Attached files

| file | filename |

|---|---|

| EX-23.3 - EX-23.3 - VALVOLINE INC | d176840dex233.htm |

| EX-23.2 - EX-23.2 - VALVOLINE INC | d176840dex232.htm |

| EX-23.1 - EX-23.1 - VALVOLINE INC | d176840dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on May 31, 2016

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Valvoline Inc.

(Exact name of registrant as specified in its Charter)

| Kentucky | 2992 | 30-0939371 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

3499 Blazer Parkway

Lexington, KY 40509

(859) 357-7777

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive office)

Samuel J. Mitchell, Jr.

Chief Executive Officer

Valvoline Inc.

3499 Blazer Parkway

Lexington, KY 40509

(859) 357-7777

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

| Peter J. Ganz Senior Vice President, General Counsel and Secretary Ashland Inc. 50 E. RiverCenter Boulevard P.O. Box 391 Covington, KY 41012-0391 (859) 815-3333 |

Susan Webster Thomas E. Dunn Andrew J. Pitts Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, NY 10019 (212) 474-1000 |

Jonathan M. DeSantis Ilir Mujalovic Shearman & Sterling LLP 599 Lexington Avenue New York, NY 10022 (212) 848-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one)

| Large Accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Offering Price(1)(2) |

Amount of Registration Fee | ||

| Common stock, par value $0.01 per share |

$100,000,000 | $10,070 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457 under the Securities Act of 1933. |

| (2) | Includes the aggregate offering price of shares of common stock that the underwriters have the option to purchase. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated May 31, 2016

PROSPECTUS

Shares

Valvoline Inc.

Common Stock

This is Valvoline Inc.’s initial public offering. We are selling shares of our common stock.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. After pricing of the offering, we expect that the shares will trade on the New York Stock Exchange under the symbol “VVV.”

Investing in the common stock involves risks that are described in the “Risk Factors” section beginning on page 19 of this prospectus.

| Per Share | Total | |||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discount and commissions(1) |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| (1) | See “Underwriting” section beginning on page 167 of this prospectus for additional information regarding total underwriter compensation. |

The underwriters may also exercise their option to purchase up to an additional shares from us, at the public offering price, less the underwriting discount, to cover over allotments for 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2016.

Joint Book-Running Managers

| BofA Merrill Lynch | Citigroup | Morgan Stanley |

The date of this prospectus is , 2016.

Table of Contents

| Page | ||||

| ii | ||||

| ii | ||||

| ii | ||||

| 1 | ||||

| 19 | ||||

| 40 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 46 | ||||

| 49 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

57 | |||

| 89 | ||||

| 108 | ||||

| 112 | ||||

| 148 | ||||

| 153 | ||||

| 154 | ||||

| 155 | ||||

| 162 | ||||

| Material U.S. Federal Income Tax Consequences for Non-U.S. Holders of Our Common Stock |

164 | |||

| 167 | ||||

| 175 | ||||

| 175 | ||||

| 175 | ||||

| F-1 | ||||

We have not and the underwriters have not authorized anyone to provide you with any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or the time of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Through and including , 2016 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

i

Table of Contents

FOR INVESTORS OUTSIDE THE UNITED STATES

Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

We use various trademarks, trade names and service marks in our business, including ValvolineTM, Valvoline Instant Oil ChangeSM, MaxLifeTM, SynPowerTM and Premium BlueTM. For convenience, we may not include the SM, ® or ™ symbols, but such omission is not meant to indicate that we would not protect our intellectual property rights to the fullest extent allowed by law. Any other trademarks, trade names or service marks referred to in this prospectus are the property of their respective owners.

This prospectus includes industry data and forecasts that we obtained from industry publications and surveys, public filings and internal company sources. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of the included information. Statements as to our ranking, market position and market estimates are based on independent industry publications, third-party forecasts, management’s estimates and assumptions about our markets and our internal research. We have not independently verified such third-party information nor have we ascertained the underlying economic assumptions relied upon in those sources, and we cannot assure you of the accuracy or completeness of such information contained in this prospectus. Such data involve risks and uncertainties and is subject to change based on various factors, including those discussed under “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.”

ii

Table of Contents

This summary highlights certain information about us and this offering contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, especially the “Risk Factors” section and our financial statements and the related notes included elsewhere in this prospectus, before making an investment decision.

As used in this prospectus, the terms “Valvoline,” the “Company,” “we,” “us” and “our” may, depending on the context, refer to Valvoline Inc., to the Valvoline business segment of Ashland Inc. as described more particularly under “Certain Relationships and Related Party Transactions—Relationship with Ashland—Historical Relationship with Ashland” or to Valvoline Inc. and its consolidated subsidiaries after giving effect to the contribution and separation transactions described under “Certain Relationships and Related Party Transactions—Relationship with Ashland—Separation Steps.”

We describe in this prospectus the businesses that will be contributed to us by Ashland as part of our separation from Ashland as if they were our businesses for all historical periods described. Our historical financial results as part of Ashland contained in this prospectus may not reflect our financial results in the future as a standalone company or what our financial results would have been had we been a standalone company during the periods presented.

Immediately prior to the closing of this offering, Ashland Inc. and we will become subsidiaries of Ashland Global Holdings Inc., or “Ashland Global,” a newly formed public holding company. Accordingly, as used in this prospectus, references to “Ashland” in the context of any time prior to the date of this offering refer to Ashland Inc., and references to “Ashland” in the context of any time on or after the date of this offering refer to Ashland Global. At the time of the contribution (as described below), Ashland and certain of its consolidated subsidiaries (other than us) will hold substantially all of the historical assets and liabilities related to the business that Valvoline Inc. and its consolidated subsidiaries will acquire pursuant to the contribution.

Our fiscal year ends on September 30 of each year. We refer to the year ended September 30, 2015 as “fiscal 2015,” the year ended September 30, 2014 as “fiscal 2014” and the year ended September 30, 2013 as “fiscal 2013.”

Our Company

We are one of the most recognized and respected premium consumer brands in the global automotive lubricant industry, known for our high quality products and superior levels of service. Established in 1866, our heritage spans 150 years, during which we have developed powerful name recognition across multiple product and service channels. We have significant positions in the United States in all of the key lubricant sales channels, and also have a strong international presence with our products sold in approximately 140 countries.

In the United States and Canada, our products are sold to consumers through over 30,000 retail outlets, to installer customers with over 12,000 locations, and to approximately 1,050 Valvoline branded franchised and company-owned stores. We serve our customer base through an extensive sales force and technical support organization, allowing us to leverage our technology portfolio and customer relationships globally, while meeting customer demands locally. This combination of scale and strong local presence is critical to our success.

1

Table of Contents

We have a history of leading innovation with revolutionary products such as All Climate™, DuraBlend™, and MaxLife™. In addition to our iconic Valvoline-branded passenger car motor oils and other automotive lubricant products, we provide a wide array of lubricants used in heavy duty equipment, as well as automotive chemicals and fluids designed to improve engine performance and lifespan. Our premium branded product offerings enhance our high quality reputation and provide our customers with solutions that address a wide variety of needs.

We deliver products and services to our customers across three business segments:

| • | Core North America: We sell to consumers in the United States and Canada who perform their own automotive maintenance, referred to as “Do-It-Yourself” or “DIY” consumers, through retail outlets, including AutoZone, O’Reilly Auto Parts and Advance Auto Parts. We also sell to installer customers such as car dealers, general repair shops and third-party quick lube locations, including Goodyear, Monro, Express Oil Change, TBC Retail Group and Sears, directly and through distributors. Installers use our products to service vehicles owned by “Do-It-For-Me” or “DIFM” consumers. Our installer channel team also sells branded products and solutions to heavy duty customers, such as on-highway fleets and construction companies, and we have a strategic relationship with Cummins Inc. (“Cummins”), a leading heavy duty engine manufacturer, for co-branding products in the heavy duty business. |

| • | Quick Lubes: We operate the second-largest United States retail quick lube service chain by number of stores, Valvoline Instant Oil Change (“VIOC”), which provides fast, trusted service through approximately 720 franchised and 330 company-owned stores. Our VIOC company-owned stores have had nine years of consecutive same-store sales growth,* and consistently outperformed our competitors, delivering on average over 36% more daily oil changes during 2015 than competing quick lube service centers. Our franchisees have also enjoyed strong results, performing on average 22% more daily oil changes in 2015 than competitors. We also sell our products and provide Valvoline branded signage to independent quick lube operators through our Express Care program. In 2015, we estimate that VIOC and Express Care stores performed approximately 13% of the total oil changes in the quick lube market. |

| • | International: Our products are sold in approximately 140 countries outside of the United States and Canada, where, like in Core North America, Valvoline is positioned as a high performance, high quality brand. International sales include both passenger car products and heavy duty products used in a wide variety of heavy duty equipment. We sell our passenger car products to installer customers primarily through distributors, and our heavy duty products directly to customers, as well as through distributors. |

| * | We have historically determined same-store sales growth on a fiscal year basis, with new stores excluded from the metric until the completion of their first full fiscal year in operation. |

2

Table of Contents

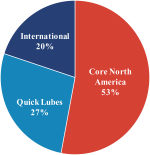

Sales and Adjusted EBITDA contribution of each of our segments is as follows:

| Fiscal 2015 Sales Contribution |

Fiscal 2015 Adj. EBITDA Contribution | |

|

FY15 Sales: $2.0 Billion |

FY15 Adjusted EBITDA: $422 Million |

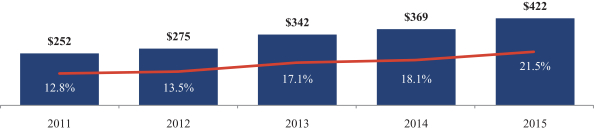

In fiscal 2015, we generated approximately $2.0 billion in sales, $422 million in Adjusted EBITDA and $196 million in net income. During the same period, our Adjusted EBITDA margin, which we define as Adjusted EBITDA as a percentage of sales, was 21.5%. In addition, we generated free cash flow of $285 million and cash flows provided by operating activities of $330 million during fiscal 2015. See “—Summary Historical and Pro Forma Combined Financial Data” for the definition of Adjusted EBITDA and free cash flow, each a non-GAAP measure, and a reconciliation of such measures to net income and cash flows provided by operating activities, as applicable.

Our Value Proposition and Business Model

Founded in 1866, the Valvoline brand stands for high quality and performance, allowing us to command premium pricing for our products. The strength of our business model is our ability to generate profitable sales across multiple channels to market, leveraging the Valvoline brand through effective marketing, innovative product technology and the capabilities of our team. We have delivered strong profits and return on capital, with balanced results across all of our sales channels. Today, Valvoline is a high margin, high free cash flow generating business, with significant growth opportunities across all of our business segments.

Our successful business model is further strengthened by our commitment to partnering with customers and channel partners to drive value-creating solutions. We drive growth by providing cutting edge innovations, high-quality products and dedicated customer service. Our “Hands on Expertise” customer service model, which pairs our deep automotive knowledge with a commitment to developing unparalleled customer solutions, is designed to help us outperform our competitors.

A Rich History of Innovation

We have a 150 year history of industry-leading innovation. The company’s history dates back to 1866, when Dr. John Ellis discovered the lubricating properties of crude oil. Valvoline was trademarked six years later, making it the first trademarked motor oil in U.S. history. By 1895 we began to cement our place in American racing culture, when a Valvoline lubricated race car won the first known automotive race in North American history. In the early 1900s, the Valvoline brand gained national prominence as one of the recommended motor oils for the iconic Ford Model T.

3

Table of Contents

During the 20th century, we furthered our tradition of innovation, pioneering one of the world’s first aircraft engine motor oils, developing All-Climate Motor Oil, which eliminated the need for seasonal oil changes, and introducing Valvoline Racing Motor Oil, which became, and is to this day, one of the best-selling racing motor oils of all time. In 1987, we expanded into the quick lube market with the acquisition of an 81 store chain. Two years later we franchised our first five VIOC stores. In 1998, we began a partnership with Cummins, a leading global designer, manufacturer and distributor of engines, filtration and power generation products, that includes the sale of Cummins-endorsed Valvoline lubricants such as Premium Blue™ heavy duty engine oil. We have been selling products outside the United States for over 90 years, and now sell products in approximately 140 countries.

We continued to be a leader in the lubricants industry in product innovation with the introduction of DuraBlend™ in 1996, our first synthetic motor oil blend, and MaxLife™ in 2000, the first motor oil specifically engineered for cars with over 75,000 miles. We continue to invest significant resources in our research and development programs and in developing relationships with original equipment manufacturers (“OEMs”) with a goal of creating new and innovative products to meet the current and future needs of our customers. It is this spirit of performance and innovation that has made us into a global business today and that we believe will continue to drive our growth in the future.

Our Market

We participate in the global finished lubricants market, which had demand of over 11.7 billion gallons, or $60 billion, in 2015. For the same period, demand for passenger car motor oil and motorcycle oil accounted for slightly over 24% of global lubricant demand, while the remaining 76% of demand was for commercial and industrial products. The United States has historically accounted for the largest amount of lubricant demand, followed by China and India. The lubricants market is impacted by the following key drivers and trends:

| • | Shift in Demand for High Performance Products: Global lubricants market demand is shifting towards higher performance finished lubricants, largely driven by advancements in vehicle/equipment design and OEM requirements for improved efficiency, reduced carbon footprints and optimized fuel consumption. This shift in customer demand requires high-end formulations from lubricant manufacturers and leads to ongoing investment in top tier base stocks (Group II/II+ and Group III/III+ base oils) to support synthetics growth in developed markets, like the United States. Establishing strong product lines of synthetic and bio-based lubricants have become key competitive aspects to attract OEMs focused on equipment efficiency and environmental sustainability. In many non-U.S. markets, older engine technologies remain more prevalent. We believe there will be an opportunity for increased sales of our high performance products as these engines are replaced by newer technology engines. |

| • | Environmental Health and Safety Regulations: There has been increasingly stringent regulation, particularly in North America and Europe, aimed at reducing toxic emissions, which has led to a continuous drive for innovation given changing specifications for lubricants. Recent regulatory trends include: European Commission Regulations; the Registration, Evaluation, Authorization, and Restriction of Chemicals (“REACH”) regulation; Euro Regulations; the Clean Air Act; and more stringent vehicle emission requirements. |

4

Table of Contents

Our Competitive Strengths

We believe the following strengths differentiate us from our competitors and are important to our success:

Iconic Brand with Premium Products

| Valvoline is a highly recognized and respected premium consumer brand. According to our research, we have a total awareness rate of 90% with consumers in the United States, and in many countries around the globe the Valvoline trademark is a symbol of high quality, which helps us to command premium prices. We are known for our high quality products, market leading technology and superior levels of service.

The consistent application of the Valvoline brand across all channels provides us with a significant marketing advantage. We use a variety of marketing techniques to build awareness of our |

|

brand, including social and digital media, search, direct marketing, radio and television. In addition, we selectively sponsor teams in high performance racing series, including a current sponsorship of Hendrick Motorsports, featuring drivers Dale Earnhardt Jr., Chase Elliott, Jimmie Johnson and Kasey Kahne. We believe our iconic brand and strong customer awareness support our ability to grow our retail base in existing and new markets.

Unique Multi-Channel Presence

We operate through multiple automotive maintenance outlets and are committed to delivering an outstanding customer experience against a diverse set of customer expectations, leveraging our strong channel partner and quick lube network. Whether the customer is a consumer driving in for a differentiated VIOC quick lube experience, an installer looking to improve the performance of its business, a heavy duty customer looking to effectively service on-road and off-road vehicles or a DIY consumer looking for high quality products to service their vehicles, we leverage our “Hands on Expertise” to provide a solution to their unique and individual needs.

Within our DIY and DIFM sales channels, we have been successful in driving premium lubricants growth through effective consumer marketing and strong retailer relationships, resulting in Valvoline holding a #3 position by volume in the United States DIY market in 2015. Within our Quick Lubes business, our “Hands on Expertise” approach is a differentiating factor and has led to nine consecutive years of VIOC company-owned same-store sales growth and resulted in VIOC being the #2 quick lube chain by store count in 2015. Internationally, we sell our products in approximately 140 countries and our relationships with leading OEMs have provided us with the opportunity to leverage the Valvoline brand to increase global growth and awareness in key markets. In particular, we have a strong partnership with Cummins, a leading global designer, manufacturer and distributor of engines, filtration and power generation products, that includes joint ventures in India and China and global marketing and product co-branding arrangements.

Industry-Leading, Valvoline-Branded Quick Lube Business

With over 330 company-owned VIOC stores and another 720 franchised locations, we are the largest franchisor of quick lube stores that owns and operates its own oil change centers. VIOC is committed to providing our customers with a quick, easy and trusted oil change experience. We believe that our ability to deliver an outstanding customer experience is based on the quality of our teams and their focus on execution and customer satisfaction. Our proprietary point-of-sale system allows us to leverage data, understand our customers’

5

Table of Contents

needs and customize service recommendations for each of our customers. SuperPro, our proprietary service process that sets forth rigorous protocols for both the steps that must be followed in the service of vehicles and for interactions with customers, is designed to deliver a consistently outstanding customer experience.

Operating our own stores allows us to continually improve all aspects of our business model, from store operations to marketing tactics, which enhances the profitability of our company-owned and franchised operations. In addition, our company-owned VIOC locations provide us with first-hand knowledge of the customer experience. We use this knowledge to improve the speed and quality of our services, resulting in performance improvements at our own stores, as well as the stores of our franchisees. Our focus on the total customer experience has resulted in consistently high customer satisfaction rates. We have had nine consecutive years of same-store sales growth, due in part to improved customer service experience and an increase in the number of oil changes per day. In addition, the visibility of approximately 1,050 VIOC and 340 Express Care stores across the United States further strengthens our brand in the markets in which our quick lube stores operate. As seen below, our company-owned VIOC stores have outperformed the competition in oil changes per day since 2009. Our franchisees have also enjoyed strong performance by executing the same business model.

Oil Changes Per Day, Per Store

Note: Represents fiscal years.

Source: National Oil and Lube News.

We believe our vertical integration through our Quick Lubes business is an additional competitive advantage. By selling our own, high-quality motor oil and family of products to our owned stores, our franchisees and other quick lube channel partners, we generate value for the overall enterprise, as well as an additional profit pool.

Strong History of Innovation

We believe that innovation is central to the successful performance of our business. As a result, we invest significant resources in our research and development programs and in developing relationships with OEMs, with a goal of developing new and innovative products to meet the current and future needs of our customers. We have an established track record of pioneering new product categories, such as synthetic blends, high mileage motor oil and racing motor oil. The introduction of MaxLifeTM and Full Synthetic High Mileage has driven significant trade-up to our higher performing synthetic and other premium products, contributing to both retailer and installer profitability.

Innovations in our sales and marketing efforts have been a cornerstone of our success. We place a high priority on sales and marketing, with a focus on the following areas, which we believe yield the highest benefits:

| • | targeted innovative digital marketing, which has allowed us to more efficiently reach our consumers with relevant messaging; |

6

Table of Contents

| • | consumer relationship marketing and social media platforms, which provide forums for ongoing dialogue with consumers to increase brand commitment; and |

| • | selective investment in national advertising and sponsorships, including our current sponsorship of Hendrick Motorsports, featuring drivers Dale Earnhardt Jr., Chase Elliott, Jimmie Johnson and Kasey Kahne, which builds on our brand’s strong equity with racing fans. |

Independent, Focused Organization

Under the leadership of our Chief Executive Officer, Samuel J. Mitchell, Jr., our management team has extensive experience in the consumer products and lubricants industry in the areas of commercial operations, sales, marketing and research and development. Our leadership team has instituted a strong, unified corporate culture focused on speed and “Hands On” customer service. Our efficient global network of businesses and technical, supply chain and product support groups allow us to bring solutions to the market quickly. Our entire business, unlike our largest competitors, is focused on lubricants and automotive maintenance, enabling us to stay customer focused.

Our separation from Ashland will provide us the flexibility to invest in Valvoline’s growth initiatives and to act quickly in making decisions for the benefit of the business, our channel partners, customers and shareholders. We will enhance our strategic focus by aligning corporate support functions, such as information technology, human resources and finance, to the distinct needs of our business, providing greater control over both strategy and execution. As a standalone public company, we will be able to more effectively pursue our distinct operating priorities and strategies and our management will be able to solely focus on our opportunities for long-term growth and profitability.

Strong Financial Performance and Free Cash Flow Generation

Our high margin business is able to generate significant free cash flow. Our premium mix improvements, VIOC same-store sales growth, international volume and profit growth and proactive approach to changes in the base oil market resulted in fiscal 2015 Adjusted EBITDA of $422 million and Adjusted EBITDA margin of 21.5%. Strong earnings combined with efficient working capital management have led to high free cash flow, which grew from $133 million in fiscal 2014 to $285 million in fiscal 2015. This strong free cash flow provides us with significant financial flexibility.

Our Business and Growth Strategy

| “We are building the world’s

leading engine and automotive maintenance business

|

We intend to achieve sustainable growth and profitability by executing the following strategies:

7

Table of Contents

Grow and Strengthen Quick Lube Network

We are committed to growing the footprint of our profitable quick lube network. We expect this growth to be driven by both organic store expansion and opportunistic, high-quality acquisitions in both core and new markets within the VIOC system, as well as strong sales efforts to partner with new Express Care operators. In addition, we plan to continue delivering same-store sales growth within our existing stores.

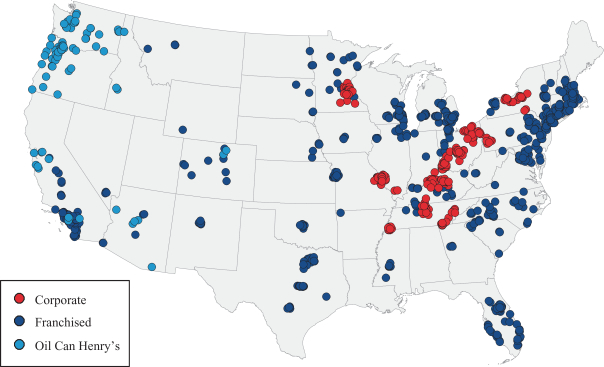

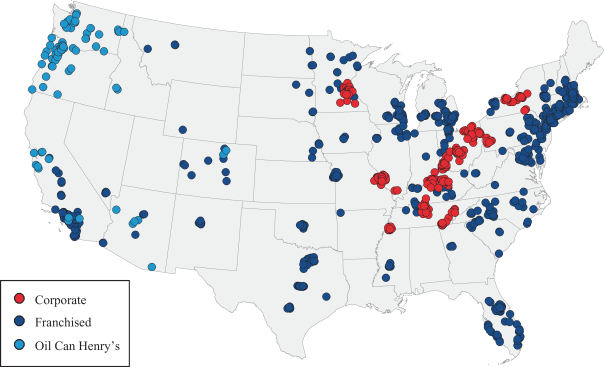

VIOC Geographic Footprint as of March 31, 2016

| • | Organic Store Expansion: We currently operate 330 company-owned and have an additional 720 franchised quick lube centers across 44 states. Given the strength of our brand and new unit economics, we believe we can continue growing our network in both new and existing company and franchise markets. Independently owned Express Care locations display Valvoline branding in exchange for a contractual obligation to purchase Valvoline motor oil and other products. We believe that continued expansion of our Express Care program will continue to provide wider exposure to our brand by penetrating channels, primarily smaller (typically single store) operators, which do not fit our franchised model and typically offer other non-quick lube services such as auto repair and car washes. |

| • | Opportunistic Acquisitions: There are over 9,000 known quick lube stores in the United States, the ownership of which, excluding the few largest networks of service centers, is largely fragmented. We believe that the large and fragmented nature of the North American quick lube market creates an opportunity for us to grow. Our distribution relationships in the DIFM installer space can be leveraged along with VIOC’s proprietary modeling tools to execute an acquisition strategy for both the larger, known systems, as well as smaller operators. VIOC’s acquisition of Oil Can Henry’s in February 2016 added 89 stores to our Quick Lube portfolio in the Pacific Northwest, Colorado, Arizona and southern California. We expect to continue to opportunistically look at acquisitions as a way of supplementing our organic store growth. |

8

Table of Contents

| • | Continue to Drive Additional Growth and Profitability from Existing Stores: We have generated nine consecutive years of VIOC same-store sales growth. We plan to continue delivering growth through the following strategies: |

| ¡ | Attract New Customers and Increase Customer Satisfaction and Loyalty: We strive to attract new customers through our targeted digital marketing efforts, which allows us to be more efficient and effective in reaching our prospective new customers. Our existing VIOC customers value our proposition as a quick, easy and trusted operator. Our proprietary point-of-sale system allows us to better understand our customers’ needs and develop performance drivers that enhance the productivity of our company-owned and franchised operations. Following the introduction of our enhanced SuperPro 10 in 2006, we have been able to deliver quicker and more consistent service times, and have seen improvements in both our overall customer satisfaction scores and retention. Our “Hands on Expertise” culture and approach has been essential in unifying our 10,000 member team across our approximately 1,050 VIOC company-owned and franchised stores towards delivering a preferred customer experience. |

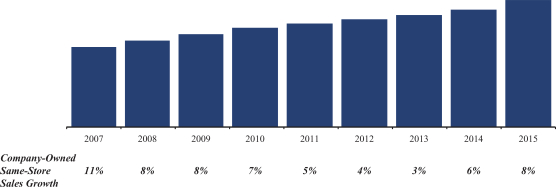

| ¡ | Increase Average Ticket Size: Between 2007 and 2015, average net ticket at our company-owned VIOC stores increased from $53.22 to $69.07. Given our focus on customer experience, our proprietary point-of-sale system, and our ability to pilot new concepts in our stores, we believe we can continue to strengthen average net ticket through improvements within our selling of premium oils, penetration of extra services, discount efficiency and pricing opportunities. |

Company-Owned Store Sales, 2007 – 2015

Accelerate International Growth across Key Markets

Our International business currently accounts for approximately 26% of combined sales. We plan to accelerate our growth internationally by focusing on key markets where demand for premium lubricants is growing. Our primary targets include China, India and select countries in Latin America. Our strategies for growth vary by market, but generally revolve around building strong distribution channels in underserved geographies, replacing less successful distributors and improving brand awareness among installer customers in those regions.

The sales, marketing and distribution capabilities that we have developed in the United States, combined with the strength of our brand, will assist our international expansion. We believe that large integrated oil brands are more focused on their upstream business in many of our targeted international markets, while local competitors often are not competitive in premium product categories. Operational expertise will allow us to benefit from these market dynamics at the same time that stricter regulations of emissions and fuel economy are increasing demand for more advanced lubricants.

9

Table of Contents

We also plan to expand our presence in the heavy duty lubricant space, which is an important channel in our targeted international markets, by developing products that will lower the total cost of ownership for fleet operators and users of other heavy duty equipment, leveraging our existing relationships with leading OEMs and building and strengthening other OEM relationships. These long-term relationships provide credibility to our International business, and we believe they will allow us to leverage the Valvoline brand to increase growth in key markets globally.

Leverage Innovation to Drive Market Share and Profitability in Core North America

Innovations in product development, packaging and marketing have driven improvements in our product mix, with United States premium-branded lubricant sales volume increasing to approximately 40% of total sales volume in 2015, up from approximately 31% in 2011.

We believe that our focus on innovation will continue to drive premium lubricant mix improvement in addition to increasing sales of our broader product portfolio, such as Valvoline Professional Series service chemicals, coolants, filters and other non-lubricant products. We plan to continue to grow higher margin synthetic sales, consistent with increased customer demand for these products due to OEM requirements.

We intend to leverage our expertise to continue to add significantly more value to our installer customers than our more cost-driven competitors. We do this by sharing our knowledge in sales, marketing and supply chain management to help them grow their businesses through improvements in customer acquisition, retention and sales volume. We believe that our differentiated service approach will allow us to continue to charge premium prices while growing our overall business.

We are also investing in e-commerce solutions with our existing business partners and a new digital infrastructure that will be used across our enterprise. We believe that this digital infrastructure will improve the speed, innovation and efficiency of our business, and also drive more effective customer engagement, acquisition and retention. Being able to interact with our customers when they need information will provide accurate real time access to training, marketing programs, product recommendations and order status and will differentiate us from our competition by building a more efficient customer-facing organization.

Ashland Ownership and Our Separation from Ashland

Prior to the completion of this offering, we will be a wholly owned subsidiary of Ashland. Immediately prior to the completion of this offering, we plan to amend and restate our articles of incorporation and by-laws and increase the total number of authorized shares of our common stock. In this prospectus, we refer to these transactions collectively as the “recapitalization.” After the completion of this offering, Ashland will own % of our outstanding common stock (or % if the underwriters exercise their overallotment option in full).

In connection with this offering, we and Ashland intend to enter into agreements and take certain actions to transfer to us substantially all of the assets and liabilities related to our business. Except for the nominal assets that we currently hold, Ashland holds all of the historical assets and liabilities related our business. We and Ashland will enter into a separation agreement that provides for the separation of our business from Ashland to take effect no later than the closing of this offering (the “Separation Agreement”). We also intend to enter into a tax matters agreement with Ashland that will govern the respective rights, responsibilities and obligations of Ashland and us after the closing of this offering with respect to all tax matters (including tax liabilities, tax attributes, tax returns and tax contests) (the “Tax Matters Agreement”). In addition, we and Ashland will enter into transition services agreements governing Ashland’s provision of various services to us, and our provision of various services to Ashland, on a transitional basis, and several other ancillary agreements in connection with the contribution and separation. In this prospectus, references to the “contribution” refer to Ashland’s transfer to us

10

Table of Contents

(in connection with certain reorganization transactions) of the assets and liabilities related to our business, and the term “separation” refers to the separation of our business from Ashland’s other businesses (including the contribution), along with the effectiveness of various agreements between us and Ashland. See “Certain Relationships and Related Party Transactions.”

Prior to the closing of this offering, we expect to incur new senior term loans (which may be secured or unsecured), new senior unsecured notes or a combination thereof in an aggregate principal amount of approximately $ million. We expect to transfer the proceeds of this indebtedness to Ashland through intercompany transfers. We also plan to obtain an accounts receivable securitization facility with up to $ million of available funding from qualified receivables. We refer to the transactions related to this incurrence of debt collectively as the “related financing transactions.” In addition to this indebtedness, in the event that the net proceeds of this offering are expected to exceed $ million, we may incur certain short-term indebtedness immediately prior to the closing of this offering and transfer the net proceeds thereof to a subsidiary of Ashland Global. See “Description of Indebtedness.” We plan to repay such short-term indebtedness in full from the net proceeds of this offering. We also intend to use the net proceeds of this offering to repay $ million of our indebtedness, with an interest rate of %. Any remaining proceeds will be used for general corporate purposes. See “Use of Proceeds.”

Ashland has informed us that, at some time in the future, but no earlier than the expiration of the 180-day lock-up period described under “Underwriting,” it intends to effect a tax-free spin-off of its remaining ownership interest in us to its shareholders (the “spin-off”). Ashland has no obligation to effect the spin-off and it may retain its ownership interest in us indefinitely or dispose of all or a portion of its ownership interest in us in a sale or other transaction. Any such spin-off or other disposition by Ashland of its remaining interest in us (an “other disposition”) would be subject to various conditions, including receipt of an opinion of tax counsel in connection with the spin-off, receipt of any necessary regulatory or other approvals and the existence of satisfactory market conditions. The conditions to a spin-off or other disposition by Ashland may not be satisfied. Ashland has no obligation to pursue or consummate any further disposition of its ownership interest in us by any specified date or at all, whether or not these conditions are satisfied.

We believe, and Ashland has advised us that it believes, that the separation, this offering and the spin-off will provide a number of benefits to our business, to Ashland’s business and to Ashland’s shareholders. These potential benefits include improving the strategic and operational flexibility of both companies, increasing the focus of the management teams on their respective business operations, and allowing each company to adopt the capital structure, investment policy and dividend policy best suited to its financial profile and business needs. In addition, as we will be a standalone company, potential investors will be able to invest directly in our business.

Risks Affecting Our Business

Investing in our common stock involves a high degree of risk. You should carefully consider the risks described in “Risk Factors” before making a decision to invest in our common stock. If any of these risks actually occurs, our business, financial condition and results of operations would likely be negatively affected. In such case, the trading price of our common stock would likely decline, and you may lose part or all of your investment. These risks include, but are not limited to:

| • | damage to our reputation or brand; |

| • | failure to meet the growth goals for our business; |

| • | reduced demand for our products or services as a result of market or other factors; |

| • | downward pressure on prices and margins due to competition; |

11

Table of Contents

| • | the loss of any of our largest customers; |

| • | failure to develop and successfully market new products and implement our digital platforms; |

| • | our substantial indebtedness and other liabilities; |

| • | failure to achieve the expected benefits and successfully execute the separation; |

| • | potential tax liabilities that may be created as a result of the spin-off or the separation; |

| • | operating as an independent publicly traded company, including compliance with applicable laws and regulations; and |

| • | our status as a controlled company and the possibility that Ashland’s interests may conflict with yours. |

Company Information

We were incorporated in Kentucky on May 13, 2016 in connection with our planned separation from Ashland. Our principal executive offices are at 3499 Blazer Parkway, Lexington, Kentucky 40509 and our telephone number is (859) 357-7777. Our website is http://www.valvoline.com. The information and other content contained on our website are not part of this prospectus.

12

Table of Contents

The Offering

| Issuer |

Valvoline Inc. |

| Common stock offered by us in this offering |

shares ( shares if the underwriters exercise their overallotment option in full) |

| Common stock to be held by Ashland immediately after this offering |

shares |

| Common stock to be outstanding immediately after this offering |

shares ( shares if the underwriters exercise their overallotment option in full) |

| Underwriters’ option |

We have granted the underwriters an option for a period of 30 days after the date of this prospectus to purchase up to additional shares of common stock solely to cover over allotments. |

| Use of proceeds |

We estimate that the net proceeds from this offering, after deducting the underwriting discount and estimated offering expenses payable by us, will be approximately $ million (or approximately $ million if the underwriters’ overallotment option is exercised in full), assuming that the shares of our common stock to be sold in this offering are sold at $ per share, the midpoint of the price range set forth on the cover page of this prospectus. |

| We intend to use the net proceeds of this offering to repay $ million of indebtedness, with an interest rate of %. As described in “Description of Indebtedness,” we may incur certain short-term indebtedness in the amount of $ million, with an interest rate of %, immediately prior to the closing of this offering. If we incur this short-term indebtedness, we plan to repay such short-term indebtedness in full with the net proceeds of this offering. Any remaining proceeds will be used for general corporate purposes. See “Use of Proceeds.” |

| Dividend policy |

We expect to pay quarterly cash dividends to holders of our common stock. The declaration and payment of dividends to holders of our common stock will be at the discretion of our board of directors in accordance with applicable law after taking into account various factors, including our financial condition, operating results, current and anticipated cash needs, cash flows, impact on our effective tax rate, indebtedness, legal requirements and other factors that our board of directors deems relevant. In addition, the instruments governing our indebtedness may limit our ability to pay dividends. |

| Risk factors |

You should read the “Risk Factors” section of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Proposed NYSE symbol |

We intend to apply for listing of our common stock on the NYSE under the symbol “VVV.” |

13

Table of Contents

Unless indicated otherwise, the number of shares of common stock to be outstanding after this offering is based on shares of common stock outstanding as of , 2016 and excludes:

Unless otherwise indicated, the information presented in this prospectus:

| • | gives effect to the transactions described under “Certain Relationships and Related Party Transactions—Relationship with Ashland—Separation Steps;” |

| • | assumes that the shares of our common stock to be sold in this offering are sold at $ per share, the midpoint of the price range set forth on the cover page of this prospectus; and |

| • | assumes the underwriters will not exercise their overallotment option. |

14

Table of Contents

Summary Historical and Pro Forma Combined Financial Data

The following financial data should be read in conjunction with our audited and unaudited combined financial statements and the related notes, and our unaudited pro forma condensed combined financial statements and the related notes, included elsewhere in this prospectus.

The following table summarizes our historical and pro forma combined financial data. The summary historical combined balance sheet data as of September 30, 2015 and 2014 and statement of operations data for the years ended September 30, 2015, 2014, and 2013 is derived from our audited combined financial statements included elsewhere in this prospectus. The summary historical combined financial data as of and for the six months ended March 31, 2016 and 2015 is derived from our unaudited interim combined financial statements included elsewhere in this prospectus. The historical combined balance sheet data as of September 30, 2013 is derived from our unaudited annual combined financial statements, which are not included in this prospectus. In the opinion of management, the unaudited combined financial statements include all normal and recurring adjustments that we consider necessary for a fair presentation of the financial position and the operating results for these periods. The operating results for the six months ended March 31, 2016 are not necessarily indicative of the results that may be expected for the year ended September 30, 2016 or any other interim periods or any future year or period.

The summary historical combined financial data includes certain expenses of Ashland that were allocated to us for certain corporate functions including, treasury, legal, accounting, insurance, information technology, payroll administration, human resources, stock incentive plans and other services. Management believes the assumptions underlying the combined financial statements, including the assumptions regarding allocated expenses, reasonably reflect the utilization of services provided to or the benefit received by us during the periods presented. However, these shared expenses may not represent the amounts that we would have incurred had we operated autonomously or independently from Ashland. Actual costs that would have been incurred if we had been a standalone company would depend on multiple factors, including organizational structure and strategic decisions in various areas, such as information technology and infrastructure. In addition, our summary historical combined financial data does not reflect changes that we expect to experience in the future as a result of our separation from Ashland, including changes in our cost structure, personnel needs, tax structure, capital structure, financing and business operations.

The summary pro forma combined financial data reflects the impact of certain transactions, which comprise the following:

| • | the recapitalization, the contribution and the separation; |

| • | the receipt of approximately $ in net proceeds from the sale of shares of our common stock in this offering at an assumed initial offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting the underwriting discount and commissions and estimated offering expenses payable by us, and the use of approximately $ of these proceeds to repay indebtedness; |

| • | the indebtedness to be incurred in the related financing transactions; and |

| • | other adjustments described in the notes to the unaudited pro forma condensed combined financial statements. |

The unaudited pro forma condensed combined balance sheet reflects the separation as if it occurred on March 31, 2016, while the unaudited pro forma condensed combined statements of operations give effect to the separation as if it occurred on October 1, 2014, the beginning of the earliest period presented. The pro forma adjustments, described in “Unaudited Pro Forma Condensed Combined Financial Statements,” are based on currently available information and certain assumptions that management believes are reasonable. Excluded from the pro forma adjustments are items that are non-recurring in nature or are not material.

The unaudited pro forma condensed combined financial statements are provided for illustrative purposes only and are not necessarily indicative of the operating results or financial position that would have occurred had

15

Table of Contents

the separation from Ashland been completed on March 31, 2016 for the unaudited pro forma condensed combined balance sheet or on October 1, 2014 for the unaudited pro forma condensed combined statements of operations. The unaudited pro forma condensed combined financial statements should not be relied on as indicative of the historical operating results that we would have achieved or any future operating results or financial position that we will achieve after the completion of this offering.

The following summary combined financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the “Unaudited Pro Forma Condensed Combined Financial Statements” and accompanying notes and the interim and annual combined financial statements and accompanying notes included elsewhere in this prospectus.

| Pro forma | Historical | |||||||||||||||||||||||||||

| (Dollars in millions) | Six months ended March 31, |

Year ended September 30, |

Six months ended March 31, |

Year ended September 30, |

||||||||||||||||||||||||

| 2016 | 2015 | 2016 | 2015 | 2015 | 2014 | 2013 | ||||||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||||||

| Sales |

$ | $ | $ | 935.7 | $ | 973.4 | $ | 1,966.9 | $ | 2,041.3 | $ | 1,996.2 | ||||||||||||||||

| Cost of sales |

567.9 | 634.9 | 1,281.8 | 1,408.9 | 1,338.3 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Gross profit |

367.8 | 338.5 | 685.1 | 632.4 | 657.9 | |||||||||||||||||||||||

| Selling, general and administrative |

137.4 | 128.4 | 290.8 | 302.8 | 213.4 | |||||||||||||||||||||||

| Corporate expense allocation |

41.1 | 39.2 | 79.5 | 95.0 | 88.2 | |||||||||||||||||||||||

| Equity and other income (loss) |

10.7 | (2.0 | ) | 8.3 | 30.1 | 24.3 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Operating income |

200.0 | 168.9 | 323.1 | 264.7 | 380.6 | |||||||||||||||||||||||

| Net loss on acquisition and divestiture |

(0.5 | ) | (26.0 | ) | (26.3 | ) | — | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income before income taxes |

199.5 | 142.9 | 296.8 | 264.7 | 380.6 | |||||||||||||||||||||||

| Income tax expense |

66.5 | 52.4 | 100.7 | 91.3 | 134.5 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income |

$ | $ | $ | 133.0 | $ | 90.5 | $ | 196.1 | $ | 173.4 | $ | 246.1 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Pro forma | Historical | |||||||||||||||||||||||

| As of March 31, |

As of March 31, |

As of September 30, |

||||||||||||||||||||||

| 2016 | 2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||||||

| Cash and cash equivalents(1) |

$ | $ — | $ — | $ — | $ — | $ — | ||||||||||||||||||

| Current assets |

514.4 | 502.0 | 477.3 | 544.7 | 519.1 | |||||||||||||||||||

| Property, plant and equipment, net |

266.5 | 248.0 | 253.5 | 272.4 | 270.2 | |||||||||||||||||||

| Total assets |

1,117.4 | 999.3 | 977.9 | 1,082.5 | 1,062.0 | |||||||||||||||||||

| Current liabilities |

300.6 | 266.1 | 298.6 | 293.5 | 312.6 | |||||||||||||||||||

| Long-term debt (less current portion) |

— | — | — | — | — | |||||||||||||||||||

| Total liabilities |

377.8 | 327.3 | 360.8 | 357.7 | 378.3 | |||||||||||||||||||

16

Table of Contents

| Six months ended March 31, |

Year ended September 30, |

|||||||||||||||||||

| 2016 | 2015 | 2015 | 2014 | 2013 | ||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||

| Cash Flow Data: |

||||||||||||||||||||

| Cash flow provided by operations |

$ | 91.1 | $ | 160.6 | $ | 329.8 | $ | 170.6 | $ | 272.9 | ||||||||||

| Capital expenditures |

14.4 | 17.7 | 45.0 | 37.2 | 40.9 | |||||||||||||||

| Six months ended March 31, |

Year ended September 30, |

|||||||||||||||||||

| Unaudited | 2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| Free cash flow (2) |

$ | 76.7 | $ | 142.9 | $ | 284.8 | $ | 133.4 | $ | 232.0 | ||||||||||

| EBITDA (3) |

218.5 | 161.7 | 334.8 | 301.8 | 416.3 | |||||||||||||||

| Adjusted EBITDA (3) |

223.2 | 204.4 | 421.8 | 369.2 | 342.3 | |||||||||||||||

| (1) | Historically, cash and cash equivalents were held at the Ashland level utilizing Ashland’s centralized approach to cash management. |

| (2) | We use free cash flow as an additional non-GAAP metric of cash flow generation. By deducting capital expenditures and certain other adjustments as applicable from operating cash flows, we are able to provide a better indication of the ongoing cash being generated that is ultimately available for both debt and equity holders as well as other investment opportunities. Free cash flow does not reflect adjustments for certain non-discretionary cash flows. Our results of operations are presented based on our management structure and internal accounting practices. The structure and practices are specific to us; therefore, our financial results and free cash flow are not necessarily comparable with similar information for other comparable companies. Free cash flow has limitations as an analytical tool and should not be considered in isolation from, or as an alternative to, or more meaningful than, cash flows provided by operating activities as determined in accordance with U.S. GAAP. In evaluating free cash flow, you should be aware that in the future we may incur expenses similar to those for which adjustments are made in calculating free cash. Our presentation of free cash flow should not be construed as a basis to infer that our future results will be unaffected by unusual or non-recurring items. Because of these limitations, you should rely primarily on cash flows provided by operating activities as determined in accordance with U.S. GAAP and use free cash flow only as a supplement. |

The following table reconciles free cash flow to cash flows provided by operating activities for the periods presented.

| Six months ended March 31, |

Year ended September 30, |

|||||||||||||||||||

| (Dollars in millions) | 2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||||||

| Cash flows provided by operating activities |

$ | 91.1 | $ | 160.6 | $ | 329.8 | $ | 170.6 | $ | 272.9 | ||||||||||

| Less: |

||||||||||||||||||||

| Additions to property, plant and equipment |

(14.4 | ) | (17.7 | ) | (45.0 | ) | (37.2 | ) | (40.9 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Free cash flow |

$ | 76.7 | $ | 142.9 | $ | 284.8 | $ | 133.4 | $ | 232.0 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (3) | In addition to our net income determined in accordance with U.S. GAAP, we evaluate operating performance using certain non-GAAP measures including EBITDA, which we define as our net income, plus income tax expense (benefit), net interest and other financing expenses, and depreciation and amortization, and Adjusted EBITDA, which we define as EBITDA adjusted for losses (gains) on pension and other postretirement plans remeasurement, net gain (loss) on acquisitions and divestitures, impairment of equity investment, restructuring, other income and (expense) and other items. Management believes the use of non-GAAP measures on a combined and reportable segment basis assists investors in understanding the ongoing operating performance of our business by presenting comparable financial results between periods. The non-GAAP information provided is used by our management and may not be comparable to similar measures disclosed by other companies, because of differing methods used by other companies in calculating EBITDA and Adjusted EBITDA. EBITDA and Adjusted EBITDA provide a supplemental presentation of our operating performance on a combined and reportable segment basis. Adjusted EBITDA generally includes adjustments for unusual, non-operational or restructuring-related activities. |

The combined financial statements include actuarial gains and losses for defined benefit pension and other postretirement benefit plans recognized annually in the fourth quarter of each fiscal year and whenever a plan is determined to qualify for a remeasurement during a fiscal year. Actuarial gains and losses occur when actual experience differs from the estimates used to allocate the change in value of pension and other postretirement benefit plans to expense throughout the year or when assumptions change, as they may each year.

17

Table of Contents

Significant factors that can contribute to the recognition of actuarial gains and losses include changes in discount rates used to remeasure pension and other postretirement obligations on an annual basis or upon a qualifying remeasurement, differences between actual and expected returns on plan assets and other changes in actuarial assumptions, for example the life expectancy of plan participants. Management believes Adjusted EBITDA, which includes the expected return on pension plan assets and excludes both the actual return on pension plan assets and the impact of actuarial gains and losses, provides investors with a meaningful supplemental presentation of our operating performance. Management believes these actuarial gains and losses are primarily financing activities that are more reflective of changes in current conditions in global financial markets (and in particular interest rates) that are not directly related to the underlying business and that do not have an immediate, corresponding impact on the compensation and benefits provided to eligible employees and retirees.

EBITDA and Adjusted EBITDA each have limitations as an analytical tool and should not be considered in isolation from, or as an alternative to, or more meaningful than, net income as determined in accordance with U.S. GAAP. Because of these limitations, you should rely primarily on net income as determined in accordance with U.S. GAAP and use EBITDA and Adjusted EBITDA only as supplements. In evaluating EBITDA and Adjusted EBITDA, you should be aware that in the future we may incur expenses similar to those for which adjustments are made in calculating EBITDA and Adjusted EBITDA. Our presentation of EBITDA and Adjusted EBITDA should not be construed as a basis to infer that our future results will be unaffected by unusual or non-recurring items.

The following table reconciles EBITDA and Adjusted EBITDA to net income for the periods presented.

| Six months ended March 31, |

Year ended September 30, |

|||||||||||||||||||

| (Dollars in millions) | 2016 | 2015 | 2015 | 2014 | 2013 | |||||||||||||||

| Net income |

$ | 133.0 | $ | 90.5 | $ | 196.1 | $ | 173.4 | $ | 246.1 | ||||||||||

| Income tax expense |

66.5 | 52.4 | 100.7 | 91.3 | 134.5 | |||||||||||||||

| Depreciation and amortization |

19.0 | 18.8 | 38.0 | 37.1 | 35.7 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

218.5 | 161.7 | 334.8 | 301.8 | 416.3 | |||||||||||||||

| Losses (gains) on pension and other postretirement plans remeasurement |

4.7 | 2.0 | 46.0 | 61.1 | (74.0 | ) | ||||||||||||||

| Net loss on divestiture |

— | 26.0 | 26.3 | — | — | |||||||||||||||

| Impairment of equity investment |

— | 14.3 | 14.3 | — | — | |||||||||||||||

| Restructuring |

— | 0.4 | 0.4 | 6.3 | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 223.2 | $ | 204.4 | $ | 421.8 | $ | 369.2 | $ | 342.3 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

18

Table of Contents

Investing in our common stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including our financial statements and the related notes included elsewhere in this prospectus, before deciding whether to invest in shares of our common stock. We describe below what we believe are currently the material risks and uncertainties we face, but they are not the only risks and uncertainties we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. If any of the following risks actually occur, our business, financial condition, results of operations and future prospects could be materially and adversely affected. In that event, the market price of our common stock could decline and you could lose part or all of your investment.

Risks Related to Our Business

Damage to our brand and reputation could have an adverse effect on our business.

Maintaining our strong reputation with both consumers and customers is a key component of our business. Product or service complaints or recalls, our inability to ship, sell or transport affected products, and governmental investigations may harm our reputation with consumers and customers, which may materially and adversely affect our business operations, decrease sales and increase costs.

We manufacture and market a variety of products, such as automotive and industrial lubricants and antifreeze, and provide automotive maintenance services. If allegations are made that some of our products have failed to perform up to consumers’ or customers’ expectations or have caused damage or injury to individuals or property, or that our services were not provided in a manner consistent with our vision and values, the public may develop a negative perception of our brands. In addition, if our franchisees or Express Care operators do not successfully operate their quick lube service centers in a manner consistent with our standards, our brand, image and reputation could be harmed, which in turn could negatively impact our business and operating results. A negative public perception of our brands, whether justified or not, could impair our reputation, involve us in litigation, damage our brand equity and have a material adverse effect on our business. In addition, damage to the reputation of our competitors or others in our industry could negatively impact our reputation and business.

We have set aggressive growth goals for our business, including increasing sales, cash flow, market share and margins, in order to achieve our long-term strategic objectives. Execution of our growth strategies and business plans to facilitate that growth involves a number of risks.

We have set aggressive growth goals for our business in order to meet our long-term strategic objectives and improve shareholder value. Our failure to meet one or more of these goals or objectives would negatively impact our business and is one of the most important risks that we face. Aspects of that risk include, among others, changes to the economic environment, changes to the competitive landscape, including those related to automotive maintenance recommendations and consumer preferences, attraction and retention of skilled employees, the potential failure of product innovation plans, failure to comply with existing or new regulatory schemes, failure to maintain a competitive cost structure and other risks outlined in greater detail in this “Risk Factors” section.

Demand for our products and services could be adversely affected by consumer spending trends, declining economic conditions, trends in our industry and a number of other factors, all of which are beyond our control.

Demand for our products and services may be affected by a number of factors we cannot control, including the number and age of vehicles in current service, regulation and legislation, technological advances in the automotive industry and changes in engine technology, including the adoption rate of electric or other alternative engine technologies. In addition, during periods of declining economic conditions, consumers may defer vehicle

19

Table of Contents

maintenance. Similarly, increases in energy prices may cause miles driven to decline, resulting in less wear and tear and lower demand for maintenance, which may lead to consumers deferring purchases of our products and services. All of these factors, which impact metrics such as drain intervals and oil changes per day, could result in a decline in the demand for our products and services and adversely affect our sales, cash flows and overall financial condition. Between 2007 and 2012, U.S. passenger car motor oil volumes declined. This decline in demand is a result of, among other factors, changing automotive OEM specifications and longer recommended intervals between oil changes. Over the past two years, however, market volume has increased, largely due to the increase in the number of cars on the road and miles driven.

The success of our growth initiatives depends on our ability to successfully develop and implement one or more integrated digital platforms that will help us better understand consumers and more effectively engage them.

We are in the process of designing and implementing a number of digital platforms that will integrate our operations with customer and consumer data. The successful development and implementation of these digital platforms will depend on our ability to identify an appropriate strategy, dedicate adequate resources and select technologies that will provide us with adequate flexibility to adapt to future developments in the marketplace and changes in consumer and customer behavior. We have incurred and expect to incur significant upfront investments to develop these digital platforms. There is a risk that once implemented, these digital platforms will not deliver all or part of the expected benefits, including additional sales. As we develop and implement our digital platforms, we may elect to modify, replace or abandon certain technology initiatives, which could result in write-downs.

Our success depends upon our ability to attract and retain key employees and the identification and development of talent to succeed senior management.

Our success depends on our ability to attract and retain key personnel, and we rely heavily on our senior management team. The inability to recruit and retain key personnel or the unexpected loss of key personnel may adversely affect our operations. This risk of unwanted employee turnover is substantial in positions that require certain technical expertise. This risk is also substantial in developing international markets we have targeted for growth and in North America, where attracting marketing and technical expertise to geographies necessary to support our management is important to our success. This risk is further enhanced by the planned separation from Ashland. In addition, because of our reliance on our senior management team, our future success depends, in part, on our ability to identify and develop or recruit talent to succeed our senior management and other key positions throughout the organization. If we fail to identify and develop or recruit successors, we are at risk of being harmed by the departures of these key employees.

We face significant competition from other companies, which places downward pressure on prices and margins and may adversely affect our business and results of operations.

We operate in highly competitive markets, competing against a number of domestic and foreign companies. Competition is based on several key criteria, including brand recognition, product performance and quality, product price, product availability and security of supply, ability to develop products in cooperation with customers, and customer service, as well as the ability to bring innovative products or services to the marketplace. Certain key competitors, including Shell/Pennzoil and Jiffy Lube, BP/Castrol and Exxon/Mobil, are significantly larger than us and have greater financial resources and more diverse portfolios of products and services, leading to greater operating and financial flexibility. As a result, these competitors may be better able to withstand adverse changes in conditions within the relevant industry, the prices of raw materials and energy or general economic conditions. In addition, competitors’ pricing decisions could compel us to decrease our prices, which could negatively affect our margins and profitability. Additional competition in markets served by us could adversely affect margins and profitability and could lead to a reduction in market share. Also, we compete in certain markets that are declining, such as the U.S. passenger car motor oil market. If our strategies for dealing with declining markets and leveraging market opportunities are not successful, our results of operations could be negatively affected.

20

Table of Contents

Because of the concentration of our sales to a small number of retailers, the loss of one or more of, or a significant reduction in orders from, our top retail customers could adversely affect our financial results, as could the loss of one of our distributor relationships.