As filed with the Securities and Exchange Commission on June 14, 2016

Registration No. 333-211858 SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 1

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Bank of Montreal

Initial Depositor

(Exact name of registrant as specified in charter)

Vaulted Gold Bullion Trust

Issuer with respect to the Gold Deposit Receipts

|

Delaware

|

1040

|

46-7176227

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(Primary Standard Industrial Classification Code Number)

|

(I.R.S. Employer Identification Number)

|

|

|

100 King Street

First Canadian Place

Toronto, Ontario

Canada M5X 1A1

(416) 867-6785

(Address, including zip code, and telephone number, including area code, or registrant’s principal executive offices)

Colleen Hennessy

Bank of Montreal

111 West Monroe Street

P. O. Box 755

Chicago, Illinois 60690

(312) 461-7745

|

|||

Copies to:

|

Anna T. Pinedo, Esq.

Morrison & Foerster LLP

250 West 55th Street

New York, New York 10019

(212) 468-8179

|

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

|

|

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ý

|

|

|

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

|

|

|

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

|

|

|

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

Non-accelerated filer x

|

Smaller reporting company o

|

(Do not check if a smaller reporting company)

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered

|

Proposed Maximum

Aggregate Offering

Price (1)

|

Amount of

Registration Fee (2)

|

|

Class A, Class F and Class F-1 Gold Deposit Receipts

|

$500,000,000.00

|

$50,350.00

|

(1) Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457 under the Securities Act.

(2) Pursuant to Rule 457(p) under the Securities Act, the securities registered pursuant to this registration statement include unsold securities previously registered by the registrant on the registrant's registration statement (File No. 333-194144) filed on October 24, 2014 and declared effective on November 21, 2014 (the “2014 Registration Statement”). The 2014 Registration Statement registered the offer and sale of Gold Deposit Receipts having an aggregate initial offering price of $500,000,000, all of which remain unsold as of the date of filing this registration statement (the “Unsold Securities”). The registrant has determined to include the Unsold Securities in this registration statement and to apply $50,350.00 of the filing fee of $64,400.00 relating to the Unsold Securities under the 2014 Registration Statement to the securities registered pursuant to this registration statement.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

$500,000,000 of Gold Deposit Receipts

Vaulted Gold Bullion Trust

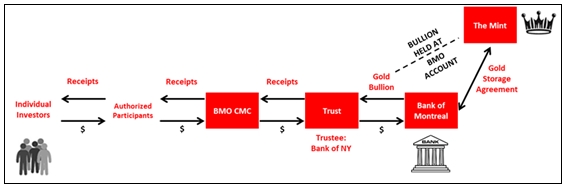

The Vaulted Gold Bullion Trust (the “Trust”) will issue Depositary Receipts (the “Gold Deposit Receipts”) representing your undivided beneficial ownership in a fixed quantity of unencumbered, allocated, physical gold bullion (“Gold Bullion”). The Gold Bullion will be held for the benefit of holders of Gold Deposit Receipts in an account operated by Bank of Montreal at the Royal Canadian Mint (the “Mint”). The Bank of New York Mellon will be the trustee of the Trust. The Gold Deposit Receipts are separate from the Gold Bullion.

Investing in the Gold Deposit Receipts involves a high degree of risk. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” starting on page 11. An investment in the Gold Deposit Receipts represents an investment in gold, which may not be appropriate for all investors.

The Trust is offering to the public on a continuous basis three classes of Gold Deposit Receipts: Class A Gold Deposit Receipts; Class F Gold Deposit Receipts; and Class F-1 Gold Deposit Receipts. The only difference among these classes of Gold Deposit Receipts relates to the sales fee applicable to each class.

The public offering price for each Gold Deposit Receipt will be based on the spot price at the time of purchase for one troy ounce of Gold Bullion, determined by BMO Capital Markets Corp. using EBS, an offering of EBS BrokerTec (“EBS”), as the source for the spot price of gold, without adjustment or modification, plus a deposit fee of 2.00%, payable to Bank of Montreal, plus (1) in the case of a Class A Gold Deposit Receipt, a sales fee of 2.00% to any participating broker-dealer that sells Gold Deposit Receipts to an investor; (2) in the case of a Class F Gold Deposit Receipt, which will be sold only through fee-based programs, a sales fee of 0.25%; and (3) in the case of Class F-1 Gold Deposit Receipts, which will be sold to trust or fiduciary accounts, no additional fee. The Trust will use the proceeds of the issuance of Gold Deposit Receipts, net of these fees, to purchase Gold Bullion from Bank of Montreal in an amount that corresponds to the amount of Gold Deposit Receipts.

The indicative initial price to public shown below is the price to public on a particular date. An investor considering a purchase or redemption of Gold Deposit Receipts may obtain end of day indicative pricing from the Trust’s website. Real-time indicative quotations are available from the Bloomberg Terminal (“Bloomberg”) using <BMOEGLDR Index Go> and these quotations also will be available (on a delayed basis) at Bloomberg.com. YOUR BROKER WILL CONFIRM THE EXECUTION PRICE TO YOU; DUE TO MOVEMENTS IN THE SPOT PRICE, THE EXECUTION PRICE MAY DIFFER FROM THE INDICATIVE OR THE QUOTED PRICE. See “Description of Gold Deposit Receipts — How to Obtain Pricing Information” and “Plan of Distribution.”

The Trust is newly formed. The Trust is not an investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust is not a commodity pool for purposes of the Commodity Exchange Act, and the initial depositor is not subject to regulation by the Commodity Futures Trading Commission as a commodity pool, or a commodity trading advisor.

The Trust is an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or JOBS Act, and, as such, may elect to comply with certain reduced reporting requirements after this offering.

The Gold Deposit Receipts are neither interests in, nor obligations of, the initial depositor, Bank of Montreal, or The Bank of New York Mellon, as trustee.

The Gold Deposit Receipts will not be listed or traded on any securities exchange. Only Authorized Participants may offer the Gold Deposit Receipts to the public. Under no circumstance may any purchase of the Gold Deposit Receipts be made with borrowed or leveraged funds advanced by an Authorized Participant. No margin purchases of the Gold Deposit Receipts will be accepted.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

Indicative Initial Price To Public*

|

Deposit and Sales Fee**

|

|

|

Per Class A Gold Deposit Receipt

|

$1,332.76

|

4.00%

|

|

Per Class F Gold Deposit Receipt

|

$1,310.33

|

2.25%

|

|

Per Class F-1 Gold Deposit Receipt

|

$1,307.13

|

2.00%

|

______________________

* The initial price to public as of 12 PM EST on June 14, 2016, which reflects a spot price of $1,281.50, as provided on EBS, plus the deposit and, if applicable, a sales fee.

** Reflects a deposit fee of 2.00%. In addition, reflects a sales fee for each Class A Gold Deposit Receipt of 2.00% and a sales fee for each Class F Gold Deposit Receipt of 0.25%. There is no sales fee for Class F-1 Gold Deposit Receipts. See “Plan of Distribution” beginning on page 52 for additional information regarding fees payable to Authorized Participants.

BMO Capital Markets Corp. will use the spot price of gold reflected on EBS as the source for the spot price of gold. BMO Capital Markets Corp. will refer to this source without adjustment or modification. If, for any reason, EBS is not posting spot prices, BMO Capital Markets Corp. will use the spot price reflected by the London Bullion Market Association (the “LBMA”) (PM) Gold Price, an offering of ICE Benchmark Administration (the “IBA”), as its source for the spot price of gold. BMO Capital Markets Corp. will refer to this source without adjustment or modification. On any given day, the price to public will vary.

A minimum of one whole Gold Deposit Receipt must be purchased in any transaction. BMO Capital Markets Corp. will act as the underwriter of this continuous offering, purchasing, on a principal basis, Gold Deposit Receipts when issued by the Trust and reselling the Gold Deposit Receipts to Authorized Participants.

BMO CAPITAL MARKETS

_____________________________

The date of this prospectus is , 2016.

|

Page

|

|

|

1

|

|

|

4

|

|

|

11

|

|

|

21

|

|

|

22

|

|

|

23

|

|

|

27

|

|

|

34

|

|

|

42

|

|

|

44

|

|

|

46

|

|

|

49

|

|

|

52

|

|

|

54

|

|

|

54

|

_______________________________________

This prospectus contains information you should consider when making your investment decision. With respect to information about Gold Deposit Receipts, you should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell Gold Deposit Receipts in any jurisdiction where the offer or sale is not permitted.

The Gold Deposit Receipts are not registered for public sale outside of the United States. Holders that are not U.S. holders (as defined under “U.S. Federal Income Tax Consequences”) should consult their tax advisors regarding U.S. withholding and other taxes that may apply to ownership of the Gold Deposit Receipts or of the Gold Bullion through an investment in the Gold Deposit Receipts.

SALES RESTRICTIONS AND NOTICES

THE GOLD DEPOSIT RECEIPTS MAY BE SOLD TO INSTITUTIONAL INVESTORS IN ANY STATE AND PUERTO RICO. RETAIL INVESTORS SHOULD FAMILIARIZE THEMSELVES WITH THE FOLLOWING RESTRICTIONS AND NOTICES:

THE GOLD DEPOSIT RECEIPTS ARE NOT APPROVED FOR SALE AND SHOULD NOT BE SOLD TO RESIDENTS OF THE STATES OF ALABAMA, ARIZONA OR TENNESSEE, OTHER THAN TO INSTITUTIONAL INVESTORS. ALL SALES IN THE STATE OF TEXAS WILL ONLY BE MADE BY A TEXAS-REGISTERED BROKER-DEALER. ALL SALES IN THE STATE OF NORTH CAROLINA WILL ONLY BE MADE BY A NORTH CAROLINA REGISTERED BROKER-DEALER.

CALIFORNIA INVESTORS MUST BE ABLE TO EVIDENCE EITHER: (A) $65,000 ANNUAL GROSS INCOME AND $250,000 LIQUID NET WORTH (AS DEFINED BELOW); OR (B) $500,000 LIQUID NET WORTH.

OREGON AND OKLAHOMA INVESTORS MUST BE ABLE TO EVIDENCE A LIQUID NET WORTH OF $250,000 OR MORE TO INVEST IN THIS OFFERING. TEXAS INVESTORS MUST BE ABLE TO EVIDENCE EITHER (A) $100,000 ANNUAL NET INCOME AND $100,000 NET WORTH OR (B) $250,000 LIQUID NET WORTH.

IT SHALL BE UNSUITABLE FOR A RETAIL INVESTOR’S AGGREGATE INVESTMENT IN GOLD DEPOSIT RECEIPTS TO EXCEED TEN PERCENT (10%) OF HIS, HER, OR ITS LIQUID NET WORTH.

“LIQUID NET WORTH” SHALL BE DEFINED AS THAT PORTION OF NET WORTH (TOTAL ASSETS EXCLUSIVE OF HOME, HOME FURNISHINGS, AND AUTOMOBILES MINUS TOTAL LIABILITIES) THAT IS COMPRISED OF CASH, CASH EQUIVALENTS, AND READILY MARKETABLE SECURITIES. PLEASE CONSULT YOUR FINANCIAL AND TAX ADVISER.

INVESTORS SHOULD REVIEW CAREFULLY THE PROSPECTUS AND UNDERSTAND, AMONG OTHER THINGS, THAT: THE GOLD DEPOSIT RECEIPTS ARE NOT LISTED OR TRADED ON A SECURITIES EXCHANGE (SEE “DESCRIPTION OF GOLD DEPOSIT RECEIPTS—PURCHASES AND SALES OF GOLD DEPOSIT RECEIPTS”), THE GOLD DEPOSIT RECEIPTS DO NOT PROVIDE FOR CURRENT PAYMENTS OF INTEREST OR PRINCIPAL, HOLDERS OF THE GOLD DEPOSIT RECEIPTS WILL HAVE NO VOTING RIGHTS, EXCEPT IN LIMITED CIRCUMSTANCES (SEE “DESCRIPTION OF THE GOLD DEPOSIT RECEIPTS—VOTING RIGHTS”), AND ONLY HOLDERS LOCATED IN A DELIVERY STATE WILL BE ABLE TO RECEIVE DELIVERY OF BULLION (SEE “DESCRIPTION OF THE GOLD DEPOSIT RECEIPTS—REDEMPTIONS OF GOLD DEPOSIT RECEIPTS FOR GOLD BULLION; SALES FOR CASH—PHYSICAL DELIVERY”).

THE PRICE OF GOLD DEPOSIT RECEIPTS ON ANY DAY REPRESENTS THE PRICE AT WHICH A HOLDER CAN SELL GOLD BULLION TO BANK OF MONTREAL AND IS BASED ON U.S. DOLLAR SPOT PRICES AT THE TIME OF PURCHASE. BMO CAPITAL MARKETS CORP. WILL USE THE SPOT PRICE OF GOLD REFLECTED ON EBS AS THE SOURCE FOR THE SPOT PRICE OF GOLD. BMO CAPITAL MARKETS CORP. WILL REFER TO THIS SOURCE WITHOUT ADJUSTMENT OR MODIFICATION. IF, FOR ANY REASON, EBS IS NOT POSTING SPOT PRICES, BMO CAPITAL MARKETS CORP. WILL USE THE SPOT PRICE REFLECTED BY THE LBMA (PM) GOLD PRICE AS ITS SOURCE FOR THE SPOT PRICE OF GOLD. BMO CAPITAL MARKETS CORP. WILL REFER TO THIS SOURCE WITHOUT ADJUSTMENT OR MODIFICATION.

BANK OF MONTREAL RESERVES THE RIGHT TO CHARGE A CUSTODY FEE WITH RESPECT TO HOLDING THE TRUST’S GOLD BULLION AT BANK OF MONTREAL’S CUSTODIAL ACCOUNT. IF BANK OF MONTREAL WERE TO CHARGE SUCH A FEE, IT WOULD AFFECT THE TRUST’S EXPENSES AND THE PRICE OF THE GOLD DEPOSIT RECEIPTS. HOWEVER, ANY CUSTODY FEE WILL NOT EXCEED 0.50% PER ANNUM OF THE DAILY AVERAGE CLOSING PRICE OF GOLD BULLION REPRESENTED BY THE GOLD DEPOSIT RECEIPTS, AS CALCULATED BY BANK OF MONTREAL ACTING IN GOOD FAITH. FOR ADDITIONAL INFORMATION ON THE CUSTODY FEE, PLEASE SEE “DESCRIPTION OF THE GOLD DEPOSIT RECEIPTS — CUSTODY OF THE GOLD BULLION”.

THE TERM “INSTITUTIONAL INVESTOR” IS UNDERSTOOD TO MEAN: A BANK, SAVINGS AND LOAN ASSOCIATION, INSURANCE COMPANY OR REGISTERED INVESTMENT COMPANY; AN INVESTMENT ADVISER REGISTERED EITHER WITH THE SEC UNDER SECTION 203 OF THE INVESTMENT ADVISERS ACT OR WITH A STATE SECURITIES COMMISSION (OR ANY AGENCY OR OFFICE PERFORMING LIKE FUNCTIONS); OR ANY OTHER PERSON (WHETHER A NATURAL PERSON, CORPORATION, PARTNERSHIP, TRUST OR OTHERWISE) WITH TOTAL ASSETS OF AT LEAST $50 MILLION.

The following is a summary of information pertaining to the Trust and does not contain all of the information about the Trust that may be important to you. You should read the entire prospectus, including “Risk Factors” beginning on page 11, before making an investment decision about the Gold Deposit Receipts.

Overview

The Vaulted Gold Bullion Trust (the “Trust”) was initially formed on December 10, 2013. The Trust is governed by the Amended and Restated Depositary Trust Agreement, dated June , 2016 by and among The Bank of New York Mellon, as trustee, BNY Trust of Delaware, as Delaware trustee, Bank of Montreal, as initial depositor, and BMO Capital Markets Corp., as underwriter (the “Depositary Trust Agreement”). The Trust has no assets or liabilities. The Trust is not a registered investment company under the 1940 Act.

At all times, the Trust will hold a fixed quantity of unencumbered, allocated, physical gold bullion (“Gold Bullion”) that corresponds to the then outstanding Gold Deposit Receipts. The Gold Bullion will be held for the benefit of holders of Gold Deposit Receipts in an account operated by Bank of Montreal at the Royal Canadian Mint (the “Mint”). One troy ounce of Gold Bullion will correspond to each Gold Deposit Receipt as specified under “Summary of Gold Deposit Receipts — The Gold Deposit Receipts.”

The Trust will issue Gold Deposit Receipts that represent your undivided beneficial ownership interest in Gold Bullion held by the Trust on your behalf.

Trust Objective

The objective of the Trust is to provide a secure and convenient way for investors to make an investment in unencumbered, allocated, physical Gold Bullion on a spot basis. As a result, at any given time, the value of the Gold Deposit Receipts is intended to reflect the spot price of gold held by the Trust for the holders of Gold Deposit Receipts.

The Trust is not actively managed and has no officers or employees. The Trust does not engage in any activities designed to obtain a profit from, or to prevent losses caused by, changes in the spot price of gold.

The Trust will issue Gold Deposit Receipts upon the contribution by Bank of Montreal to the Trust of a fixed quantity of Gold Bullion purchased with the proceeds, less the deposit fee and any sales fee, from the sale of Gold Deposit Receipts. Bank of Montreal will hold the Gold Bullion in an account that is operated by Bank of Montreal at the Mint in custody for the holders of Gold Deposit Receipts. BMO Capital Markets Corp. will act as the underwriter for the sale of Gold Deposit Receipts, pursuant to a distribution agreement among the Trust, Bank of Montreal and BMO Capital Markets Corp. BMO Capital Markets Corp. will enter into dealer agreements with certain third parties that are registered broker-dealers, or banks or trust companies regulated by the Office of the Comptroller of the Currency and/or one or more state banking regulators that are either direct or indirect DTC Participants. We refer to these third parties, as well as any other dealer that becomes a party to the distribution agreement, as Authorized Participants. Only Authorized Participants will be involved in the distribution of Gold Deposit Receipts. Holders of Gold Deposit Receipts may elect to redeem their Gold Deposit Receipts for physical gold or exchange their Gold Deposit Receipts for cash either through an Authorized Participant or through a registered broker-dealer or similar entity that is not an Authorized Participant.

The Trust may offer Gold Deposit Receipts from time to time as it receives Gold Bullion purchased on a daily basis for deposit in the Bank of Montreal account at the Mint, all as described more fully herein.

The Gold Deposit Receipts will not be listed or quoted on any national securities exchange.

Class A, Class F and Class F-1 Gold Deposit Receipts

The Trust is offering to the public three classes of Gold Deposit Receipts: Class A Gold Deposit Receipts; Class F Gold Deposit Receipts; and Class F-1 Gold Deposit Receipts. The only difference among these classes of Gold Deposit Receipts relates to the sales fee applicable to each class.

BMO Capital Markets Corp. will use the spot price of gold reflected on EBS as the source for the spot price of gold. BMO Capital Markets Corp. will refer to this source without adjustment or modification. If, for any reason, EBS is not posting spot prices, BMO Capital Markets Corp. will use the spot price reflected by the LBMA (PM) Gold Price as its source for the spot price of gold. BMO Capital Markets Corp. will refer to this source without adjustment or modification. The public offering price for each Gold Deposit Receipt will be based on the spot price at the time of purchase for one troy ounce of Gold Bullion, determined by BMO Capital Markets Corp. using EBS as the source for the spot price of gold, without adjustment or modification, plus a deposit fee of 2.00%, payable to Bank of Montreal, plus: (1) in the case of a Class A Gold Deposit Receipt, a sales fee of 2.00% to any participating broker-dealer that sells Gold Deposit Receipts to an investor; (2) in the case of a Class F Gold Deposit Receipt, which will be sold only through fee-based programs, a sales fee of 0.25%; and (3) in the case of Class F-1 Gold Deposit Receipts, which will be sold to trust or fiduciary accounts, no additional fee.

The table below summarizes the fees payable with respect to the Class A and Class F and Class F-1 Gold Deposit Receipts.

|

Deposit Fee

|

Sales Fee

|

Total

|

|

|

Class A

|

2.00%

|

2.00%

|

4.00%

|

|

Class F

|

2.00%

|

0.25%

|

2.25%

|

|

Class F-1

|

2.00%

|

0.00%

|

2.00%

|

Summary of Risks

The Gold Deposit Receipts are subject to certain risks, discussed in more detail in the section entitled “Risk Factors” below. Examples of these risks include:

|

|

·

|

the Trust has no history of operations and Bank of Montreal has a limited history of operating investment vehicles similar to the Trust; |

|

|

·

|

the value of Gold Bullion is not guaranteed, which may cause an investment in the Gold Deposit Receipts to be volatile; |

|

|

·

|

future governmental decisions may have significant impact on the price of Gold Bullion, which will impact the price of the Gold Deposit Receipts; |

|

|

·

|

the Trust is a passive investment vehicle, which means that the value of the Gold Deposit Receipts may be adversely affected by losses that, if the Trust had been actively managed, it might have been possible to avoid; and |

|

|

·

|

because the Trust holds solely Gold Bullion, an investment in the Trust may be more volatile than an investment in a more broadly diversified portfolio. |

Emerging Growth Company Status

The Trust is an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as the Trust is an “emerging growth company,” the Trust may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes–Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in the Trust’s periodic reports, and exemptions from the requirements of holding advisory “say-on-pay” votes on executive compensation and shareholder advisory votes on golden parachute compensation.

Under the JOBS Act, the Trust will remain an “emerging growth company” until the earliest of:

|

|

·

|

the last day of the fiscal year during which the Trust has total annual gross revenues of $1 billion or more;

|

|

|

·

|

the last day of the fiscal year following the fifth anniversary of the completion of this offering;

|

|

|

·

|

the date on which the Trust has, during the previous three-year period, issued more than $1 billion in non-convertible debt; and

|

|

|

·

|

the date on which the Trust is deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) (the Trust will qualify as a large accelerated filer as of the first day of the first fiscal year after the Trust has (i) more than $700 million in outstanding equity held by non-affiliates and (ii) been public for at least 12 months; the value of its outstanding equity will be measured each year on the last day of its second fiscal quarter).

|

The JOBS Act also provides that an “emerging growth company” can utilize the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards. However, the Trust is choosing to “opt out” of such extended transition period, and, as a result, the Trust will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for companies that are not “emerging growth companies.” Section 107 of the JOBS Act provides that the Trust’s decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Trustees

The trustee of the Trust is The Bank of New York Mellon, a corporation organized under the laws of the State of New York authorized to conduct a banking business. The Delaware trustee of the Trust will be BNY Mellon Trust of Delaware, a Delaware banking corporation. The Trust’s website is www.BMOGOLD.com.

Principal Office

The address of the Trust is c/o BNY Mellon Trust of Delaware, 100 White Clay Center, Suite 10, Newark, DE 19711, and the telephone number is (302) 791-3610.

This discussion highlights information regarding the Gold Deposit Receipts. We present certain information more fully in the rest of this prospectus. You should read the entire prospectus carefully before you purchase Gold Deposit Receipts.

|

Issuer

|

Vaulted Gold Bullion Trust.

|

|

The Trust

|

The Trust was initially formed on December 10, 2013. The Trust is governed by the Amended and Restated Depositary Trust Agreement, dated June , 2016 among The Bank of New York Mellon, as trustee, BNY Trust of Delaware, as Delaware trustee, Bank of Montreal, as initial depositor, and BMO Capital Markets Corp., as underwriter. The Trust is not a registered investment company under the 1940 Act.

|

|

Initial Depositor

|

Bank of Montreal.

|

|

Trustees

|

The Bank of New York Mellon, a corporation organized under the laws of the State of New York authorized to conduct a banking business, will be the trustee and receive compensation for its services as set forth in the Depositary Trust Agreement. BNY Mellon Trust of Delaware, a Delaware state chartered banking corporation, will be the Delaware trustee and receive compensation for its services as set forth in the Depositary Trust Agreement.

|

|

Purpose of Gold Deposit Receipts

|

The Gold Deposit Receipts are designed to provide investors, acting through Authorized Participants, with:

· A book-entry solution for investors interested in having their Gold Bullion reflected in a brokerage account without the inconvenience that is typical of a traditional, manual investment in Gold Bullion;

· A secure and convenient way to purchase Gold Bullion on a spot basis and hold it in an account of Bank of Montreal’s at the Mint;

· A facility whereby investors can withdraw and sell intraday for cash at the spot price for gold (i.e., intraday spot liquidity);

|

|

· A process whereby investors can request physical delivery for as little as one ounce without the inconvenience or complexity that may be associated with traditional gold-backed exchange-traded products;

· A structure which, under Canadian federal law, ensures that the Gold Bullion held by the Trust for holders of Gold Deposit Receipts would not be available to meet the claims of creditors of Bank of Montreal in the event of any bankruptcy, insolvency or similar event involving Bank of Montreal; and

· An alternative to physical gold bullion storage providers or programs that are operated by unregulated entities. Bank of Montreal, Canada’s oldest bank, is regulated by Canadian authorities, and in the United States, by U.S. bank regulators. The Gold Deposit Receipts are offered initially by and through the bank’s wholly-owned subsidiary, BMO Capital Markets Corp., which is a broker-dealer and an investment adviser, subject to SEC oversight and regulation, and is also a FINRA member firm. Bank of Montreal is a member of the LBMA and is an approved storage facility in Canada.

The Gold Deposit Receipts seek to eliminate:

· Annual fees;

· Price variance from the underlying spot market for Gold Bullion which may be associated with traditional gold-backed exchange-traded products that trade at a discount or premium to NAV;

· Derivatives risk (i.e., the use of unallocated gold, gold certificates, exchange-traded products, derivatives, financial instruments, or any product that represents encumbered gold);

· “Empty vault risk,” or Gold Bullion lending risk (i.e., the practice of the gold custodian lending, pledging, hypothecating, re-hypothecating or otherwise encumbering any of the investor’s underlying Gold Bullion); and

· Onerous restrictions on physical delivery of Gold Bullion.

|

|

Investment Objective

|

The Gold Deposit Receipts may not be suitable for all investors and are intended for investors who wish to invest in Gold Bullion on a spot basis and who are willing to forgo current income or periodic payments.

|

|

The Gold Deposit Receipts

|

The Trust will issue Gold Deposit Receipts that represent your undivided beneficial ownership interest in the Gold Bullion held by the Trust on your behalf through an account of Bank of Montreal at the Mint.

|

|

The Trust will only issue Gold Deposit Receipts when it has received through an Authorized Participant funds corresponding to at least one troy ounce of Gold Bullion, which is equivalent to one Gold Deposit Receipt.

|

|

|

CUSIP / ISIN

|

Class A Gold Deposit Receipts: 92242D205 / US92242D2053

Class F Gold Deposit Receipts: 92242D304 / US92242D3044

Class F-1 Gold Deposit Receipts: 92242D403 / US92242D4034

|

|

Trust Assets

|

At all times, for the benefit of holders of Gold Deposit Receipts, the Trust will hold a fixed quantity of Gold Bullion corresponding to the then outstanding Gold Deposit Receipts, that will be held in an account operated by Bank of Montreal at the Mint. The amount of Gold Bullion held will fluctuate each day as holders of Gold Deposit Receipts exchange their interests for physical gold or withdraw and sell for cash, and as the Trust issues additional Gold Deposit Receipts in connection with additional Gold Bullion purchased on a daily basis by Bank of Montreal and contributed to the Trust on behalf of the holders of the Gold Deposit Receipts. Under no circumstances will the Trust assets or the form of Gold Bullion be changed.

|

|

Rights Relating to

Gold Deposit Receipts

|

A holder of Gold Deposit Receipts has the right to redeem its Gold Deposit Receipts for physical gold, or to withdraw and sell for cash, at any time, subject, as discussed below, to certain suspensions.

A holder may redeem for physical gold subject to payment of a withdrawal and delivery fee (the “Withdrawal and Delivery Fee”), plus applicable taxes. The Trust, through Bank of Montreal, will deliver Gold Bullion only to addresses within the United States which are within a state specifically approved for delivery. You may check with your Authorized Participant or other broker-dealer for a current list of delivery states. Physical delivery may be suspended generally, or refused with respect to particular requested deliveries only in the case of a force majeure event or market disruption event where the Initial Depositor is prevented for reasons outside of its control from delivering the Gold Bullion, and such suspension or refusal shall only last so long as the Initial Depositor continues to be so prevented from delivering the Gold Bullion.

|

|

Alternatively, a holder of Gold Deposit Receipts may choose to sell for cash by instructing an Authorized Participant or other broker-dealer to withdraw that holder’s corresponding amount of Gold Bullion, and having the Trust facilitate the sale for cash to Bank of Montreal, if Bank of Montreal chooses to purchase the Gold Bullion at that time, as discussed further herein. From time to time, this mechanism to sell Gold Bullion may be suspended for any reason without notice, including, but not limited to, if a force majeure event should occur. Gold Deposit Receipts may also be transferred by gift or estate transfer.

|

|

|

Distributions

|

Holders of Gold Deposit Receipts will receive no cash distributions whatsoever.

|

|

Repurchases

|

Holders of Gold Deposit Receipts will only have the option on any business day to elect that Bank of Montreal repurchase your withdrawn Gold Bullion (represented by the Gold Deposit Receipts) for cash if Bank of Montreal is then effecting such purchases, however, Bank of Montreal is under no obligation to do so.

|

|

Voting Rights

|

Holders of Gold Deposit Receipt will have no voting rights, except in limited circumstances. See “Description of the Gold Deposit Receipts – Voting Rights.”

|

|

Public Offering Price

|

The Trust is offering to the public on a continuous basis three classes of Gold Deposit Receipts: Class A Gold Deposit Receipts; Class F Gold Deposit Receipts; and Class F-1 Gold Deposit Receipts. The only difference among these classes of Gold Deposit Receipts relates to the sales fee applicable to each class.

The public offering price for each Gold Deposit Receipt will be based on the spot price at the time of purchase for one troy ounce of Gold Bullion, determined by BMO Capital Markets Corp. using EBS as the source for the spot price of gold, without adjustment or modification, plus a deposit fee of 2.00%, payable to Bank of Montreal, plus (1) in the case of a Class A Gold Deposit Receipt, a sales fee of 2.00% to any participating broker-dealer that sells Gold Deposit Receipts to an investor; (2) in the case of a Class F Gold Deposit Receipt, which will be sold only through fee-based programs, a sales fee of 0.25%; and (3) in the case of Class F-1 Gold Deposit Receipts, which will be sold to trust or fiduciary accounts, no additional fee.

BMO Capital Markets Corp. will use the spot price of gold reflected on EBS as the source for the spot price of gold. BMO Capital Markets Corp. will refer to this source without adjustment or modification. If, for any reason, EBS is not posting spot prices, BMO Capital Markets Corp. will use the spot price reflected by the LBMA (PM) Gold Price as its source for the spot price of gold. BMO Capital Markets Corp. will refer to this source without adjustment or modification. An investor considering a purchase or redemption of Gold Deposit Receipts may obtain end of day indicative pricing from the Trust’s website. Real-time indicative quotations are available from Bloomberg using <BMOEGLDR Index Go> and these quotations also will be available (on a delayed basis) at Bloomberg.com. Your broker will confirm the execution price to you; due to movements in the spot price, the execution price may differ from the indicative or the quoted price. See “Description of Gold Deposit Receipts—How to Obtain Pricing Information” and “Plan of Distribution.”

|

|

Fees

|

If you purchase Gold Deposit Receipts in the initial public offering, you will pay a 2.00% deposit fee as well as the applicable sales fee, if any.

The price of the Gold Bullion will be based on the spot price of gold at the time of purchase. However, as described further below, in connection with physical delivery, you will be responsible for a Withdrawal and Delivery Fee and payment of applicable taxes.

There are no fees payable to Bank of Montreal upon a sale for cash. Holders who redeem their Gold Deposit Receipts for cash using the services of an Authorized Participant or other broker-dealer (for example, the holder’s broker) may be charged additional fees or commissions by that Authorized Participant or other broker-dealer.

|

|

Purchases and Sales

|

After the initial offering, you may acquire Gold Deposit Receipts through an Authorized Participant. Under no circumstances may any purchase of the Gold Deposit Receipts be made with borrowed or leveraged funds advanced by an Authorized Participant. No margin purchases of the Gold Bullion represented by the Gold Deposit Receipts will be accepted.

|

|

Trustee Fees

|

The Bank of New York Mellon, as trustee, will charge Bank of Montreal a quarterly trustee fee of $0.02 for each Gold Deposit Receipt, with an annual minimum fee of $75,000. The trustee fee will be paid by Bank of Montreal.

|

|

Trust Expenses

|

The Trust’s expenses will include the trustee fees payable to The Bank of New York Mellon and will be borne by Bank of Montreal.

|

|

Limitation on Liability

|

Bank of Montreal, The Bank of New York Mellon, and BNY Mellon Trust of Delaware:

· are only obligated to take the actions set forth in the Depositary Trust Agreement without gross negligence or bad faith;

· are not liable for any exercise of discretion permitted under the Depositary Trust Agreement; and

|

|

· have no obligation to prosecute any lawsuit or other proceeding on behalf of the holders of Gold Deposit Receipts or any other person.

|

|

|

U.S. Federal Income Tax Consequences

|

U.S. holders generally will be treated, for U.S. federal income tax purposes, as if they directly owned a pro rata share of the underlying Gold Bullion.

|

|

Listing

|

The Gold Deposit Receipts will not be listed or traded on any securities exchange.

|

|

Trading

|

Investors will be able to acquire, hold, transfer and surrender only whole Gold Deposit Receipts (i.e., no fractional interests), with a minimum of one Gold Deposit Receipt per transaction. Gold Deposit Receipts may only be purchased through Authorized Participants.

|

|

Clearance and settlement

|

The Trust will issue Gold Deposit Receipts in book-entry form only. Gold Deposit Receipts will be evidenced by one or more global certificates that the trustee will deposit with The Depository Trust Company, referred to as DTC. Transfers within DTC will be in accordance with DTC’s usual rules and operating procedures. Settlement for any purchase of Gold Deposit Receipts will be no later than the second business day following the date of execution of the purchase order. For further information see “Description of Gold Deposit Receipts.”

|

|

Termination events

|

The Trust will terminate if:

· The trustee resigns and no successor trustee is appointed within 60 days from the date the trustee provides notice to Bank of Montreal or BMO Capital Markets Corp. of its intent to resign;

· Holders of at least 75% of the outstanding Gold Deposit Receipts (other than those held by Bank of Montreal for its own account) acting through an Authorized Participant vote to dissolve and liquidate the Trust;

· An event of liquidation or dissolution occurs as to Bank of Montreal;

· Bank of Montreal ceases to store Gold Bullion at the Mint and does not make alternative arrangements that it deems appropriate; or

|

|

· The Trust fails to qualify for treatment, or ceases to be treated, for U.S. federal income tax purposes, as a grantor trust.

If a termination event occurs, the initial depositor will sell the Gold Bullion and the trust will deliver to you the resulting proceeds as promptly as practicable after the termination event occurs.

|

|

| Calculation Agent | BMO Capital Markets Corp., Bank of Montreal’s wholly-owned registered securities dealer in the United States, will act as the calculation agent. |

| Conflicts of Interest |

BMO Capital Markets Corp., the underwriter and one of Bank of Montreal’s affiliates, is a broker-dealer and member of the Financial Industry Regulatory Authority, Inc., or “FINRA.”

|

|

Use of Proceeds

|

The Trust will use the proceeds of the issuance of Gold Deposit Receipts, net of the deposit fee and any sales fee, to purchase Gold Bullion from Bank of Montreal in an amount that corresponds to the amount of Gold Deposit Receipts. The amount paid per ounce of Gold Bullion by the Trust will be equal to the spot price of one troy ounce of Gold Bullion on the date of purchase. See “Use of Proceeds.”

|

You should consider carefully the risks described below before making an investment decision. You should also refer to the other information included or incorporated by reference in this prospectus.

The Trust has no history of operations and Bank of Montreal has a limited history of operating investment vehicles similar to the Trust. Its experience may be inadequate or unsuitable to manage the Trust.

The Trust is a newly organized trust with no operating history and no assets or liabilities. Bank of Montreal has a limited history of operating investment vehicles like the Trust. Bank of Montreal’s performance in connection with sponsoring or managing other investment vehicles is not indicative of its ability to sponsor the Trust.

The value of the Gold Deposit Receipts relates directly to the value of the Gold Bullion held by the Trust and fluctuations in the price of gold could materially adversely affect an investment in the Gold Deposit Receipts.

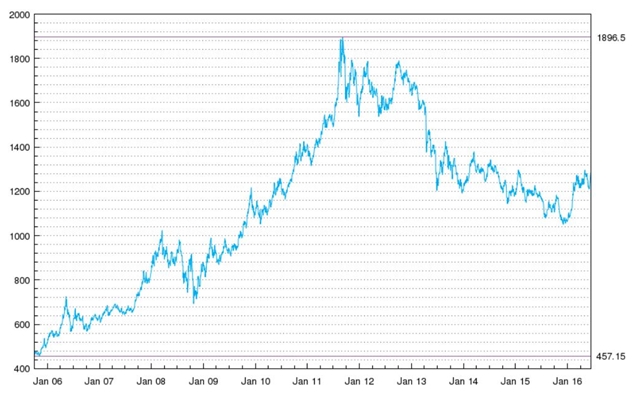

The Gold Deposit Receipts are designed to mirror as closely as possible the performance of the price of gold, and the value of the Gold Deposit Receipts relates directly to the value of the Gold Bullion held by the Trust. The price of gold has fluctuated widely over the past several years.

Several factors may affect the price of gold, including:

|

|

·

|

Global gold supply and demand, which is influenced by such factors as forward selling by gold producers, purchases made by gold producers to unwind gold hedge positions, central bank purchases and sales, and production and cost levels in major gold-producing countries such as South Africa, the United States and Australia;

|

|

|

·

|

Global or regional political, economic or financial events and situations;

|

|

|

·

|

Investors’ expectations with respect to the rate of inflation;

|

|

|

·

|

Currency exchange rates;

|

|

|

·

|

Interest rates; and

|

|

|

·

|

Investment and trading activities of hedge funds and commodity funds.

|

Throughout 2015, market participants reported a significant decrease in global demand for gold. Since 2016, gold prices have risen sharply. If gold markets continue to be subject to sharp fluctuations, the price of the Gold Deposit Receipts may experience significant price fluctuation and this may result in losses if you need to sell your Gold Deposit Receipts at a time when the price of gold is lower than it was when you made your investment. Even if you are able to hold Gold Deposit Receipts for the long-term, you may never experience a profit, since gold markets have historically experienced extended periods of flat or declining prices, in addition to sharp fluctuations.

In addition, investors should be aware that there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price of gold declines, the initial depositor expects the value of an investment in the Gold Deposit Receipts to decline proportionately.

The value of Gold Bullion is not guaranteed, which may cause your investment in the Gold Deposit Receipts to be volatile.

An investment in Gold Bullion is speculative and may be subject to greater price volatility than other investments. Appreciation in the market price of gold is the sole manner in which you can realize gains. Past performance of the price of gold is not indicative of future performance. Bank of Montreal does not provide any guarantee as to the value of Gold Bullion, which may be affected by many international, economic, monetary and political factors, many of which are unpredictable.

Future governmental decisions may have significant impact on the price of Gold Bullion, which will impact the price of the Gold Deposit Receipts.

Generally, gold prices reflect the supply and demand of available Gold Bullion. Governmental decisions, such as the executive order issued by the President of the United States in 1933 requiring all persons in the United States to deliver Gold Bullion to the Federal Reserve or the abandonment of the gold standard by the United States in 1971, have been viewed as having significant impact on the supply and demand of Gold Bullion and the price of Gold Bullion. Future governmental decisions, whether in the United States, Canada or other relevant jurisdictions, may have an impact on the price of physical bullion, and may result in a significant decrease or increase in the value of the Gold Bullion and the Gold Deposit Receipts.

Disruptions in trading may materially adversely affect the Gold Deposit Receipts.

Occasional disruptions in trading, including temporary distortions or other disruptions due to various factors, such as the lack of liquidity in markets, the participation of speculators and governmental regulation and intervention may result in a significant decrease or increase in the value of Gold Bullion, which will affect the Gold Deposit Receipts.

The Trust is a passive investment vehicle. This means that the value of the Gold Deposit Receipts may be adversely affected by Trust losses that, if the Trust had been actively managed, it might have been possible to avoid.

The trustee does not actively manage the gold held by the Trust. This means that the trustee does not sell gold at times when its price is high, or acquire gold at low prices in the expectation of future price increases. It also means that the trustee does not make use of any of the hedging techniques available to professional gold investors to attempt to reduce the risks of losses resulting from price decreases. Any losses sustained by the Trust will adversely affect the value of the Gold Deposit Receipts.

Because the Trust holds solely Gold Bullion, an investment in the Trust may be more volatile than an investment in a more broadly diversified portfolio.

The Trust holds solely Gold Bullion for the benefit of the holders of the Gold Deposit Receipts. As a result, the Trust’s holdings are not diversified. Accordingly, the asset value of the Trust may be more volatile than another investment vehicle with a broadly diversified portfolio and may fluctuate substantially over time.

Crises may motivate large-scale sales of gold which could decrease the price of gold and adversely affect an investment in the Gold Deposit Receipts.

The possibility of large-scale distressed sales of gold in times of crisis may have a short-term negative impact on the price of gold and adversely affect an investment in the Gold Deposit Receipts. For example, the 1998 Asian financial crisis resulted in significant sales of gold by individuals which depressed the price of gold. Crises in the future may impair gold’s price performance which would, in turn, adversely affect an investment in the Gold Deposit Receipts.

Purchasing activity in the gold market associated with the delivery of Gold Bullion to the Trust in exchange for Gold Deposit Receipts may cause a temporary increase in the price of gold. This increase may adversely affect an investment in the Gold Deposit Receipts.

Purchasing activity associated with acquiring the Gold Bullion that is transferred into the Trust in connection with the issuance of additional Gold Deposit Receipts may temporarily increase the market price of gold, which will result in higher prices for the Gold Deposit Receipts. Temporary increases in the market price of gold may also occur as a result of the purchasing activity of other market participants. Other market participants may attempt to benefit from an increase in the market price of gold that may result from increased purchasing activity of gold connected with the issuance of Gold Deposit Receipts. Consequently, the market price of gold may decline immediately after Gold Deposit Receipts are created. If the price of gold declines, the trading price of the Gold Deposit Receipts will also decline.

Holders of Gold Deposit Receipts do not have the protections associated with ownership of interests in an investment company registered under the 1940 Act or the protections afforded by the Commodity Exchange Act.

The Trust is not registered as an investment company under the 1940 Act and is not required to register under such act. Consequently, holders do not have the regulatory protections provided to investors in investment companies. The Trust will not hold or trade commodity interests regulated by the Commodity Exchange Act (the “CEA”), as administered by the Commodity Futures Trading Commission (the “CFTC”). Furthermore, the Trust is not a commodity pool for purposes of the CEA, and none of the initial depositor, the trustee or the Authorized Participants is subject to regulation by the CFTC in any capacity, including as a commodity pool operator or a commodity trading advisor in connection with the Gold Deposit Receipts. Consequently, holders do not have the regulatory protections provided to investors in CEA-regulated instruments or commodity pools.

The Trust may be required to terminate and liquidate at a time that is disadvantageous to holders.

If the Trust is required to terminate and liquidate, such termination and liquidation could occur at a time which is disadvantageous to holders, such as when gold prices are lower than the gold prices at the time when holders purchased their Gold Deposit Receipts. In such a case, when the Trust’s gold is sold as part of the Trust’s liquidation, the resulting proceeds distributed to holders will be less than if gold prices were higher at the time of sale.

The price of gold may be affected by the sale of gold by exchange-traded funds or other exchange-traded vehicles tracking gold markets.

To the extent existing exchange-traded funds, or ETFs, or other exchange-traded vehicles tracking gold markets represent a significant proportion of demand for Gold Bullion, large redemptions of the securities of these ETFs or other exchange-traded vehicles could negatively affect Gold Bullion prices and the price of the Gold Deposit Receipts.

An investment in the Gold Deposit Receipts may be adversely affected by competition from other methods of investing in gold.

The Trust is a new, and thus untested, type of investment vehicle. It will compete with other financial vehicles, including traditional debt and equity securities issued by gold industry participants and direct investments in gold. Market and financial conditions, and other conditions beyond Bank of Montreal’s control, may make it more attractive to invest in other financial vehicles or to invest in gold directly, which could limit the market for the Gold Deposit Receipts and reduce the liquidity of the Gold Deposit Receipts.

The Trust may postpone, suspend or reject redemption requests in certain circumstances, which may limit the ability of a holder of Gold Deposit Receipts to obtain liquidity.

If notified by Bank of Montreal or BMO Capital Markets Corp. of any postponement, suspension or rejection of settlement, as discussed under “Description of Gold Deposit Receipts―Suspensions of Redemptions and/or Purchases,” the trustee shall suspend the redemption right or postpone the settlement date for any redemption to have physical gold delivery for you. Any such postponement, suspension or rejection may affect a holder’s ability to obtain liquidity. Under the Depositary Trust Agreement, the initial depositor, the trustee and the underwriter have no liability for any loss or damage that may result from any such suspension or postponement. Physical delivery may be suspended generally, or refused with respect to particular requested deliveries only in the case of a force majeure event or market disruption event where the Initial Depositor is prevented for reasons outside of its control from delivering the Gold Bullion, and such suspension or refusal shall only last so long as the Initial Depositor continues to be so prevented from delivering the Gold Bullion.

Redemptions or repurchases of Gold Deposit Receipts by the Initial Depositor for Cash Delivery may be suspended at any time as a result of suspensions in the purchase of Gold Bullion by Bank of Montreal.

As a holder of Gold Deposit Receipts, you will only have the option to elect that Bank of Montreal repurchase the withdrawn Gold Bullion represented by your Gold Deposit Receipts for cash if Bank of Montreal is then effecting such purchases, but Bank of Montreal is under no obligation to do so. Accordingly, you should only purchase the Gold Deposit Receipts if you are prepared to maintain an ownership interest in the Gold Deposit Receipts for an indefinite period. Bank of Montreal will have no obligation to the Trust or to any holder of Gold Deposit Receipts to repurchase Gold Bullion at any time.

In the event that a holder redeems Gold Deposit Receipts for cash or physical gold, an Authorized Participant or other broker-dealer that processes that transaction may charge additional fees.

Holders who redeem their Gold Deposit Receipts for cash or physical gold using the services of an Authorized Participant or other broker-dealer (for example, the holder’s broker) may be charged additional fees or commissions by that Authorized Participant or other broker-dealer. No additional fees (other than any applicable withdrawal and delivery fee in connection with the delivery of physical gold) will be charged by the Trust or BMO Capital Markets Corp.

Physical delivery of Gold Bullion is not available in every state, and the states approved for delivery may change at any time.

Gold Bullion will be delivered only to addresses within the United States that are within a state specifically approved by the underwriter for delivery, as discussed under “Description of Gold Deposit Receipts―Redemptions of Gold Deposit Receipts for Gold Bullion; Sales for Cash—Physical Delivery.” The Initial Depositor will maintain a list of states approved for delivery and provide the same to the Authorized Participants from time to time. The Initial Depositor has no obligation to deliver Gold Bullion to a state that is not approved for delivery, and there is no guarantee that delivery will remain available in any particular state. If an investor changes its address to a state that is not approved for delivery, delivery will no longer be available to that investor.

A request for sale or redemption is irrevocable.

In order to sell or redeem Gold Deposit Receipts for cash or physical gold, a holder must provide a notice to the Trust through an Authorized Participant or another broker-dealer as described herein. Except when sales or redemptions have been suspended, once a notice has been received, it can no longer be revoked by the holder under any circumstances, though it may be rejected by the Trust if it does not comply with the requirements for such notice.

The fees charged to holders may change.

If you choose to redeem your Gold Deposit Receipts for physical gold, you will be responsible for payment of certain fees and expenses. The fees and expenses may be increased or decreased by Bank of Montreal in its sole and absolute discretion.

Holders do not have the rights enjoyed by investors in certain other vehicles.

As interests in the Gold Bullion held by the Trust, the Gold Deposit Receipts have none of the statutory rights normally associated with the ownership of shares of a corporation (including, for example, the right to bring “derivative” actions). In addition, the Gold Deposit Receipts have limited voting and distribution rights (for example, holders do not have the right to elect directors and will not receive dividends).

Substantial sales of gold by the official sector could adversely affect an investment in the Gold Deposit Receipts.

The official sector consists of central banks, other governmental agencies and multi-lateral institutions that buy, sell and hold gold as part of their reserve assets. The official sector holds a significant amount of gold, most of which is static, meaning that it is held in vaults and is not bought, sold, leased or swapped or otherwise mobilized in the open market. A number of central banks have sold portions of their gold over the past ten years, with the result that the official sector, taken as a whole, has been a net supplier to the open market. Since 1999, most sales have been made in a coordinated manner under the terms of the Central Bank Gold Agreement under which 15 of the world’s major central banks agree to limit the level of their gold sales and lending to the market. In the event that future economic, political or social conditions or pressures require members of the official sector to liquidate their gold assets all at once or in an uncoordinated manner, the demand for gold might not be sufficient to accommodate the sudden increase in the supply of gold to the market. Consequently, the price of gold could decline significantly, which would adversely affect an investment in the Gold Deposit Receipts.

The Trust does not insure its assets and there may not be adequate sources of recovery if its gold is lost, damaged, stolen or destroyed.

The Trust does not insure its assets, including the Gold Bullion stored at the Mint. Consequently, if there is a loss of assets of the Trust through theft, destruction, fraud or otherwise, the Trust and holders will need to rely on insurance carried by applicable third parties, if any, or on such third party's ability to satisfy any claims against it. The amount of insurance available or the financial resources of a responsible third party may not be sufficient to satisfy the Trust's claim against such party. Also, holders are unlikely to have any right to assert a claim directly against such third party; such claims may only be asserted by the trustee on behalf of the Trust. In addition, if a loss is covered by insurance carried by a third party, the Trust, which is not a beneficiary on such insurance, may have to rely on the efforts of the third party to recover its loss. This may delay or hinder the Trust's ability to recover its loss in a timely manner or otherwise.

A loss with respect to the Trust's gold that is not covered by insurance and for which compensatory damages cannot be recovered would have a negative impact on the Gold Deposit Receipts and would adversely affect an investment in the Gold Deposit Receipts. In addition, any event of loss may adversely affect the operations of the Trust and, consequently, an investment in the Gold Deposit Receipts.

A redeeming holder of the Gold Deposit Receipt that suffers loss of, or damage to, its Gold Bullion during delivery will not be able to claim damages from the Service Carrier, Bank of Montreal, the Trust or the storage provider.

If a holder exercises its option to redeem Gold Deposit Receipts for Gold Bullion, the holder’s Gold Bullion will be transported by the Service Carrier (as defined below). Because ownership of Gold Bullion will transfer to such holder at the time Bank of Montreal surrenders the Gold Bullion to the Service Carrier, the redeeming holder will bear the risk of loss from the moment the Service Carrier takes possession of the Gold Bullion on behalf of such holder. Under the terms of the Gold Carrier Agreement, in the event of any loss or damage in connection with the delivery of the Gold Bullion, such holder will not be able to claim damages from the Service Carrier, nor will such holder be able to claim damages from Bank of Montreal, the Trust or the Mint.

Bank of Montreal, the Mint and service providers engaged by the Trust may not carry adequate insurance to cover claims against them by the Trust.

Holders cannot be assured that Bank of Montreal or the Mint or service providers engaged by the Trust will maintain insurance with respect to the Trust's assets or the services that such parties provide to the Trust and, if they maintain insurance, that such insurance is sufficient to satisfy any losses incurred by them in respect of their relationship with the Trust. The Mint, to the extent it has any liability, will be liable only to Bank of Montreal directly in the event of loss, damage or destruction of the Trust’s Gold Bullion. In addition, none of the Trust's service providers are required to include the Trust as a named beneficiary of any such insurance policies that are purchased. Accordingly, the Trust will have to rely on the efforts of the service provider to recover from their insurer compensation for any losses incurred by the Trust in connection with such arrangements.

If there is a loss, damage or destruction of the Trust's Gold Bullion in the custody of the Mint and Bank of Montreal does not give timely notice, all claims against the Mint will be deemed waived.

In the event of loss, damage or destruction of the Trust's Gold Bullion in the Mint's custody, care and control, Bank of Montreal must give written notice to the Mint within five Mint business days (a Mint business day means any day other than a Saturday, Sunday or a holiday observed by the Mint) after the discovery by Bank of Montreal of any such loss, damage or destruction, but in any event no more than 30 days after the delivery by the Mint to Bank of Montreal of an inventory statement in which the discrepancy first appears. If such notice is not given in a timely manner, all claims against the Mint will be deemed to have been waived. In addition, no action, suit or other proceeding to recover any loss or shortage can be brought against the Mint unless timely notice of such loss or shortage has been given and such action, suit or proceeding will have commenced within 12 months from the time a claim is made. The loss of the right to make a claim or of the ability to bring an action, suit or other proceeding against the Mint may mean that any such loss will be non-recoverable, which will have an adverse effect on the value of the net assets of the Trust.

The Trustee and Trust shall have no responsibility or liability for actions taken by the Initial Depositor or the Mint.

Pursuant to the terms of the Depositary Trust Agreement, neither the Trustee nor the Trust can be held responsible, or liable, for any misconduct, bad faith or negligence of the Initial Depositor or the Mint.

Under Canadian law, the Trust may have limited recourse against the Mint.

The Mint is a Canadian Crown corporation. A Crown corporation may be sued for breach of contract or for wrongdoing in tort where it has acted on its own behalf or on behalf of the Crown. However, a Crown corporation may be entitled to immunity if it acts as agent of the Crown rather than in its own right and on its own behalf. The Mint has entered into the Gold Storage Agreement between Bank of Montreal and the Mint (the “Gold Storage Agreement”) relating to the custody of the Gold Bullion in Bank of Montreal’s account for the Trust. The Mint has entered into this agreement on its own behalf and not on behalf of the Crown; nevertheless, a court may determine that, when acting as custodian of the Trust's Gold Bullion, the Mint acted as agent of the Crown and, accordingly, that the Mint may be entitled to immunity of the Crown. Consequently, the Trust or a holder may not be able to recover for any losses incurred as a result of the Mint's acting as custodian of the Gold Bullion.

The Mint may become a private enterprise, in which case its obligations will not constitute the unconditional obligations of the Government of Canada.

In the past, there has been speculation regarding whether the Government of Canada might privatize the Mint. The Mint will not remain a Crown corporation if the Government of Canada privatizes the Mint. If the Mint were to become a private entity, its obligations would no longer generally constitute unconditional obligations of the Government of Canada and, although it would continue to be responsible for and bear the risk of loss of, and damage to, the Trust's Gold Bullion that is in its custody, there would be no assurance that the Mint would have the resources to satisfy claims of the Trust against the Mint based on a loss of, or damage to, the Trust's Gold Bullion in the custody of the Mint.

An investment in Gold Bullion may not be appropriate for all investors.

You should decide to buy the Gold Deposit Receipts, which constitute an investment in Gold Bullion, only after carefully considering with your investment or financial advisor whether Gold Bullion is a suitable investment in light of the information in this prospectus having regard to your financial or investment objectives and expectations.

Changes in laws or regulations may affect the Gold Deposit Receipts and the Gold Bullion.

The promulgation of new laws or regulations or by the reinterpretation of existing laws or regulations (including, without limitation, those relating to taxes and duties on commodities or commodity components) by one or more governments, governmental agencies or instrumentalities, courts, or other official bodies may result in a significant decrease or increase in the value of the Gold Deposit Receipts and the Gold Bullion. The United States or foreign governments may pass laws or regulations limiting metal investments for strategic or other policy reasons.

Potential risks could arise with respect to the Trust and the holders of Gold Deposit Receipts from an insolvency event relating to Bank of Montreal.

The Gold Deposit Receipts will represent interests in Gold Bullion held by the Trust. The Gold Bullion will be held by the Trust on your behalf and held at an account of Bank of Montreal with the Mint. The Gold Bullion will not be owned by Bank of Montreal. Consequently, under Canadian federal law, the Gold Bullion would not be available to meet the claims of creditors of Bank of Montreal in the event of any bankruptcy, insolvency or similar event involving Bank of Montreal. However, any such event could lead to delays in restoring the holders of Gold Deposit Receipts ability to transact in such Gold Bullion, depending upon the outcome of any relevant bankruptcy or related proceedings.

Transactions through an Authorized Participant or other broker-dealer are subject to risks related to that Authorized Participant or broker-dealer.

All transactions in the Gold Deposit Receipts will take place through an Authorized Participant or other broker-dealer, and you assume the risks of the Authorized Participant’s or broker-dealer’s failure to fulfill its obligations to you.

The Gold Deposit Receipts are not subject to deposit insurance.

The Gold Deposit Receipts are not securities of The Bank of New York Mellon, BNY Mellon Trust of Delaware, Bank of Montreal or any other bank, and do not constitute deposits that are insured under the U.S. Federal Deposit Insurance Act, the Canada Deposit Insurance Corporation Act or any other deposit insurance regime.

There is no assurance that your investment in the Gold Deposit Receipts will be subject to protection by the Securities Investor Protection Corporation.

In the case of the failure of a brokerage firm that is a member of the Securities Investor Protection Corporation (the “SIPC”), the SIPC would protect customers against the loss of cash and securities. The SIPC does not protect commodity or related futures contracts or investment contracts. The Gold Deposit Receipts are not commodity futures or investment contracts. In the opinion of Morrison & Foerster LLP, the Gold Deposit Receipts should be viewed as securities for which SIPC protection should be available. However, given that the Gold Deposit Receipts are novel instruments, there can be no assurance that the SIPC or a court having jurisdiction on this matter would concur with this legal conclusion.

The Trust is an “emerging growth company” and it cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make the Gold Deposit Receipts less attractive to investors.

The Trust is an “emerging growth company” as defined in the JOBS Act. For as long as the Trust continues to be an emerging growth company it may choose to take advantage of certain exemptions from various reporting requirements applicable to other public companies but not to emerging public companies, which include, among other things:

|

·

|

exemption from the auditor attestation requirements under Section 404 of the Sarbanes-Oxley Act;

|

|

·

|

reduced disclosure obligations regarding executive compensation in the Trust’s periodic reports;

|

|

·

|

exemption from the requirements of holding non-binding stockholder votes on executive compensation arrangements; and

|

|

·

|

exemption from any rules requiring mandatory audit firm rotation and auditor discussion and analysis and, unless the SEC otherwise determines, any future audit rules that may be adopted by the Public Company Accounting Oversight Board.

|

The Trust could be an emerging growth company until the last day of the fiscal year following the fifth anniversary after its initial public offering, or until the earliest of (i) the last day of the fiscal year in which it has annual gross revenue of $1 billion or more, (ii) the date on which it has, during the previous three year period, issued more than $1 billion in non-convertible debt or (iii) the date on which it is deemed to be a large accelerated filer under the federal securities laws. The Trust will qualify as a large accelerated filer as of the first day of the first fiscal year after it has (i) more than $700 million in outstanding equity held by non-affiliates and (ii) been public for at least 12 months. The value of the Trust’s outstanding equity will be measured each year on the last day of its second fiscal quarter.

Under the JOBS Act, emerging growth companies are also permitted to elect to delay adoption of new or revised accounting standards until companies that are not subject to periodic reporting obligations are required to comply, if such accounting standards apply to non-reporting companies. The Trust has made an irrevocable decision to opt out of this extended transition period for complying with new or revised accounting standards.

The Trust cannot predict if investors will find an investment in the Trust less attractive if it relies on these exemptions.

You should consider the applicable tax consequences of an investment in the Gold Deposit Receipts, and indirectly, in Gold Bullion.

You should consult with your own tax advisors in order to determine the impact of applicable taxes on your investment.

The statements contained in this prospectus that are not purely historical are forward-looking statements. The Trust's forward-looking statements include, but are not limited to, statements regarding its expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words "anticipates," "believe," "continue," "could," "estimate," "expect," "intends," "may," "might," "plan," "possible," "potential," "predicts," "project," "should," "would" and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus may include, for example, statements about:

|

|

·

|

success in obtaining Gold Bullion in a timely manner and allocating such gold;

|

|

|

·

|

the gold industry, sources of and demand for Gold Bullion, and the performance of the gold market; and

|

|

|

·

|

the development of a secondary market for the Gold Deposit Receipts.

|

The forward-looking statements contained in this prospectus are based on the Trust's current expectations and beliefs concerning future developments and their potential effects on the Trust. There can be no assurance that future developments affecting the Trust will be those that it has anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Trust's control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include those factors described under the heading "Risk Factors." Should one or more of these risks or uncertainties materialize, or should any of the Trust's assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. The Trust undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

The Trust will use the proceeds of the issuance of Gold Deposit Receipts, net of the deposit fee and any sales fee, to purchase Gold Bullion from Bank of Montreal in an amount that corresponds to the amount of Gold Deposit Receipts. The amount paid per ounce of Gold Bullion by the Trust will be equal to the spot price of one troy ounce of Gold Bullion on the date of purchase. Any deposit fees will be remitted promptly to Bank of Montreal. Neither Bank of Montreal nor BMO Capital Markets Corp. will receive any sales commissions in connection with the sale of Gold Deposit Receipts.

About the Trust

General. This discussion highlights information about the Trust. You should read this information, information about the Depositary Trust Agreement as well as the Depositary Trust Agreement before you purchase Gold Deposit Receipts. The material terms of the Depositary Trust Agreement are described in this prospectus under the heading “Description of the Depositary Trust Agreement.”

The Vaulted Gold Bullion Trust. The Trust was initially formed on December 10, 2013. The Trust is governed by the Amended and Restated by the Depositary Trust Agreement, dated June , 2016. The Bank of New York Mellon will be the trustee and BNY Mellon Trust of Delaware will be the Delaware trustee. The Trust is not a registered investment company under the 1940 Act.

The Trust is intended to hold Gold Bullion for the benefit of owners of Gold Deposit Receipts. The trustee will perform only administrative and ministerial acts. The property of the Trust will consist of the Gold Bullion and all monies or other property, if any, received by the trustee.

Initial Depositor. The initial depositor of the Trust is Bank of Montreal (“Bank of Montreal” or the “Bank”). The Bank commenced business in Montreal in 1817 and was incorporated in 1821 by an Act of Lower Canada as the first Canadian chartered bank. Since 1871, the Bank has been a chartered bank under the Bank Act, and is named in Schedule I of the Bank Act (Canada) (the “Bank Act”). The Bank Act is the charter of the Bank and governs its operations. The Bank is a registered holding company under the Bank Holding Company Act of 1956 and is certified as a financial holding company under the Gramm-Leach-Bliley Act. The Bank’s head office is located at 129 rue Saint Jacques, Montreal, Quebec, H2Y 1L6, and its executive offices are located at 100 King Street West, First Canadian Place, Toronto, Ontario, M5X 1A1. The Bank’s telephone number is (416) 867-6785.