Attached files

| file | filename |

|---|---|

| 8-K - 8-K - DIEBOLD NIXDORF, Inc | d173983d8k.htm |

Exhibit 99.1

Pro forma company overview

After giving pro forma effect to the Transactions, the combined company generated pro forma revenue of approximately $5,200.7 million and Pro Forma Adjusted EBITDA of approximately $453.7 million during the year ended December 31, 2015. See “—Summary historical consolidated and unaudited pro forma condensed combined financial information.”

Following completion of the Acquisition, the combined company will be named “Diebold Nixdorf” and its common shares will be publicly listed on the New York Stock Exchange and are expected to be listed on the Frankfurt Stock Exchange. The combined company will have registered offices in North Canton, Ohio and will be operated from headquarters in North Canton, Ohio and Paderborn, Germany.

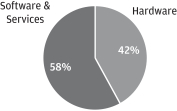

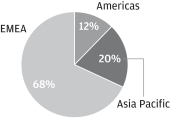

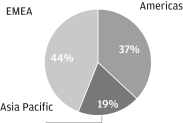

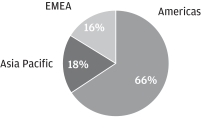

The table below provides an overview of Diebold’s and Wincor Nixdorf’s historical revenues by product and geographic regions, as well as the combined company’s revenues by product and geographic regions. In the case of Diebold, such information is based in its revenue for the year ended December 31, 2015; in the case of Wincor Nixdorf, such information is based on its revenue for the fiscal year ended September 30, 2015.

| Diebold | Wincor Nixdorf | Diebold Nixdorf(3) | ||

| Product mix(1) |

||||

|

|

|

| ||

| Diebold | Wincor Nixdorf | Diebold Nixdorf(3) | ||

| Geographic mix(1)(2) |

||||

|

|

|

| ||

| (1) | Wincor Nixdorf’s revenue by product and geographic region has been translated to U.S. dollars using the average exchange rate of €1.00 = $1.1487 for the period from October 1, 2014 to September 30, 2015. |

| (2) | The presentation of Wincor Nixdorf’s revenue by geographic region has been adjusted for purposes of this presentation to align more closely with Diebold’s presentation of revenue by geographic region. Wincor Nixdorf’s revenue for the fiscal year ended September 30, 2015 from Africa of approximately €59 million is currently reported in Asia Pacific and has been realigned to Europe, the Middle East and Africa (“EMEA”) to be consistent with Diebold’s reporting of Africa revenue. |

| (3) | The combined company’s revenue by product and geographic regions has been derived by taking Diebold’s revenue by product and geographic regions, respectively, for the year ended December 31, 2015 and adding Wincor Nixdorf’s revenue by product and geographic regions, respectively, for the fiscal year ended September 30, 2015. |

| Ranking |

As of December 31, 2015, on a pro forma basis after giving effect to the Transactions: |

| • | we would have had approximately $2,310.2 million of total indebtedness (including the notes); |

| • | of our total indebtedness, we would have had approximately $1,798.1 million of secured indebtedness, all of which would have been incurred under our Senior Credit Facility, to which the notes would have been effectively subordinated to the extent of the value of the assets securing such indebtedness; |

| • | we would have had commitments available to be borrowed under the Senior Credit Facility of $520.0 million and $79.0 million available under uncommitted lines of credit; and |

| • | our non-guarantor subsidiaries would have had approximately $1,795.2 million of total liabilities (including trade payables but excluding intercompany liabilities), all of which would have been structurally senior to the notes. |

Summary historical consolidated and unaudited pro forma condensed combined financial information

Summary historical consolidated financial information of Diebold

The following table sets forth our summary historical consolidated and unaudited pro forma condensed combined financial information for the periods ended and as of the dates indicated below.

The summary historical consolidated financial information as of December 31, 2015 and 2014 and for each of the years ended December 31, 2015, 2014 and 2013 have been prepared in accordance with GAAP. The balance sheet information as of December 31, 2015 and 2014 and the statement of operations and cash flow information for the years ended December 31, 2015, 2014 and 2013 have been derived from the audited consolidated financial statements of Diebold.

The summary unaudited pro forma condensed combined financial information as of December 31, 2015 and for the year ended December 31, 2015 have been derived from and should be read in conjunction with the more detailed unaudited pro forma condensed combined financial information and the accompanying notes thereto appearing elsewhere in this Current Report on Form 8-K. The summary unaudited pro forma condensed combined balance sheet as of December 31, 2015 combines the consolidated balance sheets of Diebold and Wincor Nixdorf as of December 31, 2015 and September 30, 2015, respectively, and gives effect to the proposed Acquisition as if it occurred on December 31, 2015. The unaudited pro forma condensed combined statement of operations combines the historical results of Diebold and Wincor Nixdorf for the years ended December 31, 2015 and September 30, 2015, respectively, and gives effect to the proposed Acquisition as if it occurred on January 1, 2015. For purposes of the unaudited pro forma condensed combined financial information presented below, the historical financial statements of Diebold and Wincor Nixdorf have been adjusted to give pro forma effect to events that are (i) directly attributable to the proposed Acquisition, (ii) factually supportable, and (iii) with respect to the combined statements of operations, expected to have a continuing impact on the combined company’s consolidated results. The unaudited pro forma condensed combined statement of operations does not include the impact of either (i) any revenue, cost or other operating synergies that may result from the Acquisition or any related restructuring costs or (ii) one-time charges or costs arising from the Acquisition, such as incremental advisory, legal and accounting expenses. The unaudited pro forma condensed combined financial information reflects adjustments to reconcile Wincor Nixdorf’s historical audited financial statements prepared in accordance with IFRS to GAAP and conversion from Euros to U.S. dollars.

The summary unaudited pro forma condensed combined financial information is for illustrative purposes only and does not purport to present what our results of operations and financial condition would have been had the Acquisition actually occurred on the dates assumed for such purposes in the preparation of such pro forma financial information, nor does it project our results of operations for any future period or our financial condition at any future date. The unaudited pro forma condensed combined financial information is based upon currently available information and estimates and assumptions that Diebold believes are reasonable as of the date hereof. Any of the factors underlying these estimates and assumptions may change or prove to be materially different, and the estimates and assumptions may not be representative of facts existing at the consummation of the Acquisition.

The information set forth below should be read in conjunction with “Use of proceeds,” “Capitalization” and “Unaudited pro forma condensed combined financial information.”

| Historical | Pro Forma | |||||||||||||||

| Year ended December 31, | Year ended December 31, 2015 |

|||||||||||||||

| (dollars in millions) | 2015 | 2014 | 2013 | |||||||||||||

| Consolidated statement of operations: |

||||||||||||||||

| Net sales: |

||||||||||||||||

| Services |

$ | 1,394.2 | $ | 1,432.8 | $ | 1,420.8 | $ | 2,824.8 | ||||||||

| Products |

1,025.1 | 1,302.0 | 1,161.9 | 2,375.9 | ||||||||||||

|

|

|

|||||||||||||||

| Total net sales |

2,419.3 | 2,734.8 | 2,582.7 | 5,200.7 | ||||||||||||

| Cost of sales: |

||||||||||||||||

| Services |

932.8 | 974.8 | 1,048.3 | 2,144.2 | ||||||||||||

| Products |

834.5 | 1,033.8 | 948.4 | 1,965.6 | ||||||||||||

|

|

|

|||||||||||||||

| Total cost of sales |

1,767.3 | 2,008.6 | 1,996.7 | 4,109.8 | ||||||||||||

|

|

|

|||||||||||||||

| Gross profit |

652.0 | 726.2 | 586.0 | 1,090.9 | ||||||||||||

| Operating expenses: |

||||||||||||||||

| Selling, general and administrative |

488.2 | 478.4 | 564.5 | 923.1 | ||||||||||||

| Research, development and engineering expense |

86.9 | 93.6 | 92.2 | 193.5 | ||||||||||||

| Impairment of assets(1) |

18.9 | 2.1 | 72.0 | 18.9 | ||||||||||||

| Gain on sale of assets, net(2) |

(0.6 | ) | (12.9 | ) | (2.4 | ) | (0.6 | ) | ||||||||

|

|

|

|||||||||||||||

| Total operating expenses |

593.4 | 561.2 | 726.3 | 1,134.9 | ||||||||||||

|

|

|

|||||||||||||||

| Operating income (loss) |

58.6 | 165.0 | (140.3 | ) | (44.0 | ) | ||||||||||

| Other income (expense): |

||||||||||||||||

| Investment income |

26.0 | 34.5 | 27.6 | 24.0 | ||||||||||||

| Interest expense |

(32.5 | ) | (31.4 | ) | (29.2 | ) | (144.2 | ) | ||||||||

| Foreign exchange (loss) gain, net |

(10.0 | ) | (11.8 | ) | 0.2 | (10.0 | ) | |||||||||

| Miscellaneous, net |

3.7 | (1.6 | ) | (0.1 | ) | (3.3 | ) | |||||||||

|

|

|

|||||||||||||||

| Total other expense, net |

(12.8 | ) | (10.3 | ) | (1.5 | ) | (133.5 | ) | ||||||||

|

|

|

|||||||||||||||

| Income (loss) from continuing operations before taxes |

45.8 | 154.7 | (141.8 | ) | (177.5 | ) | ||||||||||

| Income tax (benefit) expense |

(13.7 | ) | 47.4 | 48.4 | (73.4 | ) | ||||||||||

|

|

|

|||||||||||||||

| Income from continuing operations, net of tax |

59.5 | 107.3 | (190.2 | ) | (104.1 | ) | ||||||||||

| Income from discontinued operations, net of tax(3) |

15.9 | 9.7 | 13.7 | — | ||||||||||||

|

|

|

|||||||||||||||

| Net income (loss) |

75.4 | 117.0 | (176.5 | ) | (104.1 | ) | ||||||||||

| Less: Income attributable to non-controlling interests, net of tax(4) |

1.7 | 2.6 | 5.1 | 3.2 | ||||||||||||

|

|

|

|||||||||||||||

| Net income (loss) attributable to Diebold, Incorporated |

$ | 73.7 | $ | 114.4 | $ | (181.6 | ) | $ | (107.3 | ) | ||||||

|

|

|

|||||||||||||||

| Balance sheet information (at period end)(5): |

||||||||||||||||

| Cash and cash equivalents |

$ | 313.6 | $ | 326.1 | $ | 453.1 | ||||||||||

| Net working capital(6) |

$ | 687.8 | $ | 627.7 | $ | 1,105.7 | ||||||||||

| Property, plant and equipment, net |

$ | 175.3 | $ | 165.7 | $ | 311.2 | ||||||||||

| Total assets |

$ | 2,249.3 | $ | 2,342.1 | $ | 5,510.4 | ||||||||||

| Total debt |

$ | 645.1 | $ | 505.4 | $ | 2,310.2 | ||||||||||

| Total Diebold, Incorporated stockholders’ equity |

$ | 412.4 | $ | 531.5 | $ | 742.6 | ||||||||||

| Cash flow information: |

||||||||||||||||

| Net cash provided by (used in): |

||||||||||||||||

| Operating activities |

$ | 36.7 | $ | 186.9 | $ | 124.2 | ||||||||||

| Investing activities |

$ | (64.9 | ) | $ | 13.8 | $ | (52.7 | ) | ||||||||

| Financing activities |

$ | 42.2 | $ | (81.2 | ) | $ | (204.5 | ) | ||||||||

| Capital expenditures from continuing operations |

$ | (52.3 | ) | $ | (60.1 | ) | $ | (33.8 | ) | |||||||

| Non-GAAP financial information: |

||||||||||||||||

| EBITDA(7) |

$ | 144.0 | $ | 262.1 | $ | (25.1 | ) | $ | 164.9 | |||||||

| Adjusted EBITDA(7) |

$ | 229.4 | $ | 294.7 | $ | 232.5 | $ | 400.7 | ||||||||

| Pro Forma Adjusted EBITDA(7) |

$ | 453.7 | ||||||||||||||

| Interest expense(8) |

$ | 144.2 | ||||||||||||||

| Ratio of total debt to Pro Forma Adjusted EBITDA(7)(9) |

5.1x | |||||||||||||||

| Ratio of secured debt to Pro Forma Adjusted EBITDA(7)(10) |

4.0x | |||||||||||||||

| Ratio of Pro Forma Adjusted EBITDA to interest expense(7)(8)(11) |

3.1x | |||||||||||||||

|

|

||||||||||||||||

| (1) | As of March 31, 2015, the Company agreed to sell its equity interest in its Venezuela joint venture to its joint venture partner and recorded a $10.3 million impairment of assets in the first quarter of 2015. On April 29, 2015, the Company closed the sale for the estimated fair market value and recorded a $1.0 million reversal of impairment of assets based on final adjustments in the second quarter of 2015, resulting in a $9.3 million impairment of assets. Final fair value adjustments resulted in an overall impairment of $9.7 million. The Company no longer has a consolidating entity in Venezuela, but will continue to operate in Venezuela on an indirect basis. Additionally, the Company recorded an impairment related to other intangibles in Latin America in the second quarter of 2015 and an impairment of $9.1 million related to redundant legacy Diebold internally-developed software as a result of the acquisition of Phoenix Interactive Design, Inc. in the first quarter of 2015 in which the carrying amounts of the assets were not recoverable. The Company performed an other-than-annual assessment for its Brazil reporting unit in the third quarter of 2013 based on a two-step impairment test and concluded that the goodwill within the Brazil reporting unit was partially impaired. For 2013, the impairment primarily related to a $70.0 million pre-tax, non-cash goodwill impairment charge recorded in the third quarter due to deteriorating macro-economic outlook, structural changes to an auction-based purchasing environment and new competitors entering the market. |

| (2) | During the second quarter of 2014, the Company divested its Eras subsidiary, resulting in a gain on sale of assets of $13.7 million. During the first quarter of 2013, the Company recognized a gain on assets of $2.2 million resulting from the sale of certain U.S. manufacturing operations to a long-time supplier. |

| (3) | The Company executed a definitive asset purchase agreement with a wholly owned subsidiary of Securitas AB to divest its electronic security business located in the U.S. and Canada for an aggregate purchase price of approximately $350.0 million in cash. The transaction closed on February 1, 2016. The operating results for the electronic security business were previously included in the Company’s North America segment and have been reclassified to discontinued operations for all of the periods presented. |

| (4) | The pro-forma income attributable to non-controlling interest, net of tax, combines the historical results of Diebold and Wincor Nixdorf for the years ended December 31, 2015 and September 30, 2015, of $1.7 million and $1.5 million, respectively. The Wincor Nixdorf profit attributable to non-controlling interests of €1.3 million was translated at the historical average rate of $1.1487 per euro. Diebold’s non-controlling interest relates primarily to China and Central America. Wincor Nixdorf’s non-controlling interest relates to the remaining ownership interests in Prosystems IT GmbH. |

| (5) | The Company recast its financial statements for its divestiture of the electronic security business for its Annual Report on Form 10-K for the year ended December 31, 2015. Pursuant to GAAP, we recast our balance sheet accounts as of December 31, 2015 and 2014. As a result, audited December 31, 2013 balance sheet information is not available for the recast electronic security business. |

| (6) | We define “Net working capital” as current assets minus current liabilities. |

| (7) | We define “EBITDA” is defined as income (loss) from continuing operations before taxes, interest expense, depreciation and amortization expense less income attributable to noncontrolling interests, net of tax. We define “Adjusted EBITDA” as EBITDA before the effect of the following items: stock-based compensation, gain on sale of assets, net, restructuring expense, impairment of assets, Venezuela devaluation, legal indemnification and professional fees, acquisition/divestiture fees, acquisition related hedging, purchase accounting write-up of inventory, Brazil indirect taxes, legal settlements, executive severance and special pension charges. “Pro Forma Adjusted EBITDA” is defined as Adjusted EBITDA after cost savings. These are non-GAAP financial measurements used by management to enhance the understanding of our operating results. EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA are key measures we use to evaluate our operational performance. We provide EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA because we believe that investors and securities analysts will find EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA to be useful measures for evaluating our operating performance and comparing our operating performance with that of similar companies that have different capital structures and for evaluating our ability to meet our future debt service, capital expenditures, and working capital requirements. However, EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA should not be considered as alternatives to net income as a measure of operating results or as alternatives to cash flows from operating activities as a measure of liquidity in accordance with GAAP. In addition, the indenture that will govern the notes offered hereby and the credit agreement governing the Senior Credit Facility will contain debt incurrence ratios that are calculated by reference to measures similar, but not identical, to Pro Forma Adjusted EBITDA. Non-compliance with these debt incurrence ratios would prohibit the Company from being able to incur additional indebtedness other than pursuant to specified exceptions. |

EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA and the related ratios are not calculated or presented in accordance with GAAP, and other companies in our industry may calculate EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA differently than we do, limiting their usefulness as comparative measures. As a result, these financial measures have limitations as analytical and comparative tools, and you should not consider these items in isolation, or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

| • | they do not reflect all of our cash expenditures or future requirements for capital expenditures or contractual commitments; |

| • | they do not reflect certain impairments and adjustments for purchase accounting; |

| • | they do not reflect changes in, or cash requirements for, working capital needs; |

| • | they do not reflect the significant interest expense or the cash requirements necessary to service interest or principal payments on debt; |

| • | they do not reflect income tax expense or the cash requirements to pay taxes; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA do not reflect any cash requirements for such replacements; and |

| • | Pro Forma Adjusted EBITDA reflects adjustments for synergies expected to be achieved by the first full fiscal year following the Acquisition, which synergies may not be realized in such time period or at all, and which may cost more to achieve than we anticipated. |

EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA should not be considered as measures of discretionary cash available to us to invest in the growth of our business. In calculating these financial measures, we make certain adjustments that are based on assumptions and estimates that may prove to have been inaccurate. In addition, in evaluating these financial measures, you should be aware that in the future we may incur expenses similar to those eliminated in this presentation. Our presentation of EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items.

Because the ratios of total debt to Pro Forma Adjusted EBITDA, secured debt to Pro Forma Adjusted EBITDA and Pro Forma Adjusted EBITDA to interest expense are based in part on Pro Forma Adjusted EBITDA, these measures are similarly impacted by the limitations referenced above and should not be considered in isolation or as substitutes for GAAP measures.

The following table provides a reconciliation of EBITDA, Adjusted EBITDA and Pro Forma Adjusted EBITDA to our GAAP net income (loss):

| Historical | Pro Forma | |||||||||||||||

| (in millions) | Year ended December 31, 2015 |

Year ended December 31, 2014 |

Year ended December 31, 2013 |

Year ended December 31, 2015 |

||||||||||||

| Income (loss) from continuing operations before taxes |

$ | 45.8 | $ | 154.7 | $ | (141.8 | ) | $ | (177.5 | ) | ||||||

| Interest expense |

32.5 | 31.4 | 29.2 | 144.2 | ||||||||||||

| Depreciation and amortization expense(a) |

64.0 | 73.4 | 82.4 | 201.4 | ||||||||||||

| (Less): Income attributable to noncontrolling interests, net of tax |

(1.7 | ) | (2.6 | ) | (5.1 | ) | (3.2 | ) | ||||||||

|

|

|

|||||||||||||||

| EBITDA |

140.6 | 256.9 | (35.3 | ) | 164.9 | |||||||||||

| Stock-based compensation(b) |

12.4 | 21.5 | 15.4 | 18.3 | ||||||||||||

| Gain on sale of assets |

(0.6 | ) | (12.9 | ) | (2.4 | ) | (0.6 | ) | ||||||||

| Restructuring expense(c) |

21.2 | 11.6 | 53.2 | 113.1 | ||||||||||||

| Impairment of assets |

18.9 | 2.1 | 72.0 | 18.9 | ||||||||||||

| Venezuela devaluation(d) |

7.5 | 12.1 | 1.6 | 7.5 | ||||||||||||

| Legal, indemnification and professional fees(e) |

14.7 | 9.2 | 5.1 | 14.7 | ||||||||||||

| Acquisition/divestiture fees(f) |

21.1 | — | — | 21.1 | ||||||||||||

| Acquisition related hedging(g) |

(7.0 | ) | — | — | (7.0 | ) | ||||||||||

| Purchase accounting adjustment(h) |

— | — | — | 49.2 | ||||||||||||

| Brazil indirect tax(i) |

0.2 | (5.8 | ) | 0.8 | 0.2 | |||||||||||

| Legal settlements(j) |

— | — | 45.2 | — | ||||||||||||

| Executive severance |

— | — | 9.3 | — | ||||||||||||

| Special pension charges(k) |

— | — | 67.6 | — | ||||||||||||

| Other |

0.4 | — | — | 0.4 | ||||||||||||

|

|

|

|||||||||||||||

| Adjusted EBITDA |

$ | 229.4 | $ | 294.7 | $ | 232.5 | 400.7 | |||||||||

| Cost savings(l) |

53.0 | |||||||||||||||

|

|

|

|||||||||||||||

| Pro Forma Adjusted EBITDA |

$ | 453.7 | ||||||||||||||

|

|

||||||||||||||||

| (a) | The pro forma depreciation and amortization expense is calculated as: |

| (in millions) | Year ended December 31, 2015 |

|||||||

| Wincor consolidated depreciation expense (USD translated at the historical average rate of $1.1487 per euro) |

€ | 43.0 | $ | 49.4 | ||||

| Diebold consolidated depreciation and amortization expense |

$ | 64.0 | ||||||

| Incremental pro forma amortization expense(m) |

$ | 88.0 | ||||||

|

|

|

|||||||

| Total pro forma depreciation and amortization expense |

$ | 201.4 | ||||||

|

|

||||||||

| (b) | The pro forma stock compensation information for the year ended December 31, 2015 includes $12.4 million relating to the Diebold stock compensation plan and $5.9 million or (€5.1 million translated at the historical average rate of $1.1487 per euro) relating to the Wincor Nixdorf plan. |

| (c) | Restructuring expenses for Diebold relate to the multi-year realignment focused on globalizing the Company’s global service organization and creating a unified center-led global organization for research and development, as well as transforming the Company’s general and administrative cost structure. The pro forma information for the year ended December 31, 2015 includes $21.2 million relating to the Diebold restructuring plan and $91.9 million or (€80.0 million translated at the historical average rate of $1.1487 per euro) related to the Wincor Nixdorf restructuring plan. Wincor Nixdorf launched realignment and restructuring steps under its Delta Program aimed at evolving Wincor Nixdorf into a software and IT services company and improving Wincor Nixdorf’s margins and profitability in the second half of fiscal 2015. |

| (d) | The Company’s Venezuelan operations consisted of a fifty-percent owned subsidiary, which was consolidated. Venezuela financial results were measured using the U.S. dollar as its functional currency because its economy is considered highly inflationary. On February 10, 2015, the Venezuela government introduced a new foreign currency exchange platform called the Marginal Currency System, or SIMADI, which replaced the SICAD 2 mechanism, yielding another significant increase in the exchange rate. As of March 31, 2015, management determined it was unlikely that the Company would be able to convert bolivars under a currency exchange other than SIMADI and remeasured its Venezuela balance sheet using the SIMADI rate of 192.95 compared to the previous SICAD 2 rate of 50.86, which resulted in a loss of $7.5 recorded within foreign exchange (loss) gain, net in the consolidated statements of operations in the first quarter of 2015. On March 24, 2014, the Venezuelan government announced a currency exchange mechanism, SICAD 2, which yielded an exchange rate significantly higher than the rates established through the other regulated exchange mechanisms. Management determined that it was unlikely that the Company would be able to convert bolivars under a currency exchange other than SICAD 2. On March 31, 2014, the Company remeasured its Venezuelan balance sheet using the SICAD 2 rate of 50.86 compared to the previous official government rate of 6.30, resulting in a decrease of $6.1 million to the Company’s cash balance and net losses of $12.1 million that were recorded within foreign exchange (loss) gain, net in the consolidated statements of operations in the first quarter of 2014. |

| (e) | Legal, indemnification and professional fees primarily relate to corporate monitor efforts. The corporate monitor was assigned by the SEC and Department of Justice (“DOJ”) in connection with the remediation for Foreign Corrupt Practices Act of 1977 (“FCPA”) matters. |

| (f) | Acquisition/divestiture fees reflect acquisition and divestiture related costs of $21.1 million included within selling and administrative expense relating to the potential Acquisition and Inspur joint venture and the completed divestiture of our North America electronic security business. |

| (g) | On November 23, 2015, the Company entered into foreign exchange option contracts to purchase to hedge against the effect of exchange rate fluctuations on the euro denominated cash consideration related to the Acquisition and estimated euro denominated deal related costs and any outstanding Wincor Nixdorf borrowings. In 2015, the $7.0 million gain on these non-designated derivative instruments is reflected in other income (expense) miscellaneous, net. |

| (h) | The inventory adjustment reflects an increase in book value of $49.2 million to reflect the estimated fair value of inventory, estimates of selling price, less cost to sell that resulted in a corresponding increase in cost of sales in the unaudited pro forma condensed combined statement of operations. The fair value estimate of inventory is preliminary and is determined based on the assumptions that market participants would use in pricing an asset, based on the most advantageous market for the asset (i.e., its highest and best use). This preliminary fair value estimate could include assets that are not intended to be used, may be sold or are intended to be used in a manner other than their best use. For purposes of the accompanying unaudited pro forma condensed combined financial information, it is assumed that all assets will be used in a manner that represents its highest and best use. The final fair value determination for inventories may differ from this preliminary determination and any such difference could be material. |

| (i) | In August 2012, one of the Company’s Brazil subsidiaries was notified of a tax assessment of approximately R$270.0 million, including penalties and interest, regarding certain Brazil federal indirect taxes (Industrialized Products Tax, Import Tax, Programa de Integração Social and Contribution to Social Security Financing) for 2008 and 2009. The assessment alleges improper importation of certain components into Brazil’s free trade zone that would nullify certain indirect tax incentives. On September 10, 2012, the Company filed its administrative defenses with the tax authorities. This proceeding is currently pending an administrative level decision, which could negatively impact Brazil federal indirect taxes in other years that remain open under statute. It is reasonably possible that the Company could be required to pay taxes, penalties and interest related to this matter, which could be material to the Company’s consolidated financial statements. |

| In response to an order by the administrative court, the tax inspector provided further analysis with respect to the initial assessment in December 2013, which has now been accepted by the initial administrative court, that indicates a potential exposure that is significantly lower than the initial tax assessment received in August 2012. This revised analysis has been accepted by the initial administrative court; however, this matter remains subject to ongoing administrative proceedings and appeals. Accordingly, the Company cannot provide any assurance that its exposure pursuant to the initial assessment will be lowered significantly or at all. In addition, this matter could negatively impact Brazil federal indirect taxes in other years that remain open under statute. It is reasonably possible that the Company could be required to pay taxes, penalties and interest related to this matter, which could be material to the Company’s consolidated financial statements. The Company continues to defend itself in this matter. The calculated adjustment for the Brazil indirect tax matter relates to the additional interest and penalties accrued as well as the removal of certain accruals relates to the passage of the statute of limitations in connection with the above matter. |

| (j) | Legal settlement consists of $28.0 million related to the settlement of the FCPA investigation and $17.2 million related to the settlement of our securities class action in 2013. These charges were included within selling and administrative expense. |

| (k) | In connection with our voluntary early retirement program in the fourth quarter of 2013, we recorded a non-cash pension charge of $67.6 million recognized in selling and administrative expense within the Company’s statement of operations. The non-cash pension charge included $8.7 million curtailment loss, $20.2 million settlement loss and $38.7 million in special termination benefits. |

| (l) | Cost savings reflect the first year of total savings related to the synergies identified and include the consolidation of purchasing, standardization of components, optimization of resources, consolidation of manufacturing facilities, rationalization of service delivery and sales management and regional and corporate synergies. We expect to fully realize $160.0 million of cost savings by the third full year following the Acquisition date and currently anticipate it will cost approximately $160.0 million to achieve this level of cost savings, although (i) there can be no assurance that such cost savings will be achieved, (ii) it may take longer than anticipated to achieve such cost savings and (iii) it may require additional costs to complete our cost savings program. |

| (m) | See footnote 8(m) of “Unaudited pro forma condensed combined financial information—unaudited pro forma condensed combined statement of operations adjustments.” |

| (8) | Pro forma interest expense represents the annual GAAP treatment of interest expense on our total debt for the year ended December 31, 2015, after giving effect to the Acquisition and assuming the borrowings under the Senior Credit Facility and the notes were outstanding as of January 1, 2015. For purposes of calculating pro forma interest expense, we have used an assumed weighted average interest rate on the Senior Credit Facility and the notes offered hereby. See “Unaudited pro forma condensed combined financial information.” |

| (9) | The ratio of total debt to Pro Forma Adjusted EBITDA is determined by dividing total debt by Pro Forma Adjusted EBITDA. |

| (10) | The ratio of total secured debt to Pro Forma Adjusted EBITDA is determined by dividing total secured debt by Pro Forma Adjusted EBITDA. As of December 31, 2015, after giving effect to the Acquisition, the aggregate amount of our secured indebtedness would have been approximately $1,798.1 million, consisting of borrowings under our Senior Credit Facility. |

| (11) | The ratio of Pro Forma Adjusted EBITDA to interest expense is determined by dividing Pro Forma Adjusted EBITDA by interest expense. |

The following table summarizes our estimated sources and uses of funds in connection with the Transactions, assuming that the Transactions had occurred on December 31, 2015. The actual amounts are subject to adjustment and may be different at the time of the consummation of the Transactions depending on several factors, including the number of Wincor Nixdorf ordinary shares tendered pursuant to Diebold’s voluntary public takeover offer for all ordinary shares of Wincor Nixdorf (the “Offer”) and differences in the estimation of fees and expenses. The table below assumes that all of the Wincor Nixdorf shareholders tender their ordinary shares in the Offer or receive consideration equivalent to the Offer consideration.

You should read the following table together with the information included under “Unaudited pro forma condensed combined financial information” and the related notes included elsewhere in this Current Report on Form 8-K.

| Sources of funds | (in millions) | Use of funds | (in millions) | |||||||

| Cash proceeds from sale of North America electronic security business |

$ | 291.0 | Total consideration paid to Wincor Nixdorf shareholders(3) |

$ | 1,650.7 | |||||

| Term Loan A Facility |

230.0 | Repayment of Wincor Nixdorf debt |

150.9 | |||||||

| Delayed Draw Term Loan A Facility |

250.0 | Repayment of Diebold debt(4) |

633.0 | |||||||

| Term Loan B Facility—$(1) |

1,100.0 | Excess cash to balance sheet(5) |

331.4 | |||||||

| Term Loan B

Facility—€ |

223.9 | |||||||||

| Notes offered |

500.0 | Hedging costs and other settlements(6) |

33.2 | |||||||

| Common shares issued to Wincor Nixdorf shareholders(2) |

349.6 | Fees and expenses(7) |

145.3 | |||||||

|

|

|

|

|

|||||||

| Total sources |

$ | 2,944.5 | Total uses |

$ | 2,944.5 | |||||

|

|

||||||||||

| (1) | Represents expected funding of the Term Loan B Facility. |

| (2) | Represents an aggregate of $12.9 million of new common shares of Diebold (valued at $27.02 per share, the closing price of a Diebold common share on the NYSE on March 23, 2016). |

| (3) | Represents the total consideration of approximately $1,650.7 million, comprised of $1,301.1 million in cash and an aggregate of $349.6 million of new common shares of Diebold (valued at $27.02 per share). See the qualifications and assumptions in the preceding paragraphs. |

| (4) | Includes the repayment of the entire $175.0 million aggregate principal amount of Diebold’s outstanding 5.50% Senior Notes due 2016 in March 2016 and the expected prepayment of all $50.0 million of Diebold’s outstanding 5.55% Senior Notes due 2018 prior to, or in connection with, the consummation of the Acquisition. The payment of a $5.6 million of make-whole premium related to the 5.55% Senior Notes due 2018 is included in fees and expenses. See “Capitalization.” |

| (5) | Represents the excess of cash provided by borrowings under the Senior Credit Facility over the cash required to consummate the Transactions and pay all related costs, fees and expenses. The excess cash to the balance sheet is also intended to fund integration costs and seasonal cash needs. |

| (6) | Represents $21.9 million of net hedging costs incurred in connection with the Acquisition and various other Wincor Nixdorf settlements incurred as a result of the change in control. |

| (7) | Represents our estimate of fees, expenses and other costs payable by us in connection with the Transactions, including the initial purchasers’ discount, financing fees, premiums and prepayment penalties, bridge loan commitment fees, advisory fees and other transaction costs and professional fees. |

The following table sets forth our consolidated cash and cash equivalents and capitalization as of December 31, 2015:

| • | on an actual basis; and |

| • | on an unaudited pro forma basis, which is derived from the unaudited pro forma condensed combined financial information. |

The following table should be read in conjunction with “Use of proceeds” and “Unaudited pro forma condensed combined financial information” and the related notes thereto.

| As of December 31, 2015 | ||||||||

| Actual | Unaudited pro forma |

|||||||

| (in millions) | ||||||||

| Cash and cash equivalents(1) |

$ | 313.6 | $ | 453.1 | ||||

|

|

|

|

|

|||||

| Debt |

||||||||

| Senior Credit Facility: |

||||||||

| Term Loan A Facility |

$ | 230.0 | $ | 230.0 | ||||

| Delayed Draw Term Loan A Facility |

— | 250.0 | ||||||

| Term Loan B Facility(2) |

— | 1,318.1 | ||||||

| Revolving Facility(3) |

168.0 | — | ||||||

| Existing senior notes(4) |

225.0 | — | ||||||

| Notes offered |

— | 500.0 | ||||||

| Other debt(5) |

22.1 | 12.1 | ||||||

|

|

|

|||||||

| Total debt |

645.1 | 2,310.2 | ||||||

|

|

|

|||||||

| Total Diebold, Incorporated shareholders’ equity(6) |

412.4 | 742.6 | ||||||

|

|

|

|||||||

| Total capitalization |

$ | 1,057.5 | $ | 3,052.8 | ||||

|

|

||||||||

| (1) | Excludes net proceeds of $291.0 million from the sale of the North America electronic security business, which was completed in the first quarter of 2016. Additionally, the source and use table is based on the Wincor Nixdorf December 31, 2015 debt whereas the capitalization table is based on the September 30, 2015 pro forma amounts. |

| (2) | Represents borrowings of the full amounts available under the Term Loan B Facility, calculated using the exchange rate of €1.00 = $1.0906 at December 31, 2015 for the anticipated €200.0 million tranche thereof. |

| (3) | The Revolving Facility will provide for borrowing capacity of up to $520.0 million. As of December 31, 2015, on a pro forma basis after giving effect to the Transactions, we would have had availability of $520.0 million under the Revolving Facility. |

| (4) | Comprised of $175.0 million aggregate principal amount of Diebold’s 5.50% Senior Notes due 2016 and $50.0 million aggregate principal amount of Diebold’s 5.55% Senior Notes due 2018. In March 2016, Diebold repaid all $175.0 million aggregate principal amount of its outstanding 5.50% Senior Notes due 2016 at maturity with cash on hand. Diebold expects to prepay the entire $50.0 million aggregate principal amount of its outstanding 5.55% Senior Notes due 2018 prior to, or in connection with, the consummation of the Acquisition. |

| (5) | Primarily relates to debt outstanding under uncommitted lines of credit at foreign subsidiaries and other debt following the completion of the Acquisition. As of December 31, 2015, on a pro forma basis after giving effect to the Transactions, we would have had $79.0 million available under such uncommitted lines of credit. |

| (6) | The pro forma total Diebold, Incorporated shareholders’ equity reflects adjustments of $16.2 million and $333.4 million to common shares and additional paid-in capital, respectively, to reflect the issuance of 12,940,236 shares of Diebold common shares with a par value of $1.25 per share to satisfy the equity portion of the Offer consideration pursuant to the Offer, assuming a closing price of Diebold’s common shares on the NYSE on March 23, 2016 of $27.02 per share. In addition, an adjustment of $12.4 million to retained earnings reflects the removal of historical Diebold deferred financing cost of $6.8 million and the payment of the make-whole premium of $5.6 million related to the 5.55% Senior Notes due 2018 and the fair value adjustment of $7.0 million related to the foreign currency exchange option contracts that were entered into in connection with the financing of the Acquisition, which is expected to not have a recurring impact. Pro forma Diebold, Incorporated shareholders’ equity does not reflect non-recurring costs relating to the Transactions, nor the significant charges we will incur in connection with the integration of Diebold and Wincor Nixdorf. |

Unaudited pro forma condensed combined financial information

On November 23, 2015, Diebold entered into the Acquisition with Wincor Nixdorf. Pursuant to the Acquisition Agreement, the Company has made a voluntary public takeover offer for 100 percent of the outstanding ordinary shares of Wincor Nixdorf (the “offer”) in exchange for €38.98 in cash and 0.434 new common shares of Diebold per Wincor Nixdorf ordinary share. Diebold will issue common shares in connection with the offer up to 19.91 percent of its total outstanding common shares at the time of entry in the Acquisition Agreement and at the time of issuance. The Acquisition provides that, upon the terms and subject to the conditions set forth therein, Diebold and Wincor Nixdorf intend to consummate the Acquisition.

The following unaudited pro forma condensed combined financial information is presented to illustrate the estimated effects of the proposed Acquisition of Wincor Nixdorf by Diebold and certain other adjustments listed below (the “Acquisition Adjustments”) through the offer. The following unaudited pro forma condensed combined financial information is derived from and should be read in conjunction with the historical consolidated financial statements and related notes of Diebold and the consolidated financial statements of Wincor Nixdorf.

The unaudited pro forma condensed combined balance sheet as of December 31, 2015, and the unaudited pro forma condensed combined statement of operations for the twelve months ended December 31, 2015, are presented herein. The unaudited pro forma condensed combined balance sheet combines the unaudited consolidated balance sheets of Diebold and Wincor Nixdorf as of December 31, 2015 and September 30, 2015, respectively, and gives effect to the proposed Acquisition as if it occurred on December 31, 2015. The unaudited pro forma condensed combined statement of operations combines the historical results of Diebold and Wincor Nixdorf for the years ended December 31, 2015 and September 30, 2015, respectively, and gives effect to the proposed Acquisition as if it occurred on January 1, 2015. The historical financial information has been adjusted to give effect to pro forma adjustments that are (i) directly attributable to the proposed Acquisition, (ii) factually supportable, and (iii) with respect to the unaudited condensed combined statements of operations, expected to have a continuing impact on the combined entity’s consolidated results.

The proposed Acquisition of Wincor Nixdorf by Diebold will be accounted for using the acquisition method of accounting under the provisions of Accounting Standards Codification 805, “Business Combinations” (“ASC 805”), with Diebold representing the accounting acquirer under this guidance. The following unaudited pro forma condensed combined financial information primarily gives effect to the Acquisition Adjustments, which include:

| • | Adjustments to reconcile Wincor Nixdorf’s historical audited financial statements prepared in accordance with IFRS to GAAP and conversion from euros to U.S. dollars; |

| • | Application of the acquisition method of accounting in connection with the Acquisition to reflect aggregate offer consideration of $1.7 billion, assuming all outstanding Wincor Nixdorf ordinary shares are validly tendered in the offer and not properly withdrawn; |

| • | Adjustments to reflect financing arrangements entered into in connection with the Acquisition; and |

| • | Transaction costs in connection with the Acquisition. |

The unaudited pro forma condensed combined statement of operations also includes certain purchase accounting adjustments, including items expected to have a continuing impact on the combined results, such as increased amortization expense on acquired intangible assets. The unaudited pro forma condensed combined statement of operations does not include the impact of any revenue, cost or other operating synergies that may result from the Acquisition or any related restructuring costs.

The unaudited pro forma condensed combined financial information presented is based on the assumptions and adjustments described in the accompanying notes. The unaudited pro forma condensed combined financial information is presented for illustrative purposes and does not purport to represent what the financial position or results of operations would actually have been if the Acquisition occurred as of the dates indicated or what financial position or results would be for any future periods.

Diebold, Incorporated and subsidiaries

Unaudited pro forma condensed combined balance sheet

As of December 31, 2015

(in millions)

| Historical | ||||||||||||||||||||||||||||||||||

| Diebold (December 31, 2015) |

Wincor Nixdorf (see note 3) |

Wincor Nixdorf U.S.

GAAP |

(Note) | Wincor Nixdorf |

Purchase accounting adjustments |

(Note) | Financing adjustments |

(Note) | Pro forma |

|||||||||||||||||||||||||

| ASSETS |

||||||||||||||||||||||||||||||||||

| Current assets: |

||||||||||||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 313.6 | $ | 42.4 | $ | — | $ | 42.4 | $ | (1,301.1 | ) | 7(a) | $ | 1,398.2 | 7(i) | $ | 453.1 | |||||||||||||||||

| Short-term investments |

39.9 | — | — | — | — | — | 39.9 | |||||||||||||||||||||||||||

| Trade receivables, net |

413.9 | 544.5 | — | 544.5 | (11.3 | ) | 7(b) | — | 947.1 | |||||||||||||||||||||||||

| Inventories |

369.3 | 398.8 | — | 398.8 | 49.2 | 7(c) | — | 817.3 | ||||||||||||||||||||||||||

| Deferred income taxes |

168.8 | — | 36.0 | 5(b), (d) | 36.0 | — | — | 204.8 | ||||||||||||||||||||||||||

| Prepaid expenses |

23.6 | — | — | — | — | — | 23.6 | |||||||||||||||||||||||||||

| Refundable income taxes |

18.0 | 12.3 | — | 12.3 | — | — | 30.3 | |||||||||||||||||||||||||||

| Current assets held for sale |

148.2 | — | — | — | — | — | 148.2 | |||||||||||||||||||||||||||

| Other current assets |

148.3 | 79.6 | 12.1 | 91.7 | — | (7.0 | ) | 7(j) | 233.0 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total current assets |

1,643.6 | 1,077.6 | 48.1 | 1,125.7 | (1,263.2 | ) | 1,391.2 | 2,897.3 | ||||||||||||||||||||||||||

| Securities and other investments |

85.2 | 3.5 | — | 3.5 | — | — | 88.7 | |||||||||||||||||||||||||||

| Property, plant and equipment, net |

175.3 | 135.9 | — | 135.9 | — | — | 311.2 | |||||||||||||||||||||||||||

| Goodwill |

161.5 | 377.4 | — | 377.4 | 496.9 | 7(d) | — | 1,035.8 | ||||||||||||||||||||||||||

| Deferred income taxes |

65.3 | 53.7 | (46.1 | ) | 5(b), (d) | 7.6 | — | — | 72.9 | |||||||||||||||||||||||||

| Finance lease receivables |

36.5 | 16.3 | — | 16.3 | — | — | 52.8 | |||||||||||||||||||||||||||

| Other intangible assets |

36.7 | 19.7 | (1.2 | ) | 5(a) | 18.5 | 885.6 | 7(e) | — | 940.8 | ||||||||||||||||||||||||

| Other assets |

45.2 | 6.4 | 4.2 | 5(d) | 10.6 | — | 55.1 | 7(i) | 110.9 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total other assets, net |

605.7 | 612.9 | (43.1 | ) | 569.8 | 1,382.5 | 55.1 | 2,613.1 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total assets |

$ | 2,249.3 | $ | 1,690.5 | $ | 5.0 | $ | 1,695.5 | $ | 119.3 | $ | 1,446.3 | $ | 5,510.4 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| LIABILITIES AND EQUITY |

||||||||||||||||||||||||||||||||||

| Current liabilities: |

||||||||||||||||||||||||||||||||||

| Notes payable |

$ | 32.0 | $ | 125.8 | $ | — | $ | 125.8 | $ | — | $ | (110.1 | ) | 7(i) | $ | 47.7 | ||||||||||||||||||

| Accounts payable |

281.7 | 379.2 | — | 379.2 | (11.3 | ) | 7(b) | — | 649.6 | |||||||||||||||||||||||||

| Deferred revenue |

229.2 | 139.2 | — | 139.2 | (33.9 | ) | 7(f) | — | 334.5 | |||||||||||||||||||||||||

| Payroll and other benefits liabilities |

76.5 | 126.1 | — | 126.1 | — | — | 202.6 | |||||||||||||||||||||||||||

| Current liabilities held for sale |

49.4 | — | — | — | — | — | 49.4 | |||||||||||||||||||||||||||

| Other current liabilities |

287.0 | 260.6 | (39.8 | ) | 5(b), (d) | 220.8 | — | — | 507.8 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total current liabilities |

955.8 | 1,030.9 | (39.8 | ) | 991.1 | (45.2 | ) | (110.1 | ) | 1,791.6 | ||||||||||||||||||||||||

| Long-term debt |

613.1 | 73.6 | — | 73.6 | — | 1,575.8 | 7(i) | 2,262.5 | ||||||||||||||||||||||||||

| Pensions and other benefits |

195.6 | 93.4 | — | 93.4 | — | — | 289.0 | |||||||||||||||||||||||||||

| Post-retirement and other benefits |

18.7 | 6.0 | — | 6.0 | — | — | 24.7 | |||||||||||||||||||||||||||

| Deferred income taxes |

1.9 | 26.0 | 36.7 | 5(a), (d) | 62.7 | 261.3 | 7(g) | — | 325.9 | |||||||||||||||||||||||||

| Other liabilities |

28.7 | 21.6 | (3.9 | ) | 5(b), (c) | 17.7 | — | — | 46.4 | |||||||||||||||||||||||||

| Commitments and contingencies |

— | — | — | — | — | — | — | |||||||||||||||||||||||||||

| Equity: |

||||||||||||||||||||||||||||||||||

| Diebold, Incorporated shareholders’ equity |

||||||||||||||||||||||||||||||||||

| Preferred shares |

— | — | — | — | — | — | — | |||||||||||||||||||||||||||

| Common shares |

99.6 | 37.1 | — | 37.1 | (20.9 | ) | 7(h) | — | 115.8 | |||||||||||||||||||||||||

| Additional capital |

430.8 | — | — | — | 333.4 | 7(h) | — | 764.2 | ||||||||||||||||||||||||||

| Retained earnings |

760.3 | 534.6 | 12.0 | 5(a), (d) | 546.6 | (546.6 | ) | 7(h) | (19.4 | ) | 7(i), (j) | 740.9 | ||||||||||||||||||||||

| Treasury shares |

(560.2 | ) | (194.8 | ) | — | (194.8 | ) | 194.8 | 7(h) | — | (560.2 | ) | ||||||||||||||||||||||

| Accumulated other comprehensive items, net |

(318.1 | ) | 57.5 | — | 57.5 | (57.5 | ) | 7(h) | — | (318.1 | ) | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total Diebold, Incorporated shareholders’ equity |

412.4 | 434.4 | 12.0 | 446.4 | (96.8 | ) | (19.4 | ) | 742.6 | |||||||||||||||||||||||||

| Noncontrolling interests |

23.1 | 4.6 | — | 4.6 | — | — | 27.7 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total equity |

435.5 | 439.0 | 12.0 | 451.0 | (96.8 | ) | (19.4 | ) | 770.3 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Total liabilities and equity |

$ | 2,249.3 | $ | 1,690.5 | $ | 5.0 | $ | 1,695.5 | $ | 119.3 | $ | 1,446.3 | $ | 5,510.4 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

See accompanying notes to unaudited pro forma condensed combined financial information.

Diebold, Incorporated and subsidiaries

Unaudited pro forma condensed combined statement of operations

For the year ended December 31, 2015

(in millions, except per share data)

| Historical | ||||||||||||||||||||||||||||||||||

| Diebold (December 31, 2015) |

Wincor Nixdorf (see note 3) |

Wincor Nixdorf U.S. GAAP adjustments |

(Note) | Wincor Nixdorf (U.S. GAAP) |

Purchase accounting adjustments |

(Note) | Financing adjustments |

(Note) | Pro forma |

|||||||||||||||||||||||||

| Net sales |

||||||||||||||||||||||||||||||||||

| Services |

$ | 1,394.2 | $ | 1,436.8 | $ | — | $ | 1,436.8 | $ | (6.2 | ) | 8(a) | $ | — | $ | 2,824.8 | ||||||||||||||||||

| Products |

1,025.1 | 1,351.1 | — | 1,351.1 | (0.3 | ) | 8(a) | — | 2,375.9 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| 2,419.3 | 2,787.9 | — | 2,787.9 | (6.5 | ) | — | 5,200.7 | |||||||||||||||||||||||||||

| Cost of sales |

||||||||||||||||||||||||||||||||||

| Services |

932.8 | 1,212.9 | — | 1,212.9 | (1.5 | ) | 8(a) | — | 2,144.2 | |||||||||||||||||||||||||

| Products |

834.5 | 1,076.9 | (13.2 | ) | 5(b), (e), (f) | 1,063.7 | 67.4 | 8(a), (c) | — | 1,965.6 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| 1,767.3 | 2,289.8 | (13.2 | ) | 2,276.6 | 65.9 | — | 4,109.8 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Gross profit |

652.0 | 498.1 | 13.2 | 511.3 | (72.4 | ) | — | 1,090.9 | ||||||||||||||||||||||||||

| Selling and administrative expense |

488.2 | 367.7 | 0.2 | 5(e), (f) | 367.9 | 67.0 | 8(c), (d) | — | 923.1 | |||||||||||||||||||||||||

| Research, development and engineering expense |

86.9 | 102.9 | 4.2 | 5(a), (e), (f) | 107.1 | (0.5 | ) | 8(c) | — | 193.5 | ||||||||||||||||||||||||

| Impairment of assets |

18.9 | — | — | — | — | — | 18.9 | |||||||||||||||||||||||||||

| Gain on sale of assets, net |

(0.6 | ) | — | — | — | — | — | (0.6 | ) | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| 593.4 | 470.6 | 4.4 | 475.0 | 66.5 | — | 1,134.9 | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Operating profit (loss) |

58.6 | 27.5 | 8.8 | 36.3 | (138.9 | ) | — | (44.0 | ) | |||||||||||||||||||||||||

| Other income (expense) |

||||||||||||||||||||||||||||||||||

| Investment income |

26.0 | (2.0 | ) | — | (2.0 | ) | — | — | 24.0 | |||||||||||||||||||||||||

| Interest expense |

(32.5 | ) | (8.3 | ) | 1.8 | 5(e) | (6.5 | ) | — | (105.2 | ) | 8(g) | (144.2 | ) | ||||||||||||||||||||

| Foreign exchange loss, net |

(10.0 | ) | — | — | — | — | — | (10.0 | ) | |||||||||||||||||||||||||

| Miscellaneous, net |

3.7 | — | — | — | — | (7.0 | ) | 8(h) | (3.3 | ) | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Income (loss) from continuing operations before taxes |

45.8 | 17.2 | 10.6 | 27.8 | (138.9 | ) | (112.2 | ) | (177.5 | ) | ||||||||||||||||||||||||

| Income tax (benefit) expense |

(13.7 | ) | 8.2 | 4.9 | 5(a), (b) | 13.1 | (40.3 | ) | 8(e) | (32.5 | ) | 8(i) | (73.4 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

| Income (loss) from continuing operations, net of tax |

59.5 | 9.0 | 5.7 | 14.7 | (98.6 | ) | (79.7 | ) | (104.1 | ) | ||||||||||||||||||||||||

| Basic Weighted Average Shares Outstanding |

64.9 | 12.9 | 8(f) | — | 77.8 | |||||||||||||||||||||||||||||

| Diluted Weighted Average Shares Outstanding |

65.6 | 12.9 | 8(f) | — | 78.5 | |||||||||||||||||||||||||||||

| Basic earnings (loss) per share from continuing operations |

$ | 0.89 | $ | (1.38 | ) | |||||||||||||||||||||||||||||

| Diluted earnings (loss) per share from continuing operations |

$ | 0.88 | $ | (1.37 | ) | |||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||

|

|

||||||||||||||||||||||||||||||||||

See accompanying notes to unaudited pro forma condensed combined financial information.

Notes to unaudited pro forma condensed combined financial information

Note 1—Description of the Acquisition

On November 23, 2015, Diebold and Wincor Nixdorf entered into the Acquisition Agreement, whereby Diebold has offered to exchange a combination of cash and Diebold common shares for each outstanding Wincor Nixdorf ordinary share in a voluntary takeover offer pursuant to the German Takeover Act. The offer and the other transactions contemplated by the Acquisition Agreement are intended to result in the Acquisition of Wincor Nixdorf by Diebold. Upon consummation of the proposed Acquisition, Wincor Nixdorf would become a subsidiary of Diebold.

Subject to the terms and conditions of the offer, Wincor Nixdorf shareholders who validly tender their shares in the offer will be entitled to receive offer consideration that is the equivalent of €49.45 or $55.36 for each Wincor Nixdorf ordinary share (based on the closing price per share of Diebold common shares of $27.02 on March 23, 2016). The offer consideration for each Wincor Nixdorf ordinary share is comprised of (1) 0.434 common shares of Diebold and (2) €38.98 in cash.

The overall offer consideration is variable and subject to the price of Diebold common shares and U.S. dollar to euro exchange rate on the date of the Acquisition.

The offer is subject to customary conditions, including satisfying certain regulatory requirements.

Note 2—Basis of presentation

The unaudited pro forma condensed combined balance sheet was prepared using the historical balance sheets of Diebold as of December 31, 2015 and Wincor Nixdorf as of September 30, 2015 and assumes the proposed Acquisition occurred on December 31, 2015. Wincor Nixdorf’s fiscal year ends on September 30 and Diebold’s fiscal year ends on December 31. The unaudited pro forma condensed combined statement of operations were prepared using:

| • | the historical audited statement of income of Diebold for the year ended December 31, 2015; and |

| • | the historical audited consolidated statement of income of Wincor Nixdorf for the year ended September 30, 2015. |

Diebold’s historical audited financial statements were prepared in accordance with GAAP and presented in millions of U.S. dollars. Wincor Nixdorf’s historical audited financial statements were prepared in accordance with IFRS as issued by the IASB and presented in thousands of euros. The historical Wincor Nixdorf financial statements included within the unaudited pro forma condensed combined balance sheet and statement of income have been rounded to millions, and certain reclassifications were made to align Wincor Nixdorf’s financial statement presentation with that of Diebold. Wincor Nixdorf’s historical audited financial statements were reconciled to GAAP, and the IFRS to GAAP adjustments are reflected in the “Wincor Nixdorf GAAP Adjustments” column as presented above and discussed in the accompanying notes. Wincor Nixdorf’s historical audited financial statements, IFRS to GAAP adjustments and pro forma adjustments were translated from euros to U.S. dollars using the period-end rate of $1.1216 per euro for the unaudited pro forma condensed combined balance sheet as of September 30, 2015 and the historical average rate of $1.1487 per euro during the year ended September 30, 2015 for the unaudited pro forma condensed combined statement of operations.

The proposed Acquisition will be accounted for using the acquisition method of accounting under the provisions of ASC 805, with Diebold representing the accounting acquirer under this guidance. Accordingly, the historical consolidated financial statements have been adjusted to give effect to the impact of the offer consideration paid in connection with the Acquisition. In the unaudited pro forma condensed combined balance sheet, Diebold’s cost to acquire Wincor Nixdorf has been allocated to the assets acquired and liabilities assumed based upon management’s preliminary estimate of what their respective fair values would be as of the date of the Acquisition. The pro forma adjustments are preliminary and are based upon available information and certain assumptions which management believes are reasonable under the circumstances and which are described in the accompanying notes herein. Actual results may differ materially from the assumptions within the accompanying unaudited pro forma condensed combined financial information. Under ASC 805, generally all assets acquired and liabilities assumed are recorded at their acquisition date fair value. For purposes of the pro forma information presented herein, the fair value of Wincor Nixdorf’s identifiable tangible and intangible assets acquired and liabilities assumed is based on a preliminary estimate of fair value. Any excess of the purchase price over the fair value of identified tangible and intangible assets acquired and liabilities assumed will be recognized as goodwill. Certain current market based assumptions were used which will be updated upon completion of the Acquisition. Management believes the estimated fair values utilized for the assets to be acquired and liabilities to be assumed are based on reasonable estimates and assumptions. Preliminary fair value estimates may change as additional information becomes available and such changes could be material, as certain valuations and other studies have yet to commence or progress to a stage where there is sufficient information for definitive measurement. In addition, a preliminary review of IFRS to GAAP differences and related accounting policies has been completed based on information made available to date. However, following the consummation of the Acquisition, management will conduct a final review. As a result of that review, management may identify differences that, when finalized, could have a material impact on the unaudited pro forma condensed combined financial information.

The unaudited pro forma condensed combined statement of operations also include certain purchase accounting adjustments, including items expected to have a continuing impact on the combined results, such as increased amortization expense on acquired intangible assets. The unaudited pro forma condensed combined statements of operations do not include the impacts of any revenue, cost or other operating synergies that may result from the Acquisition or any related restructuring costs that may be contemplated. Diebold and Wincor Nixdorf have just recently begun collecting information in order to formulate detailed integration plans to deliver planned synergies. However, at this time, the status of the integration plans is too uncertain to include in the pro forma financial statements.

The unaudited pro forma condensed combined statement of operations only shows net income (loss) from continuing operations.

Financing arrangement

On November 23, 2015, Diebold entered into financing arrangements, the funding under which is conditioned upon the closing of the offer (“Acquisition Financing”), and the proceeds of which are expected to be used i) to finance a portion of the cash consideration of the purchase price to be paid in exchange for Wincor Nixdorf ordinary shares pursuant to the offer, ii) to refinance a portion of Diebold’s outstanding indebtedness and iii) to refinance Wincor Nixdorf’s outstanding indebtedness at the time of closing of the Acquisition. Upon closing of the offer, Diebold expects outstanding borrowings under the Acquisition Financing and the replacement credit facility (which it entered into on December 23, 2015 to refinance outstanding indebtedness under its existing $230.0 million term loan A senior unsecured credit facility (“Existing Term Loan A”)) to be approximately $2,298.1 million. The committed Acquisition Financing of $2,068.1 million is comprised of senior secured term loans totaling $1,568.1 million and $500.0 million of bridge facilities backstopping the $500.0 million aggregate principal of senior unsecured notes. The Acquisition Financing (other than the notes) will bear varying interest rates as explained in the accompanying notes.

Note 3—Reclassifications

Historical Wincor Nixdorf financial statements included within the unaudited pro forma condensed combined financial information have been rounded from thousands to millions and converted from euro to U.S. dollars using the period-end rate of $1.1216 per euro for the unaudited pro forma condensed combined balance sheet as of September 30, 2015 and the historical average rate of $1.1487 per euro during the year ended September 30, 2015 for the unaudited pro forma condensed combined statement of operations. In addition, certain balances presented in the historical Wincor Nixdorf financial statements included within the unaudited pro forma condensed combined financial information have been reclassified to conform the presentation to that of Diebold as indicated in the tables below:

Balance Sheet as of September 30, 2015

| Item | Amount (in US$M) |

Presentation in Wincor Nixdorf’s |

Presentation in unaudited pro forma condensed combined financial information | |||||

| Receivables from related companies |

$ | 8.0 | Receivables from related companies | Other current assets | ||||

| Finance lease receivables |

$ | 16.3 | Trade receivables | Finance lease receivables | ||||

| Trade receivables |

$ | 1.5 | Trade receivables | Other assets | ||||

| Reworkable service parts |

$ | 32.6 | Reworkable service parts | Inventories | ||||

| Investments accounted for using the equity method |

$ | 2.2 | Investments accounted for using the equity method |

Securities and other investments | ||||

| Goodwill |

$ | 377.4 | Intangible assets | Goodwill | ||||

| Acquired intangibles |

$ | 19.7 | Intangible assets | Property, plant and equipment | ||||

| Current income tax liabilities |

$ | 44.8 | Current income tax liabilities | Other current liabilities | ||||

| Liabilities to related companies |

$ | 2.7 | Liabilities to related companies | Other current liabilities | ||||

| Advances received |

$ | 23.2 | Advances received | Deferred revenue | ||||

| Financial liabilities (current) |

$ | 125.8 | Financial liabilities (current) | Notes payable | ||||

| Payroll and other benefits liabilities |

$ | 79.7 | Other accruals (current) | Payroll and other benefits liabilities | ||||

| Other current liabilities |

$ | 112.0 | Other accruals (current) | Other current liabilities | ||||

| Payroll and other benefits liabilities |

$ | 46.3 | Other current liabilities | Payroll and other benefits liabilities | ||||

| Deferred revenue |

$ | 139.2 | Other current liabilities | Deferred revenue | ||||

| Financial liabilities (noncurrent) |

$ | 73.6 | Financial liabilities (noncurrent) | Long-term debt | ||||

| Post-retirement and other benefits |

$ | 6.0 | Other accruals (noncurrent) | Post-retirement and other benefits | ||||

| Other long-term liabilities |

$ | 13.9 | Other accruals (noncurrent) | Other long-term liabilities | ||||

| Accruals for pensions and similar commitments |

$ | 93.4 | Accruals for pensions and similar commitments |

Pensions and other benefits | ||||

| Subscribed capital of Wincor Nixdorf |

$ | 37.1 | Subscribed capital of Wincor Nixdorf |

Common shares | ||||

| Other components of equity |

$ | 57.5 | Other components of equity | Accumulated other comprehensive items, net | ||||

|

| ||||||||

Statement of Income for the Year Ended September 30, 2015

| Item | Amount (in US$M) |

Presentation in Wincor Nixdorf’s IFRS financial statements |

Presentation in unaudited pro forma condensed combined financial information | |||||

| Net sales—Services |

$ | 1,436.8 | Net sales | Net sales—Services | ||||

| Net sales—Products |

$ | 1,351.1 | Net sales | Net sales—Products | ||||

| Cost of sales—Services |

$ | 1,212.9 | Cost of sales | Cost of sales—Services | ||||

| Cost of sales—Products |

$ | 1,076.9 | Cost of sales | Cost of sales—Products | ||||

| Results from equity accounted investments |

$ | (2.3 | ) | Results from equity accounted investments |

Investment income | |||

| Investment income |

$ | 0.4 | Finance income | Investment income | ||||

| Interest expense |

$ | 1.3 | Finance income | Interest expense | ||||

| Finance costs |

$ | (9.7 | ) | Finance costs | Interest expense | |||

|

| ||||||||

Note 4—Purchase price

Under the terms of the offer, Wincor Nixdorf shareholders who validly tender their shares, and do not properly withdraw, will be entitled to receive the offer consideration in cash and common shares of Diebold that is the equivalent of €49.45 or $55.36 for each Wincor Nixdorf ordinary share (based on the closing price per share of Diebold common shares of $27.02 on March 23, 2016). The estimated purchase price reflected in the unaudited pro forma condensed combined financial information assumes all outstanding Wincor Nixdorf ordinary shares are validly tendered in the offer and their holders receive the offer consideration. It is possible that Wincor Nixdorf shareholders who do not tender their shares in the offer may receive a different form and amount of consideration and may receive consideration on different dates.

For the purpose of preparing the accompanying unaudited pro forma condensed combined balance sheet as of December 31, 2015, the preliminary estimate of the purchase price was calculated as follows (amounts in millions, except share data):

| Wincor Nixdorf ordinary shares issued and outstanding prior to the closing of the offer(1) |

29,816,211 | |||

| Closing price per share of Diebold common stock on March 23, 2016 |

$ | 27.02 | ||

| Closing date exchange ratio |

0.434 | |||

|

|

|

|||

| Equity consideration per share in U.S. dollars |

$ | 11.73 | ||

|

|

|

|||

| Cash per share portion of the purchase consideration |

€ | 38.98 | ||

| Euro to US dollar exchange rate as of March 23, 2016 |

1.1195 | |||

|

|

|

|||

| Cash consideration per share in U.S. dollars |

$ | 43.64 | ||

|

|

|

|||

| Fair value of cash portion of the purchase consideration in U.S. dollars(2) |

$ | 1,301.1 | ||

| Fair value of equity portion of the purchase consideration in U.S. dollars(3) |

349.6 | |||

|

|

|

|||

| Total estimated purchase price in U.S. dollars |

$ | 1,650.7 | ||

|

|

||||

| (1) | Pursuant to terms of the offer, each Wincor Nixdorf ordinary share is subject to the offer. Wincor Nixdorf has committed, by way of a non-tender agreement, not to tender or otherwise dispose of its treasury shares (which are not considered to be outstanding). As of March 23, 2016, 29,816,211 Wincor Nixdorf ordinary shares were outstanding. |

| (2) | The fair value of cash portion of the purchase consideration in U.S. dollars is calculated as follows (amounts in millions, except share data): |

| Cash consideration per ordinary share of Wincor Nixdorf |

$ | 43.64 | ||

| Wincor Nixdorf ordinary shares issued and outstanding prior to the closing of the offer |

29,816,211 | |||

|

|

|

|||

| Total cash portion of the purchase consideration |

$ | 1,301.1 | ||

|

|

||||

| (3) | Assumes all outstanding Wincor Nixdorf shares are validly tendered in, and not properly withdrawn from, the offer. The fair value of equity portion of the purchase consideration in U.S. dollars is calculated as follows (amounts in millions, except share data): |

| Wincor Nixdorf ordinary shares issued and outstanding prior to the closing of the offer |

29,816,211 | |||

| Closing price per Diebold common shares on March 23, 2016 |

$ | 27.02 | ||

| Closing date exchange ratio |

0.434 | |||

|

|

|

|||

| Equity consideration per share in U.S. dollars |

11.73 | |||

|

|

|

|||

| Total equity portion of the purchase consideration |

$ | 349.6 | ||

|

|

||||

The estimated consideration expected to be paid reflected in the unaudited pro forma condensed combined financial information does not purport to represent what the actual consideration paid will be when the offer closes or what, if any, consideration Diebold may pay to acquire Wincor Nixdorf ordinary shares following the closing of the offer in a post-completion reorganization. In accordance with ASC 805, the fair value of equity securities issued as part of the consideration paid will be measured on the closing date of the offer at the then-current market price. This requirement will likely result in a per-share equity component different from the $27.02 assumed in these unaudited pro forma condensed combined financial information and the difference may be material. Diebold believes that an increase or decrease of 27 percent in the market price of Diebold’s common shares on the closing date of the offer as compared to the market price of Diebold’s common shares assumed for the purposes of the unaudited pro forma condensed combined financial information is possible based upon the recent history of the market price of Diebold’s common shares. This amount was derived based on historical volatility of Diebold’s common shares and is not indicative of Diebold’s expectation for future share price performance. A change of this magnitude would increase or decrease the purchase price by approximately $94.4 million, which would result in a corresponding increase or decrease to goodwill in the unaudited pro forma condensed combined financial information. Similarly, a 10 percent change in the euro to U.S. dollar exchange rate at the closing date of the offer would increase or decrease the purchase price by approximately $130.1 million, which would also result in a corresponding increase or decrease to goodwill in the unaudited pro forma condensed combined financial information.

The following is a summary of the preliminary allocation of the above purchase price as reflected in the unaudited pro forma condensed combined balance sheet as of December 31, 2015 (amounts in millions):

| Total purchase price |

$ | 1,650.7 | ||

| Recognized amounts of identifiable assets acquired and liabilities assumed |

||||

| Net book value of assets acquired |

$ | 446.4 | ||

| Write-off of pre-existing Wincor Nixdorf goodwill and intangible assets |

395.9 | |||

|

|

|

|||

| Adjusted net book value of assets acquired |

50.5 | |||

| Identifiable intangible assets at fair value |

904.1 | |||

| Increase inventory to fair value |

49.2 | |||

| Decrease deferred revenue to fair value |

33.9 | |||

| Deferred tax adjustments |

(261.3 | ) | ||

|

|

|

|||

| Fair value of assets and liabilities assumed excluding goodwill |

776.4 | |||

|

|

|

|||

| Total goodwill |

$ | 874.3 | ||

|

|

||||

The goodwill balance is primarily attributed to the assembled workforce, expanded market opportunities and cost and other operating synergies anticipated upon the integration of the operations of Diebold and Wincor Nixdorf. See Note 7 for a discussion of the methods used to determine the fair value of Wincor Nixdorf’s identifiable assets.

Note 5—IFRS to US GAAP adjustments

| (a) | Reflects adjustment to reverse certain research and development costs capitalized under IFRS for hardware and fixed assets as a result of the application of GAAP. In accordance with IFRS, certain development costs can be capitalized for hardware and fixed assets which otherwise would be expensed under GAAP. The adjustment to the unaudited pro forma condensed combined balance sheet consists of a reduction in other intangible assets and its corresponding deferred tax liability, which resulted in a decrease to retained earnings. The adjustment to the unaudited pro forma condensed combined statement of operations for the year ended December 31, 2015 consists of an increase to research, development and engineering expense and a reduction to income tax expense. |

Unaudited Pro Forma Balance Sheet Adjustments