Attached files

| file | filename |

|---|---|

| EX-23.2 - EXHIBIT 23.2 - Pattern Energy Group Inc. | pegi2015123110kexhbit232.htm |

| EX-31.1 - EXHIBIT 31.1 - Pattern Energy Group Inc. | pegi2015123110kexhbit311.htm |

| EX-31.2 - EXHIBIT 31.2 - Pattern Energy Group Inc. | pegi2015123110kexhbit312.htm |

| EX-21.1 - EXHIBIT 21.1 - Pattern Energy Group Inc. | pegi2015123110kexhbit211.htm |

| EX-23.1 - EXHIBIT 23.1 - Pattern Energy Group Inc. | pegi2015123110kexhbit231.htm |

| EX-32 - EXHIBIT 32 - Pattern Energy Group Inc. | pegi2015123110kexhbit32.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2015.

-OR-

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 001-36087

PATTERN ENERGY GROUP INC.

(Exact name of Registrant as specified in its charter)

Delaware | 90-0893251 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

Pier 1, Bay 3, San Francisco, CA 94111

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (415) 283-4000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Class A Common Stock, par value $0.01 per share | NASDAQ Global Select Market Toronto Stock Exchange | |

Securities registered pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | ¨ | |

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ¨ No ý

The aggregate market value of the voting stock and non-voting stock held by non-affiliates of the registrant based upon the last trading price of the registrant’s Class A common stock as reported on the NASDAQ Global Market on June 30, 2015 was approximately $1,462,489,654. This excludes 17,705,514 shares of Class A common stock held by directors, officers and Pattern Renewables LP and certain of its affiliates. Exclusion of shares does not reflect a determination that persons are affiliates for any other purpose.

The registrant’s Class A common stock began trading on the NASDAQ Global Market under the symbol "PEGI" and on the Toronto Stock Exchange under the symbol "PEG" on October 2, 2013.

On February 24, 2016, the registrant had 74,643,763 shares of Class A common stock, $0.01 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement relating to its 2016 annual meeting of stockholders (the "2016 Proxy Statement") are incorporated by reference into Part III of this Form 10-K where indicated. The 2016 Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

TABLE OF CONTENTS

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

2

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K ("Form 10-K") contains statements that may constitute forward-looking statements. You can identify these statements by forward-looking words such as "anticipate," "believe," "could," "estimate," "expect," "intend," "may," "plan," "potential," "should," "will," "would," or similar words. You should read statements that contain these words carefully because they discuss our current plans, strategies, prospects, and expectations concerning our business, operating results, financial condition, and other similar matters. While we believe that these forward-looking statements are reasonable as and when made, there may be events in the future that we are not able to predict accurately or control, and there can be no assurance that future developments affecting our business will be those that we anticipate. Our forward-looking statements involve significant risks and uncertainties (some of which are beyond our control) and assumptions that could cause actual results to differ materially from our historical experience and our present expectations or projections. Important factors that could cause our actual results to differ from those in the forward-looking statements, include but are not limited to, those summarized below and further described in Part I, Item 1A "Risk Factors:"

• | our ability to complete acquisitions of power projects; |

• | our ability to complete construction of construction projects and transition them into financially successful operating projects; |

• | fluctuations in supply, demand, prices and other conditions for electricity, other commodities and renewable energy credits ("RECs"); |

• | our electricity generation, our projections thereof and factors affecting production, including wind and other conditions, other weather conditions, availability and curtailment; |

• | changes in law, including applicable tax laws; |

• | public response to and changes in the local, state, provincial and federal regulatory framework affecting renewable energy projects, including the U.S. federal production tax credit ("PTC"), investment tax credit ("ITC") and potential reductions in Renewable Portfolio Standards ("RPS") requirements; |

• | the ability of our counterparties to satisfy their financial commitments or business obligations; |

• | the availability of financing, including tax equity financing, for our power projects; |

• | an increase in interest rates; |

• | our substantial short-term and long-term indebtedness, including additional debt in the future; |

• | competition from other power project developers; |

• | development constraints, including the availability of interconnection and transmission; |

• | potential environmental liabilities and the cost and conditions of compliance with applicable environmental laws and regulations; |

• | our ability to operate our business efficiently, manage capital expenditures and costs effectively and generate cash flow; |

• | our ability to retain and attract executive officers and key employees; |

• | our ability to keep pace with and take advantage of new technologies; |

• | the effects of litigation, including administrative and other proceedings or investigations, relating to our wind power projects under construction and those in operation; |

• | conditions in energy markets as well as financial markets generally, which will be affected by interest rates, foreign currency exchange rate fluctuations and general economic conditions; |

• | the effectiveness of our currency risk management program; |

• | the effective life and cost of maintenance of our wind turbines and other equipment; |

• | the increased costs of, and tariffs on, spare parts; |

• | scarcity of necessary equipment; |

• | negative public or community response to wind power projects; |

• | the value of collateral in the event of liquidation; and |

• | other factors discussed under "Risk Factors." |

3

Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. We undertake no obligation to publicly update or revise any forward-looking statements after the date they are made, whether as a result of new information, future events or otherwise.

MEANING OF CERTAIN REFERENCES

Unless the context provides otherwise, references herein to "we," "our," "us," "our company" and "Pattern" refer to Pattern Energy Group Inc., a Delaware corporation, together with its consolidated subsidiaries. In addition, unless the context requires otherwise, any reference in this Form 10-K to:

• | "Conversion Event" refers to the event pursuant to which all of our Class B shares automatically converted into Class A shares on a one-for-one basis on December 31, 2014; |

• | "employee transfer" refers to the event contemplated by the Management Services Agreement pursuant to which we have the option, exercisable by delivery of written notice of exercise to Pattern Development at any time during a period of eighteen (18) months commencing July 1, 2015, to require Pattern Development to cause the employees of Pattern Development and its subsidiaries to become employees of us and our subsidiaries. From and after the occurrence of the employee transfer event, we and Pattern Development will cooperate to cause such employee transfer to occur by the six month anniversary of the employee transfer event or as soon as reasonably practical thereafter; |

• | "FERC" refers to the U.S. Federal Energy Regulatory Commission; |

• | "FIT" refers to feed-in-tariff regime; |

• | "FPA" refers to the Federal Power Act; |

• | "Identified ROFO Projects" refers to thirteen projects that we identified as development projects, each owned by Pattern Development and subject to our Project Purchase Right, consisting of Armow, Meikle, Conejo Solar, Belle River, Henvey Inlet, Mont Sainte-Marguerite, North Kent, Broadview projects, Grady, Tsugaru, Ohorayama, Kanagi Solar and Futtsu Solar projects. The Tsugaru, Ohorayama, Kanagi Solar and Futtsu Solar projects are held through Pattern Development’s majority stake investment in Green Power Investment Corporation ("GPI") based in Tokyo, Japan; |

• | "IPPs" refers to independent power producers; |

• | "ISOs" refers to independent system organizations, which are organizations that administer wholesale electricity markets; |

• | "ITCs" refers to investment tax credits; |

• | "Management Services Agreement" refers to the bilateral services agreement between us and Pattern Development, as amended; |

• | "MW" refers to megawatts; |

• | "MWh" refers to megawatt hours; |

• | "Non-Competition Agreement" refers to a non-competition agreement between us and Pattern Development pursuant to which Pattern Development agrees that, for so long as any of our Purchase Rights are exercisable, it will not compete with us for acquisitions of power generation or transmission projects from third parties; |

• | "OCC" refers to our operations control center; |

• | "Pattern Development" refers to Pattern Energy Group LP and its subsidiaries (other than us and our subsidiaries); |

• | "Pattern Development Purchase Rights" refer to the right to acquire Pattern Development itself or substantially all of its assets, as contemplated by the Purchase Rights Agreement between us and Pattern Development; |

• | "power sale agreements" refer to PPAs and/or hedging arrangements, as applicable; |

• | "PPAs" refer to power purchase agreements; |

4

• | "Project Purchase Right" refers to a right of first offer with respect to any power project that Pattern Development decides to sell, including the Identified ROFO Projects; |

• | "Purchase Rights" refer to the Project Purchase Right and the Pattern Development Purchase Rights, as contemplated by the Purchase Rights Agreement between us and Pattern Development; |

• | "RECs" refers to renewable energy credits; |

• | "Riverstone" refers to Riverstone Holdings LLC; |

• | "ROFO" refers to right of first offer; |

• | "RPS" refers to Renewable Portfolio Standards; |

• | "Sarbanes-Oxley Act" refers to the Sarbanes-Oxley Act of 2002; |

• | "Samsung" means Samsung C&T Corporation; and |

• | "U.S. Treasury" refers to the U.S. Department of the Treasury. |

5

CURRENCY AND EXCHANGE RATE INFORMATION

In this Form 10-K, references to "C$" and "Canadian dollars" are to the lawful currency of Canada and references to "$", "US$" and "U.S. dollars" are to the lawful currency of the United States. All dollar amounts herein are in U.S. dollars, unless otherwise stated.

Our historical consolidated financial statements are presented in U.S. dollars. The following chart sets forth for each of 2015, 2014 and 2013, the high, low, period average and period end noon buying rates of Canadian dollars expressed as Canadian dollars per US$1.00.

Canadian Dollars per US$1.00 | |||||||||||||||||||

High | Low | Period Average(1) | Period End | ||||||||||||||||

Year | |||||||||||||||||||

2015 | C$ | 1.3987 | C$ | 1.1601 | C$ | 1.2788 | C$ | 1.3835 | |||||||||||

2014 | 1.1643 | 1.0614 | 1.1045 | 1.1501 | |||||||||||||||

2013 | 1.0697 | 0.9839 | 1.0300 | 1.0637 | |||||||||||||||

(1) | The average of the noon buying rates on the last business day of each month during the relevant one-year period and, in respect of monthly or interim period information, the average of the noon buying rates on each business day for the relevant period. |

The noon buying rate in Canadian dollars on February 24, 2016 was US$1.00 = C$1.3707.

The above rates differ from the actual rates used in our consolidated historical financial statements and the calculation of cash available for distribution and dividends we declared and paid described elsewhere in this Form 10-K. Our inclusion of these exchange rates is not meant to suggest that the U.S. dollar amounts actually represent such Canadian dollar amounts or that such amounts could have been converted into Canadian dollars at any particular rate or at all.

For information on the impact of fluctuations in exchange rates on our operations, see Item 1A "Risk Factors—Risks Related to Our Projects—Currency exchange rate fluctuations may have an impact on our financial results and condition" and Item 7A "Quantitative and Qualitative Disclosure About Market Risk—Foreign Currency Exchange Rate Risk."

6

PART I

Item 1. | Business. |

Overview

We are an independent power company focused on owning and operating power projects with stable long-term cash flows in attractive markets with potential for continued growth of our business. We hold interests in 16 wind power projects located in the United States, Canada and Chile that use proven, best-in-class technology and have a total owned capacity of 2,282 MW. Each of our projects has contracted to sell all or a majority of its output pursuant to a long-term, fixed-price power sale agreement. Eighty-nine percent of the electricity to be generated by our projects will be sold under our power sale agreements which have a weighted average remaining contract life of approximately 14 years.

Our growth strategy is focused on the acquisition of operational and construction-ready power projects from Pattern Development and other third parties that we believe will contribute to the growth of our business and enable us to increase our dividend per Class A share over time. Pattern Development is a leading developer of renewable energy and transmission projects. We believe Pattern Development’s ownership position in our company incentivizes Pattern Development to support the successful execution of our objectives and business strategy, including through the development of projects to the stage where they are at least construction-ready. Currently, Pattern Development has a 5,900 MW pipeline of development projects, all of which are subject to our right of first offer. We target achieving a total owned capacity of 5,000 MW by year end 2019 through a combination of acquisitions from Pattern Development and other third parties capitalizing on the large and fragmented global renewable energy market. In addition, we expect opportunities in Japan and Mexico will form part of our growth strategy.

Our Core Values and Financial Objectives

We intend to maximize long-term value for our stockholders in an environmentally responsible manner and with respect for the communities in which we operate. Our business is built around three core values of creative energy and spirit, pride of ownership and follow-through, and a team first attitude, which guide us in:

• | creating a safe and high-integrity work environment for our employees; |

• | applying rigorous analysis to all aspects of our business in a timely, disciplined and functionally integrated manner to understand patterns in wind regimes, technology developments, market trends and regulatory, financial and legal constraints; and |

• | working proactively with our stakeholders to address environmental and community concerns, which we believe is a socially responsible approach that also benefits our business by reducing operating risks at our projects. |

Our financial objectives, which we believe will maximize long-term value for our stockholders, are to:

• | produce stable and sustainable cash available for distribution; |

• | selectively grow our project portfolio and our dividend per Class A share; and |

• | maintain a strong balance sheet and flexible capital structure. |

7

Our Projects

The following table provides an overview of our wind projects:

Location and Start-up | Capacity (MW) | Power Sale Agreements | |||||||||||||||||||

Projects | Location | Construction Start(1) | Commercial Operations(2) | Rated(3) | Owned(4) | Type | Contracted Volume(5) | Counterparty | Counterparty Credit Rating(6) | Expiration | |||||||||||

Operating Projects | |||||||||||||||||||||

Gulf Wind | Texas | Q1 2008 | Q3 2009 | 283 | 283 | Hedge | (7) | ~58% | Morgan Stanley | BBB+/A3 | 2019 | ||||||||||

Hatchet Ridge | California | Q4 2009 | Q4 2010 | 101 | 101 | PPA | 100% | Pacific Gas & Electric | BBB/A3 | 2025 | |||||||||||

St. Joseph | Manitoba | Q1 2010 | Q2 2011 | 138 | 138 | PPA | 100% | Manitoba Hydro | AA/Aa2 | (8) | 2039 | ||||||||||

Spring Valley | Nevada | Q3 2011 | Q3 2012 | 152 | 152 | PPA | 100% | NV Energy | BBB+/Baa2 | 2032 | |||||||||||

Santa Isabel | Puerto Rico | Q4 2011 | Q4 2012 | 101 | 101 | PPA | 100% | Puerto Rico Electric Power Authority | CC/Caa3 | 2037 | |||||||||||

Ocotillo | California | Q3 2012 | Q4 2012 | 223 | 223 | PPA | 100% | San Diego Gas & Electric | A/A1 | 2033 | |||||||||||

Ocotillo | California | Q2 2013 | 42 | 42 | PPA | 100% | San Diego Gas & Electric | A/A1 | 2033 | ||||||||||||

South Kent | Ontario | Q1 2013 | Q2 2014 | 270 | 135 | PPA | 100% | Independent Electricity System Operator | Aa2 | (9) | 2034 | ||||||||||

El Arrayán | Chile | Q3 2012 | Q2 2014 | 115 | 81 | Hedge | (10) | ~74% | Minera Los Pelambres | NA | 2034 | ||||||||||

Panhandle 1 | Texas | Q3 2013 | Q2 2014 | 218 | 172 | Hedge | (11) | ~80% | Citigroup Energy Inc. | BBB+/Baa1 | 2027 | ||||||||||

Panhandle 2 | Texas | Q4 2013 | Q4 2014 | 182 | 147 | Hedge | (11) | ~80% | Morgan Stanley | BBB+/A3 | 2027 | ||||||||||

Grand | Ontario | Q3 2013 | Q4 2014 | 149 | 67 | PPA | 100% | Independent Electricity System Operator | Aa2 | (9) | 2034 | ||||||||||

Post Rock | Kansas | Q4 2011 | Q4 2012 | 201 | 120 | PPA | 100% | Westar Energy, Inc. | BBB+/Baa1 | 2032 | |||||||||||

Lost Creek | Missouri | Q2 2009 | Q2 2010 | 150 | 150 | PPA | 100% | Associated Electric Cooperative, Inc. | AA/A2 | 2030 | |||||||||||

K2 | Ontario | Q1 2014 | Q2 2015 | 270 | 90 | PPA | 100% | Independent Electricity System Operator | Aa2 | (9) | 2035 | ||||||||||

Logan's Gap | Texas | Q4 2014 | Q3 2015 | 200 | 164 | PPA | ~58% | Wal-Mart Stores, Inc. | AA/Aa2 | 2025 | |||||||||||

Hedge | (12) | ~17% | Merrill Lynch Commodities, Inc. | BBB+/Baa1 | 2028 | ||||||||||||||||

Amazon Wind Farm Fowler Ridge | Indiana | Q2 2015 | Q4 2015 | 150 | 116 | PPA | 100% | (13) | Amazon.com, Inc. | AA-/Baa1 | (14) | 2028 | |||||||||

2,945 | 2,282 | ||||||||||||||||||||

(1) | Represents date of commencement of construction. |

(2) | Represents date of actual or anticipated commencement of commercial operations. |

(3) | Rated capacity represents the maximum electricity generating capacity of a project in MW. As a result of wind and other conditions, a project or a turbine will not operate at its rated capacity at all times and the amount of electricity generated may be less than its rated capacity. |

8

(4) | Owned capacity represents the maximum, or rated, electricity generating capacity of the project in MW multiplied by our percentage ownership interest in the distributable cash flow of the project. |

(5) | Represents the percentage of a project’s total estimated average annual MWh of electricity generation contracted under power sale agreements or hedge arrangements. |

(6) | Reflects the counterparty’s or counterparty guarantor's corporate credit ratings issued by either S&P or Moody’s, or both S&P and Moody's, as of December 31, 2015. |

(7) | Represents a 10-year fixed-for-floating power price swap. See Item 2 "Properties—Operating Projects—Gulf Wind." |

(8) | Reflects the corporate credit ratings of the Province of Manitoba, which owns 100% of Manitoba Hydro-Electric. |

(9) | Reflects the corporate credit ratings of the Province of Ontario, which owns 100% of the Independent Electricity System Operator ("IESO"), formerly the Ontario Power Authority. |

(10) | Represents a 20-year fixed-for-floating swap. See Item 2 "Properties—Operating Projects—El Arrayán." |

(11) | Represents a fixed-for-floating swap of more than ten years duration. See Item 2 "Properties—Operating Projects—Panhandle 1 and Panhandle 2." |

(12) | Represents a 13-year fixed-for-floating swap. See Item 2 "Properties—Operating Projects—Logan’s Gap." |

(13) | Contracted volume begins at 50% and increases pro rata to 100% over a period of 18 months, beginning January 2016. |

(14) | Contractual counterparty is a wholly-owned subsidiary of Amazon Web Services and obligations are guaranteed by Amazon.com, Inc. |

Each of our projects has gone through a rigorous vetting process in order to meet our investment and our lenders’ financing criteria. As a result, our projects generally have the following characteristics:

• | multi-year on-site wind data analysis tied to one or more long-term wind energy reference sources. Pattern Development employs a full-time meteorological team that manages and verifies third party wind analysis. This wind analysis is carefully vetted through detailed studies by internal and independent experts in meteorology and statistics to derive an expected production profile based on daily and seasonal wind patterns, structural interference, topography and atmospheric conditions. Our average on-site wind data collection is over four years (or approximately seven years including post-construction data collection); |

• | long-term power sale agreements designed to ensure a predictable revenue stream. As is typical in our industry, we sell our electricity at a fixed price on a contingent, as-produced basis such that only the electricity that we generate is sold to and must be purchased by the counterparty at the agreed price. Our power sale agreements have a weighted average remaining contract life of approximately 14 years; |

• | contractually secured real estate property and easement rights for a period well in excess of the project’s expected useful life and contractual obligations. Each of our projects has land rights for 25 years or more; |

• | a firm right to interconnect to the electricity grid through interconnection agreements, which define the cost allocation and schedule for interconnection, as well as any upgrades required to connect the project to the transmission system. Our interconnection agreements allow our projects to connect to the electricity transmission system. Market rules and protocols generally govern dispatch of our electricity generation and allow it to flow freely into the grid as it is produced, except in very limited circumstances where our projects can be curtailed, for example during system emergencies; |

• | long-term, limited-recourse, amortizing project financing designed to match the long-lived nature of our power projects and the related power sales agreements. The interest rates on our long-term loans are fixed for the tenor of the loans or are subject to fixed-for-floating swaps that match the amortization schedules of the debt; |

• | all necessary construction and operating permits and other requisite federal, state or provincial and local permits, and regulatory approvals secured, which critical permits typically include federal aviation, state or provincial environmental approvals and local zoning and land-use permits and are designed to protect the community, cultural resources, plants, animal and other affected resources at or near the facility; |

• | fixed-price turbine supply and construction contracts with guaranteed completion dates to ensure that our projects are completed on time and within the estimated budget. The construction period for our projects has typically been less than one year, although in certain instances circumstances warrant a longer construction period; |

• | an operations and maintenance service program based on our own on-site personnel and central operations management as well as equipment warranties and service arrangements with qualified contractors experienced in wind project maintenance. We have existing turbine equipment warranties for approximately 75% of our operating turbine units; and |

• | safety, environmental and community programs to support our existing projects and relationships in the communities in which we operate. |

9

For additional information regarding each of our projects, see Item 2 "Properties." Our ability to transition each of our construction projects to commercial operations and achieve anticipated power output at all of our operating projects is subject to numerous risks and uncertainties as described under Item 1A "Risk Factors."

Our Business Strategy

We intend to make profitable investments in environmentally responsible power projects, while embracing a long-term commitment to the communities in which we operate. To achieve our financial objectives while adhering to our core values, we intend to execute the following business strategies:

Maintaining and Increasing the Value of Our Projects

We intend to efficiently operate our projects to meet projected revenue and cash available for distribution. We expect to maximize the long-term value of our projects by focusing on value-oriented project availability (by ensuring our projects are operational when the wind is strong and PPA prices are at their highest) and by regularly scheduled and preventative maintenance. We believe that good operating performance begins with a long-term maintenance program for our equipment. We also seek to improve performance or lower operating costs by working closely with our equipment vendors and considering contracting with third parties, when appropriate.

We believe it is important to employ our own personnel in aspects of our business that we deem critical to the value of our projects but to contract with reliable third parties for on-going major maintenance of our turbines and similar specialized services such as repairs on our substations or transmission lines. As a result, we employ on-site personnel, maintain a 24/7 operations control center to monitor our projects and control all critical aspects of commercial asset management.

Selectively Growing Our Business

Our strategy for growth is focused on the acquisition of operational and construction-ready power projects from Pattern Development and other third parties that we believe will contribute to the growth of our business and enable us to increase our dividend per Class A share over time. We expect that projects we may acquire in the future will represent a logical extension of our existing business and be consistent with our risk profile, and that any incremental assumption of risk will require commensurate expectations of higher returns. As a result, our near-term growth strategy will remain focused on largely contracted cash flows with creditworthy counterparties and operating or in-construction projects.

We expect that new opportunities will arise from our relationship with Pattern Development, which provides us with the opportunity to acquire projects that it successfully develops and efficiently completing construction and achieving commercial operations at these projects.

10

Below is a summary of the Identified ROFO Projects that we expect to acquire from Pattern Development in connection with our Project Purchase Right.

Capacity (MW) | |||||||||||||||

Identified ROFO Projects | Status | Location | Construction Start(1) | Commercial Operations(2) | Contract Type | Rated(3) | Pattern Development- Owned(4) | ||||||||

Armow | Operational | Ontario | 2014 | 2015 | PPA | 180 | 90 | ||||||||

Meikle | In construction | British Columbia | 2015 | 2016 | PPA | 180 | 180 | ||||||||

Conejo Solar | In construction | Chile | 2015 | 2016 | PPA | 104 | 84 | ||||||||

Belle River | Securing final permits | Ontario | 2016 | 2017 | PPA | 100 | 50 | ||||||||

Henvey Inlet | Late stage development | Ontario | 2016 | 2017 | PPA | 300 | 150 | ||||||||

Mont Sainte-Marguerite | Late stage development | Québec | 2016 | 2017 | PPA | 147 | 147 | ||||||||

North Kent | Late stage development | Ontario | 2016 | 2017 | PPA | 100 | 43 | ||||||||

Broadview projects | Late stage development | New Mexico | 2016 | 2017 | PPA | 324 | 259 | ||||||||

Grady | Late stage development | New Mexico | 2016 | 2017 | PPA | 220 | 176 | ||||||||

Tsugaru | Late stage development | Japan | 2015 | 2018 | PPA | 126 | 63 | ||||||||

Ohorayama | Late stage development | Japan | 2015 | 2017 | PPA | 33 | 31 | ||||||||

Kanagi Solar | In construction | Japan | 2014 | 2016 | PPA | 14 | 6 | ||||||||

Futtsu Solar | Operational | Japan | 2014 | 2016 | PPA | 42 | 19 | ||||||||

1,870 | 1,298 | ||||||||||||||

(1) | Represents date of actual or anticipated commencement of construction. |

(2) | Represents date of actual or anticipated commencement of commercial operations. |

(3) | Rated capacity represents the maximum electricity generating capacity of a project in MW. As a result of wind and other conditions, a project or a turbine will not operate at its rated capacity at all times and the amount of electricity generated may be less than its rated capacity. |

(4) | Pattern Development-owned capacity represents the maximum, or rated, electricity generating capacity of the project in MW, multiplied by Pattern Development’s percentage ownership interest in the distributable cash flow of the project. |

Our management team will rigorously review and analyze new market opportunities and selectively consider opportunities offered by Pattern Development as well as those offered by other third parties, either independently or jointly with Pattern Development. From time to time, we may submit bids in connection with third party acquisition opportunities, including opportunities to purchase the interests of projects held by our joint venture partners. These bids can be binding bids or non-binding bids, can be for single assets or a group of assets, and (if accepted) can be material acquisitions for us. There can be no assurance any such bids will be accepted.

Completing Our Construction Projects on Schedule and Within Budget

We promote our business by completing our construction projects on schedule and within budget, transitioning projects under construction to commercial operation on a timely basis and efficiently operating our projects to maximize project revenues and minimize operating costs. We utilize experienced, creditworthy contractors and proven technology to build high-quality power projects. In 2015, we completed construction at two construction projects which increased our owned capacity by 280 MW, for an aggregate of 2,282 MW together with our other operating projects.

Maintaining a Prudent Capital Structure and Financial Flexibility

We intend to maintain a conservative approach to our capital structure to protect our ability to pay regular dividends and fund investments to provide for future growth. Power projects by their nature require significant upfront capital investment and as a result we believe it prudent to match these long-lived assets with long-term debt and/or equity. The average maturity of our project-level term debt is approximately 12 years, although our scheduled loan amortization is typically 18 years or more, and we have an expected average annual debt service coverage ratio over the remaining scheduled loan amortization periods of more than 1.7 to 1.0. This prudent capital structure coupled with our predictable price for our electricity and our standard operations and maintenance programs help to achieve a stable cash flow profile.

Consistent with our existing indebtedness, we expect to typically utilize fixed-rate indebtedness (or swapping any variable rate indebtedness) with strong debt service coverage ratios to finance projects. We believe this approach, together with a strategic

11

consideration of project-level financial restructuring and recapitalization opportunities, will contribute to our ability to maintain and, over time, increase our cash available for distribution.

Working Closely With Our Stakeholders

We believe that close working relationships with our various stakeholders, including suppliers, power sales agreement counterparties, regulators, the local communities where we are located and environmental organizations and with Pattern Development and other developers enable us to best support our existing projects and will help us access attractive, construction-ready projects.

Employee Transfer of Pattern Development Employees

In 2015, we amended our Management Services Agreement with Pattern Development to change the terms upon which the employees of Pattern Development will become our employees. We refer to this event as the employee transfer. The employee transfer is no longer conditioned upon our achievement of $2.5 billion in market capitalization. Instead, we have the option, exercisable at any time until January 1, 2017, to require the employee transfer to occur. We will not be required to make any payments to Pattern Development upon the occurrence of the employee transfer, other than the payment of any statutory severance payments that may as a result be due and payable to employees in certain jurisdictions outside the United States. The employee transfer will result in our complete internalization of the administrative, technical and other services that were initially provided to us by Pattern Development under the Management Services Agreement. The occurrence of the employee transfer will neither alter our Purchase Rights nor the terms of the Management Services Agreement.

Upon the employee transfer, we expect that our principal focus will continue to be owning operational and under-construction power projects. However, the employee transfer is expected to enhance our long-term ability to independently develop projects and grow our business. Following the employee transfer, we will continue to provide management and other services to Pattern Development (including services from the reintegrated departments of Pattern Development) to the extent required by Pattern Development’s remaining development activities, and Pattern Development will continue to pay us for those services primarily on a cost reimbursement basis.

Competitive Strengths

We believe our key competitive strengths include:

Our High-Quality Projects

We believe our high-quality projects are better positioned to generate stable long-term cash flows compared to typical projects in the industry and will generate available cash in excess of our initial dividend level, providing us the financial resources for investing in new opportunities. Having high-quality projects also provides us access to low-cost project-level debt and strong stakeholder relationships. The key attributes and strengths of our projects are:

Long-Term, Fixed-Price Power Sale Agreements. We believe our long-term, fixed-price power sale agreements with 14 distinct creditworthy counterparties will deliver stable long-term revenues, although we note that the credit rating of the Puerto Rico Electric Power Authority, or "PREPA," counterparty to our Santa Isabel project’s PPA, was downgraded a number of times in each of 2014 and 2015. Our power sale agreements cover 89% of the electricity to be generated across our projects with a weighted average remaining contract life of approximately 14 years.

Geographically Diverse Markets and Wind Regimes. Our geographically diverse projects are located across regions generally characterized by high demand for renewable energy, documented reliable wind resources, deregulated energy markets and favorable renewable energy policies. The geographic diversity of our projects—from California to Puerto Rico, and Manitoba to Chile—helps insulate us against regional wind fluctuations as well as the possibility of adverse regulatory conditions in any one jurisdiction.

State-of-the-Art Wind Turbine Technologies. Our projects utilize state-of-the-art, proven, reliable wind turbine technologies. Our projects utilize Siemens 2.3 MW, Mitsubishi MWT95/2.4, General Electric 1.5-82.5 and 1.85-87 wind turbines, some of the most reliable and proven turbine technologies available in the market. The wind turbines were in each case specifically selected for the site conditions to ensure optimal performance and longevity of the machines. Our turbines have an average age of approximately three years.

12

Our Strong Reputation in the Industry

We believe the success of our team has created a highly respected organization which attracts talented people and new opportunities. Our integrity, expertise, and solutions-oriented approach is attractive to stakeholders and parties providing services to our existing projects as well as those who are looking for buyers of their assets.

In 2015, the Conejo Solar project, which is on our list of identified ROFO projects, won the Chilean International Renewable Energy Congress's ("CIREC") "Latin American Renewables Deal of the Year". In 2013, our Ocotillo project received an award for its outstanding environmental analysis and documentation from the California Association of Environmental Professionals and also received the Renewable Project Finance Deal of the Year award from Power Finance & Risk published by Power Intelligence. Our Spring Valley project received the Wind Project of the Year Award in 2012 from POWER-GEN International (the publisher of Power Engineering and Renewable Energy World), which we believe is considered among the most prestigious awards in the renewable energy industry. Our El Arrayán project also won two Chilean International Renewable Energy Awards, presented at CIREC's 2012 annual conference in Santiago. The awards were the Best Renewable Energy Project in 2012 (Mejor proyecto de Energía Renovable de 2012) and the Best Renewable Energy Joint Venture (Mejor colaboración entre dos empresas).

Our Approach to Project Selection

Our approach to project selection aims to deliver superior financial results and minimize long-term operating risks by focusing on the acquisition of projects that are operational or construction-ready and have long-term power sales agreements with creditworthy counterparties. Once we identify an attractive opportunity, we apply rigorous analysis in a timely, disciplined and functionally integrated manner to evaluate the wind regime, technology options, site design improvement, regional market trends and regulatory, financial and legal constraints. The most attractive projects offer the proper combination of land accessibility, power transmission capacity, attractive power sales markets and favorable and dependable winds. We believe the members of our management team are recognized by their industry peers as skilled in identifying, analyzing and executing successful power project acquisitions.

Our approach to project selection has also enabled us to successfully execute new projects in a complex renewable energy market characterized by economic, political and regulatory changes that affect energy investment opportunities. Examples include the cyclical nature of U.S. federal incentives and the challenge of realizing the full value of these incentives, volatility in the equity markets, increasing environmental and permitting concerns, reduced PPA opportunities that are influenced by changing power markets, a cyclical wind turbine supply environment that alternates between tight and loose supply constraints, changes in wind turbine technology, changes in availability of debt markets, and changes in electricity market structure. Our management team has had success in identifying and executing attractive acquisitions through all of these changing circumstances. For example, through our innovative approach to our business, we developed a financial structure to realize value for PTCs, implemented ground-breaking radar technology to protect bird and bat populations, became one of the first IPPs to capture value from a number of newly deregulated markets and found long-term debt solutions even when the debt markets were highly constrained.

As a fundamental principle, we seek to acquire projects that will contribute measurable improvements in our adjusted EBITDA and our cash available for distribution and that will have a risk profile consistent with our current business objectives. In addition, we view projects as long-term partnerships with all stakeholders, and the benefits that we pledge to the community are fundamental to creating a positive environment for a project’s long-term success.

Our Relationship with Pattern Development

Our continuing relationship with Pattern Development, for which Pattern Energy's ownership interest is 23%, provides us with access to a pipeline of acquisition opportunities. We believe Pattern Development’s ownership position in our company incentivizes Pattern Development to support the successful execution of our objectives and business strategy, including through the preparation of projects to the stage where they are at least construction-ready. We believe Pattern Development’s focus on project development combined with our Project Purchase Right will complement our acquisition strategy, which focuses on the identification and acquisition of operational and construction-ready power projects.

Organization of Our Business

Our business is organized around our current projects. In the future, we expect that our business will include additional operating and construction-ready projects acquired from Pattern Development and other third parties. In addition to our executive officers, we employ 116 full-time staff in key functional areas associated with construction and engineering, operations and maintenance, and commercial management. We rely on some services to be performed by third parties, including Pattern Development, but have all the core functions required for the overseeing of constructing, operating and managing our projects.

13

Operations and Maintenance

Our operations team’s objective is to maximize revenues from each of our projects. In order for us to maximize our revenues, we seek to operate and maintain our equipment so that we can ensure our equipment is productive during times of optimal wind resources and power prices. Our approach to achieving efficient operations involves the following key strategic objectives:

• | Safety. We believe that the safety of our workers, our contractors, our visitors and the community is paramount and takes precedence over all other aspects of operations. We demonstrate this through promoting a strong safety culture, implementing a formal safety management program, employing a full time in-house safety organization and conducting annual site safety audits. |

• | Equipment reliability and fleet management. We have selected high-quality equipment with a goal of having a concentration of equipment from top manufacturers. We employ the Siemens 2.3 MW turbine at 12 of our 16 project sites, the Mitsubishi MWT95/2.4 at one site, the General Electric 1.5-82.5 at two sites and the General Electric 1.85-87 at the remaining site. With a combination of high-quality equipment and scale, we have structured our fleet such that we may: |

• | expect high availability and long-term production from the equipment; |

• | continue developing operating expertise and experience, which can be shared among our operators; |

• | obtain a high level of attention and focus from the manufacturer; and |

• | maintain a shared spare parts inventory and common operating practices. |

• | Long-term service and maintenance. Good operating performance begins with a long-term maintenance approach to the equipment. While approximately 75% of our operating turbine units remain under original or extended warranty, on-going maintenance and replacement of parts is essential to equipment longevity. All of our wind turbines are managed either under service or warranty agreements that ensure regular repair and replacement of parts. |

• | Inspection. As our warranty contracts and service arrangements expire, we conduct extensive third-party end of warranty inspections to identify any potential equipment or service issues which can be remedied by the manufacturer pursuant to their contractual obligations under the warranty and ensure the projects start their post-warranty periods with reliably functioning equipment. |

• | Staff training. We employ highly experienced personnel from a variety of power generation sectors. In addition, we bring into the organization a broad base of best industry practices. After hiring, we provide our operators with on-going training, in-house and from manufacturers and from third parties, to keep them current on latest industry practices and experiences. |

• | Focus on our value-added capabilities. In order to maximize efficiencies, we concentrate our resources on our core operating areas. In particular, we believe it is critical to have on-site management personnel that are our employees and provide oversight of all site activities to ensure our safety and financial objectives have priority. We contract with third parties, often the turbine manufacturer, for on-going major maintenance of the turbines and similar specialized services such as repairs on our substations or transmission lines. |

• | Maximize structural efficiencies. Our operating resources are allocated across three key areas, site operations, our 24/7 OCC and other central support services. |

• | Site-operators. All of our projects have our employees as on-site operators, which allows for direct management of the projects and all contractors working on site. In addition, these individuals also strive for a high level of involvement in the communities we serve, including with respect to our power purchasers, the regulatory agencies and local communities. Each of our projects has the latest, state-of-the-art supervisory control and data acquisition systems that help us efficiently assess operating faults and plan preventative maintenance. |

• | 24/7 Operations Control Center. Our OCC, located in Houston, Texas, focuses on monitoring and controlling each of our wind turbines to prevent downtime, monitoring regional and local climate, tracking real time market prices and, for some of our projects, monitoring certain environmental activities. In addition, the OCC supports various other central activities such as safety, power marketing, and regulatory compliance, and it maintains constant communications with each of our site operators, which frees our site operators to concentrate on day-to-day equipment and safety activities. |

• | Central Support Services. In addition to our OCC, our Houston office also hosts the balance of our operations organization which provides critical support to the operating projects. This team includes our operations |

14

management team and specialists in safety, environmental management, regulatory compliance, contract management, turbine specialists and asset administration.

• | Equipment improvements. We believe that our foundation of reliable and proven equipment allows us to make further operating improvements over time. For example, in 2015, we implemented certain control upgrades and blade modifications at our Post Rock and Lost Creek sites. We are also in continuing discussions with the turbine manufacturers and other innovative suppliers regarding new technologies to identify additional promising solutions which will improve our projects’ performance and increase our electricity generation. |

Commercial Management

Our commercial management group is tasked with protecting the long-term value of our projects’ commercial arrangements. We have adopted a commercial strategy of managing our projects and other assets with an in-house commercial management group acting as "owners’ representatives." The role of the commercial management group is to oversee contract management, environmental management, community relations, power marketing and finance and to closely monitor the performance of each project from an owner’s point of view in order to maximize financial performance and minimize risk. Although the commercial management group manages the day-to-day aspects of commercial management, functional and managerial expertise is often brought in to support key areas such as legal, finance and power marketing.

• | Contract Management. With a group of seasoned managers, our commercial management group optimizes the commercial performance of our assets, services the project debt, manages project agreements and compliance with relevant laws, regulations and rules and has ultimate responsibility for the financial performance of each project. The team also manages our real estate obligations as well as our corporate insurance program, local government obligations, home office, remote facilities and mobile assets. Our commercial management group also facilitates a seamless transfer of responsibilities from the development team through construction to commercial operations in order to ensure all contractual and regulatory obligations are clearly captured and tracked in a formal compliance program. |

• | Environmental Management and Community Relations. Adaptive environmental management is increasingly the standard by which power projects are managed. Our company has been a leader in adopting strategies to minimize environmental impacts, such as bird and bat fatalities. Each project has different circumstances so our environmental and community programs range from hiring of local personnel and historical preservation to use of advanced radar systems to monitor birds and bats and presence of on-site biologists to assist in species recognition and mitigation management. By proactively addressing the concerns of the regions, our environmental management and community relations programs seek to minimize additional costs and burdens from a potential increase in regulations or law suits. |

• | Power Marketing. A crucial element of a successful project is assuring revenue from the sale of power and other environmental attributes. We manage the risk associated with fluctuations in electricity prices across our business by seeking to commit the electricity we generate under long-term, fixed-price power sale agreements. Our uncontracted power and renewable attributes are sold in the spot-market or under shorter term contracts to optimize revenue realization. We believe this management philosophy will result in a steady, predictable source of revenue for each of our projects. |

• | Finance. Our projects are typically funded with construction financing during the construction phase which converts to long-term financing when the project commences commercial operations. Debt at each individual project is project financed, which means that, with very limited exceptions, the lenders have no or only limited recourse to other assets of the company other than the assets that are being financed. Debt for our projects is typically provided by commercial banks and institutional lenders that have the expertise to evaluate the risks associated with the construction and operation of a wind power project, including evaluation of the equipment technology, construction, operations and wind resources. These lenders provide construction financing for many sizable industrial and infrastructure projects. Since debt comprises a significant portion of total project capitalization, achievement of construction financing is a general indication that lenders and their independent consultants have carefully evaluated the project and find it viable for long-term financing. Given the complexity involved in financing large infrastructure assets, projects are often completed with a syndicate of lenders, and the credibility we have established among the financial community allows lenders to have confidence in the quality of our projects and enables us to secure competitive financing terms and other financing efficiencies for our projects. Over the years, our team has developed close relationships with many of the active renewable energy lenders. |

Engineering and Construction

The key leadership in our engineering and construction group resides within our company, which provides us with the in-house capabilities required to evaluate and manage a project’s design and construction processes. We will rely as necessary upon

15

additional personnel from third-party sources and Pattern Development with respect to the construction of our projects. We also typically enter into fixed-price construction contracts for our projects’ with a guaranteed completion date to encourage completion on time and within budget.

Project design involves close and frequent communication with both field development personnel as well as the construction contractor in order to develop a project that conforms to local geotechnical and topographic characteristics while accommodating permitting and real estate restrictions. Pattern Development also strives to integrate experience obtained from operating projects in order to design projects with optimal maintenance and equipment-availability profiles. During construction, we are responsible for overseeing the construction contractor and turbine-vendor activities to ensure that the construction schedule is met. Collaboration among engineers and managers on each of our projects and our major equipment suppliers allows us to efficiently transition from construction to commercial operations and to identify and process technical improvements over the life-cycle of each project.

Our engineering and construction team is comprised of highly experienced project and construction managers and includes personnel who have supervised the design and on budget completion of construction of 35 wind power projects over the last 13 years. We set, and ensure compliance with, design specifications and take an active role in supervising field work, safety compliance, quality control and adherence to project schedules. Each project has a dedicated resident construction manager, and other engineering and construction functions are centralized, which allows the group to efficiently scale its resources to support our developing global platform and growth strategy.

Investing

We are organized in a manner that will allow us to independently and comprehensively evaluate investments in new projects. Key members of our management team, including Messrs. Garland, Armistead, Elkort, Lyon, and Pedersen, have spent extensive periods of their careers in the investment advisory, principal investment and finance fields.

As a major part of our growth strategy, we intend to seek to acquire projects that would contribute measurable amounts to our cash available for distribution and adjusted EBITDA. Our approach to project selection is focused on projects (i) with strong economics that will support our long-term financial goals, as determined by intensive analysis and in-depth due diligence, (ii) in which we can add value and which have characteristics that are strategically compatible with our other projects and overall business, and (iii) which meet our core values, including our commitments to environmental stewardship and being a good neighbor in the communities in which our projects are located. To achieve proper investment management, we have implemented processes to ensure rigorous analysis and proper internal approval controls, including preparing formal investment approval documentation, maintaining strict limits on delegation of authority for making capital commitments, and vetting our assumptions with independent technical experts and advisors.

Competition

We compete with other wind power, infrastructure funds and renewable energy companies, as well as conventional power companies, to acquire profitable construction-ready and operating projects. In addition, competitive conditions may be substantially affected by various forms of energy legislation and regulation considered from time to time by federal, state, provincial and local legislatures and administrative agencies.

16

Suppliers

There are a limited number of turbine suppliers and, although demand for turbines in the past has generally been high relative to manufacturing capacity, we believe that current turbine manufacturing capacity is adequate. Our turbine supply strategy is largely based on maintaining strong relationships with leading turbine suppliers to secure our supply needs.

Project | Supplier | Number of Turbines | Turbine Type | ||

Operating Projects | |||||

Gulf Wind | Mitsubishi | 118 | MWT 95/2.4 | ||

Hatchet Ridge | Siemens | 44 | SWT-2.3-93 | ||

St. Joseph | Siemens | 60 | SWT-2.3-101 | ||

Spring Valley | Siemens | 66 | SWT-2.3-101 | ||

Santa Isabel | Siemens | 44 | SWT-2.3-108 | ||

Ocotillo | Siemens | 112 | SWT-2.3-108 | ||

South Kent | Siemens | 124 | SWT-2.3-101 | ||

El Arrayán | Siemens | 50 | SWT-2.3-101 | ||

Panhandle 1 | General Electric | 118 | 1.85 - 87 | ||

Panhandle 2 | Siemens | 79 | SWT-2.3-108 | ||

Grand | Siemens | 67 | SWT-2.3-101 | ||

Post Rock | General Electric | 134 | 1.5-82.5 | ||

Lost Creek | General Electric | 100 | 1.5-82.5 | ||

K2 | Siemens | 140 | SWT-2.3-101 | ||

Logan’s Gap | Siemens | 87 | SWT-2.3-108 | ||

Amazon Wind Farm Fowler Ridge | Siemens | 65 | SWT-2.3-108 | ||

To date, our projects listed above have purchased 938 turbines from Siemens. Siemens data indicates that worldwide fleet availability for the 2.3MW turbine class exceeds 97%, and our Siemens fleet availability also exceeded 97% in 2015. Apart from Siemens we have relationships with other reputable turbine manufacturers such as General Electric and Mitsubishi. Some of our future projects may utilize turbines from these and other manufacturers.

Our Ocotillo and Santa Isabel (Siemens) and Gulf Wind (MHI) projects have experienced certain blade failures in the last three years. We believe the Siemens blade failures have been fully addressed through the completion of an agreed inspection and repair program. With respect to MHI, we worked with MHI to complete a root cause analysis, testing of the blades at the Gulf Wind facility, and development of a protocol for determining whether a blade might pose a threat to long-term reliable operation. We reached in November 2015 a long term arrangement with MHI to address potential deficiencies and, if applicable, mitigation for lost revenue resulting from blade downtime at the facility. We believe that this agreement and mitigation strategy provide adequate technical and commercial protections to the project to mitigate the impacts of this issue, but can give no assurance that additional issues will not arise for which these measures prove inadequate.

Other important suppliers include engineering and construction companies, such as M. A. Mortenson Company, RES-Americas and Blattner Energy, Inc., with whom we contract to perform civil engineering, electrical work and other infrastructure construction for our projects.

We currently depend on service providers to provide maintenance services to our project equipment. These services are currently provided by the turbine manufacturers, such as Siemens or General Electric, at most of our project sites. We believe there are currently adequate independent service provider alternatives to the turbine manufacturers to meet our needs, and in some cases we do utilize such alternative providers.

Customers

We sell our electricity and RECs, primarily to local utilities under long-term, fixed-price PPAs or, in limited instances, local liquid ISO markets. For the year ended December 31, 2015, the significant customer representing greater than 10% of total revenue was San Diego Gas & Electric ("SDG&E"), which accounted for 17% of our total revenue.

Hedging Activity

17

From time to time, we enter into hedges to manage our business exposure to commodity, foreign exchange rate and interest rate risks. In doing so, our hedging strategy is generally focused on reducing potential changes to key business drivers such as power prices, interest rates and changes in income from overseas investments.

Most of our revenue is subject to long-term PPAs. To the extent that PPAs are not available in a given market, but market prices allow for acceptable project economics, we will enter into hedging agreements to obtain a fixed price for the energy output of our projects, typically by hedging volumes that are expected to be exceeded 99.0% of the time. Those hedging agreements are executed for a monthly or hourly production profile that matches the forecasted production profile of the project. On an overnight basis, we will also consider hedging agreements beyond the initial volume up to an amount that is expected to be exceeded over half the time.

Most of our interest rate exposure is hedged either through fixed-rate debt arrangements or hedging of floating rate loans. We enter into interest rate hedging agreements to convert floating-rate debt to fixed-rate debt for some of our projects, usually at the time we close construction or term financing of a project. We also monitor our corporate-level interest rate exposure and may, from time to time, enter into interest rate hedges in order to mitigate our exposure.

In 2015, we initiated a program of exchange rate management due to the substantial portion of our electricity sales that are Canadian dollar denominated. For additional information regarding our hedging activities, see Item 7A "Quantitative and Qualitative Disclosure about Market Risk."

18

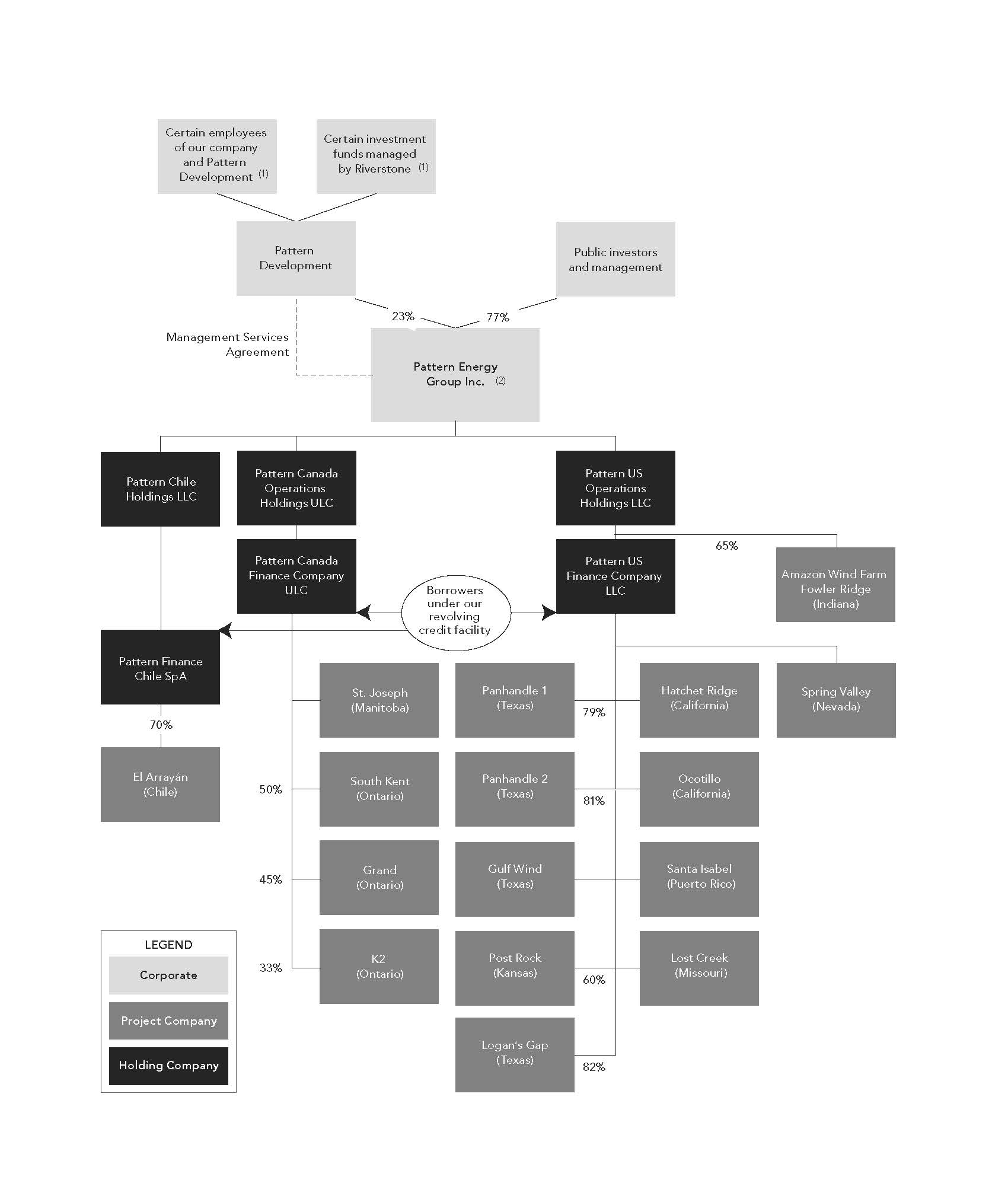

Structure of Our Company

(1) | These funds and these employees hold indirect interests in Pattern Development. |

(2) | Subsequent to our issuance of shares and the sale of certain of our shares held by Pattern Development during 2015, Pattern Development’s ownership interest in us was reduced to approximately 23%, while public and management ownership increased to approximately 77%. |

19

Employees

As of December 31, 2015, we had 116 full-time employees of whom 32 are based in our corporate headquarters, 46 are based at our project sites and 38 are based at our other offices, including our OCC, in Houston, Texas. None of our employees are represented by a labor union or covered by any collective bargaining agreement.

Insurance

We maintain insurance on terms generally carried by companies engaged in similar business and owning similar properties in the United States, Canada and Chile and whose projects are financed in a manner similar to our projects. As is common in the wind industry, however, we do not insure fully against all the risks associated with our business either because insurance is not available or because the premiums for some coverage are prohibitive. For example, we do not maintain war risk insurance. We maintain varying levels of insurance for the development, construction, and operation phases of our projects, including property insurance, which, depending on the location of each project, may include catastrophic windstorm, flood, and earthquake coverage (CAT coverage); transportation insurance; advance loss of profits insurance; business interruption insurance; general liability and umbrella liability insurance; time element pollution liability insurance; auto liability insurance; workers’ compensation and employer’s liability insurance; and (except in Chile) title insurance. The "all risk" property insurance coverage is currently maintained in amounts based on the full replacement value of our projects (subject to certain sub-limits for windstorm, flood, and earthquake risks) and the business interruption insurance generally provides 15 months of coverage in amounts that vary from project to project based on the revenue generation potential of each project. All types of coverage are subject to applicable deductibles. We generally do not maintain insurance for certain environmental risks, such as environmental contamination.

Industry

Wind power has been one of the fastest growing sources of electricity generation in North America and globally over the past decade. According to the Global Wind Energy Council, or "GWEC," from 2001 through 2013, total net electricity generation from wind power in the United States and Canada grew at a combined annual growth rate of 27% and 37%, respectively. The growth in the industry is largely attributable to renewable energy’s increasing cost competitiveness with other power generation technologies, the advantages of wind power over other renewable energy sources, and growing public support for renewable energy driven by energy security and environmental concerns. As global demand for electricity generation from wind power has increased, technology enhancements-supported by U.S. government incentives-have reduced the cost of wind power by more than 80% over the last twenty years, according to the American Wind Energy Association, or "AWEA."

The United States is the largest producer of wind power in the world. According to AWEA, wind power was the largest source of new electricity generating capacity in the U.S. in 2015, accounting for more than 35% of new generation. Wind power was the first or second largest source of new generating capacity in the United States for seven of the eight years between 2005 and 2012, according to the U.S Department of Energy and AWEA. According to AWEA, wind power became the leading source of new electricity generating capacity in the United States for the first time in 2012. The American wind energy industry installed 8,598 MW in 2015 and 4,854 MW in 2014 and the U.S. now has an installed wind capacity of 74,472 MW with over 9,400 MW of wind currently under construction across 22 states. The success of wind power in the United States is evidenced by over $120.0 billion in investments to date, according to AWEA.

Renewable energy sources in the United States have benefited from various federal and state governmental incentives, such as production tax credits and investment tax credits. Production tax credits and investment tax credits for wind energy on the federal level were extended in December of 2015, under the Consolidated Appropriations Act. The Act extended the expiration date for tax credits for wind facilities commencing construction, with a five year phase-down beginning for wind projects commencing construction after December 31, 2016. The Act also applies retroactively to January 1, 2015. In addition to an extension of the production tax credits, in August 2015, President Obama and the Environmental Protection Agency announced the Clean Power Plan, or "CPP," a key step in reducing carbon pollution from power plants which is designed to strengthen the fast-growing trend toward cleaner and lower-emitting power plants. The CPP is expected to reduce carbon dioxide emissions from power plants to 32% below 2005 levels by 2030. For each state, the CPP rules will establish a target emissions rate, or the amount of carbon dioxide that could be emitted per megawatt-hour of power produced and states are expected to start working toward interim emissions goals beginning in 2022. Depending on how the rule is implemented, it could drive demand for up to 100 GW of new wind energy by 2030 according to AWEA. However, in February 2016, the U.S. Supreme Court issued a stay prohibiting the implementation of the CPP pending a challenge to the CPP before a U.S. Court of Appeals.

The Canadian wind power industry has also experienced dramatic growth in recent years. Canada gained 1,505 MW in 2015, and 1,416 MW in 2014 of new installed wind power generating capacity. This investment resulted in wind power generating capacity in Canada reaching approximately 11,205 MW as of December 2015. According to the Canadian Wind Energy Association, or

20

"CanWEA," new installed wind power generating capacity is expected to average 1,500 MW annually over the next three years. Ontario, one of our markets, is the national leader in installed capacity, with approximately 4.4 GW of wind power generating capacity at the close of 2015, although recent changes to the Ontario government feed-in tariff, or "FIT," regime may make future projects less attractive and power purchase agreements more difficult to obtain. CanWEA forecasts total wind power generating capacity in Canada to exceed 12 GW at the end of 2016.

Chile, also one of our markets, has an abundant wind resource, which GWEC estimates could provide the potential for more than 40 GW of generating capacity. 2014 was a strong year for Chilean wind development, with the country’s new installed capacity reaching 506 MW, which is nearly four times the previous record of 130 MW set in 2013, according to the state-run Renewable Energy Centre. That brought the country’s total wind power capacity to 836 MW. Wind now supplies approximately 2% of the country’s electricity demand.

In June 2015, we added three Japanese wind projects and two Japanese solar projects to our list of Identified ROFO Projects. Following the nuclear meltdown at the Fukushima Daiichi plant in 2011, the Japanese government has placed a greater emphasis on the development of renewable resources in order to reduce its reliance on nuclear power, having released its Innovative Strategy for Energy and the Environment in September 2012. By 2030, the plan calls for renewable power generation to triple compared to 2010, reaching about 30% of total generation. In 2012, Japan also introduced a FIT program that offers fixed-term, fixed-price contracts (up to 20 years) to renewable power projects. The tariff will be re-assessed every year based on the latest market experience in Japan. At the end of 2014, 2,789 MW of wind capacity was operating in Japan. This accounted for approximately 1% of the total power supply in 2014.

Although the Company does not yet have assets or Identified ROFO Projects in Mexico, it is a key potential market for us as Pattern Development is actively working in the country and we expect to add Mexican projects to the Identified ROFO Projects list in the future. Mexico’s Congress has enacted sweeping reforms to its electric generation industry in recent years, opening new opportunities for private investment in generation and creating a mandate to obtain at least 35% of its generation from clean sources by 2024. High prices and strong load growth were key factors in encouraging the reforms, and Mexico’s SENER (Secretaria de Energia) has published rules for interconnection and a new market-oriented regime. Mexico has substantial wind and solar resources, and thus far has only developed less than two thousand megawatts of wind generation under the pre-reform system. It is anticipated by the Mexican Wind Energy Association (Asociación Mexicana de Energía Eólica) that several thousand megawatts of wind generation will be developed over the next few years. During 2014, Mexico added 634 MW of new wind power to the country’s electricity grid bringing the total capacity to 2,551 MW.

Given supply diversity requirements, falling equipment costs, the inherent stability of the cost of wind power as an energy resource and an active market for the purchase and sale of power projects, we believe that our markets present a substantial opportunity for growth. We require a relatively small share of a very large market to meet our growth objectives and we believe we will achieve growth through the acquisition of operational and construction-ready projects from Pattern Development and other third parties.

While we currently operate primarily in wind power markets, we expect to continue to evaluate other types of independent power projects for possible acquisition, including renewable energy projects other than wind power projects and non-renewable energy projects. In September 2014, we announced the addition of our first solar project, the 104 MW Conejo Solar photovoltaic power project in Chile, to our list of Identified ROFO, and in June 2015, we added two Japanese solar projects to that list.

Regulatory Matters

Environmental Regulation

We are subject to various environmental, health and safety laws and regulations in each of the jurisdictions in which we operate. These laws and regulations require us to obtain and maintain permits and approvals, undergo environmental review processes and implement environmental, health and safety programs and procedures to monitor and control risks associated with the siting, construction, operation and decommissioning of wind power projects, all of which involve a significant investment of time and can be expensive.

We incur costs in the ordinary course of business to comply with these laws, regulations and permit requirements. We do not anticipate material unplanned capital expenditures for environmental controls for our operating projects in the next several years. However, these laws and regulations frequently change and often become more stringent, or subject to more stringent interpretation or enforcement. Future changes could require us to incur materially higher costs.

Failure to comply with these laws, regulations and permit requirements may result in administrative, civil and criminal penalties, imposition of investigatory, cleanup and site restoration costs and liens, denial or revocation of permits or other authorizations and

21

issuance of injunctions to limit or cease operations. In addition, claims for damages to persons or property or for injunctive relief have been brought and may in the future result from environmental and other impacts of our activities.

Environmental Permitting—United States

We are required to obtain from U.S. federal, state and local governmental authorities a range of environmental permits and other approvals to build and operate our projects, including, but not limited to, those described below. In addition to being subject to these regulatory requirements, we could experience and have experienced significant opposition from third parties when we initially apply for permits or when there is an appeal proceeding after permits are issued. The delay or denial of a permit or the imposition of conditions that are costly or difficult to comply with can impair or even prevent the development of a project or can increase the cost so substantially that the project is no longer attractive to us.

Federal Clean Water Act

Frequently, our U.S. projects are located near wetlands, and we are required to obtain permits under the U.S. Clean Water Act from the U.S. Army Corps of Engineers, or the "Army Corps," for the discharge of dredged or fill material into waters of the United States, including wetlands and streams. The Army Corps may also require us to mitigate any loss of wetland functions and values that accompanies our activities. In addition, we are required to obtain permits under the Clean Water Act for water discharges, such as storm water runoff associated with construction activities, and to follow a variety of best management practices to ensure that water quality is protected and impacts are minimized. Certain activities, such as installing a power line across a navigable river, may also require permits under the Rivers and Harbors Appropriation Act of 1899.

Federal Bureau of Land Management Permits