Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - New Senior Investment Group Inc. | snr-2016930exhibit322.htm |

| EX-32.1 - EXHIBIT 32.1 - New Senior Investment Group Inc. | snr-2016930exhibit321.htm |

| EX-31.2 - EXHIBIT 31.2 - New Senior Investment Group Inc. | snr-2016930exhibit312.htm |

| EX-31.1 - EXHIBIT 31.1 - New Senior Investment Group Inc. | snr-2016930exhibit311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2016

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Commission File Number: 001-36499

New Senior Investment Group Inc. |

(Exact name of registrant as specified in its charter)

Delaware | 80-0912734 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1345 Avenue of the Americas, New York, NY | 10105 | |

(Address of principal executive offices) | (Zip Code) | |

(212) 479-3140 |

(Registrant's telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report) |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

ý Yes No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the last practicable date.

Common stock, $0.01 par value per share: 82,127,247 shares outstanding as of October 27, 2016.

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

This report contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements relate to, among other things, the operating performance of New Senior Investment Group Inc.’s (“New Senior,” the “Company,” “we,” “us” or "our") investments, the stability of our earnings, and our financing needs. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “endeavor,” “seek,” “anticipate,” “estimate,” “overestimate,” “underestimate,” “believe,” “could,” “project,” “predict,” “continue” or other similar words or expressions. Forward-looking statements are based on certain assumptions, discuss future expectations, describe future plans and strategies, contain projections of results of operations or of financial condition or state other forward-looking information. Our ability to predict results or the actual outcome of future plans or strategies is inherently uncertain. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements. These forward-looking statements involve risks, uncertainties and other factors that may cause our actual results in future periods to differ materially from forecasted results. Factors which could have a material adverse effect on our operations and future prospects include, but are not limited to:

• | our ability to successfully operate as a standalone public company; |

• | our ability to comply with the terms of our financings, any increase in our borrowing costs as a result of changes in interest rates or other factors, and our ability to pay down, refinance, restructure or extend our indebtedness as it becomes due or as needed to comply with the terms of our covenants or facilitate our ability to sell assets; |

• | our ability to manage our liquidity and sustain distributions to our shareholders at the current level; |

• | factors affecting the performance of our properties, such as increases in costs (including, but not limited to, the costs of labor, supplies, insurance and property taxes), the performance of our operators, and competition for residents as a result of new construction or other factors; |

• | our dependence on our property managers and tenants to operate our properties effectively and in compliance with applicable law and the terms of our financings; |

• | concentration risk with respect to Holiday Retirement ("Holiday"), which, as of September 30, 2016, managed 67 of the 96 properties in our managed portfolio and leased 51 of the 58 properties in our triple net lease portfolio, and risks associated with a change of control in the ownership or senior management of Holiday; |

• | the ability of our property managers and tenants to effectively conduct their operations, maintain and improve our properties, to deliver high-quality services, to attract and retain qualified personnel and to attract residents; |

• | our ability and the ability of our property managers and tenants to obtain and maintain adequate property, liability and other insurance from reputable, financially stable providers; |

• | changes of federal, state and local laws and regulations relating to fraud and abuse practices, Medicaid reimbursement and licensure, etc., including those affecting the healthcare industry that affect our costs of compliance or increase the costs, or otherwise affect the operations or our property managers or tenants; |

• | the ability of our property managers, tenants and their respective guarantors to maintain the financial strength and liquidity necessary to satisfy their respective obligations and liabilities to us and third parties; |

• | the ability and willingness of our tenants to make the rent and other payments due to us under our leases, and the possibility that our tenants will seek to renegotiate the terms of such leases; |

• | our ability to reposition our leased properties on the same or better terms as we compete for tenants upon the expiration or earlier termination of our leases or with respect to additional properties that we may seek to lease in the future; |

• | the quality and size of our investment pipeline, our ability to execute investments at attractive risk-adjusted prices, our ability to finance our investments on favorable terms, and our ability to deploy investable cash in a timely manner; |

• | our ability to sell properties on favorable terms and to realize the anticipated benefits from any such dispositions; |

• | changes in economic conditions generally and the real estate, senior housing and bond markets specifically; |

• | our stock price performance and any disruption or lack of access to the capital markets or other sources of financing; |

• | the impact of any current or future legal proceedings and regulatory investigations and inquiries on us, FIG LLC (our “Manager”) or our operators; |

• | potential conflicts of interest relating to our external management structure or other factors, and our ability to effectively manage and resolve actual, potential or perceived conflicts of interest; |

• | our ability to maintain effective internal control over financial reporting and our reliance on our operators for timely delivery of accurate property-level financial results; |

• | our ability to maintain our qualification as a Real Estate Investment Trust ("REIT") for U.S. federal income tax purposes and the potentially onerous consequences that any failure to maintain such qualification would have on our business; and |

• | our ability to maintain our exemption from registration under the Investment Company Act of 1940, as amended (the “1940 Act”) and the fact that maintaining such exemption imposes limits on our business strategy. |

Although we believe that the expectations reflected in any forward-looking statements contained herein are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. The factors noted above could cause our actual results to differ significantly from those contained in any forward-looking statement.

Readers are cautioned not to place undue reliance on any of these forward-looking statements, which reflect our management’s views only as of the date of this report. We are under no duty to update any of the forward-looking statements after the date of this report to conform these statements to actual results.

SPECIAL NOTE REGARDING EXHIBITS

In reviewing the agreements included as exhibits to this Quarterly Report on Form 10-Q, please remember they are included to provide you with information regarding their terms and are not intended to provide any other factual or disclosure information about the Company or the other parties to the agreements. The agreements contain representations and warranties by each of the parties to the applicable agreement. These representations and warranties have been made solely for the benefit of the other parties to the applicable agreement and:

• | should not in all instances be treated as categorical statements of fact, but rather as a way of allocating the risk to one of the parties if those statements prove to be inaccurate; |

• | have been qualified by disclosures that were made to the other party in connection with the negotiation of the applicable agreement, which disclosures are not necessarily reflected in the agreement; |

• | may apply standards of materiality in a way that is different from what may be viewed as material to you or other investors; and |

• | were made only as of the date of the applicable agreement or such other date or dates as may be specified in the agreement and are subject to more recent developments. |

Accordingly, these representations and warranties may not describe the actual state of affairs as of the date they were made or at any other time. Additional information about the Company may be found elsewhere in this Quarterly Report on Form 10-Q and the Company’s other public filings, which are available without charge through the Securities and Exchange Commission's ("SEC") website at http://www.sec.gov.

The Company acknowledges that, notwithstanding the inclusion of the foregoing cautionary statements, it is responsible for considering whether additional specific disclosures of material information regarding contractual provisions are required to make the statements in this report not misleading.

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

FORM 10-Q

INDEX

PAGE | ||

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

(dollars in thousands, except share data)

September 30, 2016 | December 31, 2015 | ||||||

Assets | (Unaudited) | ||||||

Real estate investments: | |||||||

Land | $ | 222,138 | $ | 222,795 | |||

Buildings, improvements and other | 2,557,895 | 2,568,133 | |||||

Accumulated depreciation | (197,510 | ) | (129,788 | ) | |||

Net real estate property | 2,582,523 | 2,661,140 | |||||

Acquired lease and other intangible assets | 321,634 | 308,917 | |||||

Accumulated amortization | (242,671 | ) | (166,714 | ) | |||

Net real estate intangibles | 78,963 | 142,203 | |||||

Net real estate investments | 2,661,486 | 2,803,343 | |||||

Cash and cash equivalents | 73,395 | 116,881 | |||||

Straight-line rent receivables | 68,379 | 51,916 | |||||

Receivables and other assets, net | 63,697 | 45,319 | |||||

Total Assets | $ | 2,866,957 | $ | 3,017,459 | |||

Liabilities and Equity | |||||||

Liabilities | |||||||

Mortgage notes payable, net | $ | 2,146,292 | $ | 2,151,317 | |||

Due to affiliates | 10,786 | 9,644 | |||||

Accrued expenses and other liabilities | 106,800 | 89,173 | |||||

Total Liabilities | $ | 2,263,878 | $ | 2,250,134 | |||

Commitments and contingencies | |||||||

Equity | |||||||

Preferred Stock $0.01 par value, 100,000,000 shares authorized and none outstanding as of both September 30, 2016 and December 31, 2015 | $ | — | $ | — | |||

Common stock $0.01 par value, 2,000,000,000 shares authorized, 82,127,247 and 85,447,551 shares issued and outstanding as of September 30, 2016 and December 31, 2015, respectively | 821 | 854 | |||||

Additional paid-in capital | 897,947 | 928,654 | |||||

Accumulated deficit | (295,689 | ) | (162,183 | ) | |||

Total Equity | $ | 603,079 | $ | 767,325 | |||

Total Liabilities and Equity | $ | 2,866,957 | $ | 3,017,459 | |||

See notes to Consolidated Financial Statements.

1

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(dollars in thousands, except share data)

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Revenues | |||||||||||||||

Resident fees and services | $ | 90,217 | $ | 76,726 | $ | 270,220 | $ | 187,384 | |||||||

Rental revenue | 28,240 | 28,259 | 84,723 | 82,661 | |||||||||||

Total revenues | 118,457 | 104,985 | 354,943 | 270,045 | |||||||||||

Expenses | |||||||||||||||

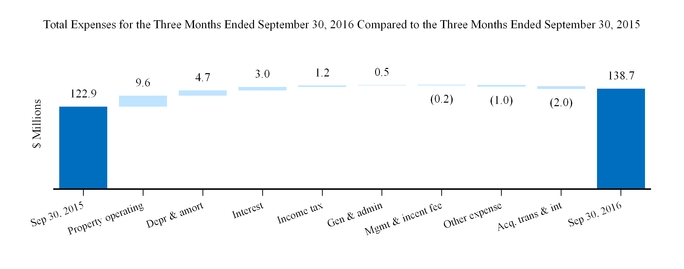

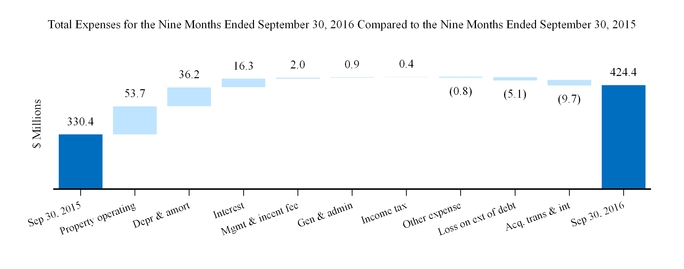

Property operating expense | 61,354 | 51,760 | 182,585 | 128,855 | |||||||||||

Depreciation and amortization | 45,510 | 40,812 | 146,743 | 110,543 | |||||||||||

Interest expense | 23,065 | 20,051 | 68,658 | 52,346 | |||||||||||

Acquisition, transaction and integration expense | 364 | 2,373 | 1,770 | 11,490 | |||||||||||

Management fees and incentive compensation to affiliate | 3,839 | 4,085 | 12,197 | 10,207 | |||||||||||

General and administrative expense | 3,676 | 3,152 | 11,600 | 10,691 | |||||||||||

Loss on extinguishment of debt | — | — | — | 5,091 | |||||||||||

Other expense | 108 | 1,089 | 806 | 1,569 | |||||||||||

Total expenses | $ | 137,916 | $ | 123,322 | $ | 424,359 | $ | 330,792 | |||||||

Loss Before Income Taxes | (19,459 | ) | (18,337 | ) | (69,416 | ) | (60,747 | ) | |||||||

Income tax expense (benefit) | 782 | (378 | ) | 31 | (344 | ) | |||||||||

Net Loss | $ | (20,241 | ) | $ | (17,959 | ) | $ | (69,447 | ) | $ | (60,403 | ) | |||

Loss Per Share of Common Stock | |||||||||||||||

Basic and diluted (A) | $ | (0.25 | ) | $ | (0.21 | ) | $ | (0.84 | ) | $ | (0.82 | ) | |||

Weighted Average Number of Shares of Common Stock Outstanding | |||||||||||||||

Basic and diluted (B) | 82,126,397 | 86,533,384 | 82,434,609 | 73,342,453 | |||||||||||

Dividends Declared Per Share of Common Stock | $ | 0.26 | $ | — | $ | 0.78 | $ | 0.49 | |||||||

(A) | Basic earnings per share ("EPS") is calculated by dividing net income by the weighted average number of shares of common stock outstanding. Diluted EPS is computed by dividing net income by the weighted average number of shares of common stock outstanding plus the additional dilutive effect, if any, of common stock equivalents during each period. |

(B) | All outstanding options were excluded from the diluted share calculation as their effect would have been anti-dilutive. |

See notes to Consolidated Financial Statements.

2

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY (Unaudited)

(dollars in thousands, except share data)

Common Stock | |||||||||||||||||||

Shares | Amount | Accumulated Deficit | Additional Paid-in Capital | Total Equity | |||||||||||||||

Equity at December 31, 2015 | 85,447,551 | $ | 854 | $ | (162,183 | ) | $ | 928,654 | $ | 767,325 | |||||||||

Repurchase of common stock | (3,333,333 | ) | (33 | ) | — | (30,851 | ) | (30,884 | ) | ||||||||||

Fair value of stock options issued | — | — | — | 5 | 5 | ||||||||||||||

Director's shares issued | 13,029 | — | — | 139 | 139 | ||||||||||||||

Dividends declared | — | — | (64,059 | ) | — | (64,059 | ) | ||||||||||||

Net loss | — | — | (69,447 | ) | — | (69,447 | ) | ||||||||||||

Equity at September 30, 2016 | 82,127,247 | $ | 821 | $ | (295,689 | ) | $ | 897,947 | $ | 603,079 | |||||||||

See notes to Consolidated Financial Statements.

3

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(dollars in thousands)

Nine Months Ended September 30, | |||||||

2016 | 2015 | ||||||

Cash Flows From Operating Activities | |||||||

Net loss | $ | (69,447 | ) | $ | (60,403 | ) | |

Adjustments to reconcile net loss to net cash provided by operating activities: | |||||||

Depreciation of tangible assets and amortization of intangible assets | 146,852 | 110,651 | |||||

Amortization of deferred financing costs | 7,216 | 6,777 | |||||

Amortization of deferred community fees | (1,384 | ) | (1,886 | ) | |||

Amortization of premium on mortgage notes payable | (447 | ) | 228 | ||||

Non-cash straight line rent | (16,463 | ) | (18,885 | ) | |||

Loss on extinguishment of debt | — | 5,091 | |||||

Equity-based compensation | 144 | 17 | |||||

Provision for bad debt | 1,552 | 1,449 | |||||

Other non-cash expense | 665 | 837 | |||||

Changes in: | |||||||

Receivables and other assets, net | (8,647 | ) | (13,148 | ) | |||

Due to affiliates | 1,142 | 4,547 | |||||

Accrued expenses and other liabilities | 18,503 | 18,641 | |||||

Net cash provided by operating activities | $ | 79,686 | $ | 53,916 | |||

Cash Flows From Investing Activities | |||||||

Cash paid for acquisitions, net of deposits | $ | — | $ | (1,212,169 | ) | ||

Capital expenditures | (15,753 | ) | (7,788 | ) | |||

Funds reserved for future capital expenditures | (1,266 | ) | (2,003 | ) | |||

Deposits refunded (paid) for real estate investments | 584 | (11,355 | ) | ||||

Net cash used in investing activities | $ | (16,435 | ) | $ | (1,233,315 | ) | |

Cash Flows From Financing Activities | |||||||

Proceeds from mortgage notes payable | $ | — | $ | 1,222,252 | |||

Principal payments of mortgage notes payable | (11,794 | ) | (11,683 | ) | |||

Repayments of mortgage notes payable | — | (304,484 | ) | ||||

Payment of exit fee on extinguishment of debt | — | (1,499 | ) | ||||

Payment of deferred financing costs | — | (12,294 | ) | ||||

Payment of common stock dividend | (64,059 | ) | (47,820 | ) | |||

Purchase of interest rate caps | — | (1,037 | ) | ||||

Repurchase of common stock | (30,884 | ) | — | ||||

Proceeds from issuance of common stock | — | 276,569 | |||||

Costs related to issuance of common stock | — | (10,056 | ) | ||||

Net cash (used in) provided by financing activities | $ | (106,737 | ) | $ | 1,109,948 | ||

Net Decrease in Cash and Cash Equivalents | (43,486 | ) | (69,451 | ) | |||

Cash and Cash Equivalents, Beginning of Period | 116,881 | 226,377 | |||||

Cash and Cash Equivalents, End of Period | $ | 73,395 | $ | 156,926 | |||

Supplemental Disclosure of Cash Flow Information | |||||||

Cash paid during the period for interest expense | $ | 61,932 | $ | 42,886 | |||

Cash paid during the period for income taxes | 266 | 190 | |||||

Supplemental Disclosure of Non-Cash Investing and Financing Activities | |||||||

Issuance of common stock | $ | 139 | $ | — | |||

Option exercise | — | 62 | |||||

Other liabilities assumed with acquisitions | — | 651 | |||||

See notes to Consolidated Financial Statements.

4

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

1. | ORGANIZATION |

New Senior is a REIT primarily focused on investing in private pay senior housing properties. As of September 30, 2016, New Senior owned a diversified portfolio of 154 primarily private pay senior housing properties located across 37 states. The Company is listed on the New York Stock Exchange (“NYSE”) under the symbol “SNR” and is headquartered in New York, New York.

The Company operates in two reportable segments: (1) Managed Properties and (2) Triple Net Lease Properties.

Managed Properties – The Company has engaged property managers to manage 96 of its properties on a day-to-day basis under the Managed Properties segment. These properties consist of 53 dedicated independent living facilities (“IL”) and 43 properties with a combination of assisted living/memory care (“AL/MC”) facilities. The Company’s Managed Properties are managed by Holiday Retirement (“Holiday”), a portfolio company that is majority owned by private equity funds managed by an affiliate of FIG LLC (the “Manager”), a subsidiary of Fortress Investment Group LLC (“Fortress”), FHC Property Management LLC (together with its subsidiaries, “Blue Harbor”), an affiliate of the Manager, Jerry Erwin Associates, Inc. (“JEA”) and Thrive Senior Living LLC ("Thrive"), collectively, the “Property Managers,” under property management agreements (the “Property Management Agreements”). Under the Property Management Agreements, the Property Managers are responsible for the day-to-day operations of the Company’s senior housing properties and are entitled to a management fee in accordance with the terms of the Property Management Agreements.

The Company's property management agreements have initial five-year or ten-year terms, with successive, automatic one-year renewal periods. The Company pays property management fees of 5% to 7% of effective gross income pursuant to its property management agreements with Holiday and, in some cases, Holiday is eligible to earn an incentive fee based on operating performance. The Company pays property management fees of 3% to 7% of gross revenues and, for certain properties, a property management fee based on a percentage of net operating income, pursuant to its property management agreements with other managers.

Triple Net Lease Properties – The Company owns 58 properties subject to triple net lease arrangements (substantially all of which are leased to Holiday). These properties consist of 52 IL properties, 5 rental Continuing Care Retirement Communities ("CCRC") properties and 1 AL/MC property. In a triple net lease arrangement, the lessee agrees to operate and maintain the property at its own expense, including repairs, maintenance, capital expenditures, utilities, taxes, insurance and the payroll expense of property-level employees. The Company’s triple net lease agreements have initial terms of approximately 15 or 17 years and include renewal options and annual rent increases ranging from 2.5% to 4.5%.

2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

Basis of Presentation and Principles of Consolidation

The accompanying Consolidated Financial Statements are prepared in accordance with U.S. Generally Accepted Accounting Principles (“GAAP’’) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. The Consolidated Financial Statements include the accounts of New Senior and its consolidated subsidiaries. All significant intercompany transactions and balances have been eliminated. New Senior consolidates those entities in which it has control over significant operating, financial and investing decisions of the entity. As of September 30, 2016 and December 31, 2015, the Company did not have any investments in Variable Interest Entities (“VIEs”). VIEs are defined as entities in which equity investors do not have the characteristics of a controlling financial interest or do not have sufficient equity at risk for the entity to finance its activities without additional subordinated financial support from other parties. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. These Consolidated Financial Statements should be read in conjunction with the results of operations, financial position and cash flows in the Company's Consolidated Financial Statements on Form 10-K for the year ended December 31, 2015.

Certain prior period amounts have been reclassified to conform to the current period’s presentation.

5

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

Use of Estimates

Management is required to make estimates and assumptions when preparing financial statements in conformity with GAAP. These estimates and assumptions affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the accompanying Consolidated Financial Statements and the reported amounts of revenue and expenses during the reporting period. Actual results may differ from management’s estimates.

Revenue Recognition

Resident Fees and Services - Resident fees and services include monthly rental revenue, care income and ancillary income recognized from the Managed Properties segment. Resident fees and services are recognized monthly as services are provided. Most lease agreements with residents are cancelable by the resident with 30 days’ notice. Ancillary income primarily relates to non-refundable community fees. Non-refundable community fees are recognized on a straight-line basis over the average length of stay of residents, which management estimates to be approximately 24 months for AL/MC properties and approximately 33 months for IL properties.

Rental Revenue - Rental revenue from the Triple Net Lease Properties segment is recognized on a straight-line basis over the applicable term of the lease when collectability is reasonably assured. Recognizing rental revenue on a straight-line basis typically results in recognizing revenue in excess of cash amounts contractually due from the Company’s tenants during the first half of the lease term, creating a straight-line rent receivable.

Acquisition Accounting

The Company has determined that all of its acquisitions should be accounted for under the acquisition method. The accounting for acquisitions requires the identification and measurement of all acquired tangible and intangible assets and assumed liabilities at their respective fair values, as of the respective transaction dates. The determination of the fair value of net assets acquired involves significant judgment and estimates, such as the Company's estimates of future cash flows based on a number of factors including property operating results, known and anticipated trends, as well as market and economic conditions.

In measuring the fair value of tangible and identified intangible assets acquired and liabilities assumed, management uses information obtained as a result of pre-acquisition due diligence, marketing, leasing activities and independent appraisals. In the case of buildings, the fair value of the tangible assets acquired is determined by valuing the property as if it were vacant. Significant estimates impacting the measurement at fair value of the Company's real property include construction cost data and qualitative selection of comparable market transactions as well as the assessment of the relative quality and condition of the acquired properties.

Recognized intangible assets primarily include the fair value of in-place resident leases. The Company estimates the fair value of in-place leases as (i) the present value of the estimated rental revenue that would have been forgone, offset by variable costs that would have otherwise been incurred during a reasonable lease-up period, as if the acquired units were vacant and (ii) the estimated absorption costs, such as additional marketing costs that would have been incurred during the lease-up period. The acquisition fair value of the in-place lease intangibles is amortized over the average length of stay of the residents on a straight-line basis.

Contingent consideration, if any, is measured at fair value on the date of acquisition. The fair value of the contingent consideration is remeasured at each reporting date with any change recorded in "Other expense" in the Consolidated Statements of Operations.

Acquisition and transaction expense includes costs related to completed and potential acquisitions and transactions and include advisory, legal, accounting, valuation and other professional or consulting fees. Integration expense includes costs directly related to the integration of acquired businesses such as lender mandated repairs, licensing, rebranding and training incurred in connection with the acquisition. Acquisition, transaction and integration costs are expensed as incurred.

6

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

Recent Accounting Pronouncements

In May 2014, the FASB issued Accounting Standards Update ("ASU") 2014-09 Revenues from Contracts with Customers (Topic 606). The standard’s core principle is that a company will recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. In doing so, companies will need to use more judgment and make more estimates than under today’s guidance. These may include identifying performance obligations in the contract, estimating the amount of variable consideration to include in the transaction price and allocating the transaction price to each separate performance obligation. In August 2015, the FASB deferred the effective date of this standard by one year, which will be for fiscal years, and interim periods within those years, beginning after December 15, 2017. Additionally, during 2016, the FASB issued ASU 2016-08 Revenue from Contracts with Customers, Principal versus Agent Considerations, ASU 2016-10 Revenue from Contracts with Customers, Identifying Performance Obligations and Licensing and ASU 2016-12 Revenue from Contracts with Customers, Narrow-Scope Improvements and Practical Expedients, which clarify the guidance on reporting revenue as a principal versus agent, identifying performance obligations, accounting for intellectual property licenses, and how to assess collectibility, present sales tax and treat noncash consideration. The Company is assessing the impact this guidance may have on its Consolidated Financial Statements and has not yet determined the method by which it will adopt the standard.

In January 2016, the FASB issued ASU 2016-01 Financial Instruments - Overall: Recognition and Measurement of Financial Assets and Financial Liabilities. The standard addresses certain aspects of recognition, measurement, presentation and disclosure of financial instruments. The effective date of the standard will be for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017. The Company does not expect adoption of this ASU to have a material impact on its Consolidated Financial Statements.

In February 2016, the FASB issued ASU 2016-02 Leases. This standard amends the existing accounting standards for lease accounting, including requiring lessees to recognize most leases on their balance sheets and making targeted changes to lessor accounting. The effective date of the standard will be for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018, and early adoption is permitted. The new leases standard requires a modified retrospective transition approach for all leases existing at, or entered into after, the date of initial application, with an option to use certain transition relief. The Company is assessing the impact this guidance may have on its Consolidated Financial Statements.

In June 2016, the FASB issued ASU 2016-13 Financial Instruments - Credit Losses, Measurement of Credit Losses on Financial Instruments. This standard replaces the current incurred loss methodology with a methodology that reflects expected credit losses. Under this methodology, a company would recognize an impairment allowance equal to its current estimate of all contractual cash flows that it does not expect to collect from financial assets measured at amortized cost. The effective date of the standard will be for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019, and early adoption is permitted beginning after December 15, 2018. The Company is assessing the impact this guidance may have on its Consolidated Financial Statements.

In August 2016, the FASB issued ASU 2016-15 Statement of Cash Flows (Topic 230) - Classification of Certain Cash Receipts and Cash Payments. This standard addresses the presentation and classification of certain cash receipts and cash payments in the statement of cash flows. The effective date of the standard will be for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017, and early adoption is permitted. The Company does not expect adoption of this ASU to have a material impact on its Consolidated Financial Statements.

7

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

3. | ACQUISITIONS |

The Company did not make any acquisitions during the nine months ended September 30, 2016.

During the nine months ended September 30, 2015, the Company acquired five portfolios representing 52 properties (49 IL, 2 AL/MC and 1 rental CCRC). The IL and AL/MC properties were integrated into the Managed Properties segment, and Holiday, Blue Harbor and Thrive manage 47, 2 and 2 of the properties, respectively. The rental CCRC was integrated into the Triple Net Lease segment.

Acquisition accounting is preliminary, pending the completion of various analyses and the finalization of estimates used in the determination of fair values. During the measurement period, additional assets or liabilities may be recognized if new information is obtained about facts and circumstances that existed as of the acquisition date that, if known, would have resulted in the recognition of those assets or liabilities as of that date. The preliminary measurement of net assets acquired may be adjusted after obtaining additional information regarding, among other things, asset valuations (including market and other information with which to determine fair values), liabilities assumed and the analysis of assumed contracts. These adjustments may be significant and will be accounted for in accordance with ASU 2015-16 Business Combinations: Simplifying the Accounting for Measurement-Period Adjustments, which became effective in the first quarter of 2016.

During the nine months ended September 30, 2016, measurement period adjustments were made based on the final valuation of net assets acquired. The adjustments included a decrease of $14,591 in real estate investments and an increase of $14,591 for in-place lease intangibles. If these adjustments had been recognized as of the acquisition date, the Company would have recognized additional depreciation and amortization expense in previous reporting periods, of which $2,163 and $7,444 were recorded during the three and nine months ended September 30, 2016, respectively.

The following table illustrates the pro forma effect of the acquisitions completed in the period from January 1, 2015 to September 30, 2016 on revenues and loss before income taxes, as if they had been consummated as of January 1, 2015:

Three Months Ended September 30, 2015 | Nine Months Ended September 30, 2015 | ||||||

Revenues | $ | 115,870 | $ | 345,322 | |||

Loss before income taxes | (22,770 | ) | (85,535 | ) | |||

The pro forma results are not necessarily indicative of the operating results that would have been obtained had the acquisitions occurred as of January 1, 2015, nor are they necessarily indicative of future operating results.

4. | SEGMENT REPORTING |

As of September 30, 2016, the Company operated in two reportable business segments: Managed Properties and Triple Net Lease Properties. Under its Managed Properties segment, the Company invests in senior housing properties throughout the United States and engages property managers to manage those senior housing properties. Under its Triple Net Lease Properties segment, the Company invests in senior housing and healthcare properties throughout the United States and leases those properties to healthcare operating companies under triple net leases that obligate the tenants to pay all property-related expenses, including repairs, maintenance, capital expenditures, utilities, taxes, insurance and the payroll expense of property-level employees.

The Company evaluates the aggregate performance of the properties in each reportable business segment based on segment net operating income (“NOI”). The Company defines NOI as total revenues less property-level operating expenses, which include property management fees, payroll expense and travel cost reimbursements to affiliates. The Company believes that net income, as defined by GAAP, is the most appropriate earnings measurement. However, the Company believes that segment NOI serves as a useful supplement to net income because it allows investors, analysts and management to measure unlevered property-level operating results and to compare the Company’s operating results between periods and to the operating results of other real estate companies on a consistent basis. Segment NOI should not be considered as an alternative to net income as determined in accordance with GAAP.

8

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

Interest expense, depreciation and amortization, general and administrative expense, acquisition, transaction and integration expense, management fees and incentive compensation to affiliate, income tax expense (benefit), other expense and discontinued operations (if any) are not allocated to individual segments for purposes of assessing segment performance. There are no intersegment sales or transfers.

Three Months Ended September 30, 2016 | Three Months Ended September 30, 2015 | ||||||||||||||||||||||

Triple Net Lease Properties | Managed Properties | Consolidated | Triple Net Lease Properties | Managed Properties | Consolidated | ||||||||||||||||||

Revenues | |||||||||||||||||||||||

Resident fees and services | $ | — | $ | 90,217 | $ | 90,217 | $ | — | $ | 76,726 | $ | 76,726 | |||||||||||

Rental revenue | 28,240 | — | 28,240 | 28,259 | — | 28,259 | |||||||||||||||||

Less: Property operating expense | — | 61,354 | 61,354 | — | 51,760 | 51,760 | |||||||||||||||||

Segment NOI | $ | 28,240 | $ | 28,863 | $ | 57,103 | $ | 28,259 | $ | 24,966 | $ | 53,225 | |||||||||||

Depreciation and amortization | 45,510 | 40,812 | |||||||||||||||||||||

Interest expense | 23,065 | 20,051 | |||||||||||||||||||||

Acquisition, transaction and integration expense | 364 | 2,373 | |||||||||||||||||||||

Management fees and incentive compensation to affiliate | 3,839 | 4,085 | |||||||||||||||||||||

General and administrative expense | 3,676 | 3,152 | |||||||||||||||||||||

Other expense | 108 | 1,089 | |||||||||||||||||||||

Income tax expense (benefit) | 782 | (378 | ) | ||||||||||||||||||||

Net Loss | $ | (20,241 | ) | $ | (17,959 | ) | |||||||||||||||||

Nine Months Ended September 30, 2016 | Nine Months Ended September 30, 2015 | ||||||||||||||||||||||

Triple Net Lease Properties | Managed Properties | Consolidated | Triple Net Lease Properties | Managed Properties | Consolidated | ||||||||||||||||||

Revenues | |||||||||||||||||||||||

Resident fees and services | $ | — | $ | 270,220 | $ | 270,220 | $ | — | $ | 187,384 | $ | 187,384 | |||||||||||

Rental revenue | 84,723 | — | 84,723 | 82,661 | — | 82,661 | |||||||||||||||||

Less: Property operating expense | — | 182,585 | 182,585 | — | 128,855 | 128,855 | |||||||||||||||||

Segment NOI | $ | 84,723 | $ | 87,635 | $ | 172,358 | $ | 82,661 | $ | 58,529 | $ | 141,190 | |||||||||||

Depreciation and amortization | 146,743 | 110,543 | |||||||||||||||||||||

Interest expense | 68,658 | 52,346 | |||||||||||||||||||||

Acquisition, transaction and integration expense | 1,770 | 11,490 | |||||||||||||||||||||

Management fees and incentive compensation to affiliate | 12,197 | 10,207 | |||||||||||||||||||||

General and administrative expense | 11,600 | 10,691 | |||||||||||||||||||||

Loss on extinguishment of debt | — | 5,091 | |||||||||||||||||||||

Other expense | 806 | 1,569 | |||||||||||||||||||||

Income tax expense (benefit) | 31 | (344 | ) | ||||||||||||||||||||

Net Loss | $ | (69,447 | ) | $ | (60,403 | ) | |||||||||||||||||

Property operating expense includes property management fees, property-level payroll expense and travel reimbursement costs. See Note 11 for additional information on these expenses related to Blue Harbor and Holiday.

9

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

Assets by reportable business segment are reconciled to total assets as follows:

September 30, 2016 | December 31, 2015 | ||||||||||||

Assets: | Amount | Percentage | Amount | Percentage | |||||||||

Triple Net Lease Properties | $ | 1,159,840 | 40.5 | % | $ | 1,196,578 | 39.7 | % | |||||

Managed Properties | 1,676,099 | 58.5 | % | 1,744,540 | 57.8 | % | |||||||

All Other Assets (A) | 31,018 | 1.0 | % | 76,341 | 2.5 | % | |||||||

Total Assets | $ | 2,866,957 | 100.0 | % | $ | 3,017,459 | 100.0 | % | |||||

(A) | Primarily consists of corporate cash which is not directly attributable to the Company's reportable business segments. |

Rental revenue attributable to our triple net leases with Holiday accounted for 18.8% and 21.2% of the Company's total revenues for the three months ended September 30, 2016 and 2015 and 18.8% and 24.8% for the nine months ended September 30, 2016 and 2015, respectively.

The following table presents the percentage of total revenues by geographic location:

Nine Months Ended September 30, 2016 | Nine Months Ended September 30, 2015 | ||||||||||

Number of Communities | % of Revenue | Number of Communities | % of Revenue | ||||||||

Florida | 26 | 19.7 | % | 26 | 21.4 | % | |||||

Texas | 19 | 11.9 | % | 17 | 14.0 | % | |||||

California | 12 | 10.1 | % | 12 | 9.0 | % | |||||

North Carolina | 9 | 6.4 | % | 9 | 5.5 | % | |||||

Pennsylvania | 7 | 6.1 | % | 7 | 6.4 | % | |||||

Oregon | 10 | 5.3 | % | 10 | 5.6 | % | |||||

Utah | 6 | 4.4 | % | 6 | 5.5 | % | |||||

Other | 65 | 36.1 | % | 65 | 32.6 | % | |||||

Total | 154 | 100.0 | % | 152 | 100.0 | % | |||||

10

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

5. | REAL ESTATE INVESTMENTS |

September 30, 2016 | December 31, 2015 | ||||||||||||||||||||||

Gross Carrying Amount | Accumulated Depreciation | Net Carrying Value | Gross Carrying Amount | Accumulated Depreciation | Net Carrying Value | ||||||||||||||||||

Land | $ | 222,138 | $ | — | $ | 222,138 | $ | 222,795 | $ | — | $ | 222,795 | |||||||||||

Building and improvements | 2,437,056 | (147,465 | ) | 2,289,591 | 2,455,170 | (97,485 | ) | 2,357,685 | |||||||||||||||

Furniture, fixtures and equipment | 120,839 | (50,045 | ) | 70,794 | 112,963 | (32,303 | ) | 80,660 | |||||||||||||||

Total | $ | 2,780,033 | $ | (197,510 | ) | $ | 2,582,523 | $ | 2,790,928 | $ | (129,788 | ) | $ | 2,661,140 | |||||||||

Depreciation expense was $24,599 and $20,020 for the three months ended September 30, 2016 and 2015 and $69,019 and $50,578 for the nine months ended September 30, 2016 and 2015, respectively.

The following table summarizes the Company’s real estate intangibles:

September 30, 2016 | December 31, 2015 | ||||||||||||||||||||||||||

Gross Carrying Amount | Accumulated Amortization | Net Carrying Value | Weighted Average Amortization Period | Gross Carrying Amount | Accumulated Amortization | Net Carrying Value | Weighted Average Amortization Period | ||||||||||||||||||||

Above/below market lease intangibles, net | $ | 5,868 | $ | (507 | ) | $ | 5,361 | 53.5 years | $ | 5,868 | $ | (361 | ) | $ | 5,507 | 52.8 years | |||||||||||

In-place lease intangibles | 309,970 | (240,110 | ) | 69,860 | 2.6 years | 297,253 | (164,772 | ) | 132,481 | 2.6 years | |||||||||||||||||

Other intangibles | 5,796 | (2,054 | ) | 3,742 | 9.5 years | 5,796 | (1,581 | ) | 4,215 | 9.4 years | |||||||||||||||||

Total intangibles | $ | 321,634 | $ | (242,671 | ) | $ | 78,963 | $ | 308,917 | $ | (166,714 | ) | $ | 142,203 | |||||||||||||

Amortization expense was $20,911 and $20,792 for the three months ended September 30, 2016 and 2015 and $77,724 and $59,965 for the nine months ended September 30, 2016 and 2015, respectively. Additionally, amortization of above/below market leases was $38 and $36 for the three months ended September 30, 2016 and 2015 and $109 and $109 for the nine months ended September 30, 2016 and 2015, respectively, and is reported as a reduction to "Rental revenue" in the Consolidated Statements of Operations.

11

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

6. | RECEIVABLES AND OTHER ASSETS, NET |

September 30, 2016 | December 31, 2015 | ||||||

Escrows held by lenders (A) | $ | 29,790 | $ | 19,694 | |||

Other receivables | 3,284 | 2,996 | |||||

Prepaid expenses | 4,051 | 4,828 | |||||

Resident receivables, net | 2,770 | 2,594 | |||||

Deferred tax assets, net | 9,043 | 8,757 | |||||

Security deposits | 2,785 | 2,932 | |||||

Income tax receivable | 1,339 | 1,920 | |||||

Interest rate caps | 28 | 283 | |||||

Assets held for sale (B) | 9,357 | — | |||||

Other assets | 1,250 | 1,315 | |||||

Total | $ | 63,697 | $ | 45,319 | |||

(A) | Escrows held by lenders represent amounts deposited in tax, insurance, and replacement reserve escrow accounts that are related to mortgage notes collateralized by New Senior's properties. |

(B) | Represents two AL/MC properties in the Managed Properties segment classified as held for sale as of September 30, 2016. The balance primarily consists of the carrying value of buildings and land as of September 30, 2016. These properties were sold on October 31, 2016; see Note 15 for further information. |

The following table summarizes the allowance for doubtful accounts and the related provision for resident receivables:

Nine Months Ended September 30, | |||||||

2016 | 2015 | ||||||

Balance, beginning of period | $ | 509 | $ | 190 | |||

Provision for bad debt | 1,552 | 1,449 | |||||

Write-offs, net of recoveries | (1,028 | ) | (916 | ) | |||

Balance, end of period | $ | 1,033 | $ | 723 | |||

The provision for resident receivables and related write-offs are included in "Property operating expense" in the Consolidated Statements of Operations.

7. | DEFERRED FINANCING COSTS |

The deferred financing costs summarized in the following table are presented as a reduction to "Mortgage notes payable, net" in the Consolidated Balance Sheets.

September 30, 2016 | December 31, 2015 | ||||||

Gross carrying amount | $ | 54,910 | $ | 54,910 | |||

Accumulated amortization | (24,691 | ) | (17,475 | ) | |||

Total | $ | 30,219 | $ | 37,435 | |||

Amortization of deferred financing costs is reported within "Interest expense" in the Consolidated Statements of Operations.

12

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

8. | MORTGAGE NOTES PAYABLE, NET |

September 30, 2016 | December 31, 2015 | ||||||||||||||||||||

Outstanding Face Amount | Carrying Value (A) | Final Stated Maturity | Stated Interest Rate | Weighted Average Maturity (Years) | Outstanding Face Amount | Carrying Value (A) | |||||||||||||||

Managed Properties | |||||||||||||||||||||

Fixed Rate | $ | 605,442 | $ | 601,813 | Dec 2018 - Sep 2025 | 3.65% to 6.76% | 7.4 | $ | 607,437 | $ | 603,460 | ||||||||||

Floating Rate (B) | 731,064 | 724,174 | Oct 2020 - May 2022 | 1M LIBOR + 2.20% to 1M LIBOR + 2.70% | 5.2 | 731,318 | 723,554 | ||||||||||||||

Triple Net Lease Properties | |||||||||||||||||||||

Fixed Rate (C) | 686,439 | 669,210 | Jan 2021 - Jan 2024 | 3.80% to 7.40% | 5.5 | 695,984 | 673,732 | ||||||||||||||

Floating Rate | 152,000 | 151,095 | Oct 2017 - Apr 2018 | 3M LIBOR + 3.00% to 3M LIBOR + 3.25% | 1.2 | 152,000 | 150,571 | ||||||||||||||

Total | $ | 2,174,945 | $ | 2,146,292 | 5.6 | $ | 2,186,739 | $ | 2,151,317 | ||||||||||||

(A) | The totals are reported net of deferred financing costs of $30,219 and $37,435 as of September 30, 2016 and December 31, 2015, respectively. |

(B) | All of these loans have LIBOR caps that range between 3.30% and 3.80% as of September 30, 2016. |

(C) | Includes loans with an outstanding face amount of $345,467 and $293,531, as of September 30, 2016, for which the Company bought down the interest rates to 4.00% and 3.80%, respectively, through January 2019. The interest rates will increase to 4.99% and 4.55%, respectively, thereafter. |

In the first quarter of 2015, the Company refinanced mortgage loans of $297,030 and recognized a loss on extinguishment of debt of $5,091, which represents the write-off of related unamortized deferred financing costs, mortgage discounts, exit fees and other costs, as of the date of the refinancing, and is included in "Loss on extinguishment of debt" in the Consolidated Statements of Operations.

The carrying value of the collateral relating to the fixed rate and floating rate mortgages was $1,603,952 and $1,057,040 as of September 30, 2016 and $1,679,646 and $1,122,960 as of December 31, 2015, respectively.

The Company’s mortgage notes payable contain various customary financial and other covenants, and in certain cases include a Debt Service Coverage Ratio, Project Yield or Minimum Net Worth and Liquid Assets provision, as defined in the agreements. As of September 30, 2016, the Company was in compliance with all of such covenants except the Project Yield covenant in one financing secured by a leased portfolio, where the Company will be in compliance upon either exercising its cure rights or finalizing an amendment, as described in more detail below.

The Project Yield covenant referenced above measures the leased portfolio's trailing 12-month operating results relative to the outstanding unpaid principal balance of the debt. Under the terms of the debt, the Company is entitled to cure non-compliance with this covenant by paying down the debt to the extent necessary to achieve the required project yield threshold. With respect to the September 30, 2016 test date, a prepayment of approximately $1,300 would be required to achieve compliance. The prepayment is not yet due and, prior to the due date, the Company expects to finalize an amendment to the Project Yield covenant that would reduce the threshold beginning with the September 30, 2016 test date and continuing for the remaining term of the loan. The amendment would eliminate the need to exercise a cure with respect to the September 30, 2016 test date, provided that the tenant's security deposit and other amounts posted by the tenant pursuant to the lease are escrowed with the lender.

The fair values of mortgage notes payable as of September 30, 2016 and December 31, 2015 was $2,192,611 and $2,217,464, respectively. Mortgage notes payable are not measured at fair value in the Consolidated Balance Sheets. The disclosed fair value of mortgage notes payable, classified as level 3 within the fair value hierarchy, is based on a discounted cash flow valuation model. Significant inputs in the model include amounts and timing of expected future cash flows and market yields which are constructed based on inputs implied from similar debt offerings.

13

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

9. | DERIVATIVE INSTRUMENTS |

As of September 30, 2016, the Company held interest rate caps to hedge future payments on floating rate debt obligations. The interest rate caps are carried at fair value and are included in "Receivables and other assets, net" in the Consolidated Balance Sheets. The Company estimates the fair value of these instruments using pricing models that consider forward yield curves, cap strike rates, cap volatility and discount rates, which are classified as level 2 inputs. Significant inputs to the valuation of level 2 derivatives can be verified to market transactions, broker or dealer quotations or other pricing sources with reasonable levels of price transparency. The Company does not apply hedge accounting. The fair value adjustment on the Company's interest rate caps was a loss of $8 and $357 for the three months ended September 30, 2016 and 2015, respectively, and a loss of $255 and $837 for the nine months ended September 30, 2016 and 2015, respectively, and is included in "Other expense" in the Consolidated Statements of Operations.

The following table presents information related to the Company's outstanding interest rate caps:

September 30, 2016 | December 31, 2015 | ||||||

Outstanding notional amount | $ | 731,092 | $ | 731,318 | |||

LIBOR cap range | 3.30% to 3.80% | 3.30% to 3.80% | |||||

LIBOR cap effective date range | Mar 2015 to Sep 2020 | Mar 2015 to Sep 2020 | |||||

Fair value | $ | 28 | $ | 283 | |||

10. | ACCRUED EXPENSES AND OTHER LIABILITIES |

September 30, 2016 | December 31, 2015 | ||||||

Security deposits payable | $ | 56,741 | $ | 54,669 | |||

Accounts payable | 8,771 | 9,552 | |||||

Mortgage interest payable | 6,381 | 6,415 | |||||

Deferred community fees, net | 5,464 | 4,450 | |||||

Rent collected in advance | 3,210 | 3,937 | |||||

Property tax payable | 7,419 | 2,564 | |||||

Other liabilities (A) | 18,814 | 7,586 | |||||

Total | $ | 106,800 | $ | 89,173 | |||

(A) | Includes liabilities held for sale of $120 related to two AL/MC properties classified as held for sale as of September 30, 2016. These properties were sold on October 31, 2016; see Note 15 for further information. |

11. | TRANSACTIONS WITH AFFILIATES |

Management Agreements

New Senior is party to a management agreement (the “Management Agreement”) with the Manager, under which the Manager advises the Company on various aspects of its business and manages its day-to-day operations, subject to the supervision of the Company’s board of directors. For its management services, the Manager is entitled to a base management fee of 1.5% per annum of the Company’s gross equity. Gross equity is generally defined as the equity invested by Newcastle Investment Corp. ("Newcastle") (including cash contributed to the Company) as of the completion of the spin-off from Newcastle, plus the aggregate offering price from stock offerings, plus certain capital contributions to subsidiaries, less capital distributions (calculated without regard to depreciation and amortization) and repurchases of common stock, calculated and payable monthly in arrears in cash. The Company incurred management fees of $3,839 and $4,085 during the three months ended September 30, 2016 and 2015, respectively, and $11,562 and $10,207 during the nine months ended September 30, 2016 and 2015, respectively, under the Management Agreement, which are included in “Management fees and incentive compensation to affiliate” in the Consolidated Statements of Operations. As of September 30, 2016 and December 31, 2015, the Company had a payable for management fees of $1,280 and $1,349, respectively, which is included in “Due to affiliates” in the Consolidated Balance Sheets.

14

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

The Manager is entitled to receive, on a quarterly basis, incentive compensation on a cumulative, but not compounding basis, in an amount equal to the product of (A) 25% of the dollar amount by which (1)(a) funds from operations (as defined in the Management Agreement) before the incentive compensation per share of common stock, plus (b) gains (or losses) from sales of property per share of common stock, plus (c) internal and third party acquisition-related expenses, plus (d) unconsummated transaction expenses, and plus (e) other non-routine items (as defined in the Management Agreement), exceed (2) an amount equal to (a) the weighted average value per share of the equity invested by Newcastle in the assets of the Company (including cash contributed to the Company) as of the completion of the spin-off and the price per share of the Company’s common stock in any offerings by the Company (adjusted for prior capital dividends or capital distributions, which shall be calculated without regard to depreciation and amortization and repurchases of common stock) multiplied by (b) a simple interest rate of 10% per annum, multiplied by (B) the weighted average number of shares of common stock outstanding. The Manager did not earn incentive compensation during the three months ended September 30, 2016 and 2015, and earned $635 and $0 during the nine months ended September 30, 2016 and 2015, respectively, which is included in "Management fees and incentive compensation to affiliate" in the Consolidated Statements of Operations. The Manager is also entitled to receive, upon the successful completion of an equity offering, options with respect to 10% of the number of shares sold in the offering with an exercise price equal to the price paid by the purchaser in the offering.

Because the Manager’s employees perform certain legal, accounting, due diligence, asset management and other services that outside professionals or outside consultants otherwise would perform, the Manager is paid or reimbursed, pursuant to the Management Agreement, for the cost of performing such tasks, provided that such costs and reimbursements are no greater than those which would be paid to outside professionals or consultants on an arm’s-length basis. The Company is also required to pay all operating expenses, except those specifically required to be borne by the Manager under the Management Agreement. The Company is required to pay expenses that include, but are not limited to, issuance and transaction costs incidental to the sourcing, evaluation, acquisition, management, disposition, and financing of the Company’s investments, legal, underwriting, sourcing, asset management and accounting and auditing fees and expenses, the compensation and expenses of independent directors, the costs associated with the establishment and maintenance of any credit facilities and other indebtedness of the Company (including commitment fees, legal fees, closing costs, etc.), expenses associated with other securities offerings of the Company, the costs of printing and mailing proxies and reports to the Company’s stockholders, costs incurred by employees or agents of the Manager for travel on the Company’s behalf, costs associated with any computer software or hardware that is used by the Company, costs to obtain liability insurance to indemnify directors and officers and the compensation and expenses of the Company’s transfer agent.

The following table summarizes the Company's reimbursement to the Manager for costs incurred for tasks and other services performed by the Manager under the Management Agreement:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Included in: | |||||||||||||||

General and administrative expense | $ | 1,843 | $ | 1,330 | $ | 6,115 | $ | 4,606 | |||||||

Acquisition, transaction and integration expense | 310 | 625 | 1,236 | 2,292 | |||||||||||

Total | $ | 2,153 | $ | 1,955 | $ | 7,351 | $ | 6,898 | |||||||

As of September 30, 2016 and December 31, 2015, the Company had a payable for Manager reimbursements of $1,473 and $1,518, respectively, which is included in “Due to affiliates” in the Consolidated Balance Sheets.

During 2015, the Company executed a plan to centralize operations in New York, New York and relocate certain personnel from the Plano, Texas office to New York, New York. The Company determined that this plan qualified as a restructuring activity under ASC 420. While the majority of restructuring-related costs were incurred in 2015, during the nine months ended September 30, 2016, the Company incurred additional costs of $141, which primarily consist of lease-related expenses associated with the office in Plano, Texas, and are included in "Other expense" in the Consolidated Statements of Operations. The Company has incurred cumulative costs associated with the restructuring of $805. The Company does not expect to incur any material costs related to this restructuring in subsequent periods.

15

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

Property Management Agreements

Within the Company’s Managed Properties segment, the Company is party to Property Management Agreements with Blue Harbor, an affiliate of Fortress, and Holiday, a portfolio company that is majority owned by a private equity fund managed by an affiliate of Fortress, to manage most of its senior housing properties. Pursuant to these Property Management Agreements, the Company pays monthly property management fees. For AL/MC properties managed by Blue Harbor and Holiday, the Company pays management fees equal to 6% of effective gross income for the first two years and 7% thereafter. For IL properties managed by Blue Harbor and Holiday, the Company generally pays management fees equal to 5% of effective gross income. For certain property management agreements, the Company may also pay an incentive fee based on operating performance of the properties. No incentive fees were incurred during the nine months ended September 30, 2016 and 2015. Property management fees are included in "Property operating expense" in the Consolidated Statements of Operations. Other amounts paid to affiliated managers that are included in property operating expense are payroll expense and travel reimbursement costs. The payroll expense is structured as a reimbursement to the Property Manager, who is the employer of record.

The following table summarizes property management fees and reimbursements paid by the Company to Property Managers affiliated with Fortress:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Property management fees | $ | 5,015 | $ | 4,267 | $ | 14,650 | $ | 11,023 | |||||||

Travel reimbursement costs | 92 | 92 | 276 | 277 | |||||||||||

Property-level payroll expenses | $ | 26,418 | $ | 23,249 | $ | 78,262 | $ | 59,630 | |||||||

As of September 30, 2016 and December 31, 2015, the Company had payables for property management fees of $1,712 and $1,689, respectively, and property-level payroll expenses of $6,321 and $5,088, respectively, which are included in “Due to affiliates” in the Consolidated Balance Sheets. The Property Management Agreements with affiliated managers have initial terms of 5 or 10 years and provide for automatic one-year extensions after the initial term, subject to termination rights.

Triple Net Lease Agreements

Within the Company’s Triple Net Lease segment, the Company is party to triple net leases with Holiday. Pursuant to the leases, the tenant is required to pay monthly rent payments in accordance with the lease terms. Such payments amounted to $17,754 and $16,989 for the three months ended September 30, 2016 and 2015, respectively, and $53,262 and $50,968 for the nine months ended September 30, 2016 and 2015, respectively.

16

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

12. | INCOME TAXES |

New Senior is organized and conducts its operations to qualify as a REIT under the requirements of the Internal Revenue Code of 1986, as amended (the "Code"). However, certain of the Company’s activities are conducted through its taxable REIT subsidiary ("TRS") and therefore are subject to federal and state income taxes at regular corporate tax rates.

The following table presents the expense (benefit) for income taxes:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Current | |||||||||||||||

Federal | $ | 95 | $ | — | $ | 95 | $ | — | |||||||

State and local | 101 | 83 | 222 | 187 | |||||||||||

Total current provision | 196 | 83 | 317 | 187 | |||||||||||

Deferred | |||||||||||||||

Federal | 529 | (427 | ) | (269 | ) | (537 | ) | ||||||||

State and local | 57 | (34 | ) | (17 | ) | 6 | |||||||||

Total deferred provision | 586 | (461 | ) | (286 | ) | (531 | ) | ||||||||

Total expense (benefit) for income taxes | $ | 782 | $ | (378 | ) | $ | 31 | $ | (344 | ) | |||||

The following table presents the significant components of deferred tax assets:

September 30, 2016 | December 31, 2015 | ||||||

Deferred tax assets: | |||||||

Prepaid fees and rent | $ | 1,857 | $ | 1,976 | |||

Net operating losses | 3,858 | 5,175 | |||||

Deferred rent | 3,590 | 2,063 | |||||

Tax credits | 95 | 26 | |||||

Other | 180 | 70 | |||||

Total deferred tax assets | 9,580 | 9,310 | |||||

Less valuation allowance | — | — | |||||

Net deferred tax assets | 9,580 | 9,310 | |||||

Deferred tax liabilities: | |||||||

Depreciation and amortization | 537 | 553 | |||||

Total deferred tax liabilities | 537 | 553 | |||||

Total net deferred tax assets | $ | 9,043 | $ | 8,757 | |||

In assessing the recoverability of deferred tax assets, management considers whether it is more likely than not that some portion or all of the deferred tax assets will not be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income by the TRS during the periods in which temporary differences become deductible and before the net operating loss carryforward expires. The Company has not recorded a valuation allowance against its deferred tax assets as of September 30, 2016 as management believes that it is more likely than not that its deferred tax assets will be realized.

17

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

13. | EQUITY |

On December 17, 2015, the board of directors authorized the Company to commence a modified “Dutch auction” self-tender offer to repurchase up to $30,000 in cash of shares of its common stock. The tender offer commenced on December 17, 2015 and expired on January 19, 2016. The Company incurred $30,884, including transaction costs, to repurchase 3,333,333 shares at a tender price of $9.00 per share.

In July 2016, the Company issued an aggregate of 13,029 shares of its common stock to its independent directors as compensation.

As of September 30, 2016, 1,302,720 shares of the Company’s common stock were held by Fortress, through its affiliates, and its principals.

14. | COMMITMENTS AND CONTINGENCIES |

As of September 30, 2016, management believes there are no material contingencies that would affect the Company’s results of operations, cash flows or financial position.

Certain Obligations, Liabilities and Litigation

The Company is and may become subject to various obligations, liabilities, investigations, inquiries and litigation assumed in connection with or arising out of its acquisitions or otherwise arising in connection with its on-going business. Some of these liabilities may be indemnified by third parties. However, if these liabilities, investigations and inquiries are greater than expected or were not known to the Company at the time of acquisition, if the Company is not entitled to indemnification, or if the responsible third party fails to indemnify the Company for these liabilities, such obligations, liabilities and litigation could have a material adverse effect on the Company. In addition, in connection with the sale or leasing of properties, the Company may incur various obligations and liabilities, including indemnification obligations, relating to the operations of those properties, which could have a material adverse effect on the Company’s financial position, cash flows and results of operations.

Certain Tax-Related Covenants

If New Senior is treated as a successor to Newcastle under applicable U.S. federal income tax rules, and if Newcastle failed to qualify as a REIT for a taxable year ending on or before December 31, 2015, New Senior could be prohibited from electing to be a REIT. Accordingly, in the separation and distribution agreement entered into to effect our spin-off from Newcastle ("Separation and Distribution Agreement"), Newcastle (i) represented that it had no knowledge of any fact or circumstance that would cause New Senior to fail to qualify as a REIT, (ii) covenanted to use commercially reasonable efforts to cooperate with New Senior as necessary to enable New Senior to qualify for taxation as a REIT and receive customary legal opinions concerning REIT status, including providing information and representations to New Senior and its tax counsel with respect to the composition of Newcastle’s income and assets, the composition of its stockholders and its operation as a REIT, and (iii) covenanted to use its reasonable best efforts to maintain its REIT status for each of Newcastle’s taxable years ending on or before December 31, 2015 (unless Newcastle obtains an opinion from a nationally recognized tax counsel or a private letter ruling from the Internal Revenue Service (“IRS”) to the effect that Newcastle’s failure to maintain its REIT status will not cause New Senior to fail to qualify as a REIT under the successor REIT rule referred to above).

Proceedings Indemnified and Defended by Third Parties

From time to time, the Company is party to certain legal actions, regulatory investigations and claims for which third parties are contractually obligated to indemnify, defend and hold the Company harmless. While the Company is presently not being defended by any tenant and other obligated third parties in these types of matters, there is no assurance that its tenants, their affiliates or other obligated third parties will continue to defend the Company in these matters, or that such parties will have sufficient assets, income and access to financing to enable them to satisfy their defense and indemnification obligations to the Company.

18

NEW SENIOR INVESTMENT GROUP INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

September 30, 2016

(dollars in thousands, except share data)

Environmental Costs

As a commercial real estate owner, the Company is subject to potential environmental costs. As of September 30, 2016, management of the Company is not aware of any environmental concerns that would have a material adverse effect on the Company’s financial position or results of operations.

Capital Improvement and Repair Commitments

The Company is committed to making $4,000 immediately available for capital improvements to the triple net lease properties under the Life Care Services Portfolio, of which $3,851 has been funded as of September 30, 2016. The Company also agreed to make available an additional $11,500 at certain intervals over the 15 year lease period to be used for further capital improvements. Upon funding the capital improvements, the Company will be entitled to a rent increase. Additionally, the Company is committed under the Watermark triple net lease property to make $1,000 available for lender mandated repairs, of which $334 has been funded as of September 30, 2016. The Company has also agreed to make $1,000 available for additional capital improvements during the 15 year lease period. Upon funding the capital improvements, the Company will be entitled to a rent increase.

15. | SUBSEQUENT EVENTS |

These Consolidated Financial Statements include a discussion of material events, if any, which have occurred subsequent to September 30, 2016 (referred to as subsequent events) through the issuance of the Consolidated Financial Statements.

On October 31, 2016, the Company sold two AL/MC properties with a net carrying value for real estate investments of $9,312 for a purchase price of $22,975, resulting in a gain of approximately $13,000. In connection with this sale, the Company repaid $13,725 of debt associated with these properties and, pursuant to the Property Management Agreement, paid a termination fee of approximately $1,800 to Blue Harbor.

On October 31, 2016, the Company's board of directors declared a cash dividend on its common stock of $0.26 per common share for the quarter ended September 30, 2016. The dividend is payable on December 22, 2016 to shareholders of record on December 8, 2016.

19

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management’s discussion and analysis of financial condition and results of operations is intended to help the reader understand the results of operations and financial condition of New Senior. The following should be read in conjunction with the unaudited Consolidated Financial Statements and notes thereto included within this Quarterly Report on Form 10-Q. This discussion contains forward-looking statements that are subject to known and unknown risks and uncertainties. Actual results and the timing of events may differ significantly from those expressed or implied in such forward-looking statements due to a number of factors, including those included in Part II, Item 1A “Risk Factors.”

OVERVIEW

Our Business

We are a REIT primarily focused on investing in private pay senior housing properties. As of September 30, 2016, we owned a diversified portfolio of 154 primarily private pay senior housing properties located across 37 states. We are listed on the NYSE under the symbol “SNR” and are headquartered in New York, New York.

We conduct our business through two reportable segments: Managed Properties and Triple Net Lease Properties. See our Consolidated Financial Statements and the related notes, including Note 1 included in Part I, Item 1 of this Quarterly Report on Form 10-Q.

We are externally managed and advised by an affiliate of Fortress (the "Manager") on various aspects of our business and our operations, subject to the supervision of our board of directors. For its services, the Manager is entitled to an annual management fee and is eligible for incentive compensation upon the satisfaction of certain performance thresholds, both as defined in, and in accordance with the terms of, the Management Agreement.

Acquisitions

For a discussion of acquisitions, see Note 3 included in Part I, Item 1 of this Quarterly Report on Form 10-Q.

MARKET CONSIDERATIONS

Senior housing is a $300 billion market, and ownership of senior housing assets is highly fragmented. Given these industry fundamentals and compelling demographics that are expected to drive increased demand for senior housing, we believe the senior housing industry presents attractive investment opportunities.

However, increased competition from other buyers of senior housing assets, as well as liquidity constraints and other factors, could impair our ability to source attractive investment opportunities. New construction, as well as increased availability and popularity of home health care or other alternatives to senior housing, could impair the value of our existing portfolio by hampering occupancy and rate growth, along with increasing operating expenses. Some market participants believe that senior housing inventory growth in 2016 could outpace growth in previous years and exceed demand growth.