in Europe principally due to a 42 percent decline in the sale of storage tanks that support North Sea oil production.

Cost of Sales

Cost of sales as a percent of net sales for 2016 and 2015 was 65.1 percent and 67.8 percent, respectively. Correspondingly, the gross profit margin increased to 34.9 percent from 32.2 percent, a 270 basis point improvement. The gross profit margin increase was primarily due to lower raw material costs and lower fixed costs. Direct materials as a percentage of sales was 44.8 percent down 210 basis points compared to 46.9 percent last year. This decrease in direct materials was primarily due to favorable pricing and lower direct material costs. The Company's consolidated gross profit was $331.4 million for 2016, up $33.8 million or 11 percent from 2015.

Selling, General and Administrative (“SG&A”)

Selling, general, and administrative (SG&A) expenses were $221.2 million in 2016 and increased by $16.9 million or about 8 percent in 2016 compared to last year. In 2016, increases in SG&A attributable to higher variable compensation expenses were about $12 million or about 6 percent. Additional year over year changes in SG&A costs were primarily in Marketing and Selling related expenses which increased about $2.5 million to support sales growth and, also, Research, Development & Engineering expense which increased by $2.3 million in the year.

Restructuring (Income)/Expense

Restructuring expenses for 2016 netted to a gain of $(0.6) million and increased diluted earnings per share about $0.01. Restructuring expenses for 2016 included a gain of $(2.0) million from the sale of land and building in Brazil and $1.4 million in expenses related to severance and pension costs, equipment relocation expenses, asset write-downs and other costs related to the transfer of production activities and other restructuring costs from continued manufacturing realignments.

Restructuring expenses for 2015 were $3.0 million and decreased diluted earnings per share about $0.04. Restructuring expenses in 2015 included severance and pension costs, equipment relocation expenses, and asset write-downs primarily related to the closure of the Wittlich, Germany facility and other manufacturing realignment activities in Europe and Brazil.

Operating Income

Operating income was $110.8 million in 2016, up $20.4 million from $90.4 million in 2015.

Operating income (loss) | ||||||||||||

(In millions) | 2016 | 2015 | 2016 v 2015 | |||||||||

Water Systems | $ | 108.2 | $ | 86.7 | $ | 21.5 | ||||||

Fueling Systems | 56.3 | 51.5 | 4.8 | |||||||||

Other | (53.7 | ) | (47.8 | ) | (5.9 | ) | ||||||

Consolidated | $ | 110.8 | $ | 90.4 | $ | 20.4 | ||||||

There were specific items in 2016 and 2015 that impacted operating income.

17

In 2016 they were as follows:

• | $(0.6) million of net restructuring charges. Restructuring (income)/expenses in 2016 included a gain of $(2.0) million from the sale of land and building in Brazil, $0.4 million in asset write-offs, $0.2 million in severance and pension cost, $0.2 million expenses related to equipment transfers and freight costs and $0.6 million in other relocation costs primarily related to other manufacturing realignment activities. |

• | $1.2 million related to executive transition. |

• | $0.1 million in other miscellaneous costs related to closed acquisitions. |

In 2015 they were as follows:

• | There were $3.0 million of restructuring charges. Restructuring expenses in 2015 were $0.6 million in severance cost, $0.6 million in pension cost, $0.6 million expenses related to equipment transfers and freight costs, $0.1 million in asset write-offs and $1.1 million in other relocation costs primarily related to the closure of the Wittlich, Germany facility and other manufacturing realignment activities in Europe and Brazil. |

• | $1.2 million related to executive transition. |

• | $0.7 million related to business realignment cost, primarily severance, in targeted fixed cost reduction actions. |

• | $0.2 million in other miscellaneous costs related to closed acquisitions. |

The Company refers to these items as “non-GAAP adjustments” for purposes of presenting the non-GAAP financial measures of operating income after non-GAAP adjustments and percent operating income to net sales after non-GAAP adjustments to net sales (operating income margin after non-GAAP adjustments). The Company believes this information helps investors and management understand underlying trends in the Company's business more easily and by presenting these matters in this way, gives our investors and management a more accurate picture of the actual operational performance of the Company. The non-GAAP adjustments are for restructuring expenses, reported separately on the income statement, as well as certain legal matters and acquisition related items which are included in SG&A on the income statement. The differences between these non-GAAP financial measures and the most comparable GAAP measures are reconciled in the following tables:

18

Operating Income and Margins | ||||||||||||

Before and After Non-GAAP Adjustments | ||||||||||||

(in millions) | For the Full Year of 2016 | |||||||||||

Water | Fueling | Other | Consolidated | |||||||||

Reported Operating Income/(Loss) | $ | 108.2 | $ | 56.3 | $ | (53.7 | ) | $ | 110.8 | |||

% Operating Income To Net Sales | 15.0 | % | 24.8 | % | 11.7 | % | ||||||

Non-GAAP Adjustments: | ||||||||||||

Restructuring | $ | (1.2 | ) | $ | 0.6 | $ | — | $ | (0.6 | ) | ||

Non-GAAP | $ | 0.1 | $ | — | $ | 1.2 | $ | 1.3 | ||||

Operating Income/(Loss) after Non-GAAP Adjustments | $ | 107.1 | $ | 56.9 | $ | (52.5 | ) | $ | 111.5 | |||

% Operating Income to Net Sales after Non-GAAP adjustments (Operating Income Margin after Non-GAAP Adjustments) | 14.8 | % | 25.1 | % | 11.7 | % | ||||||

For the Full Year of 2015 | ||||||||||||

Water | Fueling | Other | Consolidated | |||||||||

Reported Operating Income/(Loss) | $ | 86.7 | $ | 51.5 | $ | (47.8 | ) | $ | 90.4 | |||

% Operating Income To Net Sales | 12.3 | % | 23.7 | % | 9.8 | % | ||||||

Non-GAAP Adjustments: | ||||||||||||

Restructuring | $ | 2.7 | $ | 0.3 | $ | — | $ | 3.0 | ||||

Non-GAAP | $ | 0.7 | $ | 0.2 | $ | 1.2 | $ | 2.1 | ||||

Operating Income/(Loss) after Non-GAAP Adjustments | $ | 90.1 | $ | 52.0 | $ | (46.6 | ) | $ | 95.5 | |||

% Operating Income to Net Sales after Non-GAAP adjustments (Operating Income Margin after Non-GAAP Adjustments) | 12.7 | % | 23.9 | % | 10.3 | % | ||||||

Operating Income-Water Systems

Water Systems operating income was $108.2 million in 2016, up $21.5 million or 25 percent versus the 2015 as reported and up $17.0 million or 19 percent versus the 2015 after non-GAAP adjustments. The 2016 operating income margin was 15.0 percent, up 270 basis points from 12.3 percent in 2015. The 2016 operating income margin after non-GAAP adjustments was 14.8 percent, an increase of 210 basis points from the 12.7 percent of net sales in 2015 after non-GAAP adjustments. The increase in basis points was primarily due to improved margins from lower variable costs.

Operating Income-Fueling Systems

Fueling Systems operating income was $56.3 million in 2016, up $4.8 million or about 9 percent compared to $51.5 million in 2015 as reported, and up $4.9 million or 9 percent compared to $52.0 million after non-GAAP adjustments in 2015. The 2016 operating income margin was 24.8 percent, an increase of 110 basis points from the as reported 23.7 percent of net sales in 2015. The 2016 operating income margin after non-GAAP adjustments was 25.1 percent, an increase of 120 basis points from the 23.9 percent of net sales in 2015 after non-GAAP adjustments. The increase in basis points was primarily due to improved margins from lower variable costs.

Operating Income-Other

Operating income-other is composed primarily of unallocated general and administrative expenses. General and administrative expenses after non-GAAP adjustments were higher by about 13 percent, primarily due to higher variable compensation expenses.

Interest Expense

Interest expense for 2016 and 2015 was $8.7 million and $10.0 million, respectively.

Other Income or Expense

Other income or expense was a gain of $1.0 million in 2016. Included in other income or expense in 2016 was minority income of $1.7 million and interest income of $1.0 million, primarily derived from the investment of cash balances in short-term securities. In 2016, other expenses also included the reversal of an indemnification receivable related to a contingent tax liability for $1.9 million recorded at the time of a foreign acquisition. The contingent tax liability was for the same amount and

19

was also reversed in 2016 and the benefit was recorded in the income tax provision. Other income or expense was income of $6.9 million in 2015. Included in other income or expense in 2016 was minority income of $2.8 million and interest income of $1.3 million, primarily derived from the investment of cash balances in short-term securities. The Company also realized a gain on the settlement of the redeemable non-controlling interest liability in the first quarter of 2015 of about $2.7 million.

Foreign Exchange

Foreign currency-based transactions produced a gain for 2016 of $1.1 million, primarily due to the Turkish lira relative to the U.S. dollar and euro. Foreign currency-based transactions produced a loss for 2015 of $0.9 million, primarily due to the South African rand, Colombian peso and Australian dollar relative to the U.S. dollar, none of which individually were significant.

Income Taxes

The provision for income taxes in 2016 and 2015 was $24.8 million and $12.6 million, respectively. The tax rate for 2016 was 23.8 percent and 2015 was 14.6 percent. Discrete adjustments in 2016 were primarily due to the favorable impact from equity compensation share based payments and the reversal of a contingent tax liability offset by adjustments to the Company’s valuation allowance against certain state deferred tax assets that are not likely to be realized. Discrete adjustments during 2015 were the reversal of a deferred tax liability of about $4.8 million created in 2012 when the Company acquired the controlling interest in the Pioneer subsidiary and realized a gain on the then equity investment in Pioneer. This purchase transaction also resulted in other tax benefits of about $3.5 million. The tax rate before discrete adjustments for 2016 was about 26 percent and 2015 was about 27 percent. The tax rate is lower than the statutory rate of 35 percent primarily due to the indefinite reinvestment of foreign earnings and reduced taxes on foreign and repatriated earnings. The Company has the ability to indefinitely reinvest these foreign earnings based on the earnings and cash projections of its other operations, current cash on hand and available credit.

Net Income

Net income for 2016 was $79.3 million compared to 2015 net income of $73.7 million. Net income attributable to Franklin Electric Co., Inc. for 2016 was $78.7 million, or $1.65 per diluted share, compared to 2015 net income attributable to Franklin Electric Co., Inc. of $72.9 million or $1.50 per diluted share. Net income attributable to Franklin Electric Co., Inc. after Non-GAAP adjustments for 2016 was $77.4 million, or $1.66 per diluted share, compared to 2015 net income attributable to Franklin Electric Co., Inc. after Non-GAAP adjustments of $69.7 million or $1.47 per diluted share.

There were specific items in 2016 and 2015 that impacted net income attributable to Franklin Electric Co., Inc. The Company refers to these items as “non-GAAP adjustments” for purposes of presenting the non-GAAP financial measures of net income attributable to Franklin Electric Co., Inc. and adjusted EPS. The Company believes this information helps investors understand underlying trends in the Company's business more easily. The differences between these non-GAAP financial measures and the most comparable GAAP measures are reconciled in the following tables:

Earnings Before and After Non-GAAP Adjustments | For the Full Year | |||||||

(in millions) | 2016 | 2015 | Change | |||||

Net Income attributable to Franklin Electric Co., Inc. Reported | $ | 78.7 | $ | 72.9 | 8 | % | ||

Allocated Undistributed Earnings | $ | (1.7 | ) | $ | (1.5 | ) | ||

Earnings for EPS Calculations | $ | 77.0 | $ | 71.4 | 8 | % | ||

Non-GAAP adjustments (before tax): | ||||||||

Restructuring | $ | (0.6 | ) | $ | 3.0 | |||

Non-GAAP items | $ | 1.3 | $ | 2.1 | ||||

Pioneer tax benefits on equity gain | $ | — | $ | (4.8 | ) | |||

Non-GAAP adjustments, net of tax: | ||||||||

Restructuring | $ | (0.4 | ) | $ | 1.8 | |||

Non-GAAP items | $ | 0.8 | $ | 1.3 | ||||

Pioneer tax benefits on equity gain | $ | — | $ | (4.8 | ) | |||

Earnings after Non-GAAP Adjustments | $ | 77.4 | $ | 69.7 | 11 | % | ||

20

Earnings Per Share Before and After Non-GAAP Adjustments | For the Full Year | |||||||||

(in millions except per-share data) | 2016 | 2015 | Change | |||||||

Average Fully Diluted Shares Outstanding | $ | 46.7 | $ | 47.6 | (2 | )% | ||||

Fully Diluted Earnings Per Share ("EPS") Reported | $ | 1.65 | $ | 1.50 | 10 | % | ||||

Restructuring Per Share, net of tax | $ | (0.01 | ) | $ | 0.04 | |||||

Non-GAAP items, net of tax | $ | 0.02 | $ | 0.03 | ||||||

Pioneer tax benefits on equity gain | $ | — | $ | (0.10 | ) | |||||

Fully Diluted EPS after Non-GAAP Adjustments (Adjusted EPS) | $ | 1.66 | $ | 1.47 | 13 | % | ||||

2015 vs. 2014

OVERVIEW

Sales in 2015 decreased from the prior year. Net sales in 2015 were $924.9 million, a decrease of about 12 percent compared to 2014 sales of $1,047.8 million. The sales decrease was primarily the impact of foreign currency translation as the US dollar strengthened against certain foreign currencies and lower sales volume, partially offset by sales price increases, as well as the Company's acquisitions. The Company's consolidated gross profit was $297.6 million for 2015, a decrease of $46.8 million or about 14 percent from 2014. The gross profit as a percent of net sales decreased 70 basis points to 32.2 percent in 2015 from 32.9 percent in 2014. The gross profit margin change was due primarily to lost leverage on fixed cost due to lower sales. For 2015, diluted earnings per share were $1.50, an increase of 6 percent compared to 2014 diluted earnings per share of $1.41. Adjusted earnings per share were $1.47, a decrease of 16 percent versus the $1.76 adjusted earnings per share in 2014 (see the table below for a reconciliation of the GAAP EPS to the adjusted EPS).

RESULTS OF OPERATIONS

Net Sales

Net sales in 2015 were $924.9 million, a decrease of $122.9 million or about 12 percent compared to 2014 sales of $1,047.8 million. The incremental impact of sales from acquired businesses was $21.3 million or about 2 percent. Sales revenue decreased by $89.3 million or about 9 percent in 2015 due to foreign currency translation. The sales change in 2015, excluding acquisitions and foreign currency translation, was a decrease of $54.9 million or about 5 percent.

Net Sales | ||||||||||||

(In millions) | 2015 | 2014 | 2015 v 2014 | |||||||||

Water Systems | $ | 707.6 | $ | 824.6 | $ | (117.0 | ) | |||||

Fueling Systems | 217.3 | 223.2 | (5.9 | ) | ||||||||

Consolidated | $ | 924.9 | $ | 1,047.8 | $ | (122.9 | ) | |||||

Net Sales-Water Systems

Water Systems sales were $707.6 million in 2015, a decrease of $117.0 million or 14 percent versus 2014. The incremental impact of sales from acquired businesses was $20.8 million or about 2 percent. Foreign currency translation rate changes decreased sales $78.3 million, or about 9 percent, compared to sales in 2014. The sales change in 2015, excluding acquisitions and foreign currency translation, was a decrease of $59.5 million or about 7 percent.

Water Systems sales in the U.S. and Canada were 36 percent of consolidated sales and declined by about 20 percent in 2015 compared to the prior year. Sales revenue decreased by $5.9 million or about 1 percent in 2015 due to foreign currency translation. In 2015, U.S. and Canada sales of Pioneer branded mobile dewatering equipment declined by about 55 percent. The decline in mobile dewatering equipment is primarily attributed to reduced demand in the oil and gas end markets. Sales of

21

groundwater pumping equipment declined by about 14 percent, and sales of surface water pumping equipment declined by about 6 percent versus 2014. The decline in groundwater equipment sales is attributable primarily to weaker demand in the agriculture sector as a result of less favorable weather and to a lesser extent, distributor changes the Company made in its primary groundwater distribution channel. Sales of surface water pumping equipment also declined due to lower condensate pump sales as cooler temperatures delayed the start to the HVAC season.

Water Systems sales in Latin America were about 14 percent of consolidated sales for 2015 and declined by about 9 percent compared to the prior year. Acquisition related sales during 2015 were $10.4 million or about 7 percent. Foreign currency translation rate changes decreased sales $34.7 million, or about 24 percent, compared to sales in 2014. Excluding acquisition and foreign currency translation, sales in Latin America grew by about 8 percent during 2015. The growth in sales was led by increased sales in Mexico and Brazil, in local currency. This sales growth is a result of increasing demand for Franklin submersible pumps and motors, customer acceptance of the many product line upgrades that have been implemented over the past two years, and general market conditions.

Water Systems sales in the Middle East and Africa were about 11 percent of consolidated sales and decreased by about 10 percent compared to 2014. Water Systems sales in the Middle East and Africa were reduced by $16.5 million or about 14 percent in the year due to foreign currency translation. Excluding the impact of foreign currency translation, sales were up about 4 percent compared to 2014. The growth was driven by strong sales of groundwater pumping equipment in Turkey.

Water Systems sales in the Asia Pacific region were 8 percent of consolidated sales and grew by about 7 percent compared to the prior year. Acquisition related sales during 2015 increased sales by about 9 percent in Asia Pacific. Foreign currency translation rate changes decreased sales in 2015 in the Asia Pacific region by about 5 percent. Excluding acquisitions and foreign currency translation sales grew by about 3 percent during 2015. The Asia Pacific region experienced strong year over year growth in Southeast Asia and Korea. These sales increases were partially offset by smaller declines in sales in Australia, Japan and China.

Water Systems sales in Europe were about 7 percent of consolidated sales and decreased by about 20 percent compared to the prior year. Foreign currency translation rate changes decreased sales by about 21 percent compared to sales in 2014. Excluding foreign currency translation, European sales grew by about 1 percent during 2015.

Net Sales-Fueling Systems

Fueling Systems sales which represented 23 percent of consolidated sales were $217.3 million in 2015, a decrease of $5.9 million or about 3 percent versus 2014. The incremental impact of sales from acquired businesses was $0.5 million. Foreign currency translation rate changes decreased sales $11.0 million or about 5 percent compared to sales in 2014. The sales change in 2015, excluding acquisitions and foreign currency translation, was an increase of $4.6 million or about 2 percent.

Fueling Systems sales in the U.S. and Canada grew by about 6 percent in 2015 compared to the prior year with sales growth coming from most product lines, especially in piping. Fueling Systems revenues declined in India and China due to the timing of tender awards made in India and the ongoing reduction in State owned oil company procurements in China. Sales also declined in Europe principally due to a 42 percent decline in the sale of storage tanks that support North Sea oil production.

Cost of Sales

Cost of sales as a percent of net sales for 2015 and 2014 was 67.8 percent and 67.1 percent, respectively. Correspondingly, the gross profit margin decreased to 32.2 percent from 32.9 percent, a 70 basis point decline. The gross profit margin decrease was primarily due to fixed costs deleverage on lower sales and higher raw material costs. Direct materials as a percentage of sales was 46.9 percent up 50 basis points compared to 46.4 percent last year. This increase in direct materials was partially offset by lower labor and burden costs. The Company's consolidated gross profit was $297.6 million for 2015, down $46.8 million or 14 percent from 2014.

Selling, General and Administrative (“SG&A”)

Selling, general, and administrative (SG&A) expenses were $204.3 million in 2015 and decreased by $23.4 million or about 10 percent in 2015 compared to last year. In 2015, increases in SG&A attributable to acquisitions were about $6 million or about 3 percent. Additional year over year changes in SG&A costs were decreases in the year primarily due to lower marketing and selling related expenses, as well as lower costs for incentive compensation. Approximately half of the lower SG&A expenses was related to foreign exchange.

22

Restructuring Expenses

Restructuring expenses for 2015 were $3.0 million and reduced diluted earnings per share by approximately $0.04. Restructuring expenses in 2015 included severance and pension costs, equipment relocation expenses, asset write-downs and primarily related to the closure of the Wittlich, Germany facility and other manufacturing realignment activities in Europe and Brazil. There were $16.6 million of restructuring expenses in 2014 and reduced diluted earnings per share by approximately $0.24. Restructuring expenses in 2014 included severance costs, equipment relocation expenses, and asset write-downs primarily related to the closure of the Wittlich, Germany facility and other European manufacturing realignment activities.

Operating Income

Operating income was $90.4 million in 2015, down $9.7 million from $100.1 million in 2014.

Operating income (loss) | ||||||||||||

(In millions) | 2015 | 2014 | 2015 v 2014 | |||||||||

Water Systems | $ | 86.7 | $ | 103.9 | $ | (17.2 | ) | |||||

Fueling Systems | 51.5 | 49.7 | 1.8 | |||||||||

Other | (47.8 | ) | (53.5 | ) | 5.7 | |||||||

Consolidated | $ | 90.4 | $ | 100.1 | $ | (9.7 | ) | |||||

There were specific items in 2015 and 2014 that impacted operating income.

In 2015 they were as follows:

• | There were $3.0 million of restructuring charges. Restructuring expenses in 2015 were $0.6 million in severance cost, $0.6 million in pension cost, $0.6 million expenses related to equipment transfers and freight costs, $0.1 million in asset write-offs and $1.1 million in other relocation costs primarily related to the closure of the Wittlich, Germany facility and other manufacturing realignment activities in Europe and Brazil. |

• | $1.2 million related to executive transition. |

• | $0.7 million related to business realignment cost, primarily severance, in targeted fixed cost reduction actions. |

• | $0.2 million in other miscellaneous costs related to closed acquisitions. |

In 2014 they were as follows:

• | There were $16.6 million of restructuring charges. Restructuring expenses in 2014 were $14.7 million in severance cost, $1.7 million expenses related to equipment transfers, freight and other relocation costs and $0.2 million in asset write-offs primarily related to the transfer of production activities from Germany to the Czech Republic and other continued manufacturing realignments. |

• | $3.2 million in other miscellaneous costs related to closed and pending acquisitions and $0.2 million in legal fees incurred by Franklin Fueling Systems. |

• | $2.5 million related to executive transition. |

• | $1.8 million of software write-offs. |

The Company refers to these items as “non-GAAP adjustments” for purposes of presenting the non-GAAP financial measures of operating income after non-GAAP adjustments and percent operating income to net sales after non-GAAP adjustments to net sales (operating income margin after non-GAAP adjustments). The Company believes this information helps investors and management understand underlying trends in the Company's business more easily and by presenting these matters in this way, gives our investors and management a more accurate picture of the actual operational performance of the Company. The non-GAAP adjustments are for restructuring expenses, reported separately on the income statement, as well as certain legal matters and acquisition related items which are included in SG&A on the income statement. The differences between these non-GAAP financial measures and the most comparable GAAP measures are reconciled in the following tables:

23

Operating Income and Margins | ||||||||||||

Before and After Non-GAAP Adjustments | ||||||||||||

(in millions) | For the Full Year of 2015 | |||||||||||

Water | Fueling | Other | Consolidated | |||||||||