Attached files

| file | filename |

|---|---|

| 8-K - STEEL PARTNERS HOLDINGS L.P. | form8k04197004_04112016.htm |

Exhibit 99.1

April 13, 2016

To the Unitholders of Steel Partners Holdings L.P.:

Nothing in the world can take the place of hard work and persistence. Potential is interesting, but execution is everything. There is no substitute for putting in the time and effort on the road to success. Steel Partners’ philosophies and strategies continue to endure and serve us well. We work hard and play hard.

We invest on the basis of value, not popularity. We invest in good companies with simple business models at prices that have built-in margins of safety. We create a continuous improvement culture and implement operational excellence programs. We control costs and use leverage prudently. We avoid complex businesses or investments that cannot be easily explained or understood. We reward people who deliver results and ensure the right core principles and culture.

Steel Partners and our affiliates have been successful at starting, buying, operating and building businesses over long periods of time. Our capital is not short-term, and our assets and liabilities are aligned. Often, we compete with private equity firms and strategic buyers, who are bidding up prices to levels which would not provide us with the margin of safety we seek or a high enough return on our invested capital. Therefore, they buy a lot of businesses, and we don’t.

Over the past few years, we have accelerated our M&A efforts and called our friends at various private equity firms, investment banks and hedge funds in order to increase our deal flow. We have been moderately successful in creating our own deals and a proprietary pipeline, but, frankly, we have failed miserably when we have tried to buy businesses by participating in auctions. The truth is, I really don’t like participating in auctions. It is expensive, time consuming, and we never win the prize.

Undeterred, we continue to look for bolt-on acquisitions for our existing companies and companies we are invested in: OMG, Lucas Milhaupt, JPS Composite Materials, Kasco SharpTech, Handy Tube, Indiana Tube, WebBank, API Group, Steel Energy, Steel Sports, Aerojet Rocketdyne, and ModusLink Global Solutions. We are also looking to buy new platform businesses, which are within our circle of competence and fairly priced.

At Steel Partners, we have the flexibility to buy parts of businesses (10-15%) with the ability to own up to 100% over time. The more we own, the greater our ability to achieve economies of scale and implement operational excellence and strategic programs through the Steel Business System, Steel Procurement Council, Steel Environmental Health & Safety Council, and Steel Grow. We can also implement capital allocation policies, corporate development guidelines, and reduce overhead costs, such as legal and accounting, through SPH Services.

1

We did this successfully at Handy & Harman, API, JPS, and are now buying all of SL Industries through Handy & Harman. This way, we can buy part of the company and live with the business and managers for a period of time and then decide if we want to own the entire business. Granted, we have made some mistakes in the past and have lost money, and will probably make more errors in the future. But hopefully, our successes will far outweigh and outnumber our mistakes and potentially increase our ownership over time.

In addition to looking for acquisitions, we will also use our capital to purchase our own shares when they are trading at a discount. In 2015, Steel Partners and our affiliates purchased 1,091,175 shares for $19.2 million at an average price of $17.63.

We will continue to buy and build for the long-term. In a sense, we are investing for our children and future generations. Over the last few months, the prices of stocks have gone down at a number of companies we would like to own for the long run. This has created more buying opportunities at attractive prices.

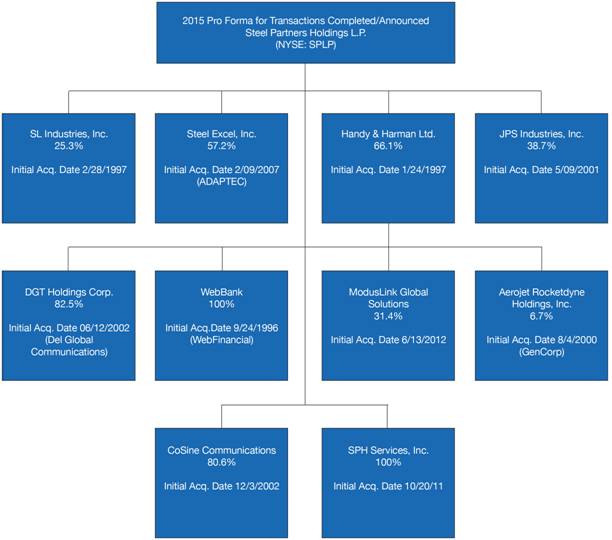

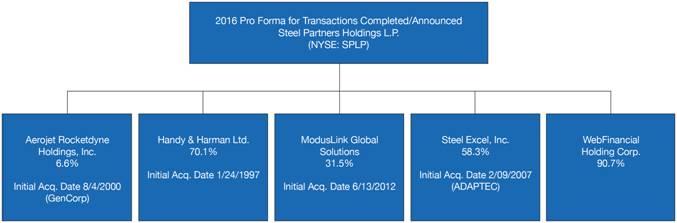

During the past year, we continued our program to simplify our business structure by reducing the number of entities, organizations, and companies we own and manage. As you can see in the org chart below, we have done a good job thus far, but still have more to do as part of this initiative.

We have publicly announced that Handy & Harman would like to acquire 100% of SL Industries. I am pleased to announce that on April 7, 2016, Handy & Harman entered into an agreement to acquire SL Industries for $40/share in cash or approximately $166 million in total.

Steel Partners and our affiliates currently own approximately 25.1% of SL Industries’ outstanding shares. In 1991, when we first purchased shares of SL Industries, it was trading at around $3.50. I was on the board from 1993-1997, and by 1997, SL Industries was trading at $11-12. I served as Chairman and CEO of SL Industries from 2002-2005, and by 2005, SL Industries was trading at $17-18. I have continued to serve on the board at various points over the past decade, as the stock has climbed. When this transaction is consummated, we will be on track with our business simplification plan.

Below you can see the progress we have made with our business simplification plan:

2

Prior State (as of May 2015):

Current State 2016 (pending Handy & Harman & SL Industries deal):

*DGT and SPH Services are included in SPLP

*CoSine and WebBank are included in WebFinancial Holding Corp.

3

* * * * *

Highlights of the important developments at Steel Partners since my last letter include:

|

-

|

Handy & Harman’s acquisition of JPS. After being an investor in JPS for more than 14 years, we successfully completed the acquisition of the shares we didn’t own. Under the terms of the parties' merger agreement, each outstanding share of JPS common stock (other than shares owned by Steel Partners) was converted into the right to receive $11.00 per share in cash.

|

|

-

|

CoSine was restructured to be a wholly owned private subsidiary of WebFinancial Holding Corporation, an indirect subsidiary of Steel Partners Holdings, LP.

|

|

-

|

The liquidation of the final SP II Trusts was completed. China Access (Trust H) was liquidated in February. Steel Partners Holdings, L.P. received $2.7 million. Japan Strategic Fund (Trust G) was liquidated in June. Steel Partners Holdings L.P. received $6.9 million. The distributions represented the Company’s proportional interest in the remaining cash in each Trust.

|

A Look at Our Financials

Currently, Steel Partners consists of 100%-owned businesses, controlled subsidiaries and some non-controlled businesses. Today, we have approximately 26 businesses with a total of more than 13,500 employees and 155 plants operating in 20 countries.

Steel Partners reported revenues of $998.0 million in 2015, as compared to $849.5 million in 2014. Our reported net income was $136.7 million, or $4.98 cents per fully diluted common unit. Due to the complexity of our financial statements, we believe one should value Steel Partners using a sum-of-the-parts methodology, which indicates a significantly higher unit value than book value. Today, our emphasis has shifted in a major way to owning and operating businesses. Many of these are worth far more than their cost-based carrying value.

As of December 31, 2015, there were 26,632,689 Steel Partners common units outstanding. Steel Partners’ total assets were $1.7 billion, and unitholders’ equity was $558 million. Per unit book value was $20.95. Steel Partners unit closing price on the NYSE at December 31, 2015 was $16.38 per unit, and management’s beneficial ownership was approximately 50.8%. Next is a sum-of-the-parts analysis.

4

|

Symbol

|

Description

|

Current Market Value

|

Per SPLP Unit

|

||||||||

|

HNH

|

HANDY & HARMAN

|

$ | 175,577,742 | $ | 6.59 | ||||||

|

SXCL

|

STEEL EXCEL INC. (a)

|

88,825,617 | 3.34 | ||||||||

| N/A |

WFH LLC (formerly CoSine Communications) (b) (d)

|

188,354,272 | 7.07 | ||||||||

|

AJRD

|

AEROJET ROCKETDYNE

|

65,474,413 | 2.46 | ||||||||

|

SLI

|

SL INDUSTRIES

|

31,715,499 | 1.19 | ||||||||

|

MLNK

|

MODUSLINK GLOBAL SOLUTIONS

|

19,939,237 | 0.75 | ||||||||

|

WEBBANK (d)

|

59,522,745 | 2.23 | |||||||||

|

OTHER INVESTMENTS (c) (d)

|

9,408,002 | 0.35 | |||||||||

|

CASH

|

7,165,084 | 0.27 | |||||||||

|

DEBT

|

(75,139,740 | ) | (2.82 | ) | |||||||

|

Total Value

|

$ | 570,842,871 | $ | 21.43 | |||||||

|

(a)

|

Includes a reduction to fair value of $15,347,536 for the fair value of SPLP units held ($8,943,000 after adjusting for SPLP’s 58.3% ownership).

|

|

(b)

|

Includes an increase to book value for intercompany loan payable to SPLP of $35,083,244, which is eliminated in consolidation ($31,824,011 after adjusting for SPLP’s ownership).

|

|

(c)

|

Includes an increase to book value for intercompany loan payable to SPLP of $9,000,000, which is eliminated in consolidation, and a reduction to book value of $50,413,742 for the fair value of SPLP units held.

|

|

(d)

|

WFH LLC and certain Other Investments are valued at Book Value at December 31, 2015.

|

|

| All values as of December 31, 2015 exclude the value of any SPLP units held. | ||

Business Updates:

Aerojet Rocketdyne Inc. (NYSE:AJRD) www.rocket.com, is a manufacturer of aerospace and defense systems, and also has a real estate business.

Our initial investment in Aerojet Rocketdyne was made on August 4, 2000.

As of March 31, 2016, Steel Partners owns approximately 6.6% of Aerojet Rocketdyne, with a market value of $65.5 million.

For the year ended November 30, 2015, Aerojet Rocketdyne Holdings, Inc. had sales of $1.7 billion compared with $1.6 billion in the prior year. The balance sheet had net debt of $441 million, and the company’s backlog was $4.1 billion as of November 30, 2015.

On June 1, 2015, Scott Seymour retired from Aerojet Rocketdyne, and Eileen Drake was named CEO. Eileen joined Aerojet Rocketdyne in March as chief operating officer, and was previously with United Technologies Corporation (UTC), where she served as president of Pratt & Whitney AeroPower's auxiliary power unit business. In her prior positions at UTC, she served as the vice president of Operations, and also vice president of Quality, Environmental, Health & Safety, and Achieving Competitive Excellence (ACE) for UTC's Carrier Corporation. Eileen is a distinguished military graduate of the U.S. Army Aviation Officer School and served on active duty for seven years as a U.S. Army aviator and airfield commander of Davison Army Airfield in Fort Belvoir, Virginia.

5

Eileen and I work very closely. This is an exciting time in the space and defense industry, and we plan to aggressively increase value of Aerojet Rocketdyne.

Handy & Harman Ltd. (NASDAQ (CM): HNH), www.handyharman.com, is a diversified manufacturer of engineered niche industrial products with leading market positions. Through its operating subsidiaries, Handy & Harman focuses on high margin products and innovative technology, and serves customers across a wide range of end markets.

Our initial investment in Handy & Harman was on February 4, 1998.

Handy & Harman manages its group of businesses on a decentralized basis, with operations principally in North America.

As of December 31, 2015, Steel Partners owned approximately 70.1% of Handy & Harman, with a market value of $175.6 million.

In July 2015, Handy & Harman acquired all the outstanding shares of JPS Industries Inc. (JPS) for $70.3 million in cash and Handy & Harman stock valued at $44.2 million, for total merger consideration of $114.5 million. JPS is a major U.S. manufacturer of mechanically formed glass and aramid substrate materials for specialty applications in a wide expanse of markets requiring highly engineered components.

For the year ended December 31, 2015, Handy & Harman reported income from continuing operations, net of tax, of $17.0 million on net sales of $649.5 million, compared with income from continuing operations, net of tax, of $15.2 million on net sales of $600.5 million in 2014.

Handy & Harman continues to carefully manage its portfolio of companies and is actively looking for strategic acquisition candidates. We are actively redeploying our pension assets and are monitoring the underfunding in today’s low discount rate environment.

ModusLink Global Solutions Inc. (NASDAQ: MLNK), www.moduslink.com, through its wholly-owned subsidiaries, ModusLink Corporation and ModusLink PTS, Inc. (together ModusLink), executes comprehensive supply chain and logistics services that are designed to improve clients’ revenue, cost, sustainability and customer experience objectives.

Our initial investment in ModusLink was made on June 13, 2012.

6

ModusLink has a July 31 year end. As of December 31, 2015, Steel Partners and Handy & Harman had a combined ownership interest of approximately 31.5% in ModusLink, with a market value of approximately $40.9 million. ModusLink has a market capitalization of $129.6 million and has federal NOLs of approximately $2.0 billion as of July 31, 2015.

For the year ended July 31, 2015, ModusLink reported net sales of $561.7 million, compared with $723.4 million for the year ended July 31, 2014. Net loss for the year ended July 31, 2015 was $18.4 million, or $0.35 per share, compared with a net loss of $16.3 million, or $0.32 per share, for the year ended July 31, 2014.

John Boucher has resigned as CEO. Jim Henderson is now the CEO of ModusLink Corporation. His strategy will be to cut costs, reduce spans and layers, and grow the top line.

ModusLink is also interested in acquiring a business with at least $25 million of EBITDA. We prefer companies with significant operations in the United States, good gross margins and returns on invested capital, sustainable competitive advantages, strong brands and excellent management.

SL Industries, Inc. (NYSE MKT: SLI), www.slindustries.com, designs, manufactures and markets power electronics, motion control, power protection, and power quality electromagnetic equipment used in a variety of medical, commercial and military aerospace, computer, datacom, industrial, and telecom applications.

Our initial investment in SL Industries was made in 1992.

As previously discussed, Handy & Harman has agreed to acquire SL Industries for $40/share in a cash transaction. As of December 31, 2015, we had an ownership interest of approximately 25.7% in SL Industries, which has a market value of $31.7 million.

For the year ended December 31, 2015, SL Industries reported net sales of $199.9 million, compared with net sales of $204.4 million for the year ended December 31, 2014. Net income for the year ended December 31, 2015 was $10.7 million, or $2.65 per diluted share, compared with net income of $18.9 million, or $4.51 per diluted share, for the year ended December 31, 2014.

Steel Excel Inc. (OTC: SXCL.PK), www.steelexcel.com, has two operating subsidiaries: Steel Energy Ltd. (Steel Energy) and Steel Sports Inc. (Steel Sports).

7

Our initial investment in Steel Excel was in 2007.

For the year ended December 31, 2015, Steel Excel reported net revenues of $132.6 million, as compared with $210.1 million in 2014. The Company incurred a loss from continuing operations before income taxes of $88.0 million in 2015, as compared with a loss of $19.5 million in 2014. The net loss for 2015 was $97.4 million, or $8.50 per diluted common share, as compared with a net loss of $23.8 million, or $2.04 per diluted common share, for 2014. The loss for 2015, included impairment charges of $25.6 million related to goodwill and intangible assets and impairment charges of $59.8 million related to marketable securities; the loss for 2014, included impairment charges of $36.7 million related to goodwill and intangible assets. At December 31, 2015, the Company had cash and marketable securities totaling $127.9 million, and an NOL of $139.1 million.

During the year, Steel Excel repurchased 231,245 shares for $4.6 million dollars at an average price of $19.95.

Steel Sports Inc. strives to provide a first-class youth sports experience emphasizing positive experiences and instilling the core values of discipline, teamwork, safety, respect, and integrity.

David Shapiro, a seasoned youth sports executive, came to us from Positive Coaching Alliance where he was the Chief Revenue Officer for the past 12 years. David was hired as the CEO of Steel Sports, and the company has made great progress under his leadership.

For more information, please visit the company’s website (www.steel-sports.com). Steel Sports currently has two operating subsidiaries, Baseball Heaven, Inc. (www.baseballheavenli.com), a premier venue for amateur and youth baseball, and UK Elite Soccer Inc., a provider of youth soccer programs and camps, and a CrossFit facility.

Steel Energy Services, Ltd. has three subsidiaries – Sun Well Service, Inc. (www.sunwellservice.com), Rogue Pressure Services, Ltd. (www.roguepressureservces.com), and Black Hawk Energy Services, Ltd. (www.blackhawkenergyservices.com) – that provide premium oil well services to exploration and production companies working in North Dakota, as well as New Mexico, Colorado, and Texas.

John Quicke, President and CEO of Steel Energy Services, retired after many years of dedicated service to Steel Partners and our affiliates. He continues to serve on the Steel Excel and Steel Energy Services boards of directors. Stewart Peterson has taken the reigns of Steel Energy, and under Stewart’s strong direction, I am confident Steel Energy Services will ride out the current industry downturn and emerge a better company.

Steel Excel also announced that they voluntarily delisted the common stock, with associated preferred stock purchase rights, from the NASDAQ Capital Market. The Company's board of directors determined, after careful consideration, that voluntarily delisting and deregistering is in the overall best interests of the Company and its stockholders. Factors that the board of directors considered include the cost savings that will occur as a result of the elimination of the Company's obligation to file reports with the SEC, the avoidance of additional accounting, audit, legal and other costs and management's attention devoted to compliance with the requirements of the Sarbanes-Oxley Act of 2002, the historically low daily trading volume in the Company's shares, and the benefit of allowing management to focus on the long-term development of our core businesses.

8

WebBank (Private), www.webbank.com, an FDIC-insured, Utah-chartered industrial bank located in Salt Lake City, is 90.7% owned by Steel Partners. The bank is engaged in a full range of banking activities, including making loans, issuing credit cards and taking federally insured deposits. It is also a leading provider of national revolving and closed end consumer and small business financing programs.

Our initial investment in WebBank was in 1996.

WebBank offers revolving and closed-end credit to consumers and small businesses nationwide, partnering with nonbank finance companies, financial technology platforms, retailers and manufacturers to offer access to WebBank's products. Revenue is largely derived from these loans, which provide fee and interest income. The bank had another successful year in 2015, growing loan volume, restructuring existing programs and adding new programs. Pretax income of $52.4 million in 2015 was a 106.3% improvement over pretax income of $25.4 million in 2014.

The bank reported net income of $31.4 million for 2015 and a return on average equity of 63.9%. The bank made $9.5 million in dividend payments to its parent in 2015. The bank’s December 31, 2015 total assets and equity capital were $327.5 million and $64.5 million, respectively.

CoSine Communications Inc. (CoSine) -

We first invested in CoSine on April 6, 2005. The first investment in API was on January 24, 1997.

As previously reported, the company acquired a controlling interest in API during 2015, and gained control of API’s operations on April 17, 2015. Net sales for the period from the acquisition date to December 31, 2015 totaled approximately $113.5 million, with operating income of $1.2 million. The company also generated cash flow from operations of $0.2 million. Included in the results are $2.2 million of non-recurring acquisition and integration costs.

9

On December 28, 2015, CoSine, merged with, and is now a subsidiary of, WebFinancial Holding Corporation.

Acquisition Criteria

Acquisitions will continue to play a major role in our growth as we continue to add value for all of our stakeholders. We are interested in acquiring companies with a minimum $25 million of EBITDA. We prefer companies with gross margins above 20%, high returns on invested capital, sustainable competitive advantages and strong brands. We like businesses participating in structural change, where the company is positioned to gain market share.

We have significant experience working through all layers of the capital structure, as well as pre-bankruptcy and bankruptcy issues. We prefer healthy companies, where the business has the characteristics stated above, but we are open minded if the balance sheet is challenged and where our balance sheet and operating system can improve the company outlook.

Economies of Scale and Shared Services

SPH Services continues to enhance the value of our companies by providing a variety of shared services, including legal, tax, accounting, human resources, analysis, treasury, lean oversight, compliance, administration, environmental, health and safety, business development, merger and acquisition services, and by providing presidents and CFOs to many of the Steel Partners operating businesses.

Through the consolidation of corporate overhead and back office functions, we continue to realize cost savings for our affiliated companies, and are able to deliver more efficient and effective services.

Steel Business System helps to increase efficiencies, eliminate waste, and improve our competitive position by using Lean Manufacturing, Design for Six Sigma, Six Sigma, Strategy Deployment and other operational efficiency initiatives. Our culture of continuous improvement is now embedded deep within our organizations, and the results show. Our competitive position and foundation for profitable growth are stronger today than ever.

10

Steel Procurement Council is composed of more than 30 members appointed by their CEOs, who continuously collaborate and continue to add value by leveraging our combined purchasing power.

In 2015, the Steel Partners Purchasing Council hosted summits in April and October. The meetings included 48 operational, strategic sourcing, and financial executives, representing 20 of our companies. The April meeting included a roundtable discussion focused on the current business environment, supply chain optimization and lean tools, setting the foundation for greater collaboration, and a formal review of Steel’s indirect spend categories. This meeting enabled the Council to discuss sourcing strategies and devise action plans to pursue and realize better terms and savings. In October, the Council invited select supply partners and affiliate executives to opine on current trends and opportunities in areas including freight, energy, MRO, office supplies, fleet management, benefits and travel. Sessions focused on not only how affiliates could both lower costs and enhance service levels, but also on developing organizational talent and process improvement.

Steel Environmental Health & Safety Council is composed of the health and safety teams at the Steel affiliate companies and representatives from the legal and human resources departments.

The Council has been conducting annual meetings for the last 10 years to foster intercompany communications on EH&S compliance issues and provides a forum for sharing best practices. In addition, the meetings are held near one of our companies which allows an opportunity to tour and showcase the facility as well as conduct a group review of site EH&S issues. Among the meeting topics and presentations at this year’s meeting were industrial accident reconstruction, electrical energy safety, property loss inspections, fall protections, site security, internal audits, agency inspections and worker compensation claim process.

Steel Partners CEO Summit was in March, and attended by approximately 60 representatives from 23 of our companies and strategic partners. Our goal was to bring the entire leadership team together to develop relationships and collaborate in areas with high impact, share best practices, and foster communication. We also focused on cost optimization strategies and capital allocation. It was a great event.

Steel Grow: Our talent management program is working well. We are retaining great people and developing an amazing bench for the future. John Quicke, President and CEO of Steel Energy Services, will retire after many years of dedicated service to Steel Partners and our affiliates. He will remain chairman of Steel Energy Services. Stewart Peterson has taken the reigns of Steel Energy, and under Stewart’s direction, I am confident Steel Energy Services will ride out the current industry downturn and emerge a better company. Handy continues to be led by Jeff Svoboda. Jeff also has oversight for API, which is now being run by Dino Kiriakopoulos, who was promoted to CEO in 2015. John McNamara continues to run WebBank as Executive Chairman. Eileen Drake is now firmly in charge of Aerojet Rocketdyne since Scott Seymour’s retirement in June. David Shapiro, a seasoned youth sports executive, is now the CEO of Steel Sports, joining us from Positive Coaching Alliance, where he was the Chief Revenue Officer for the prior 12 years. Jim Henderson has taken over as CEO of ModusLink Corporation, and under his leadership, he will focus on increasing shareholder value.

11

Proceeding into 2016, we will continue to focus on our capital allocation, our business simplification plan, and the organizational development of our people, culture and relationships in a coherent manner. We are looking to make acquisitions where we will gain a competitive advantage. We have diligently developed our culture around the Steel Business System to maximize the productivity and efficiency in all areas of our business. We are retaining great people and developing a great bench.

All of us at Steel Partners continue to be active owners who want to grow and protect our investments, and intend to have a meaningful stake in our company forever. Today, our team owns approximately 51% of Steel Partners Holding LP, so we are clearly eating our own cooking and completely aligned with our stockholders.

Thank you for your continued support and input. We look forward to a productive and prosperous future.

Respectfully,

Warren G. Lichtenstein

“Never let the fear of striking out get in your way.”

– Babe Ruth

12

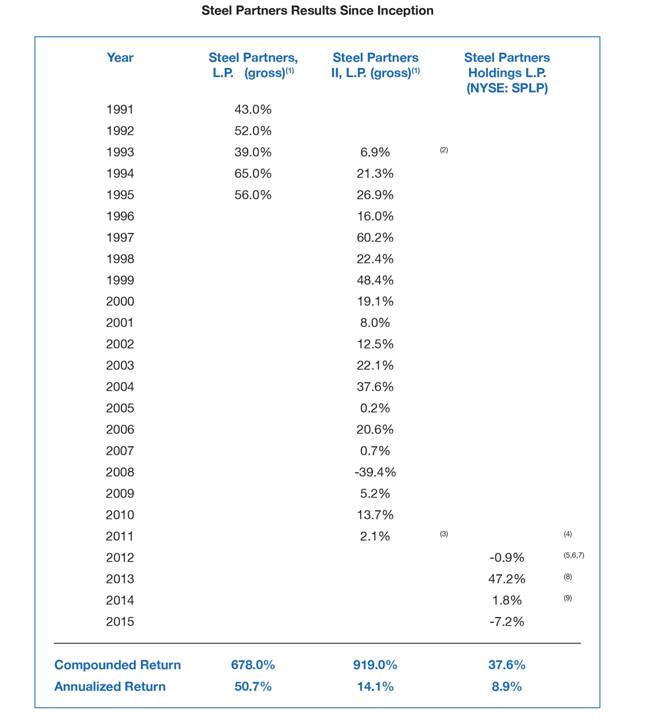

|

1.

|

Net of all fees and expenses before 20% incentive fee.

|

|

2.

|

NAV calculated from October 1, 1993, the founding date of Steel Partners II L.P.

|

|

3.

|

January 1, 2011 – April 30, 2011: NAV prepared for the full month of April 2011 though units began to trade on the OTC market on April 19, 2011.

|

|

4.

|

April 19, 2011 – December 31, 2011: The units traded on the OTC market during this period. Nearly all shares were held in book entry at American Stock Transfer, so there was little trading volume.

|

|

5.

|

January 1, 2012 – April 4, 2012: The units traded on the OTC market during this period. Nearly all shares were held in book entry at American Stock Transfer, so there was little trading volume.

|

|

6.

|

April 5, 2012 – December 31, 2014: The units were listed and began trading on the NYSE on April 5, 2012, and remain trading on the NYSE to present day.

|

|

7.

|

Unit price at 12-31-12: $11.79

|

|

8.

|

Unit price at 12-31-13: $17.35

|

|

9.

|

Unit price at 12-31-14: $17.65

|

13

Steel Partners Strategy & Philosophy - 2016

Steel Partners is in the business of finding undervalued companies, capitalizing on the inefficiencies that arise in the marketplace, and then installing time-tested disciplines to increase the value of a business over long periods of time.

We purchase securities (senior or subordinated debt, mezzanine securities and preferred and/or common stock) that we believe are selling below their intrinsic value and sell these investments when we believe prices are too high, or when we are “forced to sell” due to a buyout or merger. Value investors like Steel Partners spend their careers looking for discrepancies between market price and intrinsic value. We do not invest based on whether stocks or bonds did better in any given month, or based on which team won the Super Bowl. We are not market timers.

Steel Partners’ mission is to work with our management teams to effect catalytic events or, if required, pursue an active strategy and encourage such catalytic events. The catalytic events may include the reduction of corporate overhead, share repurchase programs, payment of special dividends, divestitures of excess or underperforming assets, acquisitions, or an outright sale of the company. In many instances, we are ready, willing and able to purchase the entire company. This is one of our competitive advantages, and, once acquired, we have the ability to improve upon capital allocation and implement our proven programs, such as Operational Excellence, Purchasing Council, Corporate Services, CEO Summits and more.

We adhere to our “blocking and tackling” style of investing in easy-to-understand businesses and situations that have built-in margins of safety. We view ourselves as business analysts, not market analysts, and we believe that with prior proper planning we will prevent poor performance. Our strategy is to remain focused on basic investment principles (which we employ to preserve and build our capital) and keep things simple. We intend to continue to focus on fundamentals, such as undervalued assets, free cash flow, and return on capital… and use common sense when making business decisions.

We have been extremely successful in identifying undervalued businesses and assets, and then figuring out how to unlock hidden values. However, identifying undervalued securities, businesses or assets is only half the battle. Value managers are constantly frustrated because value stocks generally remain cheap, unless there is a catalytic event to unlock the value. Steel Partners believes a passive approach to investing will not yield above average returns. Rather, an activist approach is required, regardless of where we invest in the capital structure. We believe the combination of investing in undervalued, neglected companies with an activist shareholder approach will, over the long-term, yield superior returns.

14

Steel Partners has no plans to alter its approach to investing or managing businesses. We believe our approach is logical and prudent. We understand risk and have no intention of investing in a concept that we don’t fully understand, have not practiced, or is out of our circle of competence. We have learned our lesson the hard way. We are owners and managers of businesses.

Our strategy continues to evolve and develop because the world is in constant transition. However, our philosophy endures.

We believe the best way to reduce the risk of losing money while enhancing our probability of making money is to combine our knowledge, experience and contacts and apply understanding to a particular situation with complete focus.

Our continued success is dependent on intangibles: Focus, Energy, Discipline, Integrity, Instinct, Desire, Persistence and Confidence. Additionally, Temperament and Perspective always matter. This is what allows us to remain level-headed, when so many others are in turmoil or euphoria. We must also continue to align ourselves with people who are self-starters and who share our values and beliefs.

Our network of investors, investment bankers, brokers, attorneys, accountants, mutual funds and hedge funds is continuing to grow and strengthen.

Our future success will be affected by our ability to remain focused and disciplined. Therefore, we seek out knowledgeable and patient investors who share our values and our long-term investment orientation. By deploying our capital with discipline, we believe we will continue to earn above-average risk-adjusted returns on our investments over a long period of time.

We have found that our approach to buying and managing businesses works on a global level. The fundamental importance we place upon our relationships with management, as well as with our fellow stakeholders, transcends borders, cultures and economies. Our approach to investing and acquiring businesses and assets has enabled us to become a global investor and manager of businesses.

At Steel Partners, we think globally and act locally. We are well-positioned to capitalize on both domestic and foreign opportunities by leveraging our expertise in various markets, both in North America and around the world. Given that many of our companies maintain leadership positions in North America, we will continue to help identify and facilitate their expansion overseas through acquisitions, joint ventures and strategic investments.

15

While searching the globe for companies and businesses is exciting, it is difficult and painstaking work. The world is a very large place with plenty of opportunity. However, the businesses in which we are looking to invest must satisfy the requirements that have always guided our approach to investing, namely, substantial current value with a margin of safety and the potential to create substantial future value.

If anyone has ideas to help grow our portfolio of businesses, we would love to hear from you.

16