Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - Johnson Controls International plc | tyc-2016325xex311.htm |

| EX-32.1 - EXHIBIT 32.1 - Johnson Controls International plc | tyc-2016325xex321.htm |

| EX-31.2 - EXHIBIT 31.2 - Johnson Controls International plc | tyc-2016325xex312.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________________________

FORM 10-Q

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended March 25, 2016 | |

or | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

333-196049

(Commission File Number)

___________________________________________________________

TYCO INTERNATIONAL PLC

(Exact name of Registrant as specified in its charter)

Ireland (Jurisdiction of Incorporation) | 98-0390500 (I.R.S. Employer Identification Number) | |

1 Albert Quay, Albert Quay, Cork, Ireland (Address of registrant's principal executive office) | ||

353-21-426-0000 (Registrant's telephone number) | ||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The number of ordinary shares outstanding as of April 22, 2016 was 425,497,785.

TYCO INTERNATIONAL PLC

INDEX TO FORM 10-Q

Page | |||

2

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

TYCO INTERNATIONAL PLC

CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(in millions, except per share data)

For the Quarters Ended | For the Six Months Ended | ||||||||||||||

March 25, 2016 | March 27, 2015 | March 25, 2016 | March 27, 2015 | ||||||||||||

Revenue from product sales | $ | 1,398 | $ | 1,458 | $ | 2,806 | $ | 2,946 | |||||||

Service revenue | 933 | 972 | 1,901 | 1,962 | |||||||||||

Net revenue | 2,331 | 2,430 | 4,707 | 4,908 | |||||||||||

Cost of product sales | 968 | 999 | 1,930 | 2,021 | |||||||||||

Cost of services | 506 | 550 | 1,042 | 1,097 | |||||||||||

Selling, general and administrative expenses | 602 | 648 | 1,175 | 1,300 | |||||||||||

Merger costs | 26 | — | 26 | — | |||||||||||

Restructuring and asset impairment charges, net (see Note 4) | 4 | 12 | 16 | 70 | |||||||||||

Operating income | 225 | 221 | 518 | 420 | |||||||||||

Interest income | 4 | 4 | 8 | 7 | |||||||||||

Interest expense | (22 | ) | (25 | ) | (46 | ) | (49 | ) | |||||||

Other (expense) income, net | — | (1 | ) | (165 | ) | 3 | |||||||||

Income from continuing operations before income taxes | 207 | 199 | 315 | 381 | |||||||||||

Income tax expense | (63 | ) | (18 | ) | (99 | ) | (37 | ) | |||||||

Income from continuing operations | 144 | 181 | 216 | 344 | |||||||||||

Income (loss) from discontinued operations, net of income taxes | 1 | (16 | ) | 5 | (18 | ) | |||||||||

Net income | 145 | 165 | 221 | 326 | |||||||||||

Less: noncontrolling interest in subsidiaries net loss | (1 | ) | (2 | ) | (1 | ) | (3 | ) | |||||||

Net income attributable to Tyco ordinary shareholders | $ | 146 | $ | 167 | $ | 222 | $ | 329 | |||||||

Amounts attributable to Tyco ordinary shareholders: | |||||||||||||||

Income from continuing operations | $ | 145 | $ | 183 | $ | 217 | $ | 347 | |||||||

Income (loss) from discontinued operations | 1 | (16 | ) | 5 | (18 | ) | |||||||||

Net income attributable to Tyco ordinary shareholders | $ | 146 | $ | 167 | $ | 222 | $ | 329 | |||||||

Basic earnings per share attributable to Tyco ordinary shareholders: | |||||||||||||||

Income from continuing operations | $ | 0.34 | $ | 0.44 | $ | 0.51 | $ | 0.83 | |||||||

(Loss) income from discontinued operations | — | (0.04 | ) | 0.01 | (0.05 | ) | |||||||||

Net income attributable to Tyco ordinary shareholders | $ | 0.34 | $ | 0.40 | $ | 0.52 | $ | 0.78 | |||||||

Diluted earnings per share attributable to Tyco ordinary shareholders: | |||||||||||||||

Income from continuing operations | $ | 0.33 | $ | 0.43 | $ | 0.51 | $ | 0.81 | |||||||

Income (loss) from discontinued operations | 0.01 | (0.04 | ) | 0.01 | (0.04 | ) | |||||||||

Net income attributable to Tyco ordinary shareholders | $ | 0.34 | $ | 0.39 | $ | 0.52 | $ | 0.77 | |||||||

Weighted average number of shares outstanding: | |||||||||||||||

Basic | 425 | 420 | 424 | 420 | |||||||||||

Diluted | 428 | 427 | 428 | 427 | |||||||||||

See Notes to Unaudited Consolidated Financial Statements.

3

TYCO INTERNATIONAL PLC

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

(in millions)

For the Quarters Ended | For the Six Months Ended | ||||||||||||||

March 25, 2016 | March 27, 2015 | March 25, 2016 | March 27, 2015 | ||||||||||||

Net income | $ | 145 | $ | 165 | $ | 221 | $ | 326 | |||||||

Other comprehensive income (loss), net of tax | |||||||||||||||

Foreign currency translation | 44 | (176 | ) | 1 | (374 | ) | |||||||||

Defined benefit and post retirement plans | 3 | 4 | 8 | 9 | |||||||||||

Unrealized gain on marketable securities and derivative instruments, net of tax | 2 | — | 3 | — | |||||||||||

Total other comprehensive income (loss), net of tax | 49 | (172 | ) | 12 | (365 | ) | |||||||||

Comprehensive income (loss) | 194 | (7 | ) | 233 | (39 | ) | |||||||||

Less: comprehensive loss attributable to noncontrolling interests | (1 | ) | (2 | ) | (1 | ) | (3 | ) | |||||||

Comprehensive income (loss) attributable to Tyco ordinary shareholders | $ | 195 | $ | (5 | ) | $ | 234 | $ | (36 | ) | |||||

See Notes to Unaudited Consolidated Financial Statements.

4

TYCO INTERNATIONAL PLC

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(in millions, except per share data)

March 25, 2016 | September 25, 2015 | ||||||

Assets | |||||||

Current Assets: | |||||||

Cash and cash equivalents | $ | 345 | $ | 1,401 | |||

Accounts receivable, less allowance for doubtful accounts of $76 and $70, respectively | 1,722 | 1,732 | |||||

Inventories | 670 | 624 | |||||

Prepaid expenses and other current assets | 864 | 754 | |||||

Deferred income taxes | 62 | 62 | |||||

Assets held for sale | — | 102 | |||||

Total Current Assets | 3,663 | 4,675 | |||||

Property, plant and equipment, net | 1,189 | 1,177 | |||||

Goodwill | 4,460 | 4,234 | |||||

Intangible assets, net | 1,025 | 863 | |||||

Other assets | 1,274 | 1,372 | |||||

Total Assets | $ | 11,611 | $ | 12,321 | |||

Liabilities and Equity | |||||||

Current Liabilities: | |||||||

Loans payable and current maturities of long-term debt | $ | 400 | $ | 987 | |||

Accounts payable | 797 | 774 | |||||

Accrued and other current liabilities | 1,643 | 1,661 | |||||

Deferred revenue | 393 | 380 | |||||

Liabilities held for sale | — | 50 | |||||

Total Current Liabilities | 3,233 | 3,852 | |||||

Long-term debt | 2,159 | 2,159 | |||||

Deferred revenue | 285 | 303 | |||||

Other liabilities | 1,756 | 1,931 | |||||

Total Liabilities | 7,433 | 8,245 | |||||

Commitments and Contingencies (see Note 11) | |||||||

Tyco Shareholders' Equity: | |||||||

Ordinary shares, $0.01 par value, 1,000,000,000 shares authorized, and 425,294,236 and 422,400,870 shares issued as of March 25, 2016 and September 25, 2015, respectively | 4 | 4 | |||||

Ordinary A shares, €1.00 par value, 40,000 shares authorized, none outstanding as of March 25, 2016 and September 25, 2015 | — | — | |||||

Preference shares, $0.01 par value, 100,000,000 shares authorized, none outstanding as of March 25, 2016 and September 25, 2015 | — | — | |||||

Ordinary shares held in treasury, 409,244 and 79,770 shares as of March 25, 2016 and September 25, 2015, respectively | (15 | ) | (3 | ) | |||

Additional paid in capital | 769 | 716 | |||||

Accumulated earnings | 5,213 | 5,165 | |||||

Accumulated other comprehensive loss | (1,829 | ) | (1,841 | ) | |||

Total Tyco Shareholders' Equity | 4,142 | 4,041 | |||||

Nonredeemable noncontrolling interest | 36 | 35 | |||||

Total Equity | 4,178 | 4,076 | |||||

Total Liabilities and Equity | $ | 11,611 | $ | 12,321 | |||

See Notes to Unaudited Consolidated Financial Statements.

5

TYCO INTERNATIONAL PLC

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(in millions)

For the Six Months Ended | |||||||

March 25, 2016 | March 27, 2015 | ||||||

Cash Flows From Operating Activities: | |||||||

Net income attributable to Tyco ordinary shareholders | $ | 222 | $ | 329 | |||

Noncontrolling interest in subsidiaries net loss | (1 | ) | (3 | ) | |||

(Income) loss from discontinued operations, net of income taxes | (5 | ) | 18 | ||||

Income from continuing operations | 216 | 344 | |||||

Adjustments to reconcile net cash provided by operating activities: | |||||||

Depreciation and amortization | 167 | 171 | |||||

Non-cash compensation expense | 27 | 30 | |||||

Deferred income taxes | 62 | (29 | ) | ||||

Provision for losses on accounts receivable and inventory | 29 | 34 | |||||

Loss on extinguishment of debt | 168 | — | |||||

Legacy legal matters | (19 | ) | — | ||||

Loss on divestitures, net | 69 | 23 | |||||

Gain on investments, net | (114 | ) | (7 | ) | |||

Other non-cash items | 5 | 7 | |||||

Changes in assets and liabilities, net of the effects of acquisitions and divestitures: | |||||||

Accounts receivable, net | 38 | 22 | |||||

Contracts in progress | (54 | ) | (30 | ) | |||

Inventories | (56 | ) | (64 | ) | |||

Prepaid expenses and other assets | (30 | ) | (66 | ) | |||

Accounts payable | 2 | (87 | ) | ||||

Accrued and other liabilities | (133 | ) | (56 | ) | |||

Tax sharing agreement, net (Note 6) | (122 | ) | — | ||||

Income taxes, net | 13 | 1 | |||||

Other | 45 | (31 | ) | ||||

Net cash provided by operating activities | 313 | 262 | |||||

Net cash (used in) provided by discontinued operating activities | (11 | ) | 3 | ||||

Cash Flows From Investing Activities: | |||||||

Capital expenditures | (143 | ) | (123 | ) | |||

Acquisition of businesses, net of cash acquired | (314 | ) | (525 | ) | |||

Acquisition of dealer generated customer accounts and bulk account purchases | (11 | ) | (8 | ) | |||

Divestiture of businesses, net of cash divested | 9 | (1 | ) | ||||

Sales and maturities of investments including restricted investments | 8 | 279 | |||||

Purchases of investments including restricted investments | (7 | ) | (288 | ) | |||

Decrease (increase) in restricted cash | 24 | (39 | ) | ||||

Other | 1 | 2 | |||||

Net cash used in investing activities | (433 | ) | (703 | ) | |||

Net cash provided by (used in) discontinued investing activities | 4 | (15 | ) | ||||

Cash Flows From Financing Activities: | |||||||

Proceeds from issuance of short-term debt | 2,498 | — | |||||

Repayment of short-term debt | (2,098 | ) | (1 | ) | |||

Repayment of current portion of long-term debt | (1,134 | ) | — | ||||

Proceeds from issuance of long-term debt | — | 567 | |||||

Proceeds from exercise of share options | 26 | 57 | |||||

Dividends paid | (174 | ) | (151 | ) | |||

Repurchase of ordinary shares | — | (417 | ) | ||||

Transfer to discontinued operations | (7 | ) | (12 | ) | |||

Payment of contingent consideration | (1 | ) | (23 | ) | |||

Debt financing costs | (23 | ) | (4 | ) | |||

Other | (13 | ) | (19 | ) | |||

Net cash used in financing activities | (926 | ) | (3 | ) | |||

Net cash provided by discontinued financing activities | 7 | 12 | |||||

Effect of currency translation on cash | (10 | ) | (16 | ) | |||

Net decrease in cash and cash equivalents | (1,056 | ) | (460 | ) | |||

Cash and cash equivalents at beginning of period | 1,401 | 892 | |||||

Cash and cash equivalents at end of period | $ | 345 | $ | 432 | |||

See Notes to Unaudited Consolidated Financial Statements.

6

TYCO INTERNATIONAL PLC

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY (UNAUDITED)

For the Six Months Ended March 25, 2016 and March 27, 2015

(in millions)

Number of Ordinary Shares | Ordinary Shares at Par Value | Treasury Shares | Additional Paid in Capital | Accumulated Earnings | Accumulated Other Comprehensive Loss | Total Tyco Shareholders' Equity | Nonredeemable Noncontrolling Interest | Total Equity | ||||||||||||||||||||||||||

Balance as of September 26, 2014 | 427 | $ | 208 | $ | (2,515 | ) | $ | 3,306 | $ | 4,873 | $ | (1,225 | ) | $ | 4,647 | $ | 23 | $ | 4,670 | |||||||||||||||

Comprehensive income: | ||||||||||||||||||||||||||||||||||

Net income attributable to Tyco ordinary shareholders | 329 | 329 | (3 | ) | 326 | |||||||||||||||||||||||||||||

Other comprehensive loss, net of tax | (365 | ) | (365 | ) | (365 | ) | ||||||||||||||||||||||||||||

Cancellation of treasury shares | (34 | ) | 2,878 | (2,844 | ) | — | — | |||||||||||||||||||||||||||

Dividends declared | 2 | (86 | ) | (84 | ) | (84 | ) | |||||||||||||||||||||||||||

Conversion of Tyco International Ltd. common shares to Tyco International plc ordinary shares | (170 | ) | 170 | — | — | |||||||||||||||||||||||||||||

Shares issued for vesting of share based equity awards | 4 | 67 | (10 | ) | 57 | 57 | ||||||||||||||||||||||||||||

Repurchase of ordinary shares | (10 | ) | (417 | ) | (417 | ) | (417 | ) | ||||||||||||||||||||||||||

Compensation expense | 30 | 30 | 30 | |||||||||||||||||||||||||||||||

Noncontrolling interest related to acquisitions | — | 29 | 29 | |||||||||||||||||||||||||||||||

Other | (13 | ) | (3 | ) | (16 | ) | (16 | ) | ||||||||||||||||||||||||||

Balance as of March 27, 2015 | 421 | $ | 4 | $ | — | $ | 651 | $ | 5,116 | $ | (1,590 | ) | $ | 4,181 | $ | 49 | $ | 4,230 | ||||||||||||||||

Number of Ordinary Shares | Ordinary Shares at Par Value | Treasury Shares | Additional Paid in Capital | Accumulated Earnings | Accumulated Other Comprehensive (Loss) Income | Total Tyco Shareholders' Equity | Nonredeemable Noncontrolling Interest | Total Equity | ||||||||||||||||||||||||||

Balance as of September 25, 2015 | 422 | $ | 4 | $ | (3 | ) | $ | 716 | $ | 5,165 | $ | (1,841 | ) | $ | 4,041 | $ | 35 | $ | 4,076 | |||||||||||||||

Comprehensive income: | ||||||||||||||||||||||||||||||||||

Net income attributable to Tyco ordinary shareholders | 222 | 222 | (1 | ) | 221 | |||||||||||||||||||||||||||||

Other comprehensive income, net of tax | 12 | 12 | 12 | |||||||||||||||||||||||||||||||

Dividends declared | (174 | ) | (174 | ) | (174 | ) | ||||||||||||||||||||||||||||

Shares issued for vesting of share based equity awards | 3 | 26 | 26 | 26 | ||||||||||||||||||||||||||||||

Compensation expense | 27 | 27 | 27 | |||||||||||||||||||||||||||||||

Other | (12 | ) | — | (12 | ) | 2 | (10 | ) | ||||||||||||||||||||||||||

Balance as of March 25, 2016 | 425 | $ | 4 | $ | (15 | ) | $ | 769 | $ | 5,213 | $ | (1,829 | ) | $ | 4,142 | $ | 36 | $ | 4,178 | |||||||||||||||

See Notes to Unaudited Consolidated Financial Statements.

7

1. Basis of Presentation and Summary of Significant Accounting Policies

Basis of Presentation—The Consolidated Financial Statements included herein are unaudited, but in the opinion of management, such financial statements include all adjustments, consisting of normal recurring adjustments, necessary to summarize fairly the Company's financial position, results of operations and cash flows for the interim period. The unaudited Consolidated Financial Statements include the consolidated results of Tyco International plc, a corporation organized under the laws of Ireland, and its subsidiaries (Tyco and all its subsidiaries, hereinafter collectively referred to as the "Company" or "Tyco"). The unaudited Consolidated Financial Statements have been prepared in United States dollars ("USD") and in accordance with the instructions to Form 10-Q under the Securities and Exchange Act of 1934, as amended. The results reported in these unaudited Consolidated Financial Statements should not be taken as indicative of results that may be expected for the entire year. These financial statements should be read in conjunction with the Consolidated Financial Statements and accompanying notes contained in the Company's Annual Report on Form 10-K for the fiscal year ended September 25, 2015 (the "2015 Form 10-K") and Current Report filed on Form 8-K filed on March 11, 2016 which recast the Company's consolidated financial statements for each of the three years in the period ended September 25, 2015 to reflect changes in the presentation of operating income by segment. The information included in this Form 8-K was presented for informational purposes only and does not amend or restate the Company’s audited consolidated financial statements, which were included in its 2015 Form 10-K, and did not affect the Company’s previously reported net income, earnings per share, cash flows, operating income or assets or liabilities for any of the periods presented therein.

References to 2016 and 2015 are to Tyco's fiscal quarters ending March 25, 2016 and March 27, 2015, respectively, unless otherwise indicated. The Company has a 52- or 53-week fiscal year that ends on the last Friday in September. Fiscal 2016 is a 53-week year as compared with fiscal 2015, which was 52 weeks, with the additional week occurring in the fourth quarter of fiscal 2016. The Company's results for the quarters and six months ended March 25, 2016 and March 27, 2015 both consisted of 13 weeks and 26 weeks, respectively.

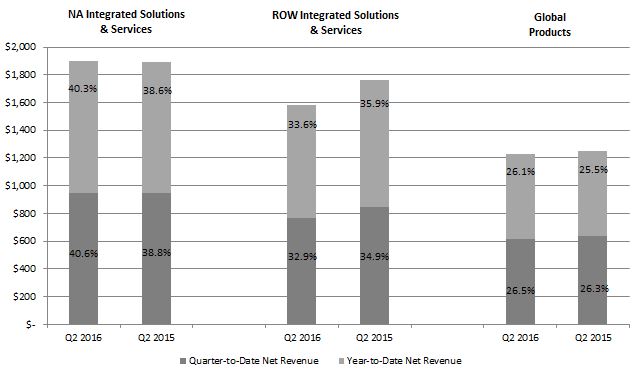

The Company operates and reports financial and operating information in the following three segments: North America Integrated Solutions & Services ("NA Integrated Solutions & Services"), Rest of World Integrated Solutions & Services ("ROW Integrated Solutions & Services") and Global Products. The Company also provides general corporate services to its segments which is reported as a fourth, non-operating segment, Corporate and Other.

Proposed Merger with Johnson Controls, Inc.— On January 24, 2016, Tyco entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Johnson Controls, Inc., a Wisconsin corporation (“Johnson Controls”), and certain other parties named therein, including Jagara Merger Sub LLC, a Wisconsin limited liability company and indirect wholly owned subsidiary of Tyco (“Merger Sub”). Pursuant to the Merger Agreement and subject to the terms and conditions set forth therein, Merger Sub will merge with and into Johnson Controls (the “Merger”), with Johnson Controls surviving the Merger as an indirect wholly owned subsidiary of Tyco. At the effective time of the Merger, Tyco will change its name to “Johnson Controls plc” and will trade under the ticker symbol “JCI.” Following such time, Tyco is referred to below as the “Combined Company.”

As a result of the Merger, each outstanding share of Johnson Controls common stock (the “Johnson Controls Shares”), other than shares held by Johnson Controls, its subsidiaries, Tyco or Merger Sub, will be converted into the right to receive (subject to proration as described below), at the holder’s election, either: (i) one (1) (the “Exchange Ratio”) ordinary share of the Combined Company (the “Share Consideration”); or (ii) an amount in cash equal to $34.88 (the “Cash Consideration”). Elections will be prorated so that Johnson Controls shareholders will receive in the aggregate approximately $3.864 billion of cash in the Merger (the “Aggregate Cash Consideration”). Holders that do not make an election will be treated as having elected to receive the Share Consideration. The Exchange Ratio takes into account the effects of a Tyco share consolidation contemplated by the Merger Agreement whereby, immediately prior to the Merger, every issued and unissued ordinary share of Tyco (each, a “Tyco Share”) will be consolidated into 0.955 of a share of Tyco.

The completion of the Merger is subject to certain closing conditions, including, among others, (i) the approval and adoption of the Merger Agreement by holders of two-thirds of the Johnson Controls Shares entitled to vote on such matter, (ii) the approval by the Tyco shareholders, at a special meeting of the Tyco shareholders (the “Tyco Special Meeting”) of (A) the issuance of Tyco shares in connection with the Merger, (B) the Tyco share consolidation and (C) the increase in Tyco’s authorized share capital, in each case, by a majority of the votes cast on these matters at the Tyco Special Meeting, and of certain amendments to Tyco’s articles of association, including a change of its name to “Johnson Controls plc,” by at least 75% of the votes cast on these matters at the Tyco Special Meeting (clause (ii), collectively, the “Tyco Shareholder Approvals”), (iii)

8

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

the expiration or termination of any waiting period applicable to the Merger under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, the consent of, or filing with, certain specified antitrust authorities, and certain other customary regulatory approvals, and (iv) Tyco’s obtaining the financing required to close the Merger on the terms set forth in the Merger Agreement.

The Merger Agreement contains specified termination rights, including, among others, the right of either party to terminate the Merger Agreement (i) if the requisite shareholder approvals have not been obtained, (ii) if the board of directors of the other party effects a change of recommendation, (iii) if the closing has not occurred by October 24, 2016, subject to extension to January 24, 2017 in certain circumstances, (iv) in response to certain intervening events (subject to the limitations set forth in the Merger Agreement) or (v) if there is a material breach by the other party of any of its representations, warranties or covenants, subject to certain conditions.

Tyco has entered into a senior unsecured term loan facility in the amount of $4 billion to finance the cash consideration for, and fees, expenses and costs incurred in connection with, the merger. In addition, the Company has entered into a revolving credit agreement in the amount of $1 billion, which is intended to replace Tyco's existing $1.5 billion revolving credit agreement. Tyco's ability to draw down on both the term loan facility and the new revolving credit agreement are contingent on the consummation of the merger with Johnson Controls. See Note 9.

Change of Jurisdiction— On May 30, 2014, Tyco entered into a Merger Agreement with Tyco International plc, a newly-formed Irish public limited company and a wholly-owned subsidiary of Tyco ("Tyco Ireland"). Under the Merger Agreement with Tyco Ireland, Tyco merged with and into Tyco Ireland, with Tyco Ireland being the surviving company. This resulted in Tyco Ireland becoming Tyco's publicly-traded parent company and changed the jurisdiction of organization of Tyco from Switzerland to Ireland. Tyco's shareholders received one ordinary share of Tyco Ireland for each ordinary share of Tyco held immediately prior to the re-domicile to Ireland. The re-domicile to Ireland became effective on November 17, 2014.

Reclassifications— Certain prior period amounts have been reclassified to conform with the current period presentation.

Effective for the first quarter of fiscal 2016, the Company has elected to present operating income by segment, as well as Corporate and Other, excluding restructuring and repositioning charges, net. Restructuring and repositioning charges, net, are shown in aggregate. This presentation is consistent with how management reviews the businesses, makes investing and resource decisions and assesses operating performance. See Note 15.

During the second quarter of fiscal 2016, the Company completed the sale of its Australian fire protection business, included in the ROW Integrated Solutions & Services segment. The assets and liabilities related to this business were classified as held for sale as of September 25, 2015. Its results of operations are included in continuing operations, as the criteria to be presented as a discontinued operation were not satisfied. See Note 3.

Recently Adopted Accounting Pronouncements— In April 2014, the Financial Accounting Standards Board ("FASB") issued authoritative guidance to change the criteria for reporting discontinued operations. Under the new guidance, only disposals representing a strategic shift that has or will have a major effect on the Company's operations and financial results should be reported as discontinued operations, with expanded disclosures. The guidance became effective for Tyco in the first quarter of fiscal 2016. The Company considers both qualitative and quantitative factors when assessing whether a disposed business represents a strategic shift that will have a major effect on the Company's operations and financial results. The Company considers the level (e.g. individual business or product line, reporting unit or reportable segment) and geographic impact (e.g. country, region, worldwide) of the disposal group. In addition, the Company considers the significance of the disposed business on certain financial measures when assessing whether or not such disposal has a major effect on the Company's operations and financial results. The adoption of this guidance did not have a material impact on the Company's financial position, results of operations or cash flows. During fiscal 2016, the divestiture of the Company's Australian fire protection business did not meet the criteria set forth in the new guidance and therefore was not classified as a discontinued operation. See Note 3.

Recently Issued Accounting Pronouncements— In May 2014, the FASB issued authoritative guidance for revenue from contracts with customers, which provides a single comprehensive revenue recognition model to apply in determining how and when to recognize revenue. The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. When applying the new revenue model to contracts with customers the guidance requires five steps to be applied, which include: 1) identify the contract(s) with a customer, 2) identify the performance obligations in the contract, 3) determine the transaction price, 4) allocate the transaction price to the performance obligations in the contract and 5) recognize revenue when (or as) the entity satisfies a performance obligation. The guidance

9

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

also requires quantitative and qualitative disclosures that are more comprehensive than existing standards. The disclosures are intended to enable financial statement users to understand the nature, timing and uncertainty of revenue and the related cash flow. The new standard permits either the full retrospective method or the modified retrospective method of adoption. In August 2015, the FASB issued authoritative guidance to defer the effective date of this guidance, which for Tyco will be the first quarter of fiscal 2019, with early adoption permitted beginning the first quarter of fiscal 2018. In March 2016, the FASB issued additional authoritative guidance clarifying its implementation guidance on principal versus agent considerations when determining whether to report revenue gross versus net. The Company is in the process of assessing the impact the guidance is expected to have upon adoption, including determining the adoption method.

In May 2015, the FASB issued authoritative guidance that is intended to improve the existing disclosure requirements for short-duration contracts for insurance entities that issue such contracts. The guidance requires additional information to be disclosed about the liability for unpaid claims and claim adjustment expenses to increase the transparency of significant estimates made in measuring those liabilities. This guidance is effective for Tyco in the first quarter of fiscal 2017, with early adoption permitted. The Company is currently assessing the impact, if any, the guidance may have upon adoption.

In July 2015, the FASB issued authoritative guidance intended to simplify the existing guidance under which an entity must measure inventory at the lower of cost or market. Under the new guidance, inventory is “measured at the lower of cost and net realizable value,” and does not apply to inventory that is measured using last-in, first-out or the retail method. Net realizable value is the estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. This guidance is effective for Tyco in the first quarter of fiscal 2017, with early adoption permitted on a prospective basis. The Company is currently assessing the impact, if any, the guidance may have upon adoption.

In September 2015, the FASB issued authoritative guidance intended to reduce the cost and complexity of financial reporting when recognizing adjustments to provisional amounts in connection with a business combination. This guidance eliminates the requirement to restate prior period financial statements, but requires entities to present separately on the face of the income statement, or disclose in the notes, the portion of the amount recorded in current-period earnings by line item that would have been recorded in previous reporting periods if the adjustment to the provisional amounts had been recognized as of the acquisition date. This guidance is effective for Tyco in the first quarter of fiscal 2017, with early adoption permitted on a prospective basis. The Company is currently assessing the impact, if any, the guidance may have upon adoption.

In November 2015, the FASB issued authoritative guidance intended to simplify the presentation of deferred income taxes. Under the new guidance, deferred tax liabilities and deferred tax assets are to be classified as noncurrent in a classified statement of financial position. The current requirement that deferred tax liabilities and assets of a tax-paying component of an entity be offset and presented as a single amount is not affected by the amendments in this update. This guidance is effective for Tyco in the first quarter of fiscal 2018, with early adoption permitted on a prospective or retrospective basis. The Company plans to adopt this guidance as of September 30, 2016 and does not expect the guidance to have a material impact on its financial statements.

In January 2016, the FASB issued authoritative guidance addressing the recognition, measurement, presentation and disclosure of financial assets and liabilities. The guidance primarily affects the accounting for equity investments, financial liabilities under the fair value option and the presentation and disclosure requirements for financial instruments. In addition, the guidance clarifies the valuation allowance assessment when recognizing deferred tax assets resulting from unrealized losses on available-for-sale debt securities. This guidance is effective for Tyco in the first quarter of fiscal 2019, and early adoption is not permitted, with certain exceptions. The amendments are required to be applied by means of a cumulative-effect adjustment on the balance sheet as of the beginning of the fiscal year of adoption. The Company is currently assessing the impact, if any, the guidance may have upon adoption.

In February 2016, the FASB issued authoritative guidance requiring the recognition of lease assets and lease liabilities by lessees for those leases previously classified as operating leases. The guidance requires quantitative and qualitative disclosures that are more comprehensive than existing standards. The disclosures are intended to enable financial statement users to understand the amount, timing and uncertainty of cash flows arising from leases. This guidance is effective for Tyco in the first quarter of fiscal 2020 with early adoption permitted. The amendments are required to be applied by means of a modified retrospective approach. The Company is currently assessing the impact, if any, the guidance may have upon adoption.

10

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

In March 2016, the FASB amended its authoritative guidance for employee share-based payment transactions by simplifying several aspects of the accounting for employee share-based payment awards, including the accounting for income taxes, withholding taxes and forfeitures, as well as classification on the statement of cash flows. The amended guidance is effective for Tyco in the first quarter of fiscal 2018 with early adoption permitted. The Company is currently assessing the impact, if any, the guidance may have upon adoption.

2. Merger Costs

On January 24, 2016, Tyco entered into a Merger Agreement with Johnson Controls. See Note 1. The Company expects to incur transaction related costs ("Merger Costs") in connection with activities taken in anticipation of the Merger, primarily related to financing, investment banking, advisory, legal, valuation, and other professional fees, and retention related costs for certain Tyco employees. The Company incurred pre-tax merger costs within continuing operations of $26 million during the quarter and six months ended March 25, 2016 primarily related to financing, advisory and professional fees. The Company received no tax benefits during the quarter and six months ended March 25, 2016 related to these charges.

3. Divestitures

The Company has continued to assess the strategic fit of its various businesses and has pursued the divestiture of certain businesses which do not align with its long-term strategy.

Fiscal 2016

During the second quarter of fiscal 2016, the Company completed the sale of its Australian fire protection business, included within its ROW Integrated Solutions & Services segment. The assets and liabilities of this business have been presented separately as held for sale within the Consolidated Balance Sheets as of September 25, 2015. The Company recorded a pre-tax loss of $75 million related to the sale for the six months ended March 25, 2016. This loss included a $57 million write-down to fair value, less costs to sell, which was recorded during the first quarter of fiscal 2016. Also included in the loss for the six month period was the write-off of a cumulative translation loss of $31 million, of which $24 million was provided for during the first quarter of fiscal 2016. This business has not been presented in discontinued operations within the Consolidated Statements of Operations, as the criteria to be presented as a discontinued operation were not satisfied.

During the second quarter of fiscal 2016, the Company completed the sale of a business within its Global Products segment. The assets and liabilities have not been presented separately as held for sale within the Consolidated Balance Sheets as the amounts were not material to the presentation of all periods. A pre-tax loss of approximately $17 million was recorded in Selling, general and administrative expenses within the Company’s Consolidated Statements of Operations during the fourth quarter of fiscal 2015 which represented the Company's best estimate to write-down the business to fair value, less costs to sell. Upon completing the sale, the Company recorded an immaterial gain. This business has not been presented in discontinued operations as the amounts were not material to the Consolidated Financial Statements.

In addition, during the second quarter of fiscal 2016, the Company completed the sale of another business within the ROW Integrated Solutions & Services segment and realized a loss that was not material. This business is accounted for as held for sale within the Consolidated Balance Sheets as of September 25, 2015, and its results of operations have been presented as discontinued operations within the Consolidated Statements of Operations for the quarters and six months ended March 25, 2016 and March 27, 2015.

During the first quarter of fiscal 2016, the Company recorded a pre-tax gain of $17 million resulting from the transfer to Pentair Ltd. (formerly known as Tyco Flow Control International Ltd.) of Tyco's equity interest in a joint venture related to the Company's former Flow Control business as repayment of a loan established at the time of the 2012 Separation. This gain was recorded in Income (loss) from discontinued operations, net of income taxes, within the Consolidated Statements of Operations for the quarter ended December 25, 2015.

Fiscal 2015

During the quarter ended March 27, 2015, the Company concluded that several businesses in the ROW Installation & Services segment which it intended to sell met the criteria to be classified as held for sale. The Company completed the sale of these businesses during fiscal 2015. To the extent the criteria required to be presented as a discontinued operation have been satisfied, the businesses results of operations have been presented as such on the Consolidated Statements of Operations during the quarters and six months ended March 27, 2015.

11

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Divestiture Charges, net

During the second quarter of fiscal 2016, the Company recorded a net loss of $17 million in Selling, general and administrative expenses within the Company's Consolidated Statements of Operations, primarily related to the loss on sale of the Australia fire protection business, as described above. The Company recorded a net divestiture loss of $22 million during the second quarter of fiscal 2015, related to a business in the ROW Integrated Solutions & Services segment which was not presented within discontinued operations, as described above.

During the six months ended March 25, 2016, the Company recorded a net loss of $69 million in Selling, general and administrative expenses within the Company's Consolidated Statements of Operations, primarily due to the sale of its Australian fire protection business, as described above. The Company recorded a net divestiture loss of $23 million during the six months ended March 27, 2015.

Discontinued Operations

The components of income (loss) from discontinued operations, net of income taxes are as follows ($ in millions):

For the Quarters Ended | For the Six Months Ended | ||||||||||||||

March 25, 2016 | March 27, 2015 | March 25, 2016 | March 27, 2015 | ||||||||||||

Net revenue | $ | — | $ | 5 | $ | 1 | $ | 10 | |||||||

Pre-tax loss from discontinued operations | (1 | ) | (6 | ) | (2 | ) | (9 | ) | |||||||

Pre-tax gain on sale of discontinued operations | — | — | 17 | 1 | |||||||||||

Income tax benefit (expense) (1) | 2 | (10 | ) | (10 | ) | (10 | ) | ||||||||

Income (loss) from discontinued operations, net of income taxes | $ | 1 | $ | (16 | ) | $ | 5 | $ | (18 | ) | |||||

(1) Income tax expense for the six months ended March 25, 2016 includes $12 million related to the Company’s settlement of an income tax matter in the first quarter of fiscal 2016 pertaining to its divested ADT Korea business for the 2012 period. This matter is unrelated to the liability established of $212 million during fiscal 2014 which relates to the indemnification for certain tax related matters in connection with the sale. The Company continues to maintain such liability until the matter is resolved.

Balance sheet information for the assets and liabilities of businesses classified as held for sale as of September 25, 2015 was as follows ($ in millions):

As of | |||

September 25, 2015 | |||

Accounts receivable, net | $ | 44 | |

Inventories | 3 | ||

Prepaid expenses and other current assets | 22 | ||

Deferred income taxes | 1 | ||

Property, plant and equipment, net | 13 | ||

Goodwill | 3 | ||

Intangible assets, net | 16 | ||

Total assets | $ | 102 | |

Accounts payable | 12 | ||

Accrued and other current liabilities | 26 | ||

Deferred revenue | 2 | ||

Other liabilities | 10 | ||

Total liabilities | $ | 50 | |

12

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Because the Company utilizes a centralized approach to cash management and the financing of its operations, all cash that is generated by discontinued operations is routinely transferred to the Company's financing subsidiaries in continuing operations. As a result, transfers from discontinued operations within the Company's Consolidated Statement of Cash Flows reflects the net cash movements from discontinued operations to continuing operations that have occurred during the period.

4. Restructuring and Asset Impairment Charges, Net

During fiscal 2016, the Company identified and pursued additional opportunities for cost savings through restructuring activities and workforce reductions to improve operating efficiencies across the Company's businesses. The Company expects to incur restructuring and restructuring related charges between $35 million and $50 million in fiscal 2016, which does not include repositioning charges, as described below.

The Company recorded restructuring and asset impairment charges by action as follows ($ in millions):

For the Quarters Ended | For the Six Months Ended | ||||||||||||||

March 25, 2016 | March 27, 2015 | March 25, 2016 | March 27, 2015 | ||||||||||||

2016 actions | $ | 6 | $ | — | $ | 15 | $ | — | |||||||

2015 actions | (2 | ) | 9 | 1 | 58 | ||||||||||

2014 and prior actions | 1 | 3 | 1 | 12 | |||||||||||

Total restructuring and asset impairment charges, net | $ | 5 | $ | 12 | $ | 17 | $ | 70 | |||||||

Charges reflected in SG&A | $ | 1 | $ | — | $ | 1 | $ | — | |||||||

Charges reflected in restructuring and asset impairments, net | 4 | 12 | 16 | 70 | |||||||||||

2016 Actions

Restructuring and asset impairment charges, net, during the quarter and six months ended March 25, 2016 related to the 2016 actions are as follows ($ in millions):

For the Quarter Ended March 25, 2016 | |||||||||||

Employee Severance and Benefits | Charges Reflected in SG&A | Total | |||||||||

ROW Integrated Solutions & Services | $ | 2 | $ | — | $ | 2 | |||||

Global Products | 2 | 1 | 3 | ||||||||

Corporate and Other | 1 | — | 1 | ||||||||

Total | $ | 5 | $ | 1 | $ | 6 | |||||

For the Six Months Ended March 25, 2016 | |||||||||||||||

Employee Severance and Benefits | Facility Exit and Other Charges | Charges Reflected in SG&A | Total | ||||||||||||

NA Integrated Solutions & Services | $ | 2 | $ | — | $ | — | $ | 2 | |||||||

ROW Integrated Solutions & Services | 3 | — | — | 3 | |||||||||||

Global Products | 4 | 1 | 1 | 6 | |||||||||||

Corporate and Other | 4 | — | — | 4 | |||||||||||

Total | $ | 13 | $ | 1 | $ | 1 | $ | 15 | |||||||

13

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The rollforward of the reserves from September 25, 2015 to March 25, 2016 is as follows ($ in millions):

Balance as of September 25, 2015 | $ | — | |

Charges | 15 | ||

Reversals | (1 | ) | |

Utilization | (7 | ) | |

Balance as of March 25, 2016 | $ | 7 | |

2015 Actions

Restructuring and asset impairment charges, net, during the quarters and six months ended March 25, 2016 and March 27, 2015 related to the 2015 actions are as follows ($ in millions):

For the Quarter Ended March 25, 2016 | For the Quarter Ended March 27, 2015 | ||||||

Employee Severance and Benefits | Employee Severance and Benefits | ||||||

NA Integrated Solutions & Services | $ | (1 | ) | $ | 4 | ||

ROW Integrated Solutions & Services | — | 4 | |||||

Global Products | — | 1 | |||||

Corporate and Other | (1 | ) | — | ||||

Total | $ | (2 | ) | $ | 9 | ||

For the Six Months Ended March 25, 2016 | |||

Employee Severance and Benefits | |||

NA Integrated Solutions & Services | $ | 1 | |

Total | $ | 1 | |

For the Six Months Ended March 27, 2015 | |||||||||||

Employee Severance and Benefits | Facility Exit and Other Charges | Total | |||||||||

NA Integrated Solutions & Services | $ | 26 | $ | — | $ | 26 | |||||

ROW Integrated Solutions & Services | 14 | 5 | 19 | ||||||||

Global Products | 3 | — | 3 | ||||||||

Corporate and Other | 10 | — | 10 | ||||||||

Total | $ | 53 | $ | 5 | $ | 58 | |||||

Restructuring and asset impairment charges, net, incurred cumulative to date from initiation of the 2015 actions are as follows ($ in millions):

Employee Severance and Benefits | Facility Exit and Other Charges | Charges Reflected in SG&A | Total | ||||||||||||

NA Integrated Solutions & Services | $ | 42 | $ | 3 | $ | 1 | $ | 46 | |||||||

ROW Integrated Solutions & Services | 81 | 9 | 1 | 91 | |||||||||||

Global Products | 21 | 1 | (1 | ) | 21 | ||||||||||

Corporate and Other | 20 | 1 | — | 21 | |||||||||||

Total | $ | 164 | $ | 14 | $ | 1 | $ | 179 | |||||||

14

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The rollforward of the reserves from September 25, 2015 to March 25, 2016 is as follows ($ in millions):

Balance as of September 25, 2015 | $ | 117 | |

Charges | 6 | ||

Reversals | (5 | ) | |

Utilization | (31 | ) | |

Currency translation | (1 | ) | |

Balance as of March 25, 2016 | $ | 86 | |

Restructuring reserves for businesses that are included in Liabilities held for sale within the Consolidated Balance Sheets are excluded from the table above. See Note 3.

2014 and prior actions

The Company continues to maintain restructuring reserves related to actions initiated prior to fiscal 2015. The total amount of these reserves was $32 million and $38 million as of March 25, 2016 and September 25, 2015, respectively. The Company incurred $1 million and $3 million of net restructuring charges and utilized $4 million and $13 million for the quarters ended March 25, 2016 and March 27, 2015, respectively, related to 2014 and prior actions. The Company incurred $1 million and $12 million of net restructuring charges and utilized $10 million and $29 million for the six months ended March 25, 2016 and March 27, 2015, respectively, related to 2014 and prior actions. The aggregate remaining reserves relate to employee severance and benefits as well as facility exit costs for long-term non-cancelable lease obligations primarily within the Company's NA Integrated Solutions & Services and ROW Integrated Solutions & Services segments.

Total Restructuring Reserves

As of March 25, 2016 and September 25, 2015, restructuring reserves related to all actions were included within the Company's Consolidated Balance Sheets as follows ($ in millions):

As of | |||||||

March 25, 2016 | September 25, 2015 | ||||||

Accrued and other current liabilities | $ | 111 | $ | 140 | |||

Other liabilities | 14 | 15 | |||||

Total | $ | 125 | $ | 155 | |||

Restructuring reserves for businesses that are included in Liabilities held for sale within the Consolidated Balance Sheets are excluded from the table above. See Note 3.

Repositioning

The Company has initiated certain global actions designed to reduce its cost structure and improve future profitability by streamlining operations and better aligning functions, which the Company refers to as repositioning actions. These actions may or may not lead to a future restructuring action. During the quarters ended March 25, 2016 and March 27, 2015, the Company recorded net repositioning charges of $5 million and $17 million, respectively, and $11 million and $34 million for the six months ended March 25, 2016 and March 27, 2015, respectively, primarily related to professional fees which have been reflected in Selling, general and administrative expenses within the Consolidated Statements of Operations.

15

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

5. Acquisitions

During the quarter ended March 25, 2016, cash consideration for acquisitions included in continuing operations was $176 million, which was comprised of $182 million of cash paid, net of cash acquired of $6 million. This was related to the acquisition of ShopperTrak, a leading global provider of retail consumer behavior insights and location-based analytics. ShopperTrak is being integrated into the NA Integrated Solutions & Services and ROW Integrated Solutions & Services segments.

During the six months ended March 25, 2016, cash consideration for acquisitions included in continuing operations was $314 million. In addition to the ShopperTrak acquisition discussed above, cash consideration for the six month period included $128 million, which was comprised of $166 million of cash paid, including $5 million to settle pre-existing matters and $6 million for prepaid agency commissions, net of cash acquired of $27 million, related to an additional investment in the Company's Tyco UAE joint venture with its local partner Suwaidi Engineering Group ("Suwaidi") in the United Arab Emirates ("UAE"). Tyco UAE is a leading provider of fire, security and integrated solutions and services in the UAE and also has operations in Qatar and Oman. Effective with the date of this transaction, the Company consolidated 100% of Tyco UAE, which is recorded in the Company's ROW Integrated Solutions & Services segment. The total enterprise fair value of the UAE joint venture was allocated as follows: $99 million of assets, $136 million of goodwill, $99 million of intangible assets and the assumption of $32 million of liabilities. The Company's proportionate share of the joint venture's net income was historically recorded in Selling, general and administrative expenses within the Consolidated Statements of Operations for periods prior to the acquisition date. As a result of this transaction, the Company recorded a net gain of $111 million which primarily relates to the Company's previously held 49% equity interest in the joint venture, which was previously accounted for under the equity method of accounting, inclusive of a charge for the settlement of pre-existing matters with the Company's former joint venture partner. The Company recorded the net gain in Selling, general and administrative expenses within the Consolidated Statements of Operations during the quarter ended December 25, 2015. The balance of the cash paid during the six months ended March 25, 2016 of $10 million related to an acquisition within the Company's ROW Integrated Solutions & Services segment which was not material.

The final determination of fair value of certain assets and liabilities related to the ShopperTrak acquisition remains subject to change based on final valuations of the assets and liabilities assumed. The Company does not expect the finalization of this matter to have a material effect on the purchase price allocation, which is expected to be completed within fiscal 2016. During the six months ended March 25, 2016, the Company finalized the determination of fair value for certain assets and liabilities relating to the acquisitions closed during the first quarter of fiscal 2016 and fourth quarter of fiscal 2015, with no material adjustment to the preliminary purchase price allocations.

During the quarter ended March 27, 2015, total consideration paid, net of $6 million of cash acquired and $5 million of holdback liability, for six acquisitions included in continuing operations was $373 million. The activity is primarily related to the acquisition of Industrial Safety Technologies International ("IST"), a global leader in gas and flame detection with operations in Europe, the Middle East, China, and the U.S., for total consideration paid, net of $5 million of cash acquired, of $327 million. IST has been integrated into the Global Products segment. The remaining $46 million in purchase price related to five acquisitions that have been integrated into the ROW Integrated Solutions & Services and Global Products segments and working capital adjustments related to fiscal year 2014 acquisitions.

During the six months ended March 27, 2015, total consideration paid, net of $26 million of cash acquired and $8 million of holdback liability, for 11 acquisitions included in continuing operations was $525 million. This includes working capital adjustments described above. In addition to the acquisition of IST within the Global Products segment, the Company made 10 acquisitions during the six months ended March 27, 2015.

16

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

6. Income Taxes

Tyco did not have a significant change to its unrecognized tax benefits during the quarter ended March 25, 2016.

Many of Tyco's uncertain tax positions relate to tax years that remain subject to audit by the taxing authorities in U.S. federal, state and local or foreign jurisdictions. Open tax years in significant jurisdictions included in continuing operations are as follows:

Jurisdiction | Years Open To Audit |

Australia | 2004-2015 |

Canada | 2006-2015 |

Germany | 2006-2015 |

Ireland | 2011-2015 |

Switzerland | 2006-2015 |

United Kingdom | 2013-2015 |

United States | 1997-2015 |

Based on the current status of its income tax audits, the Company believes the unrecognized tax benefits that may be resolved in the next twelve months are not expected to be material.

At each balance sheet date, the Company evaluates whether it is more likely than not that Tyco's deferred tax assets will be realized and if sufficient future taxable income will be available by assessing current period and projected operating results and other pertinent data. As of March 25, 2016, Tyco recorded deferred tax assets of approximately $212 million, which is comprised of $2.3 billion gross deferred tax assets net of $2.1 billion valuation allowances.

Tax Sharing Agreement and Other Income Tax Matters

In connection with the 2012 and 2007 Separations, Tyco entered into the 2012 and 2007 Tax Sharing Agreements, respectively, that govern the respective rights, responsibilities, and obligations of (i) Tyco, Pentair plc and ADT Corporation after the 2012 Separation and (ii) Tyco, Covidien (subsequently acquired by Medtronic plc) and TE Connectivity Ltd. after the 2007 Separation, with respect to taxes. Specifically, this includes taxes in the ordinary course of business and taxes, if any, incurred as a result of any failure of the respective distributions to qualify tax-free for U.S. federal income tax purposes within the meaning of Section 355 of the Internal Revenue Code ("the Code") or certain internal transactions undertaken in anticipation of the spin-offs to qualify for tax-favored treatment under the Code.

Under the 2012 Tax Sharing Agreement, Tyco, Pentair and ADT share (i) certain pre-Distribution income tax liabilities that arise from adjustments made by tax authorities to ADT's, Tyco Flow Control's and Tyco's income tax returns, and (ii) payments required to be made by Tyco with respect to the 2007 Tax Sharing Agreement, excluding approximately $175 million of pre-2012 Separation related tax liabilities (collectively, "Shared Tax Liabilities"). Tyco will be responsible for the first $500 million of Shared Tax Liabilities. Pentair and ADT will share 42% and 58%, respectively, of the next $225 million of Shared Tax Liabilities. Tyco, Pentair and ADT will share 52.5%, 20% and 27.5%, respectively, of Shared Tax Liabilities above $725 million. All costs and expenses associated with the management of these Shared Tax Liabilities will generally be shared 20%, 27.5% and 52.5% by Pentair, ADT and Tyco, respectively. In connection with the execution of the 2012 Tax Sharing Arrangement, Tyco established liabilities representing the fair market value of its obligations which is recorded in Other liabilities within the Company's Consolidated Balance Sheet with an offset to Tyco shareholders' equity.

Under the 2007 Tax Sharing Agreement, Tyco shares responsibility for certain of Tyco's, Covidien's and TE Connectivity's income tax liabilities, which result in cash payments, based on a sharing formula for periods prior to and including June 29, 2007. More specifically, Tyco, Covidien and TE Connectivity share 27%, 42% and 31%, respectively, of shared income tax liabilities that arise from adjustments made by tax authorities to Tyco's, Covidien's and TE Connectivity's U.S. and certain non-U.S. income tax returns. The costs and expenses associated with the management of these shared tax liabilities are generally shared equally among the parties. In connection with the execution of the 2007 Tax Sharing Agreement, Tyco established a net receivable from Covidien and TE Connectivity representing the amount Tyco expected to receive for pre-2007 Separation uncertain tax positions, including amounts owed to the Internal Revenue Service ("IRS"). Tyco also established liabilities representing the fair market value of its share of Covidien's and TE Connectivity's estimated obligations, primarily to the IRS, for their pre-2007 Separation taxes covered by the 2007 Tax Sharing Agreement.

17

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Tyco assesses the shared tax liabilities and related guaranteed liabilities related to both the 2012 and 2007 Tax Sharing Agreements at each reporting period. Tyco will provide payment to Pentair and ADT under the 2012 Tax Sharing Agreement and Covidien and TE Connectivity under the 2007 Tax Sharing Agreement as the shared income tax liabilities are settled. Settlement is expected to occur as the tax audit and legal processes are completed for the impacted years and cash payments are made. Due to the nature of the unresolved adjustments described in the next paragraph, the maximum amount of future payments under the 2012 and 2007 Tax Sharing Agreements is not known. Such cash payments, when they occur, will reduce the guarantor liability as they represent an equivalent reduction of risk. Tyco also assesses the sufficiency of the 2012 and 2007 Tax Sharing Agreements guarantee liabilities on a quarterly basis and will increase the liability when it is probable that cash payments expected to be made exceed the recorded balance.

Tyco and its subsidiaries' income tax returns are examined periodically by various tax authorities. In connection with these examinations, tax authorities, including the IRS, have raised issues and proposed tax adjustments, in particular with respect to years preceding the 2007 Separation. The issues and proposed adjustments related to such years are generally subject to the sharing provisions of the 2007 Tax Sharing Agreement and Tyco's liabilities under the 2007 Tax Sharing Agreement are further subject to the sharing provisions in the 2012 Tax Sharing Agreement. Tyco has previously disclosed that in connection with U.S. federal tax audits, the IRS raised a number of issues and proposed tax adjustments for periods beginning with the 1997 tax year. Although Tyco resolved substantially all of the issues and adjustments proposed by the IRS for tax years through 2007, it was not able to resolve matters related to the treatment of certain intercompany debt transactions during the period. As a result, on June 20, 2013, Tyco received Notices of Deficiency from the IRS asserting that several of Tyco's former U.S. subsidiaries owe additional taxes of $883.3 million plus penalties of $154 million based on audits of the 1997 through 2000 tax years of Tyco and its subsidiaries as they existed at that time. In addition, Tyco received Final Partnership Administrative Adjustments for certain U.S. partnerships owned by former U.S. subsidiaries with respect to which an additional tax deficiency of approximately $30 million has been asserted. These amounts excluded interest and did not reflect the roll-forward impact on subsequent audit periods.

On January 15, 2016, Tyco entered into Stipulations of Settled Issues with the IRS intended to resolve all disputes related to the intercompany debt issues described above for the 1997 - 2000 audit cycle currently before the U.S. Tax Court. The Stipulations of Settled Issues are contingent upon the IRS Appeals Division applying the same settlement to all intercompany debt issues on appeal for subsequent audit cycles (2001 - 2007) and, if applicable, review by the United States Congress Joint Committee on Taxation.

If finalized, the tentative resolution would cover all aspects of the controversy before the U.S. Tax Court described above and before the Appeals Division of the IRS, and would result in a total cash payment to the IRS in the range of $475 million to $525 million, which includes all interest and penalties. This payment would be subject to the sharing formula in each Tax Sharing Agreement, and would be shared among Tyco, Covidien and TE Connectivity 27%, 42% and 31%, respectively, with neither ADT nor Pentair being responsible for any payment related to this amount.

Assuming the tentative resolution is finalized, Tyco does not expect to recognize any additional charges related to the resolution, as it had previously recorded sufficient reserves with respect to this controversy and its obligations under the Tax Sharing Agreements. In the second quarter of fiscal 2016, the Company paid $120 million to TE Connectivity and $2 million to Covidien, which was subsequently paid to the IRS, in connection with the tentative resolution.

As noted above, Tyco has assessed its obligations under the 2007 Tax Sharing Agreement to determine that its recorded liability is sufficient to cover the indemnifications made by it under such agreement. In the absence of observable transactions for identical or similar guarantees, Tyco determined the fair value of these guarantees and indemnifications utilizing expected present value measurement techniques. Significant assumptions utilized to determine fair value included determining a range of potential outcomes, assigning a probability weighting to each potential outcome and estimating the anticipated timing of resolution. The probability weighted outcomes were discounted using Tyco's incremental borrowing rate. Until the tentative resolution is finalized, the ultimate resolution of these matters is uncertain and could result in a material adverse impact to the Company's financial position, results of operations, cash flows, or the effective tax rate in future reporting periods.

In addition to dealing with tax liabilities for periods prior to the respective Separations, the 2012 and 2007 Tax Sharing Agreements contain sharing provisions to address the contingencies that the 2012 or 2007 Separations, or internal transactions related thereto, may be deemed taxable by U.S. or non U.S. taxing authorities. In the event the 2012 Separation is determined to be taxable and such determination was the result of actions taken after the 2012 Separations by Tyco, ADT or Pentair, the party responsible for such failure would be responsible for all taxes imposed on each company as a result thereof. If such determination is not the result of actions taken by Tyco, ADT or Pentair after the 2012 Separation, then Tyco, ADT and Pentair

18

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

would be responsible for any taxes imposed on any of the companies as a result of such determination in the same manner and in the same proportions as described above. Similar provisions exist in the 2007 Tax Sharing Agreement. If either of the 2007 or 2012 Separation, or internal transactions taken in anticipation thereof, were deemed taxable, the associated liability could be significant. Tyco is responsible for all of its own taxes that are not shared pursuant to the 2012 and 2007 Tax Sharing Agreements' sharing formulas. In addition, Pentair and ADT, and Covidien and TE Connectivity are responsible for their tax liabilities that are not subject to the 2012 or 2007 Tax Sharing Agreements' sharing formula.

Each of the 2012 and 2007 Tax Sharing Agreements provides that, if any party to such agreement were to default in its obligation to another party to pay its share of the distribution taxes that arise as a result of no party's fault, each non-defaulting party to the agreement would be required to pay, equally with any other non-defaulting party to the agreement, the amounts in default. In addition, if another party to the 2012 or 2007 Tax Sharing Agreements that is responsible for all or a portion of an income tax liability were to default in its payment of such liability to a taxing authority, Tyco could be liable under applicable tax law for such liabilities and required to make additional tax payments. Accordingly, under certain circumstances, Tyco may be obligated to pay amounts in excess of its agreed-upon share of its tax liabilities under either of the 2012 or 2007 Tax Sharing Agreements.

The receivables and liabilities related to the 2012 and 2007 Tax Sharing Agreements as of March 25, 2016 and September 25, 2015, are as follows ($ in millions):

2012 Tax Sharing Agreement | 2007 Tax Sharing Agreement | ||||||||||||||

As of | As of | ||||||||||||||

March 25, 2016 | September 25, 2015 | March 25, 2016 | September 25, 2015 | ||||||||||||

Tax sharing agreement related receivables: | |||||||||||||||

Other assets | $ | — | $ | — | $ | 19 | $ | 19 | |||||||

— | — | 19 | 19 | ||||||||||||

Tax sharing agreement related liabilities: | |||||||||||||||

Accrued and other current liabilities | — | — | (87 | ) | (15 | ) | |||||||||

Other liabilities | (46 | ) | (46 | ) | — | (194 | ) | ||||||||

(46 | ) | (46 | ) | (87 | ) | (209 | ) | ||||||||

Net liability | $ | (46 | ) | $ | (46 | ) | $ | (68 | ) | $ | (190 | ) | |||

In addition to the amounts above, pursuant to the terms of the 2012 Separation and Distribution Agreement, Tyco, ADT and Pentair are each responsible for issuing their own shares upon employee exercise of a stock option award or vesting of a restricted unit award. However, the 2012 Tax Sharing Agreement provides that any allowable compensation tax deduction for such awards is to be claimed by the employee's current employer. The 2012 Tax Sharing Agreement requires the employer claiming a tax deduction for shares issued by the other companies to pay a percentage of the allowable tax deduction to the company issuing the equity. During the quarter and six months ended March 25, 2016, Tyco made a $15 million net payment to Pentair and a $1 million net payment to ADT in connection with deductions claimed for Pentair and ADT shares issued to Company employees. Payments made to Pentair and ADT for the six months ended March 27, 2015 were not material.

Other Income Tax Matters

Except for earnings that are currently distributed, no additional material provision has been made for U.S. or non-U.S. income taxes on the undistributed earnings of subsidiaries or for deferred tax liabilities for temporary differences related to investments in subsidiaries, since the earnings are expected to be permanently reinvested, the investments are essentially permanent in duration, or Tyco has concluded that no additional tax liability will arise as a result of the distribution of such earnings. A liability could arise if amounts are distributed by such subsidiaries or if such subsidiaries are ultimately disposed. It is not practicable to estimate the additional income taxes related to permanently reinvested earnings or the basis differences related to investments in subsidiaries.

19

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

7. Earnings Per Share

The reconciliations between basic and diluted earnings per share attributable to Tyco ordinary shareholders are as follows (in millions, except per share data):

For the Quarter Ended March 25, 2016 | For the Quarter Ended March 27, 2015 | ||||||||||||||||||||

Income | Shares | Per Share Amount | Income | Shares | Per Share Amount | ||||||||||||||||

Basic earnings per share attributable to Tyco ordinary shareholders: | |||||||||||||||||||||

Income from continuing operations | $ | 145 | 425 | $ | 0.34 | $ | 183 | 420 | $ | 0.44 | |||||||||||

Share options and restricted share awards | — | 3 | — | 7 | |||||||||||||||||

Diluted earnings per share attributable to Tyco ordinary shareholders: | |||||||||||||||||||||

Income from continuing operations attributable to Tyco ordinary shareholders, giving effect to dilutive adjustments | $ | 145 | 428 | $ | 0.33 | $ | 183 | 427 | $ | 0.43 | |||||||||||

For the Six Months Ended March 25, 2016 | For the Six Months Ended March 27, 2015 | ||||||||||||||||||||

Income | Shares | Per Share Amount | Income | Shares | Per Share Amount | ||||||||||||||||

Basic earnings per share attributable to Tyco ordinary shareholders: | |||||||||||||||||||||

Income from continuing operations | $ | 217 | 424 | $ | 0.51 | $ | 347 | 420 | $ | 0.83 | |||||||||||

Share options and restricted share awards | — | 4 | — | 7 | |||||||||||||||||

Diluted earnings per share attributable to Tyco ordinary shareholders: | |||||||||||||||||||||

Income from continuing operations attributable to Tyco ordinary shareholders, giving effect to dilutive adjustments | $ | 217 | 428 | $ | 0.51 | $ | 347 | 427 | $ | 0.81 | |||||||||||

The computation of diluted earnings per share for the quarter and six months ended March 25, 2016 excludes the effect of the potential exercise of share options to purchase approximately 6 million shares for both periods and excludes restricted stock units of approximately 2 million shares for both periods because the effect would be anti-dilutive.

The computation of diluted earnings per share for the quarter and six months ended March 27, 2015 excludes the effect of the potential exercise of share options to purchase approximately 3 million shares for both periods and excludes restricted stock units of approximately 1 million shares for both periods because the effect would be anti-dilutive.

20

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

8. Goodwill and Intangible Assets

Goodwill

The changes in the carrying amount of goodwill by segment are as follows ($ in millions):

NA Integrated Solutions & Services | ROW Integrated Solutions & Services | Global Products | Total | ||||||||||||

Gross goodwill | $ | 2,102 | $ | 1,969 | $ | 1,809 | $ | 5,880 | |||||||

Accumulated impairment | (126 | ) | (1,068 | ) | (567 | ) | (1,761 | ) | |||||||

Carrying amount of goodwill as of September 26, 2014 | 1,976 | 901 | 1,242 | 4,119 | |||||||||||

2015 activity: | |||||||||||||||

Acquisitions / purchase accounting adjustments | 23 | 50 | 274 | 347 | |||||||||||

Currency translation | (29 | ) | (167 | ) | (36 | ) | (232 | ) | |||||||

Gross goodwill | $ | 2,096 | $ | 1,852 | $ | 2,047 | $ | 5,995 | |||||||

Accumulated impairment | (126 | ) | (1,068 | ) | (567 | ) | (1,761 | ) | |||||||

Carrying amount of goodwill as of September 25, 2015 | 1,970 | 784 | 1,480 | 4,234 | |||||||||||

2016 activity: | |||||||||||||||

Acquisitions / purchase accounting adjustments | 69 | 182 | — | 251 | |||||||||||

Currency translation | 1 | (20 | ) | (6 | ) | (25 | ) | ||||||||

Gross goodwill | $ | 2,166 | $ | 2,014 | $ | 2,041 | $ | 6,221 | |||||||

Accumulated impairment | (126 | ) | (1,068 | ) | (567 | ) | (1,761 | ) | |||||||

Carrying amount of goodwill as of March 25, 2016 | $ | 2,040 | $ | 946 | $ | 1,474 | $ | 4,460 | |||||||

Intangible Assets

The following table sets forth the gross carrying amount and accumulated amortization of the Company's intangible assets as of March 25, 2016 and September 25, 2015 ($ in millions):

As of | |||||||||||||||

March 25, 2016 | September 25, 2015 | ||||||||||||||

Gross Carrying Amount | Accumulated Amortization | Gross Carrying Amount | Accumulated Amortization | ||||||||||||

Amortizable: | |||||||||||||||

Contracts and related customer relationships | $ | 1,372 | $ | 1,017 | $ | 1,281 | $ | 991 | |||||||

Intellectual property | 877 | 516 | 760 | 496 | |||||||||||

Other | 9 | 5 | 8 | 5 | |||||||||||

Total | $ | 2,258 | $ | 1,538 | $ | 2,049 | $ | 1,492 | |||||||

Non-Amortizable: | |||||||||||||||

Intellectual property | $ | 210 | $ | 210 | |||||||||||

Franchise rights | 76 | 76 | |||||||||||||

In-process research and development | 19 | 20 | |||||||||||||

Total | $ | 305 | $ | 306 | |||||||||||

Intangible asset amortization expense for the quarters ended March 25, 2016 and March 27, 2015 was $25 million and $21 million, respectively. Intangible asset amortization expense for the six months ended March 25, 2016 and March 27, 2015 was $48 million and $41 million, respectively.

21

TYCO INTERNATIONAL PLC

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The estimated aggregate amortization expense on intangible assets is expected to be approximately $53 million for the remainder of 2016, $95 million for 2017, $91 million for 2018, $85 million for 2019, and $396 million for 2020 and thereafter.

9. Debt

The carrying value of the Company's debt as of March 25, 2016 and September 25, 2015 is as follows ($ in millions):

As of | |||||||

March 25, 2016 | September 25, 2015 | ||||||

Commercial paper(1) | $ | 400 | $ | — | |||

3.375% public notes due 2015(2) | — | 258 | |||||

3.75% public notes due 2018 | 67 | 67 | |||||

7.0% public notes due 2019(2) | — | 245 | |||||

6.875% public notes due 2021(2) | — | 465 | |||||

4.625% public notes due 2023 | 42 | 42 | |||||

1.375% Euro-denominated public notes due 2025 | 558 | 558 | |||||

3.9% public notes due 2026 | 745 | 745 | |||||

5.125% public notes due 2045 | 746 | 746 | |||||

Other (2) | 1 | 20 | |||||

Total debt | 2,559 | 3,146 | |||||

Less current portion | 400 | 987 | |||||

Long-term debt | $ | 2,159 | $ | 2,159 | |||

_______________________________________________________________________________

(1) The current portion of debt as of March 25, 2016 is comprised of $400 million of commercial paper.

(2) The current portion of debt as of September 25, 2015 is comprised of $258 million notes due 2015, $245 million notes due 2019, $465 million notes due 2021 and $19 million of Other debt.

Fair Value

The carrying amount of Tyco's debt subject to the fair value disclosure requirements as of March 25, 2016 and September 25, 2015 was $2,558 million and $3,126 million, respectively. The Company utilizes various valuation methodologies to determine the fair value of its debt, which is primarily dependent on the type of market in which the Company's debt is traded. When available, the Company uses quoted market prices to determine the fair value of its debt that is traded in active markets. As of March 25, 2016 and September 25, 2015, the fair value of the Company's debt which was actively traded was $2,615 million and $3,291 million, respectively. As of March 25, 2016 and September 25, 2015, the Company's debt that was subject to the fair value disclosure requirements was all actively traded and is classified as Level 1 in the fair value hierarchy. Additionally, the Company believes the carrying amount of its commercial paper of $400 million as of March 25, 2016 approximates fair value based on the short-term nature of such debt.

Fiscal 2016 Debt Repayment

On September 14, 2015, the Company and the Company's wholly-owned subsidiary, Tyco International Finance S.A. ("TIFSA") announced the redemption of all of the outstanding $242 million aggregate principal amount of 7.0% notes due 2019 and $462 million aggregate principal amount of 6.875% notes due 2021. On October 14, 2015, TIFSA paid cash of $876 million to complete the redemption, resulting in a loss on extinguishment of $168 million which was recorded in Other expense, net within the Consolidated Statements of Operations during the first quarter of fiscal 2016. The charge is comprised of the make-whole premium of $172 million and the write-off of unamortized debt issuance costs of $1 million, partially offset by the write-off of the unamortized premium of $5 million.

On October 15, 2015, the Company repaid $258 million aggregate principal amount of 3.375% notes which matured on such date.

22

TYCO INTERNATIONAL PLC