Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - AYTU BIOPHARMA, INC | v432884_ex23-1.htm |

| EX-5.1 - EXHIBIT 5.1 - AYTU BIOPHARMA, INC | v432884_ex5-1.htm |

As filed with the Securities and Exchange Commission on March 2, 2016

Registration No. 333-[_____]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

AYTU BIOSCIENCE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 2834 | 47-0883144 |

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

| incorporation or organization) | Classification Code Number) | Identification Number) |

373 Inverness Parkway

Suite 206

Englewood, Colorado 80112

(720) 437-6580

(Address, including zip code and telephone number, including

area code, of registrant’s principal executive offices)

Joshua R. Disbrow

Chief Executive Officer

373 Inverness Parkway

Suite 206

Englewood, Colorado 80112

Telephone: (720) 437-6580

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copies to:

Alexander M. Donaldson, Esq.

Wyrick Robbins Yates & Ponton LLP

4101 Lake Boone Trail, Suite 300

Raleigh, North Carolina 27607

(919) 781-4000

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box. x

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ |

|

Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company x |

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered (1) | Amount to be registered | Proposed maximum aggregate offering price per share (2) | Proposed maximum aggregate offering price (2) | Amount of registration fee | ||||||||||||

| Common stock, $0.0001 par value per share | 7,879,096 | $ | 0.70 | $ | 5,515,367.20 | $ | 555.40 | |||||||||

| Common stock, $0.0001 par value per share, issuable upon exercise of warrants | 267,073 | $ | 0.70 | $ | 186,951.10 | $ | 18.83 | |||||||||

| Total | 8,146,169 | $ | 0.70 | $ | 5,702,318.30 | $ | 574.23 | |||||||||

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, this registration statement shall be deemed to cover the additional securities of the same class as the securities covered by this registration statement issued or issuable prior to completion of the distribution of the securities covered by this registration statement as a result of a split of, or a stock dividend on, the registered securities. |

| (2) | Estimated solely for the purpose of calculating the registration fee. Pursuant to Rule 457(c) under the Securities Act, the proposed maximum offering price per share is based on the average of the bid and asked prices of the registrant’s common stock on the OTCQX on February 25, 2016. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated March 2, 2016

PROSPECTUS

8,146,169 Shares

Common Stock

This prospectus relates to the sale or other disposition from time to time of up to 8,146,169 shares of our common stock, $0.0001 par value per share, issued to and issuable upon the exercise of warrants held by the selling stockholders named in this prospectus. We are not selling any shares of common stock under this prospectus and will not receive any of the proceeds from the sale of shares of common stock by the selling stockholders.

The selling stockholders may sell or otherwise dispose of the shares of common stock covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the selling stockholders may sell or otherwise dispose of their shares of common stock in the section entitled “Plan of Distribution” on page 101. The selling shareholders will pay all brokerage fees and commissions and similar expenses. We will pay all expenses (except brokerage fees and commissions and similar expenses) relating to the registration of the shares with the Securities and Exchange Commission.

Our common stock is listed on the OTCQX Market operated by OTC Markets Group, Inc. (or OTCQX) under the ticker symbol “AYTU.” On February 29, 2016, the last reported sale price of our common stock on the OTCQX was $0.63.

Investing in our common stock involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” beginning on page 6 of this prospectus, and under similar headings in any amendments or supplements to this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is [___], 2016.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus, as supplemented and amended. We have not, and the selling stockholders have not, authorized anyone to provide you with information that is different. This prospectus may only be used where it is legal to sell these securities. The information in this prospectus may only be accurate on the date of this prospectus.

We urge you to read carefully this prospectus, as supplemented and amended, before deciding whether to invest in any of the common stock being offered.

Unless the context indicates otherwise, as used in this prospectus, the terms “Aytu,” “we,” “us,” “our,” “our company” and “our business” refer to Aytu BioScience, Inc.

We own various U.S. federal trademark registrations and applications, and unregistered trademarks and servicemarks, including Zertane, Vyrix, RedoxSYS, MiOXSYS, ProstaScint and Luoxis. All other trade names, trademarks and service marks appearing in this prospectus are the property of their respective owners. We have assumed that the reader understands that all such terms are source-indicating. Accordingly, such terms, when first mentioned in this prospectus, appear with the trade name, trademark or service mark notice and then throughout the remainder of this prospectus without trade name, trademark or service mark notices for convenience only and should not be construed as being used in a descriptive or generic sense.

i

This summary highlights certain information about us and this offering contained elsewhere in this prospectus. Because it is only a summary, it does not contain all of the information that you should consider before investing in shares of our common stock and it is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this prospectus. Before you decide to invest in our common stock, you should read the entire prospectus carefully, including “Risk Factors” beginning on page 6, and the financial statements and related notes included in this prospectus.

Company Overview

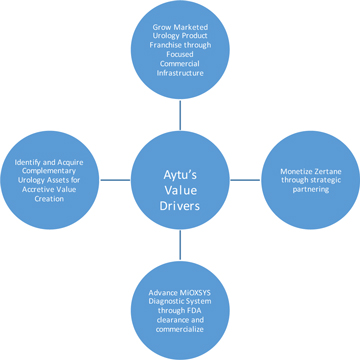

We are a commercial-stage specialty healthcare company focused on acquiring, developing and commercializing novel products in the field of urology. We have multiple urology-focused products on the market, and we seek to build a portfolio of novel therapeutics that serve large medical needs in the field of urology. We are initially concentrating on prostate cancer, male sexual dysfunction and male infertility and plan to expand into other urological indications for which there are significant medical needs.

We currently market ProstaScint® (capromab pendetide), the only radioimaging agent indicated to detect prostate specific membrane antigen, or PSMA, in the assessment and staging of prostate cancer. ProstaScint is approved by the U.S. Food and Drug Administration, or FDA, for use in both newly diagnosed, high-risk prostate cancer patients and patients with recurrent prostate cancer. We also market Primsol® (trimethoprim hydrochloride) – the only FDA-approved trimethoprim-only oral solution for urinary tract infections. We have a focused pipeline, including MiOXSYS, a novel in vitro diagnostic device that is currently CE marked (which enables it to be sold within the European Economic Area (see “Business—,Foreign Regulatory Approval”)) and for which we intend to initiate a final clinical study to enable FDA clearance in the U.S.

Our MiOXSYS™ system is a novel, point-of-care semen analysis system with the potential to become a standard of care in the diagnosis and management of male infertility. Male infertility is a prevalent and underserved condition and oxidative stress is widely implicated in its pathophysiology. MiOXSYS was developed from our core oxidation-reduction potential research platform known as RedoxSYS®.We are advancing MiOXSYS toward FDA clearance and believe we are adequately funded to complete the required clinical study.

Our late-stage therapeutic candidate is Zertane™, an oral therapeutic that has been studied for the treatment of premature ejaculation, or PE. PE is the most common sexual dysfunction for which there is not an FDA-approved treatment and affects up to 23% of men in the U.S. and major European countries. Zertane, which has demonstrated safety and efficacy in two European pivotal studies, has the potential to be the first oral therapeutic approved in the United States for the treatment of PE.

Additionally, we are actively looking to acquire additional urology products, including existing products we believe can offer distinct commercial advantages. Our management team’s prior experience has involved identifying clinical assets that can be re-launched to increase value, with a focused commercial infrastructure specializing in urology.

ProstaScint® (capromab pendetide). We became a commercial stage company by virtue of our acquisition of ProstaScint in May 2015 and are generating sales of this FDA-approved prostate cancer imaging agent. As prostate cancer is a condition commonly diagnosed and treated by urologists, ProstaScint complements our urology-focused product portfolio and pipeline. Prostate cancer is the most common cancer among men in the United States, with an estimated 241,000 annual cases (as of 2012). Further, more than 2,200,000 men were alive with some history of prostate cancer in 2006, and over 30,000 U.S. men die each year from the disease. The effect of prostate cancer on healthcare economics is substantial, which makes the need for accurate disease staging critical for treatment and management strategies. The U.S. market for the diagnosis and screening of prostate cancer is expected to total $17.4 billion by 2017, a compound annual growth rate, or CAGR, of 7.5%.

| 1 |

Primsol® (trimethoprim solution). On October 5, 2015, we purchased Primsol from FSC Laboratories, Inc. Primsol is the only FDA-approved liquid formulation of trimethoprim, an antibiotic that is well established in current guidelines for treating uncomplicated urinary tract infections, or UTIs. This differentiated product is appropriate for UTI patients that have difficulty swallowing tablets, such as the elderly, and particularly for patients that experience adverse reactions to sulfamethoxazole (“sulfa”). It is estimated that 150 million cases of urinary tract infection occur annually worldwide, and the annual estimated incidence is 0.5-0.7/persons per year. Importantly, there are more than 1 million catheter-associated UTIs in the U.S. alone. As many of these patients are elderly and unable to swallow pills, an oral liquid formulation represents a convenient formulation for easier administration. The acquisition of Primsol adds a second established brand to our product portfolio. We expect to benefit from and continue to grow Primsol’s established base of prescribers, which already includes a significant proportion of urologists despite the fact that it has not been previously marketed to these specialists. We can thus utilize the same sales channel as ProstaScint, leading to potential commercial synergies and product growth.

MiOXSYS. MiOXSYS™ is a rapid in vitro diagnostic semen analysis test used in the quantitative measurement of static oxidation reduction potential, or sORP, in human semen. MiOXSYS is a recently CE marked system and is an accurate, easy to use, and fast infertility assessment tool. It is estimated that 72.4 million couples worldwide experience infertility problems. In the United States, approximately 10% of couples are defined as infertile. Male infertility is responsible for between 40-50% of all infertility cases and affects approximately 7% of all men. Male infertility is often unexplained (idiopathic), and this idiopathic infertility is frequently associated with levels of oxidative stress in the semen. As such, having a rapid, easy-to-use diagnostic platform to measure oxidative stress should provide a practical way for male infertility specialists to improve semen analysis and infertility assessments without having to refer patients to outside clinical laboratories.

Male infertility is prevalent and underserved, and oxidative stress is widely implicated in its pathophysiology. The global male infertility market is expected to grow to over $300 million by 2020 with a CAGR of nearly 5% from 2014 to 2020. Oxidative stress is broadly implicated in the pathophysiology of male infertility, yet very few diagnostic tools exist to effectively measure oxidative stress levels in men. However, antioxidants are widely available and recommended to infertile men. With the introduction of the MiOXSYS System, we believe for the first time there will be an easy and effective diagnostic tool to assess the degree of oxidative stress, sperm motility and morphology, and potentially enable the monitoring of patients’ responses to antioxidant therapy as a treatment regimen for infertility. The MiOXSYS System received CE marking in Europe in January 2016. We expect to advance MiOXSYS into clinical trials in the United States in order to enable 510(k) clearance.

In addition to the MiOXSYS system, we are continuing to develop the global market for the RedoxSYS System across a range of applications. Specifically, we have begun initial commercializing of the RedoxSYS System for research use through distribution partners, primarily outside the U.S. In 2014, we received ISO 13485 certification, demonstrating our compliance with global quality standards in medical device manufacturing.

The technology underpinning the RedoxSYS and MiOXSYS systems was developed by Luoxis Diagnostics, Inc. in the two years immediately preceding the merger between Luoxis, Vyrix Pharmaceuticals, Inc., and us (under our former name of Rosewind Corporation) in April 2015. Upon the consummation of the merger, the RedoxSYS System and MiOXSYS System became our assets.

Zertane. The FDA has accepted an Investigational New Drug, or IND, application for our product candidate Zertane for the treatment of premature ejaculation. However, depending on our success in raising additional funds, we may decide to focus our capital resources on other strategies and not pursue clinical testing of Zertane in the U.S. If we decide not to pursue clinical testing of Zertane, we will seek strategic options to maximize the value of Zertane, inclusive of divestiture, out-licensing, and strategic commercial collaborations.

The global premature ejaculation market is expected to reach over $12 billion in annual sales by 2017, representing a compound annual growth rate of 4.1% from 2010. According to recent published analyses, PE is a highly prevalent male sexual dysfunction affecting up to 23% of men worldwide. Based on internal market research and published reports, we believe that PE is up to 1.5-times more prevalent than erectile dysfunction, or ED. Currently, there are no FDA-approved prescription products in the United States to treat PE, and to our knowledge, only two other prescription products have been approved elsewhere in the world. Treatment options for PE have traditionally included antidepressant drugs prescribed “off label,” topical numbing medications, and cognitive behavior therapy or counseling, all of which have had limited effectiveness in treating the disorder. PE therefore represents an area of significant unmet medical need.

| 2 |

Strategy

Key elements of our strategy include:

| § | Expand the commercialization of FDA-approved ProstaScint for the staging of both newly diagnosed high-risk and recurrent prostate cancer patients. We have begun commercializing ProstaScint in the U.S. and in key markets around the world. |

| § | Expand the commercialization of FDA-approved Primsol for the treatment of uncomplicated urinary tract infections. We are re-launching Primsol to urologists in the U.S. and in key markets around the world where appropriate. |

| § | Establish MiOXSYS as a leading in vitro diagnostic device in the assessment of male infertility. |

| § | Acquire additional marketed products and late-stage development assets within our core urology focus that can be efficiently marketed through our growing commercial organization. |

| § | Develop a pipeline of urology therapeutics, with a focus on identifying novel products with sufficient clinical proof of concept that require modest internal R&D expense. |

Future Products

We plan to augment our core in-development and commercial assets through efficient identification of complementary therapeutics, devices, and diagnostics related to urological disorders. We intend to seek assets that are near commercial stage or already generating revenues. Further, we intend to seek to acquire products through asset purchases, licensing, co-development, or collaborative commercial arrangements (co-promotions, co-marketing, etc.).

Our management team has extensive experience across a wide range of business development activities and have in-licensed or acquired products from large, mid-sized, and small enterprises in the United States and abroad. Through an assertive product and business development approach, we expect that we will build a substantial portfolio of complementary urology products.

Recent Developments

On October 5, 2015, we entered into and closed on an asset purchase agreement with FSC Laboratories, Inc. (the “Seller”). Pursuant to the agreement, we purchased assets related to the Seller’s product known as Primsol® (trimethoprim solution), including certain intellectual property and contracts, inventory, work in process and all marketing and sales assets and materials related solely to Primsol (together, the “Primsol Business”), and assumed certain of the Seller’s liabilities, including those related to the sale and marketing of Primsol arising after the closing.

We paid $500,000 at closing for the Primsol Business and paid an additional $142,000 of which $102,000 went to inventory and $40,000 toward the Primsol Business, for the transfer of the Primsol-related product inventory, which we now own. We also agreed to pay an additional (a) $500,000 no later than March 31, 2016, (b) $500,000 no later than June 30, 2016, and (c) $250,000 no later than September 30, 2016 for a total purchase price of $1,892,000.

The agreement also provides that for a period of one year after the closing the Seller will not directly or indirectly sell, market, promote, advertise or distribute anywhere in the world any urinary tract anti-infective pharmaceutical or treatment product containing trimethoprim.

On October 8, 2015, we and Biovest International, Inc., or Biovest, entered into a Master Services Agreement, pursuant to which Biovest is to provide manufacturing services to us. The agreement provides that we may engage Biovest from time to time to provide services in accordance with mutually agreed upon project addendums and purchase orders. We expect to use the agreement from time to time for manufacturing services, including without limitation, the manufacturing, processing, quality control testing, release or storage of our products. The agreement provides customary terms and conditions, including those for performance of services by Biovest in compliance with project addendums, industry standards, regulatory standards and all applicable laws. Biovest will be responsible for obtaining and maintaining all governmental approvals, at our expense, during the term of the agreement. The agreement has a term of four years, provided that either party may terminate the agreement or any project addendum under the agreement on 30 days written notice of a material breach under the agreement. In addition, we may terminate the agreement or any project addendum under the agreement upon 180 days written notice for any reason.

| 3 |

In conjunction with entering into the agreement, we submitted a work order to Biovest to provide us with active pharmaceutical ingredient for ProstaScint over at least a four-year period at a total cost of $5,000,000, of which we paid $1,000,000 upon submission of the work order and an additional $500,000 on January 4, 2016.

On January 20, 2016, each of Joshua R. Disbrow, our Chief Executive Officer, and Jarrett T. Disbrow, our Chief Operating Officer, purchased 153,846 shares of our common stock at a price of $0.65 per share, resulting in gross proceeds to us of $200,000.

On February 10, 2016, we completed the conversion of $4,125,000 in convertible notes and $143,000 of accrued interest. The notes were issued in financings that closed in July and August 2015. Upon the conversion, we issued an aggregate of 7,879,096 shares common stock. An aggregate of $1,050,000 of principal of convertible notes remain outstanding.

Corporate Information

We were incorporated as Rosewind Corporation on August 9, 2002 in the State of Colorado.

Vyrix Pharmaceuticals, Inc., or Vyrix, was incorporated under the laws of the State of Delaware on November 18, 2013 and was wholly owned by Ampio Pharmaceuticals, Inc. (NYSE MKT: AMPE), or Ampio, immediately prior to the completion of the Merger (defined below). Vyrix was previously a carve-out of the sexual dysfunction therapeutics business, including the late-stage men’s health product candidates, Zertane and Zertane-ED, from Ampio, which carve out was announced in December 2013. Luoxis Diagnostics, Inc., or Luoxis, was incorporated under the laws of the State of Delaware on January 24, 2013 and was majority owned by Ampio immediately prior to the completion of the Merger. Luoxis was focused on initially developing and advancing the RedoxSYS System. The MiOXSYS System was developed following the completed development of the RedoxSYS System.

On March 20, 2015, Rosewind formed Rosewind Merger Sub V, Inc. and Rosewind Merger Sub L, Inc., each a wholly-owned subsidiary formed for the purpose of the Merger, and on April 16, 2015, Rosewind Merger Sub V, Inc. merged with and into Vyrix and Rosewind Merger Sub L, Inc. merged with and into Luoxis, and Vyrix and Luoxis became subsidiaries of Rosewind. Immediately thereafter, Vyrix and Luoxis merged with and into Rosewind with Rosewind as the surviving corporation (herein referred to as the Merger). Concurrent with the closing of the Merger, Rosewind abandoned its pre-merger business plans to develop a sailing school, and we now solely pursue the specialty healthcare market, focusing on urological related conditions, including the business of Vyrix and Luoxis.

On June 8, 2015, we (i) reincorporated as a domestic Delaware corporation under Delaware General Corporate Law and changed our name from Rosewind Corporation to Aytu BioScience, Inc., and (ii) effected a reverse stock split in which each common stock holder received one share of common stock for each every 12.174 shares outstanding (herein referred to as the Reverse Stock Split). All share and per share amounts in this prospectus have been adjusted to reflect the effect of the Reverse Stock Split.

| 4 |

This prospectus relates to the resale by the selling stockholders identified in this prospectus of up to 8,146,169 shares of our common stock, as follows:

| § | 7,879,096 shares of common stock issued in February 2016 upon the conversion of convertible notes; and |

| § | 267,073 shares of common stock issuable upon the exercise of warrants issued to the placement agent for our 2015 private placement of convertible notes. |

| Common stock offered by the selling stockholders | 8,146,169 shares |

| Common stock outstanding before the offering (1) | 22,446,481 shares |

| Common stock to be outstanding after the offering (2) | 22,713,554 shares |

| Common stock OTCQX Symbol | AYTU |

| (1) | Based on the number of shares outstanding as of February 12, 2016. | |

| (2) | Assumes the exercise of all of the warrants for which the underlying shares are being offered by this prospectus. |

Use of Proceeds

We will not receive any of the proceeds from the sale of shares in this offering. The selling stockholders will receive all net proceeds from the sale of shares of our common stock in this offering.

Dividend Policy

We have never paid dividends on our capital stock and do not anticipate paying any dividends for the foreseeable future. See “Dividend Policy.”

| 5 |

Investing in our common stock includes a high degree of risk. Prior to making a decision about investing in our common stock, you should consider carefully the specific factors discussed below, together with all of the other information contained in this prospectus. If any of the following risks actually occurs, our business, financial condition, results of operations and future prospects would likely be materially and adversely affected. This could cause the market price of our common stock to decline and could cause you to lose all or part of your investment.

Risks Related to Our Financial Condition and Capital Requirements

We have limited operating history, have incurred losses, and can give no assurance of profitability.

We are a commercial-stage healthcare company with a limited operating history. Prior to implementing our commercial strategy in the fourth calendar quarter of 2015, we did not have a focus on profitability. As a result, we have not generated material revenue to date and are not profitable, and have incurred losses in each year since our inception. Our net loss for the years ended June 30, 2015 and 2014 was $7.7 million and $5.6 million, respectively. Our net loss for the six months ended December 31, 2015 was $5.6 million. We have not demonstrated the ability to be a profit-generating enterprise to date, and without significant financing, there is substantial doubt about our ability to continue as a going concern. We expect to incur substantial losses for the foreseeable future. Our ability to generate significant revenue is uncertain, and we may never achieve profitability. We have a very limited operating history on which investors can evaluate our potential for future success. Potential investors should evaluate us in light of the expenses, delays, uncertainties, and complications typically encountered by early-stage healthcare businesses, many of which will be beyond our control. These risks include the following:

| • | U.S. regulatory approval of our products and product candidates; |

| • | foreign regulatory approval of our products and product candidates; |

| • | lack of sufficient capital; |

| • | uncertain market acceptance of our products and product candidates; |

| • | unanticipated problems, delays, and expense relating to product development and implementation; |

| • | lack of sufficient intellectual property; |

| • | competition; and |

| • | technological changes. |

As a result of our limited operating history, and the increasingly competitive nature of the markets in which we compete, our historical financial data, which, prior to April 16, 2015, consists of allocations of expenses from Ampio, is of limited value in anticipating future operating expenses. Our planned expense levels will be based in part on our expectations concerning future operations, which is difficult to forecast accurately based on our stage of development. We may be unable to adjust spending in a timely manner to compensate for any unexpected budgetary shortfall.

We have not received any material revenues from the commercialization of our products or product candidates and might not receive significant revenues from the commercialization of products and our product candidates in the near term. Even though ProstaScint is an approved drug that we are marketing, we only acquired it in May 2015 and have limited experience on which to base the revenue we could expect to receive from its sales. To obtain revenues from our products and product candidates, we must succeed, either alone or with others, in a range of challenging activities, including expanding markets for our existing products and completing clinical trials of our product candidates, obtaining positive results from the clinical trials, achieving marketing approval for these product candidates, manufacturing, marketing and selling our existing products and those products for which we, or our collaborators, may obtain marketing approval, satisfying any post-marketing requirements and obtaining reimbursement for our products from private insurance or government payors. We, and our collaborators, if any, may never succeed in these activities and, even if we do, or one of our collaborators does, we may never generate revenues that are sufficient enough for us to achieve profitability.

| 6 |

We may need to raise additional funding, which may not be available on acceptable terms, or at all. Failure to obtain necessary capital when needed may force us to delay, limit or terminate our product expansion and development efforts or other operations.

We are currently advancing our product candidates through clinical development. Developing product candidates is expensive, lengthy and risky, and we expect to incur research and development expenses in connection with our ongoing clinical development activities with the MiOXSYS System. In addition, we are expending resources to expand the market for ProstaScint and Primsol, which might not be successful or might take longer and be more expensive than we anticipate.

As of December 31, 2015, our cash and cash equivalents were $11.0 million. Our operating plan may change as a result of many factors currently unknown to us, and we may need to seek additional funds sooner than planned, through public or private equity or debt financings, government or other third-party funding, marketing and distribution arrangements and other collaborations, strategic alliances and licensing arrangements or a combination of these approaches. In any event, we will require additional capital to obtain regulatory approval for, and to commercialize, our product candidates. Raising funds in the current economic environment, as well our lack of operating history, may present additional challenges. Even if we believe we have sufficient funds for our current or future operating plans, we may seek additional capital if market conditions are favorable or if we have specific strategic considerations.

Any additional fundraising efforts may divert our management from their day-to-day activities, which may adversely affect our ability to expand any existing product or develop and commercialize our product candidates. In addition, we cannot guarantee that future financing will be available in sufficient amounts or on terms acceptable to us, if at all. Moreover, the terms of any financing may adversely affect the holdings or the rights of our stockholders and the issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of our shares to decline. The sale of additional equity or convertible securities would dilute all of our stockholders. The incurrence of indebtedness would result in increased fixed payment obligations and we may be required to agree to certain restrictive covenants, such as limitations on our ability to incur additional debt, limitations on our ability to acquire, sell or license intellectual property rights and other operating restrictions that could adversely impact our ability to conduct our business. We could also be required to seek funds through arrangements with collaborative partners or otherwise at an earlier stage than otherwise would be desirable and we may be required to relinquish rights to some of our technologies or product candidates or otherwise agree to terms unfavorable to us, any of which may have a material adverse effect on our business, operating results and prospects.

If we are unable to obtain funding on a timely basis, we may be required to significantly curtail, delay or discontinue one or more of our research or development programs or the commercialization of any product candidate or be unable to expand our operations or otherwise capitalize on our business opportunities, as desired, which could materially affect our business, financial condition and results of operations.

If we do not obtain the capital necessary to fund our operations, we will be unable to successfully expand, develop, obtain regulatory approval of, and commercialize, our products and product candidates.

The development of pharmaceutical products, medical diagnostics and medical devices is capital-intensive. We anticipate we may require additional financing to continue to fund our operations. Our future capital requirements will depend on, and could increase significantly as a result of, many factors including:

| • | progress in, and the costs of, our pre-clinical studies and clinical trials and other research and development programs; |

| • | the scope, prioritization and number of our research and development programs; |

| • | the achievement of milestones or occurrence of other developments that trigger payments under any collaboration agreements we obtain; |

| • | the costs of securing manufacturing arrangements for commercial production; |

| • | the costs of establishing, expanding or contracting for sales and marketing capabilities for any existing products and if we obtain regulatory clearances to market our product candidates; |

| 7 |

| • | the extent to which we are obligated to reimburse, or entitled to reimbursement of, clinical trial costs under future collaboration agreements, if any; and |

| • | the costs involved in filing, prosecuting, enforcing and defending patent claims and other intellectual property rights. |

If funds are not available, we may be required to delay, reduce the scope of, or eliminate one or more of our technologies, research or development programs or our commercialization efforts.

We no longer can rely on funding from Ampio to support our operations.

As a part of the Merger, Ampio forgave debt incurred by Luoxis and Vyrix in exchange for shares of our common stock and also committed an additional $10.0 million for additional shares of our common stock, which was due in April 2016 and which Ampio paid in full in December 2015. We have no agreement with Ampio for future funding. Consequently, we will need to support our business with revenue from our operations or from financing from third party sources.

We will incur increased costs associated with, and our management will need to devote substantial time and effort to, compliance with public company reporting and other requirements.

As a public company, we incur significant legal, accounting and other expenses that Vyrix and Luoxis did not incur as private companies. In addition, the rules and regulations of the SEC and any national securities exchange to which we may be subject in the future impose numerous requirements on public companies, including requirements relating to our corporate governance practices, with which we will need to comply. Further, we will continue to be required to, among other things, file annual, quarterly and current reports with respect to our business and operating results. Based on currently available information and assumptions, we estimate that we will incur approximately $500,000 in expenses on an annual basis as a direct result of the requirements of being a publicly traded company. Our management and other personnel will need to devote substantial time to gaining expertise regarding operations as a public company and compliance with applicable laws and regulations, and our efforts and initiatives to comply with those requirements could be expensive.

Risks Related to Product Development, Regulatory Approval and Commercialization

We cannot be certain that we will be able to obtain regulatory approval for, or successfully commercialize, any of our product candidates.

We may not be able to develop our current or any future product candidates. Our product candidates will require substantial additional clinical development, testing, and regulatory approval before we are permitted to commence commercialization. The clinical trials of our product candidates are, and the manufacturing and marketing of our product candidates will be, subject to extensive and rigorous review and regulation by numerous government authorities in the United States and in other countries where we intend to test and, if approved, market any product candidate. Before obtaining regulatory approvals for the commercial sale of any product candidate, we must demonstrate through pre-clinical testing and clinical trials that the product candidate is safe and effective for use in each target indication. This process can take many years and may include post-marketing studies and surveillance, which will require the expenditure of substantial resources. Of the large number of drugs in development in the U.S., only a small percentage successfully completes the FDA regulatory approval process and is commercialized. Accordingly, even if we are able to obtain the requisite financing to continue to fund our development and clinical programs, we cannot assure you that any of our product candidates will be successfully developed or commercialized.

We are not permitted to market a product in the U.S. until we receive approval of a New Drug Application, or an NDA, for that product from the FDA, or in any foreign countries until we receive the requisite approval from such countries. Obtaining approval of an NDA is a complex, lengthy, expensive and uncertain process, and the FDA may delay, limit or deny approval of any product candidate for many reasons, including, among others:

| • | we may not be able to demonstrate that a product candidate is safe and effective to the satisfaction of the FDA; |

| • | the results of our clinical trials may not meet the level of statistical or clinical significance required by the FDA for marketing approval; |

| • | the FDA may disagree with the number, design, size, conduct or implementation of our clinical trials; |

| • | the FDA may require that we conduct additional clinical trials; |

| • | the FDA may not approve the formulation, labeling or specifications of any product candidate; |

| 8 |

| • | the clinical research organizations, or CROs, that we retain to conduct our clinical trials may take actions outside of our control that materially adversely impact our clinical trials; | |

| • | the FDA may find the data from pre-clinical studies and clinical trials insufficient to demonstrate that a product candidate’s clinical and other benefits outweigh its safety risks, such as the risk of drug abuse by patients or the public in general; |

| • | the FDA may disagree with our interpretation of data from our pre-clinical studies and clinical trials; |

| • | the FDA may not accept data generated at our clinical trial sites; |

| • | if an NDA, if and when submitted, is reviewed by an advisory committee, the FDA may have difficulties scheduling an advisory committee meeting in a timely manner or the advisory committee may recommend against approval of our application or may recommend that the FDA require, as a condition of approval, additional pre-clinical studies or clinical trials, limitations on approved labeling or distribution and use restrictions; |

| • | the FDA may require development of a Risk Evaluation and Mitigation Strategy, or REMS, as a condition of approval or post-approval; |

| • | the FDA may not approve the manufacturing processes or facilities of third-party manufacturers with which we contract; or |

| • | the FDA may change its approval policies or adopt new regulations. |

These same risks apply to applicable foreign regulatory agencies from which we may seek approval for any of our product candidates.

Any of these factors, many of which are beyond our control, could jeopardize our ability to obtain regulatory approval for and successfully market any product candidate. Moreover, because a substantial portion of our business is or will be dependent upon our existing products and product candidates, any such setback in our pursuit of initial or additional regulatory approval would have a material adverse effect on our business and prospects.

If we fail to successfully acquire new products, we may lose market position.

Acquiring new products is an important factor in our planned sales growth, including products that already have been developed and found market acceptance. If we fail to identify existing or emerging consumer markets and trends and to acquire new products, we will not develop a strong revenue source to help pay for our development activities as well as possible acquisitions. This failure would delay implementation of our business plan, which could have a negative adverse effect on our business and prospects.

If we do not secure collaborations with strategic partners to test, commercialize and manufacture product candidates, we may not be able to successfully develop products and generate meaningful revenues.

We may enter into collaborations with third parties to conduct clinical testing, as well as to commercialize and manufacture our products and product candidates. If we are able to identify and reach an agreement with one or more collaborators, our ability to generate revenues from these arrangements will depend on our collaborators’ abilities to successfully perform the functions assigned to them in these arrangements. Collaboration agreements typically call for milestone payments that depend on successful demonstration of efficacy and safety, obtaining regulatory approvals, and clinical trial results. Collaboration revenues are not guaranteed, even when efficacy and safety are demonstrated. The current economic environment may result in potential collaborators electing to reduce their external spending, which may prevent us from developing our product candidates.

Even if we succeed in securing collaborators, the collaborators may fail to develop or effectively commercialize our products or product candidates. Collaborations involving our product candidates pose a number of risks, including the following:

| • | collaborators may not have sufficient resources or may decide not to devote the necessary resources due to internal constraints such as budget limitations, lack of human resources, or a change in strategic focus; |

| • | collaborators may believe our intellectual property is not valid or is unenforceable or the product candidate infringes on the intellectual property rights of others; |

| 9 |

| • | collaborators may dispute their responsibility to conduct development and commercialization activities pursuant to the applicable collaboration, including the payment of related costs or the division of any revenues; |

| • | collaborators may decide to pursue a competitive product developed outside of the collaboration arrangement; |

| • | collaborators may not be able to obtain, or believe they cannot obtain, the necessary regulatory approvals; |

| • | collaborators may delay the development or commercialization of our product candidates in favor of developing or commercializing their own or another party’s product candidate; or |

| • | collaborators may decide to terminate or not to renew the collaboration for these or other reasons. |

As a result, collaboration agreements may not lead to development or commercialization of our product candidates in the most efficient manner or at all. For example, our former collaborator that licensed Zertane conducted clinical trials which we believe demonstrated efficacy in treating PE, but the collaborator undertook a merger that we believe altered its strategic focus and thereafter terminated the collaboration agreement. The Merger also created a potential conflict with a principal customer of the acquired company, which sells a product to treat premature ejaculation in certain European markets.

Collaboration agreements are generally terminable without cause on short notice. Once a collaboration agreement is signed, it may not lead to commercialization of a product candidate. We also face competition in seeking out collaborators. If we are unable to secure collaborations that achieve the collaborator’s objectives and meet our expectations, we may be unable to advance our products or product candidates and may not generate meaningful revenues.

We or our strategic partners may choose not to continue an existing product or choose not to develop a product candidate at any time during development, which would reduce or eliminate our potential return on investment for that product.

At any time and for any reason, we or our strategic partners may decide to discontinue the development or commercialization of a product or product candidate. If we terminate a program in which we have invested significant resources, we will reduce the return, or not receive any return, on our investment and we will have missed the opportunity to have allocated those resources to potentially more productive uses. If one of our strategic partners terminates a program, we will not receive any future milestone payments or royalties relating to that program under our agreement with that party.

Our pre-commercial product candidates are expected to undergo clinical trials that are time-consuming and expensive, the outcomes of which are unpredictable, and for which there is a high risk of failure. If clinical trials of our product candidates fail to satisfactorily demonstrate safety and efficacy to the FDA and other regulators, we or our collaborators may incur additional costs or experience delays in completing, or ultimately be unable to complete, the development and commercialization of these product candidates.

Pre-clinical testing and clinical trials are long, expensive and unpredictable processes that can be subject to extensive delays. We cannot guarantee that any clinical studies will be conducted as planned or completed on schedule, if at all. It may take several years to complete the pre-clinical testing and clinical development necessary to commercialize a drug or biologic, and delays or failure can occur at any stage. Interim results of clinical trials do not necessarily predict final results, and success in pre-clinical testing and early clinical trials does not ensure that later clinical trials will be successful. A number of companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in advanced clinical trials even after promising results in earlier trials and we cannot be certain that we will not face similar setbacks. The design of a clinical trial can determine whether its results will support approval of a product and flaws in the design of a clinical trial may not become apparent until the clinical trial is well advanced. An unfavorable outcome in one or more trials would be a major set-back for that product candidate and for us. Due to our limited financial resources, an unfavorable outcome in one or more trials may require us to delay, reduce the scope of, or eliminate one or more product development programs, which could have a material adverse effect on our business, prospects and financial condition and on the value of our common stock.

| 10 |

In connection with clinical testing and trials, we face a number of risks, including:

| • | a product candidate is ineffective, inferior to existing approved medicines, unacceptably toxic, or has unacceptable side effects; |

| • | patients may die or suffer other adverse effects for reasons that may or may not be related to the product candidate being tested; |

| • | the results may not confirm the positive results of earlier testing or trials; and |

| • | the results may not meet the level of statistical significance required by the FDA or other regulatory agencies to establish the safety and efficacy of the product candidate. |

If we do not successfully complete pre-clinical and clinical development, we will be unable to market and sell products derived from our product candidates and generate revenues. Even if we do successfully complete clinical trials, those results are not necessarily predictive of results of additional trials that may be needed before an NDA may be submitted to the FDA. Although there are a large number of drugs and biologics in development in the United States and other countries, only a small percentage result in the submission of an NDA to the FDA, even fewer are approved for commercialization, and only a small number achieve widespread physician and consumer acceptance following regulatory approval. If our clinical trials are substantially delayed or fail to prove the safety and effectiveness of our product candidates in development, we may not receive regulatory approval of any of these product candidates and our business, prospects and financial condition will be materially harmed.

Delays, suspensions and terminations in our clinical trials could result in increased costs to us and delay or prevent our ability to generate revenues.

Human clinical trials are very expensive, time-consuming, and difficult to design, implement and complete. We currently expect clinical trials of our therapeutic product candidates could take up to 24 months to complete, but the completion of trials for these candidates may be delayed for a variety of reasons, including delays in:

| • | demonstrating sufficient safety and efficacy to obtain regulatory approval to commence a clinical trial; |

| • | reaching agreement on acceptable terms with prospective CROs and clinical trial sites; |

| • | validating test methods to support quality testing of the drug substance and drug product; |

| • | obtaining sufficient quantities of the drug substance or device ports; |

| • | manufacturing sufficient quantities of a product candidate; |

| • | obtaining approval of an IND from the FDA; |

| • | obtaining institutional review board approval to conduct a clinical trial at a prospective clinical trial site; |

| • | determining dosing and clinical design and making related adjustments; and |

| • | patient enrollment, which is a function of many factors, including the size of the patient population, the nature of the protocol, the proximity of patients to clinical trial sites, the availability of effective treatments for the relevant disease and the eligibility criteria for the clinical trial. |

The commencement and completion of clinical trials for our product candidates may be delayed, suspended or terminated due to a number of factors, including:

| • | lack of effectiveness of product candidates during clinical trials; |

| • | adverse events, safety issues or side effects relating to the product candidates or their formulation or design; |

| • | inability to raise additional capital in sufficient amounts to continue clinical trials or development programs, which are very expensive; |

| • | the need to sequence clinical trials as opposed to conducting them concomitantly in order to conserve resources; |

| • | our inability to enter into collaborations relating to the development and commercialization of our product candidates; |

| • | failure by us or our collaborators to conduct clinical trials in accordance with regulatory requirements; |

| 11 |

| • | our inability or the inability of our collaborators to manufacture or obtain from third parties materials sufficient for use in pre-clinical studies and clinical trials; |

| • | governmental or regulatory delays and changes in regulatory requirements, policy and guidelines, including mandated changes in the scope or design of clinical trials or requests for supplemental information with respect to clinical trial results; |

| • | failure of our collaborators to advance our product candidates through clinical development; |

| • | delays in patient enrollment, variability in the number and types of patients available for clinical trials, and lower-than anticipated retention rates for patients in clinical trials; |

| • | difficulty in patient monitoring and data collection due to failure of patients to maintain contact after treatment; |

| • | a regional disturbance where we or our collaborative partners are enrolling patients in our clinical trials, such as a pandemic, terrorist activities or war, or a natural disaster; and |

| • | varying interpretations of our data, and regulatory commitments and requirements by the FDA and similar foreign regulatory agencies. |

Many of these factors may also ultimately lead to denial of an NDA for a product candidate. If we experience delay, suspensions or terminations in a clinical trial, the commercial prospects for the related product candidate will be harmed, and our ability to generate product revenues will be delayed.

In addition, we may encounter delays or product candidate rejections based on new governmental regulations, future legislative or administrative actions, or changes in FDA policy or interpretation during the period of product development. If we obtain required regulatory approvals, such approvals may later be withdrawn. Delays or failures in obtaining regulatory approvals may result in:

| • | varying interpretations of data and commitments by the FDA and similar foreign regulatory agencies; and |

| • | diminishment of any competitive advantages that such product candidates may have or attain. |

Furthermore, if we fail to comply with applicable FDA and other regulatory requirements at any stage during this regulatory process, we may encounter or be subject to:

| • | diminishment of any competitive advantages that such product candidates may have or attain; |

| • | delays or termination in clinical trials or commercialization; |

| • | refusal by the FDA or similar foreign regulatory agencies to review pending applications or supplements to approved applications; |

| • | product recalls or seizures; |

| • | suspension of manufacturing; |

| • | withdrawals of previously approved marketing applications; and |

| • | fines, civil penalties, and criminal prosecutions. |

We or our collaborators intend to seek FDA approval for some of our product candidates using an expedited process established by the FDA. If we, or our collaborators, are unable to secure clearances to use expedited development pathways from the FDA for certain of our drug product candidates, we, or they, may be required to conduct additional pre-clinical studies or clinical trials beyond those that we, or they, contemplate, which could increase the expense of obtaining, and delay the receipt of, necessary marketing approvals and of any product revenues.

Assuming successful completion of clinical trials, we expect to submit NDAs to the FDA at various times in the future under Section 505(b)(2) of the Food, Drug and Cosmetic Act, as amended, or the FDCA. NDAs submitted under this section are eligible to receive FDA approval by relying in part on the FDA’s findings of safety and efficacy for a previously approved drug. The FDA’s 1999 guidance on Section 505(b)(2) applications states that new indications for a previously approved drug, a new combination product, a modified active ingredient, or changes in dosage form, strength, formulation, and route of administration of a previously approved product are encompassed within the Section 505(b)(2) NDA process. Relying on Section 505(b)(2) is advantageous because we or our collaborators may not be required (i) to perform the full range of safety and efficacy trials that is otherwise required to secure approval of a new drug, and (ii) obtain a “right of reference” from the applicant that obtained approval of the previously approved drug. However, a Section 505(b)(2) application must support the proposed change of the previously approved drug by including necessary and adequate information, as determined by the FDA, and the FDA may still require us to perform a portion or the full range of safety and efficacy trials. There can be no assurance that we would be successful under any Section 505(b)(2) application. We specifically intended to do this for Zertane and any future collaborator could as well.

| 12 |

The medical device regulatory clearance or approval process is expensive, time consuming and uncertain, and the failure to obtain and maintain required clearances or approvals could prevent us from broadly commercializing the MiOXSYS System for clinical use.

The MiOXSYS System is subject to 510(k) clearance by the FDA prior to its marketing for commercial use in the United States, and to regulatory approvals beyond CE Marking required by certain foreign governmental entities prior to its marketing outside the United States. In addition, any changes or modifications to a device that has received regulatory clearance or approval that could significantly affect its safety or effectiveness, or would constitute a major change in its intended use, may require the submission of a new application for 510(k) clearance, pre-market approval, or foreign regulatory approvals. The 510(k) clearance and pre-market approval processes, as well as the process of obtaining foreign approvals, can be expensive, time consuming and uncertain. It generally takes from four to twelve months from submission to obtain 510(k) clearance, and from one to three years from submission to obtain pre-market approval; however, it may take longer, and 510(k) clearance or pre-market approval may never be obtained. We have limited experience in filing FDA applications for 510(k) clearance and pre-market approval. In addition, we are required to continue to comply with applicable FDA and other regulatory requirements even after obtaining clearance or approval. There can be no assurance that we will obtain or maintain any required clearance or approval on a timely basis, or at all. Any failure to obtain or any material delay in obtaining FDA clearance or any failure to maintain compliance with FDA regulatory requirements could harm our business, financial condition and results of operations.

The approval process for pharmaceutical and medical device products outside the United States varies among countries and may limit our ability to develop, manufacture and sell our products internationally. Failure to obtain marketing approval in international jurisdictions would prevent our product candidates from being marketed abroad.

In order to market and sell our products in the European Union and many other jurisdictions, we, and our collaborators, must obtain separate marketing approvals and comply with numerous and varying regulatory requirements. The approval procedure varies among countries and may involve additional testing. We may conduct clinical trials for, and seek regulatory approval to market, our product candidates in countries other than the United States. Depending on the results of clinical trials and the process for obtaining regulatory approvals in other countries, we may decide to first seek regulatory approvals of a product candidate in countries other than the United States, or we may simultaneously seek regulatory approvals in the United States and other countries. If we or our collaborators seek marketing approval for a product candidate outside the United States, we will be subject to the regulatory requirements of health authorities in each country in which we seek approval. With respect to marketing authorizations in Europe, we will be required to submit a European Marketing Authorization Application, or MAA, to the European Medicines Agency, or EMA, which conducts a validation and scientific approval process in evaluating a product for safety and efficacy. The approval procedure varies among regions and countries and may involve additional testing, and the time required to obtain approval may differ from that required to obtain FDA approval.

Obtaining regulatory approvals from health authorities in countries outside the United States is likely to subject us to all of the risks associated with obtaining FDA approval described above. In addition, marketing approval by the FDA does not ensure approval by the health authorities of any other country, and approval by foreign health authorities does not ensure marketing approval by the FDA.

| 13 |

Even if we, or our collaborators, obtain marketing approvals for our product candidates, the terms of approvals and ongoing regulation of our products may limit how we or they market our products, which could materially impair our ability to generate revenue.

Even if we receive regulatory approval for a product candidate, this approval may carry conditions that limit the market for the product or put the product at a competitive disadvantage relative to alternative therapies. For instance, a regulatory approval may limit the indicated uses for which we can market a product or the patient population that may utilize the product, or may be required to carry a warning in its labeling and on its packaging. Products with boxed warnings are subject to more restrictive advertising regulations than products without such warnings. These restrictions could make it more difficult to market any product candidate effectively. Accordingly, assuming we, or our collaborators, receive marketing approval for one or more of our product candidates, we, and our collaborators expect to continue to expend time, money and effort in all areas of regulatory compliance.

Any of our products and product candidates for which we, or our collaborators, obtain marketing approval in the future could be subject to post-marketing restrictions or withdrawal from the market and we, and our collaborators, may be subject to substantial penalties if we, or they, fail to comply with regulatory requirements or if we, or they, experience unanticipated problems with our products following approval.

Any of our approved products and product candidates for which we, or our collaborators, obtain marketing approval, as well as the manufacturing processes, post-approval studies and measures, labeling, advertising and promotional activities for such products, among other things, are or will be subject to continual requirements of and review by the FDA and other regulatory authorities. These requirements include submissions of safety and other post-marketing information and reports, registration and listing requirements, requirements relating to manufacturing, quality control, quality assurance and corresponding maintenance of records and documents, requirements regarding the distribution of samples to physicians and recordkeeping. Even if marketing approval of a product candidate is granted, the approval may be subject to limitations on the indicated uses for which the product may be marketed or to the conditions of approval, including the FDA requirement to implement a REMS to ensure that the benefits of a drug or biological product outweigh its risks.

The FDA may also impose requirements for costly post-marketing studies or clinical trials and surveillance to monitor the safety or efficacy of a product. The FDA and other agencies, including the Department of Justice, closely regulate and monitor the post-approval marketing and promotion of products to ensure that they are manufactured, marketed and distributed only for the approved indications and in accordance with the provisions of the approved labeling. The FDA imposes stringent restrictions on manufacturers’ communications regarding off-label use and if we, or our collaborators, do not market any of our product candidates for which we, or they, receive marketing approval for only their approved indications, we, or they, may be subject to warnings or enforcement action for off-label marketing. Violation of the FDCA and other statutes, including the False Claims Act, relating to the promotion and advertising of prescription drugs may lead to investigations or allegations of violations of federal and state health care fraud and abuse laws and state consumer protection laws.

If we do not achieve our projected development and commercialization goals in the timeframes we announce and expect, the commercialization of our product candidates may be delayed, and our business will be harmed.

We sometimes estimate for planning purposes the timing of the accomplishment of various scientific, clinical, regulatory and other product development objectives. These milestones may include our expectations regarding the commencement or completion of scientific studies and clinical trials, the submission of regulatory filings, or commercialization objectives. From time to time, we may publicly announce the expected timing of some of these milestones, such as the initiation or completion of an ongoing clinical trial, the initiation of other clinical programs, receipt of marketing approval, or a commercial launch of a product. The achievement of many of these milestones may be outside of our control. All of such milestones are based on a variety of assumptions which may cause the timing of achievement of the milestones to vary considerably from our estimates, including:

| • | our available capital resources or capital constraints we experience; |

| • | the rate of progress, costs and results of our clinical trials and research and development activities, including the extent of scheduling conflicts with participating clinicians and collaborators, and our ability to identify and enroll patients who meet clinical trial eligibility criteria; |

| • | our receipt of approvals from the FDA and other regulatory agencies and the timing thereof; |

| • | other actions, decisions or rules issued by regulators; |

| 14 |

| • | our ability to access sufficient, reliable and affordable supplies of compounds used in the manufacture of our product candidates; |

| • | the efforts of our collaborators with respect to the commercialization of our products; and |

| • | the securing of, costs related to, and timing issues associated with, product manufacturing as well as sales and marketing activities. |

If we fail to achieve announced milestones in the timeframes we announce and expect, the commercialization of our product candidates may be delayed and our business, prospects and results of operations may be harmed.

We rely on third parties to conduct our clinical trials and perform data collection and analysis, which may result in costs and delays that prevent us from successfully commercializing product candidates.

We rely, and will rely in the future, on medical institutions, clinical investigators, contract research organizations, contract laboratories, and collaborators to perform data collection and analysis and others to carry out our clinical trials. Our development activities or clinical trials conducted in reliance on third parties may be delayed, suspended, or terminated if:

| • | the third parties do not successfully carry out their contractual duties or fail to meet regulatory obligations or expected deadlines; |

| • | we replace a third party; or |

| • | the quality or accuracy of the data obtained by third parties is compromised due to their failure to adhere to clinical protocols, regulatory requirements, or for other reasons. |

Third party performance failures may increase our development costs, delay our ability to obtain regulatory approval, and delay or prevent the commercialization of our product candidates. While we believe that there are numerous alternative sources to provide these services, in the event that we seek such alternative sources, we may not be able to enter into replacement arrangements without incurring delays or additional costs.

In addition, for Zertane, we are using, and relying on, single suppliers and single manufacturers for drug supply for our planned Phase 3 clinical trials and our commercial supply. Although there are potential alternative suppliers and manufacturers for Zertane if need be, we have not qualified these vendors to date. If we or a collaborator were required to change vendors, it could result in a failure to meet regulatory requirements or projected timelines and necessary quality standards for successful manufacturing of the various required lots of material for our development and commercialization efforts, any of which could have an adverse effect on any business, prospects and financial condition.

Even if collaborators with which we contract in the future successfully complete clinical trials of our product candidates, those product candidates may not be commercialized successfully for other reasons.

Even if we contract with collaborators that successfully complete clinical trials for one or more of our product candidates, those candidates may not be commercialized for other reasons, including:

| • | failure to receive regulatory clearances required to market them as drugs; |

| • | being subject to proprietary rights held by others; |

| • | being difficult or expensive to manufacture on a commercial scale; |

| • | having adverse side effects that make their use less desirable; or |

| • | failing to compete effectively with products or treatments commercialized by competitors. |

| 15 |

Any third-party manufacturers we engage are subject to various governmental regulations, and we may incur significant expenses to comply with, and experience delays in, our product commercialization as a result of these regulations.

The manufacturing processes and facilities of third-party manufacturers we engage are required to comply with the federal Quality System Regulation, or QSR, which covers procedures and documentation of the design, testing, production, control, quality assurance, labeling, packaging, sterilization, storage and shipping of devices. The FDA enforces the QSR through periodic unannounced inspections of manufacturing facilities. Any inspection by the FDA could lead to additional compliance requests that could cause delays in our product commercialization. Failure to comply with applicable FDA requirements, or later discovery of previously unknown problems with the manufacturing processes and facilities of third-party manufacturers we engage, including the failure to take satisfactory corrective actions in response to an adverse QSR inspection, can result in, among other things:

| • | administrative or judicially imposed sanctions; |

| • | injunctions or the imposition of civil penalties; |

| • | recall or seizure of the product in question; |

| • | total or partial suspension of production or distribution; |

| • | the FDA’s refusal to grant pending future clearance or pre-market approval; |

| • | withdrawal or suspension of marketing clearances or approvals; |

| • | clinical holds; |

| • | warning letters; |

| • | refusal to permit the export of the product in question; and |

| • | criminal prosecution. |

Any of these actions, in combination or alone, could prevent us from marketing, distributing or selling our products, and would likely harm our business.

In addition, a product defect or regulatory violation could lead to a government-mandated or voluntary recall by us. We believe the FDA would request that we initiate a voluntary recall if a product was defective or presented a risk of injury or gross deception. Regulatory agencies in other countries have similar authority to recall drugs or devices because of material deficiencies or defects in design or manufacture that could endanger health. Any recall would divert our management attention and financial resources, expose us to product liability or other claims, and harm our reputation with customers.

We face substantial competition from companies with considerably more resources and experience than we have, which may result in others discovering, developing, receiving approval for, or commercializing products before or more successfully than us.

We compete with companies that design, manufacture and market already-existing and new urology products. We anticipate that we will face increased competition in the future as new companies enter the market with new technologies and/or our competitors improve their current products. One or more of our competitors may offer technology superior to ours and render our technology obsolete or uneconomical. Most of our current competitors, as well as many of our potential competitors, have greater name recognition, more substantial intellectual property portfolios, longer operating histories, significantly greater resources to invest in new technologies, more substantial experience in new product development, greater regulatory expertise, more extensive manufacturing capabilities and the distribution channels to deliver products to customers. If we are not able to compete successfully, we may not generate sufficient revenue to become profitable. Our ability to compete successfully will depend largely on our ability to:

| • | expand the market for any approved products; |

| • | successfully commercialize our product candidates alone or with commercial partners; |

| • | discover and develop product candidates that are superior to other products in the market; |

| • | obtain required regulatory approvals; |

| • | attract and retain qualified personnel; and |

| 16 |

| • | obtain patent and/or other proprietary protection for our product candidates. |

Established pharmaceutical companies devote significant financial resources to discovering, developing or licensing novel compounds that could make our products and product candidates obsolete. Our competitors may obtain patent protection, receive FDA approval, and commercialize medicines before us. Other companies are or may become engaged in the discovery of compounds that may compete with the product candidates we are developing.

For the MiOXSYS System and ProstaScint, we compete with companies that design, manufacture and market already existing and new in-vitro diagnostics systems and tests and radio-imaging agents for cancer detection. Additionally, with respect to Primsol, we compete with numerous companies who produce antimicrobial treatments for various pathogens inclusive of products containing trimethoprim as contained in Primsol.

While no oral medication has been approved by the FDA for PE, Priligy (dapoxetine) has been approved in some countries. Many commonly prescribed oral medications may delay orgasm and be prescribed alone or in combination with other treatments. These medications include antidepressants, treatments for erectile dysfunction and tramadol for the treatment of pain. We also are aware of topical products which are over-the-counter, or OTC, monograph products for premature ejaculation which include brands such as Promescent (Absorption Pharmaceuticals), a topical spray approved by the FDA in 2013, EjectDelay (Innovus Pharma) and PreBoost (Aspen Park Pharmaceuticals), all of which would compete with Zertane.