Attached files

| file | filename |

|---|---|

| 8-K - INDEPENDENT BANK CORPORATION 8-K 4-26-2016 - INDEPENDENT BANK CORP /MI/ | form8k.htm |

Exhibit 99.1

INDEPENDENT BANK CORPORATION2016 Annual Shareholders meeting April 26, 2016

Cautionary note regarding forward-looking statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including statements of goals, intentions, and expectations as to future trends, plans, events, or results of Independent Bank Corporation’s operations and policies, including, but not limited to, Independent Bank Corporation’s outlook on earnings and the sufficiency of the allowance for loan losses, and statements regarding asset quality, projections of future revenue, earnings or other measures of economic performance, Independent Bank Corporation’s plans and expectations regarding non-performing assets, business opportunities, and general economic conditions. Forward-looking statements include expressions such as “will,” “may,” “should,” “believe,” “expect,” “forecast,” “anticipate,” “estimate,” “project,” “intend,” “likely,” “optimistic” and “plan,” and similar words or phrases, which are necessarily statements of belief as to expected outcomes of future events. These statements are based on current and anticipated economic conditions, nationally and in Independent Bank Corporation’s markets, interest rates and interest rate policy, competitive factors, and other conditions which by their nature are not susceptible to accurate forecast and are subject to significant uncertainty. Because of these uncertainties and the assumptions on which this presentation and the forward-looking statements are based, actual future operations and results may differ materially from those indicated in this presentation. For a discussion of certain factors, risks and uncertainties which could cause actual future operations and results to differ from estimates and projections discussed in these forward-looking statements, please read the “Risk Factors” section in Independent Bank Corporation’s 2015 Annual Report on Form 10-K. You should not place undue reliance on any such forward-looking statement. These forward-looking statements are not guarantees of future performance. Independent Bank Corporation does not undertake to publicly revise or update forward-looking statements in this presentation to reflect events or circumstances that arise after the date of this presentation. 2

Today’s Agenda Welcome and Call to Order – IBC ChairmanVirtual Annual Shareholder Meeting Process and Instructions – IBC ChairmanVoting upon matters listed in the Company’s 2016 Proxy Statement – IBC ChairmanBusiness Update by IBC President & CEOQuestion and answer session – IBC President & CEO and IBC EVP & CFOAdjournment 3

IBC Board of Directors IBC Executive Officers William J. Boer Joan A. Budden Stephen L. Gulis Jr. Terry L. HaskeWilliam B. KesselMichael M. Magee Jr., ChairmanJames E. McCarty, Lead Outside DirectorMatthew J. MissadCharles C. Van Loan William B. Kessel – President and Chief Executive OfficerRobert N. Shuster – EVP/Chief Financial Officer Mark L. Collins – EVP/General Counsel Stefanie M. Kimball – EVP/Chief Risk OfficerDennis J. Mack – EVP/Chief Commercial Lending OfficerDavid C. Reglin – EVP/Retail Banking 4

2016 Annual Meeting of Shareholders Secretary for the meeting (Robert Shuster)Record date: February 26, 2016Approximate distribution date of Proxy Statement: March 11, 2016Shares entitled to vote: 21,598,586Determination of quorumVoting on proposals 5

Proposal #1Election of Directors 6 William J. Boer Joan A. Budden Charles C. Van Loan

Proposal #2Ratification of Appointment of Independent Auditors Crowe Horwath LLP has served as IBC’s independent registered public accounting firm since 2005Crowe Horwath was founded in 1942 and is one of the 10 largest accounting and consulting firms in the U.S.IBC is served primarily by Crowe Horwath’s Grand Rapids, Michigan and South Bend, Indiana offices 7

Proposal #3Advisory Vote on Executive Compensation The Board has solicited a non-binding advisory vote from our shareholders to approve the compensation of our executives as described in our proxy materials. 8

INDEPENDENT BANK CORPORATIONBusiness Update by Brad Kessel, President & CEO 9

2015 Financial Summary 2015 2014 2013 Diluted EPS $ 0.86 $ 0.77 $ 3.55 Income before income taxes 29,380 25,216 22,658 Net income 20,017 18,021 77,509 NI available to common 20,017 18,021 82,062 Total assets 2,409,066 2,248,730 2,209,943 Total loans 1,515,050 1,409,962 1,374,570 Total deposits 2,085,963 1,924,302 1,884,806 Shareholders’ equity 251,092 250,371 231,581 Tangible BV per share 11.18 10.79 10.01 TCE to tangible assets 10.34% 11.03% 10.35% Note: Dollars in 000’s, except per share data. 10

2015 Financial Highlights Income Statement Net income of $20.0 million, or $0.86 per diluted share, representing increases over 2014 of 11.1% and 11.7%, respectively.Improved asset quality metrics led to $2.7 million credit loan loss provision. Loan net charge-offs declined by 77.9% year-over year, to just $0.7 million in 2016.Non-interest income increased by $1.4 million, or 3.5%, year-over-year due primarily to gain on branch sale.Non-interest expense declined by $1.5 million, or 1.7%, year-over-year. Balance Sheet/Capital Total portfolio loans grew $105.1 million, or 7.5% year-over-year (led by commercial loan growth of $57.4 million, or 8.3%).NPA’s reduced $3.8 million, or 17.6% year-over-year. NPA’s equaled 0.74% of total assets at 12/31/15.Total deposits grew $161.7 million, or 8.4% year-over-year. TBV per share increased by 3.6% to $11.18 at 12/31/15, from $10.79 at 12/31/14.Bought back 967,199 shares in 2015. 11

Completed Initiatives in 2015 New products, services and technologyRefreshed and simplified checking account line-upConsumer payment offering (Apple Pay)Mortgage loan origination platform (EllieMae Encompass)Human Resources management platform (UltiPro)Equity-linked certificate of deposit (Altitude CD)Business continuity planning investments (data centers)Branch and backroom platform improvements (streamline workflow and enhance sales)Addition of a new director 12

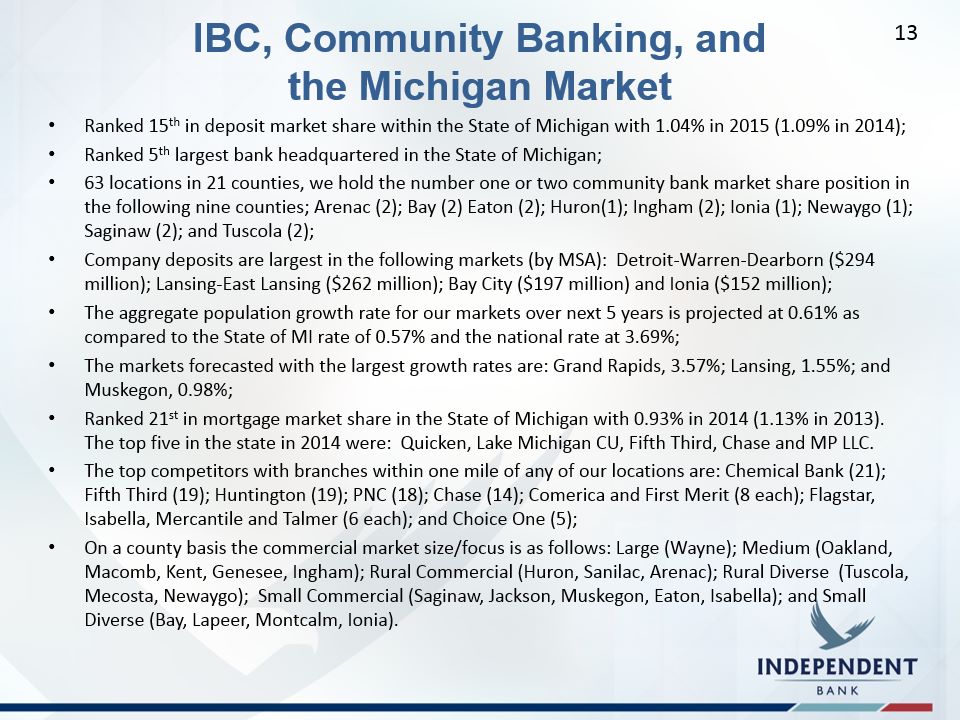

IBC, Community Banking, and the Michigan Market Ranked 15th in deposit market share within the State of Michigan with 1.04% in 2015 (1.09% in 2014);Ranked 5th largest bank headquartered in the State of Michigan;63 locations in 21 counties, we hold the number one or two community bank market share position in the following nine counties; Arenac (2); Bay (2) Eaton (2); Huron(1); Ingham (2); Ionia (1); Newaygo (1); Saginaw (2); and Tuscola (2); Company deposits are largest in the following markets (by MSA): Detroit-Warren-Dearborn ($294 million); Lansing-East Lansing ($262 million); Bay City ($197 million) and Ionia ($152 million);The aggregate population growth rate for our markets over next 5 years is projected at 0.61% as compared to the State of MI rate of 0.57% and the national rate at 3.69%;The markets forecasted with the largest growth rates are: Grand Rapids, 3.57%; Lansing, 1.55%; and Muskegon, 0.98%;Ranked 21st in mortgage market share in the State of Michigan with 0.93% in 2014 (1.13% in 2013). The top five in the state in 2014 were: Quicken, Lake Michigan CU, Fifth Third, Chase and MP LLC.The top competitors with branches within one mile of any of our locations are: Chemical Bank (21); Fifth Third (19); Huntington (19); PNC (18); Chase (14); Comerica and First Merit (8 each); Flagstar, Isabella, Mercantile and Talmer (6 each); and Choice One (5);On a county basis the commercial market size/focus is as follows: Large (Wayne); Medium (Oakland, Macomb, Kent, Genesee, Ingham); Rural Commercial (Huron, Sanilac, Arenac); Rural Diverse (Tuscola, Mecosta, Newaygo); Small Commercial (Saginaw, Jackson, Muskegon, Eaton, Isabella); and Small Diverse (Bay, Lapeer, Montcalm, Ionia). 13

1Q’16 Financial Summary 1Q’16 4Q’15 3Q’15 2Q’15 1Q’15 Diluted EPS $ 0.19 $ 0.25 $ 0.22 $ 0.24 $ 0.16 Income before taxes 6,057 8,251 7,325 8,243 5,561 Net income 4,100 5,570 5,047 5,619 3,781 Return on average assets 0.68% 0.93% 0.86% 0.98% 0.67% Return on average equity 6.70% 8.80% 7.84% 8.86% 6.05% Total assets $2,487,120 $2,409,066 $2,394,861 $2,288,954 $2,329,296 Total portfolio loans 1,538,982 1,515,050 1,467,999 1,450,007 1,422,959 Total deposits 2,154,706 2,085,963 2,060,962 1,961,417 2,000,473 Shareholders’ equity 239,545 251,092 252,980 254,375 253,625 Tangible BV per share 11.16 11.18 11.11 11.06 10.94 TCE to tangible assets 9.55% 10.34% 10.48% 11.02% 10.79% Note: Dollars in 000’s, except per share data. 14

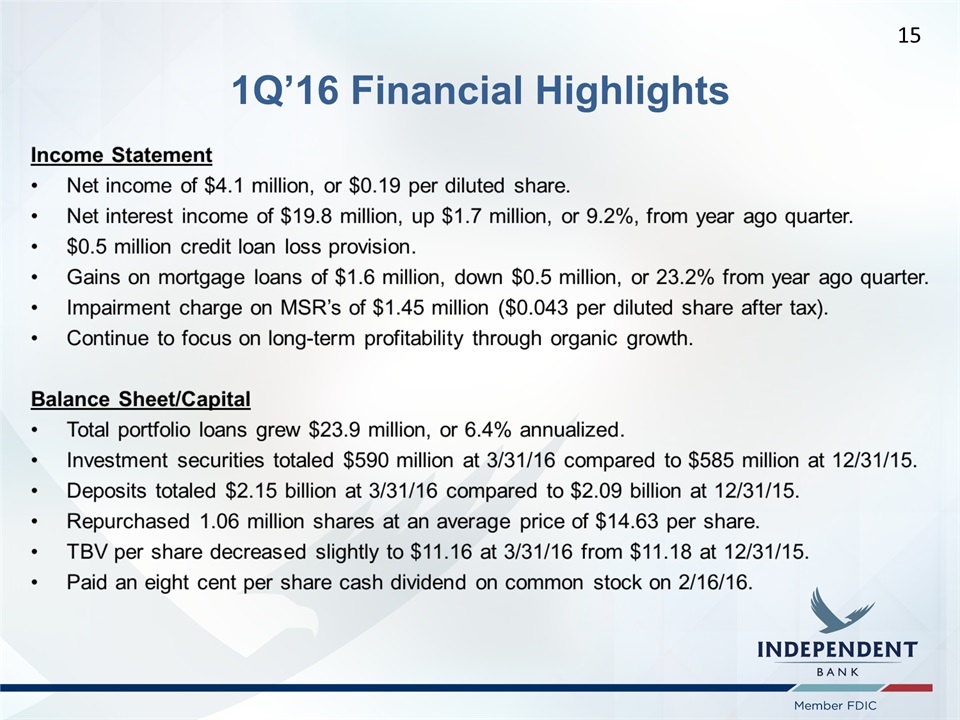

1Q’16 Financial Highlights 15

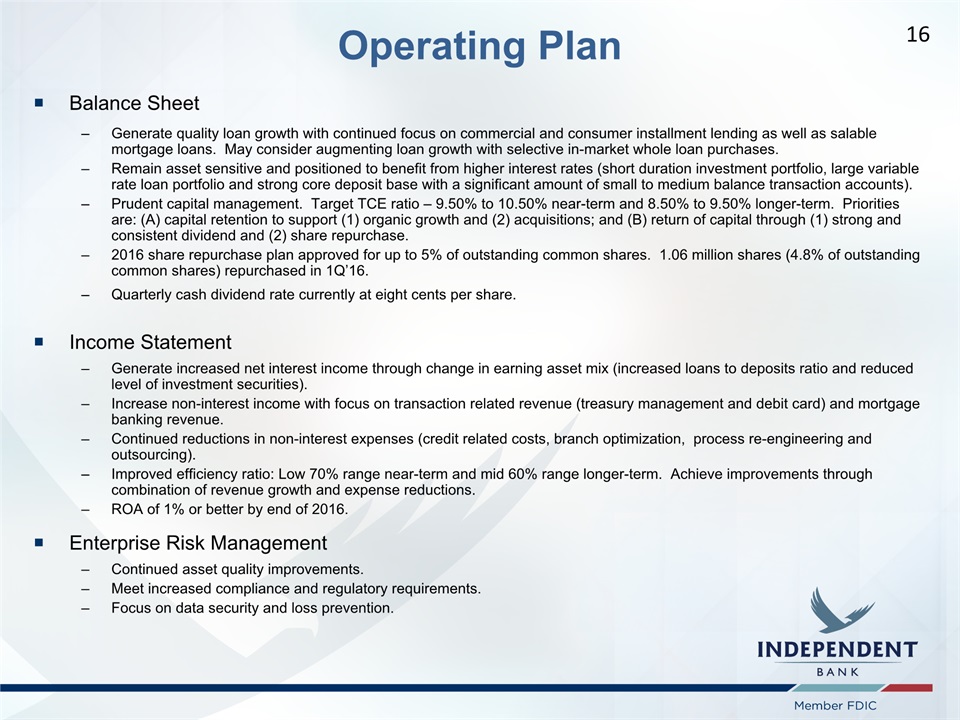

Operating Plan Balance SheetGenerate quality loan growth with continued focus on commercial and consumer installment lending as well as salable mortgage loans. May consider augmenting loan growth with selective in-market whole loan purchases.Remain asset sensitive and positioned to benefit from higher interest rates (short duration investment portfolio, large variable rate loan portfolio and strong core deposit base with a significant amount of small to medium balance transaction accounts).Prudent capital management. Target TCE ratio – 9.50% to 10.50% near-term and 8.50% to 9.50% longer-term. Priorities are: (A) capital retention to support (1) organic growth and (2) acquisitions; and (B) return of capital through (1) strong and consistent dividend and (2) share repurchase.2016 share repurchase plan approved for up to 5% of outstanding common shares. 1.06 million shares (4.8% of outstanding common shares) repurchased in 1Q’16.Quarterly cash dividend rate currently at eight cents per share. Income StatementGenerate increased net interest income through change in earning asset mix (increased loans to deposits ratio and reduced level of investment securities).Increase non-interest income with focus on transaction related revenue (treasury management and debit card) and mortgage banking revenue.Continued reductions in non-interest expenses (credit related costs, branch optimization, process re-engineering and outsourcing).Improved efficiency ratio: Low 70% range near-term and mid 60% range longer-term. Achieve improvements through combination of revenue growth and expense reductions. ROA of 1% or better by end of 2016.Enterprise Risk ManagementContinued asset quality improvements.Meet increased compliance and regulatory requirements.Focus on data security and loss prevention. 16

Recognition of Retired Directors 17 Robert L. Hetzler Charles A. Palmer

Independent Bank Corporation2016 Annual Shareholders Meeting Question and Answer SessionBrad Kessel, President & CEORob Shuster, Chief Financial Officer 18

Independent Bank Corporation2016 Annual Shareholders Meeting Voting ResultsShares entitled to vote: 21,598,586Proposal #1 – Election of DirectorsProposal #2 – Ratification of AuditorsProposal #3 – Advisory (Non-Binding) Vote on Executive Compensation 19

Independent Bank Corporation2016 Annual Shareholders Meeting Closing RemarksThank you for attending!NASDAQ: IBCP 20