Attached files

| file | filename |

|---|---|

| 8-K - HOUSTON AMERICAN ENERGY CORP 8-K 3-29-2016 - HOUSTON AMERICAN ENERGY CORP | form8k.htm |

Exhibit 99.1

Public Investor PresentationMarch 29, 2016 (NYSE MKT: HUSA)

1 Forward-Looking Statements This presentation contains forward-looking statements, including those relating to our future financial and operational results, reserves or transactions, that are subject to various risks and uncertainties that could cause the Company’s future plans, objectives and performance to differ materially from those in the forward-looking statements. Forward-looking statements can be identified by the use of forward-looking terminology such as “may”, “expect,” “intend,” “plan,” “subject to,” “anticipate,” “estimate,” “continue,” “present value,” “future,” “reserves,” “appears,” “prospective,” or other variations thereof or comparable terminology. Factors that could cause or contribute to such differences could include, but are not limited to, those relating to the results of exploratory drilling activity, the Company’s growth strategy, changes in oil and natural gas prices, operating risks, availability of drilling equipment, availability of capital, the inherent variability in early production tests, dependence on weather conditions, seasonality, expansion and other activities of competitors, changes in federal or state environmental laws and the administration of such laws, the general condition of the economy and its effect on the securities market, the availability, terms or completion of any strategic alternative or any transaction and other factors described in “Risk Factors” and elsewhere in the Company’s Form 10-K and other filings with the SEC. While we believe our forward-looking statements are based upon reasonable assumptions, these are factors that are difficult to predict and that are influenced by economic and other conditions beyond our control. The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose proved, probable and possible reserves. We use certain terms in this document, such as non-proven, resource potential, Probable, Possible, Exploration and unrisked resource potential. These terms include reserves , and prospects and leads not rising to the level of or included in reserves, with substantially less certainty than proved reserves, and no discount or other adjustment is included in the presentation of such amounts. The recipient is urged to consider closely the disclosure in our Form 10-K, filed March 18, 2016 available from us at 801 Travis, Suite 1425, Houston, Texas 77002 or our web site. You can also obtain this form from the SEC by calling 1-800-SEC-0330.

Corporate Overview Growth-oriented, exploration and production company with properties in Colombia and the United States, and plans to acquire an interest in an Australian resource development companyBuilding a portfolio of resource based projects with potential significant impact:12.5% direct Working Interest in 392 thousand gross acres in Colombia with planned drilling on Serrania block in 2016Planned 12.5% ownership in Tamboran Resources Ltd., which owns approximately 1.6 million net acres in the heart of Australia’s Beetaloo/McArthur basin shale gas play, among other projectsExperienced Management and Board of DirectorsOperations since 2002, with headquarters in Houston, TexasClean Balance Sheet with No Debt 2

3 Our Oil and Gas Projects Colombia United States Australia

Colombia 4

5 Partnered with Hupecol in Colombia Concessions are all operated by Hupecol Operating, LLC,* a privately held E&P company with offices in Bogota, Colombia and Houston, TexasOperates significant production and gathering facilities in Colombia and domestically in the U.S.Extensive staff of regional managers, geologists, petroleum engineers, and geophysical professionalsHUSA has participated in 123 wells in Colombia with Hupecol since 2003 and has experienced a 67% completion success in those wellsHUSA has a proven track record of monetizing assets with Hupecol realizing $69.9 million in gross proceeds and a ROI of 2.8X capital invested * Hughes Petroleum Colombia (Hupecol) owned by Dan A. Hughes Company, L.P. Source: www.dahughes.net

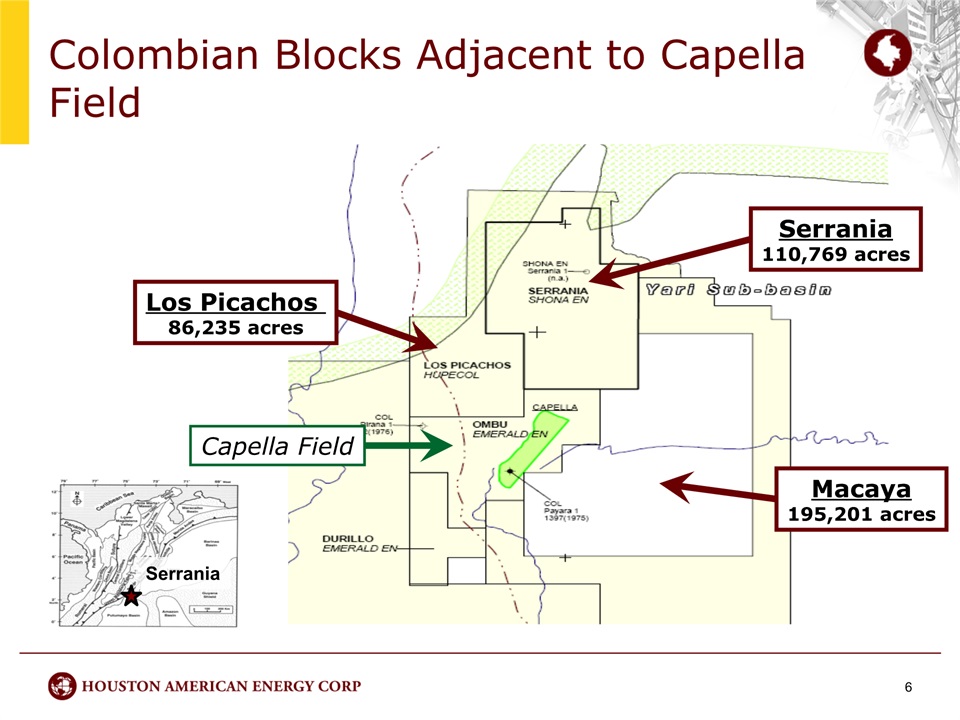

6 Colombian Blocks Adjacent to Capella Field Macaya195,201 acres Serrania110,769 acres Serrania Los Picachos 86,235 acres Capella Field

7 Capella has been a strong producer Discovered in 2008 by Emerald Energy, PLC (90% Operated Working Interest)Emerald was acquired by Sinochem in October 20091.8 billion barrels Original Oil In Place1Gross PV10 @ 12/31/15 approximately $345 million1Latest reported production of 2,200 Bpd from the Mirador Sand at ~3,000’ 2 Source: Canocol Energy owner of 10% non-operated Working Interest in the Capella Field www.canocolenergy.com / www.drillinginfo.com (Oct 2013) Source: Agencia Nacional de Hidrocarburos (referred to as the “ANH”)

Seismic identifies two large prospects on trend with Capella Field HUSA owns 12.5% Working InterestTwo Large ProspectsOn trend with Capella FieldTargeting Mirador SandShallow target sands Significant extension acreage in Macaya and PicachosOil Royalty: 8% to 5,000 Bpd & sliding scale to 20% at 125,000 Bpd South Prospect North Prospect Capella Field 8

9 Seismic interpretation indicates thicker Mirador in Serrania than Capella THIN Capella Field MiradorInterval370 Feet Payara #1 (1975) 60 feet MiradorInterval75 Feet Pirana #1 (1976) 25 feet South Prospect North Prospect THICK

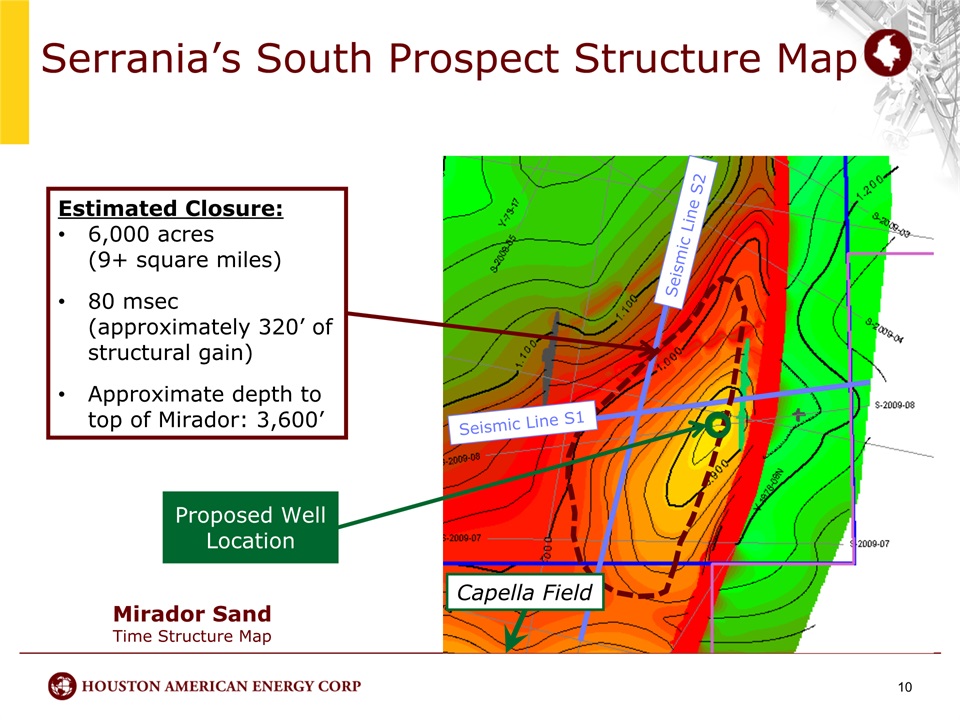

Capella Field Seismic Line S1 Seismic Line S2 10 Serrania’s South Prospect Structure Map Proposed Well Location Estimated Closure:6,000 acres(9+ square miles)80 msec(approximately 320’ of structural gain)Approximate depth totop of Mirador: 3,600’ Mirador SandTime Structure Map

Proposed Well Location Seismic Line N1 Seismic Line N2 Mirador SandTime Structure Map 11 Serrania’s North Prospect Structure Map Estimated Closure:11,000 acres(17+ square miles)45 msec(approximately 180’ of structural gain)Approximate depth totop of Mirador: 4,500’

12 Serrania well expected in 2016 HUSA expects to spud the first Serrania well on the South Prospect in 2016 What does this mean for HUSA?Ushers in a new era of activity in ColombiaAdds significant upside potential with minimal capital outlayConverts an exploratory prospect into a world class field development project Status: waiting on issuance of permits

Continental United States 13

14 U.S. Domestic Activity Partnered with familiar industry operatorsWhite OakPenningtonUnit PetroleumProduction along the Texas and Louisiana Gulf CoastNon-operated working interest in producing wellsContributes cash flow to offset low overheadReviewing distressed opportunities and acquisition candidatesHigh deal flow from HUSA CEO’s background of M&A and restructuring consulting

Australia 15

16 New Plans in Australia Partnering via definitive investment agreement with Tamboran Resources Ltd., announced on February 24th, 2016World class management team at TamboranCompelling acreage position and prospects1.6 million net acres in the Beetaloo/McArthur BasinSuccessful exploration well drilled in 201422.4 million acres in Ngalia, Pedirka, Officer, Birrindudu and ArrowieAustralia is a growing LNG market supplier with proximity to the Asia Pacific marketSydney market undersupplied over long term (LNG prices expected to climb to $8-10 per MMBtu by 2018)*Customary anti-dilution provisionsConditions to be satisfied by Tamboran prior to HUSA’s closingTamboran’s Board ApprovalCompletion of a minimum $500 thousand (max $1.0 million) additional capital raise Source: ANZ Bank analysis referenced in Australian Financial Review article dated July 23, 2015 “Rocketing Gas Prices to Hit Industry Users”.

17 Signed definitive agreement to acquire12.5% equity interest in Tamboran Resources World Class Unconventional Oil & Gas Portfolio, 5-10x growth potentialPotential ~7.6+ TCFE Gross Contingent and Unrisked Prospective Resource (Mid-Velkerri only)* Core assets linked to Asia Pacific LNG market Application of “early stage” U.S. shale expertise; aggressive, catalyst rich development program planned in 2016-18 Strategy focused on aggressive commercialization of Tanumbirini via early cash flow/production *Based on Netherland & Sewell Contingent and Prospective Resources Report dated February 19, 2015; Best Estimate (P50); Net values assume 25% Tamboran working interest (EP 161 and Mid-Velkerri section only)

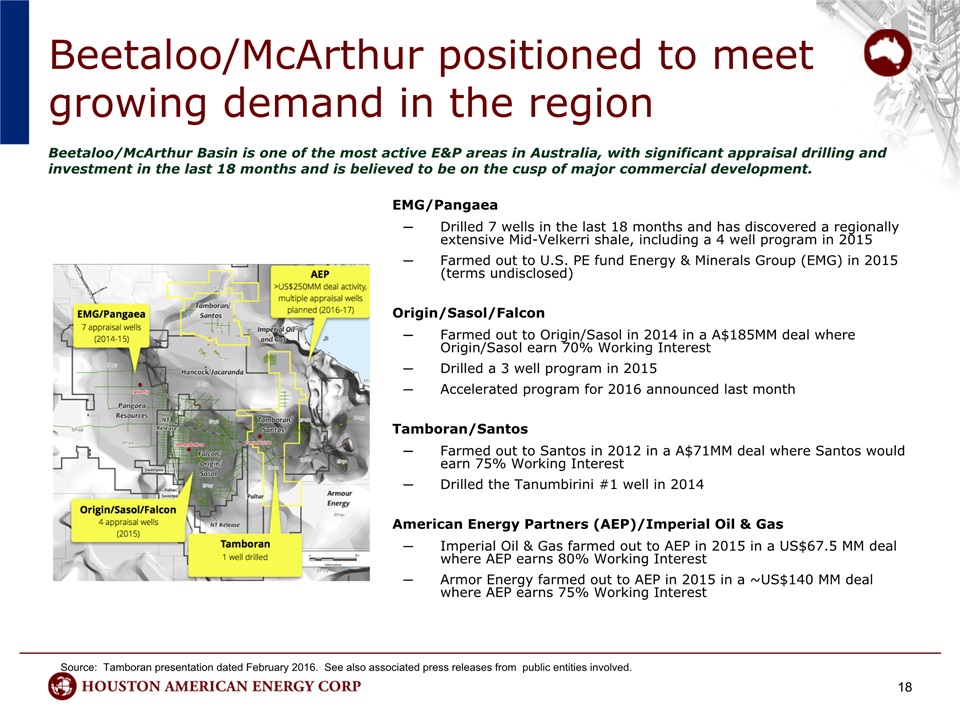

18 Beetaloo/McArthur positioned to meet growing demand in the region EMG/Pangaea Drilled 7 wells in the last 18 months and has discovered a regionally extensive Mid-Velkerri shale, including a 4 well program in 2015 Farmed out to U.S. PE fund Energy & Minerals Group (EMG) in 2015 (terms undisclosed) Origin/Sasol/FalconFarmed out to Origin/Sasol in 2014 in a A$185MM deal where Origin/Sasol earn 70% Working Interest Drilled a 3 well program in 2015 Accelerated program for 2016 announced last monthTamboran/SantosFarmed out to Santos in 2012 in a A$71MM deal where Santos would earn 75% Working Interest Drilled the Tanumbirini #1 well in 2014American Energy Partners (AEP)/Imperial Oil & GasImperial Oil & Gas farmed out to AEP in 2015 in a US$67.5 MM deal where AEP earns 80% Working Interest Armor Energy farmed out to AEP in 2015 in a ~US$140 MM deal where AEP earns 75% Working Interest Beetaloo/McArthur Basin is one of the most active E&P areas in Australia, with significant appraisal drilling and investment in the last 18 months and is believed to be on the cusp of major commercial development. Source: Tamboran presentation dated February 2016. See also associated press releases from public entities involved.

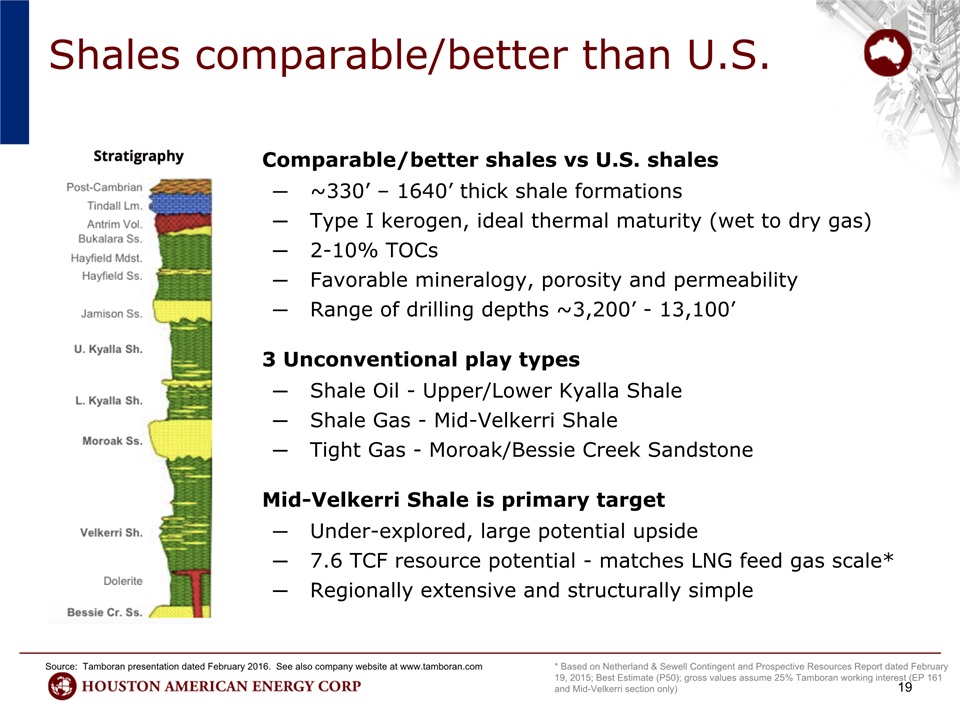

19 Shales comparable/better than U.S. Comparable/better shales vs U.S. shales~330’ – 1640’ thick shale formationsType I kerogen, ideal thermal maturity (wet to dry gas)2-10% TOCsFavorable mineralogy, porosity and permeabilityRange of drilling depths ~3,200’ - 13,100’ 3 Unconventional play types Shale Oil - Upper/Lower Kyalla Shale Shale Gas - Mid-Velkerri ShaleTight Gas - Moroak/Bessie Creek Sandstone Mid-Velkerri Shale is primary target Under-explored, large potential upside 7.6 TCF resource potential - matches LNG feed gas scale* Regionally extensive and structurally simple Source: Tamboran presentation dated February 2016. See also company website at www.tamboran.com * Based on Netherland & Sewell Contingent and Prospective Resources Report dated February 19, 2015; Best Estimate (P50); gross values assume 25% Tamboran working interest (EP 161 and Mid-Velkerri section only)

20 Tamboran’s Beetaloo/McArthur Assets Tamboran currently holds 25% interest* in 3 exploration permitsAcreage covers 1.6 MM net acres of Beetaloo/McArthur Basin, NT, Australia Estimated net recoverable Contingent and Unrisked Prospective Resource potential on EP 161 of 7.6+ TCFE** based on NSAI report (Feb 2015) Joint Venture with Santos (Nov 2012) - $10MM cash to earn ~14% equity stake in Tamboran ($1.50/share) $71MM work program to earn up to 75% working interest and operatorship over 3 years2-D seismic acquired on EP 161 in 2013Tanumbirini #1 (3,950m total depth) successfully drilled and cased in 2014 * Assumes Santos earns alleged 75% working interest of EP 161/162/189, per Joint Venture agreement** Based on Netherland & Sewell Contingent and Prospective Resources Report dated February 19, 2015; Best Estimate (P50); gross values assume 25% Tamboran working interest (EP 161 and Mid-Velkerri section only)

21 Australia’s growing LNG market

22 LNG Expected to Grow Dramatically Through 2040 Natural gas demand projected to rise much faster than overall energy demand40% of global energy demand growth expected to be met by natural gasLNG is expected to meet nearly half of global demand growth through 2040LNG shipments nearly triple to ~100 BcfdAsia Pacific comprises largest demand growth, importing 40% of gas supplies from other regionsAustralia is well positioned to meet growing LNG demand with its Ample resourcesGeographic proximity to importers Source: ExxonMobil 2016 Outlook for Energy

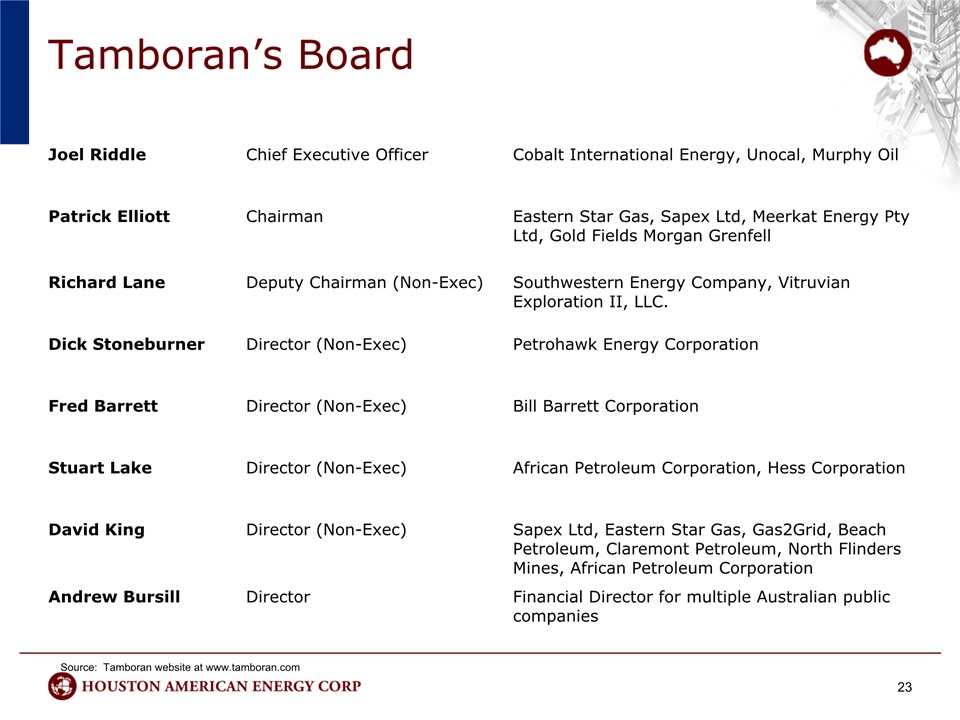

23 Tamboran’s Board Joel Riddle Chief Executive Officer Cobalt International Energy, Unocal, Murphy Oil Patrick Elliott Chairman Eastern Star Gas, Sapex Ltd, Meerkat Energy Pty Ltd, Gold Fields Morgan Grenfell Richard Lane Deputy Chairman (Non-Exec) Southwestern Energy Company, Vitruvian Exploration II, LLC. Dick Stoneburner Director (Non-Exec) Petrohawk Energy Corporation Fred Barrett Director (Non-Exec) Bill Barrett Corporation Stuart Lake Director (Non-Exec) African Petroleum Corporation, Hess Corporation David King Director (Non-Exec) Sapex Ltd, Eastern Star Gas, Gas2Grid, Beach Petroleum, Claremont Petroleum, North Flinders Mines, African Petroleum Corporation Andrew Bursill Director Financial Director for multiple Australian public companies Source: Tamboran website at www.tamboran.com

Value Creation Potential in Australia Tamboran’s Beetaloo/McArthur 6.4 million gross acreage position provides HUSA with opportunity for substantial value creation Additional upside potential in Tamboran’s 22.4 million acres in Ngalia, Pedirka, Officer, Birrindudu and Arrowie 24

25 Corporate - Financial Summary * Traded on NYSE MKT Exchange: HUSAMarket Cap (3/22/16): $10.4 million$2.10 million Cash **$0.07 million Total Liabilities (No Debt)$5.50 million Stockholder’s EquityNo Preferred Stock. No Warrants.Common shares outstanding: 52.0 million (3/8/16)Float approximately 40.0 millionInsider ownership 11.6 million (22%)Options outstanding 4.4 million @ $2.46Fully diluted O/S 56.4 million * Unless otherwise noted, information is as of 12/31/15. ** $1 million is committed to the Tamboran investment and approximately $425k budgeted for Serrania during 2016.

Management and Board 26 ChairmanJohn P. Boylan CEO and President since April 2015, member of Board since 2006. Held positions as CEO, CFO and CRO of numerous energy companies in E&P (onshore and offshore) and oilfield services. Early career experience with KPMG Peat Marwick and Coopers & Lybrand. Licensed CPA with BBA, Accounting from the University of Texas and an MBA with majors in Finance, Economics and International Business from New York University.DirectorsR. Keith Grimes President – International division of Sierra Hamilton, an international service provider to oil and gas exploration and production companies offering specialized technical consulting and E&P technology to operators worldwide. Formerly CEO of predecessor company, Hamilton Group and with Expro Group in eastern hemisphere. Stephen P. Hartzell Co-Owner of Southern Star Exploration, LLC, an independent oil and gas exploration company. Formerly an independent Consulting Geologist and held various geological positions with Amoco Production Company, Tesoro Petroleum Corporation, Moore McCormack Energy and American Hunter Exploration.Roy W. Jageman Over 25 years of experience in energy finance, mergers and acquisitions with Simmons & Co., Lehman Brothers, Solomon Brothers and Wasserstein Perella. Former CFO of Plantation Petroleum Company, Ranger Gas Storage, and Encore Acquisition Company, a publicly traded exploration and production company. O. Lee Tawes Private investor. Formerly Head of Investment Banking and a Director of Northeast Securities, Inc.. Previous management and research analyst positions with C.E. Unterberg, Towbin, Oppenheimer & Co. Inc., CIBC World Markets and Goldman Sachs & Co. from 1972 to 2001.

27 Investment Highlights NYSE MKT listedLarge shareholder base: approx. 5,000 Strong operating partners with excellent track recordsAnticipated near term goal to commence drilling on Colombian prospectsPlans to acquire an impactful position in the Beetaloo/MacArthur basin in Northern Territory, Australia via Tamboran investmentManagement experienced in E&P and acquisitionsReviewing domestic U.S. opportunitiesNo debt = no pressure

28 Thank You