Attached files

| file | filename |

|---|---|

| 8-K - 8-K - MEDICAL PROPERTIES TRUST INC | d172139d8k.htm |

| EX-99.1 - EX-99.1 - MEDICAL PROPERTIES TRUST INC | d172139dex991.htm |

Table of Contents

Exhibit 99.2

FIRST QUARTER 2016

Supplemental Information

Table of Contents

MEDICALPROPERTIESTRUST.COM

FORWARD-LOOKING STATEMENT Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results of the Company or future events to differ materially from those expressed in or underlying such forward-looking statements, including without limitation: Normalized FFO per share; expected payout ratio, the amount of acquisitions of healthcare real estate, if any; estimated debt metrics, portfolio diversification, capital markets conditions, the repayment of debt arrangements; statements concerning the additional income to the Company as a result of ownership interests in certain hospital operations and the timing of such income; the payment of future dividends, if any; completion of additional debt arrangement, and additional investments; national and international economic, business, real estate and other market conditions; the competitive environment in which the Company operates; the execution of the Company’s business plan; financing risks; the Company’s ability to maintain its status as a REIT for federal income tax purposes; acquisition and development risks; potential environmental and other liabilities; and other factors affecting the real estate industry generally or healthcare real estate in particular. For further discussion of the factors that could affect outcomes, please refer to the “Risk Factors” section of the Company’s Annual Report on Form 10-K for the year ended December 31, 2015, and as updated by the Company’s subsequently filed Quarterly Reports on Form 10-Q and other SEC filings. Except as otherwise required by the federal securities laws, the Company undertakes no obligation to update the information in this report.

On the Cover: Clinica La Vialarda - Biella, Italy. Acquired in 2015.

| Q1 2016 | SUPPLEMENTAL INFORMATION 2 |

Table of Contents

MEDICALPROPERTIESTRUST.COM

OFFICERS

| Edward K. Aldag, Jr. | Chairman, President and Chief Executive Officer | |

| R. Steven Hamner | Executive Vice President and Chief Financial Officer | |

| Emmett E. McLean | Executive Vice President, Chief Operating Officer, Treasurer and Secretary | |

| Frank R. Williams, Jr. | Senior Vice President, Senior Managing Director - Acquisitions | |

| J. Kevin Hanna | Vice President, Controller and Chief Accounting Officer | |

BOARD OF DIRECTORS

| Edward K. Aldag, Jr. |

From Left: J. Kevin Hanna, Emmett E. McLean, Edward K. Aldag, Jr., R. Steven Hamner, and Frank R. Williams, Jr. | |||

|

G. Steven Dawson |

||||

|

R. Steven Hamner |

||||

|

Robert. E. Holmes, Ph.D. |

||||

|

Sherry A. Kellett |

||||

|

William G. McKenzie |

||||

|

D. Paul Sparks, Jr.

|

||||

|

CORPORATE HEADQUARTERS |

||||

|

Medical Properties Trust, Inc. |

||||

|

1000 Urban Center Drive, Suite 501 |

||||

|

Birmingham, AL 35242 |

||||

|

(205) 969-3755 |

||||

|

(205) 969-3756 (fax)

www.medicalpropertiestrust.com |

| Q1 2016 | SUPPLEMENTAL INFORMATION 3 |

Table of Contents

MEDICALPROPERTIESTRUST.COM

COMPANY OVERVIEW (continued)

| INVESTOR RELATIONS

Tim Berryman | Director - Investor Relations (205) 397-8589 tberryman@medicalpropertiestrust.com |

|

CAPITAL MARKETS

Charles Lambert | Managing Director - Capital Markets (205) 397-8897 clambert@medicalpropertiestrust.com | ||||

|

|

| |||||

| TRANSFER AGENT | STOCK EXCHANGE | SENIOR UNSECURED | ||||

| American Stock Transfer | LISTING AND | DEBT RATINGS | ||||

| and Trust Company | TRADING SYMBOL | Moody’s – Ba1 | ||||

| 6201 15th Avenue | New York Stock Exchange | Standard & Poor’s – BBB- | ||||

| Brooklyn, NY 11219 | (NYSE): MPW | |||||

Q1 2016 | SUPPLEMENTAL INFORMATION 4

Table of Contents

MEDICALPROPERTIESTRUST.COM

RECONCILIATION OF NET INCOME TO FUNDS FROM OPERATIONS

(Unaudited)

(Amounts in thousands except per share data)

| For the Three Months Ended | ||||||||

| March 31, 2016 |

March 31, 2015 |

|||||||

| FFO INFORMATION: |

||||||||

| Net income attributable to MPT common stockholders |

$ | 57,927 | $ | 35,897 | ||||

| Participating securities’ share in earnings |

(144 | ) | (266 | ) | ||||

|

|

|

|

|

|||||

| Net income, less participating securities’ share in earnings |

$ | 57,783 | $ | 35,631 | ||||

| Depreciation and amortization(A) |

21,472 | 14,756 | ||||||

| Gain on sale of real estate |

(40 | ) | — | |||||

|

|

|

|

|

|||||

| Funds from operations |

$ | 79,215 | $ | 50,387 | ||||

| Unutilized financing fees / debt refinancing costs |

4 | 238 | ||||||

| Acquisition expenses(A) |

4,233 | 6,239 | ||||||

|

|

|

|

|

|||||

| Normalized funds from operations |

$ | 83,452 | $ | 56,864 | ||||

| Share-based compensation |

1,695 | 2,603 | ||||||

| Debt costs amortization |

1,835 | 1,377 | ||||||

| Additional rent received in advance(B) |

(300 | ) | (300 | ) | ||||

| Straight-line rent revenue and other |

(10,829 | ) | (6,332 | ) | ||||

|

|

|

|

|

|||||

| Adjusted funds from operations |

$ | 75,853 | $ | 54,212 | ||||

|

|

|

|

|

|||||

| PER DILUTED SHARE DATA: |

||||||||

| Net income, less participating securities’ share in earnings |

$ | 0.24 | $ | 0.17 | ||||

| Depreciation and amortization(A) |

0.09 | 0.08 | ||||||

| Gain on sale of real estate |

— | — | ||||||

|

|

|

|

|

|||||

| Funds from operations |

$ | 0.33 | $ | 0.25 | ||||

| Unutilized financing fees / debt refinancing costs |

— | — | ||||||

| Acquisition expenses(A) |

0.02 | 0.03 | ||||||

|

|

|

|

|

|||||

| Normalized funds from operations |

$ | 0.35 | $ | 0.28 | ||||

| Share-based compensation |

0.01 | 0.01 | ||||||

| Debt costs amortization |

0.01 | 0.01 | ||||||

| Additional rent received in advance(B) |

— | — | ||||||

| Straight-line rent revenue and other |

(0.05 | ) | (0.03 | ) | ||||

|

|

|

|

|

|||||

| Adjusted funds from operations |

$ | 0.32 | $ | 0.27 | ||||

|

|

|

|

|

|||||

| (A) | For the first quarter of 2016, we included $0.3 million and $5.3 million of our share of real estate depreciation and acquisition expenses, respectively, from unconsolidated joint ventures. These amounts are included with the activity of all of our equity interests in the “Interest and other expenses, net” line on the consolidated statements of income. |

| (B) | Represents additional rent received from one tenant in advance of when we can recognize as revenue for accounting purposes. This additional rent is being recorded to revenue on a straight-line basis over the lease life. |

Investors and analysts following the real estate industry utilize funds from operations, or FFO, as a supplemental performance measure. FFO, reflecting the assumption that real estate asset values rise or fall with market conditions, principally adjusts for the effects of GAAP depreciation and amortization of real estate assets, which assumes that the value of real estate diminishes predictably over time. We compute FFO in accordance with the definition provided by the National Association of Real Estate Investment Trusts, or NAREIT, which represents net income (loss) (computed in accordance with GAAP), excluding gains (losses) on sales of real estate and impairment charges on real estate assets, plus real estate depreciation and amortization and after adjustments for unconsolidated partnerships and joint ventures.

In addition to presenting FFO in accordance with the NAREIT definition, we also disclose normalized FFO, which adjusts FFO for items that relate to unanticipated or non-core events or activities or accounting changes that, if not noted, would make comparison to prior period results and market expectations less meaningful to investors and analysts. We believe that the use of FFO, combined with the required GAAP presentations, improves the understanding of our operating results among investors and the use of normalized FFO makes comparisons of our operating results with prior periods and other companies more meaningful. While FFO and normalized FFO are relevant and widely used supplemental measures of operating and financial performance of REITs, they should not be viewed as a substitute measure of our operating performance since the measures do not reflect either depreciation and amortization costs or the level of capital expenditures and leasing costs necessary to maintain the operating performance of our properties, which can be significant economic costs that could materially impact our results of operations. FFO and normalized FFO should not be considered an alternative to net income (loss) (computed in accordance with GAAP) as indicators of our financial performance or to cash flow from operating activities (computed in accordance with GAAP) as an indicator of our liquidity.

We calculate adjusted funds from operations, or AFFO, by subtracting from or adding to normalized FFO (i) unbilled rent revenue, (ii) non-cash share-based compensation expense, and (iii) amortization of deferred financing costs. AFFO is an operating measurement that we use to analyze our results of operations based on the receipt, rather than the accrual, of our rental revenue and on certain other adjustments. We believe that this is an important measurement because our leases generally have significant contractual escalations of base rents and therefore result in recognition of rental income that is not collected until future periods, and costs that are deferred or are non-cash charges. Our calculation of AFFO may not be comparable to AFFO or similarly titled measures reported by other REITs. AFFO should not be considered as an alternative to net income (calculated pursuant to GAAP) as an indicator of our results of operations or to cash flow from operating activities (calculated pursuant to GAAP) as an indicator of our liquidity.

| Q1 2016 | SUPPLEMENTAL INFORMATION 5 |

Table of Contents

MEDICALPROPERTIESTRUST.COM

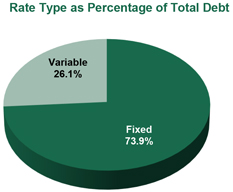

FINANCIAL INFORMATION

(as of March 31, 2016)

($ amounts in thousands)

| Debt Instrument |

Rate Type |

Rate | Balance | |||||||

| 2016 Unsecured Notes |

Fixed | 5.59 | %(A) | $ | 125,000 | |||||

| Northland – Mortgage Capital Term Loan |

Fixed | 6.20 | % | 13,326 | ||||||

| 2018 Credit Facility Revolver |

Variable | 1.84 | %(B) | 645,000 | ||||||

| 2019 Term Loan |

Variable | 2.09 | % | 250,000 | ||||||

| 5.75% Notes Due 2020 (Euro)(C) |

Fixed | 5.75 | % | 227,600 | ||||||

| 6.875% Notes Due 2021 |

Fixed | 6.88 | % | 450,000 | ||||||

| 4.00% Notes Due 2022 (Euro)(C) |

Fixed | 4.00 | % | 569,000 | ||||||

| 6.375% Notes Due 2022 |

Fixed | 6.38 | % | 350,000 | ||||||

| 6.375% Notes Due 2024 |

Fixed | 6.38 | % | 500,000 | ||||||

| 5.50% Notes Due 2024 |

Fixed | 5.50 | % | 300,000 | ||||||

|

|

|

|||||||||

| $ | 3,429,926 | |||||||||

| Debt premium |

2,079 | |||||||||

| Debt issuance costs |

(35,401 | ) | ||||||||

|

|

|

|

|

|||||||

| Weighted average rate |

4.74 | % | $ | 3,396,604 | ||||||

|

|

|

|

|

|||||||

| (A) | Represents the weighted-average rate for four tranches of the Notes at March 31, 2016, factoring in interest rate swaps in effect at that time. The Company has entered into two swap agreements which began in July and October 2011. Effective July 31, 2011, the Company is paying 5.507% on $65 million of the Notes and effective October 31, 2011, the Company is paying 5.675% on $60 million of Notes. |

| (B) | At March 31, 2016, this represents a $1.3 billion unsecured revolving credit facility with spreads over LIBOR ranging from 0.95% to 1.75%. |

| (C) | Represents 700 million of bonds issued in Euros and converted to U.S. dollars at March 31, 2016. |

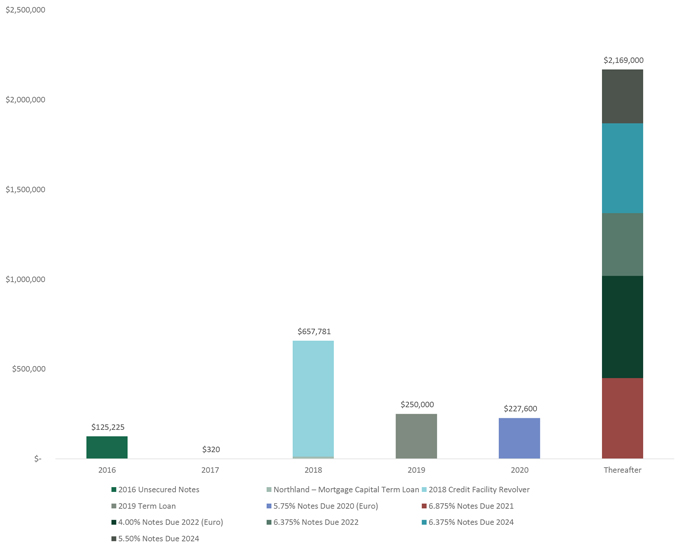

Q1 2016 | SUPPLEMENTAL INFORMATION 6

Table of Contents

MEDICALPROPERTIESTRUST.COM

FINANCIAL INFORMATION

(as of March 31, 2016)

($ amounts in thousands)

| Debt Instrument |

2016 | 2017 | 2018 | 2019 | 2020 | Thereafter | ||||||||||||||||||

| 2016 Unsecured Notes |

$ | 125,000 | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||

| Northland – Mortgage Capital Term Loan |

225 | 320 | 12,781 | — | — | — | ||||||||||||||||||

| 2018 Credit Facility Revolver |

— | — | 645,000 | — | — | — | ||||||||||||||||||

| 2019 Term Loan |

— | — | — | 250,000 | — | — | ||||||||||||||||||

| 5.75% Notes Due 2020 (Euro) |

— | — | — | — | 227,600 | — | ||||||||||||||||||

| 6.875% Notes Due 2021 |

— | — | — | — | — | 450,000 | ||||||||||||||||||

| 4.00% Notes Due 2022 (Euro) |

— | — | — | — | — | 569,000 | ||||||||||||||||||

| 6.375% Notes Due 2022 |

— | — | — | — | — | 350,000 | ||||||||||||||||||

| 6.375% Notes Due 2024 |

— | — | — | — | — | 500,000 | ||||||||||||||||||

| 5.50% Notes Due 2024 |

— | — | — | — | — | 300,000 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| $ | 125,225 | $ | 320 | $ | 657,781 | $ | 250,000 | $ | 227,600 | $ | 2,169,000 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Q1 2016 | SUPPLEMENTAL INFORMATION 7

Table of Contents

MEDICALPROPERTIESTRUST.COM

FINANCIAL INFORMATION

PRO FORMA NET DEBT / ANNUALIZED EBITDA

(Unaudited)

(Amounts in thousands)

| For the Three Months Ended | ||||

| March 31, 2016 | ||||

| Net income attributable to MPT common stockholders |

$ | 57,927 | ||

| Pro forma adjustments for capital transactions, acquisitions / dispositions that occurred after the period (A) |

(10,563 | ) | ||

|

|

|

|||

| Pro forma net income |

$ | 47,364 | ||

| Add back: |

||||

| Interest Expense |

39,369 | |||

| Debt refinancing costs |

4 | |||

| Depreciation and amortization |

22,025 | |||

| Stock-based compensation |

1,695 | |||

| Mid-quarter acquisitions |

— | |||

| Mid-quarter development openings and investments |

668 | |||

| Estimated earnings from CIP funding |

1,654 | |||

| Gain on real estate dispositions |

(40 | ) | ||

| Acquisition expenses |

4,233 | |||

| Income tax expense |

319 | |||

|

|

|

|||

| 1Q 2016 Pro forma EBITDA |

$ | 117,291 | ||

|

|

|

|||

| Annualization |

$ | 469,164 | ||

|

|

|

|||

| Total debt |

$ | 3,396,604 | ||

| Pro forma changes to debt balance after March 31, 2016 (A) |

(550,000 | ) | ||

| Cash |

(206,410 | ) | ||

|

|

|

|||

| Net debt |

$ | 2,640,194 | ||

|

|

|

|||

| Net debt / pro forma annualized EBITDA |

5.6x | |||

| (A) | Reflects impact from previously disclosed Capella transactions. |

Q1 2016 | SUPPLEMENTAL INFORMATION 8

Table of Contents

MEDICALPROPERTIESTRUST.COM

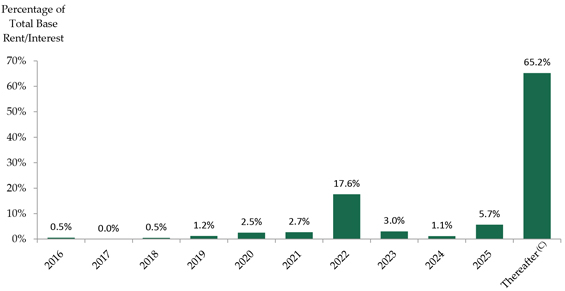

LEASE AND MORTGAGE LOAN MATURITY SCHEDULE

(as of March 31, 2016)

($ amounts in thousands)

| Years of Maturities (A) |

Total Leases/Loans | Base Rent/Interest (B) | Percent of Total Base Rent/Interest |

|||||||||

| 2016 |

1 | $ | 2,250 | 0.5 | % | |||||||

| 2017 |

— | — | 0.0 | % | ||||||||

| 2018 |

1 | 2,007 | 0.5 | % | ||||||||

| 2019 |

2 | 5,017 | 1.2 | % | ||||||||

| 2020 |

5 | 10,640 | 2.5 | % | ||||||||

| 2021 |

2 | 11,341 | 2.7 | % | ||||||||

| 2022 |

15 | 73,550 | 17.6 | % | ||||||||

| 2023 |

4 | 12,599 | 3.0 | % | ||||||||

| 2024 |

2 | 4,782 | 1.1 | % | ||||||||

| 2025 |

8 | 23,682 | 5.7 | % | ||||||||

| Thereafter (C) |

147 | 272,622 | 65.2 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| 187 | $ | 418,490 | 100.0 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| (A) | Excludes 8 of our properties that are under development. Lease/Loan expiration is based on the fixed term of the lease/loan and does not factor in potential renewal options provided for in our agreements. |

| (B) | Represents base rent/interest income on an annualized basis but does not include tenant recoveries, additional rents and other lease-related adjustments to revenue (i.e., straight-line rents and deferred revenues). |

| (C) | Excludes two Capella mortgage loans that were paid in full as of April 30, 2016. |

Q1 2016 | SUPPLEMENTAL INFORMATION 9

Table of Contents

MEDICALPROPERTIESTRUST.COM

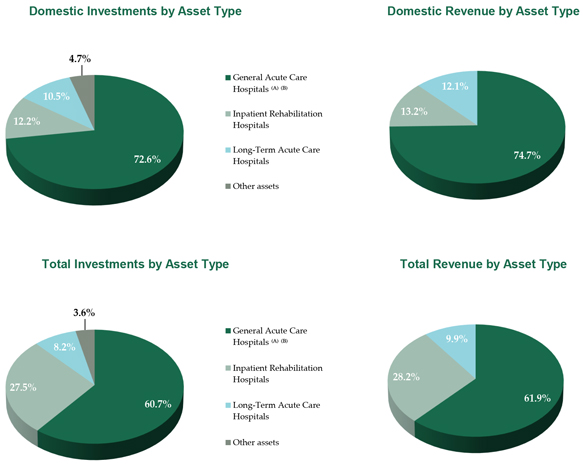

PORTFOLIO INFORMATION

INVESTMENTS AND REVENUE BY ASSET TYPE

(March 31, 2016)

($ amounts in thousands)

| Asset Types |

Total Gross Assets |

Percentage of Gross Assets |

Total Revenue |

Percentage of Total Revenue |

||||||||||||

| General Acute Care Hospitals(A)(B) |

$ | 3,437,832 | 60.7 | % | $ | 83,510 | 61.9 | % | ||||||||

| Inpatient Rehabilitation Hospitals |

1,555,102 | 27.5 | % | 38,123 | 28.2 | % | ||||||||||

| Long-Term Acute Care Hospitals |

462,794 | 8.2 | % | 13,366 | 9.9 | % | ||||||||||

| Other assets |

207,102 | 3.6 | % | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 5,662,830 | (C) | 100.0 | % | $ | 134,999 | 100.0 | % | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (A) | Includes three medical office buildings. |

| (B) | Represents the repayment of mortgage and acquisition loans, along with the sale of our equity interest in Capella as of April 30, 2016; however, it includes two new loans totaling $143 million that were issued as part of the same transaction. |

| (C) | Represents investment concentration as a percentage of gross real estate assets, other loans, and equity investments assuming all real estate commitments are fully funded. |

Q1 2016 | SUPPLEMENTAL INFORMATION 10

Table of Contents

MEDICALPROPERTIESTRUST.COM

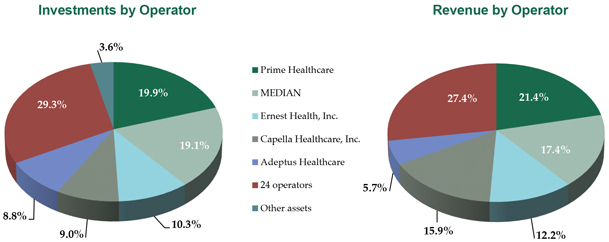

PORTFOLIO INFORMATION

INVESTMENTS AND REVENUE BY OPERATOR

(March 31, 2016)

($ amounts in thousands)

| Operators |

Total Gross Assets |

Percentage of Gross Assets |

Total Revenue |

Percentage of Total Revenue |

||||||||||||

| Prime Healthcare |

$ | 1,125,994 | 19.9 | % | $ | 28,897 | 21.4 | % | ||||||||

| MEDIAN |

1,080,381 | 19.1 | % | 23,510 | 17.4 | % | ||||||||||

| Ernest Health, Inc. |

581,087 | 10.3 | % | 16,406 | 12.2 | % | ||||||||||

| Capella Healthcare, Inc. |

510,895 | (A) | 9.0 | % | 21,477 | 15.9 | % | |||||||||

| Adeptus Healthcare |

500,000 | 8.8 | % | 7,676 | 5.7 | % | ||||||||||

| 24 operators |

1,657,371 | 29.3 | % | 37,033 | 27.4 | % | ||||||||||

| Other assets |

207,102 | 3.6 | % | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 5,662,830 | (B) | 100.0 | % | $ | 134,999 | 100.0 | % | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (A) | Reflects the repayment of mortgage and acquisition loans, along with the sale of our equity interest in Capella on April 30, 2016; however, it includes two new loans totaling $143 million that were issued as part of the same transaction. |

| (B) | Represents investment concentration as a percentage of gross real estate assets, other loans, and equity investments assuming all real estate commitments are fully funded. |

Q1 2016 | SUPPLEMENTAL INFORMATION 11

Table of Contents

MEDICALPROPERTIESTRUST.COM

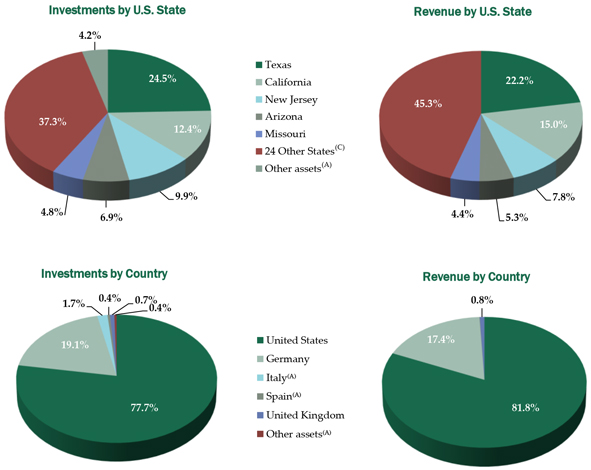

PORTFOLIO INFORMATION

INVESTMENTS AND REVENUE BY U.S. STATE AND COUNTRY

(March 31, 2016)

($ amounts in thousands)

| U.S. States and Other Countries |

Total Gross Assets |

Percentage of Gross Assets |

Total Revenue |

Percentage of Total Revenue |

||||||||||||

| Texas |

$ | 1,077,738 | 24.5 | % | $ | 24,472 | 22.2 | % | ||||||||

| California |

547,082 | 12.4 | % | 16,597 | 15.0 | % | ||||||||||

| New Jersey |

434,204 | 9.9 | % | 8,612 | 7.8 | % | ||||||||||

| Arizona |

304,663 | 6.9 | % | 5,797 | 5.3 | % | ||||||||||

| Missouri |

210,921 | 4.8 | % | 4,905 | 4.4 | % | ||||||||||

| 24 Other States(C) |

1,638,859 | 37.3 | % | 50,001 | 45.3 | % | ||||||||||

| Other assets(A) |

185,394 | 4.2 | % | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| United States |

$ | 4,398,861 | 100.0 | % | $ | 110,384 | 100.0 | % | ||||||||

| Germany |

$ | 1,080,381 | 85.5 | % | $ | 23,510 | 95.5 | % | ||||||||

| Italy(A) |

96,915 | 7.7 | % | — | — | |||||||||||

| Spain(A) |

24,399 | 1.9 | % | 83 | 0.3 | % | ||||||||||

| United Kingdom |

40,566 | 3.2 | % | 1,022 | 4.2 | % | ||||||||||

| Other assets(A) |

21,708 | 1.7 | % | — | — | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| International |

$ | 1,263,969 | 100.0 | % | $ | 24,615 | 100.0 | % | ||||||||

|

|

|

|

|

|||||||||||||

| Total |

$ | 5,662,830 | (B) | $ | 134,999 | |||||||||||

|

|

|

|

|

|||||||||||||

| (A) | Includes our equity investments, of which related income is reflected in other income in our income statement. |

| (B) | Represents investment concentration as a percentage of gross real estate assets, other loans, and equity investments assuming all real estate commitments are fully funded. |

| (C) | Reflects the repayment of mortgage and acquisition loans, along with the sale of our equity interest in Capella as of April 30, 2016; however, it includes two new loans totaling $143 million that were issued as part of the same transaction. |

Q1 2016 | SUPPLEMENTAL INFORMATION 12

Table of Contents

MEDICALPROPERTIESTRUST.COM

PORTFOLIO INFORMATION

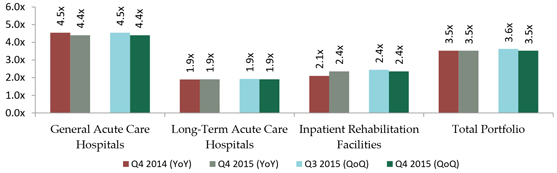

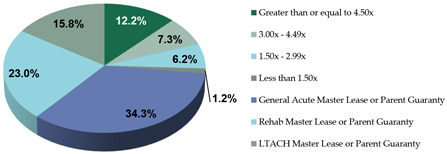

Same Store EBITDAR(A) Rent Coverage

YoY and Sequential Quarter Comparisons by Property Type

Stratification of Portfolio EBITDAR Rent Coverage

| EBITDAR Rent Coverage TTM |

Investment (in thousands) |

No. of Facilities | Percentage of Investment |

|||||||||

| Greater than or equal to 4.50x |

$ | 302,688 | 6 | 12.2 | % | |||||||

| 3.00x - 4.49x |

182,111 | 3 | 7.3 | % | ||||||||

| 1.50x - 2.99x |

153,823 | 3 | 6.2 | % | ||||||||

| Less than 1.50x |

29,833 | 1 | 1.2 | % | ||||||||

| Total Master Leased and/or with Parent Guaranty: 2.8x |

$ | 1,814,160 | 67 | 73.1 | % | |||||||

| General Acute Master Leased and/or with |

850,332 | 20 | 34.3 | % | ||||||||

| Inpatient Rehabilitation Facilities Master |

571,127 | 27 | 23.0 | % | ||||||||

| Long-Term Acute Care Hospitals Master |

392,701 | 20 | 15.8 | % | ||||||||

| (A) | EBITDAR adjusted for non-recurring items. |

Notes:

| (1) | Same Store represents properties with at least 24 months of financial reporting data as of December 31, 2015. Properties that do not provide financial reporting and disposed assets are not included. |

| (2) | Freestanding ERs will be reported as a distinct property type when MPT’s original $100 million commitment has 24 months of financial reporting data. |

| (3) | All data presented is on a trailing twelve month (“TTM”) basis. |

Q1 2016 | SUPPLEMENTAL INFORMATION 13

Table of Contents

MEDICALPROPERTIESTRUST.COM

PORTFOLIO INFORMATION

SUMMARY OF COMPLETED ACQUISITIONS / DEVELOPMENT PROJECTS IN 2016

($ amounts in thousands)

| Operator |

Location |

Costs Incurred as of 3/31/2016 |

Rent Commencement Date |

Acquisition / | ||||||

| Adeptus Health |

Houston, TX | $ | 2,866 | 3/28/2016 | Development | |||||

| Adeptus Health |

Helotes, TX | 7,381 | 3/10/2016 | Development | ||||||

| Adeptus Health |

Frisco, TX | 3,850 | 3/4/2016 | Development | ||||||

| Adeptus Health |

Longmont, CO | 3,921 | 2/10/2016 | Development | ||||||

| Adeptus Health |

Rosenberg, TX | 4,260 | 1/15/2016 | Development | ||||||

|

|

|

|||||||||

| $ | 22,278 | |||||||||

|

|

|

|||||||||

SUMMARY OF CURRENT DEVELOPMENT PROJECTS AS OF MARCH 31, 2016

($ amounts in thousands)

| Operator |

Commitment | Costs Incurred as of 3/31/2016 |

Estimated Completion Date |

|||||||||

| Ernest Health |

$ | 19,212 | $ | 16,894 | 2Q 2016 | |||||||

| Adeptus Health |

12,639 | 8,734 | 2Q 2016 | |||||||||

| Adeptus Health |

62,155 | 36,257 | 3Q 2016 | |||||||||

| Adeptus Health |

61,997 | 8,745 | 2Q 2017 | |||||||||

| Adeptus Health |

123,033 | — | Various | |||||||||

|

|

|

|

|

|||||||||

| $ | 279,036 | $ | 70,630 | |||||||||

|

|

|

|

|

|||||||||

Q1 2016 | SUPPLEMENTAL INFORMATION 14

Table of Contents

MEDICALPROPERTIESTRUST.COM

MEDICAL PROPERTIES TRUST, INC. AND SUBSIDIARIES

Consolidated Statements of Income

(Amounts in thousands except per share data)

| For the Three Months Ended | ||||||||

| March 31, 2016 |

March 31, 2015 |

|||||||

| (Unaudited) | (Unaudited) | |||||||

| Revenues |

||||||||

| Rent billed |

$ | 74,061 | $ | 53,100 | ||||

| Straight-line rent |

8,217 | 4,728 | ||||||

| Income from direct financing leases |

18,951 | 12,555 | ||||||

| Interest and fee income |

33,770 | 25,578 | ||||||

|

|

|

|

|

|||||

| Total revenues |

134,999 | 95,961 | ||||||

| Expenses |

||||||||

| Real estate depreciation and amortization |

21,142 | 14,756 | ||||||

| Property-related |

901 | 351 | ||||||

| Acquisition expenses(A) |

(1,065 | ) | 6,239 | |||||

| General and administrative |

11,471 | 10,905 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

32,449 | 32,251 | ||||||

|

|

|

|

|

|||||

| Operating income |

102,550 | 63,710 | ||||||

| Interest and other expense, net |

(44,005 | ) | (27,359 | ) | ||||

| Income tax expense |

(319 | ) | (375 | ) | ||||

|

|

|

|

|

|||||

| Income from continuing operations |

58,226 | 35,976 | ||||||

| Loss from discontinued operations |

(1 | ) | — | |||||

|

|

|

|

|

|||||

| Net income |

58,225 | 35,976 | ||||||

| Net income attributable to non-controlling interests |

(298 | ) | (79 | ) | ||||

|

|

|

|

|

|||||

| Net income attributable to MPT common stockholders |

$ | 57,927 | $ | 35,897 | ||||

|

|

|

|

|

|||||

| Earnings per common share – basic: |

||||||||

| Income from continuing operations |

$ | 0.24 | $ | 0.18 | ||||

| Loss from discontinued operations |

— | — | ||||||

|

|

|

|

|

|||||

| Net income attributable to MPT common stockholders |

$ | 0.24 | $ | 0.18 | ||||

|

|

|

|

|

|||||

| Earnings per common share – diluted: |

||||||||

| Income from continuing operations |

$ | 0.24 | $ | 0.17 | ||||

| Loss from discontinued operations |

— | — | ||||||

|

|

|

|

|

|||||

| Net income attributable to MPT common stockholders |

$ | 0.24 | $ | 0.17 | ||||

|

|

|

|

|

|||||

| Dividends declared per common share |

$ | 0.22 | $ | 0.22 | ||||

| Weighted average shares outstanding – basic |

237,510 | 202,958 | ||||||

| Weighted average shares outstanding – diluted |

237,819 | 203,615 | ||||||

| (A) | Included in the 2016 first quarter is an adjustment of $1.9 million reflecting a decrease in our estimate of real estate transfer taxes due on our 2015 acquisitions in Germany. |

| Q1 2016 | SUPPLEMENTAL INFORMATION 15 |

Table of Contents

MEDICALPROPERTIESTRUST.COM

FINANCIAL STATEMENTS

MEDICAL PROPERTIES TRUST, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

(Amounts in thousands except per share data)

| March 31, 2016 |

December 31, 2015 |

|||||||

| (Unaudited) | (A) | |||||||

| ASSETS |

||||||||

| Real estate assets |

||||||||

| Land, buildings and improvements, intangible lease assets, and other |

$ | 3,395,836 | $ | 3,297,705 | ||||

| Net investment in direct financing leases |

630,482 | 626,996 | ||||||

| Mortgage loans |

757,578 | 757,581 | ||||||

|

|

|

|

|

|||||

| Gross investment in real estate assets |

4,783,896 | 4,682,282 | ||||||

| Accumulated depreciation and amortization |

(280,099 | ) | (257,928 | ) | ||||

|

|

|

|

|

|||||

| Net investment in real estate assets |

4,503,797 | 4,424,354 | ||||||

| Cash and cash equivalents |

206,410 | 195,541 | ||||||

| Interest and rent receivables |

50,467 | 46,939 | ||||||

| Straight-line rent receivables |

90,791 | 82,155 | ||||||

| Other assets |

858,930 | 860,362 | ||||||

|

|

|

|

|

|||||

| Total Assets |

$ | 5,710,395 | $ | 5,609,351 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND EQUITY |

||||||||

| Liabilities |

||||||||

| Debt, net |

$ | 3,396,604 | $ | 3,322,541 | ||||

| Accounts payable and accrued expenses |

139,443 | 137,356 | ||||||

| Deferred revenue |

21,585 | 29,358 | ||||||

| Lease deposits and other obligations to tenants |

16,615 | 12,831 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

3,574,247 | 3,502,086 | ||||||

| Equity |

||||||||

| Preferred stock, $0.001 par value. Authorized 10,000 shares; no shares outstanding |

— | — | ||||||

| Common stock, $0.001 par value. Authorized 500,000 shares; issued and outstanding - 237,242 shares at March 31, 2016 and 236,744 shares at December 31, 2015 |

237 | 237 | ||||||

| Additional paid in capital |

2,595,725 | 2,593,827 | ||||||

| Distributions in excess of net income |

(413,108 | ) | (418,650 | ) | ||||

| Accumulated other comprehensive loss |

(51,482 | ) | (72,884 | ) | ||||

| Treasury shares, at cost |

(262 | ) | (262 | ) | ||||

|

|

|

|

|

|||||

| Total Medical Properties Trust, Inc. Stockholders’ Equity |

2,131,110 | 2,102,268 | ||||||

|

|

|

|

|

|||||

| Non-controlling interests |

5,038 | 4,997 | ||||||

|

|

|

|

|

|||||

| Total equity |

2,136,148 | 2,107,265 | ||||||

|

|

|

|

|

|||||

| Total Liabilities and Equity |

$ | 5,710,395 | $ | 5,609,351 | ||||

|

|

|

|

|

|||||

| (A) | Financials have been derived from the prior year audited financial statements. |

Q1 2016 | SUPPLEMENTAL INFORMATION 16

Table of Contents

MEDICALPROPERTIESTRUST.COM

FINANCIAL STATEMENTS

DETAIL OF OTHER ASSETS AS OF MARCH 31, 2016

($ amounts in thousands)

| Operator |

Investment | Annual Interest Rate |

YTD RIDEA Income(C) |

Security / Credit Enhancements | ||||||||||

| Non-Operating Loans |

||||||||||||||

| Vibra Healthcare acquisition loan(A) |

$ | 7,951 | 10.25 | % | Secured and cross-defaulted with real estate, other agreements and guaranteed by Parent | |||||||||

| Vibra Healthcare working capital |

5,233 | 9.50 | % | Secured and cross-defaulted with real estate, other agreements and guaranteed by Parent | ||||||||||

| Post Acute Medical working capital |

4,290 | 11.48 | % | Secured and cross-defaulted with real estate; certain loans are cross-defaulted with other loans and real estate | ||||||||||

| Alecto working capital |

16,680 | 11.21 | % | Secured and cross-defaulted with real estate and guaranteed by Parent | ||||||||||

| IKJG/HUMC working capital |

11,424 | 10.73 | % | Secured and cross-defaulted with real estate and guaranteed by Parent | ||||||||||

| Ernest Health |

22,667 | 9.10 | % | Secured and cross-defaulted with real estate and guaranteed by Parent | ||||||||||

| Other |

10,777 | |||||||||||||

|

|

|

|||||||||||||

| 79,022 | ||||||||||||||

| Operating Loans |

||||||||||||||

| Ernest Health, Inc.(B) |

93,200 | 15.00 | % | $ | 3,793 | Secured and cross-defaulted with real estate and guaranteed by Parent | ||||||||

| Capella |

487,685 | (F) | 8.00 | % | 9,754 | Secured and cross-defaulted with real estate and guaranteed by Parent | ||||||||

| IKJG/HUMC convertible loan |

3,352 | 54 | Secured and cross-defaulted with real estate and guaranteed by Parent | |||||||||||

|

|

|

|

|

|||||||||||

| 584,237 | 13,601 | |||||||||||||

| Equity investments(G) |

||||||||||||||

| Domestic |

19,202 | 56 | ||||||||||||

| International(E) |

110,626 | 573 | (H) | |||||||||||

| Lease and cash collateral |

3,494 | Not applicable | ||||||||||||

| Other assets(D) |

62,349 | Not applicable | ||||||||||||

|

|

|

|

|

|||||||||||

| Total |

$ | 858,930 | $ | 14,230 | ||||||||||

|

|

|

|

|

|||||||||||

| (A) | Original amortizing acquisition loan was $41 million; loan matures in 2019. |

| (B) | Cash rate is 10% effective March 1, 2014. Due to compounding, effective interest rate is 16.28%. |

| (C) | Income earned on operating loans is reflected in the interest income line of the income statement. |

| (D) | Includes prepaid expenses, office property and equipment and other. |

| (E) | Includes equity investments in Spain, Italy, and Germany. |

| (F) | This acquisition loan was paid in full as of April 30, 2016; however, we issued two new loans totaling $143 million as part of the same transaction. |

| (G) | All earnings in income from equity investments are reported on a one quarter lag basis. |

| (H) | Excludes $0.3 million and $5.3 million of our share of real estate depreciation and acquisition expenses of certain unconsolidated joint ventures. |

Q1 2016 | SUPPLEMENTAL INFORMATION 17

Table of Contents