Attached files

| file | filename |

|---|---|

| EX-31.01 - EX-31.01 - AUDACY, INC. | d142039dex3101.htm |

| EX-32.02 - EX-32.02 - AUDACY, INC. | d142039dex3202.htm |

| EX-21.01 - EX-21.01 - AUDACY, INC. | d142039dex2101.htm |

| EX-31.02 - EX-31.02 - AUDACY, INC. | d142039dex3102.htm |

| EX-23.01 - EX-23.01 - AUDACY, INC. | d142039dex2301.htm |

| EX-10.04 - EX-10.04 - AUDACY, INC. | d142039dex1004.htm |

| EX-10.06 - EX-10.06 - AUDACY, INC. | d142039dex1006.htm |

| EX-32.01 - EX-32.01 - AUDACY, INC. | d142039dex3201.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-14461

Entercom Communications Corp.

(Exact name of registrant as specified in its charter)

| Pennsylvania | 23-1701044 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

401 E. City Avenue, Suite 809

Bala Cynwyd, Pennsylvania 19004

(Address of principal executive offices and zip code)

(610) 660-5610

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of each class |

Name of exchange on which registered | |

| Class A Common Stock, par value $.01 per share | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of February 15, 2016, the aggregate market value of the Class A common stock held by non-affiliates of the registrant was $309,327,453 based on the June 30, 2015 closing price of $11.42 on the New York Stock Exchange on such date.

Class A common stock, $0.01 par value 32,759,616 shares outstanding as of February 15, 2016

(Class A shares outstanding includes 1,584,801 unvested and vested but deferred restricted stock units).

Class B common stock, $0.01 par value 7,197,532 shares outstanding as February 15, 2016.

Table of Contents

DOCUMENTS INCORPORATED BY REFERENCE

Certain information in the registrant’s Definitive Proxy Statement for its 2016 Annual Meeting of Shareholders, pursuant to Regulation 14A, is incorporated by reference in Part III of this report, which will be filed with the Securities and Exchange Commission no later than April 29, 2016.

| Page | ||||||

| Item 1. |

1 | |||||

| Item 1A. |

4 | |||||

| Item 1B. |

10 | |||||

| Item 2. |

10 | |||||

| Item 3. |

11 | |||||

| Item 4. |

11 | |||||

| Item 5. |

11 | |||||

| Item 6. |

15 | |||||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

18 | ||||

| Item 7A. |

35 | |||||

| Item 8. |

35 | |||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

35 | ||||

| Item 9A. |

35 | |||||

| Item 9B. |

36 | |||||

| Item 10. |

37 | |||||

| Item 11. |

37 | |||||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters |

37 | ||||

| Item 13. |

Certain Relationships and Related Transactions and Director Independence |

37 | ||||

| Item 14. |

37 | |||||

| Item 15. |

38 | |||||

| 95 | ||||||

i

Table of Contents

CERTAIN DEFINITIONS

Unless the context requires otherwise, all references in this report to “Entercom,” “we,” “us,” “our” and similar terms refer to Entercom Communications Corp. and its consolidated subsidiaries, which would include any variable interest entities that are required to be consolidated under accounting guidance.

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains, in addition to historical information, statements by us with regard to our expectations as to financial results and other aspects of our business that involve risks and uncertainties and may constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended.

Forward-looking statements, including certain pro forma information, are presented for illustrative purposes only and reflect our current expectations concerning future results and events. All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws including, without limitation, any projections of earnings, revenues or other financial items; any statements of the plans, strategies and objectives of management for future operations; any statements concerning proposed new services or developments; any statements regarding future economic conditions or performance; any statements of belief; and any statements of assumptions underlying any of the foregoing.

We report our financial information on a calendar year basis. Any reference to activity during the year is for the year ended December 31.

You can identify forward-looking statements by our use of words such as “anticipates,” “believes,” “continues,” “expects,” “intends,” “likely,” “may,” “opportunity,” “plans,” “potential,” “project,” “will,” “could,” “would,” “should,” “seeks,” “estimates,” “predicts” and similar expressions which identify forward-looking statements, whether in the negative or the affirmative. We cannot guarantee that we actually will achieve these plans, intentions or expectations. These forward-looking statements are subject to risks, uncertainties and other factors, some of which are beyond our control, which could cause actual results to differ materially from those forecasted or anticipated in such forward-looking statements. These risks, uncertainties and factors include, but are not limited to, the factors described in Part I, Item 1A, “Risk Factors.”

Any pro forma information that may be included reflects adjustments and is presented for comparative purposes only and does not purport to be indicative of what has occurred or indicative of future operating results or financial position.

You should not place undue reliance on these forward-looking statements, which reflect our view only as of the date of this report. We do not intend, and we do not undertake any obligation, to update these statements or publicly release the result of any revision(s) to these statements to reflect events or circumstances after the date of this report or to reflect the occurrence of unanticipated events.

ii

Table of Contents

| ITEM 1. | BUSINESS |

We are the fourth-largest radio broadcasting company in the United States with a portfolio of 125 radio stations in 27 top markets across the country. We were organized in 1968 as a Pennsylvania corporation.

Our Strategy

Our strategy focuses on providing compelling content in the communities we serve to enable us to offer our advertisers an effective marketing platform to reach a large targeted local audience. The principal components of our strategy are to: (i) focus on creating effective integrated marketing solutions for our customers that incorporate our audio, digital and experiential assets; (ii) build strongly-branded radio stations with highly compelling content; (iii) develop market leading station clusters; and (iv) recruit, develop, motivate and retain superior employees.

Source Of Revenue

The primary source of revenue for our radio stations is the sale of advertising time to local, regional and national advertisers and national network advertisers who purchase spot commercials in varying lengths. A growing source of revenue is from station-related digital platforms, which allow for enhanced audience interaction and participation, and integrated digital advertising solutions. A station’s local sales staff generates the majority of its local and regional advertising sales through direct solicitations of local advertising agencies and businesses. We retain a national representation firm to sell to advertisers outside of our local markets.

Our stations are typically classified by their format, such as news, sports, talk, classic rock, adult contemporary, alternative and country, among others. A station’s format enables it to target specific segments of listeners sharing certain demographics. Advertisers and stations use data published by audience measuring services to estimate how many people within particular geographical markets and demographics listen to specific stations. Our geographically and demographically diverse portfolio of radio stations allows us to deliver targeted messages to specific audiences for advertisers on a local, regional and national basis.

Competition

The radio broadcasting industry is highly competitive. Our stations compete for listeners and advertising revenue with other radio stations within their respective markets. In addition, our stations compete for audiences and advertising revenues with other media including: broadcast television, digital, satellite radio, satellite and cable television, newspapers and magazines, outdoor advertising, direct mail, yellow pages, wireless media alternatives, cellular phones and other forms of audio entertainment and advertisement.

Federal Regulation Of Radio Broadcasting

Overview. The radio broadcasting industry is subject to extensive and changing government regulation of, among other things, ownership limitations, program content, advertising content, technical operations and business and employment practices. The ownership, operation and sale of radio stations are subject to the jurisdiction of the Federal Communications Commission (the “FCC”) pursuant to the Communications Act of 1934, as amended (the “Communications Act”).

The following is a brief summary of certain provisions of the Communications Act and of certain specific FCC regulations and policies. This summary is not a comprehensive listing of all of the regulations and policies affecting radio stations. For further information concerning the nature and extent of federal regulation of radio stations, you should refer to the Communications Act, FCC rules and FCC public notices and rulings.

FCC Licenses. The operation of a radio broadcast station requires a license from the FCC. Certain of our subsidiaries hold the FCC licenses for our stations. The total number of radio stations that can simultaneously operate in any given area or market is limited by the amount of spectrum allotted by the FCC within the AM and FM radio bands, and by station-to-station interference within those bands. While there are no national station ownership caps, FCC rules do limit the number of stations within the same market that a single individual or entity may own or control.

The total number of stations authorized to operate in a local market may fluctuate from time to time, and the number of stations that can be owned by a single individual or entity in a given market can therefore vary over time. Once the FCC approves the ownership of a cluster of stations in a market, that owner may continue to hold those

1

Table of Contents

stations under “grandfathering” policies, despite a decrease in the number of stations in the market. A few of our market clusters, such as our stations in Greenville and Wilkes-Barre/Scranton, are considered to be “grandfathered.” If, at the time of a proposed future transaction, a cluster does not comply with the multiple ownership limitations based upon the number of stations then present in the market, the entire cluster cannot be transferred intact to a single party unless the purchaser qualifies as an “eligible entity” under specified small business standards and meets certain control tests.

Ownership Rules. The FCC sets limits on the number of broadcast stations (including both radio and TV) an entity may permissibly own within a market, as well as limits on the common ownership of broadcast stations and newspapers. Same-market FCC numeric ownership limitations are based: (i) on markets as defined and rated by Nielsen Audio; and (ii) in areas outside of Nielsen Audio markets, on markets ass determined by overlap of specified signal contours.

Ownership Attribution. In applying its ownership limitations, the FCC generally considers only “attributable” ownership interests. Attributable interests generally include: (i) equity and debt interests which when combined exceed 33% of a licensee’s or other media entity’s total asset value, if the interest holder supplies more than 15% of a station’s total weekly programming or has an attributable interest in any same-market media (television, radio, cable or newspaper), with a higher threshold in the case of investments in certain “eligible entities” acquiring broadcast stations; (ii) a 5% or greater direct or indirect voting stock interest, including certain interests held in trust, unless the holder is a qualified passive investor, in which case the threshold is a 20% or greater voting stock interest; (iii) any equity interest in a limited liability company or a partnership, including a limited partnership, unless properly “insulated” from management activities; and (iv) any position as an officer or director of a licensee or of its direct or indirect parent. In our case, where there is a “single majority voting shareholder,” the FCC treats as non-attributable voting stock interests held by non-single majority owners, even if they are in excess of the five percent standard described above.

Alien Ownership Rules. The Communications Act prohibits the issuance to, or holding of broadcast licenses by, foreign governments or aliens, non-U.S. citizens, whether individuals or entities, including any interest in a corporation which holds a broadcast license if more than 20% of the licensee’s capital stock is owned or voted by aliens. In addition, the FCC may prohibit any corporation from holding a broadcast license if the corporation is directly or indirectly controlled by any other corporation of which more than 25% of the capital stock is owned of record or voted by aliens if the FCC finds that the prohibition is in the public interest. The Communications Act gives the FCC discretion to allow greater amounts of alien ownership. The FCC considers investment proposals from international companies or individuals on a case-by-case basis.

License Renewal. Radio station licenses issued by the FCC are renewable ordinarily for an eight-year term. Seven of our FCC radio station license renewal applications filed in the most recent 2011-2014 renewal application window have not yet been granted. For five of those seven stations, license renewal applications filed during the prior 2003-2006 renewal application window have also not yet been granted. A station may continue to operate beyond the expiration date of its license if a timely filed license renewal application is pending.

The FCC is required to renew a broadcast station’s license if the FCC finds that the station has served the public interest, convenience and necessity; there have been no serious violations by the licensee of the Communications Act or the FCC’s rules and regulations; and there have been no other violations by the licensee of the Communications Act or the FCC’s rules and regulations that, taken together, constitute a pattern of abuse. If a challenge is filed against a renewal application, and, as a result of an evidentiary hearing, the FCC determines that the licensee has failed to meet certain fundamental requirements and that no mitigating factors justify the imposition of a lesser sanction, the FCC may deny a license renewal application. Historically, FCC licenses have generally been renewed.

Petitions to deny renewal applications are filed from time to time. Several petitions have been filed against us. Subject to the resolution of open FCC inquiries, we believe that our licenses will be renewed and that continuing challenges to already granted renewals will be resolved favorably to us, although there can be no assurance to that effect. The non-renewal of one or more of our licenses could have a material adverse effect on our business.

Transfer Or Assignment Of Licenses. The Communications Act prohibits the assignment of broadcast licenses or the transfer of control of a broadcast licensee without the prior approval of the FCC. In determining whether to grant such approval, the FCC considers a number of factors pertaining to the existing licensee and the proposed licensee, including:

| • | compliance with the various rules limiting common ownership of media properties in a given market; |

2

Table of Contents

| • | the “character” of the proposed licensee; and |

| • | compliance with the Communications Act’s limitations on alien ownership as well as general compliance with FCC regulations and policies. |

To obtain FCC consent for the assignment or transfer of control of a broadcast license, appropriate applications must be filed with the FCC. Interested parties may file objections or petitions to deny such applications.

Programming And Operation. The Communications Act requires broadcasters to serve the “public interest.” A licensee is required to present programming that is responsive to issues in the station’s community of license and to maintain records demonstrating this responsiveness. The FCC regulates, among other things, political advertising; sponsorship identification; the advertisement of contests and lotteries; the conduct of station-run contests; obscene, indecent and profane broadcasts; certain employment practices; and certain technical operation requirements, including limits on human exposure to radio-frequency radiation. The FCC considers complaints from listeners concerning a station’s public service programming, employment practices, or other operational issues when processing a renewal application filed by a station, but the FCC may consider complaints at any time and may impose fines or take other action for violations of the FCC’s rules separate from its action on a renewal application.

FCC regulations prohibit the broadcast of obscene material at any time as well as the broadcast, between the hours of 6 am and 10 pm, of material it considers “indecent” or “profane”. The FCC has historically enforced licensee compliance in this area through the assessment of monetary forfeitures. Such forfeitures may include: (i) imposition of the maximum authorized fine for egregious cases ($350,000 for a single violation, up to a maximum of $3,300,000 for a continuing violation); and (ii) imposition of fines on a per utterance basis instead of a single fine for an entire program. There are a number of outstanding indecency proceedings in which we are defending our stations’ conduct, and there may be other complaints of this nature which have been submitted to the FCC of which we have not yet been notified.

Certain FCC rules regulate the conduct of on-air station contests, requiring in general that the material rules and terms of the contest be broadcast periodically or posted online and that the contest be conducted substantially as announced. The FCC has a pending investigation into a contest at one of our stations. See Part I, Item 3, “Legal Proceedings,” for further discussion.

Enforcement Authority. The FCC has the power to impose penalties for violations of its rules under the Communications Act, including the imposition of monetary fines, the issuance of short-term licenses, the imposition of a condition on the renewal of a license, the denial of authority to acquire new stations, and the revocation of operating authority. The maximum fine for a single violation of the FCC’s rules (other than indecency rules – see discussion above) is currently $37,500.

Proposed And Recent Changes. Congress, the FCC and other federal agencies are considering or may in the future consider and adopt new laws, regulations and policies regarding a wide variety of matters that could: (1) affect, directly or indirectly, the operation, ownership and profitability of our radio stations; (2) result in the loss of audience share and advertising revenues for our radio stations; and (3) affect our ability to acquire additional radio stations or to finance those acquisitions.

Federal Antitrust Laws. The federal agencies responsible for enforcing the federal antitrust laws, the Federal Trade Commission and the Department of Justice, may investigate certain acquisitions. For an acquisition meeting certain size thresholds, the Hart-Scott-Rodino Antitrust Improvements Act of 1976 requires the parties to file Notification and Report Forms with the Federal Trade Commission and the Department of Justice and to observe specified waiting-period requirements before consummating the acquisition.

HD Radio

AM and FM radio stations may use the FCC selected In-Band On-Channel (“IBOC”) as the exclusive technology for terrestrial digital operations. IBOC, developed by iBiquity Digital Corporation, is also known as “HD Radio.”

HD Radio technology permits a station to transmit radio programming in digital format. We currently use HD Radio digital technology on most of our FM stations. The advantages of digital audio broadcasting over traditional analog broadcasting technology include improved sound quality, the availability of additional channels and the ability to offer a greater variety of auxiliary services.

3

Table of Contents

Employees

As of January 31, 2016, we had 1,608 full-time employees and 921 part-time employees. With respect to certain of our stations in our Kansas City and San Francisco markets, we are a party to collective bargaining agreements with the Screen Actors Guild - American Federation of Television and Radio Artists (known as SAG-AFTRA). Approximately ten employees are represented by these collective bargaining agreements. We believe that our relations with our employees are good.

Corporate Governance

Code Of Business Conduct And Ethics. We have a Code of Business Conduct and Ethics that applies to each of our employees including our principal executive officers and senior members of our finance department. Our Code of Business Conduct and Ethics can be found on the “Investors” sub-page of our website located at www.entercom.com/investors.

Board Committee Charters. Each of our Audit Committee, Compensation Committee and Nominating/Corporate Governance Committee has a committee charter as required by the rules of the New York Stock Exchange. These committee charters can be found on the “Investors” sub-page of our website located at www.entercom.com/investors.

Corporate Governance Guidelines. New York Stock Exchange rules require our Board of Directors to establish certain Corporate Governance Guidelines. These guidelines can be found on the “Investors” sub-page of our website located at www.entercom.com/investors.

Environmental Compliance

As the owner, lessee or operator of various real properties and facilities, we are subject to various federal, state and local environmental laws and regulations. Historically, compliance with these laws and regulations has not had a material adverse effect on our business.

Seasonality

Seasonal revenue fluctuations are common in the radio broadcasting industry and are due primarily to fluctuations in advertising expenditures. Our revenues are typically lowest in the first calendar quarter.

Internet Address And Internet Access To Periodic And Current Reports

You can find more information about us that includes a list of our stations in each of our markets at our Internet website located at www.entercom.com. Our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K and any amendments to those reports are available free of charge through our Internet website as soon as reasonably practicable after we electronically file such material with the Securities and Exchange Commission (the “SEC”). The contents of our websites are not incorporated by reference into this Annual Report on Form 10-K or in any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only. We will also provide a copy of our annual report on Form 10-K upon any written request.

| ITEM 1A. | RISK FACTORS |

Many statements contained in this report are forward-looking in nature. See Note Regarding Forward-Looking Statements at the beginning of this Form 10-K. These statements are based on current plans, intentions or expectations, and actual results could differ materially as we cannot guarantee that we will achieve these plans, intentions or expectations. Among the factors that could cause actual results to differ are the following:

BUSINESS RISKS

Our results may be impacted by economic trends.

Our net revenues increased in 2015 as compared to the prior year primarily as a result of acquisitions made during the year. Excluding the net revenues from these new radio stations and a divested radio station, net revenues improved in the low single digits for the year. The second half of the year reflected improvement over the first half of the year.

4

Table of Contents

Our results of operations could be negatively impacted by delays or reversals in the economic recovery or by future economic downturns. Also, expenditures by advertisers tend to be cyclical, reflecting overall economic conditions. The risks associated with our business could be more acute in periods of a slowing economy or recession, which may be accompanied by a decrease in advertising. A decrease in advertising expenditures can have an adverse effect on our net revenues, profit margins, cash flow, and liquidity.

There can be no assurance that we will not experience an adverse impact on our ability to access capital, which may be material to our business, financial condition and results of operations. In addition, our ability to access the capital markets may be severely restricted at a time when we would like or need to do so, which could have an adverse impact on our capacity to react to changing economic and business conditions.

Our radio stations may be adversely affected by changes in programming and competition for advertising revenues.

We operate in a highly competitive business. Our radio stations compete for audiences with advertising revenue as our principal source of income. We compete directly with other radio stations, as well as with other media, such as broadcast, cable and satellite television, digital audio, newspapers and magazines, national and local digital services, outdoor advertising and direct mail. Audience ratings and market shares are subject to change, and any decrease in our ratings or market share in a particular market could have a material adverse effect on the revenue of our stations located in that market. Audience ratings and market shares could be affected by a variety of factors, including changes in the format or content of programming (some of which may be outside of our control), personnel changes, demographic shifts and general broadcast listening trends. Adverse changes in any of these areas or trends could have a material adverse effect on our business and results of operations. In addition, the market share mix of these competing mediums could also impact the advertising market share of radio advertising.

While we already compete in some of our markets with stations with similarly programmed formats, if another radio station in a market were to convert its programming format to a format similar to one of our stations or if an existing competitor were to garner additional market share, our stations could suffer a reduction in ratings and/or advertising revenue and could incur increased promotional and other expenses. Competing companies may be larger and have more financial resources than we do. We cannot be assured that any of our stations will be able to maintain or increase their current audience ratings and advertising revenues.

We cannot predict the competitive effect on the radio broadcasting industry of changes in audio content distribution, changes in technology or changes in regulations.

The radio broadcasting industry is subject to rapid technological change, evolving industry standards and the emergence of new media technologies and services. We may lack the resources to acquire new technologies or introduce new services to allow us to compete with these new offerings. Competing technologies and services, some of which are commercial free, include: personal audio devices; national and local digital audio services; satellite-delivered digital radio services; content available over the Internet; HD Radio, which provides multi-channel, multi-format digital radio services in the same bandwidth currently occupied by traditional AM and FM radio services; and low-power FM radio, which could result in additional FM radio broadcast outlets, including additional low-power FM radio signals authorized in December 2010 under the Local Community Radio Act.

We cannot predict the effect, if any, that competition arising from new technologies or regulatory changes may have on the radio broadcasting industry or on our financial condition and results of operations.

We are subject to extensive regulations and are dependent on federally issued licenses to operate our radio stations. Failure to comply with such regulations could damage our business.

The radio broadcasting industry is subject to extensive regulation by the FCC under the Communications Act of 1934. See Federal Regulation of Radio Broadcasting under Part I, Item 1, “Business.” We are required to obtain licenses from the FCC to operate our radio stations. Licenses are normally granted for a term of eight years and are renewable. Although the vast majority of FCC radio station licenses are routinely renewed, we cannot be assured that the FCC will approve our future renewal applications or that the renewals will not include conditions or qualifications. During the periods when a renewal application is pending, informal objections and petitions to deny the renewal application can be filed by interested parties, including members of the public, on a variety of grounds. Seven of our FCC radio station license renewal applications filed in the most recent 2011-2014 renewal period have not yet been granted. For five of those seven stations, license renewal applications filed during the prior 2003-2006 renewal application window have also not yet been granted. The non-renewal, or renewal with substantial conditions or modifications, of one or more of our licenses could have a material adverse effect on us.

5

Table of Contents

We must comply with extensive FCC regulations and policies in the ownership and operation of our radio stations. FCC regulations limit the number of radio stations that a licensee can own in a market, which could restrict our ability to consummate future transactions and in certain circumstances could require us to divest some radio stations. The FCC’s rules governing our radio station operations impose costs on our operations, and changes in those rules could have an adverse effect on our business. The FCC also requires radio stations to comply with certain technical requirements to limit interference between two or more radio stations. If the FCC relaxes these technical requirements, it could impair the signals transmitted by our radio stations and could have a material adverse effect on us. Moreover, these FCC regulations may change over time, and we cannot be assured that changes would not have a material adverse effect on us. We are currently the subject of several pending investigations by the FCC, including one involving a death following a contest at one of our stations.

Congress or federal agencies that regulate us could impose new regulations or fees on our operations that could have a material adverse effect on us.

There was proposed legislation in the past and there could be again in the future that requires radio broadcasters to pay additional fees such as a spectrum fee for the use of the spectrum. In addition, there was proposed legislation which would impose a new royalty fee that would be paid to record labels and performing artists for use of their recorded music. It is currently unknown what impact any potential required royalty payments or fees would have on our results of operations, cash flows or financial position.

The FCC has engaged in vigorous enforcement of its indecency rules against the broadcast industry, which could have a material adverse effect on our business.

FCC regulations prohibit the broadcast of obscene material at any time and indecent or profane material between the hours of 6:00 a.m. and 10:00 p.m. Over the last decade, the FCC has increased its enforcement efforts relating to the regulation of indecency and has threatened on more than one occasion to initiate license revocation proceedings against a broadcast licensee who commits a “serious” indecency violation. Congress has dramatically increased the penalties for broadcasting obscene, indecent or profane programming, and these penalties may potentially subject broadcasters to license revocation, renewal or qualification proceedings in the event that they broadcast such material. In addition, the FCC’s heightened focus on the indecency regulatory scheme, against the broadcast industry generally, may encourage third parties to oppose our license renewal applications or applications for consent to acquire broadcast stations. Several of our stations are currently subject to indecency-related inquiries and/or proposed fines at the FCC’s Enforcement Bureau as well as objections to our license renewals based on such inquiries and proposed fines, and we may in the future become subject to additional inquiries or proceedings related to our stations’ broadcast of obscene, indecent or profane material. To the extent that these inquiries or other proceedings result in the imposition of fines, a settlement with the FCC, revocation of any of our station licenses or denials of license renewal applications, our results of operations and business could be materially adversely affected.

The loss of key personnel could have a material adverse effect on our business.

Our business depends upon the continued efforts, abilities and expertise of our executive officers and other key personnel. We believe that the loss of one or more of these individuals could have a material adverse effect on our business.

Our radio stations compete for creative and on-air talent with other radio stations and other media, such as broadcast, cable and satellite television, digital media and satellite radio. Our on-air talent are subject to change, due to competition and for other reasons. Changes in on-air talent could materially and negatively affect our ratings and our ability to attract local and national advertisers, which could in turn adversely affect our revenues.

We depend on selected market clusters of radio stations for a material portion of our revenues.

For 2015, we generated over 50% of our net revenues in seven of our 27 markets, which were Boston, Denver, Kansas City, Portland, Sacramento, San Francisco and Seattle. Accordingly, we have greater exposure to adverse events or conditions in any of these markets, such as changes in the economy, shifts in population or demographics, or changes in audience tastes, which could have a material adverse effect on our financial position and results of operations and cash flows.

6

Table of Contents

We may be unable to effectively integrate our acquisitions.

The integration of acquisitions involves numerous risks, including:

| • | difficulties in the integration of operations and systems and the management of a large and geographically diverse group of stations; |

| • | the diversion of management’s attention from other business concerns; and |

| • | the potential loss of key employees of acquired stations. |

The risks of integration are magnified during any period of significant growth from acquisitions. We cannot be assured that we will be able to integrate successfully any operations, systems or management that might be acquired in future acquisitions. In addition, in the event that the operations of a new business do not meet expectations, we may restructure or write off the value of some or all of the assets of the new business.

Impairments to our broadcasting licenses and goodwill have reduced our earnings.

We have incurred impairment losses that resulted in the non-cash write-downs of our broadcasting licenses and goodwill. A significant amount of these impairment losses were recorded in 2008 during the recession and the most recent impairment loss was recorded in 2012. As of December 31, 2015, our broadcasting licenses and goodwill comprise 82% of our total assets. The valuation of our broadcasting licenses and goodwill is subjective and based on our estimates and assumptions rather than precise calculations. The fair value measurements for both our broadcast licenses and goodwill use significant unobservable inputs and reflect our own assumptions including market share and profit margin for an average station, growth within a radio market, estimates of costs and losses during early years, potential competition within a radio market and the appropriate discount rate used in determining fair value. If events occur or circumstances change that would reduce the fair value of the broadcasting licenses and goodwill below the amount reflected on the balance sheet, we may be required to recognize impairment charges, which may be material, in future periods. Current accounting guidance does not permit a valuation increase.

We have significant obligations relating to our current operating leases.

As of December 31, 2015, we had future operating lease commitments of approximately $114 million that are disclosed in Note 20 in the accompanying notes to the audited consolidated financial statements. We are required to make certain estimates at the inception of a lease in order to determine whether the lease is operating or capital. In February 2016, the accounting guidance was modified to require that all leases with a term of more than one year, covering leased assets such as real estate, broadcasting towers and equipment, be reflected on the balance sheet as assets and liabilities for the rights and obligations created by these leases. While we are currently reviewing the effects of this guidance, we believe that this would result in: (1) an increase in the assets and liabilities reflected on our consolidated balance sheets; and (2) an increase in our interest expense and depreciation and amortization expense and a decrease to our station operating expense reflected on our consolidated statements of operations. This guidance is effective for us as of January 1, 2019.

Our business is dependent upon the proper functioning of our internal business processes and information systems and modification or interruption of such systems may disrupt our business, processes and internal controls.

The proper functioning of our internal business processes and information systems is critical to the efficient operation and management of our business. If these information technology systems fail or are interrupted, our operations may be adversely affected and operating results could be harmed. Our business processes and information systems need to be sufficiently scalable to support the future growth of our business and may require modifications or upgrades that expose us to a number of operational risks. Our information technology systems, and those of third-party providers, may also be vulnerable to damage or disruption caused by circumstances beyond our control. These include catastrophic events, power anomalies or outages, computer system or network failures and natural disasters. Any material disruption, malfunction or similar challenges with our business processes or information systems, or disruptions or challenges relating to the transition to new processes, systems or providers, could have a material adverse effect on our financial position, results of operations and cash flows.

Cybersecurity threats to our business

The use of our computers and digital technology in substantially all aspects of our business operations give rise to cybersecurity risks, including viruses or malware, physical or electronic intrusions and unauthorized access to

7

Table of Contents

our data. A cybersecurity attack could compromise confidential information. There can be no assurance that we, or the security systems we implement, will protect against all of these rapidly changing risks. A cyber-incident could increase our operating costs, disrupt our operations, harm our reputation, or subject us to liability under laws and regulations that protect personal data. We maintain insurance coverage against certain of such risks, but cannot guarantee that such coverage will be applicable or sufficient with respect to any given incident or on-going incidents that go undetected.

RISKS RELATED TO OUR INDEBTEDNESS

Current and future indebtedness could have an adverse impact on us.

We have outstanding debt that could have an adverse impact on us. For example, these obligations:

| • | increase our vulnerability in an economic downturn, limit our ability to withstand competitive pressures and reduce our flexibility in responding to changing business and economic conditions; |

| • | make it more difficult for us to satisfy our financial obligations; |

| • | limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions and general corporate or other purposes; |

| • | require us to dedicate a substantial portion of our cash flow from operations to debt service, thereby reducing the availability of cash flow for other purposes; |

| • | restrict us from taking advantage of opportunities to grow our business; and |

| • | limit or prohibit our ability to pay dividends and make other distributions. |

Our senior secured credit facility (the “Credit Facility”) includes a $40 million revolving commitment (the “Revolver”) of which $13.3 million was undrawn and available to us as of December 31, 2015. In December 2015, we reduced the total Revolver capacity from $50 million to $40 million. The amount of the Revolver available to us is a function of covenant compliance at the time of borrowing. Based on our financial covenant analysis as of December 31, 2015, we would not be limited in these borrowings. The Revolver matures on November 23, 2016. We expect to retire the Revolver using funds from operations. If we are not successful, a default under the Revolver could accelerate the due date for all of our outstanding debt.

We may from time to time seek to amend our existing debt agreements or obtain funding or additional debt financing, which may result in higher interest rates.

We must comply with the covenants in our debt agreements, which restrict our operational flexibility.

Our Credit Facility, which was entered into in November 2011 and subsequently amended, and the indenture governing our senior unsecured notes (the “Senior Notes”) contain provisions which, under certain circumstances, limit our ability to borrow money; make acquisitions, investments or restricted payments, including without limitation dividends and the repurchase of stock; swap or sell assets; or merge or consolidate with another company. To secure the debt under our Credit Facility, we have pledged substantially all of our assets, including the stock or equity interests of our subsidiaries. The Senior Notes are guaranteed on a senior unsecured basis by the parent and all of our existing subsidiaries.

The Credit Facility requires us to maintain compliance with specific financial covenants which are defined terms within the agreement, including: (1) a maximum Consolidated Leverage Ratio that cannot exceed 4.75 times at December 31, 2015, and which decreases to 4.50 times at March 31, 2016 and thereafter; and (2) a minimum Consolidated Interest Coverage Ratio of 2.00 times at December 31, 2015 and thereafter.

Our ability to comply with these financial covenants can be affected by operating performance or other events beyond our control, and we cannot be assured that we will comply with these covenants. A default under the indenture governing our Senior Notes or a default under our Credit Facility could cause a cross default. Any event of default, therefore, could have a material adverse effect on our business.

Failure to comply with our financial covenants or other terms of these financial instruments and the failure to negotiate and obtain any required relief from our lenders could result in the acceleration of the maturity of our outstanding debt and our lenders could proceed against our assets, including the equity interests of our subsidiaries. Under these circumstances, the acceleration of our debt could have a material adverse effect on our business.

8

Table of Contents

Because of our holding company structure, we depend on our subsidiaries for cash flow, and our access to this cash flow is restricted.

We operate as a holding company. All of our radio stations are currently owned and operated by our subsidiaries. Entercom Radio, LLC (“Radio”), our 100% owned finance subsidiary, is the borrower under our Credit Facility and is the issuer of our Senior Notes. All of our station operating subsidiaries and FCC license subsidiaries are subsidiaries of Radio. Further, we guarantee Radio’s obligations under the Credit Facility on a senior secured basis. The Senior Notes are guaranteed on an unsecured basis. Radio’s subsidiaries are all full and unconditional guarantors jointly and severally under the Credit Facility and the Senior Notes.

As a holding company, our only source of cash to pay our obligations, including corporate overhead and other expenses, is cash distributed from our subsidiaries. We currently expect that the majority of the net earnings and cash flow of our subsidiaries will be retained and used by them in their operations, including servicing Radio’s debt obligations. Even if our subsidiaries elect to make distributions to us, we cannot be assured that applicable state law and contractual restrictions, including the dividend covenants contained in our Credit Facility, would permit such dividends or distributions.

Our variable rate debt subjects us to interest rate risk, which could cause our debt service obligations to increase significantly.

Borrowings under our Credit Facility are at variable rates of interest and expose us to interest rate risk. If interest rates increase, our debt service obligations under the Credit Facility could increase even though the amount borrowed remains the same, and our net income and cash flows, including cash available for servicing our debt, could correspondingly decrease. As of December 31, 2015, and assuming the Revolver was fully drawn, a 100 basis point increase in London Interbank Offered Rate (“LIBOR”) rates as of December 31, 2015 would result in a $1.4 million increase in annual interest expense on our debt (in this hypothetical assumption, a 100 basis point increase in LIBOR only partially impacted the interest on our Credit Facility’s term loan (“Term B Loan”) as the LIBOR rate on our Term B Loan is subject to a 100 basis point minimum).

In the future, we may enter into interest rate swaps that involve the exchange of floating for fixed rate interest payments in order to reduce interest rate risk. We may, however, not maintain interest rate swaps with respect to all of our variable rate debt, and any swaps we enter into may not fully mitigate our interest rate risk.

A lowering or withdrawal of the ratings assigned to our debt securities by rating agencies may increase our future borrowing costs and reduce our access to capital.

Our debt has a non-investment grade rating, and any rating assigned could be lowered or withdrawn entirely by a rating agency if, in the rating agency’s judgment, future circumstances relating to the basis of the rating, such as adverse changes, so warrant. Any future lowering of our ratings would likely make it more difficult or more expensive for us to obtain additional debt financing.

RISKS ASSOCIATED WITH OUR STOCK

Our Chairman of the Board and our President and Chief Executive Officer own a substantial equity interest in us and effectively control our Company. Their interests may conflict with your interest.

As of February 15, 2016, Joseph M. Field, our Chairman of the Board, beneficially owned 1,563,291 shares of our Class A common stock and 6,148,282 shares of our Class B common stock, representing approximately 62% of the total voting power of all of our outstanding common stock. As of February 15, 2016, David J. Field, our President and Chief Executive Officer, one of our directors and the son of Joseph M. Field, beneficially owned 3,214,068 shares of our Class A common stock and 749,250 shares of our outstanding Class B common stock, representing approximately 11% of the total voting power of all of our outstanding common stock. Collectively, Joseph M. Field and David J. Field and other members of the Field family beneficially own all of our outstanding Class B common stock. Other members of the Field family and trusts for their benefit also own shares of Class A common stock.

9

Table of Contents

Shares of Class B common stock are transferable only to Joseph M. Field, David J. Field, certain of their family members or trusts for any of their benefit. Upon any other transfer, shares of our Class B common stock automatically convert into shares of our Class A common stock on a one-for-one basis. Shares of our Class B common stock are entitled to ten votes only when Joseph M. Field or David J. Field vote them, subject to certain exceptions when they are restricted to one vote. Joseph M. Field generally is able to control the vote on all matters submitted to a vote of shareholders and, therefore, is able to direct our management and policies, except with respect to those matters when the shares of our Class B common stock are only entitled to one vote and those matters requiring a class vote under the provisions of our articles of incorporation, bylaws or applicable law, including, without limitation, the election of the two Class A directors.

Future sales by Joseph M. Field and/or David J. Field could adversely affect the price of our Class A common stock.

The price for our Class A common stock could fall substantially if Joseph M. Field and/or David J. Field sell in the public market or transfer large amounts of shares, including any shares of our Class B common stock which are automatically converted to Class A common stock when sold (as described in the above paragraph). These sales, or the possibility of such sales, could make it more difficult for us to raise capital by selling equity or equity-related securities in the future.

The difficulties associated with any attempt to gain control of our Company could adversely affect the price of our Class A common stock.

Joseph M. Field controls the decision as to whether a change in control will occur for our Company. There are also provisions contained in our articles of incorporation, by-laws and Pennsylvania law that could make it more difficult for a third party to acquire control of our Company. In addition, FCC approval for transfers of control of FCC licenses and assignments of FCC licenses is required. These restrictions and limitations could adversely affect the trading price of our Class A common stock.

Our Class A stock price and trading volume could be volatile.

Our Class A common stock has been publicly traded on the New York Stock Exchange (“NYSE”) since January 29, 1999. The market price of our Class A common stock and our trading volume have been subject to fluctuations since the date of our initial public offering. As a result, the market price of our Class A common stock could experience volatility, regardless of our operating performance.

Our newly issued perpetual cumulative convertible preferred stock could adversely affect the price of our Class A common stock.

Our Board of Directors has the authority to issue up to 25,000,000 shares of preferred stock. We have issued 11 shares with a liquidation preference of $2.5 million per share. Our Board of Directors has the authority to determine the price, rights, preferences, privileges and restrictions, including voting rights, of our preferred stock without any further vote or action by the stockholders. The rights of the holders of our common stock may be subject to, and may be adversely affected by, the rights of the holders of any preferred stock that may be issued in the future.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

The types of properties required to support each of our radio stations include offices, studios and transmitter/antenna sites. We lease most of these sites. A station’s studios are generally housed with its offices in business districts. Our studio and office space leases typically contain lease terms with expiration dates of five to 15 years. Our transmitter/antenna sites, which may include an auxiliary transmitter/antenna as a back-up to the main site, contain lease terms that generally range from five to 30 years, which may include options to renew.

The transmitter/antenna site for each station is generally located so as to provide maximum market coverage. In general, we do not anticipate difficulties in renewing facility or transmitter/antenna site leases or in leasing additional space or sites if required.

10

Table of Contents

We have approximately $114 million in future minimum rental commitments under these leases. Many of these leases contain clauses such as defined contractual increases or cost of living adjustments.

Our principal executive offices are located at 401 E. City Avenue, Suite 809, Bala Cynwyd, Pennsylvania 19004, in 14,061 square feet of leased office space. The lease on these premises is due to expire on October 31, 2021. We generally consider our facilities to be suitable and of adequate size for our current and intended purposes.

| ITEM 3. | LEGAL PROCEEDINGS |

We currently and from time to time are involved in litigation incidental to the conduct of our business. Management anticipates that any potential liability of ours that may arise out of or with respect to these matters will not materially adversely affect our financial position, results of operations or cash flows.

Broadcast Licenses

We could face increased costs in the form of fines and a greater risk that we could lose any one or more of our broadcasting licenses if the FCC concludes that programming broadcast by our stations was obscene, indecent or profane and such conduct warrants license revocation. The FCC’s authority to impose a fine for the broadcast of such material is $325,000 for a single incident, with a maximum fine of up to $3,000,000 for a continuing violation. In the past, the FCC has issued Notices of Apparent Liability and a Forfeiture Order with respect to several of our stations proposing fines for certain programming which the FCC deemed to have been indecent. These cases are the subject of pending administrative appeals. The FCC has also investigated other complaints from the public that some of our stations broadcast indecent programming. These investigations remain pending. The FCC initiated an investigation into an incident where a person died in January 2007 after participating in a contest at one of our stations and this investigation remains pending. For a further discussion, refer to the risk factors described in Part I, Item 1A, “Risk Factors.”

| ITEM 4. | MINE SAFETY DISCLOSURE |

Not applicable.

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information For Our Common Stock

Our Class A common stock, $0.01 par value, is listed on the New York Stock Exchange under the symbol “ETM.” The table below shows, for the quarters indicated, the reported high and low trading prices of our Class A common stock on the New York Stock Exchange.

| Price Range | ||||||||

| High | Low | |||||||

| Calendar Year 2015 |

||||||||

| Fourth Quarter |

$ | 12.45 | $ | 9.75 | ||||

| Third Quarter |

$ | 11.99 | $ | 9.62 | ||||

| Second Quarter |

$ | 13.33 | $ | 11.00 | ||||

| First Quarter |

$ | 13.09 | $ | 11.16 | ||||

| Calendar Year 2014 |

||||||||

| Fourth Quarter |

$ | 12.77 | $ | 7.86 | ||||

| Third Quarter |

$ | 11.33 | $ | 8.03 | ||||

| Second Quarter |

$ | 11.11 | $ | 9.87 | ||||

| First Quarter |

$ | 11.47 | $ | 8.96 | ||||

There is no established trading market for our Class B common stock, $0.01 par value.

11

Table of Contents

Holders

As of February 15, 2016, there were approximately 266 shareholders of record of our Class A common stock. Based upon available information, we believe we have approximately 2,239 beneficial owners of our Class A common stock. There are four shareholders of record of our Class B common stock, $0.01 par value, and no shareholders of record of our Class C common stock, $0.01 par value. There is one holder of our perpetual cumulative convertible preferred stock.

Dividends

We do not currently pay, and have not paid for the past several years, any dividends on our common stock. The payment of any future dividends will be at the discretion of the Board of Directors based upon the relevant factors at the time of such consideration, including, without limitation, compliance with the restrictions set forth in our Credit Facility, the indenture governing our Senior Notes and our perpetual cumulative convertible preferred stock (“Preferred”). The payment of dividends on the Preferred and the repayment of the liquidation preference of the Preferred will take preference over any dividends or other payments to our common stockholders. A quarterly dividend on our Preferred of $0.4 million was declared and paid in October 2015 and in January 2016.

For a summary of these restrictions on our ability to pay dividends, see Liquidity under Part II, Item 7, “Management’s Discussion And Analysis Of Financial Condition And Results Of Operations,” and Note 8 in the accompanying notes to the consolidated financial statements.

Repurchases Of Our Stock

The following table provides information on our repurchases during the quarter ended December 31, 2015:

| Period (1) |

(a) Total Number Of Shares Purchased |

(b) Average Price Paid Per Share |

(c) Total Number Of Shares Purchased As Part Of Publicly Announced Plans Or Programs |

(d) Maximum Approximate Dollar Value Of Shares That May Yet Be Purchased Under The Plans Or Programs |

||||||||||||

| October 1, 2015 - October 31, 2015 |

1,950 | $ | 11.36 | — | $ | — | ||||||||||

| November 1, 2015 - November 30, 2015 |

1,215 | $ | 11.04 | — | $ | — | ||||||||||

| December 1, 2015 - December 31, 2015 |

— | $ | — | — | $ | — | ||||||||||

|

|

|

|

|

|||||||||||||

| Total |

3,165 | — | ||||||||||||||

|

|

|

|

|

|||||||||||||

| (1) | We withheld shares upon the vesting of restricted stock units (“RSUs”) in order to satisfy employees’ tax obligations. As a result, we are deemed to have purchased: (1) 1,950 shares at an average price of $11.36 per share in October 2015; and (2) 1,215 shares at an average price of $11.04 per share in November 2015. |

On July 16, 2015, we issued 11 shares of Series A Preferred Stock in connection with an acquisition. Each share of preferred stock has a conversion price of $14.35 (subject to adjustment) and a liquidation preference of $2,500,000 per share. We previously provided the information required by Item 702 of Regulation S-K in a Current Report on Form 8-K filed with the Securities and Exchange Commission on July 17, 2015.

12

Table of Contents

Equity Compensation Plan Information

The following table sets forth, as of December 31, 2015, the number of securities outstanding upon the exercise of outstanding options under our equity compensation plan, the weighted average exercise price of such securities and the number of securities available for grant under these plans:

| Equity Compensation Plan Information as of December 31, 2015 |

||||||||||||

| (a) | (b) | (c ) | ||||||||||

| Plan Category |

Number Of Shares To Be Issued Upon Exercise Of Outstanding Options, Warrants And Rights |

Weighted Average Exercise Price Of Outstanding Options, Warrants And Rights |

Number Of Securities Remaining Available For Future Issuance Under Equity Compensation Plans (Excluding Column (a)) |

|||||||||

| Equity Compensation Plans Approved by Shareholders: |

||||||||||||

| Entercom Equity Compensation Plan (1) |

466,925 | $ | 1.93 | 2,502,986 | ||||||||

| Equity Compensation Plans Not Approved by Shareholders: |

||||||||||||

| None |

— | — | — | |||||||||

|

|

|

|

|

|||||||||

| Total |

466,925 | 2,502,986 | ||||||||||

|

|

|

|

|

|||||||||

| (1) | On January 1 of each year, the number of shares of Class A common stock authorized under the Entercom Equity Compensation Plan (the “Plan”) is automatically increased by 1.5 million, or a lesser number as may be determined by our Board of Directors. The Board of Directors elected to forego the January 1, 2016 increase. As of December 31, 2015: (i) the maximum number of shares authorized under the Plan was 10.3 million shares; and (ii) 2.5 million shares remain available for future grant under the Plan. |

For a description of the Entercom Equity Compensation Plan refer to Note 13, Share-Based Compensation, in the accompanying notes to the consolidated financial statements.

13

Table of Contents

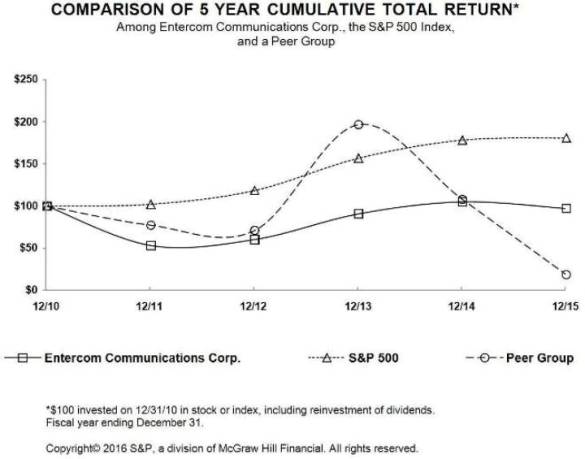

Performance Graph

The following Comparative Stock Performance Graph shall not be deemed incorporated by reference by any general statement incorporating by reference this Form 10-K into any filing under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended, except to the extent that we specifically incorporate this information by reference. This Comparative Stock Performance Graph is being furnished with this Form 10-K and shall not otherwise be deemed filed under such acts.

The following line graph compares the cumulative 5-year total return provided to shareholders of our Class A common stock relative to the cumulative total returns of: (i) the S&P 500 index; and (ii) a peer group index consisting of Cumulus Media Inc., Emmis Communications Corp., Radio One, Inc. and Beasley Broadcast Group, Inc. An investment of $100 (with reinvestment of all dividends) is assumed to have been made on December 31, 2010.

Cumulative Five-Year Return Index Of A $100 Investment

| 12/10 | 12/11 | 12/12 | 12/13 | 12/14 | 12/15 | |||||||||||||||||||

| Entercom Communications Corp. |

100.00 | 53.11 | 60.28 | 90.76 | 105.01 | 96.98 | ||||||||||||||||||

| S&P 500 |

100.00 | 102.11 | 118.45 | 156.82 | 178.29 | 180.75 | ||||||||||||||||||

| Peer Group |

100.00 | 77.25 | 71.06 | 196.65 | 107.85 | 18.47 | ||||||||||||||||||

14

Table of Contents

| ITEM 6. | SELECTED FINANCIAL DATA |

The selected financial data below, as of and for 2015 and the four prior years, were derived from our audited consolidated financial statements. The selected financial data for 2015, 2014 and 2013 and balance sheets as of December 31, 2015 and 2014 are qualified by reference to, and should be read in conjunction with, the corresponding audited consolidated financial statements, and the notes thereto, and Management’s Discussion and Analysis of Financial Condition and Results of Operations included elsewhere in this annual report. The selected financial data for 2012 and 2011 and the balance sheets as of December 31, 2013, 2012 and 2011 are derived from financial statements not included herein.

Our financial results are not comparable from year to year due to acquisitions and dispositions of radio stations, impairments of broadcasting licenses and goodwill and other significant events:

| • | In 2015, we acquired multiple radio stations, net of certain dispositions. Related to these transactions, we incurred: (1) merger and acquisition costs of $4.0 million in 2015 and $1.0 million in 2014; and (2) restructuring charges of $2.8 million in 2015 from the restructuring of operations; |

| • | In 2012 and 2011, we acquired one radio station; |

| • | In 2012, we incurred an impairment loss of $22.3 million in connection with our review of goodwill and broadcasting licenses; |

| • | In 2011, we reversed a full valuation allowance against our deferred tax assets that had been established previously; and |

| • | In the fourth quarter of 2011, we refinanced our debt which substantially increased our interest expense in 2012 as our new debt had higher borrowing rates than our prior debt. In addition, we incurred new deferred financing fees as part of the refinancing that were higher than the previous deferred financing fees. Subsequent modifications of our outstanding debt in the fourth quarters of 2013 and 2012 decreased our borrowing rate. |

15

Table of Contents

SELECTED FINANCIAL DATA

(amounts in thousands, except per share data)

| Years Ended December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Operating Data: |

||||||||||||||||||||

| Net revenues |

$ | 411,378 | $ | 379,789 | $ | 377,618 | $ | 388,924 | $ | 382,727 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating (income) expenses: |

||||||||||||||||||||

| Station operating expenses, including non-cash compensation expense |

287,711 | 259,184 | 252,596 | 252,934 | 264,195 | |||||||||||||||

| Depreciation and amortization |

8,419 | 7,794 | 8,545 | 10,839 | 11,276 | |||||||||||||||

| Corporate G & A expenses, including non-cash compensation expense |

26,479 | 26,572 | 24,381 | 25,874 | 26,609 | |||||||||||||||

| Impairment loss |

— | — | 850 | 22,307 | — | |||||||||||||||

| Merger and acquisition costs and restructuring charges |

6,836 | 1,042 | — | — | 767 | |||||||||||||||

| Net time brokerage agreement fees (income) |

(1,285 | ) | — | — | 238 | 244 | ||||||||||||||

| Net (gain) loss on sale of assets |

(2,364 | ) | (379 | ) | (1,321 | ) | 138 | 163 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses |

325,796 | 294,213 | 285,051 | 312,330 | 303,254 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (loss) |

85,582 | 85,576 | 92,567 | 76,594 | 79,473 | |||||||||||||||

| Other (income) expense: |

||||||||||||||||||||

| Net interest expense |

37,961 | 38,821 | 44,232 | 53,446 | 24,919 | |||||||||||||||

| Other income |

— | — | (165 | ) | (118 | ) | (32 | ) | ||||||||||||

| (Gain) loss on early extinguishment of debt |

— | — | — | 747 | 1,144 | |||||||||||||||

| Net loss on investments |

— | 21 | — | 123 | 30 | |||||||||||||||

| Net (gain) loss on derivative instruments |

— | — | — | (1,346 | ) | 1,346 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total other expense |

37,961 | 38,842 | 44,067 | 52,852 | 27,407 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes (benefit) |

47,621 | 46,734 | 48,500 | 23,742 | 52,066 | |||||||||||||||

| Income taxes (benefit) |

18,437 | 19,911 | 22,476 | 12,474 | (18,988 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to Company |

29,184 | 26,823 | 26,024 | 11,268 | 71,054 | |||||||||||||||

| Preferred stock dividend |

752 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to common shareholders |

$ | 28,432 | $ | 26,823 | $ | 26,024 | $ | 11,268 | $ | 71,054 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

16

Table of Contents

SELECTED FINANCIAL DATA

(amounts in thousands, except per share data)

| Years Ended December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Operating Data (continued): |

||||||||||||||||||||

| Net income (loss) attributable to common shareholders per share - basic: |

$ | 0.75 | $ | 0.71 | $ | 0.70 | $ | 0.31 | $ | 1.95 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to common shareholders per share - diluted: |

$ | 0.73 | $ | 0.69 | $ | 0.68 | $ | 0.30 | $ | 1.88 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average shares - basic |

38,084 | 37,763 | 37,418 | 36,906 | 36,369 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Weighted average shares - diluted |

39,038 | 38,664 | 38,301 | 37,810 | 37,764 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cash Flows Data: |

||||||||||||||||||||

| Cash flows related to: |

||||||||||||||||||||

| Operating activities |

$ | 64,790 | $ | 65,296 | $ | 63,349 | $ | 69,702 | $ | 85,525 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Investing activities |

$ | (91,744 | ) | $ | (7,055 | ) | $ | (4,583 | ) | $ | (29,359 | ) | $ | (14,284 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Financing activities |

$ | 4,583 | $ | (38,932 | ) | $ | (55,458 | ) | $ | (35,045 | ) | $ | (71,384 | ) | ||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Other Data: |

||||||||||||||||||||

| Dividends declared and paid on the perpetual cumulative convertible preferred stock - paid and accrued |

$ | 413 | $ | — | $ | — | $ | — | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 9,169 | $ | 31,540 | $ | 12,231 | $ | 8,923 | $ | 3,625 | ||||||||||

| Intangibles and other assets |

851,944 | 771,081 | 774,893 | 777,885 | 779,495 | |||||||||||||||

| Total assets |

1,022,108 | 926,615 | 912,688 | 920,358 | 919,269 | |||||||||||||||

| Senior secured debt, including current portion |

268,750 | 262,000 | 299,500 | 352,592 | 385,121 | |||||||||||||||

| Senior unsecured notes, senior subordinated notes and other |

218,269 | 217,929 | 217,624 | 229,959 | 229,713 | |||||||||||||||

| Deferred tax liabilities and other long-term liabilities |

109,251 | 89,904 | 70,519 | 41,455 | 23,152 | |||||||||||||||

| Perpetual cumulative convertible preferred stock (mezzanine) |

27,619 | — | — | — | — | |||||||||||||||

| Total shareholders’ equity |

361,450 | 329,021 | 298,393 | 269,494 | 253,688 | |||||||||||||||

17

Table of Contents

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

We are the fourth-largest radio broadcasting company in the United States with a portfolio of 125 radio stations in 27 top markets across the country.

Our results are based upon the aggregate performance of our radio stations. The following are some of the factors that impact a radio station’s performance at any given time: (i) audience ratings; (ii) program content; (iii) management talent and expertise; (iv) sales talent and expertise; (v) audience characteristics; (vi) signal strength; and (vii) the number and characteristics of other radio stations and other advertising media in the market area.

As opportunities arise, we may, on a selective basis, change or modify a station’s format due to changes in listeners’ tastes or changes in a competitor’s format. This could have an initial negative impact on a station’s ratings and/or revenues, and there are no guarantees that the modification or change will be beneficial at some future time. Our management is continually focused on these opportunities as well as the associated risks and uncertainties. We strive to develop compelling content and strong brand images to maximize audience ratings that are crucial to our stations’ financial success.

A radio broadcasting company derives its revenues primarily from the sale of broadcasting time to local, regional and national advertisers and national network advertisers who purchase spot commercials in varying lengths. A growing source of revenue is from station-related digital platforms, which allow for enhanced audience interaction and participation, and integrated local digital marketing solutions. A station’s local sales staff generates the majority of its local and regional advertising sales through direct solicitations of local advertising agencies and businesses. We retain a national representation firm to sell to advertisers outside of our local markets.

In the radio broadcasting industry, seasonal revenue fluctuations are common and are due primarily to variations in advertising expenditures by local and national advertisers. Typically, revenues are lowest in the first calendar quarter of the year.

In 2015, we generated the majority of our net revenues from local advertising, which is sold primarily by each individual local radio station’s sales staff, and the next largest amount from national advertising, which is sold by an independent advertising sales representative. This includes, but is not limited to, the sale of advertising during audio streaming of our radio stations over the Internet and the sale of advertising on our stations’ websites. We generated the balance of our 2015 revenues principally from network compensation, non-spot revenue, event marketing, e-commerce and integrated local digital marketing solutions.

The majority of our revenue is recorded on a net basis, which is gross revenue less advertising agency commissions. Revenues from digital marketing solutions and e-commerce are reflected on a net basis when appropriate. Revenues from event marketing are reflected on a net basis when we are not the primary party hosting the event. The revenues are determined by the advertising rates charged and the number of advertisements broadcast. We maximize our revenues by managing the inventory of advertising spots available for broadcast, which can vary throughout the day but is consistent over time.

Our most significant station operating expenses are employee compensation, programming and promotional expenses. Other significant expenses that impact our profitability are interest and depreciation and amortization expense.