Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - DANA INC | dan-20161231xex32.htm |

| EX-31.2 - EXHIBIT 31.2 - DANA INC | dan-20161231xex312.htm |

| EX-31.1 - EXHIBIT 31.1 - DANA INC | dan-20161231xex311.htm |

| EX-24 - EXHIBIT 24 - DANA INC | dan-20161231xex24.htm |

| EX-23 - EXHIBIT 23 - DANA INC | dan-20161231xex23.htm |

| EX-21 - EXHIBIT 21 - DANA INC | dan-20161231xex21.htm |

| EX-12 - EXHIBIT 12 - DANA INC | dan-20161231xex12.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended: December 31, 2016

Commission File Number: 1-1063

Dana Incorporated

(Exact name of registrant as specified in its charter)

Delaware | 26-1531856 | |

(State of incorporation) | (IRS Employer Identification Number) | |

3939 Technology Drive, Maumee, OH | 43537 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (419) 887-3000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the common stock held by non-affiliates of the registrant computed by reference to the closing price of the common stock on June 30, 2016 was $1,512,538,357.

APPLICABLE ONLY TO CORPORATE ISSUERS:

There were 144,016,355 shares of the registrant's common stock outstanding at January 31, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement to be delivered to stockholders in connection with the Annual Meeting of Stockholders to be held on April 27, 2017 are incorporated by reference into Part III.

DANA INCORPORATED

FORM 10-K

YEAR ENDED DECEMBER 31, 2016

Table of Contents

Pages | ||

PART I | ||

Item 1 | Business | |

Item 1A | Risk Factors | |

Item 1B | Unresolved Staff Comments | |

Item 2 | Properties | |

Item 3 | Legal Proceedings | |

PART II | ||

Item 5 | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

Item 6 | Selected Financial Data | |

Item 7 | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

Item 7A | Quantitative and Qualitative Disclosures about Market Risk | |

Item 8 | Financial Statements and Supplementary Data | |

Item 9 | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | |

Item 9A | Controls and Procedures | |

Item 9B | Other Information | |

PART III | ||

Item 10 | Directors, Executive Officers and Corporate Governance | |

Item 11 | Executive Compensation | |

Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

Item 13 | Certain Relationships and Related Transactions, and Director Independence | |

Item 14 | Principal Accountant Fees and Services | |

PART IV | ||

Item 15 | Exhibits and Financial Statement Schedules | |

Signatures | ||

Exhibit Index | ||

Exhibits | ||

i

Forward-Looking Information

Statements in this report (or otherwise made by us or on our behalf) that are not entirely historical constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements can often be identified by words such as “anticipates,” “expects,” “believes,” “intends,” “plans,” “predicts,” “seeks,” “estimates,” “projects,” “outlook,” “may," “will,” “should,” “would,” “could,” “potential,” “continue,” “ongoing” and similar expressions, variations or negatives of these words. These statements represent the present expectations of Dana Incorporated and its consolidated subsidiaries (Dana) based on our current information and assumptions. Forward-looking statements are inherently subject to risks and uncertainties. Our plans, actions and actual results could differ materially from our present expectations due to a number of factors, including those discussed below and elsewhere in this report and in our other filings with the Securities and Exchange Commission (SEC). All forward-looking statements speak only as of the date made and we undertake no obligation to publicly update or revise any forward-looking statement to reflect events or circumstances that may arise after the date of this report.

ii

PART I

(Dollars in millions, except per share amounts)

Item 1. Business

General

Dana Incorporated (Dana) is headquartered in Maumee, Ohio and was incorporated in Delaware in 2007. As a global provider of high technology driveline (axles, driveshafts and transmissions), sealing and thermal-management products our customer base includes virtually every major vehicle manufacturer in the global light vehicle, medium/heavy vehicle and off-highway markets. As of December 31, 2016 we employed approximately 24,900 people, operated in 25 countries and had 91 major facilities around the world.

The terms “Dana,” “we,” “our” and “us,” when used in this report are references to Dana. These references include the subsidiaries of Dana unless otherwise indicated or the context requires otherwise.

Overview of our Business

We have aligned our organization around four operating segments: Light Vehicle Driveline Technologies (Light Vehicle), Commercial Vehicle Driveline Technologies (Commercial Vehicle), Off-Highway Driveline Technologies (Off-Highway) and Power Technologies. These operating segments have global responsibility and accountability for business commercial activities and financial performance.

External sales by operating segment for the years ended December 31, 2016, 2015 and 2014 are as follows:

2016 | 2015 | 2014 | |||||||||||||||||||

Dollars | % of Total | Dollars | % of Total | Dollars | % of Total | ||||||||||||||||

Light Vehicle | $ | 2,607 | 44.8 | % | $ | 2,482 | 40.9 | % | $ | 2,496 | 37.7 | % | |||||||||

Commercial Vehicle | 1,254 | 21.5 | % | 1,533 | 25.3 | % | 1,838 | 27.8 | % | ||||||||||||

Off-Highway | 909 | 15.6 | % | 1,040 | 17.2 | % | 1,231 | 18.6 | % | ||||||||||||

Power Technologies | 1,056 | 18.1 | % | 1,005 | 16.6 | % | 1,052 | 15.9 | % | ||||||||||||

Total | $ | 5,826 | $ | 6,060 | $ | 6,617 | |||||||||||||||

Refer to Segment Results of Operations in Item 7 and Note 19 to our consolidated financial statements in Item 8 for further financial information about our operating segments.

1

Our business is diversified across end-markets, products and customers. The following table summarizes the markets, products and largest customers of each of our operating segments as of December 31, 2016.

Segment | Markets | Products | Largest Customers |

Light Vehicle | Light vehicle market: | Front axles | Ford Motor Company |

Light trucks (full frame) | Rear axles | Fiat Chrysler Automobiles* | |

Sport utility vehicles | Driveshafts/Propshafts | Renault-Nissan Alliance | |

Crossover utility vehicles | Differentials | Toyota Motor Company | |

Vans | Torque couplings | General Motors Company | |

Passenger cars | Modular assemblies | Tata Motors | |

Commercial Vehicle | Medium/heavy vehicle market: | Steer axles | PACCAR Inc |

Medium duty trucks | Drive axles | Ford Motor Company | |

Heavy duty trucks | Driveshafts | AB Volvo | |

Buses | Tire inflation systems | Daimler AG | |

Specialty vehicles | Navistar International Corporation | ||

Off-Highway | Off-Highway market: | Front axles | Deere & Company |

Construction | Rear axles | AGCO Corporation | |

Earth moving | Driveshafts | Manitou Group | |

Agricultural | Transmissions | Oshkosh Corporation | |

Mining | Torque converters | Sandvik AB | |

Forestry | Tire inflation systems | ||

Rail | Electronic controls | ||

Material handling | |||

Power Technologies | Light vehicle market | Gaskets | Ford Motor Company |

Medium/heavy vehicle market | Cover modules | General Motors Company | |

Off-Highway market | Heat shields | Renault-Nissan Alliance | |

Engine sealing systems | Mahle GmbH | ||

Cooling | Volkswagen AG | ||

Heat transfer products | |||

* Via a directed supply relationship with Hyundai Mobis.

Geographic Operations

We maintain administrative and operational organizations in North America, Europe, South America and Asia Pacific to support our operating segments, assist with the management of affiliate relations and facilitate financial and statutory reporting and tax compliance on a worldwide basis. Our operations are located in the following countries:

North America | Europe | South America | Asia Pacific | |

Canada | Belgium | South Africa | Argentina | Australia |

Mexico | France | Spain | Brazil | China |

United States | Germany | Sweden | Colombia | India |

Hungary | Switzerland | Ecuador | Japan | |

Italy | United Kingdom | South Korea | ||

Russia | Taiwan | |||

Thailand | ||||

Our non-U.S. subsidiaries and affiliates manufacture and sell products similar to those we produce in the United States. Operations outside the U.S. may be subject to a greater risk of changing political, economic and social environments, changing governmental laws and regulations, currency revaluations and market fluctuations than our domestic operations. See the discussion of risk factors in Item 1A.

Sales reported by our non-U.S. subsidiaries comprised $3,131 of our 2016 consolidated sales of $5,826. A summary of sales and long-lived assets by geographic region can be found in Note 19 to our consolidated financial statements in Item 8.

2

Customer Dependence

We are largely dependent on light vehicle, medium- and heavy-duty vehicle and off-highway original equipment manufacturer (OEM) customers. Ford Motor Company (Ford) was the only individual customer accounting for 10% or more of our consolidated sales in 2016. As a percentage of total sales from operations, our sales to Ford were approximately 22% in 2016, 20% in 2015 and 18% in 2014 and our sales to Fiat Chrysler Automobiles (via a directed supply relationship with Hyundai Mobis), our second largest customer, were approximately 9% in 2016, 9% in 2015 and 8% in 2014. Renault-Nissan Alliance, PACCAR Inc and General Motors Company were our third, fourth and fifth largest customers in 2016. Our 10 largest customers collectively accounted for approximately 62% of our sales in 2016.

Loss of all or a substantial portion of our sales to Ford or other large volume customers would have a significant adverse effect on our financial results until such lost sales volume could be replaced and there is no assurance that any such lost volume would be replaced.

Sources and Availability of Raw Materials

We use a variety of raw materials in the production of our products, including steel and products containing steel, stainless steel, forgings, castings and bearings. Other commodity purchases include aluminum, brass, copper and plastics. These materials are typically available from multiple qualified sources in quantities sufficient for our needs. However, some of our operations remain dependent on single sources for certain raw materials.

While our suppliers have generally been able to support our needs, our operations may experience shortages and delays in the supply of raw material from time to time due to strong demand, capacity limitations, short lead times, production schedule increases from our customers and other problems experienced by the suppliers. A significant or prolonged shortage of critical components from any of our suppliers could adversely impact our ability to meet our production schedules and to deliver our products to our customers in a timely manner.

Seasonality

Our businesses are generally not seasonal. However, in the light vehicle market, our sales are closely related to the production schedules of our OEM customers and those schedules have historically been weakest in the third quarter of the year due to a large number of model year change-overs that occur during this period. Additionally, third-quarter production schedules in Europe are typically impacted by the summer vacation schedules and fourth-quarter production is affected globally by year-end holidays.

Backlog

A substantial amount of the new business we are awarded by OEMs is granted well in advance of a program launch. These awards typically extend through the life of the given program. This backlog of new business does not represent firm orders. We estimate future sales from new business using the projected volume under these programs.

Competition

Within each of our markets, we compete with a variety of independent suppliers and distributors, as well as with the in-house operations of certain OEMs. With a renewed focus on product innovation, we differentiate ourselves through efficiency and performance, reliability, materials and processes, sustainability and product extension.

3

The following table summarizes our principal competitors by operating segment as of December 31, 2016.

Segment | Principal Competitors |

Light Vehicle | ZF Friedrichshafen AG |

GKN plc | |

American Axle & Manufacturing Holdings, Inc. | |

Magna International Inc. | |

Wanxiang Group Corporation | |

Hitachi Automotive Systems, Ltd. | |

IFA ROTORION Holding GmbH | |

Neapco, LLC | |

Vertically integrated OEM operations | |

Commercial Vehicle | Meritor, Inc. |

American Axle & Manufacturing Holdings, Inc. | |

Hendrickson (a subsidiary of the Boler Company) | |

Klein Products Inc. | |

Tirsan Kardan | |

Vertically integrated OEM operations | |

Off-Highway | Carraro Group |

ZF Friedrichshafen AG | |

GKN plc | |

Kessler + Co. | |

Meritor, Inc. | |

YTO Group | |

Comer Industries | |

Hema Endustri A.S. | |

Vertically integrated OEM operations | |

Power Technologies | ElringKlinger AG |

Federal-Mogul Corporation | |

Freudenberg NOK Group | |

MAHLE GmbH | |

Modine Manufacturing Company | |

Valeo Group | |

YinLun Co., LTD | |

Denso Corporation | |

Intellectual Property

Our proprietary driveline and power technologies product lines have strong identities in the markets we serve. Throughout these product lines, we manufacture and sell our products under a number of patents that have been obtained over a period of years and expire at various times. We consider each of these patents to be of value and aggressively protect our rights throughout the world against infringement. We are involved with many product lines and the loss or expiration of any particular patent would not materially affect our sales and profits.

We own or have licensed numerous trademarks that are registered in many countries, enabling us to market our products worldwide. For example, our Spicer®, Victor Reinz® and Long® trademarks are widely recognized in their market segments.

Engineering and Research and Development

Since our introduction of the automotive universal joint in 1904, we have been focused on technological innovation. Our objective is to be an essential partner to our customers and we remain highly focused on offering superior product quality, technologically advanced products, world-class service and competitive prices. To enhance quality and reduce costs, we use

4

statistical process control, cellular manufacturing, flexible regional production and assembly, global sourcing and extensive employee training.

We engage in ongoing engineering and research and development activities to improve the reliability, performance and cost-effectiveness of our existing products and to design and develop innovative products that meet customer requirements for new applications. We are integrating related operations to create a more innovative environment, speed product development, maximize efficiency and improve communication and information sharing among our research and development operations. At December 31, 2016, we had eight stand-alone technical and engineering centers and eight additional sites at which we conduct research and development activities. Our research and development costs were $81 in 2016, $75 in 2015 and $72 in 2014. Total engineering expenses including research and development were $196 in 2016, $183 in 2015 and $176 in 2014.

Our research and development activities continue to improve customer value. For all of our markets, this means drivelines with higher torque capacity, reduced weight and improved efficiency. End-use customers benefit by having vehicles with better fuel economy and reduced cost of ownership. We are also developing a number of power technologies products for vehicular and other applications that will assist fuel cell, battery and hybrid vehicle manufacturers in making their technologies commercially viable in mass production.

Employees

The following table summarizes our employees by operating segment as of December 31, 2016.

Segment | Employees | ||

Light Vehicle | 10,100 | ||

Commercial Vehicle | 5,900 | ||

Off-Highway | 2,700 | ||

Power Technologies | 4,900 | ||

Technical and administrative | 1,300 | ||

Total | 24,900 | ||

Environmental Compliance

We make capital expenditures in the normal course of business as necessary to ensure that our facilities are in compliance with applicable environmental laws and regulations. The cost of environmental compliance has not been a material part of capital expenditures and did not have a material adverse effect on our earnings or competitive position in 2016.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 as amended (Exchange Act) are available, free of charge, on or through our Internet website at http://www.dana.com/investors as soon as reasonably practicable after we electronically file such materials with, or furnish them to, the SEC. Copies of any materials we file with the SEC can also be obtained free of charge through the SEC’s website at http://www.sec.gov, at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549, or by calling the SEC’s Office of Investor Education and Advocacy at 1-800-732-0330. We also post our Corporate Governance Guidelines, Standards of Business Conduct for Members of the Board of Directors, Board Committee membership lists and charters, Standards of Business Conduct and other corporate governance materials on our Internet website. Copies of these posted materials are also available in print, free of charge, to any stockholder upon request from: Dana Incorporated, Investor Relations, P.O. Box 1000, Maumee, Ohio 43537, or via telephone in the U.S. at 800-537-8823 or e-mail at InvestorRelations@dana.com. The inclusion of our website address in this report is an inactive textual reference only and is not intended to include or incorporate by reference the information on our website into this report.

Item 1A. Risk Factors

We are impacted by events and conditions that affect the light vehicle, medium/heavy vehicle and off-highway markets that we serve, as well as by factors specific to Dana. Among the risks that could materially adversely affect our business, financial condition or results of operations are the following, many of which are interrelated.

5

Risk Factors Related to the Markets We Serve

Failure to sustain a continuing economic recovery in the United States and elsewhere could have a substantial adverse effect on our business.

Our business is tied to general economic and industry conditions as demand for vehicles depends largely on the strength of the economy, employment levels, consumer confidence levels, the availability and cost of credit and the cost of fuel. These factors have had and could continue to have a substantial impact on our business.

We expect global market conditions to result in overall comparable sales in 2017. We expect the North America economic climate will continue to be modestly strong to stable with light vehicle demand levels continuing to be strong, while the medium/heavy truck market is expected to be weaker and the off-highway market remains relatively stable at already weak levels. The economy in Europe is expected to improve modestly, with on-highway markets being slightly stronger while the off-highway market remains weak but stable. The South America countries where we do business are expected to remain relatively weak, but show signs of improvement as we progress through 2017. We expect the rate of growth to be more modest in the Asia Pacific region in 2017, with the markets we serve in the region being relatively stable or facing some headwinds.

Adverse developments in the economic conditions of any of these markets could reduce demand for new vehicles, causing our customers to reduce their vehicle production and, as a result, demand for our products would be adversely affected.

Certain political developments occurring this past year have provided increased economic uncertainty. The United Kingdom's decision to exit the European Union and the results of the presidential election in the U.S. both could result in economic and trade policy actions that would impact economic conditions in various countries, the cost of importing into the U.S. and the competitive landscape of our customers, suppliers and competitors.

Adverse global economic conditions could also cause our customers and suppliers to experience severe economic constraints in the future, including bankruptcy, which could have a material adverse impact on our financial position and results of operations.

We could be adversely impacted by the loss of any of our significant customers, changes in their requirements for our products or changes in their financial condition.

We are reliant upon sales to several significant customers. Sales to our ten largest customers accounted for 62% of our overall sales in 2016. Changes in our business relationships with any of our large customers or in the timing, size and continuation of their various programs could have a material adverse impact on us.

The loss of any of these customers, the loss of business with respect to one or more of their vehicle models on which we have high component content, or a significant decline in the production levels of such vehicles would negatively impact our business, results of operations and financial condition. Pricing pressure from our customers also poses certain risks. Inability on our part to offset pricing concessions with cost reductions would adversely affect our profitability. We are continually bidding on new business with these customers, as well as seeking to diversify our customer base, but there is no assurance that our efforts will be successful. Further, to the extent that the financial condition of our largest customers deteriorates, including possible bankruptcies, mergers or liquidations, or their sales otherwise decline, our financial position and results of operations could be adversely affected.

We may be adversely impacted by changes in international legislative and political conditions.

We operate in 25 countries around the world and we depend on significant foreign suppliers and customers. Further, we have several growth initiatives that are targeting emerging markets like China and India. Legislative and political activities within the countries where we conduct business, particularly in emerging markets and less developed countries, could adversely impact our ability to operate in those countries. The political situation in a number of countries in which we operate could create instability in our contractual relationships with no effective legal safeguards for resolution of these issues, or potentially result in the seizure of our assets. Through January 23, 2015, we operated in Venezuela where government exchange controls and policies placed restrictions on our ability to operate effectively and repatriate funds. Our risk associated with operating in this country was eliminated with the divestiture of our operations in Venezuela on January 23, 2015. However, we expect to continue exporting product to Venezuela, and our ability to do so effectively could be adversely impacted by Venezuela government policies. We operate in Argentina, where trade-related initiatives and other government restrictions limit our

6

ability to optimize operating effectiveness. At December 31, 2016, our net asset exposure related to Argentina was approximately $15, including $10 of net fixed assets.

We may be adversely impacted by the strength of the U.S. dollar relative to the currencies in the other countries in which we do business.

Approximately 54% of our sales in 2016 were from operations located in countries other than the U.S. Currency variations can have an impact on our results (expressed in U.S. dollars). Currency variations can also adversely affect margins on sales of our products in countries outside of the U.S. and margins on sales of products that include components obtained from affiliates or other suppliers located outside of the U.S. Strengthening of the U.S. dollar against the euro and currencies of other countries in which we have operations has had and could continue to have an adverse effect on our results reported in U.S. dollars. We use a combination of natural hedging techniques and financial derivatives to mitigate foreign currency exchange rate risks. Such hedging activities may be ineffective or may not offset more than a portion of the adverse financial impact resulting from currency variations.

We may be adversely impacted by new laws, regulations or policies of governmental organizations related to increased fuel economy standards and reduced greenhouse gas emissions, or changes in existing ones.

The markets and customers we serve are subject to substantial government regulation, which often differs by state, region and country. These regulations, and proposals for additional regulation, are advanced primarily out of concern for the environment (including concerns about global climate change and its impact) and energy independence. We anticipate that the number and extent of these regulations, and the costs to comply with them, will increase significantly in the future.

In the U.S., vehicle fuel economy and greenhouse gas emissions are regulated under a harmonized national program administered by the National Highway Traffic Safety Administration and the Environmental Protection Agency (EPA). Other governments in the markets we serve are also creating new policies to address these same issues, including the European Union, Brazil, China and India. These government regulatory requirements could significantly affect our customers by altering their global product development plans and substantially increasing their costs, which could result in limitations on the types of vehicles they sell and the geographical markets they serve. Any of these outcomes could adversely affect our financial position and results of operations.

Company-Specific Risk Factors

We have taken, and continue to take, cost-reduction actions. Although our process includes planning for potential negative consequences, the cost-reduction actions may expose us to additional production risk and could adversely affect our sales, profitability and ability to attract and retain employees.

We have been reducing costs in all of our businesses and have discontinued product lines, exited businesses, consolidated manufacturing operations and positioned operations in lower cost locations. The impact of these cost-reduction actions on our sales and profitability may be influenced by many factors including our ability to successfully complete these ongoing efforts, our ability to generate the level of cost savings we expect or that are necessary to enable us to effectively compete, delays in implementation of anticipated workforce reductions, decline in employee morale and the potential inability to meet operational targets due to our inability to retain or recruit key employees.

We depend on our subsidiaries for cash to satisfy the obligations of the company.

Our subsidiaries conduct all of our operations and own substantially all of our assets. Our cash flow and our ability to meet our obligations depend on the cash flow of our subsidiaries. In addition, the payment of funds in the form of dividends, intercompany payments, tax sharing payments and otherwise may be subject to restrictions under the laws of the countries of incorporation of our subsidiaries or the by-laws of the subsidiary.

Labor stoppages or work slowdowns at Dana, key suppliers or our customers could result in a disruption in our operations and have a material adverse effect on our businesses.

We and our customers rely on our respective suppliers to provide parts needed to maintain production levels. We all rely on workforces represented by labor unions. Workforce disputes that result in work stoppages or slowdowns could disrupt operations of all of these businesses, which in turn could have a material adverse effect on the supply of, or demand for, the products we supply our customers.

7

We could be adversely affected if we are unable to recover portions of commodity costs (including costs of steel, other raw materials and energy) from our customers.

We continue to work with our customers to recover a portion of our material cost increases. While we have been successful in the past recovering a significant portion of such cost increases, there is no assurance that increases in commodity costs will not adversely impact our profitability in the future.

We could be adversely affected if we experience shortages of components from our suppliers or if disruptions in the supply chain lead to parts shortages for our customers.

A substantial portion of our annual cost of sales is driven by the purchase of goods and services. To manage and minimize these costs, we have been consolidating our supplier base. As a result, we are dependent on single sources of supply for some components of our products. We select our suppliers based on total value (including price, delivery and quality), taking into consideration their production capacities and financial condition, and we expect that they will be able to support our needs. However, there is no assurance that adverse financial conditions, including bankruptcies of our suppliers, reduced levels of production, natural disasters or other problems experienced by our suppliers will not result in shortages or delays in their supply of components to us or even in the financial collapse of one or more such suppliers. If we were to experience a significant or prolonged shortage of critical components from any of our suppliers, particularly those who are sole sources, and were unable to procure the components from other sources, we would be unable to meet our production schedules for some of our key products and to ship such products to our customers in a timely fashion, which would adversely affect our sales, profitability and customer relations.

Adverse economic conditions, natural disasters and other factors can similarly lead to financial distress or production problems for other suppliers to our customers which can create disruptions to our production levels. Any such supply-chain induced disruptions to our production are likely to create operating inefficiencies that will adversely affect our sales, profitability and customer relations.

We ended the contractual relationship with one of our largest suppliers at the end of 2014 and established relationships with alternative suppliers. During the first half of 2015, as we transitioned to the new suppliers, we were challenged with relatively high levels of demand in the market segment supported by these suppliers. This resulted in increased costs in the first half of 2015. Additionally, our inability to fully satisfy customer demands led to some lost business with a significant customer. There is a risk that our operating results and customer relationships could be adversely impacted if other supplier transitions are not completed effectively.

In 2014, the financial condition of a major supplier to our South America operations led to them pursuing legal reorganization. As more fully described in Notes 2 and 3 of the consolidated financial statements in Item 8, legal actions were required in 2015 to maintain the supply of product from this supplier and, in 2016, we ultimately acquired strategic assets from this supplier necessary to satisfy our customer commitments.

In 2016, the financial condition of a single source supplier to our North American operations led them to request

significant price increases which we have not accepted. Although this supplier is providing us with the required supply, there is

continued uncertainty whether we will be able to maintain cost-effective, uninterrupted supply.

Our profitability and results of operations may be adversely affected by program launch difficulties.

The launch of new business is a complex process, the success of which depends on a wide range of factors, including the production readiness of our manufacturing facilities and manufacturing processes and those of our suppliers, as well as factors related to tooling, equipment, employees, initial product quality and other factors. Our failure to successfully launch material new or takeover business could have an adverse effect on our profitability and results of operations.

We use important intellectual property in our business. If we are unable to protect our intellectual property or if a third party makes assertions against us or our customers relating to intellectual property rights, our business could be adversely affected.

We own important intellectual property, including patents, trademarks, copyrights and trade secrets, and are involved in numerous licensing arrangements. Our intellectual property plays an important role in maintaining our competitive position in a number of the markets that we serve. Our competitors may develop technologies that are similar or superior to our proprietary technologies or design around the patents we own or license. Further, as we expand our operations in jurisdictions where the

8

protection of intellectual property rights is less robust, the risk of others duplicating our proprietary technologies increases, despite efforts we undertake to protect them. Developments or assertions by or against us relating to intellectual property rights, and any inability to protect these rights, could have a material adverse impact on our business and our competitive position.

We could encounter unexpected difficulties integrating acquisitions and joint ventures.

We acquired businesses in 2016, and we expect to complete additional acquisitions and investments in the future that complement or expand our businesses. The success of this strategy will depend on our ability to successfully complete these transactions or arrangements, to integrate the businesses acquired in these transactions and to develop satisfactory working arrangements with our strategic partners in the joint ventures. We could encounter unexpected difficulties in completing these transactions and integrating the acquisitions with our existing operations. We also may not realize the degree or timing of benefits anticipated when we entered into a transaction.

Several of our joint ventures operate pursuant to established agreements and, as such, we do not unilaterally control the joint venture. There is a risk that the partners’ objectives for the joint venture may not be aligned with ours, leading to potential differences over management of the joint venture that could adversely impact its financial performance and consequent contribution to our earnings. Additionally, inability on the part of our partners to satisfy their contractual obligations under the agreements could adversely impact our results of operations and financial position.

We could be adversely impacted by the costs of environmental, health, safety and product liability compliance.

Our operations are subject to environmental laws and regulations in the U.S. and other countries that govern emissions to the air; discharges to water; the generation, handling, storage, transportation, treatment and disposal of waste materials; and the cleanup of contaminated properties. Historically, other than an EPA settlement as part of our bankruptcy proceedings, environmental costs related to our former and existing operations have not been material. However, there is no assurance that the costs of complying with current environmental laws and regulations, or those that may be adopted in the future, will not increase and adversely impact us.

There is also no assurance that the costs of complying with current laws and regulations, or those that may be adopted in the future, that relate to health, safety and product liability matters will not adversely impact us. There is also a risk of warranty and product liability claims, as well as product recalls, if our products fail to perform to specifications or cause property damage, injury or death. (See Notes 15 and 16 to our consolidated financial statements in Item 8 for additional information on product liabilities and warranties.)

A failure of our information technology infrastructure could adversely impact our business and operations.

We recognize the increasing volume of cyber attacks and employ commercially practical efforts to provide reasonable assurance that the risks of such attacks are appropriately mitigated. Each year, we evaluate the threat profile of our industry to stay abreast of trends and to provide reasonable assurance our existing countermeasures will address any new threats identified. Despite our implementation of security measures, our IT systems and those of our service providers are vulnerable to circumstances beyond our reasonable control including acts of terror, acts of government, natural disasters, civil unrest and denial of service attacks which may lead to the theft of our intellectual property, trade secrets or business disruption. To the extent that any disruption or security breach results in a loss or damage to our data or an inappropriate disclosure of confidential information, it could cause significant damage to our reputation, affect our relationships with our customers, suppliers and employees, lead to claims against the company and ultimately harm our business. Additionally, we may be required to incur significant costs to protect against damage caused by these disruptions or security breaches in the future.

We participate in certain multi-employer pension plans which are not fully funded.

We contribute to certain multi-employer defined benefit pension plans for our union-represented employees in the U.S. in accordance with our collective bargaining agreements. Contributions are based on hours worked except in cases of layoff or leave where we generally contribute based on 40 hours per week for a maximum of one year. The plans are not fully funded as of December 31, 2016. We could be held liable to the plans for our obligation, as well as those of other employers, due to our participation in the plans. Contribution rates could increase if the plans are required to adopt a funding improvement plan, if the performance of plan assets does not meet expectations or as a result of future collectively bargained wage and benefit agreements. (See Note 11 to our consolidated financial statements in Item 8 for additional information on multi-employer pension plans.)

9

Changes in interest rates and asset returns could increase our pension funding obligations and reduce our profitability.

We have unfunded obligations under certain of our defined benefit pension and other postretirement benefit plans. The valuation of our future payment obligations under the plans and the related plan assets are subject to significant adverse changes if the credit and capital markets cause interest rates and projected rates of return to decline. Such declines could also require us to make significant additional contributions to our pension plans in the future. A material increase in the unfunded obligations of these plans could also result in a significant increase in our pension expense in the future.

We may incur additional tax expense or become subject to additional tax exposure.

Our provision for income taxes and the cash outlays required to satisfy our income tax obligations in the future could be adversely affected by numerous factors. These factors include changes in the level of earnings in the tax jurisdictions in which we operate, changes in the valuation of deferred tax assets, changes in our plans to repatriate the earnings of our non-U.S. operations to the U.S. and changes in tax laws and regulations. The 2016 presidential election in the U.S. has resulted in an administration and Congress that are controlled by the same party. Changes to tax policy and tax rates are considered likely and, depending on the nature of these changes, could have a significant impact on our business and financial results. Our income tax returns are subject to examination by federal, state and local tax authorities in the U.S. and tax authorities outside the U.S. The results of these examinations and the ongoing assessments of our tax exposures could also have an adverse effect on our provision for income taxes and the cash outlays required to satisfy our income tax obligations.

Our ability to utilize our net operating loss carryforwards may be limited.

Net operating loss carryforwards (NOLs) approximating $796 were available at December 31, 2016 to reduce future U.S. income tax liabilities. Our ability to utilize these NOLs may be limited as a result of certain change of control provisions of the U.S. Internal Revenue Code of 1986, as amended (Code). Of this amount, NOLs of approximately $577 are treated as losses incurred before the change of control upon emergence from Chapter 11 and are limited to annual utilization of $84. The balance of our NOLs, treated as incurred subsequent to the change in control, is not subject to limitation as of December 31, 2016. However, there can be no assurance that trading in our shares will not effect another change in control under the Code, which would further limit our ability to utilize our available NOLs. Such limitations may cause us to pay income taxes earlier and in greater amounts than would be the case if the NOLs were not subject to limitation.

Risk Factors Related to our Securities

Provisions in our Restated Certificate of Incorporation and Bylaws may discourage a takeover attempt.

Certain provisions of our Restated Certificate of Incorporation and Bylaws, as well as the General Corporation Law of the State of Delaware, may have the effect of delaying, deferring or preventing a change in control of Dana. Such provisions, including those governing the nomination of directors, limiting who may call special stockholders’ meetings and eliminating stockholder action by written consent, may make it more difficult for other persons, without the approval of our board of directors, to make a tender offer or otherwise acquire substantial amounts of common stock or to launch other takeover attempts that a stockholder might consider to be in such stockholder’s best interest.

Item 1B. Unresolved Staff Comments

The Company has received no written comments regarding its periodic or current reports from the staff of the SEC that were issued 180 days or more preceding the end of its 2016 fiscal year and that remain unresolved.

10

Item 2. Properties

Type of Facility | North America | Europe | South America | Asia Pacific | Total | |||||

Light Vehicle | ||||||||||

Manufacturing/Distribution | 13 | 3 | 5 | 9 | 30 | |||||

Commercial Vehicle | ||||||||||

Manufacturing/Distribution | 8 | 4 | 5 | 4 | 21 | |||||

Off-Highway | ||||||||||

Manufacturing/Distribution | 2 | 8 | 2 | 12 | ||||||

Power Technologies | ||||||||||

Manufacturing/Distribution | 12 | 4 | 1 | 17 | ||||||

Technical and Engineering Centers | 3 | 3 | ||||||||

Corporate and other | ||||||||||

Administrative Offices | 2 | 1 | 3 | |||||||

Technical and Engineering Centers - Multiple Segments | 2 | 3 | 5 | |||||||

42 | 19 | 10 | 20 | 91 | ||||||

As of December 31, 2016, we operated in 25 countries and had 91 major facilities housing manufacturing and distribution operations, technical and engineering centers and administrative offices. In addition to the eight stand-alone technical and engineering centers in the table above, we have eight technical and engineering centers housed within manufacturing sites. We lease 34 of these facilities and a portion of four others and own the remainder. We believe that all of our property and equipment is properly maintained.

Our world headquarters is located in Maumee, Ohio. This facility and other facilities in the greater Detroit, Michigan and Maumee, Ohio areas house functions that have global or North American regional responsibility for finance and accounting, treasury, risk management, legal, human resources, procurement and supply chain management, communications and information technology.

Item 3. Legal Proceedings

We are a party to various pending judicial and administrative proceedings that arose in the ordinary course of business. After reviewing the currently pending lawsuits and proceedings (including the probable outcomes, reasonably anticipated costs and expenses and our established reserves for uninsured liabilities), we do not believe that any liabilities that may result from these proceedings are reasonably likely to have a material adverse effect on our liquidity, financial condition or results of operations. Legal proceedings are also discussed in Notes 3 and 15 to our consolidated financial statements in Item 8.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market information — Our common stock trades on the New York Stock Exchange (NYSE) under the symbol "DAN." The following table shows the high and low prices of our common stock as reported by the NYSE for each of our fiscal quarters during 2016 and 2015.

2016 | 2015 | ||||||||||||||

High | Low | High | Low | ||||||||||||

Fourth quarter | $ | 19.81 | $ | 13.93 | $ | 18.12 | $ | 13.01 | |||||||

Third quarter | 15.70 | 9.80 | 20.81 | 15.33 | |||||||||||

Second quarter | 14.55 | 10.21 | 22.73 | 20.35 | |||||||||||

First quarter | 14.32 | 10.62 | 23.48 | 20.04 | |||||||||||

11

Holders of common stock — Based on reports by our transfer agent, there were approximately 3,494 registered holders of our common stock on January 31, 2017.

Reference is made to the Equity Compensation Plan Information section of Item 12 for certain information regarding our equity compensation plans.

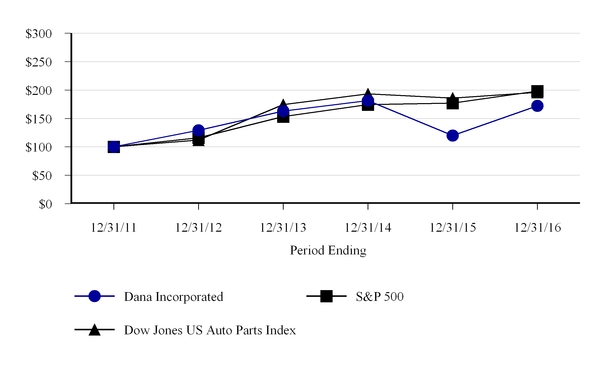

Stockholder return — The following graph shows the cumulative total shareholder return for our common stock since December 31, 2011. The graph compares our performance to that of the Standard & Poor’s 500 Stock Index (S&P 500) and the Dow Jones US Auto Parts Index. The comparison assumes $100 was invested at the closing price on December 31, 2011. Each of the returns shown assumes that all dividends paid were reinvested.

Performance chart

Index

12/31/2011 | 12/31/2012 | 12/31/2013 | 12/31/2014 | 12/31/2015 | 12/31/2016 | ||||||||||||||||||

Dana Incorporated | $ | 100.00 | $ | 129.28 | $ | 162.96 | $ | 181.52 | $ | 119.84 | $ | 172.21 | |||||||||||

S&P 500 | 100.00 | 116.00 | 153.58 | 174.60 | 177.01 | 198.18 | |||||||||||||||||

Dow Jones US Auto Parts Index | 100.00 | 111.90 | 174.63 | 193.20 | 186.03 | 196.10 | |||||||||||||||||

Dividends — We declared and paid quarterly common stock dividends in 2016 and 2015, raising the dividend from five cents to six cents per share in the second quarter of 2015.

Issuer's purchases of equity securities — Our Board of Directors approved an expansion of our existing common stock share repurchase program from $1,400 to $1,700 on January 11, 2016. The share repurchase program expires on December 31, 2017. We repurchase shares utilizing available excess cash either in the open market or through privately negotiated transactions. The stock repurchases are subject to prevailing market conditions and other considerations. During the second half of 2016, there were no shares of our common stock repurchased under the program. Approximately $219 remained available under the program for future repurchases as of December 31, 2016.

Annual meeting — We will hold an annual meeting of stockholders on April 27, 2017.

12

Item 6. Selected Financial Data

Year Ended December 31, | ||||||||||||||||||||

2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

Operating Results | ||||||||||||||||||||

Net sales | $ | 5,826 | $ | 6,060 | $ | 6,617 | $ | 6,769 | $ | 7,224 | ||||||||||

Income from continuing operations before income taxes | 215 | 292 | 260 | 368 | 364 | |||||||||||||||

Income from continuing operations | 653 | 176 | 343 | 261 | 315 | |||||||||||||||

Income (loss) from discontinued operations | 4 | (15 | ) | (1 | ) | — | ||||||||||||||

Net income | 653 | 180 | 328 | 260 | 315 | |||||||||||||||

Net income attributable to the parent company | $ | 640 | $ | 159 | $ | 319 | $ | 244 | $ | 300 | ||||||||||

Preferred stock dividend requirements | — | — | 7 | 25 | 31 | |||||||||||||||

Preferred stock redemption premium | — | — | — | 232 | — | |||||||||||||||

Net income (loss) available to common stockholders | $ | 640 | $ | 159 | $ | 312 | $ | (13 | ) | $ | 269 | |||||||||

Net income (loss) per share available to common stockholders | ||||||||||||||||||||

Basic | ||||||||||||||||||||

Income (loss) from continuing operations | $ | 4.38 | $ | 0.98 | $ | 2.07 | $ | (0.08 | ) | $ | 1.82 | |||||||||

Income (loss) from discontinued operations | — | 0.02 | (0.10 | ) | (0.01 | ) | — | |||||||||||||

Net income (loss) | 4.38 | 1.00 | 1.97 | (0.09 | ) | 1.82 | ||||||||||||||

Diluted | ||||||||||||||||||||

Income (loss) from continuing operations | $ | 4.36 | $ | 0.97 | $ | 1.93 | $ | (0.08 | ) | $ | 1.40 | |||||||||

Income (loss) from discontinued operations | — | 0.02 | (0.09 | ) | (0.01 | ) | — | |||||||||||||

Net income (loss) | 4.36 | 0.99 | 1.84 | (0.09 | ) | 1.40 | ||||||||||||||

Depreciation and amortization of intangibles | $ | 182 | $ | 174 | $ | 213 | $ | 262 | $ | 277 | ||||||||||

Net cash provided by operating activities | 384 | 406 | 510 | 577 | 339 | |||||||||||||||

Purchases of property, plant and equipment | 322 | 260 | 234 | 209 | 164 | |||||||||||||||

Financial Position | ||||||||||||||||||||

Cash and cash equivalents and marketable securities | $ | 737 | $ | 953 | $ | 1,290 | $ | 1,366 | $ | 1,119 | ||||||||||

Total assets | 4,860 | 4,301 | 4,893 | 5,068 | 5,097 | |||||||||||||||

Long-term debt, less debt issuance costs | 1,595 | 1,553 | 1,588 | 1,541 | 790 | |||||||||||||||

Total debt | 1,664 | 1,575 | 1,653 | 1,598 | 891 | |||||||||||||||

Preferred stock | — | — | — | 372 | 753 | |||||||||||||||

Common stock and additional paid-in capital | 2,329 | 2,313 | 2,642 | 2,842 | 2,670 | |||||||||||||||

Treasury stock | (83 | ) | (1 | ) | (33 | ) | (366 | ) | (25 | ) | ||||||||||

Total parent company stockholders' equity | 1,157 | 728 | 1,080 | 1,309 | 1,836 | |||||||||||||||

Book value per share | $ | 7.92 | $ | 4.58 | $ | 6.83 | $ | 8.94 | $ | 12.41 | ||||||||||

Common Share Information | ||||||||||||||||||||

Dividends declared per common share | $ | 0.24 | $ | 0.23 | $ | 0.20 | $ | 0.20 | $ | 0.20 | ||||||||||

Weighted-average common shares outstanding | ||||||||||||||||||||

Basic | 146.0 | 159.0 | 158.0 | 146.4 | 148.0 | |||||||||||||||

Diluted | 146.8 | 160.0 | 173.5 | 146.4 | 214.7 | |||||||||||||||

Market prices | ||||||||||||||||||||

High | $ | 19.81 | $ | 23.48 | $ | 24.82 | $ | 23.46 | $ | 16.76 | ||||||||||

Low | 9.80 | 13.01 | 16.81 | 15.17 | 11.13 | |||||||||||||||

Note: | Total assets for 2015, 2014, 2013 and 2012 have been recast to reflect the adoption of the accounting standard requiring all deferred income tax liabilities and assets to be classified as noncurrent on the balance sheet rather than separated into current and noncurrent amounts. The recasting of total assets resulted in reductions of $25, $12, $35 and $34 for 2015, 2014, 2013 and 2012. See Note 1 to our consolidated financial statements in Item 8 for additional information. |

13

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations (Dollars in millions)

Management's discussion and analysis of financial condition and results of operations should be read in conjunction with the financial statements and accompanying notes in Item 8.

Management Overview

We are a global provider of high technology driveline, sealing and thermal-management products for virtually every major vehicle manufacturer in the on-highway and off-highway markets. Our driveline products – axles, driveshafts and transmissions – are delivered through our Light Vehicle Driveline Technologies (Light Vehicle), Commercial Vehicle Driveline Technologies (Commercial Vehicle) and Off-Highway Driveline Technologies (Off-Highway) operating segments. Our fourth global operating segment – Power Technologies – is the center of excellence for the sealing and thermal technologies that span all customers in our on-highway and off-highway markets. We have a diverse customer base and geographic footprint which minimizes our exposure to individual market and segment declines. In 2016, 54% of our sales came from North American operations and 46% from operations throughout the rest of the world. Our sales by operating segment were Light Vehicle – 45%, Commercial Vehicle – 21%, Off-Highway – 16% and Power Technologies – 18%.

Operational and Strategic Initiatives

In 2016 we outlined our current enterprise strategy which leverages our strong technology foundation and our commitment to continuous improvement. Our strategy places increased focus leveraging resources across the organization, satisfying customer requirements, expanding products and markets and accelerating commercialization of new technology.

Central to our strategy is leveraging our core operations by sharing our capabilities, technology, assets and people across the enterprise, leading to improved execution and increased customer satisfaction. Although we have taken significant strides to improve our profitability and margins, particularly through streamlining and rationalizing our manufacturing activities, we believe additional opportunities remain to further improve our cost performance. Leveraging investments across multiple end markets and making disciplined, value enhancing acquisitions, will allow us to bring product to market faster, grow our top-line sales and enhance financial returns.

Strengthening customer centricity and expanding global markets are key elements of our strategy that focus on market penetration. Foundational to growing the business is directing the entire organization to putting the customer at the center of our value system and shifting from transactional to relationship-based interactions. These relationships are built on a foundation of providing unparalleled technology with exceptional quality, delivery and value. With even stronger relationships we will be better positioned to support our customers’ most important global and flagship programs and capitalize on future growth opportunities.

We continue to enhance and expand our global footprint, optimizing it to capture growth across all of our end markets. Specifically, our manufacturing and technology center footprint positions us to support customers globally – an important factor as many of our customers are increasingly focused on common solutions for global platforms. While growth opportunities are present in each region of the world, we have a primary focus on building our presence and local capability in the Asia Pacific region. Over the last few years, we have opened two new engineering facilities in the region and recently new gear manufacturing facilities were established in India and Thailand.

In addition to Asia, we see further growth opportunity in Eastern Europe where we recently announced plans to establish a new gear manufacturing facility in Hungary. This will be our third facility in the country and will give us the capability to cost effectively manufacture gears, one of our core technologies, and efficiently service our customers within the region.

The final two elements of our enterprise strategy, commercializing new technology and accelerating hybridization and electrification, focus on opportunities for product expansion. Bringing new innovations to market as industry leading products will drive growth as our new products and technology provide our customers with cutting edge solutions, address end user needs and capitalize on key market trends. An example is our industry leading electronically disconnecting all-wheel drive technology, which we believe is the most fuel efficient rapidly disconnecting system in the market, was recently selected by a major global customer for a significant new global vehicle platform – opening up new commercial channels for us in the passenger car, crossover and sport utility vehicle markets.

Initiatives to capitalize on evolving hybridization and electrification vehicle trends are a core ingredient of the current strategy. In addition to our current technologies in battery cooling and fuel cells, this element of the strategy is leveraging our electronics controls expertise across all our business units and applications such as advanced vehicle hybridization and

14

electrification initiatives. We are working with customers to develop new solutions for those markets where electrification will be adopted first such as hybrids, buses and urban delivery vehicles. These new solutions, which include advanced electric propulsion systems with fully integrated motors and controls, are included in our recently launched Spicer Electrified portfolio of products.

The development and implementation of this enterprise strategy is positioning Dana to grow profitably over the next few years due to increased customer focus as we leverage our core capabilities, expand into new markets, develop and commercialize new technologies including for hybrid and electric vehicles.

Shareholder returns and capital structure actions — When evaluating capital structure initiatives, we balance our growth opportunities and shareholder value initiatives with maintaining a strong balance sheet and access to capital. Our strong financial position has enabled us to simplify our capital structure while providing returns to our shareholders in the form of cash dividends and reduction in the number of shares outstanding. Over the past four years, we returned $1,481 of cash to shareholders in connection with redemption of all of our preferred stock and repurchase of common shares. From program inception in 2012 through December 31, 2016, we repurchased approximately 74 million shares, inclusive of the common share equivalent reduction resulting from redemption of preferred shares. Remaining share repurchase authorization under the program approved by our Board of Directors is $219. We declared and paid quarterly common stock dividends over the past four years, raising the dividend from five cents to six cents per share in the second quarter of 2015.

We have taken advantage of the lower interest rate environment to refinance our senior notes at lower rates while extending the maturities. In December 2014 and the first quarter of 2015, we completed the redemption of notes maturing in 2019, replacing them with notes maturing in 2024. During the second quarter of 2016, we redeemed notes maturing in 2021, replacing them with notes maturing in 2026.

Aftermarket opportunities — We have a global group dedicated to identifying and developing aftermarket growth opportunities that leverage the capabilities within our existing businesses – targeting increased future aftermarket sales. In January 2016, we completed the acquisition of Magnum® Gaskets' (Magnum) aftermarket distribution business which includes the Magnum brand, product portfolio, existing customer contracts and distribution rights. The Magnum brand is the third largest aftermarket sealing brand in the U.S. and Canada, providing us with access to new customers for sealing products and an additional aftermarket channel for other products.

Selective acquisitions — Our acquisition focus is principally directed at “bolt-on” or adjacent acquisition opportunities that have a strategic fit with our existing core businesses, particularly opportunities that support our enterprise strategy and enhance the value proposition of our product offerings. Any potential acquisition will be evaluated in the same manner we currently consider customer program opportunities and other uses of capital – with a disciplined financial approach designed to ensure profitable growth and increased shareholder value.

Acquisitions

SIFCO — On December 23, 2016, we acquired strategic assets of the commercial vehicle steer axle systems and related forged components businesses of SIFCO. The acquisition enables us to enhance our vertically integrated supply chain, which will further improve our cost structure and customer satisfaction by leveraging SIFCO's extensive experience and knowledge of sophisticated forged components. In addition to strengthening our position as a central source for products that use forged and machined parts throughout the region, this acquisition enables us to better accommodate the local content requirements of our customers, which reduces their import and other region-specific costs.

In 2011, we began purchasing parts from SIFCO under an exclusive supply agreement. In April 2014, SIFCO began operating with judicial oversight under reorganization proceedings in Brazil. We continued purchasing parts from SIFCO under an interim agreement while also pursuing the purchase of certain assets through the judicial reorganization proceedings. In connection with the December 2016 acquisition, we acquired the assets supporting the business previously conducted under the exclusive supply agreement along with certain additional related business. As part of the acquisition, we added two manufacturing facilities and approximately 1,400 employees. The strategic assets were acquired by Dana free and clear of any liens, claims or encumbrances, and without assumption of any legacy liabilities of SIFCO. We had sales of $86 in 2016 resulting from business conducted under the previous supply agreement with SIFCO. With the acquisition completed in December 2016, we obtained additional business relationships that are expected to generate incremental sales of approximately $50 at current production levels.

The purchase price was $69, with the payment of $9 of the purchase price deferred until December 2017 pending any claims under indemnification provisions of the purchase agreement. The purchase price is subject to customary post-closing

15

adjustments for final determination of working capital and other items. Reference is made to Note 2 of the consolidated financial statements in Item 8 of Part II for the allocation of purchase consideration to assets acquired and liabilities assumed. The results of operations of the SIFCO related business are reported within our Commercial Vehicle operating segment.

Magnum — On January 29, 2016, we acquired the aftermarket distribution business of Magnum, a U.S.-based supplier of gaskets and sealing products for automotive and commercial vehicle applications, for a purchase price of $18 at closing and additional cash payments of up to $2 contingent upon the achievement of certain sales metrics over a future two-year period. As of the closing date of the acquisition, the contingent consideration was assigned a fair value of approximately $1. Assets acquired included trademarks and trade names, customer relationships and goodwill. The results of operations of Magnum are reported within our Power Technologies operating segment.

Brevini — On February 1, 2017, we acquired 80% ownership interests in Brevini Fluid Power S.p.A. (BFP) and Brevini Power Transmission S.p.A. (BPT) from Brevini Group S.p.A. (Brevini). The acquisition expands our Off-Highway operating segment product portfolio to include technologies for tracked vehicles, doubling our addressable market for off-highway driveline systems and establishing Dana as the only off-highway solutions provider that can manage the power to both move the equipment and perform its critical work functions. This acquisition also brings a platform of technologies that can be leveraged in our light and commercial vehicle end markets, helping to accelerate our hybridization and electrification initiatives. The acquisition is expected to add approximately $350 of sales and $35 of adjusted EBITDA in 2017.

We paid €167 at closing, using cash on hand, and intend to refinance debt assumed in the transaction during the first quarter of 2017. The purchase price is subject to adjustment upon determination of the net indebtedness and net working capital levels of BFP and BPT as of the closing date. The terms of the agreement provide Dana the right to call Brevini's noncontrolling interests in BFP and BPT, and Brevini the right to put its noncontrolling interests in BFP and BPT to Dana, assuming Dana does not exercise its call rights, at dates and prices defined in the agreement.

Divestitures

Nippon Reinz — On November 30, 2016, we sold our 53.7% interest in Nippon Reinz Co. Ltd. (Nippon Reinz) to Nichias Corporation. Dana received net cash proceeds of $5 and recognized a pre-tax loss of $3 on the divestiture of Nippon Reinz, inclusive of the derecognition of the related noncontrolling interest. Nippon Reinz had sales of $42 in 2016 through the transaction date.

Dana Companies — On December 30, 2016, we completed the divestiture of Dana Companies, LLC (DCLLC), a consolidated wholly-owned limited liability company that was established as part of our reorganization in 2008 to hold and manage personal injury asbestos claims retained by the reorganized Dana Corporation, which was merged into DCLLC. The assets of DCLLC at time of sale included cash and marketable securities along with the rights to insurance coverage in place to satisfy a significant portion of its liabilities. We received net cash proceeds of $29 at closing on December 30, 2016, with $3 retained by the purchaser subject to the satisfaction of certain future conditions that we expect will be achieved in 2017. We recognized a pre-tax loss of $77 in 2016 upon completion of the transaction. In the event the conditions associated with the retained purchase price of $3 are satisfied in the future, income of $3 will be recognized at such time. Following completion of the sale, Dana has no obligation with respect to current or future asbestos claims. The sale of this business also enhanced our available liquidity since the net proceeds from the sale are available for use in our core businesses.

Disposal of operations in Venezuela — The operating, political and economic environment in Venezuela in recent years was very challenging. Foreign exchange controls restricted our ability to import required parts and material and satisfy the related U.S. dollar obligations. Production activities were curtailed for most of 2014 as our major original equipment customers suspended production, with a limited amount of activity coming back on line later in the year. Our sales in Venezuela during 2014 approximated $110 as compared to $170 in 2013. Results of operations were adversely impacted by the reduced production levels making break-even operating performance a significant challenge. Further, devaluations of the bolivar along with other foreign exchange developments provided added volatility to results of operations and increased uncertainty around future performance.

In December 2014, we entered into an agreement to divest our operations in Venezuela (the disposal group) to an unaffiliated company for no consideration. We completed the divestiture in January 2015. In connection with the divestiture, we entered into a supply and technology agreement whereby Dana will supply product and technology to the operations at competitive market prices. Dana has no obligations to otherwise provide support to the operations. The disposal group was classified as held for sale at December 31, 2014, and we recognized a net charge of $77 – an $80 loss to adjust the carrying value of the net assets to fair value less cost to sell, with a reduction of $3 for the noncontrolling interest share of the loss. These assets and liabilities were presented as held for sale on our December 31, 2014 balance sheet. Upon completion of the

16

divestiture of the disposal group in January 2015, we recognized a gain of $5 on the derecognition of the noncontrolling interest in a former Venezuelan subsidiary in Other income, net. We also credited other comprehensive loss attributable to the parent for $10 and other comprehensive loss attributable to noncontrolling interests for $1 to eliminate the unrecognized pension expense recorded in accumulated other comprehensive loss. See Note 3 to our consolidated financial statements in Item 8 for additional information. With the completion of the sale in January 2015, Dana has no remaining investment in Venezuela.

Structural Products Business — In 2010, we completed the sale of substantially all of the assets of our Structural Products business to Metalsa S.A. de C.V. (Metalsa) and reached a final agreement with the buyer on disputed issues in May 2014. Prior to the third quarter of 2012, Structural Products was reported as an operating segment of continuing operations. With the cessation of the retained operations in the third quarter of 2012, we began reporting the activities relating to the Structural Products business as discontinued operations. Legal and other costs incurred in 2014 to settle a customer complaint and the remaining disputes with Metalsa and insurance recoveries in 2015 related to previously outstanding claims have extended the reporting of discontinued operations.

Segments

We manage our operations globally through four operating segments. Our Light Vehicle and Power Technologies segments primarily support light vehicle original equipment manufacturers (OEMs) with products for light trucks, SUVs, CUVs, vans and passenger cars. The Commercial Vehicle segment supports the OEMs of on-highway commercial vehicles (primarily trucks and buses), while our Off-Highway segment supports OEMs of off-highway vehicles (primarily wheeled vehicles used in construction, mining and agricultural applications).

Trends in Our Markets

Global Vehicle Production

Actual | |||||||||||||

(Units in thousands) | Dana 2017 Outlook | 2016 | 2015 | 2014 | |||||||||

North America | |||||||||||||

Light Truck (Full Frame) | 4,200 | to | 4,300 | 4,438 | 4,136 | 3,834 | |||||||

Light Vehicle Engines | 15,800 | to | 16,200 | 16,065 | 15,474 | 15,119 | |||||||

Medium Truck (Classes 5-7) | 235 | to | 250 | 235 | 237 | 226 | |||||||

Heavy Truck (Class 8) | 190 | to | 210 | 227 | 323 | 297 | |||||||

Agricultural Equipment | 50 | to | 60 | 53 | 58 | 64 | |||||||

Construction/Mining Equipment | 150 | to | 160 | 150 | 158 | 158 | |||||||

Europe (including Eastern Europe) | |||||||||||||

Light Truck | 9,300 | to | 9,500 | 9,279 | 8,546 | 7,790 | |||||||

Light Vehicle Engines | 23,800 | to | 24,300 | 23,224 | 22,570 | 21,510 | |||||||

Medium/Heavy Truck | 440 | to | 470 | 471 | 434 | 397 | |||||||

Agricultural Equipment | 190 | to | 210 | 193 | 202 | 220 | |||||||

Construction/Mining Equipment | 290 | to | 310 | 290 | 299 | 301 | |||||||

South America | |||||||||||||

Light Truck | 1,000 | to | 1,050 | 1,010 | 940 | 1,146 | |||||||

Light Vehicle Engines | 2,000 | to | 2,100 | 2,091 | 2,439 | 3,176 | |||||||

Medium/Heavy Truck | 75 | to | 85 | 70 | 88 | 167 | |||||||

Agricultural Equipment | 25 | to | 35 | 29 | 32 | 43 | |||||||

Construction/Mining Equipment | 10 | to | 15 | 10 | 13 | 17 | |||||||

Asia-Pacific | |||||||||||||

Light Truck | 26,500 | to | 27,500 | 27,179 | 24,160 | 22,337 | |||||||

Light Vehicle Engines | 50,000 | to | 51,500 | 50,075 | 47,209 | 46,497 | |||||||

Medium/Heavy Truck | 1,450 | to | 1,550 | 1,620 | 1,383 | 1,573 | |||||||

Agricultural Equipment | 680 | to | 720 | 648 | 676 | 710 | |||||||

Construction/Mining Equipment | 380 | to | 410 | 396 | 405 | 509 | |||||||

17

North America

Light vehicle markets — Improving economic conditions during the past few years have contributed to increased light vehicle sales and production levels in North America. Release of built-up demand to replace older vehicles, greater availability of credit, stronger consumer confidence and other factors have combined to stimulate new vehicle sales. Light vehicle sales in 2016 increased about 1% from 2015, with sales that year being up 6% from 2014. Many of our programs are focused in the full frame light truck segment. Helped by comparatively lower fuel prices, sales in this segment were especially strong, being up about 6% in 2016 and 9% in 2015. Production levels were reflective of the stronger light vehicle sales. Production of approximately 17.8 million light vehicles in 2016 was 2% higher than in 2015, following an increase in production that year of about 3% from 2014. Light vehicle engine production was similarly higher, up 4% in 2016 and 2% in 2015. In the key full frame light truck segment, production levels increased about 7% in 2016 compared with an increase of 8% in 2015. Days’ supply of total light vehicles in the U.S. at the end of December 2016 was around 62 days, up slightly from 61 days at December 2015 and 2014. In the full frame light truck segment, inventory levels have been relatively stable – 65 days at the end of December 2016, compared with 62 days at the end of 2015 and 63 days at the end of 2014.

Looking ahead to 2017, we expect steady employment levels, stable fuel prices and favorably trending consumer confidence will provide a generally solid economic climate in North America. However, with the strength in this market the past couple years, we believe slightly lower production levels are likely. Our full year 2017 outlook for light vehicle engine production is 15.8 to 16.2 million units, a decrease of 2% to an increase of 1% compared with 2016. In the full frame light truck segment where the past two years have been especially strong, our 2017 production outlook is 4.2 to 4.3 million units, a decrease of 3 to 5% from 2016.

Medium/heavy vehicle markets — Similar to the light vehicle market, the commercial vehicle segment benefited from an improving North America economy in recent years. After increasing 12% in 2014, Medium duty Classes 5-7 truck production the past three years has been relatively stable, between 226,000 and 237,000 units. In the Class 8 segment, production levels increased 21% in 2014 and another 9% in 2015 to reach 323,000 units. High levels of production in 2014 and the first half of 2015 led to more trucks than required for freight demand. As such, order levels and production began declining in the second half of 2015 and continued into 2016, resulting in Class 8 production of around 227,000 units, a decline of about 30% from 2015.