Attached files

| file | filename |

|---|---|

| 8-K - 8-K - NAVIENT CORP | d254866d8k.htm |

Exhibit 99.1

NAVIENT R

Barclays Global

Financial Services Conference

September 12, 2016

Forward-Looking Statements; Non-GAAP Financial Measures

The following information is current as of June 30, 2016 (unless otherwise noted) and should be read in connection with Navient Corporation’s (Navient) Annual Report on Form

10-K for the year ended December 31, 2015 (the “2015 Form 10-K”), filed by Navient with the Securities and Exchange Commission (the “SEC”) on February 25, 2016 and subsequent reports filed by Navient with the SEC. Definitions for

capitalized terms in this presentation not defined herein can be found in our 2015 Form 10-K. This presentation contains “forward-looking” statements and other information that is based on management’s current expectations as of the

date of this presentation. Statements that are not historical facts, including statements about our beliefs, opinions, or expectations and statements that assume or are dependent upon future events, are forward-looking statements and often contain

words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “see,” “will,” “would,” or “target.” Forward-looking statements are

subject to risks, uncertainties, assumptions and other factors that may cause actual results to be materially different from those reflected in such forward-looking statements.

For us, these factors include, among others, the risks and uncertainties associated with:

increases in financing costs;

the availability of financing;

limits on liquidity resulting from disruptions in the capital markets or other factors;

unanticipated increases in costs associated with compliance with laws and regulations;

changes in the marketplaces in which we compete (including changes in demand or changes resulting from new laws and regulations);

changes in accounting standards pertaining to loan loss reserves and estimates or other accounting standards that may impact our operations;

adverse outcomes in any significant litigation to which we are a party;

credit risk associated

with our exposure to third parties, including counterparties to hedging or other derivative transactions; and

changes in the terms of education loans and the

educational credit marketplace (including changes resulting from new laws and the implementation of existing laws).

We could also be affected by, among other

things:

unanticipated deferrals in our FFELP securitization trusts that would delay repayment of the bonds beyond their legal final maturity date;

reductions to our credit ratings, the credit ratings of asset-backed securitizations we sponsor or the credit ratings of the United States of America;

failures of our operating systems or infrastructure, or those of third-party vendors;

risks

related to cybersecurity including the potential disruption of our systems or potential disclosure of confidential customer information;

damage to our reputation

resulting from the politicization of student loan servicing;

failures to successfully implement cost-cutting initiatives and adverse effects of such initiatives on

our business;

delays or errors in converting portfolio acquisitions to our servicing platform

risks associated with restructuring initiatives;

changes in law and regulations with respect

to the student lending business and financial institutions generally;

increased competition from banks and other consumer lenders who are not subject to the same

level of regulation;

the creditworthiness of our customers;

changes in the

general interest rate environment, including the relationship between the relevant money-market index rate and the rate at which our assets are priced;

our ability

to successfully effectuate any acquisitions and other strategic initiatives;

changes in the demand for debt management services;

changes in general economic conditions; and

the other factors that are described in the

“Risk Factors” section of the 2015 Form 10-K and in our future reports filed with the SEC.

The preparation of our consolidated financial statements also

requires management to make certain estimates and assumptions including estimates and assumptions about future events. These estimates or assumptions may prove to be incorrect and actual results could differ materially. All forward-looking

statements contained in this presentation are qualified by these cautionary statements and are made only as of the date of this presentation. We do not undertake any obligation to update or revise these forward-looking statements except as required

by law.

Navient reports financial results on a GAAP basis and also provides certain non-GAAP core earnings performance measures. When compared to GAAP results,

core earnings exclude the impact of: (1) the financial results of the consumer banking business for historical periods prior to the April 30, 2014 spin-off of Navient from SLM Corporation as well as related restructuring and reorganization expenses

incurred in connection with the spin-off, including the restructuring initiated in the second quarter of 2015; (2) unrealized, mark-to-market gains/losses on derivatives; and (3) goodwill and acquired intangible asset amortization and impairment.

Navient provides core earnings measures because this is what management uses when making management decisions regarding Navient’s performance and the allocation of corporate resources. Navient core earnings are not defined terms within GAAP and

may not be comparable to similarly titled measures reported by other companies. For additional information, see “Differences Between ‘Core Earnings’ and GAAP” on slide 20 of this presentation for a further discussion and a

complete reconciliation between GAAP net income and core earnings.

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights

reserved.

2

NAVIENTSM

We are the

leading loan management, servicing and asset recovery company

$117 billion education loan portfolio, of which 79% is insured or guaranteed

Servicing more than $300 billion in student loans, the company supports the educational and economic achievements of more than 12 million Americans

Asset recovery and business processing platform provide services for over 1,000 public and private sector clients

Helping our customers navigate the path to financial success is everything we stand for

As of

June 30, 2016

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

3

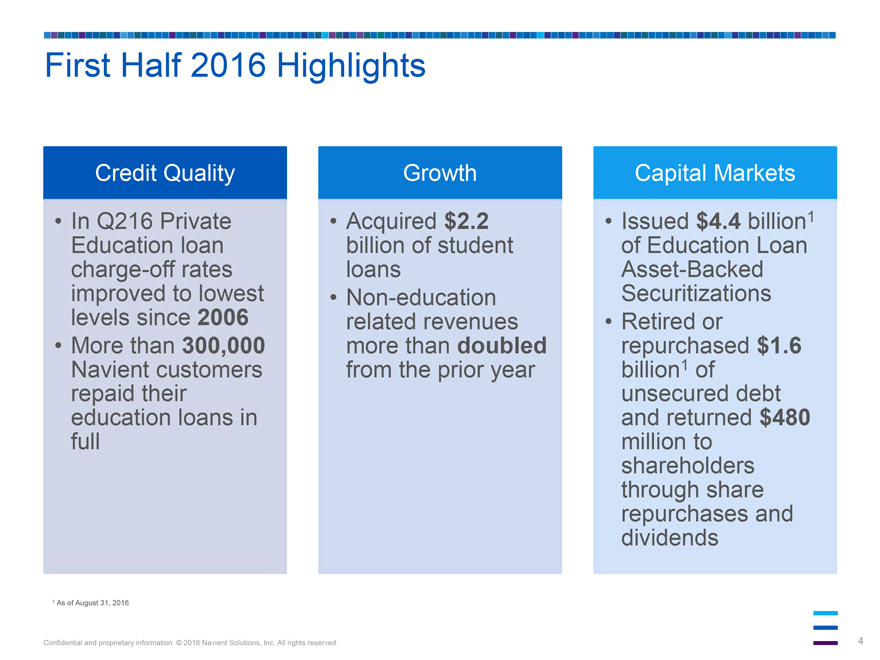

First Half 2016 Highlights

Credit Quality

In Q216 Private Education loan charge-off rates improved to

lowest levels since 2006

More than 300,000 Navient customers repaid their education loans in full

Growth

Acquired $2.2 billion of student loans

Non-education related revenues more than doubled from the prior year

Capital Markets

Issued $4.4 billion1 of Education Loan Asset-Backed Securitizations

Retired

or repurchased $1.6 billion1 of unsecured debt and returned $480 million to shareholders through share repurchases and dividends

1 As of August 31, 2016

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

4

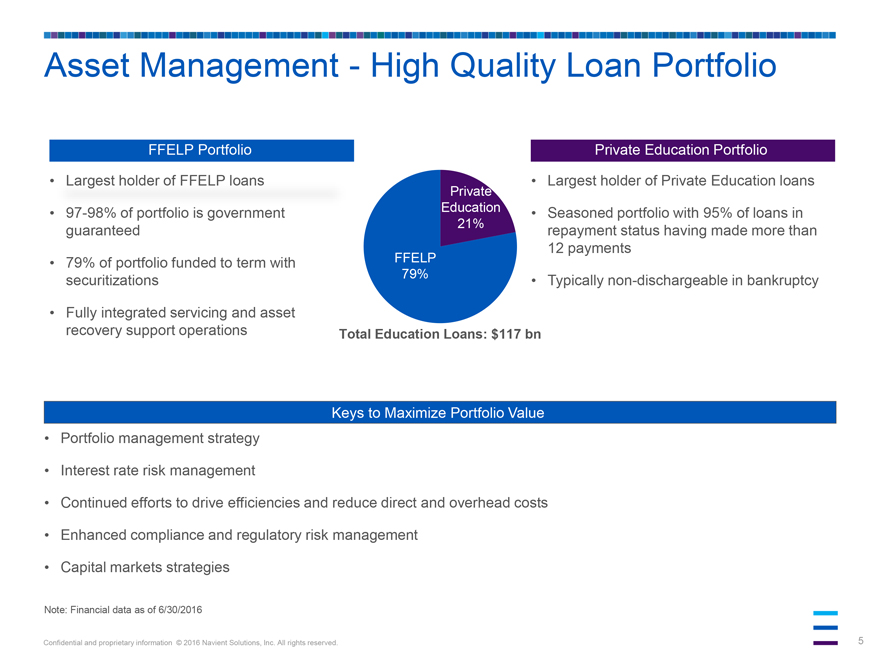

Asset Management - High Quality Loan Portfolio

FFELP Portfolio

Largest holder of FFELP loans

97-98% of portfolio is government guaranteed

79% of portfolio funded to term with

securitizations

Fully integrated servicing and asset recovery support operations

FFELP 79%

Private Education 21%

Total Education Loans: $117 bn

Private Education Portfolio

Largest holder of Private Education loans

Seasoned portfolio with 95% of loans in repayment

status having made more than 12 payments

Typically non-dischargeable in bankruptcy

Keys to Maximize Portfolio Value

Portfolio management strategy

Interest rate risk management

Continued efforts to drive efficiencies and reduce direct and

overhead costs

Enhanced compliance and regulatory risk management

Capital

markets strategies

Note: Financial data as of 6/30/2016

Confidential and

proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

5

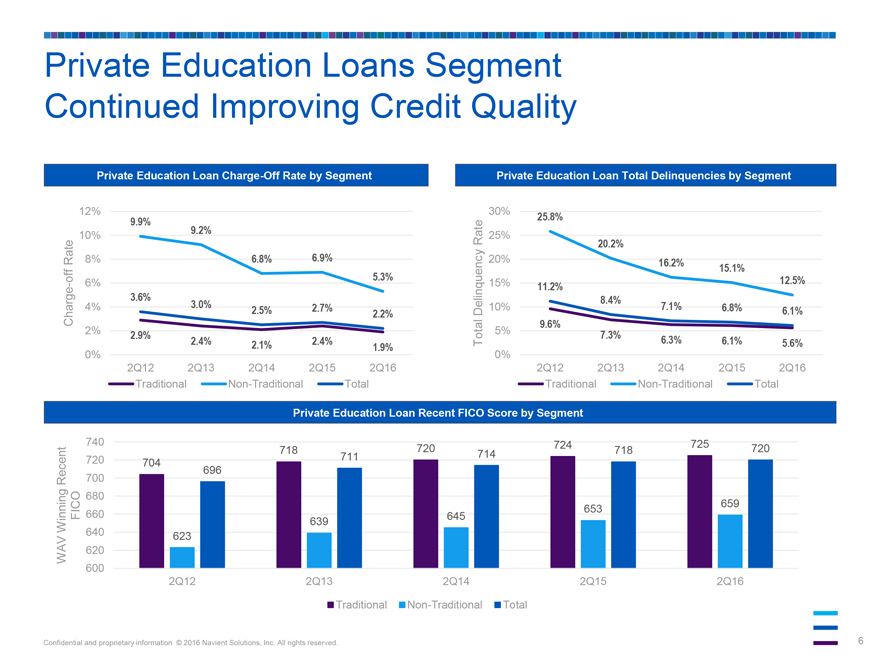

Private Education Loans Segment

Continued Improving Credit Quality

Private Education Loan Charge-Off Rate by Segment

Charge-off Rate

12% 10% 8% 6% 4% 2% 0%

9.9% 9.2% 6.8% 6.9% 5.3%

3.6% 3.0% 2.5% 2.7% 2.2%

2.9% 2.4% 2.1% 2.4% 1.9%

2Q12 2Q13 2Q14 2Q15 2Q16

Traditional Non-Traditional Total

Private Education Loan Total Delinquencies by Segment

Total Delinquency Rate

30% 25% 20% 15% 10% 5% 0%

25.8% 20.2% 16.2% 15.1% 12.5%

11.2% 8.4% 7.1% 6.8% 6.1%

9.6% 7.3% 6.3% 6.1% 5.6%

2Q12 2Q13 2Q14 2Q15 2Q16

Traditional Non-Traditional Total

Private Education Loan Recent FICO Score by Segment

WAV Winning Recent

FICO

740 720 700 680 660 640 620 600

704 623 696 718 639 711 720 645 714 724 653 718 725 659 720

2Q12 2Q13 2Q14 2Q15 2Q16

Traditional Non-Traditional Total

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

6

Education Loan Portfolio Generates Significant Cash Flows

Projected Life of Loan Cash Flows over ~20 Years

$’s in Billions

FFELP Cash Flows 6/30/16

Secured

Residual (including O/C) $6.9

Floor Income 2.4

Servicing 3.3

Total Secured $12.6

Unencumbered 1.1

Total FFELP Cash Flows $13.7

Private Credit Cash Flows

Secured

Residual (including O/C) $11.5

Servicing 1.0

Total Secured $12.5

Unencumbered 3.9

Total Private Cash Flows $16.4

Combined Cash Flows

before Unsecured Debt $30.1

These projections are based on internal estimates and assumptions

and are subject to ongoing review and modification. These projections may prove to be incorrect.

Enhancing Cash Flows1

Acquired $2.2 billion of student loans in the first half 2016

Reduced unsecured debt by $0.9

billion through August 31st, 2016

Returned $0.5 billion to shareholders through share repurchases and dividends in the first half 2016

$30.1 billion of estimated future cash flows over ~ 20 years

- Includes ~$11 billion of

overcollateralization2 (O/C) to be released from residuals

$3.9 billion of unencumbered student loans

Decreasing FFELP CPR assumptions by 1% would increase projected FFELP cash flows by $0.4 billion

$1.1 billion of FFELP Loan floor income is hedged

1 As of June 30, 2016

2 Includes $1.4B O/C related to six private education ABS trusts securing our private education loan ABS repurchase transactions

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

7

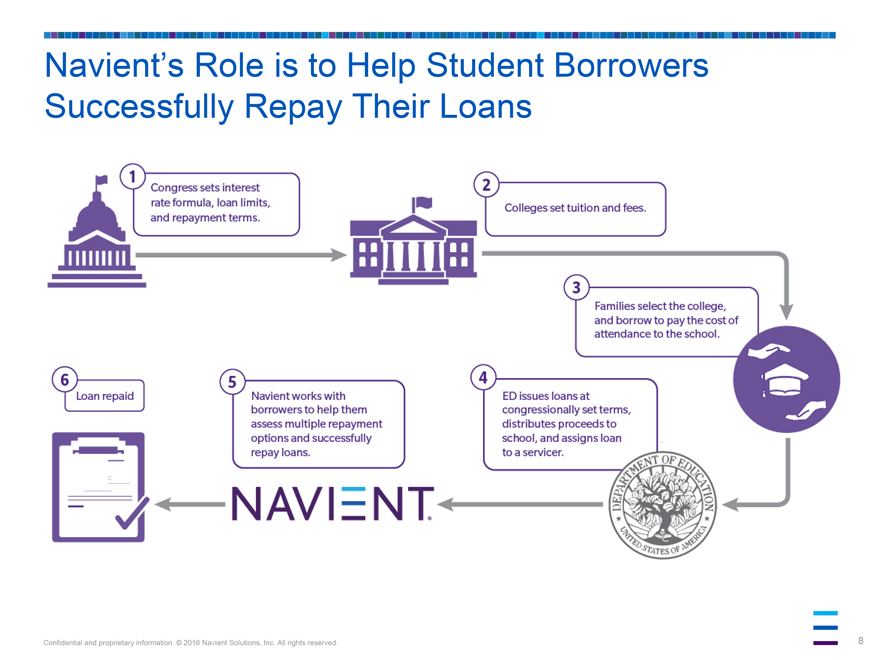

Navient’s Role is to Help Student Borrowers Successfully Repay Their Loans

1 Congress sets interest rate formula, loan limits, and repayment terms.

2 Colleges set

tuition and fees.

3 Families select the college, and borrow to pay the cost of attendance to the school.

4 ED issues loans at congressionally set terms, distributes proceeds to school, and assigns loan to a servicer.

5 Navient works with borrowers to help them assess multiple repayment options and successfully repay loans.

6 Loan repaid

DEPARTMENT OF EDUCATION

UNITED STATES OF AMERICA

NAVIENT

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

8

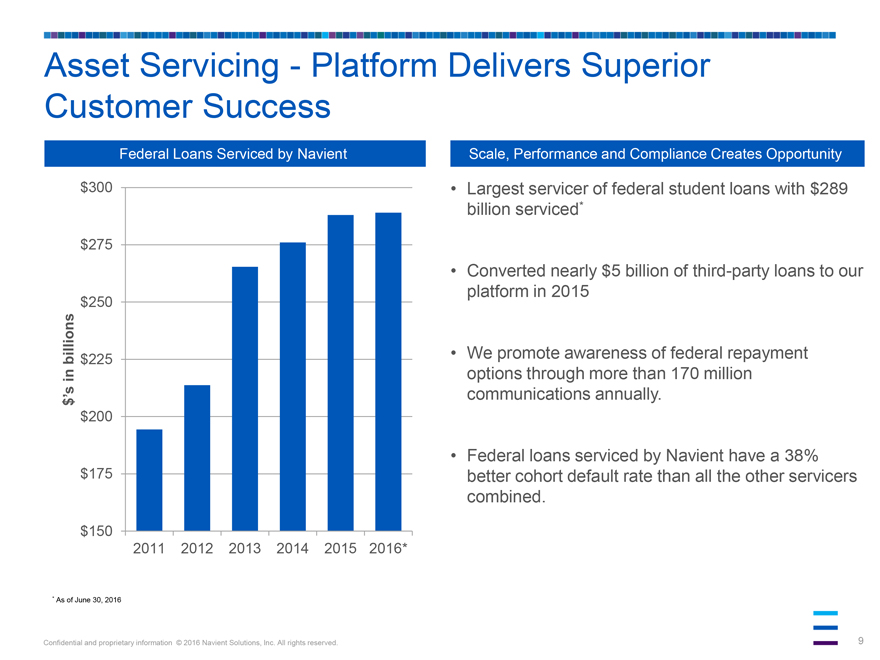

Asset Servicing - Platform Delivers Superior Customer Success

Federal Loans Serviced by Navient

$’s in billions

$300 $275 $250 $225 $200 $175 $150

2011 2012 2013 2014 2015 2016*

Scale, Performance and Compliance Creates Opportunity

Largest servicer of federal student

loans with $289 billion serviced*

Converted nearly $5 billion of third-party loans to our platform in 2015

We promote awareness of federal repayment options through more than 170 million communications annually.

Federal loans serviced by Navient have a 38% better cohort default rate than all the other servicers combined.

* As of June 30, 2016

Confidential and proprietary information © 2016 Navient Solutions,

Inc. All rights reserved.

9

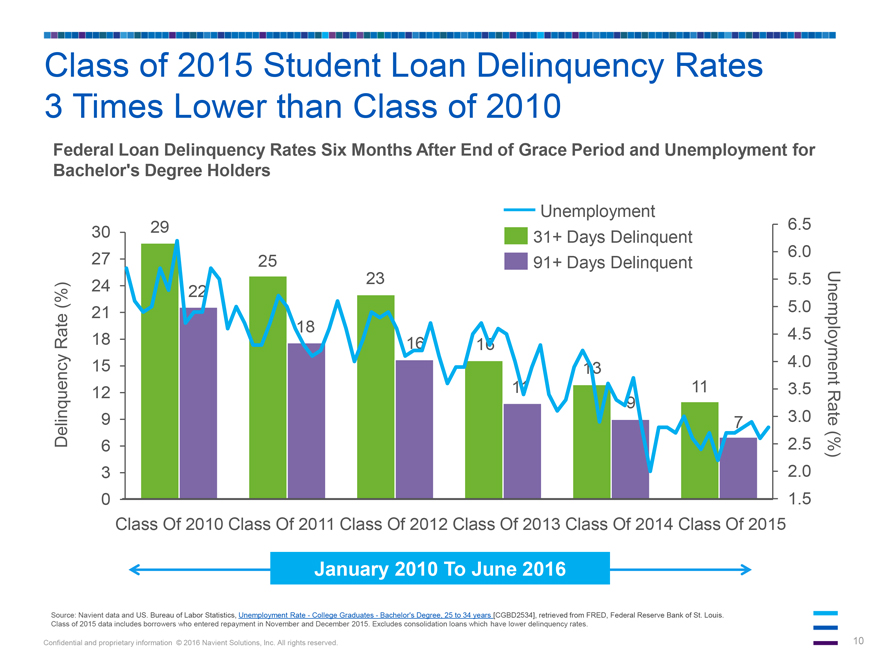

Class of 2015 Student Loan Delinquency Rates

3 Times Lower than Class of 2010

Federal Loan Delinquency Rates Six Months After End of Grace

Period and Unemployment for Bachelor’s Degree Holders

Delinquency Rate (%)

30

27

24

21

18

15

12

9

6

3

0

29

22

25

18

23

16

16

11

13

9

11

7

Unemployment

31+ Days Delinquent

91+ Days Delinquent

6.5

6.0

5.5

5.0

4.5

4.0

3.5

3.0

2.5

2.0

1.5

Unemployment Rate (%)

Class Of 2010 Class Of 2011 Class Of 2012 Class Of 2013 Class Of 2014 Class Of 2015

January

2010 To June 2016

Source: Navient data and US. Bureau of Labor Statistics, Unemployment Rate - College Graduates - Bachelor’s Degree, 25 to 34 years

[CGBD2534], retrieved from FRED, Federal Reserve Bank of St. Louis. Class of 2015 data includes borrowers who entered repayment in November and December 2015. Excludes consolidation loans which have lower delinquency rates.

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

10

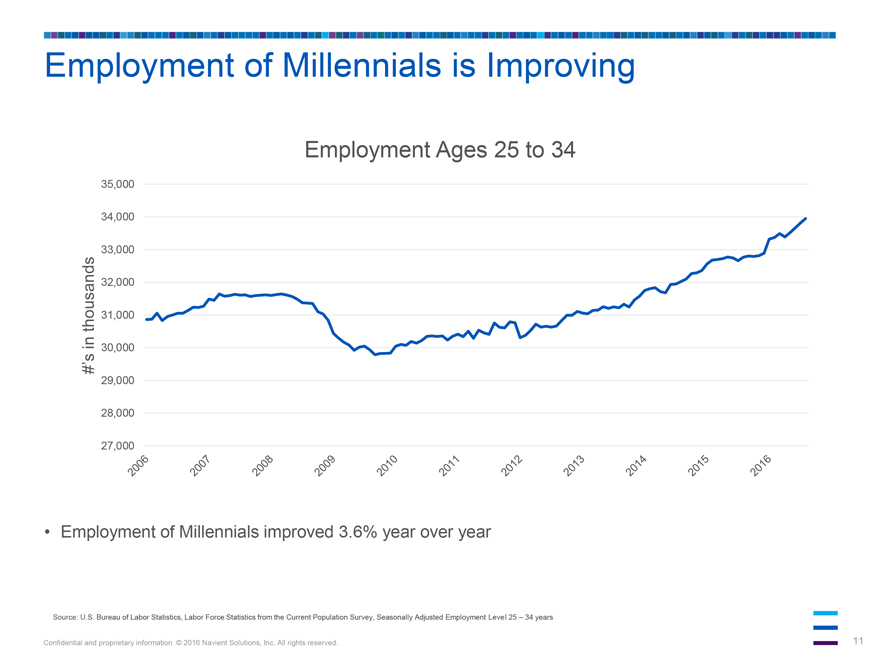

Employment of Millennials is Improving

Employment Ages 25 to 34

#’s in thousands

35,000 34,000 33,000 32,000 31,000 30,000 29,000 28,000 27,000

2006 2007 2008 2009 2010 2011

2012 2013 2014 2015 2016

• Employment of Millennials improved 3.6% year over year

Source: U.S. Bureau of Labor Statistics, Labor Force Statistics from the Current Population Survey, Seasonally Adjusted Employment Level 25 – 34 years

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

11

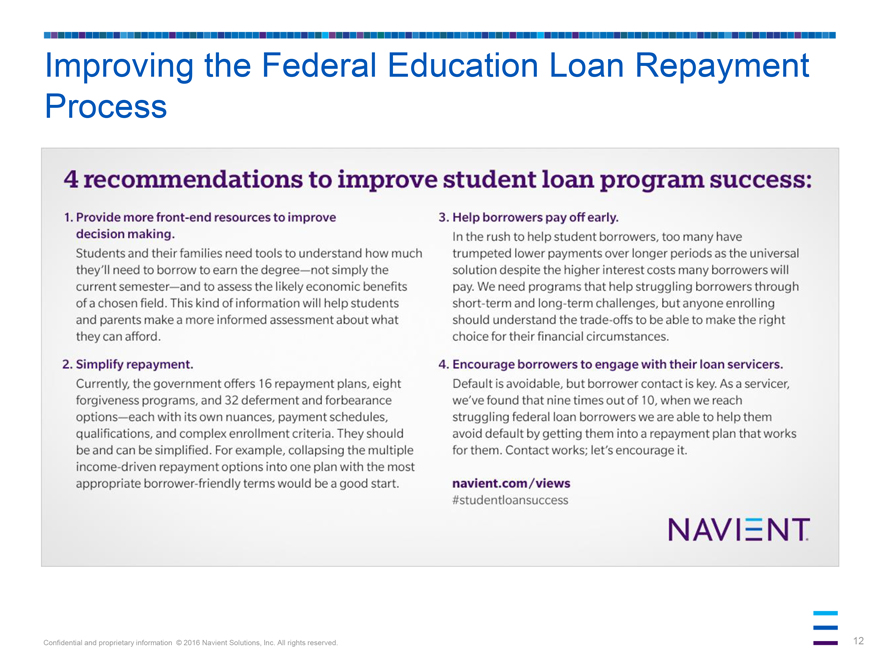

Improving the Federal Education Loan Repayment Process

4 recommendations to improve student loan program success:

1. Provide more front-end resources

to improve decision making.

Students and their families need tools to understand how much they’ll need to borrow to earn the degree—not simply the

current semester—and to assess the likely economic benefits of a chosen field. This kind of information will help students and parents make a more informed assessment about what they can afford.

2. Simplify repayment.

Currently, the government offers 16 repayment plans, eight forgiveness

programs, and 32 deferment and forbearance options—each with its own nuances, payment schedules, qualifications, and complex enrollment criteria. They should be and can be simplified. For example, collapsing the multiple income-driven repayment

options into one plan with the most appropriate borrower-friendly terms would be a good start.

3. Help borrowers pay off early.

In the rush to help student borrowers, too many have trumpeted lower payments over longer periods as the universal solution despite the higher interest costs many borrowers will

pay. We need programs that help struggling borrowers through short-term and long-term challenges, but anyone enrolling should understand the trade-offs to be able to make the right choice for their financial circumstances.

4. Encourage borrowers to engage with their loan servicers.

Default is avoidable, but borrower

contact is key. As a servicer, we’ve found that nine times out of 10, when we reach struggling federal loan borrowers we are able to help them avoid default by getting them into a repayment plan that works for them. Contact works; let’s

encourage it.

navient.com/views

#studentloansuccess

NAVIENT

Confidential and proprietary information © 2016 Navient Solutions, Inc. All

rights reserved.

12

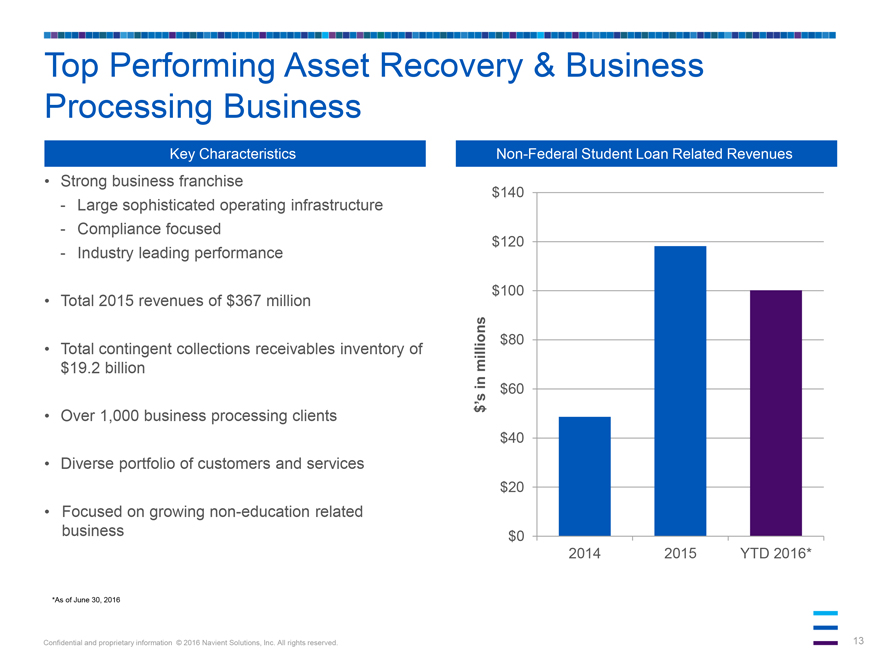

Top Performing Asset Recovery & Business Processing Business

Key Characteristics

Strong business franchise

Large sophisticated operating infrastructure

Compliance focused

Industry leading performance

Total 2015 revenues of $367 million

Total contingent collections receivables inventory of $19.2 billion

Over 1,000 business

processing clients

Diverse portfolio of customers and services

Focused on

growing non-education related business

Non-Federal Student Loan Related Revenues

$’s in millions

$140 $120 $100 $80 $60 $40 $20 $0

2014 2015 YTD 2016*

*As of June 30, 2016

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

13

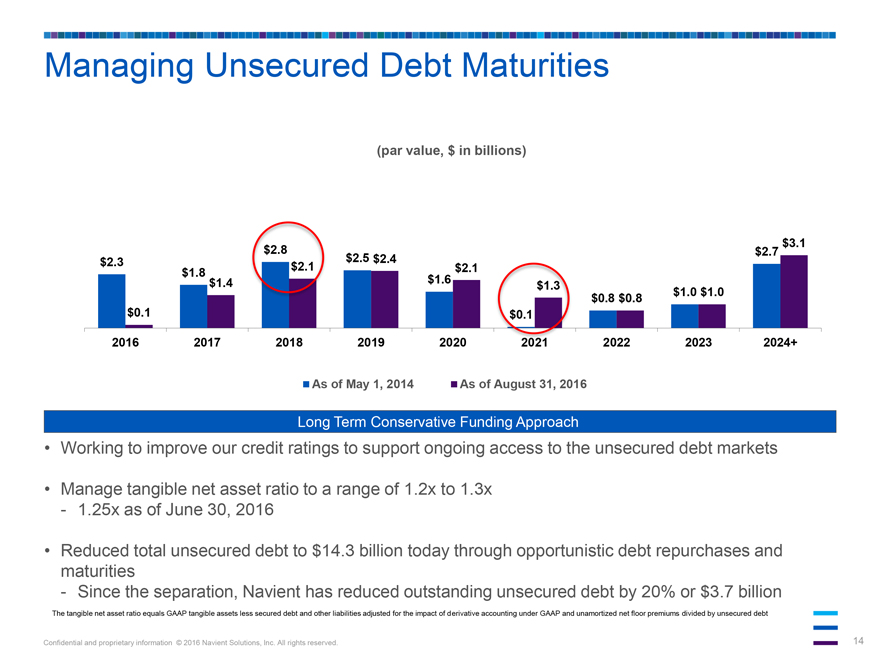

Managing Unsecured Debt Maturities

(par value, $ in billions)

$2.3

$0.1

$1.8

$1.4

$2.8

$2.1

$2.5 $2.4

$1.6

$2.1

$0.1

$1.3

$0.8 $0.8

$1.0 $1.0

$2.7

$3.1

2016 2017 2018 2019 2020 2021 2022 2023 2024+

As of May 1, 2014 As of August

31, 2016

Long Term Conservative Funding Approach

Working to improve our

credit ratings to support ongoing access to the unsecured debt markets

Manage tangible net asset ratio to a range of 1.2x to 1.3x

1.25x as of June 30, 2016

Reduced total unsecured debt to $14.3 billion today through

opportunistic debt repurchases and maturities

Since the separation, Navient has reduced outstanding unsecured debt by 20% or $3.7 billion

The tangible net asset ratio equals GAAP tangible assets less secured debt and other liabilities adjusted for the impact of derivative accounting under GAAP and unamortized net

floor premiums divided by unsecured debt

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

14

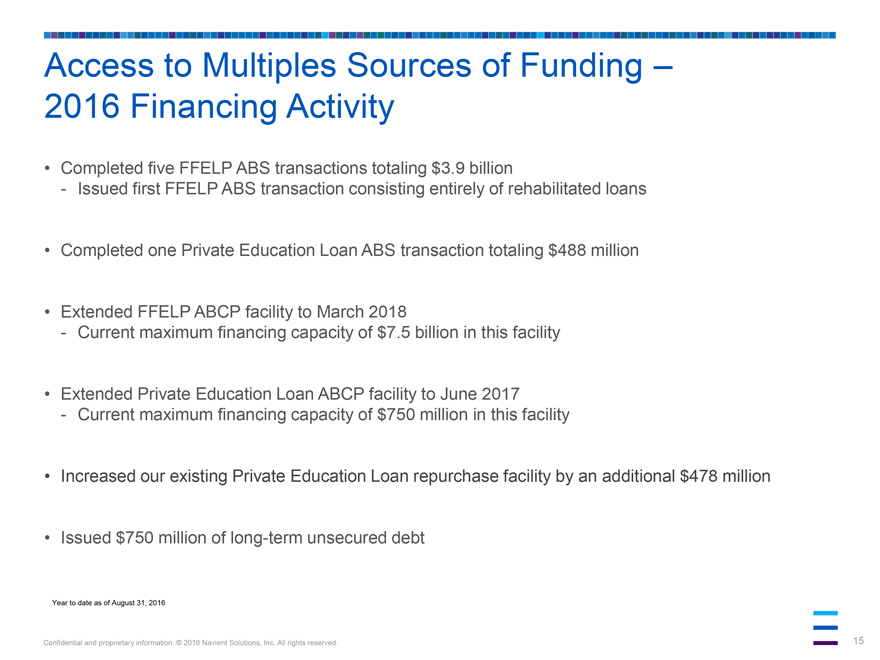

Access to Multiples Sources of Funding –2016 Financing Activity

Completed five FFELP ABS transactions totaling $3.9 billion

Issued first FFELP ABS transaction

consisting entirely of rehabilitated loans

Completed one Private Education Loan ABS transaction totaling $488 million

Extended FFELP ABCP facility to March 2018

Current maximum financing capacity of $7.5 billion

in this facility

Extended Private Education Loan ABCP facility to June 2017

Current maximum financing capacity of $750 million in this facility

Increased

our existing Private Education Loan repurchase facility by an additional $478 million

Issued $750 million of long-term unsecured debt

Year to date as of August 31, 2016

Confidential and proprietary information © 2016

Navient Solutions, Inc. All rights reserved.

15

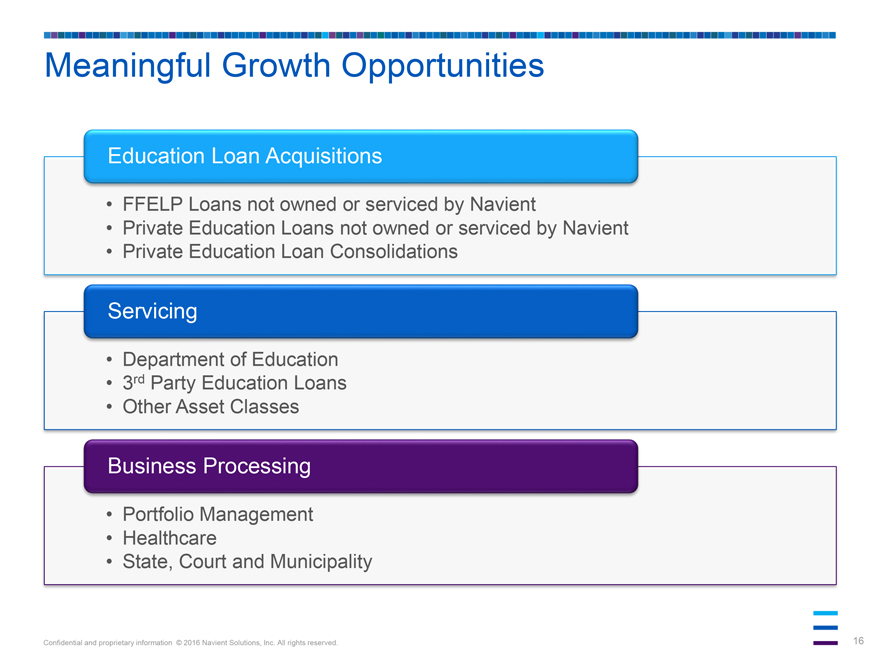

Meaningful Growth Opportunities

Education Loan Acquisitions

FFELP Loans not owned or serviced by Navient

Private Education Loans not owned or serviced by Navient

Private Education Loan Consolidations

Servicing

Department of Education

3rd Party Education Loans

Other Asset Classes

Business Processing

Portfolio Management

Healthcare

State, Court and Municipality

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

16

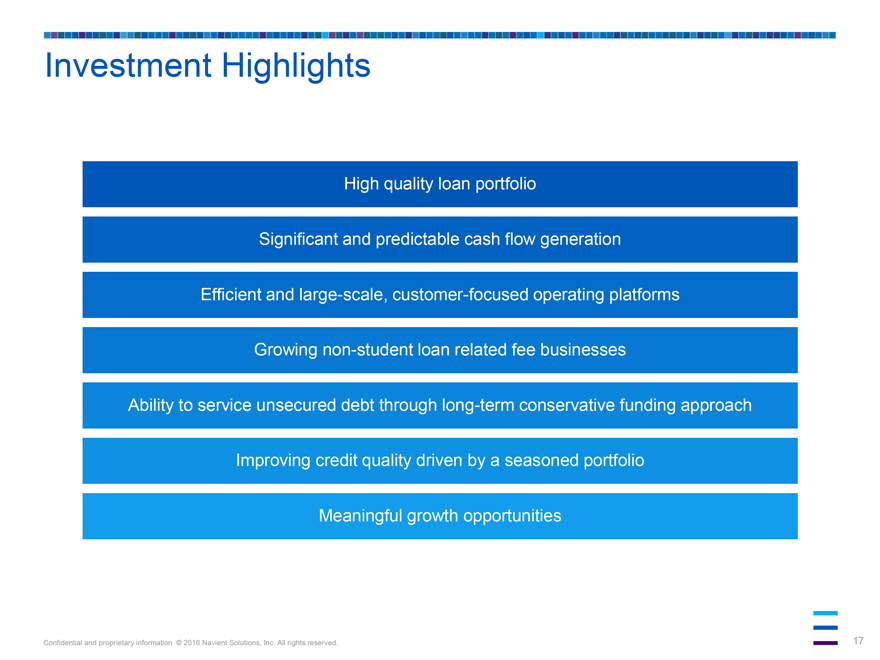

Investment Highlights

High quality loan portfolio

Significant and predictable cash flow generation

Efficient and large-scale, customer-focused operating platforms

Growing

non-student loan related fee businesses

Ability to service unsecured debt through long-term conservative funding approach

Improving credit quality driven by a seasoned portfolio

Meaningful growth opportunities

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

17

NAVIENT®

Appendix

Confidential and

proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

19

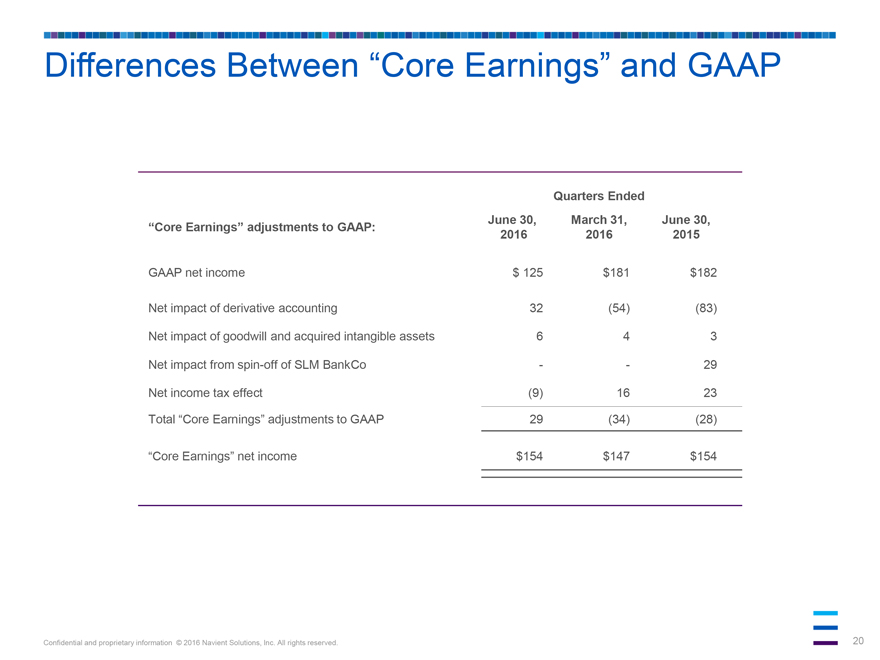

Differences Between “Core Earnings” and GAAP

Quarters Ended

“Core Earnings” adjustments to GAAP: June 30, 2016 March 31, 2016

June 30, 2015

GAAP net income $125 $181 $182

Net impact of derivative

accounting 32 (54) (83)

Net impact of goodwill and acquired intangible assets 6 4 3

Net impact from spin-off of SLM BankCo - - 29

Net income tax effect (9) 16 23

Total “Core Earnings” adjustments to GAAP 29 (34) (28)

“Core Earnings” net

income $154 $147 $154

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

20

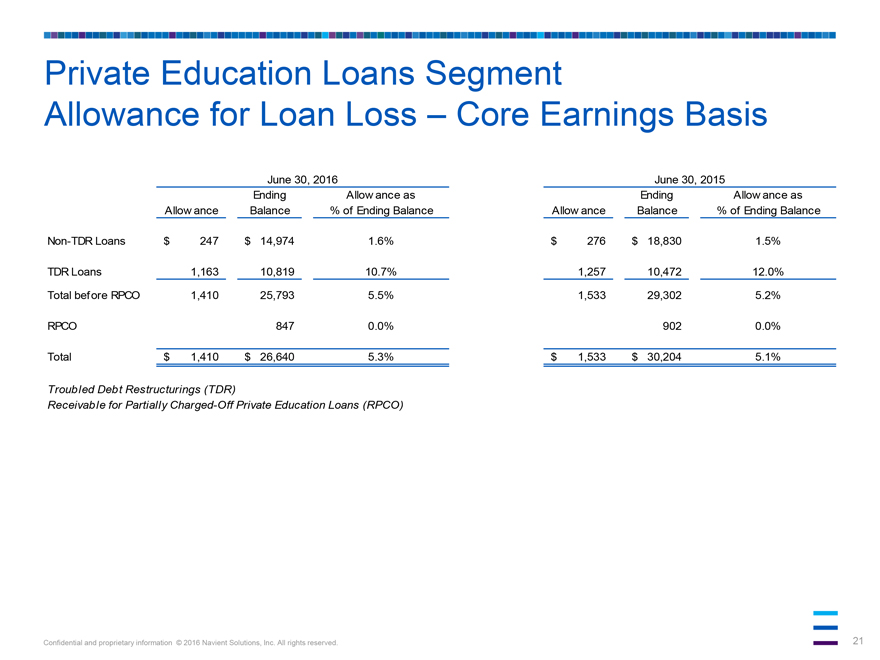

Private Education Loans Segment

Allowance for Loan Loss - Core Earnings Basis

June 30, 2016

June 30, 2015

Allowance

Ending Balance

Allowance as % of Ending Balance

Allowance

Ending Balance

Allowance as % of Ending Balance

Non-TDR Loans $247 $14,974 1.6% $276 $18,830 1.5%

TDR Loans 1,163 10,819 10.7% 1,257 10,472 12.0%

Total before RPCO 1,410 25,793 5.5% 1,533

29,302 5.2%

RPCO 847 0.0% 902 0.0%

Total $1,410 $26,640 5.3% $1,533 $30,204

5.1%

Troubled Debt Restructurings (TDR)

Receivable for Partially Charged-Off

Private Education Loans (RPCO)

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

21

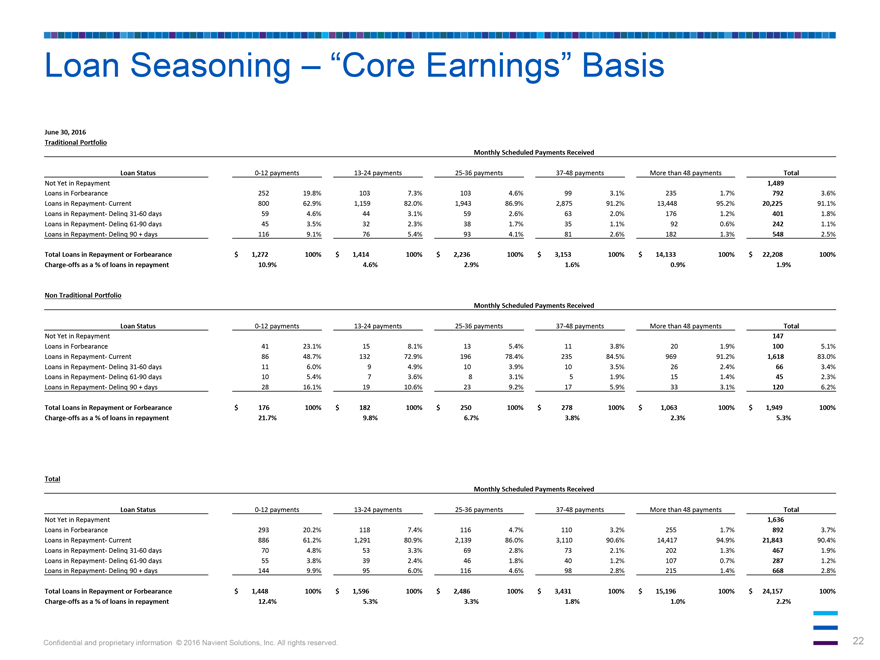

Loan Seasoning - “Core Earnings” Basis

June 30, 2016

Traditional Portfolio

Monthly Scheduled Payments Received

Loan Status

0-12 payments

13-24 payments

25-36 payments

37-48 payments

More than 48 payments

Total

Not Yet in Repayment

1,489

Loans in Forbearance 252 19.8% 103 7.3% 103 4.6% 99 3.1% 235 1.7% 792 3.6%

Loans in Repayment-

Current 800 62.9% 1,159 82.0% 1,943 86.9% 2,875 91.2% 13,448 95.2% 20,225 91.1%

Loans in Repayment- Delinq 31-60 days 59 4.6% 44 3.1% 59 2.6% 63 2.0% 176 1.2% 401

1.8%

Loans in Repayment- Delinq 61-90 days 45 3.5% 32 2.3% 38 1.7% 35 1.1% 92 0.6% 242 1.1%

Loans in Repayment- Delinq 90 + days 116 9.1% 76 5.4% 93 4.1% 81 2.6% 182 1.3% 548 2.5%

Total

Loans in Repayment or Forbearance $1,272 100% $1,414 100% $2,236 100% $3,153 100% $14,133 100% $22,208 100%

Charge-offs as a % of loans in repayment 10.9% 4.6%

2.9% 1.6% 0.9% 1.9%

Non Traditional Portfolio

Monthly Scheduled Payments

Received

Loan Status

0-12 payments

13-24 payments

25-36 payments

37-48 payments

More than 48 payments

Total

Not Yet in Repayment 147

Loans in Forbearance 41 23.1% 15 8.1% 13 5.4% 11 3.8% 20 1.9% 100 5.1%

Loans in Repayment-

Current 86 48.7% 132 72.9% 196 78.4% 235 84.5% 969 91.2% 1,618 83.0%

Loans in Repayment- Delinq 31-60 days 11 6.0% 9 4.9% 10 3.9% 10 3.5% 26 2.4% 66 3.4%

Loans in Repayment- Delinq 61-90 days 10 5.4% 7 3.6% 8 3.1% 5 1.9% 15 1.4% 45 2.3%

Loans in Repayment- Delinq 90 + days 28 16.1% 19 10.6% 23 9.2% 17 5.9% 33 3.1% 120 6.2%

Total

Loans in Repayment or Forbearance $176 100% $182 100% $250 100% $278 100% $1,063 100% $1,949 100%

Charge-offs as a % of loans in repayment 21.7% 9.8% 6.7% 3.8%

2.3% 5.3%

Total

Monthly Scheduled Payments Received

Loan Status

0-12 payments

13-24 payments

25-36 payments

37-48 payments

More than 48 payments

Total

Not Yet in Repayment 1,636

Loans in Forbearance 293 20.2% 118 7.4% 116 4.7% 110 3.2% 255 1.7% 892 3.7%

Loans in

Repayment- Current 886 61.2% 1,291 80.9% 2,139 86.0% 3,110 90.6% 14,417 94.9% 21,843 90.4%

Loans in Repayment- Delinq 31-60 days 70 4.8% 53 3.3% 69 2.8% 73 2.1%

202 1.3% 467 1.9%

Loans in Repayment- Delinq 61-90 days 55 3.8% 39 2.4% 46 1.8% 40 1.2% 107 0.7% 287 1.2%

Loans in Repayment- Delinq 90 + days 144 9.9% 95 6.0% 116 4.6% 98 2.8% 215 1.4% 668 2.8%

Total

Loans in Repayment or Forbearance $1,448 100% $1,596 100% $2,486 100% $3,431 100% $15,196 100% $24,157 100%

Charge-offs as a % of loans in repayment 12.4% 5.3%

3.3% 1.8% 1.0% 2.2%

Confidential and proprietary information © 2016 Navient Solutions, Inc. All rights reserved.

22

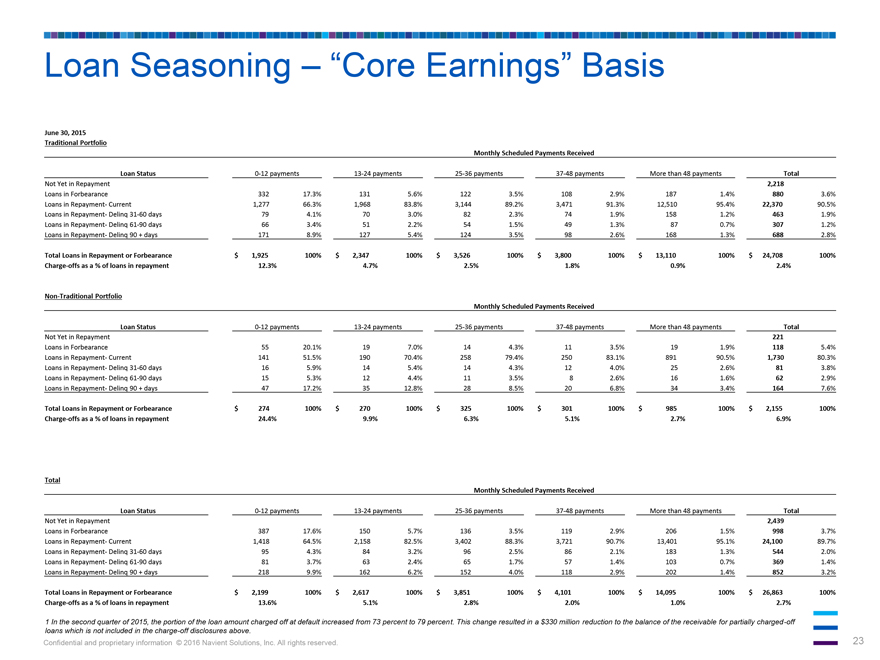

Loan Seasoning - “Core Earnings” Basis

June 30, 2015

Traditional Portfolio

Monthly Scheduled Payments Received

Loan Status 0-12 payments 13-24 payments 25-36 payments

37-48 payments More than 48 payments Total

Not Yet in Repayment 2,218

Loans

in Forbearance 332 17.3% 131 5.6% 122 3.5% 108 2.9% 187 1.4% 880 3.6%

Loans in Repayment- Current 1,277 66.3% 1,968 83.8% 3,144 89.2% 3,471 91.3% 12,510 95.4%

22,370 90.5%

Loans in Repayment- Delinq 31-60 days 79 4.1% 70 3.0% 82 2.3% 74 1.9% 158 1.2% 463 1.9%

Loans in Repayment- Delinq 61-90 days 66 3.4% 51 2.2% 54 1.5% 49 1.3% 87 0.7% 307 1.2%

Loans

in Repayment- Delinq 90 + days 171 8.9% 127 5.4% 124 3.5% 98 2.6% 168 1.3% 688 2.8%

Total Loans in Repayment or Forbearance $1,925 100% $2,347 100% $3,526 100%

$3,800 100% $13,110 100% $24,708 100%

Charge-offs as a % of loans in repayment 12.3% 4.7% 2.5% 1.8% 0.9% 2.4%

Non-Traditional Portfolio

Monthly Scheduled Payments Received

Loan Status 0-12 payments 13-24 payments 25-36 payments 37-48 payments More than 48 payments Total

Not Yet in Repayment 221

Loans in Forbearance 55 20.1% 19 7.0% 14 4.3% 11 3.5% 19 1.9% 118

5.4%

Loans in Repayment- Current 141 51.5% 190 70.4% 258 79.4% 250 83.1% 891 90.5% 1,730 80.3%

Loans in Repayment- Delinq 31-60 days 16 5.9% 14 5.4% 14 4.3% 12 4.0% 25 2.6% 81 3.8%

Loans in

Repayment- Delinq 61-90 days 15 5.3% 12 4.4% 11 3.5% 8 2.6% 16 1.6% 62 2.9%

Loans in Repayment- Delinq 90 + days 47 17.2% 35 12.8% 28 8.5% 20 6.8% 34 3.4% 164 7.6%

Total Loans in Repayment or Forbearance $274 100% $270 100% $325 100% $301 100% $985 100% $2,155 100%

Charge-offs as a % of loans in repayment 24.4% 9.9% 6.3% 5.1% 2.7% 6.9%

Total

Monthly Scheduled Payments Received

Loan Status 0-12 payments 13-24 payments 25-36 payments

37-48 payments More than 48 payments Total

Not Yet in Repayment 2,439

Loans

in Forbearance 387 17.6% 150 5.7% 136 3.5% 119 2.9% 206 1.5% 998 3.7%

Loans in Repayment- Current 1,418 64.5% 2,158 82.5% 3,402 88.3% 3,721 90.7% 13,401 95.1%

24,100 89.7%

Loans in Repayment- Delinq 31-60 days 95 4.3% 84 3.2% 96 2.5% 86 2.1% 183 1.3% 544 2.0%

Loans in Repayment- Delinq 61-90 days 81 3.7% 63 2.4% 65 1.7% 57 1.4% 103 0.7% 369 1.4%

Loans

in Repayment- Delinq 90 + days 218 9.9% 162 6.2% 152 4.0% 118 2.9% 202 1.4% 852 3.2%

Total Loans in Repayment or Forbearance $2,199 100% $2,617 100% $3,851 100%

$4,101 100% $14,095 100% $26,863 100%

Charge-offs as a % of loans in repayment 13.6% 5.1% 2.8% 2.0% 1.0% 2.7%

1 In the second quarter of 2015, the portion of the loan amount charged off at default increased from 73 percent to 79 percent. This change resulted in a $330 million reduction to

the balance of the receivable for partially charged-off loans which is not included in the charge-off disclosures above.

Confidential and proprietary information

© 2016 Navient Solutions, Inc. All rights reserved.

23