Attached files

| file | filename |

|---|---|

| EX-32.2 - ADAMANT DRI PROCESSING & MINERALS GROUP | e614914_ex32-2.htm |

| EX-31.2 - ADAMANT DRI PROCESSING & MINERALS GROUP | e614914_ex31-2.htm |

| EX-32.1 - ADAMANT DRI PROCESSING & MINERALS GROUP | e614914_ex32-1.htm |

| EX-31.1 - ADAMANT DRI PROCESSING & MINERALS GROUP | e614914_ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015

Commission File Number: 000-49729

Adamant DRI Processing and Minerals Group

(Exact name of registrant as specified in its charter)

|

Nevada

|

61-1745150

|

|

|

(State or Other Jurisdiction of Incorporation)

|

(IRS Employer Identification Number)

|

ChunshugouLuanzhuang Village, Zhuolu County

Zhangjiakou, Hebei Province, China, 075600

(Address of principal executive offices) (Zip code)

86-313-6732526

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of class

|

Name of each exchange on which registered

|

|

|

None

|

N/A

|

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (ss. 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. (Check one):

|

Large accelerated filer o

Non-accelerated filer o (Do not check if a smaller reporting company)

|

Accelerated filer o

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

As of June 30, 2015, the number of outstanding shares of the registrant's common stock held by non-affiliates (excluding shares held by directors, officers and others holding more than 5% of the outstanding shares of the class) was 2,829,760 shares. However, since there was no trading market for the common stock as of that date, it is impracticable to ascertain the aggregate market value of those shares as of that date.

As of March 20, 2016, we had 63,760,110 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

|

PAGE NO.

|

||

|

PART I

|

||

|

1

|

||

|

21

|

||

|

39

|

||

|

40

|

||

|

40

|

||

|

Part II

|

||

|

40

|

||

|

42

|

||

|

42

|

||

|

51

|

||

|

51

|

||

|

51

|

||

|

52

|

||

|

53

|

||

|

Part III

|

||

|

53

|

||

|

54

|

||

|

55

|

||

|

56

|

||

|

59

|

||

|

Part IV

|

||

|

59

|

||

|

63

|

SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS

This report contains forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and are subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on forward-looking statements. Forward-looking statements include, among other things, statements relating to:

● our ability to produce concentrated iron powder at a profitable margin;

|

●

|

the uncertainty of acquiring mining rights in the areas around our production facilities;

|

|

●

|

the impact that a downturn or negative changes in the steel market may have on sales;

|

|

●

|

our ability to obtain additional capital to fund our expansion;

|

|

●

|

economic, political, regulatory, legal and foreign exchange risks associated with our operations; and

|

|

●

|

the loss of key members of our senior management.

|

Also, forward-looking statements represent our estimates and assumptions only as of the date of this report. You should read this report and the documents that we reference and filed as exhibits to the report completely and with the understanding that our actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

Use of Certain Defined Terms

Except where the context otherwise requires and for the purposes of this report only:

|

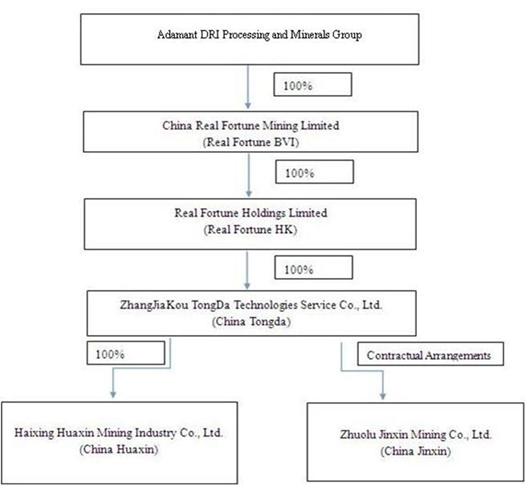

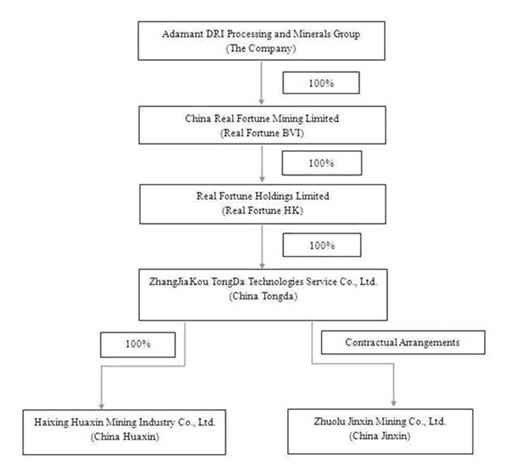

the “Company,” “we,” “us,” and “our” refer to the combined business of (i) Adamant DRI Processing and Minerals Group, a Nevada corporation and formerly a wholly-owned subsidiary of UHF Incorporated into which UHF merged on August 29, 2014, (ii) Target Acquisitions I, Inc., or “Target Acquisitions,” a Delaware corporation, which became a wholly owned subsidiary of UHF Incorporated, the registrant, or “UHF” pursuant to a share exchange agreement completed in June 2014 and which was subsequently merged into UHF in July 2014, (iii) China Real Fortune Mining Limited, or “Real Fortune BVI,” a BVI limited company, (iv) Real Fortune Holdings Limited, or “Real Fortune HK,” a Hong Kong limited company and wholly-owned subsidiary of Real Fortune BVI, (v) Zhangjiakou TongDa Mining Technologies Service Co., Ltd., or “China Tongda,” a Chinese limited company and wholly-owned subsidiary of Real Fortune HK, (vi) Zhuolu Jinxin Mining Co., Ltd., or “China Jinxin,” a Chinese limited company which is effectively and substantially controlled by China Tongda through a series of agreements, and (vii) Haixing Huaxin Mining Industry Co., Ltd. or “China Huaxin”, a Chinese limited liability company and wholly-owned subsidiary of China Tongda, as the case may be;

|

|

|

“BVI” refers to the British Virgin Islands;

|

|

|

“Exchange Act” refers to the Securities Exchange Act of 1934, as amended;

|

|

|

“Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China;

|

|

|

“PRC,” “China,” and “Chinese,” refer to the People’s Republic of China (excluding Hong Kong and Taiwan);

|

|

|

“Renminbi” and “RMB” refer to the legal currency of China;

|

|

|

“Securities Act” refers to the Securities Act of 1933, as amended;

|

|

|

“US dollars,” “dollars” and “$” refer to the legal currency of the United States; and

|

|

|

“tons” or “tonnes” refer to metric tonnes (2,205 pounds).

|

In this report we refer to information contained in government reports and third party publications. Although we are unable to verify the accuracy of all of such information we believe you may rely upon such information in evaluating the prospects of our Company. We are responsible for the accuracy of the third party information to which we make reference and for all information contained in this report.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an "emerging growth company" as defined in the Jumpstart our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

• a requirement to have only two years of audited financial statements and only two years of related Management's Discussion and Analysis of Financial Condition and Results of Operations disclosure; and

• an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002.

We may take advantage of these provisions until the end of the fiscal year ending after the fifth anniversary of our initial public offering or such earlier time that we are no longer an emerging growth company and if we do, the information that we provide stockholders may be different than you might get from other public companies in which you hold equity.

We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenue, have more than $700 million in market value of our ordinary shares held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period.

The JOBS Act permits an "emerging growth company" like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies.

PART I

|

Business.

|

Acquisition of Target Acquisitions I, Inc.

On June 30, 2014, we, then known as UHF Incorporated, a shell company incorporated under the laws of Delaware (“UHF”), completed a reverse acquisition transaction through a share exchange with Target Acquisitions I, Inc. (“Target”) and the its shareholders (the “Target Shareholders”) whereby we acquired 100% of the outstanding shares of common stock of Target in exchange for a total of 43,375,638 shares of our common stock and one share of our series A convertible preferred stock, convertible into an additional 17,839,800 shares common stock at such time as we amended our certificate of incorporation to increase the number of authorized shares of common stock or merge with and into another corporation which had sufficient shares of authorized but unissued shares of common stock for issuance upon conversion. On July 2, 2014, we merged Target into UHF pursuant to Section 253 of the Delaware General Corporation Law. The preferred stock was subsequently converted into shares of common stock upon the merger of UHF with and into its newly-formed wholly-owned Nevada subsidiary, Adamant DRI Processing and Minerals Group, the surviving corporation in the merger, as discussed below under the caption “Reincorporation as a Nevada Corporation.” As a result of the reverse acquisition, Target became our wholly-owned subsidiary and the Target Shareholders became our controlling stockholders. For accounting purposes, the share exchange transaction with Target and the Target Stockholders was treated as a reverse acquisition, with Target as the acquirer and UHF as the acquired party.

As a result of our acquisition of Target, we now own all of the issued and outstanding capital stock of Real Fortune BVI, which in turn owns all of the issued and outstanding capital stock of Real Fortune Holdings Limited, a Hong Kong limited company (“Real Fortune HK”), which in turn owns all of the issued and outstanding capital stock of Zhangjiakou TongDa Mining Technologies Service Co., Ltd., a Chinese limited company (“China Tongda”). Real Fortune BVI was established in the BVI in September 2010 to serve as an intermediate holding company. Real Fortune HK was established in Hong Kong in April 2010. China Tongda was established in the PRC in August 2010, and in August 2010, the local government of the PRC issued a certificate of approval regarding the foreign ownership of China Tongda by Real Fortune HK. China Jinxin, our operating affiliate, was established in the PRC in December 2006.

We have effective control of the management and operations of Zhuolu Jinxin Mining Co., Ltd., a Chinese limited company (“China Jinxin”), through a series of agreements among China Tongda, China Jinxin and its shareholders, referred to as “VIE Agreements.” China Jinxin owns an iron ore processing and high grade iron ore concentrate producing facility with a production line located in Zhuolu County, Zhangjiakou City, Hebei Province, China. The production line has an annual capacity of approximately 300,000 tons. Under the VIE Agreements, China Tongda is entitled to receive the pre-tax profits of China Jinxin. For a more detailed description of the VIE Agreements, see “Item 13. Certain Relationships And Related Transactions, And Director Independence – Transactions with Related Persons –VIE Agreements.”

On January 17, 2014, China Tongda acquired all of the outstanding shares of Haixing Huaxin Mining Industry Co., Ltd. (“China Huaxin”). China Huaxin intends to produce Direct Reduced Iron (DRI) at its DRI production facility (the “DRI Facility”) in Haixing County, Hebei Province, about 50 km from the nearest port, using advanced reduction rotary kiln technology with iron sand as the principal raw material. China Huaxin intends to imports iron sands from New Zealand, Australia, Indonesia and the Philippines. The total amount expended to construct the DRI Facility, inclusive of both hard and soft costs, was approximately 244,270,000 RMB or US $39 million. We expect the DRI Facility will commence full scale operations in the second half of 2016. Unlike China Jinxin, which we control through the VIE agreements, China Huaxin is directly owned by China Tongda, our wholly owned subsidiary. China Huaxin was established in August 2010 and is located in Haixing Qingxian Industrial Park, Cangzhou, Hebei Province PRC.

Reincorporation as a Nevada Corporation

By written consents dated July 4, 2014, our Board of Directors and holders of approximately 67.58% of our outstanding voting shares authorized and approved an Agreement and Plan of Merger pursuant to which on August 29, 2014, our company, a Delaware corporation, then known as UHF Incorporated, was merged with and into its newly formed wholly owned subsidiary, Adamant DRI Processing and Minerals Group, a Nevada corporation, with Adamant as the surviving corporation. As a result of the merger, we became a Nevada corporation, with authorized common stock of 100,000,000 shares and 1,000,000 shares of undesignated preferred stock. Adamant is deemed to be the successor issuer of UHF under Rule 12g-3 of the Securities Exchange Act of 1934, as amended.

Corporate History

UHF Incorporated was incorporated in Michigan on March 13, 1964 with the name State Die & Manufacturing Company. On March 4, 1992 its name was changed to UHF Incorporated.

In 1991, the Company became a holding company by transferring its assets to a newly-formed, wholly-owned corporation and by purchasing the outstanding stock of two closely held corporations. These three subsidiaries sold their businesses in 1994, and the Company paid its debts.

On December 28, 2011, we effected a one for five (1-for-5) reverse stock split of our shares of common stock, with special treatment for shareholders owning less than 500 shares, but at least 250 shares, to preserve round lot holders. Holders of less than 500 shares but at least 250 shares received 100 post-split shares. All information in this report has been adjusted to give effect to the reverse split. No fractional shares were issued.

On December 29, 2011, we completed a domicile merger with our newly-formed wholly owned subsidiary, the surviving company, UHF Incorporated, a Delaware corporation, pursuant to an Agreement and Plan of Merger dated December 1, 2011, as a result of which we became a Delaware corporation and the corporate existence of UHF Incorporated, a Michigan corporation (“UHF Michigan”), was terminated. Each shareholder of UHF Michigan received a number of shares of our common stock equal to the number of shares previously owned in UHF Michigan after giving effect to the reverse split.

From 1994 until the consummation of the reverse acquisition with Target on June 30, 2014, the Company was inactive and had no assets or employees, and was a “shell company,” as that term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

On July 2, 2014, we merged Target, our wholly-owned subsidiary, into our company pursuant to Section 253 of the Delaware General Corporation Law.

On August 29, 2014, we changed our state of incorporation from Delaware to Nevada as a result of a merger with and into our newly formed wholly-owned subsidiary, Adamant DRI Processing and Minerals Group, a Nevada corporation (“Adamant”) and the surviving entity, pursuant to an Agreement and Plan of Merger dated as of July 4, 2014. The reincorporation was approved by written consent of stockholders of UHF owning in the aggregate 67.58% of its outstanding voting shares as of July 4, 2014. Adamant is deemed to be the successor issuer of UHF under Rule 12g-3 of the Exchange Act.

The chart below presents our corporate structure:

Business Overview

Overview

The demand for iron and steel products in China increased rapidly for a period of years before the recent slowdown in the Chinese economy. We believe demand for high quality iron ore concentrate will resume growing domestically and globally, and intend to seek to profit from this growth by participating in various aspects of the production of iron suitable for steelmaking, including, as suitable opportunities arise, through the acquisition of mines or mining rights, and the acquisition of iron processing facilities.

To date, we have constructed two facilities. Our first facility is an iron ore processing facility in Zhuolu County, Zhangjiakou City, Hebei Province, China. For a variety of reasons described below, this facility has not been able to operate continuously and we have upgraded this facility to improve the grade of iron concentrate it will produce and to add the capacity to produce Direct Reduced Iron (DRI).

Our second facility is a DRI production facility in Haixing County, Hebei Province.

DRI Processing (Haixing Huaxin Mining Industry Co., Ltd.)

China Huaxin intends to produces Direct Reduced Iron (DRI) using advanced reduction rotary kiln technology with iron sand as the principal raw material. China Huaxin imports iron sands from New Zealand, Australia, Indonesia and the Philippines. The total amount expended to construct the DRI Facility, inclusive of both hard and soft costs, was approximately 244,270,000 RMB or US $39 million.

‘Reduced iron’ derives its name from the chemical change that iron ore undergoes when it is heated in a furnace at high temperatures in the presence of hydrocarbon-rich gasses. ‘Direct reduction’ refers to processes which reduce iron oxides to metallic iron below the melting point of iron. The product of such solid state processes are called direct reduced iron (DRI). The Company’s DRI Facility is projected to produce DRI with an iron grade of over 92%.

China Huaxin completed trial production and anticipated commencing commercial production in May 2015. However, due to environmental initiatives by government authorities in China, starting in June 2015, China Huaxin commenced upgrading the DRI facilities by converting the existing coal-gas station systems to liquefied natural gas (“LNG”) station systems. The conversion to LNG systems will reduce pollutants and produce higher quality DRIs with less impurity. China Huaxin is in the final stages of this upgrade and expects to commence commercial production with upgraded DRI facilities in the second half of 2016.

The Company’s DRI Facility occupies an area of 200,000 m2 The DRI Facility occupies 60,000 m2, of land and there is a raw material storage area of 14,000 m2 with a 100,000 ton storage capacity, a workshop area of 4500 m2, a water storage pool of 4000 m3 to supplement water supplies, and an office building of 2,400 m2. The plant design is intended to permit the processing of 2,000,000 tons of iron sand per annum with an annual output capacity of 1,000,000 tons of DRI.

The equipment installed in the DRI Facility includes 2 sets of Rotary Kilns that are 36m each in length and capable of processing 6000 tons of raw material per day, and 3 sets of Gas Furnaces to produce carbon monoxide for use in the reduction process. The equipment also includes 6 sets of Grinding Equipment and 3 sets of Wet Magnetic Separation Machineries with processing capacity of 7200 tons per day. In addition there are 30 sets of Hydraulic Machines with a capacity of 5,000 tons per day to press block the finished product.

Iron Ore (ZhuoluJinxin Mining Co., Ltd.)

China Jinxin is engaged in iron ore processing and the production of iron ore concentrate. China Jinxin has an iron ore concentrate production line with an annual capacity of 300,000 tons and associated plant and office buildings located in Zhuolu County, Zhangjiakou City, Hebei Province, China. Construction of the production facilities commenced in May 2007 and was completed in February 2010. In December 2011, the Company halted production due to its inability to agree upon the price of its product with its principal customer and to implement certain design changes to upgrade the production lines at the facility to improve iron ore refinement and increase the iron ore concentration rate and, subsequently, add the ability to produce DRI. The construction for China Jinxin’s DRI facility upgrade was mostly complete as of the date of this report date and we are currently testing and adjusting the equipment prior to commencing production. The Company expects it will have the ability to resume commercial production in the second half of 2016.

Temporary manufacturing licenses for the production facilities were obtained from Zhangjiakou City on March 22, 2009, March 23, 2010, January 1, December 30, 2011 and December 27, 2014, respectively. The Company is currently in the process of applying for the new license; however, it is not able to give the expected date for the license approval.

China Jinxin has entered into a 10 year contract with Handan Steel Group Company (“HSG”), a subsidiary of Hebei Steel and Iron Company, a state owned enterprise, which expires in January 2019, whereby China Jinxin agreed to sell and HSG agreed to purchase all of the output from our production facility. The price we receive for our output is determined by HSG in light of market prices and the quality of our product and is to result in a reasonable profit margin to us. If China Jinxin is not satisfied with the price set by HSG it can attempt to renegotiate the price. China Jinxin has withheld deliveries from HSG since the end of 2011 because of its dissatisfaction with the price offered by HSG. If this dispute should continue, we will not be able to generate revenue from our production of iron ore which would have a materially adverse effect on our operations.

China Jinxin was established in December 2006 in Zhuolu County, Hebei Province, Northern China. China Jinxin has registered capital of RMB 36 million ($5.7 million). When formed, China Jinxin had registered capital of RMB 6 million ($909,000).

We operate China Jinxin as a variable interest entity through the VIE Agreements, a series of contractual agreements with China Tongda, our WFOE, which gives us effective control of the management and operations of China Jinxin. As compensation for its services China Tongda is entitled to receive each month an amount equal to the pre-tax profits of China Jinxin. Through the VIE Agreements, we are irrevocably given the right to control the operations of China Jinxin and to exercise the rights of its shareholders and Board of Directors (“BOD”). The rights we were granted include the right to make all decisions implicating the operational management, financial management, capital management, asset management, human resource management and daily operations of China Jinxin. Pursuant to the VIE Agreements, we also assume all the operational risks associated with China Jinxin and are responsible for any loss incurred by China Jinxin.

The PRC government continues to exercise substantial control over many sectors of the Chinese economy. Part of this control is through regulations. Among these are regulations on foreign ownership of certain companies and regulations on the ability of Chinese citizens to shift ownership of domestic Chinese companies to offshore enterprises. In August 2006, the Ministry of Commerce, or MOFCOM, the China Securities Regulatory Commission, or CSRC, the State-owned Assets Supervision and Administration Commission, the State Administration of Taxation, or SAT, the State Administration of Industry and Commerce and the State Administration of Foreign Exchange, or SAFE, jointly promulgated the “Rules on the Mergers and Acquisition of Domestic Enterprises by Foreign Investors,” which became effective in September 2006, and were amended on June 22, 2009. These rules are referred to herein as the “M&A Rules.” The M&A Rules confirmed that MOFCOM is a key regulator for mergers and acquisitions in China and require MOFCOM approval of a broad range of mergers, acquisitions and investment transactions. Among other things, the M&A Rules include provisions that purport to require that an offshore special purpose vehicle, or SPV, controlled directly or indirectly by PRC companies or individuals, formed for the purpose of offering their equity interests in domestic companies they control, must obtain the approval of the CSRC prior to the listing and trading of such SPV’s securities on an overseas stock exchange.

On September 21, 2006, the CSRC published on its official website procedures specifying documents and materials required to be submitted to it by SPVs seeking CSRC approval of their overseas listings. However, the application of these regulations remains unclear with no consensus currently existing among the leading PRC law firms regarding the scope and applicability of the CSRC approval requirement to various types of transactions, including those which involve the use of VIE agreements.

At the time of the acquisition of Real Fortune BVI by Target, the shareholders of China Jinxin desired to access the capital markets outside of China to expand its operations. These shareholders believed that prior consent of the CSRC would be required if they were to cause the shares of China Jinxin to be owned by a foreign entity but that consent would not be required if they and China Jinxin entered into the VIE Agreements with China Tongda, even if China Tongda was owned by a foreign entity. Through these contractual arrangements or VIE Agreements, acting through China Tongda, we have the ability to substantially influence China Jinxin’s daily operations and financial affairs, appoint its senior executives and approve all matters requiring stockholder approval. As a result of these contractual arrangements pursuant to generally accepted accounting principles in the United States (“US GAAP”), we are considered the primary beneficiary of China Jinxin. The shareholders further believed that there was no need to obtain the approval of the CSRC pursuant to the M&A Rules given that:

|

●

|

Our Company and its offshore subsidiaries did not acquire an equity interest in any PRC company.

|

|

●

|

China Tongda was incorporated as a wholly foreign-owned enterprise by means of direct investment rather than by merger or acquisition by our Company of the equity interests or assets of any “domestic company” as defined under the M&A Rules, and no provision in the M&A Rules classifies the contractual arrangements between China Jinxin and China Tongda as a type of acquisition transaction falling under the M&A Rules.

|

Although we believe there are no justifiable grounds for the PRC government to terminate or amend the VIE Agreements, the PRC government has taken actions to assert control over businesses regardless of whether or not there was clear authority or precedent for it to do so. Further, on August 25, 2011, MOFCOM issued Announcement No. 53 “Measures on the Security Review System of Foreign Investors Merging and Acquiring Domestic Enterprises” which came into effect on September 1, 2011, and to implement Circular 6, the “Notice on Establishing a Security Review System for Acquisition of Domestic Enterprises by Foreign Investors.” Circular 6 gives the PRC Government authority to determine what transactions affect national security interests and to change the terms of a transaction or cancel it to mitigate national security risks. Announcement No. 53 makes it clear that use of a VIE structure does not exempt a transaction from review pursuant to Circular 6. The list of industries which may be deemed to implicate national security interests is broad and may be increased by the PRC authorities. The grant of such broad authority and the absence of relevant guidelines and precedent creates the risk that the PRC authorities, for reasons not known to us, could determine that the VIE Agreements need to be canceled or amended.

Our Industry:

Introduction to iron ore

Iron ore is the main source of iron for the world’s iron and steel industries. It is an essential component used in the production of steel. Approximately 98% of the global supply of iron ore is used in steelmaking. Iron ore refers to rock that contains a sufficient level of iron minerals that can be mined economically. Iron ore is mainly composed of compounds of iron and oxygen (iron oxides) mixed with gangue, or impurities that are not generally utilized commercially. The most common types of iron ore are magnetite and hematite. Other iron ore types that naturally occur include limonite, siderite geothite, pyrite, chamosite and greenalite. When heated in the presence of a reductant, iron ore will yield metallic iron (Fe). Iron ore is graded according to size as “lumps” or “fines” based on whether the individual particles have a diameter of more or less than six millimeters. Iron concentrate is the valuable fines that are separated commercially from iron ore in the form of rock with gangue by crushing, grinding, and beneficiation and can be agglomerated before being used in an iron making blast furnace or a direct reduction furnace. Iron ore is used directly as lump ore, or as concentrate or fines converted into pellets or sinter.

Our Iron Ore Production Facilities

China Jinxin

China Jinxin has an iron ore concentrate production line with an annual capacity of 300,000 tons and associated plant and office buildings (hereinafter collectively referred to as "production facilities") in Zhangjiakou, Hebei Province (coordinates of N 40°16’-40°17’, E 115°16’~117°17’). The production facilities include a crushing line, a magnetic separation facility, a tailing disposal line and electric transformers. China Jinxin started building these facilities in May 2007 and started production in March 2010. During the six months of 2010 during which our plant was in operation and the seven months of 2011 during which we processed iron ore, we processed 397,860 tons and 326,293 tons, respectively, of crude iron ore from which we recovered 110,569 tons and 70,440 tons, respectively, of iron ore concentrate. In December 2011, the Company halted production due to a pricing dispute with its principal customer and to implement certain design changes to upgrade the production lines at the facility to improve iron ore refinement and increase the iron ore concentration rate and later to add the capacity to produce DRI. As of the date of this report, this upgrade was nearly complete and we expect to commence production at this facility in the second half of 2016. China Jinxin’s production facilities were constructed on the surface of a portion of the Zhuolu Mine. The Zhuolu Mine is currently state-owned. The local Zhuolu county government is in the process of registering the Zhuolu Mine with the State Department of Land and Resources of Hebei Province and once such process is completed, the rights to explore the mine will be granted by the Province to the Zhuolu County government and then it will be in a position to grant mining rights to a mining and exploration company through public bidding.

The production facilities were granted a Record-keeping Certificate of Fixed Assets Investment by the development and reform commission of the county-level government in July 2007. The evaluation report of the environmental effects of the project was approved by the city-level environmental protection authorities in July 2007. In connection with the development of these facilities China Jinxin acquired the necessary water permit which was originally valid through December 2011 and which was extended until April 13, 2016. The Company is currently applying for the new water permit.

China Jinxin successively obtained temporary manufacturing licenses for metallurgical mineral production from Zhangjiakou City on March 22, 2009, March 23, 2010, January 1, December 30, 2011 and December 27, 2014, respectively. The Company is currently in the process of applying for the new license; however,it is not able to give the expected date for the license approval. The licenses permit China Jinxin to produce only metallic iron and no other metals. The right to grant manufacturing licenses is held by Zhangjiakou City and if the Company receives the mining rights on Zhuolu Mine, it intends to apply for a permanent manufacturing license, which, if granted, will have a term of three years.

China Jinxin’s production facility includes a crushing line which can process up to 8,000 tons of crude iron ore per day. It has 45 crushing machines, six ball mills, three belt conveyors. The facility also includes 24 magnetic separation machines and 16 mechanical flotation machines. The magnetic separators can process up to 8,000 tons of crude iron ore per day. Ore is generally run through the magnetic separators three times before it moves to the next stage of processing.

The facility’s tailing disposal line can process up to 5,000 cubic meters of water per day. In addition, there is an impounding reservoir on the mine which has a capacity of 50 million cubic meter of water for use in processing iron ore.

.

When the upgrade of the China Jinxin facility is completed, the facility will include the equipment necessary to produce DRI. The facility will utilize both iron ore produced at the facility and iron sands as the raw material to produce DRI. The DRI equipment being installed at the China Jinxin facility is substantially identical to the equipment in China Huaxin's facility and includes 2 sets of Rotary Kiln with 36m in length and processing 6000 tons raw material per day and 3 sets of Gas Furnace to produce carbon monoxide for reducing. The upgraded facility also has 6 sets of Grinding Equipment and 3 sets of Wet Magnetic Separation Machinery with processing capacity 7200 tons per day. The finished products use 30 sets Hydraulic Machine to press block with 5,000 tons designed production capacity.

China Huaxin

China Huaxin has constructed a DRI production facility (the “DRI Facility”) in Haixing County, Hebei Province, about 50 km from the nearest port. The total amount expended to construct the DRI Facility, inclusive of both hard and soft costs, was approximately 244,270,000 RMB or US $39 million. This DRI Facility will produce direct reduced iron using advanced reduction rotary kiln technology with iron sand as the principal raw material. China Huaxin intends to import iron sands from New Zealand, Australia, Indonesia and the Philippines.

‘Reduced iron’ derives its name from the chemical change that iron ore undergoes when it is heated in a furnace at high temperatures in the presence of hydrocarbon-rich gasses. ‘Direct reduction’ refers to processes which reduce iron oxides to metallic iron below the melting point of iron. The product of such solid state processes are called direct reduced iron (DRI). The Company’s DRI Facility is projected to produce DRI with an iron grade of over 92%.

The Company’s DRI Facility occupies an area of 200,000 m2 The DRI Facility occupies 60,000 m2, of land and there is a raw material storage area of 14,000 m2 with a 100,000 ton storage capacity, a workshop area of 4500 m2, a water storage pool of 4000m3 to supplement water supplies, and an office building of 2,400 m2. The plant design is intended to permit the processing of 2,000,000 tons of iron sand per annum with an annual output capacity of 1,000,000 tons of DRI.

The equipment installed in the DRI Facility includes 2 sets of Rotary Kilns that are 36m each in length and capable of processing 6000 tons of raw material per day, and 3 sets of Gas Furnaces to produce carbon monoxide for use in the reduction process. The equipment also includes 6 sets of Grinding Equipment and 3 sets of Wet Magnetic Separation Machineries with processing capacity of 7200 tons per day. In addition there are 30 sets of Hydraulic Machines with a capacity of 5,000 tons per day to press block the finished product.

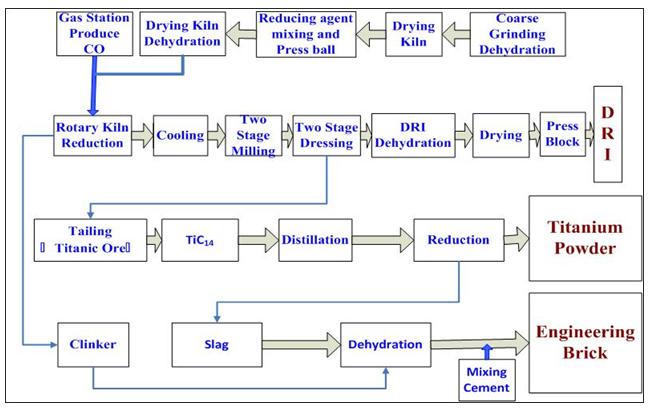

DRI Production Process

A DRI kiln is a cylindrical vessel, inclined slightly to the horizontal, which is rotated slowly around its axis. The material to be processed is fed into the upper end of the cylinder. As the kiln rotates, the materials gradually move down towards the lower end, and may undergo a certain amount of stirring and mixing. Hot gases pass along the kiln sometimes in the same direction as the process material (co-current), but usually in the opposite direction (counter-current). The hot gases may be generated in an external furnace, or may be generated by a flame inside the kiln. Such a flame is projected from a burner-pipe (or 'firing pipe') which acts like a large burner. The fuel may be gas, oil or pulverized coal.

As illustrated below, the production process consists of the following steps:

|

1)

|

Blending iron sand and reducing agent together,

|

|

2)

|

Placing the mixed raw material into ball press machinery,

|

|

3)

|

Transferring the globular raw material to rotary kiln for high-temperature drying,

|

|

4)

|

Transferring the dry material to secondary rotary kiln and reaction with carbon oxide generated from coal-gas furnaces to produce low grade directly reduced iron (DRI),

|

|

5)

|

Cooling the DRI and subjecting it to crushing, milling and beneficiation (CMB) circuit to get high grade DRI; and

|

|

6)

|

Press blocking the DRI to get the finished product.

|

Our Products

To date we have produced iron ore concentrate from iron ore extracted from the state-owned Zhuolu Mine. The concentrate we produced has had a number of commercially attractive characteristics, including high iron content and relatively low levels of impurities, such as sulphur, phosphorus, silicon and titanium, the presence of which is generally undesirable for steel production. As a result, we have been able to efficiently produce high quality iron ore concentrate through simple, low-cost magnetic processing methods. Our iron concentrate has been graded at 66%, sufficient for the production of crude steel which generally requires concentrated iron graded at 63.5%~66%.

We have mined and processed iron ore from the Zhuolu Mine. In connection with the construction of our facilities we were granted the right to process ore displaced during the course of construction. However, the ore from the Zhuolu Mine we mined and processed exceeds what we were permitted to mine, and we have not been granted mining rights by the Department of Land and Resources of Hebei. Pursuant to the Mineral Resources Law of PRC, promulgated on March 19, 1986, effective on October 1, 1986 and amended on August 29, 1996, and the related implementation rules promulgated on March 26, 1994 (collectively, the “Mineral Resources Law”), any entity which mines without a mining permit shall be ordered to cease mining and compensate for the losses caused; any mineral products and unlawful proceeds it realized shall be confiscated; and it also should receive fines of up to 50% of its unlawful proceeds. If we were sanctioned in accordance with these rules, all of the net income from our mining activities could be confiscated, and we could be subject to fines of up to 50% of the total net income. In such event, our results of operation and financial condition would be materially and adversely affected.

Although we have ceased mining while we upgrade our facilities, the authorities in Hebei know we have mined iron ore in excess of what we were permitted to mine when constructing our facilities and have taken no action to halt our activities. In any event we will seek to acquire iron ore from third parties due to the uncertainty over our ability to extract ore from the Zhuolu Mine. The failure to obtain iron ore reserves for processing at all or on reasonably acceptable terms would have a material adverse impact on our business and financial results.

Raw Material- Iron Sand

Iron sand is a type of sand with heavy concentrations of iron. It is typically dark grey or blackish in color. It comprises mainly magnetite, Fe3O4, and also contains small amounts of titanium, silica, manganese, calcium and vanadium. New Zealand, Australia, Indonesia and the Philippines have significant quantities of iron sand.

Huaxin plans to import iron sand from New Zealand and Australia. The management is negotiating with two companies in terms of price, quantity, grade and contract terms. As the designed production capacity releases, Huaxin will also consider importing from other regions to satisfy expansion requirements.

Customers

China Jinxin

To date, one customer, Handan Steel Group Company (“HSG”), a subsidiary of Hebei Steel and Iron Company, a state owned enterprise, has accounted for nearly 100% of our sales. China Jinxin has entered into a 10 years contract with HSG expiring in January 2019 whereby China Jinxin agreed to sell and HSG agreed to purchase all of the output from our production facility. The price we receive for our output is determined by HSG in light of market prices and the quality of our product and is to result in a proper profit margin to us. If China Jinxin is not satisfied with the price set by HSG it can attempt to renegotiate the price. China Jinxin has withheld deliveries from HSG since the end of 2011 because of its dissatisfaction with the price offered by HSG. There is no assurance as to what recourse China Jinxin would have if the prices set by HSG were unacceptable.

China Huaxin

China Huaxin plans to sell its DRI to companies located in the southern provinces of China, including Shanghai, Jiangsu and Zhejiang province.

Suppliers

Our major suppliers include suppliers of machinery and equipment, spare parts, diesel fuel, electricity and water. Our operations use electricity supplied by the local power grid. We use water sourced from nearby rivers at our processing plants. We also recycle and reuse water from our tailings ponds.

We obtain gas and diesel fuel from local gas stations and incurred costs of $0 for 2015 and 2014 due to no production. We did not have any specific major suppliers for 2015 and 2014 due to no material production activities.

The energy produced in parts of China is not yet sufficient to satisfy the needs of all businesses seeking to obtain power. Consequently, there are occasional power outages and brownouts. We ceased production from September 2010 to March 2011 due to the implementation by the local government of an “Energy Saving and Emission Reduction Plan.” To reduce power consumption for a certain period the local government adopted this plan whereby nearly all construction and processing plants in Zhuolu County were required to halt production for a specified period. In an effort to insulate ourselves from this problem, we have installed an Electricity Converting Station which can convert high voltage electricity to low voltage electricity, and it can also use diesel to generate power when there’s no electricity. This should enable us to maintain full production should we once again be cut off from electricity generated by the local power company. Nevertheless, management believes that the Energy Saving and Emission Reduction Plan enacted by the local government which forced all iron ore producers in the area of our plant to shut down was a one-time event and disruptions to our access to energy will not have material impact on our production in the future.

Huaxin plans to import iron sand from New Zealand and Australia. We are negotiating supply contracts with two companies in terms of price, quantity and grade.

Mining Rights

Iron ore mining enterprises in China must obtain a mining permit and a production safety permit for each mine prior to conducting mining operations. In connection with the construction of our facilities at the Zhuolu Mine we were granted the right to process ore displaced during the course of construction. However, the ore from the Zhuolu Mine we have mined and processed since August 2011, exceeds what we were permitted to mine, and we have not been granted mining rights by the Department of Land and Resources of Hebei or by any other mining authority We have, however, obtained a temporary manufacturing license for metallurgical mineral production, which enables us to process iron ore. Pursuant to the Mineral Resources Law, any entity which mines without a mining permit shall be ordered to cease mining and compensate for the losses caused; any mineral products and unlawful proceeds it realized shall be confiscated; and it also should receive fines of up to 50% of its unlawful proceeds. If we were sanctioned in accordance with these rules, all of the net income from our mining activities will be confiscated, and we will be subject to fines of up to 50% of the total net income. In such event, our results of operation and financial condition would be materially and adversely affected. So far, we have not received any penalty notice from any relevant authorities.

If we do not obtain mining rights to the Zhuolu Mine in the foreseeable future, we will seek to acquire iron ore from third parties. The failure to obtain iron ore reserves for processing at all or on reasonably acceptable terms would have a material adverse impact on our business and financial results. The Company is currently in the process of applying for mining rights, and expects to be granted such rights, though there is no assurance that such rights will be obtained.

The Zhuolu county government engaged the Hebei Province Institute of Geological Survey (“the Institute”), an independent state-owned authorized geological survey entity, to carry out a geological survey on the Zhuolu Mine. The Institute obtained survey approval from the State Department of Land and Resources of Hebei Province and conducted the survey. In May 2011, the Institute issued its Geological Evaluation Report (“the Report”) and submitted the Report to Department of Land and Resources of Hebei. The Zhuolu county government has applied to the State Department of Land and Resources of Hebei for mining permit for the Zhuolu Mine (“Mining Rights”) and expects to receive the rights within one year. Once the Mining Rights are granted by the Province, the Zhuolu county government will assign the Mining Rights to outside mining and exploration companies through public bidding.

To accelerate the process whereby China Jinxin might obtain a mining permit, China Jinxin entered an agreement dated April 11, 2011, with the Zhuolu county government regarding the geological survey of the Zhuolu Mine. Pursuant to this agreement, China Jinxin prepaid all the fees related to the geological survey for the Zhuolu county government, RMB1.98 million ($313,000). The Zhuolu county government agreed that if China Jinxin obtains the Mining Rights through public bidding, the amount paid for the survey by China Jinxin will be credited against the price of the Mining Rights and if China Jinxin does not obtain the Mining Rights, the Zhuolu county government will reimburse the geological survey fees to China Jinxin. The county government also agreed that if China Jinxin were not to obtain the mining rights it would cause the winning bidder to give China Jinxin priority to purchase the crude iron ores extracted from the Zhuolu Mine.

Research and Development

We had no research and development expenses in 2014 or 2015. We currently have no plans for any research and development activities and do not anticipate any material research and development costs.

Our Growth Strategy

Chinese demand for iron or steel products has increased rapidly in recent years until the slowdown which began in 2008. We believe demand for high quality iron ore concentrate will resume growing domestically and globally, thus affording us an opportunity to grow and expand our business operations. We intend to seek to grow our business through the acquisition of mines and other production facilities, in particular, by acquiring the right to mine in the areas surrounding our current production facilities.

We anticipate some of our acquisitions will be of existing mines and some of undeveloped properties. In all cases, they will be properties with established reserves. Our five-year goal is to control 50 million tons of reserves and to produce up to 1.1 million tons of iron ore concentrate per year. Our primary criteria for selecting target mines are as follows:

|

1.

|

the resources, reserves and mining operations of the target mines;

|

|

2.

|

the grade, mining costs and sustainability of the target resources and reserves;

|

|

3.

|

exploration potential;

|

|

4.

|

the financial costs and benefits of the acquisition;

|

|

5.

|

valid land use rights and property ownership and no material legal risks; and

|

|

6.

|

the contributions of the acquisition towards the overall sustainability of our business.

|

We will finance our acquisitions, as well as the improvements necessary to existing mines and the development of mines on undeveloped properties, by using internally generated cash, if available, as well as cash raised by issuing equity securities and debt financing.

We anticipate all of our acquisitions will be in China. We also expect that our customer base will increase as we gain access to additional steel manufacturers.

Government Regulation

Regulations Relating to Exploitation and Mineral Rights

The PRC government maintains a Catalogue for the Guidance of Foreign Investment Industries (“Catalogue”), which was promulgated and is amended from time to time by the Ministry of Commerce (“MOFCOM”) and the National Development and Reform Commission (“NDRC”). The Catalogue divides industries into three categories: encouraged, restricted and prohibited. Industries not listed in the Catalogue are generally open to foreign investment unless specifically restricted by other PRC regulations. According to the Catalogue as revised on October 31, 2007, iron ore exploration, mining and mineral processing projects belong to the category of Encouraged Foreign Investment Industries. Despite the fact that iron ore exploration, mining and mineral processing projects belong to Category of Encouraged Foreign Investment Industries, the shareholders of China Jinxin elected to utilize the VIE structure in their efforts to raise capital because this structure has been accepted by investors in the United States and the shareholders believed that because it did not involve an acquisition of a domestic Chinese company it reduced the filings required to be made with and the permissions to be obtained from Chinese regulatory authorities relating to what could be deemed to be the transfer of their ownership interests outside of China.

Mining activities in the PRC are subject to the PRC Mineral Resources Law (“Mineral Resources Law”), promulgated by the PRC Government on March 19, 1986 and amended on August 29, 1996. The Mineral Resources Law regulates matters relating to the planning or engaging in the exploration, exploitation and mining of mineral resources. According to the Mineral Resources Law all mineral resources, including iron ore, are owned by the State. Except under limited circumstances, any enterprise planning to engage in the exploration, exploitation and mining of mineral resources must first apply for and obtain exploration rights and mining rights before commencing the relevant activities. The Mineral Resources Law prohibits the transfer of exploration and exploitation rights in general unless the transfer falls within certain specified circumstances. China Jinxin currently does not own any mines or hold any mining rights.

Pursuant to the Mineral Resources Law, any entity which mines without a mining permit shall be ordered to cease mining and compensate for the losses caused; any mineral products and unlawful proceeds it realized shall be confiscated; and it also should receive fines of up to 50% of it unlawful proceeds. Although we have extracted iron ore from the Zhuolu Mine, we do not have the right to do so. If we were sanctioned in accordance with the rules promulgated under the Mineral Resources Law, we could be required to cease operations at the mining site, all of the net income from our mining activities could be confiscated, and we could be subject to fines of up to 50% of the total net income. In such event, our results of operation and financial condition would be materially and adversely affected. So far, we have not received any penalty notice from any relevant authorities. If we do not obtain mining rights to the Zhuolu Mine in the future, we will seek to acquire iron ore from third parties. The failure to obtain iron ore reserves for processing at all or on reasonably acceptable terms would have a material adverse impact on our business and financial results.

Exploration, exploitation and mining operations must comply with the relevant provisions of the Mineral Resources Law and other relevant regulations, and are under the supervision of the Ministry of Land and Resources. Exploration and exploitation of mineral resources also are subject to examination and approval by the Ministry of Land and Resources and relevant local authorities. Upon approval, a mining permit is issued by the relevant administrative authorities, which are responsible for supervision and inspection of mining exploitation in their jurisdictions. The holders of mining rights are required to file annual reports with the relevant administrative authorities.

Mineral products illegally extracted and incomes derived from such activities may be confiscated and may result in fines, revocation of the mining permit and, in serious circumstances, criminal liability.

Regulations Relating to Metallurgical Mineral Production License

The Hebei Provincial Government implemented a production license system for metallurgical mineral products. On November 1, 2006, the Hebei Provincial Government promulgated Regulations on Supervision and Administration of Production and Operation of Metallurgical Mineral Products, and on January 28, 2011, issued its implementation regulations. According to these regulations, any company that engages in metallurgical mineral production must acquire a metallurgical mineral production license with a valid period of three years from the Hebei Provincial Government. If the business license, mining right or non-coal mine safety production license of the company is revoked or withdrawn, the metallurgical mineral production license will lapse.

China Jinxin obtained and then renewed its annual basis temporary metallurgical mineral production licenses issued by Zhangjiakou Metallurgical and Mineral Industrial Administration Agency. The current temporary license expires on February 26, 2015. The Company has filed an application to have the license renewed and expects its renewal application to be granted in the second quarter of 2015. China Jinxin intends to apply to the Hebei Provincial Government for a formal metallurgical mineral production license after obtaining its mining rights. There can be no assurance China Jinxin will be able to obtain a formal metallurgical production license. The failure to obtain the licenses necessary to continue to operate would have a material adverse effect on our operations and financial results.

Regulation Relating to Investment Projects

According to the Decision of the State Council on Reforming the Investment System promulgated on July 6, 2004, with the exception of iron ore projects with proved industrial reserves equal or above 50 million tons and iron making, steel making and steel rolling projects increasing production capacity, which shall be verified and approved by the investment administration authority of the State Council; all other iron ore development projects must be verified and approved by the investment administration authorities of provincial governments. China Jinxin’s iron ore concentration projects with annual production capacity of 300,000 tons was verified and approved by the Hebei Development and Reform Commission on January 22, 2007.

Regulations on Environmental Protection

The major environmental regulations applicable to us include the Environmental Protection Law of the PRC, the Water Pollution Prevention Law of the PRC, the Atmospheric Pollution Prevention Law of the PRC, the Environmental Impact Assessment Law of the PRC and the Law of the PRC on the Prevention and Control of Environmental Pollution by Solid Waste and the Regulations Governing Environmental Protection in Construction Projects. Also, general environmental regulations relating to noise and the treatment of industrial waste are applicable to our operations.

All phases of our operations are subject to environmental regulations and discharge standards promulgated by governmental agencies in China. Before we may begin project development and production, we must comply with environmental regulations and standards. Environmental regulations set forth limits and prohibitions on spills, releases or emissions of various substances produced in association with certain processing and manufacturing operations. A breach of any regulations may result in imposition of fines and penalties and even curtailment or suspension of our operations. Furthermore, future changes in environmental laws and regulations could result in stricter standards and enforcement, larger fines and liability, and increased capital expenditures and operating costs, any of which could have a material adverse effect on our financial condition or results of operations.

China Jinxin entrusted the Environmental Protection and Research Institute of Zhangjiakou city to conduct the environmental impact assessment of its iron ore mining and selecting project, and the Environmental Impact Report was issued in May 2007. Based on this report, Zhangjiakou Environmental Protection Department approved constructing and upgrading China Jinxin's production facility on July 26, 2007.

Regulations on Water Drawing

Pursuant to the Regulation on the Administration of the License for Water Drawing and the Levy of Water Resource Fees promulgated on February 21, 2006, effective on April 15, 2006, any entity or individual that draws water resources shall, except for the circumstances prescribed in the Regulation, apply for a license certificate for water drawing, and pay water resource fees. The valid term of a license certificate for water drawing is generally five years, and may not exceed 10 years. If, at expiry of the valid term, the license certificate needs to be renewed, the water drawing entity or individual shall file an application with the organization, which granted the certificate within 45 days prior to the expiry of the term. The organization shall, prior to the expiry of the term, decide whether or not to approve the renewal.

China Jinxin received a License for Water Drawing from the local water bureau with yearly water drawing of 20,000 cubic meters of water on December 7, 2006. In April 2011, China Jinxin renewed the License and the current water license expires on April 13, 2016, with yearly water drawing of 15,000 cubic meters of water per annum. The Company is currently applying for the new water license.

Regulations on Annual Inspection

In accordance with relevant PRC laws, all types of enterprises incorporated under PRC laws are required to conduct annual inspections with the State Administration for Industry and Commerce of the PRC or its local branches. In addition, foreign-invested enterprises are subject to annual inspections conducted by other applicable PRC governmental authorities. In order to reduce enterprises’ burden of submitting inspection documentation to different governmental authorities, the Measures on Implementing Joint Annual Inspection on Foreign-invested Enterprises issued in 1998 by SAFE, together with six other ministries, stipulated that foreign-invested enterprises must participate in an annual inspection jointly conducted by all relevant PRC governmental authorities.

Regulation Relating to Mining Safety

Pursuant to the Work Safety Law of the PRC promulgated on June 29, 2002 and effective on November 1, 2002 and the Law of the PRC on Safety in Mines and its related implementation rules promulgated on November 7, 1992 and October 30, 1996 and effective on May 1, 1993 and October 30, 1996, respectively, (a) safety facilities in mine construction projects must be designed, constructed and put into operation at the same time as the commencement of the principal parts of the projects; (b) the design of a mine shall comply with the safety rules and technological standards of the mining industry and shall be approved by the relevant authorities; and (c) such mines may start production or operations only after they have passed the safety check and approval process as required by the relevant PRC laws and administrative regulations.

The Regulation on Work Safety Licenses was promulgated and became effective on January 13, 2004. Pursuant to the regulation, (a) the work safety licensing system is applicable to any enterprise engaging in mining and such enterprise may not produce any products without obtaining a work safety license; (b) prior to producing any products, the mining enterprise shall apply for a work safety license, which is valid for three years; and (c) if a work safety license is required to be extended, the enterprise must apply for an extension with the administrative authority who issued the original license within three months prior to the expiration of the original license.

In addition, the Implementation Measures for non-coal mining enterprises work safety licenses was promulgated and became effective on June 8, 2009. Under this legislation, non-coal mining enterprises, i.e., metal and non-metal mine enterprises, and also its tailings ponds, geological exploration units, mining engineering corporations, oil and natural gas enterprises need to obtain a safety production permit before any productive activities, every independent productive system of the metal and nonmetal mine enterprises need to obtain a separate safety production permit. The licenses last for three years, and can be extended if the non-coal mining enterprises apply to the administrative authority three months before its expiration date.

Pursuant to the Provisional Regulations on the Installation, Use, Monitoring and Inspection of the ‘‘Six Major Systems’’ for Safety and Refuge in Underground Metal and Non-metal Mines promulgated on October 9, 2010 by the State Administration of Work Safety, underground metal and non-metal mines should install the ‘‘six major systems’’ for safety and refuge, namely monitoring and control systems, underground workers positioning system, emergency refuge system, pressurizing self-rescue system, water supply rescue system and communications system according to the time limit set down by the regulations, and should also have in place specially designated staff for the management and maintenance of these systems. The safety production permits shall be withheld by safety production regulation authorities above county level for enterprises operating on underground mines which have failed to comply with the requirements to complete the construction of such ‘‘six major systems’’ for safety and refuge within the time limit, which shall be ordered to make rectifications within a time limit, failing which the local government is entitled to shut down the operations of such enterprises.

Pursuant to the Provisional Regulations on Requirements for Management Members of Metal and Non-metal Mining Enterprises to Accompany Workers in Descending and Ascending Underground Mines and the Monitoring and Inspection of Compliance Therewith in effect from November 15, 2010, mining enterprises must ensure there is at least one responsible person (person-in-charge, member of the management or deputy chief engineer) for each group to carry out on-site underground mining operations and that he shall accompany workers in descending and ascending the underground mines. Where mining enterprises have failed to establish a complete and sound or any system for management members to lead workers in underground mining operations in accordance with the regulations, such enterprises shall be given warnings and shall be fined RMB 30,000 ($4,800); the persons-in-charge shall also be warned and fined RMB 10,000 ($1,600); where the contravention is serious, the safety production permit shall be withheld and the operation shall be suspended for rectifications in accordance with the law. Where management members of mining enterprises have failed to lead workers in underground mining operations, such enterprises shall be given warnings and be fined RMB 30,000; where the contravention is serious, the operation shall be suspended for rectifications in accordance with the law, and management members who have breached the regulations shall be deemed to have left their post without permission and shall be fined RMB 10,000 ($1,600).

Pursuant to the Law Of The PRC On Safety In Mines adopted on November 7, 1992, and Implementing Rules on the Law Of The PRC On Safety In Mines of Hebei Province effective in September 1995, as amended in December 1997, the designs of safety facilities in mine construction projects must be examined by the administration department of mining enterprises together with the participation of the competent department of labor administration; and upon completion, the safety facilities in mine construction projects shall be subject to inspection for acceptance by the authorities in charge of mining enterprises, with participation of the competent department of labor administration; those failing to comply with the safety rules and technological standards for mining industry may not pass inspection for acceptance, and may not be put into operation; managers of mines must prove, through examination, to have special knowledge of safety and the capability of leading safe production and disposing of accidents in mines; personnel in charge of safety work in mining enterprises must possess necessary specialized knowledge of safety and experience in safety work in mines; special operators in charge of safe production in mining enterprises must receive special training; they may take up a post of such duty only after they have obtained a certificate of operation qualification after passing due examination and verification. The law also provides for the conditions for safe production, the requirements to implement safety rules and industry technical specifications, and to prepare and implement operational procedures.

In March 2009 China Jinxin received its first temporary production license pursuant to which it began production in March 2010. Because China Jinxin has not been granted a mining license, as opposed to a production license, it is not required to obtain the production safety licenses described above. If China Jinxin was to obtain mining rights, it would apply for the required production safety licenses. Currently, China Jinxin is recruiting mining managers with experience in obtaining the required safety certificates.

Pursuant to the Regulation on the Safety Administration of Explosives for Civilian Use adopted on April 26, 2006, the State applies a licensing system to the production, sale, purchase, transport and blasting operation of explosives for civilian use. As a mining company, China Jinxin needs to obtain the Purchase Permit of Explosives for Civil Use and Blasting Operation Permit to purchase and use explosives legally. China Jinxin is currently applying for the two permits.

Regulations on Work Safety

The Work Safety Law of PRC (the “Work Safety Law”) was promulgated as of June 29, 2002. It regulates the work safety of entities that engage in production and business operation activities within the territory of the PRC (hereinafter referred to as “production and business operation entities”). All production and business operation entities must observe the Work Safety Law and any other relevant laws or regulations concerning work safety, strengthen the administration of work safety, establish and perfect the system of responsibility for work safety, perfect the conditions for safe production, and ensure safety during production. The production and business operation entities must provide conditions for safe production as provided in the Work Safety Law and other relevant laws, administrative regulations, national standards and industrial standards.

Any entity that does not maintain the conditions for safe production may not engage in production and business operation activities.

The Department of the State Council in charge of the supervision and administration of work safety is required to implement comprehensive supervision and administration of work safety in the PRC. The relevant governmental authorities superior to the county level and in charge of the supervision and administration of work safety are required to implement comprehensive supervision and administration of work safety within their respective administrative jurisdictions according to the Work Safety Law.

In case of a violation of the Work Safety Law, the relevant authorities can order the decision-making department or key person-in-charge of any production and business operation entity to correct the violation, suspend production or business and can take other administrative measures. If a work safety accident has resulted and a crime has been committed, the key person-in-charge may assume criminal liabilities according to the relevant provisions of the Criminal Law.

Regulations on Foreign Currency Exchange

Pursuant to the Foreign Currency Administration Rules promulgated in 1996 and amended in 2008 and various regulations issued by the State Administration of Industry and Commerce and the State Administration of Foreign Exchange (“SAFE”) and other relevant PRC governmental authorities, Renminbi are freely convertible only to the extent of current account items, such as trade related receipts and payments, interest and dividends. Capital account items, such as direct equity investments, loans and repatriation of investment, require prior approval from SAFE or its local counterpart for conversion of Renminbi into a foreign currency, such as US dollars, and remittance of the foreign currency outside the PRC.

Payments for transactions that take place within the PRC must be made in Renminbi. Unless otherwise approved, PRC companies must repatriate foreign currency payments received from abroad. Foreign-invested enterprises may retain foreign exchange in accounts with designated foreign exchange banks subject to a cap set by SAFE or its local counterpart. Unless otherwise approved, domestic enterprises must convert all of their foreign currency receipts into Renminbi.

On August 29, 2008, SAFE promulgated a circular regulating the conversion by a foreign-invested company of its registered capital in foreign currency into Renminbi by restricting how the converted Renminbi may be used. This circular stipulates that the registered capital of a foreign-invested company settled in Renminbi converted from foreign currencies may only be used for purposes within the business scope approved by the applicable governmental authority and may not be used for equity investments within China. Violations of this circular can result in severe penalties, including monetary fines.

In addition, any foreign loans to an operating subsidiary in China that is a foreign invested enterprise, cannot, in the aggregate, exceed the difference between its respective approved total investment amount and its respective approved registered capital amount.

Regulation on Foreign Exchange in Certain Onshore and Offshore Transactions

In October 2005, SAFE issued Circular 75, which regulates foreign exchange matters in relation to the use of a “special purpose vehicle” by PRC residents to seek offshore equity financing and conduct “return investment” in China. Under Circular 75, a “special purpose vehicle” refers to an offshore entity established or controlled, directly or indirectly, by PRC citizens or PRC entities (collectively, as PRC residents) for the purpose of seeking offshore equity financing using assets or interests owned by such PRC residents or PRC entities in onshore companies, while “round trip investment” refers to the direct investment in China by PRC residents through the use of “special purpose vehicles,” including without limitation, establishing foreign invested enterprises and using such foreign invested enterprises to purchase or control (by way of contractual arrangements) onshore assets. Circular 75 requires that, before establishing or controlling a “special purpose vehicle,” PRC residents are required to complete foreign exchange registration with the competent local counterparts of SAFE for their overseas investments. In addition, such PRC resident is required to amend his or her SAFE registration or to file with SAFE or its competent local branch, with respect to that offshore special purpose vehicle in connection with any increase or decrease of capital, transfer of shares, merger, division, equity investment or creation of any security interest over any assets located in China by the offshore special purpose vehicle. To further clarify the implementation of such amendment or filing procedure, SAFE requires domestic enterprises under Circular 75 to coordinate and supervise such amendment or filings with SAFE or its local counterparts by such PRC residents. If PRC residents fail to comply, the domestic enterprises are required to report to the local SAFE authorities.

Failure to comply with the registration procedures set forth in Circular 75 may result in restrictions being imposed on the foreign exchange activities of the relevant onshore company, including being prohibited from distributing its profits and proceeds from any reduction in capital, share transfer or liquidation to its offshore parent or affiliate, and restrictions on the ability to contribute additional capital from the offshore entity to the PRC entities, and may also subject relevant PRC residents to penalties under PRC foreign exchange administration regulations.

Regulation on Overseas Listings

On August 8, 2006, MOFCOM, the CSRC, the State-owned Assets Supervision and Administration Commission, the SAT, the State Administration of Industry and Commerce and SAFE jointly promulgated the “Rules on the Mergers and Acquisition of Domestic Enterprises by Foreign Investors,” which became effective on September 8, 2006, and was further amended on June 22, 2009, or the M&A Rules.

Among other things, the M&A Rules include provisions that purport to require that an offshore special purpose vehicle, or SPV, formed for listing purposes and controlled directly or indirectly by PRC companies or individuals must obtain the approval of the CSRC prior to the listing and trading of such SPV’s securities on an overseas stock exchange. On September 21, 2006, the CSRC published on its official website procedures specifying documents and materials required to be submitted to it by SPVs seeking CSRC approval of their overseas listings. However, the application of this PRC regulation remains unclear with no consensus currently existing among the leading PRC law firms regarding the scope and applicability of the CSRC approval requirement to various types of transactions, including those which involve the use of variable interest entity agreements.

Regulations on Dividend Distribution