Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - TopBuild Corp | bld-20151231ex312769f75.htm |

| EX-10.10 - EX-10.10 - TopBuild Corp | bld-20151231ex10102fb61.htm |

| EX-31.1 - EX-31.1 - TopBuild Corp | bld-20151231ex3113f4a31.htm |

| EX-10.11 - EX-10.11 - TopBuild Corp | bld-20151231ex10110fc1d.htm |

| EX-10.9 - EX-10.9 - TopBuild Corp | bld-20151231ex10983c784.htm |

| EX-32.1 - EX-32.1 - TopBuild Corp | bld-20151231ex32195401d.htm |

| EX-32.2 - EX-32.2 - TopBuild Corp | bld-20151231ex322d540d8.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

(Mark One) |

|

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 1-36870

TopBuild Corp.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware

(State or Other Jurisdiction of Incorporation or |

47-3096382

(I.R.S. Employer |

|

260 Jimmy Ann Drive Daytona Beach, Florida (Address of Principal Executive Offices) |

32114 (Zip Code) |

(386) 304-2200

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Name of each exchange on which registered |

|

|

Common stock, par value $0.01 per share |

New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.

☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporate by reference in Part III of this Form 10-K or any amendment to this Form 10-K.☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☐ Smaller reporting company ☐ Non-accelerated filer ☒ (Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant based on the closing price of $29.00 per share as reported on the New York Stock Exchange on June 30, 2015, was approximately $1.1 billion.

Number of shares of common stock outstanding as of February 26, 2016: 37,833,855

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for its 2016 Annual Meeting of Shareholders, to be filed with the Securities and Exchange Commission no later than 120 days after December 31, 2015, are incorporated by reference into Part III of this Form 10-K.

TOPBUILD CORP.

2

Overview

TopBuild Corp., headquartered in Daytona Beach, Florida, is the leading installer and distributor of insulation products to the United States construction industry, based on revenue. Prior to June 30, 2015, we operated as a subsidiary of Masco Corporation, which trades on the New York Stock Exchange (“NYSE”) under the symbol “MAS.” We were incorporated in Delaware in February 2015 as Masco SpinCo Corp. and we changed our name to TopBuild Corp. on March 20, 2015. On June 30, 2015, the separation from Masco (“Separation”) was completed and on July 1, 2015, we began trading on the NYSE under the symbol “BLD.”

Segment Overview

Installation (TruTeam)

We provide insulation installation services nationwide through our TruTeam contractor services business which has over 180 installation branches located in 44 states.

Various insulation applications we install include:

|

· |

Fiberglass batts and rolls |

|

· |

Blown-in loose fill fiberglass |

|

· |

Blown-in loose fill cellulose |

|

· |

Polyurethane spray foam |

In addition to insulation products, which represented 73% of our installation segment’s sales, we also install other building products including rain gutters, garage doors, fireplaces, shower enclosures, and closet shelving.

We handle every stage of the installation process including material procurement supplied by leading manufacturers, project scheduling and logistics, multi-phase professional installation, and installation quality assurance. The amount of insulation in a new home is regulated by various building and energy codes.

Our TruTeam customer base includes the largest single-family homebuilders in the United States (“U.S.”) as well as local/single-family custom builders, multi-family builders, commercial general contractors, remodelers, and individual homeowners.

Through our Home Services subsidiary and our Environments For Living® program, we offer a number of services and tools designed to assist builders with applying the principles of building science to new home construction. This includes pre-construction plan reviews that use industry-standard home-energy analysis software, various inspection services, and diagnostic testing. We believe our Home Services subsidiary is one of the largest Home Energy Rating System Index (HERS) raters in the U.S.

Distribution (Service Partners)

We distribute insulation and other building products including rain gutters, fireplaces, closet shelving, and roofing materials through our Service Partners business, which has over 70 distribution centers in 35 states.

Our Service Partners customer base consists of thousands of insulation contractors of all sizes, gutter contractors, weatherization contractors, other contractors, dealers, metal building erectors, and modular home builders.

3

For further information on our segments, see Item 8, Financial Statements and Supplementary Data, Note 7 - Segment Information.

Background

Demand for our insulation products and services is driven by new single-family residential and multi-family construction, remodeling and repair activity, commercial construction, building codes, and the growing need for energy efficiency. Being a leader in both installation and distribution allows us to more effectively reach a broader set of customers, regardless of their size or geographic location within the U.S. We recognize that competition for the installation and sale of insulation and other building products occurs in localized geographic markets throughout the country, and as such our operating model is based on branches building and maintaining local customer relationships. At the same time, our local operations benefit from centralized functions such as information technology, credit, and purchasing.

Competitive Advantages

The market for the distribution and installation of building products is highly fragmented and competitive. Barriers to entry for local competitors are relatively low, increasing the risk that additional competitors will emerge. Our ability to maintain our competitive position in our industry depends on a number of factors including our national scale, sales channels, diversified product lines, a strong local presence, and strong cash flows.

National scale. With our national footprint, we provide products and services to each major construction line of business in the U.S. Our national scale, together with our centralized TopBuild executive management team, allows us to compete locally by:

•Providing national and regional builders with broad geographic reach, while maintaining consistent policies and practices that enable reliable, high‑quality products and services across many geographies and building sites

•Establishing strong ties to major manufacturers of insulation and other building products that help ensure we are buying competitively, have availability of supply to our local branches and distribution centers and are driving efficiencies throughout our supply chain

•Providing consistent, customized support and geographic coverage to our customers

•Maintaining an operating capacity that allows us to ramp‑up rapidly, without major incremental investment, to target forecasted growth in housing starts and construction activity in each of our lines of business anywhere in the U.S.

•Leveraging investments in systems and processes and sharing best practices across both our installation and distribution businesses

Two avenues to reach the builder. We believe having both an installation and distribution business provides a number of advantages to reaching our customers and driving share gains. Our installation business customer base includes builders of all sizes. Our branches go to market with the local brands that small builders recognize and value, and our national footprint is appealing to large builders who value consistency across a broad geography. Our distribution business focuses on selling to small contractors who are particularly adept at cultivating the local relationships with small custom builders. Being a leader in both installation and distribution allows us to more effectively reach a broader set of builder customers, regardless of their size or geographic location within the U.S., and leverage housing growth wherever it occurs.

Diversified lines of business. In response to the housing downturn in prior years, we enhanced our ability to serve the residential repair/remodel and commercial construction markets. Although the residential repair/remodel and commercial construction markets are affected by many of the same macroeconomic and local economic factors that drive residential new construction, residential repair/remodel and commercial construction have historically followed different cycles than

4

residential new construction. We have thus positioned our business to benefit from a greater mix of residential repair/remodel activity and commercial construction activity than we have historically, which helps reduce volatility because we are less dependent on residential new construction, and also enables us to better respond to changes in customer demand.

Strong local presence. Competition for the installation and sale of insulation and other building products to builders occurs in localized geographic markets throughout the country. Builders in each local market have different options in terms of choosing among insulation installers and distributors for their projects, and value local relationships, quality and timeliness. Our installation branches are locally branded businesses that are recognized within the communities in which they operate. Our distribution centers service primarily local contractors, lumberyards, retail stores and others who, in turn, service local homebuilders and other customers. Our branch‑ and distribution center‑based operating model, in which individual branches and distribution centers maintain local customer relationships, enables us to develop local, long‑tenured relationships with these customers, build local reputations for quality, service and timeliness and provide specialized products and personalized services tailored to a geographic region. At the same time, our local operations benefit from centralized functions such as information technology, credit and purchasing, and the resources and scale efficiencies of an installation and distribution business that has a presence across the U.S.

Reduced exposure to residential housing cyclicality. During industry downturns many insulation contractors, who buy directly from manufacturers during industry peaks, return to purchasing through distributors for small, “Less Than Truckload” shipments, reduced warehousing needs, and access to purchases on credit. This drives incremental customers to Service Partners during these points in the business cycle. As a result, our leadership position in both installation and distribution helps to reduce exposure to cyclical swings in our lines of business.

Strong cash flow, low capital investment, and favorable working capital fund organic growth. Over the last several years, we have reduced fixed costs. As a result, we can achieve profitability at lower levels of demand as compared to historical periods. For further discussion on our cash flows and liquidity, see Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources.

Major Customers

We have a diversified portfolio of customers and no single customer accounted for 3% or more of our total revenues. Our top ten customers accounted for approximately 10% of our total sales in 2015.

Backlog

Due to our customers’ need for timely installation of our products, our installation jobs are scheduled and completed within a short timeframe. We do not consider backlog material to our business.

Suppliers

Our businesses depend on our ability to obtain an adequate supply of high quality products and components from manufacturers and other suppliers. We rely heavily on third party suppliers for our products and key components. We source the majority of our building products from four primary U.S. based residential fiberglass insulation manufacturers: Owens Corning, Knauf, CertainTeed, and Johns Manville. Failure by our suppliers to provide us with an adequate supply of high quality products on commercially reasonable terms, or to comply with applicable legal requirements, could have a material, adverse effect on our financial condition or operating results. We believe we have good relationships with our suppliers.

Employees

At December 31, 2015, we had approximately 8,000 employees. Approximately 490 of our employees are currently covered by collective bargaining or other similar labor agreements.

5

Executive Management

See Item 10, Directors, Executive Officers, and Corporate Governance.

Legislation and Regulation

We are subject to U.S., state and local regulations, particularly those pertaining to health and safety (including protection of employees and consumers), labor standards/regulations, contractor licensing, and environmental issues. In addition to complying with current effective requirements and requirements that will become effective at a future date, even more stringent requirements could eventually be imposed on our industries. Additionally, some of our products and services may require certification by industry or other organizations. Compliance with these regulations and industry standards may require us to alter our distribution and installation processes and our sourcing, which could adversely impact our competitive position. Further, if we do not effectively and timely comply with such regulations and industry standards, our operating results could be negatively affected.

Additional Information

We make available free of charge on our website, www.topbuild.com, our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, and our Current Reports on Form 8-K as soon as reasonably practicable after these reports are filed with or furnished to the Securities and Exchange Commission (the “SEC”).

There are a number of business risks and uncertainties that could affect our business. These risks and uncertainties could cause our actual results to differ from past performance or expected results. We consider the following risks and uncertainties to be most relevant to our business activities. Additional risks and uncertainties not presently known to us, or that we currently believe to be immaterial, also may impact our business, financial condition, and results of operations. We urge investors to consider carefully the risk factors described below in evaluating the information contained in this Report.

Our historical financial information is not necessarily indicative of our future financial condition or future results of operations, nor does it reflect what our financial condition or results of operations would have been as an independent public company during the periods presented prior to the Separation.

Our historical financial information included in this Report is not necessarily indicative of our future financial condition, future results of operations or future cash flows, nor does it reflect what our financial condition, results of operations, or cash flows would have been as an independent public company during the periods presented prior to the Separation. In particular, the historical financial information included in this Report is not necessarily indicative of our future financial condition, results of operations, or cash flows primarily because of the following factors:

|

· |

Our historical financial results for the periods prior to the Separation reflect allocations of expenses for services historically provided by Masco, and this allocation of Masco corporate expenses may be significantly lower than the comparable expenses we would have incurred as an independent company. |

|

· |

Our working capital requirements and capital expenditures historically have been satisfied as part of Masco’s corporate‑wide cash management and capital expenditure programs, and our cost of debt and other capital may have significantly differed from that reflected in our historical financial statements. |

|

· |

The historical financial information prior to the Separation may not fully reflect the costs associated with being an independent public company. |

6

We have limited history operating as an independent public company. We have incurred significant costs to create the corporate infrastructure necessary to operate as an independent public company, and may continue to do so.

We currently pay Masco for certain support services on a transitional basis and Masco will continue to provide some of these services to us, generally through June 30, 2016, with a possible extension of 12 months, pursuant to the Transition Services Agreement. Any interruption in these services could have a material adverse effect on our business, financial condition, results of operations, and cash flows. In addition, at the end of this transition period, we will need to perform these functions ourselves or hire third parties to perform these functions on our behalf. The costs associated with performing or outsourcing these functions may exceed the amounts reflected in our historical financial statements or that we have agreed to pay Masco during the transition period. A significant increase in the costs of performing or outsourcing these functions could materially and adversely affect our business, financial condition, results of operations, and cash flows.

Our business relies on residential new construction activity, and to a lesser extent on residential repair/remodel and commercial construction activity, all of which are cyclical and not fully recovered from the housing crisis.

Our business relies on residential new construction activity and, to a lesser but significant extent on residential repair/remodel and commercial construction activity in the U.S., which is cyclical. Macroeconomic and local economic conditions, including consumer confidence levels, fluctuations in home prices, unemployment and underemployment levels, student loan debt, household formation rates, the age and volume of the housing stock, the availability of home equity loans and mortgages and the interest rates for such loans, and other factors, affect consumers’ discretionary spending on both residential new construction projects and residential repair/remodel activity. The commercial construction market is affected by macroeconomic and local economic factors such as interest rates, credit availability for commercial construction projects, material costs, employment rates, office vacancy rates, and office absorption rates. Adverse changes or uncertainty regarding these and other factors could result in a decline in spending on residential new construction, residential repair/remodel, and commercial construction projects, which could adversely affect our results of operations and our financial position.

While improving, residential new construction, residential repair/remodel, and commercial construction activity (including consumer spending for big ticket remodeling projects) continue to be below historical average levels, which has affected our operating results. While markets have stabilized from the downturn in recent years, there remains significant uncertainty regarding the timing and extent of a full recovery in residential new construction and residential repair/remodel activity and the resulting demand levels for building products we install and/or distribute. In addition to the influence of cyclical macroeconomic and local conditions discussed above, other factors that pose challenges for the markets to return to historical levels of activity include:

|

· |

A significant number of homeowners have outstanding principal balances on their mortgage loans which exceed the market value of their homes, impeding their ability to purchase another home or begin a remodeling project they may desire and otherwise be able to afford. |

|

· |

While decreasing, there are relatively high levels of mortgage loan delinquencies, defaults, and foreclosures that could add to an inventory of lender‑owned homes that may be sold in competition with new and resale homes at low, distressed prices or that generate short sales activity at such price levels. |

|

· |

The size and nature of new homes decreased during the downturn and shifted to a greater mix of multi‑family housing units such as apartments and condominiums, which are often smaller than single‑family housing units and require less insulation and other building products. |

|

· |

Tighter lending standards and practices for mortgage loans limit consumers’ ability to qualify for mortgage financing to purchase a home. |

|

· |

Tighter lending standards for commercial credit for smaller builders, as well as for the development of new lots, limit builders’ ability to qualify for financing for new development. |

7

|

· |

Relatively high levels of student debt and consumer debt, and relatively low consumer confidence, inhibit consumers’ willingness to accept available financing for new construction. |

|

· |

Certain unfavorable demographic trends, such as historically low household formation rates, tend to result in lower home ownership rates than historical averages. |

Given these challenges, the present recovery may not continue or gain further momentum and activity in our lines of business may not return to historic levels, which would have a significant adverse effect on the growth potential of our business, and on our financial condition, operating results, and cash flows.

We may not be successful in integrating acquisitions.

Part of our strategy to grow our business is dependent on our ability to make acquisitions that result in an increase in revenues and operating profit.

Our acquisition strategy requires that we successfully integrate acquired companies into our business practices as well as our procurement, management, and our enterprise-wide information technology systems. We may not be successful in implementing our business practices or systems. Any such difficulties, or increased costs associated with such integration, could affect our financial performance and operations.

If we are unable to integrate acquisitions, it could have a material adverse effect on our growth strategy, business, financial condition, and results of operations.

We are dependent on third‑party suppliers and manufacturers providing us with an adequate supply of high quality products, and the loss of a key supplier or manufacturer could negatively affect our operating results.

Our installation and distribution businesses depend on our ability to obtain an adequate supply of high quality products and components from manufacturers and other suppliers. We rely heavily on third‑party suppliers for our products and key components. Failure by our suppliers to provide us with an adequate supply of high quality products on commercially reasonable terms, or to comply with applicable legal requirements, could have a material adverse effect on our financial condition or operating results. We procure our materials, primarily fiberglass insulation, from leading manufacturers in the industry. While we believe that we have strong relationships with our suppliers, the fiberglass insulation industry has encountered both shortages and periods of significant oversupply during past housing market cycles, leading to volatility in prices and allocations of supply. This volatility of selling prices and materials availability has in the past had, and may in the future have, a significant impact on our results of operation. While we do not believe we depend on any sole or limited source of supply, we do source the majority of our building products, primarily insulation, from a limited number of large suppliers. Any re-sourcing of building products to one or more new supplier could, therefore, take time and involve significant costs. Accordingly, the loss of a key supplier, or a substantial decrease in the availability of products or components from our suppliers, could disrupt our business and adversely impact our operating results.

The long‑term performance of our businesses relies on our ability to attract, develop, and retain talented personnel, including sales representatives, branch managers, installers, and truck drivers, while controlling our labor costs.

To be successful, we must attract, develop, and retain highly qualified and talented personnel who have the experience, knowledge, and expertise to successfully implement our key business strategies. We also must attract, develop, and retain our sales and labor force while maintaining labor costs. We compete for employees, including branch managers, sales people, regional management, and executive officers, with a broad range of employers in many different industries, and we invest significant resources in recruiting, developing, motivating, and retaining them. The failure to attract and retain key employees, or to develop effective succession planning to assure smooth transitions of those employees and their knowledge, customer relationships, and expertise could negatively affect our competitive position and operating results. Further, as the economy continues to recover, if we are unable to cost‑effectively recruit, train, and retain sufficient skilled sales and labor personnel, including sales representatives, branch managers, installers, and truck drivers, we may not be able to adequately satisfy increased demand for our products and services, which could impact our operating results. In

8

the past, we have also experienced challenges securing personnel for certain of our labor force due to lack of proper immigration status.

Our ability to control labor costs and attract qualified labor is subject to numerous external factors including prevailing wage rates, labor shortages, the impact of legislation or regulations governing wages and hours, labor relations, immigration, healthcare benefits, and other insurance costs. In addition, we compete with other companies to recruit and retain qualified installers and truck drivers in a tight labor market, and we invest significant resources in training and motivating them to maintain a high level of job satisfaction. These positions generally have high turnover rates, which can lead to increased training and retention costs. If we are unable to attract or retain qualified employees, it could adversely impact our operating results.

Because we operate our business through highly dispersed locations across the U.S., our operations may be materially adversely affected by inconsistent practices and the operating results of individual branches and distribution centers may vary.

We operate our business through a network of dispersed branch locations and distribution facilities throughout the U.S., supported by corporate executives and services in our headquarters, with branch and regional management retaining responsibility for day‑to‑day operations and adherence to applicable local laws. Our operating structure can make it difficult for us to coordinate procedures across our operations. In addition, our branches and distribution facilities may require significant oversight and coordination from headquarters to support their growth. Inconsistent implementation of corporate strategy and policies at the local or regional level could materially and adversely affect our overall profitability, business, results of operations, financial condition, and prospects.

In addition, the operating results of a specific individual branch or distribution facility may differ from that of another branch or distribution facility for a variety of reasons including business apportionment, management practices, competitive landscape, regulatory requirements, and local economic conditions. As a result, certain of our branches or distribution facilities may experience higher or lower levels of growth than other branches or distribution facilities. Therefore, our overall financial performance and results of operations may not be indicative of the performance and results of operations of any individual branch or distribution facility.

Our profit margins could decrease due to changes in the costs of the products we install and/or distribute.

The principal building products that we install and distribute have been subject to price changes in the past, some of which have been significant. Our results of operations for individual quarters can be, and have been, hurt by a delay between the time building product cost increases are implemented and the time we are able to increase prices for our installation or distribution services, if at all. Our supplier purchase prices may depend on our purchasing volume or other arrangements with any given supplier. While we have been able to achieve cost savings through volume purchasing or other arrangements with suppliers in the past, we may not be able to continue to receive advantageous pricing for the products we distribute and install. If we are unable to maintain pricing consistent with prior periods, our costs could increase and our margins may be adversely affected, which could have a material adverse effect on our financial condition, results of operations, and cash flows.

Increases in fuel costs could adversely affect our results of operations.

The price of oil has fluctuated over the last few years, creating volatility in our fuel costs. We do not currently hedge our fuel costs. Increases in fuel costs can negatively impact our costs to deliver our products to our customers and thus increase our cost of sales. If we are unable to increase the selling price of our products to our customers to cover any increases in fuel costs, results of operations may be adversely affected.

We face significant competition.

The market for the distribution and installation of building products is highly fragmented and competitive. Barriers to entry for local competitors are relatively low, increasing the risk that additional competitors will emerge. We face significant pricing pressure from competitors in both our installation and distribution businesses. In addition to price, we

9

believe that competition in our industry is based largely on customer service and the quality and timeliness of installation services and distribution product deliveries in each local market. Our installation competitors include national contractors, regional contractors, and local contractors, and we face many or all of these competitors for each project on which we bid. Our insulation distribution competitors include specialty insulation distributors (one multi‑regional, several regional, and numerous local). In some instances, our insulation distribution business sells products to companies that may compete directly with our installation service business. We also compete with broad line building products distributors, big box retailers, and insulation manufacturers.

Our ability to maintain our competitive position in our industry and grow our businesses depends upon successfully maintaining our relationships with major suppliers and customers; cost‑effectively recruiting and retaining our sales and labor force including key sales representatives, branch managers, installers, and truck drivers in a tight labor market; delivering superior customer service and quality installations; implementing growth strategies; leveraging our scale; and managing our cost structure, none of which is assured. If we are unable to compete effectively, our business, financial condition, results of operations, and cash flows would be materially and adversely affected.

Our business is seasonal and is susceptible to adverse weather conditions and natural disasters.

Our industry is seasonal. We normally experience stronger sales during the third and fourth calendar quarters, corresponding with the peak season for residential new construction and residential repair/remodel activity. Sales during the winter weather months are seasonally slower due to the lower construction activity. Historically, the installation of insulation lags housing starts by several months.

In addition, to the extent that hurricanes, severe storms, earthquakes, droughts, floods, fires, other natural disasters, or similar events occur in the geographic areas in which we operate, our business may be adversely affected.

Severe weather and natural disasters can cause delays or halts and increased costs in the construction of new homes, residential repair/remodeling projects, and commercial construction projects. We may underestimate the impact of seasonality in any given period. Severe weather is often unpredictable, which contributes to earnings volatility and makes forecasting our results of operation more difficult. Severe weather and seasonality may have an adverse impact on our business, including our financial position, cash flows from operations, and results of operations.

In addition, we may experience business interruptions and property or other damage due to severe weather or natural disasters. If insurance is unavailable to us or is unavailable on acceptable terms, or if our insurance is not adequate to cover business interruption or losses resulting from adverse weather or natural disasters, our business and results of operations will be adversely affected. In addition, damage to homes or commercial sites caused by adverse weather or a natural disaster can cause our insurance costs to increase.

Claims and litigation could be costly.

We are, from time to time, involved in various claims, litigation matters, and regulatory proceedings that arise in the ordinary course of our business and which could have a material adverse effect on us. These matters may include contract disputes, automobile liability and other personal injury claims, warranty disputes, environmental claims or proceedings, other tort claims, employment and tax matters, and other proceedings and litigation, including class actions.

We rely on our suppliers to provide us with the building products that we install and/or distribute. Due to the difficulty of controlling the quality of products sourced from our suppliers, we are exposed to risks relating to the quality of such products and to limitations on our recourse against such suppliers.

In addition, we are exposed to potential claims by our employees or others based on job related hazards. For example, certain types of insulation, particularly spray foam applications, require our employees to handle potentially hazardous or toxic substances. While we place significant focus on employee safety and our employees who handle potentially hazardous or toxic materials, including but not limited to lead‑based paint, receive specialized training and wear protective clothing, there is still a risk that they, or others, may be exposed to these substances. Exposure to these substances could

10

result in significant injury to our employees and others, including site occupants, and damage to our property or the property of others, including natural resource damage, for which we may be liable.

We have also experienced class action lawsuits in recent years predicated upon claims for antitrust, product liability, construction defects, competition, and wage and hour issues. We have generally denied liability and have vigorously defended these cases. Due to their scope and complexity, however, these lawsuits can be particularly costly to defend and resolve, and we have and may continue to incur significant costs as a result of these types of lawsuits.

Our builder and contractor customers are subject to construction defect and warranty claims in the ordinary course of their business. Our contractual arrangements with these customers may include our agreement to defend and indemnify them against various liabilities. These claims, often asserted several years after completion of construction, can result in complex lawsuits or claims against the builders, contractors, and many of their subcontractors, including us, and may require us to incur defense and indemnity costs even when our services or distributed products are not the principal basis for the claims.

Although we intend to defend all claims and litigation matters vigorously, given the inherently unpredictable nature of claims and litigation, we cannot predict with certainty the outcome or effect of any claim or litigation matter.

We expect to maintain insurance against some, but not all, of these risks of loss resulting from claims and litigation. We may elect not to obtain insurance if we believe the cost of available insurance is excessive relative to the risks presented. The levels of insurance we maintain may not be adequate to fully cover any and all losses or liabilities. If any significant accident, judgment, claim, or other event is not fully insured or indemnified against, it could have a material adverse impact on our business, financial condition, and results of operations.

We may not be able to identify new products and new product lines and integrate them into our distribution network, which may impact our ability to compete. Our expansion into new markets may present competitive, distribution, and regulatory challenges that differ from current ones.

Our business depends in part on our ability to identify future products and product lines that complement existing products and product lines and that respond to our customers’ needs. We may not be able to compete effectively unless our product selection keeps up with trends in the markets in which we compete or trends in new products. In addition, our ability to integrate new products and product lines into our distribution network could affect our ability to compete. The success of new products and new product lines will depend on market demand and there is a risk that new products and new product lines will not deliver expected results, which could negatively impact our future sales and results of operations. Our expansion into new markets may present competitive, distribution, and regulatory challenges that differ from current ones. We may be less familiar with new product categories and may face different or additional risks, as well as increased or unexpected costs, compared to existing operations. Growth into new markets may also bring us into direct competition with companies with whom we have little or no past experience as competitors and may not be supported by our historical product suppliers. To the extent we are reliant upon expansion into new geographic, industry, and product markets for growth and do not meet the new challenges posed by such expansion, our future sales growth could be negatively impacted, our operating costs could increase, and our business operations and financial results could be negatively affected.

We may be adversely affected by any natural or man‑made disruptions to our facilities.

We currently maintain a broad network of distribution facilities and installation branches throughout the U.S. Any widespread disruption to our facilities resulting from fire, earthquake, weather‑related events, an act of terrorism, or any other cause could damage a significant portion of our inventory and supply stock, and could materially impair our ability to provide installation and/or distribution services for our customers. Moreover, we could incur significantly higher costs and longer lead times associated with our installation and distribution services to our customers during the time that it takes for us to reopen or replace a damaged facility. If any of these events were to occur, our financial condition, operating results, and cash flows could be materially and adversely affected.

11

We are subject to competitive pricing pressure from our customers.

Residential homebuilders historically have exerted significant pressure on their outside suppliers to keep prices low because of their market share, and ability to leverage such market share, in the highly fragmented building products supply and services industry. The housing industry downturn resulted in significantly increased pricing pressures from homebuilders and other customers. These pricing pressures have adversely affected our operating results and cash flows. In addition, consolidation among homebuilders, and changes in homebuilders’ purchasing policies or payment practices could result in additional pricing pressure. Moreover, during the housing downturn, several of our homebuilder customers defaulted on amounts owed to us or extended their payable days as a result of their financial condition. If such payment failures or delays were to recur, it could significantly adversely affect our financial condition, operating results, and cash flows.

The development of alternatives to distributors in the supply chain could cause a decrease in our sales and operating results and limit our ability to grow our business.

Our distribution customers could begin purchasing more of their product needs directly from manufacturers, which would result in decreases in our net sales and earnings. Our suppliers could invest in infrastructure to expand their own local sales force and sell more products directly to our distribution customers, which also would negatively impact our business. In addition, our distribution customers may elect to establish their own building products manufacturing and distribution facilities, or give advantages to manufacturing or distribution intermediaries in which they have an economic stake. These changes in the supply chain could adversely affect our financial condition, operating results, and cash flows.

Union organizing activity and work stoppages could delay or reduce availability of products that we install and increase our costs.

Approximately 490 of our employees are currently covered by collective bargaining or other similar labor agreements that expire on various dates from May 2016 through June 2019. Any inability by us to negotiate collective bargaining arrangements could cause strikes or other work stoppages, and new contracts could result in increased operating costs. If any such strikes or other work stoppages occur, or if other employees become represented by a union, we could experience a disruption of our operations and higher labor costs. Further, if a significant number of additional employees were to unionize, including in the wake of any future legislation that makes it easier for employees to unionize, these risks would increase. In addition, certain of our suppliers have unionized work forces, and certain of the products we install and/or distribute are transported by unionized truckers. Strikes, work stoppages, or slowdowns could result in slowdowns or closures of facilities where the products that we install and/or distribute are manufactured, or could affect the ability of our suppliers to deliver such products to us. Any interruption in the production or delivery of these products could delay or reduce availability of these products and increase our costs.

If we are required to take significant non‑cash charges, our financial resources could be reduced and our financial flexibility may be negatively affected.

We have recorded significant goodwill and other intangible assets related to prior business combinations on our balance sheet. The valuation of these assets is largely dependent upon the expectations for future performance of our businesses. Expectations about the growth of residential new construction, residential repair/remodel, and commercial construction activity may impact whether we are required to recognize non‑cash, pre‑tax impairment charges for goodwill and other indefinite‑lived intangible assets or other long‑lived assets. If the value of our goodwill, other intangible assets, or long‑lived assets is further impaired, our earnings and stockholders’ equity would be adversely affected.

Compliance with government regulation and industry standards could impact our operating results.

We are subject to federal, state, and local government regulations, particularly those pertaining to health and safety, including protection of employees and consumers; employment laws, including immigration and wage and hour regulations; contractor licensing; and environmental issues. In addition to complying with current requirements, even more stringent requirements could be imposed in the future. Compliance with these regulations and industry standards is costly and may require us to alter our installation and distribution processes, product sourcing, or business practices, and

12

makes recruiting and retaining labor in a tight labor market more challenging. Compliance with these regulations and industry standards could also divert our attention and resources to compliance activities, and could cause us to incur higher costs. Further, if we do not effectively and timely comply with such regulations and industry standards, our results of operations could be negatively affected and we could become subject to substantial penalties or other legal liability.

If we encounter difficulties with our information technology systems, we could experience problems with customer service, inventory, collections, and cost control.

Our operations are dependent upon our information technology systems, which encompass all of our major business functions. We rely upon such information technology systems to manage customer orders on a timely basis, to coordinate our installation and distribution activities across locations, and to manage invoicing. If we experience problems with our information technology systems we could experience, among other things, delays in receiving customer orders, placing orders with suppliers, and scheduling production, installation services, or shipments. Any failure by us to properly maintain and protect our information systems could thus adversely impact our ability to attract and serve customers, and could cause us to incur higher operating costs and experience delays in the execution of our business strategies.

Since we rely heavily on information technology, both in serving our customers and in our enterprise infrastructure, in order to achieve our objectives, we may be vulnerable to damage or intrusion from a variety of cyber‑attacks including computer viruses, worms, or other malicious software programs that gain access to our systems. Despite the precautions we take to mitigate the risks of such events, an attack on our enterprise information technology system could result in theft or disclosure of our proprietary or confidential information, or a breach of confidential customer or employee information. Such events could have an adverse impact on revenue, harm our reputation, and cause us to incur legal liability and costs, which could be significant, to address and remediate such events and related security concerns.

Our business relies significantly on the expertise of our employees, and we generally do not have an intellectual property position that is protected by patents.

Our business is significantly dependent upon our expertise in installation and distribution logistics, including significant expertise in the application of building science to our installation services. We rely on a combination of trade secrets and contractual confidentiality provisions and, to a much lesser extent, copyrights and trademarks, to protect our proprietary rights. Accordingly, our intellectual property position is more vulnerable than it would be if it were protected primarily by patents. If we fail to protect our proprietary rights successfully, our competitive position could suffer, which could harm our operating results. We may be required to spend significant resources to monitor and protect our proprietary rights, and in the event a misappropriation or breach of our proprietary rights occurs our competitive position in the market may be harmed. In addition, competitors may develop competing technologies and expertise that renders our expertise obsolete or less valuable.

Changes in building codes and consumer preferences could affect our ability to market our service offerings and our profitability. Moreover, if we do not respond to evolving customer preferences or changes in building standards, or if we do not maintain or expand our leadership in building science, our business, results of operation, financial condition, and cash flow would be adversely affected.

Each of our lines of business is impacted by local and state building codes and consumer preferences, including a growing focus on energy efficiency. Recently, building codes and consumer preferences have begun to shift towards environmentally friendly and energy‑efficient building products. In addition, state and local governments may change building codes periodically for perceived safety or other reasons. Our competitive advantage is due, in part, to our ability to respond to changes in consumer preferences and building codes. In particular, our Environments For Living® program is designed to make homes more energy‑efficient, comfortable, and durable. However, if our installation and distribution services do not adequately or quickly adapt to changing preferences and building standards, we may lose market share to competitors, which would adversely affect our business, results of operation, financial condition, and cash flows. Further, our growth prospects could be harmed if consumer preferences and building standards evolve more slowly than we anticipate towards energy‑efficient service offerings, which are more profitable than minimum code service offerings.

13

The volatile and challenging economic environment of recent years has caused shifts in consumer preferences and purchasing practices, and changes in the business models and strategies of our customers. This has led to a shift in the quantity, type, and prices of products demanded by our customers. For example, demand has increased for multi‑family housing units such as apartments and condominiums, which are typically smaller, with correspondingly less insulation, than single‑family houses. These shifts have negatively impacted our sales and profitability, and it is uncertain whether these shifts represent long‑term changes in preferences.

We may have future capital needs and may not be able to obtain additional financing on acceptable terms.

Economic and credit market conditions, the performance of the construction industry, and our financial performance, as well as other factors including restrictions under the Tax Matters Agreement related to the Separation, may constrain our financing abilities. Our ability to secure additional financing and to satisfy our financial obligations will depend upon our future operating performance; the availability of credit; economic conditions; and financial, business, and other factors, many of which are beyond our control. Any worsening of current housing market or other construction industry conditions, and the macroeconomic and local economic factors that affect our industry, could require us to seek additional capital and may have a material adverse effect on our ability to secure such capital on favorable terms, if at all. In addition, from and until the second anniversary of the Separation, the Tax Matters Agreement generally will prohibit us and our affiliates from taking certain actions that could cause the Separation and certain related transactions to fail to qualify as tax‑free transactions, which includes certain issuances of our common stock.

Restrictions in our existing credit facility, or any other indebtedness we may incur in the future, could adversely affect our business, financial condition, results of operations, ability to make distributions to shareholders, and the value of our common stock.

Our existing term loan and revolving credit facility, or any future credit facility or other indebtedness we enter into, may limit our ability to, among other things:

|

· |

Incur or guarantee additional debt |

|

· |

Make distributions or dividends on, or redeem or repurchase shares of, common stock |

|

· |

Make certain investments, acquisitions, or other restricted payments |

|

· |

Incur certain liens or permit them to exist |

|

· |

Acquire, merge, or consolidate with another company |

|

· |

Transfer, sell, or otherwise dispose of substantially all of our assets |

Our revolving credit facility contains, and any future credit facility or other debt instrument we may enter into will also likely contain, covenants requiring us to maintain certain financial ratios and meet certain tests, such as a fixed charge coverage ratio, a leverage ratio, and a minimum test. (See Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.) Our ability to comply with those financial ratios and tests can be affected by events beyond our control, and we may not be able to comply with those ratios and tests when required to do so under the applicable debt instruments.

The provisions of our credit facility or other debt instruments may affect our ability to obtain future financing and pursue attractive business opportunities and our flexibility in planning for, and reacting to, changes in business conditions. In addition, a failure to comply with the provisions of our existing credit facility, any future credit facility, or other debt instruments could result in a default or an event of default that could enable our lenders or other debt holders to declare the outstanding principal of that debt, together with accrued and unpaid interest, to be immediately due and payable. If the payment of our debt is accelerated, our assets may be insufficient to repay such debt in full, and our stockholders could experience a partial or total loss of their investment.

14

Any adverse credit rating could increase our costs of borrowing money and limit our access to capital markets and commercial credit.

We do not currently intend to seek credit ratings from Moody’s Investor Service, Standard & Poor’s, or another rating service. However, if Moody’s, Standard & Poor’s, or another rating service rates our credit, such rating could be below investment grade. Further, an initial credit rating could be lowered or withdrawn entirely by a ratings agency if, in its judgment, the circumstances warrant. If any such ratings are lowered, or are otherwise below investment grade, our borrowing costs could increase and our funding sources could decrease. Actual or anticipated changes or downgrades in future ratings, including any announcement that our ratings are under review for a downgrade, could adversely affect our business, cash flows, financial condition, and operating results.

We may be affected by significant restrictions due to the Separation in order to avoid triggering significant tax‑related liabilities.

The Tax Matters Agreement generally will prohibit us from taking certain actions that could cause the Separation and certain related transactions to fail to continue to qualify as tax‑free transactions, including the following:

|

· |

From and until the second anniversary of the Separation, neither we nor any of our subsidiaries may sell, exchange, distribute, or otherwise dispose of any assets held by us or our subsidiaries, except for assets that, in the aggregate, do not constitute more than 15% of our total assets. |

|

· |

From and until the second anniversary of the Separation (or otherwise pursuant to a “plan” within the meaning of Section 355(e) of the Internal Revenue Code of 1986, as amended (the “Code”)), we may not cause or permit any business combination or transaction which, individually or in the aggregate, could result in one or more persons acquiring directly or indirectly a forty percent (40%) or greater interest in us for purposes of Section 355(e) of the Code. |

|

· |

From and until the second anniversary of the Separation, we may not discontinue the active conduct of our business (within the meaning of Section 355(b)(2) of the Code). |

|

· |

From and until the second anniversary of the Separation, we may not sell or otherwise issue our common stock, other than pursuant to issuances that satisfy certain regulatory safe harbors set forth in Treasury Regulations related to stock issued to employees and retirement plans. |

|

· |

From and until the second anniversary of the Separation, we may not redeem or otherwise acquire any of our common stock, other than pursuant to open‑market repurchases of less than 20% of our common stock (in the aggregate). |

|

· |

From and until the second anniversary of the Separation, we may not amend our certificate of incorporation or other organizational documents, or take any other action, whether through a stockholder vote or otherwise, affecting the voting rights of our common stock. |

|

· |

More generally, we may not take any action that could reasonably be expected to cause the Separation and certain related transactions to fail to qualify as tax‑free transactions under Section 368(a)(1)(D) and Section 355 of the Code. |

If we take any of the actions above and such actions result in tax‑related losses to Masco, then we generally will be required to indemnify Masco for such tax‑related losses. Due to these restrictions and indemnification obligations under the Tax Matters Agreement, we may be limited in our ability to pursue strategic transactions, equity or convertible debt financings, or other transactions that may otherwise be in our best interests. Our potential indemnity obligation to Masco might discourage, delay, or prevent a change of control that our stockholders may consider favorable to our ability to pursue strategic transactions, equity or convertible debt financings, or other transactions that may otherwise be in our best interests.

15

In connection with the Separation, Masco indemnified us for certain liabilities and we indemnify Masco for certain liabilities. If we are required to act under these indemnities to Masco, we may need to divert cash to meet those obligations, which could adversely affect our financial results. Moreover, the Masco indemnity may not be sufficient to insure us against the full amount of liabilities for which it will be allocated responsibility, and Masco may not be able to satisfy its indemnification obligations to us in the future.

Pursuant to the Separation and Distribution Agreement and other agreements with Masco, Masco agreed to indemnify us for certain liabilities, and we agreed to indemnify Masco for certain liabilities. Indemnities that we may be required to provide Masco are not subject to any cap, may be significant, and could negatively affect our business, particularly indemnities relating to our actions that could affect the tax‑free nature of the Separation. Third parties could also seek to hold us responsible for any of the liabilities that Masco has agreed to retain, and under certain circumstances, we may be subject to continuing contingent liabilities of Masco following the Separation, such as certain shareholder litigation claims. Further, Masco may not be able to fully satisfy its indemnification obligations or such indemnity obligations may not be sufficient to cover our liabilities. Moreover, even if we ultimately succeed in recovering from Masco any amounts for which we are held liable, we may be temporarily required to bear these losses ourselves. Each of these risks could negatively affect our business, results of operations, liquidity, and financial condition.

Some of our directors and officers may have actual or potential conflicts of interest because of their equity ownership in Masco, and some of our directors may have actual or potential conflicts of interest because they also serve on the Masco board of directors.

Because of their current or former positions with Masco, some of our directors and executive officers may own shares of Masco common stock or have options to acquire shares of Masco common stock, and such holdings may be significant for some of these individuals compared to their total assets. In addition, one of our directors, Mr. Dennis Archer, serves on the Masco board of directors. This ownership or service on both boards of directors may create, or may create the appearance of, conflicts of interest when these directors and officers are faced with decisions that could have different implications for Masco and us. For example, potential conflicts of interest could arise in connection with the resolution of any dispute that may arise between Masco and us regarding the terms of the agreements governing the Separation and the relationship between the companies.

Compliance with and changes in tax laws could adversely affect our performance.

We are subject to extensive tax liabilities imposed by multiple jurisdictions including income taxes; indirect taxes which include excise and duty, sales and use, and gross receipts taxes; payroll taxes; franchise taxes; withholding taxes; and ad valorem taxes. New tax laws and regulations, and changes in existing tax laws and regulations, are continuously being enacted or proposed which could result in increased expenditures for tax liabilities in the future. Many of these liabilities are subject to periodic audits by the respective taxing authority. Subsequent changes to our tax liabilities as a result of these audits may subject us to interest and penalties.

Risks Relating to Our Common Stock

The price of our common stock may fluctuate substantially, and your investment may decline in value.

The market price of our common stock could fluctuate significantly due to a number of factors, many of which are beyond our control, including:

|

· |

Fluctuations in our quarterly or annual earnings results, or those of other companies in our industry |

|

· |

Failures of our operating results to meet the estimates of securities analysts or the expectations of our stockholders, or changes by securities analysts in their estimates of our future earnings |

|

· |

Announcements by us or our customers, suppliers, or competitors |

|

· |

Changes in laws or regulations which adversely affect our industry or us |

16

|

· |

Changes in accounting standards, policies, guidance, interpretations, or principles |

|

· |

General economic, industry, and stock market conditions |

|

· |

Future sales of our common stock by our stockholders |

|

· |

Future issuances of our common stock by us |

|

· |

Other factors described in these “Risk Factors” and elsewhere in this Report |

Future sales of our common stock, or the perception in the public markets that these sales may occur, may depress our stock price.

The market price of our common stock could decline significantly as a result of sales of a large number of shares of our common stock. These sales, or the perception that these sales might occur, could depress the market price of our common stock.

All of our shares of common stock, other than those held by our “affiliates”, are freely tradable without restriction or registration under the Securities Act. Shares held by our affiliates, which include our directors and executive officers, can be sold subject to volume, manner of sale, and notice provisions under Rule 144. We estimate that our directors and executive officers, who may be considered “affiliates” for purposes of Rule 144, beneficially own less than 1% of our common stock.

In the future, we may issue shares of our common stock in connection with investments or acquisitions. The amount of shares of our common stock issued in connections with an investment or acquisition could constitute a material portion of our then-outstanding shares of our common stock.

Provisions in our certificate of incorporation and bylaws, and certain provisions of Delaware law, could delay or prevent a change in control.

The existence of some provisions of our certificate of incorporation and bylaws and Delaware law could discourage, delay, or prevent a change in control that a stockholder may consider favorable. These include provisions:

|

· |

Providing for a classified board of directors |

|

· |

Providing that our directors may be removed by our stockholders only for cause |

|

· |

Establishing supermajority vote requirements for our stockholders to amend certain provisions of our certificate of incorporation and our bylaws |

|

· |

Authorizing a large number of shares of stock that are not yet issued, which could have the effect of preventing or delaying a change in control if our board of directors issued shares to persons that did not support such change in control, or which could be used to dilute the stock ownership of persons seeking to obtain control |

|

· |

Prohibiting stockholders from calling special meetings of stockholders or taking action by written consent |

|

· |

Establishing advance notice requirements for nominations of candidates for election to our board of directors or for proposing matters that can be acted on by stockholders at the annual stockholder meetings |

In addition, we are subject to Section 203 of the Delaware General Corporation Law, which may have an anti‑takeover effect with respect to transactions not approved in advance by our board of directors, including discouraging takeover attempts that could have resulted in a premium over the market price for shares of our common stock.

17

These provisions apply even if a takeover offer may be considered beneficial by some stockholders and could delay or prevent an acquisition that our board of directors determines is not in our and our stockholders’ best interests.

Our bylaws designate a state or federal court located within the State of Delaware as the sole and exclusive forum for certain types of actions and proceedings that may be initiated by our stockholders, which could limit our stockholders’ ability to obtain a preferred judicial forum for disputes with us or our directors, officers, or other employees.

Our bylaws provide that, unless we consent in writing to the selection of an alternative forum, the sole and exclusive forum for (i) any derivative action or proceeding brought on our behalf, (ii) any action asserting a claim of breach of a fiduciary duty owed by any director, officer, or other employee to us or our stockholders, (iii) any action asserting a claim arising pursuant to any provision of Delaware General Corporation Law, our certificate of incorporation (including any certificate of designations for any class or series of our preferred stock), or our bylaws, in each case, as amended from time to time, or (iv) any action asserting a claim governed by the internal affairs doctrine, shall be a state or federal court located within the State of Delaware, in all cases subject to the court’s having personal jurisdiction over the indispensable parties named as defendants. Any person or entity purchasing or otherwise acquiring any interest in shares of our capital stock is deemed to have received notice of, and consented to, the foregoing provision. This forum selection provision may limit a stockholder’s ability to bring a claim in a judicial forum that it finds favorable or cost‑effective for disputes with us or our directors, officers, or other employees, which may discourage such lawsuits against us and our directors, officers, and employees.

Item 1B. UNRESOLVED STAFF COMMENTS

None.

We operate over 180 installation branch locations and over 70 distribution centers in the United States, most of which are leased. We currently lease a 63,404 square foot facility for our corporate and TruTeam (Installation segment) headquarters located at 260 Jimmy Ann Drive, Daytona Beach, Florida, 32114. Our existing headquarters lease will be terminated when we move into our new, 65,700 square foot corporate office, currently under construction at 75 N. Williamson Boulevard in Daytona Beach, FL 32114. The new office is expected to be completed during the fourth quarter of 2016. The lease on our new corporate office will expire approximately 12 years after substantial completion of the landlord’s work, assuming no exercise of any options set forth in the lease. Additionally, we also lease a 17,510 square foot facility for our Service Partners (Distribution Segment) corporate headquarters located at 1029 Technology Park Drive, Glen Allen, Virginia, 23059. Our Service Partners headquarters lease expires on May 31, 2020, assuming no exercise of any options set forth in the lease. We believe that our facilities have sufficient capacity and are adequate for our installation and distribution requirements.

None.

Item 4. MINE SAFETY DISCLOSURES

Not applicable.

18

Item 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information. Our common stock is traded on the NYSE under the symbol “BLD”. The following table presents the high and low sales prices of our common stock for each quarter starting July 1, 2015, the date on which our stock began trading “regular way” on the NYSE:

|

2015 |

|

|

High |

|

|

Low |

|

Third quarter |

|

$ |

36.36 |

|

$ |

26.67 |

|

Fourth quarter |

|

$ |

33.33 |

|

$ |

27.58 |

As of February 26, 2016, there were approximately 3,500 holders of our issued and outstanding common stock.

Dividends. No dividends were paid during the years ended December 31, 2015 and 2014. Our credit agreement, in certain circumstances, limits the amount of dividends we may distribute. We do not anticipate declaring any such cash dividends to holders of our common stock in the foreseeable future.

Issuer Purchases of Equity Securities. During the fourth quarter ended December 31, 2015, we did not repurchase any of our equity securities.

Securities Authorized for Issuance under Equity Compensation Plans. The information required by this item will be set forth under the heading “Compensation of Executive Officers” in our 2016 Proxy Statement and is incorporated herein by reference.

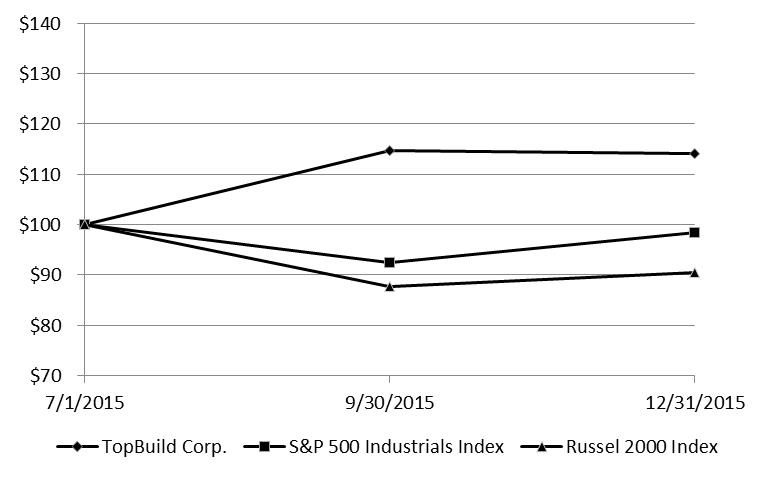

Performance Graph and Table. The following graph and table compares the cumulative total return of our common stock from July 1, 2015, the date on which our stock began trading “regular way” on the NYSE, through December 31, 2015, with the total cumulative return of the Russel 2000 Index and the Standard and Poor’s Industrials Index (“S&P 500 Industrials Index). The graph and table assumes an initial investment of $100 in our common stock and each of the two indices at the close of business on July 1, 2015, and reinvestment of dividends.

|

|

|

Period ended: |

|||||||

|

Index |

|

7/1/2015 |

|

9/30/2015 |

|

12/31/2015 |

|||

|

TopBuild Corp. |

|

$ |

100 |

|

$ |

115 |

|

$ |

114 |

|

S&P 500 Industrials Index |

|

|

100 |

|

|

92 |

|

|

98 |

|

Russel 2000 Index |

|

|

100 |

|

|

88 |

|

|

90 |

19

Item 6. SELECTED HISTORICAL FINANCIAL DATA

The following table sets forth selected historical financial data that should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and notes thereto, included in this Report. The Consolidated Statements of Operations data for the years ended December 31, 2015, 2014, and 2013, and the Consolidated Balance Sheet data as of December 31, 2015, and 2014, are derived from our audited financial statements included in this Report. The Consolidated Statements of Operations data for the year ended December 31, 2012, and the Consolidated Balance Sheet data as of December 31, 2013, were derived from our audited financial statements not included in this report. The Consolidated Statements of Operations data for the year ended December 31, 2011, and the Consolidated Balance Sheet data as of December 31, 2012, and 2011, are derived from our unaudited financial statements not included in this Report. The selected historical financial data in this section is not intended to replace our historical financial statements and the related notes thereto. Prior to the Separation, our historical financial results included allocations of general and corporate expense from Masco and as such our historical results are not necessarily indicative of future results. For more information, see Item 8. Financial Statements and Supplementary Data, Note 1 – Summary of Significant Accounting Policies: Basis of Presentation.

|

|

|

Year ended December 31, |

|||||||||||||

|

(in thousands) |

|

2015 |

|

2014 |

|

2013 |

|

2012 (b) |

|

2011 |

|||||

|

Net sales |

|

$ |

1,616,580 |

|

$ |

1,512,077 |

|

$ |

1,411,524 |

|

$ |

1,207,889 |

|

$ |

1,076,557 |

|

Operating profit (loss) |

|

|

83,531 |

|

|

40,717 |

|

|

24,103 |

|

|

(115,928) |

|

|

(98,158) |

|

Income (loss) from continuing operations |

|

$ |

79,123 |

|

$ |

10,496 |

|

$ |

(11,551) |

|

$ |

(154,375) |

|

$ |

(137,893) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income (loss) per common share on income (loss) from continuing operations (a): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basic |

|

$ |

2.10 |

|

$ |

0.28 |

|

$ |

(0.31) |

|

$ |

(4.10) |

|

$ |

(3.66) |

|

Diluted |

|

$ |

2.09 |

|

$ |

0.28 |

|

$ |

(0.31) |

|

$ |

(4.10) |

|

$ |

(3.66) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

At period end: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ |

1,642,249 |

|

$ |

1,476,424 |

|

$ |

1,466,946 |

|

$ |

1,450,663 |

|

$ |

1,451,294 |

|

Long-term debt |

|

|

193,457 |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

Equity |

|

$ |

915,729 |

|

$ |

952,291 |

|

$ |

1,002,685 |

|

$ |

1,026,749 |

|

$ |

1,103,657 |

|

(a) |

For comparative purposes, the computation of basic and diluted earnings per common share for prior year periods presented was calculated using the shares distributed at Separation. |

|

(b) |