Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - SURO CAPITAL CORP. | v441758_8-k.htm |

Exhibit 99.1

|

6.5.2016 |

To the Stockholders of GSV Capital:

In 2015, we achieved significant milestones, including realizing $54.2 million of net gains and distributing a $2.76 per share dividend. Additionally, we elected to be treated as a regulated investment company (RIC), which provides significant tax advantages for GSV Capital (GSVC) stockholders. Importantly, our Net Asset Value (NAV) reached an all-time high on September 30, 2015 of $16.17 per share, before our distribution on December 31st.

We believe the dramatic changes in the growth company ecosystem that catalyzed the opportunity for GSV Capital to be launched in May of 2011 are, if anything, becoming more pronounced. Specifically:

| • | The supply of rapidly growing, small companies with the potential for large IPOs is a fraction of what it has been historically. From 1990 to 2000, there was an average of 406 IPOs in the United States per year. From 2001 to 2015, there has been an average of 111 IPOs.1 |

| • | Private companies are staying private much longer. The time from initial Venture Capital investment to monetization has gone from an average of three years in 2000 to approximately ten years today.2 This causes liquidity issues for both early investors and company employees. |

| • | By the time a company chooses to go public, it is typically larger and more mature, with much of the growth — and corresponding rapid value creation —behind it. |

| • | The “Digital Tracks” that have been laid over the last twenty years, with over 3.1 billion Internet users, 2.6 billion smartphone users, and more than 226 billion apps downloaded in 2015.3 This allows technology entrepreneurs to go from an idea to reaching tens of millions of people at breathtaking speeds, with corresponding growth. Dropbox, for example, was launched in 2008 and has over 500 million users and 150,000 enterprise customers.4 Our new investment, Snapchat, was started in 2011, and it has reported that users now watch over 10 billion videos on the platform per day (subsequent to first quarter-end 2016, through May 9, 2016, GSV Capital invested approximately $4.0 million in Snapchat). |

| 1 | University of Florida (Professor Jay Ritter, Cordell Professor of Finance, 2016) |

| 2 | National Venture Capital Association (NVCA) |

| 3 | Gartner, Ericsson |

| 4 | Dropbox Disclosures |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 1 |

| | 6.5.2016 |

| • | Despite the IPO market being weak for much of the past fifteen years, Venture Capitalists haven’t stopped investing. VCs have invested in average of 3,200 companies per year since 2001, including 3,709 companies in 2015.5 We estimate that there are over 2,000 VC-backed private companies with a market value of $100 million or greater. |

As a liquid, publicly traded stock, GSVC is a unique vehicle that enables public investors to access this asset class, which has increasingly been limited to select venture capital firms and institutional investors. We believe that growth drives enterprise value, and accordingly, our mission is to build a portfolio of the most dynamic, rapidly growing, late-stage private companies.

2015 in Review

In 2015, we made important progress on several fronts to achieve our mission. Here are some of GSVC’s important developments:

| • | We continued to demonstrate the ability to monetize our portfolio positions at attractive returns in both public markets as well as private transactions. Our net realized gains of $54.2 million for the year ended December 31, 2015 break out as follows: |

| 5 | National Venture Capital Association (NVCA) |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 2 |

| | 6.5.2016 |

Full Year 2015 Realized Gains + Losses

| Company | Realized Gains + (Losses) | IRR* | ||||||

| $ | 26,886,514 | 40.9 | % | |||||

| 2U | $ | 37,160,718 | 65.1 | % | ||||

| SugarCRM | $ | 549,710 | 12.6 | % | ||||

| Totus Solutions | $ | (6,052,203 | ) | (85.2 | )% | |||

| DailyBreak | $ | (2,854,204 | ) | (94.8 | )% | |||

| The rSmart Group | $ | (1,264,160 | ) | (79.7 | )% | |||

| NewZoom | $ | (260,476 | ) | (98.5 | )% | |||

*IRRs are calculated based on the cash flow returns generated and corresponding dates of realized gains or losses that occurred in FY 2015. GSVC made partial sales of Twitter and SugarCRM in 2015, and still holds both positions as of 3/31/16. All other positions above were liquidated or written ot during FY 2015.

| • | On December 31, 2015, we made a $2.76 per share distribution to stockholder of record as of November 16, 2015, GSVC’s first such dividend. Following stockholder elections, the dividend consisted of approximately 2,860,903 shares of common stock issued, or approximately 14.8% of our outstanding shares prior to the dividend, as well as cash of approximately $26.4 million. |

| • | GSV Capital elected to be treated as a RIC under Subchapter M of the Internal Revenue Code, as amended, for U.S. federal income tax purposes for the 2014 taxable year, and qualified to elect to be treated as a RIC for the 2015 taxable year. We expect to continue to operate in a manner so as to qualify for the tax treatment applicable to RICs. To qualify for RIC tax treatment, among other things, GSV Capital must distribute to its stockholders, for each taxable year, at least 90% of its “investment company taxable income,” which is generally the Company’s ordinary income plus the excess of its realized net short-term capital gains over its realized net long-term capital losses. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 3 |

| | 6.5.2016 |

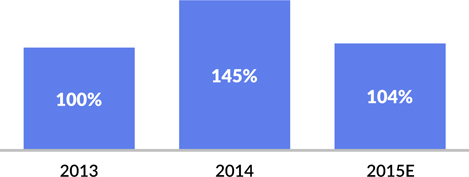

| • | The overall growth in portfolio company revenues from 2014 to 2015 was an estimated 104%, the third straight year of 100% or greater growth.6 |

| • | GSV Capital invested in the following companies in 2015:7 |

| - | Spotify ($10.0 million invested in FY 2015): Spotify is a disruptive music-streaming platform with over 100 million users and 30 million subscribers paying $10 per month, according to Reuters. In 2015, CEO Daniel Ek revealed that more than 50% of Spotifiers are under the age of 27. Remarkably, given the young demographic, 70% of Spotify’s initial 2010 subscribers are still paying customers. College kids would rather have their electricity shut off than their Spotify account. |

| - | Enjoy ($4.0 million invested in FY 2015): Enjoy is a personal commerce platform built to revolutionize the way people buy and enjoy the world’s best technology products. The central feature of the company is hand-delivery of every item to the customer, including product set-up by an Enjoy product expert, at a time and place of their choosing. The founder and CEO of Enjoy is Ron Johnson, who created the Apple retail store, including the Genius Bar, and was the former CEO of J.C. Penney. Effectively, Enjoy is Lyft-meets-Apple Genius Bar. |

| - | Declara ($2.0 million invested in FY 2015): Declara is a social learning platform that uses Artificial Intelligence to accelerate the way people discover and exchange knowledge. It helps users learn faster and smarter. In August 2015, Declara participated in the White House’s first-ever “Demo Day”, which highlighted game-changing startups tackling global challenges. |

6 Average of annual portfolio company revenue growth rates as reported by portfolio companies, excluding extreme outlier growth periods.

7 Investments shown represent a minimum aggregate $2 million 2015 investment. All amounts shown are approximate.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 4 |

| | 6.5.2016 |

In President Obama’s words, Declara is “Google meets Facebook” (Video of the President’s remarks is available HERE).

| - | GSV Sustainability Partners ($2.3 million invested in FY 2015): GSV Sustainability Partners (GSV SP) is a transformative finance company unlocking value from savings generated by sustainable energy, water, and waste management technology. GSV SP is pioneering Sustainability as a Service™—the green-tech sector’s own “SaaS”. Co-founder John Denniston is a leading authority on green-tech investing, and is a former Investment Partner at Kleiner Perkins. CEO and co-founder Tom Cain has invested in a range of breakthrough water and energy technologies for over a decade. |

| - | PayNearMe ($4.0 million invested in FY 2015): PayNearMe is a next-generation, electronic cash payment platform. It serves what the Federal Deposit Insurance Corporation (FDIC) estimates to be 93 million “unbanked” and “underbanked” residents of the United States, allowing them to pay auto, rent, and utilities bills through retail locations. The company currently has relationships with 7-Eleven, Family Dollar, and ACE Cash Express stores. PayNearMe is continuing to aggressively expand its retail footprint, as well as the breadth of industries that its payment system covers. |

| - | Lyft ($2.5 million invested in FY 2015): Lyft is an on-demand, ride-sharing platform for friendly and affordable rides. Drivers are matched with passengers who request rides through the Lyft iPhone or Android app. Transactions are automated through the app and drivers can earn income on something they already own — their car. Forbes recently reported that ride volume grew 300% from 2014 to 2015, noting that Lyft completed 11 million rides in April 2016 alone. |

| - | GSVlabs ($3.5 million invested in FY 2015): As the access point to a startup ecosystem, major corporations like AT&T, Intel, Google Developers Launchpad, IBM, The Times of India, 3M, and JetBlue choose to partner with GSVlabs in order to launch new initiatives, identify talent, attack new markets, and propel new business models. GSVlabs creates value through this virtuous circle, attracting and accelerating promising entrepreneurs, while providing targeted innovation services for forward-thinking corporations. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 5 |

| | 6.5.2016 |

| • | Notable 2016 investments for GSV Capital to date include8: |

| - | Snapchat ($4.0 million invested subsequent to first quarter-end, through May 9, 2016): Snapchat is emerging as the most popular and engaging social media platform for the Millennial generation, driven by innovative new offerings such as Stories, Discover Media Partners, and Lenses + Filters. Snapchat’s 100 million+ users watch more than 10 billion videos per day, up from just two billion in May 2015. |

| - | Curious.com ($2.0 million invested in first quarter 2016): Curious helps people learn anything, from how to play the banjo to basic business skills. Described by Forbes as the “Netlix for learning,” the Curious platform offers “all you can eat” access to over 20,000 high quality digital lessons on virtually any topic through a subscription model. Curious is powered by leading cognitive science research, which demonstrates that learning doesn’t just make you smarter — it makes you happier, healthier, and more productive. |

| - | Lytro ($2.5 million invested in first quarter 2016): Lytro is a pioneering Light Field Imaging platform that is redefining the way images are captured and created across a broad range of applications — from virtual reality to photography and filmmaking. The company has the opportunity to make transformative improvements on any imaging device with a lens and sensor. |

8 Investments shown represent a minimum aggregate $2 million 2016 investment. All amounts shown are approximate.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 6 |

| | 6.5.2016 |

2015 FINANCIAL INFORMATION

GSV Capital’s Net Asset Value (NAV) was $268.0 million on December 31, 2015. This compares to a NAV of $285.9 million on December 31, 2014. NAV per share was $12.08 on December 31, 2015 (reflecting the $3.16 cumulative per share effect of GSVC’s distribution to shareholders in the fourth quarter of 2015), versus $14.80 on December 31, 2014.

We believe the most useful (but imperfect) measure to track GSV Capital’s progress is to compare the change in NAV, both on an absolute and relative basis, to the performance of the S&P 500. We use NAV as a tracking device because it is tangible. But the most important measurement is the growth of the intrinsic value of GSV Capital’s portfolio.

Our NAV changes primarily as a result of the changes in our investment portfolio, which under U.S. GAAP is measured at fair value. We calculate NAV on a quarterly basis using a rigorous process that values every security in the portfolio.

GSV Capital’s Board of Directors also engages an outside valuation firm, Andersen Tax, to perform an independent appraisal of the portfolio and its corresponding NAV each quarter. When there are differences between the analyses done by GSVC management and Andersen, the Valuation Committee of the Board decides which value to apply.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 7 |

| | 6.5.2016 |

PORTFOLIO REVIEW

As of March 31, 2016, GSV Capital held positions in 46 portfolio companies with an aggregate fair value of $325.3 million. Excluding Treasuries, our three largest investments comprised 25.1% of the total portfolio, at fair value, while GSVC’s top ten portfolio companies accounted for 53.8% of the total portfolio.

Top 10 Investments as of March 31, 2016 $ in millions (rounded)

| Company | Fair Value | % of portfolio | ||||||||

| 1 | Palantir Technologies | $ | 46.1 | 14.2 | % | |||||

| 2 | Dropbox | $ | 19.2 | 5.9 | % | |||||

| 3 | Spotify | $ | 16.2 | 5.0 | % | |||||

| 4 | Coursera | $ | 14.4 | 4.4 | % | |||||

| 5 | Solexel | $ | 14.0 | 4.3 | % | |||||

| 6 | PayNearMe | $ | 14.0 | 4.3 | % | |||||

| 7 | Lyft | $ | 13.7 | 4.2 | % | |||||

| 8 | $ | 13.2 | 4.1 | % | ||||||

| 9 | Declara | $ | 12.0 | 3.7 | % | |||||

| 10 | Curious.com | $ | 12.0 | 3.7 | % | |||||

| Total (rounded) | $ | 174.9 | 53.8 | % | ||||||

Please refer to Appendix A on page 41 for further detail about each company.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 8 |

| | 6.5.2016 |

It is our belief, based on our research and experience, that a disproportionate number of the big winners are found by focusing on themes where significant change and growth are taking place. Megatrends are powerful technological, economic, and social forces that provide a tailwind at the back of growth sectors. The convergence of Megatrends and growth themes is how we develop investment themes focused on identifying the “Stars of Tomorrow”… the fastest-growing, most dynamic companies in the world. We have identified five themes that we believe are the most fertile for investments in companies with the greatest potential:

| 1. | Cloud + Big Data (32.9% of portfolio Fair Value as of 3/31/16): Over 90% of the world’s data has been created in the last two years.9 According to the MIT Technology Review, by 2020, 1.7 megabytes of new information will be created every second for every human being on the planet. To put that in perspective, in 1969, we sent astronauts to the moon and back using computers with only 2 kilobytes (0.002 megabytes) of memory. At the same time, organizations are struggling to make use of abundant new sources of information. EMC projects that less than 5% of target-rich data is analyzed today, let alone used. Powerful software analytics are creating massive opportunities for innovative companies that are attacking a global Big Data services market that surpassed $125 billion in 2015.10 |

| 2. | Education Technology (30.3% of portfolio Fair Value as of 3/31/16): In a Knowledge Economy and Global Marketplace, education makes the difference in terms of how well an individual does, how well a company does, and for that matter, how well a country does. The Internet, combined with ubiquitous smartphones, democratizes education access by lowering cost, and now, improving quality. We are starting to see the rise of what we call “Weapons of Mass Instruction” — rapidly scaling education companies attracting millions of students in a short period of time. |

| 3. | Social Mobile (17.6% of portfolio Fair Value as of 3/31/16): In 2008, the average American spent 2.7 hours per day on digital media. In 2015, we spent 2.8 hours per day on smartphones alone — more time than we used to spend on desktops, laptops, mobile, and other connected devices combined.11 Over 87% of Millennials sleep with their smartphones and 97% U.S. high school and college students would rather lose every other possession before giving up their smartphone.12 Facebook-owned WhatsApp processes a mind-bending 60 billion messages per day while Snapchat users upload 9,000 photos per second. Social everything — communication, collaboration, photography, music, shopping, education, and healthcare — is the future and it is going to be done anytime, anywhere on mobile devices. |

| 9 | IBM |

| 10 | Forbes, IDC |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 9 |

| | 6.5.2016 |

| 4. | Marketplaces (13.3% of portfolio Fair Value as of 3/31/16): The foundation of modern economics is Adam Smith’s “invisible hand.” As people make economic decisions in their own self-interest, it ultimately brings economic benefits to others. But the rise of modern information technology and ubiquitous mobile computing has made the invisible hand a lot more collaborative. On any given night, roughly one million travelers who would have typically checked into a hotel are instead using Airbnb’s marketplace to rent unused houses, apartments, and bedrooms for a better price — and a more unique experience. Millions more are saving time and money by ditching taxis for rides with services like Uber and Lyft. The Internet is exceptionally suited to aggregate supply and demand within an industry, and smartphones amplify the tremendous network effects that can be created. |

| 5. | Sustainability (5.9% of portfolio Fair Value as of 3/31/16): The good news is that the world’s middle class will more than double to five billion over the next 15 years.13 The bad news is that the strain this will put on the environment will be extreme, with wealthier people traveling more, consuming more, and using more electricity for everything — from air conditioning to lighting larger homes. Sustainability is not just green technology — it is water and wellness. There is no longer a debate between being “green” or “growing” — both are important. Water is even more precious, with California’s drought being a living example of how vital access to “blue gold” is for everything. Despite the prolonged slump in oil prices, Moore’s Law has taken effect with numerous sustainable technologies being able to compete on cost with dirty fossil fuels. |

11 eMarketer, KPCB

| 12 | Chegg |

| 13 | OECD |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 10 |

| | 6.5.2016 |

GSV Capital Portfolio Distribution by Sector/Theme

Figures are based upon the fair value of each holding as of March 31, 2016, or the cost basis of the holding (exclusive of transaction costs) if the investment closed subsequent to March 31, 2016. In either case, these values are divided by the net assets of GSV Capital as of March 31, 2016.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 11 |

| | 6.5.2016 |

Ten Lessons from GSVC’s First Five Years

We took the “idea”of GSV Capital public in May 2011. While our original thesis has remained solid over the past five years, we have learned a lot, which will be reflected in our future investments.14

1) Focus on emerging growth companies… Series B and beyond.

From the outset, our strategy was for 90% of GSV Capital investments to be in emerging growth companies, with the remaining 10% allocated to early stage opportunities. While our record for early stage investments has been in line with our expectations, we have learned that these holdings are not ideally suited for a publicly traded fund.

91% of the GSV Capital Portfolio is “B Round” or Later

GSV Capital Portfolio Distribution by Investment Stage

Figures are based upon the fair value of each holding as of March 31, 2016, or the cost basis of the holding (exclusive of transaction costs) if the investment closed subsequent to March 31, 2016. In either case, these values are divided by the net assets of GSV Capital as of March 31, 2016.

14 These items are solely the opinion of GSVC management and should not be construed as investment advice or an offer to sell, or solicitation of an offer to buy, securities.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 12 |

| | 6.5.2016 |

At the same time, we believe there is an enormous opportunity to invest in growth stage, VC-backed private companies. Accordingly, we expect future investments to be in the “B Round” or above — essentially investing in companies that would have historically reached an IPO stage.

2) Don’t buy shares too close to the IPO.

We have found that the closer a company is to an IPO, the more it becomes a “seller’s market”. Buyers have comparatively less leverage on terms and valuation. Additionally, as growth investors, GSVC’s investments typically need more than 12 months to realize value. Within a year of an IPO, there is a limited margin of safety.

GSV Capital’s Power Alley

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 13 |

| | 6.5.2016 |

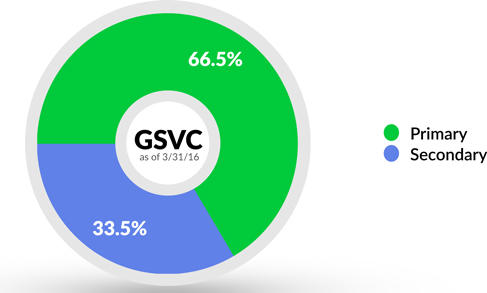

3) We’re agnostic between primary and secondary shares, but GSV Capital has a competitive advantage in secondaries.

When GSV Capital was launched, we expected that the majority of our investments would be secondary transactions. And in fact, some of our portfolio’s most recognizable names — such as Facebook, Twitter, Dropbox, Spotify, and Palantir — were almost entirely secured through secondaries. But we have also found great opportunities to invest in primary rounds alongside premier institutional investors.

GSV Capital Portfolio Distribution by Primary + Secondary Investment

Figures are based upon the fair value of each holding as of March 31, 2016, or the cost basis of the holding (exclusive of transaction costs) if the investment closed subsequent to March 31, 2016. In either case, these values are divided by the net assets of GSV Capital as of March 31, 2016.

We are agnostic in terms of whether we invest in secondaries or primaries. Our goal is simply to invest in the top private companies in the world at a fair price. While primaries offer certain benefits, including an abundance of information, GSVC’s deep experience with secondaries creates advantages in terms of access, diligence, and timing. Given that investing in secondary shares can be more challenging for many investors, we believe it presents an opportunity for GSVC to secure better pricing, which can help drive superior returns.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 14 |

| | 6.5.2016 |

4) Avoid “lead” investments and make sure there are top institutional investors involved.

GSV Capital invests alongside or behind leading VCs, including 12 deals with Kleiner Perkins (KPCB), and 8 deals each with Institutional Venture Partners (IVP), Benchmark, and New Enterprise Associates (NEA). A strong, well-networked investor base creates unfair advantages for emerging growth companies, including superior access to talent, counsel, and strategic partnership opportunities, as well as greater visibility into follow-on financings.

GSV Capital Invests Alongside Leading VCs

Investments as of May 9, 2016

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 15 |

| | 6.5.2016 |

5) Sell when you have an opportunity at a fair price.

While we believe we have done a good job monetizing positions at compelling prices as opportunities have arisen, in hindsight, we would have been more aggressive sellers in some cases.

For example, in 2014 and 2015 we sold a total of 1.1 million shares of Twitter for a $37.1 million realized gain and a 41% IRR. We kept our remaining 800,600 shares for the upside we believe exists. The subsequent decline in the value of Twitter shares will provide a strong reminder to exit positions when we can realize a fair value relative to the lifecycle of our investment, rather than holding out for the last nickel.

6) Create unfair advantages through a GSV ecosystem… A strong brand creates opportunities.

In April 2016, we hosted the 7th Annual ASU GSV Summit. Launched in partnership with Arizona State University, the Summit convenes key leaders from across the global innovation economy with the goal of improving educational outcomes through exponential ideas. Ultimately, we believe it provides a window to future opportunities and is a platform to accelerate investments we’ve made.

Called “The Must-Attend Event for Education Technology Investors” by the New York Times, the ASU GSV Summit welcomed over 3,700 attendees in 2016, including a wide range of entrepreneurs, investors, foundation leaders, educators, policymakers, and CEOs of leading global companies. Keynote speakers included Bill Gates, Former U.S. Secretary of State Condoleezza Rice, Khan Academy Founder Sal Khan, business strategy visionary Jim Collins, General Stanley McChrystal, Common, and many others. Over 300 of the most important education and human capital companies in the world presented.

On September 14-15, 2016, GSVlabs will host the 2nd Annual Pioneer Summit, which is focused on transformative entrepreneurs and ideas that are changing the world for good.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 16 |

| | 6.5.2016 |

7) Being right on the fundamentals is more important than being perfect on valuation.

We complete a rigorous valuation process and underwrite our investments with a minimum 30% IRR expectation. The cold hard fact is that we believe the mistakes that have negatively impacted us are not on valuation but on incorrectly forecasting growth fundamentals.

The GSVC management team has done numerous studies over the last 20 years — both before and after the launch of GSV Capital — that consistently demonstrate a high correlation between sustainable growth and increasing enterprise value (you can find our most recent annual 10-Year Top Performing Stocks study HERE). Accordingly, we aspire to build a portfolio that has the highest and most sustainable growth rate.

We believe the growth characteristics of GSV Capital’s portfolio companies are very strong, with expected year-over-year revenue growth exceeding 100%. Our focus is on investing in enterprises that align with our target fundamentals, not purchasing shares of companies in the “bargain basement”.

Average GSV Capital Portfolio Revenue Growth Rate, 2013-2015 E*

*Average of annual portfolio company revenue growth rates as reported by portfolio companies, excluding extreme outlier growth periods

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 17 |

| | 6.5.2016 |

8) Create your own research rather than listening to the “experts” and pundits.

One of the characteristics of great companies is that they are systematic and strategic in how they operate their business. Similarly, if you want to be a great investor, you need to be systematic and strategic in how you analyze companies.

Research is the foundation of our investment process. With that in mind, we publish a weekly research newsletter, A2Apple, which focuses on key trends in the global growth economy, rotating topically across GSV Capital’s core investment themes.

We also recently released 2020 Vision: History of the Future, our seventh in a series of white papers focused on the future of human capital and education innovation. It provides in-depth analysis around transformational ideas, models, organizations, and companies, including over 100 case studies and profiles.

9) Short-term market volatility creates long term investment opportunity.

The overall market environment has been volatile, particularly in early 2016, with NASDAQ dropping nearly 10% from January 1st to February 11th, before ending up flat for the first quarter.

We have also seen markdowns across the board for private companies. The good news is that this dynamic enabled us to acquire shares in Spotify in the fourth quarter of 2015 at a nearly 25% discount to the company’s Series G financing earlier in the year. The bad news is that we have recorded some near-term markdowns to the portfolio.

An example of this trend is Snapchat. Last fall, Fidelity Investments marked down its position in the company by 25%, only to mark it up again 15% in December. In March, Fidelity invested $175 million in Snapchat at a flat valuation to its previous financing.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 18 |

| | 6.5.2016 |

10) It’s all about the PEOPLE. Great TEAMS find a way to win.

In business, sports, and life, winners typically find a way to win. While we often invest in enterprises that don’t have long histories, the people in charge typically do. While it’s not a new lesson, the power of people to create transformative businesses has never rang more true. Our goal is to find winning TEAMS and stick with them.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 19 |

| | 6.5.2016 |

INVESTING IN EXPONENTIAL IDEAS

The Race to $1 Trillion

While the U.S. Presidential race is of huge interest, for investors, the race to become the first trillion-dollar market value company is fascinating. The four horses in the race are Amazon, Apple, Facebook, and Alphabet (Google). The favorite to reach $1 trillion has been Apple for some time, with its market value exceeding $700 billion in 2015. But post-Steve Jobs, Apple struggled to regain its mojo, with a series of ho-hum product introductions, from the Apple Watch to Apple Music.

Alphabet has started to gain some real traction with bets on YouTube, Adwords, and Android all producing dominant services in their respective areas. Amazon, powered by its Amazon Web Services (AWS), has continued to surge. Estimated to be worth over $160 billion, AWS entered 2016 with customers in 190 out of 196 countries — just about every corner of the world.

In 2013, we wrote about the “Race to a Trillion”, adding Facebook to the mix as a dark horse candidate. With a $119 billion market cap at the time, “long shot” sounded like an understatement:

Facebook with a market cap of $119 billion is definitely the underdog of the Big Four to reach $1 trillion first, and with just $7 billion in sales and a rich price-to-sales of 17.5x and 67x price-to-earnings, tough to see FB getting to a $1 trillion on multiple expansion. That said, as the World’s communication and collaboration platform, the leverage to its model is enormous and while it’s a long way back in the pack — it has the opportunity to grow at the highest rate for the longest time. So, if it could grow its revenues at its historic 100% growth and keep the current valuation ratio, it would reach the $1 trillion club by 2017… unlikely but not beyond the realm of possibilities.

Coming from relatively way back, however, Facebook is starting to look like it might make it to the trillion dollar finish line first. It has been propelled by a monster network of nearly 2 billion people and the home runs Mark Zuckerberg hit with his high-risk venture bets on Instagram, WhatsApp, and Oculus.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 20 |

| | 6.5.2016 |

Facebook Transformation by Acquisition

| Acquisition | Type | Price | Year | Impact | ||||

|

Social Media |

$1B | 2012 | Slammed as an overpriced acquisition, Instagram commands 400M+ enthusiastic users | |||||

| Atlas |

Advertising |

$100M | 2013 | Cross-device advertising platform leveraging Facebook’s 1.7B+ installed user base | ||||

| Parse |

App Development |

$85M | 2013 | App development platform situates Facebook as an integration hub for emerging mobile apps and IoT platforms | ||||

|

Messaging |

$22B | 2014 | With 1B+ users, WhatsApp is the most popular messaging app worldwide | |||||

| Oculus VR |

AR/VR |

$2B | 2014 | Oculus is a pioneer of high-quality, mass market Virtual Reality (VR); It is pioneering the consumerization of VR | ||||

| LiveRail |

Advertising |

$400M+ | 2014 | Video advertising platform delivers 90%+ accuracy on age and gender segments | ||||

| Pebbles |

AR/VR |

$60M+ | 2015 | AR/VR gesture-control technology enhances Oculus capabilities |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 21 |

| | 6.5.2016 |

Today, Facebook has a market value of $339 billion and a P/E of 26x. But it is growing earnings at over 40% per year. Hold P/E constant and assume growth of 40%, and Facebook will hit the trillion dollar mark in the summer of 2019. But it will be a photo finish with Alphabet, which would cross the line in early 2020.

The Race to $1 Trillion

| Market | Growth | |||||||

| Company | Cap | Rate** | P/E (NTM) | Timing to $1T | ||||

|

$342B | 30% | 75x | Q3 2020 | ||||

|

$536B | 10% | 11x | Q4 2022 | ||||

|

$339B | 40% | 26x | Q3 2019 | ||||

|

(Alphabet) |

$496B | 20% | 18x | Q2 2020 |

Source: Capital IQ, GSV Asset Management

*Data current as of 6/3/2016

**GSVC Estimate

The Race to a Trillion underscores a broader point. We have entered an age of exponential ideas. “Linear” businesses are going extinct. Looking at the changes that have taken place in the world’s largest market cap companies in the past 15 years, it is interesting to note that Apple wasn’t on the list, Facebook didn’t exist, and Google and Amazon were just babies. We continue to be reminded that change is like gravity, and that opportunities for the forward-looking abound.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 22 |

| | 6.5.2016 |

Top 10 Companies by Market Value, 2000 vs. 2015

| 2000 | 2015* | |||||

| Company | Market Cap | Company | Market Cap | |||

| 1. General Electric | $477 Billion | 1. Apple | $605 Billion | |||

| 2. Cisco | $305 Billion | 2. Google (Alphabet) | $527 Billion | |||

| 3. Exxon Mobil | $286 Billion | 3. Microsoft | $446 Billion | |||

| 4. Pfizer | $264 Billion | 4. Exxon Mobil | $332 Billion | |||

| 5. Microsoft | $258 Billion | 5. Berkshire Hathaway | $331 Billion | |||

| 6. Walmart | $251 Billion | 6. Amazon | $311 Billion | |||

| 7. Citigroup | $250 Billion | 7. Facebook | $296 Billion | |||

| 8. Vodafone | $227 Billion | 8. General Electric | $292 Billion | |||

| 9. Intel | $227 Billion | 9. Johnson & Johnson | $287 Billion | |||

| 10. Royal Dutch Shell | $206 Billion | 10. Wells Fargo | $280 Billion | |||

Source: Capital IQ, GSV Asset Management

*2015 Year End Market Capitalization

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 23 |

| | 6.5.2016 |

The Age of Exponential Ideas

Why does electric carmaker Tesla trade at 15 times the P/E of General Motors? Because a Tesla now gives you the ability to drive 270 miles, and you can recharge your car in the time it takes to grab lunch. If Teslas could travel only 40 miles, the company would be dead in the water. Add in the fact that Teslas are effectively computers on wheels (with hands-free mode they drive themselves) and you have a game-changing product.

Tesla’s Battery Outpaces the Competition

Drivable Miles on a Single Battery Charge by Car Brands

General Motors, in contrast, spends over $7.2 billion per year on R&D, and the net result has been the Cadillac ELR, which will take you 35 miles on a charge. In early January 2016, the company announced a $500 million investment in the ride-sharing platform, Lyft, and laid out plans to develop a network of on-demand self-driving cars. A week later, it announced the acquisition of the ride-sharing service, Sidecar. As millennials continue to opt for cars on demand, as opposed to cars in the garage, GM is scrambling to catch up with the future.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 24 |

| | 6.5.2016 |

We are riding powerful tailwinds that are rapidly transforming the world as we know it. In 2000, there were only 370 million people on the Internet (roughly 5% of the world’s population), no one had heard of a smartphone yet, broadband was a fantasy, and applications off of a platform had not been invented.

Bubble vs. Boom

| Global Indicator | 2000 | Today | ||

| Internet Penetration | 370 million (6%) | 3.1 billion (43%) | ||

| Broadband Penetration | 60 million (1%) | 2.3 billion (32%) | ||

| PC Penetration | 180 million (3%) | 1.4 billion (20%) | ||

| Mobile Phone Penetration | 740 million (12%) | 7 billion (98%) | ||

| Smartphone Penetration | 0 | 2.6 billion (40%) | ||

| Tablet Penetration | 0 | 500 million (7%) | ||

| Mobile App Downloads | 0 | 226 billion | ||

| Computing Cost | $7.03 per MM Transistors | $0.04 per MM Transistors | ||

| Computer Storage Cost | $4.77 per GB | $0.02 per GB | ||

| Digital Natives in Workforce | 6% | 35% | ||

| Global Middle Class (OECD Estimates) | 1.4 billion | 2.5 billion |

Source: Gartner, Nielsen, A.T. Kearney, eMarketer, Deloitte, Ericsson, OECD

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 25 |

| | 6.5.2016 |

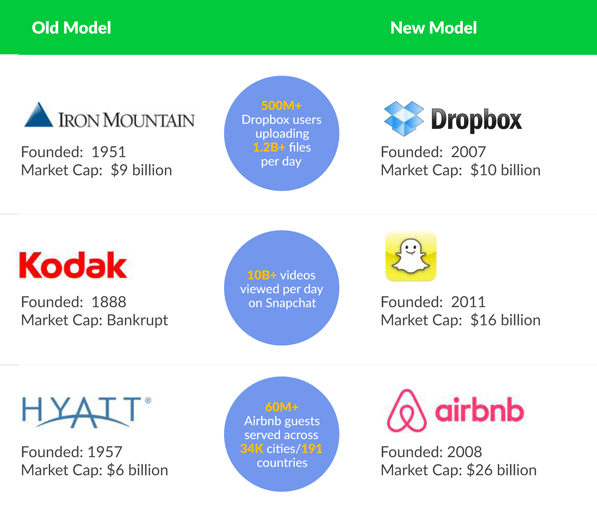

Today, digital infrastructure is in place, with three billion people on the Internet, over 2.6 billion smartphones in the hands of Digital Natives, and 226 billion apps having been downloaded from Apple and Google. These dynamics have paved the way for disruptive businesses to launch at lightening speeds. Companies like Uber, which is upending the transportation industry, and Airbnb, which is redefining the hotel industry, have gone from idea to “Billion Dollar Baby” seemingly overnight.

Billion Dollar Babies: Transformational Private Companies

Source: Yahoo Finance, Company Disclosures, GSV Asset Management

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 26 |

| | 6.5.2016 |

On a related front, these new fundamentals have increasingly created a “winner take all economy”. With technology in general, and the Internet specifically, disproportionate gains typically accrue to the leader in a category.

YouTube has over 1.1 billion users, while its closest competitor, Vimeo, has 170 million. With $113 billion in revenue over the last 12 months, Amazon is roughly 1,000x larger than its nearest open-market competitor, Jet. Facebook is now the largest “country” in the world, with nearly 1.7 billion users connected across a portfolio of highly engaging social apps. It has become the undisputed global center for communication and collaboration.

Making Private Public

In the United States, there are now half as many publicly traded companies as there were 20 years ago. The drop from 7,313 listed companies in 1997 to 3,700 today has been driven by a combination of fewer IPOs and increased M&A activity15.

First, VC-backed private companies are staying private longer (a three-year median in 2000 versus approximately ten years in 2015). According to the annual National Venture Capital Association Yearbook, 3,709 companies received VC investment in 2015. There were just 152 IPOs in the same period.

At the same time, global M&A deal volume surpassed $5 trillion in 2015, breaking a previous record of $4.6 trillion set in 2007.16

Today, corporate cash reserves stand at $1.9 trillion, a 176% increase over the past decade.17 That’s about as large as India’s entire GDP. Technology companies have continued to “roll up” the industry, with the “Big 8” completing over 500 acquisitions worth more than a combined $112 billion since 2010.

| 15 | Bloomberg |

| 16 | MarketWatch |

| 17 | New York Times |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 27 |

| | 6.5.2016 |

The Big 8 of Tech M&A

Total M&A Transactions (504) + Disclosed Transaction Value ($112B), 2010-2015*

| Company | # M&As |

Transaction Value |

Company | # M&As |

Transaction Value* | |||||

|

36 | $3.1 Billion |  |

76 | $8.2 Billion | |||||

|

39 | $5.8 Billion |  |

46 | $17.7 Billion | |||||

|

56 | $24.8 Billion |  |

55 | $19.9 Billion | |||||

|

(Alphabet) |

139 | $23.9 Billion |  |

57 | $8.6 Billion |

Source: Capital IQ, GSV Asset Management

*Based on announcement date; Includes private placement

Like a society that is dying faster than new kids are born, we believe the public markets will continue to shrink and won’t reverse until it becomes more attractive to be a public company. Two consequences we expect to become increasingly pronounced are higher P/E multiples for listed companies due to supply-demand imbalances, coupled with increasing interest in private company investments.

Investors used to have access to emerging, rapidly growing companies with big potential earlier in the life-cycle — jumping in on IPOs at $100 million or $300 million market caps. Times have indeed changed. Dramatic growth and value creation are increasingly taking place in the private marketplace, where the next generation of “exponential businesses” is emerging.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 28 |

| | 6.5.2016 |

Where Have All the Public Companies Gone?

Number of Listed Firms in U.S. Stock Market, 1975-2015*

Source: Wilshire Associates, GSV Asset Management

*Excluding Investment Funds and Trusts

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 29 |

| | 6.5.2016 |

Silicon Valley 3.0

In 1970, Xerox Corporation launched Xerox PARC in Palo Alto to develop captive innovation for the company. The charter for the initiative was to create “The Office of the Future”. Assembling a world-class team of experts in information technology and physical sciences, Xerox PARC was a catalyst for innovation — it yielded the original design for the personal computer (and famously inspired Steve Jobs to create the first Macintosh), the first Graphical User Interface, and even the computer mouse.

Founded in 2012, GSVlabs is a global innovation platform based in Silicon Valley that accelerates startups and connects corporations to exponential technologies, business models, and entrepreneurs. We believe it is a next generation Xerox PARC.

At the core of GSVlabs is a community of game-changing entrepreneurs focused on key verticals, including Big Data, Sustainability, Education Technology (EdTech), Entertainment, and Mobile. GSVlabs is home to over 170 startups, which raised $200 million in 2015.

As the access point to a startup ecosystem, major corporations like AT&T, Intel, IBM, Intuit, and JetBlue choose to partner with GSVlabs in order to launch new initiatives, identify talent, attack new markets, and propel new business models. GSVlabs creates value through this virtuous circle, attracting and accelerating promising entrepreneurs, while providing targeted innovation services for forward-thinking corporations.

GSVlabs generates outsized economic value by accelerating both startups and corporate innovation, enhanced by a proprietary talent and advisory network. By combining these elements in a single platform, GSVlabs unlocks powerful network effects. Top entrepreneurs are typically drawn to an ecosystem with high-value resources and relationships, which in turn draws in global businesses and talent.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 30 |

| | 6.5.2016 |

GSVlabs Innovation Platform

Connecting Startups, Corporations, and Talent to Produce Game-Changing Innovation

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 31 |

| | 6.5.2016 |

The GSVlabs economic model is built on the interplay of startups, corporations, and talent:

| • | Startups: GSVlabs attracts and accelerates entrepreneurs by offering high-value programming (e.g. Events, General + Sector-Specific Educational Resources, etc.), connectivity to leading corporations, and access to a network of relevant mentors and investors. Revenue sources include monthly membership fees (desk rental) and capturing company equity through GSVlabs accelerator programs. |

| • | Corporations: GSVlabs offers end-to-end solutions for corporations seeking to jumpstart innovation initiatives, ranging from in-house Talent Development, to Idea Generation, Research & Development, and Corporate VC. GSVlabs drives corporate innovation through basic and bespoke services, including startup accelerators, innovation showcases, “ideathons,” hackathons, workshops, and design-thinking programs. |

| • | Talent: GSVlabs offers highly relevant educational programming for entrepreneurs and corporations, as well as a broader network of job-seekers and professionals who would like to upgrade their skills. “ReBoot”, for example, is a proprietary educational and networking program that empowers women to restart their careers through immersive technology education and professional networking. |

GSVlabs sits at the intersection of proven models — co-working platforms like WeWork ($16 billion valuation), which generate recurring revenue from startups, and accelerators like Y-Combinator, which capture equity in potentially game-changing businesses (Y-Combinator alumni include Dropbox and Airbnb, valued at $10 billion and $26 billion, respectively).

In May 2016, GSVlabs announced a partnership with the $2 billion venture capital arm of the Times of India to launch two centers in India — one in Bangalore and one in Delhi (Gurgaon). We envision GSVlabs expanding to the top innovation centers around the World.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 32 |

| | 6.5.2016 |

Top 50 Innovation Centers in the World

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 33 |

| | 6.5.2016 |

GSV CAPITAL INVESTMENT PROCESS

GSVC’s research and investment process is structured to accomplish the identification of large, open-ended growth opportunities as well as individual companies that possess the critical elements necessary to capture meaningful market share in these opportunities.

Our top-down perspective focuses on the intersection of Megatrends (technological, economic, and social forces that disrupt the status quo) across growth sectors of the economy to identify game-changing businesses with innovative technologies and services. We’re looking for large, open-ended growth opportunities as well as individual companies that possess the critical elements necessary to capture meaningful market share in these opportunities.

GSVC’s bottom-up analysis is centered on the Four Ps — People, Product, Potential, and Predictability — an objective framework to assess a company’s potential to realize sustained long-term growth resulting from market Megatrends.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 34 |

| | 6.5.2016 |

GSV Capital’s 10 Commandments

GSVC’s 10 Commandments are embedded in our investment process. These simple principles provide the foundation of our investment framework:

| 1. | Be right on the fundamentals. Earnings growth drives long-term value creation. There is essentially a 100% correlation between how a company does and how it is valued over time. Focus on the fastest-growing companies. |

| 2. | Be proactive, not reactive. Looking ahead and anticipating where the world is going is how we catch winners early on. Try to predict tomorrow’s headlines as opposed to reacting to what is in today’s. |

| 3. | Be rigorous, but don’t have rigor mortis. Looking at the balance sheet to make sure a company has enough cash to support your “blink” decision is important, but it is possible to overanalyze opportunities. The best investments are often intuitive. |

| 4. | When wrong, admit it. The best investors are wrong a lot. The worst thing to do is rationalize a mistake. Be intellectually honest. Make decisions based on current facts, not what you thought to begin with. |

| 5. | The cockroach theory: You seldom find just one cockroach in the kitchen. Likewise, if you find a problem at a growth company, there are always more behind it. It is rarely a one-quarter issue. |

| 6. | Investment ideas are about information and insight. Information is valuable if it is proprietary. Insight is valuable if we know what that information means. |

| 7. | The Four Ps (People, Product, Potential + Predictability) are key for any successful growth company. The first “P”, People, is the most important. |

| 8. | Use five independent sources for each company you invest in. If possible, have a regular dialogue with the company’s management team, but remember that they will always see the glass as being half-full. |

| 9. | Find the three key reasons for the company to achieve our expectations and objectives. In addition, identify near-term catalysts for performance changes. Maintaining a thesis for why you own the company is key. |

| 10. | Be passionate about investing but dispassionate about the investment. We need to fight hard for our management teams, but also make decisions that are based on the current realities. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 35 |

| | 6.5.2016 |

Megatrend Analysis + Investment Themes

GSVC’s 10 Commandments create a consistent framework to cement our philosophy and are integrated into everything that we do. We then start with a top-down view of each growth sector to determine how Megatrends and industry drivers are influencing the potential of an industry. From that top-down approach, we create investment themes, which are where we focus our research and resources.

GSV Capital Megatrends + Investment Themes

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 36 |

| | 6.5.2016 |

The nature of Megatrends is that they are relatively slow to develop, driven by bottom-up “local” events that slowly gain in critical mass until they come to define large-scale and pervasive change. Identifying new trends is always difficult.

But only by continuing to look for the forces that shape the world’s trajectory — and how those forces will impact key sectors — is it possible to capitalize on opportunities and catalyze change.

For example, the Internet Age, which was born with the commercialization of Netscape Navigator, is only 20 years old. But it has already reshaped virtually every industry. Virtual networks connecting over three billion people define the ways we communicate, collaborate, shop, enjoy entertainment, and learn. Broad Megatrends that are transforming the world as we know it include Globalization, the Mobile Internet, and Sustainability.

The Four Ps

Next, we strive to identify and track the key companies within the themes we have identified. We evaluate investment opportunities through a lens that combines the Megatrends that we highlighted with company-specific attributes — an approach we call the “4 Ps”.

The first “P” is for “People” and it is the most important “P” by far. There is no shortage of interesting ideas, but it’s always the TEAM’s ability to execute against the opportunity that determines success or failure. Our experience is that “winners” find a way to win and attract other winners.

The Second “P” stands for “Product.” We want to support companies that are leaders in what they do, have a proprietary product or service, or better yet, a “one-of-a-kind” type of business. Said another way, a company needs to have a claim to fame. “Me too” enterprises are of no interest to us.

Technology, in general, and the Internet, in particular, are all about disproportionate gains to the leader in a category. We want to back businesses that not only survive, but thrive, during their corporate evolution.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 37 |

| | 6.5.2016 |

The Third “P” is for “Potential” — how big can the company become? Determining total future market potential is a pillar of our research. Megatrends influence our analysis as they provide “tailwinds” to accelerate growth. Often, the companies with the most potential are where the biggest problems are —the bigger the problem, the bigger the opportunity.

GSV Capital’s “4Ps” Analytical Framework

People Organizations led by strong management teams with in-depth operational focus

Potential Large addressable markets and scalable impact |

|

Product Leading product or service

Predictability Business model lends itself to high and visible growth |

The last “P” is for “Predictability” — how visible is the company’s growth and what kind of operating leverage does it get with scale? For most new enterprises, having any degree of confidence in the forecast is a challenge. But we are looking for business models that create predictability, whether it’s through recurring revenue or a clear articulation of operating metrics that drive the business.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 38 |

| | 6.5.2016 |

Disciplined Valuation Approach + Selection Process

After we rate the companies within our investment themes, we have a disciplined valuation approach based on growth potential and future prospects.

Disciplined Valuation Approach

| Fundamental Analysis: | Management

Team Analysis: | ||

• Proprietary

company “Fact • Systematic

framework for • Megatrends analysis • Four

Ps (People, Product,

Financial Analysis:

• Proprietary

growth • Forward

Model: Income • Breakeven analysis • Capital Structure

|

|

• Deep, forensic People analysis • References including customers, CEOs + investors • Leverage broad sector relationships across GSV’s proprietary ecosystem

Returns Analysis:

• DCF • Comparables • IRR • Exit scenarios • Follow-on financings • Deal Structure |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 39 |

| | 6.5.2016 |

Investment Selection Process

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 40 |

| | 6.5.2016 |

APPENDIX A

GSV Capital Top 10 Positions — Company Profiles

Position size and fair value as of March 31, 2016

| Palantir | Page 42 |

| Dropbox | Page 43 |

| Spotify | Page 44 |

| Coursera | Page 45 |

| Solexel | Page 46 |

| PayNearMe | Page 47 |

| Lyft | Page 48 |

| Page 49 | |

| Declara | Page 50 |

| Curious | Page 51 |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 41 |

| | 6.5.2016 |

| Company Snapshot |

|

||

| GSVC Position (Fair Value): | Founded: |

| $46.1 million (14.2% of portfolio) | 2004 |

NOTE: Palantir prohibits the communication of company information.

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 42 |

| | 6.5.2016 |

| Company Snapshot |

|

||

| GSVC Position (Fair Value): | Founded: | Capital Raised: | ||

| $19.2 million (5.9% of Portfolio) | 2007 | $1.1 billion | ||

| Other Investors: | Megatrends: | Milestones: | ||

| Sequoia, Accel, Benchmark, Index Ventures, IVP, Greylock, Goldman Sachs, Salesforce Ventures, T. Rowe Price, BlackRock | Freemium, Cloud Computing, Internet, Globalization, Convergence | 500+ million users uploading 1.2 billion files per day; 150,000 business customers |

| Overview: | Competitors: | |

| Dropbox is the leader in cloud-based digital file storage and device-agnostic sharing/syncing. Its service enables users to access and edit files from any device at any time. Frustrated by working from multiple computers, founder Drew Houston was inspired to create a service that would let people access their files anywhere, with no need for email attachments or sharing via physical media. | Box, Google, Microso$, Apple |

GSVC THESIS

As services and products continue their relentless “march to the cloud,” Dropbox is strongly positioned to both capture and accelerate this move, from individual consumers to entire enterprises. Dropbox is disrupting the file storage space by providing a best-in-class solution for users to easily share, edit, store, and access files from any device at any time. The company’s freemium model has proven to be a powerful driver of user growth, ultimately creating a massive barrier to entry for competitors.

GSVC 4Ps Analysis  |

| People | Product | Potential | Predictability | |||

| Dropbox was founded in 2007 by CEO Drew Houston and Arash Ferdowsi. Prior to Dropbox, Houston founded Accolade, an online SAT prep course while he was a student at MIT. | Dropbox’s cloud-based platform enables people to securely save, share and sync files across multiple devices and users. Additionally, Dropbox for Business provides teams with enterprise collaboration and security features. | Dropbox has established itself as the leader in the Storage-as-a-Service market, a subset of the Cloud Computing market. According to Forrester Research, the global cloud computing market is expected to reach $241 billion in 2020 compared to $41 billion in 2010. | Dropbox is building a formidable economic moat around its core business using a freemium model. Users quickly reach their data storage limit, triggering the option to pay for additional capacity. Given the proliferation of personal and enterprise content/data, Dropbox should continue to see rapid revenue growth. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 43 |

| | 6.5.2016 |

| Company Snapshot |

| GSVC Position (Fair Value): | Founded: | Capital Raised: | ||

| $16.2 million (5.0% of portfolio) | 2006 | $1.6 billion | ||

| Other Investors: | Megatrends: | Milestones: | ||

| KPCB, Accel, Founders Fund, Fidelity, Goldman Sachs, DST Global, TCV | Mobile, Internet, Globalization, Convergence, Consolidation | 100 million active users and 30 million subscribers; 50% younger than 27. |

| Overview: | Competitors: | |

| Spotify is an online music provider that offers digital streaming of selected songs from a wide range of artists and music genres, including both major and independent labels. Spotify is currently available both in the United States and over 50 other countries around the globe. Spotify uniquely allows users to precisely choose the artists, songs, and genres they wish to appear on their playlist, in direct contrast with Pandora that uses an algorithm to select similar music. | Alphabet (YouTube), Apple, Pandora, SoundCloud, Tidal, Deezer, Saavn |

GSVC THESIS

Consumer preferences have shifted from owning music to “renting” it, allowing listeners to access their favorite songs seamlessly from their tablet, smartphone, and computer. We believe this trend will only continue to expand in the future as the world undergoes this shift.

| GSVC 4Ps Analysis |

| People | Product | Potential | Predictability | |||

| Daniel Ek, Founder and CEO, has been a lifelong entrepreneur, founding his first company at age 14. Previously he was CTO at Jajja Communications, CTO at Stardoll, and CEO of uTorrent, the world’s most popular BitTorrent client. Since its emergence as a leading music platform, Spotify has been able to recruit a highly experienced executive team and practiced engineers. | While the online music space is packed with competition, Spotify provides a differentiated product. By creating a mobile-centric application, users are able to instantly access and listen to specific tracks without a buffering delay. Users can register for free, advertising-supported accounts, or paid subscriptions without ads that include extra features. | Spotify has gained an enormous market share in the digital music space and already has more than 100 million monthly active users. We see tremendous potential growth both in the U.S. and abroad as access to mobile technology continues to improve. | Spotify has a rapidly expanding user base and is continually building upon its current universe of tracks to accommodate the changing preferences of consumers. We believe that in the foreseeable future, Spotify will remain the market leader because of its current contracts and expansive library. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 44 |

| | 6.5.2016 |

| Company Snapshot |

| GSVC Position (Fair Value): | Founded: | Capital Raised: | ||

| $14.4 million (4.4% of portfolio) | 2012 | $146 million | ||

| Other Investors: | Megatrends: | Milestones: | ||

| KPCB, NEA, International Finance Corporation (IFC), Laureate Education, Learn Capital, Times of India | Knowledge Economy, Freemium, Mobile, Internet, Network Effects, Brands, Globalization | 18+ million learners, 1,800+ courses, 140 university partners; most instructors teach more students in one Coursera course than in an entire teaching career on campus. |

| Overview: | Competitors: | |

| Coursera is an education platform that partners with top universities and organizations worldwide, offering free and paid (when electing to earn a credit) courses for anyone to take. | edX, Udacity, NovoED |

GSVC THESIS

Coursera is capitalizing on the convergence of increasing global education demand with new technology fundamentals that enable people to learn anytime, anywhere. The twin forces of globalization and automation are making career obsolescence a new reality. You can no longer fill up your knowledge tank until age 25 and drive off through life. Effective workers will be refilling their “knowledge tank” continuously. In this new paradigm, education technology platforms like Coursera will be like air — invisible, ubiquitous, and life-sustaining. Living will be learning.

| GSVC 4Ps Analysis |

| People | Product | Potential | Predictability | |||

| Coursera’s CEO, Rick Levin, is the former president of Yale University. Co- Founders Andrew Ng and Daphne Koller are Stanford Computer Science professors. Ng also serves as Chief Scientist of Baidu, China’s leading search engine. | Coursera partners with universities to provide best-in-class online courses in a freemium model, charging for certification of program completion. Courses include short, modular videos, embedded quizzes and auto-graded assignments, peer-to-peer collaboration, and capstone projects. Coursera has also launched a first of its kind, fully accredited, online MBA program at a fraction of the cost. | Coursera has the potential to democratize global access to high quality education. It has the potential to become the leading platform for online learning, with a massive user base and a significant share of the higher- education and lifelong- learning market. | Coursera’s model is driven by the convergence of increasing global education demand with technology- enabled access to high- value, online learning resources produced by the world’s leading academic institutions. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 45 |

| | 6.5.2016 |

| Company Snapshot |

| GSVC Position (Fair Value): | Founded: | Capital Raised: | ||

| $14.0 million (4.3% of portfolio) | 2005 | $248 million | ||

| Other Investors: | Megatrends: | Milestones: | ||

| KPCB, Technology Partners, SunPower, DAG Ventures, GAF | Sustainability, Convergence, Demographics, Globalization | Researched, developed and produced industry-leading high-performance, low-cost, thin, light-weight solar cells; achieved a NREL-certified cell efficiency of 21.2% in 2014. |

| Overview: | Competitors: | |

| Solexel is developing high-efficiency, low-cost, crystalline silicon solar cells and modules for photovoltaic electricity generation. Solexel’s innovative manufacturing process and product design minimize the use of expensive materials while providing industry- leading performance. | SunPower, First Solar |

GSVC THESIS

Solexel has the potential to become the leading photovoltaic solar manufacturer in the “Solar 2.0” era, producing the best price to performance energy generation products in the world. Low material usage allows Solexel to manufacture solar modules at substantially reduced costs, putting solar-based electricity on a near-term path to the Solar Holy Grail: true grid parity.

| GSVC 4Ps Analysis |

| People | Product | Potential | Predictability | |||

| President and CEO Mike Wingert was a successful executive in the semiconductor industry as the EVP of Seagate, President and COO of Maxtor, and CEO of Cornice. Founder, Executive Chairman, and CTO Mehrdad Moslehi has an extensive science and engineering background and holds over 220 issued patents. | Solexel is developing and producing crystalline silicon-based PV modules that achieve the highest efficiency at the lowest cost in the industry. The company plans to ship 20% efficient modules in 2015. Solexel employs a disruptive, IP-protected, high-efficiency technology that uses approximately ten times less silicon than traditional processes. | From a promising technology in the 1970s to an emerging industry less than a decade ago, the solar energy market has grown to approximately $100 billion in 2015. Solexel is eliminating the key structural roadblocks to broad solar adoption by enabling an industry- leading levelized cost of electricity through lowest cost and highest efficiency. | Solexel has proven its core technology and is prepared to produce at scale in 2015. The company has a manufacturing process that is protected by patents and proprietary tools. Solexel has also demonstrated strong customer demand – the largest top-tier strategic customers have already indicated purchase interest with Solexel. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 46 |

| | 6.5.2016 |

| Company Snapshot |

| GSVC Position (Fair Value): | Founded: | Capital Raised: | ||

| $14.0 million (4.3% of portfolio) | 2009 | $71 million | ||

| Other Investors: | Megatrends: | Milestones: | ||

| Khosla Ventures, True Ventures, Maveron, August Capital | Network Effects, Globalization, Mobile | Established integrated network of 17,000 retailers and 1,000+ merchants; processed 1.6+ million transactions since inception. |

| Overview: | Competitors: | |

| PayNearMe is a next-generation, electronic cash payment platform. It serves what the Federal Deposit Insurance Corporation (FDIC) estimates to be 93 million “unbanked” and “underbanked” residents of the United States, allowing them to pay auto, rent, and utilities bills through retail locations. The company currently has relationships with 7-Eleven, Family Dollar, and ACE Cash Express stores. PayNearMe is continuing to aggressively expand its retail footprint, as well as the breadth of industries that its payment system covers. | Western Union, Blackhawk |

GSVC THESIS

PayNearMe services the millions of underbanked and unbanked Americans who are virtually locked out of the digital economy. Using PayNearMe’s sophisticated technology platform and network, cash consumers are able to pay their rent, utility bills and loans, buy tickets online and more.

| GSVC 4Ps Analysis |

| People | Product | Potential | Predictability | |||

| PayNearMe is led by CEO Danny Shader, the former CEO of Jasper Wireless and the former President and CEO of Good Technology, which was acquired by Motorola in 2007. Shader was also a Vice President and General Manager at Amazon, where he gained exposure to the extensive challenges facing the underbanked in commerce. | PayNearMe enables consumers to use cash to make payments in less than a minute at any of the 17,000 participating 7- Eleven, Family Dollar, and ACE Cash Express stores throughout the United States. | PayNearMe estimates that there are over $1 trillion in U.S. cash transactions per year. PayNearMe is focused on capitalizing on the velocity of money by the underbanked and unbanked, allowing them to pay in cash for bills or other purchases that would normally require a credit card or bank account information. | PayNearMe has created a product that is both user-friendly to a broad range of socioeconomic groups and highly defensible from a technology perspective. The company will continue to scale as it grows its portfolio of retailer relationships. |

| Statements included herein may constitute “forward-looking statements” which relate to future events or our future performance or financial condition. Please see the section entitled “Forward-Looking Statements” on page 52 of this letter. | 47 |

| | 6.5.2016 |

| Company Snapshot |

| GSVC Position (Fair Value): | Founded: | Capital Raised: | ||

| $13.7 million (4.2% of Portfolio) | 2012 | $2.0 billion | ||

| Other Investors: | Megatrends: | Milestones: | ||

| A16Z, Founders Fund, Floodgate, Alibaba, Tencent, Coatue, Didi Kuaidi, GM, Rakuten, Ichan Enterprises, Kingdom Holding | Mobile, Sharing Economy, Network Effects, Globalization | Ride volume grew 300% from 2014 to 2015 with 11 million rides delivered in April 2016 (Forbes); $1 billion 2015 financing led by GM. |

| Overview: | Competitors: | |

| Lytf is an on-demand ride-sharing platform for friendly and affordable rides. Drivers are matched with passengers who request rides through the Lyft iPhone or Android app. The transaction is automated through the app and drivers can earn income on something they already own — their car. | Uber, Didi Chuxing, Go-Jek, Ola, BlaBlaCar, Grab, Gett |

GSVC THESIS