Attached files

| file | filename |

|---|---|

| EX-21.1 - EXHIBIT 21.1 - Energous Corp | v433541_ex21-1.htm |

| EX-31.1 - EXHIBIT 31.1 - Energous Corp | v433541_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - Energous Corp | v433541_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - Energous Corp | v433541_ex32-1.htm |

| EX-10.21 - EXHIBIT 10.21 - Energous Corp | v433541_ex10-21.htm |

| EX-23.1 - EXHIBIT 23.1 - Energous Corp | v433541_ex23-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2015

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________________ to __________________

Commission file number: 001-36379

| ENERGOUS CORPORATION | ||

| (Exact Name of Registrant as Specified in Its Charter) | ||

Delaware |

46-1318953 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

| 3590 North First Street, Suite 210, San Jose, CA | 95134 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

(408) 963-0200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Securities registered pursuant to Section 12 (g) of the Act: Common Stock, par value $0.001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act): Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $84,664,580. Solely for the purposes of this calculation, shares held by directors, executive officers and 10% owners of the registrant have been excluded. Such exclusion should not be deemed a determination or an admission by the registrant that such individuals are, in fact, affiliates of the registrant.

As of March 10, 2016, there were 16,409,739 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A within 120 days after the end of the fiscal year ended December 31, 2015. Portions of such proxy statement are incorporated by reference into Part III of this Form 10-K.

ENERGOUS CORPORATION

TABLE OF CONTENTS

As used in this Form 10-K, unless the context otherwise requires the terms “we,” “us,” “our,” and “Energous” refer to Energous Corporation, a Delaware corporation.

| 1 |

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that are intended to be covered by the “safe harbor” created by those sections. Forward-looking statements, which are based on certain assumptions and describe our future plans, strategies and expectations, can generally be identified by the use of forward-looking terms such as “believe,” “expect,” “may,” “will,” “should,” “could,” “seek,” “intend,” “plan,” “estimate,” “anticipate” or other comparable terms. All statements other than statements of historical facts included in this Annual Report on Form 10-K regarding our strategies, prospects, financial condition, operations, costs, plans and objectives are forward-looking statements. Examples of forward-looking statements include, among others, statements we make regarding proposed services, market opportunities and acceptance, expectations for revenues, cash flows and financial performance, intentions for the future and the anticipated results of our development efforts. Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: our ability to develop a commercially feasible technology; receipt of necessary regulatory approval; our ability to find and maintain development partners, market acceptance of our technology, the amount and nature of competition in our industry; our ability to protect our intellectual property; and the other risks and uncertainties described in the Risk Factors and in Management's Discussion and Analysis of Financial Condition and Results of Operations sections of this Annual Report on Form 10-K and our subsequently filed Quarterly Reports on Form 10-Q. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

Overview

We are developing a technology called WattUp® that consists of proprietary semiconductor chipsets, software, hardware designs and antennas that can enable RF-based wire-free charging for electronic devices, providing power at a distance and ultimately enabling charging with mobility under full software control. Our anticipated business model is to supply silicon components with reference designs and license our WattUp technology to device and chip manufacturers, wireless service providers and other commercial partners to make wire-free charging an affordable, ubiquitous and convenient option for end users. We believe our proprietary technology can potentially be utilized in a variety of devices, including wearables, Internet of Things (“IoT”) devices, smartphones, tablets, e-book readers, keyboards, mice, remote controls, rechargeable lights, cylindrical batteries and any other device with similar charging requirements that would otherwise need a battery or a connection to a power outlet.

We believe our technology is novel in its approach, in that we are developing a solution that charges electronic devices by surrounding them with a contained three dimensional (“3D”) radio frequency (“RF”) energy pocket (“RF energy pocket”). We are engineering solutions that we expect to enable the wire-free transmission of energy from multiple WattUp transmitters to multiple WattUp receiving devices within a range of up to fifteen (15) feet in radius or in a circular charging envelope of up to thirty (30) feet. We are also developing our transmitter technology to seamlessly mesh, (much like a network of WiFi routers) to form a wire-free charging network that will allow users to charge their devices as they walk from room-to-room or throughout a large space. To date, we have developed multiple transmitter prototypes in various form factors and power capabilities. We have also developed multiple receiver prototypes including smartphone battery cases, toys, fitness trackers, Bluetooth headsets as well as stand-alone receivers.

When the company was first founded, we recognized the need to build and design an enterprise-class network management and control system (“NMS”) that was integral to the architecture and development of our wire-free charging technology. Our NMS system can be scaled up to control an enterprise consisting of thousands of devices or scaled down to work in a home or IoT environment.

The power, distance and mobility capabilities of the WattUp technology were validated independently by Underwriters Laboratories (UL) in October, 2015 and the results published on both the UL and the Energous websites.

| 2 |

Our technology solution consists principally of transmitter and receiver application specific standard product (“ASSPs”) and novel antenna designs driven through innovative algorithms and software applications. We submitted our first ASSP design for wafer fabrication in November 2013 and have since then been developing multiple generations of transmitter and receiver ASSPs, multiple antenna designs, as well as algorithms and software designs that we believe, in the aggregate, will optimize our technology by reducing size and cost, while increasing performance to a level that will enable our technology to be integrated into a broad spectrum of devices. We have developed a “building block” approach which allows us to scale our product implementations by combining multiple transmitter building blocks and/or multiple receiver building blocks to provide the power, distance, size and cost performance necessary to meet application requirements. While the technology is very scalable, in order to provide the necessary strategic focus to grow the company effectively, we have defined our market as devices that require 10 watts or less of power to charge. We will continue to invest in ASSP development as well as in the other components of the WattUp system to improve product performance, efficiency, cost-performance and miniaturization as required to grow the business and expand the ecosystem while also distancing us from any potential competition.

We believe that if our development, regulatory and commercialization efforts are successful, our transmitter and receiver technology will support a broad spectrum of charging solutions ranging from contact-based charging or charging at distances of no more than a few centimeters (“nearfield”) to charging at distances of up to 15 feet (“farfield”).

In February of 2015 we signed a Development and License Agreement with one of the top consumer electronic companies in the world based on total worldwide revenues. The agreement is milestone-based and, while there are no guarantees that the WattUp® technology will ever be integrated into our strategic partner’s consumer devices, we continue to progress the relationship as evidenced by the achievement of our first revenues in late 2015 from Engineering Services resulting from the achievement of certain milestones under the agreement. We anticipate continued progress with the relationship which we expect will result in additional Engineering Services Revenue and ultimately, if fully executed, significant revenues from royalties based on the WattUp® technology being integrated into products being shipped to the consumer.

In February of 2016 we began delivering evaluation kits to potential licensees to allow their respective engineering and product management departments to test and evaluate our technology. We expect that the testing and evaluations currently taking place will lead to an expansion of our licensing partners and will result in products beginning to be shipped to the consumer in late 2016/early 2017.

We have implemented an aggressive intellectual property strategy and are continuing to pursue patent protection for new innovations. As of March 14, 2016, we had in excess of 250 pending patent and provisional patent applications. Additionally, the U.S. Patent and Trademark Office (or the PTO) has issued our first five patents and notified us of the allowance of three additional patents. In addition to the inventions covered by these patents and patent applications, we have identified a significant number of additional specific inventions we believe are novel and patentable. We intend to file for patent protection for the most valuable of these, as well as for other new inventions that we expect to develop. Our strategy is to continually monitor the costs and benefits of each patent application and pursue those that will best protect our business and expand the core value of the Company.

We have recruited and hired a seasoned management team with both private and public company experience and relevant industry experience to develop and execute our operating plan. In addition, we have identified and hired key engineering resources in the areas of ASSP development, antenna development, hardware, software and firmware engineering as well as integration and testing which will allow us to continue to expand our technology and intellectual property as well as meet the support requirements of our licensees.

Our common stock is quoted on the NASDAQ Capital Market under the symbol “WATT”. As of March 8, 2016 we had 52 full-time employees, 42 of which were engineers. We were incorporated in Delaware in October 2012. Our corporate headquarters is located at 3590 North First Street, Suite 210, San Jose, CA 95134. Our website can be accessed at www.energous.com. The information contained on, or that may be obtained from our website, is not, and shall not be deemed to be, part of this Annual Report on Form 10-K.

Our Technology

The wire-free charging solution we are developing employs transmitter technology that creates a targeted 3D RF energy pocket around a receiving device (which may be mobile or fixed).

| 3 |

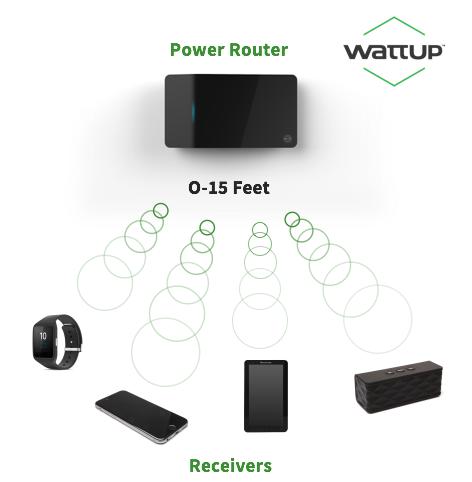

Figure 1 below shows a basic diagram of our solution. Today this solution is able to send RF energy from the transmitter (also referred to as a Power Router) to individual receiver devices in our laboratory.

Figure 1: Our Wire-free Charging Solution Diagram

First, our proprietary power router, or transmitter, locates the receiver(s) in 3-dimensional space via technology we have developed using standard Bluetooth® communications. Next, the transmitter, through software control, generates a controlled and contained RF-waveform to create an RF energy pocket around the receiver(s). We expect that receiver(s) equipped with our antennas and ASSPs and controlled by our software, will be able to harvest power from this contained RF energy pocket. We believe that these receivers will be incorporated into various devices such as smartphones, wearables, fitness trackers, keyboards and mice, cameras, tablets, toys, IoT devices, sensors, remote controls and other small electronics which contain embedded batteries.

Our transmitter uses proprietary software algorithms to dynamically direct, focus and control our RF waveform in three dimensions as it transmits energy to a moving object (such as a user holding their mobile device as they walk around a room).

Our initial demonstration system was able to transmit energy to multiple devices within a range of fifteen (15) feet in radius or in a circular charging envelope of thirty (30) feet. We believe our current generation ASSPs and those in development will also allow us to significantly reduce the size and cost of both our transmitters and our receivers as well as provide increased delivered power and efficiency and faster synchronization speeds.

In January of 2016 we unveiled a new Miniature WattUp Transmitter as well as a small form factor receiver, both of which were developed as a direct result of our efforts to reduce cost and size. The Miniature WattUp Transmitter can offer either contact-based or non contact-based charging. Non contact-based charging allows for low power charging capabilities within a few millimeters or centimeters distance from the miniature transmitter. Due to its low cost and small size, the miniature transmitter is anticipated to be bundled in-box with WattUp-enabled receivers replacing alternative charging solutions like power adapters and charging cables. The ability to bundle and provide a low cost, portable charging solution for receivers provides portability to the WattUp solution and is anticipated to accelerate the ecosystem build out.

| 4 |

Our Competition

There are numerous existing and commercially available methods to provide charging for battery-powered fixed and mobile devices, including wall plug-in charging, inductive charging, magnetic resonance charging, charging stations and more. To our knowledge, almost all mobile consumer electronic devices equipped with a rechargeable battery come bundled with a method to charge the device (for example, a power cord). Studies indicate that the consumer has grown tired and frustrated with tethered charging solutions and that the market is poised and will be receptive to untethered wire-free power solutions like WattUp developed by Energous Corporation. We believe that the positive market response and interest in the WattUp technology we have seen suggests that consumer electronic companies that develop products incorporating our technology will generate incremental sales and realize highly differentiated competitive advantages.

We believe our WattUp technology has a number of advantages compared to traditional charging technologies in terms of size, cost, mobility and portability. Further, our technology allows us to target a fixed or mobile device, track that device if it moves or is moving, and transmit focused energy to the targeted device to charge the device without having to remove the battery or plug in the device. However, there are a variety of other wireless charging technologies on the market or under development today. These competitive technologies fall into the following categories:

Magnetic Induction. Magnetic induction uses a magnetic coil to create resonance, which can transmit energy over very short distances. Power is delivered as a function of coil size (the larger the coil, the more power), and coils must be directly paired (one receiver coil to one transmitter coil = directly coupled pair) within a typical distance of less than one inch. Products utilizing magnetic induction have been available for 10+ years in products such as rechargeable electronic toothbrushes.

Magnetic Resonance. Magnetic resonance is similar to magnetic induction, as it uses magnetic coils to transmit energy. This technology uses coils that range in size depending on the power levels being transmitted. It has the ability to transmit power at distances up to ~11 inches (30cm) which can be increased with the use of resonance repeaters.

Conductive. Conductive charging uses conductive power transfer to eliminate wires between the charger (often a charging mat) and the charging device. It requires the use of a charging board as the power transmitter to deliver the power, and a charging device, with a built-in receiver, to receive the power. This technology requires direct metal contact between the charging board and the receiver. Once the charging board recognizes the receiver, the charging begins.

RF Harvesting. Harvesting RF energy is at the core of our WattUp technology. RF harvesting typically utilizes directional antennas to target and deliver energy. To our knowledge, there are two other companies attempting to utilize a directional pocket of energy similar to that being developed by Energous.

Laser. Laser charging technology uses very short wavelengths of light to create a collimated beam that maintains its size over distance, using what is described as distributed resonance to deliver power to an optical receiver.

Ultrasound. Ultrasound charging technology converts electric energy into acoustic energy in the form of ultrasound waves. It then reconverts those waves through an “energy-harvesting” receiver.

Our Business Strategy

We intend to be both a supplier of our proprietary ASSPs and a licensor of our antenna designs, software and hardware designs to companies who design, manufacture (or contract for manufacture) and market devices to consumers, military, industrial and other users who would benefit from wire-free charging. We intend to pursue these paths because we believe there are several verticals with total available markets measured in the tens of millions of units per year that would benefit from our technology and, as a result, will purchase our proprietary ASSPs and pay us a royalty for licensing our technology. Our intent is not to compete with our strategic partners by designing and manufacturing competing consumer electronic products, but rather to support the development and proliferation of the WattUp® technology to form a ubiquitous wire-free charging ecosystem along the lines of Wi-Fi.

| 5 |

We believe that our greatest market opportunity lies in creating a ubiquitous ecosystem for wire-free charging at a distance, in much the same way as the Wi-Fi ecosystem has developed. The goal is to ensure interoperability between transmitters and receivers that are based on our technology, regardless of who made them, installed them into finished goods, or marketed them. The implementation of previous ubiquitous solutions such as Wi-Fi and Bluetooth should help to illustrate our goal. For example, Wi-Fi routers, regardless of their designer or manufacturer, work with Wi-Fi receivers installed in various consumer electronic devices, regardless of the manufacturer. As a result, we are following the same roll out strategy as Wi-Fi in that we have:

| • | Carefully selected initial target markets; |

| • | Built multiple silicon-based chips to advance the technology; |

| • | Partnered with leading product companies; |

| • | Developed reference designs to reduce early adopter risks and foster adoption; |

| • | Provided game-changing benefits to the consumer in terms of utility and convenience; |

| • | Designed initial iterations of the technology to be small but scalable implementations that are compatible on both a local and enterprise scale; |

| • | Invested in ease of use; |

| • | Developed a strategy to build out the ecosystem starting with the consumer and expanding to enterprise, industrial and military; |

| • | Implemented a plan to initially sell ASSPs migrating to a combination of selling ASSPs and integrating our device libraries into third-party silicon such as Bluetooth Low Energy and Power Management Chips; and |

| • | Supported an association like the Air Fuel Alliance (AFA) that is expected to lead to a qualification process to insure compatibility of the WattUp technology across vendors and develop a common user experience at the application level. |

In order for our solution to become a ubiquitous solution for charging at a distance, we intend to pursue an ecosystem strategy for our technology, engaging not only potential licensees for our transmitter and receiver technologies, but also their upstream and downstream value chain partners. We also intend to prioritize protecting our intellectual property portfolio, as we believe this strategy will make it less likely that a competing platform will be able to gain a solid foothold in the uncoupled wireless market and compete with our technology in a meaningful way.

We believe strategic relationships with key licensees will enable us to reap the benefits of our technology much faster and with greater penetration than by manufacturing and distributing products ourselves. We believe this business model will also allow us to concentrate our efforts and resources on future projects to accelerate the introduction and adoption of the WattUp solution. As we develop new applications for our technology, we expect to target new strategic relationships in different market sectors.

In order to engage with potential licensees of the WattUp technology we have developed evaluation kits consisting of a transmitter and a receiver along with the enabling software to allow potential strategic partners to test the technology in their labs. The kits form a base “building block” component that is scalable to meet the needs of specific applications. We are developing processes and the support capabilities to assist potential strategic partners as they evaluate the technology and develop specific designs to incorporate it.

In selecting our initial licensees, our goal is to identify partners who are willing to make a significant engineering investment in the integration of the technology and have an internal product cycle that will support rapid deployment with the end goal to release WattUp devices to the consumer as quickly as possible thereby securing a first to market advantage and accelerating the path to revenue and profitability.

Since we are developing a new paradigm as to how consumers will charge their mobile devices and other consumer electronics products, the operational details of our strategy continue to evolve as our technology matures and our engagements with strategic partners solidify. As a result, we expect to make operational course corrections as we steer the company towards our goal of a ubiquitous wirefree charging solution. For example, we may enable third party technology companies to support second and third tier licensing opportunities as a way to expand Energous’ scope and accelerate adoption as opposed to trying to expand our internal support capabilities at a cost and pace sufficient to meet the needs of what we anticipate will be strong demand for our technology.

| 6 |

Our Initial Target Markets

We believe that our technology will be compelling to many end markets, each of which may have several potential customers. In an effort to focus our activities and deliver a WattUp-enabled product to the consumer as quickly as possible, we will likely select certain initial target markets and strategic partners because of their time-to-market capabilities and their market potential. As we continue to develop our technology, we intend to add additional markets and partners to expand our market presence.

We identify our initial target markets within these two hardware categories:

Transmitter Target Markets

We believe our transmitters will be developed and released to the consumer in three basic categories:

| • | Stand-alone transmitters that are either sold independently or bundled as part of a pairing with a WattUp-enabled receiver device; |

| • | Transmitters that are integrated into third party devices like televisions, computer monitor bezels and refrigerator doors; and |

| • | Transmitters that are integrated with Wi-Fi routers to form a single device that provides both connectivity and wire-free power. |

Stand-Alone Transmitters:

Our current plans call for stand-alone transmitters to be released in three separate and distinct categories:

Miniature WattUp Transmitters:

Because of their ease of manufacturing and their relative ease of regulatory approval, we expect that products using our miniature transmitter technology will be the first WattUp enabled products to market. Our miniature transmitters are ideally suited to wearables, IoT devices and other small electronics which require a small form factor receiver and a low cost total charging solution. These small, inexpensive transmitters will likely be USB-powered, and will have a range of zero distance from the transmitter (contact-based) to a few millimeters or centimeters from the transmitter. These solutions will initially be one-to-one (one transmitter to one receiver) with follow-on versions being one to many.

Midsize WattUp Transmitters:

We expect that our Midsize WattUp transmitters will be geared to the desktop and will likely have a range of a few centimeters to three feet from the transmitter. We also intend for the midsize transmitters to have tracking ability to support mobile applications and multiple receiving devices. Likely implementations of midsized WattUp transmitters will include small desktop and nightstand transmitters designed to send low power at distances for accessories and wearables. The same technology may also likely be integrated into third party devices like computer monitor bezels, nightstand consumer electronics, accessories such as 12-volt portable chargers and integrated automotive applications.

Full Size WattUp Transmitters:

Full Size WattUp transmitters are full featured transmitters with the power to charge multiple devices at distances of up to fifteen feet or anywhere within a 30-foot diameter circle. We also expect that full size WattUp transmitters will have the ability to “pair” with other full size WattUp transmitters allowing the user to create a large charging envelope encompassing many different rooms or large spaces while seamlessly providing charging to mobile devices that are moving through the coverage space. Full size WattUp transmitters may also play a significant role in the powering of IoT devices that are fixed such as security cameras and sensors.

| 7 |

Transmitters Integrated into Third Party Devices:

The “building block” core architecture developed for the WattUp technology is ideally suited to a broad spectrum of third party devices like televisions and refrigerator doors. The flexibility of the architecture in terms of size, power, distance, and cost affords Energous licensees the opportunity to match our technology with specific requirements and limitations typically found with complex integrations. For example, the WattUp technology could be integrated into the door of a small refrigerator typically found in college dorm rooms providing charging capabilities to mobile devices anywhere in the room. Further, the “pairing” capabilities of the transmitter technology could enable licensees to develop venue-specific consumer electronics products like integrated televisions that are paired with integrated picture frames to provide mobile charging across a large room such as an airport lounge.

Wi-Fi Routers

We see the combination of the wire-free power router and the Wi-Fi router as a natural integration point and a synergistic application of both technologies. The WattUp wire-free power router shares a number of technical characteristics with Wi-Fi routers in that both devices operate in the airwaves in the unlicensed industrial, scientific and medical (“ISM”) bands, both devices owe their success to the utility and convenience they bring to the consumer, both devices rely on antenna structures to send power and data, and both devices “pair” or provide hand off capabilities which allow for large “enabled” sites similar to a mesh network. We also believe that our 3D pocket-forming technology may enhance the data signal of a Wi-Fi router, which we believe will provide an even stronger value proposition to wireless data router manufacturers. Finally, we plan to collaborate with our tier-one consumer electronics company partner to engage with third party Wi-Fi transmitter companies. Our belief is that through this joint approach we will be able to enhance the marketing and manufacturing of transmitters which in turn would help drive the demand for receiving devices and accelerate the build out of the WattUp ecosystem.

The Wi-Fi router market has two segments: commercial and residential. The key differentiator between these segments is that commercial routers tend to have much more robust security features, including virtual private networks and advanced content filtering. We believe that our technology is applicable to both the commercial and residential Wi-Fi router markets based on the building block capabilities mentioned earlier that will enable the WattUp technology to effectively serve and support both markets.

In addition, the Wi-Fi router market has other key players. These include consumer electronics supply chain firms, including original equipment manufacturers (“OEMs”), original design manufacturers (“ODMs”), component manufacturers and branded consumer electronics firms. We believe that each of these categories of players can help to integrate our technology into a commercially available Wi-Fi router.

An ODM designs products either collaboratively with their customers or on their own and manufactures them for sale to companies under the end customer’s brand. Additionally, an ODM may engage multiple companies with similar designs that are then marketed under several different end customers’ brands. An OEM manufactures products for sale under another firm’s brand. We believe that engaging with both types of organizations will be necessary to speed our entry into the market and extend our market reach.

We have ongoing interest from various ODM companies that are exploring the production of the recently announced (January 2016) miniature WattUp transmitter. This miniaturized transmitter design is intended to replace the typical USB cord and power adapter included with many small electronics products today. Incorporation of the WattUp® technology into a mini transmitter would allow the intended product to become waterproof as there is no longer a need for a power input port on the device, while still allowing for an in-box charging solution.

Component suppliers are also a key part of our go-to-market strategy, as most ODMs and OEMs do not design their own components. We expect to be actively engaged with component companies that supply antennas, as well as mixed-signal, power and RF components to the major ODM and OEMs in the Wi-Fi router market.

| 8 |

As part of our go-to-market strategy, we intend to market to major infrastructure developers, both for consumer and commercial applications. Within these consumer markets, we expect that engagements will primarily be with consumer product companies who manufacture and market products to major residential home builders. For commercial installations, we intend to engage with the wireless network operators and private Wi-Fi system operators. We also intend to engage with concentrated consumer destinations (for example, coffee shop and restaurant chains, airport lounges and airports) by educating them on the benefits of our solutions to drive them to seek out and demand our solution from their vendors and suppliers.

Receiver Target Markets

We believe there are a wide variety of potential uses for our receiver technology, including:.

| • | Smart phones |

| • | Wearable devices |

| • | IOT devices |

| • | Tablets |

| • | Mice |

| • | Gaming consoles and controllers |

| • | Keyboards |

| • | e-book readers |

| • | Remote controls |

| • | Sensors (such as thermostats) |

| • | Toys |

| • | Rechargeable batteries |

| • | Rechargeable lights |

| • | Automotive accessories |

| • | Personal care products (such as toothbrushes or shavers) |

| • | Retail inventory management (such as RFID tags) |

| • | Hand-held industrial devices (such as scanners or keypads) |

This list is meant for illustrative purposes only; we cannot guarantee that we will address any of these markets, and we may decide to address a market that is not on the above list. We intend to continuously evaluate our target markets and choose new markets based on factors including (but not limited to) time-to-market, market size and growth, and the strength of our value proposition for a specific application.

Key Strategic Partnership

In January 2015, we signed a Development and License Agreement with a tier-one consumer electronics company to embed WattUp wire-free charging receiver technology in various products including mobile consumer electronics and related accessories.

This Development and License Agreement and subsequent amendments contains both invention and development milestones that we will need to achieve through fiscal 2016 and potentially beyond. If we achieve such milestones, we are entitled to receive milestone-based development payments under the agreement.

During the development phase until one year after the first customer shipment, we will afford this customer a time to market advantage in the licensed product categories.

This agreement was amended in July of 2015 to include transmitter technology which we believe is a key to expanding the WattUp ecosystem given the numbers of transmitters this strategic partner could potentially distribute to the consumer.

We believe that this agreement, and the close collaboration with our partner it entails, will enable us to accelerate commercial development on a number of fronts. If successful, we believe this agreement also paves a very clear path to attaining critical mass in the market for WattUp® wire-free power. We believe that this critical mass could be driven first by the wide adoption of our receiver technology and second by the broad distribution of bundled stand-alone and integrated transmitters into other consumer electronics devices. Finally, having this wide adoption on both the transmitter and the receiver side should create pull and demand for broad adoption of our technology from circles outside of our key strategic partner. With the goal of promoting the establishment of a wire-free charging ecosystem based on the WattUp® technology, we, and this partner, plan to collaborate to introduce WattUp® technology to potential partner companies including router and accessory manufacturers.

Research and Development

Research and development costs account for a substantial portion of our operating expenses. Our research and development expenses were $18.8 million, $12.5 million and $2.1 million for the years ended December 31, 2015, 2014 and 2013, respectively. Research and development expenses are expected to increase in the future as we concentrate our efforts and resources on the commercialization of our technology.

Our Intellectual Property

As a company with a primary focus on licensing, we expect that our most valuable asset will be our intellectual property. This includes U.S. and foreign patents, patent applications and know-how. We are pursuing an aggressive intellectual property strategy and are developing new patents. As of March 14, 2016, we have in excess of 250 pending patent and provisional patent applications. Additionally, the PTO has issued our first five patents and notified us of the allowance of three additional patents. In addition to the inventions covered by these patents and patent applications, we have identified a significant number of additional specific inventions we believe may be novel and patentable. We intend to file for patent protection for the most valuable of these, as well as for other new inventions that we expect to develop.

Government Regulation

Our wire-free charging technology involves the transmission of power using RF energy waves, which is subject to regulation by the Federal Communications Commission (“FCC”), and may be subject to regulation by other federal, state and local agencies. We believe our technology is safe, and we are consulting with the FCC to establish a process by which devices incorporating WattUp® technology can secure required FCC approvals.

| 9 |

As part of the regulatory approval process, we believe devices incorporating the WattUp® technology will need to obtain approvals under both FCC Part 15 and FCC Part 18. We are confident that our technology allows devices to be approved under Part 15. In addition, because our technology involves the transmission of power greater than the power threshold limits of Part 15, we also expect devices incorporating our technology will need to obtain FCC Part 18 approval. The design of the WattUp® technology is such that we believe we will be able to demonstrate that our power transmissions do not violate current FCC regulations pertaining to human exposure to RF emissions and that WattUp® technology complies with the Part 18 technical requirements. However, to our knowledge, the transmission of power in this manner by a consumer product at the ranges we are proposing has not yet been approved by the FCC. There can be no assurance that the FCC will determine that devices incorporating WattUp® technology are eligible for Part 18 approval, that FCC approval will be able to be obtained for specific devices, or that other governmental approvals will not be required.

Employees

As of March 14, 2016, we had 52 full-time employees. None of these employees are covered by a collective bargaining agreement, and we believe our relationship with our employees is good. We also employ consultants, including technical advisors, on an as-needed basis to supplement existing staff. Consultants and technical advisors provide us with expertise in electrical engineering, software development and other specialized areas of engineering and science.

We are subject to various risks that may materially harm our business, prospects, financial condition and results of operations. This discussion highlights some of the risks that may affect future operating results. These are the risks and uncertainties we believe are most important for you to consider. We cannot be certain that we will successfully address these risks. If we are unable to address these risks, our business may not grow, our stock price may suffer and we may be unable to stay in business. Additional risks and uncertainties not presently known to us, which we currently deem immaterial or which are similar to those faced by other companies in our industry or business in general, may also impair our business, prospects, results of operations and financial condition. The risks discussed below include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements.

Risks Related to Our Business

Other than Engineering Services revenues, we have no history of generating revenue, have a history of operating losses, and we may never achieve or maintain profitability.

We have a limited operating history upon which investors may evaluate our prospects. Other than Engineering Services revenues, we have not generated any revenues to date and we have a history of losses from operations. As of December 31, 2015, we had an accumulated deficit of $78,707,180, that included accumulated expense of $26,265,177 from changes in value of derivative liabilities and, accumulated stock based compensation expense of $8,515,540. Our ability to achieve material revenue-generating operations and, ultimately, achieve profitability will depend on whether we can obtain additional capital when we need it, complete the development of our technology and incorporate that technology into the products sold by our customers. There can be no assurance that we will ever generate revenues or achieve profitability.

Terms of our Development and License Agreement with a tier-one consumer electronics company could inhibit potential licensees from working with us in specific markets.

We have entered into a Development and License Agreement with a tier-one consumer electronics company to embed WattUp® wire-free charging receiver technology in various products including mobile consumer electronics and related accessories. This agreement provides our strategic partner a time-to-market advantage during the development until one year after the first customer shipment for certain consumer products. The time-to-market advantage might inhibit another potential licensee from engaging with us or they may be pressured to seek other solutions which could have a negative impact on our future revenue opportunities.

| 10 |

Our efforts may never demonstrate the feasibility of our technology.

We have developed a working prototype of our technology but significant additional research and development activity will be required before we achieve a commercial product. Our research and development efforts remain subject to all of the risks associated with the development of new products based on emerging technologies, including without limitation unanticipated technical or other problems, the inability to develop a product that may be sold at an acceptable price point and the possible insufficiency of funds needed in order to complete development of these products and enable us to render services. Technical problems may result in delays and cause us to incur additional expenses that would increase our losses. If we cannot complete, or if we experience significant delays in developing our technology, and products and services based on such technology, for use in potential commercial applications, particularly after incurring significant expenditures, our business may fail. In particular, to our knowledge, the technological concepts we are applying to develop commercial applications of wire-free power for fixed and mobile low-power rechargeable devices have not been previously successfully applied by anyone else, if we fail to develop a practical, efficient or economical commercial product based on those technological concepts, our business may fail.

We may not obtain FCC approval for our technology and existing laws or regulations or future legislative or regulatory changes may affect our business.

Our wire-free charging technology involves the transmission of power using RF energy waves, which are subject to regulation by the FCC, and may be subject to regulation by other federal, state and local agencies. We intend to design our technology so that it will operate primarily in the 2.4/5.8 GHz radio frequency range, which is the same range as Wi-Fi routers and several other wireless consumer electronics. Different customer applications may require us to develop our technology to work at different frequencies. For those types of products, the FCC grants what is known as Part 15 approval if, among other things, the human exposure to RF emissions is below certain thresholds. In addition, because our technology involves the transmission of power greater than the power threshold limits of Part 15, we also expect WattUp® devices to need FCC Part 18 approval. To our knowledge, the transmission of power using RF energy waves by a consumer product at the ranges we are proposing has not yet been approved by the FCC, and there can be no assurance that devices incorporating WattUp® technology will be able to obtain FCC approval or that other governmental approvals will not be required. Our efforts to cause the FCC to establish a procedure for the authorization of devices using WattUp® technology by their manufacturers could be costly and time consuming, and if such manufacturers are unable to receive any such required approvals in a timely and cost-efficient manner our business and operating results may be materially adversely affected. The cost of compliance with new laws or regulations governing our technology or future products could adversely affect our financial results. New laws or regulations may impose restrictions or obligations on us that could force us to redesign our technology under development or other future products, and may impose restrictions that are not possible or practicable to comply with, which could cause our business to fail. We cannot predict the impact on our business of any legislation or regulations related to our technology or future products that may be enacted or adopted in the future.

We anticipate future losses and negative cash flow, and it is uncertain if or when we will become profitable.

Other than Engineering Services revenues, we have not generated any revenues to date, and we may never be able to produce material revenues or operate on a profitable basis. As a result, we have incurred losses since our inception and expect to experience operating losses and negative cash flow for the foreseeable future.

We expect to expend significant resources on hiring of personnel and startup costs, including payroll and benefits, product and ASSP testing and development, intellectual property development and prosecution, marketing and promotion, capital expenditures, working capital and general and administrative expenses. We expect to incur costs and expenses related to prototype development, consulting costs, laboratory development costs, obtaining regulatory approvals required for our technology and reference product designs, marketing and other promotional activities, hiring of personnel, and the continued development of relationships with strategic business partners. We may not be able to obtain financing in a sufficient amount or at all. We anticipate our losses will continue to increase from current levels during our development stage.

We may require additional financing to achieve our business plans.

We believe our technology is novel in offering the potential to make wire-free charging an affordable, ubiquitous and convenient service for end users. However, the consumer and commercial electronics industry in general and the power, recharging and alternative recharging segments of that industry in particular are subject to intense and increasing competition and rapidly evolving technologies. Accordingly, for our business plans to succeed we believe it will be important for us to move quickly to develop our technology, obtain required regulatory approvals and engage with strategic partners. As a small company, we may be unable to successfully implement our ambitions of targeting very large markets in an intensely competitive industry segment without significantly increasing our resources. We may not have sufficient funds to fully implement our business plan, the ultimate goal of which is to license our technology to device manufacturers, wireless service providers and other commercial partners to make wire-free charging an affordable, ubiquitous and convenient service for end users. While we believe our current cash on hand, together with anticipated payments received under product development projects entered into with customers, will be sufficient to fund our operations into the second quarter of 2017 depending on how soon we are able to begin to generate meaningful commercial revenue we may need to raise capital through new financings. Such financings could include equity financing, which may be dilutive to stockholders, or debt financing, which would likely restrict our ability to borrow from other sources. In addition, such securities may contain rights, preferences or privileges senior to those of the rights of our current stockholders. There can be no assurance that additional funds will be available on terms attractive to us, or at all. If adequate funds are not available, we may be required to curtail the development of our technology or materially curtail or reduce our operations. We could be forced to sell or dispose of our rights or assets. Any inability to raise adequate funds on commercially reasonable terms could have a material adverse effect on our business, results of operation and financial condition, including the possibility that a lack of funds could cause our business to fail and liquidate with little or no return to investors.

| 11 |

We may have difficulty managing growth in our business.

As we expand our activities, there will be additional demands on our financial, technical, operational and management resources. The failure to continue to upgrade our technical, administrative, operating and financial control systems or the occurrence of unexpected expansion difficulties, including issues relating to our research and development activities and retention of experienced scientists, managers and engineers, could have a material adverse effect on our business, financial condition and results of operations and our ability to timely execute our business plan. If we are unable to implement these actions in a timely manner, our results may be adversely affected.

If products incorporating our technology are commercially launched, and those products does not achieve widespread market acceptance, we will not be able to generate the revenue necessary to support our business.

Achieving acceptance of a wire-free recharging system as a preferred method to recharge low-power fixed and mobile electronic devices will be crucial to our continued success. Consumers and commercial customers will not begin to use or increase the use of products incorporating our technology unless they agree that the convenience of our wire-free charging solution would be worth the additional expense of purchasing such products. We have no history of marketing any product and we and our commercialization partners may fail to generate significant interest in the initial commercial products or any other product incorporating our technology that may be developed. These and other factors, including the following factors, may affect the rate and level of the market acceptance:

| • | the price products incorporating our technology relative to other products or competing methods of recharging; |

| • | the effectiveness of our sales and marketing efforts or those of our commercialization partners; |

| • | the support and rate of acceptance of our technology and solutions with our joint development partners; |

| • | perception by users, both individual and enterprise users, of our wire-free charging solution’s convenience, safety, efficiency, and benefits compared to competing methods of recharging; |

| • | press and blog coverage, social media coverage, and other publicity and public relations factors which are not within our control; and |

| • | regulatory developments related to marketing our solution or their inclusion in others’ products. |

If we are unable to achieve or maintain market acceptance, our business would be significantly harmed.

If our products or products incorporating our technology are commercially launched, we may experience seasonality or other unevenness in our financial results in consumer markets or a long and variable sales cycle in enterprise markets.

While we do not now have license revenue or a commercial product, our strategy depends on the development of a successful commercial product and effectively licensing our technology into the consumer, enterprise and commercial markets. We will need to understand procurement and buying cycles to be successful in licensing our technology into those markets. We anticipate it is possible that demand for our technology could vary similarly with the market for products with which our technology may be used, for example, the market for new purchases of laptops, tablet, mobile phones, gaming systems, toys, wearables and the like. Such consumer markets are often seasonal, with peaks in and around the December holiday season and the August-September back-to-school season. Enterprises and commercial markets may have annual or other budgeting and buying cycles that could affect us, and, particularly if we are designated as a capital improvement project, we may have a long or unpredictable sales cycle.

We may not be able to achieve all the features we seek to include in our technology.

We have developed a prototype of our product concept that displays limited functionality in a laboratory setting. There are a variety of features we seek to include in our technology that we have not yet achieved. For example, while we believe recharging multiple devices on one transmitter at a commercially acceptable level may be possible theoretically, we have not yet achieved these results, even in the laboratory. We believe our research and development efforts will yield additional functionality over time. However, there can be no assurance that we will be successful in achieving all the features we are targeting and our inability to do so may limit the appeal of our technology to consumers.

| 12 |

Use of our technology under development or other future products may require the user to purchase additional products to use with existing devices. To the extent these additional purchases are inconvenient, the adoption of our technology under development or other future products could be slowed, which would harm our business.

For rechargeable devices that will utilize our receiver technology, the technology may be embedded in a sleeve, case or other enclosure. For example, certain products such as remote controls or toys equipped with replaceable AA size or other sized batteries, would need to be outfitted with enhanced batteries and other hardware that would enable the devices to be rechargeable by our system. In each case, to use a device with our system, an end user will be required to retrofit the device with a receiver and may be required to upgrade the battery technology used with the device (unless, for example, a consumer electronics supply chain firm has built compatible battery technology and a receiver into the device). These additional steps and expenses may offset the convenience for some users and discourage some users from purchasing our technology under development or other future products. Such factors may inhibit adoption of our technology, which would harm our business. We have not developed the enhanced battery to be used in devices, and our ability to enable use of our technology with devices that will require an enhanced battery will depend on our ability to develop a commercial version of such an enhanced battery that could be manufactured at a reasonable cost. If we fail to develop or enable a commercially practicable enhanced battery, we expect our business would be harmed, and we may need to change our strategy and target markets.

Laboratory conditions differ from field conditions, which could affect the effectiveness of our technology under development or other future products. Failures to effectively move from laboratory to the field would harm our business.

Our technology, when used in the field, may not be able to match the observations, developments, test results and performance that our technology may be able to achieve (and we may be able to document) under controlled laboratory circumstances. As one example of the difference between ideal laboratory conditions and field use, consider that in the laboratory, we can arrange for the transmitter to have line-of-sight transmission to a receiver. If we intend to test the performance through obstructions, we can control the configurations of the obstructions and the materials from which such obstructions are made. In the field, however, the receiver may be obscured or obstructed, or placed around a corner. Also, in the field we will have no control over the configuration of the obstructions or the materials that comprise each obstruction. These conditions may significantly decrease or eliminate the power received at the receiver or the effective range, because the RF energy from the transmitter may be absorbed by obscuring or blocking material or may need to be reflected off of a surface to reach the receiver, making the transmission distance longer than straight-line distances. The failure of our technology under development or other future products to be able to meet the demands of users in the field would harm our business.

Safety concerns and legal action by private parties may affect our business.

We believe that our technology is safe. However, it is possible that we could discover safety issues with our technology or that some people may be concerned with wire-free transmission of power in a manner that has occurred with some other wireless technologies as they were put into residential and commercial use, such as the safety concerns that were raised by some regarding the use of cellular telephones and other devices to transmit data wirelessly in close proximity to the human body. While we plan to at least partially address this potential concern by developing our management software and sensor technology to be configurable by users to selectively recharge devices in ways that would be intended to avoid recharging in close proximity to a human body, such as recharging only during predetermined time periods or recharging only when the device is not moving, we do not plan to conduct any tests to determine whether RF waves produce harmful effects on humans or other animals. We may be unable to effectively prevent recharging in close proximity to a user’s body, which could affect the marketability of our technology or could result in requests for law or regulation governing our technology under development or a class of products in which our technology under development would be included. In addition, while we believe our technology is safe, users of our technology under development or other future products who suffer medical ailments may blame the use of products incorporating our technology, as occurred with a small number of users of cellular telephones. A discovery of safety issues relating to our technology would have a material adverse effect on our business and any legal action against us claiming our technology caused harm could be expensive, divert management and adversely affect us or cause our business to fail, whether or not such legal actions were ultimately successful.

| 13 |

Our industry is subject to intense competition and rapid technological change, which may result in products or new solutions that are superior to our technology under development or other future products we may bring to market from time to time. If we are unable to anticipate or keep pace with changes in the marketplace and the direction of technological innovation and customer demands, our technology and products may become less useful or obsolete and our operating results will suffer.

The consumer and commercial electronics industry in general and the power, recharging and alternative recharging segments of that industry in particular are subject to intense and increasing competition and rapidly evolving technologies. Because products incorporating our technology are expected to have long development cycles, we must anticipate changes in the marketplace and the direction of technological innovation and customer demands. To compete successfully, we will need to demonstrate the advantages of our products and technologies over well-established alternative solutions, products and technologies, as well as newer methods of power delivery and convince consumers and enterprises of the advantages of our products and technologies. Traditional wall plug-in recharging remains an inexpensive alternative to our technology under development. Also, directly competing technologies such as inductive charging, magnetic resonance charging, conductive charging, ultrasound and other yet unidentified solutions may have greater consumer acceptance than the technologies we have developed. Furthermore, certain competitors may have greater resources than us and may be better established in the market than we are. We cannot be certain which other companies may have already decided to or may in the future choose to enter our markets. For example, consumer electronics products companies may invest substantial resources in wireless power or other recharging technologies and may decide to enter our target markets. Successful developments of competitors that result in new approaches for recharging could reduce the attractiveness of our products and technologies or render them obsolete.

Our future success will depend in large part on our ability to establish and maintain a competitive position in current and future technologies. Rapid technological development may render our technology under development or future products based on our technology obsolete. Many of our competitors have or may have greater corporate, financial, operational, sales and marketing resources, and more experience in research and development than we have. We cannot assure you that our competitors will not succeed in developing or marketing technologies or products that are more effective or commercially attractive than our products or that would render our technologies and products obsolete. We may not have or be able to raise or develop the financial resources, technical expertise, marketing, distribution or support capabilities to compete successfully in the future. Our success will depend in large part on our ability to maintain a competitive position with our technologies.

Our competitive position also depends on our ability to:

| • | generate widespread awareness, acceptance and adoption by the consumer and enterprise markets of our technology under development and future products; |

| • | design a product that may be sold at an acceptable price point; |

| • | develop new or enhanced technologies or features that improve the convenience, efficiency, safety or perceived safety, and productivity of our technology under development and future products; |

| • | properly identify customer needs and deliver new products or product enhancements to address those needs; |

| • | limit the time required from proof of feasibility to routine production; |

| • | limit the timing and cost of regulatory approvals; |

| • | attract and retain qualified personnel; |

| • | protect our inventions with patents or otherwise develop proprietary products and processes; and |

| • | secure sufficient capital resources to expand both our continued research and development, and sales and marketing efforts. |

If our technology is not competitive based on these or other factors, our business would be harmed.

It is difficult and costly to protect our intellectual property and our proprietary technologies, and we may not be able to ensure their protection.

Our success depends significantly on our ability to obtain, maintain and protect our proprietary rights to the technologies used in our products and products incorporating our technologies. Patents and other proprietary rights provide uncertain protections, and we may be unable to protect our intellectual property. For example, we may be unsuccessful in defending our patents and other proprietary rights against third party challenges.

| 14 |

We have in excess of 250 pending U.S. patents and provisional patent applications on file. The PTO issued our first five patents and notified us of the allowance of three additional patents to protect our technology.

In addition to patents, we expect to rely on a combination of trade secrets, copyright and trademark laws, nondisclosure agreements and other contractual provisions and technical security measures to protect our intellectual property rights. These measures may not be adequate to safeguard our technology. If they do not protect our rights adequately, third parties could use our technology, and our ability to compete in the market would be reduced. Although we are attempting to obtain patent coverage for our technology where available and where we believe appropriate, there are aspects of the technology for which patent coverage may never be sought or received. We may not possess the resources to or may not choose to pursue patent protection outside the United States or any or every country other than the United States where we may eventually decide to sell our future products. Our ability to prevent others from making or selling duplicate or similar technologies will be impaired in those countries in which we have no patent protection. Although we have in excess of 250 pending and provisional patent applications on file in the United States protecting aspects of our technology under development, our patents may not issue as a result of those applications drawing priority or otherwise based on those patent applications, may issue only with limited coverage or may issue and be subsequently successfully challenged by others and held invalid or unenforceable.

Similarly, even if patents do issue based on our applications or future applications, any issued patents may not provide us with any competitive advantages. Competitors may be able to design around our patents or develop products that provide outcomes comparable or superior to ours. Our patents may be held invalid or unenforceable as a result of legal challenges by third parties, and others may challenge the inventorship or ownership of our patents and pending patent applications. In addition, if we choose to and are able to secure protection in countries outside the United States, the laws of some foreign countries may not protect our intellectual property rights to the same extent as do the laws of the United States. In the event a competitor infringes upon our patent or other intellectual property rights, enforcing those rights may be difficult and time consuming. Even if successful, litigation to enforce our intellectual property rights or to defend our patents against challenge could be expensive and time consuming and could divert our management’s attention. We may not have sufficient resources to enforce our intellectual property rights or to defend our patents against a challenge.

We may also in the future as one of our strategies to deploy our technology into the market, license patent and other proprietary rights to aspects of our technology to third parties and customers. Disputes with our licensors may arise regarding the scope and content of these licenses. Further, our ability to expand into additional fields with our technologies may be restricted by our existing licenses or licenses we may grant to third parties in the future.

The policies we use to protect our trade secrets may not be effective in preventing misappropriation of our trade secrets by others. In addition, confidentiality agreements executed by our employees, consultants and advisors may not be enforceable or may not provide meaningful protection for our trade secrets or other proprietary information in the event of unauthorized use or disclosure. Litigating a trade secret claim is expensive and time consuming, and the outcome is unpredictable. In addition, courts outside the United States are sometimes less willing to protect trade secrets. Moreover, our competitors may independently develop equivalent knowledge methods and know-how. If we are unable to protect our intellectual property rights, we may be unable to prevent competitors from using our own inventions and intellectual property to compete against us, and our business may be harmed.

We may be subject to patent infringement or other intellectual property lawsuits which may be costly to defend.

Because our industry is characterized by competing intellectual property, we may be sued for violating the intellectual property rights of others. Determining whether a product infringes a patent involves complex legal and factual issues, and the outcome of patent litigation actions is often uncertain. We have not conducted any significant search of patents issued to third parties, and no assurance can be given that third party patents containing claims covering our products, parts of our products, technology or methods do not exist, have not been filed, or could not be filed or issued. Because of the number of patents issued and patent applications filed in our technical areas or fields (including some pertaining specifically to wireless charging technologies), our competitors or other third parties may assert that our products and technology and the methods we employ in the use of our products and technology are covered by United States or foreign patents held by them. In addition, because patent applications can take many years to issue and because publication schedules for pending applications vary by jurisdiction, there may be applications now pending of which we are unaware, and which may result in issued patents that our technology under development or other future products would infringe. Also, because the claims of published patent applications can change between publication and patent grant, there may be published patent applications that may ultimately issue with claims that we infringe. There could also be existing patents that one or more of our technologies, products or parts may infringe and of which we are unaware. As the number of competitors in the market for wire-free power and alternative recharging solutions increases, and as the number of patents issued in this area grows, the possibility of patent infringement claims against us increases. Some of our competitors may be able to sustain the costs of complex patent litigation more effectively than we can because they have substantially greater resources. In addition, any uncertainties resulting from the initiation and continuation of any litigation could have a material adverse effect on our ability to raise the funds necessary to continue our operations.

| 15 |

In the event that we become subject to a patent infringement or other intellectual property lawsuit and if the relevant patents or other intellectual property were upheld as valid and enforceable and we were found to infringe or violate the terms of a license to which we are a party, we could be prevented from selling any infringing products of ours unless we could obtain a license or were able to redesign the product to avoid infringement. If we were unable to obtain a license or successfully redesign, we might be prevented from selling our technology under development or other future products. If there is an allegation or determination that we have infringed the intellectual property rights of a competitor or other person, we may be required to pay damages, or a settlement or ongoing royalties. In these circumstances, we may be unable to sell our products or license our technology at competitive prices or at all, our business and operating results could be harmed.

We could become subject to product liability claims, product recalls, and warranty claims that could be expensive, divert management’s attention and harm our business.

Our business exposes us to potential liability risks that are inherent in the marketing and sale of products used by consumers. We may be held liable if our technology under development now or in the future causes injury or death or are found otherwise unsuitable during usage. Our technology under development incorporates sophisticated components and computer software. Complex software can contain errors, particularly when first introduced. In addition, new products or enhancements may contain undetected errors or performance problems that, despite testing, are discovered only after installation. While we believe our technology is safe, users could allege or possibly prove defects (some of which could be alleged or proved to cause harm to users or others) because we design our technology to perform complex functions involving RF energy, possibly in close proximity to users. A product liability claim, regardless of its merit or eventual outcome, could result in significant legal defense costs. The coverage limits of our insurance policies we may choose to purchase to cover related risks may not be adequate to cover future claims. If sales of products incorporating our technology increase or we suffer future product liability claims, we may be unable to maintain product liability insurance in the future at satisfactory rates or with adequate amounts. A product liability claim, any product recalls or excessive warranty claims, whether arising from defects in design or manufacture or otherwise, could negatively affect our sales or require a change in the design or manufacturing process, any of which could harm our reputation and business, harm our relationship with licensors of our products, result in a decline in revenue and harm our business.

In addition, if a product we or a strategic partner design is defective, whether due to design or manufacturing defects, improper use of the product or other reasons, we or our strategic partners may be required to notify regulatory authorities and/or to recall the product. A required notification to a regulatory authority or recall could result in an investigation by regulatory authorities of products incorporating our technology, which could in turn result in required recalls, restrictions on the sale of such products or other penalties. The adverse publicity resulting from any of these actions could adversely affect the perception of our customers and potential customers. These investigations or recalls, especially if accompanied by unfavorable publicity, could result in our incurring substantial costs, losing revenues and damaging our reputation, each of which would harm our business.

We are subject to risks associated with our utilization of consultants.