Attached files

| file | filename |

|---|---|

| 8-K - 8-K - POPULAR, INC. | d185355d8k.htm |

| Exhibit 99.1

|

Investor

Presentation

First Quarter 2016

|

|

Forward Looking Statements

The information contained in this presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on managements current expectations and are subject to risks and uncertainties that may cause the Corporation’s actual results to differ materially from any future results expressed or implied by such forward-looking statements. Please refer to our Annual Report on Form 10-K for the year ended December 31, 2015 and our other filings with the SEC for a discussion of factors that could impact our future results. Other than to the extent required by applicable law, the Corporation undertakes no obligation to publicly update or revise any forward-looking statement to reflect events or circumstances after the date of such statements.

|

|

Q1 2016 Highlights

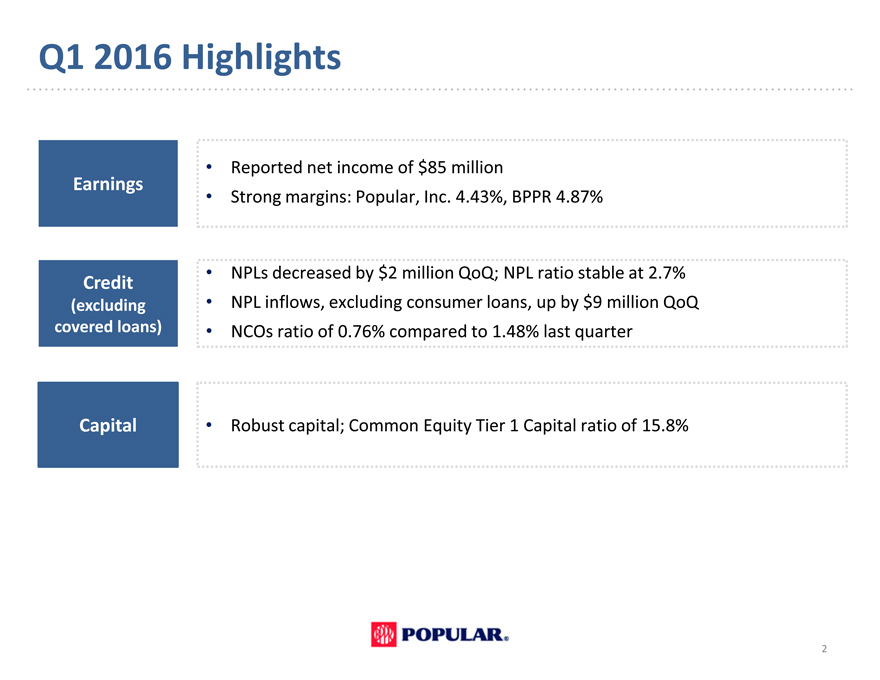

Reported net income of $85 million

Earnings

Strong margins: Popular, Inc. 4.43%, BPPR 4.87%

Credit NPLs decreased by $2 million QoQ; NPL ratio stable at 2.7%

(excluding NPL inflows, excluding consumer loans, up by $9 million QoQ

covered loans) NCOs ratio of 0.76% compared to 1.48% last quarter

Capital Robust capital; Common Equity Tier 1 Capital ratio of 15.8%

2

|

|

P.R. Public Sector Exposure

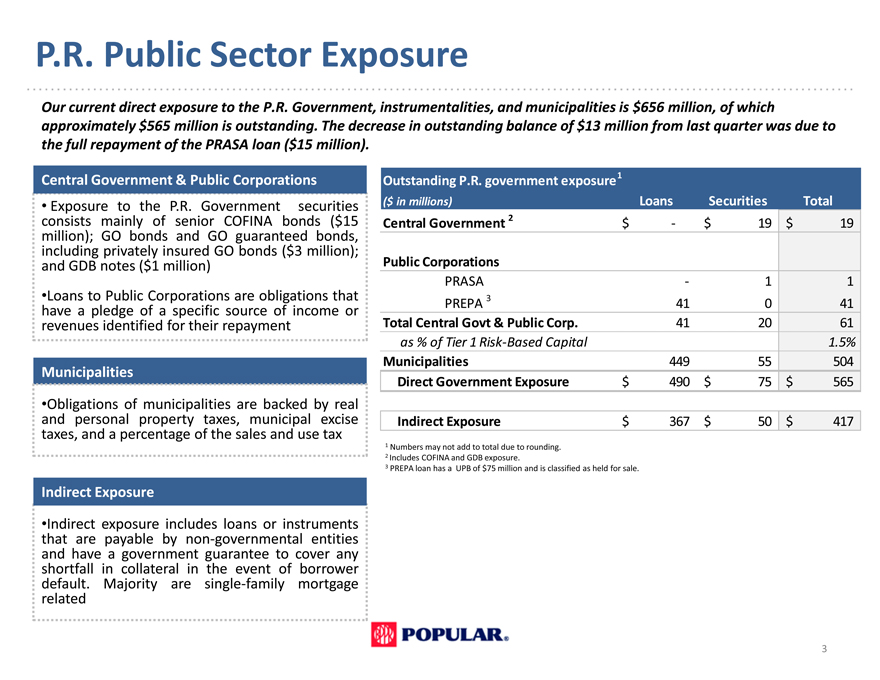

Our current direct exposure to the P.R. Government, instrumentalities, and municipalities is $656 million, of which approximately $565 million is outstanding. The decrease in outstanding balance of $13 million from last quarter was due to

the full repayment of the PRASA loan ($15 million).

Central Government & Public Corporations

Exposure to the P.R. Government securities consists mainly of senior COFINA bonds ($15 million); GO bonds and GO guaranteed bonds, including privately insured GO bonds ($3 million); and GDB notes ($1 million)

Loans to Public Corporations are obligations that have a pledge of a specific source of income or revenues identified for their repayment

Municipalities

Obligations of municipalities are backed by real and personal property taxes, municipal excise taxes, and a percentage of the sales and use tax

Indirect Exposure

Indirect exposure includes loans or instruments that are payable by non-governmental entities and have a government guarantee to cover any shortfall in collateral in the event of borrower default. Majority are single-family mortgage related

Outstanding P.R. government exposure 1

($ in millions) Loans Securities Total

Central Government 2 $—$ 19 $ 19

Public Corporations

PRASA—1 1

PREPA 3 41 0 41

Total Central Govt & Public Corp. 41 20 61

as % of Tier 1 Risk-Based Capital 1.5%

Municipalities 449 55 504

Direct Government Exposure $ 490 $ 75 $ 565

Indirect Exposure $ 367 $ 50 $ 417

1 Numbers may not add to total due to rounding. 2 Includes COFINA and GDB exposure.

3 PREPA loan has a UPB of $75 million and is classified as held for sale.

3

|

|

Financial Summary

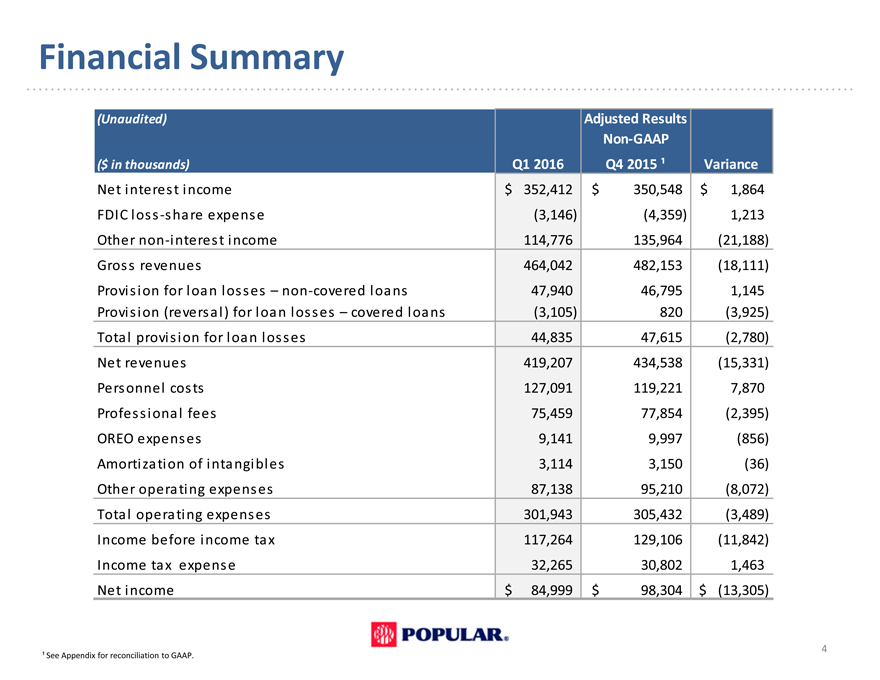

(Unaudited) Adjusted Results

Non-GAAP

($ in thousands) Q1 2016 Q4 2015 Variance

Net interest income $ 352,412 $ 350,548 $ 1,864

FDIC loss -share expense(3,146)(4,359) 1,213

Other non -interest income 114,776 135,964(21,188)

Gross revenues 464,042 482,153(18,111)

Provision for loan losses non -covered loans 47,940 46,795 1,145

Provision (reversal) for loan losses covered loans(3,105) 820(3,925)

Total provision for loan losses 44,835 47,615(2,780)

Net revenues 419,207 434,538(15,331)

Personnel costs 127,091 119,221 7,870

Professional fees 75,459 77,854(2,395)

OREO expenses 9,141 9,997(856)

Amortization of intangibles 3,114 3,150(36)

Other operating expenses 87,138 95,210(8,072)

Total operating expenses 301,943 305,432(3,489)

Income before income tax 117,264 129,106(11,842)

Income tax expense 32,265 30,802 1,463

Net income $ 84,999 $ 98,304 $(13,305)

See Appendix for reconciliation to GAAP.

4

|

|

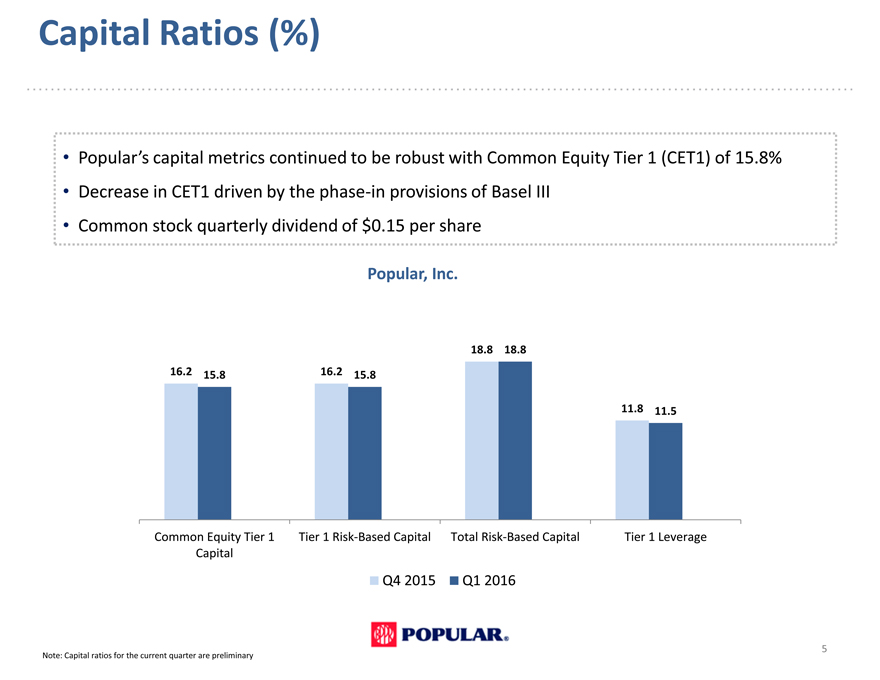

Capital Ratios (%)

Populars capital metrics continued to be robust with Common Equity Tier 1 (CET1) of 15.8%

Decrease in CET1 driven by the phase-in provisions of Basel III

Common stock quarterly dividend of $0.15 per share

Popular, Inc.

18.8 18.8

16.2 15.8 16.2 15.8

11.8 11.5

Common Equity Tier 1 Tier 1 Risk-Based Capital Total Risk-Based Capital Tier 1 Leverage

Capital

Q4 2015 Q1 2016

Note: Capital ratios for the current quarter are preliminary

5

|

|

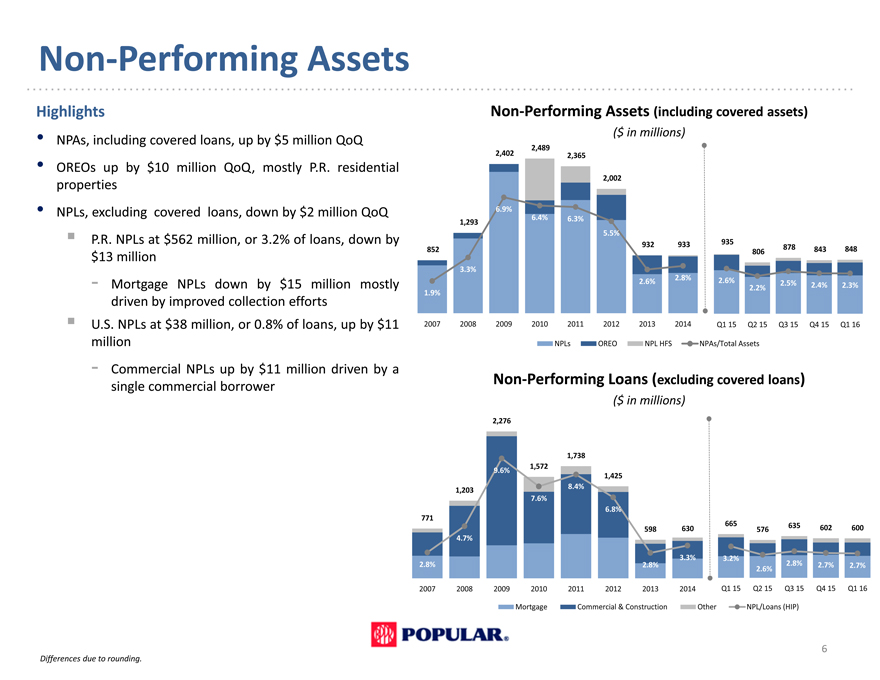

Non-Performing Assets

Highlights

NPAs, including covered loans, up by $5 million QoQ

OREOs up by $10 million QoQ, mostly P.R. residential

properties

NPLs, excluding covered loans, down by $2 million QoQ

P.R. NPLs at $562 million, or 3.2% of loans, down by

$13 million

- Mortgage NPLs down by $15 million mostly

driven by improved collection efforts

U.S. NPLs at $38 million, or 0.8% of loans, up by $11

million

- Commercial NPLs up by $11 million driven by a

single commercial borrower

Non-Performing Assets (including covered assets)

($ in millions)

2,489

2,402 2,365

2,002

6.9%

1,293 6.4% 6.3%

5.5%

935

852 932 933 806 878 843 848

3.3%

2.6% 2.8% 2.6% 2.5% 2.4% 2.3%

2.2%

1.9%

2007 2008 2009 2010 2011 2012 2013 2014 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

NPLs OREO NPL HFS NPAs/Total Assets

Non-Performing Loans (excluding covered loans)

($ in millions) 14.0%

2,276 12.0%

1,738 10.0%

9.6% 1,572

1,425 8.0%

1,203 8.4%

7.6%

6.8% 6.0%

771

598 630 665 576 635 602 600

4.7% 4.0%

3.3% 3.2%

2.8% 2.8% 2.8% 2.7% 2.7% 2.0%

2.6%

2007 2008 2009 2010 2011 2012 2013 2014 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 0.0%

Mortgage Commercial & Construction Other NPL/Loans (HIP)

6

Differences due to rounding.

|

|

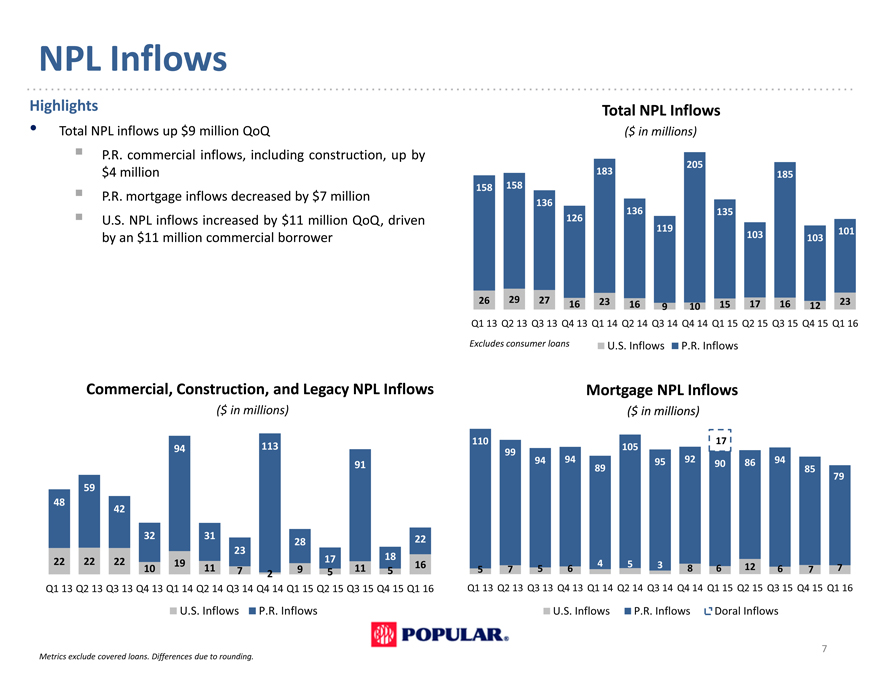

NPL Inflows

Highlights

Total NPL inflows up $9 million QoQ

P.R. commercial inflows, including construction, up by

$4 million

P.R. mortgage inflows decreased by $7 million

U.S. NPL inflows increased by $11 million QoQ

driven by an $11 million commercial borrower

Commercial, Construction, and Legacy NPL Inflows

($ in millions)

94 113

91

59

48

42

32 31 28 22

23

22 22 22 19 17 18 16

10 11 7 2 9 5 11 5

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 U.S. Inflows P.R. Inflows

Total NPL Inflows

($ in millions)

205

183 185

158 158

136

136 135

126

119 101

103 103

26 29 27 16 23 16 9 10 15 17 16 12 23

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Excludes consumer loans U.S. Inflows P.R. Inflows

Mortgage NPL Inflows

($ in millions)

110 17

99 105

94 94 95 92 90 86 94

89 85

79

5 7 5 6 4 5 3 8 6 12 6 7 7

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

U.S. Inflows P.R. Inflows Doral Inflows

7

Metrics exclude covered loans. Differences due to rounding.

|

|

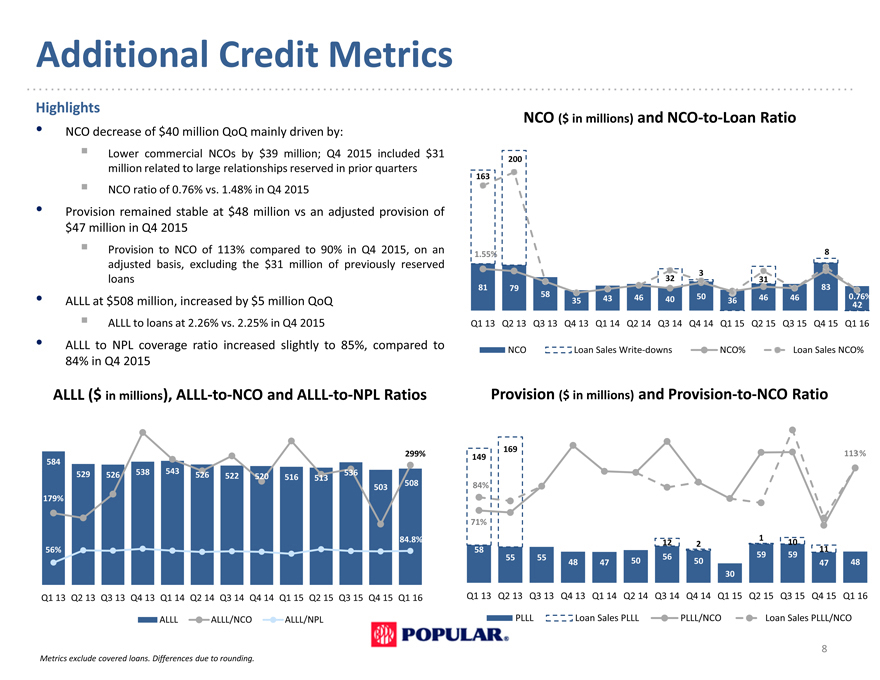

Additional Credit Metrics

Highlights

NCO decrease of $40 million QoQ mainly driven by:

Lower commercial NCOs by $39 million; Q4 2015 included $31

million related to large relationships reserved in prior quarters

NCO ratio of 0.76% vs. 1.48% in Q4 2015

Provision remained stable at $48 million vs an adjusted provision of

$47 million in Q4 2015

Provision to NCO of 113% compared to 90% in Q4 2015, on an

adjusted basis, excluding the $31 million of previously reserved

loans

ALLL at $508 million, increased by $5 million QoQ

ALLL to loans at 2.26% vs. 2.25% in Q4 2015

ALLL to NPL coverage ratio increased slightly to 85%, compared to

84% in Q4 2015

ALLL ($ in millions), ALLL-to-NCO and ALLL-to-NPL Ratios

299%

584

529 526 538 543 526 522 520 516 513 536

503 508

179%

84.8%

56%

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

ALLL ALLL/NCO ALLL/NPL

NCO ($ in millions) and NCO-to-Loan Ratio

200

163

1.55% 8

3

32 31

81 79 83

58 35 43 46 40 50 36 46 46 0.76%

42

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

NCO Loan Sales Write-downs NCO% Loan Sales NCO%

Provision ($ in millions) and Provision-to-NCO Ratio

169

149 113%

84%

71%

1

12 2 10

58 11

55 55 56 59 59

48 47 50 50 47 48

30

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

PLLL Loan Sales PLLL PLLL/NCO Loan Sales PLLL/NCO

8

Metrics exclude covered loans. Differences due to rounding.

|

|

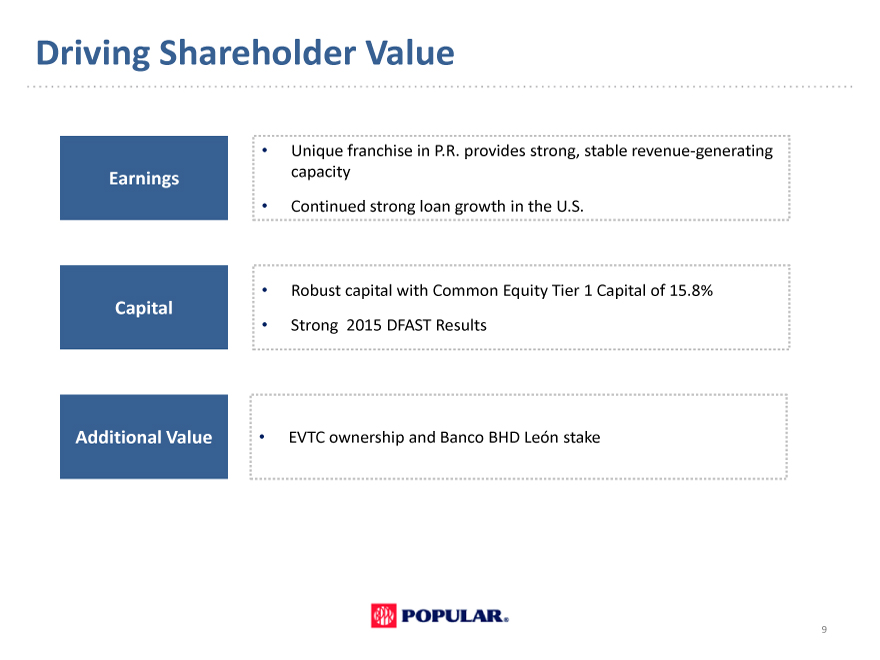

Driving Shareholder Value

Unique franchise in P.R. provides strong, stable revenue-generating

Earnings capacity

Continued strong loan growth in the U.S.

Robust capital with Common Equity Tier 1 Capital of 15.8%

Capital

Strong 2015 DFAST Results

Additional Value EVTC ownership and Banco BHD León stake

9

|

|

Investor

Presentation

First Quarter

2016

APPENDIX

|

|

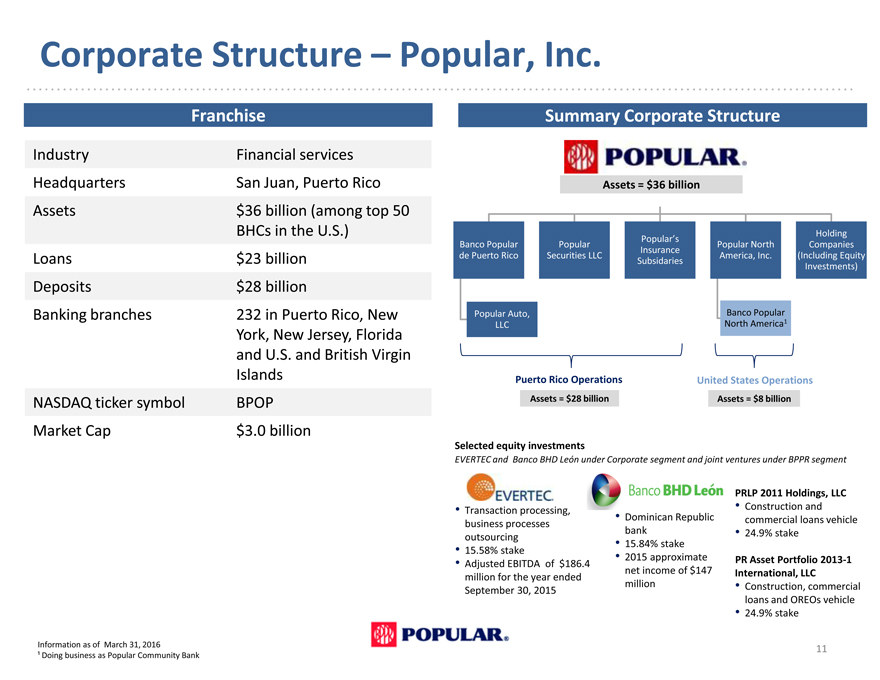

Who We Are Popular, Inc.

Corporate Structure Popular, Inc.

Franchise

Industry Financial services

Headquarters San Juan, Puerto Rico

Assets $36 billion (among top 50

BHCs in the U.S.)

Loans $23 billion

Deposits $28 billion

Banking branches 232 in Puerto Rico, New

York, New Jersey, Florida

and U.S. and British Virgin

Islands

NASDAQ ticker symbol BPOP

Market Cap $3.0 billion

Information as of March 31, 2016

Doing business as Popular Community Bank

Summary Corporate Structure

Assets = $36 billion

Populars Holding

Banco Popular Popular Popular North Companies

Insurance

de Puerto Rico Securities LLC America, Inc.(Including Equity

Subsidaries Investments)

Popular Auto, Banco Popular

LLC North America1

Puerto Rico Operations

Assets = $28 billion

United States Operations

Assets = $8 billion

Selected equity investments

EVERTEC and Banco BHD Len under Corporate segment and joint ventures under BPPR segment

[Graphic Appears Here]

Transaction processing,

business processes

outsourcing

15.58% stake

Adjusted EBITDA of $186.4

million for the year ended

September 30, 2015

[Graphic Appears Here]

Dominican Republic

bank

15.84% stake

2015 approximate

net income of $147

million

PRLP 2011 Holdings, LLC

Construction and

commercial loans vehicle

24.9% stake

PR Asset Portfolio 2013-1 International, LLC

Construction, commercial

loans and OREOs vehicle

24.9% stake

11

|

|

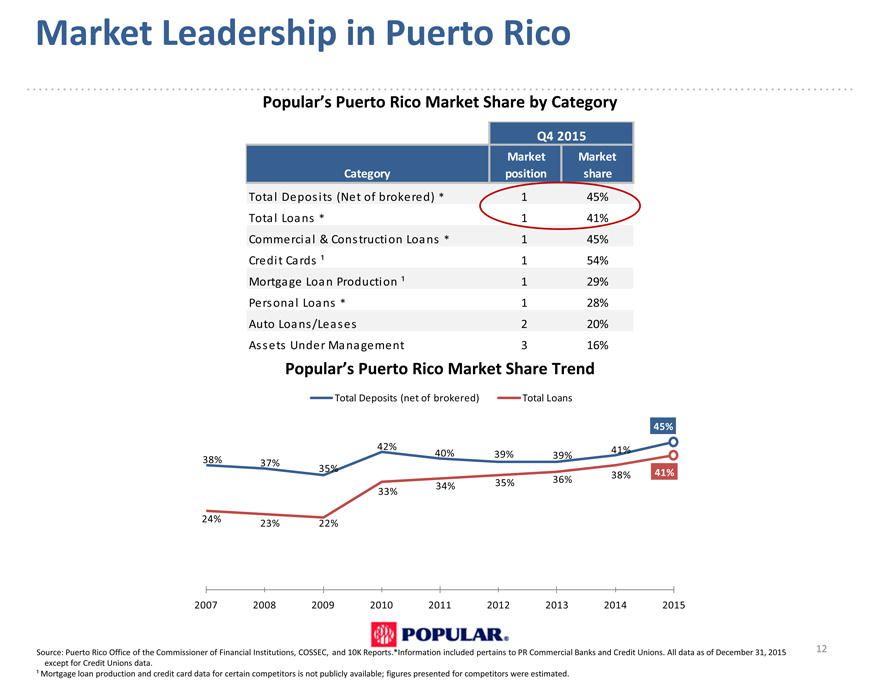

Market Leadership in Puerto Rico

Populars Puerto Rico Market Share by Category

Q4 2015

Market Market

Category position share

Total Deposits (Net of brokered) * 1 45%

Total Loans * 1 41%

Commercial & Construction Loans * 1 45%

Credit Cards 1 54%

Mortgage Loan Production 1 29%

Personal Loans * 1 28%

Auto Loans/Leases 2 20%

Assets Under Management 3 16%

Populars Puerto Rico Market Share Trend

Total Deposits (net of brokered) Total Loans

45%

42% 41%

40% 39% 39%

38% 37%

35% 38% 41%

36%

33% 34% 35%

24% 23% 22%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Puerto Rico Office of the Commissioner of Financial Institutions, COSSEC, and 10K Reports.*Information included pertains to PR Commercial Banks and Credit Unions. All data as of December 31, 2015 12

except for Credit Unions data.

Mortgage loan production and credit card data for certain competitors is not publicly available; figures presented for competitors were estimated.

|

|

De-Risked Loan Portfolios

(Excluding covered loans) ($ in millions)

Highlights

The Corporation has de-risked its loan portfolios by

reducing its exposure to asset classes with historically

high loss content

The P.R. commercial portfolio reductions include:

Commercial portfolio, including construction, has

decreased from 55% of total loans held-in-portfolio

to 43%

Construction portfolio is down by 91% since Q4

2007

SME1 lending is down by 47% from Q4 2007

Collateralized exposure now represents a larger portion

of consumer loan portfolio

Unsecured loan credit quality has improved as overall

FICO scores have increased

Note: Numbers may not add to total due to rounding.

Loan Composition (Held-in Portfolio)

P.R. U.S. Total

$ in millions Q4 2007 Q1 2016 Q4 2007 Q1 2016 Q4 2007 Q1 2016 Variance

Commercial $7,774 $7,368 $4,515 $2,860 $ 12,288 $ 10,228($2,060)

Consumer 3,552 3,309 1,698 552 5,249 3,861(1,388)

Mortgage 2,933 6,100 3,139 879 6,071 6,979 908

Construction 1,231 105 237 630 1,468 735(733)

Leases 814 643 — 814 643(171)

Legacy — 2,130 61 2,130 61(2,069)

Total $16,304 $17,525 $11,718 $4,982 $ 28,021 $ 22,508($5,514)

P.R. Commercial & Construction Distribution

Q4 2007 Q1 2016 Variance NCOs

($mm)(%)($mm)(%)($mm)(%) Distribution 2

CRE SME 1 $2,938 33% $1,983 27%($955) -32% 25%

C&I SME 1 2,287 25% 762 10%(1,525) -67% 29%

C&I Corp 1,592 18% 1,905 25% 313 20% 6%

Construction 1,231 14% 105 1%(1,126) -91% 35%

CRE Corp 892 10% 2,544 34% 1,652 185% 5%

Multifamily 64 1% 175 2% 111 173% 1%

Total $9,004 $7,473($1,531) -17% 100%

1 Small and Medium Enterprise

2 NCOs distribution represents the percentage allocation of net charge-offs from Q1 2008 through Q1 2016 per each loan category, excluding net charge-offs from previously covered loans up to Q2 2015.

13

|

|

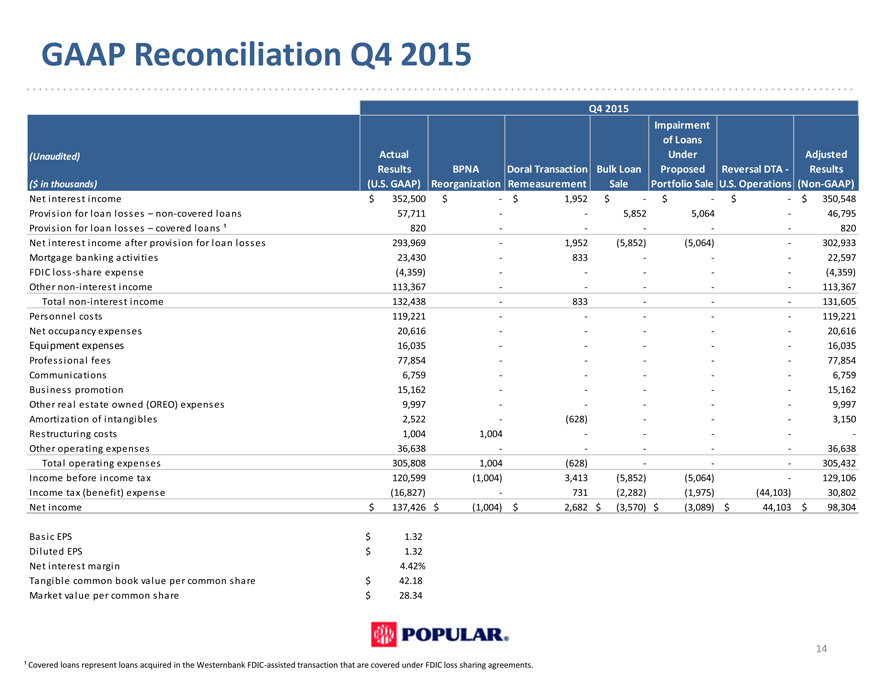

GAAP Reconciliation Q4 2015

Q4 2015

Impairment

of Loans

(Unaudited) Actual Under Adjusted

Results BPNA Doral Transaction Bulk Loan Proposed Reversal DTA—Results

($ in thousands)(U.S. GAAP) Reorganization Remeasurement Sale Portfolio Sale U.S. Operations (Non-GAAP)

Net interest income $ 352,500 $—$ 1,952 $—$—$—$ 350,548

Provision for loan losses non-covered loans 57,711 — 5,852 5,064—46,795

Provision for loan losses covered loans 820 — ——820

Net interest income after provision for loan losses 293,969—1,952(5,852)(5,064)—302,933

Mortgage banking activities 23,430—833 ——22,597

FDIC loss -share expense(4,359) — — -(4,359)

Other non-interest income 113,367 — ——113,367

Total non-interest income 132,438—833 ——131,605

Personnel costs 119,221 — ——119,221

Net occupancy expenses 20,616 — ——20,616

Equipment expenses 16,035 — ——16,035

Professional fees 77,854 — ——77,854

Communications 6,759 — ——6,759

Business promotion 15,162 — ——15,162

Other real estate owned (OREO) expenses 9,997 — ——9,997

Amortization of intangibles 2,522 -(628) ——3,150

Restructuring costs 1,004 1,004 — — -

Other operating expenses 36,638 — ——36,638

Total operating expenses 305,808 1,004(628) ——305,432

Income before income tax 120,599(1,004) 3,413(5,852)(5,064)—129,106

Income tax (benefit) expense(16,827)—731(2,282)(1,975)(44,103) 30,802

Net income $ 137,426 $(1,004) $ 2,682 $(3,570) $(3,089) $ 44,103 $ 98,304

Basic EPS $ 1.32

Diluted EPS $ 1.32

Net interest margin 4.42%

Tangible common book value per common share $ 42.18

Market value per common share $ 28.34

14

Covered loans represent loans acquired in the Westernbank FDIC-assisted transaction that are covered under FDIC loss sharing agreements.

|

|

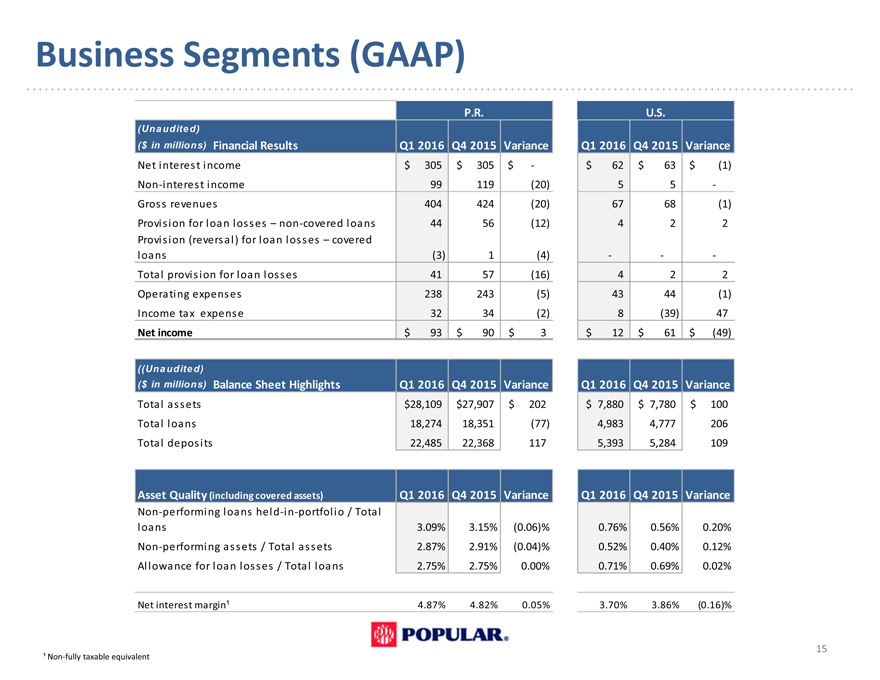

Business Segments (GAAP)

P.R. U.S.

(Una udite d)

($ in millions) Financial Results Q1 2016 Q4 2015 Variance Q1 2016 Q4 2015 Variance

Net interest income $ 305 $ 305 $—$ 62 $ 63 $(1)

Non-interest income 99 119(20) 5 5 -

Gross revenues 404 424(20) 67 68(1)

Provision for loan losses non-covered loans 44 56(12) 4 2 2

Provision (reversal) for loan losses covered

loans(3) 1(4) — -

Total provision for loan losses 41 57(16) 4 2 2

Operating expenses 238 243(5) 43 44(1)

Income tax expense 32 34(2) 8(39) 47

Net income $ 93 $ 90 $ 3 $ 12 $ 61 $(49)

((Una udite d)

($ in millions) Balance Sheet Highlights Q1 2016 Q4 2015 Variance Q1 2016 Q4 2015 Variance

Total assets $28,109 $27,907 $ 202 $ 7,880 $ 7,780 $ 100

Total loans 18,274 18,351(77) 4,983 4,777 206

Total deposits 22,485 22,368 117 5,393 5,284 109

Asset Quality (including covered assets) Q1 2016 Q4 2015 Variance Q1 2016 Q4 2015 Variance

Non-performing loans held-in-portfolio / Total

loans 3.09% 3.15%(0.06)% 0.76% 0.56% 0.20%

Non-performing assets / Total assets 2.87% 2.91%(0.04)% 0.52% 0.40% 0.12%

Allowance for loan losses / Total loans 2.75% 2.75% 0.00% 0.71% 0.69% 0.02%

Net interest margin 4.87% 4.82% 0.05% 3.70% 3.86%(0.16)%

15

Non-fully taxable equivalent

|

|

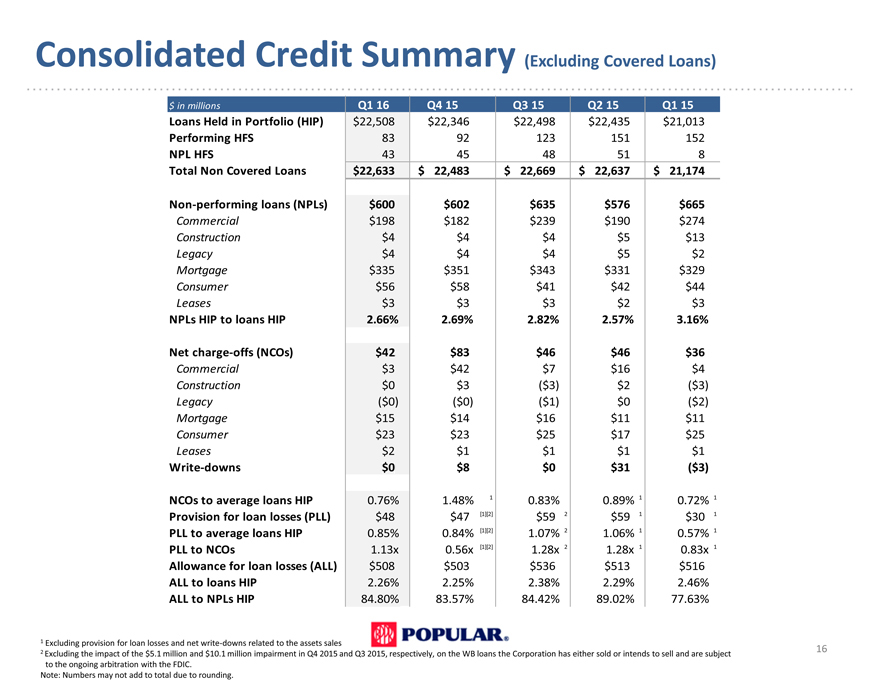

Consolidated Credit Summary (Excluding Covered Loans)

$ in millions Q1 16 Q4 15 Q3 15 Q2 15 Q1 15

Loans Held in Portfolio (HIP) $22,508 $22,346 $22,498 $22,435 $21,013

Performing HFS 83 92 123 151 152

NPL HFS 43 45 48 51 8

Total Non Covered Loans $22,633 $ 22,483 $ 22,669 $ 22,637 $ 21,174

Non-performing loans (NPLs) $600 $602 $635 $576 $665

Commercial $198 $182 $239 $190 $274

Construction $4 $4 $4 $5 $13

Legacy $4 $4 $4 $5 $2

Mortgage $335 $351 $343 $331 $329

Consumer $56 $58 $41 $42 $44

Leases $3 $3 $3 $2 $3

NPLs HIP to loans HIP 2.66% 2.69% 2.82% 2.57% 3.16%

Net charge-offs (NCOs) $42 $83 $46 $46 $36

Commercial $3 $42 $7 $16 $4

Construction $0 $3($3) $2($3)

Legacy($0)($0)($1) $0($2)

Mortgage $15 $14 $16 $11 $11

Consumer $23 $23 $25 $17 $25

Leases $2 $1 $1 $1 $1

Write-downs $0 $8 $0 $31($3)

NCOs to average loans HIP 0.76% 1.48% 1 0.83% 0.89% 1 0.72% 1

Provision for loan losses (PLL) $48 $47 [1][2] $59 2 $59 1 $30 1

PLL to average loans HIP 0.85% 0.84% [1][2] 1.07% 2 1.06% 1 0.57% 1

PLL to NCOs 1.13x 0.56x [1][2] 1.28x 2 1.28x 1 0.83x 1

Allowance for loan losses (ALL) $508 $503 $536 $513 $516

ALL to loans HIP 2.26% 2.25% 2.38% 2.29% 2.46%

ALL to NPLs HIP 84.80% 83.57% 84.42% 89.02% 77.63%

1 Excluding provision for loan losses and net write-downs related to the assets sales

2 Excluding the impact of the $5.1 million and $10.1 million impairment in Q4 2015 and Q3 2015, respectively, on the WB loans the Corporation has either sold or intends to sell and are subject 16

to the ongoing arbitration with the FDIC.

Note: Numbers may not add to total due to rounding.

|

|

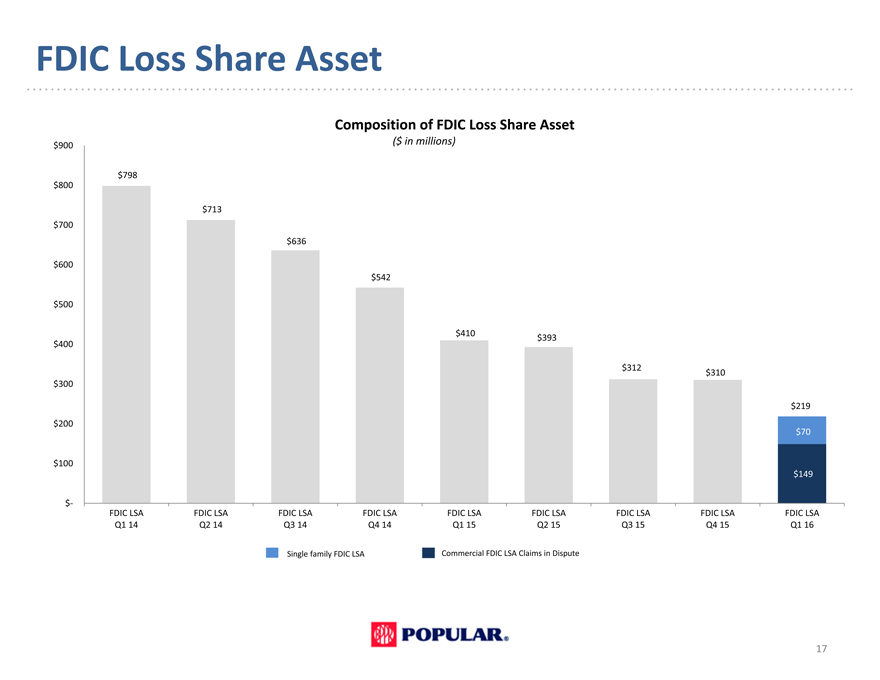

FDIC Loss Share Asset

Composition of FDIC Loss Share Asset

$900($ in millions)

$798

$800

$713

$700

$636

$600

$542

$500

$410 $393

$400

$312 $310

$300

$219

$200

$70

$100

$149

$-

FDIC LSA FDIC LSA FDIC LSA FDIC LSA FDIC LSA FDIC LSA FDIC LSA FDIC LSA FDIC LSA

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Single family FDIC LSA Commercial FDIC LSA Claims in Dispute

17

|

|

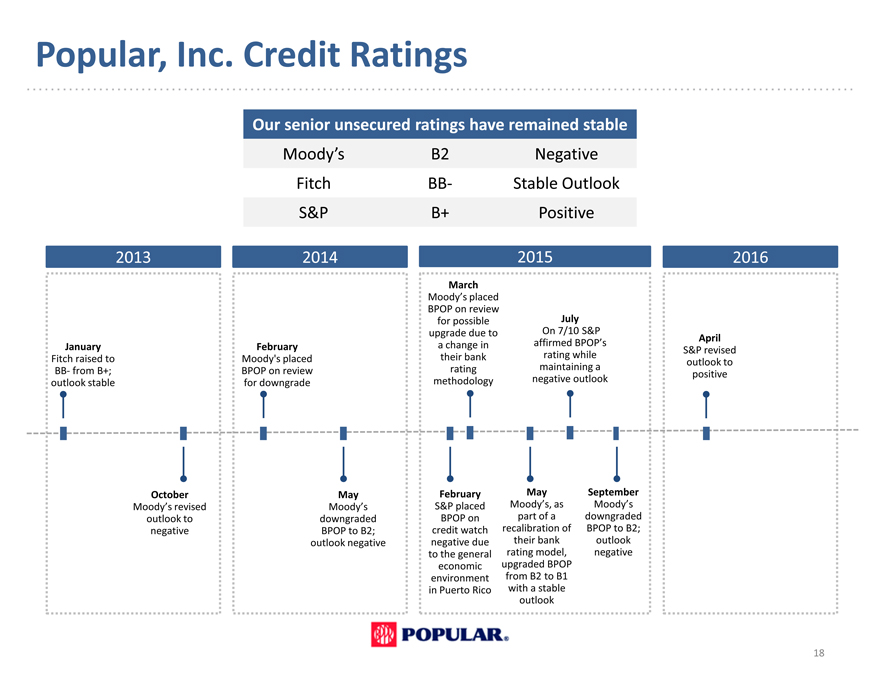

Popular, Inc. Credit Ratings

Our senior unsecured ratings have remained stable

Moodys B2 Negative

Fitch BB- Stable Outlook

S&P B+ Positive

2013 2014 2015 2016

March

Moodys placed

BPOP on review

for possible July

upgrade due to On 7/10 S&P

January February a change in affirmed BPOPs April

S&P revised

Fitch raised to Moody’s placed their bank rating while outlook to

BB- from B+; BPOP on review rating maintaining a

positive

outlook stable for downgrade methodology negative outlook

October May February May September

Moodys revised Moodys S&P placed Moodys, as Moodys

outlook to downgraded BPOP on part of a downgraded

negative BPOP to B2; credit watch recalibration of BPOP to B2;

outlook negative negative due their bank outlook

to the general rating model, negative

economic upgraded BPOP

environment from B2 to B1

in Puerto Rico with a stable

outlook

18

|

|

Investor

Presentation

First Quarter 2016