Attached files

| file | filename |

|---|---|

| EX-31.2 - RULE 13A-14(A)/15D-14(A) CERTIFICATION OF CHIEF FINANCIAL OFFICER - BAKKEN RESOURCES INC | bakken3123911_1-ex312.htm |

| EX-32.1 - SECTION 1350 CERTIFICATION OF CHIEF FINANCIAL OFFICER AND PRINCIPAL EXECUTIVE - BAKKEN RESOURCES INC | bakken3123911_1-ex321.htm |

| EX-31.1 - RULE 13A-14(A)/15D-14(A) CERTIFICATION OF CHIEF EXECUTIVE OFFICER - BAKKEN RESOURCES INC | bakken3123911_1-ex311.htm |

| |

UNITED

STATES

SECURITIES AND

EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

10-K/A

(Amendment No. 1)

| [X] | Annual Report under Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended December 31, 2013. | |

| [ ] | Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from _____ to _____. |

Commission File Number: 000-53632

![]()

BAKKEN RESOURCES, INC.

(Exact name

of small business issuer as specified in its

charter)

| Nevada | 26-2973652 |

| (State or other jurisdiction of | (I.R.S. employer |

| incorporation or organization) | identification number) |

825 Great Northern

Boulevard

Expedition Block, Suite 304

Helena, Montana

59601

(Address of principal executive offices and zip code)

(406)

442-9444

(Registrant’s telephone

number, including area code)

Securities

registered pursuant to Section

12(b) of the Act:

None

Securities

registered pursuant to Section

12(g) of the Act:

Common Stock, $.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES [ ] NO [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. YES [ ] NO [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [ ] NO [X]

1

Indicate by check mark if the disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained in this herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” “larger accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [ ] | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES [ ] NO [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, as of June 28, 2013 is $6,134,777 based on the average closing price of the Registrant’s common stock as currently listed on the OTC Bulletin Board exchange. Shares of Common Stock held by each officer and director and in that such persons may be deemed to be affiliates of the registrant. The determination of affiliate status is not necessarily a conclusive determination for any other purpose. The shares of our company are currently listed on the OTC Bulletin Board exchange, symbol “BKKN”.

Number of shares outstanding of the issuer’s common stock as of August 31, 2016 is 56,735,350 shares.

DOCUMENTS INCORPORATED BY

REFERENCE

Bakken’s Annual Report on Form 10-K for fiscal year ended December 31, 2013,

Accession No. 0001145443-14-000485, submitted to Edgar on Tuesday, April 15, 2014.

EXPLANATORY NOTES

Bakken Resources, Inc. (the “Company”) is filing this Amendment No. 1 (“Amendment No. 1”) to amend its Annual Report on Form 10-K for the fiscal year ended December 31, 2013, filed with the Securities and Exchange Commission (“SEC” or the “Commission”) on April 15, 2014 (the “Original Form 10-K”). The purpose of this Amendment No. 1 is to (1) restate certain financial statements consistent with Note 7 of Item 1 on the Company’s Q3 2014 Form 10-Q, filed with the SEC on November 19, 2014 (“Restatement”), (2) include disclosures of certain related person or potential related person transactions relating to the Company, its officers, or its directors, (3) adjust risk factors under Item 1A of Part I, (4) update information related to the Company’s legal proceedings under Item 3 of Part I, (5) modify the Management’s Discussion and Analysis of Financial Condition and Results of Operation under Item 7 of Part II. New Company certifications are being filed with this Amendment No. 1 as exhibits signed by the principal executive and financial officers as required by Rule 12b-15 under the Securities Exchange Act of 1934, as amended.

No other material changes have been made to the Original Form 10-K except to make this Amendment No. 1 consistent with the Restatement. This Amendment No. 1 does not necessarily reflect events that may have occurred subsequent to the original filing date and does not modify or update in any way the disclosures made in the Original Form 10-K except as described above.

This Amendment No. 1 is being filed concurrently with the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2014. The Company anticipates filing additional delinquent filings shortly.

2

3

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

We are including the following discussion to inform our existing and potential security holders generally of some of the risks and uncertainties that can affect our company and to take advantage of the “safe harbor” protection for forward-looking statements that applicable federal securities law affords.

From time to time, our management or persons acting on our behalf may make forward-looking statements to inform existing and potential security holders about our company. All statements other than statements of historical facts included in this report regarding our financial position, business strategy, plans and objectives of management for future operations, industry conditions, and indebtedness covenant compliance are forward-looking statements. When used in this report, forward-looking statements are generally accompanied by terms or phrases such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “target,” “plan,” “intend,” “seek,” “goal,” “will,” “should,” “may,” or other words and similar expressions that convey the uncertainty of future events or outcomes. Items contemplating or making assumptions about, actual or potential future sales, market size, collaborations, and trends or operating results also constitute such forward-looking statements.

Forward-looking statements involve inherent risks and uncertainties, and important factors (many of which are beyond our company's control) that could cause actual results to differ materially from those set forth in the forward-looking statements, including the following: general economic or industry conditions, nationally and/or in the communities in which our company conducts business, changes in the interest rate environment, legislation or regulatory requirements, conditions of the securities markets, our ability to raise capital, changes in accounting principles, policies or guidelines, financial or political instability, acts of war or terrorism, other economic, competitive, governmental, regulatory and technical factors affecting our company's operations, products, services and prices.

We have based these forward-looking statements on our current expectations and assumptions about future events. While our management considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. Accordingly, results actually achieved may differ materially from expected results in these statements. Forward-looking statements speak only as of the date they are made. You should consider carefully the statements in “Item 1A. Risk Factors” and other sections of this report, which describe factors that could cause our actual results to differ from those set forth in the forward-looking statements.

Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. We assume no obligation to update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, other than as may be required by applicable law or regulation. Readers are urged to carefully review and consider the various disclosures made by us in our reports filed with the United States Securities and Exchange Commission (the “Commission” or “SEC”) which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operation and cash flows. If one or more of these risks or uncertainties materialize, or if the underlying assumptions prove incorrect, our actual results may vary materially from those expected or projected.

4

BAKKEN RESOURCES,

INC.

ANNUAL REPORT OF FORM 10-K

FOR FISCAL YEAR ENDED DECEMBER 31, 2013

PART I

Overview and Background

Bakken Resources, Inc. (the “Company,” “BRI,” “we,” “us,” or “our”) owns mineral rights to approximately 7,200 gross acres and 2,400 net mineral acres of land located about 8 miles southeast of Williston, North Dakota. The Company’s net mineral acres consist generally of 2,400 net mineral acres deriving from the sub-surface to the base of the rock unit in the region commonly referred to as the Bakken formation. Approximately 800 of such 2,400 net mineral acres, consist also of mineral rights extending below the Bakken formation (which include, without limitation, the source rock commonly referred to as the Three Forks formation(s)).

These mineral rights currently bear to us an average of 12% royalty from the oil and gas produced on such lands until November 2020, at which time a 5% overriding royalty currently held by Holms Energy, LLC, a private Nevada company (“Holms Energy”) will revert back to the Company. The Holms Energy overriding royalty is a common practice in the oil and natural gas industry. When mineral rights are sold it is a usual and customary practice for the seller to retain a portion of the royalty stream. This retained royalty is usually stated in percentage terms; that is, the percentage points of the original royalty stream that is retained by the seller. In the case of Holms Energy, the Asset Purchase Agreement provided a five percentage point retained overriding royalty. Therefore, Holms Energy retains five percentage points of a seventeen percentage point royalty stream, or 29.41% (5/17). The Company’s Annual Report on Form 10-K for the year ended December 31, 2011 contained an erroneous example of this overriding royalty.

The overriding royalty, 5/17 or 29.41%, is applied to Bakken’s monthly net royalty paid by the company’s well operators, Oasis Petroleum, Continental Resources, and Statoil. The operators discount the gross monthly production value (gross oil and natural gas volume times the current unit price) by the company’s net mineral interest to derive the company’s net monthly royalty. The Holms Energy overriding royalty factor (29.41%) is then applied to the net monthly royalty to derive the monthly override payment. The methodology employed by Bakken is consistent with the methodology employed by Oasis Petroleum and Continental Resources to calculate the overriding royalty that Bakken retained with the sale of certain mineral rights to Apollo Global Management in February 2014. Bakken has consistently applied this methodology since the company’s inception. Prior SEC filings included examples which erroneously discussed the application of the overriding royalty and included examples of such.

|

Overriding royalty calculation example: Missoula 1-21H | ||

| ○ |

Gross Mineral Acres: 640.00 (Independently Confirmed by Third Party Certified Landman) | |

| ○ |

Net Mineral Interest: 16.18993% (Independently Confirmed by Third Party Certified Landman) | |

| ○ |

Net Mineral Acres: 103.62 (640.00 x 16.18993%) | |

| ○ |

Stated Lease Royalty Percentage: 17% | |

| ○ |

North Dakota Industrial Commission Established Spacing Unit: 1280 acres | |

| ○ |

Bakken Net Royalty Percentage: 1.3761433% (derived as (103.62 x 17%)/1280) | |

| ○ |

December 2013 Oil Production: 4,565 Barrels (Continental Resources 1/2014 Remittance Statement) | |

| ○ |

December 2013 Oil Sales Price: 85.8941 (Continental Resources Remittance Statement) | |

| ○ |

Post Production Costs - $206.31 | |

Holms Energy Override: 5/17 x 4,565 barrels x $85.8941 per barrel x 1.3761433% - $206.31 Post Production Costs = $1,587.04

According to the U.S. Geological Survey, the Bakken Formation, is “a thin but widespread unit within the central and deeper portions of the Williston Basin in Montana, North Dakota, and the Canadian Provinces of Saskatchewan and Manitoba. The formation consists of three members: (1) lower shale member, (2) middle sandstone member, and (3) upper shale member. Each succeeding member is of greater geographic extent than the underlying member. Both the upper and lower shale members are organic-rich marine shale of fairly consistent lithology; they are the petroleum source rocks and part of the continuous reservoir for hydrocarbons produced from the Bakken Formation. The middle sandstone member varies in thickness, lithology, and petrophysical properties, and local development of matrix porosity enhances oil production in both continuous and conventional Bakken reservoirs.” (source: USGS Fact Sheet, April 2008). Generally, the source rock commonly referred to as the “Three Forks Formation” is located geologically below the Bakken formation.

We currently have leases with three contracted oil drilling operators on various parcels of land constituting the 7,200 gross acres (and approximately 2,400 net mineral acres) on which we have mineral rights royalty interests. The contracted oil drilling companies with whom we are parties in interest pursuant to lease agreements (collectively, the “Lessees”) that we acquired rights to in November 2010 include: Oasis Petroleum, Continental Resources, Inc., and Statoil ASA. We have no rights to influence the activities conducted by these Lessees of our mineral rights, but if the Lessees do not accomplish the agreed upon drilling programs within the timeline, they can lose their leases.

5

The predecessor to our company was incorporated on June 6, 2008, under the laws of the state of Nevada, under the name Multisys Language Solutions, Inc. (“MLS”). Holms Energy contributed the primary assets that formed the basis of our current business operations. In connection with the closing of the transactions resulting in the contribution of the mineral rights held by Holms Energy in November 2010, Holms Energy received forty million (40,000,000) shares of common stock of the Company. Holms Energy retained a 5% overriding royalty (until November 2020, at which time it reverts back to the Company) on all gross revenue generated from the Company's gas and oil production royalty revenues.

Also in connection with the November 2010 transactions, the Company purchased approximately 800 net mineral acres from the Revocable Living Trust of Rocky G. Greenfield and Evenette G. Greenfield. The mineral rights received by the Company from the contribution by Holms Energy in connection with the November 2010 transactions included mineral rights from the surface to the base of the Bakken formation. The mineral rights received by the Company from the Greenfields include all mineral rights from the surface to the basement. After closing of the Asset Purchase Agreement with Holms Energy, on December 10, 2010, MLS changed its name to Bakken Resources, Inc. These transactions and changes of control are described below under Acquisition of Assets.

Description of Oil Leases and Oil Production

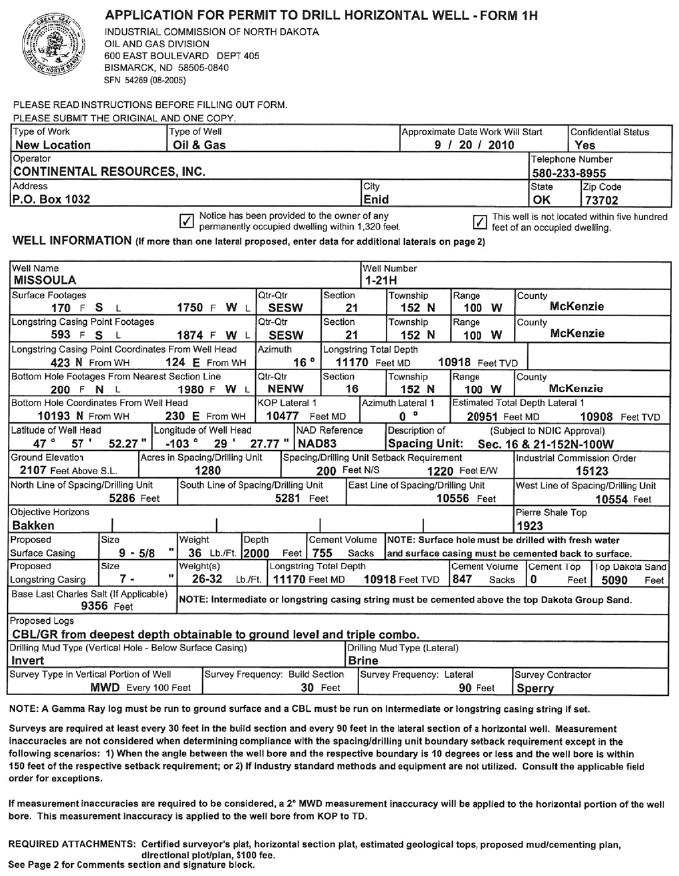

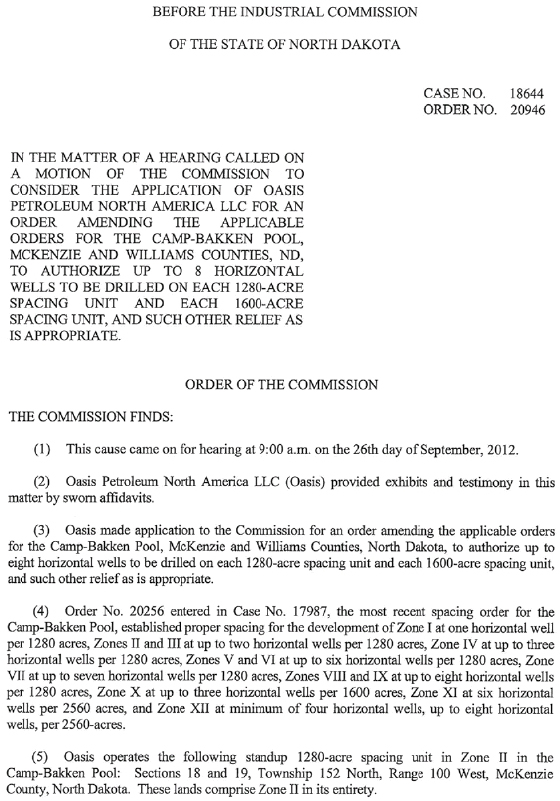

BRI currently derives its primary source of revenue from royalties generated by leasing its mineral acreage. BRI’s mineral acreage consists of approximately 2,400 net mineral acres located primarily in McKenzie County, North Dakota. Such 2,400 net mineral acres are currently spread across 16 spacing units. Operators in the area where BRI’s minerals are located have been approved for up to eight wells per spacing unit (typically 1,280 acres), but generally petition for permits prior to the commencement of drilling in a particular spacing unit. Assuming this would apply for all spacing units under which BRI has mineral acres, BRI would have a royalty interest in up to 112 wells. Note, however, that the royalties due to BRI under any particular well would vary based on the number of acres BRI has under any particular spacing unit where there is a producing well. An example of an application for permit to drill a horizontal well is shown below. This permit is for a well in the area where BRI’s minerals are located (section 21, T152N R100W). Section 21 currently has 7 wells drilled. Order number 20946 of the North Dakota Industrial Commission shows that Oasis Petroleum, one of the operators in the BRI mineral acres area, has applied for up to 8 wells per 1280-acre spacing unit (1st page of order 20946 follows).

6

7

8

As of December 31, 2013, BRI received royalty income primarily from 28 Bakken formation producing wells, 12 Three Forks formation wells, and 3 Madison formation producing wells. During 2013, the dollar amount of such royalties received from the aggregate number of producing wells was approximately $3,800,000. BRI has interest under several other wells which have been drilled and are likely producing, but for which royalties have yet to be received as of December 31, 2013. BRI is currently receiving royalty income from five wells which have been determined to be drilled in the Three Forks formation.

With respect to drilling operations, pursuant to the North Dakota Oil and Gas Commission, long lateral deep horizontal multi-stage fracking wells in the Bakken Formation must be permitted in spacing unit of not less than 640 acres, up to 5,560 acres, with some exceptions. The spacing units have to be approved and permitted in advance of drilling by the North Dakota Oil and Gas Commission. Recently, the North Dakota Industrial Commission (“NDIC”) has approved multi-well permits for wells drilled in the Three Forks formation along several of the defined “benches” typically associated with separate geologic benchmarks contained in the Three Forks formation. Since approximately one-third of the Company’s current net mineral acres include acreage in the Three Forks formation, any increase in the drilling operations on the Company’s net mineral acres may result in an increased number of total wells from which the Company may derive royalty income.

When our lessees drill a horizontal well in the area where the subject property is located, they typically drill down to about 10,800 vertical feet and then utilize a downhole directional drilling tool to flatten the hole to 90 degrees and drill horizontally down the oil and gas producing formation. Horizontal directional drilling provides more contact area to the oil bearing formation than a typical vertical well. This method of drilling together with fracking is referred to as an enhanced oil recovery method, and is the primary source of recovery from the Bakken Formation. BRI does, however, have interests in certain wells not drilled into the Bakken Formation.

Well activity information for wells in which the company has mineral interest is compiled in a table which is available on the Company web site at http://www.BakkenResourcesInc.com/WellActivity.php.

The information provided in our website’s table is categorized by well name, the operator, field and pool, the NDIC identifying number, and the well status and location description. Well status is defined by several categories: Producing; Confidential; Drilling; and Permitted Location to Drill. The table is updated as new information becomes available on the NDIC website at https://www.dmr.nd.gov/oilgas/. Included on the table are NDIC file numbers which can be used when searching for information for each well listed on the BRI webpage. Individuals may subscribe to the NDIC website following the prompts on the homepage. A premium service subscription is also available for a fee.

9

Currently, most of the leases covering the Company’s mineral acres contain what is commonly referred to as “continuous drilling clauses”. Generally, a continuous drilling clause requires an operator to maintain active drilling operations in order to hold or extend an oil and gas lease past the natural expiration date of the lease. A majority of the Company’s current leases currently have active drilling operations and are likely to have active operations in the foreseeable future.

Acquisition of Assets

On June 11, 2010, Multisys Language Solutions, Inc. or MLS, Multisys Acquisition, and Holms Energy entered into an Option to Purchase Assets Agreement, pursuant to which Holms Energy agreed to grant Multisys Acquisition an option to exercise an Asset Purchase Agreement to assign all right, title, and interest of specific Holms Energy owned oil and gas mineral rights to Multisys Acquisition. On November 26, 2010, MLS completed an initial closing of a private placement in the amount of $1,545,000 that issued 6,180,000 shares at $0.25 per share and 3,090,000 three-year warrants exercisable for 3,090,000 shares at $.50 per share, callable at $0.01 per share at any time after November 26, 2011, if the underlying shares are registered, and the common stock trades for 20 consecutive trading days at an average closing sales price of $1.00 or more. Such warrants are now expired. The option agreement expired on its terms before the Asset Purchase Agreement was executed. Despite the expiration of the option, the Asset Purchase Agreement was duly executed by all parties and hence is a legally binding agreement.

10

We concurrently exercised the option with Holms Energy and executed an Asset Purchase Agreement by and between MLS, Holms Energy, and Multisys Acquisition in order to acquire certain interests in mineral rights and assets from Holms Energy. The option was exercised on November 26, 2010, and the Asset Purchase Agreement was entered into on November 26, 2010 by paying the consideration to Holms Energy detailed in the Asset Purchase Agreement. Under the Asset Purchase Agreement, Multisys Acquisition paid Holms Energy $100,000, issued Holms Energy 40,000,000 shares of restricted common stock, and granted to Holms Energy a 5% overriding royalty on all revenue generated from the Holms Property (defined herein) for ten years from the date of the acquisition closing (i.e. November 2010). With the issuance of the 40,000,000 shares to the Holms Energy members, the Holms Energy members own a controlling interest in BRI. Holms Energy disbursed 40,000,000 shares to its members on a ratable ownership basis as a liquidating dividend to members.

The Asset Purchase Agreement related to the acquisition of: (1) certain Holms Energy mineral rights in oil and gas rights on approximately 7,200 gross acres and 2,400 net mineral acres of land located in McKenzie County, 8 miles southeast of Williston, North Dakota (the “Holms Property”); (2) potential production royalty income from wells to be drilled on the property whose oil and gas mineral rights are owned by Holms Energy; and (3) the transfer of all right, title and interest to an Option to Purchase the mineral rights from Rocky G. Greenfield and Evenette G. Greenfield entered into between Holms Energy and the Revocable Living Trust of Rocky G. Greenfield and Evenette G. Greenfield related to purchasing additional oil and gas mineral rights and production royalty income on the Holms Property for One Million Six Hundred Forty Nine Thousand ($1,649,000) Dollars (the “Greenfield Option”) (altogether, the “Asset Acquisition”). The Greenfield mineral rights were acquired by Multisys Acquisition through the Asset Purchase Agreement with Holms Energy on November 12, 2010. Holms Energy entered into a $485,000 one month non-interest bearing loan from BRI (the “Greenfield Note”) to complete the initial payment of $400,000 for the purchase of the Greenfield mineral rights. The purchase price of the Greenfield mineral rights under the agreement with Holms Energy (which was assumed by the Company in connection with the completion of the November 2010 transactions) was an aggregate of $1,649,000 plus interest as follows: an initial payment of $400,000; installment payments generally in the amount of $30,000 per quarter plus interest at 5% per annum for 8 years and an original balloon payment in the amount of $289,000 (which is subject to reduction in the event the Company accelerates payments under the Greenfield Note). The scheduled installment payments of $30,000 per quarter are subject to the amount of 35% of net revenues received in connection with the purchased Greenfield mineral rights. Payments made in excess of the amounts originally scheduled are applied to the outstanding principal amount of the loan. The collateral for the Greenfield Note are the Greenfield mineral rights. Under the terms of the loan from BRI to Holms Energy, Holms Energy, in conjunction with the entry into the Asset Purchase Agreement on November 26, 2010, assigned the Greenfield mineral rights to Multisys Acquisition in exchange for forgiveness of $385,000 of the loan. The other $100,000 of the loan was to be applied to the Asset Purchase Agreement between BRI and Holms Energy, and on November 26, 2010, that $100,000 was applied to the Asset Purchase Agreement and the loan was forgiven.

Although the Greenfield Note included an eight year amortization of the former Greenfield properties, the Company accelerated these payments, retiring the debt in 2013.

In conjunction with the exercise of the option and execution of the Asset Purchase Agreement with Holms Energy, Multisys Acquisition acquired the rights to the Asset Purchase Agreement between Holms Energy and the Greenfields and therefore purchased the gas and oil production royalty rights of the Revocable Living Trust of Rocky G. Greenfield and Evenette G. Greenfield.

Change of Control of Bakken Resources, Inc.

After the closing of the Asset Purchase Agreement on November 26, 2010 which involved, in part, the issuance of 40 million (40,000,000) shares of BRI common stock to Holms Energy, the Company subsequently declared a special liquidating dividend distribution of such 40 million shares to its members. Following such distribution, the members of Holms Energy beneficially then held in aggregate approximately 76.2% of the outstanding shares of common stock of Multisys Language Solutions after the closing of the Asset Purchase Agreement on November 26, 2010. After the closing of the transaction, based on an informal agreement in place, the current directors of MLS appointed the nominees designated by Holms Energy as members of the board of directors of MLS on December 1, 2010. Subsequently, the officers and directors of MLS resigned their positions, clearing the way for the appointment of new executive officers by a new board of directors of MLS. Pursuant to the authorization from MLS stockholders for the amendment of the articles of incorporation of MLS at a special meeting of stockholders, MLS changed its corporate name from Multisys Language Solutions, Inc. to Bakken Resources, Inc. on December 10, 2010 to reflect its new business focus.

11

Business Strategy

We plan to focus on evolving into a growth-orientated independent energy company engaged in the acquisition, exploration, exploitation, and development of oil and natural gas properties. We plan to initially focus our activities mainly in the Williston Basin, a large sedimentary basin in eastern Montana, Western North and South Dakota, and Southern Saskatchewan known for its rich deposits of petroleum and potash. To date, we have collected approximately $6.6 million in revenues from royalties generated from our mineral rights.

Per our business plan and strategy, we have pursued relationships to gather information on future potential oil and gas drilling projects and explored and contemplated possible joint partnerships in other drilling programs. We previously announced our acquisition of mineral acreage in the Duck Lake region of Western Montana, in a potential oil play commonly referred to as the Alberta Bakken. We also announced our acquisition of a 17% working interest in an operating well located in Archer County, Texas. The Company remains in discussion with various groups for strategic partnerships and plans to announce the completion of such arrangements if and when they are consummated.

Geology of the Bakken Formation and the Three Forks Formation

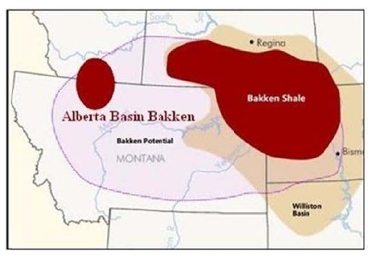

The geological formation, as well as many other criteria, determines the production level of any commercial wells, which impact the potential future royalty revenue, if any. The following profile of the Williston Basin gives an idea as to the value of our mineral assets. Our leases are in a geographic area known as the Williston Basin, which is a large intracratonic sedimentary basin in eastern Montana, western North and South Dakota and southern Saskatchewan known for its rich deposits of petroleum and potash. The basin is a geologic structural basin but not a topographic depression; it is transected by the Missouri River. The oval-shaped depression extends approximately 475 miles (764 km) north-south and 300 miles (480 km) east-west. The map below shows the general location of the Bakken Formation and the Alberta Bakken (not intended to show or represent the location of any oil fields). (Source: http://seekingalpha.com/article/284628-the-alberta-bakken-the-smaller-sibling-offers-compelling-prospects).

The smaller area shown in the northwest portion of Montana shows generally the location of mineral acreage BRI purchased in Fall 2011 (referred to as the “Duck Lake Property”). Drilling has not begun on the Duck Lake Property.

The Bakken formation has received considerable recognition for its oil production capabilities. Oil was discovered in this formation in 1951 but production was difficult to achieve at that time. Technological developments and improvements since then have given operators the capabilities in recent years to develop the formation. In April 2008, the United States Geological Service (USGS) released a report estimating the amount of oil recoverable with current technology ranged from 3.0 to 4.3 billion barrels. At the same time, the State of North Dakota also released a report estimating recoverable oil at 2.1 billion barrels. Other industry estimates place the total oil available, which includes oil that cannot be recovered with current technology, at 18 billion barrels. The USGS is currently further reassessing the amount of technically recoverable oil in the Bakken formation and such report is expected to be released in late 2014.

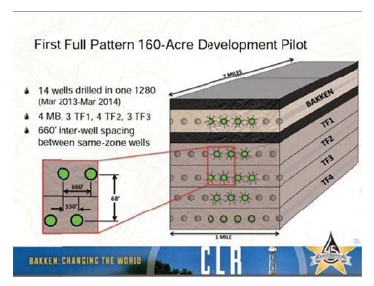

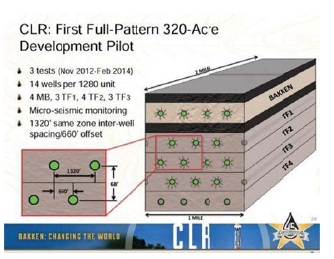

There are several formations below the subsurface of the Bakken formation known commonly as the Three Forks. Evaluative wells have already been drilled to these “benches” of the Three Forks. Operators have recently begun exploratory drilling into these benches. Several operators have announced plans to evaluate high density drilling possibilities to these benches. The graphic below shows a development pilot program Continental has announced as part of its Three Forks drilling program.

(Source: Seeking Alpha (http://seekingalpha.com/article/1248431-bakken-the-downspacing-bounty-and-birth-of-array-fracking)

12

The drilling pattern in this graphic is known as array drilling. The offset pattern of drilling is expected to allow high density drilling for a spacing unit (1,280 acres). The goal is to increase the number of wells without impacting the number of barrels produced from each well.

BRI owns mineral acres in the Three Forks formation through its ownership of the former Greenfield mineral assets.

According to the NDIC’s Oil and Gas Division, the Bakken Shale in the Williston Basin is over 11,000 ft. deep at the center of the formation and rises to 3,100 ft. on the edges of the basin. The Bakken Formation is composed of three distinct members. The first layer averages twenty three feet in depth and consists of blackish marine shale. The second member runs from 30 ft. to 80 ft. and composed of interbedded limestone, siltstone, sandstone and dolomite. The bottom member is a dark black marine shale that averages 10 ft. to 30 ft. in thickness. All three formations that make up the Bakken are rich in an organic material called Kerogen. When Kerogen is heated (thermogenic processes) or broken down by organic means (biogenic processes), natural gas and oil are created. The Bakken Formation is capped by a very thick limestone formation called the Lodgepole. It is because of this limestone cap that there is so much gas and oil trapped in the shale horizon. The Bakken Formation is what is considered a thermally mature deposit and the oil from the Bakken has a 41 specific gravity and is deemed to be commercially high grade crude oil.

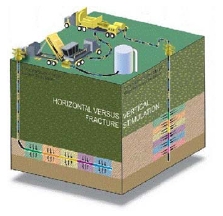

Horizontal Drilling

Horizontal or directional drilling has revolutionized the way the oil and gas wells are being drilled in the Williston Basin. The reason that horizontal drilling is changing the oil and gas business is that a well drilled horizontally through a formation that contains oil and gas should produce many more times that of a vertical well. A vertical well will only penetrate a limited area of the productive zone, whereas a well drilled horizontally may penetrate up to 10,000’ of the zone. This also means that previously tight shale formations such as the Bakken formation can result in prolific production.

13

The Bakken formation has poor porosity which reduces the ability of the gas and oil to flow out of this horizon. Recently, horizontal drilling of lateral holes combined with hydraulic fracturing (commonly referred to as ‘fracking’) has resulted in substantial production from thick formations that have poor porosity. It should be noted, however, that porosity and the permeability of the oil shale rock can vary widely and unpredictably over short distances, thus dry wells can be found next to prolific wells with little explanation geologically.

Fracking is a procedure whereby packers (plugs) are set every 250’ to 300’ and up to ten 2,000 horsepower hydraulic pumps deliver high pressure fluids that contain a high percentage of round ceramic beads and sand are utilized as proppants and keep the fissures and fractures open along the bedding-planes that are created by the high pressure fluids. The fissures and channels created by the high pressure fluid and held open by the ceramic beads that are left behind; provide a pathway to allow the gas and oil to flow into the drill hole.

Two technologies are currently being used to enhance horizontal drilling: (1) log while drilling (“LWD”); and (2) drill string radar (“DST”). LWD uses long sensors which read gamma radiation given off by the formation, which provides real time information to the drillers and this information is gathered and assists drillers to drill in the optimum sections of the formation. DST provides information to the driller on the surface as to what direction, angle and depth the well is being drilled. The combination of the two technologies greatly assists keeping the drill bit in the optimum location within the Bakken formation. Below is a diagram example of horizontal drilling.

Governmental Regulations

Our operations are not directly subject to various rules, regulations and limitations impacting the oil and natural gas exploration and production industry as whole, however, operators who operate on our properties may be impacted by such rules and regulations.

Regulation of Oil and Natural Gas Production. Oil and natural gas exploration, production and related operations, when developed, are subject to extensive rules and regulations promulgated by federal, state and local authorities and agencies. For example, the state of North Dakota and Montana requires permits for exploration drilling, operation of commercial wells, submission of several reports concerning operations of wells and imposes other requirements relating to the production of oil and natural gas. Such states may also have statutes and regulations addressing conservation matters, including provisions for the unitization or pooling of oil and natural gas properties, the establishment of maximum rates of production from wells, and the regulation of spacing, plugging and abandonment of such wells. Failure to comply with any such rules and regulations by our operators can result in substantial penalties, which in turn may impact the amount of royalty revenue we derive from our leased properties. Although we believe that we are currently in substantial compliance with all applicable laws and regulations, to the extent they apply to us, because such rules and regulations are frequently amended or reinterpreted, we are unable to predict the future cost or impact of complying with such laws. Significant expenditures may be required to comply with governmental laws and regulations and may have a material adverse effect on our financial condition and results of operations.

Environmental Matters

The following environmental discussion may be applicable directly to our operators; however, we could be indirectly impacted, since environmental laws and regulations could significantly impact production of the wells on our properties. Our operators and properties are impacted by extensive and changing federal, state and local laws and regulations relating to environmental protection, including the generation, storage, handling, emission, transportation and discharge of materials into the environment, and relating to safety and health, as such regulations relate to our operators. The recent trend in environmental legislation and regulation generally is toward stricter standards, and this trend will likely continue. These laws and regulations may:

| ● | require the acquisition of a permit or other authorization before construction or drilling commences and for certain other activities; |

| ● | limit or prohibit construction, drilling and other activities on certain lands lying within wilderness and other protected areas; and |

| ● | impose substantial liabilities for pollution resulting from its operations. |

14

The permits required by our operators may be subject to revocation, modification and renewal by issuing authorities. Governmental authorities have the power to enforce their regulations, and violations are subject to fines or injunctions, or both. In the opinion of management, we are in substantial compliance with current applicable environmental laws and regulations, and have no material commitments for capital expenditures to comply with existing environmental requirements. Nevertheless, changes in existing environmental laws and regulations or in interpretations thereof could have a significant impact on BRI, as well as the oil and natural gas industry in general.

The Comprehensive Environmental, Response, Compensation, and Liability Act (“CERCLA”) and comparable state statutes impose strict, joint and several liabilities on owners and operators of sites and on persons who disposed of or arranged for the disposal of “hazardous substances” found at such sites. It is not uncommon for the neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the hazardous substances released into the environment. The Federal Resource Conservation and Recovery Act (“RCRA”) and comparable state statutes govern the disposal of “solid waste” and “hazardous waste” and authorize the imposition of substantial fines and penalties for noncompliance. Although CERCLA excludes petroleum from its definition of “hazardous substance,” state laws affecting our operators may impose clean-up liability relating to petroleum and petroleum related products. In addition, although RCRA classifies certain oil field wastes as “non-hazardous,” such exploration and production wastes could be reclassified as hazardous wastes thereby making such wastes subject to more stringent handling and disposal requirements.

Our operations are also subject to the federal Clean Water Act and analogous state laws. The Clean Water Act and similar state acts regulate other discharges of wastewater, oil, and other pollutants to surface water bodies, such as lakes, rivers, wetlands, and streams. Failure to obtain permits for such discharges could result in civil and criminal penalties, orders to cease such discharges, and costs to remediate and pay natural resources damages. Under the Clean Water Act, the U.S. Environmental Protection Agency (“EPA”) has adopted regulations concerning discharges of storm water runoff. This program requires covered facilities to obtain individual permits, or seek coverage under a general permit. Some of our properties may require permits for discharges of storm water runoff and our operators may apply for storm water discharge permit coverage and updating storm water discharge management practices at some of our facilities. These laws also require the preparation and implementation of Spill Prevention, Control, and Countermeasure Plans in connection with on-site storage of significant quantities of oil.

The federal Clean Air Act and comparable state laws regulate emissions of various air pollutants through air emissions permitting programs and the imposition of other requirements. In addition, the EPA has developed and continues to develop stringent regulations governing emissions of toxic air pollutants at specified sources. Federal and state regulatory agencies can impose administrative, civil and criminal penalties for non-compliance with air permits or other requirements of the federal Clean Air Act and associated state laws and regulations. The operations provided by our operators, may be, in certain circumstances and locations, subject to permits and restrictions under these statutes for emissions of air pollutants.

The Endangered Species Act (“ESA”) seeks to ensure that activities do not jeopardize endangered or threatened animal, fish and plant species, nor destroy or modify the critical habitat of such species. Under ESA, exploration and production operations, as well as actions by federal agencies, may not significantly impair or jeopardize the species or its habitat. ESA provides for criminal penalties for willful violations of the Act. Other statutes that provide protection to animal and plant species and that may apply to our operations include, but are not necessarily limited to, the Fish and Wildlife Coordination Act, the Fishery Conservation and Management Act, the Migratory Bird Treaty Act and the National Historic Preservation Act. Although we believe that our operators will be in substantial compliance with such statutes, any change in these statutes or any reclassification of a species as endangered could subject our operators to significant expenses or could force our operators to discontinue certain operations altogether, which could materially impact our revenues.

Competition

The oil and natural gas industry is intensely competitive, and we compete with numerous other oil and gas exploration and production companies who may also be seeking oil well operators for leasehold interests. Many of these companies have substantially greater resources than we have. Not only do they explore for and produce oil and natural gas, but many also carry on midstream and refining operations and market petroleum and other products on a regional, national or worldwide basis. The operations of other companies may be able to pay more for exploratory prospects and productive oil and natural gas properties. They may also have more resources to define, evaluate, bid for, and purchase a greater number of properties and prospects than our financial or human resources permit.

15

Our larger or integrated competitors may have the resources to be better able to absorb the burden of existing, and any changes to federal, state, and local laws and regulations more easily than we can, which would adversely affect our competitive position. Our ability to determine reserves and acquire additional properties in the future will be dependent upon our ability and resources to evaluate and select suitable properties and to consummate transactions in this highly competitive environment. In addition, we may be at a disadvantage in producing oil and natural gas properties and bidding for exploratory prospects, because we have fewer financial and human resources than many other companies in our industry. Should a larger and better financed company decide to directly compete with us, and be successful in its efforts, our business could be adversely affected.

Marketing and Customers

The market for oil and natural gas that our operators depends on factors beyond our control, including the extent of domestic production and imports of oil and natural gas, the proximity and capacity of natural gas pipelines and other transportation facilities, demand for oil and natural gas, the marketing of competitive fuels and the effects of state and federal regulation. The oil and gas industry also competes with other industries in supplying the energy and fuel requirements of industrial, commercial and individual consumers.

Our production royalties derived from oil and gas production from our properties are expected to be sold by the Lessees at prices tied to the spot oil markets. We derive certain royalty revenues from gas produced from wells drilled on our property, but currently this amount is small relative to the royalties we receive from oil production. We will be required to rely on the Lessees to market and sell any future gas production.

Employees and Consultants

We currently have two full-time employees and one part-time employee, respectively, Val Holms, President, Chief Executive Officer and Chairman; Karen Midtlyng, Secretary and Director and David Deffinbaugh, Chief Financial Officer and Director. All of our appointed executives have entered into written employments agreements. As drilling production activities continue to increase by our Lessees, and if additional revenue from production royalties develops as anticipated and continues to increase, we may hire additional technical, operational or administrative personnel as appropriate. We are using and will continue to use the services of independent consultants and contractors to perform various professional services. We believe that this use of third-party service providers may enhance our ability to contain general and administrative expenses.

Office Location

Our offices are located at 1425 Birch Ave., Suite A, Helena, MT 59601. We also maintain a presence in New York City with a part-time office.

Available Information—Reports to Security Holders

Our website address is www.bakkenresourcesinc.com. We make available on this website free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, Section 16 reports for officers and directors, and amendments to those reports as soon as reasonably practicable after we electronically file those materials with, or furnish those materials to, the SEC. These filings are also available to the public at the SEC's Public Reference Room at 100 F Street, NE, Room 1580, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Electronic filings with the SEC are also available on the SEC internet website at www.sec.gov.

In addition, BRI regularly monitors and maintains information relating to drilling activity on wells which it has a mineral interest. Such information can also be found on our website.

16

You should carefully consider the risks, uncertainties, and other factors described below. The statements contained in or incorporated herein that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. Any of the factors could materially and adversely affect our business, financial condition, operating results and prospects and could negatively impact the market price of our common stock. Also, you should be aware that the risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties, of which we are not yet aware, or that we currently consider to be immaterial may also impair our business operations.

Risks Associated with Our Business

We are an early stage company. We may never attain profitability.

We have a limited operating history for you to consider in evaluating our business and prospects. Our business relies upon receiving royalties on our lease mineral assets. The business of acquiring, exploring for, developing and producing hydrocarbon reserves is inherently risky. Our operations are therefore subject to all of the risks inherent in acquiring, exploring for, developing and producing hydrocarbon reserves, particularly in light of our limited experience in undertaking such activities. We may never overcome these obstacles.

Our business is speculative and dependent upon the implementation of our business plan and our ability to enter into agreements with third parties for the rights to exploit potential oil and natural gas reserves on terms that will be commercially viable for us.

Our current business model relies exclusively on uncertain future royalty payments as a source of future revenue. We have no influence on the activities conducted by the Lessees with regards to the exploitation of mineral rights owned by the company.

Our current business model relates to the potential generation of revenue from royalties tied to certain leases. These leases have been granted to experienced exploration and operating companies, both of whom have prior experience in drilling deep lateral multi-fracture horizontal wells. Even after wells are drilled on property where the Company owns mineral rights, future income may be uncertain. Pursuant to the terms and conditions of the leases, we have no influence with regard to when the drilling will be undertaken, no decision making ability as to the location of any future wells and no influence as to the rate the wells are produced, if the operators are successful, of which there is no assurance. In the event the Lessees fail to meet their drilling commitment, the company has only three options: (1) it can agree to grant an extension; (2) it can renegotiate the terms of the existing leases; or (3) it can legally terminate the leases.

We may be unable to obtain additional capital or generate significant production royalty income that we will require to implement our business plan, which could restrict our ability to grow.

We expect that our current capital and our other existing resources will be sufficient only to provide a limited amount of working capital, and the potential of production royalty revenues generated from our oil and gas mineral rights properties, of which there is no assurance, may not be sufficient to fund both our continuing operations and our planned growth. We may require additional capital to continue to operate our business beyond the initial phase of development and to further expand our exploration and development programs to additional properties. We may be unable to obtain additional capital, and if we are able to secure additional capital, it may not be pursuant to terms deemed to be favorable to BRI and its shareholders.

Future acquisitions and future exploration, development, production and marketing activities, as well as our administrative requirements (such as salaries, insurance expenses and general overhead expenses, as well as legal compliance costs and accounting expenses) may require a substantial amount of additional capital and cash flow.

We may pursue sources of additional capital through various financing transactions or arrangements, including joint venturing of projects, debt financing, equity financing or other means. We may not be successful in locating suitable financing transactions in the time period required or at all, and we may not obtain the capital we require by other means. If we do not succeed in raising additional capital, our resources may not be sufficient to fund our planned operations going forward beyond twelve months from now.

Any additional capital raised through the sale of equity may dilute the ownership percentage of our stockholders. This could also result in a decrease in the fair market value of our equity securities because our assets would be owned by a larger pool of outstanding equity. The terms of securities we issue in future capital transactions may be more favorable to our new investors, and may include preferences, superior voting rights and the issuance of other derivative securities, and issuances of incentive awards under equity employee incentive plans, which may have a further dilutive effect.

17

Our ability to obtain financing may be impaired by such factors as the capital markets (both generally and in the oil and gas industry in particular), our status as a new enterprise without a significant demonstrated operating history, production royalty revenue from our mineral rights property, currently our only oil and natural gas property and prices of oil and natural gas on the commodities markets (which will impact the amount of asset-based financing available to us) and/or the loss of key management. Further, if oil and/or natural gas prices on the commodities markets decline, our revenues from the anticipated royalties will decrease and such decreased revenues may increase our requirements for capital. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs (even to the extent that we reduce our operations), we may be required to cease our operations.

We may incur substantial costs in pursuing future capital financing, including investment banking fees, legal fees, accounting fees, securities law compliance fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes or warrants, which may adversely impact our financial condition.

Under the terms of the lease agreements with our contract oil drilling company leaseholders or Lessees, we have very little control over the number of wells that our Lessees choose to drill on our mineral rights properties and how much production they generate.

Our current business model relates to the potential generation of revenue from royalties tied to certain leases on property covered in part by mineral rights owned by us. These leases have been granted to Lessees who are experienced exploration and operating oil companies, who have prior experience in drilling deep lateral multi-fracture horizontal wells. Pursuant to the terms and conditions of the leases, we have no influence with regard to when the drilling will be undertaken, no decision making ability as to the location of any future wells and no influence as to the rate the wells are produced, if the operators are successful, of which there is no assurance.

The success and timing of development activities by Lessees will depend on a number of factors that will largely be out of our control, including:

| ● | the timing and amount of capital expenditures; |

| ● | their expertise and financial resources; |

| ● | approval of other participants in drilling wells; |

| ● | selection of technology; and |

| ● | the rate of production of reserves, if any. |

We have no control over the operational effectiveness or financial wherewithal of our operators.

Our current business model relies heavily upon our operators and their operational effectiveness and financial wherewithal. Therefore, our operating revenue and cash flow may be heavily impacted if our operators are not effective or accurate when determining our net royalty revenue.

Similarly, our business model is heavily predicated upon our operator’s ability to pay royalty when due and to have sufficient capital to maintain existing wells and to drill new wells.

We have no previous operating history in the oil and gas industry, which may raise substantial doubt as to our ability to successfully develop profitable business operations.

We have a limited operating history. Our business operations must be considered in light of the risks, expenses, and difficulties frequently encountered in establishing a business in the oil and natural gas industries. There is nothing at this time on which to base an assumption that our business operations will prove to be successful in the long-term. Our future operating results will depend on many factors, including:

| ● | our ability to raise adequate working capital; |

| ● | success of the development and exploration program conducted by the oil company Lessees operating on our property; |

| ● | demand for natural gas and oil; |

| ● | the level of our competition; |

| ● | our ability to attract and maintain key management and employees; and |

| ● | the ability of the of the oil company Lessees to efficiently explore, develop and produce sufficient quantities of marketable natural gas or oil in a highly competitive and speculative environment while maintaining quality and controlling costs. |

18

To achieve profitable operations in the future, we are primarily dependent upon the oil company Lessees to successfully execute on the factors stated above, along with continuing to develop strategies and relationships to enhance our revenue by financially participating and investing in various drilling programs with third parties. Despite their best efforts, our Lessees may not be successful in their exploration or development efforts or obtain required regulatory approvals on the property where BRI is entitled to a production royalty. There is a possibility that some, or most, of the wells to be drilled on our mineral rights properties may never produce natural gas or oil.

Our management team does not have extensive experience in public company matters, which could impair our ability to comply with legal and regulatory requirements.

Our management team has had limited public company management experience or responsibilities, which could impair our ability to comply with legal and regulatory requirements such as the Sarbanes-Oxley Act of 2002 and other federal securities laws applicable to reporting companies, including filing required reports and other information required on a timely basis. It may be expensive to implement programs and policies in an effective and timely manner that adequately respond to increased legal, regulatory compliance and reporting requirements imposed by such laws and regulations, and we may not have the resources to do so. Our failure to comply with such laws and regulations could lead to the imposition of fines and penalties and further result in the deterioration of our business and decreased value of our stock.

If we fail to maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud.

Internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate. If we cannot provide reliable financial reports or prevent fraud, our reputation and operating results could be harmed. We cannot be certain that our efforts to maintain our internal controls will be successful, that we will be able to maintain adequate controls over our financial processes and reporting in the future or that we will be able to continue to comply with our obligations under Section 404 of the Sarbanes-Oxley Act of 2002. Any failure to maintain effective internal controls, or difficulties encountered in implementing or improving our internal controls, could harm our operating results or cause us to fail to meet certain reporting obligations.

Our lack of diversification will increase the risk of an investment in BRI, and our financial condition and results of operations may deteriorate if we fail to diversify.

Our business focus predominately is on the oil and gas industry on our oil and gas mineral rights property, located in McKenzie County, North Dakota. Larger companies have the ability to manage their risk by diversification. However, we currently lack diversification, in terms of both the nature and geographic scope of our business. As a result, we will likely be impacted more acutely by factors affecting our industry or the regions in which we operate than we would if our business were more diversified, enhancing our risk profile. If we cannot diversify or expand our operations, our financial condition and results of operations could deteriorate. We have been solely dependent on the expertise of our Lessees as the operator of our property.

Uncertain future royalty payment and limited influence on future drilling and exploration.

Our current business model relates to the potential generation of revenue from royalties tied to certain leases owned by us. These leases have been granted to experienced exploration and operating companies, both of whom have prior experience in drilling deep lateral multi-fracture horizontal wells. Pursuant to the terms and conditions of the leases, we have no influence with regard to when the drilling will be undertaken, no decision making ability as to the location of any future wells and no influence as to the rate the wells are produced, there are no assurances as to the success of the operators.

Strategic relationships upon which we may rely on are subject to change, which may diminish our ability to conduct our operations.

Our ability to successfully acquire additional mineral rights properties, to participate in drilling opportunities, and to identify and enter into commercial arrangements with other third party companies will depend on developing and maintaining close working relationships with industry participants and on our ability to select and evaluate suitable properties and to consummate transactions in a highly competitive environment. These realities are subject to change and may impair our ability to grow.

To continue to develop our business, we will endeavor to use the business relationships of our management to identify, screen, and enter into strategic relationships, which may take the form of joint ventures with other private parties and contractual arrangements with other operating oil and gas exploration companies. We may not be able to establish these strategic relationships, or if established, we may not be able to maintain them. Even if we are able to engage in joint venture and enter into strategic investment relationships with existing operators, they may not be pursuant to terms and conditions that are favorable to us. In addition, the dynamics of our relationships with strategic partners may require us to incur expenses or undertake activities we would not otherwise be inclined to in order to fulfill our obligations to these partners or maintain our relationships. If our strategic relationships are not established or maintained, our business prospects may be limited, which could diminish our ability to conduct our operations.

19

Our acquisition or disposition strategy will subject us to certain risks associated with the inherent uncertainty in evaluating such transactions.

Our decision to acquire or dispose of a property will depend in part on the evaluation of data obtained from production reports and engineering studies, geophysical and geological analyses and seismic and other information, the results of which are often inconclusive and subject to various interpretations. Also, our reviews of acquired properties are inherently incomplete because it generally is not feasible to perform an in-depth review of the individual properties involved in each acquisition. Similarly, if we elect to see any of our current assets, we cannot be assured that all material information will be available to us to adequately evaluate the merits of such a sale. Even a detailed review of records and properties may not necessarily reveal existing or potential problems, nor will it permit us to become sufficiently familiar with the properties to assess fully their deficiencies and potential. Inspections may not always be performed on every well, and environmental problems, such as ground water contamination, are not necessarily observable even when an inspection is undertaken.

Any acquisition involves other potential risks, including, among other things:

| ● | the validity of our assumptions about reserves, future production, revenues and costs; |

| ● | in the case of an acquisition, a decrease in our liquidity by using a significant portion of our cash from operations or borrowing capacity to finance acquisitions; |

| ● | in the case of an acquisition, a significant increase in our interest expense or financial leverage if we incur additional debt to finance acquisitions; |

| ● | the assumption of unknown liabilities, losses or costs for which we are not indemnified or for which our indemnity is inadequate; |

| ● | an inability to hire, train or retain qualified personnel to manage and operate our growing business and assets; and |

| ● | an increase in our costs or a decrease in our revenues associated with any potential royalty owner or landowner claims or disputes; |

| ● | in the case of any disposition, the risk that any such transaction may be undervalued based on information that may become available following the disposition of such assets |

Competition in obtaining rights to explore and develop oil and gas reserves and for our Lessee to market any future production may impair our business.

The oil and gas industry is highly competitive. This competition is increasingly intense as prices of oil and natural gas on the commodities markets have increased in recent years. Additionally, other companies engaged in our line of business may compete with us from time to time in obtaining capital from investors. Competitors include larger companies which, in particular, may have access to greater resources, may be more successful in the recruitment and retention of qualified employees and may conduct their own refining and petroleum marketing operations, which may give them a competitive advantage. In addition, actual or potential competitors may be strengthened through acquisitions. If we are unable to compete effectively or adequately respond to competitive pressures, this inability may materially adversely affect our results of operation and financial condition.

Seasonal weather conditions adversely affect operators’ ability to conduct drilling activities in the areas where our properties are located.

Seasonal weather conditions can limit drilling and producing activities and other operations in our operating areas and as a result, a majority of the drilling on our properties is generally performed during the summer and fall months. These seasonal constraints can pose challenges for meeting well drilling objectives and increase competition for equipment, supplies and personnel during the summer and fall months, which could lead to shortages and increase costs or delay operations. Additionally, many municipalities impose weight restrictions on the paved roads that lead to jobsites due to the muddy conditions caused by spring thaws. This could limit access to jobsites and operators’ ability to service wells in these areas.

Reliance on Consultants

Since Bakken uses a number of consultants, such consultants may not be subject to the standard internal controls that the Company has for its employees. Therefore, certain risks may be difficult for the Company to detect with respect to its consultants, such as direct, day-to-day oversight of consultant activities.

20

Net Royalty Interest Volatility

The Company’s cumulative net royalty interest is a result of (a) the product of net mineral acreage for each well and (b) the royalty percentage divided by (c) the spacing unit acreage declared by the state of North Dakota. The Company’s cumulative net royalty interest is subject to volatility for the following reasons:

| 1) |

Split Mineral Estate: When the minerals were transferred into the Company from HEDC, only the mineral rights from the surface to the base of the Bakken formation were transferred. Therefore, the Company does not accrue royalty revenue from gross production from the any formation below the Bakken formation relating to the mineral rights that were purchased from HEDC. | ||

| 2) |

Varying Lease Royalty Percentages: The Company has sixteen different leases, each with stated royalty percentages that vary from 16% to 20%. Each lease can support many wells. Therefore, the Company’s cumulative net royalty interest is affected by the number of wells producing from each lease. If more wells are producing from leases with lower stated royalty percentages, this will reduce the Company’s net royalty interests and reduce revenue as well. |

Operator Affiliate Sales

Many oil and natural gas production companies (operators) have wholly owned subsidiaries that purchase natural gas for resale. These sales, called affiliate sales, are not the result of an arm’s length transaction and are sometimes not permitted under the applicable mineral lease. Since royalties are based upon the gross revenue from the wellhead sale, the Company’s royalty revenue may be adversely impacted by such an affiliate sale.

Large Shareholders

Certain shareholders hold large portions of shares of the Company’s stock. As a result, the possibility exists that significant actions (such as voting or changing members of the Company’s Board of Directors) may occur by written consent rather than following a publicly filed document soliciting the vote or consent of the Company’s shareholders.

Risks Relating to the Ownership of Bakken Resources, Inc. Common Stock

Risks relating to low priced stocks will likely apply to our common stock.

Although our common stock is approved for trading on the OTC Bulletin Board, there has only been little trading activity in the stock. Accordingly, there is limited history on which to estimate the future trading price range of the common stock. If the common stock trades below $5.00 per share, trading in the common stock will be subject to the requirements of certain rules promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which require additional disclosure by broker-dealers in connection with any trades involving a stock defined as a penny stock (generally, any non-FINRA equity security that has a market price share of less than $5.00 per share, subject to certain exceptions). Such rules require the delivery, prior to any penny stock transaction, of a disclosure schedule explaining the penny stock market and the risks associated therewith and impose various sales practice requirements on broker-dealers who sell penny stocks to persons other than established customers and accredited investors (generally defined as an investor with a net worth in excess of $1,000,000 or annual income exceeding $200,000 individually or $300,000 together with a spouse). For these types of transactions, the broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to the sale. The broker-dealer also must disclose the commissions payable to the broker-dealer, current bid and offer quotations for the penny stock and, if the broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market. Such information must be provided to the customer orally or in writing before or with the written confirmation of trade sent to the customer. Monthly statements must be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks. The additional burdens imposed upon broker-dealers by such requirements could discourage broker-dealers from effecting transactions in the common stock which could severely limit the market liquidity of the common stock and the ability of holders of the common stock to sell it.

21

Limitations on the liability of our directors and officers under our Articles of Incorporation and our Bylaws may result in us indemnifying such officers and directors.

Our Articles of Incorporation include provisions to eliminate, to the fullest extent permitted by Nevada General Corporation Law as in effect from time to time, the personal liability of directors of BRI for monetary damages arising from a breach of their fiduciary duties as directors. The Articles of Incorporation also includes provisions to the effect that we shall, to the maximum extent permitted from time to time under the laws of the State of Nevada, indemnify any director or officer. In addition, our bylaws require us to indemnify, to the fullest extent permitted by law, any director, officer, employee or agent of BRI for acts which such person reasonably believes are not in violation of our corporate purposes as set forth in the Articles of Incorporation.

Potential future issuances of additional common and preferred stock would dilute our current stockholders.

We are authorized to issue up to 100,000,000 shares of common stock. To the extent of such authorization, the board of directors of BRI will have the ability, without seeking stockholder approval, to issue additional shares of common stock in the future for such consideration as the board of directors may consider sufficient. The issuance of additional common stock in the future will reduce the proportionate ownership and voting power of the common stock offered hereby. We are also authorized to issue up to 10,000,000 shares of preferred stock, the rights and preferences of which may be designated in series by the board of directors. To the extent of such authorization, such designations may be made without stockholder approval. The designation and issuance of series of preferred stock in the future would create additional securities which would have dividend and liquidation preferences over the currently outstanding common stock. In addition, the ability to issue any future class or series of preferred stock could impede a non-negotiated change in control and thereby prevent stockholders from obtaining a premium for their common stock.

There is no assurance that a liquid public market for our common stock will develop.

Although our shares of common stock are currently eligible for quotation on the OTC Bulletin Board and the Pink Sheets, there has been no significant trading in our common stock. There has been no long term established public trading market for our common stock, and there can be no assurance that a regular and established market will be developed and maintained for the securities in the future. There can also be no assurance as to the depth or liquidity of any market for the common stock or the prices at which holders may be able to sell the shares.

The market price of our common stock is, and is likely to continue to be, highly volatile and subject to wide fluctuations.

In the event that a public market for our common stock is created, market prices for the common stock will be influenced by many factors, some of which are beyond our control, including:

| ● | dilution caused by our issuance of additional shares of common stock and other forms of equity securities, which we expect to make in connection with future capital financings to fund our operations and growth, to attract and retain valuable personnel and in connection with future strategic partnerships with other companies; |

| ● | announcements of new acquisitions, reserve discoveries or other business initiatives by our competitors; |

| ● | our ability to take advantage of new acquisitions, reserve discoveries or other business initiatives; |

| ● | fluctuations in revenue from our oil and gas business as new reserves come to market; |

| ● | changes in the market for oil and natural gas commodities and/or in the capital markets generally; |

| ● | changes in the demand for oil and natural gas, including changes resulting from the introduction or expansion of alternative fuels; |

| ● | quarterly variations in our revenues and operating expenses; |

| ● | changes in the valuation of similarly situated companies, both in our industry and in other industries; |

| ● | changes in analysts’ estimates affecting our company, our competitors and/or our industry; |

| ● | changes in the accounting methods used in or otherwise affecting our industry; |

| ● | additions and departures of key personnel; |