Attached files

| file | filename |

|---|---|

| EX-23 - JMG 12-31-15 EXHIBIT 23 - Journal Media Group, Inc. | jmg-20151231xex23.htm |

| EX-21 - JMG 12-31-2015 EXHIBIT 21 - Journal Media Group, Inc. | jmg-20151231xex21.htm |

| EX-31.1 - JMG 12-31-2015 EXHIBIT 31.1 - Journal Media Group, Inc. | jmg-20151231xex311.htm |

| EX-31.2 - JMG 12-31-2015 EXHIBIT 31.2 - Journal Media Group, Inc. | jmg-20151231xex312.htm |

| EX-32 - JMG 12-31-2015 EXHIBIT 32 - Journal Media Group, Inc. | jmg-20151231xex32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2015 OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission File Number 001-36879

JOURNAL MEDIA GROUP, INC.

(Exact name of registrant as specified in its charter)

Wisconsin (State or other jurisdiction of incorporation or organization) | 47-1939596 (IRS Employer Identification Number) | |

333 West State Street Milwaukee, Wisconsin (Address of principal executive offices) | 53203 (Zip Code) | |

Registrant’s telephone number, including area code: (414) 224-2000

Title of each class Securities registered pursuant to Section 12(b) of the Act: | Name of each exchange on which registered New York Stock Exchange | |

Common Stock, $0.01 par value | ||

Securities registered pursuant to Section 12(g) of the Act: | ||

Not applicable | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company “in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer o | Non-accelerated filer þ (do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the common stock of the registrant held by non-affiliates of the registrant on June 30, 2015 was approximately $195,823,654.

As of March 23, 2016, there were 24,407,533 shares of the registrant’s Common Stock, $0.01 par value per share, outstanding.

JOURNAL MEDIA GROUP, INC.

INDEX TO FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2015

Page No. | ||

15. Exhibits and Financial Statement Schedules | ||

SIGNATURES | ||

2

Forward-Looking Statements

We make certain statements in this Annual Report on Form 10-K that are “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements relate to our outlook or expectations for earnings, revenues, results of operations, financing plans, expenses, competitive position or other future financial or business performance, strategies or expectations or the impact of legal or regulatory matters on our business, results of operations or financial condition. Specifically, forward-looking statements may include:

• | statements relating to our plans, intentions, expectations, objectives or goals, including certain matters relating to the proposed merger with Gannett Co., Inc. (“Gannett”) and certain matters relating to the benefits of the newspaper mergers (as defined below); |

• | statements relating to our future performance, business prospects, revenue, income and financial condition and competitive position following the newspaper mergers, and any underlying assumptions relating to those statements; and |

• | statements preceded by, followed by or that include the words “anticipate,” “approximate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “project,” “seek,” “should,” “target,” “will” or similar expressions. |

These statements reflect our judgment based upon currently available information and involve a number of risks and uncertainties that could cause actual results to differ materially from those expressed in, or implied by, the forward-looking statements. You should evaluate our forward-looking statements, which are as of the date of this filing, with the understanding of their inherent uncertainty. We undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of the statement.

With respect to these forward-looking statements, we have made assumptions regarding, among other things, customer growth and retention, pricing, operating costs, technology and the economic and regulatory environment.

Future performance cannot be ensured. Actual results may differ materially from those expressed in, or implied by, the forward-looking statements. Some of the factors that could cause our actual results to differ include those described in Item 1A “Risk Factors” on this Annual Report on Form 10-K, as such may be amended or supplemented in Part II, Item 1A of our subsequently filed Quarterly Reports on Form 10-Q, as well as, among others, the following:

• | uncertainties as to the expected closing date of the proposed merger with Gannett; |

• | potential disruption from the proposed merger with Gannett making it more difficult to maintain business and operational relationships; |

• | the risk that unexpected costs will be incurred in connection with the proposed merger with Gannett; |

• | the risk of litigation and other legal proceedings related to the proposed merger with Gannett; |

• | changes in economic, business or political conditions, licensing requirements or tax matters in connection with the proposed merger with Gannett; |

• | risks related to the timing (including possible delays) of the expiration or termination of the applicable waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended, in connection with the proposed merger with Gannett; |

• | the possibility that the proposed merger with Gannett does not close, including, but not limited to, due to the failure to satisfy the closing conditions; |

• | the risk that the merger agreement with Gannett may be terminated in certain circumstances that require us to pay Gannett a termination fee of $9 million; |

• | competition in the markets we serve; |

• | the possibility that expected synergies and value creation from the newspaper mergers will not be realized, or will not be realized in the expected time period; |

• | the possibility that the newspaper businesses of Journal Communications, Inc. (“Journal”) and The E.W. Scripps Company (“Scripps”) will not be integrated successfully; |

3

• | inability to retain and attract qualified personnel; |

• | disruption from the newspaper mergers making it more difficult to maintain business and operational relationships; |

• | the risk that unexpected costs will be incurred; |

• | our expectations regarding the period during which we qualify as an "emerging growth company" under the Jumpstart our Business Startups Act; and |

• | changes in economic, business or political conditions, or licensing requirements or tax matters. |

4

PART I

ITEM 1. | BUSINESS |

Background

Journal Media Group, Inc. (the "Company" or "Journal Media Group") was incorporated in Wisconsin on July 25, 2014. From our incorporation until the consummation of the newspaper mergers on April 1, 2015, Scripps and Journal each owned 50% of our common stock. On April 1, 2015, we became a holding company owning various subsidiaries that own and operate the former newspaper publishing businesses of Scripps and Journal. In this Annual Report on Form 10-K, we refer to the newspapers published by subsidiaries of Scripps as the “Scripps Newspapers” and to the newspapers published by subsidiaries of Journal as the "Journal Newspapers" or "JRN Newspapers."

Since our inception, and until April 1, 2015, our activities were limited to our organization, the preparation of our registration statement on Form S-4 and other matters related to the transactions (as defined below). Throughout 2014 and the first quarter of 2015, we conducted no business operations nor owned or leased any real estate or other property. Accordingly, our only assets prior to the consummation of the newspaper mergers on April 1, 2015 arose from the issuance of two shares of our common stock, one to Scripps and one to Journal, upon our inception. We did not have any costs or liabilities arising out of our operations prior to the consummation of the newspaper mergers on April 1, 2015. As a result, the financial statements and related disclosures (including Management’s Discussion and Analysis of Financial Condition and Results of Operations) included in this Annual Report on Form 10-K for periods prior to April 1, 2015 are those of our predecessor, Scripps Newspapers.

On July 30, 2014, we entered into a master transaction agreement with Scripps, Journal, Scripps Media, Inc., Desk Spinco, Inc. ("Scripps Spinco"), Scripps NP Operating, LLC (f/k/a Desk NP Operating, LLC), Desk BC Merger, LLC, Boat Spinco, Inc., ("Journal Spinco"), Desk NP Merger Co., and Boat NP Merger Co.

Pursuant to the master transaction agreement, Scripps and Journal, through a series of transactions, (i) separated Journal’s newspaper business pursuant to a spin-off of Journal Spinco to the shareholders of Journal (the "Journal newspaper spin-off"), (ii) separated Scripps’ newspaper business pursuant to a spin-off of Scripps Spinco to the shareholders of Scripps ( the "Scripps newspaper spin-off" and together with the Journal newspaper spin-off, the "spin-offs"), (iii) combined these two spun-off newspaper businesses through two mergers, resulting in each of them becoming a wholly owned subsidiary of Journal Media Group (the "newspaper mergers"), and (iv) then merged Journal with and into a wholly owned subsidiary of Scripps (we sometimes refer to the spin-offs, mergers and other transactions contemplated by the master transaction agreement, taken as a whole, as the "transactions"). Upon consummation on April 1, 2015, the transactions resulted in two separate public companies: one, Journal Media Group, continuing the combined newspaper businesses of Journal and Scripps; and the other, Scripps, continuing the combined broadcast businesses of Journal and Scripps. In connection with the transactions, each share of Journal class A common stock and Journal class B common stock outstanding on the share exchange record date received 0.5176 Scripps class A common shares and 0.1950 shares of Journal Media Group common stock, and each Scripps class A common share and common voting share outstanding received 0.2500 shares of Journal Media Group common stock. Immediately following completion of the transactions on April 1, 2015, holders of Journal’s common stock owned approximately 41% of the common shares of Journal Media Group and approximately 31% of the common shares of Scripps, in the form of Scripps class A common shares, with the remaining common shares of each entity owned by the Scripps shareholders. Pursuant to the master transaction agreement, prior to the completion of the transactions, Journal contributed to Journal Spinco $10.0 million in cash and Scripps distributed a special cash dividend in the aggregate amount of $60.0 million to the holders of its common shares (and certain common share equivalents in the form of restricted share units held by Scripps employees). Scripps class A shares issued in the broadcast merger to Journal shareholders did not participate in the Scripps special cash dividend.

At the effective time of the newspaper mergers on April 1, 2015, the shares of our common stock owned by Scripps and Journal were returned to us, and the outstanding shares of Scripps Spinco and Journal Spinco common stock were converted into shares of our common stock. Following the conversion on April 1, 2015, we became a stand-alone, publicly traded company, owned initially by Scripps and Journal shareholders, and neither Scripps nor Journal have any ownership interest in us.

In this Annual Report on Form 10-K, unless the context requires otherwise, references to "we," "us" and "our" with respect to periods before the April 1, 2015 consummation of the newspaper mergers refer to the business and operations of the Scripps Newspapers, as our predecessor, and references to the "Company," "Journal Media Group," “JMG,” "we," "us" and "our" with respect to periods after the consummation of the newspaper mergers refer to Journal Media Group and its consolidated subsidiaries.

On October 7, 2015, we entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Gannett and Jupiter Merger Sub, Inc., a wholly owned subsidiary of Gannett (“Merger Sub”). The Merger Agreement provides that, subject to the satisfaction

5

or waiver of specified conditions, Merger Sub will merge with and into us and we will become a wholly owned subsidiary of Gannett (the “merger”). If the merger is completed, our shareholders will receive $12.00 in cash, without interest and less any applicable withholding taxes, for each share of our common stock owned. This transaction was unanimously approved by the boards of directors of both companies and was also approved by our shareholders (Gannett’s shareholders are not required to vote on this transaction). The closing of the merger remains subject to customary closing conditions, including antitrust regulatory clearance. We and Gannett are continuing to work through the review process with the U.S. Department of Justice and look forward to closing the transaction on a timely basis.

More information regarding us is available at our website at www.journalmediagroup.com. We are not including information contained on our website as part of, or incorporating it by reference into, this Annual Report on Form 10-K. Copies of all of our filings filed or furnished with the Securities and Exchange Commission (the "SEC") pursuant to Section 13(a) of the Exchange Act are available free of charge on this website as soon as reasonably practicable after we electronically file the material with, or furnish it to, the SEC. Our website also includes copies of the charters for our Compensation, Nominating and Corporate Governance and Audit Committees, our Corporate Governance Guidelines, our Code of Conduct and Ethics for Employees, our Code of Conduct and Ethics for Financial Executives, our Code of Conduct and Ethics for Members of the Board of Directors, and our Director Independence Standards. All of these documents are also available to shareholders in print upon request or by request via e-mail to investors@jmg.com.

Overview

We are a media enterprise with interests in newspapers and local digital media sites. With the ultimate goal of informing, engaging, and empowering readers in the communities we serve, we provide news, information and value to customers, employees and advertisers. We serve audiences and businesses through a portfolio of print and digital media brands, including 17 daily newspapers in 14 markets across the United States, and operate an expanding collection of local digital journalism and information businesses.

We distribute content primarily through four platforms — print, web, smartphones and tablets, with the objective to develop content and applications designed to deliver engaging content and enhance the user experience on each of these platforms. We expect that our ability to serve our communities by providing content across digital platforms will allow us to expand audiences beyond traditional print boundaries.

The newspapers that we publish have an excellent reputation for journalistic quality and content, key to retaining readership. The Milwaukee Journal Sentinel has been awarded the Pulitzer Prize — U.S. journalism’s highest honor — three times in recent years, and has been a Pulitzer finalist six additional times. Many of the other newspapers we publish were recognized in 2015 by regional and national journalism organizations for high-quality reporting across multiple platforms. This quality journalism enhances our impact and engagement in our local communities as we build out news reports in all formats that readers will turn to and trust.

Our digital sites offer comprehensive local news, information and user-generated content. We intend to enhance our digital offerings, using features such as streaming video and audio, to deliver news and information. Many of the journalists who work for us produce videos for consumption through digital sites and use an array of social media sites, such as Facebook, YouTube and Twitter, to communicate with and build audiences. The newspapers we publish have embraced mobile technology by offering products on apps available on Apple, Android, and Kindle Fire platforms, as well as providing mobile optimized sites accessible by all smartphones and tablets.

Over the years, the newspapers we publish have supplemented daily editions with an array of niche products, including direct mail advertising, total market coverage publications, zoned editions, specialty publications and event-based publications. These product offerings allow existing advertisers to reach their target audiences in multiple ways and to attract new clients, particularly small- and mid-sized advertisers.

6

The daily circulation, which includes print and E-edition, for the newspaper markets and audiences that we serve is as follows:

(in thousands) | 2015 (1) | 2014(2) | 2013(2) | 2012(2) | 2011(2) | ||||||||||

Abilene (TX) Reporter-News | 16 | 18 | 21 | 22 | 24 | ||||||||||

Anderson (SC) Independent-Mail | 17 | 19 | 21 | 22 | 23 | ||||||||||

Corpus Christi (TX) Caller-Times | 36 | 35 | 39 | 42 | 43 | ||||||||||

Evansville (IN) Courier & Press | 37 | 41 | 43 | 47 | 52 | ||||||||||

Henderson (KY) Gleaner | 6 | 7 | 8 | 9 | 10 | ||||||||||

Kitsap (WA) Sun | 16 | 18 | 19 | 20 | 21 | ||||||||||

Knoxville (TN) News Sentinel | 65 | 71 | 73 | 80 | 92 | ||||||||||

Memphis (TN) Commercial Appeal | 69 | 85 | 88 | 96 | 109 | ||||||||||

Milwaukee (WI) Journal Sentinel | 148 | 182 | 194 | 207 | 189 | ||||||||||

Naples (FL) Daily News | 60 | 51 | 58 | 59 | 54 | ||||||||||

Redding (CA) Record-Searchlight | 17 | 18 | 19 | 20 | 21 | ||||||||||

San Angelo (TX) Standard-Times | 14 | 16 | 17 | 18 | 18 | ||||||||||

Treasure Coast (FL) News/Press/Tribune (3) | 58 | 59 | 67 | 69 | 76 | ||||||||||

Ventura County (CA) Star | 46 | 46 | 49 | 54 | 62 | ||||||||||

Wichita Falls (TX) Times Record News | 17 | 18 | 19 | 22 | 22 | ||||||||||

Total Daily Circulation | 622 | 684 | 735 | 787 | 816 | ||||||||||

Circulation information for the Sunday edition of those newspapers is as follows:

(in thousands) | 2015 (1) | 2014(2) | 2013(2) | 2012(2) | 2011(2) | ||||||||||

Abilene (TX) Reporter-News | 19 | 23 | 25 | 28 | 31 | ||||||||||

Anderson (SC) Independent-Mail | 23 | 27 | 27 | 28 | 30 | ||||||||||

Corpus Christi (TX) Caller-Times | 47 | 46 | 51 | 55 | 58 | ||||||||||

Evansville (IN) Courier & Press | 53 | 57 | 61 | 68 | 73 | ||||||||||

Henderson (KY) Gleaner | 8 | 8 | 9 | 10 | 11 | ||||||||||

Kitsap (WA) Sun | 19 | 20 | 21 | 23 | 23 | ||||||||||

Knoxville (TN) News Sentinel | 86 | 96 | 100 | 108 | 121 | ||||||||||

Memphis (TN) Commercial Appeal | 105 | 120 | 124 | 131 | 147 | ||||||||||

Milwaukee (WI) Journal Sentinel | 246 | 294 | 319 | 338 | 326 | ||||||||||

Naples (FL) Daily News | 55 | 59 | 70 | 71 | 65 | ||||||||||

Redding (CA) Record-Searchlight | 20 | 21 | 21 | 23 | 24 | ||||||||||

San Angelo (TX) Standard-Times | 16 | 18 | 20 | 22 | 22 | ||||||||||

Treasure Coast (FL) News/Press/Tribune (3) | 74 | 75 | 84 | 88 | 94 | ||||||||||

Ventura County (CA) Star | 59 | 59 | 64 | 74 | 81 | ||||||||||

Wichita Falls (TX) Times Record News | 19 | 20 | 22 | 25 | 25 | ||||||||||

Total Sunday Circulation | 849 | 943 | 1,018 | 1,092 | 1,131 | ||||||||||

(1) | Based on Alliance for Audited Media (“AAM”) statements for the three-month period ended December 31, 2015. |

(2) | Based on AAM statements for the six-month periods ended September 30, except figures for the Naples Daily News and the Treasure Coast News/Press/Tribune, which are from the Statements for the 12-month periods ended September 30. |

(3) | Represents the combined daily and Sunday circulation of The Stuart News, the Indian River Press Journal and The St. Lucie News Tribune. |

Revenues Sources

Our newspapers derive revenue by selling marketing and advertising services to businesses in our markets and news and information content to subscribers.

7

Advertising

We believe that compelling news and information content and a diverse portfolio of product offerings on multiple platforms are critical components to garnering the most profitable share of local advertising dollars in our markets.

Our range of products and audience reach gives us the ability to deliver specific audiences desired by advertisers. While many advertisers want the broad reach of daily newspapers, others want to target their message by demography, geography, buying habits or consumer behavior. Where we can, we use our newspaper network to build partnerships with national advertisers. We also design programs on the local level for local merchants — customizing print and digital products into tailored messages to meet our local market objectives. We sell advertising based upon audience size, demographics, price and effectiveness. Advertising rates and revenues vary among our newspapers, depending on circulation, type of advertising, local market conditions and competition. Each of these newspapers operate in a highly competitive local media marketplace, where advertisers and media consumers can choose from a wide range of alternatives, including other news publications, radio, broadcast and cable television, magazines, websites, other digital platforms, outdoor advertising, directories and direct mail products.

Print advertising

Print advertising is the largest component of our operating revenues. Print advertising includes Run-of-Press (“ROP”) advertising, preprinted inserts, advertising in niche publications, and direct mail. Advertisements throughout a newspaper include retail, which consists of local and national advertising, and classified advertising. Local advertising refers to any advertising purchased by in-market advertisers that is not included in the newspapers' classified section. National advertising includes advertising purchased by businesses outside local markets. National advertisers typically procure advertising from numerous newspapers using advertising agency buying services. Classified advertising includes all auto, real estate and employment advertising and other ads listed in sequence by the nature of the ads. Preprinted inserts are stand-alone, multi-page circulars inserted into and distributed with daily newspapers, niche publications and shared mail products.

Digital advertising and marketing services

We sell advertising across all of our digital platforms. Digital advertising includes fixed duration campaigns whereby a banner, text or other advertisement appears for a specified period of time for a fee; impression-based campaigns where the fee is based upon the number of times the advertisement appears in webpages viewed by a user; and click-through campaigns where the fee is based upon the number of users who click on an advertisement and are directed to the advertiser’s website. We are developing local sponsorship programs that feature elements of fixed-duration and impression-based campaigns. These may include print elements (such as run-of-press or inserts) as part of the creative package designed to reach the reader/viewer/customer. We utilize a variety of audience-extension programs to enhance the reach of our websites and garner a larger share of local advertising dollars that are spent online.

We are a member of a newspaper consortium that partners with Yahoo! in an advertising and content sharing arrangement that increases access to local web-focused advertising dollars. We intend to have similar arrangements with other digital marketing services. We offer local advertising customers additional marketing services, such as managing search engine marketing campaigns.

Circulation (Subscriptions)

We deliver news and other content on four platforms — print, web, smartphones and tablets — and meter access to content delivered on our digital platforms. We introduced bundled subscription offerings for print and digital products in all of our markets by the end of 2013.

As we implemented metered access to our digital content in 2012 and 2013, we significantly increased subscription prices to many of our subscribers. Going forward we expect to manage price increases in an effort to obtain the highest yield from our subscriber base. Many customers are price-sensitive, particularly when we have reduced content they consider valuable. In an effort to minimize customer churn and maximize profitability, we have and will continue to use analysis of customer price sensitivity to drive price increases on targeted subscribers and limit the price increases on other subscribers.

We have also implemented marketing strategies to gain new customers, primarily through digital channels with special offers designed to obtain subscribers, particularly digital customers. We have also run a number of in-paper advertisements encouraging subscribers to register their account on-line, which allows us to monetize their online activity with certain advertisers who target specific customers based on demographics, which drives higher advertising rates.

8

Finally, we have implemented membership programs for customers allowing them to receive special offers not available to non-subscribers. Examples include discounts on certain products, specialized content and other exclusive offers.

Our print products are delivered directly to subscribers (home delivery) or purchased from a retail store or vending machine (single copy). Home delivery copies account for the majority of our total daily subscription revenues.

Daily and Sunday circulation has declined during the past five years, due in part to readers who consume more news and information online. Some of the declines were due to a deliberate decision to eliminate distribution to outlying areas. More recently we have implemented marketing and pricing strategies intended to stabilize home delivery subscription revenues.

Industry and Competition

Newspaper publishing was the first segment of the consumer media industry. Metropolitan and community publications often represent the primary medium for news and local advertising due to their historic importance to the communities they serve.

In recent years, newspaper industry fundamentals have declined as a result of secular industry change. Retail and classified ROP advertising have decreased from historic levels due in part to department store consolidation, weakened employment, automotive and real estate economics and a migration of advertising to the Internet and other advertising forms. Circulation declines and online competition have also negatively impacted newspaper industry revenues. Additionally, the housing market downturn, while now showing signs of recovery, has adversely impacted the newspaper industry, including real estate classified advertising as well as the home improvement, furniture and financial services advertising categories.

Advertising revenue is the largest component of a newspaper’s total revenue and it is affected by cyclical changes in national and regional economic conditions, as well as secular changes in the newspaper industry. Classified advertising is generally the most sensitive to economic cycles and secular changes in the newspaper business because it is driven primarily by the demand for employment, real estate transactions and automotive sales, as well as the migration of advertising to the Internet and other advertising forms. Newspaper advertising revenue is seasonal and we tend to see increased revenue due to increased advertising activity during certain holidays.

We believe newspapers and their online and niche products continue to be one of the most effective mediums for retail and classified advertising because they allow advertisers to promote the price and selection of goods more timely than most broadcast media, and to maximize household reach within a local retail trading area. Notwithstanding the advertising advantages newspapers offer, newspapers have many competitors for advertising dollars and subscription revenue. These competitors include local, regional and national newspapers, shoppers, magazines, broadcast and cable television, radio, direct mail, Yellow Pages, the Internet, mobile devices and other media. Competition for newspaper advertising revenue is based largely upon advertiser results, advertising rates, readership, demographics and circulation levels, while competition for subscription revenue is based largely upon the content of the newspaper, its price, editorial quality and customer service.

Newsprint

The basic raw material of newspapers is newsprint. We have been able to receive an adequate supply of newsprint for our needs. Newsprint is a basic commodity and its price is sensitive to changes in the balance of worldwide supply and demand. Mill closures and industry consolidation have decreased overall newsprint production capacity and could lead to future price increases.

Employees

As of December 31, 2015, we had approximately 2,800 full-time equivalent employees. Various labor unions represented approximately 800 of these employees. We have not experienced any work stoppages at current operations since 1985.

Properties

Our corporate headquarters are located in Milwaukee, Wisconsin and we operate in 14 markets in the United States. We believe all properties we own are well maintained, are in good condition and suitable for our contemplated operations. There are no material encumbrances on any of these properties. We own substantially all of the facilities and equipment used in our operations.

9

Quantitative and Qualitative Disclosures About Market Risk

Price fluctuations for newsprint may have a significant effect on our results of operations. We have not entered into derivative instruments to manage our exposure to newsprint price risk.

ITEM 1A. | RISK FACTORS |

You should consider carefully the risks described below, together with all of the other information included or incorporated by reference in this Annual Report on Form 10-K, in evaluating our company and our common stock. If any of the risks described below actually occurs, it could have a material adverse effect on our business, financial results, financial condition and/or stock price.

Risk Factors Relating to Our Business

We have a limited history operating as a stand-alone, publicly traded company, and limited combined financial statements, on which you can evaluate our performance.

We have operated as a combined business and as a stand-alone, publicly traded company since April 1, 2015. Accordingly, we have a limited operating history and limited financial statements as an independent, stand-alone company upon which you can evaluate us. We may not be able to grow or integrate our business as planned and may not be profitable.

Certain historical financial information contained in this Annual Report on Form 10-K is not indicative of our future results as a stand-alone, publicly traded company.

The financial statements and related disclosures (including Management’s Discussion and Analysis of Financial Condition and Results of Operations) included in this Annual Report on Form 10-K for periods prior to April 1, 2015 are those of our predecessor, Scripps Newspapers, and the historical carve-out financial statements of Scripps Newspapers were created from Scripps’ financial information. Accordingly, the historical carve-out financial information for Scripps Newspapers included in this Annual Report on Form 10-K does not reflect the Journal newspaper business and, thereby, does not reflect what our financial position, results of operations and cash flows would have been had those businesses been operated as a combined business and a stand-alone, publicly traded company during the periods before April 1, 2015. Nor is such information indicative of what our results of operations, financial position and cash flows may be in the future. This is primarily a result of the following factors:

• | the historical Journal newspaper business financial statements are not included in this Annual Report on Form 10-K and pursuant to Securities and Exchange Commission guidance are not required to be so included; |

• | the historical carve-out financial statements of Scripps Newspapers do not reflect certain changes that occurred in our funding and operations as a result of the separation of Scripps Spinco and Journal Spinco from Scripps and Journal, respectively, on April 1, 2015; |

• | our financial information prior to April 1, 2015 reflects estimated allocations for services historically provided by Scripps to Scripps Spinco, and these allocations are different from the costs we incur for these services following April 1, 2015; and |

• | the historical financial information prior to April 1, 2015 does not reflect certain increased or duplicative costs we incurred in becoming a stand-alone, publicly traded company as of April 1, 2015, such as costs attributable to transition service agreements we have with Scripps, or changes in historical cost structure due to our differing personnel needs, financing activities and operations. |

For these or other reasons, our future financial performance will be different from the performance implied by the historical carve-out information of Scripps Newspapers to April 1, 2015 presented in this Annual Report on Form 10-K.

For additional information about the past financial performance of Scripps Newspapers, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the historical carve-out financial statements and the accompanying notes of Scripps Newspapers included elsewhere in this Annual Report on Form 10-K.

10

The integration of the newspaper businesses of Journal and Scripps is time consuming, may distract our management from operations, and is expensive, all of which could have a material adverse effect on our operating results.

If we are not successful in integrating the newspaper operations of Scripps and Journal, or if the integration is more difficult or costly than anticipated, we may experience disruptions to our operations. A difficult or unsuccessful integration of these businesses would likely have a material adverse effect on our results of operations.

Some of the risks that may affect our ability to integrate or realize any anticipated benefits include those associated with:

• | adverse effects on employees and business relationships with customers and suppliers; |

• | difficulties in conforming standards, processes, procedures and controls of the businesses; |

• | difficulties in transferring processes and know-how; |

• | difficulties in the assimilation of acquired operations, technologies or products; and |

• | diversion of management’s attention from business concerns. |

We may not realize the benefits expected by combining the newspaper businesses of Scripps and Journal into a new publicly traded company and may experience increased costs that could decrease overall profitability.

Before the April 1, 2015 newspaper mergers, our business was part of two separate public companies. Following the consummation of the newspaper mergers, we may experience difficulties in integrating the two businesses into one company, and the newspaper mergers may result in increased costs and inefficiencies in our business operations and management. Integration of our businesses may cost significantly more or take longer than anticipated, which could decrease profitability or otherwise impact expected cost-savings. In addition, prior to the newspaper mergers our businesses took advantage of the economies of scale of Scripps and Journal. As a separate, standalone, publicly traded company, we may be unable to obtain goods, services and technology at prices or on terms as favorable as those obtained prior to the newspaper mergers, which could decrease overall profitability. Furthermore, we may not be successful in transitioning from the services and systems provided by Scripps and Journal and may incur substantially higher costs for implementation than currently anticipated. Failure on our part to realize the anticipated benefits of the newspaper mergers, including, without limitation, the anticipated cost-savings resulting from operating synergies and growth opportunities from combining the businesses, could have a material adverse effect on our profitability.

Restrictions on our operations, and our obligations to indemnify Scripps and its shareholders in connection with the tax-free treatment of the spin-offs and newspaper mergers, could materially and adversely affect us.

Certain tax-related restrictions and indemnities set forth in the tax matters agreements agreed to by Scripps, Journal and us in order to maintain the tax-free treatment of the spin-offs and newspaper mergers limit our discretion in the operation of our business and could adversely affect us. Under these provisions, we:

• | have generally undertaken to maintain the current newspaper business of Scripps and Journal as an active business for a period of two years following the completion of the newspaper mergers; |

• | are generally restricted, for a period of two years following the newspaper mergers, from (i) reacquiring our stock, (ii) issuing stock to any person other than as compensation for services, (iii) making changes in equity structure, (iv) liquidating, merging or consolidating certain of our subsidiaries, (v) transferring certain material assets except in the ordinary course of business, and (vi) entering into negotiations with respect to, or consenting to, certain acquisitions of our stock; |

• | are generally restricted from taking any other action (including an action that would be inconsistent with the representations relied upon by Scripps and Journal described above) that could jeopardize the tax-free status of the spin-offs; and |

• | have generally agreed to indemnify Scripps and Journal for taxes and related losses incurred as a result of the spin-offs (other than the spin-off of Journal Spinco, which was taxable to Journal) failing to qualify as tax-free transactions provided such taxes and related losses are attributable to any act, failure to act or omission by us or our subsidiaries, including our failure to comply with applicable representations, undertakings and restrictions placed on our actions under the tax matters agreements. |

11

These prohibitions could discourage, delay or prevent equity financings, acquisitions, investments, strategic alliances, mergers and other transactions, possibly resulting in a material adverse effect on our business. In addition, any indemnity obligations to Scripps or Journal could have a material adverse effect on our financial position and liquidity.

Our credit facility subjects us to various restrictions that could limit operating flexibility.

Our credit facility contains certain covenants and other restrictions that, among other things, requires us to maintain certain financial ratios and restricts our ability to pay dividends, repurchase shares, incur additional indebtedness, make dispositions and create liens. These restrictions and covenants may limit our ability to respond to market conditions, provide for capital investment needs or take advantage of business opportunities by limiting the amount of additional borrowings we may incur.

We may be required to satisfy certain indemnification obligations to our former parent companies or may not be able to collect on indemnification rights from our former parent companies.

Under the terms of the master transaction agreement, Scripps (as successor to Journal) will indemnify us, and we will indemnify Scripps (as successor to Journal), for all damages, liabilities and expenses resulting from a breach by the applicable party of the covenants contained in the master transaction agreement that continue in effect after the April 1, 2015 closing. Scripps (as successor to Journal) will indemnify us for all damages, liabilities and expenses incurred by us relating to the entities, assets and liabilities retained by Scripps or Journal, and we will indemnify Scripps (as successor to Journal) for all damages, liabilities and expenses incurred by us relating to our entities, assets and liabilities.

In addition, Scripps will indemnify us, and we will indemnify Scripps, for all damages, liabilities and expenses resulting from a breach by the other of any of the representations, warranties or covenants contained in the tax matters agreements. We will also indemnify Scripps for all damages, liabilities and expenses arising out of any tax imposed with respect to the Scripps Spinco spin-off if such tax is attributable to any act, any failure to act or any omission by us or any of our subsidiaries. Scripps will indemnify us for all damages, liabilities and expenses relating to pre-closing taxes or taxes imposed on us or our subsidiaries because Scripps Spinco or Journal Spinco was part of the consolidated return of Scripps or Journal, and we will indemnify Scripps for all damages, liabilities and expenses relating to post-closing taxes of ours or our subsidiaries.

The indemnification obligations described above could be significant, although we do not presently believe there are any indemnification obligations for which we will be liable or for which we will seek payment from Scripps. Our ability to satisfy any such indemnities depends upon our future financial performance. Similarly, the ability of Scripps to satisfy any such obligations to us depends on its future financial performance. We cannot assure you that we will have the ability to satisfy any substantial obligations to Scripps or that Scripps (including Scripps as successor to Journal) will have the ability to satisfy any substantial indemnity obligations to us.

Decreases in advertising spending, resulting from economic downturn, war, terrorism, advertiser consolidation or other factors, could adversely affect our financial condition and results of operations.

Approximately 60% of our revenue in 2015 was generated from the sale of local, regional and national advertising appearing in newspapers and shoppers. Advertisers generally reduce their advertising spending during economic downturns and some advertisers may go out of business or declare bankruptcy. The merger or consolidation of advertisers, such as in the banking and airline industries, also generally leads to a reduced amount of collective advertising spending. A recession or economic downturn, as well as a consolidation of advertisers in the future could have an adverse effect on our financial condition and results of operations. Terrorist attacks or other wars involving the United States or any other local or national crisis could also adversely affect our financial condition and results of operations.

Additionally, some of our printed publications generate, and in the future are expected to generate, a large percentage of their advertising revenue from a limited number of sources, including the automotive industry. As a result, even in the absence of a recession or economic downturn, adverse changes specifically affecting these advertising sources could significantly reduce advertising revenue and have a material adverse effect on our financial condition and results of operations.

In addition, advertising revenue and subscription revenue depend upon a variety of other factors specific to the communities that we serve. Changes in those factors could negatively affect those revenues. These factors include, among others, the size and demographic characteristics of the local population, the concentration of retail stores and local economic conditions in general. If the population demographics, prevailing retail environment or local economic conditions of a community to be served by us were to change adversely, revenue could decline and our financial condition and results of operations could be adversely affected.

12

We operate in highly competitive markets, and during a time of rapid competitive changes, we may lose market share and advertising revenue to competing publications, or other competitors, as well as through consolidation of competitors or changes in advertisers' buying strategies.

Our businesses operate in highly competitive markets. Our newspapers, shoppers and Internet sites compete for audiences and advertising revenue with other newspapers, television and radio stations, shoppers and Internet sites as well as with other media such as magazines, outdoor advertising, direct mail and the evolving mobile and digital advertising space. Some of our potential competitors have greater financial, marketing and programming resources than we have or, even if smaller in size or in terms of financial resources, a greater ability to create digital niche products and communities and may respond faster or more aggressively to changing competitive dynamics. This competition has intensified as a result of digital media technologies.

In newspapers and shoppers, our revenue primarily consists of advertising revenue and subscription revenue. Competition for advertising expenditures and subscription revenue comes from local, regional and national newspapers, shoppers, magazines, broadcast and cable television, radio, direct mail, Yellow Pages, digital Internet and mobile products and other media. Competition for newspaper advertising revenue is based largely upon advertiser results, advertising rates, readership, demographics and circulation levels, while competition for subscription revenue is based largely upon the content of the newspaper, its price, editorial quality and customer service. Our local and regional competitors in community publications are typically unique to each market, but we have many competitors for advertising revenue that are larger and have greater financial and distribution resources than us. Subscription revenue and our ability to achieve price increases for our print products are affected by competition from other publications and other forms of media available in our various markets, declining consumer spending on discretionary items like newspapers, decreasing amounts of free time, and declining frequency of regular newspaper buying among young people. We may incur increasing costs competing for advertising expenditures and paid print and digital subscriptions. If we are not able to compete effectively for advertising expenditures and paid print and digital subscriptions, our revenue may decline and our financial condition and results of operations may be adversely affected.

The print newspaper business is in secular decline. Our profitability may be adversely affected if we are not successful in creating other revenue opportunities or in aligning costs with declining revenues.

In recent years, the advertising industry generally has experienced a secular shift toward digital advertising and away from other traditional media. In addition, our historical newspaper circulation has declined, reflecting general trends in the newspaper industry, including consumer migration toward the Internet and other media for news and information. We face, and in the future expect to continue to face, increasing competition from other digital sources for both advertising and subscription revenues. This competition has intensified as a result of the continued development of digital media technologies. Distribution of news, entertainment and other information over the Internet, as well as through smartphones, tablets and other devices, continues to increase in popularity. These technological developments are increasing the number of media choices available to advertisers and audiences. As media audiences fragment, we expect advertisers to continue to allocate larger portions of their advertising budgets to digital media.

In response to the ongoing secular changes, we must continually monitor and align cost structure to declining revenues. The alignment of our costs includes measures such as reduction in force initiatives, standardization and centralization of systems and processes, outsourcing of certain financial processes and the implementation of new software for circulation, advertising and editorial systems.

If we are not successful in creating other revenue opportunities, developing digital media or aligning costs with declining revenues, our profitability could be adversely affected.

We expect a significant portion of operating cost to come from newsprint, so an increase in price or reduction in supplies may adversely affect our operating results.

Newsprint is a significant portion of our operating costs. The price of newsprint has historically been volatile, and increases in the price of newsprint could materially reduce our operating results. In addition, the continued reduction in the capacity of newsprint producers increases the risk that supplies of newsprint could be limited in the future. Our publishing business may suffer if there is a significant increase in the cost of newsprint or a reduction in the availability of newsprint.

Changes relating to consumer information collection and use could adversely affect our ability to collect and use data, which could harm our business.

Public concern over methods of information gathering has led to the enactment of legislation in most jurisdictions that restricts the collection and use of consumer information. Our publishing business relies in part on telemarketing sales, which are affected

13

by “do not call” legislation at both the federal and state levels. We also engage in e-mail marketing and the collection and use of consumer information in connection with our publishing businesses and our growing digital efforts. Further legislation, government regulations, industry regulations, the issuance of judicial interpretations or a change in customs relating to the collection, management, aggregation and use of consumer information could materially increase the cost of collecting that data, or limit our ability to provide information to our customers or otherwise utilize telemarketing or e-mail marketing or distribute our digital products across multiple platforms, and could adversely affect our results of operations.

Decreases in circulation may adversely affect subscription revenues, and circulation decreases may accelerate as we offer expanded digital content and digital subscriptions.

Advertising and subscription revenues are affected by the number of subscribers and single copy purchasers, readership levels and overall audience reach. The newspaper industry as a whole is experiencing difficulty maintaining paid print circulation and related revenues. This is due to, among other factors, increased competition from new media products and sources other than traditional newspapers (often free to consumers), and shifting preferences among some consumers to receive all or a portion of their news other than from a newspaper. In addition, our planned expanded digital content and new digital subscriptions could negatively impact print circulation volumes if readers cancel subscriptions.

A prolonged decrease in circulation could have a material effect on our revenues, particularly if we are not able to otherwise grow readership levels and overall audience reach. To maintain our circulation base, we may incur additional costs, and we may not be able to recover these costs through subscription and advertising revenues.

Changes in the legal and regulatory environment could increase our operating costs or result in litigation.

The conduct of our business is subject to various laws and regulations administered by federal, state and local government agencies. These laws and regulations, as well as judicial and administrative interpretations of these laws and regulations, may change, sometimes dramatically, as a result of political, economic or social events. Such regulatory environment changes may include changes in employment laws, environmental laws, occupational health and safety laws, accounting standards and taxation requirements. Changes in laws, regulations or governmental policy and the related interpretations may alter the environment in which we do business, and therefore, may impact our results or increase our costs or liabilities.

If we are unable to respond to changes in technology and evolving industry standards and trends, our publishing operations may not be able to effectively compete.

The publishing industry is being challenged by the preferences of today’s “on demand” culture, particularly among younger segments of the population. Some consumers prefer to receive all or a portion of their news in new media formats and from sources other than traditional newspapers. Information delivery and programming alternatives such as the Internet, various mobile devices, electronic readers, cable, direct satellite-to-home services, pay-per-view and home video and entertainment systems have fractionalized newspaper readership. New digital subscription offerings may not attract readers in sufficient numbers to generate significant revenues or offset losses in paid print subscription revenues. The shift in consumer behaviors has the potential to introduce new market competitors or change the means by which traditional newspaper advertisers can most efficiently and effectively reach their target audiences. We may not have the resources to acquire new technologies or to introduce new products or services that could compete with these evolving technologies.

We face cybersecurity and similar risks, which could result in the disclosure of confidential information, disruption of our operations, damage to our brands and reputation, legal exposure and financial losses.

Security breaches, computer malware or other “cyber attacks” could harm our business by disrupting our delivery of services, jeopardizing our confidential information and that of our vendors and clients, and damaging our reputation. Our operations routinely involve receiving, storing, processing and transmitting sensitive information. Although we monitor our security measures regularly and believe we are not in a key target industry, any unauthorized intrusion, malicious software infiltration, theft of data, network disruption, denial of service, or similar act by any party could disrupt the integrity, continuity, and security of our systems or the systems of our clients or vendors. These events could create financial liability, regulatory sanction, or a loss of confidence in our ability to protect information, and adversely affect our revenue by causing the loss of current or potential clients.

Risk Factors Relating to Ownership of Our Common Stock

The market price and trading volume of our common stock may be volatile.

14

The market price and trading volume of our common stock could fluctuate significantly for many reasons, including, without limitation:

• | as a result of the risk factors listed in this Annual Report on Form 10-K; |

• | actual or anticipated fluctuations in our operating results; |

• | for reasons unrelated to our specific performance, such as reports by industry analysts, investor perceptions, or negative announcements by our customers or competitors regarding their own performance; and |

• | general economic and industry conditions. |

Certain provisions of our articles of incorporation and bylaws, and provisions of Wisconsin law, could delay or prevent a change of control that you may favor.

Provisions of our articles of incorporation and bylaws may discourage, delay or prevent a merger or other change of control that shareholders may consider favorable or may impede the ability of the holders of our common stock to change our board or management. The provisions of our articles of incorporation and bylaws, among other things:

• | prohibit shareholder action except at an annual or special meeting, thus not allowing our shareholders to act by written consent; |

• | regulate how shareholders may present proposals or nominate directors for election at annual meetings of shareholders by requiring advance notice of such proposals or nominations; |

• | regulate how special meetings of shareholders may be called; and |

• | authorize our board of directors to issue preferred stock in one or more series, without shareholder approval. Under this authority, our board of directors could adopt a rights plan which could ensure continuity of management by rendering it more difficult for a potential acquirer to obtain control of us. |

Our indemnification obligations under the tax matters agreement entered into in connection with the newspaper mergers could prevent a change in control.

An acquisition of our stock or further issuance of our stock could cause Scripps or the shareholders of Scripps or Journal to recognize a taxable gain or income on the spin-off of Scripps Spinco. Under the tax matters agreement we are required to indemnify Scripps or the shareholders of Scripps or Journal, as the case may be, for the resulting tax, and this indemnity obligation might discourage, delay or prevent a change of control that you may consider favorable.

Our ability to pay dividends or repurchase shares is limited by our financial results and our credit facility.

Our credit facility limits our ability to declare and pay dividends or make other distributions on our shares of common stock and limits dividends and share repurchases from borrowed funds to no more than $10 million in any fiscal year. The dividend amounts and share repurchases, if any, will be determined by our board of directors, which will consider a number of factors, including our financial condition, capital requirements, funds generated from operations, future business prospects and applicable contractual restrictions.

Our accounting and other management systems and resources may not be adequate to meet our reporting obligations as a public company.

We are responsible for ensuring that all aspects of our business comply with Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), which requires an annual management assessment of the effectiveness of our internal control over financial reporting. Although our management has experience with these reporting and related obligations, ensuring compliance with respect to our business may place significant demands on management, administrative and operational resources, including accounting systems and resources.

Under the Sarbanes-Oxley Act, we are required to maintain effective disclosure controls and procedures and internal controls over financial reporting. To comply with these requirements, we may need to upgrade our systems; implement additional financial and management controls, reporting systems and procedures; and hire additional accounting and finance staff. We expect to incur

15

additional annual expenses for the purpose of addressing these requirements, and those expenses may be significant. If we are unable to upgrade financial and management controls, reporting systems, information technology systems and procedures in a timely and effective fashion, our ability to comply with our financial reporting requirements and other rules that apply to reporting companies under the Exchange Act could be impaired. Any failure to achieve and maintain effective internal controls could have a material adverse effect on our business, financial condition, results of operations and cash flows.

We are an “emerging growth company,” and we cannot be certain if the reduced reporting requirements applicable to emerging growth companies will make our common stock less attractive to investors.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as we continue to be an emerging growth company, we may take advantage of exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including the exemption from compliance with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation and exemptions from the requirements of holding a non-binding advisory vote on executive compensation. We cannot predict if investors will find our common stock less attractive because we rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile. We will remain an emerging growth company for up to five years, or until the earliest of (a) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (b) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, or (c) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period.

Under the JOBS Act, emerging growth companies can also delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards and, therefore, are subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

Risks Relating to the Proposed Merger with Gannett

On October 7, 2015, we entered into the Merger Agreement with Gannett and Merger Sub. The Merger Agreement provides that, subject to the satisfaction or waiver of specified conditions, Merger Sub will merge with and into us and we will become a wholly owned subsidiary of Gannett. If the merger is completed, our shareholders will receive $12.00 in cash, without interest and less any applicable withholding taxes, for each share of our common stock owned.

Completion of the merger is subject to the satisfaction of certain customary closing conditions. The following risk factors relate to risks posed to our shareholders from the proposed merger.

The merger is subject to conditions, including certain conditions that may not be satisfied or completed on a timely basis, if at all.

Completion of the merger is subject to closing conditions that make the completion and timing of the merger uncertain. The conditions include, among others, the expiration or termination of the waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended (the “HSR Act”); the absence of any law or governmental order enacted or issued prohibiting the merger; since October 7, 2015, there not having occurred any event, occurrence or development that is continuing and that, individually or in the aggregate, has had or would reasonably be expected to have a Company material adverse effect; and the non-modification or withdrawal of the tax opinion delivered by Foley & Lardner LLP to Scripps on October 7, 2015 (relating to the continued tax-free nature of the April 1, 2015 transactions between Scripps and Journal Communications, Inc.) and no change in law or facts having occurred since October 7, 2015 that would make such tax opinion no longer reasonably acceptable to Gannett as of the closing date of the merger.

Although we and Gannett have agreed in the Merger Agreement to use our respective reasonable best efforts to obtain the requisite approvals and consents, there can be no assurance that these approvals and consents will be obtained, and these approvals and consents may be obtained later than anticipated. If permitted under applicable law, either of we or Gannett may waive a condition for its own benefit and consummate the merger even though one or more of these conditions has not been satisfied. Any determination whether to waive any condition will be made by us or Gannett at the time of such waiver based on the facts and circumstances as they exist at that time.

The Merger Agreement contains provisions that restrict our ability to pursue alternatives to the merger and, in specified circumstances, could require us to pay to Gannett a termination fee.

16

Under the Merger Agreement, we are restricted, subject to certain exceptions, from (i) encouraging, soliciting, requesting, initiating or negotiating, or furnishing nonpublic information with regard to, any proposal or offer for a competing acquisition proposal from any person and (ii) withdrawing or modifying our board of directors’ recommendation in favor of the merger or approving or recommending any competing acquisition proposal. We may terminate the Merger Agreement and enter into an agreement with respect to a superior proposal only if specified conditions have been satisfied, including a determination by our board of directors (after having received the advice of a nationally recognized financial advisor and outside legal counsel) that such proposal is more favorable from a financial point of view to our shareholders than the merger. A termination in this instance would result in us being required to pay Gannett a termination fee of $9.0 million. These provisions could discourage a third party that may have an interest in acquiring us from considering or proposing a competing acquisition proposal with us, even if such third party were prepared to pay consideration with a higher value than the value of the merger consideration.

Failure to complete the merger may negatively impact our share price and our future business and financial results.

The Merger Agreement provides that either us or Gannett may terminate the Merger Agreement if the merger is not consummated on or before April 7, 2016, subject to an automatic extension for up to 60 days in order to satisfy the regulatory closing conditions. In addition, the Merger Agreement contains certain termination rights for both us and Gannett including, among others, by us, in the event our board of directors determines to enter into a definitive agreement with respect to a superior proposal. Upon termination of the Merger Agreement under specific circumstances, we will be required to pay Gannett a termination fee of $9.0 million.

If the merger is not completed on a timely basis, our ongoing business may be adversely affected. If the merger is not completed at all, we will be subject to a number of risks, including the following:

• | being required to pay costs and expenses relating to the merger, such as legal and accounting fees and, if applicable, termination fees, whether or not the merger is completed; and |

• | loss of time and resources committed by our management to matters relating to the merger that could have been devoted to pursuing other beneficial opportunities. |

If the merger is not completed, the price of our common stock may decline to the extent that the current market price reflects a market assumption that the merger will be completed, or to the extent there is a market perception that the merger was not consummated due to an adverse change in our business.

We will incur significant costs in connection with the merger.

We expect to pay significant transaction costs in connection with the merger. These costs include investment banking, legal fees and expenses, SEC and HSR Act filing fees, printing expenses, mailing expenses and other related charges. We estimate our aggregate transaction costs will be approximately $8 million to $10 million. A portion of the transaction costs will be incurred regardless of whether the merger is consummated.

While the merger is pending, we are subject to business uncertainties and contractual restrictions under the Merger Agreement that could have an adverse effect on our business.

Prior to the merger, current and prospective employees may experience uncertainty about their future roles and choose to pursue other opportunities, which could have an adverse effect on us. In addition, uncertainty about the effect of the merger on our business relationships may also have an adverse effect on us. These uncertainties could impair our ability to retain and motivate key personnel prior to completion of the merger and could cause third parties who deal with us to seek to change existing business relationships with us. In addition, the Merger Agreement restricts us, without Gannett’s consent and subject to certain exceptions, from making certain acquisitions and taking other specified actions until the merger closes or the Merger Agreement terminates. These restrictions may prevent us from pursuing otherwise attractive business opportunities that may arise prior to completion of the merger or termination of the Merger Agreement, and from making other changes to our business.

Pending litigation against us and Gannett could result in an injunction preventing completion of the merger, the rescission of the merger in the event it is completed and/or the payment of damages in the event the merger is completed.

In connection with the merger, purported shareholders of ours filed two class action lawsuits (which have been consolidated into a single lawsuit) against us, the members of our board of directors, Gannett and the other parties to the Merger Agreement. Among other remedies, the plaintiffs seek to enjoin the merger. As discussed in our Current Report on Form 8-K filed with the Securities and Exchange Commission on February 16, 2016, we entered into a memorandum of understanding with the plaintiffs regarding the settlement of all claims that were or could have been brought in connection with the merger. Pursuant to the terms of the memorandum of understanding, the consolidated lawsuit is currently stayed pending finalization of proposed settlement

17

documentation, confirmatory discovery and a decision by the relevant court regarding approval of the proposed settlement. There can be no assurance that the parties to the memorandum of understanding will ultimately enter into a settlement agreement or that the court will approve the settlement even if the parties were to enter into a settlement agreement.

One of the conditions to the closing of the merger is that no law or judgment, injunction, ruling, order or decree issued by any court of competent jurisdiction shall be in effect that makes the merger illegal or otherwise prohibits the consummation of the merger. If for any reason the consolidated lawsuit is not settled, the litigation may recommence and the plaintiffs may be successful in obtaining an injunction prohibiting us or Gannett from consummating the merger on the agreed-upon terms. In that event, the injunction may prevent the merger from being completed within the expected timeframe, or at all. Furthermore, if the proposed settlement is not approved and the defendants are not able to resolve the consolidated lawsuit, the consolidated lawsuit could result in substantial costs to us, including any costs associated with the indemnification of directors.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

ITEM 2. | PROPERTIES |

We operate in 14 markets in the United States. We believe all properties we own are well maintained, are in good condition and suitable for our operations. There are no material encumbrances on any of these properties. We own substantially all of the facilities and equipment used in our operations.

ITEM 3. | LEGAL PROCEEDINGS |

See Note 16 – Commitments and Contingencies of this Annual Report on Form 10-K for information on legal proceedings.

ITEM 4. | MINE SAFETY DISCLOSURES |

None.

18

PART II

ITEM 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

We are authorized to issue 100 million shares of common stock and 10 million shares of preferred stock and each share of our common stock is entitled to one vote. Our common stock has traded on the New York Stock Exchange (the “NYSE”), under the symbol "JMG," since we began operations as a separate company on April 1, 2015. The following table sets forth, for the periods indicated, the high and low sale prices per share of our common stock as reported on the NYSE.

High | Low | |||||||

Second quarter | $ | 10.79 | $ | 7.60 | ||||

Third quarter | $ | 8.82 | $ | 5.99 | ||||

Fourth quarter | $ | 12.45 | $ | 7.34 | ||||

As of March 23, 2016, there were approximately 1,693 registered holders of our common stock. We have no outstanding shares of preferred stock.

Dividends

We currently intend to distribute a portion of our free cash flow to our common shareholders, through a quarterly dividend, subject to satisfactory financial performance, approval of our board of directors and dividend restrictions in our credit agreement (for additional information, see Note 11 - Long-Term Debt). Our board of directors’ determination regarding dividends will depend on a variety of factors, including earnings, free cash flow generated from operations or other sources, liquidity position and potential alternative uses of cash, as well as economic conditions and expected future financial results. The Merger Agreement with Gannett, effective October 7, 2015, limits our quarterly dividends to $0.06 per share.

Since we began operations as a separate company on April 1, 2015, we paid cash dividends of $0.04 per share on June 5, 2015 and cash dividends of $0.06 per share on September 4, 2015, December 4, 2015 and March 1, 2016.

Securities Authorized For Issuance Under Equity Compensation Plans

See Part III, Item 12, "Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters," of this Annual Report on Form 10-K for certain information regarding our equity compensation plans.

Purchases of Equity Securities

On August 13, 2015, our board of directors authorized a share repurchase program of up to $25 million of our outstanding common stock over 36 months. Under the program, share repurchases may be made at our discretion, from time to time, in the open market and/or in private transactions. Share purchases by us will depend on market conditions, share price, trading volume and other factors. The Merger Agreement with Gannett precludes us from repurchasing shares.

Stock Performance Information

The following information in this Item 5 of this Annual Report on Form 10-K is not deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to the liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed to be incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent we specifically incorporate it by reference into such a filings.

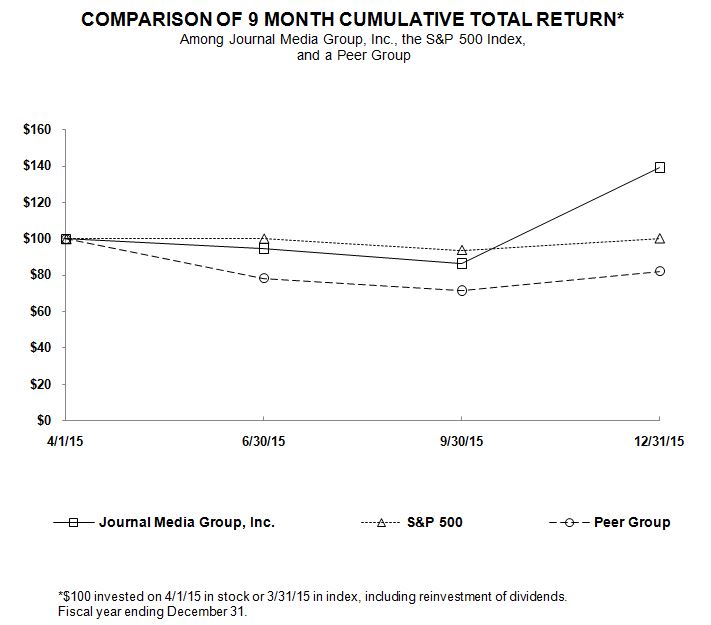

The following graph compares, on a cumulative basis, changes in the total return on our common stock with the total return on the Standard & Poor’s 500 Stock Index and the total return on a peer group comprised of six corporations that concentrate on newspaper publishing in local markets. Our peer group is comprised of A.H. Belo Corp., Gannett Co. Inc., Lee Enterprises Inc., McClatchy Co., New Media Investment Group, Inc., and Tribune Publishing Co. This graph assumes the investment of $100.00 on April 1, 2015, the first day our common stock traded publicly, and the reinvestment of any dividends since that date.

19

4/1/15 | 6/30/15 | 9/30/15 | 12/31/15 | ||

Journal Media Group, Inc. | 100.00 | 94.68 | 86.46 | 139.26 | |

S&P 500 | 100.00 | 100.28 | 93.82 | 100.43 | |

Peer Group | 100.00 | 78.35 | 71.66 | 82.29 | |

20

ITEM 6. | SELECTED FINANCIAL DATA |