Attached files

| file | filename |

|---|---|

| EX-23.3 - EX-23.3 - Evolve Transition Infrastructure LP | a2230168zex-23_3.htm |

| EX-23.2 - EX-23.2 - Evolve Transition Infrastructure LP | a2230168zex-23_2.htm |

| EX-23.1 - EX-23.1 - Evolve Transition Infrastructure LP | a2230168zex-23_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

As filed with the Securities and Exchange Commission on November 4, 2016

Registration No. 333-213219

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Sanchez Production Partners LP

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

1311 (Primary Standard Industrial Classification Code Number) |

11-3742489 (I.R.S. Employer Identification Number) |

1000 Main Street, Suite 3000

Houston, Texas 77002

(713) 783-8000

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Charles C. Ward

Chief Financial Officer

Sanchez Production Partners GP LLC

1000 Main Street, Suite 3000

Houston, Texas 77002

(713) 783-8000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Scott L. Olson Andrews Kurth Kenyon LLP 600 Travis, Suite 4200 Houston, Texas 77002 (713) 220-4200 |

Hillary H. Holmes Baker Botts L.L.P. One Shell Plaza 910 Louisiana Street Houston, Texas 77002 (713) 229-1234 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable following effectiveness of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED NOVEMBER 4, 2016

PROSPECTUS

Sanchez Production Partners LP

8,823,529 Common Units

Representing Limited Partner Interests

Sanchez Production Partners LP is offering 8,823,529 common units representing limited partner interests. We expect the public offering price will be between $16.00 and $18.00 per common unit. Our common units are listed on the NYSE MKT LLC, or the NYSE MKT, under the symbol "SPP." The last reported sales price of the common units on the NYSE MKT on November 3, 2016 was $14.05 per common unit.

Investing in our common units involves a high degree of risk. Before making a decision to purchase common units in this offering, you should read "Risk Factors" beginning on page 14 of this prospectus and the other risks identified in the documents incorporated by reference herein.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| |

Per Common Unit |

Total | ||

|---|---|---|---|---|

| Public offering price | $ | $ | ||

| Underwriting discounts and commissions(1) | $ | $ | ||

| Proceeds, before expenses, to us | $ | $ |

- (1)

- Excludes a structuring fee payable to Johnson Rice & Company L.L.C. equal to 0.50% of the aggregate gross proceeds of this offering, including any proceeds from the exercise by the underwriters of their option to purchase additional common units. See "Underwriting" beginning on page 93 of this prospectus for additional information regarding underwriting compensation.

The underwriters may also purchase up to an additional 1,323,530 common units from us at the public offering price, less underwriting discounts and commissions and the structuring fee payable by us, within 30 days from the date of this prospectus. If the underwriters exercise their option in full, the total underwriting discounts and commissions will be $ , and the total net proceeds to us from this offering, after deducting the underwriting discounts and commissions, the structuring fee and estimated offering expenses, will be $ .

The underwriters expect to deliver the common units on or about , 2016.

Joint Book-Running Managers

| Citigroup | RBC Capital Markets | |

BofA Merrill Lynch |

Johnson Rice & Company L.L.C. |

Co-Managers

| Seaport Global Securities | Stephens Inc. |

Tudor, Pickering, Holt & Co.

Prospectus dated , 2016

We and the underwriters have not authorized any other person to provide you with information or to make any representations other than that contained in this prospectus and any free writing prospectus that we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. You should read this prospectus, including the documents incorporated by reference herein, and any free writing prospectus that we have authorized for use in connection with this offering in their entirety before making an investment decision. We and the underwriters are not making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. The information in this prospectus and in any free writing prospectus that we prepared is accurate only as of the date of this prospectus or such free writing prospectus, regardless of the time of delivery of this prospectus or such free writing prospectus or any sale of the common units. Our business, financial condition, results of operations and prospects may have changed since such dates. We will update this prospectus as required by federal securities laws.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. Please read "Risk Factors" beginning on page 14 of this prospectus and "Cautionary Note Regarding Forward-Looking Statements" beginning on page 18.

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications or other published independent sources. Some data is also based on our good faith estimates. Although we believe these third-party sources are reliable and that the information is accurate and complete, we have not independently verified the information.

i

This summary highlights certain information about us, this offering and selected information contained elsewhere in or incorporated by reference into this prospectus. This summary is not complete and does not contain all of the information that you should consider before deciding whether to invest in our common units. Unless otherwise indicated, the information in this prospectus assumes (1) a public offering price of $17.00 per common unit (the midpoint of the price range set forth on the cover page of this prospectus) and (2) that the underwriters do not exercise their option to purchase additional common units. For a more complete understanding of our business and this offering, we encourage you to read and consider carefully the more detailed information in this prospectus, including the information incorporated by reference in this prospectus, and the information included in any free writing prospectus that we have authorized for use in connection with this offering, including the information under the heading "Risk Factors" beginning on page 14 of this prospectus, the financial statements and related notes, and the other information that we incorporate by reference into this prospectus.

As used in this prospectus, unless we indicated otherwise: (i) "Sanchez Production Partners," "the partnership," "we," "us," "our" or like terms refer collectively to Sanchez Production Partners LP and its consolidated subsidiaries. Such terms also refer to Sanchez Production Partners LLC, our predecessor-in-interest prior to our conversion from a limited liability company to a limited partnership, (ii) "our general partner" refers to Sanchez Production Partners GP LLC, our general partner, (iii) "Sanchez Energy" refers to Sanchez Energy Corporation (NYSE: SN) and its consolidated subsidiaries, (iv) "SOG" refers to Sanchez Oil & Gas Corporation, an entity that provides operational support to us, (v) "SP Holdings" refers to SP Holdings, LLC, the sole member of our general partner, and (vi) "Carnero Gathering" refers to Carnero Gathering, LLC, an entity in which we own a 50% equity interest. We include a glossary of some of the oil and natural gas terms used in this prospectus in Appendix A.

Sanchez Production Partners LP

Overview

We are a growth-oriented limited partnership focused on the acquisition, development, ownership and operation of midstream and production assets in North America. We believe that our relationships with Sanchez Energy and SOG provide us with organic growth opportunities across multiple basins and facilitate accretive acquisition opportunities from both Sanchez Energy and other third parties.

In October 2015, we purchased from Sanchez Energy approximately 150 miles of gathering pipelines, four main gathering and processing facilities, including stabilizers, storage tanks, compressors and dehydration units and other related assets in Western Catarina (the "Western Catarina Midstream System"). The Western Catarina Midstream System has capacity of 40 MBbl/d for crude oil and NGLs and 200 MMcf/d for natural gas, provides connectivity to multiple markets via four takeaway pipelines and is anchored by a long term fee-based contract with Sanchez Energy. As of December 31, 2015, according to its filings with the SEC, Sanchez Energy had approximately 200,000 net leasehold acres in the oil and condensate windows of the Eagle Ford Shale in Texas, with total proved reserves of 128 MMBoe, including 85 MMBoe in the 35,000 dedicated acreage area under our gathering agreement with Sanchez Energy for the Western Catarina Midstream System. Average daily throughput for the third quarter of 2016 was 175.6 MMcf/d of natural gas and 12.1 MBbl/d of crude oil and NGLs. These quantities were approximately 124% and 119% of the minimum quarterly throughput requirements for natural gas and oil, respectively.

In July 2016, we purchased from Sanchez Energy a 50% interest in Carnero Gathering which owns approximately 45 miles (10 miles of which remain under construction) of high pressure natural gas gathering pipelines that currently connect our Western Catarina Midstream System to nearby pipelines in South Texas (the "Carnero Gathering System") and, is designed to directly connect to a cryogenic natural gas processing plant currently expected to be operational in the spring of 2017. The Carnero

1

Gathering System generates substantially all of its revenues under long-term agreements with Sanchez Energy by charging fees for the transportation of natural gas through the pipeline. We do not engage in the marketing and trading of any commodities.

In addition to these midstream assets, we also own production assets in oil and natural gas properties in Texas, Louisiana, Kansas and Oklahoma, including escalating working interests ("EWI") in producing wells located in the Eagle Ford Shale that we purchased from Sanchez Energy in 2015. No maintenance capital expenditures are required by us in order to sustain the production volume in connection with our EWIs.

Our Relationship with Sanchez Energy, SP Holdings and SOG

We believe that our relationship with Sanchez Energy provides us with a strategic advantage and will continue to provide us with significant growth opportunities. Since March 2015, we have completed two midstream acquisitions and one EWI acquisition from Sanchez Energy for an aggregate purchase price of approximately $474.4 million, which includes the assumption of approximately $7.4 million of remaining capital contribution commitments as of July 5, 2016. See "—Recent Acquisitions and Midstream Strategy." Pursuant to a right-of-first-offer, Sanchez Energy has agreed to offer us the right to acquire any midstream assets that it desires to sell. However, Sanchez Energy is under no obligation to sell any assets to us or to accept any offer for its assets that we may choose to make.

We have a shared services agreement in place with SP Holdings (the "Services Agreement"), which in turn has a shared services agreement in place with SOG. SOG also has a shared services agreement in place with Sanchez Energy. We believe that our relationships with SP Holdings and SOG provide us with competitive advantages, including a cost-efficient means of operating our assets. SP Holdings is the sole member of our general partner and has an interest in us through its ownership of all of our incentive distribution rights. SP Holdings and SOG provide services that we require to operate our business, including overhead, technical, administrative, marketing, accounting, operational, information systems, financial, compliance, insurance, acquisition, disposition and financing services. SOG has a senior management team that averages over 20 years of industry experience and employs over 200 full-time employees, including approximately 50 technical staff and engineers. SOG also provides us a dedicated business development team that screens approximately 150 acquisition opportunities per year. SOG was formed in 1972 and has drilled or participated in over 3,000 wells, directly and through joint ventures, and has successfully built and operated extensive midstream and gathering assets associated with its exploration and production assets. Since Sanchez Energy's initial public offering in December 2011, SOG has been responsible for executing on approximately $2.2 billion in total drilling and completion budgets and has assisted in closing approximately $1.3 billion in acquisitions. Since its inception, SOG has cultivated relationships with mineral and surface rights owners in and around the Western Catarina formation and other oil and natural gas basins in North America and has compiled an extensive technological database, including more than 8,500 square miles of 3D seismic data, more than 450,000 well logs, greater than 15,000 wells of electronic documents, as well as a fully integrated suite of the latest interpretive geological software. We plan on leveraging SOG's extensive expertise and experience to execute on our business strategies. While we believe that our relationships with Sanchez Energy, SP Holdings and SOG are a significant strength, they are also a source of potential risks and conflicts. Please read "Risk Factors" and "Conflicts of Interest and Fiduciary Duties."

Business Strategies

Our primary business objective is to create long-term value by generating stable and predictable cash flows that allow us to make and grow our cash distributions per unit over time through the safe

2

and reliable operation of our assets. Our business strategies are subject to risks, please read "Risk Factors." We plan to achieve this objective by executing the following business strategies:

- •

- Grow our business by acquiring fee-based midstream and production assets with minimal maintenance

capital requirements and low overhead to increase unitholder value. We plan to continue growing our business through acquisitions of

midstream and production assets from Sanchez Energy and, as warranted, third parties. We believe that Sanchez Energy will offer us opportunities to acquire additional midstream and production assets

that it currently owns or may acquire or develop in the future, including pursuant to our right-of-first-offer to acquire certain midstream assets from Sanchez Energy. Sanchez Energy has identified

over $800 million of potential divestment targets, including two divestment targets of immediate interest to us that represent more than $100 million in potential capital spending in

2016 and 2017. The identified acquisitions consist of a mix of midstream and production assets, including the EWIs and the Raptor Plant described below under "—Pending Acquisitions" on

page 7.

- •

- Support stable cash flows by aligning our asset base and operations with SOG's operational

platform and Sanchez Energy's asset base. Each of the Western Catarina Midstream System and the Carnero Gathering System is underpinned

by long term, fee-based contracts with Sanchez Energy that contain minimum volume commitments. We believe that Sanchez Energy plans to continue to develop its Catarina lease, which has been dedicated

to the Western Catarina Midstream System and the Carnero Gathering System, and has a 50 well annual drilling commitment on its Catarina acreage. According to its filings with the SEC, Sanchez Energy

has identified over 1,350 net potential drilling locations on its Catarina acreage and will continue to require access to infrastructure assets as it develops the lease. We will continue to

strategically align our asset base with Sanchez Energy's needs, which we anticipate will allow us to increase our distributions over time.

- •

- Focus on stable, fixed-fee

businesses. We intend to mitigate direct commodity price exposure by providing midstream services underpinned by long-term contracts

with fixed-fee components. The majority of our identified acquisitions and capital projects for the remainder of 2016 and the full year 2017 involve midstream assets and would contain fixed-fee

contracts consistent with this strategy. Similar to our existing contracts with Sanchez Energy, we anticipate that any new long-term commitments arising from these assets, or other assets we may

identify in the future, will be governed by contracts that include fixed fees, reservation-based charges, minimum volume commitments and/or acreage dedications.

- •

- Grow our business through increased throughput. We expect to realize increased throughput on the Western Catarina Midstream System due to the increased drilling plan announced by Sanchez Energy and production activity of Sanchez Energy in the Catarina lease and in other areas of the Catarina lease. Such drilling and production activity is expected to result in additional midstream infrastructure at Catarina, which we may be in a position to acquire pursuant to our right-of-first offer to acquire midstream assets from Sanchez Energy. We also plan to actively market our midstream services to, and pursue strategic relationships with, third-party producers in adjacent geographical areas in order to attract additional services and expansion opportunities. Numerous large independent exploration and production companies offset the Catarina acreage including Anadarko Petroleum Corporation (NYSE: APC), Noble Energy Inc. (NYSE: NBL), and SM Energy Company (NYSE: SM). We believe that the strategic location of the Western Catarina Midstream System and Carnero Gathering System, available capacity on these systems, and access to multiple takeaway pipelines will allow us to capture additional third-party volumes and increase the utilization of these assets. We also expect to realize increased throughput from our pending acquisitions. See "—Pending Acquisitions" on page 7 for more detail.

3

- •

- Maintain financial flexibility and strong capital structure. As of September 30, 2016, we had approximately $52.7 million of availability under our credit facility. We anticipate that this borrowing capacity, together with cash and cash equivalents maintained by us as of September 30, 2016 will result in approximately $89.7 million of liquidity immediately following the closing of this offering. For the quarter ended September 30, 2016, we had a pro forma debt-to-Adjusted EBITDA (as defined in our third amended and restated credit agreement (our "credit agreement")) ratio of 2.5x. We anticipate maintaining this ratio below 3.0x. We believe that our liquidity position and strong capital structure will provide us with the financial flexibility to execute on our identified acquisitions and our other business strategies.

Competitive Strengths

The following competitive strengths involve risks, please read "Risk Factors." We believe that we are well positioned to successfully execute our business strategies because of the following competitive strengths:

- •

- Stable cash flows through long term fixed-fee

agreements. Sanchez Energy's production in the Eagle Ford Shale that we service is pursuant to long-term, fixed-fee contracts. We

believe that the gathering agreements with Sanchez Energy related to the Western Catarina Midstream System and the Carnero Gathering System, and the dedication of the Catarina lease acreage to the

Western Catarina Midstream System and the Carnero Gathering System, combined with our hedging activities related to production assets, enable us to generate stable, predictable cash flows and

substantially mitigate our direct exposure to commodity price risk.

- •

- Well-positioned assets in a high-growth area. Our midstream assets currently serve all of Sanchez Energy's production on its Catarina lease acreage in the Eagle Ford Shale in South Texas, from which Sanchez Energy produced an average of approximately 3,795 net MBoe/d of crude oil, condensate, natural gas and NGLs during the three months ended September 30, 2016. Our Western Catarina Midstream System is located entirely within a large, contiguous acreage position in the core of the Eagle Ford Shale, which we believe provides Sanchez Energy with a low risk, multi-year development drilling inventory. Substantially all of Sanchez Energy's drilling locations within our dedicated area are within two miles of our midstream assets. These drilling locations are located within Sanchez Energy's core position in the Eagle Ford Shale where it has achieved strong production growth since the completion of its acquisition of the Catarina leasehold in June 2014, and has increased potential drilling inventory by more than 600% as of September 30, 2016. Development activity at Catarina is further supported by the Carnero Gathering System, which provides high pressure natural gas gathering pipelines that currently connect our Western Catarina Midstream System to nearby pipelines and will directly connect to a cryogenic natural gas processing plant that is under construction. Due to the close proximity of our gathering systems to substantially all of Sanchez Energy's drilling locations in our dedicated acreage, we believe that Sanchez Energy's recently announced increased drilling program on the Catarina lease will result in increasing our throughput volumes with minimal capital expenditures or financing requirements. In addition, the lease terms on the Catarina acreage require Sanchez Energy to drill 50 wells per year, giving us further confidence in stable or growing volumes over time. We expect that our acreage dedication from Sanchez Energy along with our operating footprint will allow us to capture the majority of incremental production volumes associated with Sanchez Energy's horizontal drilling program throughout the Eagle Ford Shale. We are strategically positioned to expand our delivery of midstream services within the Eagle Ford Shale as Sanchez Energy executes on its drilling and development strategy. We believe that production growth in this area should increase utilization of our midstream assets and create organic growth opportunities over time.

4

- •

- Our relationships with SOG and Sanchez

Energy. One of our principal strengths is our relationships with both SOG and Sanchez Energy. In addition to the benefits that we

receive as a result of having Sanchez Energy as the anchor customer for the Western Catarina Midstream System and the Carnero Gathering System, we believe that our relationships with both SOG and

Sanchez Energy will provide us with the following opportunities for growth over time:

- •

- Acquisitions of midstream assets sold by Sanchez

Energy. Sanchez Energy has identified over $800 million of potential divestment targets, including two divestment targets of immediate interest to us that

represent more than $100 million in potential capital spending in 2016 and 2017. These identified acquisitions consist of a mix of midstream and production assets, including the EWIs and the

Raptor Plant described below under "—Pending Acquisitions" on page 7. We believe that our relationship with Sanchez Energy and its affiliates will provide us with significant growth

opportunities stemming from its assets, as well as others that may be developed by Sanchez Energy in the normal course of its business. We have a right-of-first offer to acquire any future

divestitures of Sanchez Energy's midstream assets, including equipment, pipelines, tanks and tangible personal property used for the gathering, transportation and plant separation of hydrocarbons from

wells. Because of our strategic relationship with SOG, we believe that Sanchez Energy is incentivized to offer us these and similar assets that it may develop in the future outside of our current

dedicated acreage areas because our expected competitive cost of capital will allow us to acquire assets at values that increase the realized rates of return on Sanchez Energy's investment in these

assets.

- •

- Access to Operational and Industry Expertise. We expect to

benefit from the extensive operational, commercial and technical expertise of SOG, Sanchez Energy and SP Holdings, as well as their industry relationships, as we seek to optimize and expand our

existing asset base. We also expect that we will benefit from SOG's history of operating safe and reliable pipelines.

- •

- Producing assets acquired under an EWI structure provide visibility of

volumes with no capital expenditure exposure. A significant portion of our production assets were acquired from Sanchez Energy under an

EWI structure, which provides payments on stable production of approximately 1,000 Boe/d over the first five years given the escalating nature of our working interest and then transitions to payments

based on naturally declining production. Combined with our hedging activities, we believe that this structure provides better visibility and predictability of cash flow when compared to other

acquisition structures. During the initial term of ownership, no maintenance capital expenditures by us are required to sustain the production volumes. We expect to use a portion of the proceeds from

this offering to fund the acquisition of certain wellbores and EWIs and other production assets from Sanchez Energy for $27 million. These interests include working interests in 23 producing

Eagle Ford wellbores located in Dimmit and Zavala counties in South Texas together with escalating working interests in an additional 11 producing wellbores located in the Palmetto Field in Gonzales

County, Texas. We anticipate seeking additional acquisition opportunities utilizing EWI structures with Sanchez Energy in the future.

- •

- Financial flexibility and strong capital structure. We believe that our borrowing capacity and our expected ability to access debt and equity capital markets provide us with the financial flexibility necessary to execute our business strategies. As of September 30, 2016, we had approximately $52.7 million of availability under our credit facility. We anticipate that this borrowing capacity, together with cash and cash equivalents maintained by us as of September 30, 2016 will result in approximately $89.7 million of liquidity immediately following the closing of this offering. For the quarter ended September 30, 2016, we had a pro forma debt-to-Adjusted EBITDA (as defined in our credit agreement) ratio of 2.5x. We anticipate maintaining this ratio below 3.0x.

5

- •

- Proven and unitholder-aligned management team and partner. Our management team and members of SOG's management team possess substantial experience in the management and operation of pipeline, storage facilities and other midstream assets and extensive expertise in the acquisition, exploration and development of oil and natural gas in unconventional resource plays in North America. SOG was formed in 1972 and has drilled or participated in over 3,000 wells, directly and through joint ventures, and has successfully built and operated the extensive midstream and gathering assets associated with its exploration and production assets. Our management team includes certain owners of our general partner who, along with SOG and other insiders, own approximately 16.2% of our common units and all of our incentive distribution rights as of September 30, 2016. Please see "—Organizational Structure" on page 10 for more ownership information.

We believe that our liquidity position and strong capital structure will provide us with the financial flexibility to execute on our identified acquisitions, our capital projects and our other business strategies.

Recent Acquisitions and Midstream Strategy

Historically, our operations have consisted of the exploration and production of proved reserves. Beginning in 2015, we refocused our business on the acquisition and operation of midstream assets. As a result of our executed and planned acquisitions of midstream assets from Sanchez Energy and our disposition of most of our operated crude oil and natural gas properties during the last 12 months, we expect that our historical financial statements and results of operations will differ substantially from our future financial statements and results of operations. In the future, we expect that the majority of our revenues will be derived from long-term, fee-based gathering and processing agreements with Sanchez Energy and other third parties, rather than from oil and natural gas production.

On July 5, 2016, we purchased from Sanchez Energy a 50% equity interest in Carnero Gathering, a joint venture that is 50% owned by Targa Resources Corp. (NYSE: TRGP) ("Targa"), for an initial payment of approximately $37.0 million and the assumption by us of remaining capital commitments to Carnero Gathering, estimated at approximately $7.4 million as of that date. In addition, we are required to pay Sanchez Energy an earnout based on natural gas received above a threshold volume and tariff at Carnero Gathering's delivery points from Sanchez Energy and other producers. Carnero Gathering owns a total of approximately 45 miles (10 miles of which remain under construction) of high pressure natural gas gathering pipelines that currently connect our Western Catarina Midstream System to nearby pipelines in South Texas. The Carnero Gathering System is designed to directly connect to a cryogenic natural gas processing plant in South Texas that is expected to be operational in the spring of 2017. The processing plant is currently owned by another joint venture between Sanchez Energy and Targa. Sanchez Energy has entered into a 15-year gathering agreement benefiting Carnero Gathering pursuant to which Sanchez Energy is required to maintain a minimum quarterly volume delivery commitment for the first five years after the processing plant is operational.

On October 14, 2015, we acquired the Western Catarina Midstream System from Sanchez Energy for approximately $345.8 million. The system consists of approximately 150 miles of gathering pipelines, four main gathering and processing facilities, including stabilizers, storage tanks, compressors and dehydration units and other related assets in Western Catarina, which are located in Dimmit and Webb Counties, Texas, and services upstream production from the Eagle Ford Shale. The gathering pipelines range in diameter from 4 to 12 inches, with capacity of 40 MBbl/d for crude oil and NGLs and 200 MMcf/d for natural gas. There are four main gathering and processing facilities, which include eight stabilizers of 5,000 barrels per day, approximately 25,000 barrels of storage capacity, NGL pressurized storage, approximately 18,000 horsepower of compression and approximately 300 MMcf/d of dehydration capacity. The gathering system is currently used solely to support the gathering, processing and transportation of crude oil, NGLs and natural gas produced by Sanchez Energy in

6

Western Catarina. The gathering system has crude oil interconnections with the Plains All American Pipeline header system delivered to the Gardendale terminal, and to all four takeaway pipelines to Corpus Christi, and has natural gas interconnections with affiliates of Southcross Energy Partners, L.P., Kinder Morgan, Energy Transfer Partners, L.P. and Transwestern Pipeline Company, LLC. Pipeline capacity on the Western Catarina Midstream System can be expanded through small compression projects at a nominal cost, with approximately $1.0 million in capital expenditures planned per year. Pursuant to a 15-year gathering agreement, Sanchez Energy has agreed to tender all of its crude petroleum, natural gas and other hydrocarbon-based product volumes on approximately 35,000 dedicated acres in the Western Catarina area of the Eagle Ford Shale in South Texas for processing and transportation through the Western Catarina Midstream System, with the potential to tender additional volumes from production activities outside of the dedicated acreage. During the first five years of the contract term (or through 2020), Sanchez Energy is required to meet a minimum quarterly volume delivery commitment for crude oil and natural gas, subject to certain adjustments. In addition, Sanchez Energy is required to pay contractually agreed upon gathering and processing fees for crude oil and natural gas volumes tendered through the Western Catarina Midstream System.

On March 31, 2015, we purchased EWIs from Sanchez Energy for total consideration of $85.0 million. Components of the acquisition included working interests in 59 wellbores located in the Palmetto Field in Gonzales County, Texas, which working interest averaged 18.2% as of January 1, 2015 and will increase annually up to a maximum of 47.5% on January 1, 2019 for the remaining life of the wellbores.

Pending Acquisitions

On October 6, 2016, we entered into a purchase and sale agreement with subsidiaries of Sanchez Energy to acquire certain EWIs and other production assets for $27 million in cash from Sanchez Energy (the "Production Acquisition"). These interests include working interests in 23 producing Eagle Ford wellbores located in Dimmit and Zavala counties in South Texas together with escalating working interests in an additional 11 producing wellbores located in the Palmetto Field in Gonzales County, Texas.

On October 6, 2016, we entered into a purchase and sale agreement with Sanchez Energy and a subsidiary thereof to acquire a 50% equity interest in Carnero Processing, LLC ("Carnero Processing"), a joint venture that is 50% owned by Targa for an initial payment of approximately $47.7 million in cash and the assumption by us of approximately $32.3 million of remaining capital commitments to Carnero Processing. Carnero Processing is developing the Raptor Gas Processing Facility (the "Raptor Plant"), which is a 200MMcf/d cryogenic natural gas processing plant that is being constructed in La Salle County, Texas, and is expected to be completed in April 2017. The Raptor Plant is a strategic asset that we believe will allow us to capture more of the value chain from Sanchez Energy's South Texas production and realize further upside from third party volumes.

On October 6, 2016, we entered into a purchase and sale agreement with Sanchez Energy and a subsidiary thereof ("Lessee") to obtain an option to acquire Lessee's right, title and interest in and to a ground lease with the Calhoun Port Authority. We expect to invest approximately $15 million in a joint venture for the construction of a marine crude storage terminal on or nearby such lease in Point Comfort, Texas. We expect the operation of this terminal to result in the realization of higher netbacks for crude oil produced from certain of Sanchez Energy's acreage and will allow us to realize significant cash flows from terminaling fees of third party volumes. The terminal is expected to be completed in April 2017.

The pending acquisitions for Carnero Processing and the production assets are anticipated to be consummated in connection with the closing of this offering and funded with the net proceeds from this offering. However, there can be no assurances that these pending acquisitions will be consummated

7

or that the expected benefits of such transactions will be realized. The closing of this offering is not conditioned on the consummation of these pending acquisitions. If these pending acquisitions are not consummated, our management will have broad discretion in the application of the net proceeds of this offering. Accordingly, if you decide to purchase common units in this offering, you should be willing to do so whether or not we complete these pending acquisitions. The conflicts committee of the board of directors of our general partner, consisting solely of independent directors, evaluated and approved our two pending acquisitions. The conflicts committee engaged an independent financial advisor and independent legal counsel.

Financial and Operating Results

For the nine months ended September 30, 2016, we had production of 871 MBoe, revenue of $55.4 million, net income of $32.1 million and Adjusted EBITDA of $43 million. In addition, at September 30, 2016, we had cash and cash equivalents of $0.6 million and long-term debt of $146 million.

As a result of our executed and planned acquisitions of midstream assets from Sanchez Energy and our dispositions of most of our operated oil and natural gas properties during the last twelve months as described above under "—Recent Acquisitions and Midstream Strategy", we believe that our historical financial statements and results of operation will differ substantially from our future financial statements and results of operations.

To supplement our financial results and guidance presented in accordance with U.S. generally accepted accounting principles ("GAAP"), we use certain non-GAAP financial measures in this prospectus, including Adjusted EBITDA. We believe that non-GAAP financial measures are helpful in understanding our past financial performance and potential future results, particularly in light of the effect of various transactions effected by us. We define Adjusted EBITDA as net income (loss) adjusted by: (i) interest (income) expense, net which includes interest expense, interest expense net (gain) loss on interest rate derivative contracts, and interest (income); (ii) income tax expense (benefit); (iii) depreciation, depletion and amortization; (iv) asset impairments; (v) accretion expense; (vi) (gain) loss on sale of assets; (vii) (gain) loss from equity investment; (viii) unit-based compensation programs; (ix) unit-based asset management fees; (x) (gain) loss on mark-to-market activities; and (xi) (gain) loss on embedded derivatives.

Adjusted EBITDA is a significant performance metric used by our management to indicate (prior to the establishment of any cash reserves by the board of directors of our general partner) the distributions that we would expect to pay to our unitholders. Specifically, this financial measure indicates to investors whether or not we are generating cash flow at a level that can sustain or support a quarterly distribution or any increase in our quarterly distribution rates. Adjusted EBITDA is also used as a quantitative standard by our management and by external users of our financial statements such as investors, research analysts, our lenders and others to assess: (i) the financial performance of our assets without regard to financing methods, capital structure or historical cost basis; (ii) the ability of our assets to generate cash sufficient to pay interest costs and support our indebtedness; and (iii) our operating performance and return on capital as compared to those of other companies in our industry, without regard to financing or capital structure.

We believe that the presentation of Adjusted EBITDA provides useful information to investors in assessing our financial condition and results of operations. The GAAP measure most directly comparable to Adjusted EBITDA is net income. Our non-GAAP financial measure of Adjusted EBITDA should not be considered as an alternative to GAAP net income. Adjusted EBITDA has important limitations as an analytical tool because it excludes some but not all items that affect net income. Adjusted EBITDA should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP. Because Adjusted EBITDA may be defined differently by other

8

companies in our industry, our definition of Adjusted EBITDA may not be comparable to similarly titled measures of other companies, thereby diminishing its utility.

The following table sets forth a reconciliation of Adjusted EBITDA to net income, its most directly comparable GAAP performance measure, for the nine months ended September 30, 2016 (amounts in thousands) (unaudited).

| |

Actual | |||

|---|---|---|---|---|

Net income |

$ | 32,132 | ||

Adjusted by: |

||||

Interest expense, net |

3,545 | |||

Income tax expense |

— | |||

Depreciation, depletion and amortization |

20,824 | |||

Asset impairments |

1,309 | |||

Accretion expense |

901 | |||

(Gain) Loss on sale of assets |

219 | |||

Unit-based compensation programs |

1,619 | |||

Unit-based asset management fees |

4,903 | |||

Distributions in excess of equity earnings |

1,094 | |||

(Gain) Loss on mark-to-market activities |

22,852 | |||

Commodity derivatives settlements applied to future positions |

(3,197 | ) | ||

Gain on embedded derivatives |

(43,204 | ) | ||

| | | | | |

Adjusted EBITDA |

$ | 42,997 | ||

| | | | | |

| | | | | |

| | | | | |

Distributions for Third Quarter 2016

On October 31, 2016, the board of directors of our general partner declared a cash distribution of $0.4246 per common unit ($1.6984 per common unit on an annualized basis) for the third quarter of 2016. The board of directors of our general partner also declared a third quarter 2016 cash distribution of $0.45 per unit on our Class B preferred units. The distributions will be paid on November 30, 2016 to unitholders of record on November 10, 2016.

Risk Factors

An investment in our common units involves risks associated with our business, our partnership structure and the tax characteristics of our common units. You should carefully consider the following risk factors, the risks described in "Risk Factors" beginning on page 14 of this prospectus, our other filings with the SEC and the other information in this prospectus and incorporated herein by reference before investing in our common units. Please also read "Cautionary Note Regarding Forward-Looking Statements."

- •

- The assumptions underlying the forecast of cash available for distribution, as set forth in "Cash Distribution Policy and Restrictions

on Distributions," are inherently uncertain and subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause actual results to differ

materially from those forecasted.

- •

- You may experience future dilution as a result of future equity offerings or conversion of our Class B preferred units.

- •

- Future sales of our common units in the public market could depress our unit price.

- •

- Our management team may spend the proceeds of this offering in ways with which you may not agree or in ways that may not yield a significant return, if any.

9

Principal Executive Office

We are a Delaware limited partnership. Our principal executive office is located at 1000 Main Street, Suite 3000, Houston, Texas 77002, and our telephone number is (713) 783-8000. Our website address is www.sanchezpp.com. We make our periodic reports and other information filed with or furnished to the U.S. Securities and Exchange Commission ("SEC") available free of charge through our website as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into, and does not constitute a part of, this prospectus.

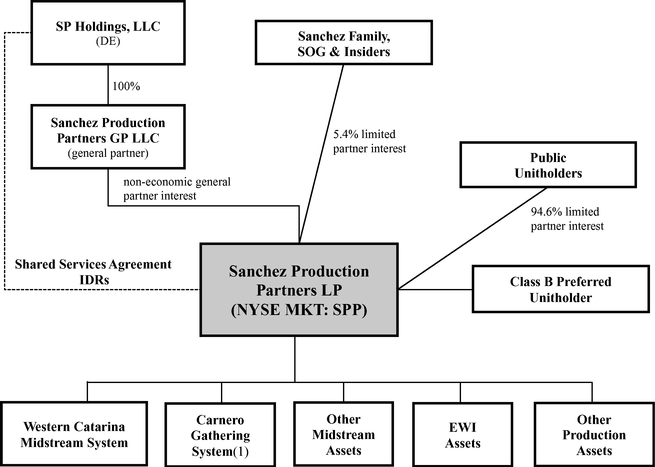

Organizational Structure

The following table depicts our ownership structure as of September 30, 2016, pro forma for the issuance of all of the common units offered pursuant to this prospectus, assuming the underwriters' option to purchase additional common units from us is not exercised.

Common Units: |

||||

Public |

94.6 | % | ||

Sanchez family, SOG and other insiders |

5.4 | % | ||

Class B Preferred Units: |

||||

Stonepeak Infrastructure Partners |

100 | % | ||

General Partner: |

||||

SP Holdings |

100 | % | ||

Incentive Distribution Rights: |

||||

SP Holdings |

100 | % |

- (1)

- Represents our 50% equity interest in Carnero Gathering.

10

Common units offered by us |

8,823,529 common units (or 10,147,059 common units if the underwriters exercise in full their option to purchase additional common units). | |

Common units to be outstanding immediately after this offering |

13,253,444 common units (or 14,576,974 common units if the underwriters exercise in full their option to purchase additional common units)(1). |

|

Underwriters' option |

We have granted the underwriters a 30-day option to purchase up to 1,323,530 additional common units on the same terms as the initial common units. |

|

Use of proceeds |

We expect to receive approximately $139.5 million in net proceeds from the sale of the common units we are offering hereby, or approximately $160.5 million in net proceeds if the underwriters exercise in full their option to purchase additional common units, in each case based on an assumed public offering price of $17.00 per common unit (the midpoint of the price range set forth on the cover page of this prospectus), after deducting the underwriting discounts and commissions, the structuring fee and estimated offering expenses payable by us. |

|

|

We intend to use the net proceeds received in connection with this offering as follows: (i) approximately $80 million to pay the purchase price for the 50% equity interest in Carnero Processing that we intend to acquire from Sanchez Energy and to cash collateralize a letter of credit to be issued to Carnero Processing in connection therewith, (ii) approximately $24.9 million to pay the purchase price for certain wellbores and EWIs and other production assets that we intend to acquire from Sanchez Energy in the Production Acquisition; and (iii) the remaining net proceeds to repay borrowings outstanding under our credit facility (including borrowings that may results from our letters of credit, if any). Affiliates of certain of the underwriters are lenders under our credit facility and accordingly, will receive a portion of the net proceeds of this offering. Please see "Use of Proceeds." |

|

Cash distributions |

We paid a quarterly cash distribution of $0.4183 per common unit ($1.6732 per unit on an annualized basis) and $0.45 per Class B preferred unit for the second quarter of 2016 on August 31, 2016 to unitholders of record as of August 22, 2016. The second quarter 2016 common unit distribution represented an approximate 1.5% increase from the first quarter 2016 distribution of $0.4121 per common unit. We will pay a quarterly cash distribution of $0.4246 per common unit ($1.6984 per common unit on an annualized basis) and $0.45 per Class B preferred unit for the third quarter of 2016 on November 30, 2016 to unitholders of record as of November 10, 2016. |

11

|

Our second amended and restated agreement of limited partnership (our "partnership agreement") requires us to distribute on or about the last day of each February, May, August and November, all of our available cash from operations, after the establishment of permitted cash reserves and the payment of fees and expenses, as follows: |

|

|

• first, 100% to all unitholders holding Class B preferred units, pro rata, until each receives an amount equal to the Class B Preferred Quarterly Distribution (as defined in our partnership agreement); |

|

|

• second, 100% to common unitholders, pro rata, until each receives an amount equal to $0.50 per common unit for that quarter; |

|

|

• third, 100% to common unitholders, pro rata, until each receives an amount equal to $0.575 per common unit for that quarter; |

|

|

• fourth, 87% to common unitholders, pro rata, and 13.0% to the holders of our incentive distribution rights, until each unitholder receives an amount equal to $0.625 per common unit for that quarter; |

|

|

• fifth, 77% to common unitholders, pro rata, and 23.0% to the holders of our incentive distribution rights, until each unitholder receives an amount equal to $0.875 per common unit for that quarter; and |

|

|

• thereafter, 64.5% to common unitholders, pro rata, and 35.5% to the holders of our incentive distribution rights. |

|

|

Distributions on our preferred units will be made prior to distributions of available cash and, as a result, will reduce the amount of available cash for distribution to our common unitholders. |

|

|

If we do not have sufficient available cash at the end of each quarter, we may, but are under no obligation to, borrow funds to pay distributions to our unitholders. We do not have a legal obligation to pay distributions at our minimum quarterly distribution rate or at any other rate. |

|

Issuance of additional units |

Our partnership agreement authorizes us to issue an unlimited number of additional units without the approval of our unitholders. Our unitholders will not have preemptive or participation rights to purchase their pro rata share of any additional units issued. Please read "The Partnership Agreement—Issuance of Additional Interests." |

12

Limited voting rights |

Our general partner manages and operates us. Unlike the holders of common stock in a corporation, our unitholders have only limited voting rights on matters affecting our business. Our unitholders have no right to elect our general partner or its directors on an annual or other continuing basis. Our general partner may not be removed except for cause by a vote of the holders of at least 662/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Please read "The Partnership Agreement—Voting Rights." |

|

Limited call right |

If at any time our general partner and its affiliates own more than 80% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price equal to the greater of (1) the average of the daily closing price of the common units over the 20 trading days preceding the date three days before notice of exercise of the call right is first mailed and (2) the highest per-unit price paid by our general partner or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. Please read "The Partnership Agreement—Limited Call Right." |

|

Material federal income tax consequences |

For a discussion of the material federal income tax consequences that may be relevant to prospective unitholders who are individual citizens or residents of the United States, please read "Material Tax Considerations." |

|

Risk factors |

Please read "Risk Factors" beginning on page 14 of this prospectus, our other filings with the SEC and in the other documents incorporated by reference into this prospectus for a discussion of risks that you should consider before investing in our common units. |

|

NYSE MKT symbol |

SPP |

- (1)

- The number of common units to be outstanding after this offering is based on 4,429,915 common units outstanding as of November 3, 2016 and excludes an aggregate of 235,832 additional common units reserved for future issuance under our equity incentive plan.

13

Limited partner interests, such as our common units, are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. Investing in our common units involves a high degree of risk. Before investing in our common units, you should carefully consider the risk factors included in our Annual Report on Form 10-K for the year ended December 31, 2015, our Quarterly Reports on Form 10-Q for the quarters ended March 31, 2016, June 30, 2016 and September 30, 2016 and our Current Reports on Form 8-K, each of which are incorporated by reference into this prospectus, as well as the risks described below and in "Cautionary Note Regarding Forward-Looking Statements" included in this prospectus, together with all of the other information included or incorporated by reference in this prospectus. If any of these risks were to occur, our business, financial condition and results of operations could be materially adversely affected. In that case, the value of our common units could decline and you could lose some or all of your investment.

Risks Related to this Offering

The assumptions underlying our forecast of cash available for distribution, as set forth in "Cash Distribution Policy and Restrictions on Distributions," are inherently uncertain and subject to significant business, economic, financial, regulatory and competitive risks and uncertainties that could cause actual results to differ materially from those forecasted.

The forecast of cash available for distribution set forth in "Cash Distribution Policy and Restrictions on Distributions" includes our forecasted results of operations, Adjusted EBITDA and cash available for distribution for the fifteen months ending December 31, 2017. Our ability to pay the full minimum quarterly distribution in the forecast period is based on a number of assumptions that may not prove to be correct and that are discussed in "Cash Distribution Policy and Restrictions on Distributions." The forecast has been prepared by our management. Neither our independent registered public accounting firm nor any other independent accountants have examined, compiled or performed any procedures with respect to the forecast nor have they expressed any opinion or any other form of assurance on such information or its achievability, and they assume no responsibility for the forecast. The assumptions and estimates underlying the forecast are inherently uncertain and are substantially driven by our historical production activities and Sanchez Energy's anticipated drilling and completion schedule and, although we consider our assumptions as to Sanchez Energy's ability to maintain that schedule reasonable as of the date of this prospectus, those estimates and Sanchez Energy's ability to achieve anticipated drilling and production targets are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the forecast. If we do not achieve the forecasted results, we may not be able to pay the full minimum quarterly distribution or any amount on our units, in which event the market price of our common units may decline materially. Please read "Cash Distribution Policy and Restrictions on Distributions."

The price at which you purchase our common units may not be a reliable indicator of the future market price.

We expect the public offering price to be between $16.00 and $18.00 per common unit. The last reported sales price of our common units on the NYSE MKT on November 3, 2016 was $14.05. We and the underwriters considered multiple factors in considering the proposed offering price range and such considerations may prove not to be accurate. As a result, the proposed offering price range may not be a reliable indicator of what the market price for our common units may be in the future, and the market price may be less than the public offering price. Please read "Price Range of Our Common Units."

14

You may experience future dilution as a result of future equity offerings.

In order to raise additional capital, we may in the future offer additional common units or other securities convertible into or exchangeable for our common units at prices that may not be the same as the price per unit in this offering, including through our "at-the-market" equity offering program. Based on the $14.05 per common unit closing price of our common units on November 3, 2016, common units having an aggregate value of approximately $100 million remain available for sale under this program. We may sell common units or other securities in any other offering at a price per unit that is different from the price per unit paid by investors in this offering, and investors purchasing common units or other securities in the future could have rights superior to existing unitholders. The price per unit at which we sell additional common units, or securities convertible into or exchangeable for common units, in future transactions may be higher or lower than the price per unit paid by investors in this offering. As of November 3, 2016, 235,832 common units were reserved for future issuance under our equity incentive plan. You will incur additional dilution upon the issuance of additional common units under our "at-the-market" equity offering program, or the grant of any common units under our equity incentive plan.

In addition, as part of our growth strategy, we may in the future consummate acquisitions in which a portion of the purchase price consideration consists of our common units. Any future issuances of common units, or other securities that may be convertible into or exchangeable for common units, in connection with acquisitions would dilute the percentage ownership held by the investors who purchase our common units pursuant to this offering.

Following the conversion of the Class B preferred units, you may experience dilution of your common units and we may not have sufficient available cash to enable us to maintain or increase the quarterly distribution amount on our common units.

As of the date of this prospectus, there were 19,444,445 Class B preferred units issued and outstanding which are convertible into not less than 19,444,445 common units (plus additional common units resulting from the issuance of paid-in-kind distributions, if any, on such preferred units). As of November 3, 2016, the Class B preferred units were convertible into 21,943,574 common units. Each of the holders of Class B preferred units (including a Class B Preferred PIK Unit) has the right, at any time at the option of such holder, to convert any number of its Class B preferred units into an aggregate amount exceeding the minimum conversion amount of $17,500,000 (or all of the Class B preferred units held by such holder if such holder's Class B preferred units do not exceed the minimum conversion amount) at the Class B conversion rate. As of the close of market trading on November 3, 2016, the Class B conversion rate was $15.9475 and the trading price of our common units was $14.05. Please read "The Partnership Agreement—Conversion of Class B Preferred Units." Any future conversion of the Class B preferred units would dilute the percentage ownership held by the investors who purchase our common units pursuant to this offering. Additionally, any future conversion of Class B preferred units will result in the payment of distributions on any additional common units issued as a result of such conversion, and we may not have sufficient available cash to maintain or increase the quarterly distribution amount on our common units following the payment of such distributions.

Future sales of our common units in the public market could depress our unit price.

Sales of a substantial number of our common units in the public market, or the perception that these sales might occur, could depress the market price of our common units and could impair our ability to raise capital through the sale of additional equity securities. As of November 3, 2016, we had 4,429,915 common units outstanding, all of which common units, other than those common units held by the directors and officers of our general partner, were eligible for sale in the public market, subject in some cases to compliance with the requirements of Rule 144, including the volume limitations and

15

manner of sale requirements. In addition, common units issuable upon conversion of our Class B preferred units and common units reserved for future issuance under our equity incentive plan will become eligible for sale in the public market to the extent permitted by applicable vesting requirements and subject in some cases to compliance with the requirements of Rule 144. We cannot predict the effect that future sales of our common units would have on the market price of our common units.

Our management team may invest or spend the proceeds of this offering in ways with which you may not agree or in ways that may not yield a significant return, if any.

We intend to use a portion of the net proceeds from this offering to repay borrowings outstanding under our credit facility (including borrowings that may result from our letters of credit, if any). Our management will have considerable discretion in the application of our cash and available borrowing base capacity under our credit facility and you will not have the opportunity, as part of your investment decision, to assess whether such proceeds are being used appropriately. The net proceeds may be used for purposes that do not increase our operating results or market value. Until the net proceeds are used, they may be placed in investments that do not produce significant income or investments that lose value.

Our participation in joint ventures exposes us to liability or harm to our reputation for failures of our partner.

In July 2016, we purchased from Sanchez Energy a 50% equity interest in Carnero Gathering, a joint venture that is 50% owned by Targa, for an initial payment of approximately $37.0 million and the assumption by us of remaining capital commitments to Carnero Gathering, estimated at approximately $7.4 million as of the acquisition date. In addition, we are required to pay Sanchez Energy an earnout based on natural gas received above a threshold volume and tariff at Carnero Gathering's delivery points from Sanchez Energy and other producers. In October 2016, we entered into a purchase and sale agreement with Sanchez Energy to acquire a 50% equity interest in Carnero Processing, a joint venture that is 50% owned by Targa, for an initial payment of approximately $47.7 million in cash and the assumption by us of remaining capital commitments to Carnero Processing, estimated at approximately $32.3 million as of October 6, 2016. We may enter into additional joint venture arrangements in the future. Success with Carnero Gathering, Carnero Processing and any future joint ventures depends in large part on whether our joint venture partner satisfies its contractual obligations.

We and our joint venture partner, TPL SouthTex Processing Company LP ("TPL"), an affiliate of Targa, are jointly and severally liable for all liabilities and obligations of Carnero Gathering and, if consummated, will be jointly and severally liable for all liabilities and obligations of Carnero Processing. If TPL fails to perform or is financially unable to bear its portion of required capital contributions or other obligations, including liabilities stemming from claims or lawsuits, we could be required to make additional investments, provide additional services or pay more than our proportionate share of a liability to make up for TPL's shortfall. Further, if we are unable to adequately address TPL's performance issues, Sanchez Energy, the main customer on the systems, may terminate the projects, which could result in legal liability to us, harm our reputation and reduce cash flows from the Carnero Gathering System and the Raptor Plant.

Even if this offering is completed, the pending acquisitions may not be consummated.

The pending acquisitions for Carnero Processing and the production assets are expected to close shortly following the closing of this offering, but are subject to customary and other closing conditions. There can be no assurances that these conditions will be satisfied or that these pending acquisitions will be consummated. The closing of this offering is not conditioned on the consummation of these pending acquisitions. If these pending acquisitions are delayed, not consummated or consummated in a manner different than described herein, (i) we may not realize the anticipated benefits of these pending acquisitions, (ii) our future business, operations and Cash Available for Distribution could be adversely

16

impacted from what we anticipate and (iii) our common unit price could be negatively impacted. In addition, if these pending acquisitions are not consummated, our management will have broad discretion in the application of the net proceeds of this offering.

Risks Related to the Partnership

We are a "smaller reporting company" and the reduced disclosure requirements applicable to smaller reporting companies may make our common units less attractive to investors.

We are considered a "smaller reporting company" (a company that has a public float of less than $75 million). We are therefore entitled to rely on certain reduced disclosure requirements, such as an exemption from providing selected financial data and executive compensation information. We are also exempt from the requirement to obtain an external audit on the effectiveness of internal control over financial reporting provided in Section 404(b) of the Sarbanes-Oxley Act. We have utilized this exemption for each year since the year ended December 31, 2011. These exemptions and reduced disclosures in our SEC filings due to our status as a smaller reporting company mean our auditors do not review our internal control over financial reporting and may make it harder for investors to analyze our results of operations and financial prospects. We cannot predict if investors will find our common units less attractive because we may rely on these exemptions. If some investors find our common units less attractive as a result, there may be a less active trading market for our common units and our unit prices may be more volatile.

17

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 that are subject to a number of risks and uncertainties, many of which are beyond our control. These statements may include discussions about our business strategy; acquisition strategy; financing strategy; ability to make, maintain and grow distributions; the ability of our customers to meet their drilling and development plans on a timely basis or at all and perform under gathering and processing agreements; future operating results; future capital expenditures; and plans, objectives, expectations, forecasts, outlook and intentions. All of these types of statements, other than statements of historical fact included in this prospectus, are forward-looking statements. In some cases, forward-looking statements can be identified by terminology such as "may," "could," "should," "expect," "plan," "project," "intend," "anticipate," "believe," "estimate," "predict," "potential," "pursue," "target," "continue," the negative of such terms or other comparable terminology.

The forward-looking statements contained in this prospectus are largely based on our expectations, which reflect estimates and assumptions made by our management. These estimates and assumptions reflect our best judgment based on currently known market conditions and other factors. Although we believe such estimates and assumptions to be reasonable, they are inherently uncertain and involve a number of risks and uncertainties that are beyond our control. In addition, management's assumptions about future events may prove to be inaccurate.

Important factors that could cause our actual results to differ materially from the expectations reflected in the forward-looking statements include, among others:

- •

- our ability to successfully execute our business, acquisition and financing strategies;

- •

- our ability to utilize the services, personnel and other assets of SP Holdings pursuant to existing services agreements;

- •

- our ability to make, maintain and grow distributions;

- •

- the timing and extent of changes in prices for, and demand for, crude oil and condensate, NGLs, natural gas and related commodities;

- •

- the realized benefits of our transactions with Sanchez Energy, including previous production asset acquisitions and the pending

Production Acquisition, the Western Catarina Midstream System acquisition and the acquisition of a 50% interest in Carnero Gathering and Carnero Processing;

- •

- the accuracy of reserve estimates, which by their nature involve the exercise of professional judgment and may, therefore, be

imprecise;

- •

- the ability of our customers to meet their drilling and development plans on a timely basis or at all and perform under gathering and

processing agreements;

- •

- our ability to successfully execute our hedging strategy and the resulting realized prices therefrom;

- •

- the credit worthiness and performance of our counterparties, including financial institutions, operating partners and other parties;

- •

- competition in the oil and natural gas industry for employees and other personnel, equipment, materials and services and, related

thereto, the availability and cost of employees and other personnel, equipment, materials and services;

- •

- our ability to access the credit and capital markets to obtain financing on terms we deem acceptable, if at all, and to otherwise satisfy our capital expenditure requirements;

18

- •

- the availability, proximity and capacity of, and costs associated with, gathering, processing, compression and transportation

facilities;

- •

- our ability to compete with other companies in the oil and natural gas industry;

- •

- the impact of, and changes in, government policies, laws and regulations, including tax laws and regulations, environmental laws and

regulations relating to air emissions, waste disposal, hydraulic fracturing and access to and use of water, laws and regulations imposing conditions and restrictions on drilling and completion

operations and laws and regulations with respect to derivatives and hedging activities;

- •

- the extent to which our crude oil and natural gas properties operated by others are operated successfully and economically;

- •

- the use of competing energy sources and the development of alternative energy sources;

- •

- unexpected results of litigation filed against us;

- •

- the extent to which we incur uninsured losses and liabilities or losses and liabilities in excess of our insurance coverage; and

- •

- the other factors described under "Risk Factors" and elsewhere in this prospectus and in the other documents incorporated herein by reference.

Management cautions all readers that the forward-looking statements contained in this prospectus are not guarantees of future performance, and we cannot assure any reader that such statements will be realized or the forward-looking events and circumstances will occur. The forward-looking statements speak only as of the date made, and other than as required by law, we do not intend to publicly update or revise any forward-looking statements as a result of new information, future events or otherwise. These cautionary statements qualify all forward-looking statements attributable to us or persons acting on our behalf.

19

We expect to receive approximately $139.5 million in net proceeds from the sale of the 8,823,529 common units we are offering hereby, or approximately $160.5 million in net proceeds if the underwriters exercise in full their option to purchase additional common units, in each case based on an assumed public offering price of $17.00 per common unit (the midpoint of the price range set forth on the cover page of this prospectus), after deducting the underwriting discounts and commissions, the structuring fee and estimated offering expenses payable by us.

We intend to use the net proceeds received in connection with this offering as follows: (i) approximately $80 million to pay the purchase price for the 50% equity interest in Carnero Processing that we intend to acquire from Sanchez Energy and to cash collateralize a letter of credit to be issued to Carnero Processing in connection therewith, (ii) approximately $24.9 million to pay the purchase price for certain wellbores and EWIs and other production assets that we intend to acquire from Sanchez Energy in the Production Acquisition; and (iii) the remaining net proceeds to repay borrowings outstanding under our credit facility (including borrowings that may results from our letters of credit, if any). Affiliates of certain of the underwriters are lenders under our credit facility and accordingly, will receive a portion of the net proceeds of this offering.

At our election, interest for borrowings under the credit facility are determined by reference to (i) the London interbank rate ("LIBOR") plus an applicable margin between 2.25% and 3.25% per annum based on utilization or (ii) a domestic bank rate ("ABR") plus an applicable margin between 1.25% and 2.25% per annum based on utilization plus (iii) a commitment fee of 0.500% per annum based on the unutilized borrowing base. Interest on the borrowings for ABR loans and the commitment fee are generally payable quarterly. As of November 3, 2016, we had $146 million of outstanding indebtedness under our credit facility, which matures March 31, 2020, at an interest rate of 3.0% plus LIBOR. The outstanding indebtedness under our credit facility was incurred to partially fund the cash consideration in the Western Catarina Midstream System and Carnero Gathering System acquisitions.

An increase or decrease in the initial public offering price of $1.00 per common unit would cause the net proceeds from this offering, after deducting underwriting discounts, structuring fees and estimated offering expenses, to increase or decrease by approximately $8.2 million, based on an assumed initial public offering price of $17.00 per common unit (the midpoint of the price range set forth on the cover of this prospectus).

20

The following table sets forth our capitalization as of September 30, 2016 on:

- •

- an actual basis; and

- •

- an as adjusted basis to reflect the issuance and sale of common units in this offering, assuming a public offering price of $17.00 per common unit (the midpoint of the price range set forth on the cover page of this prospectus), that the underwriters do not exercise their option to purchase additional common units, and the application of the net proceeds as set forth under "Use of Proceeds."