Attached files

| file | filename |

|---|---|

| EX-10.2 - EXHIBIT 10.2 - China United Insurance Service, Inc. | v439124_ex10-2.htm |

| EX-32.1 - EXHIBIT 32.1 - China United Insurance Service, Inc. | v439124_ex32-1.htm |

| EX-10.1 - EXHIBIT 10.1 - China United Insurance Service, Inc. | v439124_ex10-1.htm |

| EX-31.2 - EXHIBIT 31.2 - China United Insurance Service, Inc. | v439124_ex31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - China United Insurance Service, Inc. | v439124_ex31-1.htm |

| EX-32.2 - EXHIBIT 32.2 - China United Insurance Service, Inc. | v439124_ex32-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2016

OR

| ¨ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE EXCHANGE ACT |

For the transition period from __________ to __________

COMMISSION FILE NUMBER: 000-54884

CHINA UNITED INSURANCE SERVICE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 30-0826400 |

|

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

7F, No. 311 Section 3

Nan-King East Road

Taipei City, Taiwan

(Address of principal executive offices)

+8862-87126958

(Registrant’s Telephone Number, Including Area Code)

N/A

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

| Large Accelerated Filer ¨ | Non-Accelerated Filer ¨ |

| Accelerated Filer x | Smaller Reporting Company ¨ |

Indicate by check mark whether the registrant is a shell company as defined in Rule 12b-2 of the Exchange Act.

Yes ¨ No x

As of April 30, 2016, there are 29,452,669 shares of common stock issued and outstanding, and 1,000,000 preferred shares issued and outstanding.

TABLE OF CONTENTS

| PART I. | FINANCIAL INFORMATION | F-1 |

| ITEM 1. | CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) | F-1 |

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 5 |

| ITEM 3. | QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK | 14 |

| ITEM 4. | CONTROLS AND PROCEDURES | 14 |

| PART II. | OTHER INFORMATION | 15 |

| ITEM 1. | LEGAL PROCEEDINGS | 15 |

| ITEM 1A. | RISK FACTORS | 15 |

| ITEM 2. | UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS | 15 |

| ITEM 3. | DEFAULTS UPON SENIOR SECURITIES | 15 |

| ITEM 4. | MINE SAFETY DISCLOSURES | 15 |

| ITEM 5. | OTHER INFORMATION | 15 |

| ITEM 6. | EXHIBITS | 16 |

| SIGNATURES | 17 |

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This report contains forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievement expressed or implied by the forward-looking statements. These risks and uncertainties include, but are not limited to, the factors described under Part 1 Item 2 “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Forward-looking statements represent our estimates and assumptions only as of the date of this report. You should read this report and the documents that we reference in this report, or that we filed as exhibits to this report completely and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

3

OTHER PERTINENT INFORMATION

References in this report to “we,” “us,” “our” and the “Company” and words of like import refer to China United Insurance Service, Inc., its subsidiaries and variable interest entities.

References to China or the PRC refer to the People’s Republic of China (excluding Hong Kong, Macao and Taiwan). References to Taiwan refer to Taiwan, Republic of China.

Our business is conducted in Taiwan and China using NT$, the currency of Taiwan and RMB, the currency of China, respectively, and our financial statements are presented in United States dollars (“USD” or “$”). In this report, we refer to assets, obligations, commitments and liabilities in our financial statements in USD. These dollar references are based on the exchange rate of NT$ and RMB to USD, determined as of a specific date. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of USD which may result in an increase or decrease in the amount of our obligations (expressed in USD) and the value of our assets, including accounts receivable (expressed in USD).

4

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| March 31, 2016 | December 31, 2015 | |||||||

| (UNAUDITED) | ||||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and equivalents | $ | 20,433,158 | $ | 20,831,824 | ||||

| Marketable securities | 2,417,995 | 2,369,082 | ||||||

| Accounts receivable, net | 4,158,754 | 9,630,993 | ||||||

| Other current assets | 673,053 | 1,055,015 | ||||||

| Total current assets | 27,682,960 | 33,886,914 | ||||||

| Property, plant and equipment, net | 958,418 | 918,798 | ||||||

| Intangible assets | 718,517 | 468,779 | ||||||

| Goodwill | 2,071,491 | 2,071,491 | ||||||

| Long-term Investment | 1,289,848 | 1,264,611 | ||||||

| Other assets | 770,437 | 791,223 | ||||||

| TOTAL ASSETS | $ | 33,491,671 | $ | 39,401,816 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities | ||||||||

| Taxes payable | $ | 1,533,115 | $ | 1,521,962 | ||||

| Other current liabilities | 5,819,644 | 10,867,607 | ||||||

| Short-term loan | 178,691 | 222,235 | ||||||

| Deferred tax liability | - | 3,143 | ||||||

| Due to related parties | 350,041 | 945,932 | ||||||

| TOTAL CURRENT LIABILITIES | 7,881,491 | 13,560,879 | ||||||

| Long-term liabilities | 6,726,129 | 6,594,530 | ||||||

| TOTAL LIABILITIES | 14,607,620 | 20,155,409 | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Preferred stock, par value $0.00001, 10,000,000 authorized, 1,000,000 issued and outstanding | 10 | 10 | ||||||

| Common stock, par value $0.00001, 100,000,000 authorized, 29,452,669 issued and outstanding | 295 | 295 | ||||||

| Additional paid-in capital | 8,157,512 | 8,157,512 | ||||||

| Statutory Reserves | 2,385,529 | 2,385,327 | ||||||

| Accumulated other comprehensive gain/(loss) | (518,214 | ) | (680,133 | ) | ||||

| Retained earnings | 1,164,770 | 1,808,665 | ||||||

| Stockholders’ equity attribute to parent’s shareholders | 11,189,902 | 11,671,676 | ||||||

| Noncontrolling interest | 7,694,149 | 7,574,731 | ||||||

| TOTAL STOCKHOLDERS’ EQUITY | 18,884,051 | 19,246,407 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 33,491,671 | $ | 39,401,816 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

F-1

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND OTHER COMPREHENSIVE INCOME / (LOSS)

(UNAUDITED)

| Three Months Ended March 31, | ||||||||

| 2016 | 2015 | |||||||

| Revenues | $ | 9,562,296 | $ | 9,856,115 | ||||

| Cost of revenue | 6,468,859 | 6,446,411 | ||||||

| Gross profit | 3,093,437 | 3,409,704 | ||||||

| Operating expenses: | ||||||||

| Selling | 898,265 | 369,259 | ||||||

| General and administrative | 2,887,108 | 3,053,644 | ||||||

| Total operating expense | 3,785,373 | 3,422,903 | ||||||

| Loss from operations | (691,936 | ) | (13,199 | ) | ||||

| Other income (expenses): | ||||||||

| Interest income | 50,569 | 37,715 | ||||||

| Other - net | (29,350 | ) | 13,015 | |||||

| Total other income | 21,219 | 50,730 | ||||||

| Income (loss) before income taxes | (670,717 | ) | 37,531 | |||||

| Income tax expense | 3,199 | 129,629 | ||||||

| Net loss | (673,916 | ) | (92,098 | ) | ||||

| Net income (loss) attributable to the noncontrolling interests | (30,215 | ) | 188,568 | |||||

| Net loss attributable to parent's shareholders | (643,701 | ) | (280,666 | ) | ||||

| Other comprehensive items | ||||||||

| Foreign currency translation gain (loss) | 163,512 | 94,676 | ||||||

| Other | (1,593 | ) | - | |||||

| Other comprehensive income attributable to parent's shareholders | 161,919 | 94,676 | ||||||

| Other comprehensive items attributable to noncontrolling interest | 149,633 | 108,730 | ||||||

| Comprehensive income (loss) attributable to | ||||||||

| parent's shareholders | $ | (481,782 | ) | $ | (185,990 | ) | ||

| Comprehensive income (loss) attributable to | ||||||||

| noncontrolling interest | $ | 119,418 | $ | 297,298 | ||||

| Weighted average shares outstanding: | ||||||||

| Basic | 29,452,669 | 29,452,669 | ||||||

| Diluted | 29,452,669 | 29,452,669 | ||||||

| Income (loss) per share: | ||||||||

| Basic | $ | (0.022 | ) | $ | (0.010 | ) | ||

| Diluted | $ | (0.022 | ) | $ | (0.010 | ) | ||

The accompanying notes are an integral part of these consolidated financial statements.

F-2

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Three Months Ended March 31, | ||||||||

| 2016 | 2015 | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | (673,916 | ) | $ | (92,098 | ) | ||

| Adjustments to reconcile net income to net cash | ||||||||

| Depreciation and amortization | 155,099 | 106,287 | ||||||

| Gain on valuation of financial assets | (1,594 | ) | (4,463 | ) | ||||

| Loss (Gain) on disposal of fixed assets | 37,938 | 1,525 | ||||||

| Deferred income tax | (3,122 | ) | (18,901 | ) | ||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | 5,509,467 | 4,035,097 | ||||||

| Other current assets | 388,380 | (512,678 | ) | |||||

| Other assets | 32,045 | (115,544 | ) | |||||

| Tax payable | (17,523 | ) | 5,267 | |||||

| Other current liabilities | (5,096,789 | ) | (4,267,422 | ) | ||||

| Net cash provided by (used in) operating activities | 329,985 | (862,930 | ) | |||||

| Cash flows from investing activities: | ||||||||

| Cash from acquisition | - | 319 | ||||||

| Purchase of property, plant and equipment | (217,985 | ) | (69,927 | ) | ||||

| Purchase of intangible assets | (233,400 | ) | (140,537 | ) | ||||

| Net cash used in investing activities | (451,385 | ) | (210,145 | ) | ||||

| Cash flows from financing activities: | ||||||||

| Proceeds from related party borrowing | 11,254 | 26,561 | ||||||

| Repayment to related parties | (604,906 | ) | (312,625 | ) | ||||

| Repayment to loans | (45,368 | ) | - | |||||

| Net cash used in financing activities | (639,020 | ) | (286,064 | ) | ||||

| Foreign currency translation | 361,754 | 283,129 | ||||||

| Net increase in cash and cash equivalents | (398,666 | ) | (1,076,010 | ) | ||||

| Cash and cash equivalents, beginning balance | 20,831,824 | 19,571,799 | ||||||

| Cash and cash equivalents, ending balance | $ | 20,433,158 | $ | 18,495,789 | ||||

| SUPPLEMENTARY DISCLOSURE: | ||||||||

| Interest paid | $ | 447 | $ | 2,291 | ||||

| Income tax paid | $ | 9,037 | $ | 9,882 | ||||

| SUPPLEMENTAL DISCLOSURES OF CASH FLOW FOR NON-CASH TRANSACTION: | ||||||||

| Issuance of common stock for acquisition of GHFL | $ | - | $ | 3,482,923 | ||||

The accompanying notes are an integral part of these financial statements.

F-3

CHINA UNITED INSURANCE SERVICE, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

NOTE 1 – ORGANIZATION

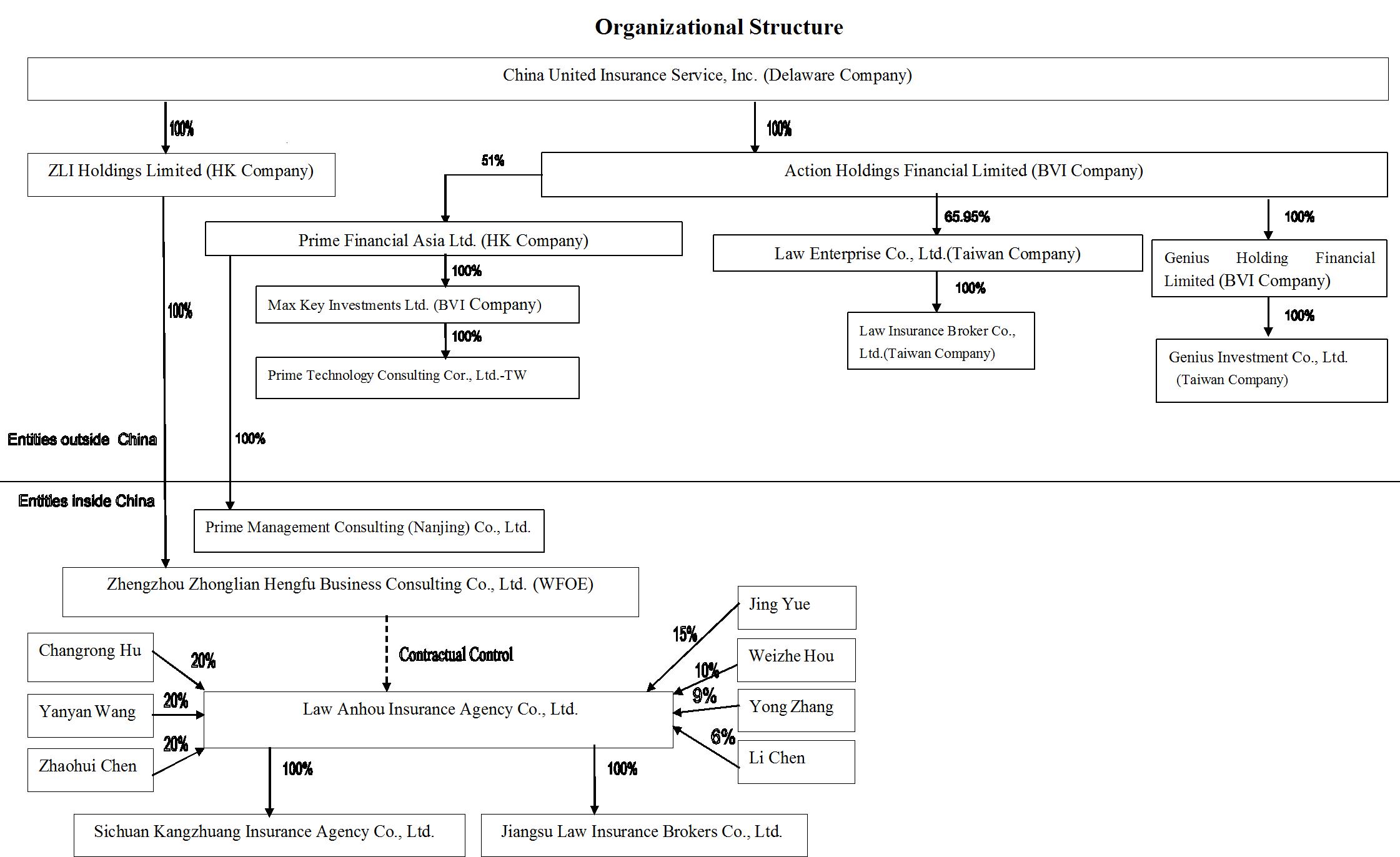

China United Insurance Service, Inc. (“China United”, “CUIS” or the “Company”) is a Delaware corporation organized on June 4, 2010 by Yi Hsiao Mao, a Taiwanese citizen, as a listing vehicle for ZLI Holdings Limited (“CU Hong Kong”) to be quoted on the United States Over the Counter Bulletin Board (the “OTCBB”).

The corporate structure as of March 31, 2016 is as follows:

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Principles of Consolidation

The unaudited accompanying condensed consolidated financial statements include the accounts of China United and its subsidiaries as shown in the organization structure in Note 1 above. All significant intercompany transactions and balances were eliminated in consolidation.

Basis of Presentation

The unaudited condensed consolidated financial statements presented herein have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information and in accordance with the instructions to Form 10-Q and Regulation S-X. Accordingly, the financial statements do not include all of the information and notes required by GAAP for complete financial statements. In the opinion of management, all adjustments, including normal recurring adjustments, considered necessary for a fair statement of the financial statements have been included. Operating results for the three months ended March 31, 2016 are not necessarily indicative of the results that may be expected for the year ended December 31, 2016.

F-4

These unaudited condensed consolidated financial statements and notes thereto should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto for the year ended December 31, 2015, which were included in the Company’s 2015 Annual Report on Form 10-K. The accompanying condensed consolidated balance sheet as of December 31, 2015, has been derived from the Company’s audited consolidated financial statements as of that date.

Concentration of Risk

Financial instruments that potentially subject the Company to significant concentrations of credit risk consist principally of cash and equivalents and accounts receivable. As of March 31, 2016, $1,346,439 of the Company’s cash and equivalents held by financial institutions was insured, and the remaining balance of $19,086,719 was not insured. With respect to accounts receivable, the Company generally does not require collateral and does not have an allowance for doubtful accounts.

For the three months ended March 31, 2016 and 2015, the Company’s revenues from sale of insurance policies underwritten by these companies were:

| Three months ended March 31, | ||||||||||||||||

| 2016 | 2015 | |||||||||||||||

| Amount | % of Total Revenue | Amount | % of Total Revenue | |||||||||||||

| Farglory Life Insurance Co., Ltd. | $ | 2,242,125 | 23 | % | $ | 2,217,851 | 23 | % | ||||||||

| Fubon Life Insurance Co., Ltd. | 1,377,986 | 14 | % | 1,275,718 | 13 | % | ||||||||||

| AIA International Ltd., Taiwan | (* | ) | (* | ) | 1,051,534 | 11 | % | |||||||||

| TransGlobe Life Insurance Inc. | (* | ) | (* | ) | 1,108,691 | 11 | % | |||||||||

| CTBC Life Insurance Co., Ltd. | (* | ) | (* | ) | 994,481 | 10 | % | |||||||||

| (*) | Revenue for the three months ended had not exceeded 10% or more of the consolidated revenue. |

As of March 31, 2016 and December 31, 2015, the Company’s accounts receivable from these companies were:

| March 31, 2016 | December 31, 2015 | |||||||||||||||

| Amount | % of Total Accounts Receivable | Amount | % of Total Accounts Receivable | |||||||||||||

| Farglory Life Insurance Co., Ltd. | $ | 1,231,335 | 30 | % | $ | 3,689,404 | 43 | % | ||||||||

| Fubon Life Insurance Co., Ltd | 533,268 | 13 | % | 990,327 | 11 | % | ||||||||||

| AIA International Ltd., Taiwan | (* | ) | (* | ) | (** | ) | (**) | |||||||||

| TransGlobe Life Insurance Inc. | (* | ) | (* | ) | (** | ) | (**) | |||||||||

| CTBC Life Insurance Co., Ltd | (* | ) | (* | ) | 994,978 | 11 | % | |||||||||

| (**) | Accounts receivable for the year ended had not exceeded 10% or more of the consolidated accounts receivable. |

The Company's operations are in the PRC and Taiwan. Accordingly, the Company's business, financial condition and results of operations may be influenced by the political, economic, foreign currency exchange and legal environments in the PRC and Taiwan, and by the state of each economy. The Company’s results may be adversely affected by changes in the political and social conditions in the PRC and Taiwan, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, and rates and methods of taxation, among other things.

F-5

Recent Accounting Pronouncements

In May 2014, the FASB issued Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers (Topic 606). ASU 2014-09 outlines a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers and supersedes current revenue recognition guidance. In August 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date. The amendment in this update defers the effective date of ASU 2014-09 for all entities by one year to annual periods beginning after December 15, 2017. Early adoption is permitted as of the original effective date, interim and annual reporting periods after December 15, 2016. Entities have the option of using either a full retrospective or a modified retrospective approach to adopt ASU 2014-09. The Company is still in the process of analyzing the effect of this new standard, including the transition method, to determine the impact on the Company's consolidated financial position, results of operations, cash flows, and related disclosures.

In September 2015, the FASB issued Accounting Standards Update No. 2015-16, "Simplifying the Accounting for Measurement-Period Adjustments". Measurement period adjustments are changes to provisional amounts recorded when the accounting for a business combination is incomplete as of the end of a reporting period. The measurement period can extend for up to a year following the transaction date. The new guidance requires companies to recognize these adjustments, including any related impacts to net income, in the reporting period in which the adjustments are determined. Companies are no longer required to retroactively apply measurement period adjustments to the prior period. This update is effective for annual and interim periods beginning after December 15, 2016. We have early adopted this standard beginning in fiscal 2016. There was no material impact to the Consolidated Financial Statements.

In November 2015, the FASB issued Accounting Standards Update No. 2015-17, "Balance Sheet Classification of Deferred Taxes". The new guidance requires that all deferred tax assets and liabilities, along with any related valuation allowance, be classified as noncurrent on the balance sheet. This update is effective for annual periods beginning after December 15, 2016 and interim periods within those annual periods. ASU 2015-17 will be effective for us, but will not cause a material impact on our financial condition or the results of our operations.

In January 2016, the FASB issued Accounting Standards Update No. 2016-01, "Financial Instruments-Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities," which amends the guidance in U.S. GAAP on the classification and measurement of financial instruments. Changes to the current guidance primarily affect the accounting for equity investments, financial liabilities under the fair value option, and the presentation and disclosure requirements for financial instruments. In addition, the ASU clarifies guidance related to the valuation allowance assessment when recognizing deferred tax assets resulting from unrealized losses on available-for-sale debt securities. The new standard is effective for fiscal years and interim periods beginning after December 15, 2017, and upon adoption, an entity should apply the amendments by means of a cumulative-effect adjustment to the balance sheet at the beginning of the first reporting period in which the guidance is effective. Early adoption is not permitted except for the provision to record fair value changes for financial liabilities under the fair value option resulting from instrument-specific credit risk in other comprehensive income. The Company is currently evaluating the impact of adopting this guidance.

In February 2016, the FASB issued Accounting Standards Update No. 2016-02, Leases (Topic 842). The guidance in ASU 2016-02 supersedes the lease recognition requirements in ASC Topic 840, Leases (FAS 13). ASU 2016-02 requires an entity to recognize assets and liabilities arising from a lease for both financing and operating leases, along with additional qualitative and quantitative disclosures. ASU 2016-02 is effective for fiscal years beginning after December 15, 2018, with early adoption permitted. The Company is currently evaluating the effect this standard will have on its Consolidated Financial Statements.

In March 2016, the FASB issued ASU 2016-03, “Intangibles-Goodwill and Other (Topic 350); Business Combinations (Topic 805); Consolidation (Topic 810); Derivatives and Hedging (Topic 815): Effective Date and Transition Guidance”. The amendments in this ASU make the guidance in ASUs 2014-02, 2014-03, 2014-07, and 2014-18 effective immediately by removing their effective dates. The amendments also include transition provisions that provide that private companies are able to forgo a preferability assessment the first time they elect the accounting alternatives within the scope of this ASU. Any subsequent change to an accounting policy election requires justification that the change is preferable under Topic 250, Accounting Changes and Error Corrections. The amendments in this ASU also extend the transition guidance in ASUs 2014-02, 2014-03, 2014-07, and 2014-18 indefinitely. While this ASU extends transition guidance for Updates 2014-07 and 2014-18, there is no intention to change how transition is applied for those two ASUs. The Company is currently in the process of evaluating the impact of the adoption on its consolidated financial statements.

F-6

In March 2016, the FASB issued ASU No. 2016-07, "Investments - Equity Method and Joint Ventures (Topic 323): Simplifying the Transition to the Equity Method of Accounting." ASU No. 2016-07 eliminates the requirement for an investment that qualifies for the use of the equity method of accounting as a result of an increase in the level of ownership or degree of influence to adjust the investment, results of operations and retained earnings retrospectively. ASU No. 2016-07 will be effective prospectively for the Company for increases in the level of ownership interest or degree of influence that result in the adoption of the equity method that occur during or after the quarter ending December 31, 2017, with early adoption permitted. The impact of this guidance for the Company is dependent on any future increases in the level of ownership interest or degree of influence that result in the adoption of the equity method.

In March 2016, the FASB issued ASU 2016-08, “Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net)”. 'The amendments in this ASU are intended to improve the operability and understandability of the implementation guidance on principal versus agent considerations by amending certain existing illustrative examples and adding additional illustrative examples to assist in the application of the guidance. The effective date and transition of these amendments is the same as the effective date and transition of ASU 2014-09, “Revenue from Contracts with Customers (Topic 606)”. Public entities should apply the amendments in ASU 2014-09 for annual reporting periods beginning after December 15, 2017, including interim reporting periods therein. The Company is currently in the process of evaluating the impact of the adoption on its consolidated financial statements.

In March 2016, the FASB issued ASU No. 2016-09, "Compensation - Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting." ASU No. 2016-09 impacts certain aspects of the accounting for share-based payment transactions, including income tax consequences, classification of awards as either equity or liabilities, and classification on the statements of cash flows. ASU No. 2016-09 will be effective for the Company for the quarter ending December 31, 2017, with early adoption permitted. The Company is currently assessing the impact adoption of this guidance will have on its consolidated financial statements.

NOTE 3 – CASH AND EQUIVALENTS

As of March 31, 2016 and December 31, 2015, our cash and equivalents primarily consisted of cash and certificates of deposits. The carrying amounts reported on the consolidated balance sheets for cash and cash equivalents approximate fair value.

NOTE 4 - MARKETABLE SECURITIES

Marketable securities represent investment in equity securities of listed stocks and funds, which are classified as Level 1 securities as follows:

| March 31, 2016 | ||||||||||||

| Cost or | Gross | |||||||||||

| Amortized | Unrealized | Total | ||||||||||

| Cost | Gains (Losses) | Fair Value | ||||||||||

| Level 1 securities: | ||||||||||||

| Stocks | $ | 28,863 | $ | (8 | ) | $ | 28,855 | |||||

| Funds | 2,340,219 | 48,921 | 2,389,140 | |||||||||

| $ | 2,369,082 | $ | 48,913 | $ | 2,417,995 | |||||||

F-7

| December 31, 2015 | ||||||||||||

| Cost or | Gross | |||||||||||

| Amortized | Unrealized | Total | ||||||||||

| Cost | Gains (Losses) | Fair Value | ||||||||||

| Level 1 securities: | ||||||||||||

| Stocks | $ | 28,278 | $ | 585 | $ | 28,863 | ||||||

| Funds | 2,408,728 | (68,509 | ) | 2,340,219 | ||||||||

| $ | 2,437,006 | $ | (67,924 | ) | $ | 2,369,082 | ||||||

NOTE 5 – OTHER CURRENT ASSETS

The Company’s other current assets consisted of the following as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| Prepaid expenses | $ | 273,998 | $ | 603,557 | ||||

| Current assets associated with discontinued operations | - | 224,140 | ||||||

| Prepaid rent and rent deposit | 269,169 | 133,179 | ||||||

| Other receivable | 16,141 | 86,539 | ||||||

| Other commission receivable | 43,758 | - | ||||||

| Interest receivable | 61,386 | - | ||||||

| Refundable business tax | 8,524 | 7,600 | ||||||

| Deferred tax assets | 77 | - | ||||||

| Total other current assets | $ | 673,053 | $ | 1,055,015 | ||||

NOTE 6 – PROPERTY, PLANT AND EQUIPMENT, NET

Property, plant and equipment consisted of the following, as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| Office Equipment | $ | 1,038,435 | $ | 1,080,621 | ||||

| Office Furniture | 177,412 | 125,746 | ||||||

| Leasehold improvements | 527,595 | 511,874 | ||||||

| Transportation equipment | 84,958 | 84,398 | ||||||

| Other equipment | 102,907 | 97,996 | ||||||

| Total | 1,931,307 | 1,900,635 | ||||||

| Less: accumulated depreciation | (972,889 | ) | (981,837 | ) | ||||

| Total property, plant and equipment, net | $ | 958,418 | $ | 918,798 | ||||

NOTE 7 – INTANGIBLE ASSETS

As of March 31, 2016 and December 31, 2015, the Company’s intangible assets consisted the following:

| March 31, 2016 | December 31, 2015 | |||||||

| Software | $ | 1,211,498 | $ | 780,355 | ||||

| Less: accumulated amortization | (492,981 | ) | (311,576 | ) | ||||

| Total intangible assets | $ | 718,517 | $ | 468,779 | ||||

F-8

Estimated future intangible amortization as of March 31, 2016 is as follows:

| Years ending March 31, | Amount | |||

| 2017 | $ | 215,784 | ||

| 2018 | 138,329 | |||

| 2019 | 138,329 | |||

| 2020 | 128,626 | |||

| 2021 | 87,124 | |||

| Thereafter | 10,325 | |||

| Total | $ | 718,517 | ||

The Company reclassified amount of $175,925 and $89,340 from property, plant and equipment and accumulated depreciation to intangible assets and accumulated amortization, respectively, in January 2016.

NOTE 8 – ACQUISITION AND GOODWILL

(1) Acquisition of PFAL

On April 23, 2014, AHFL entered into a capital increase agreement (“Agreement”) with Chun Kwok Wong (“Mr. Wong”), the owner of Prime Financial Asia Ltd (PFAL) which is a re-insurance broker company resided in Hong Kong. Upon the Agreement, Mr. Wong would increase PFAL’s capital contribution from HK$500,000 to HK$1,470,000, and AHFL would contribute HK$1,530,000, approximately $197,000, to PFAL’s capital contribution. Upon the completion of capital increase by both parties, Mr. Wong and AHFL would own 49% and 51% of PFAL’s equity interest, respectively. The transaction was completed on April 30, 2014.

The FV of the net identifiable assets of PFAL at acquisition date was $324,871, and 51% of which was $165,684. The Company recorded $31,651 excess of purchase price over the FV of assets acquired and liabilities assumed as goodwill. No intangible assets were identified as of the acquisition date. As of March 31, 2016, there were no indications of the impairment of the goodwill.

(2) Acquisition of GHFL

On February 13, 2015, CUIS and AHFL entered into an acquisition agreement with the selling shareholder (Mr. Chwanhau Li, the director of the Company) of Genius Holdings Financial Limited ( “GHFL”), a company with limited liability incorporated under the laws of British Virgin Islands, to issue 352,166 fully paid and non-assessable shares of AHFL Common Stock together with an granted option for 352,166 shares of common stock of CUIS (“Option”), in exchange for 704,333 shares of common stock of GHFL, being all of the issued and outstanding capital stock of GHFL. Subsequent to the acquisition, GHFL became a wholly-owned subsidiary of CUIS. GHFL holds 100% issued and outstanding shares of Genius Investment Consultant Co., Ltd. (“Taiwan Genius”), a limited company incorporated under the laws of Taiwan, which in turn holds 15.64% issued and outstanding shares of Genius Insurance Broker Co., Ltd. (“Genius Broker”), a company limited by shares incorporated under the laws of Taiwan. Both GHFL and Taiwan Genius have no substantive business operation other than the holding of shares of its subsidiary. Genius Broker is primarily engaged in broker business across Taiwan. On February 13, 2015, the acquisition was completed; the selling shareholder transferred 100% shares in GHFL to AHFL. The Option has been exercised by the selling shareholder on March 31, 2015. The total fair value of AHFL 352,166 shares ($1,771,395) and CUIS 352,166 option ($1,711,562) at acquisition date was $3,482,957. The Company recorded $2,039,840 excess of purchase price as goodwill. As of March 31, 2016, there were no indications of the impairment of the goodwill.

The acquisition was accounted for under the purchase method of accounting. Accordingly, the results of GHFL have been included in the consolidated financial statements since the date of acquisition. The purchase price has been allocated to the assets acquired and liabilities assumed based upon their estimated fair values and the price were allocated as follows:

F-9

| February 13, 2015 | ||||

| Current assets | $ | 321 | ||

| Long-term investment | 1,488,829 | |||

| Goodwill | 2,039,840 | |||

| Current liabilities | (46,033 | ) | ||

| Total purchase price | $ | 3,482,957 | ||

No supplemental pro forma information is presented for the acquisition due to the immaterial effect of the acquisition on the Company’s results of operations.

NOTE 9 – LONG-TERM INVESTMENT

The Company classifies its investments as available-for-sale in accordance with ASC 320 “Debt and Equity Securities”, Investments – Debt and Equity Securities, which are reported at fair value. Unrealized gains and losses as a result of changes in the fair value of the available-for-sale investments are recorded as a separate component within accumulated other comprehensive income in the accompanying consolidated balance sheets.

The Company uses the cost method of accounting for investments in companies that do not have a readily determinable fair value in which it holds an interest of less than 20% and over which it does not have the ability to exercise significant influence. Investments are considered to be impaired when a decline in fair value is judged to be other-than-temporary. Once a decline in fair value is determined to be other-than-temporary, an impairment charge is recorded and a new cost basis in the investment is established.

As of March 31, 2016 and December 31, 2015, the Company’s long-term investment consisted the following:

| March 31, 2016 | December 31, 2015 | |||||||

| Equity Investment Co., Ltd | $ | 1,193,583 | $ | 1,170,230 | ||||

| Government Bonds | 96,265 | 94,381 | ||||||

| Total | $ | 1,289,848 | $ | 1,264,611 | ||||

As of March 31, 2016 and December 31, 2015, the Company had the following long-term investment in equity:

| Type | Investee | March 31, 2016 Investment Ownership | Amount | |||||||

| Cost | Genius Insurance Broker Co., Ltd | 15.64 | % | $ | 1,193,583 | |||||

| Type | Investee | December 31, 2015 Investment Ownership |

Amount | |||||||

| Cost | Genius Insurance Broker Co., Ltd | 15.64 | % | $ | 1,170,230 | |||||

According to Taiwan regulatory requirements, Law Broker is required to maintain a minimum of NT$3,000,000 ($96,265) in a separate account. Law Broker chose to buy government bonds and has the right to trade such bonds with other debt or equity instruments. The amount, however, was defined as restricted asset.

F-10

| March 31, 2016 | ||||||||||||

| Gross | ||||||||||||

| Fair Value at | Unrealized | Total | ||||||||||

| December 31, 2015 | Gains (Losses) | Fair Value | ||||||||||

| Government bonds | 94,381 | 1,884 | 96,265 | |||||||||

| $ | 94,381 | $ | 1,884 | $ | 96,265 | |||||||

| December 31, 2015 | ||||||||||||

| Cost or | Gross | |||||||||||

| Amortized | Unrealized | Total | ||||||||||

| Cost | Gains (Losses) | Fair Value | ||||||||||

| Government bonds | 93,089 | 1,292 | 94,381 | |||||||||

| $ | 93,089 | $ | 1,292 | $ | 94,381 | |||||||

NOTE 10 – OTHER ASSETS

The Company’s other assets consisted of the following as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| Rental deposits | $ | 403,012 | $ | 401,920 | ||||

| Restricted cash | 232,634 | 231,100 | ||||||

| Prepayments | 133,331 | 156,772 | ||||||

| Other | 1,460 | 1,431 | ||||||

| Total other assets | $ | 770,437 | $ | 791,223 | ||||

Rental deposits include long-term leasing deposits. Restricted cash is a deposit in bank by the Company in conformity with Provisions of the Supervision and Administration of Specialized Insurance Agencies, and cannot be withdrawn without the permission of the regulatory commission. Prepayments are prepaid long-term software-maintenance contract pending for final acceptance, and will be transferred to intangible assets upon acceptance.

NOTE 11 – TAXES PAYABLE

The Company’s taxes payable consisted of the following as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| PRC Tax | $ | 81,363 | $ | 99,505 | ||||

| Taiwan Tax | 1,451,752 | 1,422,457 | ||||||

| Total tax payable | $ | 1,533,115 | $ | 1,521,962 | ||||

PRC tax represents income tax and other taxes accrued according to PRC tax law by our subsidiaries and CAE in the PRC. Taiwan tax represents income tax and other taxes accrued according to Taiwan tax law by our subsidiaries and branches in Taiwan. Both will be settled within the next twelve months according to the respective tax laws.

F-11

NOTE 12 – OTHER CURRENT LIABILITIES

Other current liabilities are as follows, as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| Commissions payable to sub-agents | $ | 3,256,281 | $ | 6,644,989 | ||||

| Accrued bonus | 481,489 | 1,050,411 | ||||||

| Refund to AIATW | - | 502,532 | ||||||

| Accrued tax penalties | 370,000 | 370,000 | ||||||

| Accrued business tax | 116,701 | 326,954 | ||||||

| Withholding employee personal tax | 211,970 | 295,989 | ||||||

| Salary payable to administrative staff | 111,115 | 229,624 | ||||||

| Due to previous shareholders of AHFL | 685,057 | 685,059 | ||||||

| Accrued advertisement fee | 73,584 | 151,535 | ||||||

| Accrued labor, health insurance and employee retirement plan | 84,431 | 84,138 | ||||||

| Other accrued expenses | 253,922 | 396,117 | ||||||

| Others | 175,094 | 130,259 | ||||||

| Total other current liabilities | $ | 5,819,644 | $ | 10,867,607 | ||||

Commissions payable to sub-agents, salaries payable to administrative staff, accrued bonus, and accrued advertisement fee are usually settled within 12 months. Refund to AIATW is described in Note 14. Accrued tax penalties are estimated potential penalty in the event of a tax audit. Withholding employee personal tax and accrued labor, health insurance and employee retirement plan will be paid to local tax bureau within one month. The amount due to previous shareholders of AHFL is the remaining balance of the acquisition cost. Other accrued expenses are mainly for operating expenses payable within the credit terms provided by suppliers. Others mainly represent short term payable for expenses such as training and travelling.

NOTE 13 – SHORT TERM LOANS

| March 31, 2016 | December 31, 2015 | |||||||

| Loan A, interest at 1.5%, maturity date December 31, 2016 | $ | 70,000 | $ | 70,000 | ||||

| Loan B, interest at 1.5%, maturity date December 31, 2016 | 108,691 | 152,235 | ||||||

| Total short term loans | $ | 178,691 | $ | 222,235 | ||||

On October 12, 2015, the Company entered into a loan agreement ("Loan A") with Zhengxiong Huang. The Short-term Loan Agreement provided for a $70,000 loan to the Company. The Short-term Loan bore an interest rate of 1.5% per annum and the principle and interest were due on December 31, 2015. On December 31, 2015, the Company extended this loan agreement to December 31, 2016 with same conditions.

On December 3, 2015, the Company entered into a loan agreement ("Loan B") with Yuzhen Chen. The Short-term Loan Agreement provided for a $152,235 (NT$ 5,000,000) loan to the Company. The Short-term Loan bore an interest rate of 1.5% per annum and the principle and interest were due on December 31, 2015. On December 31, 2015, the Company extended this loan agreement to December 31, 2016 with same conditions. On January 13, 2016, the Company paid amount of $46,582 (NT$ 1,500,000) back. As of March 31, 2016, the Company had a loan amount of $108,691 (NT$3,500,000).

NOTE 14 – LONG-TERM LIABILITIES

Long-term liabilities are as follows as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| Unearned revenue | 6,726,129 | 6,594,530 | ||||||

| Total other long-term liabilities | $ | 6,726,129 | $ | 6,594,530 | ||||

F-12

On June 10, 2013, AHFL entered into a Strategic Alliance Agreement (the “Alliance Agreement”) with AIA International Limited Taiwan Branch (“AIATW”). The purpose of the Alliance Agreement is to promote life insurance products provided by AIATW within Taiwan by insurance agencies or brokerage companies affiliated with AHFL or CUIS. The term of the Alliance Agreement is from April 15, 2013 to August 31, 2018. Pursuant to the terms of the Alliance Agreement, AIATW paid AHFL the Execution Fee of $8,326,700 (NT$250,000,000, including the tax of NT$11,904,762), which is to be recorded as revenue upon fulfilling sales targets and the 13-month persistency ratio, as defined, over the next five years. The Execution Fee may be required to be recalculated if certain performance targets are not met by AHFL. On September 30, 2014, AHFL entered into a Strategic Alliance Supplemental Agreement (the “Supplemental Agreement”) with AIATW. In the Supplemental Agreement, the performance targets and the provision about refunding the Execution Fee when the performance targets are not met were revised. On January 6, 2016, AHFL entered into an Amendment 2 to Strategic Alliance Agreement (the “Amendment No. 2”) with AIATW to further revise certain provisions in the Strategic Alliance Agreement and the previous amendment entered into by and between AHFL and AIATW. The purpose of the Strategic Alliance Agreement is to promote life insurance products provided by AIATW within the territory of Taiwan through insurance agency companies or insurance brokerage companies. To the extent permitted by applicable laws and regulations, AHFL shall assist and encourage any insurance agency company or insurance brokerage company duly approved by the competent government authorities of Taiwan (the “Appointed Broker/Agent”), to cooperate with AIATW for the promotion of life insurance products of AIATW. Pursuant to the Amendment No. 2, the expiration date of the Strategic Alliance Agreement has been extended from May 31, 2018 to December 31, 2021, and the effect of the Strategic Alliance Agreement during the period from October 1, 2014 to December 31, 2015 has been suspended. In addition, both AHFL and AIATW agreed to adjust certain terms and conditions set forth in the Strategic Alliance Agreement, among which: (i) expand the scope of services to be provided by AHFL to AIATW to include, without limitation, assessment and advice on suitability of cooperative partners, advice on product strategies suitable for promotion channel development, advice on promotion/sales channel improvement, advice on promotion channel marketing and strategic planning, and promotion channel talent training; and (ii) remove certain provisions related to performance milestones and refund of Execution Fees. On March 15, 2016, AHFL issued a promise letter to AIATW that AHFL is required to (i) fulfill sales targets and (ii) the 13-month persistency ratio.

AHFL refunded amount of $152,235 (NTD 5,000,000) and $502,532 (NTD 16,505,144) to AIATW on December 3, 2015 and February 23, 2016, respectively, due to the portion of performance sales targets are not met during the period from June 10, 2013 to September 30, 2014. AHFL did not book any short-term unearned revenue since the Strategic Alliance Agreement will end on December 31, 2021 and the performance will calculate then to determine how much revenue AHFL can book accordingly, and the Company booked the whole $6,726,129 as long-term liability.

NOTE 15 – PREFERRED STOCK

The Company is authorized to issue 10,000,000 shares of preferred stock, $.00001 par value. We currently have 1,000,000 shares of Series A Preferred Stock (“Series A Stock”) outstanding as of December 31, 2014. The Series A Stock has the following rights and preferences:

Voting Rights. Except as otherwise provided by law, the Series A Stock and the common stock vote together on all matters submitted to a vote of our shareholders. Each holder of Series A Stock is entitled to ten votes for each share of Series A Stock held of record by such holder as of the applicable record date on any matter that is submitted to a vote of the stockholders of the Registrant.

Series A Board Designee and Board Restriction. In addition to the voting rights disclosed above, the holders of the Series A Stock shall be entitled to appoint one director (the “Series A Director”). No Board resolution regarding certain material Company actions can be made without the affirmative vote of the Series A Director.

Dividends. The holders of Series A Stock are entitled to share equally with the holders of common stock, on a per share basis, in such dividends and other distributions of cash, property or shares of stock of the Registrant as may be declared by the Board.

F-13

Liquidation. In the event of a voluntary or involuntary liquidation, dissolution, distribution of assets or winding up of the Registrant, the holders of common stock and the holders of Series A Stock shall be entitled to share equally on a per share basis, in all assets of the Registrant of whatever kind available for distribution.

Conversion Rights. The holders of the Series A Stock have the right to convert their shares thereof at any time into shares of the Registrant's common stock. Each share of Series A Stock is convertible into one share of common stock.

If the Registrant in any manner subdivides or combines the outstanding shares of common stock, the outstanding shares of the Series A Stock will be subdivided or combined in the same manner.

Business Combinations. In any merger, consolidation, reorganization or other business combination, the consideration received per share by the holders the common stock and the holders of the Series A Stock in such merger, consolidation, reorganization or other business combination shall be identical; provided however, that if such consideration consists, in whole or in part, of certain equity interests, the rights and limitations of such equity interests may differ to the extent that the rights and limitations of the common stock and the Series A Stock differ.

Fully Paid and Nonassessable. All of our outstanding shares of preferred stock are fully paid and nonassessable.

The fair value of the 1,000,000 preferred shares was $225,000 at the time of the preferred share issuance. The Fair value of the common shares was $200,000 at the time of the preferred share issuance based on its market price at the date of the transaction. Therefore, the incremental value of the preferred shares was $25,000. This amount may be deemed compensation.

From the qualitative aspect, the Company notes the following regarding this deemed compensation:

Does not violate any debt or other contract covenants;

Does not change any earnings or EPS trends;

Does not affect any previous earnings or EPS guidance;

Does not affect any segment or class of revenue;

Does not affect any regulatory compliance matters;

Does not affect cash compensation of management;

Does not involve concealment of an unlawful act.

Additional preferred stock may be authorized and issued in the future in connection with acquisitions, financings, or other matters, as the Board of Directors deems appropriate. In the event that the Registrant issues any shares of preferred stock, a certificate of designation containing the rights, privileges and limitations of this series of preferred stock will be filed with the Secretary of State of the State of Delaware. The effect of this preferred stock designation power is that our Board of Directors alone, subject to Federal securities laws, applicable blue sky laws, and Delaware law, may be able to authorize the issuance of preferred stock which could have the effect of delaying, deferring, or preventing a change in control without further action by our stockholders, and may adversely affect the voting and other rights of the holders of our common stock.

F-14

NOTE 16 – STATUTORY RESERVES

According to Taiwan accounting rules and corporation regulations, the company’s subsidiaries in Taiwan must appropriate 10% of net income to statutory reserves until the accumulated reserve hits registered capital. The reserve can be converted into share capital by issuing new shares to existing shareholders in proportion to their shareholding or by increasing the par value of the shares currently held by them, with a limitation that the reserve left is not less than 25% of the registered capital after converting to share capital.

Pursuant to the PRC regulations, the Company’s Consolidated Affiliated Entities (“CAE”) are required to transfer 10% of their net profit, as determined under the PRC accounting regulations, to a Statutory Common Reserve Fund (“Reserve Fund”). Appropriation to the Reserve Fund may cease when the fund equals 50% of a company’s registered capital or when a company has accumulated losses. The transfer to this reserve must be made before distribution of dividends to shareholders. The Company’s CAE did not appropriate such reserve as they have accumulated losses.

NOTE 17 – NON-CONTROLLING INTERESTS

Non-controlling interests consisted of the following:

| Acquisition and | Adjustments /Net | |||||||||||||||||||||||

| % of Non- | As of | Increase | Income of | As of | ||||||||||||||||||||

| controlling | December 31, | Investment | Non-controlling | March 31, | ||||||||||||||||||||

| Name of Affiliate | Interest | 2015 | (Fair Value) | Interest | Discontinued | 2016 | ||||||||||||||||||

| Law Enterprise | 34.05 | % | $ | 199,699 | $ | - | $ | 146,295 | $ | - | $ | 345,994 | ||||||||||||

| Law Broker | 34.05 | % | 7,197,128 | - | 687 | - | 7,197,815 | |||||||||||||||||

| PFAL | 49.00 | % | 206,098 | - | (3,626 | ) | - | 202,472 | ||||||||||||||||

| MKI | 49.00 | % | (1,065 | ) | - | (51 | ) | - | (1,116 | ) | ||||||||||||||

| PTC Taiwan | 49.00 | % | (26,292 | ) | - | (23,946 | ) | - | (50,238 | ) | ||||||||||||||

| PTC Nanjing | 49.00 | % | (837 | ) | - | 59 | - | (778 | ) | |||||||||||||||

| Total | $ | 7,574,731 | $ | - | $ | 119,418 | $ | - | $ | 7,694,149 | ||||||||||||||

| Acquisition and | Adjustments /Net | |||||||||||||||||||||||

| % of Non- | As of | Increase | Income of | As of | ||||||||||||||||||||

| controlling | December 31, | Investment | Non-controlling | December 31, | ||||||||||||||||||||

| Name of Affiliate | Interest | 2014 | (Fair Value) | Interest | Discontinued | 2015 | ||||||||||||||||||

| Law Enterprise | 34.05 | % | $ | 882,327 | $ | - | $ | (682,628 | ) | $ | - | $ | 199,699 | |||||||||||

| Law Broker | 34.05 | % | 5,471,140 | - | 1,725,988 | - | 7,197,128 | |||||||||||||||||

| Law Agent | 36.69 | % | 24,689 | - | (1,033 | ) | (23,656 | ) | - | |||||||||||||||

| Risk Management | 35.47 | % | (91,809 | ) | - | 22,309 | 69,500 | - | ||||||||||||||||

| PFAL | 49.00 | % | 97,080 | - | 109,018 | - | 206,098 | |||||||||||||||||

| MKI | 49.00 | % | - | - | (1,065 | ) | - | (1,065 | ) | |||||||||||||||

| PTC Taiwan | 49.00 | % | - | - | (26,292 | ) | - | (26,292 | ) | |||||||||||||||

| PTC Nanjing | 49.00 | % | - | - | (837 | ) | - | (837 | ) | |||||||||||||||

| Total | $ | 6,383,427 | $ | - | $ | 1,145,460 | $ | 45,844 | $ | 7,574,731 | ||||||||||||||

NOTE 18– INCOME TAX

CU WFOE and the VIEs in the PRC are governed by the Income Tax Law of the PRC concerning the private-run enterprises, which are generally subject to tax at 25% on income reported in the statutory financial statements after appropriated adjustments. Except for Jiangsu, according to the requirement of local tax authorities, the tax basis is deemed as 10% of total revenue, instead of net income. The tax rate of Jiangsu is also 25%.

F-15

The Company’s subsidiaries in Taiwan are governed by the Income Tax Law of Taiwan, and are generally subject to tax at 17% on income reported in the statutory financial statements after appropriate adjustments. In the meanwhile, Income Tax Law of Taiwan provides that a company is taxed at additional 10% on any undistributed earnings to its shareholders.

The following table reconciles the US statutory rates to the Company’s effective tax rate for the three months ended March 31, 2016 and 2015:

| March 31, 2016 | March 31, 2015 | |||||||

| US statutory rate | 34 | % | 34 | % | ||||

| Tax rate difference | (8 | )% | 80 | % | ||||

| Tax base difference | (4 | )% | (2 | )% | ||||

| Loss in subsidiaries | (28 | )% | 266 | % | ||||

| Un-deductible and non-taxable items | 6 | % | (33 | )% | ||||

| Tax per financial statements | 0 | % | 345 | % | ||||

Un-deductible and non-taxable items mainly represent un-deductible expenses according to PRC tax laws and the non-taxable tax income or loss.

NOTE 19 - RELATED PARTY TRANSACTIONS

On February 13, 2015, CUIS and AHFL entered into an acquisition agreement with Mr. Chwanhau Li (the director of the Company), the selling shareholder of Genius Holdings Financial Limited. (Please see detail in Note 8 (2))

Due to related parties

The related parties listed below loaned money to the Company for working capital. Due to related parties consisted of the following as of March 31, 2016 and December 31, 2015:

| March 31, 2016 | December 31, 2015 | |||||||

| Due to Mr. Mao (Principal Shareholder of the Company) | $ | 314,666 | $ | 297,414 | ||||

| Due to Xude Investment (Owned by Mr. Chwan Hau Li) | 32,397 | 32,223 | ||||||

| Due to Mr. Zhu (Legal Representative of Jiangsu) | 2,147 | 2,133 | ||||||

| Due to Ms. Lee (Director of CUIS) | 831 | 826 | ||||||

| Due to Multiple Capital Enterprise | - | 608,941 | ||||||

| Due to other shareholders | - | 4,395 | ||||||

| Total | $ | 350,041 | $ | 945,932 | ||||

On December 23, 2014, AHFL entered into a Loan Agreement (the “Loan Agreement”) with Shu-Fen Lee (“Ms. Lee”), the Series A Director of the Company. Pursuant to the Loan Agreement, Ms. Lee provided a loan in the amount of $314,644 (NT$10 million) (the “Loan”) to AHFL. The term for the Loan is from December 23, 2014 to December 22, 2015 with a fixed interest rate at 1.5%. The entire loan and interest amount of $314,928 (NT$10,009,041) have been paid off on January 14, 2015.

F-16

On December 25, 2015, the Company entered into a loan agreement (the “Short-term Loan Agreement”) with Multiple Capital Enterprise Co., Ltd. The Short-term Loan Agreement provided for a $608,941 (NT$20,000,000) loan to the Company. The Short-term Loan bore an interest rate of 1.5% per annum and the principle and interest were due on June 30, 2016. Majority of Multiple Capital Enterprise shareholders are the Company’s management level. The entire loan and interest amount of $598,905 (NT$20,014,795) have been paid off on January 12, 2016.

Except for the two aforementioned loans, the loans arose from Due to related parties bore no interest and were payable on demand.

NOTE 20 – COMMITMENTS

Operating Leases

The Company has operating leases for its offices. Rental expenses for the three months ended March 31, 2016 and 2015 were $507,460 and $410,459 respectively. On March 31, 2016, total future minimum annual lease payments under operating leases were as follows, by years:

| Twelve months ended March 31, 2017 | $ | 1,794,846 | ||

| Twelve months ended March 31, 2018 | 1,184,502 | |||

| Twelve months ended March 31, 2019 | 684,686 | |||

| Twelve months ended March 31, 2020 | 22,471 | |||

| Twelve months ended March 31, 2021 | 13,631 | |||

| Thereafter | - | |||

| Total | $ | 3,700,136 |

Acquisition Agreement

On February 22, 2015, the Company and the selling shareholder of GHFL entered into an Amendment to the Acquisition Agreement dated February 13, 2015, pursuant to which if the Guaranteed Price per share is higher than the Average Price per share, then the Parties shall negotiate in good faith on an adjustment to the Purchase Price as necessary, if any.

On February 17, 2016, the Company and AHFL entered into an Amendment 2 to the Genius Acquisition Agreement (the “Genius Amendment”) with Mr. Li, pursuant to which, on or prior to February 28, 2016, (i) the Company is committed to complete the listing of the Company into major capital markets, where the net proceeds raised through such public offering financing shall be at least $10,000,000; and (ii) failure to timely complete the above-mentioned criteria shall be deemed as a material breach of the Company under Article 8 of the Genius Acquisition Agreement, whereby the Selling Shareholder shall be entitled to revoke the exercised Put Option right set forth in Section 2.8 as if the Put Option had never been exercised. The right to revoke the Put Option has not been exercised as of reporting date.

F-17

The following table summarizes what the results of operations of the Company would have been on a pro forma basis for the three months ended March 31, 2016, if the Put Option has not been exercised on March 31, 2015. These results do not purport to represent what the results of operations for the Company would have actually been or to be indicative of the future results of operations of the Company.

Three Months Ended March 31, 2016 | ||||

| Net loss attributable to the noncontrolling interests | $ | (32,123 | ) | |

| Net loss attributable to parent’s shareholders | (641,793 | ) | ||

| Other comprehensive items | ||||

| Other comprehensive income attributable to parent's shareholders | 150,978 | |||

| Other comprehensive items attributable to noncontrolling interest | 160,574 | |||

| Comprehensive loss attributable to parent’s shareholders | (490,815 | ) | ||

| Comprehensive income attributable to noncontrolling interest | 128,451 | |||

On February 17, 2016, the Company and the selling shareholders of AHFL entered into a third Amendment to the Acquisition Agreement (the “Third Amendment”), pursuant to which, on or prior to June 30, 2016, (i) the Company is committed to complete the listing of the Company’s shares in a major capital market, where the net proceeds raised through such public offering financing shall be at least $10,000,000; (ii) the Company is committed to distribute the cash payment in the amount of NT$22.5 million (approximately $676,466), on a pro rata basis, to the selling shareholders of AHFL and issue 5 million common shares to its selected employees pursuant to its employee stock/option plan, or any alternative plan mutually accepted by the Company and such selling shareholders; and (iii) failure to timely complete either of the above-mentioned criteria shall be deemed as a material breach of the Company under Article 8 of the Acquisition Agreement, whereby the non-breaching party shall be entitled to terminate the Acquisition Agreement and unwind the Acquisition of AHFL by CUIS and restore the status quo of the Company and the Selling Shareholders as if the said acquisition had never happened. The Company is doing its best to achieve the targeted milestones as set forth in the third Amendment to the Acquisition Agreement. However, given the tight schedule and harsh general environment, despite every efforts of the Company, it might be really difficult for the Company to do so within the stipulated deadline. Therefore, the Company is actually negotiating with the Selling Shareholders of AHFL to convince them to give up such termination rights in case of failure to comply with the first and second requirements under Third Amendment within the stipulated deadline while continuously using its best efforts to fulfill such obligations.

NOTE 21 – DISCONTINUED OPERATION

In the fourth quarter of 2014, the shareholders of the Risk Management and Law Agent made the resolution to dissolve Risk Management and Law Agent, respectively, because those companies have not been in operation. The dissolution of Risk Management and Law Agent was approved by the Taiwan (R.O.C) Government on November 26, 2014 and on January 13, 2015, respectively. Abide by the law in Taiwan, the liquidator was appointed by the shareholders of the Risk Management and Law Agent and the liquidator shall complete the liquidation process no later than six months from the appointment date. Both Risk Management and Law Agent completed the process of liquidation in April 2016.

Risk Management and Law Agent were acquired by the Company together with their parent Company, Law Enterprise, on August 24, 2012. The Total Assets and Total Liabilities of Risk Management as of March 31, 2016 and December 31, 2015 are as follows:

As of March 31, 2016 | As of December 31, 2015 | |||||||

| Total Assets (including cash) | - | 224,140 | ||||||

| Total Liabilities | - | 4,834 | ||||||

The combined Revenue, Net Loss and EPS of Risk Management and Law Agent for the three months ended March 31, 2016 and 2015 are as follows:

Three Months Ended March 31, 2016 | Three Months Ended March 31, 2015 | |||||||

| Revenue | - | - | ||||||

| Net Income (Loss) | - | (2,362 | ) | |||||

| EPS | - | - | ||||||

NOTE 22 – FINANCIAL RISK MANAGEMENT AND FAIR VALUE

The Company has exposure to credit, liquidity and market risks which arise in the normal course of its business. This note presents information about the Company's exposure to each of these risks, the Company's objectives, policies and processes for measuring and managing risk, and the Company's management of capital. Further quantitative disclosures are included throughout these consolidated financial statements.

F-18

The Board of Directors (“BOD”) has overall responsibility for the establishment and oversight of the Company's risk management framework. The Company's risk management policies are established to identify and analyze the risks faced by the Company, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Company's activities. The Company, through its training and management standards and procedures, aims to develop a disciplined and constructive control environment in which all employees understand their roles and obligations.

The Company's BOD oversees how management monitors compliance with the Company's risk management policies and procedures and reviews the adequacy of the risk management framework in relation to the risks faced by the Company.

| (a) | Credit risk |

The Company's credit risk arises principally from accounts and other receivables, pledged deposits and cash and equivalents. Management has a credit policy in place and monitors exposures to these credit risks on an ongoing basis. The carrying amounts of trade and other receivables, pledged deposits and cash and cash equivalents represent the Company's maximum exposure to credit risks. Accounts receivable are due within 30 days from the date of billing.

| (b) | Liquidity risk |

The BOD of the Company is responsible for the overall cash management and raising borrowings to cover expected cash demands. The Company regularly monitors its liquidity requirements, to ensure it maintains sufficient reserves of cash and readily realizable marketable securities and adequate committed lines of funding from major financial institutions to meet its liquidity requirements in the short and longer term.

| (c) | Currency risk |

The functional currency for the subsidiaries in Taiwan is NT$ and the functional currency for the subsidiaries and VIEs in PRC is RMB. The financial statements of the Company are in USD. The fluctuation of NT$ and RMB will affect our operating results expressed in USD. The Company reviews its foreign currency exposures. The management does not consider its present foreign exchange risk to be significant.

NOTE 23 – GEOGRAPHICAL REVENUE

The geographical distribution of China United’s revenue for the three months ended March 31, 2016 and 2015 were as follows:

| Geographical Areas | Three months ended March 31, 2016 | Three months ended March 31, 2015 | ||||||

| PRC | $ | 1,585,767 | $ | 1,245,575 | ||||

| Taiwan | 7,976,529 | 8,610,540 | ||||||

| Total | $ | 9,562,296 | $ | 9,856,115 | ||||

NOTE 24 – LOAN TO SHAREHOLDERS

Anhou Registered Capital Increase

On April 27, 2013, China Insurance Regulatory Commission mandated any insurance agency have a minimum registered capital requirement of RMB50 million (approximately $ 8 million). At the time, Anhou, a professional insurance agency with a PRC nationwide license, had a registered capital of RMB10 million (approximately $ 1.6 million). To better implement its expansion strategies, Anhou intends to increase its registered capital to RMB50 million so that it can set up new branches in any province beyond its current operations in Mainland China.

F-19

Due to certain restriction on direct foreign investment in insurance agency business under current PRC legal requirements, Anhou sought investments from certain Investor Borrowers who in turn needed funds through individual loans.

On June 9, 2013, AHFL entered into a Loan Agreement with ZLI Holdings, whereby AHFL agreed to provide a loan to ZLI Holdings of RMB40 million ($6,389,925). The term for such loan is 10 years which may be extended upon the agreement of the parties. The loan was remitted to ZLI Holdings on August 30, 2013. In August 2013, ZLI Holdings entered into three loan agreements (“Investor Loan Agreements”) with the following independent third parties, collectively, the Investor Borrowers:

| 1. | Able Capital Holding Co., Ltd., a limited liability company established and registered in Hong Kong (RMB29,500,000 ($4,712,570)) |

| 2. | Mr. Li Chen, PRC citizen (RMB3,000,000 ($479,244)) |

| 3. | Ms. Jing Yue, PRC citizen (RMB7,500,000 ($1,198,111)) |

The term for the above loans is 10 years which may be extended upon the agreement of the parties. Pursuant to the Investor Loan Agreements, each of the Investor Borrowers entered into a binding VIE agreement with Anhou, the WFOE and certain existing shareholders of Anhou. The proceeds received from the said loans by the Investor Borrowers were solely used to increase the registered capital of Anhou. As of December 31, 2014 and 2013, the loan was offset against equity.

On October 20, 2013, the Investor Borrowers increased Anhou’s registered capital by RMB 40 million ($6,389,925).

NOTE 25 - SUBSEQUENT EVENTS

On April 15, 2016, the Company entered into a loan agreement (“Loan Agreement”) with Chinchiang Lin (“Mr. Lin”). Pursuant to the Loan Agreement, Mr. Lin provided a loan in the amount of $77,637 (NT$2.5 million) to the Company. The term for the Loan is from April 15, 2016 to December 31, 2016 with a fixed interest rate at 1.5% per annum and the principle and interest is due on December 31, 2016.

The Company has entered into a service agreement (“Service Agreement”) with Farglory Life Insurance Co., Ltd. (Farglory), pursuant to which AHFL provides consulting services to Farglory for NT$ 4,000,000 per year. The term for the Service Agreement is from May 1, 2016 to April 30, 2021.

The Company has evaluated all other subsequent events through the date these consolidated financial statements were issued, and determine that there were no other subsequent events or transactions that require recognition or disclosures in the consolidated financial statements.

F-20

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONS AND RESULTS OF OPERATIONS.

The following discussion of the results of operations and financial condition should be read in conjunction with our condensed consolidated financial statements and notes thereto included in Item 1 of this report. This report, including the information incorporated by reference, contains forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. The use of any of the words “believe,” “expect,” “anticipate,” “plan,” “estimate,” and similar expressions are intended to identify such statements. Forward-looking statements include statements concerning our possible or assumed future results. The actual results that we achieve may differ materially from those discussed in such forward-looking statements due to the risks and uncertainties described in the Risk Factors section of this report, in Management’s Discussion and Analysis of Financial Condition and Results of Operations, and in other sections of this report, as well as in our annual report on Form 10-K. We undertake no obligation to update any forward-looking statements.

Overview

We provide two broad categories of insurance products, life insurance products and property and casualty insurance products, in Taiwan and People’s Republic of China (“PRC”). The insurance products that the Company’s subsidiaries sell are underwritten by some of leading insurance companies in Taiwan and PRC, respectively.

| (1) | Life Insurance Products |

Total net revenues from Taiwan life insurance products were 74.81% and 81.17% of total net revenues for the three months ended March 31, 2016 and 2015, respectively. Total net revenues from PRC life insurance products were 15.21% and 11.81% of total net revenues for the three month ended March 31, 2016 and 2015, respectively.

In addition to the periodic premium payment schedules, most of the individual life insurance products we distribute also allow the insured to choose to make a single, lump-sum premium payment at the beginning of the policy term. If a periodic payment schedule is adopted by the insured, a life insurance policy can generate periodic payment of fixed premiums to the insurance company for a specified period of time. This means that once the Company sells a life insurance policy with a periodic premium payment schedule, they will be able to derive commission and fee income from that policy for an extended period of time, sometimes up to 25 years. Because of this feature and the expected sustained growth of life insurance sales in China and Taiwan, we have focused significant resources ever since the incorporation of Anhou and Law Broker on developing our capability to distribute individual life insurance products with periodic payment schedules. We expect that sales of life insurance products will continuously be our primary source of revenue in the next several years.

| (2) | Property and Casualty Insurance Products |

Taiwan subsidiary commenced sale of automobile insurance, casualty insurance and liability insurance business in August 2003. Total net revenues from Taiwan property and casualty insurance products were 8.09% and 6.19% of total net revenues for the three months ending March 31, 2016 and 2015, respectively. CAE commenced its sales of commercial property insurance in 2009 and developed its automobile insurance business in 2010. Total net revenues from PRC property and casualty insurance products were 1.89% and 0.83% of total net revenues for the three months ending March 31, 2016 and 2015, respectively.

Critical Accounting Policies and Estimates

A critical accounting policy is one that is both important to the portrayal of our financial condition and results of operation and requires our management’s most difficult, subjective or complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain. Our significant accounting policies are described in Note 2 of “Summary of Significant Accounting Policies” included within our 2015 Annual Report on Form 10-K filed with the Securities and Exchange Commission. Following is a discussion of the accounting policies that we believe involve the most difficult, subjective or complex judgments and estimates.

Accrued Expense

As part of the process of preparing our financial statements, we are required to estimate accrued expenses. The estimation basis of the majority of theaccrued expenses is dependent on our sales force’s achievement of the sales targets identified by our clients. Examples of estimated accrued expensesinclude brokerage commission bonus, such as bonus payable to our sales agents, and incentive program rewards, such as the estimated expenditures tofund the reward programs. We develop estimates of liabilities using our judgment based upon the facts and circumstances known at the time.

Long-term investment

The Company classifies its investments as available-for-sale in accordance with ASC 320 “Debt and Equity Securities”, Investments – Debt and EquitySecurities, and are reported at fair value. Unrealized gains and losses as a result of changes in the fair value of the available-for-sale investments arerecorded as a separate component within accumulated other comprehensive income in the accompanying consolidated balance sheets.

The Company uses the cost method of accounting for investments in companies that do not have a readily determinable fair value in which it holds aninterest of less than 20% and over which it does not have the ability to exercise significant influence. Investments are considered to be impaired when adecline in fair value is judged to be other-than-temporary. Once a decline in fair value is determined to be other-than-temporary, an impairment charge isrecorded and a new cost basis in the investment is established.

5

Recent Accounting Pronouncements

In May 2014, the FASB issued Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers (Topic 606). ASU 2014-09 outlines a single comprehensive model for entities to use in accounting for revenue arising from contracts with customers and supersedes current revenue recognition guidance. In August 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date. The amendment in this update defers the effective date of ASU 2014-09 for all entities by one year to annual periods beginning after December 15, 2017. Early adoption is permitted as of the original effective date, interim and annual reporting periods after December 15, 2016. Entities have the option of using either a full retrospective or a modified retrospective approach to adopt ASU 2014-09. The Company is still in the process of analyzing the effect of this new standard, including the transition method, to determine the impact on the Company's consolidated financial position, results of operations, cash flows, and related disclosures.

In September 2015, the FASB issued Accounting Standards Update No. 2015-16, "Simplifying the Accounting for Measurement-Period Adjustments". Measurement period adjustments are changes to provisional amounts recorded when the accounting for a business combination is incomplete as of the end of a reporting period. The measurement period can extend for up to a year following the transaction date. The new guidance requires companies to recognize these adjustments, including any related impacts to net income, in the reporting period in which the adjustments are determined. Companies are no longer required to retroactively apply measurement period adjustments to the prior period. This update is effective for annual and interim periods beginning after December 15, 2016. We have early adopted this standard beginning in fiscal 2016. There was no material impact to the Consolidated Financial Statements.

In November 2015, the FASB issued Accounting Standards Update No. 2015-17, "Balance Sheet Classification of Deferred Taxes". The new guidance requires that all deferred tax assets and liabilities, along with any related valuation allowance, be classified as noncurrent on the balance sheet. This update is effective for annual periods beginning after December 15, 2016 and interim periods within those annual periods. ASU 2015-17 will be effective for us, but will not cause a material impact on our financial condition or the results of our operations.