Attached files

| file | filename |

|---|---|

| EX-32.2 - EXHIBIT 32.2 - LSI INDUSTRIES INC | ex32-2.htm |

| EX-32.1 - EXHIBIT 32.1 - LSI INDUSTRIES INC | ex32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - LSI INDUSTRIES INC | ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - LSI INDUSTRIES INC | ex31-1.htm |

| EX-23.1 - EXHIBIT 23.1 - LSI INDUSTRIES INC | ex23-1.htm |

| EX-21 - EXHIBIT 21 - LSI INDUSTRIES INC | ex21.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

☑ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED JUNE 30, 2016.

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO .

Commission File No. 0-13375

LSI INDUSTRIES INC.

(Exact name of Registrant as specified in its charter)

|

|

10000 Alliance Road |

|

(513) 793-3200

(Telephone number of principal executive offices)

Securities Registered Pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Name of each exchange on which registered |

|

|

|

|

|

Common shares, no par value |

|

The NASDAQ Stock Market LLC |

Securities Registered Pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☑ |

Non-accelerated filer ☐ |

Smaller reporting company ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

As of December 31, 2015, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was approximately $300,176,800 based upon a closing sale price of $12.19 per share as reported on The NASDAQ Global Select Market.

At August 27, 2016 there were 24,978,016 no par value Common Shares issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement filed with the Commission for its 2016 Annual Meeting of Shareholders are incorporated by reference in Part III, as specified.

LSI INDUSTRIES INC.

2016 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

|

|

Begins on | |

|

|

Page | |

|

PART I | ||

|

|

||

|

ITEM 1. BUSINESS |

1 | |

|

|

||

|

ITEM 1A. RISK FACTORS |

6 | |

|

|

||

|

ITEM 1B. UNRESOLVED STAFF COMMENTS |

10 | |

|

|

||

|

ITEM 2. PROPERTIES |

10 | |

|

|

||

|

ITEM 3. LEGAL PROCEEDINGS |

11 | |

|

|

||

|

ITEM 4. MINE SAFETY DISCLOSURES |

11 | |

|

|

||

|

PART II | ||

|

|

||

|

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

11 | |

|

|

||

|

ITEM 6. SELECTED FINANCIAL DATA |

13 | |

|

|

||

|

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

13 | |

|

|

||

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

13 | |

|

|

||

|

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

14 | |

|

|

||

|

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

15 | |

|

|

||

|

ITEM 9A. CONTROLS AND PROCEDURES |

15 | |

|

|

||

|

ITEM 9B. OTHER INFORMATION |

15 | |

|

|

||

|

PART III | ||

|

|

||

|

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

15 | |

|

|

||

|

ITEM 11. EXECUTIVE COMPENSATION |

15 | |

|

|

||

|

ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

15 | |

|

|

||

|

ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

15 | |

|

|

||

|

ITEM 14. PRINCIPAL ACCOUNTANT FEES AND SERVICES |

15 | |

|

|

||

|

PART IV | ||

|

|

||

|

ITEM 15. EXHIBITS AND FINANCIAL STATEMENT SCHEDULES |

16 | |

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995

This Annual Report on Form 10-K contains certain forward-looking statements that are subject to numerous assumptions, risks or uncertainties. The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements. Forward-looking statements may be identified by words such as “estimates,” “anticipates,” “projects,” “plans,” “expects,” “intends,” “believes,” “seeks,” “may,” “will,” “should” or the negative versions of those words and similar expressions, and by the context in which they are used. Such statements, whether expressed or implied, are based upon current expectations of the Company and speak only as of the date made. Actual results could differ materially from those contained in or implied by such forward-looking statements as a result of a variety of risks and uncertainties over which the Company may have no control. These risks and uncertainties include, but are not limited to, the impact of competitive products and services, product demand and market acceptance risks, potential costs associated with litigation and regulatory compliance, reliance on key customers, financial difficulties experienced by customers, the cyclical and seasonal nature of our business, the adequacy of reserves and allowances for doubtful accounts, fluctuations in operating results or costs whether as a result of uncertainties inherent in tax and accounting matters or otherwise, unexpected difficulties in integrating acquired businesses, the ability to retain key employees of acquired businesses, unfavorable economic and market conditions, the results of asset impairment assessments, the Company’s ability to maintain an effective system of internal control over financial reporting, our ability to remediate any material weaknesses in our internal control over financial reporting and any other risk factors that are identified herein. You are cautioned to not place undue reliance on these forward-looking statements. In addition to the factors described in this paragraph, the risk factors identified in this Annual Report on Form 10-K and other filings the Company may make with the SEC constitute risks and uncertainties that may affect the financial performance of the Company and are incorporated herein by reference. The Company does not undertake and hereby disclaims any duty to update any forward-looking statements to reflect subsequent events or circumstances.

PART I

|

ITEM 1. |

BUSINESS |

Our Company

We are a customer-centric company that positions itself as a value-added, trusted partner in developing superior image solutions through our lighting, graphics, and technology capabilities. Our products and services include digital signage, screen graphics, and structural graphics capabilities, a wide variety of high quality indoor and outdoor lighting products, lighting control systems, and related professional services including engineering, installation, and project management. We also provide graphics and lighting products on a stand-alone basis. Our company is the leading provider of corporate visual image solutions to the petroleum / convenience store industry. We use this leadership position to penetrate national retailers and multi-site retailers, including quick service and casual restaurants, retail chain stores and automobile dealerships, located primarily in the United States as well as internationally. We seek to expand our market share in the traditional commercial / industrial lighting market by combining our LED product innovation and lighting control solutions utilizing the latest technology along with a strong emphasis on high service levels and market focused solutions. Our solutions are targeted at both renovation and new construction markets. We design and develop most aspects of the solid-state LED lighting, from the electronic circuit board, to the software to drive and control the LEDs, to the structure of the LED product. We also provide a variety of lighting control solutions which allow our customers to reduce energy and maintenance costs. In addition to designing and producing screen graphics and structural graphics, we design and produce most aspects of our digital signage offering where customers are provided a turnkey solution that includes design, software, hardware content development, implementation, service and support.

We believe that national retailers and other companies in the markets we serve are increasingly seeking single-source suppliers with the project management skills and service expertise necessary to execute a comprehensive visual image program. The integration of our graphics, lighting, and technology coupled with our professional services capabilities allows our customers to outsource to us the development of an entire visual image program from the planning and design stage through installation. Our approach is to combine our lighting products and custom graphics applications utilizing the latest technology along with our professional service capabilities to create complete customer-focused visual image solutions. We also offer our lighting products and graphics elements on a stand-alone basis to service our existing image solutions customers, to establish a presence in a new market or to create a relationship with a new customer. We believe that our ability to combine lighting, graphics, and technology coupled with professional services into a comprehensive visual image solution differentiates us from our competitors who offer only stand-alone products for lighting or graphics and who lack professional services offerings. During the past several years, we have continued to enhance our ability to provide comprehensive corporate visual image solutions by adding additional graphics capabilities such as digital signage and media content management, wireless lighting control systems, new and innovative LED lighting products and professional services through acquisitions and internal development.

Our focus on product development and innovation creates products that are essential components of our customers’ corporate visual image strategy. Our spending on research and development was $5.5 million in fiscal 2016 and $5.6 million in fiscal 2015, and $8.2 million in fiscal 2014. We develop and manufacture lighting including solid-state LED lighting, lighting control systems, and graphics and distribute them through an extensive multi-channel distribution network that allows us to effectively service our target markets. Representative customers include BP, Chevron Texaco, 7-Eleven, ExxonMobil, Shell, Burger King, Dairy Queen, Taco Bell, Wendy’s, Best Buy, CVS Caremark, Phillips 66, Target Stores, Wal-Mart Stores, Chrysler, Ford, General Motors, Nissan, and Toyota. We service our customers at the corporate, franchise and local levels.

We also focus on the elimination of non-value added activities throughout our organization through the LSI Business System, a Lean Management System utilizing kaizen events and lean tools to drive continuous improvement in our processes. The LSI Business System improves shareholder value by increasing customer satisfaction and eliminating waste, both of which will improve the bottom line. We are committed to this company-wide initiative through employee education and training with the ultimate goal to make it part of the corporate culture and way of thinking of all employees.

Our business is organized as follows: the Lighting Segment, which represented 70% of our fiscal 2016 net sales; the Graphics Segment, which represented 24% of our fiscal 2016 net sales; and the Technology Segment, which represented 6% of our fiscal 2016 net sales. See Note 2 of Notes to Consolidated Financial Statements beginning on page 46 of this Form 10-K for additional information on business segments. Net sales by segment are as follows (in thousands):

|

2016 |

2015 |

2014 |

||||||||||

|

Lighting Segment |

$ | 226,889 | $ | 219,920 | $ | 222,604 | ||||||

|

Graphics Segment |

77,039 | 64,895 | 50,970 | |||||||||

|

Technology Segment |

18,268 | 23,001 | 24,515 | |||||||||

|

All Other Category |

-- | 41 | 1,374 | |||||||||

|

Total Net Sales |

$ | 322,196 | $ | 307,857 | $ | 299,463 | ||||||

Lighting Segment

Our Lighting Segment manufactures and markets outdoor and indoor lighting and lighting controls for the commercial, industrial and multi-site retail markets including the petroleum / convenience store, quick-service, and automotive markets. Our products are designed and manufactured to provide maximum value and meet the high-quality, competitively-priced product requirements of the markets we serve. We generally avoid specialty or custom-designed, low-volume products for single order opportunities. Our concentration is on our high-volume, standard product lines that meet our customers’ needs. By focusing our product offerings, we achieve significant manufacturing and cost efficiencies.

Our lighting fixtures, poles and brackets are produced in a variety of designs, styles and finishes. Important functional variations include types of mounting, such as pole, bracket and surface, and the nature of the light requirement, such as interior and exterior down-lighting, wall-wash lighting, canopy lighting, flood-lighting, area lighting and security lighting. Our engineering staff performs photometric analyses and wind load safety studies for all light fixtures and also designs our fixtures and lighting systems. Our lighting products utilize a variety of different light sources, with the primary light source being solid-state LED, along with high-intensity discharge and fluorescent. The major products and services offered within our lighting segment include: exterior area lighting, interior lighting, canopy lighting, landscape lighting, lighting controls, light poles, lighting system design, and photometric layouts. All of our products are designed for performance, reliability, ease of installation and service, as well as attractive appearance. The Company also has a focus on designing lighting system solutions and implementing strategies related to energy savings in substantially all markets served.

We offer our customers expertise in developing and utilizing high-performance solid-state LED solutions, which when combined with the Company’s lighting fixture expertise and technology, has the potential to result in a broad spectrum of white light LED fixtures that offer equivalent or improved lighting performance with significant energy and maintenance savings as compared to the present metal halide and fluorescent lighting fixtures.

Lighting Segment net sales of $226,889,000 in fiscal 2016 increased 3.2% from fiscal 2015 net sales of $219,920,000. The Lighting Segment’s net sales of light fixtures having solid-state LED technology totaled $155.5 million in fiscal 2016 (68.5% of total lighting net sales), representing a $24.1 million or 18.4% increase from fiscal 2015 net sales of solid-state LED light fixtures of $131.3 million (59.7% of total lighting net sales). There was a reduction in the Company’s traditional lighting sales (metal halide and fluorescent light sources) from fiscal 2015 to fiscal 2016 as customers converted from traditional lighting to light fixtures having solid-state LED technology.

Graphics Segment

Our Graphics Segment manufactures and sells exterior and interior visual image elements related to signage and graphics, including integrated digital solutions. These products are used in graphics displays and visual image programs in several markets, including the petroleum / convenience store market and multi-site retail operations. Our extensive lighting and graphics expertise, product offering, visual image solution implementation capabilities and other professional services represent significant competitive advantages. We work with corporations and design firms to establish and implement cost effective corporate visual image programs to advance our customer’s brand. Increasingly, we have become the primary supplier of exterior and interior graphics for our customers. We also offer installation management services for those customers who require the installation of interior or exterior products (utilizing pre-qualified independent subcontractors throughout the United States).

Our business can be significantly impacted by participation in a customer’s “image conversion program,” especially if it were to involve a “roll out” of that new image to a significant number of that customer’s and its franchisees’ retail sites. The impact to our business can be very positive with growth in net sales and profitability when we are engaged in an image conversion program. This can be followed in subsequent periods by lesser amounts of business or negative comparisons following completion of an image conversion program, unless we are successful in replacing that completed business with participation in new image conversion programs of similar size with one or more customers. An image conversion program can potentially involve any or all of the following improvements, changes or refurbishments at a customer’s retail site: interior or exterior lighting (see discussion above about our lighting segment), interior or exterior store signage and graphics, and installation of these products in both the prototype and roll out phases of their program.

The major products and services offered within our Graphics Segment include the following: signage and canopy graphics, pump dispenser graphics, building fascia graphics and ACM systems, decals, interior signage and marketing graphics, aisle markers, wall mural graphics, fleet graphics, prototype program graphics, and digital signage and media content management. Our Company also manages and executes the implementation of large rollout programs.

Graphics Segment net sales of $77,039,000 in fiscal 2016 increased $12.1 million or 18.7% from fiscal 2015 net sales of $64,895,000. The $12.1 million increase in Graphics Segment net sales is primarily the net result of sales to the petroleum / convenience store market ($16.9 million net increase), sales to the national drug store market ($0.8 million decrease), sales to the quick-service restaurant market ($4.0 million net decrease), sales to the banking industry ($0.4 million decrease), sales to the retail grocery market ($1.7 million increase), and changes in volume to several other markets ($1.3 million decrease). The Graphics Segment net sales of graphic identification products that contain solid-state LED light sources and LED lighting for signage totaled $2.7 million in fiscal 2016, representing a $1.3 million increase from fiscal 2015 net sales of $1.4 million.

Technology Segment

Our Technology Segment designs, engineers, and manufactures electronic circuit boards, assemblies, lighting controls and large format solid state LED video displays. Applications for these products include, but are not limited to, OEM, transportation, commercial, industrial, entertainment, sports, and medical markets. This segment also has significant inter-segment sales to the Lighting Segment to support that segment’s customer sales of solid-state LED lighting and lighting controls.

Technology Segment net customer sales of $18,268,000 in fiscal 2016 decreased 20.6% from fiscal 2015 net sales of $23,001,000. The $4.7 million decrease in Technology Segment net sales is primarily the net result of a $2.4 million decrease in sales to the transportation market, a $0.3 million decrease in sales to original equipment manufacturers, a $0.8 million decrease in sales to the medical markets, a $1.3 million decrease in sales to the sports market, and a $0.1 million net increase in sales to various other markets. The decrease in net customer sales is due to the cyclic nature of the markets the Company serves in this segment. While net customer sales decreased, the Technology Segment inter-segment sales increased $6.3 million or 21.5%. The increase in inter-segment sales is the direct result of the Lighting Segment’s increase in net sales of light fixtures having solid-state LED technology along with light fixtures with integrated controls. The Technology Segment’s intercompany support of electronic circuit boards and lighting control systems to the Lighting Segment is core to the strategic growth of the Company. The Technology Segment’s net sales of LED video screens were $0.7 million in fiscal 2016 compared to $2.3 million net sales of video screens in fiscal 2015.

Goodwill and Intangible Asset Impairment

There was no impairment of the Company’s goodwill or indefinite-lived intangible assets in fiscal 2016 or 2015.

Our Competitive Strengths

Single Source Comprehensive Visual Image Solution Provider. We believe that we are the only company serving our target markets that combines significant graphics capabilities, lighting products and installation implementation capabilities to create comprehensive image solutions. We believe that our position as a single-source provider creates a competitive advantage over competitors who can only address either the lighting or the graphics component of a customer’s corporate visual image program. Using our broad visual image solutions capabilities, our customers can maintain complete control over the creation of their visual image programs while avoiding the added complexity of coordinating separate lighting and graphics suppliers and service providers. We can use high technology software to produce computer-generated virtual prototypes of a customer’s new or improved retail site image. We believe that these capabilities are unique to our target markets and they allow our customers to make educated, cost-effective decisions quickly.

Proven Ability to Penetrate Target Markets. We have grown our business by establishing a leadership position in many of the markets we serve, including petroleum / convenience stores, automobile dealerships and specialty retailers. Although our relationship with our customers may begin with the need for a single product or service, we leverage our broad product and service offering to identify additional products and solutions. We promote the combination of graphics, lighting, and technology, along with image element offerings, and services to create comprehensive solutions for our customers.

Focus on Product Innovation. We believe that our ability to successfully identify, develop and patent new products has allowed us to expand our market opportunity and enhance our market position. Our product innovation initiatives are designed to increase the value of our product offering by addressing the needs of our customers and target markets through retrofit enhancements to existing products or the development of new products. New product development includes developing an expanding portfolio of technology patents related to the design of LED based products. We believe our product innovation process creates value for our customers by producing products that offer energy efficiency, low maintenance requirements and long-term operating performance at competitive prices based upon the latest technologies available.

Strong Relationships with our Customers. We have used our innovative products and high-quality services to develop close, long-standing relationships with a large number of our customers. Many of our customers are recognized among the leaders in their respective markets, including customers such as Wal-Mart, BP, Phillips 66, Exxon Mobil, Carmax, Chevron, CVS Caremark, Stop & Shop, and Burger King. Their use of our products and services raises the visibility of our capabilities and facilitates the acceptance of our products and services in their markets. Within each of these markets, our ability to be a single source provider of image solutions often creates repeat business opportunities through corporate reimaging programs. We have served some of our customers since our inception in 1976.

Well-capitalized Balance Sheet. As part of our long-term operating strategy, we believe the Company maintains a conservative capital structure. With a strong equity base, we are able to preserve operating flexibility in times of industry expansion and contraction. In the current business environment, a strong balance sheet demonstrates financial viability to our existing and targeted customers. In addition, a strong balance sheet enables us to invest in the company through research and development and allows the Company to invest in capital projects that support the Company’s growth.

Aggressive Use of Our Marketing Center. The capabilities of our Image Center, Innovation Center, Inspiration Center and, I-Zone Marketing Center provide us with a distinct competitive advantage to demonstrate the effectiveness of integrating graphics, lighting, and technology into a complete corporate visual image program. These four centers, which demonstrate the depth and breadth of our product and service offerings, have become an effective component of our sales process.

Maintain our Vertically Integrated Business Model. We consider our Company to be a vertically integrated manufacturer rather than just a product assembler. We focus on developing lighting and graphics products coupled with technology, and outsource certain non-core processes and product components as necessary.

Commitment to Continuous Improvement. We are committed to a philosophy of continuous improvement through the LSI’s Business System which is a Lean Management System utilizing Kaizen events and lean tools to identify and eliminate waste and increase customer satisfaction with the ultimate goal to improve shareholder value.

Sales, Marketing and Customers

Sales: Our lighting products including lighting controls, are sold primarily throughout the United States, but also in Canada, Australia, and Latin America (about 5.9% of consolidated net sales are outside the United States) using a combination of regional sales managers and independent sales representatives exclusively serving primarily the commercial / industrial market along with several of the other markets we serve. Although in some cases we sell directly to national accounts, more frequently we are designated as a preferred vendor for product sales to customer-owned as well as franchised, licensed and dealer operations. Our graphics products, which in many instances are program-driven, are sold primarily through our own sales force. Our marketing approach and means of distribution vary by product line and by type of market.

Sales are developed through a wide variety of contacts such as, but not limited to, national retail marketers, branded product companies, franchise and dealer operations. In addition, sales are also achieved through recommendations from local architects, engineers, petroleum and electrical distributors and contractors. The Company utilizes the latest technology to track sales leads and customer quotes with the ultimate goals to turn these into orders from our customers. Our sales are partially seasonal as installation of outdoor lighting and graphic systems in the northern states decreases during the winter months.

Marketing: The capabilities of our Image Center, Innovation Center, Inspiration Center, and iZone Marketing Center are important parts of our sales process. These four centers, unique within the lighting and graphics industry, are facilities that can produce a computer-generated virtual prototype of a customer’s facility on a large screen through the combination of high technology software and audio/visual presentation. The i-Zone marketing center is a digitally controlled facility containing a large solid-state LED video screen and several displays that showcase our LED technology and LED products. With these capabilities, our customers can instantly explore a wide variety of lighting and graphics alternatives to develop consistent day and nighttime images. These centers give our customers more options, greater control, and more effective time utilization in the development of lighting, graphics and visual image solutions, all with much less expense than traditional prototyping. In addition to being cost and time effective for our customers, we believe that the capabilities of these marketing centers capabilities result in the best solution for our customers’ needs.

The Image and iZone marketing centers also contain comprehensive indoor and outdoor product display areas that allow our customers to see many of our products and services in one setting. This aids our customers in making quick and effective lighting and graphic design decisions through hands-on product demonstrations and side-by-side comparisons. More importantly, these capabilities allow us to expand our customer’s interest from just a single product into other products and solutions. We believe that the capabilities of these centers have further enhanced our position as a highly qualified outsourcing partner capable of guiding a customer through image alternatives utilizing our lighting and graphics products and services. We believe this capability distinguishes us from our competitors and will become increasingly beneficial in attracting additional customers.

In addition to the capabilities of our Image Center, Innovation Center, Inspiration Center, and iZone Marketing Center, the Company markets its products and service capabilities to end users in multiple channels through a broad spectrum of marketing and promotional methods, including direct customer contact, trade shows, on-site training, print advertising in industry publications, product brochures and other literature, as well as the internet and social media.

Manufacturing and Operations

We design, engineer and manufacture substantially all of our lighting and graphics products through a vertically integrated business model. By emphasizing high-volume production of standard product lines, we achieve significant manufacturing efficiencies. We periodically invest in new machinery and equipment utilizing the latest technology in order to leverage the manufacturing efficiencies gained from our high-volume production. When appropriate, we utilize alliances with domestic and international vendors to outsource certain products and components. LED products and related software are engineered, designed and final-assembled by the Company, while a portion of the manufacturing has been performed by select qualified vendors. We are not dependent on any one supplier for any of our component parts.

The principal raw materials and purchased components used in the manufacturing of our products are steel, aluminum, castings, fabrications, LEDs, power supplies, powder paint, steel and aluminum poles, wire harnesses, acrylic and glass lenses, inks, various graphics substrates such as foam board and vinyls, and digital screens. We source these materials and components from a variety of suppliers. Although an interruption of these supplies and components could disrupt our operations, we believe generally that alternative sources of supply exist and could be readily arranged. We strive to reduce price volatility in our purchases of raw materials and components through annual contracts with strategic suppliers. Our Lighting operations generally carry a certain level of sub-assemblies in inventory and relatively small amounts of finished goods inventory, except for certain products that are stocked to meet quick delivery requirements. Most often, lighting products are made to order and shipped shortly after they are manufactured. Our Graphics operations manufacture custom graphics products for customers who require us to stock certain amounts of finished goods in exchange for their commitment to that inventory. In some Graphics programs, customers also give us a cash advance for the inventory that we stock for them. The Company’s operations dealing with LED products generally carry LED and LED component inventory due to longer lead times. Our Technology Segment operations purchase electronic components from multiple suppliers and manufacture custom electronic circuit boards and lighting control systems. Most products are made to order and, as a result, these operations do not carry very many finished goods.

We currently operate out of ten manufacturing facilities and two sales/service/technology facilities in eight U.S. states.

Our Lighting Business operations received ISO 9001:2015 Certification thru ANAB (Cert# 5369-Eagle Registrations Inc.), with plans to seek additional certifications in future years. Our manufacturing operations are subject to various federal, state and local regulatory requirements relating to environmental protection and occupational health and safety. We do not expect to incur material capital expenditures with regard to these matters and believe our facilities are in compliance with such regulations.

Competition

We experience strong competition in all segments of our business, and in all markets served by our product lines. Although we have many competitors, some of which have greater financial and other resources, we do not compete with the same companies across our entire product and service offerings. We believe product quality and performance, price, customer service, prompt delivery, and reputation to be important competitive factors. We also have several product and process patents which have been obtained in the normal course of business which provide a competitive advantage in the marketplace.

Additional Information

Our sales are partially seasonal as installation of outdoor lighting and graphic systems in the northern states lessens during the harshest winter months. We had a backlog of orders, which we believe to be firm, of $29.1 million and $33.8 million at June 30, 2016 and 2015, respectively. All orders are expected to be shippable or installed within twelve months.

We have 1,292 full-time employees and 186 agency employees as of June 30, 2016. We offer a comprehensive compensation and benefits program to most employees, including competitive wages, a cash-based incentive plan that is based upon the achievement of the Company’s business plan goals, a profit-sharing plan and retirement plan, and a 401(k) savings plan, a nonqualified deferred compensation plan (for certain employees), an equity compensation plan, and medical and dental insurance.

We file reports with the Securities and Exchange Commission (“SEC”) on Forms 10-K, 10-Q and 8-K. You may read and copy any materials filed with the SEC at its public reference room at 100 F. Street, N.E., Room 1580, Washington, D.C. 20549. You may also obtain that information by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet website that contains reports, proxy and information statements and other information regarding us. The address of that site is http://www.sec.gov. Our internet address is http://www.lsi-industries.com. We make available free of charge through our internet website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practical after we electronically file them with the SEC. LSI is not including the other information contained on its website as part of or incorporating it by reference into this Annual Report on Form 10-K.

LSI Industries Inc. is an Ohio corporation, incorporated in 1976.

|

ITEM 1A. |

RISK FACTORS |

In addition to the other information set forth in this report, you should carefully consider the following factors which could materially affect our business, financial condition, cash flows or future results. Any one of these factors could cause the Company’s actual results to vary materially from recent results or from anticipated future results. The risks described below are not the only risks facing our Company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results.

The markets in which we operate are subject to competitive pressures that could affect selling prices, and therefore could adversely affect our operating results.

Our businesses operate in markets that are highly competitive, and we compete on the basis of price, quality, service and/or brand name across the industries and markets served. Some of our competitors for certain products, primarily in the Lighting Segment, have greater sales, assets and financial resources. Some of our competitors are based in foreign countries and have cost structures and prices in foreign currencies. Accordingly, currency fluctuations could cause our U.S. dollar-priced products to be less competitive than our competitors’ products which are priced in other currencies. Competitive pressures could affect prices we charge our customers or demand for our products, which could adversely affect our operating results. Additionally, customers for our products may attempt to reduce the number of vendors from which they purchase in order to reduce the size and diversity of their inventories and their transaction costs. To remain competitive, we will need to invest continuously in research and development, manufacturing, marketing, customer service and support, and our distribution networks. We may not have sufficient resources to continue to make such investments and we may be unable to maintain our competitive position.

Lower levels of economic activity in our end markets could adversely affect our operating results.

Our businesses operate in several market segments including, but not limited to, commercial, industrial, retail, petroleum / convenience store and automotive. Operating results can be negatively impacted by volatility in these markets. Future downturns in any of the markets we serve could adversely affect our overall sales and profitability.

Our operating results may be adversely affected by unfavorable economic, political and market conditions.

Economic and political conditions worldwide have from time to time contributed to slowdowns in our industry at large, as well as to the specific segments and markets in which we operate. When combined with ongoing customer consolidation activity and periodic manufacturing and inventory initiatives, an uncertain macro-economic and political climate, including but not limited to the effects of possible weakness in domestic and foreign financial and credit markets, could lead to reduced demand from our customers and increased price competition for our products, increased risk of excess and obsolete inventories and uncollectible receivables, and higher overhead costs as a percentage of revenue. If the markets in which we participate experience further economic downturns, as well as a slow recovery period, this could negatively impact our sales and revenue generation, margins and operating expenses, and consequently have a material adverse effect on our business, financial condition and results of operations.

Price increases or significant shortages of raw materials and components could adversely affect our operating margin.

The Company purchases large quantities of raw materials and components — mainly steel, aluminum, light bulbs and fluorescent tubes, lighting ballasts, sockets, wire harnesses, plastic lenses, glass lenses, vinyls, inks, LEDs, electronic components and corrugated cartons. Materials comprise the largest component of costs, representing approximately 58% and 59% of the cost of sales in 2016 and 2015, respectively. While we have multiple sources of supply for most of our material requirements, significant shortages could disrupt the supply of raw materials. Further increases in the price of these raw materials and components could further increase the Company’s operating costs and materially adversely affect margins. Although the Company attempts to pass along increased costs in the form of price increases to customers, the Company may be unsuccessful in doing so for competitive reasons. Even when price increases are successful, the timing of such price increases may lag significantly behind the incurrence of higher costs. On occasion, there are selected electronic component parts and certain other parts shortages in the market place, some of which have affected the Company’s manufacturing operations and shipment schedules even though multiple suppliers may be available. The lead times of these suppliers can increase and the prices of some of these parts have increased during periods of shortages. Fluorescent tubes and other light bulbs contain rare earth minerals, which have become more expensive and in short supply throughout the world, thereby affecting the Company’s supply and cost of these light sources.

We have a concentration of net sales to the petroleum / convenience store market, and any substantial change in this market could have an adverse affect on our business.

Approximately 35% of our net sales in fiscal year 2016 are concentrated in the petroleum / convenience store market. Sales to this market segment are dependent upon the general conditions prevailing in and the profitability of the petroleum and convenience store industries and general market conditions. Our petroleum market business can be subject to reactions by the petroleum industry to world political events, particularly those in the Middle East, and to the price and supply of oil. Major disruptions in the petroleum industry generally result in a curtailment of retail marketing efforts, including expansion and refurbishing of retail outlets, by the petroleum industry and adversely affect our business. Any substantial change in purchasing decisions by one or more of our larger customers whether due to actions by our competitors, customer financial constraints, industry factors or otherwise, could have an adverse effect on our business.

Difficulties with integrating acquisitions could adversely affect operating costs and expected benefits from those acquisitions.

We have pursued and may continue to seek potential acquisitions to complement and expand our existing businesses, increase our revenues and profitability, and expand our markets. We cannot be certain that we will be able to identify, acquire or profitably manage additional companies or successfully integrate such additional companies without substantial costs, delays or other problems. Also, companies acquired recently and in the future may not achieve revenues, profitability or cash flows that justify our investment in them. We expect to spend significant time and effort in expanding our existing businesses and identifying, completing and integrating acquisitions. We expect to face competition for acquisition candidates which may limit the number of acquisition opportunities available to us, possibly leading to a decrease in the rate of growth of our revenues and profitability, and may result in higher acquisition prices. The success of these acquisitions we do make will depend on our ability to integrate these businesses into our operations. We may encounter difficulties in integrating acquisitions into our operations, retaining key employees of acquired companies and in managing strategic investments. Therefore, we may not realize the degree or timing of the benefits anticipated when we first enter into a transaction.

Goodwill and intangible assets that are recorded on the balance sheet from a previous or future acquisition could be written off if circumstances arise whereby the goodwill or intangible assets have been impaired.

We have pursued and will continue to seek potential acquisitions, at the appropriate time, to complement and expand our existing businesses, increase our revenues and profitability, and expand our markets through acquisitions. As a result of acquisitions, we have significant goodwill and intangible assets recorded on our balance sheet. We will continue to evaluate the recoverability of the carrying amount of our goodwill and intangible assets on an ongoing basis, and we may incur substantial non-cash impairment charges, which would adversely affect our financial results. There can be no assurance that the outcome of such reviews in the future will not result in substantial impairment charges. Impairment assessment inherently involves judgment as to assumptions about expected future cash flows and the impact of market conditions on those assumptions. Future events and changing market conditions may impact our assumptions as to prices, costs, holding periods or other factors that may result in changes in our estimates of future cash flows. Although we believe the assumptions we used in testing for impairment are reasonable, significant changes in any one of our assumptions could produce a significantly different result. If there were to be a decline in our market capitalization and a decline in estimated forecasted discounted cash flows, there could be an impairment of the goodwill and intangible assets. A non-cash impairment charge could be material to the earnings of the reporting period in which it is recorded.

If we do not develop the appropriate new products or if customers do not accept new products, we could experience a loss of competitive position which could adversely affect future revenues.

The Company is committed to product innovation on a timely basis to meet customer demands. Development of new products for targeted markets requires the Company to develop or otherwise leverage leading technologies in a cost-effective and timely manner. Failure to meet these changing demands could result in a loss of competitive position and seriously impact future revenues. Products or technologies developed by others may render the Company’s products or technologies obsolete or noncompetitive. A fundamental shift in technologies in key product markets could have a material adverse effect on the Company’s operating results and competitive position within the industry. More specifically, the development of new or enhanced products is a complex and uncertain process requiring the anticipation of technological and market trends. Rapidly changing product technologies could adversely impact operating results due to potential technological obsolescence of certain inventories or increased warranty expense related to newly developed LED lighting products. We may experience design, manufacturing, marketing or other difficulties, such as an inability to attract a sufficient number of experienced engineers that could delay or prevent our development, introduction or marketing of new products or enhancements and result in unexpected expenses. Such difficulties could cause us to lose business from our customers and could adversely affect our competitive position. In addition, added expenses could decrease the profitability associated with those products that do not gain market acceptance.

Our business is cyclical and seasonal, and in downward economic cycles our operating profits and cash flows could be adversely affected.

Historically, sales of our products have been subject to cyclical variations caused by changes in general economic conditions. Our revenues in our third quarter ending March 31 are also affected by the impact of weather on construction and installation programs and the annual budget cycles of major customers. The demand for our products reflects the capital investment decisions of our customers, which depend upon the general economic conditions of the markets that our customers serve, including, particularly, the petroleum and convenience store industries. During periods of expansion in construction and industrial activity, we generally have benefited from increased demand for our products. Conversely, downward economic cycles in these industries result in reductions in sales and pricing of our products, which may reduce our profits and cash flow. During economic downturns, customers also tend to delay purchases of new products. The cyclical and seasonal nature of our business could at times adversely affect our liquidity and financial results.

A loss of key personnel or inability to attract qualified personnel could have an adverse affect on our operating results.

The Company’s future success depends on the ability to attract and retain highly skilled technical, managerial, marketing and finance personnel, and, to a significant extent, upon the efforts and abilities of senior management. The Company’s management philosophy of cost-control results in a lean workforce. Future success of the Company will depend on, among other factors, the ability to attract and retain other qualified personnel, particularly management, research and development engineers and technical sales professionals. The loss of the services of any key employees or the failure to attract or retain other qualified personnel could have a material adverse effect on the Company’s results of operations.

The costs of litigation and compliance with environmental regulations, if significantly increased, could have an adverse affect on our operating profits.

We are, and may in the future be, a party to any number of legal proceedings and claims, including those involving patent litigation, product liability, employment matters, and environmental matters, which could be significant. Given the inherent uncertainty of litigation, we can offer no assurance that existing litigation or a future adverse development will not have a material adverse impact. We are also subject to various laws and regulations relating to environmental protection and the discharge of materials into the environment, and it could potentially be possible we could incur substantial costs as a result of the noncompliance with or liability for clean up or other costs or damages under environmental laws.

Regulations related to conflict minerals could adversely impact our business.

The Dodd-Frank Wall Street Reform and Consumer Protection Act contains provisions to improve transparency and accountability concerning the supply of certain minerals, known as conflict minerals, originating from the Democratic Republic of Congo (DRC) and adjoining countries. As a result, the SEC adopted annual disclosure and reporting requirements for those companies who use conflict minerals mined from the DRC and adjoining countries in their products. We incurred certain costs associated with complying with these disclosure requirements, including the due diligence to determine the sources of conflict minerals used in our products. Ongoing compliance with these rules could adversely affect the sourcing, supply and pricing of materials used in our products. As there may be only a limited number of suppliers offering “conflict free" conflict minerals, we cannot be sure that we will be able to obtain necessary conflict minerals from such suppliers in sufficient quantities or at competitive prices. Also, we may face reputational challenges if we determine that certain of our products contain minerals that are not conflict free or if we are unable to sufficiently verify the origins for all conflict minerals used in our products through the procedures we have already implemented or may implement.

The turnover of commissioned sales representatives could cause a significant disruption in sales volume.

Commissioned sales representatives are critical to generating business in the Lighting Segment. From time to time, commissioned sales representatives representing a particular region resign or are terminated and replaced with new commissioned sales representatives. During this period of transition from the previous agency to the new one, sales in the particular region will likely fall as business is disrupted. It may take several months for the new sales representative to generate sales that will equal or exceed the previous sales representative. There is also the risk that the new sales agency will not attain the sales volume of the previous agency. These sales representative changes may occur individually as one agency is replaced due to lack of performance. On the other hand, these sales representative changes can be widespread as a result of the competitive nature of the lighting industry as LSI and its competition vie for the strongest sales agency in a particular region.

Changes in a customer’s demands and commitment to proprietary inventory could result in significant inventory write-offs.

Upgrading or replacing a customer’s current image requires the manufacture of inventory that is specific to the particular customer. This is particularly true in the Graphics Segment. In as many instances as possible, we require a commitment from the customer before the inventory is produced. Our request for a commitment can range from a single site or store to a large roll-out program involving many sites or stores. The risk does exist that a customer cannot or will not honor its commitment to us. The reasons a customer cannot or will not honor its commitment can range from the bankruptcy of the customer, to the change in the image during the roll-out program, to canceling the program before its completion and before the inventory is sold to the customer. In each of these instances, we could be left with significant amounts of inventory required to support the customer’s re-imaging. While all efforts are made to hold the customer accountable for its commitment, there is the risk that a significant amount of inventory could be deemed obsolete or no longer usable which could result in significant inventory write-offs.

If we are unable to adequately protect our intellectual property, we may lose some of our competitive advantage.

Our success is determined in part by our ability to obtain United States and foreign patent protection for our technology and to preserve our trade secrets. Our ability to compete and the ability of our business to grow could suffer if our intellectual property rights are not adequately protected. There can be no assurance that our patent applications will result in patents being issued or that current or additional patents will afford protection against competitors. We rely on a combination of patents, copyrights, trademarks and trade secret protection and contractual rights to establish and protect our intellectual property. Failure of our patents, copyrights, trademarks and trade secret protection, non-disclosure agreements and other measures to provide protection of our technology and our intellectual property rights could enable our competitors to more effectively compete with us and have an adverse effect on our business, financial condition and results of operations. In addition, our trade secrets and proprietary know-how may otherwise become known or be independently discovered by others. No guarantee can be given that others will not independently develop substantially equivalent proprietary information or techniques, or otherwise gain access to our proprietary technology.

Sudden or unexpected changes in a customer’s creditworthiness could result in significant accounts receivable write-offs.

The Company takes a conservative approach when extending credit to its customers. Customers are granted an appropriate credit limit based upon the due diligence performed on the customer which includes, among other things, the review of the company’s financial statements and banking information, various credit checks, payment history the customer has with the Company. At any given time, the Company can have a significant amount of credit exposure with its larger customers. While the Company is frequently monitoring its outstanding receivables with its customers, the likelihood does exist that a customer with large credit exposure is unable to make payment on its outstanding receivables which could result in a significant write-off of accounts receivable.

Failure of the Company’s operating or information system or a compromise of security with respect to its operating system or portable electronic devices could adversely affect the Company’s results of operations and financial condition or the effectiveness of internal controls over operations and financial reporting.

Information technology system failures, network disruptions and breaches of data security caused by such factors, including, but not limited to, earthquakes, fire, theft, fraud, malicious attack or other causes could disrupt the Company’s operations by causing delays or cancellation of customer orders, negatively affecting the Company’s online offerings and services, impeding the manufacture or shipment of products, processing transactions and reporting financial results, resulting in the unintentional disclosure of customer or Company information, or damage to the Company’s reputation. While management has taken steps to address these concerns by implementing network security and internal control measures, there can be no assurance that a system failure or loss or data security breach will not materially adversely affect the Company’s financial condition and operating results.

|

ITEM 1B. |

UNRESOLVED STAFF COMMENTS |

None.

|

ITEM 2. |

PROPERTIES |

The Company has twelve facilities:

|

Description |

|

Size |

|

Location |

|

Status | ||

|

|

|

|

|

|

|

|

|

|

|

1) |

|

LSI Industries Corporate Headquarters and lighting fixture manufacturing |

|

243,000 sq. ft. (includes 66,000 sq. ft. of office space) |

|

Cincinnati, OH |

|

Owned |

|

|

|

|

|

|

|

|

|

|

|

2) |

|

LSI Industries pole manufacturing and dry powder-coat painting |

|

122,000 sq. ft. |

|

Cincinnati, OH |

|

Owned |

|

|

|

|

|

|

|

|

|

|

|

3) |

LSI Industries technology center |

9,000 sq. ft. |

Cincinnati, OH |

Leased | ||||

|

4) |

LSI Industries lighting assembly |

12,000 sq. ft. |

Hawthorne, CA |

Leased | ||||||

|

5) |

|

LSI Metal Fabrication and LSI Images manufacturing and dry powder-coat painting |

|

96,000 sq. ft. (includes 5,000 sq. ft. of office space) |

Independence, KY |

|

Owned | |||

|

6) |

LSI Integrated Graphics office; screen printing manufacturing; and architectural graphics manufacturing |

141,000 sq. ft. (includes 34,000 sq. ft. of office space) |

Houston, TX |

Leased | ||||||

|

7) |

Grady McCauley office and manufacturing |

212,000 sq. ft. (includes 20,000 sq. ft. of office space) |

North Canton, OH |

Owned | ||||||

|

8) |

LSI MidWest Lighting office and manufacturing |

138,000 sq. ft. (includes 6,000 sq. ft. of office space) |

Kansas City, KS |

Owned | ||||||

|

9) |

LSI Retail Graphics office and manufacturing |

33,000 sq. ft. (includes 5,000 sq. ft. of office space) |

Woonsocket, RI |

Owned | ||||||

|

10) |

LSI Lightron office and manufacturing |

170,000 sq. ft. (includes 10,000 sq. ft. of office space) |

New Windsor, NY |

Owned and Leased (a) | ||||||

|

11) |

LSI Adapt offices |

2,000 sq. ft. |

North Canton, OH |

Owned | ||||||

| Pineville, NC | Leased | |||||||||

|

12) |

LSI ADL Technology office and manufacturing |

57,000 sq. ft. (includes 5,000 sq. ft. of office space) |

Columbus, OH |

Owned | ||||||

|

|

(a) |

The land at this facility is leased and the building is owned. |

The Company considers these facilities (total of 1,235,000 square feet) adequate for its current level of operations.

|

ITEM 3. |

LEGAL PROCEEDINGS |

Nothing to report.

|

ITEM 4. |

MINE SAFETY DISCLOSURES |

None.

PART II

|

ITEM 5. |

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

|

|

(a) |

Common share information appears in Note 17 — SUMMARY OF QUARTERLY RESULTS (UNAUDITED) under “Range of share prices” beginning on page 63 of this Form 10-K. Information related to “Earnings (loss) per share” and “Cash dividends paid per share” appears in SELECTED FINANCIAL DATA on page 64 of this Form 10-K. LSI’s shares of common stock are traded on the NASDAQ Global Select Market under the symbol “LYTS.” |

The Company’s Board of Directors has adopted a dividend policy which indicates that dividends will be determined by the Board of Directors in its discretion based upon its evaluation of earnings, cash flow requirements, financial condition, debt levels, stock repurchases, future business developments and opportunities, and other factors deemed relevant. The Company has paid annual cash dividends beginning in fiscal 1987 through fiscal 1994, and quarterly cash dividends since fiscal 1995. The Company’s indicated annual rate for payment of a cash dividend at the end of fiscal 2016 was $0.20 per share.

At August 27, 2016, there were 620 shareholders of record. The Company believes this represents approximately 3,000 beneficial shareholders.

|

|

(b) |

The Company does not purchase into treasury its own common shares for general purposes. However, the Company does purchase its own common shares, through a Rabbi Trust, as investments of employees/participants of the LSI Industries Inc. Nonqualified Deferred Compensation Plan. Purchases of Company common shares for this Plan in the fourth quarter of fiscal 2016 were as follows: |

ISSUER PURCHASES OF EQUITY SECURITIES

|

(d) Maximum Number |

||||||||||||||||||

|

(c) Total Number of |

(or Approximate Dollar |

|||||||||||||||||

|

(a) Total |

Shares Purchased as |

Value) of Shares that |

||||||||||||||||

|

Number of |

(b) Average |

Part of Publicly |

May Yet Be Purchased |

|||||||||||||||

|

Shares |

Price Paid |

Announced Plans or |

Under the Plans or |

|||||||||||||||

|

Period |

Purchased |

per Share |

Programs |

Programs |

||||||||||||||

| 4/1/16 |

to |

4/30/16 | — | $ | — | — | (1 | ) | ||||||||||

| 5/1/16 |

to |

5/31/16 | 2,752 | $ | 11.89 | 2,752 | (1 | ) | ||||||||||

| 6/1/16 |

to |

6/30/16 | 1,174 | $ | 11.15 | 1,174 | (1 | ) | ||||||||||

| Total | 3,926 | $ | 11.67 | 3,926 | (1 | ) | ||||||||||||

|

(1) |

|

All acquisitions of shares reflected above have been made in connection with the Company’s Nonqualified Deferred Compensation Plan, which does not contemplate a limit on shares to be acquired. |

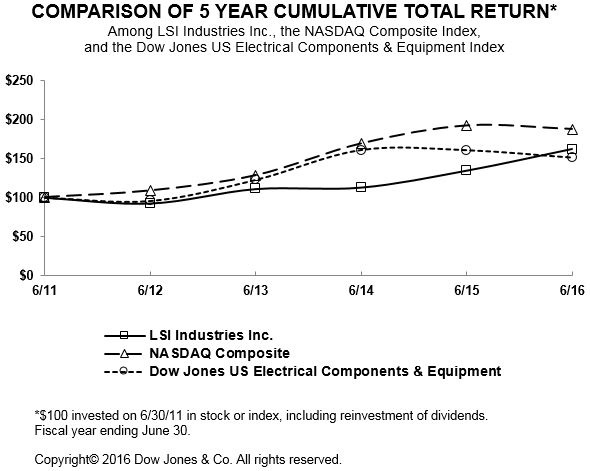

The following graph compares the cumulative total shareholder return on the Company’s common shares during the five fiscal years ended June 30, 2016 with a cumulative total return on the NASDAQ Stock Market Index (U.S. companies) and the Dow Jones Electrical Equipment Index. The comparison assumes $100 was invested June 30, 2011 in the Company’s Common Shares and in each of the indexes presented; it also assumes reinvestment of dividends.

|

|

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

|

ITEM 6. |

SELECTED FINANCIAL DATA |

“Selected Financial Data” begins on page 64 of this Form 10-K.

|

ITEM 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” appears on pages 20 through 33 of this Form 10-K.

|

ITEM 7A. |

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

The Company is exposed to market risk from changes in variable interest rates, changes in prices of raw materials and component parts, and changes in foreign currency translation rates. Each of these risks is discussed below.

Interest Rate Risk

The Company earns interest income on its cash, cash equivalents, and short-term investments (if any) and pays interest expense on its debt (if any). Because of variable interest rates, the Company is exposed to the risk of interest rate fluctuations, which impact interest income, interest expense, and cash flows. With the current balance in the Company’s short-term cash investments and absence of any outstanding variable rate debt, the adverse exposure to interest rate fluctuations has decreased considerably.

The Company’s $30,000,000 line of credit is subject to interest rate fluctuations, should the Company borrow certain amounts on this line of credit. Additionally, the Company expects to generate cash from its operations that will subsequently be used to pay down as much of the debt (if any is outstanding) as possible or invest cash in short-term investments (if no debt is outstanding), while still funding the growth of the Company.

Raw Material Price Risk

The Company purchases large quantities of raw materials and components, mainly steel, aluminum, castings, fabrications, LEDs, power supplies, powder paint, wire harnesses, plastic and glass lenses, vinyls, inks, electronic components, and corrugated cartons. The Company’s operating results could be affected by the availability and price fluctuations of these materials. The Company’s strategic sourcing plans include mitigating risk by utilizing multiple suppliers for a commodity to avoid significant dependence on any single supplier. Other than the possibility of industry-wide supply shortages, the Company has not experienced any significant supply problems in recent years. In a prior fiscal year, the Company dealt with a lengthy longshoreman’s negotiations on the west coast that caused some minor delays. Also in a prior fiscal year, the Company experienced supply shortages of certain electronic components and certain other parts which caused some production and shipment delays. Price risk for these materials is related to price increases in commodity items that affect all users of the materials, including the Company’s competitors. For the fiscal year ended June 30, 2015, the raw material component of cost of goods sold subject to price risk was approximately $138 million. The Company does not actively hedge or use derivative instruments to manage its risk in this area. The Company does, however, seek and qualify new suppliers, negotiate with existing suppliers, and arranges stocking agreements to mitigate risk of supply and price increases. On occasion, the Company’s Lighting Segment has announced price increases with customers in order to offset raw material price increases. In May 2015, the Company announced a 6% to 8% price increase for all non-LED lighting and pole products. The price increase went into effect for all orders placed on or after July 1, 2015. The Company’s Graphics Segment generally establishes new sales prices, reflective of the then current raw material prices, for each custom graphics program as it begins.

Foreign Currency Translation Risk

The Company has essentially no foreign currency risk as all operations are conducted in U.S. dollars.

|

ITEM 8. |

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA |

Index to Financial Statements

|

|

Begins | ||

|

on Page | |||

|

Financial Statements: |

|

| |

|

|

|

| |

|

Management’s Report On Internal Control Over Financial Reporting |

|

34 | |

|

|

|

| |

|

Report of Independent Registered Public Accounting Firm |

|

35 | |

|

|

|

||

|

Report of Independent Registered Public Accounting Firm |

|

36 | |

|

|

|

||

|

Consolidated Statements of Operations for the years ended June 30, 2016, 2015, and 2014 |

|

37 | |

|

|

|

||

|

Consolidated Balance Sheets at June 30, 2016 and 2015 |

|

38 | |

|

|

|

||

|

Consolidated Statements of Shareholders’ Equity for the years ended June 30, 2016, 2015, and 2014 |

|

40 | |

|

|

|

||

|

Consolidated Statements of Cash Flows for the years ended June 30, 2016, 2015, and 2014 |

|

41 | |

|

|

|

||

|

Notes to Consolidated Financial Statements |

|

42 | |

|

|

|

||

|

Financial Statement Schedules: |

|

||

|

|

|

||

|

Schedule II – Valuation and Qualifying Accounts for the years ended June 30, 2016, 2015, and 2014 |

|

65 | |

Schedules other than those listed above are omitted for the reason(s) that they are either not applicable or not required or because the information required is contained in the financial statements or notes thereto. Selected quarterly financial data is found in Note 17 of the accompanying consolidated financial statements.

|

|

ITEM 9. |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

None.

|

|

ITEM 9A. |

CONTROLS AND PROCEDURES |

Disclosure Controls and Procedures

The Company maintains disclosure controls and procedures (as such term is defined Rules 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that are designed to ensure that information required to be disclosed by the Company in the reports that it files under the Exchange Act is recorded, processed, summarized and reported within required time periods specified in the SEC’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed is accumulated and communicated to management, including the Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure.

We conducted, under the supervision of our management, including the Chief Executive Officer and Chief Financial Officer, an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures as defined in Rules 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934. Based upon our evaluation, our Chief Executive Officer and Chief Financial Officer concluded that, as of June 30, 2016, our disclosure controls and procedures were effective. Management believes that the consolidated financial statements included in this Annual Report on Form 10-K are fairly presented in all material respects in accordance with U.S GAAP, and the Company’s Chief Executive Officer and Chief Financial Officer have certified that, based on their knowledge, the consolidated financial statements included in this report fairly present in all material respects the Company’s financial condition, results of operations, statement of shareholders’ equity, and cash flows for each of the periods presented in this report.

Changes in Internal Control

There have been no changes in the Company’s internal control over financial reporting (as defined in Rules 13a-15(f) and 15d-15(f) under the Exchange Act) during the fiscal quarter ended June 30, 2016, that have materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting, except as otherwise described in this Item 9A. See Management’s Report On Internal Control Over Financial Reporting on page 34.

|

|

ITEM 9B. |

OTHER INFORMATION |

None.

PART III

ITEMS 10, 11, 12, 13 and 14 of Part III are incorporated by reference to the LSI Industries Inc. Proxy Statement for its Annual Meeting of Shareholders to be held November 17, 2016, as filed with the Commission pursuant to Regulation 14A.

|

|

ITEM 12. |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENTAND RELATED SHAREHOLDER MATTERS |

The description of equity compensation plans required by Regulation S-K, Item 201(d) is incorporated by reference to the LSI Industries Inc. Proxy Statement for its Annual Meeting of Shareholders to be held November 17, 2016, as filed with the Commission pursuant to Regulation 14A.

The following table presents information about the Company’s equity compensation plans (LSI Industries Inc. 2003 Equity Compensation Plan and the 2012 Stock Incentive Plan) as of June 30, 2016.

|

Plan category |

(a) Number of securities to be issued upon exercise of outstanding options, warrants and rights |

(b) Weighted average exercise price of outstanding options, warrants and rights |

(c) Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) |

|||||||||

|

Equity compensation plans approved by security holders |

3,038,990 | $ | 8.98 | 1,612,095 | ||||||||

|

Equity compensation plans not approved by security holders |

— | — | — | |||||||||

|

Total |

3,038,990 | $ | 8.98 | 1,612,095 | ||||||||

PART IV

|

ITEM 15. |

EXHIBITS AND FINANCIAL STATEMENT SCHEDULES |

|

|

(a) |

The following documents are filed as part of this report: |

|

|

(1) |

Consolidated Financial Statements |

|

|

(2) |

Exhibits — Exhibits set forth below are either on file with the Securities and Exchange Commission and are incorporated by reference as exhibits hereto, or are filed with this Form 10-K. |

|

Exhibit No. |

Exhibit Description | |||

|

|

|

| ||

|

3.1 |

|

Articles of Incorporation of LSI (incorporated by reference to Exhibit 3.1 to LSI’s Form S-3 Registration Statement File No. 33-65043). | ||

|

|

| |||

|

3.2 |

|

Amended Article Fourth of LSI’s Amended and Restated Articles of Incorporation (incorporated by reference to Exhibit 3.1 to LSI’s Form 8-K filed November 19, 2009). | ||

|

|

| |||

|

3.3 |

|

Amended and Restated Code of Regulations of LSI (incorporated by reference to Exhibit 3 to LSI’s Form 8-K filed January 22, 2009). | ||

|

|

| |||

|

10.1 |

|

Second Amendment to Loan Documents dated March 31, 2016 by and between the Registrant and PNC Bank, National Association (incorporated by reference to Exhibit 10.1 to LSI’s Form 10-Q filed April 29, 2016). | ||

|

|

| |||

|

10.9 |

* |

LSI Industries Inc. Retirement Plan (Amended and Restated as of April 22, 2015) (incorporated by reference to Exhibit 10.9 to LSI’s Form 10-K filed September 8, 2015). | ||

|

|

| |||

|

10.10 |

* |

LSI Industries Inc. 2003 Equity Compensation Plan (Amended and Restated through November 19, 2009) (incorporated by reference to Exhibit 10.1 to LSI’s Form 8-K filed November 19, 2009). | ||

|

|

| |||

|

10.11 |

* |

Amended and Restated 2012 Stock Incentive Plan as of November 19, 2015 (incorporated by reference to Exhibit 10.1 to LSI’s Form 10-Q filed February 4, 2016). | ||

|

10.12 |

* |

Trust Agreement Establishing the Rabbi Trust Agreement by and between LSI Industries Inc. and Prudential Bank & Trust, FSB (incorporated by reference to Exhibit 10.1 to LSI’s Form 8-K filed January 5, 2006). | ||

|

|

| |||

|

10.13 |

* |

LSI Industries Inc. Nonqualified Deferred Compensation Plan (Amended and Restated as of November 20, 2014) (incorporated by reference to Exhibit 10.2 to LSI’s Form 10-Q filed February 5, 2015). | ||

|

10.14 |

* |

Amended Agreement dated January 25, 2005 with James P. Sferra (incorporated by reference to Exhibit 10.2 to LSI’s Form 8-K filed January 27, 2005). |

|

|

|

|