Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - HALLMARK FINANCIAL SERVICES INC | v429419_ex21.htm |

| EX-31.B - EXHIBIT 31.B - HALLMARK FINANCIAL SERVICES INC | v429419_ex31b.htm |

| EX-32.A - EXHIBIT 32.A - HALLMARK FINANCIAL SERVICES INC | v429419_ex32a.htm |

| EX-32.B - EXHIBIT 32.B - HALLMARK FINANCIAL SERVICES INC | v429419_ex32b.htm |

| EX-31.A - EXHIBIT 31.A - HALLMARK FINANCIAL SERVICES INC | v429419_ex31a.htm |

| EX-23.A - EXHIBIT 23.A - HALLMARK FINANCIAL SERVICES INC | v429419_ex23a.htm |

| EX-10.23 - EXHIBIT 10.23 - HALLMARK FINANCIAL SERVICES INC | v429419_ex10-23.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended DECEMBER 31, 2015

Or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________________________ to _________________________________

Commission file number 001-11252

Hallmark Financial Services, Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 87-0447375 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

| 777 Main Street, Suite 1000, Fort Worth, Texas | 76102 | |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant's Telephone Number, Including Area Code: (817) 348-1600

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

| Common Stock $.18 par value | Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer”, “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $151.0 million

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date. 19,007,727 shares of common stock, $.18 par value per share, outstanding as of March 10, 2016.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III is incorporated by reference from the Registrant's definitive proxy statement to be filed with the Commission pursuant to Regulation 14A not later than 120 days after the end of the fiscal year covered by this report.

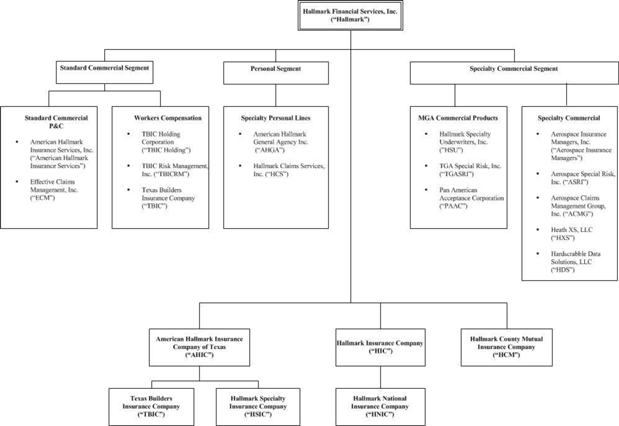

Unless the context requires otherwise, in this Form 10-K the term “Hallmark” refers solely to Hallmark Financial Services, Inc. and the terms “we,” “our,” and “us” refer to Hallmark and its subsidiaries. The direct and indirect subsidiaries of Hallmark are referred to in this Form 10-K in the manner identified in the chart under “Item 1. Business – Operational Structure.”

Risks Associated with Forward-Looking Statements Included in this Form 10-K

This Form 10-K contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, which are intended to be covered by the safe harbors created thereby. Forward-looking statements include statements which are predictive in nature, which depend upon or refer to future events or conditions, or which include words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate” or similar expressions. These statements include the plans and objectives of management for future operations, including plans and objectives relating to future growth of our business activities and availability of funds. Statements regarding the following subjects are forward-looking by their nature:

| · | our business and growth strategies; |

| · | our performance goals; |

| · | our projected financial condition and operating results; |

| · | our understanding of our competition; |

| · | industry and market trends; |

| · | the impact of technology on our products, operations and business; and |

| · | any other statements or assumptions that are not historical facts. |

The forward-looking statements included in this Form 10-K are based on current expectations that involve numerous risks and uncertainties. Assumptions relating to these forward-looking statements involve judgments with respect to, among other things, future economic, competitive and market conditions, legislative initiatives, regulatory framework, weather-related events and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the assumptions underlying these forward-looking statements are reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurance that the forward-looking statements included in this Form 10-K will prove to be accurate. In light of the significant uncertainties inherent in these forward-looking statements, the inclusion of such information should not be regarded as a representation that our objectives and plans will be achieved.

2

PART I

Item 1. Business.

Who We Are

We are a diversified property/casualty insurance group that serves businesses and individuals in specialty and niche markets.

We offer standard commercial insurance, specialty commercial insurance and personal insurance in selected market subcategories that are characteristically low-severity and predominately short-tailed risks. We focus on marketing, distributing, underwriting and servicing property/casualty insurance products that require specialized underwriting expertise or market knowledge. We believe this approach provides us the best opportunity to achieve favorable policy terms and pricing. The insurance policies we produce are written by our six insurance company subsidiaries as well as unaffiliated insurers.

We market, distribute, underwrite and service our property/casualty insurance products primarily through subsidiaries whose operations are organized into product-specific operating units that are supported by our insurance company subsidiaries. Our Standard Commercial P&C operating unit offers industry-specific commercial insurance products and services in the standard market. Our Workers Compensation operating unit specializes in small and middle market workers compensation business. Effective July 1, 2015, this operating unit no longer markets or retains any risk on new or renewal policies. Our MGA Commercial Products operating unit offers commercial insurance products and services in the excess and surplus lines market. Our Specialty Commercial operating unit offers general aviation and satellite launch insurance products and services, low and middle market commercial umbrella and primary/excess liability insurance, medical professional liability insurance products and services, and primary/excess commercial property coverages for both catastrophe and non-catastrophe exposures. Our Specialty Personal Lines operating unit offers non-standard personal automobile and renters insurance products and services.

Each operating unit has its own management team with significant experience in distributing products to its target markets and proven success in achieving underwriting profitability and providing efficient claims management. Each operating unit is responsible for marketing, distribution, underwriting and claims management while we provide capital management, reinsurance, actuarial, investment, financial reporting, technology and legal services and other administrative support at the parent level. We believe this approach optimizes our operating results by allowing us to effectively penetrate our selected specialty and niche markets while maintaining operational controls, managing risks, controlling overhead and efficiently allocating our capital across operating units. We expect future growth to be derived from organic growth in the premium production of our existing operating units and selected opportunistic acquisitions that meet our criteria.

What We Do

We market commercial and personal lines property/casualty insurance products which are tailored to the risks and coverages required by the insured. We believe that most of our target markets are underserved by larger property/casualty insurers because of the specialized nature of the underwriting required. We are able to offer these products profitably as a result of the expertise of our experienced underwriters. We also believe our long-standing relationships with independent general agencies and retail agents and the service we provide differentiate us from larger property/casualty insurers.

Our Standard Commercial P&C operating unit primarily underwrites low-severity, short-tailed commercial property/casualty insurance products in the standard market. These products have historically produced stable loss results and include general liability, commercial automobile, commercial property and umbrella coverages. Our Standard Commercial P&C operating unit currently markets its products through a network of 347 independent agents primarily serving businesses in the non-urban areas of Texas, New Mexico, Oregon, Idaho, Montana, Washington, Utah, Wyoming, Arkansas, Hawaii and Missouri. In addition, our Standard Commercial P&C operating unit offers occupational accident coverage in Texas through an underwriting agency that specializes in the occupational accident insurance market.

Our MGA Commercial Products operating unit primarily offers commercial property/casualty insurance products in the excess and surplus lines market. Excess and surplus lines insurance provides coverage for difficult to place risks that do not fit the underwriting criteria of insurers operating in the standard market. Our MGA Commercial Products operating unit focuses on middle market commercial risks that do not meet the underwriting requirements of standard insurers due to factors such as loss history, number of years in business, minimum premium size and types of business operation. Our MGA Commercial Products operating unit primarily writes commercial automobile, general liability, commercial property and excess casualty. Our MGA Commercial Products operating unit markets its products in 27 states through 9 wholesale brokers, a program underwriter and 89 general agency offices, as well as 110 independent retail agents in Texas and Oregon.

3

Our Specialty Commercial operating unit offers small and middle market commercial excess liability, umbrella and general liability insurance on both an admitted and non-admitted basis; general aviation property/casualty insurance primarily for private and small commercial aircraft and airports; satellite launch property/casualty insurance products; medical professional liability insurance on an excess and surplus lines basis; and primary/excess commercial property coverages on an excess and surplus lines basis for both catastrophe and non-catastrophe exposures. The principal focus of the excess & umbrella insurance products offered is transportation (trucking for hire and specialty automobile coverage). The Specialty Commercial operating unit also provides excess liability coverage for small to midsize businesses in class categories such as contracting, manufacturing, hospitality and service (non-transportation). Typical risks range from one power unit to fleets of up to 200 power units and up to $75M in receipts (non-construction) or $30M in receipts (construction) from operations. Our Specialty Commercial operating unit markets these excess & umbrella products through 132 wholesale brokers in 50 states. The aircraft liability and hull insurance products underwritten by our Specialty Commercial operating unit are targeted to transitional or non-standard pilots who may have difficulty obtaining insurance from a standard carrier. Airport liability insurance is marketed to smaller, regional airports. Our Specialty Commercial operating unit markets these general aviation insurance products through 182 independent specialty brokers in 48 states. The satellite launch property/casualty policies produced by our Specialty Commercial operating unit are marketed through underwriting agencies with technical knowledge of space insurance. We can retain up to $2.0 million per risk for satellite launches and in-orbit coverage for up to 12 months. The medical professional liability insurance underwritten on an excess and surplus basis by our Specialty Commercial operating unit focuses on healthcare professionals that do not meet the underwriting requirements of standard insurers due to factors such as loss history, number of years in business, minimum premium size and types of business operation. Our Specialty Commercial operating unit markets these medical professional liability insurance products through 23 wholesale brokers in 49 states. The primary/excess commercial property coverages underwritten by our Specialty Commercial operating unit specializes in shared and layered accounts on a non-admitted basis which target regional and national property programs. Our Specialty Commercial operating unit markets these products through 60 wholesale brokers in 42 states.

Our Specialty Personal Lines operating unit offers non-standard personal automobile policies, which generally provide the minimum limits of liability coverage mandated by state law to drivers who find it difficult to obtain insurance from standard carriers due to various factors including age, driving record, claims history or limited financial resources. Our Specialty Personal Lines operating unit also provides a renters insurance product that complements our non-standard auto offering and fits well in our distribution channel. During the fourth quarter of 2014, our Specialty Personal Lines operating unit discontinued the low value dwelling/homeowner’s and manufactured homes insurance products it previously offered. Our Specialty Personal Lines operating unit markets these policies through 3,702 independent retail agents in 14 states.

Our insurance company subsidiaries are American Hallmark Insurance Company of Texas (“AHIC”), Hallmark Insurance Company (“HIC”), Hallmark Specialty Insurance Company (“HSIC”), Hallmark County Mutual Insurance Company (“HCM”), Hallmark National Insurance Company (“HNIC”) and Texas Builders Insurance Company (“TBIC”). AHIC, HIC, HSIC and HNIC have entered into a pooling arrangement, pursuant to which AHIC retains 34% of the net premiums written by any of them, HIC retains 32% of the net premiums written by any of them, HSIC retains 24% of the net premiums written by any of them and HNIC retains 10% of the net premiums written by any of them. A.M. Best Company (“A.M. Best”), a nationally recognized insurance industry rating service and publisher, has pooled its ratings of these four insurance company subsidiaries and assigned a financial strength rating of “A–” (Excellent) and an issuer credit rating of “a-” to each of these individual insurance company subsidiaries and to the pool formed by these four insurance company subsidiaries. Also, A.M. Best has assigned a financial strength rating of “A–” (Excellent) and an issuer credit rating of “a-” to HCM. A.M. Best does not assign a financial strength rating or an issuer credit rating to TBIC.

4

These operating units are segregated into three reportable industry segments for financial accounting purposes. The Standard Commercial Segment consists of the Standard Commercial P&C operating unit and the Workers Compensation operating unit. The Specialty Commercial Segment includes our MGA Commercial Products operating unit and Specialty Commercial operating unit, as well as certain specialty risk programs (“Specialty Programs”) which are managed at the parent level. The Personal Segment consists solely of our Specialty Personal Lines operating unit. The following table displays the gross premiums written and net premiums written by these reportable segments for affiliated and unaffiliated insurers for the years ended December 31, 2015, 2014 and 2013.

| Year Ended December 31, | ||||||||||||

| 2015 | 2014 | 2013 | ||||||||||

| (dollars in thousands) | ||||||||||||

| Gross Premiums Written: | ||||||||||||

| Standard Commercial Segment | $ | 81,892 | $ | 84,679 | $ | 87,147 | ||||||

| Specialty Commercial Segment | 351,050 | 324,547 | 296,108 | |||||||||

| Personal Segment | 81,281 | 63,992 | 76,772 | |||||||||

| Total | $ | 514,223 | $ | 473,218 | $ | 460,027 | ||||||

| Net Premiums Written: | ||||||||||||

| Standard Commercial Segment | $ | 71,097 | $ | 76,912 | $ | 79,466 | ||||||

| Specialty Commercial Segment | 241,775 | 230,638 | 235,655 | |||||||||

| Personal Segment | 44,072 | 16,802 | 45,644 | |||||||||

| Total | $ | 356,944 | $ | 324,352 | $ | 360,765 | ||||||

5

Operational Structure

Our insurance company subsidiaries retain a portion of the premiums produced by our operating units. The following chart reflects the operational structure of our organization, including the subsidiaries comprising our operating units and the operating units included in each reportable segment as of December 31, 2015.

Standard Commercial Segment

The Standard Commercial Segment of our business includes our Standard Commercial P&C operating unit and our Workers Compensation operating unit. During 2015, our Standard Commercial P&C operating unit accounted for 92% and our Workers Compensation operating unit accounted for the remaining 8% of the aggregate premiums produced by the Standard Commercial Segment.

Standard Commercial P&C operating unit. Our Standard Commercial P&C operating unit markets, underwrites and services standard commercial lines insurance primarily in the non-urban areas of Texas, New Mexico, Idaho, Oregon, Montana, Washington, Utah, Wyoming, Arkansas, Hawaii and Missouri. The subsidiaries comprising our Standard Commercial P&C operating unit include American Hallmark Insurance Services, a regional managing general agency, and ECM, a claims administration company. American Hallmark Insurance Services targets customers that are in low-severity classifications in the standard commercial market, which as a group have relatively stable loss results. The typical customer is a small to midsize business with a policy that covers property, general liability and automobile exposures. Our Standard Commercial P&C operating unit underwriting criteria exclude lines of business and classes of risks that are considered to be high-severity or volatile, or which involve significant latent injury potential or other long-tailed liability exposures. ECM administers the claims on the insurance policies produced by American Hallmark Insurance Services. In addition, our Standard Commercial P&C operating unit offers occupational accident coverage in Texas through an underwriting agency that is a specialist in the occupational accident insurance market. Products offered by our Standard Commercial P&C operating unit include the following:

6

| · | Commercial automobile. Commercial automobile insurance provides third-party bodily injury and property damage coverage and first-party property damage coverage against losses resulting from the ownership, maintenance or use of automobiles and trucks in connection with an insured’s business. |

| · | General liability. General liability insurance provides coverage for third-party bodily injury and property damage claims arising from accidents occurring on the insured’s premises or from their general business operations. |

| · | Umbrella. Umbrella insurance provides coverage for third-party liability claims where the loss amount exceeds coverage limits provided by the insured’s underlying general liability and commercial automobile policies. |

| · | Commercial property. Commercial property insurance provides first-party coverage for the insured’s real property, business personal property, and business interruption losses caused by fire, wind, hail, water damage, theft, vandalism and other insured perils. |

| · | Commercial multi-peril. Commercial multi-peril insurance provides a combination of property and liability coverage that can include commercial automobile coverage on a single policy. |

| · | Business owner’s. Business owner’s insurance provides a package of coverage designed for small to midsize businesses with homogeneous risk profiles. Coverage includes general liability, commercial property and commercial automobile. | |

| · | Occupational accident. Occupational accident insurance provides an alternative to statutory workers compensation insurance in Texas. Coverage includes medical, short term disability and accidental death and dismemberment. |

Our Standard Commercial P&C operating unit markets its property/casualty insurance products through 347 independent agencies operating in its target markets. Our Standard Commercial P&C operating unit applies a strict agent selection process and seeks to provide its independent agents some degree of non-contractual geographic exclusivity. Our Standard Commercial P&C operating unit also strives to provide its independent agents with convenient access to product information and personalized service. As a result, the Standard Commercial P&C operating unit has historically maintained excellent relationships with its producing agents, as evidenced by the 23 year average tenure of the 16 agency groups that each produced more than $1.0 million in premium during the year ended December 31, 2015. During 2015, the top ten agency groups produced 37%, and no individual agency group produced more than 10%, of the total premium volume of our Standard Commercial P&C operating unit.

Our Standard Commercial P&C operating unit writes most risks on a package basis using a commercial multi-peril policy or a business owner’s policy. Umbrella policies are written only when our Standard Commercial P&C operating unit also writes the insured’s underlying general liability and commercial automobile coverage. Through December 31, 2005, our Standard Commercial P&C operating unit marketed policies on behalf of Clarendon National Insurance Company (“Clarendon”), a third-party insurer. Our Standard Commercial P&C operating unit earns a commission based on a percentage of the earned premium it produced for Clarendon. The commission percentage is determined by the underwriting results of the policies produced. Our Standard Commercial P&C operating unit presently markets all new and renewal policies exclusively for AHIC.

All of the commercial policies written by our Standard Commercial P&C operating unit are for a term of 12 months. If the insured is unable or unwilling to pay for the entire premium in advance, we provide an installment payment plan that requires the insured to pay 20% or 25% down and the remaining payments over eight months. We charge installment fees of up to $7.50 per payment for the installment payment plan.

Workers Compensation operating unit. Effective July 1, 2015, this operating unit no longer markets or retains any risk on new or renewal policies. The subsidiaries comprising our Workers Compensation operating unit included TBIC Holding which has two wholly-owned subsidiaries, TBIC, a Texas domiciled workers compensation insurance carrier and TBICRM, which provided risk management services to customers of TBIC. The run-off of existing policies issued by TBIC is being administered by an independent third party.

7

Specialty Commercial Segment

The Specialty Commercial Segment of our business includes our MGA Commercial Products operating unit and our Specialty Commercial operating unit, as well as certain Specialty Programs which are managed at the parent level. During 2015, our MGA Commercial Products operating unit accounted for 70% of the aggregate premiums produced by the Specialty Commercial Segment, with our commercial umbrella and excess liability, general aviation, medical professional liability, satellite launch and primary/excess commercial property insurance products accounting for 19%, 5%, 2%, 2% and 1%, respectively. Our Specialty Programs accounted for the remaining 1% of the premium produced by the Specialty Commercial Segment during 2015.

MGA Commercial Products operating unit. Our MGA Commercial Products operating unit markets, underwrites, finances and services commercial lines insurance in 27 states with a particular emphasis on commercial automobile, general liability and commercial property risks produced on an excess and surplus lines basis. Excess and surplus lines insurance provides coverage for difficult to place risks that do not fit the underwriting criteria of insurers operating in the standard market. The subsidiaries comprising our MGA Commercial Products operating unit include HSU, which is a regional managing general underwriter, TGASRI which is a Texas managing general agency, and PAAC, which provides premium financing for policies marketed by HSU and certain unaffiliated general and retail agents. HSU accounts for 99% of the premium volume financed by PAAC.

Our MGA Commercial Products operating unit focuses on middle market commercial risks that do not meet the underwriting requirements of traditional standard insurers due to issues such as loss history, number of years in business, minimum premium size and types of business operation. During 2015, commercial automobile, general liability and all other property & casualty accounted for 87%, 9% and 4%, respectively, of the premiums produced by our MGA Commercial Products operating unit. Target risks for commercial automobile insurance are business auto and trucking for hire fleets, excluding hazardous or flammable materials haulers. Target risks for general liability insurance are small business risk exposures including artisan contractors, sales and service organizations, and building and premises liability exposures. Target risks for commercial property insurance are low- to mid-value structures including office buildings, mercantile shops, restaurants and rental dwellings, in each case with aggregate property limits of less than $500,000. The commercial insurance products offered by our MGA Commercial Products operating unit include the following:

| · | Commercial automobile. Commercial automobile insurance provides third-party bodily injury and property damage coverage and first-party property damage coverage against losses resulting from the ownership, maintenance or use of automobiles and trucks in connection with an insured’s business. | |

| · | General liability. General liability insurance provides coverage for third-party bodily injury and property damage claims arising from accidents occurring on the insured’s premises or from their general business operations. | |

| · | Commercial property. Commercial property insurance provides first-party coverage for the insured’s real property, business personal property, theft and business interruption losses caused by fire, wind, hail, water damage, vandalism and other insured perils. Windstorm, hurricane and hail are generally excluded in coastal areas. | |

| · | Commercial excess liability. Commercial excess liability insurance is designed to provide an extra layer of protection for bodily injury, personal and advertising injury, or property damage losses above the primary layer of commercial automobile, general liability and employer’s liability insurance. The excess insurance does not begin until the limits of liability in the primary layer have been exhausted. The excess layer provides not only higher limits, but catastrophic protection from large losses. | |

| · | Commercial umbrella. Commercial umbrella insurance protects businesses for bodily injury, personal and advertising injury, or property damage claims in excess of the limits of their primary commercial automobile, general liability and employers liability policies, and for some claims excluded by their primary policies (subject to a deductible). Umbrella insurance provides not only higher limits, but catastrophic protection for large losses. |

8

Our MGA Commercial Products operating unit markets its products in 27 states through 9 wholesale brokers, a program underwriter and 89 general agency offices, as well as 110 independent retail agents in Texas and Oregon. Our MGA Commercial Products operating unit strives to simplify the placement of its excess and surplus lines policies by providing our general agents with a web rating portal which allows for instantaneous quoting and signature-ready applications which can be emailed or faxed to its independent retail agents. During 2015, general agents produced 79%, the program underwriter produced 15%, retail agents produced 3% and wholesale brokers produced 3% of total premiums produced by our MGA Commercial Products operating unit. During 2015, the top ten general agents produced 37%, the nine wholesale brokers produced 3% and no general agent produced more than 9%, of the total premium volume of our MGA Commercial Products operating unit. During the same period, the top ten retail agents produced 2%, and no retail agent produced more than 1%, of the total premium volume of our MGA Commercial Products operating unit.

Through 2008, all business of our MGA Commercial Products operating unit was produced under a fronting agreement with member companies of the Republic Group (“Republic”), which granted our MGA Commercial Products operating unit the authority to develop underwriting programs, set rates, appoint retail and general agents, underwrite risks, issue policies and adjust and pay claims. We assumed 70% of the risk under this arrangement in 2008. In 2009, our MGA Commercial Products operating unit wrote a portion of its policies under a fronting arrangement with Republic pursuant to which we assumed 100% of the risk. Commission revenue was generated under the fronting agreement on the portion of premiums not assumed by AHIC. An additional commission may be earned if certain loss ratio targets are met. Additional revenue was generated from fully earned policy fees and installment billing fees charged on legacy personal lines products. Since 2010, in states where we were not yet licensed to offer a non-admitted product, we utilized a fronting arrangement with a third party pursuant to which we assumed all of the risk and then retroceded a portion of the risk to third party reinsurers.

The majority of the commercial policies written by our MGA Commercial Products operating unit are for a term of 12 months. Exceptions include certain commercial automobile policies that are written for a term that coincides with the annual harvest of crops and special event general liability policies that are written for the term of the event, which is generally one to two days. Commercial lines policies are paid in full up front or financed with various premium finance companies, including PAAC.

Specialty Commercial operating unit. Our Specialty Commercial operating unit offers small and middle market commercial excess liability, umbrella and general liability insurance on both an admitted and non-admitted basis focusing primarily on trucking, specialty automobile, and non-fleet automobile coverage, general aviation property/casualty insurance primarily for private and small commercial aircraft and airports, satellite launch insurance products, medical professional liability insurance on an excess and surplus lines basis and primary/excess commercial property coverage for both catastrophe and non-catastrophe exposures on an excess and surplus lines basis.

The small and middle market commercial excess liability, umbrella and general liability insurance underwritten by our Specialty Commercial operating unit is offered on an admitted and non-admitted basis in 49 states plus the District of Columbia. Limits of liability offered are from $1,000,000 to $5,000,000 (transportation) and $1,000,000 to $10,000,000 (non-transportation) in coverage in excess of the primary carrier’s limits of liability. The principal focus of the excess & umbrella insurance products offered is transportation, specifically trucking for hire, specialty automobile and non-fleet automobile coverage. The Specialty Commercial operating unit also provides umbrella and excess liability coverage for small to midsize businesses in class categories such as contracting, manufacturing, hospitality and service. The majority of the excess & umbrella and general liability insurance policies written by our Specialty Commercial operating unit are on an annual basis. However, exceptions are common in an attempt to have policy effective dates coincide with those of the primary insurance policies. Policy premiums are due in full 30 days from the inception date of the policy. Our excess & umbrella insurance and general liability insurance products are offered through 132 wholesale brokers. During 2015, the top ten wholesale brokers accounted for 46% of our excess & umbrella and general liability premium volume, with no single wholesale broker accounting for more than 15%. During 2015, commercial transportation excess liability risks accounted for 89% of the premiums, with the remaining 11% coming from non-transportation commercial excess and general liability risks. The commercial excess & umbrella and general liability insurance products offered by our Specialty Commercial operating unit include the following:

| · | Commercial excess liability. Commercial excess liability insurance is designed to provide an extra layer of protection for bodily injury, personal and advertising injury, or property damage losses above the primary layer of commercial automobile, general liability and employer’s liability insurance. The excess insurance does not begin until the limits of liability in the primary layer have been exhausted. The excess layer provides not only higher limits, but catastrophic protection from large losses. | |

| · | Commercial umbrella. Commercial umbrella insurance protects businesses for bodily injury, personal and advertising injury, or property damage claims in excess of the limits of their primary commercial automobile, general liability and employers liability policies, and for some claims excluded by their primary policies (subject to a deductible). Umbrella insurance provides not only higher limits, but catastrophic protection for large losses. |

9

| · | Commercial general liability. General liability insurance provides coverage for third-party bodily injury and property damage claims arising from accidents occurring on the insured’s premises or from their general business operations. |

We generally cede 80% of the excess & umbrella and general liability risk on policies presently written by our Specialty Commercial operating unit.

Our Specialty Commercial operating unit markets, underwrites and services general aviation property/casualty insurance in 48 states. The subsidiaries marketing our general aviation insurance products include Aerospace Insurance Managers, which markets standard aviation coverages, ASRI, which markets excess and surplus lines aviation coverages, and ACMG, which handles claims management. Aerospace Insurance Managers is one of only a few similar entities in the U.S. and has focused on developing a well-defined niche centering on transitional pilots, older aircraft and small airports and aviation-related businesses. In addition, our Specialty Commercial operating unit offers satellite launch property/casualty policies marketed through underwriting agencies with technical knowledge of space insurance. The general aviation and satellite launch products offered by our Specialty Commercial operating unit include the following:

| · | Aircraft. Aircraft insurance provides third-party bodily injury and property damage coverage and first-party hull damage coverage against losses resulting from the ownership, maintenance or use of aircraft. |

| · | Airport liability. Airport liability insurance provides coverage for third-party bodily injury and property damage claims arising from accidents occurring on airport premises or from their operations. | |

| · |

Satellite. We can retain up to $2.0 million per risk for satellite launches and in-orbit coverage for up to 12 months. |

We presently cede 80% of the general aviation risk on policies written by our Specialty Commercial operating unit.

Our Specialty Commercial operating unit distributes its general aviation insurance products through 182 aviation specialty brokers. These specialty brokers submit to Aerospace Insurance Managers requests for aviation insurance quotations received from the states in which we operate and our Specialty Commercial operating unit selectively determines the risks fitting its target niche for which it will prepare a quote. During 2015, the top ten independent specialty brokers produced 32%, and no broker produced more than 5%, of the total general aviation premium volume of our Specialty Commercial operating unit. Our Specialty Commercial operating unit independently develops, underwrites and prices each general aviation coverage written. We target pilots who may lack experience in the type of aircraft they have acquired or are transitioning between types of aircraft. We also target pilots who may be over the age limits of other insurers. We do not accept aircraft that are used for hazardous purposes such as crop dusting or heli-skiing. Liability limits are controlled, with 89% of the aircraft written in 2015 bearing per-occurrence limits of $1,000,000 and per-passenger limits of $100,000 or less. The average insured aircraft hull value for aircraft written in 2015 was approximately $126,000. All general aviation policies produced by our Specialty Commercial operating unit are written through our insurance company subsidiaries.

Our Specialty Commercial operating unit markets medical professional liability insurance on an excess and surplus lines basis. Medical professional liability insurance provides coverage for third-party bodily injury claims resulting from professional services provided by physicians, surgeons, podiatrists and medical entities. Our Specialty Commercial operating unit distributes its medical professional liability insurance products through 23 wholesale brokers in 49 states.

Our Specialty Commercial operating unit markets primary/excess commercial property coverages, on a non-admitted basis, for both catastrophe and non-catastrophe exposures. Our Specialty Commercial operating unit distributes its primary/excess commercial property insurance products through 60 wholesale brokers in 42 states. We presently cede 90% of the primary/excess commercial property risk on policies underwritten by our insurance companies and we receive a fee on the portion of the business written as a cover-holder through a Lloyds Syndicate.

10

Specialty Programs. Our Specialty Programs consist of fronting and agency arrangements which are managed at the parent level. The Specialty Programs business presently consists primarily of a fronting arrangement in Texas for a third party insurance company.

Personal Segment / Specialty Personal Lines operating unit

The Personal Segment of our business consists solely of our Specialty Personal Lines operating unit. Our Specialty Personal Lines operating unit markets and services non-standard personal automobile policies and renters insurance in 14 states. During the fourth quarter of 2014, the Specialty Personal Lines operating unit discontinued the low value dwelling/homeowner’s and manufactured homes insurance products it previously offered. Our Specialty Personal Lines operating unit provides management, policy and claims administration services to HIC and includes the operations of American Hallmark General Agency, Inc. and Hallmark Claims Services, Inc. Our non-standard personal automobile insurance generally provides for the minimum limits of liability coverage mandated by state laws to drivers who find it difficult to purchase automobile insurance from standard carriers as a result of various factors, including driving record, vehicle, age, claims history, or limited financial resources. Products offered by our Specialty Personal Lines operating unit include the following:

| · | Personal automobile. Personal automobile insurance is the primary product offered by our Specialty Personal Lines operating unit. Our policies typically provide third-party coverage to individuals for bodily injury and property damage at the minimum limits required by law, and for physical damage to an insured’s own vehicle from collision and various other perils. In addition, many states require policies to provide for first party personal injury protection, frequently referred to as no-fault coverage. |

| · | Renters. Renters insurance provides coverage for the contents of a renter’s home or apartment and for liability. Renter’s policies are similar to homeowners insurance, except they do not cover the structure. |

We presently cede 50% of the personal automobile risk on policies written by our Specialty Personal Lines operating unit.

Our Specialty Personal Lines operating unit markets its products through 3,702 independent retail agents operating in its target geographic markets. Non-standard automobile represented 98% of the premiums produced during 2015. Our Specialty Personal Lines operating unit qualifies new agent appointments in order to establish an efficient network of independent agents to effectively penetrate its highly competitive markets. Our Specialty Personal Lines operating unit periodically evaluates its independent agents and discontinues the appointment of agents whose production history does not satisfy certain standards. During 2015, the top ten independent agency groups produced 27%, and no individual agency group produced more than 8%, of the total premium volume of our Specialty Personal Lines operating unit.

During 2015, personal automobile liability coverage accounted for 78% and personal automobile physical damage coverage accounted for the remaining 22% of the total non-standard automobile premiums produced by our Specialty Personal Lines operating unit. Our most common policy term is a six month policy. We offer additional terms of one-, two-, three- and twelve-month policies in certain markets. Our typical non-standard personal automobile customer is unable or unwilling to pay a full or half year premium in advance. Accordingly, we currently offer a direct bill program where the premiums are directly billed to the insured on a monthly basis. We charge installment fees for each payment under the direct bill program. Our Specialty Personal Lines operating unit markets its products in 14 states directly for HIC, AHIC, HCM and HNIC.

Our Competitive Strengths

We believe that we enjoy the following competitive strengths:

| · | Specialized market knowledge and underwriting expertise. All of our operating units possess extensive knowledge of the specialty and niche markets in which they operate, which we believe allows them to effectively structure and market their property/casualty insurance products. Our Specialty Personal Lines operating unit has a thorough understanding of the unique characteristics of the non-standard personal automobile market. Our Standard Commercial P&C operating unit has significant underwriting experience in its target market for standard commercial property/casualty insurance products. In addition, our MGA Commercial Products operating unit and Specialty Commercial operating unit have developed specialized underwriting expertise which enhances their ability to profitably underwrite non-standard property/casualty insurance coverages. |

11

| · | Tailored market strategies. Each of our operating units has developed its own customized strategy for penetrating the specialty or niche markets in which it operates. These strategies include distinctive product structuring, marketing, distribution, underwriting and servicing approaches by each operating unit. As a result, we are able to structure our property/casualty insurance products to serve the unique risk and coverage needs of our insureds. We believe these market-specific strategies enable us to provide policies tailored to the target customer that are appropriately priced and fit our risk profile. |

| · | Superior agent and customer service. We believe performing the underwriting, billing, customer service and claims management functions at the operating unit level allows us to provide superior service to both our independent agents and insured customers. The easy-to-use interfaces and responsiveness of our operating units enhance their relationships with the independent agents who sell our policies. We also believe our consistency in offering our insurance products through hard and soft markets helps to build and maintain the loyalty of our independent agents. Our customized products, flexible payment plans and prompt claims processing are similarly beneficial to our insureds. |

| · | Market diversification. We believe operating in various specialty and niche segments of the property/casualty insurance market diversifies both our revenues and our risks. We also believe our operating units generally operate on different market cycles, producing more earnings stability than if we focused entirely on one product. As a result of the pooling arrangement among four of our insurance company subsidiaries, we are able to efficiently allocate our capital among these various specialty and niche markets in response to market conditions and expansion opportunities. We believe this market diversification reduces our risk profile and enhances our profitability. |

| · | Experienced management team. Our senior corporate management has an average of over 20 years of insurance experience. In addition, our operating units have strong management teams, with an average of more than 20 years of insurance industry experience for the heads of our operating units and an average of more than 15 years of underwriting experience for our underwriters. Our management has significant experience in all aspects of property/casualty insurance, including underwriting, claims management, actuarial analysis, reinsurance and regulatory compliance. In addition, Hallmark’s senior management has a strong track record of acquiring businesses that expand our product offerings and improve our profitability profile. |

Our Strategy

We strive to become a “Best in Class” specialty insurance company offering products in specialty and niche markets through the following strategies:

| · | Focusing on underwriting discipline and operational efficiency. We seek to consistently generate an underwriting profit on the business we write in hard and soft markets. Our operating units have a strong track record of underwriting discipline and operational efficiency, which we seek to continue. We believe that in soft markets our competitors often offer policies at a low or negative underwriting profit in order to maintain or increase their premium volume and market share. In contrast, we seek to write business based on its profitability rather than focusing solely on premium production. To that end, we provide financial incentives to many of our underwriters and independent agents based on underwriting profitability. |

| · | Achieving organic growth in our existing business lines. We believe we can achieve organic growth in our existing business lines by consistently providing our insurance products through market cycles, expanding geographically, expanding our product offerings, expanding our agency relationships and further penetrating our existing customer base. We believe our extensive market knowledge and strong agency relationships position us to compete effectively in our various specialty and niche markets. We also believe there is a significant opportunity to expand some of our existing business lines into new geographical areas and through new agency relationships while maintaining our underwriting discipline and operational efficiency. In addition, we believe there is an opportunity for some of our operating units to further penetrate their existing customer bases with additional products offered by other operating units. |

12

| · | Pursuing selected, opportunistic acquisitions. We seek to opportunistically acquire insurance organizations that operate in specialty or niche property/casualty insurance markets that are complementary to our existing operations. We seek to acquire companies with experienced management teams, stable loss results and strong track records of underwriting profitability and operational efficiency. Where appropriate, we intend to ultimately retain profitable business produced by the acquired companies that would otherwise be retained by unaffiliated insurers. Our management has significant experience in evaluating potential acquisition targets, structuring transactions to ensure continued success and integrating acquired companies into our operational structure. |

| · | Maintaining a strong balance sheet. We seek to maintain a strong balance sheet by employing conservative investment, reinsurance and reserving practices and to measure our performance based on long-term growth in book value per share. |

Distribution

We market our property/casualty insurance products predominately through independent general agents, retail agents and specialty brokers. Therefore, our relationships with independent agents and brokers are critical to our ability to identify, attract and retain profitable business. Each of our operating units has developed its own tailored approach to establishing and maintaining its relationships with these independent distributors of our products. These strategies focus on providing excellent service to our agents and brokers, maintaining a consistent presence in our target niche and specialty markets through hard and soft market cycles and fairly compensating the agents and brokers who market our products. Our operating units also regularly evaluate independent general and retail agents based on the underwriting profitability of the business they produce and their performance in relation to our objectives.

Except for the products of our Specialty Commercial operating unit, the distribution of property/casualty insurance products by our operating units is geographically concentrated. For the twelve months ended December 31, 2015, five states accounted for 63% of the gross premiums written by our insurance company subsidiaries. The following table reflects the geographic distribution of our insured risks, as represented by direct and assumed premiums written by our business segments for the twelve months ended December 31, 2015.

| State | Standard Commercial Segment | Specialty Commercial Segment | Personal Segment | Total | Percent of Total | |||||||||||||||

| (dollars in thousands) | ||||||||||||||||||||

| Texas | $ | 29,741 | $ | 188,955 | $ | 21,733 | $ | 240,429 | 46.7 | % | ||||||||||

| Louisiana | - | 24,576 | - | 24,576 | 4.8 | % | ||||||||||||||

| Arizona | - | 1,443 | 20,697 | 22,140 | 4.3 | % | ||||||||||||||

| Oklahoma | - | 8,724 | 9,145 | 17,869 | 3.5 | % | ||||||||||||||

| New Mexico | 8,821 | 997 | 7,584 | 17,402 | 3.4 | % | ||||||||||||||

| All other states | 43,330 | 126,355 | 22,122 | 191,807 | 37.3 | % | ||||||||||||||

| Total gross premiums written | $ | 81,892 | $ | 351,050 | $ | 81,281 | $ | 514,223 | ||||||||||||

| Percent of total | 15.9 | % | 68.3 | % | 15.8 | % | 100.0 | % | ||||||||||||

Underwriting

The underwriting process employed by our operating units involves securing an adequate level of underwriting information, identifying and evaluating risk exposures and then pricing the risks we choose to accept. Each of our operating units offering commercial, healthcare professional or aviation insurance products employs its own underwriters with in-depth knowledge of the specific niche and specialty markets targeted by that operating unit. We employ a disciplined underwriting approach that seeks to provide policies appropriately tailored to the specified risks and to adopt price structures that will be supported in the applicable market. Our experienced commercial, healthcare professional and aviation underwriters have developed underwriting principles and processes appropriate to the coverages offered by their respective operating units.

13

We believe that managing the underwriting process through our operating units capitalizes on the knowledge and expertise of their personnel in specific markets and results in better underwriting decisions. All of our underwriters have established limits of underwriting authority based on their level of experience. We also provide financial incentives to many of our underwriters based on underwriting profitability.

To better diversify our revenue sources and manage our risk, we seek to maintain an appropriate business mix among our operating units. At the beginning of each year, we establish a target net loss ratio for each operating unit. We then monitor the actual net loss ratio on a monthly basis. If any line of business fails to meet its target net loss ratio, we seek input from our underwriting, actuarial and claims management personnel to develop a corrective action plan. Depending on the particular circumstances, that plan may involve tightening underwriting guidelines, increasing rates, modifying product structure, re-evaluating independent agency relationships or discontinuing unprofitable coverages or classes of risk.

An insurance company’s underwriting performance is traditionally measured by its statutory loss and loss adjustment expense ratio, its statutory expense ratio and its statutory combined ratio. The statutory loss and loss adjustment expense ratio, which is calculated as the ratio of net losses and loss adjustment expenses (“LAE”) incurred to net premiums earned, helps to assess the adequacy of the insurer’s rates, the propriety of its underwriting guidelines and the performance of its claims department. The statutory expense ratio, which is calculated as the ratio of underwriting and operating expenses to net premiums written, assists in measuring the insurer’s cost of processing and managing the business. The statutory combined ratio, which is the sum of the statutory loss and LAE ratio and the statutory expense ratio, is indicative of the overall profitability of an insurer’s underwriting activities, with a combined ratio of less than 100% indicating profitable underwriting results.

The following table shows, for the periods indicated, (i) our gross premiums written (in thousands); and (ii) our underwriting results as measured by the net statutory loss and LAE ratio, the net statutory expense ratio, and the net statutory combined ratio of our insurance company subsidiaries.

| Year Ended December 31, | ||||||||||||

| 2015 | 2014 | 2013 | ||||||||||

| Gross premiums written | $ | 514,223 | $ | 473,218 | $ | 460,027 | ||||||

| Net statutory loss & LAE ratio | 65.4 | % | 64.8 | % | 72.2 | % | ||||||

| Net statutory expense ratio | 30.6 | % | 33.1 | % | 34.7 | % | ||||||

| Net statutory combined ratio | 96.0 | % | 97.9 | % | 106.9 | % | ||||||

These statutory ratios do not reflect the deferral of policy acquisition costs, investment income, premium finance revenues, or the elimination of inter-company transactions required by U.S. generally accepted accounting principles (“GAAP”).

The premium-to-surplus percentage measures the relationship between net premiums written in a given period (premiums written, less returned premiums and reinsurance ceded to other carriers) to policyholders surplus (admitted assets less liabilities), determined on the basis of statutory accounting practices prescribed or permitted by insurance regulatory authorities. State insurance department regulators expect insurance companies to maintain a premium-to-surplus percentage of not more than 300%. For the years ended December 31, 2015, 2014 and 2013, our consolidated premium-to-surplus ratios were 144%, 154% and 184%, respectively.

Claims Management and Administration

We believe that effective claims management is critical to our success and that our claims management process is cost-effective, delivers the appropriate level of claims service and produces superior claims results. Our claims management philosophy emphasizes the delivery of courteous, prompt and effective claims handling and embraces responsiveness to policyholders and agents. Our claims strategy focuses on thorough investigation, timely evaluation and fair settlement of covered claims while consistently maintaining appropriate case reserves. We seek to compress the cycle time of claim resolution in order to control both loss and claim handling cost. We also strive to control legal expenses by negotiating competitive rates with defense counsel and vendors, establishing litigation budgets and monitoring invoices.

14

Each of our operating units maintains its own dedicated staff of specialized claims personnel to manage and administer claims arising under policies produced through their respective operations. The claims process is managed through a combination of experienced claims managers, seasoned claims supervisors, trained staff adjusters and independent adjustment or appraisal services, when appropriate. All adjusters are licensed in those jurisdictions for which they handle claims that require licensing. Limits on settlement authority are established for each claims supervisor and staff adjuster based on their level of experience. Certain independent adjusters have limited authority to settle claims. Claim exposures are periodically and systematically reviewed by claim supervisors and managers as a method of quality and loss control. Large loss exposures are reviewed at least quarterly with senior management of the operating unit and monitored by Hallmark senior management.

Claims personnel receive in-house training and are required to attend various continuing education courses pertaining to topics such as best practices, fraud awareness, legal environment, legislative changes and litigation management. Depending on the criteria of each operating unit, our claims adjusters are assigned a variety of claims to enhance their knowledge and ensure their continued development in efficiently handling claims. As of December 31, 2015, our operating units had a total of 100 claims managers, supervisors and adjusters with an average experience of approximately 15 years.

Analysis of Losses and LAE

Our consolidated financial statements include an estimated reserve for unpaid losses and LAE. We estimate our reserve for unpaid losses and LAE by using case-basis evaluations and statistical projections, which include inferences from both losses paid and losses incurred. We also use recent historical cost data and periodic reviews of underwriting standards and claims management practices to modify the statistical projections. We give consideration to the impact of inflation in determining our loss reserves, but do not discount reserve balances.

The amount of reserves represents our estimate of the ultimate cost of all unpaid losses and LAE incurred. These estimates are subject to the effect of trends in claim severity and frequency. We regularly review the estimates and adjust them as claims experience develops and new information becomes known. Such adjustments are included in current operations, including increases and decreases, net of reinsurance, in the estimate of ultimate liabilities for insured events of prior years.

Changes in loss development patterns and claim payments can significantly affect the ability of insurers to estimate reserves for unpaid losses and related expenses. We seek to continually improve our loss estimation process by refining our ability to analyze loss development patterns, claim payments and other information within a legal and regulatory environment that affects development of ultimate liabilities. Future changes in estimates of claim costs may adversely affect future period operating results. However, such effects cannot be reasonably estimated currently.

15

Reconciliation of reserve for unpaid losses and LAE. The following table provides a reconciliation of our beginning and ending reserve balances on a net-of-reinsurance basis for the years ended December 31, 2015, 2014 and 2013, to the gross-of-reinsurance amounts reported in our balance sheets at December 31, 2015, 2014 and 2013.

| As of and for Year Ended December 31 | ||||||||||||

| 2015 | 2014 | 2013 | ||||||||||

| (dollars in thousands) | ||||||||||||

| Reserve for unpaid losses and LAE, net of reinsurance recoverables, January 1 | $ | 323,192 | $ | 312,468 | $ | 263,832 | ||||||

| Provision for losses and LAE for claims occurring in the current period | 237,102 | 215,258 | 251,391 | |||||||||

| (Decrease) increase in reserve for unpaid losses and LAE for claims occurring in prior periods | (6,953 | ) | (5,203 | ) | 9,954 | |||||||

| Payments for losses and LAE, net of reinsurance: | ||||||||||||

| Current period | (83,132 | ) | (76,231 | ) | (101,897 | ) | ||||||

| Prior periods | (122,122 | ) | (123,100 | ) | (110,812 | ) | ||||||

| Reserve for unpaid losses and LAE at December 31, net of reinsurance recoverable | 348,087 | 323,192 | 312,468 | |||||||||

| Reinsurance recoverable on unpaid losses and LAE at December 31 | 102,791 | 91,943 | 70,172 | |||||||||

| Reserve for unpaid losses and LAE at December 31, gross of reinsurance | $ | 450,878 | $ | 415,135 | $ | 382,640 | ||||||

The $7.0 million favorable development, $5.2 million favorable development and $10.0 million unfavorable development in prior accident years recognized in 2015, 2014 and 2013, respectively, represent normal changes in our loss reserve estimates. In 2015 and 2014, the aggregate loss reserve estimates for prior years were decreased to reflect favorable loss development when the available information indicated a reasonable likelihood that the ultimate losses would be less than the previous estimates. In 2013, the aggregate loss reserve estimates for prior years were increased to reflect unfavorable loss development when the available information indicated a reasonable likelihood that the ultimate losses would be more than the previous estimates. Generally, changes in reserves are caused by variations between actual experience and previous expectations and by reduced emphasis on the Bornhuetter-Ferguson method due to the aging of the accident years. (See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Estimates and Judgments - Reserves for unpaid losses and loss adjustment expenses.”)

The $7.0 million decrease in reserves for unpaid losses and LAE recognized in 2015 was attributable to $7.4 million favorable development on claims incurred in the 2014 accident year, $1.5 million unfavorable development on claims incurred in the 2013 accident year and $1.1 million favorable development on claims incurred in the 2012 and prior accident years. Our Standard Commercial P&C operating unit, Workers Compensation operating unit, Specialty Commercial operating unit and our MGA Commercial Products operating unit accounted for $5.4 million, $2.0 million, $2.0 million and $0.2 million, respectively, of the decrease in reserves recognized during 2015. The decrease in reserves for our Standard Commercial P&C operating unit was primarily related to our general liability lines of business. The decrease in reserves for our Workers Compensation operating unit was attributable to the 2014, 2013 and 2012 and prior accident years. The decrease in reserves for our Specialty Commercial operating unit was primarily related to $0.9 million favorable development in our general aviation line of business, $0.8 million favorable development in our medical professional liability products and $0.3 million favorable development in our commercial excess liability line of business. The decrease in reserves in our MGA Commercial Products operating unit primarily related to our commercial auto liability and general liability lines of business. These favorable developments were partially offset by unfavorable development of $2.6 million in our Specialty Personal Lines operating unit primarily attributable to the 2014 accident year.

16

The $5.2 million decrease in reserves for unpaid losses and LAE recognized in 2014 was attributable to $7.2 million favorable development on claims incurred in the 2013 accident year, $4.4 million unfavorable development on claims incurred in the 2012 accident year and $2.4 million favorable development on claims incurred in the 2011 and prior accident years. Our Standard Commercial P&C operating unit, Specialty Personal Lines operating unit, Workers Compensation operating unit and Specialty Commercial operating unit accounted for $4.1 million, $2.9 million, $1.9 million and $1.0 million, respectively, of the decrease in reserves recognized during 2014. The decrease in reserves for our Standard Commercial P&C operating unit was primarily related to our commercial auto and general liability lines of business. The decrease in reserves for our Specialty Personal Lines operating unit was primarily attributable to the 2013 accident year. The decrease in reserves for our Workers Compensation operating unit was attributable to the 2013, 2012 and 2011 and prior accident years. The decrease in reserves for our Specialty Commercial operating unit was primarily related to $0.9 million favorable development in our commercial excess liability line of business and $0.4 million favorable development in our medical professional liability products, partially offset by a $0.3 million unfavorable development in our general aviation line of business. These favorable developments were partially offset by unfavorable development of $4.7 million in our MGA Commercial Products operating unit primarily related to our commercial auto liability and general liability lines of business.

The $10.0 million increase in reserves for unpaid losses and LAE recognized in 2013 was attributable to $5.0 million unfavorable development on claims incurred in the 2012 accident year, $1.7 million unfavorable development on claims incurred in the 2011 accident year and $3.3 million unfavorable development on claims incurred in the 2010 and prior accident years. Our MGA Commercial Products operating unit and Specialty Personal Lines operating unit accounted for $16.0 million and $1.8 million of the increase in reserves recognized during 2013. The increase in reserves for our MGA Commercial Products operating unit was primarily related to commercial auto liability line of business. The increase in reserves for our Specialty Personal Lines operating unit was primarily related to personal auto in the 2012 accident year. These unfavorable developments were partially offset by favorable prior years’ loss development of $3.7 million in our Standard Commercial P&C operating unit, $2.6 million in our Specialty Commercial operating unit and $1.5 million in our Workers Compensation operating unit. The decrease in reserves for our Standard Commercial P&C operating unit was primarily related to commercial auto and general liability lines of business. The decrease in reserves for our Specialty Commercial operating unit was driven by $2.3 million of favorable claims development in the 2011 and prior accident years related to our aircraft liability lines of business, partially offset by $0.1 million unfavorable claims development in the 2012 accident year related to our aircraft hull coverage. Further contributing to the decrease in reserves for our Specialty Commercial operating unit was $0.4 million of favorable claims development in our excess & umbrella lines of business. The decrease in reserves for our Workers Compensation operating unit was related to the 2012 and 2011 accident years.

Analysis of loss and LAE reserve development. The following table shows the development of our loss reserves, net of reinsurance, for years ended December 31, 2005 through 2015. Section A of the table shows the estimated liability for unpaid losses and LAE, net of reinsurance, recorded at the balance sheet date for each of the indicated years. This liability represents the estimated amount of losses and LAE for claims arising in prior years that are unpaid at the balance sheet date, including losses that have been incurred but not yet reported to us. Section B of the table shows the re-estimated amount of the previously recorded liability, based on experience as of the end of each succeeding year. The estimate is increased or decreased as more information becomes known about the frequency and severity of claims.

Cumulative Redundancy/ (Deficiency) (Section C of the table) represents the aggregate change in the estimates over all prior years. Thus, changes in ultimate development estimates are included in operations over a number of years, minimizing the significance of such changes in any one year.

17

ANALYSIS OF LOSS AND LAE DEVELOPMENT

As of and for Year Ended December 31

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | ||||||||||||||||||||||||||||||||||

| A. Reserve for unpaid loss & LAE, net of reinsurance recoverables | $ | 25,997 | $ | 72,801 | $ | 120,849 | $ | 150,025 | $ | 176,250 | $ | 213,723 | $ | 254,901 | $ | 263,832 | $ | 312,468 | $ | 323,192 | $ | 348,087 | ||||||||||||||||||||||

| B. Net reserve re-estimated as of: | ||||||||||||||||||||||||||||||||||||||||||||

| One year later | 24,820 | 66,387 | 119,034 | 151,645 | 185,440 | 230,089 | 251,226 | 273,786 | 307,265 | 316,239 | ||||||||||||||||||||||||||||||||||

| Two years later | 24,903 | 68,490 | 118,646 | 155,155 | 183,689 | 226,856 | 256,198 | 275,778 | 307,793 | |||||||||||||||||||||||||||||||||||

| Three years later | 23,144 | 68,809 | 120,444 | 154,738 | 181,268 | 230,145 | 253,814 | 274,704 | ||||||||||||||||||||||||||||||||||||

| Four years later | 23,455 | 69,847 | 119,771 | 155,520 | 185,848 | 227,555 | 251,968 | |||||||||||||||||||||||||||||||||||||

| Five years later | 24,425 | 71,879 | 123,949 | 158,842 | 184,995 | 227,357 | ||||||||||||||||||||||||||||||||||||||

| Six years later | 25,403 | 78,396 | 128,006 | 159,151 | 185,666 | |||||||||||||||||||||||||||||||||||||||

| Seven years later | 30,704 | 79,939 | 128,907 | 159,747 | ||||||||||||||||||||||||||||||||||||||||

| Eight years later | 32,395 | 80,439 | 129,724 | |||||||||||||||||||||||||||||||||||||||||

| Nine years later | 32,825 | 81,737 | ||||||||||||||||||||||||||||||||||||||||||

| Ten years later | 33,403 | |||||||||||||||||||||||||||||||||||||||||||

| C. Net cumulative (deficiency) redundancy | (7,406 | ) | (8,936 | ) | (8,875 | ) | (9,722 | ) | (9,416 | ) | (13,634 | ) | 2,933 | (10,872 | ) | 4,675 | 6,953 | |||||||||||||||||||||||||||

| D. Cumulative amount of claims paid, net of reserve recoveries through: | ||||||||||||||||||||||||||||||||||||||||||||

| One year later | 16,721 | 30,061 | 50,458 | 64,810 | 73,647 | 105,848 | 109,538 | 110,812 | 123,100 | 122,122 | ||||||||||||||||||||||||||||||||||

| Two years later | 22,990 | 46,860 | 78,314 | 95,385 | 121,222 | 156,176 | 163,803 | 174,684 | 194,925 | |||||||||||||||||||||||||||||||||||

| Three years later | 24,562 | 58,322 | 93,286 | 120,133 | 146,956 | 188,044 | 200,637 | 209,619 | ||||||||||||||||||||||||||||||||||||

| Four years later | 27,231 | 65,084 | 105,251 | 131,912 | 162,704 | 207,484 | 216,349 | |||||||||||||||||||||||||||||||||||||

| Five years later | 28,833 | 71,082 | 112,029 | 140,618 | 172,330 | 220,627 | ||||||||||||||||||||||||||||||||||||||

| Six years later | 30,367 | 75,225 | 118,171 | 146,581 | 179,880 | |||||||||||||||||||||||||||||||||||||||

| Seven years later | 31,058 | 75,141 | 122,410 | 152,232 | ||||||||||||||||||||||||||||||||||||||||

| Eight years later | 33,171 | 83,865 | 126,144 | |||||||||||||||||||||||||||||||||||||||||

| Nine years later | 34,552 | 85,724 | ||||||||||||||||||||||||||||||||||||||||||

| Ten years later | 35,423 | |||||||||||||||||||||||||||||||||||||||||||

| Net reserve-December 31 | 25,997 | 72,801 | 120,849 | 150,025 | 176,250 | 213,723 | 254,901 | 263,832 | 312,468 | 323,192 | 348,087 | |||||||||||||||||||||||||||||||||

| Reinsurance recoverables | 324 | 4,763 | 4,489 | 6,338 | 8,412 | 37,954 | 42,044 | 49,584 | 70,172 | 91,943 | 102,791 | |||||||||||||||||||||||||||||||||

| Gross reserve-December 31 | 26,321 | 77,564 | 125,338 | 156,363 | 184,662 | 251,677 | 296,945 | 313,416 | 382,640 | 415,135 | 450,878 | |||||||||||||||||||||||||||||||||

| Net re-estimated reserve | 33,403 | 81,737 | 129,724 | 159,747 | 185,666 | 227,357 | 251,968 | 274,704 | 307,793 | 316,239 | ||||||||||||||||||||||||||||||||||

| Re-estimated reinsurance recoverable | 1,776 | 6,704 | 7,919 | 8,627 | 10,156 | 35,968 | 40,755 | 50,631 | 65,443 | 93,541 | ||||||||||||||||||||||||||||||||||

| Gross re-estimated reserve | 35,179 | 88,441 | 137,643 | 168,374 | 195,822 | 263,325 | 292,723 | 325,335 | 373,236 | 409,780 | ||||||||||||||||||||||||||||||||||

| Gross cumulative redundancy (deficiency) | $ | (8,858 | ) | $ | (10,877 | ) | $ | (12,305 | ) | $ | (12,011 | ) | $ | (11,160 | ) | $ | (11,648 | ) | $ | 4,222 | $ | (11,919 | ) | $ | 9,404 | $ | 5,355 | |||||||||||||||||

18

Reinsurance

We reinsure a portion of the risk we underwrite in order to control the exposure to losses and to protect capital resources. We cede to reinsurers a portion of these risks and pay premiums based upon the risk and exposure of the policies subject to such reinsurance. Ceded reinsurance involves credit risk and is generally subject to aggregate loss limits. Although the reinsurer is liable to us to the extent of the reinsurance ceded, we are ultimately liable as the direct insurer on all risks reinsured. Reinsurance recoverables are reported after allowances for uncollectible amounts. We monitor the financial condition of reinsurers on an ongoing basis and review our reinsurance arrangements periodically. Reinsurers are selected based on their financial condition, business practices and the price of their product offerings. In order to mitigate credit risk to reinsurance companies, most of our reinsurance recoverable balance as of December 31, 2015 was with reinsurers that had an A.M. Best rating of “A–” or better. We also mitigate our credit risk for the remaining reinsurance recoverable by obtaining letters of credit.

The following table presents our gross and net premiums written and earned and reinsurance recoveries for each of the last three years (in thousands).

| Year Ended December 31 | ||||||||||||

| 2015 | 2014 | 2013 | ||||||||||

| Gross premiums written | $ | 514,223 | $ | 473,218 | $ | 460,027 | ||||||

| Ceded premiums written | (157,279 | ) | (148,866 | ) | (99,262 | ) | ||||||

| Net premiums written | $ | 356,944 | $ | 324,352 | $ | 360,765 | ||||||

| Gross premiums earned | $ | 494,643 | $ | 461,694 | $ | 437,226 | ||||||

| Ceded premiums earned | (145,562 | ) | (140,477 | ) | (76,685 | ) | ||||||

| Net premiums earned | $ | 349,081 | $ | 321,217 | $ | 360,541 | ||||||

| Reinsurance recoveries | $ | 89,892 | $ | 99,911 | $ | 45,456 | ||||||

Investment Portfolio

Our investment objective is to maximize current yield while maintaining safety of capital together with sufficient liquidity for ongoing insurance operations. Our investment portfolio is composed of fixed-income and equity securities. As of December 31, 2015, we had total invested assets of $578.8 million. If market rates were to increase by 1%, the fair value of our fixed-income securities as of December 31, 2015 would decrease by approximately $16.6 million. The following table shows the fair values of various categories of fixed-income securities, the percentage of the total fair value of our invested assets represented by each category and the tax equivalent book yield of each category of invested assets as of December 31, 2015 and 2014.

19

| As of December 31, 2015 | As of December 31, 2014 | |||||||||||||||||||||||

| Fair | Percent of | Fair | Percent of | |||||||||||||||||||||

| Value | Total | Yield | Value | Total | Yield | |||||||||||||||||||

| (in thousands) | (in thousands) | |||||||||||||||||||||||

| Category: | ||||||||||||||||||||||||