Attached files

| file | filename |

|---|---|

| 8-K - ANNALY CAPITAL MANAGEMENT, INC. 8-K - ANNALY CAPITAL MANAGEMENT INC | a51419598.htm |

Exhibit 99.1

September 14, 2016 Barclays 2016 Global Financial Services Conference

This presentation, other written or oral communications and our public documents to which we refer contain or incorporate by reference certain forward-looking statements which are based on various assumptions (some of which are beyond our control) and may be identified by reference to a future period or periods or by the use of forward-looking terminology, such as "may," "will," "believe," "expect," "anticipate," "continue," or similar terms or variations on those terms or the negative of those terms. Actual results could differ materially from those set forth in forward-looking statements due to a variety of factors, including, but not limited to, changes in interest rates; changes in the yield curve; changes in prepayment rates; the availability of mortgage-backed securities and other securities for purchase; the availability of financing and, if available, the terms of any financings; changes in the market value of our assets; changes in business conditions and the general economy; our ability to grow our commercial business; our ability to grow our residential mortgage credit business; credit risks related to our investments in credit risk transfer securities, residential mortgage-backed securities and related residential mortgage credit assets, commercial real estate assets and corporate debt; risks related to investments in mortgage servicing rights and ownership of a servicer; any potential business disruption following the acquisition of Hatteras Financial Corp.; our ability to consummate any contemplated investment opportunities; changes in government regulations affecting our business; our ability to maintain our qualification as a REIT; and our ability to maintain our exemption from registration under the Investment Company Act of 1940, as amended. For a discussion of the risks and uncertainties which could cause actual results to differ from those contained in the forward-looking statements, see "Risk Factors" in our most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q. We do not undertake, and specifically disclaim any obligation, to publicly release the result of any revisions which may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements, except as required by law. This presentation includes unaudited pro forma information reflecting the acquisition of Hatteras Financial Corp. The unaudited pro forma information should be read in conjunction with the historical financial information and accompanying notes of Annaly Capital Management, Inc. and Hatteras Financial Corp.Non-GAAP Financial MeasuresThis presentation includes certain non-GAAP financial measures. The non-GAAP financial measures should not be viewed in isolation and are not a substitute for financial measures computed in accordance with GAAP. Please see the section entitled “Non-GAAP Reconciliations” in the attached Appendix for a reconciliation to the most directly comparable GAAP financial measures. Safe Harbor Notice

Sector Assets ($bn) Capital(2) ($bn) Sector Rank(3) Agency(4) $93.9 $10.1 #1 Commercial Real Estate(4) $2.5 $1.4 #4 Residential Credit $2.1 $1.0 #8 Middle Market Lending (MML) $0.7 $0.7 #16 Over $14bn Dividends Paid Since IPO Performance Track Record Annaly is a Leading Real Estate Finance Company Largest mREIT with a $13 billion equity base, 15x the size of the median mREITPermanent capital solution for the redistribution of mortgage-backed securities (“MBS”), residential credit, commercial real estate (“CRE”) assets and middle market loansDiversified investment platform built to manage various interest rate and economic environmentsConservative leverage profile with a variety of potential financing sources for each investment class Business Profile (1) Note: Market data as of September 2, 2016. Financial Data as of June 30, 2016. Financial data is unaudited and shown pro forma for Hatteras acquisitionDedicated capital excludes non-portfolio related activity and may differ from total stockholders’ equity.Sector ranking compares Annaly dedicated capital in each of its business strategies (Agency, CRE, Residential Credit and MML) pro forma for Hatteras acquisition as of June 30, 2016, adjusted for the relevant sector average price to book multiple, to the market capitalization of the companies in each respective sector as of September 2, 2016. Comparative sectors include the Bloomberg mREIT Index for Agency, CRE and Residential Credit and the S&P BDC Index for MML.Agency assets include TBA purchase contracts (market value). Commercial Real Estate assets are exclusive of consolidated variable interest entities (“VIEs”) associated with B Piece commercial mortgage-backed securities.

Diversified Business Model: $3 Trillion Total Market Opportunity Annaly is positioned as a permanent capital solution for the redistribution of MBS, residential credit, commercial real estate assets and corporate loans Corporate Loan Maturities Source: Fannie Mae, Freddie Mac, JPMorgan, Federal Reserve Flow of Funds Report, Trepp, Goldman Sachs, Leveraged Commentary & Data (“LCD”) and Mortgage Bankers Association (“MBA”). Analytics provided by The YieldBook Software. Note: $3 trillion opportunity represents the sum of estimated Fed and GSE runoff, CRE maturities and institutional loan maturities from 2016 to 2020. Excludes new CRE originations.Retained portfolios include both MBS and unsecuritized loans and represent 15% annual declines from 2015YE target of $719bn (10% below originally agreed upon target in Senior Preferred Stock Purchase Agreement).Current Fed holdings as of September 2, 2016. Future Fed holdings and runoff are projected assuming reinvestments continue until July 31, 2018 using forward interest rates.CMBS Data from RSS as of March 31, 2016.Mortgage Bankers Originations from MBA Commercial/Multifamily Real Estate Forecast from February 1, 2016. N drive:\\nyprodfs02\fidac\Capital Markets\Marketing\Presentations\Backup\GSE Run Off - Fed Run Off.xlsx CRE Maturities & New Originations(3) CRE Maturities $1.8tn New Originations(4) $1.9tn Loan Maturities $357bn GSE (1) / Federal Reserve (2) GSE (1) / Federal Reserve (2) Fed/GSE Run Off(1)$789bn

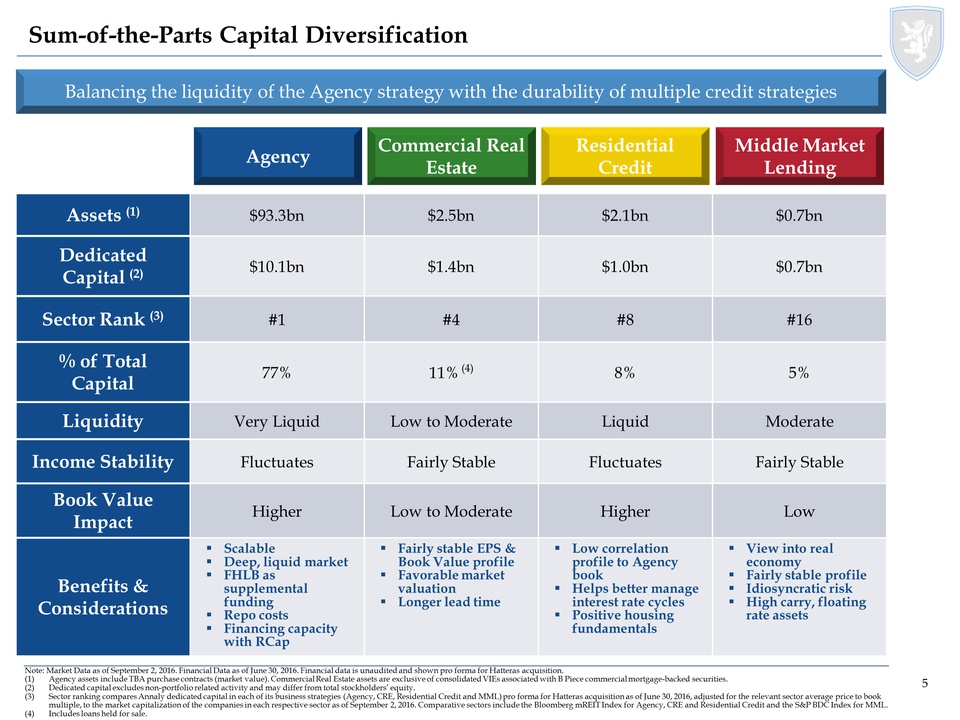

Balancing the liquidity of the Agency strategy with the durability of multiple credit strategies Sum-of-the-Parts Capital Diversification Agency Residential Credit Commercial Real Estate Middle Market Lending Assets (1) $93.3bn $2.5bn $2.1bn $0.7bn Dedicated Capital (2) $10.1bn $1.4bn $1.0bn $0.7bn Sector Rank (3) #1 #4 #8 #16 % of Total Capital 77% 11% (4) 8% 5% Liquidity Very Liquid Low to Moderate Liquid Moderate Income Stability Fluctuates Fairly Stable Fluctuates Fairly Stable Book Value Impact Higher Low to Moderate Higher Low Benefits &Considerations ScalableDeep, liquid marketFHLB as supplemental fundingRepo costsFinancing capacity with RCap Fairly stable EPS & Book Value profileFavorable market valuationLonger lead time Low correlation profile to Agency bookHelps better manage interest rate cyclesPositive housing fundamentals View into real economyFairly stable profileIdiosyncratic riskHigh carry, floating rate assets Note: Market Data as of September 2, 2016. Financial Data as of June 30, 2016. Financial data is unaudited and shown pro forma for Hatteras acquisition.Agency assets include TBA purchase contracts (market value). Commercial Real Estate assets are exclusive of consolidated VIEs associated with B Piece commercial mortgage-backed securities.Dedicated capital excludes non-portfolio related activity and may differ from total stockholders’ equity.Sector ranking compares Annaly dedicated capital in each of its business strategies (Agency, CRE, Residential Credit and MML) pro forma for Hatteras acquisition as of June 30, 2016, adjusted for the relevant sector average price to book multiple, to the market capitalization of the companies in each respective sector as of September 2, 2016. Comparative sectors include the Bloomberg mREIT Index for Agency, CRE and Residential Credit and the S&P BDC Index for MML.Includes loans held for sale.

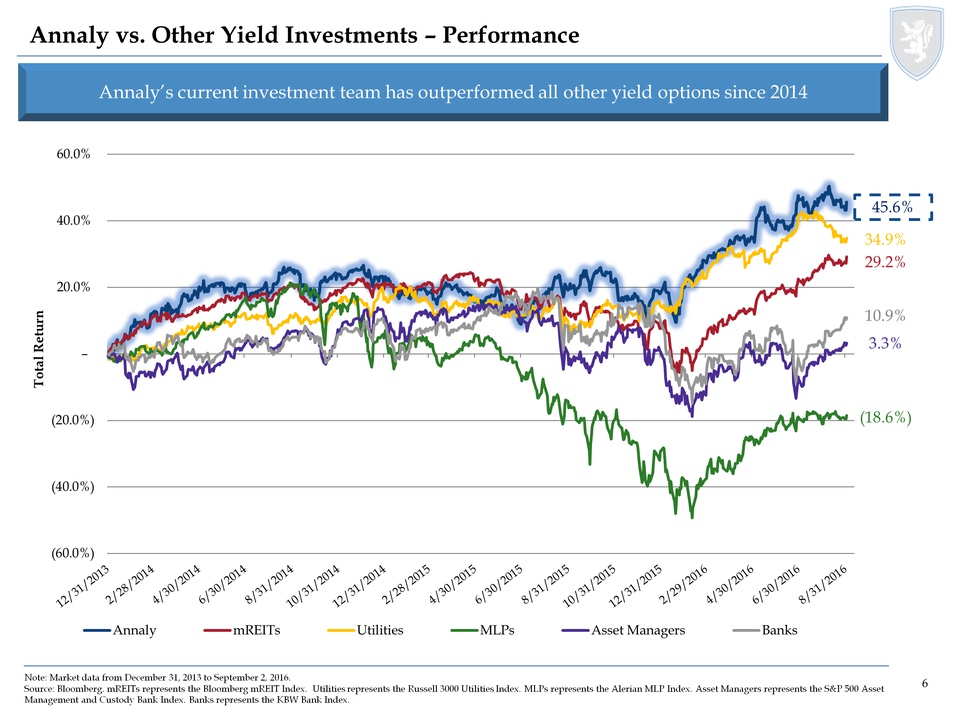

Annaly vs. Other Yield Investments – Performance Note: Market data from December 31, 2013 to September 2, 2016.Source: Bloomberg. mREITs represents the Bloomberg mREIT Index. Utilities represents the Russell 3000 Utilities Index. MLPs represents the Alerian MLP Index. Asset Managers represents the S&P 500 Asset Management and Custody Bank Index. Banks represents the KBW Bank Index. Annaly’s current investment team has outperformed all other yield options since 2014 N:\Capital Markets\Marketing\Internal\OpCo Offsite\June 2016\Excel\VIX and Yield Sectors vs NLY TR (AM Index) Since 2014.xlsx 45.6% 34.9% 29.2% (18.6%) 10.9% 3.3%

Annaly vs. Other Yield Investments – Valuation Annaly pays a superior dividend yield with a more conservative valuation compared to other income-oriented sectors Source: Bloomberg, Company filings and SNL Financial. mREITs represents the Bloomberg Mortgage REIT Index. Utilities represents the Russell 3000 Utilities Index. MLPs represents the Alerian MLP Index. Asset Managers represents the S&P 500 Asset Management and Custody Bank Index. Banks represent the KBW Bank Index.Note: Market data as of September 2, 2016. Quarterly data as of June 30, 2016. Leverage for other yield investments (excluding mREITs) represents financial leverage defined as average assets over average equity per Bloomberg. ADTV represents 3-month average daily trading volume per Bloomberg.Total Return since December 31, 2013 to September 2, 2016 per Bloomberg. Utilities MLPs Asset Managers Banks mREITs

\\nyprodfs02\fidac\Capital Markets\Marketing\Presentations\Roadshow\June 2016\VIX Analysis.xlsx Recession Annaly Has Outperformed in Periods of Heightened Volatility… Source: Bloomberg. Weekly data from October 10, 1997 until September 2, 2016.Note: S&P represents the SPX Index. Brexit Financial Crisis Greek Debt Crisis China Stock Market Turbulence

…While Providing Stable Earnings and Superior Returns Over Time Note: SNL Financial, Bloomberg, Company Filings. *Represents a non-GAAP measure. See appendix.2016 YTD reflects total return as of September 2, 2016. Reflects annualized core return on average equity. 2014 – 2016 YTD(1) 13.1% 2.6% 6.9% 2.3% (4.0%) 2.3% 4.0% 7.2% (1.1%) (2.1%) (8.8%) 1.7% 10.6% (6.7%) (1.9%) 5.9% 12.6% (5.1%) 45.6% 18.3% Total Return S&P Financials 10.9% 2.1%

From 2012 through annualized 1H 2016, Annaly significantly outperformed its mREIT peers with respect to operating expenditures as a percentage of equity and as a percentage of assetsAnnaly’s average expense levels over the period were 49% lower as a percentage of average equity and 65% lower as a percentage of average assets Annaly expense levels averaged 1.60% as a percentage of equity and 0.23% as a percentage of assets, while mREIT peers averaged 3.30% and 0.71%, respectively Efficiency of Operating Model Source: Company Filings, SNL and Bloomberg. Averages are market weighted based on market capitalization as of December 31st of each respective year, except 2016E which is as of September 12, 2016.Note: Internal Management and External Management represent the respective internally- and externally-managed members of the BBREMTG Index with market capitalization above $200mm as of the corresponding year end. Excludes Annaly and companies during years in which they became public or first listed. Operating Expense is defined as: (i) for Internally-Managed Peers, the sum of compensation & benefits, general & administrative expenses and other operating expenses, and (ii) for Externally-Managed Peers, the sum of net management fees, compensation & benefits (if any), general & administrative expenses and other operating expenses.2016E represents annualized operating expenses as of 1H 2016. Average Equity and Average Assets are as of June 30, 2016. Annaly outperforms internally and externally managed mREITs

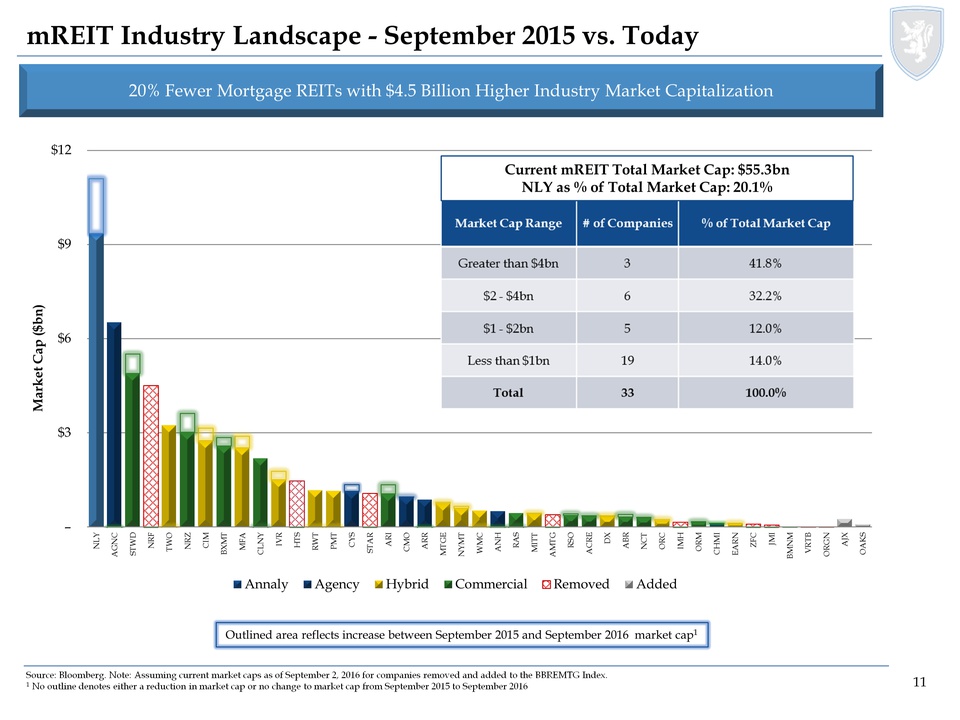

mREIT Industry Landscape - September 2015 vs. Today Source: Bloomberg. Note: Assuming current market caps as of September 2, 2016 for companies removed and added to the BBREMTG Index.1 No outline denotes either a reduction in market cap or no change to market cap from September 2015 to September 2016 20% Fewer Mortgage REITs with $4.5 Billion Higher Industry Market Capitalization Outlined area reflects increase between September 2015 and September 2016 market cap1

Progress on Our Strategy in 2016 On July 12, 2016 Annaly completed its acquisition of Hatteras Financial Corp. for approximately $1.5 billionRepresents largest mREIT acquisition in historyAdded complementary assets to Annaly’s existing investment portfolio External Growth Focused Agency MBS runoff into high quality prepay protected securitiesResidential Credit portfolio comprised of Credit Risk Transfer (CRT), Jumbo AAA Securities, NPL/RPL Securities, Legacy bonds and Whole LoansCRE portfolio growth only in high credit quality, risk-adjusted opportunitiesMML new deal flows increased with repeat sponsor business and larger ownership positions Increased FHLB borrowings to $3.6 billion with a weighted average maturity of over four yearsIncreased capacity under existing credit facility to $350 million for Annaly Commercial Real Estate GroupObtained $300 million credit facility for Middle Market Lending business Financing Strategy Portfolio Strategy

Pass Through Coupon Type Agency MBS Portfolio Update Data as of June 30, 2016. Data is unaudited and shown pro forma for Hatteras acquisition. Note: Percentages based on fair market value and may not sum to 100% due to rounding. Asset type is inclusive of TBA contracts.“High Quality” protection is defined as pools backed by original loan balances of up to $150K, higher LTV pools (CR/CQ), geographic concentrations (NY/PR). “Other Specified Pools” includes $175K loan balance, high LTV pools, FICO < 700. As of Q2 2016, the market value of Agency portfolio was approximately $93.9 billion in assets, inclusive of the TBA positionApproximately 92% of the portfolio is positioned in securities with prepayment protectionMBS performed well over the course of Q2 2016 in light of elevated volatility; however, low absolute yield levels have increased prepayment expectationsStrategy has focused on continued rotation into bonds with durable and stable cash flows Asset Type(1) Call Protection(2) Total Dedicated Capital: $10.1bn

Residential Credit Portfolio Update Data as of June 30, 2016. Data is unaudited and shown pro forma for Hatteras acquisitionNote: Percentages based on fair market value and may not sum to 100% due to rounding. As of Q2 2016, the portfolio grew to just over $2.1 billion in assets and is comprised of the following sectors:Credit Risk Transfer (CRT): Expect supply to remain in line with expectations in coming months and pick up modestly in Q4/early 2017 as faster prepayment speeds translate into modest increase in gross issuance Jumbo “AAA” Securities: Limited issuance given aggregators preferred funding mechanism of whole loan sales relative to securitizationNPL/RPL Securities: Yields on these products have tightened significantly year to date, as fundamentals remain strongLegacy: Market continues to be supported primarily by both short and long term positive technicals, as well as positive fundamentals Sector Type Coupon Type Total Dedicated Capital: $1.0bn

Commercial Real Estate Portfolio Update Data as of June 30, 2016. Data is unaudited and shown pro forma for Hatteras acquisitionNote: Percentages based on economic interest and may not sum to 100% due to rounding. Commercial Real Estate assets are exclusive of consolidated variable interest entities (“VIEs”) associated with B Piece commercial mortgage-backed securities.Other includes 24 states, none of which represent more than 5% of total portfolio value. As of Q2 2016, the commercial real estate portfolio was approximately $2.5 billion in assets(1)The combination of a significant decline in new acquisition activity by sponsors, a volatile marketplace and a cautious stance on credit led us to slow originations in the first half of 2016$365 million of new originations/purchases in first half of 2016Increased financing capacity to $350 million with recent $150 million upsize to existing credit facility$305 million funded under the facility in July 2016Active pipeline with quality opportunities, but will remain disciplined Will only grow with the right risk-adjusted opportunities1.9 billion Asset Type Sector Type Geographic Concentration(2) Total Dedicated Capital: $1.4bn

Middle Market Lending Portfolio Update Lien Position Industry (1) Loan Size(2) As of Q2 2016, the middle market lending portfolio grew to approximately $700 million in assetsA combination of repeat sponsor business, sectors of origination focus and larger ownership positions have garnered demonstrably increased new deal flow during the latter half of Q2 2016Unlevered portfolio yield increased from 7.8% at the end of Q1 2016 to 8.0% at the end of Q2 2016Closed $300 million credit facility in Q2 2016 $228 million funded under the facility in July 2016 Total Dedicated Capital: $0.7bn Data as of June 30, 2016 unless otherwise noted. Data is unaudited and shown pro forma for Hatteras acquisitionNote: Percentages based on principal outstanding and may not sum to 100% due to rounding.Based on Moody’s industry categories.Breakdown based on aggregate $ amount of individual investments made within the respective loan size buckets. Multiple investment positions with a single obligor shown as one individual investment. [ TBU ]

Transaction Overview Source: SNL Financial, Company Websites, Company Filings and Wells Fargo as of time of announcement.Excludes segment, portfolio or asset sales. Target assets exclude VIE assets. On April 11, 2016, Annaly Capital Management, Inc. (NLY) announced the acquisition of Hatteras Financial Corp. (HTS) for $1.5 billion in cash and stock11.2% premium to the closing price of HTS common stock ending April 8, 2016Price reflects 0.85x multiple of estimated book value per share at February 29, 2016Proration used to ensure an aggregate consideration of 65% stock/35% cashTransaction closed July 12, 2016, within 3 months of announcement Management’s Strategic Rationale Expands and Further Diversifies Annaly’s Investment PortfolioTransaction Expected to be Accretive to Annaly Shareholders Reinforces Annaly’s Stature as Industry Leader Strong Liquidity Position Closed $1.5 Billion Acquisition of July 2016 Annaly Acquisition of Hatteras Financial Corp Announcement of acquisition [ Replace with Final Transaction terms or Deal Highlights? ] (2) Largest Mortgage REIT to Mortgage REIT Transaction Ever, by Deal Value and Target Asset Value Third Largest Transaction in the Entire REIT Sector Since the Financial Crisis, by Target Asset Value Third Largest Specialty Finance Transaction Since the Financial Crisis, by Target Asset Value (1)

Significant Financing Advantages Agency Resi Credit MML PotentialFinancingSource RepoRCap SecuritiesFHLB SecuritizationCredit Facilities1st MortgagesNote SalesFHLB RepoFHLBSecuritization Credit FacilitiesCLO Target Leverage 6.0x - 8.0x 2.0x – 3.0x 2.0x – 3.0x 0.5x – 1.5x Commentary Maintain significant funding capacity with RCap Securities and the StreetSunset(1) for FHLB funding provides competitive advantage Able to attain non-recourse leverage via securitization market for certain asset classesCredit facilities provide term leverageNote sales expand liquidity scope for institutional lendingFHLB funding for certain asset classes remains attractive Significant appetite across the Street to fund Resi Credit collateralFHLB funding for certain asset classes remains attractive Portfolio generates attractive risk-adjusted yields on an unlevered basisSignificant capacity exists for bank funding Annaly has a variety of potential financing sources for each asset class in which the Company invests Note: Potential financing sources and target leverage represent the current views of Annaly’s management with respect to financing. Check mark indicates that Annaly currently uses this form of financing.(1) Sunset reflects an FHLB membership termination date of February 2021. Agency Residential Credit Commercial Real Estate Middle Market Lending

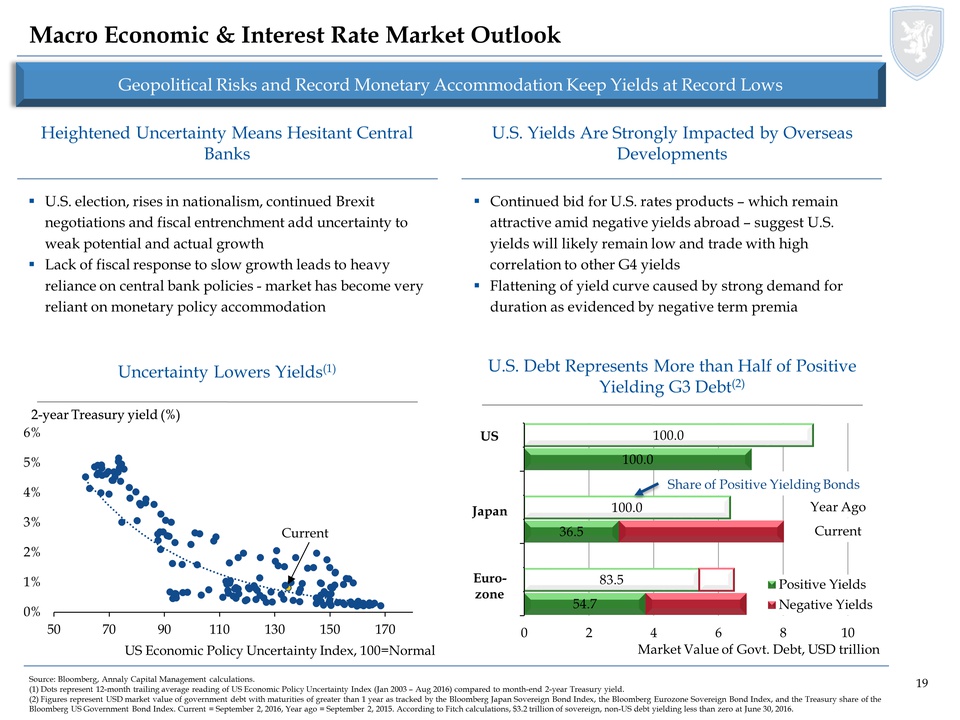

Macro Economic & Interest Rate Market Outlook U.S. election, rises in nationalism, continued Brexit negotiations and fiscal entrenchment add uncertainty to weak potential and actual growthLack of fiscal response to slow growth leads to heavy reliance on central bank policies - market has become very reliant on monetary policy accommodation Continued bid for U.S. rates products – which remain attractive amid negative yields abroad – suggest U.S. yields will likely remain low and trade with high correlation to other G4 yieldsFlattening of yield curve caused by strong demand for duration as evidenced by negative term premia Heightened Uncertainty Means Hesitant Central Banks U.S. Yields Are Strongly Impacted by Overseas Developments Geopolitical Risks and Record Monetary Accommodation Keep Yields at Record Lows Source: Bloomberg, Annaly Capital Management calculations.(1) Dots represent 12-month trailing average reading of US Economic Policy Uncertainty Index (Jan 2003 – Aug 2016) compared to month-end 2-year Treasury yield.(2) Figures represent USD market value of government debt with maturities of greater than 1 year as tracked by the Bloomberg Japan Sovereign Bond Index, the Bloomberg Eurozone Sovereign Bond Index, and the Treasury share of the Bloomberg US Government Bond Index. Current = September 2, 2016, Year ago = September 2, 2015. According to Fitch calculations, $3.2 trillion of sovereign, non-US debt yielding less than zero at June 30, 2016. Uncertainty Lowers Yields(1) U.S. Debt Represents More than Half of Positive Yielding G3 Debt(2)

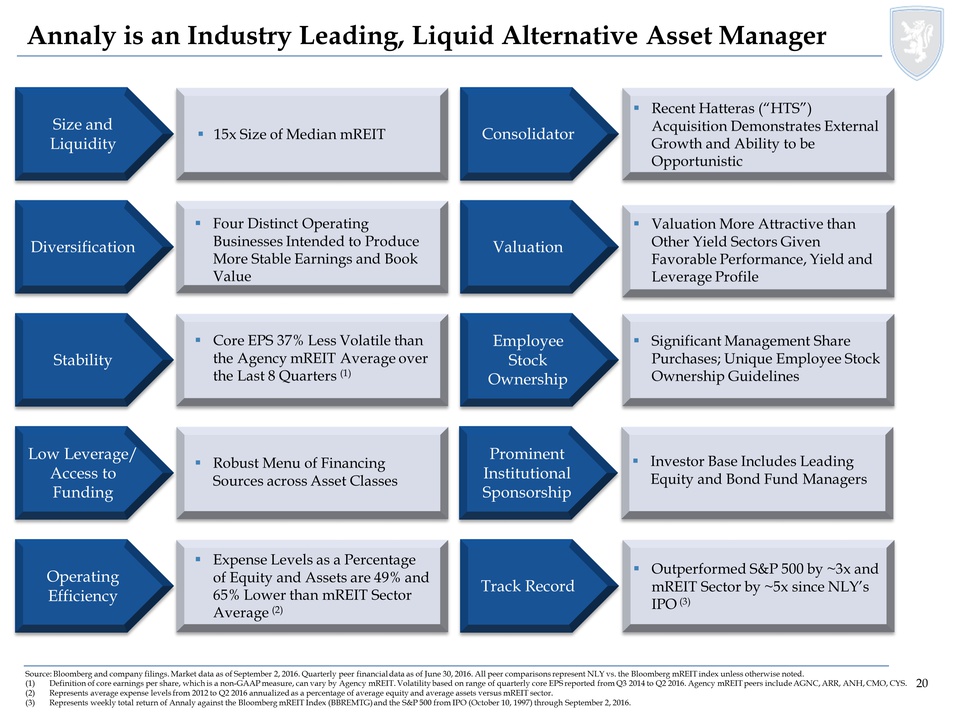

15x Size of Median mREIT Size and Liquidity Consolidator Recent Hatteras (“HTS”) Acquisition Demonstrates External Growth and Ability to be Opportunistic Diversification Four Distinct Operating Businesses Intended to Produce More Stable Earnings and Book Value Valuation Valuation More Attractive than Other Yield Sectors Given Favorable Performance, Yield and Leverage Profile Stability Employee Stock Ownership Core EPS 37% Less Volatile than the Agency mREIT Average over the Last 8 Quarters (1) Significant Management Share Purchases; Unique Employee Stock Ownership Guidelines Operating Efficiency Track Record Expense Levels as a Percentage of Equity and Assets are 49% and 65% Lower than mREIT Sector Average (2) Outperformed S&P 500 by ~3x and mREIT Sector by ~5x since NLY’s IPO (3) Low Leverage/ Access to Funding Prominent Institutional Sponsorship Robust Menu of Financing Sources across Asset Classes Investor Base Includes Leading Equity and Bond Fund Managers Source: Bloomberg and company filings. Market data as of September 2, 2016. Quarterly peer financial data as of June 30, 2016. All peer comparisons represent NLY vs. the Bloomberg mREIT index unless otherwise noted.Definition of core earnings per share, which is a non-GAAP measure, can vary by Agency mREIT. Volatility based on range of quarterly core EPS reported from Q3 2014 to Q2 2016. Agency mREIT peers include AGNC, ARR, ANH, CMO, CYS.Represents average expense levels from 2012 to Q2 2016 annualized as a percentage of average equity and average assets versus mREIT sector.Represents weekly total return of Annaly against the Bloomberg mREIT Index (BBREMTG) and the S&P 500 from IPO (October 10, 1997) through September 2, 2016. Annaly is an Industry Leading, Liquid Alternative Asset Manager

Appendix: Non-GAAP Reconciliation

Non-GAAP Reconciliations Unaudited, dollars in thousands except per share amounts