Attached files

| file | filename |

|---|---|

| EX-21 - ASPIRITY HOLDINGS LLC | ex21.htm |

| EX-3.1 - ASPIRITY HOLDINGS LLC | ex3-1.htm |

| EX-4.1 - ASPIRITY HOLDINGS LLC | ex4-1.htm |

| EX-10.2 - ASPIRITY HOLDINGS LLC | ex10-2.htm |

| EX-32.1 - ASPIRITY HOLDINGS LLC | ex32-1.htm |

| EX-12.2 - ASPIRITY HOLDINGS LLC | ex12-2.htm |

| EX-12.1 - ASPIRITY HOLDINGS LLC | ex12-1.htm |

| EX-23.1 - ASPIRITY HOLDINGS LLC | ex23-1.htm |

| EX-31.1 - ASPIRITY HOLDINGS LLC | ex31-1.htm |

| EX-10.11 - ASPIRITY HOLDINGS LLC | ex10-11.htm |

| EX-10.12 - ASPIRITY HOLDINGS LLC | ex10-12.htm |

| EX-31.2 - ASPIRITY HOLDINGS LLC | ex31-2.htm |

UNITED STATES OF AMERICA

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015

or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from __ to __

Commission File Number: 333-203994

Aspirity Holdings, LLC

(Exact name of registrant as specified in its charter)

| Minnesota | 27-1658449 | |

| (State of organization) | (IRS Employer Identification Number) |

701 Xenia Avenue, Suite 475

Minneapolis, Minnesota 55416

(Address of principal executive offices, zip code)

(763) 432-1500

(Registrant’s telephone number, including area code)

| Securities registered under Sections 12(b) or 12(g) of the Act | Name of each exchange on which registered | |

| None | None |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act

$75,000,000

3 and 6 Month and 1, 2, 3, 4, 5 and 10 Year Renewable Unsecured Subordinated Notes

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation ST (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or smaller reporting company. See definition of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer [] Accelerated filer [] Non-accelerated filer [ ] Smaller reporting company [X]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

TABLE OF CONTENTS

| i |

| Abbreviation

or acronym |

Definition | |

| ABACCUS | The Annual Baseline Assessment of Choice in Canada and the United States is a study of U.S. states and Canadian provinces with respect to their efforts and achievements in the promotion of a competitive retail electric sector. The annual studies are prepared by DEFG, LLC, a management consulting firm specializing in energy | |

| AEMS | Aspirity Energy Mid States, LLC, a wholly owned subsidiary of Aspirity Energy | |

| AENE | Aspirity Energy Northeast, LLC, a wholly owned subsidiary of Aspirity Energy | |

| AES | Aspirity Energy South, LLC, a wholly owned subsidiary of Aspirity Energy | |

| AESO | Alberta Electric System Operator, a statutory corporation of the Province of Alberta, is an ISO serving the Alberta Interconnected Electric System | |

| AOCI | Accumulated other comprehensive income | |

| Angell | Angell Energy, LLC, a Texas limited liability company that purchased TCP and SUM on June 1, 2015. | |

| Apollo | Apollo Energy Services, LLC, a wholly-owned, first-tier subsidiary of Krieger Enterprises, LLC | |

| ASC | Accounting Standards Codification | |

| Aspirity or the Company | Aspirity Holdings LLC, formerly known as Twin Cities Power Holdings, LLC, and its subsidiaries | |

| Aspirity Energy | Aspirity Energy LLC, a wholly owned subsidiary of Aspirity | |

| Aspirity Financial | Aspirity Financial LLC, a wholly owned subsidiary of Aspirity | |

| ASU | Accounting Standards Update | |

| BLS | Bureau of Labor Statistics, an agency within the U.S. Department of Labor | |

| Btu; therm; MMBtu | A “Btu” or British thermal unit is a measure of thermal energy or the amount of heat needed to raise the temperature of one pound of water from 39°F to 40°F. A “therm” is one hundred thousand Btu. One “MMBtu” is one million Btu. | |

| CEF | Cygnus Energy Futures, LLC, a wholly-owned subsidiary of CP and a second-tier subsidiary of Enterprises | |

| CFTC | Commodity Futures Trading Commission, an independent agency of the United States government that regulates futures and option markets | |

| CHP | Abbreviates “combined heat and power”, a type of generating facility | |

| CME | CME Group Inc. operates the CME (Chicago Mercantile Exchange), CBOT (Chicago Board of Trade), NYMEX (New York Mercantile Exchange), and COMEX (Commodities Exchange) derivatives exchanges and also offers certain cleared over-the-counter products and services |

| 1 |

| Abbreviation or acronym | Definition | |

| CoV | Abbreviates the coefficient of variation, a simple measure of volatility useful for comparing two or more data series; equal to the standard deviation divided by the mean | |

| CP | Cygnus Partners, LLC, a wholly-owned, first-tier subsidiary of Enterprises | |

| CSE | Comparison shopping engine, a web site that compares prices for specific products. While most comparison shopping engines do not offer the products or services themselves, some may earn commissions when users follow the links in the search results and make a purchase from an online vendor | |

| CTG | Chesapeake Trading Group, LLC, a wholly-owned subsidiary of Enterprises | |

| Cyclone | Cyclone Partners, LLC, a wholly-owned, first-tier subsidiary of Enterprises | |

Degree-days; CDD; HDD |

A “degree-day” compares outdoor temperatures to a standard of 65°F. Hot days require energy for cooling and are measured in cooling degree-days or “CDD” while cold days require energy for heating and are measured in heating degree-days or “HDD”. For example, a day with a mean temperature of 80°F would result in 15 CDD and a day with a mean temperature of 40°F would result in 25 HDD.

If heating degree-days are less than the average for an area for a period, the weather was “warmer than normal”; if they were greater, it was “colder than normal”. The converse is true for cooling degree-days - if CDD are less than the average for an area for a period, the weather was “colder than normal”; if they were greater, it was “warmer than normal”. | |

| Distribution | That certain distribution of 100% of the equity of Enterprises to the members of Aspirity as the final step of the Restructuring. | |

| Distribution Date | The date of the Distribution is the date that the registration statement was declared effective by the SEC (November 12, 2015); for tax and accounting purposes, November 1, 2015. | |

| DOE | U.S. Department of Energy | |

| EDC; LDC | Energy distribution company, may also be known as a local distribution company; see also “electric utility” | |

| EDI compliant | In order for a licensed competitive electricity supplier to sell to, bill, and collect from retail customers within a given utility’s service territory, it must establish an electronic connection or become “EDI compliant” with such utility | |

| EEI | The Edison Electric Institute is a trade association representing U.S. investor-owned electric companies. Its 160 U.S. operating utility and parent company members provide electricity for 220 million Americans, operate in all 50 states and the District of Columbia, and directly employ more than 500,000 workers. The association also has 70 international electric company members and 270 industry suppliers and related organizations as associate members |

| 2 |

| Abbreviation or acronym | Definition | |

| EIA | Energy Information Administration, an independent agency within DOE | |

| Electric utility | A corporation, person, agency, authority, or other legal entity or instrumentality aligned with distribution facilities for delivery of electric energy for use primarily by the public such as investor-owned utilities (“IOUs”), municipally-owned utilities (“munis”), utilities owned by states or political subdivisions thereof (“POUs”), federal utilities, and rural electric cooperatives (“co-ops”). A few entities that are tariff based and corporately aligned with companies that own distribution facilities are also included. | |

| Enterprises | Krieger Enterprises, LLC, a former first tier subsidiary of Aspirity, the equity interests of which were distributed to the then members of the Company on the Distribution Date | |

| ERCOT | Electric Reliability Council of Texas, an ISO managing about 85% of the electric Load of Texas and subject to oversight by the Public Utility Commission of Texas and the Texas Legislature but not FERC | |

| Exelon | Exelon Generation Company, LLC, a Pennsylvania limited liability company and wholly-owned subsidiary of Exelon Corporation | |

| FASB | Financial Accounting Standards Board | |

| FERC | Federal Energy Regulatory Commission, an independent regulatory agency within DOE | |

| FTR | Financial Transmission Rights are financial instruments traded in certain ISOs and RTOs that entitle their holders to receive or pay charges based on congestion price differences in the day-ahead energy market across specific transmission paths. The value of an FTR reflects the difference in congestion prices rather than the difference in locational marginal prices, which includes energy, congestion, and marginal losses. FTRs are specified between any two pricing nodes on the system, including hubs, control zones, aggregates, generator buses, load buses and interface pricing points. FTRs are generally available in increments of 0.1 MW and for periods ranging from 1 month to multiple years. The value of an FTR can be positive or negative depending on the sink minus source congestion price difference, with a negative differences resulting in liability for the holder. | |

| GAAP | Generally accepted accounting principles in the United States | |

| ICE | Intercontinental Exchange, Inc. is the leading global network of regulated exchanges and clearing houses for financial and commodity markets in the U.S., Canada, Europe, and Asia. In November 2013, ICE completed the acquisition of NYSE Euronext. | |

| INC and DEC | An increment offer or “INC” is an offer in the day-ahead market to sell energy at a specified source bus. An INC will clear if the LMP at the bus equals or exceeds the offer price. A decrement bid or “DEC” is a bid in the day-ahead market to purchase energy at a specified sink bus. A DEC will clear if the LMP at the bus does not exceed the bid price. | |

| IPP | An “independent power producer” or IPP is a corporation, person, agency, authority, or other legal entity or instrumentality that owns or operates facilities for the generation of electricity for use primarily by the public and that is not an electric utility. |

| 3 |

| Abbreviation or acronym | Definition | |

| ISO; RTO | An Independent System Operator or “ISO” is a non-profit organization formed at the direction or recommendation of FERC that coordinates, controls, and monitors the operation of a bulk electric power system. A Regional Transmission Organization or “RTO” typically performs the same functions as an ISO but covers a larger area. ISOs and RTOs may also operate centrally cleared wholesale markets for electric power quoted on both a “real-time” and “day ahead” basis. ISOs and RTOs are collectively referred to as ISOs. | |

| ISO-NE | ISO New England Inc., an RTO serving Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, and Vermont | |

| Legacy Businesses | The wholesale energy trading, real estate investments, investments in private companies, and legacy retail energy business operated by Enterprises, a former first tier subsidiary of the Company | |

| LMP | One of the unique aspects of FERC-regulated wholesale electricity markets is the availability of “locational marginal prices” or “LMPs”. The theoretical price of electricity at each node on a network is calculated based on the assumptions that one additional megawatt-hour of energy is demanded at the node in question, and the marginal cost to the system that would result from the re-dispatch of available generating units to serve such load can establish the production cost of the additional energy. LMPs are typically quoted on a “real-time” and “day-ahead” basis. In the real-time market, prices at specific nodes are updated every 5 minutes based on current and targeted supply and demand. Day-ahead prices are for power to be delivered at a specified hour and transmission point during the next day. LMPs vary by time and location due to physical system limitations, congestion, and loss factors; however, in an unconstrained system with no losses, all LMPs would be equal. This means that LMPs can be conceptually separated into three components - an energy price, a congestion component, and a loss component. | |

| MCF | One thousand cubic feet, a common unit of price measure for natural gas. In 2010, one MCF of natural gas had a heat content of 1,025 Btu. | |

| MISO | Midcontinent Independent System Operator, Inc., formerly the Midwest Independent Transmission System Operator, Inc., an RTO serving all or part of Arkansas, Illinois, Indiana, Iowa, Louisiana, Manitoba, Michigan, Minnesota, Mississippi, Missouri, Montana, North Dakota, South Dakota, Texas, and Wisconsin | |

| NERC | North American Electric Reliability Corporation, a non-profit corporation formed on March 28, 2006 as the successor to the National Electric Reliability Council, also known as NERC, formed in 1968. NERC is the designated Electric Reliability Organization (“ERO”) for the U.S. and operates under the auspices of FERC. | |

| S-1, Old and New | The Company’s Registration Statement on Form S-1, declared effective by the Securities and Exchange Commission on November 12, 2015 with respect to the Notes Offering is defined as the “New S-1”, while that declared effective on May 10, 2012 is defined as the “Old S-1” | |

| NGX | Natural Gas Exchange Inc., headquartered in Calgary, Alberta provides electronic trading, central counterparty clearing, and data services to the North American natural gas and electricity markets. NGX is wholly owned by TMX Group Inc. which collectively manages all aspects of Canada’s senior and junior equity markets. |

| 4 |

| Abbreviation or acronym | Definition | |

| NOAA | National Oceanic and Atmospheric Administration, an agency of the U.S. Department of Commerce | |

| Noble | Noble Conservation Solutions, Inc., a Minnesota corporation. On September 1, 2015, Enterprises purchased 60% of the outstanding shares of Noble. | |

| Notes | The Company’s Renewable Unsecured Subordinated Notes issued pursuant to its ongoing Notes Offering | |

| Notes Offering | The direct public offering the Company’s Notes pursuant to Registration Statements on Form S-1 | |

| NRSRO | A SEC-recognized Nationally Recognized Statistical Rating Organization; The major NRSROs that rate utilities are Standard & Poor’s Financial Services LLC (“S&P”), Moody’s Investor Services, Inc. (“Moody’s”), and Fitch Ratings Inc. (“Fitch”) | |

| NYISO | New York Independent System Operator, an ISO serving New York state | |

| Operating Agreement | Aspirity’s Amended and Restated Operating Agreement dated March 30, 2016 | |

| Prospectus | That prospectus dated November 12, 2015 as part of the New S-1, as supplemented from time to time | |

| PJM | PJM Interconnection, a RTO serving all or part of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia, and the District of Columbia | |

| POR; non-POR | All states with restructured retail markets have implemented laws and regulations with respect to permitted billing, credit, and collections practices. Some of these states require an EDC billing customers in their service territory on behalf of suppliers operating there to purchase the receivables generated as a result of energy sales, generally at a modest discount to reflect bad debt experience. These states are known as “purchase of receivables” or “POR” jurisdictions while those without this provision are known as “non-POR” areas | |

| PSA | A “preferred supply agreement” | |

| PURPA | Public Utilities Regulatory Policy Act of 1978 | |

| RECs | “Renewable energy certificates” represent the property rights to the environmental, social, and other non-power qualities of renewable electricity generation and can be sold separately from the underlying physical electricity. As renewable generators produce electricity, they create one REC per megawatt-hour. If the physical electricity and the associated RECs are sold to separate buyers, the electricity is no longer considered “renewable” or “green” as the REC is what conveys the attributes and benefits of the renewable electricity, not the electricity itself | |

| REH | Retail Energy Holdings, LLC, a wholly-owned, first-tier subsidiary of Enterprises |

| 5 |

| Abbreviation or acronym | Definition | |

| Restructuring | The restructuring of the Company that was approved by the Board on May 27, 2015 and was completed effective November 1, 2015 and effected the legal separation of the Legacy Businesses from the Company | |

| SEC | U.S. Securities and Exchange Commission, an independent agency of the United States government with primary responsibility for enforcing federal securities laws and regulating the securities industry and stock exchanges | |

| SUM | Summit Energy, LLC, a wholly-owned subsidiary of TCP | |

| TCE | Twin Cities Energy, LLC, an inactive, wholly-owned, first-tier subsidiary of Enterprises | |

| TCP | Twin Cities Power, LLC, formerly, a wholly-owned, first-tier subsidiary of the Company | |

| TCPC | Twin Cities Power – Canada, Ltd., an inactive, wholly-owned subsidiary of TCE and a second-tier subsidiary of Enterprises | |

| TCPH | Twin Cities Power Holdings, LLC | |

| Term Loan | Term Loan Agreement between Enterprises as borrower and Aspirity Financial as lender dated July 1, 2015, as amended on November 1, 2015 and January 27, 2016. Pursuant to the Term Loan, Enterprises borrowed an aggregate principal amount of $22,206,000 from Aspirity Financial. | |

| Term Loan Notes | Each of the Company’s Notes outstanding as of June 30, 2015 in an aggregate principal amount of $22,206,000, including any renewals of such Notes | |

| TSE | Town Square Energy, initially, an accounting division of TCP resulting from the acquisition of the business and assets of Community Power & Utility, LLC on June 29, 2012. Effective June 1, 2013, TSE became a wholly-owned first-tier subsidiary of the Company and on October 25, 2013, it became a wholly owned subsidiary of REH | |

| TSEC | Town Square Energy Canada, Ltd, a wholly-owned subsidiary of REH and a second-tier subsidiary of Enterprises | |

| TSEE | Town Square Energy East, LLC, formerly known as Discount Energy Group, LLC (“DEG”), a wholly-owned subsidiary of REH and a second-tier subsidiary of Enterprises | |

| Ultra Green | Ultra Green Packaging, Inc. develops, manufactures, and markets “ecopaper” products made from wheat straw, bamboo, or sugarcane fibers and bioplastic products made from cornstarch. Ultra Green’s ecopaper and bioplastic products are certified as biodegradable and sustainable, and are compostable in about 160 days. | |

| UTC | In an up-to-congestion or “UTC” transaction, a day-ahead market participant offers to inject energy at a specified source and simultaneously withdraw the same quantity at a specific sink at a maximum bid price difference between the two locations. The transaction will clear if the price differential between sink and source does not exceed the bid price. |

| 6 |

| Abbreviation or acronym | Definition | |

| VaR | Value-at-Risk is a measure of the risk of loss on a specific portfolio of financial assets. For a given portfolio, probability, and time horizon, VaR is the value at which the probability that a mark-to-market loss over the given time horizon exceeds the calculated value, assuming normal markets and no trading. For example, if a portfolio has a one-day, 5% VaR of $1 million, there is a 5% probability that the portfolio will fall in value by more than $1 million over a one-day period. | |

| Watt (W); Watt-hour (Wh) | Although in everyday usage, the terms “energy” and “power” are essentially synonyms, scientists, engineers, and the energy business distinguish between them. Technically, energy is the ability to do work, or move a mass a particular distance by the application of force while power is the rate at which energy is generated or consumed. | |

| In the case of electricity, power is measured in watts (W) and is equal to voltage or the difference in charge between two points multiplied by amperage also known as current or rate of electrical flow. The energy supplied or consumed by a circuit is measured in watt-hours (Wh). For example, when a light bulb with a power rating of 100W is turned on for one hour, the energy used is 100 watt-hours. This same amount of energy would light a 40-watt bulb for 2.5 hours or a 50-watt bulb for 2.0 hours. | ||

| Multiples of watts and watt-hours are measured using International Systems of Units (“SI”) conventions. For example: |

| Prefix | Symbol | Multiple (Number) | Value | |||||||

| kilo | k | one thousand (1,000) | 103 | |||||||

| mega | M | one million (1,000,000) | 106 | |||||||

| giga | G | one billion (1,000,000,000) | 109 | |||||||

| tera | T | one trillion (1,000,000,000,000) | 1012 | |||||||

| Kilowatt (kW) or kilowatt-hour (kWh): one thousand watts or watt-hours. Kilowatt-hours are typically used to measure residential energy consumption and retail prices. One kWh is equal to 3,412 Btu, but fuel with a heat content of 7,000 to 11,500 Btu must be consumed to generate and deliver one kWh of electricity. | ||

| Megawatt (MW) or megawatt-hour (MWh): one million watts or watt-hours or one thousand kilowatts or kilowatt-hours. Megawatts are typically used to measure electrical generation capacity and megawatt-hours are the pricing units used in the wholesale electricity market. |

| 7 |

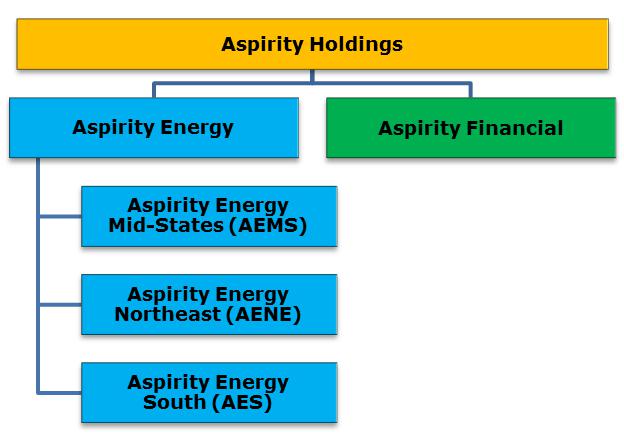

Aspirity Holdings (the “Company” or “Aspirity”), formerly known as Twin Cities Power Holdings, is a holding company that conducts its operations principally through wholly-owned subsidiaries. We currently have two direct operating subsidiaries, Aspirity Energy, which houses a start-up retail energy business, and Aspirity Financial, which was formed to provide energy-related financial services to businesses and households. Both subsidiaries are Minnesota limited liability companies as is the Company.

In 2015, we restructured as more fully described below. The Restructuring included the sale of two of our wholesale trading businesses and the spin-off of Krieger Enterprises, incorporating our three legacy business segments – wholesale trading, retail energy services, and diversified investments.

As a result, we currently have limited operations and assets although we are largely isolated from the inherent earnings volatility and regulatory exposure associated with the wholesale electricity markets.

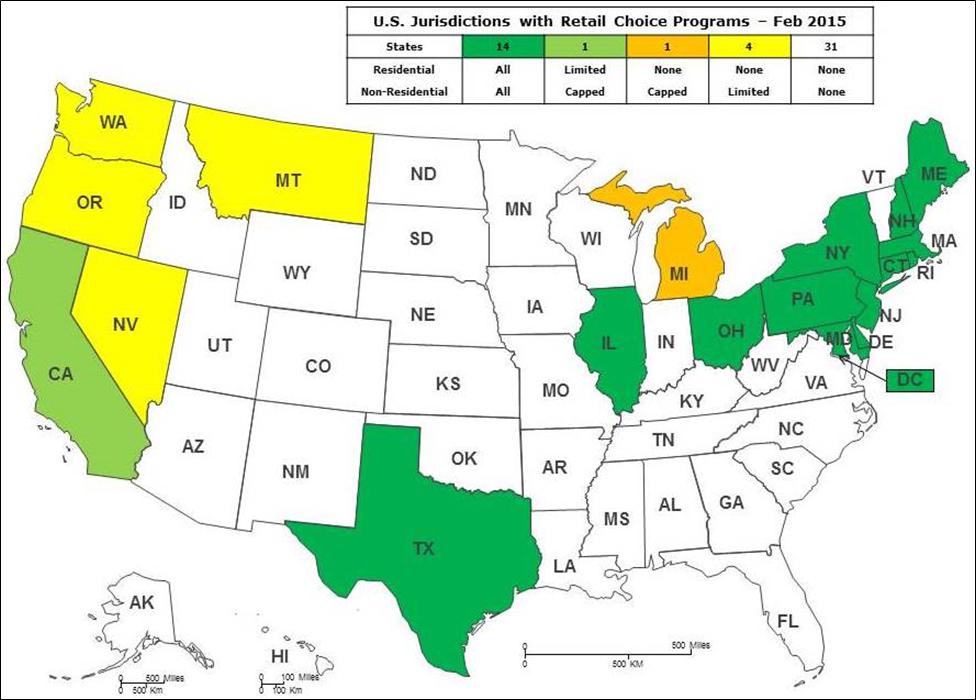

By the end of 2016, our goal is to be able to market power to approximately 38 million residential customers located in 50 service areas in the 14 jurisdictions that allow all retail customers of investor-owned utilities to choose who supplies them with electricity.

Until our retail energy business has gained scale, our primary sources of cash flow will be Note sales and loan payments received by Aspirity Financial from Enterprises, our first financial services customer.

We are headquartered at 701 Xenia Avenue South, Suite 475, Minneapolis MN 55416, telephone (763) 432-1500.

For some time, the Company had been considering ways to access the public equity markets. In order to be successful in reaching this goal, management and the Board concluded that:

| ● | Public equity markets value stability and predictability of earnings. |

| ● | There are a handful of publicly traded retail energy companies and no publicly traded wholesale energy trading businesses. |

| ● | Retail energy companies tend to be valued on a per customer basis, with recent transactions occurring at prices ranging from $200-$500 per customer. |

| ● | Combining a proprietary wholesale trading operation with a retail energy business results in a reduced overall valuation, as the market generally assigns little value to trading profits due to their extreme volatility. |

| ● | While wholesale electricity trading makes for a good private equity investment, the earnings volatility and regulatory exposure endemic to the business make it unattractive as a publicly traded equity. For example, on August 29, 2014, FERC commenced a regulatory action in PJM seeking to retroactively impose new fees - in still to be determined amounts - on trades in PJM’s up-to-congestion product. Since the announcement of the proceeding, UTC trading volume has decreased substantially and a number of companies have exited the market1. |

| ● | The cash flow of retail energy and financial services businesses are generally much more stable than those of wholesale trading, as each customer represents a reasonably predictable revenue stream, either of energy sales or interest income. |

| 8 |

Consequently, and as a result of these conclusions, to effect an initial public offering of its common equity, the Company would need to be restructured and recast. During May 2015, the Company developed plans to separate its Legacy Businesses from a proposed retail energy and financial services business. The Restructuring was designed so that Aspirity (the publicly reporting company) would hold new retail energy and financial services businesses while Enterprises would continue to operate the more volatile Legacy Businesses as a private company. At a special meeting on May 27, 2015, the Board gave management the authorization to proceed with the Restructuring.

The restructuring plan called for:

| ● | The formation of Aspirity Energy, Aspirity Financial, and Krieger Enterprises as first tier subsidiaries of the Company; |

| ● | The sale of TCP2; |

| ● | The transfer of all legacy businesses, operations, and private investment assets and directly associated liabilities to Enterprises. The Company’s Legacy Businesses included: |

| ● | A wholesale segment trading virtual electricity and energy-based derivatives contracts in North American markets regulated by FERC and the CFTC; | |

| ● | A retail energy business providing electricity supply services to residential and small business customers in 8 states that permit retail choice; and | |

| ● | Certain asset management activities, including real estate development and investments in privately held businesses; |

| ● | The creation of a Term Loan between Financial as lender and Enterprises as borrower3; |

| ● | A name change from Twin Cities Power Holdings to Aspirity Holdings to reflect the new focus |

| 1 | The Company’s former subsidiary, Twin Cities Power, and its subsidiary, Summit Energy (collectively, “TCP”) were active traders of UTCs. |

| 2 | On June 1, the Company closed on the sale of TCP to Angell. The sale price was initially $20.7 million, paid in the form of $500,000 cash and a $20.2 million, 3 year secured note bearing 6.00% interest and payable quarterly. Effective September 1, the purchase price was adjusted to $15.0 million due to the return of TCP’s Minnesota operations to Enterprises. The note amount and amortization period were amended to $15.02 million and 4 years. The gain on sale is being recognized as payments on the note are collected. In selling TCP, the Company partially accomplished its goal of reducing its regulatory exposure and earnings volatility. |

| 3 | Although initially an intercompany relationship, the loan between Enterprises and Aspirity Financial closed on July 1, is constructed on an arm’s length basis, and ensures that the cash flows generated by the Legacy Businesses are used to pay interest and principal on a substantial portion of the Notes. Accordingly, the Term Loan initially reflected the outstanding principal amount ($22.2 million) and weighted average interest rate (14.08%) of the Notes as of Jun 30, 2015, with a final maturity date of December 30, 2019. Further, subject to true-ups for actual Note redemptions and interest paid, the monthly repayment schedule provides for payment by Enterprises of maximum possible redemptions and interest. |

| 9 |

| ● | The distribution or spin-off of 100% of the common equity interests in Enterprises to Timothy Krieger (99.50% owner) and Summer Enterprises (0.50% owner), subject to: |

| ● | Determination that the transaction would be tax-free; | |

| ● | The approval of the holders of a majority of the Notes[4]. This occurred June 26, 2015; and | |

| ● | The declaration of effectiveness of the Company’s New S-1 by the SEC[5]. This occurred November 12, 2015; and |

| ● | Concurrently with the Distribution Date, certain executive management changes and a plan to add new common equity owners, ultimately decreasing Mr. Krieger’s common equity interest in the Company to 45%. |

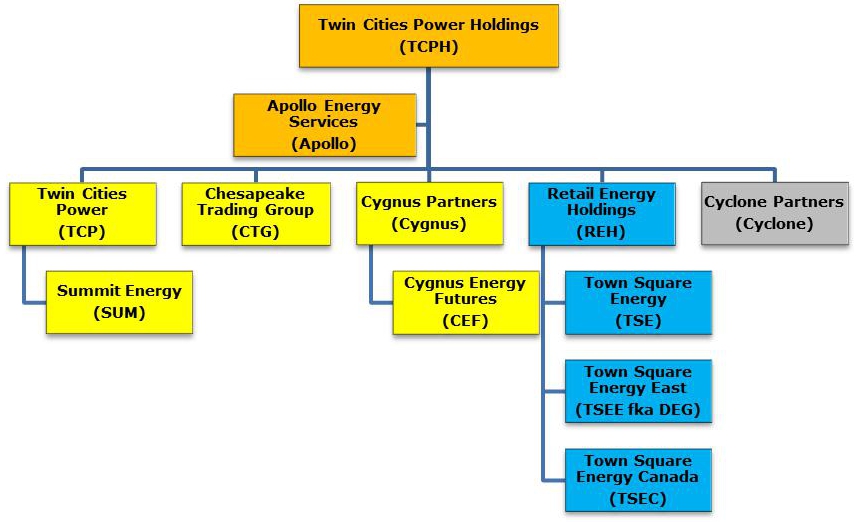

As shown by the chart below, prior to the start of the Restructuring on May 31, 2015, the Company’s active first tier subsidiaries consisted of Apollo, TCP, CTG, Cygnus, REH, and Cyclone.

| 4 | Under the terms of the Indenture governing the Notes, the disposition of all or substantially all of the Company’s assets requires the approval of the holders of a majority of Notes by principal amount. Consequently, on June 3, 2015, a proposal was submitted to the holders of the $21.9 million of Notes outstanding as of May 27, 2015 asking them to approve the transfer of the Legacy Businesses. Noteholders were asked to vote YES or NO to the proposal by June 26, 2015 with an abstention counting as a NO. The Company received YES votes from holders of $15.0 million, representing 68.6% of total Notes outstanding and 137% of the number required to pass the measure. Holders of $202,000 voted NO and $6.7 million abstained. |

| 5 | For tax and accounting purposes, November 1, 2015 is considered to be the Distribution Date. |

| 10 |

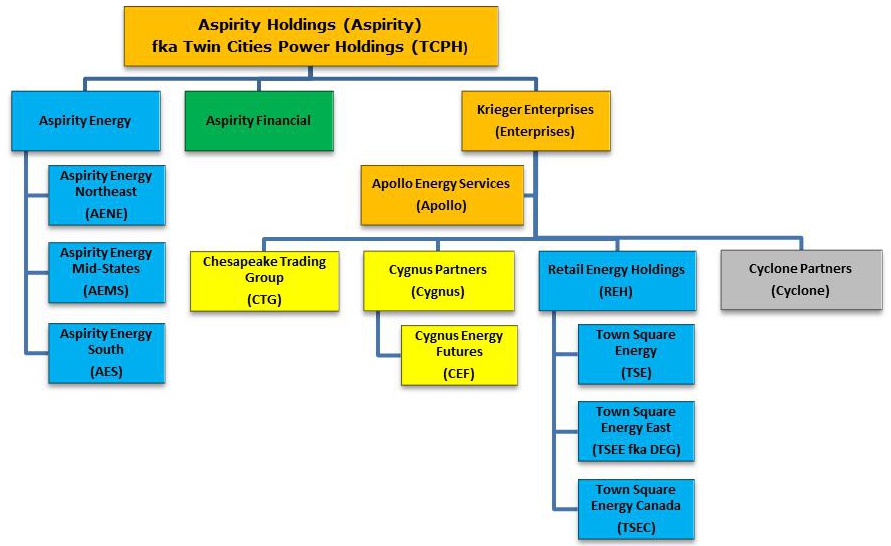

The chart below reflects the organizational structure and business lines of the Company on October 31, after the formation of the Aspirity operating companies, the sale of TCP, and the contribution of the legacy businesses to Enterprises, but before its spin-off on the Distribution Date:

As shown below, after the Restructuring and distribution of Enterprises, the Company has operations in two business segments. Note that under the terms of the PSA with Exelon, we have agreed to merge AEMS and AENE into Aspirity Energy.

| 11 |

As a result of the Restructuring, we currently have limited operations and limited assets. We are developing our new retail energy business, and while we are in the process of applying for licenses and EDI compliance in all 14 jurisdictions and with 50 investor owned utilities serving about 38 million residential accounts, we began to offer service in late January 2016 and are essentially a start-up. Until our retail energy business is generating significant revenue, our primary sources of cash flow will be loan payments received by Aspirity Financial from Enterprises and note sales. In addition to building the Aspirity Energy business, we may also decide to lend additional funds to Enterprises, as well as other companies in the power sector, an industry in which we have significant experience.

The U.S. Electric Power Industry

By virtually any measure, the electric power industry in the U.S. is substantial. According to EIA data, in 2014, the most recent year for which full data is available, the industry sold 3,765 TWh (up 1.1% from 2013) for more than $393.1 billion (up 4.6%) to over 147.3 million residential, commercial, and industrial customers (up 0.7%).

Electric power in commercial quantities, unlike other energy commodities such as coal or natural gas, cannot be stored, i.e., the supply must be produced or generated exactly when used or demanded by customers. Further, the laws of physics dictate that power flows within a network along the lines of least resistance, not necessarily where we may want it to go. These facts, coupled with the essential nature of the service to modern life, have obvious implications for electricity market structures and regulations.

Today, the industry includes any entity producing, distributing, trading, or selling electricity.

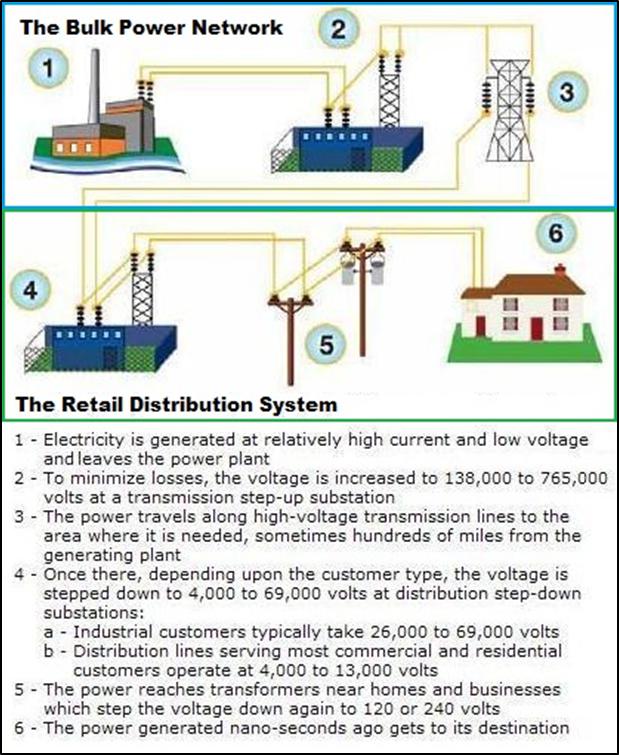

Physically, the nation’s power system includes generation resources, transmission lines, and retail distribution systems. As of the end of 2014, participants in the generation segment of the industry included investor-owned, publicly-owned, cooperative, and federal utilities, and non-utility power producers, including independent power producers and commercial and industrial entities that operate co-generation facilities, also known as CHP or combined-heat-and-power plants. These entities owned over 19,700 generating units with total nameplate capacity of 1,172 GW incorporated into over 7,600 power plants.

In addition to generation, the nation’s bulk power system also includes about 200,000 miles of high-voltage (over 144kV) transmission lines. Our retail distribution network includes substations, wires, poles, metering, billing, and related support systems.

Power marketers and retail energy providers do not own any generation, transmission, or distribution assets, but buy and sell in wholesale and retail markets. Finally, participants in wholesale power markets include banks, hedge funds, private equity firms, and trading houses. |

|

\

| 12 |

U.S. Electric Power Capacity & Generation, 2014

| Nameplate Capacity | Generation | Capacity | ||||||||||||||||||||||||

| Plants | Generators | GW | Percent | TWh | Percent | Factor (1) | ||||||||||||||||||||

| By Energy Source | ||||||||||||||||||||||||||

| Coal | 491 | 1,145 | 325.8 | 27.8 | % | 1,582 | 38.6 | % | 55.4 | % | ||||||||||||||||

| Petroleum | 1,082 | 3,573 | 46.9 | 4.0 | % | 30 | 0.7 | % | 7.4 | % | ||||||||||||||||

| Natural gas & other gases | 1,792 | 5,820 | 497.3 | 42.4 | % | 1,139 | 27.8 | % | 26.1 | % | ||||||||||||||||

| Nuclear | 62 | 99 | 103.9 | 8.9 | % | 797 | 19.5 | % | 87.6 | % | ||||||||||||||||

| Other (2) | 94 | 131 | 3.3 | 0.3 | % | 13 | 0.3 | % | 47.0 | % | ||||||||||||||||

| Total non-renewable | 3,521 | 10,768 | 977.2 | 83.3 | % | 3,561 | 87.0 | % | 41.6 | % | ||||||||||||||||

| Hydroelectric | 1,482 | 4,185 | 100.4 | 8.6 | % | 253 | 6.2 | % | 28.8 | % | ||||||||||||||||

| Wind | 1,032 | 65.3 | 5.6 | % | 182 | 4.4 | % | 31.8 | % | |||||||||||||||||

| Biomass | 1,192 | 2,317 | 15.5 | 1.3 | % | 64 | 1.6 | % | 47.2 | % | ||||||||||||||||

| Geothermal | 194 | 3.8 | 0.3 | % | 16 | 0.4 | % | 48.2 | % | |||||||||||||||||

| Sola | 1,249 | 10.4 | 0.9 | % | 18 | 0.4 | % | 19.3 | % | |||||||||||||||||

| Total renewable | 2,674 | 8,977 | 195.4 | 16.7 | % | 532 | 13.0 | % | 31.1 | % | ||||||||||||||||

| Total, all sources | 6,195 | 19,745 | 1,172.6 | 100.0 | % | 4,094 | 100.0 | % | 39.9 | % | ||||||||||||||||

| By Producer Type | ||||||||||||||||||||||||||

| Electric utilities | 3,118 | 9,510 | 675.7 | 57.6 | % | 2,382 | 58.2 | % | 40.3 | % | ||||||||||||||||

| Non-CHP IPPs | 3,189 | 6,975 | 423.8 | 36.1 | % | 1,555 | 38.0 | % | 41.9 | % | ||||||||||||||||

| CHP IPPs | 247 | 559 | 37.9 | 3.2 | % | — | 0.0 | % | 0.0 | % | ||||||||||||||||

| Commercial (3) | 649 | 1,085 | 4.1 | 0.4 | % | 13 | 0.3 | % | 34.7 | % | ||||||||||||||||

| Industrial (3) | 474 | 1,616 | 31.1 | 2.7 | % | 144 | 3.5 | % | 52.9 | % | ||||||||||||||||

| Total, all producers (4) | 7,677 | 19,745 | 1,172.6 | 100.0 | % | 4,094 | 100.0 | % | 39.9 | % | ||||||||||||||||

| Disposition of Generation | ||||||||||||||||||||||||||

| Total, all sources | 4,094 | 108.7 | % | |||||||||||||||||||||||

| Line losses, plant, and direct use, net | (329) | -8.7 | % | |||||||||||||||||||||||

| Retail sales to ultimate consumers | 3,765 | 100.0 | % | |||||||||||||||||||||||

Source: EIA Electric Power Annual with data for 2014, released February 2016, next release February 2017.

Notes

1 - The capacity factor is a measure of how often a generator runs and compares how much electricity it actually produces with the maximum it could produce during a specific period of time. For example, if a 1 MW generator produced 5,000 MWh over a year, its capacity factor would be 57%, because 5,000 MWh is 57% of the electricity it could have produced if it operated all 8,760 hours in the year at full capacity. Generators with relatively low fuel costs are usually operated to supply base load power, and typically have average annual capacity factors of 70% or more. Generators with lower capacity factors may indicate that they are operated during peak demand periods or have high fuel costs, or their operation depends on the availability of the energy source, such as hydro, solar, and wind energy.

2 - Other non-renewable sources of energy include batteries, chemicals, hydrogen, pitch, purchased steam, sulfur, tire-derived fuels and miscellaneous technologies.

3 - The industrial sector includes only independent power producers’ CHP facilities while the commercial sector Includes a small number of electricity-only, non-combined heat and power plants.

4 - Excludes distributed and dispersed generators and net metering customers. Distributed and dispersed generators are commercial and industrial generators that are, respectively, connected and un-connected to the grid. Both types may be installed at or near a customer’s site or at other locations and may be owned by either by customers or the distribution utility. Net metering is a service under which electricity generated by a consumer from an eligible facility and delivered to the utility may be used to offset energy provided by the utility during the applicable billing period.

| 13 |

U.S. Electric Power Industry Revenue, Unit Sales, Customers, and Average Retail Prices, All Sectors, 2014

| Entities (count) | Revenues ($millions) | % of Total | Unit Sales (TWh) | % of Total | Customers (000s) | % of Total | Avg Retail Price (¢/kWh) | |||||||||||||||||||||||||

| By Energy Provider | ||||||||||||||||||||||||||||||||

| Investor-owned utilities | 208 | 228,353 | 58.1 | % | 1,935 | 51.4 | % | 86,838 | 58.9 | % | 11.80 | |||||||||||||||||||||

| Retail energy providers | 652 | 57,019 | 14.5 | % | 743 | 19.7 | % | 20,070 | 13.6 | % | 7.67 | |||||||||||||||||||||

| Non-utility power producers | 213 | 974 | 0.2 | % | 16 | 0.4 | % | 1 | 0.0 | % | 5.93 | |||||||||||||||||||||

| Behind the meter | 94 | 228 | 0.1 | % | 2 | 0.0 | % | 167 | 0.1 | % | 12.92 | |||||||||||||||||||||

| Subtotal | 1,167 | 286,574 | 72.9 | % | 2,696 | 71.6 | % | 107,076 | 72.7 | % | 10.63 | |||||||||||||||||||||

| Cooperatives | 859 | 44,624 | 11.4 | % | 429 | 11.4 | % | 18,947 | 12.9 | % | 10.39 | |||||||||||||||||||||

| Municipally-owned utilities | 827 | 39,898 | 10.1 | % | 395 | 10.5 | % | 15,008 | 10.2 | % | 10.09 | |||||||||||||||||||||

| Public power districts | 81 | 9,640 | 2.5 | % | 109 | 2.9 | % | 3,861 | 2.6 | % | 8.83 | |||||||||||||||||||||

| State-owned utilities | 11 | 5,807 | 1.5 | % | 52 | 1.4 | % | 1,340 | 0.9 | % | 11.21 | |||||||||||||||||||||

| Federally-owned utilities | 26 | 1,295 | 0.3 | % | 32 | 0.8 | % | 35 | 0.0 | % | 4.11 | |||||||||||||||||||||

| Subtotal | 945 | 56,640 | 14.4 | % | 588 | 15.6 | % | 20,245 | 13.7 | % | 9.64 | |||||||||||||||||||||

| Adjustments (1) | 69 | 5,258 | 1.3 | % | 51 | 1.4 | % | 1,106 | 0.8 | % | 10.28 | |||||||||||||||||||||

| Total U.S. | 3,040 | 393,096 | 100.0 | % | 3,765 | 100.0 | % | 147,374 | 100.0 | % | 10.44 | |||||||||||||||||||||

| By Choice Type (2) | ||||||||||||||||||||||||||||||||

| Type 0 | 2,292 | 222,213 | 56.5 | % | 2,312 | 61.4 | % | 81,657 | 55.4 | % | 9.61 | |||||||||||||||||||||

| Type 1 | 679 | 112,947 | 28.7 | % | 987 | 26.2 | % | 42,589 | 28.9 | % | 11.44 | |||||||||||||||||||||

| Type 2 | 25 | 35,457 | 9.0 | % | 249 | 6.6 | % | 13,590 | 9.2 | % | 14.26 | |||||||||||||||||||||

| Type 3 | 21 | 14,248 | 3.6 | % | 129 | 3.4 | % | 5,839 | 4.0 | % | 11.06 | |||||||||||||||||||||

| Type 4 | 23 | 8,231 | 2.1 | % | 87 | 2.3 | % | 3,699 | 2.5 | % | 9.41 | |||||||||||||||||||||

| Subtotal | 748 | 170,883 | 43.5 | % | 1,452 | 38.6 | % | 65,717 | 44.6 | % | 11.77 | |||||||||||||||||||||

| Total U.S. | 3,040 | 393,096 | 100.0 | % | 3,765 | 100.0 | % | 147,374 | 100.0 | % | 10.44 | |||||||||||||||||||||

| By Census Region (3) | ||||||||||||||||||||||||||||||||

| New England | 266 | 18,557 | 4.7 | % | 120 | 3.2 | % | 7,133 | 4.8 | % | 15.45 | |||||||||||||||||||||

| Middle Atlantic | 323 | 49,331 | 12.5 | % | 368 | 9.8 | % | 18,099 | 12.3 | % | 13.41 | |||||||||||||||||||||

| South Atlantic | 422 | 81,153 | 20.6 | % | 572 | 15.2 | % | 30,246 | 20.5 | % | 14.19 | |||||||||||||||||||||

| East North Central | 423 | 56,337 | 14.3 | % | 301 | 8.0 | % | 22,215 | 15.1 | % | 18.71 | |||||||||||||||||||||

| East South Central | 246 | 28,973 | 7.4 | % | 806 | 21.4 | % | 9,517 | 6.5 | % | 3.60 | |||||||||||||||||||||

| West North Central | 514 | 27,477 | 7.0 | % | 319 | 8.5 | % | 10,730 | 7.3 | % | 8.61 | |||||||||||||||||||||

| West South Central | 300 | 50,925 | 13.0 | % | 589 | 15.6 | % | 17,587 | 11.9 | % | 8.65 | |||||||||||||||||||||

| Mountain | 267 | 25,651 | 6.5 | % | 272 | 7.2 | % | 10,728 | 7.3 | % | 9.42 | |||||||||||||||||||||

| Pacific - contiguous | 241 | 50,445 | 12.8 | % | 402 | 10.7 | % | 20,299 | 13.8 | % | 12.55 | |||||||||||||||||||||

| Pacific - noncontiguous | 38 | 4,248 | 1.1 | % | 16 | 0.4 | % | 820 | 0.6 | % | 27.14 | |||||||||||||||||||||

| Total US | 3,040 | 393,096 | 100.0 | % | 3,765 | 100.0 | % | 147,374 | 100.0 | % | 10.44 | |||||||||||||||||||||

Source: Company analysis of U.S. EIA Form 861 data, released February 2016, next release October 2016.

Notes

1 - Adjustments are required to reconcile federal and state reporting requirements.

2 - Retail choice types defined as follows: Type 0 - no retail customers have choice of generation services provider (“GSP”); Type 1 - all residential, commercial, and industrial customers in investor-owned utility (“IOU”) service areas have choice of GSP; Type 2 - limited number of residential customers have choice, choice of commercial and industrial customers is capped; Type 3 - no residential customers have choice, choice of commercial and industrial customers is capped; and Type 4 - no residential customers have choice, choice of commercial and industrial customers is limited.

3 - Census regions defined as follows: New England - CT, ME, MA, NH, RI, VT; Middle Atlantic - NJ, NY, PA; South Atlantic - DE, DC, FL, GA, MD, NC, SC, VA, WV; East North Central - IL, IN, MI, OH, WI; East South Central - AL, KY, MS, TN; West North Central - IA, KS, MN, MO, NE, ND, SD; West South Central - AR, LA, OK, TX; Mountain - AZ, CO, ID, MT, NV, NM, UT, WY; Pacific-contiguous - CA, OR, WA; and Pacific-noncontiguous - AK, HI.

| 14 |

The investor-owned portion of the industry, including utilities, retail energy providers, and non-utility generators, and constitutes over 70% of the industry’s revenues, unit sales, and customers as shown by the table above. According to the Edison Electric Institute, a trade group representing the largest investor-owned utilities, in 2014, total energy operating revenues of shareholder-owned electric companies were $377 billion[6]. As of December 31, 2014, consolidated holding company-level assets of these entities were $1.378 trillion, and of these assets, $833 billion were net property in service. In 2014, shareholder-owned electric utilities spent $19.5 billion on transmission investment, compared to $16.9 billion in 2013, are projected to spend $20.7 billion in 2015, and are planning to invest approximately $85 billion in transmission construction between 2015 and 2018. The total market capitalization of U.S. shareholder-owned electric companies was $632 billion on December 31, 2014.

Since the passage of the Public Utilities Regulatory Policy Act of 1978, the industry has been undergoing a massive restructuring process that has had a particular impact on investor-owned utilities. PURPA stimulated development of renewable energy sources and co-generation facilities and laid the groundwork for deregulation and competition by opening wholesale power markets to non-utility producers of electricity for the first time.

Since PURPA, the nation has moved from a system of vertically integrated monopolies providing retail service at state-determined, cost-based rates to one where the ownership of generation assets is no longer regulated and the majority of the nation’s bulk power systems are operated under the supervision of the Federal Energy Regulatory Commission, an independent agency within the DOE. Furthermore, while some states have restructured their markets such that individual consumers are allowed to choose their electricity supplier, most state public utility commissions continue to regulate their utilities under the traditional cost-based framework.

Today, wholesale prices are subject to a federal regulatory framework focused on ensuring fair competition and reliability of supply. At the state level, under the traditional system which most states continue to employ, a vertically integrated utility (a “full service provider”) is responsible for serving all consumers in a defined territory and customers are obligated to pay the regulated rate for their class of service.

However, in a state with a restructured or “deregulated” market, that is, the “restructured retail” business or one with retail choice, the generation, transmission, distribution, and retail marketing functions of the business are legally separated and pricing of energy is unbundled from delivery services. In 2014, according to EIA data, all customer types eligible to choose bought over 563 GWh from competitive suppliers, up 0.8% from 559 GWh in 2013.

6 Note that this figure also includes revenues from the sale of natural gas.

| 15 |

U.S. Electric Power Industry Revenue, Unit Sales, Customers, and Average Retail Prices, 2014

| Revenues ($millions) | % of Total | Unit Sales (TWh) | % of Total | Customers (000s) | % of Total | Avg Retail Price (¢/kWh) | ||||||||||||||||||||||

| By Customer Type | ||||||||||||||||||||||||||||

| Residential | 176,178 | 44.8 | % | 1,407 | 37.4 | % | 128,680 | 87.3 | % | 12.52 | ||||||||||||||||||

| Commercial | 145,253 | 37.0 | % | 1,352 | 35.9 | % | 17,854 | 12.1 | % | 10.74 | ||||||||||||||||||

| Industrial & other | 71,665 | 18.2 | % | 1,005 | 26.7 | % | 839 | 0.6 | % | 7.13 | ||||||||||||||||||

| Total industry | 393,096 | 100.0 | % | 3,765 | 100.0 | % | 147,374 | 100.0 | % | 10.44 | ||||||||||||||||||

| Residential | 160,637 | 40.9 | % | 1,301 | 34.6 | % | 117,231 | 79.5 | % | 12.34 | ||||||||||||||||||

| Commercial | 113,880 | 29.0 | % | 1,084 | 28.8 | % | 15,942 | 10.8 | % | 10.51 | ||||||||||||||||||

| Industrial & other | 57,328 | 14.6 | % | 816 | 21.7 | % | 790 | 0.5 | % | 7.03 | ||||||||||||||||||

| Full service providers | 331,845 | 84.4 | % | 3,201 | 85.0 | % | 133,963 | 90.9 | % | 10.37 | ||||||||||||||||||

| Residential | 15,541 | 4.0 | % | 106 | 2.8 | % | 11,450 | 7.8 | % | 14.70 | ||||||||||||||||||

| Commercial | 31,373 | 8.0 | % | 268 | 7.1 | % | 1,912 | 1.3 | % | 11.69 | ||||||||||||||||||

| Industrial & other | 14,338 | 3.6 | % | 189 | 5.0 | % | 49 | 0.0 | % | 7.57 | ||||||||||||||||||

| Restructured retail | 61,251 | 15.6 | % | 563 | 15.0 | % | 13,411 | 9.1 | % | 10.87 | ||||||||||||||||||

| Residential | 9,079 | 2.3 | % | — | — | — | — | 8.59 | ||||||||||||||||||||

| Commercial | 19,948 | 5.1 | % | — | — | — | — | 7.43 | ||||||||||||||||||||

| Industrial & other | 11,250 | 2.9 | % | — | — | — | — | 5.94 | ||||||||||||||||||||

| Energy only providers | 40,277 | 10.2 | % | — | — | — | — | 7.15 | ||||||||||||||||||||

| Residential | 6,462 | 1.6 | % | — | — | — | — | 6.11 | ||||||||||||||||||||

| Commercial | 11,425 | 2.9 | % | — | — | — | — | 4.26 | ||||||||||||||||||||

| Industrial & other | 3,088 | 0.8 | % | — | — | — | — | 1.63 | ||||||||||||||||||||

| Delivery service only | 20,975 | 5.3 | % | — | — | — | — | 3.72 | ||||||||||||||||||||

Source: Company analysis of U.S. EIA Form 861 data for 2014, re-released February 19, 2016, next release October 2016.

Wholesale prices are typically quoted as “on-peak”, “off-peak”, or “flat”, and in dollars per megawatt-hour ($/MWh). Peak hours are generally the 16 hours ending 0800 (8:00 am) to 2300 (11:00 pm) on weekdays, except for the NERC holidays of New Year’s Day, Memorial Day, Independence Day, Labor Day, Thanksgiving Day, and Christmas Day. Off-peak periods are all NERC holidays and weekend hours plus the 8 weekday hours from the hour ending at 2400 (midnight) until the hour ending at 0700 (7:00 am). Each month in a calendar year has a different number of on- and off- peak hours, consequently, the flat price for a given month takes this into account. The flat price for a day is simply the average of the 24 hourly prices. Retail prices are quoted in cents per kilowatt-hour (¢/kWh).

Wholesale electricity prices are driven by supply and demand and actually change minute-by-minute. Near term demand is largely affected by the weather and consumer behavior while supply is driven by plant availability and fuel prices, particularly for natural gas as it is the fuel of choice for marginal generation requirements.

Factors that affect electricity prices in the long term include climate, fuel prices and availability, generation and efficiency technologies deployed, population growth, economic activity, and governmental policies and regulatory actions with respect to energy and the environment.

After PURPA, the Energy Policy Act of 1992 was the next major legislative step towards full deregulation of wholesale power markets and in 1996, FERC issued Orders 888 and 889, which led to the creation of the network of “OASIS” or Open Access Same-Time Information System nodes, which allowed for energy to be scheduled across multiple power systems. In December 1999, FERC issued Order 2000 calling for electric utilities to form RTOs or ISOs to operate the nation’s bulk power system with the intended benefits of eliminating discriminatory access to transmission for all generators, improving operating efficiency, and increasing system reliability. ISOs are typically not-for-profit entities, use governance models developed by FERC, and operate under its regulatory authority.

| 16 |

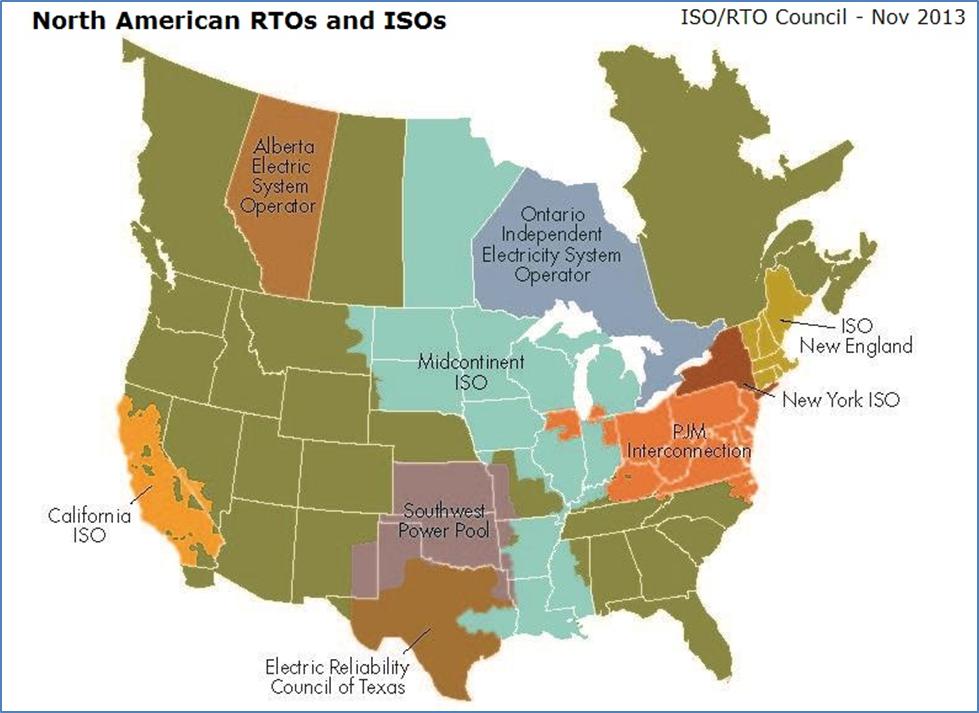

In addition to controlling the physical flow of power within its area of responsibility, many ISOs also operate financial markets for real-time and day-ahead electricity, as well as ancillary services required to ensure system reliability. To date, seven ISOs have been formed in the U.S., including those managed by CAISO, ERCOT, ISO-NE, MISO, NYISO, PJM, and SPP. In the parts of the country where ISOs have not been established, active wholesale markets are still present, although they operate with different structures.

In general, wholesale market activity is characterized by the acquisition of electricity at a given location such as a node or hub and its delivery to another. Short-term financial contracts offered by ISOs such as INCs, DECs, and UTCs are also known as “virtual” trades, are outstanding overnight, and settle the next day. ISOs may also offer longer term financial contracts known as FTRs. Physical transactions are settled by the delivery of the commodity. In any case, the ISO serves as the counter-party and central clearinghouse for all trades.

In addition to the markets operated by the ISOs, derivative contracts such as swaps, options, and futures keyed to a wholesale electricity price are traded over-the-counter and on exchanges regulated by the CFTC, including ICE, NGX, and CME. Derivative contracts are available for many terms and pricing points and always settle in cash with profit or loss determined by price movements in the underlying commodity.

| 17 |

One of the unique aspects of wholesale electricity markets run by ISOs is the availability of “locational marginal prices” (“LMPs”), also known as “nodal pricing”. The theoretical price of electricity at each node on the network is calculated based on the assumptions that one additional kilowatt-hour is demanded at the node in question, and that the marginal cost to the system that would result from the optimized re-dispatch of available generating units to serve the load can establish the production cost of the additional energy. LMPs are typically quoted on a “real-time” and “day-ahead” basis. In the real-time market, prices at specific nodes on the grid are updated every 5 minutes based on current and targeted supply and demand. Day-ahead prices are for power to be delivered at a specified hour and transmission point during the next day.

LMPs vary by time and location due to physical system limitations, congestion, and loss factors; however, in an unconstrained system with no losses, all LMPs would be equal. This means that LMPs can be conceptually separated into three components - an energy price, a marginal congestion component or “MCC”, and a loss component or “MLC”.

As generators are dispatched to meet load, the energy transfer capacity of transmission lines is used. Bulk power systems must be operated to allow for continuity of supply even if a contingent event, like the loss of a line, generator, or transformer were to occur. At times, transmission lines may also reach their maximum thermal capacity. These “security constraints”, also known as “congestion”, limit the ability to use the least expensive generation. In other words, when constraints exist on a transmission network, there is a need for more expensive generation to be used, and separate prices on either side of a node give rise to congestion pricing to relieve the constraint and reduce line loadings. Finally, since transmission lines act as resistors to the flow of energy, to receive a specific quantity at a particular destination, more than the expected quantity must be injected into the line at origination to compensate for losses.

Restructured Retail Electricity Markets

Historically, at the state level, electricity was a regulated market, where vertically-integrated utilities owned all or a major part of the bulk power and distribution infrastructure and were responsible for generating electricity or buying it from other producers and distributing it to homes and businesses. Regulated utilities are responsible for serving all consumers in their defined territory and customers are obligated to pay the regulated rate for their class of service. Neither provider nor consumer has a choice about who they do business with.

In the 1990s, many states, particularly those in the Northeast and California where retail prices were historically among the highest in the country, began restructuring their electric power industries in an effort to bring the benefits of competition to retail customers. This new regulatory approach centered on deregulation of generation and retail marketing while continuing the traditional cost-of-service plan for transmission and distribution. The regulated portions of formerly vertically-integrated utilities, now generally known as electric distribution companies (“EDCs”) or local distribution companies (“LDCs”) are responsible for delivering power, billing consumers, and resolving any service issues, but customers can shop around and buy power from any licensed supplier or broker doing business in the state, hence “retail choice”.

Restructuring created new business opportunities in an established industry. In general, there are two types of non-utility businesses participating in the deregulated retail energy marketing function in the U.S. today – “brokers” and “suppliers” – but each state licenses these businesses in a different way. For example, not every jurisdiction makes a broker/supplier distinction and some divide licenses based on potential customer categories such as “residential” or “non-residential” while other states divide their markets based on historical utility service territories and license an entity to only provide services in particular areas. Overall, as of January 2014, there were about 700 of these licensed retail energy businesses in the U.S.

| 18 |

Brokers, also known as “aggregators”, negotiate supply agreements between retail customers, typically large commercial or industrial entities, and wholesale suppliers. Brokers collect commissions from the supplier that wins a particular piece of business. Brokers do not bill customers directly and never take title to energy; they work for the customer. Their major expense is signing up new customers. As a result, brokers generally have relatively limited margins but high quality cash flows and comparatively small balance sheets.

Suppliers, also known as retail energy providers (each, a “REP”), energy service companies (each, an “ESCO”), competitive energy providers (each, a “CEP”), or the like depending upon the state, are also licensed to deal with retail customers. They have an up-stream supply arrangement which may include purchasing directly from a pool like PJM or NYISO or bilaterally from large integrated energy companies or independent power producers. In contrast to brokers, suppliers potentially have higher margins on the energy sold but require larger amounts of capital to acquire energy and carry receivables and payables for some period of time.

Today, years after Massachusetts and Rhode Island became the first states to effectively implement choice in 1998, 20 jurisdictions have some form of choice[7]. We define these forms of retail choice as follows:

| Type 1 | All residential, commercial, and industrial customers served by investor-owned utilities may choose their energy provider; |

| Type 2 | A limited number of residential customers have choice and the choice of non-residential customers is capped, usually at a specific number of megawatt-hours per year; |

| Type 3 | No residential customers have choice and the choice of non-residential customers is capped; and |

| Type 4 | No residential customers have choice and the number of non-residential with choice is limited. |

In addition, we define Type 0 jurisdictions as those in which no retail customers of any class have choice.

| 7 | Generally,only customers of investor-owned utilities are eligible to choose their electric supplier while those served by a municipal, cooperative, or other type of non-investor owned utility are ineligible. However, there are certain areas where customers of specific cooperatives and public utilities may have choice but these instances are rare. |

| 19 |

Some states require that utilities billing customers in their service territory on behalf of a retailer purchase the receivables generated as a result of energy sales. These states are known as “purchase of receivables” or “POR” jurisdictions. The purchase generally occurs at a modest discount of 0% to 2.5% to reflect bad debt experience by customer class within the service territory.

In POR areas, retailers have no customer credit exposure other than the bad debt charge because the utility pays regardless of whether or not the customer does. However, if a customer fails to pay, the utility will typically disconnect service, which results in the loss of the account for the retailer. In areas with without POR programs - non-POR areas - retailers are exposed to the credit risk of the customer. New Jersey is currently the only “recourse POR” state. Under these rules, retailers have no exposure to customer credit risk provided that the customer is billed under a utility’s consolidated billing program. However, if an electric account is in default for 90 days (about 120 days from the last invoice date), the utility has the option to convert the customer to dual billing.

POR laws have the effect of converting the retailer’s exposure to its customers’ credit to that of the applicable utility, which is generally “investment grade” under the scales of the Nationally Recognized Statistical Rating Organizations recognized by the SEC, such as Standard & Poor’s. A “BBB-” by S&P is considered to be the lowest investment grade by market participants.

The Type 1 retail choice jurisdictions incorporate 54 investor-owned utility service territories. In addition to obtaining licenses from appropriate state regulatory authorities, in order to supply power to customers within a given LDC service area, a retailer must become “EDI compliant” with that utility, which allows for access to their billing systems. In general, there are three billing structures available to competitive suppliers in restructured markets:

| 20 |

| ● | Under a “utility consolidated billing” system, also known as “UCB”, the utility is responsible for billing all retail customers for all electric service charges as well as the collection of outstanding accounts. Retailer charges included in the utility’s bill are calculated in one of two ways: |

| ● | For “rate ready” utilities, the retailer posts its rates with the utility and the utility calculates the charges for inclusion on the customer’s bill. | |

| ● | For “bill ready” utilities, retailers receive usage data from the utility and calculate the amount owed by the customer. This amount is then communicated back to the utility for inclusion on the customer’s bill. |

| ● | Under the “dual billing” framework, the utility sends bills to the customer for transmission and distribution charges and retailers send separate bills for generation charges. Each is responsible for the collection of its outstanding accounts and has direct credit exposure to the customer. |

| ● | Under the “retailer consolidated billing” structure or “RCB”, retailers are responsible for billing customers for all charges and, consequently, have direct credit exposure to the customer and are responsible for collection of all outstanding amounts. |

In the 14 areas where all rate classes had choice during 2014, according to the ABACCUS 2015 study supplemented by Company research, just over 38.0 million residential customers were eligible to choose their supplier. Of these totals, over 23.5 million or just under 62% had not switched away from the incumbent utility. 14.3 million or about 38% (in a range from 0.1% to 80.7%) had switched at least once.

| 21 |

For the Type 1 retail choice markets, the table below summarizes the POR status, number and credit of investor-owned utilities, the number of eligible residential customers, and recent prices:

Type 1 Retail Choice Residential Markets Overview

| Utilities | Customers | Prices (¢/ kWh, 1) | |||||||||||||||||||||||||||||||||||||||

| Avg | Switch | 2014 | 2015 | 2015 | |||||||||||||||||||||||||||||||||||||

| POR | Credit | Rate | Energy | Delivery | Avg | Avg | vs | ||||||||||||||||||||||||||||||||||

| State | Status | IO Us | Rating | Eligible | Unswitched | (2,3) | Only | Only | Price | Price | 2014 | ||||||||||||||||||||||||||||||

| CT | full | 2 | A- | 1,401,000 | 916,000 | 34.6 | % | 11.79 | 8.03 | 19.82 | 20.95 | 5.7 | % | ||||||||||||||||||||||||||||

| DE | none | 1 | BBB+ | 273,000 | 245,000 | 10.3 | % | 10.12 | 2.69 | 12.81 | 13.09 | 2.2 | % | ||||||||||||||||||||||||||||

| DC | in proces: | 1 | BBB+ | 243,000 | 209,000 | 14.0 | % | 10.06 | 3.35 | 13.41 | 13.61 | 1.5 | % | ||||||||||||||||||||||||||||

| IL | full | 4 | BBB+ | 4,604,000 | 1,780,000 | 61.3 | % | 6.77 | 5.23 | 12.00 | 12.58 | 4.8 | % | ||||||||||||||||||||||||||||

| ME | none | 2 | BBB+ | 767,000 | 595,000 | 22.4 | % | 7.41 | 10.00 | 17.41 | 19.80 | 13.7 | % | ||||||||||||||||||||||||||||

| MD | full | 4 | BBB | 2,028,000 | 1,543,000 | 23.9 | % | 10.15 | 3.52 | 13.67 | 14.04 | 2.7 | % | ||||||||||||||||||||||||||||

| MA | full | 4 | A- | 3,347,000 | 2,749,000 | 17.9 | % | 10.71 | 4.60 | 15.31 | 15.66 | 2.2 | % | ||||||||||||||||||||||||||||

| NH | none | 3 | BBB+ | 522,000 | 377,000 | 27.8 | % | 9.60 | 7.99 | 17.59 | 18.50 | 5.2 | % | ||||||||||||||||||||||||||||

| NJ | recourse | 4 | BBB+ | 3,377,000 | 2,913,000 | 13.7 | % | 13.06 | 2.67 | 15.73 | 15.89 | 1.0 | % | ||||||||||||||||||||||||||||

| NY | full | 6 | BBB+ | 5,811,000 | 4,486,000 | 22.8 | % | 12.02 | 8.04 | 20.06 | 18.54 | -7.6 | % | ||||||||||||||||||||||||||||

| full | 1 | BBB- | 618,000 | 316,000 | 48.9 | % | |||||||||||||||||||||||||||||||||||

| OH | in process: | 1 | BBB- | 1,274,000 | 885,000 | 30.5 | % | 6.51 | 6.08 | 12.59 | 12.69 | 0.8 | % | ||||||||||||||||||||||||||||

| none | 4 | BBB- | 2,303,000 | 740,000 | 67.9 | % | |||||||||||||||||||||||||||||||||||

| PA | full | 10 | BBB | 4,985,000 | 3,187,000 | 36.1 | % | 9.13 | 4.22 | 13.35 | 13.92 | 4.3 | % | ||||||||||||||||||||||||||||

| RI | none | 1 | BBB+ | 493,000 | 457,000 | 7.3 | % | 10.39 | 6.84 | 17.23 | 19.35 | 12.3 | % | ||||||||||||||||||||||||||||

| TX | none | 6 | BBB+ | 5,986,000 | 2,144,000 | 64.2 | % | — | — | 11.86 | 11.66 | -1.7 | % | ||||||||||||||||||||||||||||

| Sum/avg | 54 | BBB+ | 38,032,000 | 20,542,000 | 08.1 | % | 0.82 | 5.64 | 15.20 | 15.73 | 3.5 | % | |||||||||||||||||||||||||||||

| full | 31 | BBB+ | 22,794,000 | 14,977,000 | 34.3 | % | |||||||||||||||||||||||||||||||||||

| recourse | 4 | BBB+ | 3,377,000 | 2,913,000 | 13.7 | % | |||||||||||||||||||||||||||||||||||

| in process: | 2 | BBB+ | 1,517,000 | 1,094,000 | 27.9 | % | |||||||||||||||||||||||||||||||||||

| none | 17 | BBB | 10,344,000 | 4,558,000 | 55.9 | % | |||||||||||||||||||||||||||||||||||

| Sum/avg | 54 | BBB+ | 38,032,000 | 20,542,000 | 08.1 | % | |||||||||||||||||||||||||||||||||||

Sources

ABACCUS 2015; EIA Electric Power Annual 2014; EEI website accessed March 4, 2015; Company analysis of company websites.

Notes

| 1 | “Energy Only” providers sell energy to customers and incumbent utilities provide “Delivery Only” services for these customers. In Texas, customers served by REPs must be provided with bundled energy and delivery services. |

| 2 | “Switch rate” refers to the percentage of customers that have migrated away from the incumbent provider’s default service product (the standard offer, basic service, generation service, etc.). |

| 3 | In Texas’ competitive markets (ERCOT), all eligible residential customers take competitive electric service and the switch rate indicates the number not served by the incumbent retail energy provider. Total eligible customers refer to those within ERCOT, or about 60% of the 9,954,000 residential accounts in the state. |

| 22 |

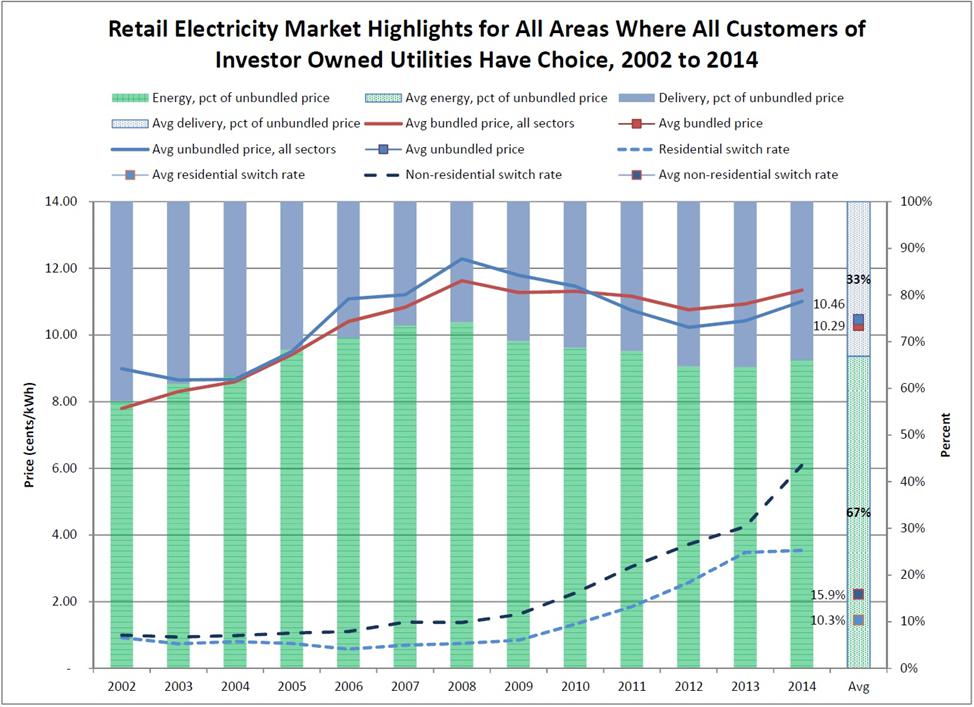

Overall, we believe that choice is proving to be a boon for consumers with respect to providing them with the ability to manage their electricity costs. According to an analysis of data from the EIA, between 2002 and 2014, retail rates for all customer sectors in states with restructured retail markets increased by 47.2% compared with a 39.5% increase in states that rely on regulated utilities. However, as shown by the chart below, unbundled prices in all Type 1 areas since 2011 have been consistently lower that the bundled service offered by the incumbent utilities.

Unbundling of electric bills in restructured markets made many aware for the first time exactly what they were paying for. In general, the bills of retail electricity customers include numerous costs and charges that can be classified into energy costs, delivery charges, and governmental policy costs. These include the costs of federal and state polices with respect to electricity and may include transition charges or costs associated with moving from a regulated market to a restructured one, allowing EDCs to recapture stranded costs that would otherwise be unrecoverable after deregulation, societal benefits charges such as the costs of mandated programs such as universal service, lifeline service, and energy efficiency programs, and sales and use taxes collected by state and local authorities on retail electricity sales.

According to analysis of EIA data for states with restructured markets, on average between 2002 and 2014 (the latest year for which information is available) energy and delivery costs accounted for about 67% and 33%, respectively, of the average retail electricity price. Of course, these percentages fluctuate from year to year and state to state, primarily due to wholesale energy market conditions, weather, and state rules.

| 23 |

As of March 30, 2016, we are licensed in five full choice jurisdictions and are EDI compliant with three utilities serving a total of 4.5 million residential accounts. As of the same date, we have 1,587 confirmed customers. By the end of 2016, we plan on being licensed in all 14 Type 1 jurisdictions and EDI compliant with 50 IOUs serving about 38 million residential customers as shown by the table below:

Aspirity Energy Expected Market Rollout Plan

Last updated March 23, 2016

| ISOs | States | EDI

Ready IOU Service Areas | Accessable Customers (000s) | ||||||||||||||||||||||||||||||

| Period | Inc | EoP | Inc | EoP | Inc | EoP | Inc | EoP | |||||||||||||||||||||||||

| 2015 | 1 | 1 | 3 | 3 | 1 | 1 | 618 | 618 | |||||||||||||||||||||||||

| Jan 2016 | - | 1 | - | 3 | 1 | 2 | 3,463 | 4,081 | |||||||||||||||||||||||||

| Feb 2016 | - | 1 | 1 | 4 | 1 | 3 | 455 | 4,536 | |||||||||||||||||||||||||

| Mar 2016 | - | 1 | 3 | 7 | - | 3 | - | 4,536 | |||||||||||||||||||||||||

| Q1 2016 | - | 4 | 2 | 3,918 | |||||||||||||||||||||||||||||

| Apr 2016 | 1 | 2 | - | 7 | 6 | 9 | 5,566 | 10,102 | |||||||||||||||||||||||||

| May 2016 | 2 | 4 | 1 | 8 | - | 9 | - | 10,102 | |||||||||||||||||||||||||

| Jun 2016 | 1 | 5 | 2 | 10 | 12 | 21 | 6,214 | 16,316 | |||||||||||||||||||||||||

| Q2 2016 | 4 | 3 | 18 | 11,780 | |||||||||||||||||||||||||||||

| Jul 2016 | - | 5 | 4 | 14 | 2 | 23 | - | 16,316 | |||||||||||||||||||||||||

| Aug 2016 | - | 5 | - | 14 | 5 | 28 | 11,770 | 28,086 | |||||||||||||||||||||||||

| Sep 2016 | - | 5 | - | 14 | 9 | 37 | 2,897 | 30,983 | |||||||||||||||||||||||||

| Q3 2016 | - | 4 | 16 | 14,667 | |||||||||||||||||||||||||||||

| Oct 2016 | - | 5 | - | 14 | 1 | 38 | 7,011 | 37,994 | |||||||||||||||||||||||||

| Nov 2016 | - | 5 | - | 14 | 12 | 50 | - | 37,994 | |||||||||||||||||||||||||

| Dec 2016 | - | 5 | - | 14 | - | 50 | - | 37,994 | |||||||||||||||||||||||||

| Q4 2016 | - | - | 13 | 7,011 | |||||||||||||||||||||||||||||

| 2016 | 5 | 14 | 50 | 37,994 | |||||||||||||||||||||||||||||

Our services are made available to customers under fixed price contracts as well as some that may provide for renewable energy percentages in excess of state requirements. All contracts regardless of price, term, and renewable energy percentage are subject to standard terms and conditions as filed from time to time with state regulatory authorities. Retail customers make purchase decisions based on a variety of factors, including price, customer service, brand, product choices, bundles, or value-added features.

The prices we offer customers are determined by us and are not subject to regulation. The terms we offer are also determined by us, and we develop such to align with regulatory requirements within each state where we do business. The electricity we sell is generally metered and delivered to our customers by local utilities. As such, we do not have a maintenance or service staff for customer locations. These utilities also provide billing and collection services for the majority of our customers on our behalf, generally under the utility consolidated billing structure.

Although our marketing efforts just began in the first quarter of 2016, we plan to reach residential prospects utilizing offline and online marketing channels. The offline channel includes vehicles such as outbound telemarketing, door-to-door, direct mail, events, brokers, out-of-home, etc. The online channel includes paid search, display ads, retargeting ads, affiliate, email, state-run comparison-shopping engines, etc. Our goal is to invest an optimal amount in new customer acquisition, and focus on customer retention and the lifetime value inherent in satisfied customer relationships.

| 24 |

The retail energy business involves the purchase of electricity in wholesale markets and the virtually simultaneous resale of such to retail customers. In general, ISOs require payment for energy purchased on a weekly or twice-weekly basis. In some markets, retailers are also required to buy capacity and certain ancillary services on a monthly basis. In all cases, retailers are required to provide market operators with “financial assurance” or “collateral”, typically in the form of cash in an amount equal to 60 to 75 days’ worth of such purchases. However, retailers typically only receive payment from customers on a monthly basis. Consequently, a substantial amount of liquidity and capital may be required to both satisfy payables and carry receivables. We do not own any generation, transmission, or distribution facilities and utilize wholesale suppliers for our supply requirements and utilities for our transmission and distribution needs.

On March 30, 2016 we entered into a full requirements preferred supply agreement with Exelon Generation Company, LLC, a Pennsylvania limited liability company and wholly-owned subsidiary of Exelon Corporation (“Exelon”), to provide us with all the power and ancillary services we need to serve our customers for an initial term expiring on March 30, 2019 (the “PSA”). As of December 31, 2015, Exelon was the operator of the second largest generation fleet in the U.S. and its long-term S&P credit rating was BBB.

Under the terms of the PSA, on a daily or weekly basis as we request, Exelon will provide firm, fixed quotes for power for terms of one, 3, 6, 9, 12, 15, 18, 24, 27, 30, and 36 months out for each of the service areas in which we operate. Such quotes will include all costs of energy, capacity, and ancillary services necessary to serve residential and small commercial customers. We may also meet state minimum “green” energy supply criteria by acquiring renewable energy certificates or RECs from Exelon via the PSA. If necessary, we may also buy additional RECs to satisfy the requirements of customers selecting a product with a percentage of green power higher than state minimums. We then mark up these costs to obtain selling prices. In addition, under the PSA, Exelon absorbs all volumetric risk or deviations between forecasted and actual customer usage. Finally, the PSA provides that Exelon will post any collateral required of us by an ISO or EDC.

Exelon will invoice us for all purchases under the agreement every month. The PSA also incorporates the ability for us to defer payment of all or a portion of these invoices based on certain financial criteria as defined in the agreement. We are exposed to the risk that Exelon may fail to deliver. If this were to occur, we would then be forced to pledge collateral and buy the required power from either an ISO or another wholesale supplier and the costs of such may be higher or lower than those embodied in the PSA.

In connection with our retail electricity business, we intend to provide trade credit to our customers. We are considering implementing the policies and underwriting strategy presented below to allow us to accept any business by taking deposits only from the riskiest accounts. If implemented, collection activity and cost will be largely eliminated since if a customer fails to pay in a timely fashion, then we will simply cease providing service and apply the deposit to the outstanding bill. This credit policy is summarized as follows:

| ● | If a prospect is located in a POR area, we will accept the account as the utility is the account obligor. |

| ● | If a prospect is located in a non-POR area and is a residential account, we will check their three-bureau FICO score: |

| ● | If the score is above a certain threshold, we will accept the account without a deposit. | |

| ● | If the score is below the threshold, we will accept the account with a deposit equal to the dollar value of 90 days of expected energy sales. |

| 25 |

| ● | If a prospect is located in a non-POR area and is a non-residential account, we will check their trade credit score: |

| ● | If the score is above the threshold level, we will accept the account without a deposit. | |

| ● | If the score is below the threshold, we will accept the account with a deposit equal to the dollar value of 90 days of expected energy sales. |