Attached files

| file | filename |

|---|---|

| EX-10.51 - EXHIBIT 10.51 - REALOGY HOLDINGS CORP. | ex10-51.htm |

| EX-32.2 - EXHIBIT 32.2 - REALOGY HOLDINGS CORP. | ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - REALOGY HOLDINGS CORP. | ex32-1.htm |

| EX-31.4 - EXHIBIT 31.4 - REALOGY HOLDINGS CORP. | ex31-4.htm |

| EX-31.3 - EXHIBIT 31.3 - REALOGY HOLDINGS CORP. | ex31-3.htm |

| EX-31.2 - EXHIBIT 31.2 - REALOGY HOLDINGS CORP. | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - REALOGY HOLDINGS CORP. | ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - REALOGY HOLDINGS CORP. | ex23-1.htm |

| EX-21.1 - EXHIBIT 21.1 - REALOGY HOLDINGS CORP. | ex21-1.htm |

| EX-10.50 - EXHIBIT 10.50 - REALOGY HOLDINGS CORP. | ex10-50.htm |

| EX-10.20 - EXHIBIT 10.20 - REALOGY HOLDINGS CORP. | ex10-20.htm |

| EX-4.18 - EXHIBIT 4.18 - REALOGY HOLDINGS CORP. | ex4-18.htm |

| EX-4.15 - EXHIBIT 4.15 - REALOGY HOLDINGS CORP. | ex4-15.htm |

| EX-4.8 - EXHIBIT 4.8 - REALOGY HOLDINGS CORP. | ex4-8.htm |

_____________________________________________________________________________________________________________________________________________________________________________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________

FORM 10-K

þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2016

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____

Commission File No. 001-35674

REALOGY HOLDINGS CORP.

(Exact name of registrant as specified in its charter)

20-8050955

(I.R.S. Employer Identification Number)

Commission File No. 333-148153

REALOGY GROUP LLC

(Exact name of registrant as specified in its charter)

20-4381990

(I.R.S. Employer Identification Number)

Delaware

(State or other jurisdiction of incorporation or organization)

175 Park Avenue

Madison, NJ 07940

(Address of principal executive offices) (Zip Code)

(973) 407-2000

(Registrants' telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | |||

Title of each class | Name of each exchange on which registered | ||

Realogy Holdings Corp. | Common Stock, par value $0.01 per share | New York Stock Exchange | |

Realogy Group LLC | None | None | |

Securities registered pursuant to Section 12(g) of the Act: None

___________________________

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Realogy Holdings Corp. Yes þ No ¨ Realogy Group LLC Yes ¨ No þ

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Realogy Holdings Corp. Yes ¨ No þ Realogy Group LLC Yes þ No ¨

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Realogy Holdings Corp. Yes þ No ¨ Realogy Group LLC Yes ¨ No þ

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).

Realogy Holdings Corp. Yes þ No ¨ Realogy Group LLC Yes þ No ¨

Indicate by check mark if disclosure of delinquent filer pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Realogy Holdings Corp. þ Realogy Group LLC þ

Indicate by check mark whether the Registrant is a large accelerated filer, accelerated filer, non-accelerated filer, or smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | Accelerated filer | Non-accelerated filer | Smaller reporting company | ||||

(Do not check if a smaller reporting company) | |||||||

Realogy Holdings Corp. | þ | ¨ | ¨ | ¨ | |||

Realogy Group LLC | ¨ | ¨ | þ | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Realogy Holdings Corp. Yes ¨ No þ Realogy Group LLC Yes ¨ No þ

The aggregate market value of the voting and non-voting common equity of Realogy Holdings Corp. held by non-affiliates as of the close of business on June 30, 2016 was $4.2 billion. There were 139,617,861 shares of Common Stock, $0.01 par value, of Realogy Holdings Corp. outstanding as of February 21, 2017.

Realogy Group LLC meets the conditions set forth in General Instruction I(1)(a) and (b) of Form 10-K and is therefore filing this Form with the reduced disclosure format applicable to Realogy Group LLC.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement prepared for the Annual Meeting of Stockholders to be held May 3, 2017 are incorporated by reference into Part III of this report.

_______________________________________________________________________________________________________________________________________________________________________________

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Item 16. | ||

FORWARD-LOOKING STATEMENTS

Forward-looking statements included in this Annual Report and our other public filings or other public statements that we make from time to time are based on various facts and derived utilizing numerous important assumptions and are subject to known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Forward-looking statements include the information concerning our future financial performance, business strategy, projected plans and objectives, as well as projections of macroeconomic and industry trends, which are inherently unreliable due to the multiple factors that impact economic trends, and any such variations may be material. Statements preceded by, followed by or that otherwise include the words "believes," "expects," "anticipates," "intends," "projects," "estimates," "plans," and similar expressions or future or conditional verbs such as "will," "should," "would," "may" and "could" are generally forward-looking in nature and not historical facts. You should understand that the following important factors could affect our future results and cause actual results to differ materially from those expressed in the forward-looking statements:

• | risks related to general business, economic, employment and political conditions and the U.S. residential real estate markets, either regionally or nationally, including but not limited to: |

◦ | a lack of improvement or a decline in the number of homesales, stagnant or declining home prices and/or a deterioration in other economic factors that particularly impact the residential real estate market and the business segments in which we operate; |

◦ | increasing mortgage rates and/or constraints on the availability of mortgage financing; |

◦ | insufficient or excessive home inventory levels by market and price point; |

◦ | a decrease in consumer confidence; |

◦ | the impact of recessions, slow economic growth, disruptions in the U.S. government or banking system, disruptions in a major geoeconomic region, or equity or commodity markets and high levels of unemployment in the U.S. and abroad, which may impact all or a portion of the housing markets in which we and our franchisees operate; |

◦ | legislative, tax or regulatory changes (including changes in regulatory interpretations or enforcement practices) that would adversely impact the residential real estate market, including changes relating to the Real Estate Settlement Procedures Act ("RESPA"), potential reforms of Fannie Mae and Freddie Mac, and potential tax code reform; |

◦ | a decrease in housing affordability; |

◦ | high levels of foreclosure activity; |

◦ | changing attitudes towards home ownership, particularly among potential first-time homebuyers who may delay, or decide not to, purchase a home, as well as the potential impact of decisions to rent versus purchase a home; and |

◦ | the inability or unwillingness of current homeowners to purchase their next home due to various factors, including limited or negative equity in their current home, difficult mortgage underwriting standards, attractive rates on existing mortgages and the lack of available inventory in their market; |

• | increased competition whether through traditional competitors or competitors with alternative business models, including companies employing technologies intended to disrupt the traditional brokerage model, as well as eliminating brokers or agents from, or minimizing the role they play in, the homesale transaction; |

• | competition for more productive sales associates, sales associate teams, and manager talent may continue to impact the ability of our company owned brokerage business and our affiliated franchisees to attract and retain independent sales associates, either individually or as members of a team, without significantly impacting the commission split rates currently paid by our company owned brokerages and our affiliated franchisees; |

• | our geographic and high-end market concentration, particularly with respect to our company owned brokerage operations; |

• | our inability to enter into franchise agreements with new franchisees at current net effective royalty rates, or to realize royalty revenue growth from them; |

• | our inability to renew existing franchise agreements at current net effective royalty rates or without increasing the amount and prevalence of non-standard incentives, or to maintain or enhance our value proposition to franchisees; |

1

• | the lack of revenue growth or declining profitability of our franchisees and company owned brokerage operations, including the impact of lower average broker commission rates; |

• | disputes or issues with entities that license us their tradenames for use in our business that could impede our franchising of those brands; |

• | actions by our franchisees that could harm our business or reputation, non-performance of our franchisees, controversies with our franchisees or actions against us by their independent sales associates or employees or third parties with which our franchisees have business relationships; |

• | loss or attrition among our senior executives, other key employees or our inability to recruit top talent; |

• | our inability to achieve or maintain cost savings and other benefits from our restructuring activities; |

• | our inability to realize the benefits from acquisitions due to the loss of key personnel or productive agents of the acquired companies, as well as the possibility that expected benefits and synergies of the transactions may not be achieved in a timely manner or at all; |

• | our failure or alleged failure to comply with laws, regulations and regulatory interpretations and any changes in laws and regulations or stricter interpretations of regulatory requirements, including but not limited to (1) state or federal employment laws or regulations that would require reclassification of independent contractor sales associates to employee status, (2) RESPA or state consumer protection or similar laws and (3) privacy or data security laws and regulations; |

• | any adverse resolution of litigation, governmental or regulatory proceedings or arbitration awards as well as any adverse impact of decisions to voluntarily modify business arrangements or enter into settlement agreements to avoid the risk of protracted and costly litigation or other proceedings; |

• | our inability to obtain new technologies and systems, to replace or introduce new technologies and systems as quickly as our competitors and in a cost-effective manner or to achieve the benefits anticipated from new technologies or systems; |

• | the failure or significant disruption of our operations from various causes related to our critical information technologies and systems including cybersecurity threats to our data and customer, franchisee and independent sales associate data as well as reputational or financial risks associated with a loss of any such data; |

• | risks related to our international operations, including compliance with the Foreign Corrupt Practices Act and similar anti-corruption laws as well as risks relating to the master franchisor model that we deploy internationally; |

• | risks associated with our substantial indebtedness and interest obligations and restrictions contained in our debt agreements, including risks relating to having to dedicate a significant portion of our cash flows from operations to service our debt; |

• | risks relating to our ability to refinance or repay our indebtedness, incur additional indebtedness or return capital to stockholders; |

• | changes in corporate relocation practices resulting in fewer employee relocations, reduced relocation benefits or the loss of one or more significant affinity clients; |

• | an increase in the claims rate of our title underwriter and an increase in mortgage rates could adversely impact the revenue of our title and settlement services segment; |

• | our inability to securitize certain assets of our relocation business, which would require us to find an alternative source of liquidity that may not be available, or if available, may not be on favorable terms; |

• | risks that could materially adversely impact our equity investment in our mortgage origination joint venture, including increases in mortgage rates, the impact of joint venture operational or liquidity risks, the impact of a transition from our current joint venture to our new joint venture, regulatory changes, litigation, investigations and inquiries or any termination of the venture; |

• | any remaining resolutions or outcomes with respect to contingent liabilities of our former parent, Cendant Corporation ("Cendant"), under the Separation and Distribution Agreement and the Tax Sharing Agreement (described elsewhere in this Annual Report and incorporated by reference as exhibits to this Annual Report), including any adverse impact on our future cash flows; and |

• | new types of taxes or increases in state, local or federal taxes that could diminish profitability or liquidity. |

Other factors not identified above, including those described under "Item 1A.—Risk Factors" and "Item 7.—Management’s Discussion and Analysis of Financial Condition and Results of Operations" of this Annual Report, may also cause actual results to differ materially from those described in our forward-looking statements. Most of these factors are

2

difficult to anticipate and are generally beyond our control. You should consider these factors in connection with any forward-looking statements that may be made by us and our businesses generally.

Except for our ongoing obligations to disclose material information under the federal securities laws, we undertake no obligation to release publicly any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events unless we are required to do so by law. For any forward-looking statement contained in this Annual Report, our public filings or other public statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

TRADEMARKS AND SERVICE MARKS

We own or have rights to use the trademarks, service marks and trade names that we use in conjunction with the operation of our business. Some of the more important trademarks that we own or have rights to use that appear in this Annual Report include the CENTURY 21®, COLDWELL BANKER®, ERA®, CORCORAN®, COLDWELL BANKER COMMERCIAL®, SOTHEBY’S INTERNATIONAL REALTY®, BETTER HOMES AND GARDENS®, ZIPREALTY® and ZAPLABSSM marks, which are registered in the United States and/or registered or pending registration in other jurisdictions, as appropriate to the needs of our relevant business. Each trademark, trade name or service mark of any other company appearing in this Annual Report is owned by such company.

MARKET AND INDUSTRY DATA AND FORECASTS

This Annual Report includes data, forecasts and information obtained from independent trade associations, industry publications and surveys and other information available to us. Some data is also based on our good faith estimates, which are derived from management’s knowledge of the industry and independent sources. As noted in this Annual Report, the National Association of Realtors ("NAR"), the Federal National Mortgage Association ("Fannie Mae") and the Federal Home Loan Mortgage Corporation ("Freddie Mac") were the primary sources for third-party industry data and forecasts. While data provided by NAR and Fannie Mae are two indicators of the direction of the residential housing market, we believe that homesale statistics will continue to vary between us and NAR and Fannie Mae because:

• | they use survey data and estimates in their historical reports and forecasting models, which are subject to sampling error, whereas we use data based on actual reported results; |

• | there are geographical differences and concentrations in the markets in which we operate versus the national market. For example, many of our company owned brokerage offices are geographically located where average homesale prices are generally higher than the national average and therefore NAR survey data will not correlate with NRT's results; |

• | comparability is also impaired due to NAR’s utilization of seasonally adjusted annualized rates whereas we report actual period-over-period changes and their use of median price for their forecasts compared to our average price; |

• | NAR historical data is subject to periodic review and revision and these revisions have been and could be material in the future; and |

• | NAR and Fannie Mae generally update their forecasts on a monthly basis and a subsequent forecast may change materially from a forecast that was previously issued. |

While we believe that the industry data presented herein is derived from the most widely recognized sources for reporting U.S. residential housing market statistical data, we do not endorse or suggest reliance on this data alone.

Forecasts regarding rates of home ownership, median sales price, volume of homesales, and other metrics included in this Annual Report to describe the housing industry are inherently uncertain or speculative in nature and actual results for any period could materially differ. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but such information may not be accurate or complete. We have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon therein. Statements as to our market position are based on market data currently available to us. While we are not aware of any misstatements regarding industry data provided herein, our estimates involve risks and uncertainties and are subject to change based upon various factors, including those discussed under the headings "Risk Factors" and "Forward-Looking Statements." Similarly, we believe our internal research is reliable, even though such research has not been verified by any independent sources.

3

PART I

Except as otherwise indicated or unless the context otherwise requires, the terms "we," "us," "our," "our company," "Realogy," "Realogy Holdings" and the "Company" refer to Realogy Holdings Corp., a Delaware corporation, and its consolidated subsidiaries, including Realogy Intermediate Holdings LLC, a Delaware limited liability company ("Realogy Intermediate"), and Realogy Group LLC, a Delaware limited liability company ("Realogy Group"). Neither Realogy Holdings, the indirect parent of Realogy Group, nor Realogy Intermediate, the direct parent company of Realogy Group, conducts any operations other than with respect to its respective direct or indirect ownership of Realogy Group. As a result, the consolidated financial positions, results of operations and cash flows of Realogy Holdings, Realogy Intermediate and Realogy Group are the same.

Realogy Holdings is not a party to the Senior Secured Credit Facility and Term Loan A Facility and certain references in this Annual Report to our consolidated indebtedness exclude Realogy Holdings with respect to indebtedness under the Senior Secured Credit Facility and Term Loan A Facility. In addition, while Realogy Holdings is a guarantor of Realogy Group's obligations under its unsecured notes, Realogy Holdings is not subject to the restrictive covenants in the indentures governing such indebtedness.

As used in this Annual Report, the terms "3.375% Senior Notes," "4.50% Senior Notes," "5.25% Senior Notes" and "4.875% Senior Notes" refer to our 3.375% Senior Notes due 2016 (paid in full at maturity in 2016), our 4.50% Senior Notes due 2019, our 5.25% Senior Notes due 2021 and our 4.875% Senior Notes due 2023, respectively, and referred to collectively as "Unsecured Notes."

Item 1. Business.

Our Company

We are the preeminent and most integrated provider of residential real estate services in the U.S. We are the world's largest franchisor of residential real estate brokerages with some of the most recognized brands in the real estate industry, the largest owner of U.S. residential real estate brokerage offices, one of the largest U.S. and a leading global provider of outsourced employee relocation services and a significant provider of title and settlement services.

Our revenue is derived on a fee-for-service basis, and given our breadth of complementary service offerings, we are able to generate fees from multiple aspects of a residential real estate transaction. Our operating platform is supported by our portfolio of industry leading franchise brokerage brands, including Century 21®, Coldwell Banker®, Coldwell Banker Commercial®, ERA®, Sotheby's International Realty® and Better Homes and Gardens® Real Estate. We also own and operate Corcoran®, Citi HabitatsSM and ZipRealty® brands. Our multiple brands and operations allow us to derive revenue from many different segments of the residential real estate market, in many different geographies and at varying price points.

Segment Overview

We report our operations in four segments, each of which receives fees based upon services performed for our customers: Real Estate Franchise Services ("RFG"), Company Owned Real Estate Brokerage Services ("NRT"), Relocation Services ("Cartus®") and Title and Settlement Services ("TRG"). See "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the financial statements, including the notes thereto, included elsewhere in this Annual Report, for further information on our reportable segments.

Real Estate Franchise Services. We are the largest franchisor of residential real estate brokerages in the world through our portfolio of well-known brokerage brands, including Century 21®, Coldwell Banker®, Coldwell Banker Commercial®, ERA®, Sotheby's International Realty® and Better Homes and Gardens® Real Estate. At December 31, 2016, our real estate franchise systems (inclusive of our company owned brokerage operations) had approximately 14,100 offices worldwide in 112 countries and territories. This included approximately 6,000 brokerage offices in the U.S. and approximately 273,200 independent sales associates worldwide, including approximately 186,300 independent sales associates operating under our franchise and proprietary brands in the U.S. The average tenure among U.S. franchisees is approximately 21 years as of December 31, 2016. Our franchisees pay us fees for the right to operate under one of our trademarks and to enjoy the benefits of the systems and business enhancing tools provided by our real estate franchise operations. In addition to highly competitive brands that provide unique offerings to our franchisees, we support our franchisees with dedicated national marketing and servicing programs, technology including the Zap® technology platform described below, training and education to facilitate our franchisees in growing their business and increasing their revenue and profitability. We believe

4

that one of our strengths is the strong relationships that we have with our franchisees, as evidenced by our 98% retention rate as of December 31, 2016. Our retention rate represents the annual franchisee gross commission income for the year ended December 31, 2015 generated by our franchisees that remain in our franchise systems as of December 31, 2016, measured against the annual gross commission income of all franchisees for the year ended December 31, 2015.

Our wholly-owned subsidiary, ZapLabs LLC (which changed its name from ZipRealty LLC in 2016) is the developer of our proprietary technology platform for the real estate brokerages and independent sales associates in our franchise system as well as their customers. During 2016, we rolled out ZapLabs' comprehensive, integrated Zap technology platform to approximately 1,110 franchisees, bringing the total enrolled to 1,500 at December 31, 2016 of our approximately 2,600 franchisees. Consistent with our previously disclosed plan, we anticipate rolling this product out to a majority of our remaining franchisees within the next twelve months. We believe the Zap technology platform will increase the value proposition to franchisees, independent sales associates and customers as well as improve the productivity of independent sales associates.

Company Owned Real Estate Brokerage Services. We own and operate the largest residential real estate brokerage business in the U.S. under the Coldwell Banker®, Corcoran®, Sotheby's International Realty®, ZipRealty® and Citi HabitatsSM brand names. We offer full-service residential brokerage services through approximately 790 company owned brokerage offices with approximately 47,500 independent sales associates in more than 50 of the 100 largest metropolitan areas of the U.S. NRT, as the broker for a home buyer or seller, derives revenues primarily from gross commission income received at the closing of real estate transactions. NRT also has relationships with developers, primarily in major cities, to provide marketing and brokerage services in new developments. To complement its residential brokerage services, NRT offers home ownership services that include comprehensive single-family residential property management in many of the nation's largest rental markets. In addition, we participate in the mortgage process through our 49.9% ownership of PHH Home Loans LLC ("PHH Home Loans"), our home mortgage venture with PHH. See Item 7. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" under the heading "Recent Developments" for information regarding the formation of our new mortgage origination joint venture.

Relocation Services. We are a leading global provider of outsourced employee relocation services. We are one of the largest providers of such services in the U.S. and also operate in key international relocation destinations. We offer a broad range of world-class employee relocation services designed to manage all aspects of an employee's move to facilitate a smooth transition in what otherwise may be a complex and difficult process for the employee and employer. Our relocation services business serves corporations, including 56% of the Fortune 50 companies. We also service affinity organizations such as insurance companies and credit unions that provide our services to their members. In 2016, we assisted in approximately 163,000 corporate and affinity relocations in nearly 150 countries for approximately 800 active clients. As of December 31, 2016, our top 25 relocation clients had an average tenure of approximately 20 years with us. Member brokers of the Cartus Broker Network, including certain franchisees and NRT, receive referrals from the relocation services, affinity services and from each other in exchange for a referral fee.

Title and Settlement Services. We assist with the closing of real estate transactions by providing full-service title and settlement (i.e., closing and escrow) services to customers, real estate companies, including our company owned real estate brokerage and relocation services businesses, as well as a targeted channel of large financial institution clients. In 2016, TRG was involved in the closing of approximately 204,000 transactions of which approximately 60,000 related to NRT. In addition to our own title and settlement services, we also coordinate a nationwide network of attorneys, title agents and notaries to service financial institution and relocation clients on a national basis. We also serve as an underwriter of title insurance policies in connection with residential and commercial real estate transactions.

* * *

Our headquarters is located at 175 Park Avenue, Madison, New Jersey 07940. Our general telephone number is (973) 407-2000. We were incorporated on December 14, 2006 in the State of Delaware. The Company files electronically with the Securities and Exchange Commission (the "SEC") required reports on Form 8-K, Form 10-Q and Form 10-K; proxy materials; ownership reports for insiders as required by Section 16 of the Securities Exchange Act of 1934; registration statements and other forms or reports as required. Certain of the Company's officers and directors also file statements of changes in beneficial ownership on Form 4 with the SEC. The public may read and copy any materials that the Company has filed with the SEC at the SEC's Public Reference Room located at 100 F Street, NE, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 800-SEC-0330. Such materials may also be accessed electronically on the SEC's Internet site (www.sec.gov). We maintain an Internet website at http://www.realogy.com and make available free of charge on or through our website our annual report

5

on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, Section 16 reports and any amendments to these reports in the Investor Relations section of our website as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. Our website address is provided as an inactive textual reference. The contents of our website are not incorporated by reference herein or otherwise a part of this Annual Report.

Industry Trends

Industry definition. We primarily operate in the U.S. residential real estate industry, which is approximately a $1.7 trillion industry based on 2016 transaction volume (i.e. average homesale price times number of new and existing homesale transactions) and derive substantially all of our revenues from serving the needs of buyers and sellers of existing homes rather than those of new homes. Residential real estate brokerage companies typically realize revenues in the form of a commission that is based on a percentage of the price of each home sold. As a result, the real estate industry generally benefits from rising home prices and increasing homesale transactions (and conversely is adversely impacted by falling prices and lower homesale transactions). We believe that existing homesale transactions and the services associated with these transactions, such as mortgage origination, title services and relocation services, represent one of the most attractive segment of the residential real estate industry for the following reasons:

• | the existing homesales segment represents a significantly larger addressable market than new homesales. Of the approximately 6.0 million homesales in the U.S. in 2016, NAR estimates that approximately 5.5 million were existing homesales, representing approximately 91% of the overall sales as measured in units; |

• | existing homesales afford us the opportunity to represent either the buyer or the seller and in some cases both the buyer and the seller; and |

• | we are able to generate revenues from ancillary services provided to our customers. |

We also believe that the traditional broker-assisted business model compares favorably to alternative channels of the residential brokerage industry, such as discount brokers and "for sale by owner" for the following reasons:

• | a real estate transaction has certain characteristics that we believe are best suited for full-service brokerages, such as: |

◦ | the average homesale transaction size is very high and generally is the largest transaction one does in a lifetime; |

◦ | homesale transactions occur infrequently; |

◦ | there is a compelling need for personal service as home preferences are unique to each buyer; |

◦ | a high level of support is required given the complexity associated with the process; |

◦ | there is a high variance in price, depending on neighborhood, floor plan, architecture, fixtures, and outdoor space; and |

◦ | there is a need for specific marketing and technology services and support given the complexity of the transaction. |

• | while substantially all homebuyers start their search for a home using the internet, according to NAR, 88% of homes were sold using an agent or broker in 2016 compared to 79% in 2001. We believe that the enhanced service and value offered by a traditional agent or broker is such that using a traditional agent or broker will continue to be the primary method of buying and selling a home in the long term. |

Cyclical nature of industry. The U.S. residential real estate industry is cyclical, but has historically shown strong growth over time. Based on information published by NAR, existing homesale units increased at a compound annual growth rate, or CAGR, of 2.0% from 1972 through 2016, with 28 annual increases, versus 16 annual decreases. During that same period, median existing homesale prices increased at a CAGR of 4.9% (not adjusted for inflation) from 1972 through 2016, a period that included four economic recessions. According to NAR, the existing homesale transaction volume (median homesale price times existing homesale transactions) grew at a CAGR of 7.0% from 1972 through 2016.

Commencing in the second half of 2005 and continuing through 2011, the U.S. residential real estate industry was in a significant and lengthy downturn. Based upon data published by NAR from 2005 to 2011, the number of annual U.S. existing homesale transactions declined by 40% and the median existing homesale price declined by 24%.

Beginning in 2012, the U.S. residential real estate industry began its recovery with the first two years—2012 and 2013—showing double digit volume growth with single digit annual growth thereafter. Based upon data published by NAR from

6

2011 to 2016, the number of annual U.S. existing homesale units and the median existing homesale price improved by 28% and 41%, respectively.

Long-term demographics. We believe that long-term demand for housing and the growth of our industry is primarily driven by affordability, the economic health of the U.S. economy, demographic trends such as population growth, increases in the number of U.S. households, low interest rates, increases in renters that qualify as homebuyers and locally based factors. We believe that the residential real estate market will benefit over the long term from expected positive fundamentals, including the following factors:

• | based on U.S. Census data and NAR, from 1991 through 2016, the average number of existing homesale transactions as a percentage of U.S. households was approximately 4.4%, compared to an average of approximately 3.9% from 2007 through 2016. During the same period, the number of U.S. households grew from 94 million in 1991 to 126 million in 2016; and |

• | according to the 2016 State of the Nation's Housing Report compiled by the Harvard Joint Center for Housing Studies, household growth is projected to average over 1.3 million annually over the coming decade. The millennial generation is poised to form millions of new households over the next decade. |

Participation in Multiple Aspects of the Residential Real Estate Market

We participate in services associated with many aspects of the residential real estate market. Our four complementary businesses and mortgage joint venture work together, allowing us to generate revenue at various points in a residential real estate transaction, including the purchase or sale of homes, corporate relocation and affinity services, settlement and title services, and franchising of our brands. The businesses each benefit from our deep understanding of the industry, strong relationships with real estate brokers, sale associates and other real estate professionals and expertise across the transactional process. Unlike other industry participants who offer only one or two services, we can offer homeowners, our franchisees and our corporate and affinity clients ready access to numerous associated services that facilitate and simplify the home purchase and sale process. These services provide further revenue opportunities for our owned businesses and those of our franchisees. Specifically, our brokerage offices and those of our franchisees participate in purchases and sales of homes involving relocations of corporate transferees and affinity members using Cartus® relocation services and we offer customers (purchasers and sellers) of both our owned and franchised brokerage businesses convenient title and settlement services. These services produce incremental revenues for our businesses and franchisees. In addition, we participate in the mortgage process through our 49.9% ownership of PHH Home Loans. All four of our businesses and our mortgage joint venture can derive revenue from the same real estate transaction.

7

Our Brands

Our brands are among the most well-known and established real estate brokerage brands in the real estate industry. Our real estate franchise brands are listed in the following chart, which includes information as of December 31, 2016 for both our franchised and company owned offices:

Franchise Brands (1) |  |  |  |  |  |  | |||||||||||

Worldwide Offices (2) | 7,300 | 3,000 | 2,300 | 850 | 300 | 180 | |||||||||||

Worldwide Brokers and Sales Associates (2) | 110,800 | 88,400 | 37,900 | 20,300 | 10,900 | 2,100 | |||||||||||

U.S. Annual Sides | 420,184 | 727,415 | 128,812 | 111,950 | 70,980 | N/A | |||||||||||

# of Countries with Owned or Franchised Operations | 77 | 49 | 31 | 66 | 3 | 47 | |||||||||||

Characteristics | World's largest residential real estate sales organization Identified by consumers as the most recognized name in real estate Significant international office footprint | Longest running national real estate brand in the U.S. (since 1906) Known for innovative consumer services, marketing and technology | Driving value through innovation and collaboration Highest percentage of international offices among international brands | Synonymous with luxury Strong ties to auction house established in 1744 Rapid international growth | Growing real estate brand launched in July 2008 Unique relationship with a leading media company, including largest lifestyle magazine in the U.S. | A commercial real estate franchise organization Serves a wide range of clients from corporations to small businesses to individual clients and investors | |||||||||||

_______________

(1) | Does not include Corcoran®, ZipRealty® and Citi HabitatsSM. |

(2) | Includes an aggregate of 8,100 offices and 86,900 related brokers and sales associates of non-US franchisees and franchisors, based upon information they reported to us. |

Real Estate Franchise Services

Our primary objectives as the largest franchisor of residential real estate brokerages in the world are to sell new franchises, retain and expand existing franchises and most importantly, provide branding and support to our franchisees. At December 31, 2016, our real estate franchise systems had approximately 14,100 offices worldwide in 112 countries and territories in North and South America, Europe, Asia, Africa, the Middle East and Australia, including approximately 6,000 brokerage offices in the U.S.

We derive substantially all of our real estate franchising revenues from royalties received under long-term franchise agreements with our domestic franchisees (typically ten years in duration) and NRT. These royalties are based on a percentage of the franchisees' sales commission earned from closed homesale sides (either the "buy" side and/or the "sell" side of a real estate transaction), which we refer to as gross commission income. Our franchisees pay us royalties, net of volume incentives achieved (other than NRT), for the right to operate under one of our trademarks and to utilize the benefits of the franchise systems. We provide our franchisees with systems and tools that are designed to help our franchisees serve their customers, attract new or retain existing independent sales associates, and support our franchisees with servicing programs, technology including the Zap® technology platform described under "Marketing and Technology," and education, as well as branding-related marketing which is funded through contributions by our franchisees and us (including NRT). We operate and maintain an Internet-based reporting system for our domestic franchisees which generally allows them to electronically transmit listing information and other relevant reporting data to our websites. We also own and operate websites for each of our brands for the benefit of our franchisees.

8

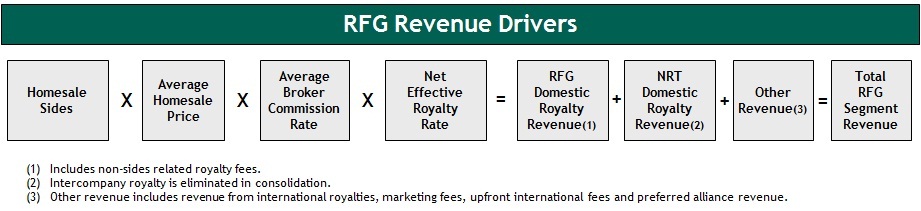

RFG's domestic annual net royalty revenues from franchisees other than our company owned brokerages can be represented by multiplying (1) that year's total number of closed homesale sides in which those franchisees participated by (2) the average sale price of those homesales by (3) the average brokerage commission rate charged by these franchisees by (4) RFG's net effective royalty rate. The net effective royalty rate represents the average percentage of our franchisees' commission revenues paid to us as a royalty, net of volume incentives achieved and does not include the effect of non-standard incentives granted to franchisees. Non-standard incentives may be used as consideration for new or renewing franchisees, however, most of our franchisees do not receive these non-standard incentives. In addition, in contrast to royalties and volume incentives, they are not homesale transaction based. We have accordingly excluded the non-standard incentives from the calculation of the net effective royalty rate. The domestic royalty revenue from NRT is calculated by multiplying homesale sides by average sale price by average brokerage commission rate by 6% royalty rate. NRT does not receive volume incentives or non-standard incentives. In addition to domestic royalty revenue, RFG earns revenue from marketing fees, the preferred alliance program, international affiliates and upfront international fees. The following chart illustrates the key drivers for revenue earned by RFG:

We believe one of our strengths is the strong relationships that we have with our franchisees as evidenced by the retention rate of 98% as of December 31, 2016. Our retention rate represents the annual franchisee gross commission income for the year ended December 31, 2015 generated by our franchisees that remain in our franchise systems as of December 31, 2016, measured against the annual gross commission income of all franchisees for the year ended December 31, 2015. On average, our domestic franchisees' tenure with our brands was approximately 21 years as of December 31, 2016. During 2016, none of our franchisees (other than NRT) generated more than 1% of our real estate franchise business revenues.

The franchise agreements impose restrictions on the business and operations of the franchisees and require them to comply with the operating and identity standards set forth in each brand's policy and procedures manuals. A franchisee's failure to comply with these restrictions and standards could result in a termination of the franchise agreement. The franchisees generally are not permitted to terminate the franchise agreements prior to their expiration, and in those cases where termination rights do exist, they are very limited (e.g., if the franchisee retires, becomes disabled or dies). Generally, new domestic franchise agreements have a term of ten years and require the franchisees to pay us an initial franchise fee for the franchisee's principal office plus, upon the receipt of any commission income, a royalty fee in most cases equal to 6% of their commission income. Each of our franchise systems (other than Coldwell Banker Commercial®) offers a volume incentive program, whereby each franchisee is eligible to receive a refund of a portion of the royalties paid upon the satisfaction of certain conditions. The volume incentive is calculated for each eligible franchisee as a progressive percentage of each franchisee's annual gross revenue (paid timely) for each calendar year. Under the current form of the franchise agreements, the volume incentive varies for each franchise system, and generally ranges from zero to 3% of gross revenues. We provide a detailed table to each franchisee that describes the gross revenue thresholds required to achieve a volume incentive and the corresponding incentive amounts. We reserve the right to increase or decrease the percentage and/or dollar amounts in the table on an annual basis, subject to certain limitations. Our company owned brokerage offices do not participate in the volume incentive program.

Each franchise system requires all franchisees and company owned offices to make monthly contributions to marketing funds maintained by each brand. These contributions are used primarily for the development, implementation, production, placement and payment of national and regional advertising, marketing, promotions, public relations and/or other marketing-related activities, such as lead generation, all to promote and further the recognition of each brand and its independent franchisees. In addition to the contributions from franchisees and company owned offices, the Real Estate Franchise Services group is generally required to make contributions to one of the marketing funds and may make discretionary contributions (at its option) to any of the marketing funds.

9

The 2014 acquisition of ZipRealty reflects the Company's ongoing commitment to enhancing the value proposition we provide to our franchisees, including technology-enabled solutions. During 2016, we continued the roll out of our ZapLabs' comprehensive, integrated Zap technology platform and at December 31, 2016 had approximately 1,500 of our approximately 2,600 franchisees using the platform. Consistent with our previously disclosed plan, we anticipate rolling this product out to a majority of our remaining franchisees over the next twelve months. ZapLabs has developed the Zap technology platform from a real estate brokerage perspective to enhance the real estate transaction experience for customers, independent sales associates and our franchisees. We believe the Zap technology platform will increase the value proposition to our franchisees, their independent sales associates and their customers by:

• | aiding in obtaining additional homesale transactions for our franchisees and their independent sales associates; |

• | connecting those associates to a predictive customer relationship management (CRM) tool; and |

• | informing them with valuable client insight to help those associates increase their productivity. |

Under certain circumstances, we extend conversion notes (development advance notes were issued prior to 2009) to eligible franchisees for the purpose of providing an incentive to join the brand, to renew their franchise agreements, or to facilitate their growth opportunities. Growth opportunities include the expansion of franchisees' existing businesses by opening additional offices, through the consolidation of operations of other franchisees, as well as through the acquisition of independent sales associates and offices operated by independent brokerages. Many franchisees use the proceeds from the conversion notes to change stationery, signage and marketing materials, upgrade technology and websites, or to assist in acquiring companies or recruiting agents. The notes are not funded until appropriate credit checks and other due diligence matters are completed and the business is opened and operating under one of our brands. Upon satisfaction of certain revenue performance based thresholds, the notes are forgiven ratably over the term of the franchise agreement. If the revenue performance thresholds are not met, franchisees may be required to repay all or a portion of the outstanding notes.

In addition to offices owned and operated by our franchisees, we, through NRT, own and operate approximately 750 offices under the Coldwell Banker®, Coldwell Banker Commercial® and Sotheby's International Realty® brand names. NRT pays intercompany royalty fees and marketing fees to our Real Estate Franchise Services Segment in connection with its operation of these offices. These fees are recognized as income or expense by the applicable segment level and eliminated in the consolidation of our businesses.

In the U.S., we employ a direct franchising model whereby we contract with and provide services directly to independent owner-operators. Elsewhere, for all brands other than Sotheby's International Realty, we generally employ a master franchise model, whereby we contract with a qualified third party to build a franchise network in the country or region in which franchising rights have been granted. In the case of Sotheby's International Realty, a direct franchising model is generally utilized. Under both the direct and the master franchise model, we typically enter into long-term franchise agreements (often 25 years in duration) and receive an initial area development fee and ongoing royalties. Under the master franchise model, the ongoing royalties we receive are generally a percentage of the royalties received by the master franchisor from its franchisees with which it contracts. Under the direct franchise model, a royalty fee is paid to us on transactions conducted by our franchisees in the applicable country or region.

We also offer third-party service providers an opportunity to market their products to our franchisees and their independent sales associates and customers through our preferred alliance program. To participate in this program, service providers generally agree to provide preferred pricing to our franchisees and/or their customers or independent sales associates and to pay us a combination of an initial licensing or access fee, subsequent marketing fees and/or commissions based upon our franchisees' or independent sales associates' usage of the preferred alliance vendors.

We own the trademarks Century 21®, Coldwell Banker®, Coldwell Banker Commercial®, ERA® and related trademarks and logos, and such trademarks and logos are material to the businesses that are part of our real estate franchise segment. Our franchisees and our subsidiaries actively use these trademarks, and all of the material trademarks are registered (or have applications pending) with the United States Patent and Trademark Office as well as with corresponding trademark offices in major countries worldwide where these businesses have significant operations.

We have an exclusive license to own, operate and franchise the Sotheby's International Realty® brand to qualified residential real estate brokerage offices and individuals operating in eligible markets pursuant to a license agreement with SPTC Delaware LLC, a subsidiary of Sotheby's ("Sotheby's"). Such license agreement has a 100-year term, which consists of an initial 50-year term ending February 16, 2054 and a 50-year renewal option. We pay a licensing fee to Sotheby's for the use of the Sotheby's International Realty® name equal to 9.5% of the net royalties earned by our Real Estate Franchise

10

Services Segment attributable to franchisees affiliated with the Sotheby's International Realty® brand, including our company owned offices.

In October 2007, we entered into a long-term license agreement to own, operate and franchise the Better Homes and Gardens® Real Estate brand from Meredith. The license agreement between Realogy and Meredith is for a 50-year term, with a renewal option for another 50 years at our option. We pay a licensing fee to Meridith for the use of the Better Homes and Gardens® Real Estate brand name equal to 9.0% of the net royalties earned by our Real Estate Franchise Services Segment, subject to a minimum annual licensing fee.

Each of our brands has a consumer website that offers real estate listings, contacts and services. Century21.com, coldwellbanker.com, coldwellbankercommercial.com, sothebysrealty.com, era.com and bhgrealestate.com are the official websites for the Century 21®, Coldwell Banker®, Coldwell Banker Commercial®, Sotheby's International Realty®, ERA® and Better Homes and Gardens® Real Estate franchise systems, respectively. The contents of these websites are not incorporated by reference herein or otherwise a part of this Annual Report.

Company Owned Real Estate Brokerage Services

Through our subsidiary, NRT, we own and operate a full-service real estate brokerage business in more than 50 of the 100 largest metropolitan areas in the U.S. Our company owned real estate brokerage business operates under the Coldwell Banker® and Sotheby's International Realty® franchised brands as well as proprietary brands that we own, but do not currently franchise, such as Corcoran®, ZipRealty® and Citi HabitatsSM. As of December 31, 2016, we had approximately 790 company owned brokerage offices, approximately 5,200 employees and approximately 47,500 independent sales associates working with these company owned offices.

Our company owned real estate brokerage business derives revenue primarily from gross commission income received serving as the broker at the closing of real estate transactions. For the year ended December 31, 2016, our average homesale broker commission rate was 2.46% which represents the average commission rate earned on either the "buy" side or the "sell" side of a homesale transaction. Gross commission income is also earned on non-sale transactions such as home rentals. NRT, as a franchisee of RFG, pays a royalty fee of 6% per transaction to RFG from the commission earned on a real estate transaction. The following chart illustrates the key drivers for revenue earned by NRT:

In addition, as a full-service real estate brokerage company, we promote the complementary services of our relocation and title and settlement services businesses, as well as PHH Home Loans. We believe we provide integrated services that enhance the customer experience.

When we assist the seller in a real estate transaction, independent sales associates generally provide the seller with a full-service marketing program, which may include developing a direct marketing plan for the property, assisting the seller in pricing the property and preparing it for sale, listing it on multiple listing services, advertising the property (including on websites), showing the property to prospective buyers, assisting the seller in sale negotiations, and assisting the seller in preparing for closing the transaction. When we assist the buyer in a real estate transaction, independent sales associates generally help the buyer in locating specific properties that meet the buyer's personal and financial specifications, show properties to the buyer, assist the buyer in negotiating (where permissible) and preparing for closing the transaction.

At December 31, 2016, we operated approximately 90% of our offices under the Coldwell Banker® brand name, 5% of our offices under the Sotheby's International Realty® brand name and 5% of our offices under the Corcoran®, Citi HabitatsSM and ZipRealty® brand names combined. Our offices are geographically diverse with a strong presence in the east and west coast areas, where home prices are generally higher. We operate our Coldwell Banker® offices in numerous regions throughout the U.S., our Sotheby's International Realty® offices in several regions throughout the U.S, and Corcoran® offices in New York City, the Hamptons (New York), and Palm Beach, Florida.

We intend to grow our business both organically and through strategic acquisitions. To grow organically, we will focus on working with office managers to attract, retain and effectively coordinate with independent sales associates who can

11

successfully engage and promote transactions from new and existing clients. To complement our residential brokerage services, NRT offers home ownership services that include comprehensive single-family residential property management in many of the nation's largest rental markets.

We are continuously evaluating acquisitions that will allow us to enter into new markets and to profitably expand our existing markets through "tuck-in" acquisitions. Following the completion of an acquisition, we tend to consolidate the newly acquired operations with our existing operations. By consolidating operations, we reduce or eliminate duplicative costs, such as advertising, rent and administrative support. By utilizing our existing infrastructure to coordinate with a broader network of independent sales associates and revenue base, we can enhance the profitability of our operations. We also seek to enhance the profitability of newly acquired operations by strategies that increase the productivity of the newly affiliated independent sales associates. We offer these independent sales associates supplemental tools and marketing information that are often unavailable at smaller firms, such as access to sophisticated information technology and ongoing technical support, increased brand advertising and brand marketing support, relocation referrals, and a wide offering of brokerage-related services.

Our real estate brokerage business has a contract with Cartus under which the brokerage business provides brokerage services to relocating employees of the clients of Cartus. When receiving a referral from Cartus, our brokerage business seeks to assist the relocating employee in completing a homesale or home purchase. Upon completion of a homesale or home purchase, our brokerage business receives a commission on the purchase or sale of the property and is obligated to pay Cartus a portion of such commission as a referral fee. We believe that these fees are comparable to the fees charged by other relocation companies.

PHH Home Loans, our home mortgage venture with PHH, a publicly traded company, has a 50-year term, subject to earlier termination. We own 49.9% of the home mortgage venture and PHH owns the remaining 50.1%. All mortgage loans originated by the venture are sold to PHH or other third-party investors after a hold period, and PHH Home Loans does not hold any mortgage loans for investment purposes or perform servicing functions for any loans it originates. Accordingly, we have no mortgage servicing rights asset risk. See Item 7. "Management’s Discussion and Analysis of Financial Condition and Results of Operations" under the heading "Recent Developments" for information regarding the formation of our new mortgage origination joint venture.

Relocation Services

Through our subsidiary, Cartus, we are a leading global provider of outsourced employee relocation services. We primarily offer corporate clients employee relocation services, such as:

• | homesale assistance, including: |

◦ | the valuation, inspection, purchasing and selling of a transferee's home; |

◦ | the issuance of home equity advances to transferees permitting them to purchase a new home before selling their current home (these advances are generally guaranteed by the client); |

◦ | certain home management services; |

◦ | assistance in locating a new home; and |

◦ | closing on the sale of the old home, generally at the instruction of the client; |

• | expense processing, relocation policy counseling, relocation-related accounting, including international assignment compensation services, and other consulting services; |

• | arranging household goods moving services, approximately 64,000 domestic and international shipments in 2016, and providing support for all aspects of moving a transferee's household goods, including the handling of insurance and claim assistance, invoice auditing and quality control; |

• | coordinating visa and immigration support, intercultural and language training, and expatriation/repatriation counseling and destination services; and |

• | group move management services providing coordination for moves involving a large number of transferees to or from a specific regional area over a short period of time. |

The wide range of our services allows our Cartus clients to outsource their entire relocation programs to us.

In 2016, we assisted in approximately 163,000 corporate and affinity relocations in nearly 150 countries for approximately 800 active clients, including 56% of the Fortune 50 companies as well as affinity organizations. Cartus has

12

operations in the U.S. and internationally in the United Kingdom, Canada, Hong Kong, Singapore, China, India, Brazil, Germany, France, Switzerland and the Netherlands.

Substantially all homesale service transactions for clients are classified as "no risk." Under "no risk" business, the client is responsible for reimbursement of all direct expenses associated with the homesale. Such expenses include, but are not limited to, appraisal, inspection and real estate brokerage commissions. The client also bears the risk of loss on the resale of the transferee's home. Clients are responsible for reimbursement of all other direct costs associated with the relocation including, but not limited to, costs to move household goods, mortgage origination points, temporary living and travel expenses. Generally, we fund the direct expenses associated with the homesale as well as those associated with the relocation on behalf of the client and the client then reimburses us for these costs plus interest charges on the advanced funds. This limits our exposure on "no risk" homesale services to the credit risk of our clients rather than to the potential fluctuations in the real estate market or to the creditworthiness of the individual transferring employee. Historically, due to the credit quality of our clients, we have had minimal losses with respect to these "no risk" homesale services.

The "at risk" business that we conduct is minimal. In "at risk" homesale service transactions, we acquire the home being sold by relocating employees, incur the cost for all direct expenses (acquisition, carrying and selling costs) associated with the homesale and bear any loss on the sale of the home.

Substantially all of our contracts with our relocation clients are terminable at any time at the option of the client and are non-exclusive. If a client terminates its contract, we will be compensated for all services performed up to the time of termination and reimbursed for all expenses incurred to the time of termination.

There are a number of different revenue streams associated with relocation services. We earn referral commissions primarily from real estate brokers and household goods moving companies that provide services to the transferee. Clients may also pay transactional fees for the services performed. We also earn net interest income which represents interest earned from clients on the funds we advance on behalf of the transferring employee net of costs associated with the securitization obligations used to finance these payments. Cartus measures operating performance based on initiations, which represent the total number of transferees and affinity members we serve, and referrals, which represent the number of referrals from which we earn revenue from real estate brokers.

About 15% of our relocation revenue in 2016 was derived from our affinity services, which provides real estate services, including home buying and selling assistance, as well as mortgage assistance to organizations such as insurance companies and credit unions that have established members who are buying or selling a home. Often these organizations offer our affinity services to their members at no cost and, where permitted, provide their members with a financial incentive for using these services. These member benefits and services help the organizations attract new members and retain current members.

We also manage the Cartus Broker Network, which is a network of real estate brokers consisting of our company owned brokerage operations, select franchisees and independent real estate brokers who have been approved to become members. Cartus requires experienced brokers and independent sales associates and obtains background checks on all members of the network. Member brokers of the Cartus Broker Network receive referrals from our relocation services, affinity business and each other in exchange for a referral fee. The Cartus Broker Network closed approximately 79,000 real estate transactions in 2016 related to relocation, affinity, and broker-to-broker activity.

The following chart illustrates the key drivers for revenue generated by Cartus:

13

Title and Settlement Services

Our title and settlement services business, TRG, provides full-service title and settlement (i.e., closing and escrow) services to real estate companies and financial institutions. We act in the capacity of a title agent and sell title insurance to property buyers and mortgage lenders. We are licensed as a title agent in 42 states and Washington, D.C., and have physical locations in 25 states and Washington, D.C. We issue title insurance policies on behalf of large national underwriters as well as through our Dallas-based subsidiary, Title Resources Guaranty Company ("Title Resources"). Title Resources is a title insurance underwriter licensed in 29 states and Washington, D.C. We operate mostly in major metropolitan areas. As of December 31, 2016, we had approximately 439 offices, approximately 221 of which are co-located within one of our company owned brokerage offices.

Virtually all lenders require their borrowers to obtain title insurance policies at the time mortgage loans are made on real property. The terms and conditions upon which the real property will be insured are determined in accordance with the standard policies and procedures of the title underwriter. When our title agencies sell title insurance, the title search and examination function is performed by the agent. The title agent and underwriter split the premium. The amount of such premium "split" is determined by agreement between the agency and underwriter, or is promulgated by state law. We derive revenue through fees charged in real estate transactions for rendering the services described above, fees charged for escrow and closing services, and a percentage of the title premium on each title insurance policy sold. We have entered into underwriting agreements with various underwriters, which state the conditions under which we may issue a title insurance policy on their behalf. For policies issued through our agency operations, assuming no negligence on our part, we are not typically liable for losses under those policies; rather the title insurer is typically liable for such losses.

Our company owned brokerage operations are the principal source of our title and settlement services business for homesale transactions. Other sources of our title and settlement services homesale business include our real estate franchise business, Cartus and unaffiliated brokerage operations. For refinance transactions, we generate title and escrow revenues from PHH and other financial institutions throughout the mortgage lending industry. Many of our offices have subleased space from, and are co-located within, our company owned brokerage offices. The capture rate of our title and settlement services business from company owned brokerage operations was approximately 41% in 2016.

We coordinate a national network of escrow and closing agents (some of whom are our employees, while others are attorneys in private practice and independent title companies) to provide full-service title and settlement services to a broad-based group that includes lenders, home buyers and sellers, developers and independent real estate sales associates. Our role is generally that of an intermediary managing the completion of all the necessary documentation and services required to complete a real estate transaction.

Our title and settlement services business measures operating performance based on purchase and refinance closing units and the related title premiums and escrow fees earned on such closings. In addition, we measure net title premiums earned for title policies issued by our underwriting operation.

The following chart illustrates the key drivers for revenue generated by our title and settlement services business:

We intend to grow our title and settlement services business by attracting title and escrow sales associates in existing markets and by completing acquisitions to expand our geographic footprint or complement existing operations. We also intend to continue to increase our capture rate of title business from our NRT homesale sides. In addition, we expect to continue to grow and diversify our lender channel and our underwriting businesses by expanding and adding clients and increasing our agent base, respectively.

14

Competition

Real Estate Brokerage Industry. The residential real estate brokerage industry is highly competitive with low barriers to entry for new participants. Recruitment and retention of independent sales associates and independent sales associate teams are critical to the business and financial results of a brokerage—whether or not they are affiliated with a franchisor. Most of a brokerage's real estate listings are sourced through the sphere of influence of their independent sales associates, notwithstanding the growing influence of internet-generated leads. Competition for independent sales associates in our industry is high and has intensified particularly with respect to more productive independent sales associates. Competition for independent sales associates is generally subject to numerous factors, including remuneration (such as sales commission percentage and other financial incentives paid to independent sales associates), other expenses charged to independent sales associates, leads or business opportunities generated for the independent sales associate from the brokerage, independent sales associates' perception of the value of the broker's brand affiliation, marketing and advertising efforts by the brokerage, the office manager, staff and fellow independent sales associates with whom they collaborate daily and technology, continuing professional education, and other services provided by the brokerage. See "Item 7.—Management's Discussion and Analysis of Financial Condition and Results of Operations—Key Drivers" for a discussion of the various compensation models being utilized by real estate brokerages to compensate their independent sales associates.

According to NAR, approximately 41% of individual brokers and independent sales associates are affiliated with a franchisor. Competition among the national real estate brokerage brand franchisors to grow their franchise systems is intense. We believe that competition for the sale of franchises in the real estate brokerage industry is based principally upon the perceived value that the franchisor provides to enhance the franchisee's ability to grow its business and improve the recruitment, retention and productivity of its independent sales associates. The value provided by a franchisor encompasses many different aspects including the quality of the brand, tools, technology, marketing and other services, such as the availability of financing, provided to the franchisees, and the fees the franchisees must pay. Our largest national competitors in this industry include, but are not limited to, three large franchisors: Keller Williams Realty, Inc.; HSF Affiliates LLC (a joint venture controlled by HomeServices of America that operates Berkshire Hathaway HomeServices, Prudential Real Estate and Real Living Real Estate); and RE/MAX International, Inc.

Our Company owned brokerages compete with national independent real estate brokerages, franchisees of national and regional real estate franchisors -- including our own brands and the other national franchisors described in the preceding paragraph -- regional independent real estate brokerages and discount and limited service brokerages. We and others within the industry also encounter competition from companies employing technologies intended to disrupt the traditional brokerage model including the elimination of brokers or agents from the transaction.

The ability of our real estate brokerage franchisees and our company owned brokerage businesses to successfully compete is important to our prospects for growth. Their ability to compete may be affected by the performance of independent sales associates, the location of offices and target markets, the services provided to independent sales associates, the fees charged to independent sales associates, the number and nature of competing offices in the vicinity, affiliation with a recognized brand name, community reputation, technology and other factors. A franchisee's success may also be affected by national, regional and local economic conditions.

We estimate that our U.S. market share of all existing homesale transaction volume was approximately 15.7% in 2016, a decline of approximately 1.0% since 2014 and that our U.S. market share for all existing homesale transactions was approximately 13.5% in 2016, a decline of approximately 0.4% since 2014. We measure our market share transaction volume by the ratio of (a) the existing homesale transaction volume in which we and our franchisees participate to (b) NAR's existing homesale transaction volume—calculated by doubling the number of existing homesale transactions reported by NAR to account for both the buy and sell sides of a transaction multiplied by average sales price. Transaction market share is calculated similarly but without including average sales price in either the numerator or denominator.

Relocation Business. Competition in our relocation business is based on capabilities, price and quality. We compete primarily with global and regional outsourced relocation services providers. The larger outsourced relocation services providers that we compete with include Brookfield Global Relocation Services, SIRVA, Inc. and Weichert Relocation Resources, Inc. As the relocation business continues to become more global in nature with greater emphasis on relocation of employees throughout the world, we expect to face greater competition from firms that provide global services.

Title and Settlement Business. The title and settlement business is highly competitive and fragmented. The number and size of competing companies vary in the different areas in which we conduct business. We compete with other title insurers, title agents and vendor management companies. The title and settlement business competes with a large, fragmented group of smaller underwriters and agencies. In addition, we compete with the various brands of national

15

competitors including Fidelity National Title Insurance Company, First American Title Insurance Company, Stewart Title Guaranty Company and Old Republic Title Company.

Marketing and Technology

Real Estate Franchise Operations. Each of our franchise brands operates a marketing fund that is funded by our franchisees and us. The primary focus of each marketing fund is to build and maintain brand awareness, which is accomplished through a variety of media, including increased use of Internet advertising. Our Internet presence, for the most part, features our entire listing inventory on our brand websites in our regional and national markets, plus community profiles, home buying and selling advice, relocation tips and mortgage financing information. Each brand manages a comprehensive system of marketing tools, systems and sales information and data that can be accessed through free-standing brand intranet sites to assist independent sales associates in becoming the best marketer of their listings. In addition to the Sotheby's International Realty® brand, a leading luxury brand, our franchisees and our company owned brokerages also participate in luxury marketing programs, such as Century 21 Fine Homes & Estates®, Coldwell Banker Previews International®, ERA® International Collection and Better Homes and Gardens® real estate Distinctive Collection.