Attached files

| file | filename |

|---|---|

| 8-K - 8-K EARNINGS RELEASE - SUN COMMUNITIES INC | form8-kearningsreleaseq420.htm |

Table of Contents

Summary - Earnings Press Release | i - vi |

Investor Information | |

Portfolio Overview | |

Financial Information | |

Balance Sheets | |

Statements of Operations | 4 - 6 |

Outstanding Securities | |

Reconciliations to Non-GAAP Financial Measures | |

Reconciliation of Net (Loss) Income to Funds from Operations | |

Reconciliation of Recurring EBITDA to Net (Loss) Income | |

Reconciliation of Net Operating Income to Net (Loss) Income | |

Non-GAAP and Other Financial Measures | |

Financial Highlights | |

Debt Analysis | |

Selected Financial Information | |

Statement of Operations – Same Community | |

Rental Program Summary | |

Home Sales Summary | |

Acquisitions Summary | |

Other Information | |

Property Summary | 19 - 20 |

Capital Improvements, Development, and Acquisitions | |

Operating Statistics for Manufactured Homes and Annual/Seasonal RV’s | |

Footnotes and Definitions | 23 - 25 |

NEWS RELEASE

February 23, 2017

Sun Communities, Inc. Reports 2016 Fourth Quarter Results

Southfield, Michigan, February 23, 2017 – Sun Communities, Inc. (NYSE: SUI) (the "Company"), a real estate investment trust ("REIT") that owns and operates, or has an interest in, manufactured housing ("MH") and recreational vehicle ("RV") communities, today reported its fourth quarter results.

Financial Results for the Quarter and Year Ended December 31, 2016

For the quarter ended December 31, 2016, total revenues increased $50.4 million, or 30.0 percent, to $218.6 million compared to $168.2 million for the same period in 2015. Net loss attributable to Common Stockholders was $1.6 million, or $0.02 per diluted common share, as compared to net income attributable to Common Stockholders of $89.4 million, or $1.56 per diluted common share, for the same period in 2015.

For the year ended December 31, 2016, total revenues increased $159.1 million, or 23.6 percent, to $833.8 million compared to $674.7 million for the same period in 2015. Net income attributable to Common Stockholders for the year ended December 31, 2016 was $17.4 million, or $0.26 per diluted common share, as compared to $137.3 million, or $2.52 per diluted common share, for the same period in 2015.

Non-GAAP Financial Measures and Portfolio Performance

• | For the quarter ended December 31, 2016, Funds from Operations ("FFO")(1) excluding certain items was $0.91 per diluted share and OP unit ("Share") as compared to $0.81 in the prior year, an increase of 12.3 percent. |

• | For the year ended December 31, 2016, FFO(1) excluding certain items was $3.79 per Share as compared to $3.63 in the prior year, an increase of 4.4 percent. |

• | Home sales increased by 27.8 percent as compared to the year ended December 31, 2015. |

• | Revenue producing sites increased by 301 sites for the quarter bringing total portfolio occupancy to 96.2 percent, up 120 basis points from year end 2015. |

• | For the quarter, same community Net Operating Income ("NOI")(1) increased by 9.1 percent as compared to the three months ended December 31, 2015. |

“Sun’s most recent results demonstrate the ongoing power of our platform. We achieved industry leading internal growth, increased or maintained occupancy for the 20th consecutive quarter and sold a record number of homes into our communities, while integrating our largest acquisition to date,” said Gary A. Shiffman, Chairman and Chief Executive Officer. “As we proceed through 2017, we are keenly focused on continuing to deliver exceptional results to our shareholders. Along with continuing to drive NOI growth from our core portfolio, we anticipate the most meaningful opportunities will come from value-add assets that we can reposition to deliver superior returns over the long term. Sun is well positioned to continue our track record of value creation.”

i

OPERATING HIGHLIGHTS

Community Occupancy

Total portfolio occupancy increased to 96.2 percent at December 31, 2016 from 95.0 percent at December 31, 2015. During the fourth quarter of 2016, revenue producing sites increased by 301 sites, as compared to 548 revenue producing sites gained in the fourth quarter of 2015.

Revenue producing sites gained during the year ended December 31, 2016 were 1,686 as compared to 1,905 revenue producing sites gained for the same period in 2015.

Same Community Results

For the 219 communities owned throughout 2016 and 2015, fourth quarter 2016 total revenues increased 6.2 percent and total expenses decreased 0.9 percent, resulting in an increase in NOI(1) of 9.1 percent over the fourth quarter of 2015. Same community occupancy increased to 96.6 percent at December 31, 2016 from 94.7 percent at December 31, 2015.

For the year ended December 31, 2016, total revenues increased 6.1 percent and total expenses increased 3.7 percent, resulting in an increase in NOI(1) of 7.1 percent over the year ended December 31, 2015.

Home Sales

Total homes sales were 762 for the fourth quarter of 2016 as compared to 738 total homes sold during the same period in 2015.

During the year ended December 31, 2016, the Company sold 3,172 homes as compared to the 2,483 homes sold during the same period ending 2015, resulting in an additional 689 homes sold during 2016, or a 27.8 percent increase.

Rental homes sales, which are included in total home sales, were 231 and 297 for the three months ended and 1,089 and 908 for the year ended December 31, 2016 and 2015, respectively.

BALANCE SHEET AND CAPITAL MARKETS ACTIVITY

Debt Transactions

During the quarter ended December 31, 2016, the Company completed a $58.5 million secured borrowing that bears interest at a fixed rate of 3.33 percent and has a seven-year term. The Company repaid mortgage loans totaling $79.1 million in the fourth quarter and $28.9 million subsequent to year end, substantially addressing all of its 2017 maturities.

As of December 31, 2016, the Company had approximately $3.1 billion of debt outstanding. The weighted average interest rate was 4.48 percent and the weighted average maturity was 8.5 years. The Company had $8.2 million of unrestricted cash on hand. At period-end the Company’s net debt to trailing twelve month EBITDA(1) ratio was 7.5 times.

ii

Equity Transactions

During the fourth quarter of 2016 and in January 2017, the Company sold 300,000 shares of common stock through its At-the-Market equity sales program at a weighted average price of $76.43 per share. Net proceeds from the sales were $22.6 million.

PORTFOLIO ACTIVITY

Acquisitions (2)

As noted in its third quarter earnings release, the Company acquired two communities shortly after September 30, 2016, for total consideration of $9.8 million. These communities, located in Colorado and New York, contain 495 RV sites and have expansion potential of approximately 350 sites.

Additionally, during the fourth quarter, the Company acquired a community adjacent to one of its existing communities in Florida, for consideration of $3.4 million. This community has 178 RV sites.

These communities are located in high demand destination locations and will undergo repositioning or expansion activities to fully realize the inherent value in the zoned and entitled land that was previously under-managed or under-utilized.

GUIDANCE 2017

The Company estimates full year 2017 FFO(1) per Share to be in the range of $4.16 to $4.24 per Share and the first quarter 2017 to be in the range of $1.06 to $1.08 per Share. Guidance does not include prospective acquisitions or capital markets activity.

Total Portfolio

Number of communities: | 341 | 341 | ||||||

2017 Guidance | 2016 Actual | |||||||

(in Millions) | (in Millions) | % Change | ||||||

MH Revenues | $479.3 - $479.9 | |||||||

RV Seasonal/Annual | 109.0 - 109.5 | |||||||

RV Transient | 74.5 - 75.1 | |||||||

Other Revenue | 69.0 - 69.5 | |||||||

Income from real property | $731.8 - $734.0 | $ | 620.9 | 17.9% - 18.2% | ||||

Real estate taxes | 52.7 - 52.6 | 44.3 | 19.0% - 18.7% | |||||

Property operating and maintenance | 208.0 - 205.6 | 173.3 | 20.0% - 18.6% | |||||

Total property operating expenses | $260.7 - $258.2 | $ | 217.6 | 19.8% - 18.7% | ||||

Net operating income ("NOI")(1) | $471.1 - $475.8 | $ | 403.3 | 16.8% - 18.0% | ||||

iii

2017 Guidance | 2016 Actual | |||||||

(in Millions, except share data) | (in Millions, except share data) | % Change | ||||||

Rental program, net | $25.9 - $26.0 | $ | 23.5 | 10.2% - 10.6% | ||||

Home sales gross profit | 32.0 - 32.8 | 30.1 | 6.3% - 9.0% | |||||

Ancillary revenues, net | 10.7 - 10.8 | 10.0 | 7.0% - 8.0% | |||||

Interest, brokerage commissions, and other revenues, net | 24.4 - 24.5 | 21.2 | 15.1% - 15.6% | |||||

Home selling expenses | 13.0 - 12.9 | 9.7 | 34.0% - 33.0% | |||||

General and administrative | 72.7 - 72.0 | 64.1 | 13.4% - 12.3% | |||||

Weighted average common shares outstanding, fully diluted | 78.1 | |||||||

Q1 FFO(1) per Share | $1.06 - $1.08 | |||||||

2017 FFO(1) per Share | $4.16 - $4.24 | |||||||

Supplementary Information:

1Q17 | 2Q17 | 3Q17 | 4Q17 | |||||

Seasonality of FFO(1) | 25.5% | 22.3% | 28.3% | 23.9% | ||||

2017 | |||

New home sales volume | 470 - 485 | ||

Pre-owned home sales volume | 3,000 - 3,100 | ||

Increase in revenue producing sites | 2,600 - 2,800 | ||

Weighted average monthly rent increase | 3.6 | % | |

Gross profit from rental home sales included above (non-FFO) (in millions) | $15.6 | ||

Same Community Portfolio:

Number of communities | 231 | 231 | ||||||

2017 Guidance | 2016 Actual | |||||||

(in Millions) | (in Millions) | % Change | ||||||

MH revenues | $401.9 - $402.4 | |||||||

RV seasonal/annual | 54.1 - 54.3 | |||||||

RV transient | 47.3 - 47.6 | |||||||

Other revenue | 28.7 - 28.9 | |||||||

Income from real property | $532.0 - $533.2 | $ | 504.0 | 5.6% - 5.8% | ||||

Real estate taxes | 39.1 - 39.0 | 36.8 | 6.3% - 6.0% | |||||

Property operating and maintenance | 112.2 - 112.1 | 109.3 | 2.7% - 2.6% | |||||

Total property operating expenses | $151.3 - $151.1 | $ | 146.1 | 3.6% - 3.4% | ||||

Net operating income ("NOI")(1) | $380.7 - $382.1 | $ | 357.9 | 6.4% - 6.8% | ||||

The estimates and assumptions presented above represent a range of possible outcomes and may differ materially from actual results. The estimates and assumptions are forward looking based on the Company's current assessment of economic and market conditions, as well as other risks outlined below under the caption "Forward-Looking Statements."

iv

EARNINGS CONFERENCE CALL

A conference call to discuss fourth quarter operating results will be held on Thursday, February 23, 2017 at 11:00 A.M. (ET). To participate, call toll-free 877-407-4018. Callers outside the U.S. or Canada can access the call at 201-689-8471. A replay will be available following the call through March 9, 2017 and can be accessed toll-free by calling 844-512-2921 or by calling 412-317-6671. The Conference ID number for the call and the replay is 13652683. The conference call will be available live on Sun Communities' website www.suncommunities.com. Replay will also be available on the website.

Sun Communities, Inc. is a REIT that, as of December 31, 2016, owned or had an interest in a portfolio of 341 communities comprising approximately 117,000 developed sites in 29 states and Ontario, Canada.

For more information about Sun Communities, Inc., please visit the website at www.suncommunities.com.

CONTACT

Please address all inquiries to our investor relations department at our website www.suncommunities.com, by phone (248) 208-2500, by email investorrelations@suncommunities.com or by mail Sun Communities, Inc. Attn: Investor Relations, 27777 Franklin Road, Ste. 200, Southfield, MI 48034.

v

Forward-Looking Statements

This press release contains various "forward-looking statements" within the meaning of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended, and the Company intends that such forward-looking statements will be subject to the safe harbors created thereby. Forward-looking statements can be identified by words such as "will," "may," "could," "expect," "anticipate," "believes," "intends," "should," "plans," "estimates," "approximate," "guidance," and similar expressions in this press release that predict or indicate future events and trends and that do not report historical matters.

These forward-looking statements reflect the Company’s current views with respect to future events and financial performance, but involve known and unknown risks, uncertainties, and other factors, some of which are beyond the Company's control. These risks, uncertainties, and other factors may cause the actual results of the Company to be materially different from any future results expressed or implied by such forward-looking statements. Such risks and uncertainties include national, regional and local economic climates, the ability to maintain rental rates and occupancy levels, competitive market forces, the performance of recent acquisitions, the ability to integrate future acquisitions smoothly and efficiently, changes in market rates of interest, changes in foreign currency exchange rates, the ability of manufactured home buyers to obtain financing and the level of repossessions by manufactured home lenders. Further details of potential risks that may affect the Company are described in our periodic reports filed with the U.S. Securities and Exchange Commission, including in the "Risk Factors" section of the Company's Annual Report on Form 10-K for the year ended December 31, 2016.

The forward-looking statements contained in this press release speak only as of the date hereof and the Company expressly disclaims any obligation to provide public updates, revisions or amendments to any forward-looking statements made herein to reflect changes in the Company’s assumptions, expectations of future events, or trends.

vi

Investor Information

RESEARCH COVERAGE | |||

BMO Capital Markets | Paul Adornato | ||

(212) 885-4170 | |||

paul.adornato@bmo.com | |||

Citi Research | Michael Bilerman/Nicholas Joseph | ||

(212) 816-1383 | |||

michael.bilerman@citi.com | |||

nicholas.joseph@citi.com | |||

Evercore ISI | Steve Sakwa | ||

(212) 446-9462 | |||

steve.sakwa@evercoreisi.com | |||

Gwen Clark | |||

(212) 446-5611 | |||

gwen.clark@evercoreisi.com | |||

Green Street Advisors | Ryan Burke | ||

(949) 640-8780 | |||

rburke@greenstreetadvisors.com | |||

Robert W. Baird & Co. | Drew Babin | ||

(610) 238-6634 | |||

dbabin@rwbaird.com | |||

Wells Fargo | Todd Stender | ||

(562) 637-1371 | |||

todd.stender@wellsfargo.com | |||

INQUIRIES | |||

Sun Communities welcomes questions or comments from stockholders, analysts, investment managers, media, or | |||

any prospective investor. Please address all inquiries to our Investor Relations department. | |||

At Our Website | www.suncommunities.com | ||

By Email | investorrelations@suncommunities.com | ||

By Phone | (248) 208-2500 | ||

4th Quarter 2016 Supplemental Information 1 Sun Communities, Inc.

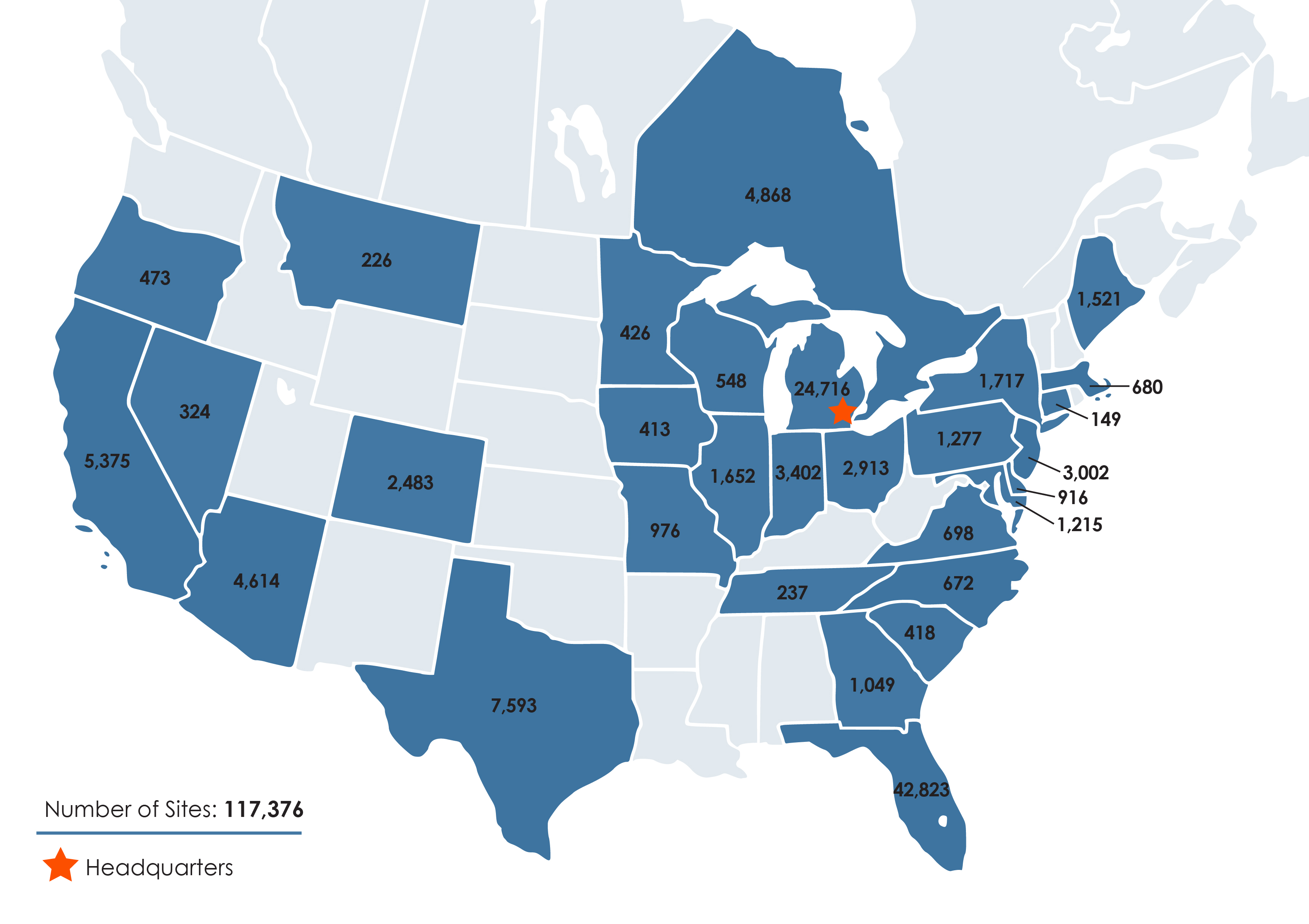

Portfolio Overview

(As of December 31, 2016)

4th Quarter 2016 Supplemental Information 2 Sun Communities, Inc.

Balance Sheets

(amounts in thousands)

Quarter Ended | ||||||||||||||||||||

12/31/2016 | 9/30/2016 | 6/30/2016 | 3/31/2016 | 12/31/2015 | ||||||||||||||||

ASSETS: | ||||||||||||||||||||

Land | $ | 1,027,976 | $ | 1,072,964 | $ | 458,349 | $ | 456,380 | $ | 451,340 | ||||||||||

Land improvements and buildings | 4,825,043 | 4,682,920 | 5,294,663 | 3,586,969 | 3,535,909 | |||||||||||||||

Rental homes and improvements | 489,633 | 485,340 | 477,875 | 469,217 | 460,480 | |||||||||||||||

Furniture, fixtures and equipment | 130,127 | 125,603 | 107,123 | 104,855 | 102,746 | |||||||||||||||

Land held for future development | 23,560 | 23,497 | 23,497 | 23,047 | 23,047 | |||||||||||||||

Investment property | 6,496,339 | 6,390,324 | 6,361,507 | 4,640,468 | 4,573,522 | |||||||||||||||

Accumulated depreciation | (1,026,858 | ) | (977,486 | ) | (928,882 | ) | (889,941 | ) | (852,407 | ) | ||||||||||

Investment property, net | 5,469,481 | 5,412,838 | 5,432,625 | 3,750,527 | 3,721,115 | |||||||||||||||

Cash and cash equivalents | 8,164 | 69,829 | 31,441 | 410,408 | 45,086 | |||||||||||||||

Inventory of manufactured homes | 21,632 | 24,147 | 29,044 | 16,636 | 14,828 | |||||||||||||||

Notes and other receivables, net | 81,179 | 87,856 | 76,466 | 54,124 | 47,972 | |||||||||||||||

Collateralized receivables, net (3) | 143,870 | 143,888 | 144,017 | 142,944 | 139,768 | |||||||||||||||

Other assets, net | 146,450 | 166,148 | 109,598 | 188,247 | 213,030 | |||||||||||||||

Total assets, net | $ | 5,870,776 | $ | 5,904,706 | $ | 5,823,191 | $ | 4,562,886 | $ | 4,181,799 | ||||||||||

LIABILITIES: | ||||||||||||||||||||

Mortgage loans payable | $ | 2,819,567 | $ | 2,854,831 | $ | 2,792,021 | $ | 2,114,818 | $ | 2,125,267 | ||||||||||

Secured borrowings (3) | 144,477 | 144,522 | 144,684 | 143,664 | 140,440 | |||||||||||||||

Preferred OP units - mandatorily redeemable | 45,903 | 45,903 | 45,903 | 45,903 | 45,903 | |||||||||||||||

Lines of credit | 100,095 | 57,737 | 357,721 | 58,065 | 24,687 | |||||||||||||||

Distributions payable | 51,896 | 51,100 | 47,992 | 45,351 | 41,265 | |||||||||||||||

Other liabilities | 279,667 | 275,650 | 257,423 | 184,102 | 184,859 | |||||||||||||||

Total liabilities | 3,441,605 | 3,429,743 | 3,645,744 | 2,591,903 | 2,562,421 | |||||||||||||||

Series A-4 preferred stock | 50,227 | 50,227 | 50,227 | 61,732 | 61,732 | |||||||||||||||

Series A-4 preferred OP units | 16,717 | 19,906 | 20,266 | 20,762 | 21,065 | |||||||||||||||

STOCKHOLDERS' EQUITY: | ||||||||||||||||||||

Series A preferred stock | 34 | 34 | 34 | 34 | 34 | |||||||||||||||

Common stock | 732 | 730 | 686 | 646 | 584 | |||||||||||||||

Additional paid-in capital | 3,321,441 | 3,313,905 | 2,980,382 | 2,706,657 | 2,319,314 | |||||||||||||||

Accumulated other comprehensive loss | (3,181 | ) | (4,876 | ) | 1 | — | — | |||||||||||||

Distributions in excess of accumulated earnings | (1,023,415 | ) | (975,511 | ) | (947,988 | ) | (896,896 | ) | (864,122 | ) | ||||||||||

Total SUI stockholders' equity | 2,295,611 | 2,334,282 | 2,033,115 | 1,810,441 | 1,455,810 | |||||||||||||||

Noncontrolling interests: | ||||||||||||||||||||

Common and preferred OP units | 69,598 | 73,284 | 76,166 | 80,018 | 82,538 | |||||||||||||||

Consolidated variable interest entities | (2,982 | ) | (2,736 | ) | (2,327 | ) | (1,970 | ) | (1,767 | ) | ||||||||||

Total noncontrolling interest | 66,616 | 70,548 | 73,839 | 78,048 | 80,771 | |||||||||||||||

Total stockholders' equity | 2,362,227 | 2,404,830 | 2,106,954 | 1,888,489 | 1,536,581 | |||||||||||||||

Total liabilities & stockholders' equity | $ | 5,870,776 | $ | 5,904,706 | $ | 5,823,191 | $ | 4,562,886 | $ | 4,181,799 | ||||||||||

4th Quarter 2016 Supplemental Information 3 Sun Communities, Inc.

Statements of Operations

(amounts in thousands, except per share amounts)

Quarter Ended | |||||||||||||||||||

12/31/2016 | 9/30/2016 | 6/30/2016 | 3/31/2016 | 12/31/2015 | |||||||||||||||

REVENUES: | |||||||||||||||||||

Income from real property (excluding transient revenue) | $ | 156,533 | $ | 158,020 | $ | 129,117 | $ | 119,084 | $ | 117,604 | |||||||||

Transient revenue | 10,824 | 26,304 | 10,884 | 10,151 | 5,568 | ||||||||||||||

Revenue from home sales | 28,520 | 31,211 | 26,039 | 24,737 | 25,169 | ||||||||||||||

Rental home revenue | 12,084 | 12,031 | 11,957 | 11,708 | 11,756 | ||||||||||||||

Ancillary revenues | 4,982 | 16,446 | 7,383 | 4,613 | 3,576 | ||||||||||||||

Interest | 4,791 | 4,705 | 4,672 | 3,945 | 4,074 | ||||||||||||||

Brokerage commissions and other revenues, net | 900 | 984 | 747 | 406 | 491 | ||||||||||||||

Total revenues | 218,634 | 249,701 | 190,799 | 174,644 | 168,238 | ||||||||||||||

EXPENSES: | |||||||||||||||||||

Property operating and maintenance | 47,917 | 57,089 | 37,067 | 31,201 | 33,360 | ||||||||||||||

Real estate taxes | 12,184 | 12,384 | 10,153 | 9,585 | 8,683 | ||||||||||||||

Cost of home sales | 21,617 | 21,935 | 18,684 | 18,184 | 19,296 | ||||||||||||||

Rental home operating and maintenance | 6,657 | 6,350 | 5,411 | 5,876 | 6,841 | ||||||||||||||

Ancillary expenses | 4,728 | 9,449 | 5,599 | 3,649 | 3,888 | ||||||||||||||

Home selling expenses | 2,504 | 2,643 | 2,460 | 2,137 | 2,079 | ||||||||||||||

General and administrative | 17,177 | 16,575 | 16,543 | 13,792 | 10,511 | ||||||||||||||

Transaction costs | 4,023 | 4,191 | 20,979 | 2,721 | 4,653 | ||||||||||||||

Depreciation and amortization | 62,205 | 61,483 | 49,670 | 48,412 | 47,530 | ||||||||||||||

Extinguishment of debt | 1,127 | — | — | — | — | ||||||||||||||

Interest | 30,641 | 33,800 | 28,428 | 26,294 | 28,066 | ||||||||||||||

Interest on mandatorily redeemable preferred OP units | 789 | 789 | 787 | 787 | 790 | ||||||||||||||

Total expenses | 211,569 | 226,688 | 195,781 | 162,638 | 165,697 | ||||||||||||||

Income / (loss) before other items | 7,065 | 23,013 | (4,982 | ) | 12,006 | 2,541 | |||||||||||||

Other expenses, net (4) | (5,848 | ) | — | — | — | — | |||||||||||||

Gain on disposition of properties, net | — | — | — | — | 98,430 | ||||||||||||||

Current tax (expense) / benefit | (116 | ) | (283 | ) | (56 | ) | (228 | ) | 71 | ||||||||||

Deferred tax benefit / (expense) | 400 | — | — | — | (1,000 | ) | |||||||||||||

Income from affiliate transactions | — | 500 | — | — | — | ||||||||||||||

Net income / (loss) | 1,501 | 23,230 | (5,038 | ) | 11,778 | 100,042 | |||||||||||||

Less: Preferred return to preferred OP units | (1,213 | ) | (1,257 | ) | (1,263 | ) | (1,273 | ) | (1,281 | ) | |||||||||

Less: Amounts attributable to noncontrolling interests | 310 | (879 | ) | 695 | (276 | ) | (6,922 | ) | |||||||||||

Less: Preferred stock distribution | (2,198 | ) | (2,197 | ) | (2,197 | ) | (2,354 | ) | (2,440 | ) | |||||||||

NET (LOSS) / INCOME ATTRIBUTABLE TO SUI | $ | (1,600 | ) | $ | 18,897 | $ | (7,803 | ) | $ | 7,875 | $ | 89,399 | |||||||

Weighted average common shares outstanding: | |||||||||||||||||||

Basic | 72,277 | 68,655 | 64,757 | 57,736 | 56,181 | ||||||||||||||

Diluted | 72,685 | 69,069 | 64,757 | 58,126 | 57,639 | ||||||||||||||

Earnings / (loss) per share: | |||||||||||||||||||

Basic | $ | (0.02 | ) | $ | 0.27 | $ | (0.12 | ) | $ | 0.14 | $ | 1.57 | |||||||

Diluted | $ | (0.02 | ) | $ | 0.27 | $ | (0.12 | ) | $ | 0.14 | $ | 1.56 | |||||||

4th Quarter 2016 Supplemental Information 4 Sun Communities, Inc.

Statements of Operations - Quarter to Date Comparison

(amounts in thousands, except per share amounts)

Three Months Ended December 31, | |||||||||||||||

2016 | 2015 | Change | % Change | ||||||||||||

REVENUES: | |||||||||||||||

Income from real property (excluding transient revenue) | $ | 156,533 | $ | 117,604 | $ | 38,929 | 33.1 | % | |||||||

Transient revenue | 10,824 | 5,568 | 5,256 | 94.4 | % | ||||||||||

Revenue from home sales | 28,520 | 25,169 | 3,351 | 13.3 | % | ||||||||||

Rental home revenue | 12,084 | 11,756 | 328 | 2.8 | % | ||||||||||

Ancillary revenues | 4,982 | 3,576 | 1,406 | 39.3 | % | ||||||||||

Interest | 4,791 | 4,074 | 717 | 17.6 | % | ||||||||||

Brokerage commissions and other revenues, net | 900 | 491 | 409 | 83.3 | % | ||||||||||

Total revenues | 218,634 | 168,238 | 50,396 | 30.0 | % | ||||||||||

EXPENSES: | |||||||||||||||

Property operating and maintenance | 47,917 | 33,360 | 14,557 | 43.6 | % | ||||||||||

Real estate taxes | 12,184 | 8,683 | 3,501 | 40.3 | % | ||||||||||

Cost of home sales | 21,617 | 19,296 | 2,321 | 12.0 | % | ||||||||||

Rental home operating and maintenance | 6,657 | 6,841 | (184 | ) | (2.7 | )% | |||||||||

Ancillary expenses | 4,728 | 3,888 | 840 | 21.6 | % | ||||||||||

Home selling expenses | 2,504 | 2,079 | 425 | 20.4 | % | ||||||||||

General and administrative | 17,177 | 10,511 | 6,666 | 63.4 | % | ||||||||||

Transaction costs | 4,023 | 4,653 | (630 | ) | (13.5 | )% | |||||||||

Depreciation and amortization | 62,205 | 47,530 | 14,675 | 30.9 | % | ||||||||||

Extinguishment of debt | 1,127 | — | 1,127 | N/A | |||||||||||

Interest | 30,641 | 28,066 | 2,575 | 9.2 | % | ||||||||||

Interest on mandatorily redeemable preferred OP units | 789 | 790 | (1 | ) | (0.1 | )% | |||||||||

Total expenses | 211,569 | 165,697 | 45,872 | 27.7 | % | ||||||||||

Income before other items | 7,065 | 2,541 | 4,524 | 178.0 | % | ||||||||||

Other expenses, net (4) | (5,848 | ) | — | (5,848 | ) | N/A | |||||||||

Gain on disposition of properties, net | — | 98,430 | (98,430 | ) | (100.0 | )% | |||||||||

Current tax (expense) / benefit | (116 | ) | 71 | (187 | ) | (263.4 | )% | ||||||||

Deferred tax benefit / (expense) | 400 | (1,000 | ) | 1,400 | (140.0 | )% | |||||||||

Net income | 1,501 | 100,042 | (98,541 | ) | (98.5 | )% | |||||||||

Less: Preferred return to preferred OP units | (1,213 | ) | (1,281 | ) | 68 | 5.3 | % | ||||||||

Less: Amounts attributable to noncontrolling interests | 310 | (6,922 | ) | 7,232 | 104.5 | % | |||||||||

Less: Preferred stock distribution | (2,198 | ) | (2,440 | ) | 242 | 9.9 | % | ||||||||

NET (LOSS) / INCOME ATTRIBUTABLE TO SUI | $ | (1,600 | ) | $ | 89,399 | $ | (90,999 | ) | (101.8 | )% | |||||

Weighted average common shares outstanding: | |||||||||||||||

Basic | 72,277 | 56,181 | 16,096 | 28.7 | % | ||||||||||

Diluted | 72,685 | 57,639 | 15,046 | 26.1 | % | ||||||||||

Earnings / (loss) per share: | |||||||||||||||

Basic | $ | (0.02 | ) | $ | 1.57 | $ | (1.59 | ) | (101.3 | )% | |||||

Diluted | $ | (0.02 | ) | $ | 1.56 | $ | (1.58 | ) | (101.3 | )% | |||||

4th Quarter 2016 Supplemental Information 5 Sun Communities, Inc.

Statements of Operations - Year to Date Comparison

(amounts in thousands, except per share amounts)

Year Ended December 31, | ||||||||||||||

2016 | 2015 | Change | % Change | |||||||||||

REVENUES: | ||||||||||||||

Income from real property (excluding transient revenue) | $ | 562,754 | $ | 467,114 | $ | 95,640 | 20.5 | % | ||||||

Transient revenue | 58,163 | 38,964 | 19,199 | 49.3 | % | |||||||||

Revenue from home sales | 110,507 | 79,728 | 30,779 | 38.6 | % | |||||||||

Rental home revenue | 47,780 | 46,236 | 1,544 | 3.3 | % | |||||||||

Ancillary revenues | 33,424 | 24,532 | 8,892 | 36.3 | % | |||||||||

Interest | 18,113 | 15,938 | 2,175 | 13.7 | % | |||||||||

Brokerage commissions and other revenues, net | 3,037 | 2,219 | 818 | 36.9 | % | |||||||||

Total revenues | 833,778 | 674,731 | 159,047 | 23.6 | % | |||||||||

EXPENSES: | ||||||||||||||

Property operating and maintenance | 173,274 | 135,797 | 37,477 | 27.6 | % | |||||||||

Real estate taxes | 44,306 | 34,714 | 9,592 | 27.6 | % | |||||||||

Cost of home sales | 80,420 | 58,941 | 21,479 | 36.4 | % | |||||||||

Rental home operating and maintenance | 24,294 | 24,956 | (662 | ) | (2.7 | )% | ||||||||

Ancillary expenses | 23,425 | 17,519 | 5,906 | 33.7 | % | |||||||||

Home selling expenses | 9,744 | 7,476 | 2,268 | 30.3 | % | |||||||||

General and administrative | 64,087 | 47,455 | 16,632 | 35.1 | % | |||||||||

Transaction costs | 31,914 | 17,803 | 14,111 | 79.3 | % | |||||||||

Depreciation and amortization | 221,770 | 177,637 | 44,133 | 24.8 | % | |||||||||

Extinguishment of debt | 1,127 | 2,800 | (1,673 | ) | (59.8 | )% | ||||||||

Interest | 119,163 | 107,659 | 11,504 | 10.7 | % | |||||||||

Interest on mandatorily redeemable preferred OP units | 3,152 | 3,219 | (67 | ) | (2.1 | )% | ||||||||

Total expenses | 796,676 | 635,976 | 160,700 | 25.3 | % | |||||||||

Income before other items | 37,102 | 38,755 | (1,653 | ) | (4.3 | )% | ||||||||

Other expenses, net (4) | (5,848 | ) | — | (5,848 | ) | N/A | ||||||||

Gain on disposition of properties, net | — | 125,376 | (125,376 | ) | (100.0 | )% | ||||||||

Current tax expense | (683 | ) | (158 | ) | (525 | ) | (332.3 | )% | ||||||

Deferred tax benefit / (expense) | 400 | (1,000 | ) | 1,400 | 140.0 | % | ||||||||

Income from affiliate transactions | 500 | 7,500 | (7,000 | ) | (93.3 | )% | ||||||||

Net income | 31,471 | 170,473 | (139,002 | ) | (81.5 | )% | ||||||||

Less: Preferred return to preferred OP units | (5,006 | ) | (4,973 | ) | (33 | ) | (0.7 | )% | ||||||

Less: Amounts attributable to noncontrolling interests | (150 | ) | (10,054 | ) | 9,904 | 98.5 | % | |||||||

Less: Preferred stock distribution | (8,946 | ) | (13,793 | ) | 4,847 | 35.1 | % | |||||||

Less: Preferred stock redemption costs | — | (4,328 | ) | 4,328 | N/A | |||||||||

NET INCOME ATTRIBUTABLE TO SUI | $ | 17,369 | $ | 137,325 | $ | (119,956 | ) | (87.4 | )% | |||||

Weighted average common shares outstanding: | ||||||||||||||

Basic | 65,856 | 53,686 | $ | 12,170 | 22.7 | % | ||||||||

Diluted | 66,321 | 53,702 | $ | 12,619 | 23.5 | % | ||||||||

Earnings per share: | ||||||||||||||

Basic | $ | 0.27 | $ | 2.53 | $ | (2.26 | ) | (89.3 | )% | |||||

Diluted | $ | 0.26 | $ | 2.52 | $ | (2.26 | ) | (89.7 | )% | |||||

4th Quarter 2016 Supplemental Information 6 Sun Communities, Inc.

Summary of Securities Outstanding as of December 31, 2016

(units/stock/shares in thousands)

Number of Units/Stock/Shares Outstanding | Conversion Rate | If Converted | Issuance Price per unit | Annual Distribution Rate | |||||

Convertible Securities | |||||||||

Series A-1 preferred OP Units | 367 | 2.4390 | 895 | $100 | 6.0% | ||||

Series A-3 preferred OP Units | 40 | 1.8605 | 74 | $100 | 4.5% | ||||

Series A-4 preferred OP Units | 634 | 0.4444 | 282 | $25 | 6.5% | ||||

Series C preferred OP Units | 333 | 1.1100 | 370 | $100 | 4.0% | ||||

Common OP Units | 2,759 | 1.0000 | 2,759 | N/A | Mirrors the Common Share distributions | ||||

Series A-4 cumulative convertible Preferred Stock | 1,682 | 0.4444 | 747 | $25 | 6.5% | ||||

Non-Convertible Securities | |||||||||

Preferred Stock ( SUI-PrA) | 3,400 | N/A | N/A | $25 | 7.125% | ||||

Common Shares | 73,206 | N/A | N/A | N/A | $2.60* | ||||

* Annual distribution is based on the last quarter distribution annualized. | |||||||||

4th Quarter 2016 Supplemental Information 7 Sun Communities, Inc.

Reconciliations to Non-GAAP Financial Measures

4th Quarter 2016 Supplemental Information 8 Sun Communities, Inc.

Reconciliation of Net (Loss) Income Attributable to Sun Communities, Inc. Common Stockholders to Funds from Operations

(amounts in thousands except for per share data)

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Net (loss) income attributable to Sun Communities, Inc. common stockholders | $ | (1,600 | ) | $ | 89,399 | $ | 17,369 | $ | 137,325 | ||||||

Adjustments: | |||||||||||||||

Preferred return to preferred OP units | 604 | 631 | 2,462 | 2,612 | |||||||||||

Amounts attributable to noncontrolling interests | (296 | ) | 6,941 | (41 | ) | 9,644 | |||||||||

Depreciation and amortization | 62,351 | 47,801 | 221,576 | 178,048 | |||||||||||

Gain on disposition of properties, net | — | (98,430 | ) | — | (125,376 | ) | |||||||||

Gain on disposition of assets, net | (3,487 | ) | (3,060 | ) | (15,713 | ) | (10,125 | ) | |||||||

Funds from operations ("FFO") attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities (1) (6) | 57,572 | 43,282 | 225,653 | 192,128 | |||||||||||

Adjustments: | |||||||||||||||

Transaction costs | 4,023 | 4,653 | 31,914 | 17,803 | |||||||||||

Other acquisition related costs (5) | 1,861 | — | 3,328 | — | |||||||||||

Income from affiliate transactions | — | — | (500 | ) | (7,500 | ) | |||||||||

Foreign currency exchange (4) | 5,005 | — | 5,005 | — | |||||||||||

Contingent liability re-measurement (4) | 181 | — | 181 | — | |||||||||||

Gain on acquisition of property (4) | (510 | ) | — | (510 | ) | — | |||||||||

Hurricane related costs (4) | 1,172 | — | 1,172 | — | |||||||||||

Preferred stock redemption costs | — | — | — | 4,328 | |||||||||||

Extinguishment of debt | 1,127 | — | 1,127 | 2,800 | |||||||||||

Debt premium write-off | (839 | ) | — | (839 | ) | — | |||||||||

Deferred tax (benefit) expense | (400 | ) | 1,000 | (400 | ) | 1,000 | |||||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities excluding certain items (1) (6) | $ | 69,192 | $ | 48,935 | $ | 266,131 | $ | 210,559 | |||||||

Weighted average common shares outstanding - basic: | 72,277 | 56,181 | 65,856 | 53,686 | |||||||||||

Add: | |||||||||||||||

Common stock issuable upon conversion of stock options | 1 | 13 | 8 | 16 | |||||||||||

Restricted stock | 407 | 423 | 457 | 411 | |||||||||||

Common OP units | 2,793 | 2,863 | 2,844 | 2,803 | |||||||||||

Common stock issuable upon conversion of Series A-1 preferred OP units | 901 | 947 | 925 | 988 | |||||||||||

Common stock issuable upon conversion of Series A-3 preferred OP units | 75 | 75 | 75 | 75 | |||||||||||

Weighted average common shares outstanding - fully diluted | 76,454 | 60,502 | 70,165 | 57,979 | |||||||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities (6) per share - fully diluted | $ | 0.75 | $ | 0.72 | $ | 3.22 | $ | 3.31 | |||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities (6) per share excluding certain items - fully diluted | $ | 0.91 | $ | 0.81 | $ | 3.79 | $ | 3.63 | |||||||

4th Quarter 2016 Supplemental Information 9 Sun Communities, Inc.

Reconciliation of Recurring EBITDA to Net (Loss) Income Attributable to Sun Communities, Inc. Common Stockholders

(amounts in thousands)

The following table reconciles Recurring EBITDA to consolidated net (loss) income:

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

RECURRING EBITDA (1) | $ | 105,850 | $ | 83,580 | $ | 414,228 | $ | 347,873 | |||||||

Interest | 30,641 | 28,066 | 119,163 | 107,659 | |||||||||||

Interest on mandatorily redeemable preferred OP units | 789 | 790 | 3,152 | 3,219 | |||||||||||

Depreciation and amortization | 62,205 | 47,530 | 221,770 | 177,637 | |||||||||||

Extinguishment of debt | 1,127 | — | 1,127 | 2,800 | |||||||||||

Transaction costs | 4,023 | 4,653 | 31,914 | 17,803 | |||||||||||

Gain on disposition of properties, net | — | (98,430 | ) | — | (125,376 | ) | |||||||||

Other expenses, net | 5,848 | — | 5,848 | — | |||||||||||

Current tax expense / (benefit) | 116 | (71 | ) | 683 | 158 | ||||||||||

Deferred tax (benefit) / expense | (400 | ) | 1,000 | (400 | ) | 1,000 | |||||||||

Income from affiliate transactions | — | — | (500 | ) | (7,500 | ) | |||||||||

Net income | 1,501 | 100,042 | 31,471 | 170,473 | |||||||||||

Less: Preferred return to preferred OP units | 1,213 | 1,281 | 5,006 | 4,973 | |||||||||||

Less: Amounts attributable to noncontrolling interests | (310 | ) | 6,922 | 150 | 10,054 | ||||||||||

Net income attributable to Sun Communities, Inc. | 598 | 91,839 | 26,315 | 155,446 | |||||||||||

Less: Preferred stock distributions | 2,198 | 2,440 | 8,946 | 13,793 | |||||||||||

Less: Preferred stock redemption costs | — | — | — | 4,328 | |||||||||||

Net (loss) / income attributable to Sun Communities, Inc., common stockholders | $ | (1,600 | ) | $ | 89,399 | $ | 17,369 | $ | 137,325 | ||||||

4th Quarter 2016 Supplemental Information 10 Sun Communities, Inc.

Reconciliation of Net Operating Income to Net (Loss) Income Attributable to Sun Communities, Inc. Common Stockholders

(amounts in thousands)

The following table reconciles net operating income to consolidated net (loss) income:

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Real Property NOI | $ | 107,256 | $ | 81,129 | $ | 403,337 | $ | 335,567 | |||||||

Rental Program NOI | 20,863 | 20,427 | 85,086 | 83,232 | |||||||||||

Home Sales NOI/Gross Profit | 6,903 | 5,873 | 30,087 | 20,787 | |||||||||||

Ancillary NOI/Gross Profit (Loss) | 254 | (312 | ) | 9,999 | 7,013 | ||||||||||

Site rent from Rental Program (included in Real Property NOI) (7) | (15,436 | ) | (15,512 | ) | (61,600 | ) | (61,952 | ) | |||||||

NOI/Gross profit | 119,840 | 91,605 | 466,909 | 384,647 | |||||||||||

Adjustments to arrive at net (loss) income: | |||||||||||||||

Other revenues | 5,691 | 4,565 | 21,150 | 18,157 | |||||||||||

Home selling expenses | (2,504 | ) | (2,079 | ) | (9,744 | ) | (7,476 | ) | |||||||

General and administrative | (17,177 | ) | (10,511 | ) | (64,087 | ) | (47,455 | ) | |||||||

Transaction costs | (4,023 | ) | (4,653 | ) | (31,914 | ) | (17,803 | ) | |||||||

Depreciation and amortization | (62,205 | ) | (47,530 | ) | (221,770 | ) | (177,637 | ) | |||||||

Extinguishment of debt | (1,127 | ) | — | (1,127 | ) | (2,800 | ) | ||||||||

Interest expense | (31,430 | ) | (28,856 | ) | (122,315 | ) | (110,878 | ) | |||||||

Other expenses, net | (5,848 | ) | — | (5,848 | ) | — | |||||||||

Gain on disposition of properties, net | — | 98,430 | — | 125,376 | |||||||||||

Current tax (expense) / benefit | (116 | ) | 71 | (683 | ) | (158 | ) | ||||||||

Deferred tax benefit / (expense) | 400 | (1,000 | ) | 400 | (1,000 | ) | |||||||||

Income from affiliate transactions | — | — | 500 | 7,500 | |||||||||||

Net income | 1,501 | 100,042 | 31,471 | 170,473 | |||||||||||

Less: Preferred return to preferred OP units | 1,213 | 1,281 | 5,006 | 4,973 | |||||||||||

Less: Amounts attributable to noncontrolling interests | (310 | ) | 6,922 | 150 | 10,054 | ||||||||||

Net income attributable to Sun Communities, Inc. | 598 | 91,839 | 26,315 | 155,446 | |||||||||||

Less: Preferred stock distributions | 2,198 | 2,440 | 8,946 | 13,793 | |||||||||||

Less: Preferred stock redemption costs | — | — | — | 4,328 | |||||||||||

Net (loss) / income attributable to Sun Communities, Inc. common stockholders | $ | (1,600 | ) | $ | 89,399 | $ | 17,369 | $ | 137,325 | ||||||

4th Quarter 2016 Supplemental Information 11 Sun Communities, Inc.

Non-GAAP and Other Financial Measures

4th Quarter 2016 Supplemental Information 12 Sun Communities, Inc.

Financial Highlights

(amounts in thousands, except per share data)

Quarter Ended | |||||||||||||||||||

12/31/2016 | 9/30/2016 | 6/30/2016 | 3/31/2016 | 12/31/2015 | |||||||||||||||

OPERATING INFORMATION | |||||||||||||||||||

Total revenues | $ | 218,634 | $ | 249,701 | $ | 190,799 | $ | 174,644 | $ | 168,238 | |||||||||

Net income (loss) | $ | 1,501 | $ | 23,230 | $ | (5,038 | ) | $ | 11,778 | $ | 100,042 | ||||||||

Net (loss) income attributable to common stockholders | $ | (1,600 | ) | $ | 18,897 | $ | (7,803 | ) | $ | 7,875 | $ | 89,399 | |||||||

(Loss) earnings per share basic | $ | (0.02 | ) | $ | 0.27 | $ | (0.12 | ) | $ | 0.14 | $ | 1.57 | |||||||

(Loss) earnings per share diluted | $ | (0.02 | ) | $ | 0.27 | $ | (0.12 | ) | $ | 0.14 | $ | 1.56 | |||||||

Recurring EBITDA (1) | $ | 105,850 | $ | 123,276 | $ | 94,882 | $ | 90,220 | $ | 83,580 | |||||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities(1) (6) | $ | 57,572 | $ | 78,023 | $ | 37,473 | $ | 53,270 | $ | 43,282 | |||||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities excluding certain items(1) (6) | $ | 69,192 | $ | 83,181 | $ | 58,452 | $ | 55,991 | $ | 48,935 | |||||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities (6) per share - fully diluted | $ | 0.75 | $ | 1.06 | $ | 0.54 | $ | 0.86 | $ | 0.72 | |||||||||

FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities (6) per share excluding certain items - fully diluted | $ | 0.91 | $ | 1.13 | $ | 0.85 | $ | 0.90 | $ | 0.81 | |||||||||

BALANCE SHEETS | |||||||||||||||||||

Total assets | $ | 5,870,776 | $ | 5,904,706 | $ | 5,823,191 | $ | 4,562,886 | $ | 4,181,799 | |||||||||

Total debt | $ | 3,110,042 | $ | 3,102,993 | $ | 3,340,329 | $ | 2,362,450 | $ | 2,336,297 | |||||||||

Total liabilities | $ | 3,441,605 | $ | 3,429,743 | $ | 3,645,744 | $ | 2,591,903 | $ | 2,562,421 | |||||||||

4th Quarter 2016 Supplemental Information 13 Sun Communities, Inc.

Debt Analysis

(amounts in thousands)

Quarter Ended | |||||||||||||||||||

12/31/2016 | 9/30/2016 | 6/30/2016 | 3/31/2016 | 12/31/2015 | |||||||||||||||

DEBT OUTSTANDING | |||||||||||||||||||

Lines of credit | $ | 100,095 | $ | 57,737 | $ | 357,721 | $ | 58,065 | $ | 24,687 | |||||||||

Mortgage loans payable | 2,819,567 | 2,854,831 | 2,792,021 | 2,114,818 | 2,125,267 | ||||||||||||||

Preferred OP units - mandatorily redeemable | 45,903 | 45,903 | 45,903 | 45,903 | 45,903 | ||||||||||||||

Secured borrowing (3) | 144,477 | 144,522 | 144,684 | 143,664 | 140,440 | ||||||||||||||

Total debt | $ | 3,110,042 | $ | 3,102,993 | $ | 3,340,329 | $ | 2,362,450 | $ | 2,336,297 | |||||||||

% FIXED/FLOATING | |||||||||||||||||||

Fixed | 91.8% | 93.1% | 84.5% | 90.7% | 92.0% | ||||||||||||||

Floating | 8.2% | 6.9% | 15.5% | 9.3% | 8.0% | ||||||||||||||

Total | 100.0% | 100.0% | 100.0% | 100.0% | 100.0% | ||||||||||||||

WEIGHTED AVERAGE INTEREST RATES | |||||||||||||||||||

Lines of credit | 2.14% | 1.93% | 1.89% | 1.87% | 1.62% | ||||||||||||||

Mortgage loans payable | 4.24% | 4.30% | 4.38% | 4.67% | 4.65% | ||||||||||||||

Preferred OP units - mandatorily redeemable | 6.87% | 6.87% | 6.87% | 6.87% | 6.87% | ||||||||||||||

Average before Secured borrowing | 4.21% | 4.29% | 4.13% | 4.64% | 4.66% | ||||||||||||||

Secured borrowing (3) | 10.03% | 10.06% | 10.09% | 10.12% | 10.17% | ||||||||||||||

Total average | 4.48% | 4.56% | 4.39% | 4.98% | 4.99% | ||||||||||||||

DEBT RATIOS | |||||||||||||||||||

Net Debt/(T-12) Recurring EBITDA (1) | 7.5 | 7.7 | 9.1 | 5.5 | 6.6 | ||||||||||||||

Net Debt/Enterprise Value | 33.8% | 32.8% | 36.6% | 27.7% | 34.0% | ||||||||||||||

Net Debt + Preferred Stock/Enterprise Value | 35.2% | 34.2% | 38.0% | 29.7% | 36.1% | ||||||||||||||

Net Debt/Gross Assets | 45.0% | 44.1% | 49.0% | 35.8% | 45.6% | ||||||||||||||

COVERAGE RATIOS | |||||||||||||||||||

(T-12) Recurring EBITDA/ Interest (1) | 3.2 | 3.1 | 3.1 | 3.0 | 3.1 | ||||||||||||||

(T-12) Recurring EBITDA/ Interest + Pref. Distributions + Pref. Stock Distribution (1) | 2.9 | 2.9 | 2.8 | 2.7 | 2.6 | ||||||||||||||

MATURITIES/PRINCIPAL AMORTIZATION NEXT FIVE YEARS | 2017 | 2018 | 2019 | 2020 | 2021 | ||||||||||||||

Lines of credit | $ | — | $ | 2,889 | $ | — | $ | 97,455 | $ | — | |||||||||

Mortgage loans payable: | |||||||||||||||||||

Maturities | 32,688 | 26,186 | 64,314 | 58,078 | 270,680 | ||||||||||||||

Weighted average rate of maturities | 6.67 | % | 6.22 | % | 5.35 | % | 3.39 | % | 5.53 | % | |||||||||

Principal amortization | 51,878 | 53,318 | 54,035 | 54,575 | 53,436 | ||||||||||||||

Preferred OP units - mandatorily redeemable | 11,240 | — | — | — | — | ||||||||||||||

Secured borrowing (3) | 5,645 | 6,186 | 6,727 | 7,341 | 7,888 | ||||||||||||||

Total | $ | 101,451 | $ | 88,579 | $ | 125,076 | $ | 217,449 | $ | 332,004 | |||||||||

4th Quarter 2016 Supplemental Information 14 Sun Communities, Inc.

Statements of Operations – Same Community

(amounts in thousands except for Other Information)

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||

2016 | 2015 | Change | % Change | 2016 | 2015 | Change | % Change | ||||||||||||||||||||||

REVENUES: | |||||||||||||||||||||||||||||

Income from real property | $ | 113,884 | $ | 107,224 | $ | 6,660 | 6.2 | % | $ | 466,967 | $ | 440,202 | $ | 26,765 | 6.1 | % | |||||||||||||

PROPERTY OPERATING EXPENSES: | |||||||||||||||||||||||||||||

Payroll and benefits | 8,809 | 8,944 | (135 | ) | (1.5 | )% | 38,688 | 36,465 | 2,223 | 6.1 | % | ||||||||||||||||||

Legal, taxes & insurance | 1,224 | 1,412 | (188 | ) | (13.3 | )% | 5,398 | 6,633 | (1,235 | ) | (18.6 | )% | |||||||||||||||||

Utilities | 5,761 | 5,958 | (197 | ) | (3.3 | )% | 26,161 | 25,674 | 487 | 1.9 | % | ||||||||||||||||||

Supplies and repair | 3,884 | 4,651 | (8) | (767 | ) | (16.5 | )% | 16,617 | 17,154 | (8) | (537 | ) | (3.1 | )% | |||||||||||||||

Other | 3,283 | 2,333 | 950 | 40.7 | % | 12,945 | 11,823 | 1,122 | 9.5 | % | |||||||||||||||||||

Real estate taxes | 7,936 | 7,880 | 56 | 0.7 | % | 34,239 | 31,563 | 2,676 | 8.5 | % | |||||||||||||||||||

Property operating expenses | 30,897 | 31,178 | (281 | ) | (0.9 | )% | 134,048 | 129,312 | 4,736 | 3.7 | % | ||||||||||||||||||

NET OPERATING INCOME (NOI)(1) | $ | 82,987 | $ | 76,046 | $ | 6,941 | 9.1 | % | $ | 332,919 | $ | 310,890 | $ | 22,029 | 7.1 | % | |||||||||||||

As of December 31, | ||||||||||||||

2016 | 2015 | Change | % Change | |||||||||||

OTHER INFORMATION | ||||||||||||||

Number of properties | 219 | 219 | — | |||||||||||

Overall occupancy (9) | 96.6 | % | 94.7 | % | (10) | 1.9 | % | |||||||

Sites available for development | 6,542 | 5,906 | 636 | 10.8 | % | |||||||||

Monthly base rent per site - MH | $ | 498 | $ | 482 | $ | 16 | 3.3 | % | ||||||

Monthly base rent per site - RV (11) | $ | 436 | $ | 423 | $ | 13 | 3.1 | % | ||||||

Monthly base rent per site - Total | $ | 489 | $ | 474 | $ | 15 | 3.2 | % | ||||||

4th Quarter 2016 Supplemental Information 15 Sun Communities, Inc.

Rental Program Summary

(amounts in thousands except for *)

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||

2016 | 2015 | Change | % Change | 2016 | 2015 | Change | % Change | ||||||||||||||||||||||

REVENUES: | |||||||||||||||||||||||||||||

Rental home revenue | $ | 12,084 | $ | 11,756 | $ | 328 | 2.8 | % | $ | 47,780 | $ | 46,236 | $ | 1,544 | 3.3 | % | |||||||||||||

Site rent included in Income from real property | 15,436 | 15,512 | (76 | ) | (0.5 | )% | 61,600 | 61,952 | (352 | ) | (0.6 | )% | |||||||||||||||||

Rental Program revenue | 27,520 | 27,268 | 252 | 0.9 | % | 109,380 | 108,188 | 1,192 | 1.1 | % | |||||||||||||||||||

EXPENSES: | |||||||||||||||||||||||||||||

Commissions | 532 | 775 | (243 | ) | (31.4 | )% | 2,242 | 3,216 | (974 | ) | (30.3 | )% | |||||||||||||||||

Repairs and refurbishment | 3,537 | 4,198 | (661 | ) | (15.8 | )% | 12,825 | 12,326 | 499 | 4.1 | % | ||||||||||||||||||

Taxes and insurance | 1,556 | 973 | 583 | 59.9 | % | 5,734 | 5,638 | 96 | 1.7 | % | |||||||||||||||||||

Marketing and other | 1,032 | 895 | 137 | 15.3 | % | 3,493 | 3,776 | (283 | ) | (7.5 | )% | ||||||||||||||||||

Rental Program operating and maintenance | 6,657 | 6,841 | (184 | ) | (2.7 | )% | 24,294 | 24,956 | (662 | ) | (2.7 | )% | |||||||||||||||||

NET OPERATING INCOME (NOI) (1) | $ | 20,863 | $ | 20,427 | $ | 436 | 2.1 | % | $ | 85,086 | $ | 83,232 | $ | 1,854 | 2.2 | % | |||||||||||||

Occupied rental home information as of December 31, 2016 and 2015: | |||||||||||||||||||||||||||||

Number of occupied rentals, end of period* | 10,733 | 10,685 | 48 | 0.5 | % | ||||||||||||||||||||||||

Investment in occupied rental homes, end of period | $ | 457,691 | $ | 448,837 | $ | 8,854 | 2.0 | % | |||||||||||||||||||||

Number of sold rental homes* | 1,089 | 908 | 181 | 19.9 | % | ||||||||||||||||||||||||

Weighted average monthly rental rate, end of period* | $ | 882 | $ | 858 | $ | 24 | 2.8 | % | |||||||||||||||||||||

4th Quarter 2016 Supplemental Information 16 Sun Communities, Inc.

Homes Sales Summary

(amounts in thousands except for *)

Three Months Ended December 31, | Year Ended December 31, | ||||||||||||||||||||||||||||

2016 | 2015 | Change | % Change | 2016 | 2015 | Change | % Change | ||||||||||||||||||||||

New home sales | $ | 10,505 | $ | 7,318 | $ | 3,187 | 43.6 | % | $ | 30,977 | $ | 22,208 | $ | 8,769 | 39.5 | % | |||||||||||||

Pre-owned home sales | 18,015 | 17,851 | 164 | 0.9 | % | 79,530 | 57,520 | 22,010 | 38.3 | % | |||||||||||||||||||

Revenue from home sales | 28,520 | 25,169 | 3,351 | 13.3 | % | 110,507 | 79,728 | 30,779 | 38.6 | % | |||||||||||||||||||

New home cost of sales | 9,289 | 6,272 | 3,017 | 48.1 | % | 26,802 | 18,620 | 8,182 | 43.9 | % | |||||||||||||||||||

Pre-owned home cost of sales | 12,328 | 13,024 | (696 | ) | (5.3 | )% | 53,618 | 40,321 | 13,297 | 33.0 | % | ||||||||||||||||||

Cost of home sales | 21,617 | 19,296 | 2,321 | 12.0 | % | 80,420 | 58,941 | 21,479 | 36.4 | % | |||||||||||||||||||

NOI / Gross Profit (1) | $ | 6,903 | $ | 5,873 | $ | 1,030 | 17.5 | % | $ | 30,087 | $ | 20,787 | $ | 9,300 | 44.7 | % | |||||||||||||

Gross profit – new homes | $ | 1,216 | $ | 1,046 | $ | 170 | 16.3 | % | $ | 4,175 | $ | 3,588 | $ | 587 | 16.4 | % | |||||||||||||

Gross margin % – new homes | 11.6 | % | 14.3 | % | (2.7 | )% | 13.5 | % | 16.2 | % | (2.7 | )% | |||||||||||||||||

Average selling price – new homes* | $ | 105,050 | $ | 89,242 | $ | 15,808 | 17.7 | % | $ | 94,156 | $ | 81,346 | $ | 12,810 | 15.8 | % | |||||||||||||

Gross profit – pre-owned homes | $ | 5,687 | $ | 4,827 | $ | 860 | 17.8 | % | $ | 25,912 | $ | 17,199 | $ | 8,713 | 50.7 | % | |||||||||||||

Gross margin % – pre-owned homes | 31.6 | % | 27.0 | % | 4.6 | % | 32.6 | % | 29.9 | % | 2.7 | % | |||||||||||||||||

Average selling price – pre-owned homes* | $ | 27,213 | $ | 27,211 | $ | 2 | — | % | $ | 27,974 | $ | 26,027 | $ | 1,947 | 7.5 | % | |||||||||||||

Home sales volume: | |||||||||||||||||||||||||||||

New home sales* | 100 | 82 | 18 | 22.0 | % | 329 | 273 | 56 | 20.5 | % | |||||||||||||||||||

Pre-owned home sales* | 662 | 656 | 6 | 0.9 | % | 2,843 | 2,210 | 633 | 28.6 | % | |||||||||||||||||||

Total homes sold* | 762 | 738 | 24 | 3.3 | % | 3,172 | 2,483 | 689 | 27.8 | % | |||||||||||||||||||

4th Quarter 2016 Supplemental Information 17 Sun Communities, Inc.

Acquisitions Summary - Properties Acquired in 2016 and 2015

(amounts in thousands except for statistical data)

Three Months Ended December 31, 2016 | Year Ended December 31, 2016 | ||||||

REVENUES: | |||||||

Income from real property | $ | 53,473 | $ | 153,950 | |||

PROPERTY AND OPERATING EXPENSES: | |||||||

Payroll and benefits | 7,363 | 18,056 | |||||

Legal, taxes & insurance | 330 | 543 | |||||

Utilities | 12,893 | 41,334 | |||||

Supplies and repair | 1,774 | 4,115 | |||||

Other | 2,596 | 9,417 | |||||

Real estate taxes | 4,248 | 10,067 | |||||

Property operating expenses | 29,204 | 83,532 | |||||

NET OPERATING INCOME (NOI) (1) | $ | 24,269 | $ | 70,418 | |||

As of December 31, 2016 | |||||||

Other information: | |||||||

Number of properties | 122 | ||||||

Occupied sites (12) | 24,359 | ||||||

Developed sites (12) | 25,055 | ||||||

Occupancy % (12) | 97.2 | % | |||||

Transient sites | 8,703 | ||||||

Monthly base rent per site - MH | $ | 596 | |||||

Monthly base rent per site - RV (11) | $ | 398 | |||||

Monthly base rent per site - Total (11) | $ | 509 | |||||

Ancillary revenues, net (in thousands) | $ | 2,992 | |||||

Home sales: | |||||||

Gross profit from home sales (in thousands) | $ | 4,452 | |||||

New homes sales | 95 | ||||||

Pre-owned homes sales | 306 | ||||||

Occupied rental home information: | |||||||

Rental program NOI (1) (in thousands) | $ | 540 | |||||

Number of occupied rentals, end of period | 292 | ||||||

Investment in occupied rental homes (in thousands) | $ | 9,716 | |||||

Weighted average monthly rental rate | $ | 955 | |||||

4th Quarter 2016 Supplemental Information 18 Sun Communities, Inc.

Property Summary | ||||||||||||||||

(includes MH and Annual/Seasonal RV’s) | ||||||||||||||||

COMMUNITIES | 12/31/2016 | 9/30/2016 | 6/30/2016 | 3/31/2016 | 12/31/2015 | |||||||||||

FLORIDA | ||||||||||||||||

Communities | 121 | 121 | 121 | 61 | 61 | |||||||||||

Developed sites (12) | 36,326 | 36,050 | 36,119 | 24,312 | 24,216 | |||||||||||

Occupied (12) | 35,021 | 34,745 | 34,720 | 23,359 | 23,201 | |||||||||||

Occupancy % (12) | 96.4 | % | 96.4 | % | 96.1 | % | 96.1 | % | 95.8 | % | ||||||

Sites for development | 1,465 | 1,259 | 1,259 | 823 | 823 | |||||||||||

MICHIGAN | ||||||||||||||||

Communities | 67 | 67 | 66 | 66 | 65 | |||||||||||

Developed sites (12) | 24,512 | 24,388 | 24,387 | 24,363 | 23,966 | |||||||||||

Occupied (12) | 23,248 | 23,218 | 23,198 | 23,079 | 22,677 | |||||||||||

Occupancy % (12) | 94.8 | % | 95.2 | % | 95.1 | % | 94.7 | % | 94.6 | % | ||||||

Sites for development | 2,589 | 2,628 | 2,248 | 2,105 | 2,105 | |||||||||||

TEXAS | ||||||||||||||||

Communities | 21 | 21 | 21 | 17 | 16 | |||||||||||

Developed sites (12) | 6,186 | 6,088 | 6,071 | 5,970 | 5,965 | |||||||||||

Occupied (12) | 5,862 | 5,774 | 5,771 | 5,602 | 5,517 | |||||||||||

Occupancy % (12) | 94.8 | % | 94.8 | % | 95.1 | % | 93.8 | % | 92.5 | % | ||||||

Sites for development | 1,474 | 1,455 | 1,347 | 1,347 | 1,347 | |||||||||||

CALIFORNIA | ||||||||||||||||

Communities | 22 | 22 | 22 | 3 | 3 | |||||||||||

Developed sites (12) | 4,862 | 4,863 | 4,864 | 198 | 198 | |||||||||||

Occupied (12) | 4,793 | 4,792 | 4,796 | 192 | 192 | |||||||||||

Occupancy % (12) | 98.6 | % | 98.5 | % | 98.6 | % | 97.0 | % | 97.0 | % | ||||||

Sites for development | 332 | 332 | 332 | 332 | 332 | |||||||||||

ARIZONA | ||||||||||||||||

Communities | 11 | 11 | 11 | 10 | 10 | |||||||||||

Developed sites (12) | 3,565 | 3,567 | 3,532 | 3,302 | 3,301 | |||||||||||

Occupied (12) | 3,338 | 3,305 | 3,281 | 3,102 | 3,078 | |||||||||||

Occupancy % (12) | 93.6 | % | 92.7 | % | 92.9 | % | 93.9 | % | 93.2 | % | ||||||

Sites for development | 358 | 358 | 358 | 393 | 393 | |||||||||||

ONTARIO, CANADA | ||||||||||||||||

Communities | 15 | 15 | 15 | — | — | |||||||||||

Developed sites (12) | 3,368 | 3,453 | 3,375 | — | — | |||||||||||

Occupied (12) | 3,368 | 3,453 | 3,375 | — | — | |||||||||||

Occupancy % (12) | 100.0 | % | 100.0 | % | 100.0 | % | — | % | — | % | ||||||

Sites for development | 1,599 | 2,029 | 2,029 | — | — | |||||||||||

INDIANA | ||||||||||||||||

Communities | 11 | 11 | 11 | 11 | 11 | |||||||||||

Developed sites (12) | 2,900 | 2,900 | 2,900 | 2,900 | 2,900 | |||||||||||

Occupied (12) | 2,724 | 2,712 | 2,700 | 2,674 | 2,628 | |||||||||||

Occupancy % (12) | 93.9 | % | 93.5 | % | 93.1 | % | 92.2 | % | 90.6 | % | ||||||

Sites for development | 316 | 316 | 316 | 363 | 363 | |||||||||||

4th Quarter 2016 Supplemental Information 19 Sun Communities, Inc.

Property Summary | ||||||||||||||||

(includes MH and Annual/Seasonal RV’s) | ||||||||||||||||

COMMUNITIES | 12/31/2016 | 9/30/2016 | 6/30/2016 | 3/31/2016 | 12/31/2015 | |||||||||||

OHIO | ||||||||||||||||

Communities | 9 | 9 | 9 | 9 | 9 | |||||||||||

Developed sites (12) | 2,715 | 2,719 | 2,718 | 2,700 | 2,703 | |||||||||||

Occupied (12) | 2,595 | 2,602 | 2,616 | 2,585 | 2,560 | |||||||||||

Occupancy % (12) | 95.6 | % | 95.7 | % | 96.2 | % | 95.7 | % | 94.7 | % | ||||||

Sites for development | — | — | — | — | — | |||||||||||

COLORADO | ||||||||||||||||

Communities | 8 | 7 | 7 | 7 | 7 | |||||||||||

Developed sites (12) | 2,335 | 2,335 | 2,335 | 2,335 | 2,335 | |||||||||||

Occupied (12) | 2,325 | 2,323 | 2,320 | 2,319 | 2,315 | |||||||||||

Occupancy % (12) | 99.6 | % | 99.5 | % | 99.4 | % | 99.3 | % | 99.1 | % | ||||||

Sites for development | 656 | 304 | 304 | 304 | 304 | |||||||||||

OTHER STATES | ||||||||||||||||

Communities | 56 | 55 | 54 | 49 | 49 | |||||||||||

Developed sites (12) | 14,313 | 14,415 | 14,337 | 13,683 | 13,657 | |||||||||||

Occupied (12) | 13,919 | 13,991 | 13,912 | 13,237 | 13,142 | |||||||||||

Occupancy % (12) | 97.3 | % | 97.1 | % | 97.0 | % | 96.7 | % | 96.2 | % | ||||||

Sites for development | 1,827 | 1,823 | 1,728 | 1,514 | 1,514 | |||||||||||

TOTAL - PORTFOLIO | ||||||||||||||||

Communities | 341 | 339 | 337 | 233 | 231 | |||||||||||

Developed sites (12) | 101,082 | 100,778 | 100,638 | 79,763 | 79,241 | |||||||||||

Occupied (12) | 97,193 | 96,915 | 96,689 | 76,149 | 75,310 | |||||||||||

Occupancy % (12) | 96.2 | % | 96.2 | % | 96.1 | % | 95.5 | % | 95.0 | % | ||||||

Sites for development | 10,616 | 10,504 | 9,921 | 7,181 | 7,181 | |||||||||||

% Communities age restricted | 33.1 | % | 33.3 | % | 33.5 | % | 26.2 | % | 26.4 | % | ||||||

TRANSIENT RV PORTFOLIO SUMMARY | ||||||||||||||||

Location | ||||||||||||||||

Florida | 6,497 | 7,232 | 6,990 | 2,664 | 2,823 | |||||||||||

Ontario, Canada | 1,500 | 1,485 | 1,657 | — | — | |||||||||||

Texas | 1,407 | 1,446 | 1,455 | 799 | 414 | |||||||||||

Arizona | 1,049 | 1,047 | 1,055 | 1,096 | 1,087 | |||||||||||

New Jersey | 1,042 | 1,047 | 1,084 | 995 | 981 | |||||||||||

New York | 830 | 484 | 483 | 489 | 499 | |||||||||||

Maine | 555 | 556 | 571 | 575 | 604 | |||||||||||

California | 513 | 478 | 518 | 296 | 296 | |||||||||||

Indiana | 502 | 501 | 501 | 501 | 501 | |||||||||||

Michigan | 204 | 203 | 126 | 150 | 160 | |||||||||||

Ohio | 198 | 194 | 195 | 213 | 210 | |||||||||||

Other States | 1,997 | 1,801 | 1,864 | 2,099 | 2,092 | |||||||||||

Total transient RV sites | 16,294 | 16,474 | 16,499 | 9,877 | 9,667 | |||||||||||

4th Quarter 2016 Supplemental Information 20 Sun Communities, Inc.

Capital Improvements, Development, and Acquisitions

(amounts in thousands except for *)

Recurring | ||||||||||||||||||||||||

Capital | Recurring | |||||||||||||||||||||||

Expenditures | Capital | Lot | Expansion & | Revenue | ||||||||||||||||||||

Average/Site* | Expenditures (13) | Modifications (14) | Acquisitions (15) | Development (16) | Producing (17) | |||||||||||||||||||

2016 | $ | 211 | $ | 17,613 | $ | 19,040 | $ | 1,822,564 | $ | 47,958 | $ | 2,631 | ||||||||||||

2015 | $ | 230 | $ | 20,344 | $ | 13,961 | $ | 1,214,482 | $ | 28,660 | $ | 4,497 | ||||||||||||

2014 | $ | 227 | $ | 18,077 | $ | 9,414 | $ | 785,624 | $ | 22,196 | $ | 1,454 | ||||||||||||

4th Quarter 2016 Supplemental Information 21 Sun Communities, Inc.

Operating Statistics for Manufactured Homes and Annual/Seasonal RV’s

Resident | Net Leased | New Home | Pre-owned | Brokered | |||||||||||

MARKETS | Move-outs | Sites (18) | Sales | Home Sales | Re-sales | ||||||||||

Michigan | 439 | 310 | 9 | 1,231 | 152 | ||||||||||

Florida | 358 | 662 | 186 | 338 | 987 | ||||||||||

Texas | 180 | 249 | 14 | 377 | 49 | ||||||||||

Indiana | 54 | 96 | — | 213 | 9 | ||||||||||

Ohio | 100 | 36 | 1 | 102 | 6 | ||||||||||

Arizona | 49 | 127 | 40 | 28 | 133 | ||||||||||

Colorado | 12 | 12 | 16 | 204 | 46 | ||||||||||

Other states and Ontario, Canada | 530 | 194 | 63 | 350 | 273 | ||||||||||

Year Ended December 31, 2016 | 1,722 | 1,686 | 329 | 2,843 | 1,655 | ||||||||||

Resident | Net Leased | New Home | Pre-owned | Brokered | |||||||||||

TOTAL FOR YEAR ENDED | Move-outs | Sites (18) | Sales | Home Sales | Re-sales | ||||||||||

2015 | 1,344 | 1,905 | 273 | 2,210 | 1,244 | ||||||||||

2014 | 1,504 | 1,890 | 113 | 1,853 | 618 | ||||||||||

Resident | Resident | |||||

PERCENTAGE TRENDS | Move-outs | Re-sales | ||||

2016 | 2.0 | % | 6.1 | % | ||

2015 | 2.0 | % | 5.9 | % | ||

2014 | 2.6 | % | 5.0 | % | ||

4th Quarter 2016 Supplemental Information 22 Sun Communities, Inc.

Footnotes and Definitions

(1) | Investors in and analysts following the real estate industry utilize funds from operations (FFO), net operating income (NOI), and recurring earnings before interest, tax, depreciation and amortization (Recurring EBITDA) as supplemental performance measures. We believe FFO, NOI, and Recurring EBITDA are appropriate measures given their wide use by and relevance to investors and analysts. FFO, reflecting the assumption that real estate values rise or fall with market conditions, principally adjusts for the effects of GAAP depreciation/amortization of real estate assets. NOI provides a measure of rental operations and does not factor in depreciation/amortization and non-property specific expenses such as general and administrative expenses. Recurring EBITDA, a metric calculated as EBITDA exclusive of certain nonrecurring items, provides a further tool to evaluate ability to incur and service debt and to fund dividends and other cash needs. Additionally, FFO, NOI, and Recurring EBITDA are commonly used in various ratios, pricing multiples/yields and returns and valuation calculations used to measure financial position, performance and value. |

FFO is defined by the National Association of Real Estate Investment Trusts (NAREIT) as net income (loss) computed in accordance with generally accepted accounting principles (GAAP), excluding gains (or losses) from sales of depreciable operating property, plus real estate-related depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures. FFO is a non-GAAP financial measure that management believes is a useful supplemental measure of the Company's operating performance. Management generally considers FFO to be a useful measure for reviewing comparative operating and financial performance because, by excluding gains and losses related to sales of previously depreciated operating real estate assets, impairment and excluding real estate asset depreciation and amortization (which can vary among owners of identical assets in similar condition based on historical cost accounting and useful life estimates), FFO provides a performance measure that, when compared period over period, reflects the impact to operations from trends in occupancy rates, rental rates, and operating costs, providing perspective not readily apparent from net income (loss). Management believes that the use of FFO has been beneficial in improving the understanding of operating results of REITs among the investing public and making comparisons of REIT operating results more meaningful. FFO is computed in accordance with the Company's interpretation of standards established by NAREIT, which may not be comparable to FFO reported by other REITs that do not define the term in accordance with the current NAREIT definition or that interpret the current NAREIT definition differently than the Company. The Company also uses FFO excluding certain items, which excludes certain gain and loss items that management considers unrelated to the operational and financial performance of our core business. We believe that this provides investors with another financial measure of our operating performance that is more comparable when evaluating period over period results.

Because FFO excludes significant economic components of net income (loss) including depreciation and amortization, FFO should be used as an adjunct to net income (loss) and not as an alternative to net income (loss). The principal limitation of FFO is that it does not represent cash flow from operations as defined by GAAP and is a supplemental measure of performance that does not replace net income (loss) as a measure of performance or net cash provided by operating activities as a measure of liquidity. In addition, FFO is not intended as a measure of a REIT’s ability to meet debt principal repayments and other cash requirements, nor as a measure of working capital. FFO only provides investors with an additional performance measure that, when combined with measures computed in accordance with GAAP such as net income (loss), cash flow from operating activities, investing activities and financing activities, provide investors with an indication of our ability to service debt and to fund acquisitions and other expenditures. Other REITs may use different methods for calculating FFO, accordingly, our FFO may not be comparable to other REITs.

NOI is derived from revenues minus property operating expenses and real estate taxes. NOI does not represent cash generated from operating activities in accordance with GAAP and should not be considered to be an alternative to net income (loss) (determined in accordance with GAAP) as an indication of the Company's financial performance or to be an alternative to cash flow from operating activities (determined in accordance with GAAP) as a measure of the Company's liquidity; nor is it indicative of funds available for the Company's cash needs, including its ability to make cash distributions. The Company believes that net income (loss) is the most directly comparable GAAP measurement to NOI. Because of the inclusion of items such as interest, depreciation, and amortization, the use of net income (loss) as a performance measure is limited as these items may not accurately reflect the actual change in market value of a property, in the case of depreciation and in the case of interest, may not necessarily be linked to the operating performance of a real estate asset, as it is often incurred at a parent company level and not at a property level. The Company believes that NOI is helpful to investors as a measure of operating performance because it is an indicator of the return on property investment, and provides a method of comparing property performance over time. The Company uses NOI as a key management tool when evaluating performance and growth of particular properties and/or groups of properties. The principal limitation of NOI is that it excludes depreciation, amortization interest expense and non-property specific expenses such as general and administrative expenses, all of which are significant

4th Quarter 2016 Supplemental Information 23 Sun Communities, Inc.

costs, therefore, NOI is a measure of the operating performance of the properties of the Company rather than of the Company overall.

EBITDA is defined as NOI plus other income, plus (minus) equity earnings (loss) from affiliates, minus general and administrative expenses. EBITDA includes EBITDA from discontinued operations. The Company believes that net income (loss) is the most directly comparable GAAP measurement to EBITDA.

(2) The consideration amounts presented with respect to acquired communities represent the economic transaction and do not contemplate the fair value purchase accounting required by GAAP.

(3) This is a transferred asset transaction which has been classified as collateralized receivables and the cash received from this transaction has been classified as a secured borrowing. The interest income and interest expense accrue at the same rate/amount.

(4) Other expenses, net on the Consolidated Statements of Operations is comprised of: foreign currency exchange $5.0 million; hurricane related costs $1.2 million; and contingent liability re-measurement $0.2 million; partially offset by gain on acquisition of property $0.5 million.

(5) These costs represent the first year expenses incurred to bring acquired properties up to the Company's operating standards, including items such as tree trimming and painting costs that do not meet the Company's capitalization policy. As these costs have become more significant in connection with the size of our acquisitions, they are included as an adjustment to FFO for the year ended December 31, 2016. The Company incurred $1.1 million and $2.8 million of these first year expenses for the three months and year ended December 31, 2015, and had a similar adjustment been made, FFO attributable to Sun Communities, Inc. common stockholders and dilutive convertible securities per share excluding certain items would have been $0.83 and $3.68 for the three months and year ended December 31, 2015.

(6) The effect of certain anti-dilutive convertible securities is excluded from these items.

(7) The renter's monthly payment includes the site rent and an amount attributable to the leasing of the home. The site rent is reflected in Real Property NOI. For purposes of management analysis, the site rent is included in the Rental Program revenue to evaluate the incremental revenue gains associated with implementation of the Rental Program, and to assess the overall growth and performance of the Rental Program and financial impact on our operations.

(8) Three months and year ended December 31, 2015 excludes $1.1 million and $2.8 million of first year expenses for properties acquired in late 2014 and 2015 incurred to bring the properties up to Sun's operating standards. These costs did not meet the Company's capitalization policy.

(9) Includes manufactured housing (MH) and annual/seasonal recreational vehicle (RV) sites, and excludes transient RV sites and recently completed but vacant expansion sites.

(10) Occupancy reflects current year gains from expansion sites and the conversion of transient RV guests to annual/seasonal RV contracts as vacant in 2015.

(11) Monthly base rent per site pertains to annual/seasonal RV sites and excludes transient RV sites.

(12) Includes MH and annual/seasonal RV sites, and excludes transient RV sites.

(13) Includes capital expenditures necessary to maintain asset quality, including purchasing and replacing assets used to operate the community. These capital expenditures include items such as: major road, driveway, and pool improvements; clubhouse renovations; adding or replacing street lights; playground equipment; signage; maintenance facilities; manager housing and property vehicles. The minimum capitalized amount is five hundred dollars.

(14) Includes capital expenditures which improve the asset quality of the community. These costs are incurred when an existing older home moves out, and the site is prepared for a new home, more often than not, a multi-sectional home. These activities which are mandated by strict manufacturer’s installation requirements and state building code include items such as new foundations, driveways, and utility upgrades.

4th Quarter 2016 Supplemental Information 24 Sun Communities, Inc.

(15) Acquisitions represent the purchase price of existing operating communities and land parcels to develop expansions or new communities. Acquisitions also include deferred maintenance identified during due diligence and those capital improvements necessary to bring the community up to the Company’s standards. These include items such as: upgrading clubhouses; landscaping; new street light systems; new mail delivery systems; pool renovation including larger decks, heaters, and furniture; new maintenance facilities; and new signage including main signs and internal road signs. These are considered acquisition costs and although identified during due diligence, they sometimes require up to twelve months after closing to complete.

(16) Expansion and development costs consist primarily of construction costs and costs necessary to complete home site improvements.

(17) | Capital costs related to revenue generating activities, consisting primarily of garages, sheds, and sub-metering of water, sewer and electricity. Revenue generating attractions at our RV resorts are also included here and, occasionally, a special capital project requested by residents and accompanied by an extra rental increase will be classified as revenue producing. |

(18) Net leased sites do not include occupied sites acquired in that year.

Certain financial information has been revised to reflect reclassifications in prior periods to conform to current period presentation.

4th Quarter 2016 Supplemental Information 25 Sun Communities, Inc.