Attached files

| file | filename |

|---|---|

| 8-K - TAIWAN FUND INC | fp0020439_8k.htm |

Investment objective

The Fund’s investment objective is to seek long-term capital appreciation primarily through investments in equity securities listed in Taiwan.

|

Fund facts

|

(as at 06/30/16)

|

|

Net asset value per share

|

$17.66

|

|

Market price

|

$15.25

|

|

Premium/discount

|

-13.65%

|

|

Total net assets

|

$145.26 m

|

|

Market cap

|

$125.42 m

|

|

Fund statistics

|

|

|

Investment adviser (date of appointment)

|

JF International Management, Inc. (07/22/14)

|

|

Fund manager

|

Shumin Huang

|

|

Listed

|

NYSE

|

|

Launch date

|

12/23/86

|

|

Shares outstanding

|

8,224,330

|

|

Last dividend (Ex-dividend date)

|

$2.6332

(December 26, 2014)

|

|

Benchmark

|

TAIEX Total Return Index

|

|

Fund codes

|

|

|

Bloomberg

|

TWN

|

|

Sedol

|

286987895

|

|

CUSIP

|

874036106

|

|

ISIN

|

US8740361063

|

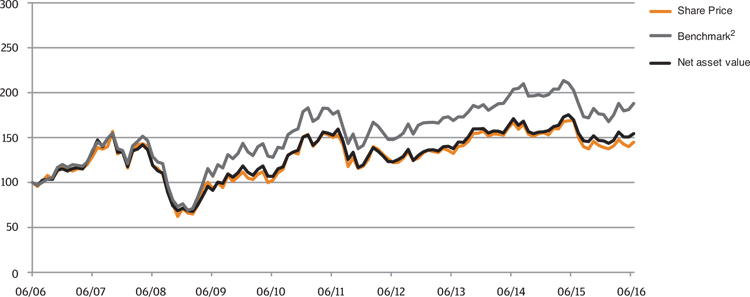

| 10 year performance data |

(as at 06/30/16)

|

|

Cumulative Performance1

|

(as at 06/30/16)

|

||||||

|

%

|

1m

|

3m

|

YTD

|

1Y

|

3Y

|

5Y

|

10Y

|

|

The Taiwan Fund, Inc.

|

2.5

|

-1.1

|

5.5

|

-9.1

|

12.2

|

1.1

|

54.5

|

|

Market Price

|

3.5

|

-1.9

|

4.2

|

-14.3

|

9.5

|

-3.5

|

44.9

|

|

TSE Index

|

2.6

|

-1.1

|

5.8

|

-11.1

|

-0.1

|

-10.8

|

29.7

|

|

TAIEX Total Return Index2

|

3.8

|

0.0

|

7.0

|

-7.3

|

11.2

|

6.8

|

87.9

|

|

MSCI Taiwan Index

|

4.5

|

0.7

|

8.5

|

-8.8

|

12.7

|

8.4

|

55.0

|

|

Rolling 12 month performance1

|

(as at 06/30/16)

|

||||

|

%

|

2016/2015

|

2015/2014

|

2014/2013

|

2013/2012

|

2012/2011

|

|

The Taiwan Fund, Inc.

|

-9.1

|

-0.7

|

24.3

|

11.7

|

-19.4

|

|

Market Price

|

-14.3

|

1.3

|

26.1

|

8.3

|

-18.7

|

|

TSE Index

|

-11.1

|

-4.0

|

16.9

|

10.2

|

-19.0

|

|

TAIEX Total Return Index2

|

-7.3

|

-0.5

|

20.6

|

14.3

|

-16.0

|

|

MSCI Taiwan Index

|

-8.8

|

3.0

|

20.0

|

14.1

|

-15.7

|

|

Top 10 holdings

|

(as at 06/30/16)

|

|

Holding

|

Fund %

|

|

Taiwan Semiconductor Manufacturing Co., Ltd.

|

10.0

|

|

Largan Precision Co., Ltd.

|

5.9

|

|

Tung Thih Electronic Co., Ltd.

|

3.9

|

|

Ennoconn Corp.

|

3.5

|

|

Yeong Guan Energy Technology Group Co., Ltd.

|

3.1

|

|

Hon Hai Precision Industry Co., Ltd.

|

3.1

|

|

Advanced Semiconductor Engineering, Inc.

|

3.1

|

|

Eclat Textile Co., Ltd.

|

3.0

|

|

Formosa Petrochemical Corp.

|

2.9

|

|

Uni-President Enterprises Corp.

|

2.9

|

|

1

|

In US Dollar terms

|

|

2

|

TAIEX Total Return Index (prior to January 1, 2003, TAIEX Index)

|

|

Sector breakdown

|

(as at 06/30/16)

|

||

|

Sector Allocation

|

Fund %

|

Benchmark

|

Deviation

|

|

Automobile

|

0.0%

|

1.4%

|

-1.4%

|

|

Biotechnology & Medical Care

|

0.0%

|

0.9%

|

-0.9%

|

|

Building Material & Construction

|

0.0%

|

1.7%

|

-1.7%

|

|

Cement

|

0.9%

|

1.0%

|

-0.1%

|

|

Chemical

|

0.0%

|

1.0%

|

-1.0%

|

|

Communications & Internet

|

2.1%

|

7.4%

|

-5.3%

|

|

Computer & Peripheral Equipment

|

8.9%

|

6.1%

|

2.8%

|

|

Electric & Machinery

|

9.1%

|

1.9%

|

7.2%

|

|

Electrical & Cable

|

0.0%

|

0.3%

|

-0.3%

|

|

Electronic Parts & Components

|

4.7%

|

4.4%

|

0.3%

|

|

Electronic Products Distribution

|

0.0%

|

0.8%

|

-0.8%

|

|

Financial & Insurance

|

6.7%

|

12.5%

|

-5.8%

|

|

Foods

|

2.9%

|

2.3%

|

0.6%

|

|

Glass & Ceramic

|

0.0%

|

0.2%

|

-0.2%

|

|

Information Service

|

0.0%

|

0.2%

|

-0.2%

|

|

Iron & Steel

|

0.0%

|

1.9%

|

-1.9%

|

|

Oil, Gas & Electricity

|

2.9%

|

3.5%

|

-0.6%

|

|

Optoelectronic

|

7.3%

|

3.9%

|

3.4%

|

|

Other

|

6.7%

|

3.7%

|

3.0%

|

|

Other Electronic

|

8.7%

|

7.1%

|

1.6%

|

|

Paper & Pulp

|

0.0%

|

0.3%

|

-0.3%

|

|

Plastics

|

3.2%

|

6.4%

|

-3.2%

|

|

Rubber

|

0.0%

|

1.4%

|

-1.4%

|

|

Semiconductor

|

24.1%

|

24.2%

|

-0.1%

|

|

Shipping & Transportation

|

0.3%

|

1.5%

|

-1.2%

|

|

Textiles

|

4.7%

|

1.8%

|

2.9%

|

|

Tourism

|

0.0%

|

0.5%

|

-0.5%

|

|

Trading & Consumers' Goods

|

3.2%

|

1.7%

|

1.5%

|

|

Cash

|

3.6%

|

0.0%

|

3.6%

|

|

Overal Total

|

100.0%

|

100.0%

|

0.0%

|

Review

The TAIEX Total Return Index (TAIEX) gained 3.8% in the month of June. The index had a positive start to the month but suffered declines on concerns over the potential US Federal Reserve interest rate increase and the result of the United Kingdom's referendum vote to leave the European Union (Brexit). Bargain hunters stepped in towards the end of June and bought mainly large-cap stocks, driving the market back up. The cement and property sectors experienced a strong performance in June. The technology sector also outperformed, led by undervalued areas such as Liquid Crystal Display (LCD), Light Emitting Diode (LED) and Dynamic Random Access Memory (DRAM). The Fund underperformed the TAIEX by 1.3% in June.

Positioning and Contributors

The Fund's overweight holdings in auto parts companies in the electrical & machinery sector contributed to returns after rebounding from a severe correction following weaker than expected April sales. A key Apple component supplier also rose on signs of increasing adoption of dual lens cameras in Apple smartphones. In contrast, the Fund's overweight position in textile continued to take a toll on performance. Several other growth names in the electric & machinery and semiconductor sectors also suffered declines as investors favored value and searched for yield. The rising strength of the micro-chip industry also detracted from performance due to the Fund's underweight position in that sector.

There was no change to the Fund's investment strategy with a continued focus on quality companies with strong growth profiles. The Fund's preference is for sustainable consumer discretionary growth names with a sustainable franchise. This includes the sportswear and auto parts sector. Given the weak overall demand for personal computers (PC), note books (NB), televisions (tv) and handsets, the Fund's positions in tech stocks remain focused on the cloud, the internet of things (IOT), gaming and the semi-conductor sectors. The Fund also continues to be underweight in communications, basic material and financial sectors.

Outlook

The key market risk in the third quarter of 2016 (3Q16) is expected to be the market reaction to the Brexit vote. The potential for weak consumer demand for the new iPhone seems to be another factor concerning the market, although market expectations are already anticipating modest demand. However, the Taiwan market could be regarded as relatively defensive, supported by companies with strong free-cash-flow and an average potential dividend yield of 4.2%. Given the low base, we expect to see sequential improvement in the technology and consumer areas in 3Q16.

|

Full portfolio holdings

|

(as at 06/30/16)

|

|

|

Holding

|

Market Value

USD

|

Fund

%

|

|

Semiconductor

|

35,085,061

|

24.1

|

|

Taiwan Semiconductor Manufacturing Co., Ltd.

|

14,497,505

|

10.0

|

|

Advanced Semiconductor Engineering, Inc.

|

4,488,798

|

3.1

|

|

MediaTek, Inc.

|

3,282,681

|

2.2

|

|

Win Semiconductors Corp.

|

3,024,216

|

2.1

|

|

Realtek Semiconductor Corp.

|

2,604,417

|

1.8

|

|

ASPEED Technology, Inc.

|

2,153,907

|

1.5

|

|

Silicon Motion Technology Corp.

|

1,912,000

|

1.3

|

|

Silergy Corp.

|

1,792,802

|

1.2

|

|

Siliconware Precision Industries Co.

|

1,194,199

|

0.8

|

|

Egis Technology, Inc.

|

134,536

|

0.1

|

|

Electric & Machinery

|

13,194,942

|

9.1

|

|

Yeong Guan Energy Technology Group Co., Ltd.

|

4,520,176

|

3.1

|

|

Iron Force Industrial Co., Ltd.

|

2,554,288

|

1.8

|

|

Airtac International Group

|

2,178,183

|

1.5

|

|

Macauto Industrial Co., Ltd.

|

1,530,643

|

1.1

|

|

Hota Industrial Manufacturing Co., Ltd.

|

1,329,861

|

0.9

|

|

Hiwin Technologies Corp.

|

1,081,791

|

0.7

|

|

Computer & Peripheral Equipment

|

12,910,109

|

8.9

|

|

Ennoconn Corp.

|

5,131,901

|

3.5

|

|

Inventec Co., Ltd.

|

2,649,152

|

1.8

|

|

Pegatron Corp.

|

2,179,503

|

1.5

|

|

Advantech Co., Ltd.

|

1,826,607

|

1.3

|

|

Micro-Star International Co., Ltd.

|

987,473

|

0.7

|

|

Posiflex Technology, Inc.

|

135,473

|

0.1

|

|

Other Electronic

|

12,571,674

|

8.7

|

|

Tung Thih Electronic Co., Ltd.

|

5,624,539

|

3.9

|

|

Hon Hai Precision Industry Co., Ltd.

|

4,516,087

|

3.1

|

|

Catcher Technology Co., Ltd.

|

1,604,979

|

1.1

|

|

Voltronic Power Technology Corp.

|

826,069

|

0.6

|

|

Optoelectronic

|

10,595,416

|

7.3

|

|

Largan Precision Co., Ltd.

|

8,581,481

|

5.9

|

|

Innolux Corp.

|

1,708,100

|

1.2

|

|

Au Optronics Corp.

|

305,835

|

0.2

|

|

Financial & Insurance

|

9,804,098

|

6.7

|

|

Mega Financial Holding Co., Ltd.

|

3,056,050

|

2.1

|

|

Cathay Financial Holding Co., Ltd.

|

2,530,798

|

1.7

|

|

Fubon Financial Holding Co., Ltd.

|

2,266,539

|

1.6

|

|

E. Sun Financial Holding Co., Ltd.

|

1,950,711

|

1.3

|

|

Other

|

9,735,245

|

6.7

|

|

Taiwan Paiho Ltd.

|

2,879,196

|

2.0

|

|

Nan Liu Enterprise Co., Ltd.

|

1,673,952

|

1.1

|

|

Nien Made Enterprise Co., Ltd.

|

1,335,162

|

0.9

|

|

Feng TAY Enterprise Co., Ltd.

|

1,319,322

|

0.9

|

|

Sunspring Metal Corp.

|

1,106,445

|

0.8

|

|

KMC Kuei Meng International, Inc.

|

995,459

|

0.7

|

|

Pou Chen Corp.

|

425,709

|

0.3

|

|

Textiles

|

6,810,132

|

4.7

|

|

Eclat Textile Co., Ltd.

|

4,382,902

|

3.0

|

|

Toung Loong Textile Manufacturing Co., Ltd.

|

2,427,230

|

1.7

|

|

Full portfolio holdings (cont'd)

|

||

|

Holding

|

Market Value

USD

|

Fund

%

|

|

Electronic Parts & Components

|

6,775,450

|

4.7

|

|

Delta Electronics, Inc.

|

3,666,331

|

2.6

|

|

King Slide Works Co., Ltd.

|

2,208,779

|

1.5

|

|

Himax Technologies, Inc.

|

900,340

|

0.6

|

|

Trading & Consumers' Goods

|

4,708,112

|

3.2

|

|

President Chain Store Corp.

|

2,349,794

|

1.6

|

|

Poya Co., Ltd.

|

1,707,089

|

1.2

|

|

Taiwan FamilyMart Co., Ltd.

|

651,229

|

0.4

|

|

Plastics

|

4,605,028

|

3.2

|

|

Formosa Plastics Corp.

|

2,320,084

|

1.6

|

|

Formosa Chemicals & Fibre Corp.

|

2,284,944

|

1.6

|

|

Oil, Gas & Electricity

|

4,277,488

|

2.9

|

|

Formosa Petrochemical Corp.

|

4,277,488

|

2.9

|

|

Foods

|

4,157,342

|

2.9

|

|

Uni-President Enterprises Corp.

|

4,157,342

|

2.9

|

|

Communications & Internet

|

3,010,710

|

2.1

|

|

Wistron NeWeb Corp.

|

2,633,262

|

1.8

|

|

Visual Photonics Epitaxy Co., Ltd.

|

377,448

|

0.3

|

|

Cement

|

1,325,357

|

0.9

|

|

Taiwan Cement Corp.

|

1,325,357

|

0.9

|

|

Shipping & Transportation

|

508,757

|

0.3

|

|

Aerospace Industrial Development Corp.

|

508,757

|

0.3

|

|

Cash

|

5,186,515

|

3.6

|

|

Cash

|

5,186,515

|

3.6

|

|

Grand Total

|

145,261,436

|

100.0

|

Source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express of implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

No further distribution or dissemination of the MSCI data is permitted without MSCI's express written consent.

Important Information

This document is issued and approved by JF International Management, Inc. (“JFIMI”), as investment advisor of The Taiwan Fund, Inc. (the ‘'Fund''). JFIMI is an investment advisor registered with the US Securities and Exchange Commission. Certain information herein is believed to be reliable but has not been verified by JFIMI. JFIMI makes no representation or warranty and does not accept any responsibility in relation to such information or for opinion or conclusion which the reader may draw from this newsletter.

The Fund is classified as a diversified investment company under the US Investment Company Act of 1940 as amended. It meets the criteria of a closed end US fund and its shares are listed on the New York Stock Exchange. JFIMI has been appointed investment advisor to the Fund.

This newsletter does not constitute an offer of shares. Closed-end funds, unlike open-end funds, are not continuously offered. After the initial public offering, shares are bought and sold on the open market through a stock exchange. JFIMI, its ultimate and intermediate holding companies, subsidiaries, affiliates, clients, directors or staff may, at any time, have a position in the market referred to herein, and may buy or sell securities, currencies, or any other financial instruments in such markets. The information or opinion expressed in this newsletter should not be construed to be a recommendation to buy or sell any security, including the securities, commodities, currencies or financial instruments referred to herein.

Portfolio holdings are subject to change daily.

It should not be assumed that any of the securities transactions or holdings discussed here were or will prove to be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance of the securities discussed herein.

Investing in the Fund involves certain considerations in addition to the risks normally associated with making investments in securities. The value of the shares issued by the Fund, and the income from them, may go down as well as up and there can be no assurance that upon sale, or otherwise, investors will receive back the amount originally invested. There can be no assurance that you will receive comparable performance returns. Movements in foreign exchange rates may have a separate effect, unfavorable as well as favorable, on the gain or loss otherwise experienced on an investment. Past performance is not a guide to future returns. Accordingly, the Fund is only suitable for investment by investors who are able and willing to withstand the total loss of their investment. In particular, prospective investors should consider the following risks:

Discretionary investment is not risk-free. The past operating performance does not guarantee a minimum return for the discretionary investment fund. Apart from exercising the duty of care of a prudent adviser, JFIMI will not be responsible for the profit or loss of the discretionary investment fund, nor guarantee a minimum return.

| • | It should be noted that investment in the Fund is only suitable for sophisticated investors who are aware of the risk of investing in Taiwan and should be regarded as long term. Funds which invest in one country carry a higher degree of risk than those with portfolios diversified across a number of markets. |

| • | Investment in the securities of smaller and unquoted companies can involve greater risk than is customarily associated with investment in larger, more established, companies. In particular, smaller companies often have limited product lines, markets or financial resources and their management may be dependent on a smaller number of key individuals. In addition, the market for stock in smaller companies is often less liquid than that for stock in larger companies, bringing with it potential difficulties in acquiring, valuing and disposing of such stock. Proper information for determining their value, or the risks to which they are exposed, may not be available. |

| • | Investments within emerging markets such as Taiwan can be of higher risk. Many emerging markets, and the companies quoted on their stock exchanges, are exposed to the risks of political, social and religious instability, expropriation of assets or nationalization, rapid rates of inflation, high interest rates, currency depreciation and fluctuations and changes in taxation which may affect the Fund's income and the value of its investments. |

| • | The marketability of quoted shares may be limited due to foreign investment restrictions, wide dealing spreads, exchange controls, foreign ownership restrictions, the restricted opening of stock exchanges and a narrow range of investors. Trading volume may be lower than on more developed stock markets, and equities are less liquid. Volatility of prices can also be greater than in more developed stock markets. The infrastructure for clearing, settlement and registration on the primary and secondary markets may be undeveloped. Under certain circumstances, there may be delays in settling transactions in some of the markets. |