Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - Atlantic Alliance Partnership Corp. | f8k050516_atlanticalliance.htm |

| EX-99.2 - TRANSCRIPT OF CONFERENCE CALL, DATED MAY 5, 2016 - Atlantic Alliance Partnership Corp. | f8k050516ex99ii_atlanticall.htm |

| EX-99.1 - PRESS RELEASE - Atlantic Alliance Partnership Corp. | f8k050516ex99i_atlanticall.htm |

Exhibit 99.3

Atlantic Alliance Partnership Corp Investor Presentation May 2016

Disclaimer 2 Where You Can Find More Information This communication may be deemed to be solicitation material in respect of the proposed combination (the “Business Combinatio n”) of TLA Worldwide plc (“TLA”) and Atlantic Alliance Partnership Corp. (the “Company”), including the issuance of the Company’s ordinary shares in respect of the proposed Business Combination. In connection with the foregoing proposed Business Combination and issuance of the Company ’s ordinary shares, the Company expects to file a proxy statement on Schedule 14A with the Securities and Exchange Commission (the “SEC”) . T o the extent the Company effects the Business Combination as a court - sanctioned scheme of arrangement between TLA and TLA shareholders (the “Sche me”) under the UK Companies Act of 2006, as amended, the issuance of the Company’s ordinary shares in the Business Combination would not be expected to require registration under the Securities Act of 1933, as amended (the “Act”), pursuant to an exemption provided by Section 3(a) (10) under the Act. In the event that the Company determines to conduct an acquisition of TLA pursuant to an offer or otherwise in a manner that is not exempt from the registration requirements of the Act, it will file a registration statement with the SEC containing a prospectus with respect to the Company’s ordinary shares that would be issued in the acquisition. INVESTORS AND SECURITY HOLDERS OF THE COMPANY ARE URGED TO READ THESE MATERIALS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND ANY OTHER RELEVANT DOCUMENTS IN CONNECTION WITH THE BUSINESS COMBINATION THAT THE COMPANY WILL FILE WITH THE SEC WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE COMPANY, THE PROPOSED ISSUANCE OF THE COMPANY’S ORDINARY SHARES, AND THE PROPOSED BUSINESS COMBINATION. The preliminary proxy statement, the definitive proxy statement, and any registration statement/prospectus, in each case as applicable, and other relevant materials in connection with the proposed issuance of th e C ompany’s ordinary shares and the Business Combination (when they become available), and any other documents filed by the Company with the SEC, may be obtained free of charge at the SEC’s website at www.sec.gov. In addition, investors and security holders may obtain free copies of the do cuments filed with the SEC by contacting the Company in writing at 590 Madison Avenue, New York, NY 10022 . Participants in Solicitation The Company and its directors and executive officers may be deemed to be participants in the solicitation of proxies from the Co mpany’s ordinary shareholders with respect to the proposed Business Combination, including the proposed issuance of the Company’s ordinary sha res in respect of the proposed Business Combination. Information about the Company’s directors and executive officers and their ownership of the Co mpa ny’s ordinary shares is set forth in the Company’s Annual Report on Form 10 - K for the fiscal year ended December 31, 2015, which was filed wit h the SEC on March 23, 2016. Information regarding the identity of the potential participants, and their direct or indirect interests in t he solicitation, by security holdings or otherwise, will be set forth in the proxy statement and other materials to be filed with the SEC in connection wi th the proposed Business Combination and issuance of the Company’s ordinary shares in the proposed Business Combination. TLA is organized under the laws of England and Wales. Some of the officers and directors of TLA are residents of countries ot her than the United States. As a result, it may not be possible to sue TLA or such persons in a non - US court for violations of US securities laws. I t may be difficult to compel TLA and its respective affiliates to subject themselves to the jurisdiction and judgment of a US court or for investor s t o enforce against them the judgments of US courts.

Disclaimer (Continued) 3 Cautionary Note Regarding Forward - Looking Statements This presentation may include “forward - looking statements” within the meaning of the “safe harbor” provisions of the United Stat es Private Securities Litigation Reform Act of 1995. Forward - looking statements may be identified by the use of words such as “anticipates”, “believes ”, “continue”, “expects”, “estimates”, “intends”, “may”, “outlook”, “plans”, “potential”, “projects”, “predicts”, “should”, “will”, or, in e ach case, their negative or other variations or comparable terminology. Such forward - looking statements with respect to the timing of the proposed Business Combi nation, as well as the expected performance, strategies, prospects and other aspects of the businesses of the parties to the Scheme and the comb ine d company after completion of the proposed Business Combination, are based on current expectations that are subject to risks and uncertaintie s. A number of factors could cause actual results or outcomes to differ materially from those indicated by such forward - looking sta tements. These factors include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could give rise to the t erm ination of the Business Combination; (2) the outcome of any legal proceedings that may be instituted against the Company, TLA or others following an nou ncement of the Business Combination and the transactions contemplated therein; (3) the inability to complete the transactions contemplated b y t he Business Combination due to the failure to obtain approval of the shareholders of the Company or TLA or other conditions to closing in th e Business Combination; (4) the risk that the proposed transaction disrupts current plans and operations as a result of the announcement an d consummation of the Business Combination and the transactions described herein; (5) the ability to recognize the anticipated benefits of the Bus iness Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth prof ita bly, maintain relationships with customers and retain its key employees; (6) costs related to the proposed Business Combination; (7) change s i n applicable laws or regulations or their interpretation or application; (8) the possibility that the Company or TLA may be adversely affected by oth er economic, business, and/or competitive factors; (9) future exchange and interest rates; (10) delays in obtaining, adverse conditions contained in , o r the inability to obtain necessary regulatory approvals or complete regulatory reviews required to complete the Business Combination; and (11) other r isk s and uncertainties indicated in the proxy statement to be filed by the Company with the SEC, including those under “Risk Factors” therein, and o the r filings with the SEC by the Company. These factors are not intended to be an all - encompassing list of risks and uncertainties. Additional informatio n regarding these and other factors can be found in the Company’s reports filed with the SEC, including its Annual Report on Form 10 - K for the year en ded December 31, 2015. The forward - looking statements contained in this presentation are based on our current expectations and beliefs concerning futur e developments and their potential effects on us. Future developments affecting us may not be those that we have anticipated. These forward - looking statements involve a number of risks, uncertainties (some of which are beyond our control) and other assumptions that may cause actual results or per formance to be materially different from those expressed or implied by these forward - looking statements. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projec ted in these forward - looking statements. We undertake no obligation to update or revise any forward - looking statements, whether as a result of new i nformation, future events or otherwise, except as may be required under applicable securities laws.

Disclaimer (Continued) 4 By their nature, forward - looking statements involve risks and uncertainties because they relate to events and depend on circumstanc es that may or may not occur in the future. We caution you that forward - looking statements are not guarantees of future performance and that ou r actual results of operations, financial condition and liquidity, and developments in the industry in which we operate may differ materially fro m t hose made in or suggested by the forward - looking statements contained in this Report. In addition, even if our results or operations, financial condition and liquidity, and developments in the industry in which we operate are consistent with the forward - looking statements contained in this presen tation, those results or developments may not be indicative of results or developments in subsequent periods . Disclaimer This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall the re be any sale of securities in any jurisdiction in which the offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction.

Presenters 5 Bart Campbell Chairman and Co - founder Michael J. Principe CEO and Co - founder Jonathan Goodwin President and CEO Atlantic Alliance Partnership Corp.

Table of Contents 1. Introduction 7 2. Baseball Representation Overview 18 3. Sports Marketing Business Overview 26 A. Talent Marketing Business Overview 27 B. Events Business Overview 33 C. Consultancy Business Overview 37 4. Company Financials & Transaction Details 41 Appendix 48

1. Introduction

TLA Worldwide Business Overview 8 TLA is a fully integrated sports marketing and management agency, currently listed on the AIM market of the London Stock Exchange Owns and operates unique sporting events, provides sponsorship activation, sales, merchandising and media services to corporate clients and provides individual clients with “cradle to grave” representation . Offices in US (New York, Newport Beach, San Francisco, Houston and Charleston SC), UK (London, Largs ), Australia (Melbourne, Sydney, Adelaide and Perth) Over 880 clients and over 170 full - time personnel globally A cquired Australian based Elite Sports Properties (“ESP ”) in March 2015 for a maximum consideration of $19.5mm Sports Marketing 66% $29.3 Baseball Rep. 34% $15.1 Business Overview Business Mix and Service Offerings (FY 2015 Revenue, $ in mm) Talent Marketing Core Sports: NFL, Olympics , Golf, AFL, Cricket Events Event Creation and Ownership Event Management and Implementation Consultancy Sponsorship Leveraging, Activation and Negotiation Sports PR and Advisory Merchandise Licensing Management / Production Full Service Talent Management & Marketing Source: TLA Management and company filings.

TLA Worldwide Financial Overview 9 2015 Full Year Financial Highlights Total operating income grew 68% to $35.0 million (2014: $20.8 million) and organic operating income grew 22% (2014: 16%) Headline EBITDA increased 49% to $13.4 million (2014: $9.0 million) and organic Headline EBITDA grew 10 % (2014: 24%) Headline profit before tax increased 45.7% to $12.5 million (2014: $8.6 million) 2015 Full Year Operational Highlights Sports Marketing – Sports Marketing revenue grew 283% to $29.3 million (2014: $7.7 million), organic operating income was $11.6 million, growth of 51% – In July 2015, delivered the first International Champions Cup tournament in Australia with 225,000 spectators attending three soccer games at the Melbourne Cricket Ground featuring Manchester City, Real Madrid and AS Roma – Concluded a three - year extension with the State Government of Victoria to continue to host the Australian leg of the International Champions Cup until 2018, following the 2015 success Baseball Representation – Baseball Representation revenue up 15% to $15.1 million (2014: $13.2 million) – 22 baseball players were added to TLA’s client list in 2015 bringing the total baseball client list to 289 (2014: 267) – Major League Baseball (MLB) clients up 13%, 94 as of December 31, 2015 (2014: 83) – Signed Rookie of the Year Carlos Correa and number 2 MLB draft pick Alex Bregman – $ 174 million contracts negotiated in 2015 (2014: $194 million) Source: C ompany filings. Note: Operating Income is described as “gross profit” in the published accounts.

TLA Worldwide Overview 10 Baseball Representation Sports Marketing Consultancy Events Scott Kazmir George Springer Marcus Stroman Carlos Correa Talent Marketing DeMarco Murray Steve Young Kerri Walsh Jennings Jim Furyk

TLA Worldwide History 11 2012 2013 2014 2015 October 2012 Announced acquisition of Peter E. Greenberg and Associates Summer 2013 Launched Events and Consulting business June 2014 Secured event rights for International Champions Cup for Asia Pacific for 4 years, starting in 2015 March 2015 Acquired Elite Sports Properties , the Australian and UK based athlete management and sports marketing agency July 2015 Hosted ICC in Melbourne, featuring Real Madrid, AS Roma and Manchester City with over 225,000 fans attending July 2016 Second annual ICC in Melbourne featuring Juventus, Tottenham Hotspur and Atletico Madrid December 2011 TLA completed initial public offering on AIM with proceeds used to finance the acquisition of Legacy and Agency October 2014 Launched TLA Sales November 2014 Sold - out Rugby match between the New Zealand All Blacks and US Eagles played at Chicago’s Soldier Field Summer 2013 Launched TLA Media and TV r ights consultancy 2016 August 2016 NCAA College Football Season Opener in Sydney featuring University of California vs. University of Hawaii November 2016 All Blacks returning to Chicago’s Soldier Field vs. Ireland National Rugby Team

TLA Worldwide Global Presence 12 San Francisco Newport Beach Phoenix Houston Miami New York City Charleston Perth, AU Adelaide, AU Melbourne, AU Sydney , AU Maracay, VZ Largs , Scotland, UK London, UK Dominican Republic (1) (1) (1) Remote office.

TLA Worldwide Global Presence 12 San Francisco Newport Beach Phoenix Houston Miami New York City Charleston Perth, AU Adelaide, AU Melbourne, AU Sydney , AU Maracay, VZ Largs , Scotland, UK London, UK Dominican Republic (1) (1) (1) Remote office.

TLA Worldwide Global Presence 12 San Francisco Newport Beach Phoenix Houston Miami New York City Charleston Perth, AU Adelaide, AU Melbourne, AU Sydney , AU Maracay, VZ Largs , Scotland, UK London, UK Dominican Republic (1) (1) (1) Remote office.

TLA Is Poised to Capture Opportunity 13 Talent representation business provides clients with “cradle to grave” service from playing career through broadcast, coaching and other post - retirement positions – Expertise in MLB, PGA TOUR, NCAA coaching, on - air broadcasting, talent marketing, Olympics, Cricket and Australian Rules Football – across USA, UK and Australia Global Consulting business engages in brand and media consulting, venue sponsorship & in - stadium advertising, sponsorship leveraging and strategy, Sports PR and the development and activation of integrated marketing and media campaigns, events and merchandising programs TLA creates, develops and delivers unique events on a worldwide scale, for example: – All Blacks vs US Eagles rugby match, Chicago, November 2014 – International Champions Cup, Melbourne, July 2015 - 2018 – All Blacks vs Ireland rugby match, Chicago 2016 – University of California vs University of Hawaii NCAA Football Season Opener, Sydney 2016 TLA has a global presence with significant operations in the United States, Australia and the UK – Purchased Elite Sports Properties (ESP), a leading Australian Sports Marketing, Events and Management company in March of 2015, expanding the TLA global presence with six offices in Australia and the UK TLA has 880+ clients globally What TLA Provides TLA Capabilities Opportunities Strong Industry Relationships Range of Expertise Career Long Representation Successful Negotiation History Media Rights and Events Creation Scalable Platform Highly - Rated Management and Agents Global Presence Consulting Services

Why Sports are a Unique Opportunity 14 Sports Consumption has Grown Significantly 96% of its viewing was done live in 2013 95% of sports program viewing happened live in 4Q15 Hours of Sports Programming Available 49k 127k Collective Hours Viewed 31bn 22bn 160% 41% Sports are “DVR - Proof” Content 2005 2015 93% of the top 100 live viewed TV programs in 2015 were sports programing, vs 14% in 2005 North American Sports Advertising Spend on the Rise 6.5% 6.9% 7.2% 7.4% 8.3% 8.8% 9.4% 2011 2012 2013 2014 2015 2016 2017 In 2017, sports advertising will represent 9.4% of total advertising revenue 2005 2015 Sports Programs All Other Programs Source: Nielsen Year in Sports Media Report 2015, PwC Sports Outlook / October 2015, Disney ESPN Investor Day presentation 20 14, SNL Kagan.

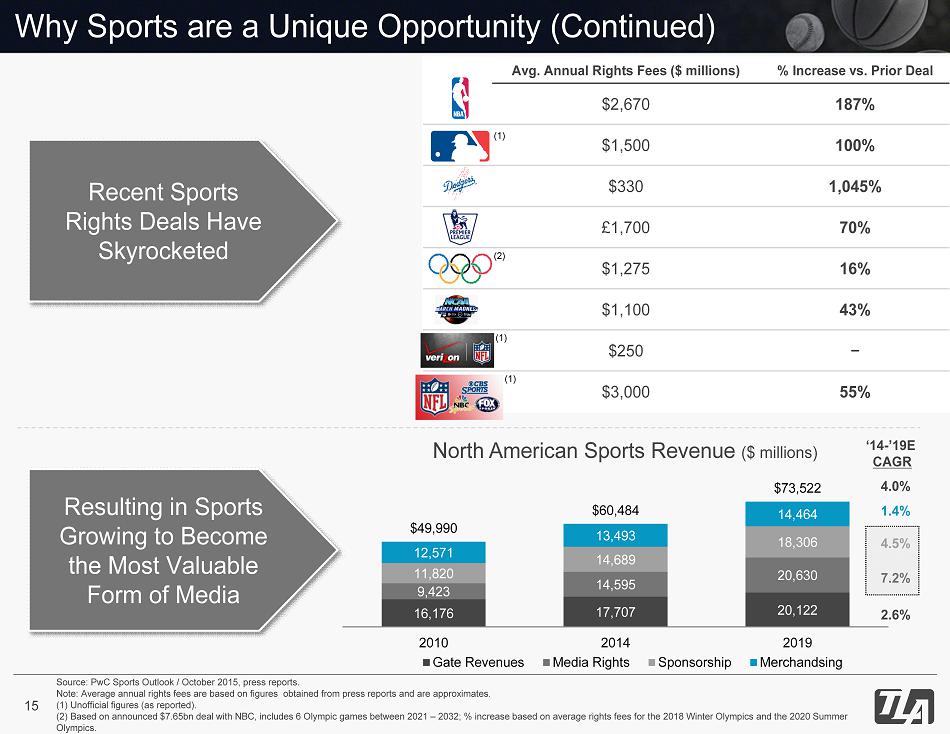

Why Sports are a Unique Opportunity (Continued) 15 Avg. Annual Rights Fees ($ millions) % Increase vs. Prior Deal $2,670 187% $1,500 100% $330 1,045% £1,700 70% $1,275 16% $1,100 43% $250 − $3,000 55% Recent Sports Rights Deals Have Skyrocketed 16,176 17,707 20,122 9,423 14,595 20,630 11,820 14,689 18,306 12,571 13,493 14,464 $49,990 $60,484 $73,522 2010 2014 2019 Resulting in Sports Growing to Become the Most Valuable Form of Media Gate Revenues Media Rights Sponsorship Merchandsing North American Sports Revenue ($ millions) ‘14 - ’19E CAGR 4.0% 1.4% 4.5% 7.2% 2.6% (2) Source: PwC Sports Outlook / October 2015, press reports. Note: Average annual rights fees are based on figures obtained from press reports and are approximates. ( 1) Unofficial figures (as reported). (2) Based on announced $ 7.65bn deal with NBC, includes 6 Olympic games between 2021 – 2032; % increase based on average rights fees for the 2018 Winter Olympic s and the 2020 Summer Olympics. (1) (1) (1)

Why a NASDAQ Listing Makes Sense 16 Source: NASDAQ and AIM. Note: Market data as of May 2, 2016 for NASDAQ and March 31, 2016 for AIM ; ADTV for Q1 2016. USA UK $, £ in millions (NASDAQ) (AIM) Financial Statistics Total Number of Listed Companies ~3,100 ~1,020 Median Market Capitalization $256 £18 Liquidity Statistics ADTV - Shares (mm) 2,114 1,415 ADTV - ($, £) 79,749 112 Dedicated Media Investor Base Small - Cap Knowledge Management Team Location Location of Majority of TLA Clients

Why Invest in TLA? 17 Strong Industry Fundamentals Recurring and Predictable Revenues Further Organic Growth Opportunities Attractive Financial Profile M&A Opportunities Best In - class Management Team and Agents NASDAQ More Aligned with Business

2. Baseball Representation Overview

Baseball Representation Overview 19 Michael Brantley Martin Prado Carl Crawford Francisco Liriano Carlos Correa A.J. Pollock Brett Anderson Wily Peralta Sports Marketing Baseball Representation Talent Marketing Consultancy Events

A Leading Major League Baseball Agency 20 A market leader, TLA represents baseball players in all aspects of their careers, both in their playing contract negotiations as well as their commercial endorsements TLA’s Baseball Representation business includes agents with a significant amount of experience in the field – 289 Baseball Clients – Expertise in representing LATAM baseball players – 94 MLB players as of FYE 2015 – 19 All Stars Added 14 new MLB clients in Q1 2016 via agent hires – 195 MiLB players – 67 All Stars Average age of TLA’s baseball clients: ~25 years old Average age of TLA’s MLB clients: ~27 years old Evan Gattis Andrew Susac Pedro Strop Mookie Betts Aaron Hill Angel Pagan Starling Marte Alcides Escobar Billy Butler Yasmani Grandal Melky Cabrera Carlos Correa Source: TLA Management and company filings. Note: Statistics as of FYE 2015 unless otherwise stated.

Strong Industry Fundamentals 21 $2.2 $2.7 $2.8 $3.5 $5.0 $6.5 $7.0 $9.0 2005 2008 2011 2014 ’05 – ’14 CAGR 6.7% Historical MLB Revenues and Player Pass - Through ($ billions) Guaranteed MLB Contracts Provides S tability to TLA 5.0% Source: www.forbes.com and www.baseballcube.com Note: Yearly revenue represents calendar year revenue. Amount Passed to Players Total MLB Revenue

Baseball Representation Lifecycle 22 MLB Player Career Lifecycle Investment Period Monetization Period The Draft Minor League Service Rookie Arbitration Free Agency Post Career • Broadcasting • Coaching • Endorsements 3 - 5 years 3 years 6 years TLA’s MLB player cycle is maturing into more revenue generating opportunities 64 83 94 2013 2014 2015 21.2% CAGR Source: C ompany filings. TLA MLB Player Clients

Baseball Representation Player Fee Schedule 23 • Players can be drafted at a young age, while still in high school • Agencies earn a percentage of any signing bonus negotiated Draft • A player’s Minor League service typically lasts 3 to 5 years • Due to low minor league salaries, TLA typically does not collect fees from its clients in the minors Potential 3 - 5 Years (Minor Leagues) • A player’s “Rookie” MLB service lasts 3 years • Compensation is determined by the club, but subject to a minimum salary • Agencies do not charge a fee on this contract, although they do earn a fee on negotiated amounts in excess of the minimum 0 - 2 Years (“Rookie”) • After the first three years in the MLB, a player is able to benchmark his salary against peers based on performance and tenure • The vast majority (~90 %) of players reach an agreement with their club before a binding arbitration hearing • Contracts are typically one year and agencies earn a fee on these contracts 3 - 5 Years (Arbitration Eligibility Rights) • After approximately six years in the MLB, if a player is coming out of contract with his club he can become a free agent • This is the most valuable period for a player as he can negotiate a contract with any MLB club and thereby maximize his earning potential 6 Years+ (“Free Agent”) • Other opportunities in broadcasting, coaching and endorsements offer the potential to extend the paying life of a player’s career • As a fully - integrated agency, TLA has the ability to capture additional revenues during this stage Post Career

Strong MLB Pipeline Featuring Young Major Leaguers 24 The Below Selected Rising Stars Are All Arbitration Eligible in the Next 12 - 24 Months GEORGE SPRINGER ● Right fielder on the Houston Astros ● MLB debut in April 2014 ● Former 1st - round draft pick & top prospect in Astros ● Rookie of the Month in his 1st month ● Astros’ rookie record with 10 HR in a month MARCUS STROMAN ● Pitcher on the Toronto Blue Jays ● MLB debut in May 2014 as a top Blue Jays prospect ● Former 1st - round draft pick ● Ace of Blue Jays rotation KEVIN GAUSMAN ● Pitcher on the Baltimore Orioles ● MLB debut in May 2013 as a top Orioles prospect ● Former 1st - round draft pick ● Projects as front - of - the - rotation starter ROBERTO OSUNA ● Pitcher on the Toronto Blue Jays ● MLB debut in April 2015 ● Signed by the Blue Jays at 16 years old ● Youngest pitcher in history to record an Opening Day Save CARLOS CORREA ● Shortstop on the Houston Astros ● MLB debut in June 2015 ● 2012 #1 overall draft pick by the Houston Astros ● Named 2015 American League Rookie of the Year MOOKIE BETTS ● Right fielder on the Boston Red Socks ● MLB debut in June 2014 ● At age 22, finished 19 th in American League MVP voting in 2015

MLB Agency Market 25 We believe that TLA has the opportunity to consolidate smaller agencies in MLB, as well as grow meaningfully in areas where it has established a beachhead (golf, NFL). Boutique / Single Agent Firms MLB Agency Market Share (Total Active Roster Clients as a % of Total MLB 40 Man Active Roster Players) 1,200 MLB Players on 40 Man Rosters ~9% Source: TLA Management estimates. Note: TLA Market share pie may not be to scale.

3. Sports Marketing Business Overview

A. Talent Marketing Business Overview

Talent Marketing Overview 28 Jim Furyk Steve Young Jameis Winston DeMarco Murray Sports Marketing Baseball Representation Talent Marketing Consultancy Events Kerri Walsh Jennings Dan Hicks Chris Hoy John Senden

Talent Management and Marketing 29 TLA is a leading talent management and marketing agency for the sports industry managing some of the biggest names in worldwide sports and media As their marketing representatives, TLA has experience working with high profile athletes and personalities across the world, both on and off the field including: – Baseball – American Football – Golf – Basketball – Olympics Sports Expertise includes: – Coaches – Sporting Legends – Media Personalities / Broadcasting – Cricket – Australian Rules Football Endorsements Personal Appearances Speaking Engagements Licensing Memorabilia Contract Negotiation Sponsorship Sales Literary Opportunities

Consistent Growth in Client Roster 30 474 259 380 440 474 801 884 FY 2011 FY 2012 FY 2013 FY 2014 March 2015 FY 2015 (1) (2) As of December 31, 2015, TLA had a total of 884 clients 327 Elite Sports Properties Source: TLA filings and press releases. (1) Includes baseball players to whom TLA represents talent marketing only. (2) Includes clients from acquisition of PEG in baseball only . 10% Organic Client Growth Since Acquisition

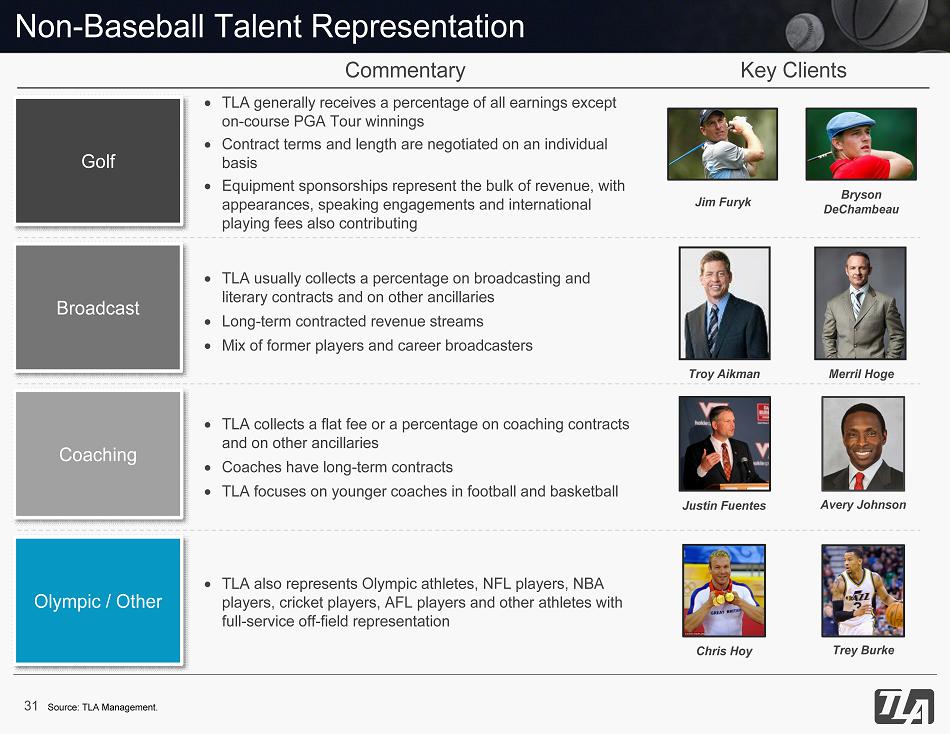

Non - Baseball Talent Representation 31 TLA generally receives a percentage of all earnings except on - course PGA Tour winnings Contract terms and length are negotiated on an individual basis Equipment sponsorships represent the bulk of revenue, with appearances, speaking engagements and international playing fees also contributing Golf Commentary Broadcast TLA usually collects a percentage on broadcasting and literary contracts and on other ancillaries Long - term contracted revenue streams Mix of former players and career broadcasters Coaching TLA collects a flat fee or a percentage on coaching contracts and on other ancillaries Coaches have long - term contracts TLA focuses on younger coaches in football and basketball Key Clients Olympic / Other TLA also represents Olympic athletes, NFL players, NBA players, cricket players, AFL players and other athletes with full - service off - field representation Jim Furyk Bryson DeChambeau Troy Aikman Justin Fuentes Avery Johnson Chris Hoy Trey Burke Merril Hoge Source: TLA M anagement.

Talent Marketing Rising Stars 32 Jameis Winston ● At Florida State, 2013 Heisman Trophy Winner and the 2013 AP Player of the Year, becoming the youngest player ever to do so ● 2014 BCS National Championship winner and MVP ● Selected 1st overall in 2015 NFL Draft by Tampa Bay Buccaneers and signed a 4 year, $25.35 million dollar deal, fully guaranteed ● Selected for the 2015 Pro Football Writers of America’s All - Rookie Team and the 2016 NFL Pro Bowl Bryson DeChambeau ● Won both NCAA Individual Championship and the U.S. Amateur title in 2015 ● Competed in his first major at the 2015 U.S. Open, then finished as the low amateur at the 2016 Masters, tied for 21 st place overall ● Finished 4th in his first tournament as a professional, the RBC Heritage in Hilton Head, SC in April 2016 ● In his first week since turning pro, signed endorsement deals with Puma and Bridgestone

B. Events Business Overview

Events Overview 34 International Rugby NCAAF in Australia International Champions Cup USA vs. Canada Hockey Professional Rugby Sports Marketing Baseball Representation Talent Marketing Consultancy Events

Events 35 TLA creates, develops and delivers unique events in the marketplace and manages large sporting events with an aim of driving annuity income and proprietary I.P.: Creation and Ownership Management and Implementation In addition to creating events that TLA has ownership, TLA also works with, and on behalf of, governing bodies, sporting organizations and corporate clients to create events and activations that extend beyond the boundaries of the sporting arena Provide complete event solutions through a range of services including event activation and management, tours and travel experiences, corporate hospitality, consumer promotions, staging, production and design – USA vs. Australia Rugby in Chicago, 2015 – Jeep Portsea Polo – the largest Polo event in Australia – International Champions Cup in Melbourne Australia, featuring some of the biggest teams in world football, 2015 - 2018 – Ice Hockey Series between USA and Canada across five cities in Australia, June 2015, 2016 – NCAA Football in Sydney, Australia, 2016 – New Zealand All Blacks in the United States at Soldier Field November 1 st , 2014 versus the US Eagles November 5 th , 2016 versus the Irish National Rugby Team

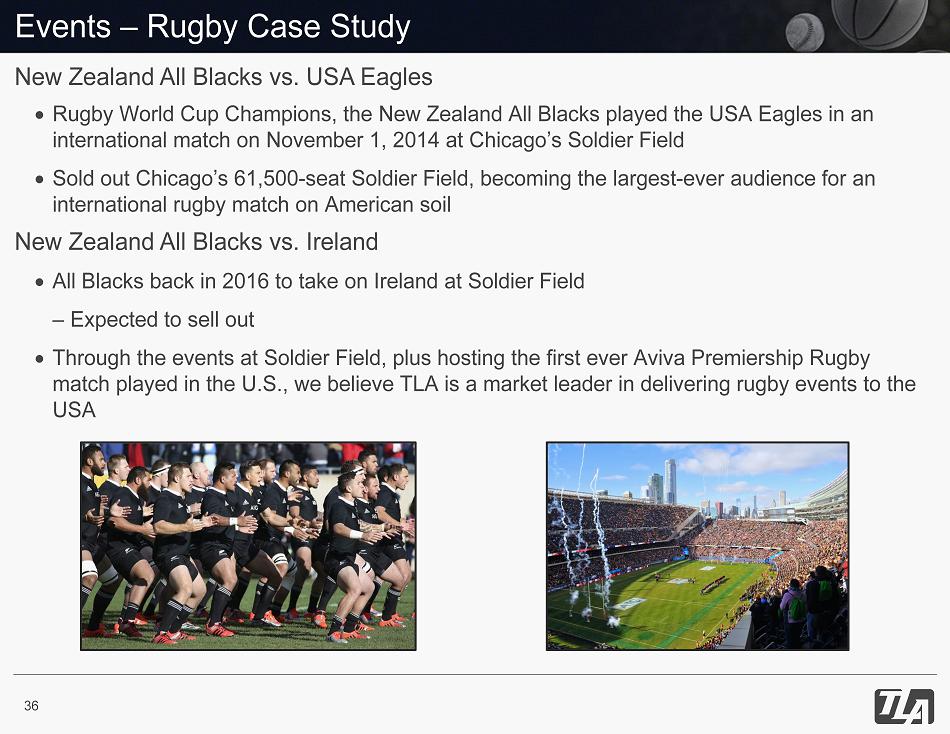

Events – Rugby Case Study 36 Rugby World Cup Champions, the New Zealand All Blacks played the USA Eagles in an international match on November 1, 2014 at Chicago’s Soldier Field Sold out Chicago’s 61,500 - seat Soldier Field, becoming the largest - ever audience for an international rugby match on American soil All Blacks back in 2016 to take on Ireland at Soldier Field – Expected to sell out Through the events at Soldier Field, plus hosting the first ever Aviva Premiership Rugby match played in the U.S., we believe TLA is a market leader in delivering rugby events to the USA New Zealand All Blacks vs. USA Eagles New Zealand All Blacks vs. Ireland

C. Consultancy Business Overview

Consultancy Overview 38 Sports Marketing Baseball Representation Talent Marketing Sponsorship Leveraging and Activation Sports Public Relations Sponsorship Negotiations and Sales Media Rights and Advisory Content and Digital Production Merchandise Events Consultancy

Consultancy Service Offerings 39 Competency TLA works for a number of the world’s leading brands leveraging and activating their sponsorships. TLA has worked on campaigns across some of the world’s largest sporting events Sponsorship Leveraging and Activation Description & Capabilities Sports Public Relations TLA is a leading Sports PR agency in Australia and has a strong presence in both the USA and the UK, with capabilities to implement comprehensive PR campaigns Sponsorship Negotiations and Sales TLA has expertise with team, venue and league negotiations, having negotiated in the USA and Australia on behalf of dozens of corporate marketers TLA represents teams within the following leagues to sell camera visible assets: Australia TLA is a sponsorship agency for: UK US Brings sports partnerships to life for: Australia Manages PR for sponsors, sports bodies and events: UK US Manages PR for 2 High Profile Olympic Legends: Implemented comprehensive PR Campaigns for: Recent Successes (1) Through commission on athlete endorsement deals. (1) (1) (1)

Consultancy Service Offerings (Continued) 40 Media Rights and Advisory Content and Digital Production Merchandise Competency Description & Capabilities Recent Successes TLA’s expertise includes advising teams, colleges, conferences and potential owners on media rights operators and opportunities, in addition to providing advice to ensure proper preparation for a constantly evolving landscape Clients include TLA’s Digital and Content team aim to provide our clients with a unique offering, using our extensive experience and knowledge of working in sport, and insights from our PR background Many of TLA’s clients have enlisted their services for content and digital production TLA’s Merchandise team are international specialists in the creation of licensed products, promotions and loyalty / membership programs TLA UK won the ‘Best Sports Licensed Property’ at the 2015 Licensing Awards for their master licensing program for the 2015 Rugby World Cup Clients include

4. Company Financials & Transaction Details

25,301 9,700 $13,793 $14,497 $17,972 $20,791 $35,001 2011 2012 2013 2014 2015 Total Operating Income (Ex-ESP) ESP Consolidated Financial Overview 42 $6,108 $6,566 $7,269 $9,021 $13,432 2011 2012 2013 2014 2015 TLA Has Nearly Doubled its Operating Income Since 2011 Operating Income (1) ($ in ‘000s) Headline EBITDA ($ in ‘000s) Note: Figures represent reported numbers by TLA and are not pro forma for acquisitions (except 2011 which are unaudited, pro forma numbers) . Operating Income is described as “gross profit” in the published accounts. Source: TLA filings and press releases. (1) Includes Unallocated / Corporate EBITDA. (2) Defined as Headline EBITDA divided by Operating Income. 44.3% 45.3% 40.4% 43.4% 38.4% % Margin (2) 26.2% ’11 - ’15 Reported CAGR % 21.8% ’11 - ’15 Reported CAGR % Represents ESP Results beginning March 15, 2015

Historical Segment Financial Overview 43 Baseball Representation 4,697 5,464 6,342 7,405 6,830 $8,785 $9,710 $13,081 $13,130 $13,755 2011 2012 2013 2014 2015 Headline EBITDA Operating Income Sports Marketing 2,711 2,525 2,532 4,565 9,842 $5,008 $4,787 $4,891 $7,661 $21,246 2011 2012 2013 2014 2015 Headline EBITDA Operating Income Market leading baseball agency with 289 clients as of FY 2015 Negotiated close to $1 billion in contracts, including many record setting deals (three $125 million+ deals ) • Leading independent representation across multiple business and sport lines • G rowing E vents & Consulting business Source: TLA filings and press releases Note : Figures represent reported numbers by TLA and are not pro forma for acquisitions. 2015 metrics only include ESP results beginning on March 15, 2015. (1) Operating Income is described as “gross profit” in the published accounts. 11.9% ’11 - ’15 Reported CAGR % 43.5% ’11 - ’15 Reported CAGR % 9.8% 38.0% (1) (1)

Public Comparables 44 Firm Value to EBITDA ’16E and ’17E 16.5x 14.6x 12.2x 8.7x 14.3x 12.3x 10.7x 7.9x FV / ’16E EBITDA FV / ’17E EBITDA Note: Market data as of 04/29/16 Source: Factset, Wall Street research and press reports (1) Based on a EV / EBIT Multiple. Precedent Transactions 13.0x 12.7x 11.9x 13.0x 10.0x 9.4x 10.2x Wanda / World Trathlon Chime / Providence Infront / Wanda IMG / WME & Silver Lake Provide Partners / Learfield World Sports Group / Lagardere Sportfive / Lagardere September 2013 August 2015 July 2015 February 2015 December 2013 May 2008 May 2008 (1) Target Buyer

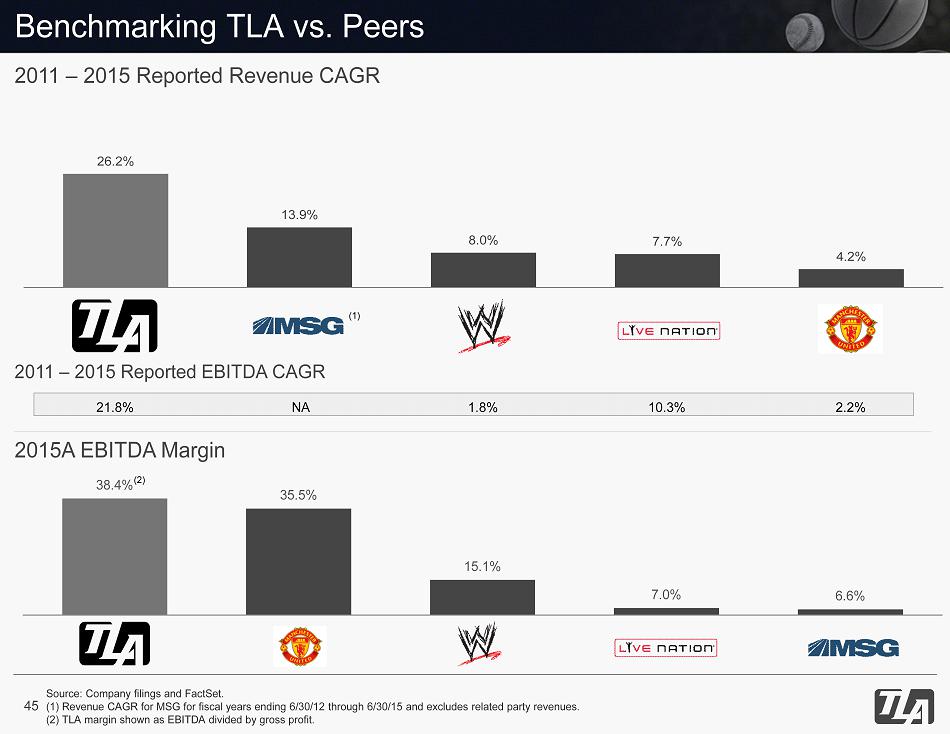

Benchmarking TLA vs. Peers 45 26.2% 13.9% 8.0% 7.7% 4.2% 2011 – 2015 Reported EBITDA CAGR 38.4% 35.5% 15.1% 7.0% 6.6% 2011 – 2015 Reported Revenue CAGR 2015A EBITDA Margin Source: Company filings and FactSet . (1) Revenue CAGR for MSG for fiscal years ending 6/30/12 through 6/30/15 and excludes related party revenues. (2) TLA margin shown as EBITDA divided by gross profit. ( 2 ) 21.8% NA 1.8% 10.3% 2.2% ( 1)

Overview of Offering and Transaction Rationale 46 Transaction Summary Atlantic Alliance Partnership Corp. (“AAPC”), a blank check company which raised $77 million in an Initial Public Offering in May of 2015, and TLA Worldwide plc (“TLA”) have agreed to an offer for TLA by AAPC subject to certain conditions The merged company will retain TLA’s name and will trade on the NASDAQ stock exchange AAPC and TLA anticipate closing the transaction in August 2016 Terms of the merger include: As part of the Proposed Offer, AAPC will offer TLA shareholders a partial cash alternative, in respect of some or all of their TLA shares, for up to $60 million in total (£41 million based on an exchange rate of £1 to $1.4633) at 61.5 pence per share in cash Implied Offer Price per Share (1) Consideration Exchange Ratio for Share Consideration Pro forma Firm Value 65 Pence ($0.95 (2) ) per TLA Share AAPC Shares and a partial c ash alternative 10 AAPC Shares per 107 TLA Shares $204 million (2) (1) Based on the weighted average AAPC Share price over the three month period ended on March 23, 2016 of US$10.18 and the UK pound to US dollar spot rate of 1.4633 as at 4:30 p.m. (London time) on April 29, 2016 . (2) Based on the UK pound to US dollar spot rate of 1.4633 as at 4:30 p.m. (London time) on April 29, 2016.

Illustrative Transaction Overview 47 Transaction Summary Sources AAPC Cash in Trust Used in Transaction $69.0 Rolled Equity: Founders 25.1 Rolled Equity: Agents 22.8 Rolled Equity: Other TLA Shareholders 32.8 Total Rolled Equity 80.7 Assumption of Deferred Consideration Liability 9.1 Assumption of Existing Net Debt 20.1 Amount Drawn Under New Senior Credit Facility - Excess Cash In Trust 11.8 Total Sources $190.7 Sources and Uses ($ in millions) Implied Firm Value (Numbers in millions, except Share Price) Uses Cash Purchase of TLA Shares from Selling Shareholders $60.0 Rolled Equity: Founders 25.1 Rolled Equity: Agents 22.8 Rolled Equity: Other TLA Shareholders 32.8 Total Rolled Equity 80.7 Assumption of Deferred Consideration Liability 9.1 Assumption of Existing Net Debt 20.1 Cash to Balance Sheet 11.8 Estimated Transaction Fees & Expenses 9.0 Total Uses $190.7 (2)( 3 ) Note: Exchange rate based on the UK pound to US dollar spot rate of 1.4633 as at 4:30 p.m. (London time) on April 29, 2016 . (1) Based on the weighted average AAPC Share price over the three month period ended on March 23 , 2016 of US$10.18 and the UK pound to US dollar spot rate of 1.4633 as at 4:30 p.m. (London time) on April 29, 2016 . (2) Assumes no redemptions . (3) Assumes $60 million participation in partial cash alternative shown for illustrative purposes. (4) (4) (4) (3) $10.18/sh Shares AAPC Founders Common Equity $27.5 2.7 TLA Founders Common Equity 25.1 2.5 TLA Agents Common Equity 22.8 2.2 Other TLA Shareholders 32.8 3.2 Other Common Equity 78.3 7.7 Market Value of Equity $186.5 18.3 Plus: Amount Drawn Under New Senior Credit Facility - Plus: Amount Outstanding Under Existing Credit Facility 22.8 Plus: Deferred Consideration Liability 9.1 Less: Cash & Equivelents (14.4) Firm Value $204.0 (4)( 5 ) (4)( 5 ) (2)( 3 ) (4) Deferred Consideration assumes the $1.6 million due in 2016 has been paid. (5) Net of 0.2 pence per share interim dividend (~$0.4 million) and 0.8 pence per share final dividend (~$ 1.7 million) payable to TLA shareholders on 1/8/2016 and 7/10/2016, respectively. (6) $24.5 million senior secured credit facility. (6) (6) Implied Offer Price per Share (1) Consideration Exchange Ratio for Share Consideration Pro forma Firm Value 65 Pence ($0.95) per TLA Share AAPC Shares and a partial c ash alternative 10 AAPC Shares per 107 TLA Shares $204 million

Appendix

Strong and Experienced Management Team 49 Former Group COO of CSM Sports & Entertainment, Chime Communications plc's sports division, and executive board member of Chime Communications plc. Former Group CEO of Essentially Group plc , a sports marketing and management business now owned by Chime Communications plc During his tenure as CEO of Essentially, Bart grew the business from 20 to 120 professionals with offices in London, Australia, South Africa, New Zealand, India and Japan Bart Campbell Chairman and Co - founder Former Managing Director of Blue Entertainment Sports Television (BEST), an industry leader in sports marketing, management and production Prior to joining BEST, Michael held various executive positions with SFX Sports Group Inc., including serving as a member of its executive committee and that of executive vice president and as general counsel Brings over 15 years of experience in sports and entertainment deal making, management, and operations Michael J. Principe CEO and Co - founder

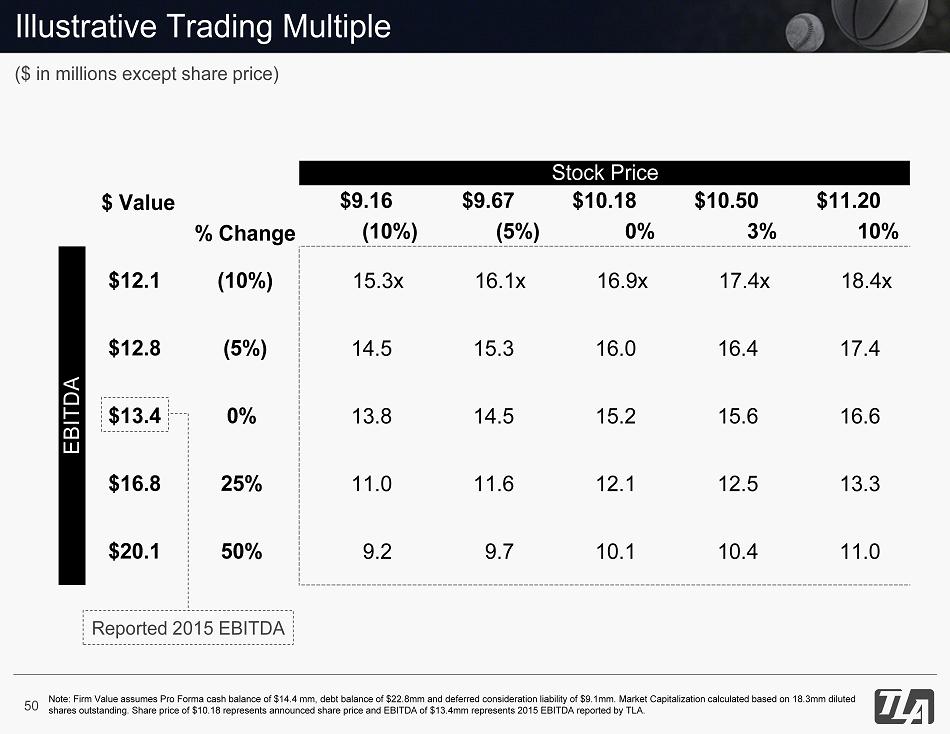

Illustrative Trading Multiple 50 Stock Price $ Value $9.16 $9.67 $10.18 $10.50 $11.20 % Change (10%) (5%) 0% 3% 10% $12.1 (10%) 15.3x 16.1x 16.9x 17.4x 18.4x $12.8 (5%) 14.5 15.3 16.0 16.4 17.4 $13.4 0% 13.8 14.5 15.2 15.6 16.6 $16.8 25% 11.0 11.6 12.1 12.5 13.3 $20.1 50% 9.2 9.7 10.1 10.4 11.0 EBITDA ($ in millions except share price) Note: Firm Value assumes Pro Forma cash balance of $14.4 mm, debt balance of $22.8mm and deferred consideration liability of $9. 1mm. Market Capitalization calculated based on 18.3mm diluted s hares outstanding. Share price of $10.18 represents announced share price and EBITDA of $13.4mm represents 2015 EBITDA report ed by TLA. Reported 2015 EBITDA

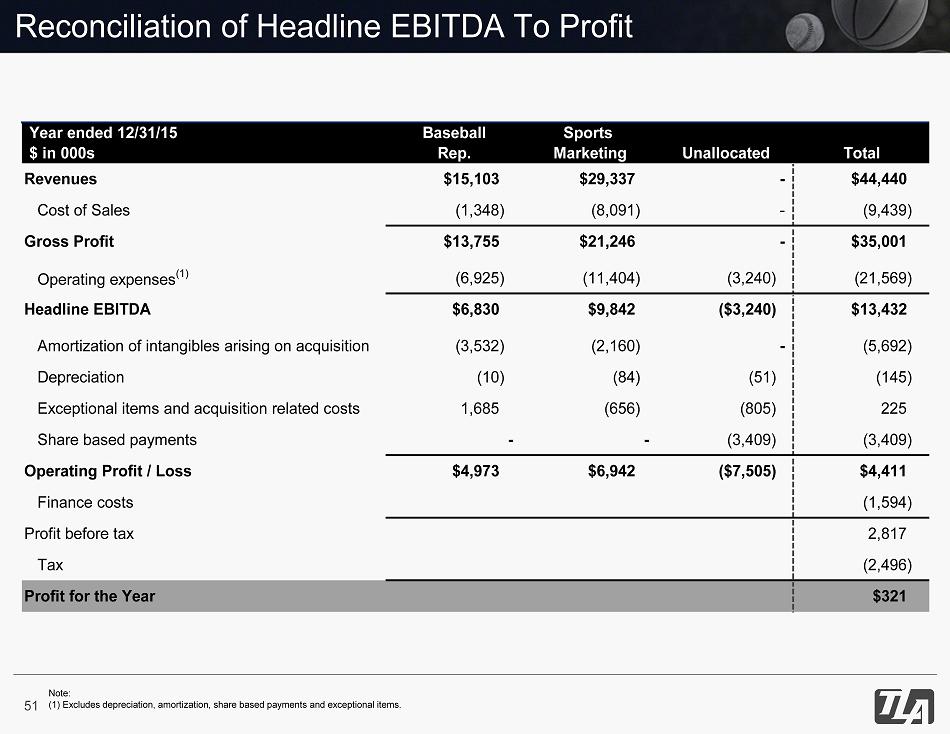

Reconciliation of Headline EBITDA To Profit 51 Year ended 12/31/15 Baseball Sports $ in 000s Rep. Marketing Unallocated Total Revenues $15,103 $29,337 - $44,440 Cost of Sales (1,348) (8,091) - (9,439) Gross Profit $13,755 $21,246 - $35,001 Operating expenses (1) (6,925) (11,404) (3,240) (21,569) Headline EBITDA $6,830 $9,842 ($3,240) $13,432 Amortization of intangibles arising on acquisition (3,532) (2,160) - (5,692) Depreciation (10) (84) (51) (145) Exceptional items and acquisition related costs 1,685 (656) (805) 225 Share based payments - - (3,409) (3,409) Operating Profit / Loss $4,973 $6,942 ($7,505) $4,411 Finance costs (1,594) Profit before tax 2,817 Tax (2,496) Profit for the Year $321 Note: ( 1) Excludes depreciation, amortization, share based payments and exceptional items.