Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - Hunting Dog Capital Corp. | v432129_ex23-1.htm |

As filed with the Securities and Exchange Commission on March 4, 2016.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

HUNTING DOG CAPITAL CORP.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 6199 | 47-4989389 | ||

|

(State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

One Maritime Plaza, Suite 825

San Francisco, California 94111

(415) 236-1993

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

Paul Clausing

Chief Financial Officer

One Maritime Plaza, Suite 825

San Francisco, CA 94111

(415) 236-1993

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copy of correspondence to:

Steven B. Boehm, Esq.

Harry S. Pangas, Esq.

Sutherland Asbill & Brennan LLP

700 Sixth Street NW, Suite 700

Washington, DC 20001

(202) 383-0100

As soon as practicable after the effective date of this Registration Statement.

(Approximate date of commencement of proposed sale to the public)

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | Smaller reporting company | x |

(do not check if a smaller reporting company)

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price (1) | Amount of Registration Fee (1) | ||||||

| Common Stock, $0.01 par value per share | $ | 50,000,000 | $ | 5,035 | ||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated March 4, 2016

PRELIMINARY PROSPECTUS

![]()

Hunting Dog Capital Corp.

One Maritime Plaza, Suite 825

San Francisco, CA 94111

Tel: (415) 942-5316

Shares of Common Stock

This is an initial public offering of Hunting Dog Capital Corp. and no public market currently exists for our shares. The initial public offering price of our common stock is expected to be between $ and $ per share. We have applied to list our common stock on the NASDAQ Capital Market under the symbol “HDCC.”

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act of 1933, as amended, and, as such, will be subject to reduced public reporting requirements.

Investing in our common stock may be considered speculative and involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 11 to read about the risks you should consider before buying shares of our common stock.

| Per share | Underwriting discounts and commissions (1) | Proceeds to issuer (1) | ||||||

| Initial public offering price | ||||||||

| Underwriting discounts and commissions (1) | ||||||||

| Proceeds to us | ||||||||

| (1) | We refer you to “Underwriting” beginning on page 54 of this prospectus for additional information regarding total underwriter compensation. |

The underwriter has agreed to use its best efforts to procure potential purchasers for the shares of common stock offered pursuant to this prospectus.

The shares are being offered on an all-or-none basis. The offering will commence on the date of this preliminary prospectus. All investor funds received from the date of this preliminary prospectus to the closing date of this offering, which shall take place on , 2016, will be deposited into an escrow account until closing. The closing date is also the termination date of this offering. If investor funds are not received for the full amount of shares to be sold in this offering on the closing date, the offering will terminate and any funds received will be returned promptly, without interest. A more detailed description of this process is included in “Underwriting” beginning on page 54.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2016.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or in any amended prospectus that we may authorize to be delivered or made available to you. We and the underwriter have not authorized anyone to provide you with different information. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this preliminary prospectus is accurate only as of the date of the circular, regardless of the time of its delivery or any sale of shares of our common stock.

Persons outside the United States who come into possession of this preliminary prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of our common stock and the distribution of the preliminary prospectus outside the United States. See "Underwriting."

2

This summary highlights selected information appearing elsewhere in this preliminary prospectus. This summary does not contain all of the information that you should consider before deciding to invest in our common stock. You should read the entire preliminary prospectus carefully, especially the matters discussed in “Risk Factors.”

Hunting Dog Capital LLC commenced operations in 2006. In connection with the completion of this offering, Hunting Dog Capital LLC will be acquired by Hunting Dog Capital Corp., a Delaware corporation that was formed in August 2015 (as part of the “Transactions” described in this prospectus). Except as otherwise indicated, the terms “we,” “us,” “our” and the “Company” refer to Hunting Dog Capital LLC prior to the Transactions and Hunting Dog Capital Corp. after the Transactions.

Hunting Dog Capital Corp.

Overview of Hunting Dog Capital Corp.

Hunting Dog Capital Corp. is a holding company that intends to operate through several wholly owned subsidiaries to provide financing solutions to lower middle-market companies, which we define as businesses with revenues between $5 million and $50 million, and needing financing typically under $20 million. We will seek long-term equity appreciation through modest equity exposure that does not subject us to the risk of material capital loss. We intend to use the net proceeds of this offering to invest, through our subsidiaries, in a diversified portfolio of financial assets, including direct loans, convertible debt instruments, trade finance, structured credit, and preferred and common equity investments, issued by or relating to lower middle-market companies. We intend to pursue these opportunities and conduct our operations such that we and our subsidiaries will qualify for exemptions under the Investment Company Act of 1940, as amended (the “Investment Company Act”).

Additionally, as part of this offering, we will acquire Hunting Dog Capital LLC, an investment manager of lower middle-market private debt funds. Hunting Dog Capital LLC will become our wholly owned subsidiary and continue to manage HD Special-Situations II, LP, and HD Special-Situations III, LP (“Fund II” and “Fund III,” respectively, and collectively, the “Existing Funds”), whose assets under management total approximately $83 million as of the date of this preliminary prospectus. As a result, we will be entitled to receive the management fees associated with Hunting Dog Capital LLC’s management of each of the Existing Funds. We will not, however, be entitled to receive any incentive fees associated with operating performance of the Existing Funds. Instead, certain of our directors and executive officers will continue to be entitled to receive those incentive fees. Hunting Dog Capital LLC earned approximately $3.0 million of management fees for the periods covered by this prospectus, which include the fiscal years ended December 31, 2013 and 2014 and the nine months ended September 30, 2015. Historical management fees and anticipated future management fees relate exclusively to assets under management in the Existing Funds and, as noted above, do not include incentive fees. For the period of October 23, 2009 through September 30, 2015, the Existing Funds generated gross and net returns on called capital of approximately 17.3% and 13.3%, respectively, without the use of “leverage” (borrowing funds to enhance equity holders’ returns), and without any material capital gains. We have been able to generate these returns while maintaining a senior position by typically not requiring principal amortization during the term of our loans as well as requiring relatively little warrant coverage, if any, with our loans. Gross and net IRRs reflect historical results relating to our past performance and are not necessarily indicative of our future results. These returns were generated exclusively by making senior secured term-loans to lower middle-market companies. These loans are characterized by two common traits:

| · | They are all secured by tangible collateral, the value of which typically exceeds the amount of the loan; and |

| · | The borrowers typically have significant at-risk equity. |

We intend to use the net proceeds of this offering to capitalize our wholly owned subsidiaries. They will deploy this capital in various forms of financing to lower middle-market companies unable to access sufficient amounts of traditional financing, such as bank debt or private equity on terms acceptable to their owners. We believe U.S.-based lower middle-market companies represent a market both underserved by institutional capital, and capable of generating favorable risk-adjusted returns for investors. We believe that historically, however, access to these opportunities has been limited, such that individual and institutional investors have been unable to participate efficiently in this market segment. The significant time and effort required and the cost of sourcing new opportunities among lower middle-market companies are disproportionately high relative to the typically small transaction size. Since its inception in 2006, however, Hunting Dog Capital LLC has developed a proprietary transaction-referral network that consists of over 7,000 sources across the United States specializing in raising capital for this market segment. This network provides Hunting Dog Capital LLC access to hundreds of opportunities on an annual basis, and will enable us to maintain a high level of selectivity in those opportunities. We intend to use this network of sources to enable us to access opportunities to finance the needs of lower middle-market companies in transactions that fit within our investment strategy. We refer to companies to which we have provided financing as our “investments.”

3

Our Objective and the Market Opportunity

Our objective is to become the capital partner of choice to lower middle-market companies, and consistently to generate favorable risk-adjusted returns for our shareholders through both current income and long-term capital gains. Our investment strategy will focus primarily on structured finance involving the advancement of capital backed by tangible collateral, including real estate, inventory, trade receivables, machinery, and equipment, among other assets that can be liquidated in the event of ongoing unremedied negative events. We intend to implement our investment strategy by focusing exclusively on lower middle-market companies, which are generally overlooked by institutional investors, appropriately structuring financings to mitigate the risk of principal loss and continuing to grow our transaction-referral network aggressively. We believe these opportunities will persist for the foreseeable future.

We believe that lower middle-market companies lack ready access to the form and quantity of growth capital available to larger companies that can rely on efficient, well-developed U.S. and international capital markets. We believe two factors are primarily responsible for this limited access: first, small transaction sizes and fragmentation within the capital markets for lower middle-market companies; and second, the increasingly complex regulatory environment for regulated financial institutions.

The U.S. capital markets are among the world’s most developed, efficient, and transparent. They are also increasingly highly regulated due to the size, interrelationships, and systemic importance of their participants. The capital pools served by major investment banks are large, typically managed by small groups, and hence predisposed to pursue larger transactions to reap efficiencies from their own investment platforms. Major investment banks similarly prefer to employ smaller, nimble teams to pursue fewer, larger fee opportunities. Commercial and investment banks alike, in search of efficiencies, and to most readily accommodate increasing regulation, favor larger transactions concentrated across a smaller discrete number of high-quality clients. Smaller transactions, such as those that we will pursue, are inefficient for the vast majority of all institutional investors, and do not generate the requisite level of fee income for most major investment banks. Consequently, U.S. capital markets generally function best for larger companies engaging in larger transactions than for lower middle-market companies seeking smaller amounts of capital. The lower middle-market segment of the U.S. capital markets is characterized by significant fragmentation among companies, advisors, and capital providers. Generally, these capital markets are significantly less developed than those serving larger entities with larger transaction sizes. There is, nonetheless, significant transaction volume, although not publicized, and effectively “uninvestable” as an asset class by the vast majority of all market participants.

Lower middle-market companies lack the same access to institutionally funded, developed, and transparent capital markets that larger companies rely on for efficient funding. We believe that a host of factors will continue to cause restricted access for these lower middle-market companies. Among the factors are the following:

| 1. | Ongoing consolidation of the banking industry has resulted in a long decline in the number of FDIC-insured institutions, in particular, community banks (generally, those banks with less than $10 billion in assets), which historically have been critical to the lower middle-market; |

| 2. | The Dodd–Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”) significantly increased the regulatory requirements for all banks. Its impact is particularly high on community banks, however, as these banks have a smaller asset base across which to spread the costs of incremental regulatory requirements; |

| 3. | As bank consolidation continues and the remaining banks become increasingly large, regulatory oversight becomes greater and the cost of accommodating these regulations increases. As a result, we believe banks are motivated to hold more assets of the highest quality, thereby further abandoning the lower middle-market; |

| 4. | Numerous business development companies have arisen in recent years to fill the void left by community banks, but most of these entities focus on transactions in excess of $25 million. We believe this is primarily due to the motivation to increase assets under management, and hence increase management fees. Transactions below certain thresholds consequently become inefficient to pursue, even though they may generate above-market risk-adjusted returns; |

| 5. | The same circumstances associated with lower middle-market business development companies apply to lower middle-market private equity funds, also shifting the focus of these funds to increasingly larger transactions; and |

| 6. | The sheer amount of capital held by America’s major institutional-investor classes – pensions, endowments, insurance companies, and other large asset managers – favors deploying at least $50 million or 5-10% of a given fund’s total committed capital. This further precludes large funds from deploying capital among lower middle-market companies. |

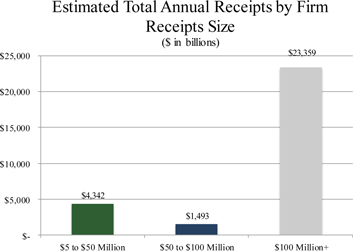

As a result, lower middle-market companies are forced to seek capital either on their own or through the types of advisors that comprise our transaction-referral network, but, in any case, without the benefit of developed, transparent capital markets. We believe the best lower middle-market opportunities generally arise from businesses with between $5 million and $50 million of annual revenue. According to U.S. Census data from 2012, this market consists of approximately 322,000 firms that generated estimated receipts of approximately $4.3 trillion, or approximately 13% of the annual total estimated business receipts in the United States. By comparison, the entire market of firms that generated $100 million or more in estimated receipts is only approximately 22,000, far smaller numerically, yet significantly larger – over 5 times – as measured by total estimated receipts of $23.4 trillion. We believe that the focus of U.S. capital markets is on the latter larger, but fewer, businesses because they can more easily be identified and because they permit the deployment of capital at significant scale. Yet this causes capital markets generally to ignore the numerous financing opportunities presented by lower middle-market companies, which we intend to capitalize upon.

4

Competitive Advantages

We believe that we are well-positioned to achieve significant, sustainable financial growth, primarily driven by:

| · | Our Capital Preservation Focus, Enhanced with Favorable Anticipated Cash Yield and Opportunity for Long-Term Capital Gains |

The guiding principle in our investment philosophy is capital preservation while earning of the highest risk-adjusted returns possible. We believe the inefficiencies of the lower middle-market present myriad opportunities to achieve our return goals while simultaneously protecting our capital. We focus on opportunities where there is frequently little competition from alternative capital providers, and where we can earn a relatively high cash return on our principal. Historically, we have accomplished this by making senior secured term-loans typically under $20 million with a blanket lien on all assets of the borrower. We anticipate pursuing transactions with companies similar to those the Existing Funds have invested in, but structured in a manner that fits our investment strategy; we intend to pursue transactions that generate favorable cash yield so that we can pay dividends to our shareholders, but structure them so that a portion of our returns arises from modest long-term equity appreciation. We believe this strategy will allow us to take the greatest advantage of our network and avail ourselves of otherwise neglected opportunities.

| · | Experienced Management Team with Significant Equity |

Our senior management team has extensive experience in the structuring and management of portfolios of lower middle-market investments across the capital structure, as well as broad, relevant investment-banking experience in capital markets, mergers, acquisitions, and restructurings. Subsequent to the completion of the organizational transactions (which are described below under “Summary of the Transactions”), management will have aggregate beneficial ownership in the Company of approximately %, which we believe aligns management’s interests with those of our shareholders. Christopher Allick and Todd Blankfort, our Chairman/Chief Executive Officer and President, respectively, have also jointly committed 2% of the total limited partners’ commitments in the Existing Funds. Their interests in the Existing Funds are currently valued at approximately $2.0 million (as of September 30, 2015), including their original cash contributions and their deferred incentive fees.

| · | Our Transaction-Referral Network |

We believe one of our greatest strengths is the network of over 7,000 transaction-referral sources that Hunting Dog Capital LLC has cultivated over the course of the last ten years. These sources consist of many regional and boutique investment banks in the United States, hundreds of self-employed investment bankers/advisors, as well as attorneys, accountants, auditors, business brokers, and other contract financial professionals. Additionally, our network includes numerous partners at both sponsored and sponsorless lower middle-market private equity funds. We believe transaction volume is predicated in part on market dynamics, but we attempt to cultivate our network constantly, making it aware of our transaction parameters and ensuring we respond to all outreaches. We carefully monitor the flow of transaction opportunities we receive, and have seen significant long-term growth in them. In 2012, our network referred 121 transaction opportunities with a gross value of approximately $1.5 billion to Hunting Dog Capital LLC. For only the nine-month period ended September 30, 2015, Hunting Dog Capital LLC saw 178 transaction opportunities with a gross value of approximately $2.2 billion. We believe our efforts with members of our network will result in continued growth in transaction-opportunity volume, and will enable us rapidly to avail ourselves of opportunities appropriate for the Company’s investment strategy.

| · | Structured, Diversified Anticipated Portfolio of Assets |

We believe that both transaction structure and portfolio diversification are critical elements to generating favorable risk-adjusted returns in lower middle-market companies. Our transaction-referral network facilitates a robust and growing set of opportunities, enabling us to be highly selective in those we pursue. Further, we believe the most appropriate investment strategy for exposure to lower middle-market companies is one predicated on structured finance, involving the advancement of capital backed by tangible collateral, including real estate, inventory, trade receivables, machinery, and equipment, among other assets that can be liquidated in the event of ongoing unremedied negative events. We typically require transaction expense deposits from potential clients, further mitigating risk of loss to our investors. Additionally, we will seek long-term equity appreciation through modest equity exposure that does not subject us to the risk of material capital loss. We intend to pursue these opportunities and conduct our operations such that we and our subsidiaries will qualify for exemptions from regulation under the Investment Company Act.

| · | Increasing Sophistication of Lower Middle-Market Companies Resulting from Rapidly Evolving Technology |

Based on our experience, as well as on the opportunities we obtain through our transaction-referral network, we believe that lower middle-market companies are increasingly technologically and organizationally sophisticated. Widespread availability and decreasing costs of computing, data analysis, communications, and enterprise resource-planning systems have enabled lower middle-market companies to operate on a par with larger peers, for which this infrastructure is more expensive and cumbersome to deploy, especially against the backdrop of legacy systems. Given our requirements for frequent data and regular monitoring of our investments, these advances have materially reduced the costs and burden on the management teams of our investments. We believe our monitoring requirements also mitigate the risks associated with investing in this asset class to a degree not previously possible.

5

Risk Factors Summary

We are subject to a number of risks, including risks that may prevent us from achieving our business objectives or that may adversely affect our business, financial condition, results of operations, cash flow, and prospects. You should carefully consider the risks discussed in the section entitled “Risk Factors,” including the following risks, before investing in our common stock:

| · | Our lack of operating history limits your ability to evaluate our business and prospects and may increase your investment risk. |

| · | We may be adversely affected by deteriorating economic or business conditions. |

| · | Our income associated with Existing Funds may be reduced or eliminated earlier than anticipated due to the loss of certain key persons under the Existing Funds or repayments of principal without the opportunity to redeploy such capital. |

| · | There are significant potential conflicts of interest which could adversely impact the returns to our investors. |

| · | In the future, we may borrow money, which may amplify our potential for loss. |

| · | We may not recover the capital that we advance in our transactions. |

| · | Our clients are lower middle-market companies, which present greater risks than those associated with larger companies. |

| · | We may be unable to recognize or act upon an operational or financial problem with a client in a timely fashion, so as to prevent a loss of our capital advanced to that client. |

| · | The non-amortizing loans which we may make, i.e., that do not require periodic repayment of principal, involve a greater degree of risk than other types of financings. |

| · | We may make errors in evaluating accurate information reported by our clients and, as a result, we may suffer losses on loans or advances that we would not have made if we had properly evaluated the information. |

| · | A concentration of loans or other assets with a limited number of clients within a particular industry, such as the retail or manufacturing industry, or within a geographic region, could impair our revenues if the industry or region were to experience economic difficulties. |

| · | The collateral securing a loan or a particular asset, such as a mortgage or lease, may not be sufficient to protect us from a partial or complete loss if the loan or asset becomes non-performing and we are required to foreclose. |

| · | There will be uncertainty as to the value of our financial assets. |

| · | Our ability to grow depends in part on our ability to obtain additional capital. |

| · | Maintaining our exclusion from the definition of an investment company under the Investment Company Act will place material restrictions on our business. If we fail to comply with those restrictions, however, we could become subject to more stringent restrictions on the operation of our business under the Investment Company Act. |

6

Investment Company Act Considerations

We anticipate conducting our operations so that we and our subsidiaries may avail ourselves of exemptions under the Investment Company Act, and/or will not otherwise be subject to regulation as an investment company under the Investment Company Act.

Section 3(a)(1)(A) of the Investment Company Act defines an investment company as any issuer that is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting, or trading in securities. Section 3(a)(1)(C) of the Investment Company Act defines an investment company as any issuer that is engaged or proposes to engage in the business of investing, reinvesting, owning, holding, or trading in securities, and owns or proposes to acquire investment securities having a value exceeding 40% of the value of the issuer’s total assets (exclusive of U.S. Government securities and cash items) on an unconsolidated basis. Excluded from the term “investment securities,” among other things, are U.S. Government securities and securities issued by majority-owned subsidiaries that are not themselves investment companies and that are not relying on exemptions from the definition of investment company set forth in Section 3(c)(1) or 3(c)(7) of the Investment Company Act.

We intend to conduct our business primarily through our wholly owned subsidiaries, which will be formed to carry out specific activities. We intend to manage our business so as to minimize any investment securities we may hold and in all cases, attempt to ensure that they do not exceed 40% our total assets. Further, we will not hold ourselves out as being engaged primarily, or actually engage, in the business of investing in securities. Consequently, we expect that we will not be subject to registration or regulation as an investment company of any kind under the Investment Company Act. The securities issued to us by our wholly owned subsidiaries, other than our wholly owned subsidiary that will rely on the exemption set forth in Section 3(c)(7) of the Investment Company Act, will not be investment securities for the purpose of this 40% test.

One or more of our subsidiaries will seek to qualify for an exemption from regulation as an investment company under the Investment Company Act pursuant to: (a) Section 3(c)(5)(A), which is available for entities “primarily engaged in the business of purchasing or otherwise acquiring notes, drafts, acceptances, open accounts receivable, and other obligations representing part or all of the sales price of merchandise, insurance and services”; (b) Section 3(c)(5)(B), which is available for entities “primarily engaged in the business of making loans to manufacturers, wholesalers, and retailers of, and to prospective purchasers of, specified merchandise, insurance and services”; or (c) Section 3(c)(5)(C), which is available for entities “purchasing or otherwise acquiring mortgages and other liens on and interests in real estate.” Each of these exemptions generally requires that at least 55% of such subsidiary’s assets consist of eligible loans, receivables or assets and, in the case of Section 3(c)(5)(C), an additional 25% of its assets consist of real estate related assets. To qualify for any of the foregoing exemptions, the subsidiary would be required to comply with interpretations issued by the staff of the Securities and Exchange Commission (the “SEC”) that govern the respective activities.

We will monitor our assets and those of our subsidiaries to ensure continuing and ongoing compliance with these and/or other applicable tests, and we will be responsible for making the determinations and calculations required to confirm our compliance with the tests. If the SEC does not agree with our determinations, we may be required to adjust our activities and/or those of our subsidiaries.

Qualification for these or other exemptions could affect our ability to originate, participate in, or hold certain investments, or, in order to remain qualified for such exemptions, we could be required to dispose of investments that we might prefer to retain. Changes in current policies by the SEC and its staff could also require that we alter our business activities for this purpose. For a discussion of certain risks associated with the Investment Company Act, please see “Risk Factors.” If we are required to register under the Investment Company Act, our ability to conduct our business could be materially adversely effected.

Summary of the Transactions

In connection with the completion of this offering, we will consummate the following organizational transactions (collectively, the “Transactions”):

| · | Hunting Dog Capital LLC members will exchange their interests in Hunting Dog Capital LLC for consideration consisting exclusively of shares of Hunting Dog Capital Corp. There is no readily available market value for the Hunting Dog Capital LLC interests and the book value of these interests as of September 30, 2015 was approximately ($0.1) million. The value of the consideration the members of Hunting Dog Capital LLC will receive has been determined by Hunting Dog Capital Corp.’s management, who are also members of Hunting Dog Capital LLC, based on the expected market demand for shares of Hunting Dog Capital Corp. in this offering and with the input of W. R. Hambrecht + Co., LLC. The range of value implied by the estimated offering price range set forth on the cover page of this prospectus was determined using industry standard valuation methodologies that we believe are reasonable and commonplace. These include, among others, the estimated present value of net distributable income related to the management fees to which Hunting Dog Capital LLC is or may be entitled to receive in the future, comparable public market transactions, and estimated future dividends and growth therein. Christopher Allick, Todd Blankfort, and Paul Clausing, members of Hunting Dog Capital LLC, will be appointed as our Chairman/Chief Executive Officer, President, and Chief Financial Officer, respectively and we will appoint a board of directors; |

| · | Hunting Dog Capital LLC will then become a wholly owned subsidiary of Hunting Dog Capital Corp., but will continue to manage the Existing Funds and any future funds; |

| · | Hunting Dog Capital Corp. will become the sole owner of the following subsidiaries, to be formed under Delaware law (the “Finance Subsidiaries”). The Finance Subsidiaries will seek to engage in financing transactions with lower middle-market companies, which the Company defines as businesses with annual revenues between $5 and $50 million. These transactions may, to a lesser extent, include the Finance Subsidiaries acquiring warrants or instruments with other equity-like characteristics, giving them the potential to realize enhanced returns on a portion of their portfolio. Transactions will typically not exceed $20 million in size and will be funded by debt or equity capital contributed by the Company. In addition, the Finance Subsidiaries may seek to obtain debt financing in the future. The business of each of the Finance Subsidiaries is described below: |

| o | HDC Factor Co.’s business operations will consist of entering into factoring transactions, primarily on a recourse basis, pursuant to which it will purchase the accounts receivable of a business and advance the business a percentage of the invoice total. Recourse factoring is when a business sells its accounts receivables to a factor, with the promise that the business will buy back any uncollected invoices. In non-recourse factoring, the business has no liability with respect to any uncollected invoices. HDC Factor Co. will operate under the exemption from the definition of an investment company provided by Section 3(c)(5)(A) of the Investment Company Act; |

7

| o | HDC Manufacturer Co. business operations will involve providing loans to finance the operations of manufacturers of products, or wholesalers and retailers of products and services, provided the proceeds of each loan will be used to pay for specific products or services. This business will include purchase order financing, where HDC Manufacturer Co. will lend the supplier of goods, whether a manufacturer, wholesaler or retailer, the capital needed in order to fulfill a customer order. HDC Manufacturer Co. will operate under the exemption from the definition of an investment company provided by Section 3(c)(5)(B) of the Investment Company Act; |

| o | HDC Equipment Finance Co.’s business will involve (i) the purchase of leases representing part or all of the sales price of equipment, (ii) leases made by HDC Equipment Finance Co. directly to finance the purchase of specified equipment, and (iii) sale-leaseback transactions in which HDC Equipment Finance Co. purchases equipment from an operating company and then leases the equipment back to that company (such leases and transactions are collectively referred to herein as the “Equipment Financed Assets”). HDC Equipment Finance Co. will operate under the exemptions provided by Section 3(c)(5)(A) with respect to (i) above and Section 3(c)(5)(B) with respect to (ii) and (iii) above. |

| o | HDC Mortgage Co. will invest its funds largely in first mortgage loans secured by office buildings, shopping centers, hotels, multi-family residential properties and mixed-use and industrial/warehouse developments, and, to a limited extent, in equity ownership of such real estate and other real-estate related investments. HDC Mortgage Co. will operate under the exemption provided by Section 3(c)(5)(C) of the Investment Company Act.; |

| o | HDC Special Opportunities Co. will make senior secured term loans to borrowers that are unable to structure financing solutions to fit within the business operations of any of the aforementioned subsidiaries. HDC Special Opportunities Co. will operate under the exemption provided by Section 3(c)(7) of the Investment Company Act. It is intended that the value of HDC Special Opportunities Co.’s securities owned by Hunting Dog Capital Corp. will not exceed 40% of Hunting Dog Capital Corp.’s total assets (exclusive of U.S. Government securities and cash items). |

Organizational Structure Following this Offering

The diagram below depicts our organizational structure after giving effect to the Transactions, including this offering.

Our Corporate Information

Hunting Dog Capital Corp., the issuer of the common stock in this offering, was incorporated as a Delaware corporation on August 28, 2015. Our corporate headquarters are located at One Maritime Plaza, Suite 825, San Francisco, CA 94111. Our telephone number is (415) 942-5316. Our principal website address is . The information on any of our websites is deemed not to be incorporated in this prospectus or to be part of it.

Implications of Being an “Emerging Growth Company” and “Smaller Reporting Company”

As a company with less than $1 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An “emerging growth company” may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These reduced requirements include:

| · | We are required to have only two years of audited financial statements and only two years of related Management's Discussion and Analysis of Financial Condition and Results of Operations disclosure; |

8

| · | We are not required to engage an auditor to report on our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”); |

| · | We are not required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board (the “PCAOB”) regarding mandatory audit firm rotation or a supplement to the auditor's report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

| · | We are not required to submit certain executive compensation matters to stockholder advisory votes, such as “say-on-pay,” “say-on-frequency,” and “say-on-golden parachutes;” and |

| · | We are not required to disclose certain executive compensation-related items, such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to median employee compensation. |

We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the first sale of our common equity securities in an offering registered under the Securities Act of 1933 (the “Securities Act”), or such earlier time as we are no longer an “emerging growth company.” We would cease to be an “emerging growth company” if we have more than $1 billion in annual revenue, have more than $700 million in market value of our common stock held by non-affiliates, or issue more than $1 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. In that regard, we have elected to adopt the reduced disclosure with respect to financial statements and the related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure. As a result of this election, the information that we provide stockholders may be different from that you might get from other public companies in which you hold equity.

The JOBS Act permits an “emerging growth company” like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards when they are adopted.

In addition, we are also currently a “smaller reporting company,” meaning that we are not an investment company, an asset-backed issuer, or a majority-owned subsidiary of a parent company that is not a “smaller reporting company,” and have a public float of less than $75 million and annual revenues of less than $50 million during the most recently completed fiscal year. In the event that we are still considered a “smaller reporting company” when we cease being an “emerging growth company,” the disclosures we will be required to provide in our SEC filings will increase, but will remain less than they would be if we were not considered a “smaller reporting company.” Specifically, similar to “emerging growth companies,” “smaller reporting companies” (a) are able to provide simplified executive compensation disclosures in their filings; (b) are exempt from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that independent registered public accounting firms provide an attestation report on the effectiveness of internal control over financial reporting; and (c) have certain other decreased disclosure obligations in their SEC filings, including, among other things, only being required to provide two years of audited financial statements in annual reports.

Decreased disclosures in our SEC filings due to our status as an “emerging growth company” or “smaller reporting company” may make it harder for investors to analyze the Company’s operations results and financial prospects.

9

The Offering

| Common stock to be offered | shares of common stock | |

| Shares to be outstanding after this offering | (1) | |

| Use of proceeds | Our net proceeds from this offering will be approximately $ million, after deducting underwriting discounts and commissions and the estimated expenses of this offering. We will use these net proceeds to fund investments in our subsidiaries for further deployment to our clients and for other general corporate purposes. | |

| Proposed NASDAQ Capital Market symbol | HDCC | |

| Dividend policy | Our Board of Directors intends to maintain a variable dividend policy, with the objective of optimizing quarterly dividends and long-term equity growth. |

(1) Excludes shares of our common stock currently reserved for issuance under our 2016 Incentive Award Plan, of which no shares have yet been granted.

Unless otherwise indicated, all information in this prospectus gives effect to the acquisition of Hunting Dog Capital LLC, a Delaware limited liability company, by Hunting Dog Capital Corp., a Delaware corporation, immediately before the closing of this offering. The acquisition will result in our being taxed as a corporation under the Internal Revenue Code. In the acquisition, existing members of Hunting Dog Capital LLC will receive shares of Hunting Dog Capital Corp. common stock in exchange for their units of membership interest in Hunting Dog Capital LLC. The share information in the table above is based on shares outstanding as of , 2016.

10

You should carefully consider the risks described below, together with all other information included in this preliminary prospectus, before making an investment decision. The risks set out below are not the only risks we face. Additional risks and uncertainties not presently known to us or not presently deemed material by us might also impair our operations and performance. Our business, financial condition, and results of operations could be materially and adversely affected by any of these risks or uncertainties.

Risks Related to Our Operations and Financial Results

Our lack of operating history limits your ability to evaluate our business and prospects and may increase your investment risk.

Hunting Dog Capital LLC commenced operations in 2006, but Hunting Dog Capital Corp. is a newly formed entity whose anticipated operations differ from the historical operations of Hunting Dog Capital LLC. Upon completion of the Transactions, Hunting Dog Capital Corp. will be entitled to the entirety of the management fees, but not any incentive fees, associated with the Existing Funds. It is anticipated that Hunting Dog Capital Corp. will also generate income from future financings, thus the historical results of Hunting Dog Capital LLC will not materially reflect our future results.

Further, the results of the Existing Funds are not necessarily indicative of the results that we may achieve from the financings we anticipate funding with the net proceeds of this offering. We anticipate pursuing transactions with companies similar to those the Existing Funds have invested in, but structured in a manner that fits our investment strategy. Because we expect to employ different strategies and techniques from those of the Existing Funds, in particular with respect to the structure of our transactions, our results may differ from and be independent of the results obtained by the Existing Funds. However, only the operating history of Hunting Dog LLC is available for purposes of your evaluation of our business and prospects of Hunting Dog Capital Corp. In that regard, we may not be able to:

| · | Successfully implement the strategy of Hunting Dog Capital Corp., which is different from that of Hunting Dog Capital LLC; |

| · | Successfully compete with competitors for the new financing opportunities we will seek; |

| · | Find financing opportunities that meet our parameters; |

| · | Grow and manage our growth; |

| · | Predict the level of defaults or impairments to our loans or other financings we may experience over longer periods of time; |

| · | Raise additional capital that may be required to fund our ongoing operations; or |

| · | Respond to changes in the marketplace. |

Our operating results may fluctuate, and therefore you should not rely on our results in any current or prior reporting period to be indicative of our performance in future reporting periods. Many different factors could cause our operating results to vary from quarter to quarter, including those factors discussed in this “Risk Factors” section.

Management fees received from the Existing Funds will comprise a significant portion of our revenues and a reduction in such fees, including from the termination of Hunting Dog Capital LLC’s role as manager to the Existing Funds, could have an adverse effect on our revenues and results of operations.

With respect to each of the Existing Funds, Hunting Dog Capital LLC is entitled to a management fee described in this prospectus under the heading “Business—Hunting Dog Capital LLC.” If the limited partners of the Existing Funds, or any future managed fund, default on their capital commitments to the fund or the value of investments held by such funds were to decline significantly for any reason, including without limitation, due to short-term changes in market value, mark-to-market accounting requirements or the poor performance of their investments, the amount of the management fees we receive from the Existing Funds, or any future managed funds, would also decline significantly, which could have an adverse effect on our revenues and results of operations.

Fees paid to us, through Hunting Dog Capital LLC, by the Existing Funds and any future managed funds could vary quarter to quarter due to a number of factors, including the limited partners of such funds defaulting on their capital commitments to the funds, such fund’s ability or inability to make investments in companies that meet its investment criteria, the level of its expenses, variations in and the timing of the recognition of realized and unrealized gains or losses of investments held by such funds, the degree to which it encounters competition in its market and its ability to fund investments and general economic conditions. Variability in revenues received from the Existing Funds or any future managed funds would have an adverse effect on our revenues, results of operations and could cause volatility or a decline in the market price of our common stock.

We may be adversely affected by deteriorating economic or business conditions.

Our business, financial condition and results of operations may be adversely affected by various economic factors, including the level of economic activity in the markets in which we operate. Delinquencies, foreclosures, and credit losses generally increase during economic slowdowns or recessions. Because our clients will primarily be lower middle-market businesses, they may be particularly susceptible to economic slowdowns or recessions and may be unable to fulfill their contractual obligations to us pursuant to our financing agreements during these periods. Therefore, to the extent that economic activity or conditions deteriorate, the value of our assets is likely to decrease. Adverse economic conditions also may decrease the value of the collateral securing some of our loans and other financings, as well as the value of any equity in our clients we may hold. Further economic slowdowns or recessions could lead to financial losses and a decrease in our revenues, net income, and assets.

Unfavorable economic conditions may also make it more difficult for us to maintain both our volume of new business origination and the quality of new business at levels previously attained by Hunting Dog Capital LLC. Unfavorable economic conditions also could increase our cost of capital and limit our access to the capital markets. These events could significantly harm our business operations and financial results.

11

Our income associated with Existing Funds may be reduced or eliminated earlier than anticipated due to the loss of certain key persons under the Existing Funds or repayments of principal without the opportunity to redeploy such capital.

Messrs. Allick and Blankfort are each a “key person” pursuant to the limited partnership agreements for the Existing Funds. If either were unable to continue in this capacity, it could constitute a “key person event” which could ultimately lead to reduced or suspended management fees. Additionally, if the Existing Funds experience repayments of principal earlier than anticipated and we are required to remit that principal to the limited partners of the Existing Funds or the Existing Funds incur losses, management fees associated with the Existing Funds could be reduced earlier than we currently anticipate. This could significantly harm our operating results.

There are significant potential conflicts of interest which could adversely impact the returns to our investors.

As part of this offering, we will acquire Hunting Dog Capital LLC, an investment manager of lower middle-market private debt funds that invest in assets similar to those that we will target. Hunting Dog Capital LLC will continue to manage the Existing Funds and may manage similar funds in the future. We will be entitled to receive the management fees associated with Hunting Dog Capital LLC’s management of the Existing Funds and any future managed funds. We will not, however, be entitled to receive any incentive fees associated with operating performance of the Existing Funds and we may not be entitled to receive any incentive fees associated with any similar managed funds in the future. Instead, certain of our directors and executive officers will continue to be entitled to receive the incentive fees associated with the Existing Funds and may be entitled to receive incentive fees associated with any future managed funds.

There may be certain investment opportunities that satisfy the investment criteria for the Existing Funds, any future funds managed by us and us. Although we will endeavor to allocate investment opportunities in a fair and equitable manner, including in accordance with our different investment strategy, we may face conflicts in allocating investment opportunities between us and the Existing Funds or any future managed funds. Because certain of our directors and executive officers may receive incentive fees as a result of their general partnership interests in the Existing Funds or any future managed funds, this may provide an incentive to allocate opportunities to such funds instead of to us. We intend to implement an allocation policy to ensure the equitable distribution of investment opportunities and, as a result, may be unable to participate in certain investments based upon such allocation policy. Please refer to “Business — Transaction Opportunity Allocation”.

In the future, we may borrow money, which may amplify our potential for loss.

As part of our business strategy, we may borrow money from various lenders or investors. These lenders or investors would have fixed-dollar claims on our assets superior to the claims of our common stockholders. If the value of our assets decreases, such leverage would cause the value of our common stock to decline more sharply than it otherwise would if we did not employ leverage. Similarly, any decrease in our income would cause net income to decline more sharply than it would had we not borrowed. Such a decline could negatively affect our ability to make common stock dividend payments, to the extent we make any at all. Our ability to service any debt that we incur will depend largely on our financial performance and will be subject to prevailing economic conditions and competitive pressures.

Any future lenders would likely be secured by a first-priority security interest in our assets. In the case of a liquidation event, those lenders would receive proceeds before our stockholders.

Conversely, we may be unable to obtain leverage we might desire, which could, in turn, adversely affect your return on investment.

We are in a competitive business and some of our competitors have greater resources than we do.

The finance industry is highly competitive, and our competitors also offer financing similar to ours to the lower middle-market companies that are our target clients.

Our competitors include, among others:

| · | Specialty and commercial finance companies; |

| · | Business development companies; |

| · | National and regional commercial and investment banks; |

| · | Private investment funds; |

| · | Private mezzanine funds; |

| · | Factoring companies; |

| · | Insurance companies; and |

| · | Other equity and non-equity based investment funds. |

Some of our competitors have greater financial, technical, marketing, and other resources than we do. We would expect to face increased competition if competitors seek to expand within or enter our target markets. As a result, we may not be able to attract and retain new clients and grow our business, and our market share and future revenues may decline.

12

Risks Related to Our Business

We may not recover the capital that we advance in our transactions.

Although we have not suffered any material credit losses historically, we may experience losses in the future. A credit loss occurs when we determine that all or part of the principal of a particular financing has become unrecoverable and will not be repaid. If we were to experience material losses on the assets held by our subsidiaries, those losses may result in a material adverse effect on our ability to fund our business, as well as to generate revenue, net income, and growth in assets.

While we have not suffered any material credit losses historically, we have experienced missed payments, late payments, failures by clients to comply with operational and financial covenants in their loan agreements, client performance materially below that which we expected when we originated the loan, and the need to pursue principal recovery through receiverships and bankruptcy. In circumstances where we experience difficulty recovering capital, although we may recover all or nearly all of our capital, the cost of doing so may materially harm our operating results.

Our clients are lower middle-market companies, which present greater risks than those associated with larger companies.

The portfolio companies within the Existing Funds, as well as the target market for Hunting Dog Capital Corp. consist exclusively of lower middle-market businesses with annual revenues ranging from approximately $5 million to $50 million. Compared to larger, publicly owned firms, or firms funded by large private equity sponsors, these companies generally have more limited access to capital and higher funding costs, may be in a weaker financial position, and may need more capital to expand or compete. These financial challenges may make it difficult for our clients to make scheduled payments related to our financing transactions, whether mortgage payments, lease payments, or other types of payments. Accordingly, advances made to these types of clients entail higher risks than advances to companies that are able to access traditional credit sources and capital markets.

A number of factors may influence a client’s ability to make scheduled payments on a financing transaction, including the failure to meet its projections or a downturn in its industry. In part because of their smaller size, our clients may:

| · | Experience significant variations in operating results; |

| · | Have narrower product lines and market shares than their larger competitors; |

| · | Be particularly vulnerable to changes in customer preferences and market conditions; |

| · | Be more dependent than larger companies on one or more major customers, the loss of which could materially impair their business, financial condition, and prospects; |

| · | Face intense competition, including from companies with greater financial, technical, managerial, and marketing resources; |

| · | Depend on the management talents and efforts of a single individual or a small group of persons for their success, the death, disability, or resignation of whom could materially harm the client’s financial condition or prospects; |

| · | Have less skilled or experienced management personnel than larger companies; or |

| · | Do business in regulated industries, such as the healthcare industry, and could be affected by policy or regulatory changes. |

Accordingly, any of these factors could impair a client’s cash flow or result in other events, such as bankruptcy, which could limit our ability to recover our capital from that client, and may lead to impairing our assets and decreasing our revenues, net income, and assets.

A client’s fraud could cause us to suffer losses.

A client could defraud us by, among other things:

| · | Directing the proceeds of collections of its accounts receivable to bank accounts other than our established lockboxes or controlled accounts; |

| · | Failing to record accounts-receivable aging accurately; |

| · | Overstating or falsifying records showing accounts receivable; or |

| · | Providing inaccurate reporting of other financial information. |

The failure of a client accurately to report its financial position, compliance with loan covenants, or eligibility for additional financing could result in the loss of some of our principal, including amounts we may not have advanced had we possessed complete and accurate information.

We may be unable to recognize or act upon an operational or financial problem with a client in a timely fashion, so as to prevent a loss of our capital advanced to that client.

Our clients may experience operational or financial problems that, if not timely addressed by us, could result in a substantial impairment or loss of our principal advanced to the client. We may fail to identify problems because our client did not report them in a timely manner or, even if the client did report the problem, we may fail to address it quickly enough or at all. As a result, we could suffer losses which could have a material adverse effect on our assets, revenues, net income, and results of operations.

13

We may not have all of the material information relating to a potential client to enable us to make sound financing decisions with respect to these clients, and we may make errors in evaluating accurate information reported by our clients.

There is generally no publicly available information about the predominantly privately owned companies that are our clients. Therefore, we must rely on information provided by our clients and the due diligence efforts of our employees when making our financing decisions. To some extent, our employees depend and rely upon the management of these companies to provide full and accurate disclosure of material information concerning their business and financial condition. If we do not have access to all the material information about a particular client’s business, financial condition, and prospects, or if a client’s accounting records are poorly maintained or organized, we may not make a fully informed financing decision which may lead ultimately to a failure or inability to recover our funds in their entirety.

We underwrite our loans and will evaluate all future financings based on detailed financial information and projections provided to us by our clients. Even if clients provide us with full and accurate disclosure of all material information concerning their business, we may misinterpret or incorrectly analyze this information. Mistakes by our staff may cause us to engage in transactions that we otherwise would not have, to fund advances that we otherwise would not have funded, or result in losses on one or more of our loans in the Existing Funds. These errors may lead to losses on loans or advances that we would not have made if we had properly evaluated the information.

The non-amortizing loans which we may make, i.e., that do not require periodic repayment of principal, involve a greater degree of risk than other types of financings.

Historically, nearly all of the loans within the Existing Funds have been non-amortizing. A non-amortizing loan is a loan with no scheduled payments of principal before the maturity date of the loan. On the maturity date, the entire unpaid balance of the loan is due. We anticipate that a significant portion of the financing transactions in which Hunting Dog Capital Corp. will engage will similarly require no periodic return of principal.

Non-amortizing loans and similar transactions involve a greater degree of risk than other types of loans and transactions because they require the borrower to make a large final payment upon the maturity of the loan or transaction. The ability of a client to make this final payment typically depends upon its ability either to generate sufficient cash flow, to obtain new financing, or to sell any collateral securing the loan or transaction, if any. The ability of the client to accomplish any of these goals will be affected by many factors, including the availability of financing at rates acceptable to the client, the financial condition of the client, the marketability of any related collateral, the operating history of the related business, tax laws, and the prevailing general economic conditions. Consequently, the client may not have the ability to repay our principal at maturity and we could lose all or most of the principal associated with the transaction.

There is no active trading market for the loans or assets we anticipate creating or acquiring with the net proceeds of this offering. Consequently, we may not be able to convert any of these loans or assets to cash at a favorable price, or at all.

We may seek to dispose of one or more of our loans or other assets to obtain liquidity or to reduce potential losses with respect to non-performing assets. There is no established trading market for our loans or the other assets we anticipate creating or acquiring with the net proceeds of this offering. Consequently, if we seek to sell a loan or other asset, or otherwise convert a loan or other asset to cash, there is no guarantee that we will be able to do so at a favorable price, or at all.

A concentration of loans or other assets with a limited number of clients within a particular industry, such as the retail or manufacturing industry, or within a geographic region, could impair our revenues if the industry or region were to experience economic difficulties.

Our clients’ failing to comply with their contractual obligations to us may be correlated with economic conditions affecting particular industries or geographic regions. As a result, if any particular industry or geographic region were to experience economic difficulties, the overall timing and amount of principal, interest, lease, mortgage, or other payments to us by our clients operating in those industries or geographic regions may differ from what we expected, and result in material harm to our revenues, net income, and assets.

The collateral securing a loan or a particular asset, such as a mortgage or lease, may not be sufficient to protect us from a partial or complete loss if the loan or asset becomes non-performing and we are required to foreclose.

While all of the loans in the Existing Funds are secured by a blanket lien on nearly all of our clients’ assets, there is no assurance that the collateral securing any particular loan will protect us from suffering a partial or complete loss if the loan becomes non-performing and we move to foreclose on the collateral. The collateral securing the loans in the Existing Funds is subject to inherent risks that may limit our ability to recover the principal of a non-performing loan. Shareholders in Hunting Dog Capital Corp. will not suffer any capital loss if loans within the Existing Funds were to be impaired or written off, but may suffer reduced or foregone management fee income.

14

We anticipate engaging in financings with tangible assets as underlying collateral, such as mortgage financings or financings based on specified receivables. That collateral is subject to inherent risks that may limit our ability to recover our principal. Listed below are some of the risks that may affect the value of different types of collateral.

Inventory. Inventory may not be adequate to secure our loans or other financings fully, if, among other things, any of the following occur:

| · | Our valuation of the inventory at the inception of the transaction was not accurate; |

| · | The demand for the inventory declines or the inventory becomes obsolete; |

| · | The value of the inventory, for example, inventory in the retail industry, decreases because of seasonal fluctuation; |

| · | The inventory is made up of several component parts and the value of those parts falls below expected levels; or |

| · | The client misrepresents, or does not keep adequate records of, important information concerning the inventory, such as the quantity or quality of the inventory on hand. |

Accounts Receivable. Factors that could reduce the value of accounts receivable securing our loans or other financings include, among other things:

| · | Problems with the clients’ underlying product or services that result in greater than anticipated returns or disputed accounts; |

| · | Unrecorded liabilities, such as rebates, warranties, or offsets; |

| · | The disruption or bankruptcy of key customers responsible for material amounts of the accounts receivable; or |

| · | The client misrepresents or does not keep adequate records of important information concerning the amounts or aging of its accounts receivable. |

Equipment. The equipment of a client securing a loan or related to another financing, such as a lease where we own the equipment and lease it to a client, could lose value as a result of, among other things:

| · | Changes in market or industry conditions; |

| · | The failure of the client to maintain or repair the equipment; or |

| · | Changes in technology or advances in new equipment that render the equipment obsolete or of limited value. |

Real Estate. The real estate of a client securing a loan or related to another financing could lose value as a result of, among other things:

| · | Changes in general or local market conditions; |

| · | Changes in the occupancy or rental rates of the property or, for a property that requires leasing, a failure to lease the property in accordance with the projected leasing schedule; |

| · | Limited availability of mortgage funds or fluctuations in interest rates, which may render the sale and refinancing of a property difficult; |

| · | Development projects that experience cost overruns or otherwise fail to perform as projected; |

| · | Unanticipated increases in real estate taxes and other operating expenses; |

| · | Challenges to the client’s claim of title to the real property; |

| · | Environmental considerations; |

| · | Zoning laws; |

| · | Other governmental rules and policies; or |

| · | Uninsured losses, including possible acts of terrorism or a decline in the operational performance at a facility on the real property, such as a nursing home, hospital, or other facility. |

Any one or more of the preceding factors could materially impair our ability to recover principal in a foreclosure on the related loan or other financing. To the extent we are unable to underwrite and manage our loans or other financings successfully, or the credit quality of our clients or the value of any underlying collateral declines, our financial results may suffer materially.

Our business model depends to a significant extent upon strong referral relationships and our inability to maintain or develop these relationships, or the failure of these relationships to generate investment opportunities, could adversely affect our business.

We expect that members of our management team will maintain their relationships with regional and boutique banks and self-employed investment bankers/advisers, as well as attorneys, accountants, auditors, business brokers, and other contract financial professionals, and we will rely to a significant extent upon these relationships to provide us with potential investment opportunities. Historically, approximately 75% of the investments made by Hunting Dog Capital LLC through its managed funds were derived from the referral network. If our management team fails to maintain its existing relationships or develop new relationships with other sponsors or sources of investment opportunities, we will not be able to grow our investment portfolio. In addition, individuals with whom members of our management team have relationships are not obligated to provide us with investment opportunities, and, therefore, there is no assurance that such relationships will generate investment opportunities for us.

There will be uncertainty as to the value of our financial assets.

A large percentage of our investments will be in the form of financial assets that are not publicly traded, and their fair value may not be readily determinable. We will value these assets in accordance with our valuation policy, which is consistent with U.S. generally accepted accounting principles (“GAAP”), based on various factors, including (a) the nature and realizable value of any collateral; (b) the portfolio company’s ability to make payments and its earnings; (c) the markets in which the portfolio company does business; (d) comparisons to publicly traded companies; and (e) discounted cash flow. We may also use the services of third-party valuation firms to aid in determining the fair value of these assets.

Because such valuations, and particularly valuations of private securities and private companies, are inherently uncertain, may fluctuate over short periods of time, and may be based on estimates, our determinations of fair value may differ materially from the values that would have been used if a ready market for these securities existed. Our results of operations could be adversely affected if our determinations of the fair value of our investments were to be materially higher than the values that we ultimately realize upon the disposal of such assets.

15

To the extent payment-in-kind (“PIK”) interest constitutes a portion of our income, we will be exposed to typical risks associated with such income being required to be included in taxable and accounting income prior to receipt of cash representing such income.

Our loans may include contractual PIK interest. To the extent PIK interest constitutes a portion of our income, we will be exposed to typical risks associated with such income being required to be included in taxable and accounting income prior to receipt of cash, including the following:

| • | PIK loans may have unreliable valuations because their continuing accruals require continuing judgments about the collectability of the deferred payments and the value of the collateral; |

| • | PIK interest typically has the effect of increasing the outstanding principal amount of a loan, resulting in a borrower owing more at the end of the term of the loan than what it owed when the loan was originated; and |

| • | PIK instruments may represent a higher credit risk than coupon loans. |

Our ability to grow depends in part on our ability to obtain additional capital.

We anticipate that we will need to access the capital markets periodically to raise cash to fund new investments. If we do not have adequate capital available for investment, our performance could be adversely affected. We may use debt financing and issue additional securities to fund our growth. Unfavorable economic or capital market conditions may increase our funding costs, limit our access to the capital markets, or result in a decision by lenders not to extend credit to us. An inability to access the capital markets successfully could limit our ability to grow our business and fully execute our business strategy, and could decrease our earnings, if any.

Risks Related to the Investment Company Act and Being a Public Company

If we are required to register under the Investment Company Act, our ability to conduct our business could be materially adversely affected.

We do not intend to become registered as an “investment company” under the Investment Company Act because we believe the nature of our assets and the sources of our income exclude us from the definition of an investment company pursuant to Section (3)(a)(1)(C) under the Investment Company Act. Accordingly, we are not subject to the provisions of the Investment Company Act, such as conflict of interest rules, requirements for disinterested directors and other substantive provisions which were enacted to protect investors in “investment companies.”

Generally, a company is an “investment company” if it is or holds itself out as being engaged primarily in the business of investing, reinvesting or trading in securities or owns or proposes to own investment securities having a value exceeding 40% of the value of its total assets (exclusive of U.S. government securities and cash items) on an unconsolidated basis, unless an exception, exemption or safe harbor applies. We refer to this investment company definition test as the “40% Test.”