Attached files

| file | filename |

|---|---|

| EX-99.2 - EXHIBIT 99.2 - Forest City Realty Trust, Inc. | fcrtex992erq4-2015.htm |

| 8-K - 8-K - Forest City Realty Trust, Inc. | a8kforsupppackq4-2015.htm |

Exhibit 99.1

Supplemental Package

For the Quarter Ended December 31, 2015

Forest City Realty Trust, Inc. and Subsidiaries - Supplemental Package

Fourth Quarter 2015

Index

Corporate Description | |

Selected Financial Information | |

Consolidated Balance Sheets | |

Consolidated Statements of Operations | |

Net Asset Value Components | |

Supplemental Operating Information | |

Occupancy Data | |

Retail Sales Data | |

Leasing Summary | |

Comparable Net Operating Income (NOI) | |

NOI Detail | |

NOI by Product Type | |

NOI by Core Market | |

Reconciliation of NOI to Earnings (Loss) Before Income Taxes | |

Segment Operating Results | |

Reconciliation of Net Earnings (Loss) to FFO | |

Reconciliation of FFO to Operating FFO | |

Reconciliation of Net Earnings (Loss) to EBITDA | |

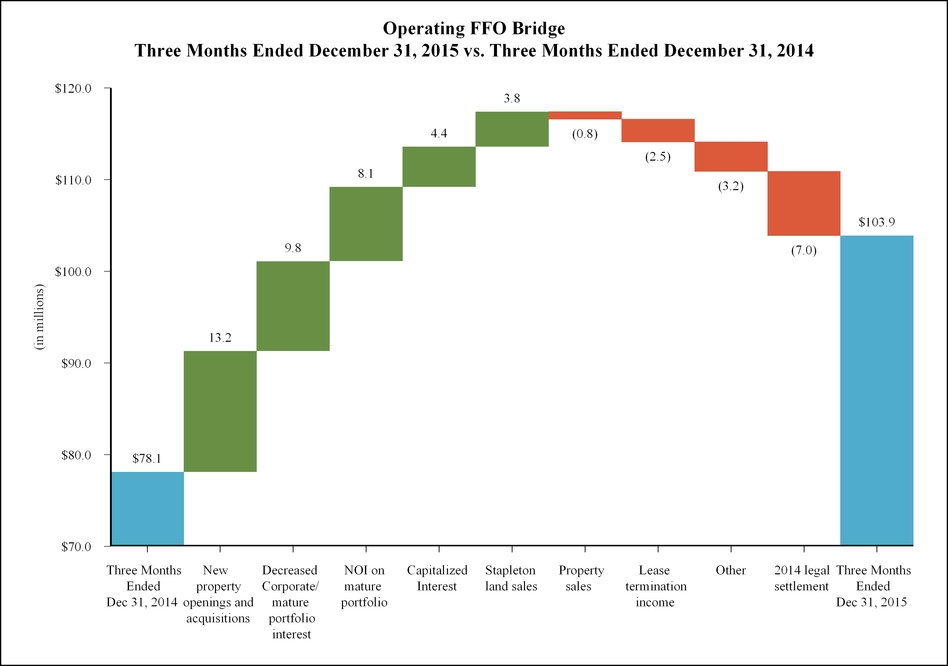

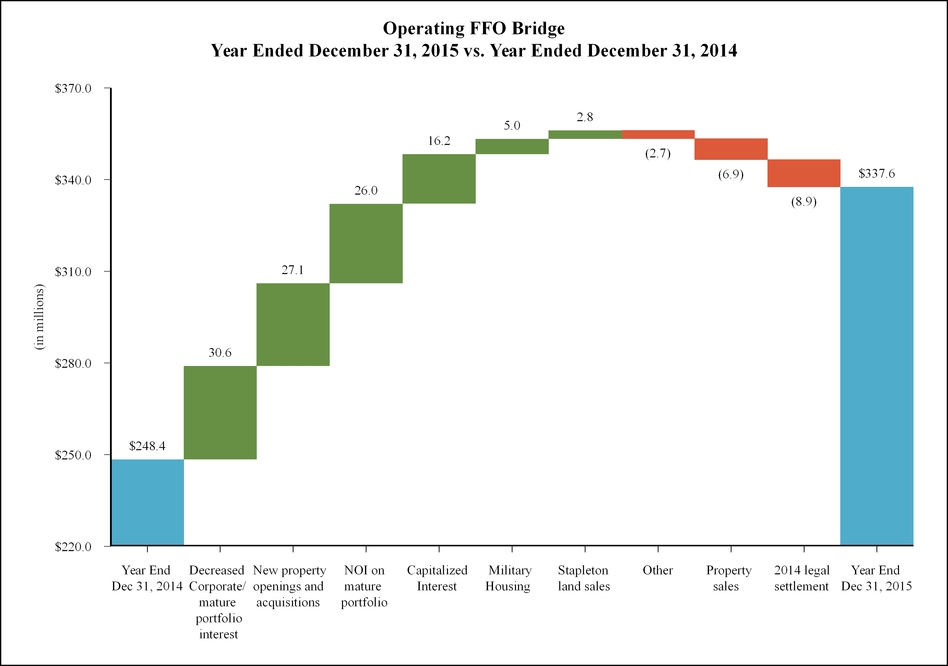

Operating FFO Bridges | |

Retail and Office Lease Expirations | |

Retail and Office Significant Tenants | |

Historical Trends | |

Development Pipeline | |

Military Housing | |

Supplemental Financial Information | |

Common Stock Data/Financial Covenants | |

Nonrecourse Debt Maturities Table | |

Summary of FFO by Segment | |

Property Listing | |

This supplemental package, together with other statements and information publicly disseminated by us, contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such statements reflect management’s current views with respect to financial results related to future events and are based on assumptions and expectations that may not be realized and are inherently subject to risks and uncertainties, many of which cannot be predicted with accuracy and some of which might not even be anticipated. Future events and actual results, financial or otherwise, may differ, perhaps materially, from the results discussed in the forward-looking statements. Risk factors discussed in Item 1A of our Form 10-K for the year ended December 31, 2015 and other factors that might cause differences, some of which could be material, include, but are not limited to, our ability to qualify or to remain qualified as a REIT, our ability to satisfy REIT distribution requirements, the impact of issuing equity, debt or both, and selling assets to satisfy our future distributions required as a REIT or to fund capital expenditures, future growth and expansion initiatives, the impact of the amount and timing of any future distributions, the impact from complying with REIT qualification requirements limiting our flexibility or causing us to forego otherwise attractive opportunities beyond rental real estate operations, the impact of complying with the REIT requirements related to hedging, our lack of experience operating as a REIT, legislative, administrative, regulatory or other actions affecting REITs, including positions taken by the Internal Revenue Service, the possibility that our Board of Directors will unilaterally revoke our REIT election, the possibility that the anticipated benefits of qualifying as a REIT will not be realized, or will not be realized within the expected time period, the impact of current lending and capital market conditions on our liquidity, our ability to finance or refinance projects or repay our debt, the impact of the slow economic recovery on the ownership, development and management of our commercial real estate portfolio, general real estate investment and development risks, using modular construction as a new construction methodology and owning a factory to produce modular units, litigation risks, vacancies in our properties, risks associated with developing and managing properties in partnership with others, competition, our ability to renew leases or re-lease spaces as leases expire, illiquidity of real estate investments, bankruptcy or defaults of tenants, anchor store consolidations or closings, the impact of terrorist acts and other armed conflicts, our substantial debt leverage and the ability to obtain and service debt, the impact of restrictions imposed by our credit facility and senior debt, exposure to hedging agreements, the level and volatility of interest rates, the continued availability of tax-exempt government financing, our ability to receive payment on the notes receivable issued by Onexim in connection with their purchase of our interests in the Barclays Center and the Nets, the impact of credit rating downgrades, effects of uninsured or underinsured losses, effects of a downgrade or failure of our insurance carriers, environmental liabilities, competing interest of our directors and executive officers, the ability to recruit and retain key personnel, risks associated with the sale of tax credits, downturns in the housing market, the ability to maintain effective internal controls, compliance with governmental regulations, increased legislative and regulatory scrutiny of the financial services industry, changes in federal, state or local tax laws, volatility in the market price of our publicly traded securities, inflation risks, cybersecurity risks, cyber incidents, conflicts of interest, and risks related to our organizational structure including operating through our Operating Partnership and our UPREIT structure, as well as other risks listed from time to time in the company’s SEC filings, including but not limited to, the company’s annual and quarterly reports. We have no obligation to revise or update any forward-looking statements, other than as imposed by law, as a result of future events or new information. Readers are cautioned not to place undue reliance on such forward-looking statements.

1

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Financial and Operating Information

Corporate Description

We principally engage in the ownership, development, management and acquisition of commercial and residential real estate and land throughout the United States. We have approximately $10.0 billion of consolidated assets in 24 states and the District of Columbia at December 31, 2015. Our core markets include Boston, Chicago, Dallas, Denver, Los Angeles, Philadelphia and the greater metropolitan areas of New York City, San Francisco and Washington D.C. We have regional offices in Boston, Dallas, Denver, Los Angeles, New York City, San Francisco, Washington, D.C. and our corporate headquarters in Cleveland, Ohio.

REIT Conversion

On January 13, 2015, the board of directors of Forest City Enterprises, Inc., our predecessor, approved a plan to pursue conversion to REIT status. On May 29, 2015, Forest City Enterprises, Inc. formed Forest City Realty Trust, Inc. (with its subsidiaries, the “Company”) as a Maryland corporation and wholly-owned subsidiary of Forest City Enterprises, Inc. On October 20, 2015, the shareholders of Forest City Enterprises, Inc. approved and adopted the merger agreement that implemented the restructuring of Forest City Enterprises, Inc. into a holding company so as to facilitate its conversion to a REIT.

Pursuant to the merger agreement, effective as of 11:59 pm, Eastern Time, on December 31, 2015 (the “Effective Time”), (i) a wholly-owned subsidiary of the Company merged with and into Forest City Enterprises, Inc., with Forest City Enterprises, Inc. as the surviving corporation, (ii) each outstanding share of Forest City Enterprises, Inc. Class A common stock, par value $.33 1/3 per share, and Class B common stock, par value $.33 1/3 per share, automatically converted into one share of Forest City Realty Trust, Inc. Class A common stock, $.01 par value per share, and Class B common stock, $.01 par value per share, respectively, (iii) Forest City Enterprises, Inc. became a wholly-owned subsidiary of the Company and (iv) the Company became the publicly-traded New York Stock Exchange-listed parent company that succeeded to and continued to operate substantially all of the existing businesses of Forest City Enterprises, Inc. and its subsidiaries. In addition, each share of Class A common stock of Forest City Enterprises, Inc. held in treasury at December 31, 2015 ceased to be outstanding at the Effective Time of the Merger, and a corresponding adjustment was recorded to Class A common stock and additional paid-in capital. Immediately following the merger, Forest City Enterprises, Inc. converted into a Delaware limited partnership named “Forest City Enterprises, L.P.” (the “Operating Partnership”).

In this supplemental package, unless otherwise specifically stated or the context otherwise, all references to “the Company,” “Forest City,” “we,” “our,” “us” and similar terms refer to Forest City Enterprises, Inc. and its consolidated subsidiaries prior to the Effective Time and Forest City Realty Trust, Inc. and its consolidated subsidiaries, including the Operating Partnership, as of the Effective Time and thereafter.

Company Operations

As of January 1, 2016, we believe that we are organized in a manner that enables us to qualify, and intend to operate in a manner that will allow us to continue to qualify, as a real estate investment trust (“REIT”) for federal income tax purposes. As such, we intend to elect REIT status for our taxable year ending December 31, 2016, upon filing the 2016 Form 1120-REIT with the Internal Revenue Service on or before September 15, 2017.

We hold substantially all of our assets, and conduct substantially all of our business, through the Operating Partnership. We are the sole general partner of the Operating Partnership and, as of December 31, 2015, following the conversion of Forest City Enterprises, Inc. into the Operating Partnership, we directly or indirectly own all of the limited partnership interests in the Operating Partnership.

We hold and operate certain of our assets through one or more taxable REIT subsidiaries (“TRSs”). A TRS is a subsidiary of a REIT that is subject to applicable corporate income tax. Our use of TRSs enables us to continue to engage in certain businesses while complying with REIT qualification requirements and also allows us to retain income generated by these businesses for reinvestment without the requirement of distributing those earnings. The non-REIT qualified businesses that we hold through TRSs primarily include our investments in our Land Development Group, Barclays Center arena and the Brooklyn Nets (the “Nets”), a member of the National Basketball Association (“NBA”) (subsequently sold in January 2016), B2 BKLYN, an apartment building under construction in Brooklyn, New York, military housing operations (subsequently sold in February 2016), and Pacific Park Brooklyn project. In the future, we may elect to reorganize and transfer certain assets or operations from our TRSs to other subsidiaries, including qualified REIT subsidiaries.

2

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Financial and Operating Information

We operate through five reportable operating segments. The Commercial Group, Residential Group and Land Development Group (collectively, the “Real Estate Groups”) represent four reportable operating segments:

• | Commercial Group owns, develops, acquires and operates regional malls, specialty/urban retail centers, office and life science buildings and mixed-use projects. Additionally, it operated Barclays Center, a sports and entertainment arena located in Brooklyn, New York, which is reported as a separate operating segment (“Arena”). The Arena, which was disposed of during January 2016, is classified as held for sale and reported in discontinued operations for all periods presented. |

• | Residential Group owns, develops, acquires and operates residential rental properties, including upscale and middle-market apartments, adaptive re-use developments, for-sale condominium projects and subsidized senior housing. Additionally, it owns interests in entities that develop and manage military family housing, which was disposed of during February 2016. |

• | Land Development Group acquires and sells both land and developed lots to residential, commercial and industrial customers at our Stapleton project in Denver, Colorado. |

Corporate Activities is the other reportable operating segment, which includes our equity method investment in the Nets, which was disposed of during January 2016. The Nets is classified as held for sale and is reported in discontinued operations for all periods presented.

Supplemental Financial and Operating Information

We recommend this supplemental package be read in conjunction with our Form 10-K for the year ended December 31, 2015. This supplemental package contains information prepared in accordance with generally accepted accounting principles (“GAAP”) under the full consolidation accounting method and information prepared under the pro-rata consolidation method, a non-GAAP measure. We present certain financial amounts under the pro-rata consolidation method because we believe this information is useful to financial statement users as this method reflects the manner in which we operate our business. We believe the non-GAAP financial and operating information presented under the pro-rata consolidation method, net operating income (“NOI”), comparable NOI, Funds From Operations (“FFO”), Operating FFO, Earnings Before Interest, Taxes, Depreciation and Amortization (“EBITDA”) and Adjusted EBITDA are necessary to understand our business and operating results, along with net earnings and other GAAP measures. Our financial statement users can use these non-GAAP measures as supplementary information to evaluate our business. Our non-GAAP measures are not intended to be performance measures that should be regarded as alternatives to, or more meaningful than, our GAAP measures.

Consolidation Methods

In line with industry practice, we have a number of investments in which our economic ownership is less than 100% as a means of procuring opportunities and sharing risk. Under GAAP, the full consolidation method is used to report assets and liabilities at 100% if deemed to be under our control or if we are deemed to be the primary beneficiary of the variable interest entity (“VIE”), even if our ownership is not 100%. Under the pro-rata consolidation method, we generally present our investments proportionate to our economic share of ownership. We provide reconciliations from the full consolidation method to the pro-rata consolidation method throughout this supplemental package.

FFO

The majority of our peers in the publicly traded real estate industry are REITs and report operations using FFO as defined by the National Association of Real Estate Investment Trusts (“NAREIT”). Although we did not operate as a REIT for the periods presented in this supplemental package, we believe it is important to publish this measure to allow for easier comparison of our performance to our peers. The major difference between us and our REIT peers is that we were a taxable entity and any taxable income we generated could result in payment of federal or state income taxes. Our REIT peers typically do not pay federal or state income taxes on their qualified REIT investments, but distribute a significant portion of their taxable income to shareholders. Due to our effective tax management policies, we have not historically been a significant payer of income taxes. This has allowed us to retain our internally generated cash flows but has also resulted in large non-cash expenses for deferred taxes as required by GAAP.

FFO is defined by NAREIT as net earnings excluding the following items at our proportionate share: i) gain (loss) on full or partial disposition of rental properties, divisions and other investments (net of tax); ii) non-cash charges for real estate depreciation and amortization; iii) impairment of depreciable real estate (net of tax); and iv) cumulative or retrospective effect of change in accounting principle (net of tax).

In connection with our conversion to REIT status, we were required to reverse our net deferred tax liabilities related to our subsidiaries that will be held as qualified REIT investments of $588,607,000 during the three months ended December 31, 2015, which we have excluded from our December 31, 2015 FFO calculation.

3

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Financial and Operating Information

Operating FFO

In addition to reporting FFO, we report Operating FFO as an additional measure of our operating performance. We believe it is appropriate to adjust FFO for significant items driven by transactional activity and factors relating to the financial and real estate markets, rather than factors specific to the on-going operating performance of our properties. We use Operating FFO as an indicator of continuing operating results in planning and executing our business strategy. Operating FFO should not be considered to be an alternative to net earnings computed under GAAP as an indicator of our operating performance and may not be directly comparable to similarly-titled measures reported by other companies.

We define Operating FFO as FFO adjusted to exclude: i) impairment of non-depreciable real estate; ii) write-offs of abandoned development projects and demolition costs; iii) income recognized on state and federal historic and other tax credits; iv) gains or losses from extinguishment of debt; v) change in fair market value of nondesignated hedges; vi) gains or losses on change in control of interests; vii) the adjustment to recognize rental revenues and rental expense using the straight-line method; viii) participation payments to ground lessors on refinancing of our properties; ix) other transactional items; x) the Nets pre-tax FFO; and xi) income taxes on FFO.

EBITDA

EBITDA, a non-GAAP measure, is defined as net earnings excluding the following items at our proportionate share: i) non-cash charges for depreciation and amortization; ii) interest expense; iii) amortization of mortgage procurement costs; and iv) income taxes. EBITDA may not be directly comparable to similarly-titled measures reported by other companies.

Adjusted EBITDA

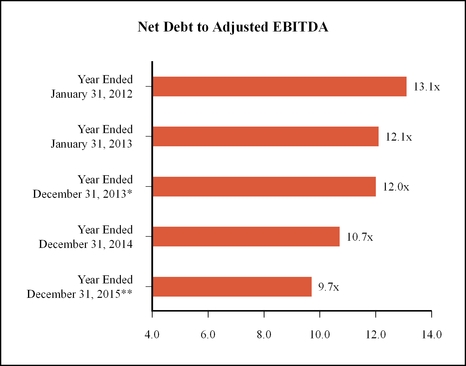

We define Adjusted EBITDA as EBITDA adjusted to exclude: i) impairment of real estate; ii) gains or losses from extinguishment of debt; iii) gain (loss) on full or partial disposition of rental properties, development projects and other investments; iv) gains or losses on change in control of interests; v) other transactional items; and vi) the Nets pre-tax EBITDA. We believe EBITDA, Adjusted EBITDA and net debt to Adjusted EBITDA provide additional information in evaluating our credit and ability to service our debt obligations. Adjusted EBITDA may not be directly comparable to similarly-titled measures reported by other companies.

NOI

NOI, a non-GAAP measure, reflects our share of the core operations of our rental real estate portfolio, prior to any financing activity. NOI is defined as revenues less operating expenses of consolidated and unconsolidated subsidiaries within our Commercial Group and our Residential Group, except for revenues and cost of sales associated with sales of land held in these segments. The activities of the Land Development Group and Corporate Activities do not involve the operations of our rental property portfolio and therefore are not included in NOI.

Our historical NOI was calculated based on an entire company perspective rather than focusing on the core operations of our rental real estate portfolio. It included amounts associated with the Land Development Group and Corporate Activities, all of which are now excluded to arrive at our rental real estate portfolio property NOI measure. In addition, we evaluated revenue and expense items in the Commercial and Residential segments and determined straight-line rent adjustments should be included in NOI (previously excluded) and land sales less cost of land sales, interest and other income and write-offs of abandoned development projects should be excluded (previously included). We believe the NOI calculation provides a financial measure that better reflects the ongoing operating performance of our rental property portfolio and aligns our NOI reporting closer to that of our peers. Prior periods were adjusted for comparability purposes.

We believe NOI provides important information about our core operations and, along with earnings, is necessary to understand our business and operating results. NOI may not be directly comparable to similarly-titled measures reported by other companies.

Comparable NOI

We use comparable NOI as a metric to evaluate the performance of our multi-family, office and retail properties. This measure provides a same-store comparison of operating results of all stabilized properties that are open and operating in all periods presented. Non-capitalizable development costs and unallocated management and service company overhead are not directly attributable to an operating property and are considered non-comparable NOI. In addition, certain income and expense items at the property level, such as lease termination income, real estate tax assessments or rebates and NOI impacts of changes in ownership percentages, are excluded from comparable NOI and are considered non-comparable NOI. Retained operating properties considered non-comparable are disclosed in the Segment Operating Results of this supplemental package. Other properties and activities such as Arena, subsidized senior housing, military housing, straight-line rent adjustments and participation payments as a result of refinancing transactions are not evaluated on a comparable basis and the NOI from these properties and activities is considered non-comparable NOI.

4

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Financial and Operating Information

Comparable NOI is an operating statistic defined as NOI from stabilized properties operated in all periods presented, net of noncontrolling interests. Comparable NOI is useful because it measures the performance of the same properties on a period-to-period basis and is used to assess operating performance and resource allocation of the operating properties. While property dispositions, acquisitions or other factors impact net earnings in the short term, we believe comparable NOI presents a more consistent view of the overall performance of our operating portfolio from period to period. A reconciliation of NOI to earnings (loss) before income taxes, the most comparable financial measure calculated in accordance with GAAP, a reconciliation of NOI to earnings (loss) before income taxes for each operating segment and a reconciliation from NOI to comparable NOI are included in this supplemental package.

Supplemental Operating Information

The operating information contained in this document includes: occupancy data, retail sales data, leasing summaries, comparable NOI, NOI by product type and core market, reconciliation of NOI to earnings (loss) before income taxes, segment operating results discussion, reconciliation of net earnings (loss) to FFO, reconciliation of FFO to Operating FFO, reconciliation of net earnings (loss) to EBITDA, Operating FFO bridges, retail and office lease expirations, retail and office significant tenants, historical trends and our development pipeline. We believe this information gives interested parties a better understanding and more information about our operating performance. The term “comparable,” which is used throughout this document, is generally defined as including stabilized properties open and operated in both the three months and years ended December 31, 2015 and 2014. We believe occupancy data, retail sales data, leasing spreads on retail and office properties, and other rental rate information on multi-family properties represent meaningful operating statistics about us.

5

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Financial and Operating Information

Corporate Headquarters

Forest City Realty Trust, Inc.

Terminal Tower

50 Public Square, Suite 1100

Cleveland, Ohio 44113

Annual Report on Form 10-K

A copy of the Annual Report on Form 10-K as filed with the Securities and Exchange Commission (“SEC”) for the year ended December 31, 2015, can be found on our website under SEC Filings or may be obtained without charge upon written request to:

Jeffrey B. Linton

Senior Vice President - Corporate Communication

JeffLinton@forestcity.net

Website

www.forestcity.net

The information contained on this website is not incorporated herein by reference and does not constitute a part of this supplemental package.

Investor Relations

Michael E. Lonsway

Senior Vice President - Planning

MikeLonsway@forestcity.net

Investor Presentations

Please note we periodically post updated investor presentations on the Investors page of our website at www.forestcity.net. It is possible the periodic updates may include information deemed to be material. Therefore, we encourage investors, the media, and other interested parties to review the Investors page of our website at www.forestcity.net for the most recent investor presentation.

Transfer Agent and Registrar

Wells Fargo

Shareowner Services

P.O. Box 64854

St. Paul, MN 55164-9440

(800) 468-9716

www.shareowneronline.com

NYSE Listings

FCEA - Class A Common Stock ($.01 par value)

FCEB - Class B Common Stock ($.01 par value)

Dividend Reinvestment and Stock Purchase Plan

We offer our shareholders the opportunity to purchase additional shares of common stock through the Forest City Realty Trust, Inc. Dividend Reinvestment and Stock Purchase Plan (the “Plan”). You may obtain a copy of the Plan prospectus and an enrollment card by contacting Wells Fargo Shareowner Services at (800) 468-9716 or by visiting www.shareowneronline.com.

6

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Balance Sheet – December 31, 2015 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Pro-Rata Consolidation (Non-GAAP) | |||||||||

(in thousands) | ||||||||||||

Assets | ||||||||||||

Real Estate | ||||||||||||

Completed rental properties | ||||||||||||

Residential | $ | 2,657,399 | $ | 413,832 | $ | 989,971 | $ | 3,233,538 | ||||

Commercial | ||||||||||||

Retail centers | 1,385,662 | — | 1,685,051 | 3,070,713 | ||||||||

Office buildings | 3,640,468 | 110,389 | 97,431 | 3,627,510 | ||||||||

Corporate and other equipment | 10,542 | — | — | 10,542 | ||||||||

Total completed rental properties | 7,694,071 | 524,221 | 2,772,453 | 9,942,303 | ||||||||

Projects under construction | ||||||||||||

Residential | 545,574 | 302,782 | 129,117 | 371,909 | ||||||||

Commercial | ||||||||||||

Retail centers | — | — | — | — | ||||||||

Office buildings | 84,253 | — | 70,988 | 155,241 | ||||||||

Total projects under construction | 629,827 | 302,782 | 200,105 | 527,150 | ||||||||

Projects under development | ||||||||||||

Operating properties | 36,152 | — | 5,275 | 41,427 | ||||||||

Residential | 109,616 | — | 245,608 | 355,224 | ||||||||

Commercial | ||||||||||||

Retail centers | 23,777 | — | 3,941 | 27,718 | ||||||||

Office buildings | 90,246 | 8,876 | 3,276 | 84,646 | ||||||||

Total projects under development | 259,791 | 8,876 | 258,100 | 509,015 | ||||||||

Total projects under construction and development | 889,618 | 311,658 | 458,205 | 1,036,165 | ||||||||

Land inventory | 69,318 | 5,191 | 8,796 | 72,923 | ||||||||

Total Real Estate | 8,653,007 | 841,070 | 3,239,454 | 11,051,391 | ||||||||

Less accumulated depreciation | (1,624,920 | ) | (71,249 | ) | (656,127 | ) | (2,209,798 | ) | ||||

Real Estate, net | 7,028,087 | 769,821 | 2,583,327 | 8,841,593 | ||||||||

Cash and equivalents | 265,677 | 15,705 | 59,977 | 309,949 | ||||||||

Restricted cash | 161,891 | 7,482 | 119,165 | 273,574 | ||||||||

Notes and accounts receivable, net | 376,147 | 18,337 | 65,307 | 423,117 | ||||||||

Investments in and advances to unconsolidated entities | 678,872 | (105,382 | ) | (658,763 | ) | 125,491 | ||||||

Lease and mortgage procurement costs, net | 143,672 | 11,432 | 81,554 | 213,794 | ||||||||

Prepaid expenses and other deferred costs, net | 111,619 | 9,040 | 16,621 | 119,200 | ||||||||

Intangible assets, net | 198,672 | 14,572 | 16,509 | 200,609 | ||||||||

Deferred income taxes, net | 83,645 | — | — | 83,645 | ||||||||

Assets held for sale | 944,727 | 583,840 | — | 360,887 | ||||||||

Total Assets | $ | 9,993,009 | $ | 1,324,847 | $ | 2,283,697 | $ | 10,951,859 | ||||

7

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Balance Sheet – December 31, 2015 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Pro-Rata Consolidation (Non-GAAP) | |||||||||

(in thousands) | ||||||||||||

Liabilities and Equity | ||||||||||||

Liabilities | ||||||||||||

Mortgage debt and notes payable, nonrecourse | ||||||||||||

Completed rental properties | ||||||||||||

Residential | $ | 1,452,790 | $ | 254,578 | $ | 690,321 | $ | 1,888,533 | ||||

Commercial | ||||||||||||

Retail centers | 631,901 | — | 1,238,611 | 1,870,512 | ||||||||

Office buildings | 1,798,622 | 42,990 | 76,264 | 1,831,896 | ||||||||

Total completed rental properties | 3,883,313 | 297,568 | 2,005,196 | 5,590,941 | ||||||||

Projects under construction | ||||||||||||

Residential | 59,113 | 44,324 | 20,175 | 34,964 | ||||||||

Commercial | ||||||||||||

Retail centers | — | — | — | — | ||||||||

Office buildings | 28,167 | — | 47,913 | 76,080 | ||||||||

Total projects under construction | 87,280 | 44,324 | 68,088 | 111,044 | ||||||||

Projects under development | ||||||||||||

Operating properties | — | — | — | — | ||||||||

Residential | 32,857 | — | 152,815 | 185,672 | ||||||||

Commercial | ||||||||||||

Retail centers | — | — | — | — | ||||||||

Office buildings | — | — | — | — | ||||||||

Total projects under development | 32,857 | — | 152,815 | 185,672 | ||||||||

Total projects under construction and development | 120,137 | 44,324 | 220,903 | 296,716 | ||||||||

Land inventory | — | — | 8,580 | 8,580 | ||||||||

Total mortgage debt and notes payable, nonrecourse | 4,003,450 | 341,892 | 2,234,679 | 5,896,237 | ||||||||

Revolving credit facility | — | — | — | — | ||||||||

Convertible senior debt | 271,006 | — | — | 271,006 | ||||||||

Construction payables | 166,811 | 63,303 | 39,259 | 142,767 | ||||||||

Operating accounts payable and accrued expenses | 622,327 | 23,975 | 154,372 | 752,724 | ||||||||

Accrued derivative liability | 73,679 | — | 6,839 | 80,518 | ||||||||

Total Accounts payable, accrued expenses and other liabilities | 862,817 | 87,278 | 200,470 | 976,009 | ||||||||

Cash distributions and losses in excess of investments in unconsolidated entities | 150,255 | (19,859 | ) | (151,452 | ) | 18,662 | ||||||

Liabilities held for sale | 570,947 | 398,334 | — | 172,613 | ||||||||

Total Liabilities | 5,858,475 | 807,645 | 2,283,697 | 7,334,527 | ||||||||

Redeemable Noncontrolling Interest | 159,978 | 159,978 | — | — | ||||||||

Equity | ||||||||||||

Shareholders’ Equity | ||||||||||||

Shareholders’ equity before accumulated other comprehensive loss | 3,586,237 | — | — | 3,586,237 | ||||||||

Accumulated other comprehensive loss | (67,905 | ) | — | — | (67,905 | ) | ||||||

Total Shareholders’ Equity | 3,518,332 | — | — | 3,518,332 | ||||||||

Noncontrolling interest | 456,224 | 357,224 | — | 99,000 | ||||||||

Total Equity | 3,974,556 | 357,224 | — | 3,617,332 | ||||||||

Total Liabilities and Equity | $ | 9,993,009 | $ | 1,324,847 | $ | 2,283,697 | $ | 10,951,859 | ||||

8

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Balance Sheet – December 31, 2014 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Pro-Rata Consolidation (Non-GAAP) | |||||||||

(in thousands) | ||||||||||||

Assets | ||||||||||||

Real Estate | ||||||||||||

Completed rental properties | ||||||||||||

Residential | $ | 2,470,813 | $ | 370,855 | $ | 1,060,830 | $ | 3,160,788 | ||||

Commercial | ||||||||||||

Retail centers | 1,747,127 | — | 1,654,140 | 3,401,267 | ||||||||

Office buildings | 2,584,854 | 107,656 | 262,524 | 2,739,722 | ||||||||

Corporate and other equipment | 10,738 | — | — | 10,738 | ||||||||

Total completed rental properties | 6,813,532 | 478,511 | 2,977,494 | 9,312,515 | ||||||||

Projects under construction | ||||||||||||

Residential | 176,148 | 96,567 | 9,262 | 88,843 | ||||||||

Commercial | ||||||||||||

Retail centers | — | — | — | — | ||||||||

Office buildings | 8,940 | — | 42,923 | 51,863 | ||||||||

Total projects under construction | 185,088 | 96,567 | 52,185 | 140,706 | ||||||||

Projects under development | ||||||||||||

Operating properties | 29,187 | — | 12,589 | 41,776 | ||||||||

Residential | 139,923 | 22,769 | 214,084 | 331,238 | ||||||||

Commercial | ||||||||||||

Retail centers | 33,807 | — | 4,014 | 37,821 | ||||||||

Office buildings | 89,952 | 8,791 | 3,180 | 84,341 | ||||||||

Total projects under development | 292,869 | 31,560 | 233,867 | 495,176 | ||||||||

Total projects under construction and development | 477,957 | 128,127 | 286,052 | 635,882 | ||||||||

Land inventory | 97,469 | 5,351 | 8,537 | 100,655 | ||||||||

Total Real Estate | 7,388,958 | 611,989 | 3,272,083 | 10,049,052 | ||||||||

Less accumulated depreciation | (1,480,611 | ) | (59,001 | ) | (680,584 | ) | (2,102,194 | ) | ||||

Real Estate, net | 5,908,347 | 552,988 | 2,591,499 | 7,946,858 | ||||||||

Cash and equivalents | 290,668 | 17,437 | 79,716 | 352,947 | ||||||||

Restricted cash | 251,443 | 20,528 | 125,680 | 356,595 | ||||||||

Notes and accounts receivable, net | 408,517 | 19,158 | 59,786 | 449,145 | ||||||||

Investments in and advances to unconsolidated entities | 620,466 | (94,212 | ) | (605,009 | ) | 109,669 | ||||||

Lease and mortgage procurement costs, net | 154,039 | 11,480 | 81,617 | 224,176 | ||||||||

Prepaid expenses and other deferred costs, net | 102,112 | 7,326 | 14,702 | 109,488 | ||||||||

Intangible assets, net | 123,778 | 17,554 | 16,436 | 122,660 | ||||||||

Assets held for sale | 955,570 | 579,282 | — | 376,288 | ||||||||

Total Assets | $ | 8,814,940 | $ | 1,131,541 | $ | 2,364,427 | $ | 10,047,826 | ||||

9

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Balance Sheet – December 31, 2014 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Pro-Rata Consolidation (Non-GAAP) | |||||||||

(in thousands) | ||||||||||||

Liabilities and Equity | ||||||||||||

Liabilities | ||||||||||||

Mortgage debt and notes payable, nonrecourse | ||||||||||||

Completed rental properties | ||||||||||||

Residential | $ | 1,376,329 | $ | 202,112 | $ | 740,668 | $ | 1,914,885 | ||||

Commercial | ||||||||||||

Retail centers | 638,310 | — | 1,252,645 | 1,890,955 | ||||||||

Office buildings | 1,652,685 | 72,277 | 247,424 | 1,827,832 | ||||||||

Total completed rental properties | 3,667,324 | 274,389 | 2,240,737 | 5,633,672 | ||||||||

Projects under construction | ||||||||||||

Residential | 61,905 | 4,266 | 1,293 | 58,932 | ||||||||

Commercial | ||||||||||||

Retail centers | — | — | — | — | ||||||||

Office buildings | 29,422 | — | 23,370 | 52,792 | ||||||||

Total projects under construction | 91,327 | 4,266 | 24,663 | 111,724 | ||||||||

Projects under development | ||||||||||||

Operating properties | — | — | — | — | ||||||||

Residential | 32,267 | — | 97,467 | 129,734 | ||||||||

Commercial | ||||||||||||

Retail centers | — | — | — | — | ||||||||

Office buildings | — | — | — | — | ||||||||

Total projects under development | 32,267 | — | 97,467 | 129,734 | ||||||||

Total projects under construction and development | 123,594 | 4,266 | 122,130 | 241,458 | ||||||||

Land inventory | — | — | 8,580 | 8,580 | ||||||||

Total mortgage debt and notes payable, nonrecourse | 3,790,918 | 278,655 | 2,371,447 | 5,883,710 | ||||||||

Revolving credit facility | — | — | — | — | ||||||||

Convertible senior debt | 700,000 | — | — | 700,000 | ||||||||

Construction payables | 110,108 | 26,866 | 34,557 | 117,799 | ||||||||

Operating accounts payable and accrued expenses | 561,689 | 23,245 | 162,154 | 700,598 | ||||||||

Accrued derivative liability | 102,362 | — | 7,755 | 110,117 | ||||||||

Total Accounts payable, accrued expenses and other liabilities | 774,159 | 50,111 | 204,466 | 928,514 | ||||||||

Cash distributions and losses in excess of investments in unconsolidated entities | 211,493 | (21,775 | ) | (211,486 | ) | 21,782 | ||||||

Deferred income taxes, net | 482,474 | — | — | 482,474 | ||||||||

Liabilities held for sale | 520,135 | 358,398 | — | 161,737 | ||||||||

Total Liabilities | 6,479,179 | 665,389 | 2,364,427 | 8,178,217 | ||||||||

Redeemable Noncontrolling Interest | 183,038 | 183,038 | — | — | ||||||||

Equity | ||||||||||||

Shareholders’ Equity | ||||||||||||

Shareholders’ equity before accumulated other comprehensive loss | 1,776,793 | — | — | 1,776,793 | ||||||||

Accumulated other comprehensive loss | (58,846 | ) | — | — | (58,846 | ) | ||||||

Total Shareholders’ Equity | 1,717,947 | — | — | 1,717,947 | ||||||||

Noncontrolling interest | 434,776 | 283,114 | — | 151,662 | ||||||||

Total Equity | 2,152,723 | 283,114 | — | 1,869,609 | ||||||||

Total Liabilities and Equity | $ | 8,814,940 | $ | 1,131,541 | $ | 2,364,427 | $ | 10,047,826 | ||||

10

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Statement of Operations – Three Months Ended December 31, 2015 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Plus Discontinued Operations | Pro-Rata Consolidation (Non-GAAP) | |||||||||||

(in thousands) | |||||||||||||||

Revenues | |||||||||||||||

Rental | $ | 167,916 | $ | 12,275 | $ | 57,588 | $ | — | $ | 213,229 | |||||

Tenant recoveries | 32,588 | 1,573 | 15,145 | — | 46,160 | ||||||||||

Service and management fees | 13,869 | 60 | 1,498 | — | 15,307 | ||||||||||

Parking and other | 18,732 | 780 | 4,893 | — | 22,845 | ||||||||||

Arena | — | — | — | 30,423 | 30,423 | ||||||||||

Land sales | 31,580 | 2,302 | 297 | — | 29,575 | ||||||||||

Subsidized Senior Housing | — | — | 12,230 | — | 12,230 | ||||||||||

Military Housing | 8,145 | — | 1,413 | — | 9,558 | ||||||||||

Total revenues | 272,830 | 16,990 | 93,064 | 30,423 | 379,327 | ||||||||||

Expenses | |||||||||||||||

Property operating and management | 100,748 | 5,092 | 25,011 | — | 120,667 | ||||||||||

Real estate taxes | 24,315 | 2,074 | 7,002 | — | 29,243 | ||||||||||

Ground rent | 1,972 | 80 | 3,351 | — | 5,243 | ||||||||||

Arena operating | — | — | — | 21,903 | 21,903 | ||||||||||

Cost of land sales | 15,697 | 695 | — | — | 15,002 | ||||||||||

Subsidized Senior Housing operating | — | — | 7,580 | — | 7,580 | ||||||||||

Military Housing operating | 1,841 | — | 719 | — | 2,560 | ||||||||||

Corporate general and administrative | 12,479 | — | — | — | 12,479 | ||||||||||

REIT conversion and reorganization costs | 22,627 | — | — | — | 22,627 | ||||||||||

179,679 | 7,941 | 43,663 | 21,903 | 237,304 | |||||||||||

Depreciation and amortization | 72,546 | 4,374 | 22,792 | 4,862 | 95,826 | ||||||||||

Write-offs of abandoned development projects | 3,756 | 116 | — | — | 3,640 | ||||||||||

Impairment of real estate | 25,971 | — | 12,460 | — | 38,431 | ||||||||||

Total expenses | 281,952 | 12,431 | 78,915 | 26,765 | 375,201 | ||||||||||

Operating income (loss) | (9,122 | ) | 4,559 | 14,149 | 3,658 | 4,126 | |||||||||

Interest and other income | 9,762 | 670 | 722 | — | 9,814 | ||||||||||

Net loss on change in control of interests | (1,405 | ) | — | — | — | (1,405 | ) | ||||||||

Interest expense | (37,481 | ) | (2,383 | ) | (22,079 | ) | (4,917 | ) | (62,094 | ) | |||||

Amortization of mortgage procurement costs | (1,793 | ) | (80 | ) | (802 | ) | (226 | ) | (2,741 | ) | |||||

Loss on extinguishment of debt | (3,133 | ) | — | — | — | (3,133 | ) | ||||||||

Earnings (loss) before income taxes | (43,172 | ) | 2,766 | (8,010 | ) | (1,485 | ) | (55,433 | ) | ||||||

Income tax expense (benefit) | |||||||||||||||

Current | (9,631 | ) | — | — | 919 | (8,712 | ) | ||||||||

Deferred | (595,886 | ) | — | — | (2,398 | ) | (598,284 | ) | |||||||

(605,517 | ) | — | — | (1,479 | ) | (606,996 | ) | ||||||||

Earnings (loss) from unconsolidated entities, gross of tax | (8,488 | ) | 46 | 8,010 | (2,325 | ) | (2,849 | ) | |||||||

Earnings (loss) from continuing operations | 553,857 | 2,812 | — | (2,331 | ) | 548,714 | |||||||||

Discontinued operations, net of tax | |||||||||||||||

Operating loss from rental properties | (3,058 | ) | (2,150 | ) | — | 908 | — | ||||||||

Equity in earnings (loss) | (1,423 | ) | — | — | 1,423 | — | |||||||||

(4,481 | ) | (2,150 | ) | — | 2,331 | — | |||||||||

Net earnings | 549,376 | 662 | — | — | 548,714 | ||||||||||

Noncontrolling interests | |||||||||||||||

Earnings from continuing operations attributable to noncontrolling interests, gross of tax | (2,812 | ) | (2,812 | ) | — | — | — | ||||||||

Loss from discontinued operations attributable to noncontrolling interests | 2,150 | 2,150 | — | — | — | ||||||||||

(662 | ) | (662 | ) | — | — | — | |||||||||

Net earnings attributable to Forest City Realty Trust, Inc. | $ | 548,714 | $ | — | $ | — | $ | — | $ | 548,714 | |||||

11

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Statement of Operations – Year Ended December 31, 2015 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Plus Discontinued Operations | Pro-Rata Consolidation (Non-GAAP) | |||||||||||

(in thousands) | |||||||||||||||

Revenues | |||||||||||||||

Rental | $ | 625,725 | $ | 46,623 | $ | 242,863 | $ | — | $ | 821,965 | |||||

Tenant recoveries | 133,829 | 7,354 | 66,211 | — | 192,686 | ||||||||||

Service and management fees | 45,263 | 207 | 6,646 | — | 51,702 | ||||||||||

Parking and other | 62,376 | 2,799 | 18,758 | — | 78,335 | ||||||||||

Arena | — | — | — | 74,598 | 74,598 | ||||||||||

Land sales | 79,169 | 6,998 | 1,780 | — | 73,951 | ||||||||||

Subsidized Senior Housing | — | — | 48,411 | — | 48,411 | ||||||||||

Military Housing | 31,869 | 1,655 | 5,614 | — | 35,828 | ||||||||||

Total revenues | 978,231 | 65,636 | 390,283 | 74,598 | 1,377,476 | ||||||||||

Expenses | |||||||||||||||

Property operating and management | 386,688 | 17,985 | 99,741 | — | 468,444 | ||||||||||

Real estate taxes | 91,274 | 7,035 | 31,376 | — | 115,615 | ||||||||||

Ground rent | 11,348 | 328 | 12,014 | — | 23,034 | ||||||||||

Arena operating | — | — | — | 52,655 | 52,655 | ||||||||||

Cost of land sales | 31,413 | 2,069 | — | — | 29,344 | ||||||||||

Subsidized Senior Housing operating | — | — | 30,570 | — | 30,570 | ||||||||||

Military Housing operating | 8,130 | 923 | 2,739 | — | 9,946 | ||||||||||

Corporate general and administrative | 48,374 | — | — | — | 48,374 | ||||||||||

REIT conversion and reorganization costs | 48,125 | — | — | — | 48,125 | ||||||||||

625,352 | 28,340 | 176,440 | 52,655 | 826,107 | |||||||||||

Depreciation and amortization | 252,925 | 16,069 | 85,345 | 20,104 | 342,305 | ||||||||||

Write-offs of abandoned development projects | 9,534 | 116 | 10,191 | — | 19,609 | ||||||||||

Impairment of real estate | 451,434 | — | 13,844 | — | 465,278 | ||||||||||

Total expenses | 1,339,245 | 44,525 | 285,820 | 72,759 | 1,653,299 | ||||||||||

Operating income (loss) | (361,014 | ) | 21,111 | 104,463 | 1,839 | (275,823 | ) | ||||||||

Interest and other income | 37,739 | 2,105 | 1,779 | — | 37,413 | ||||||||||

Net gain on disposition of full or partial interests in rental properties | 1,746 | — | 20,293 | — | 22,039 | ||||||||||

Net gain on change in control of interests | 486,279 | — | — | — | 486,279 | ||||||||||

Interest expense | (157,166 | ) | (9,158 | ) | (97,430 | ) | (18,861 | ) | (264,299 | ) | |||||

Amortization of mortgage procurement costs | (7,549 | ) | (285 | ) | (3,110 | ) | (226 | ) | (10,600 | ) | |||||

Loss on extinguishment of debt | (65,086 | ) | (719 | ) | (736 | ) | — | (65,103 | ) | ||||||

Earnings (loss) before income taxes | (65,051 | ) | 13,054 | 25,259 | (17,248 | ) | (70,094 | ) | |||||||

Income tax expense (benefit) | |||||||||||||||

Current | 7,187 | — | — | (5,849 | ) | 1,338 | |||||||||

Deferred | (588,286 | ) | — | — | (16,649 | ) | (604,935 | ) | |||||||

(581,099 | ) | — | — | (22,498 | ) | (603,597 | ) | ||||||||

Earnings (loss) from unconsolidated entities, gross of tax | 28,762 | 204 | (25,259 | ) | (40,760 | ) | (37,461 | ) | |||||||

Earnings (loss) from continuing operations | 544,810 | 13,258 | — | (35,510 | ) | 496,042 | |||||||||

Discontinued operations, net of tax | |||||||||||||||

Operating loss from rental properties | (27,520 | ) | (16,962 | ) | — | 10,558 | — | ||||||||

Equity in earnings (loss) | (24,952 | ) | — | — | 24,952 | — | |||||||||

(52,472 | ) | (16,962 | ) | — | 35,510 | — | |||||||||

Net earnings (loss) | 492,338 | (3,704 | ) | — | — | 496,042 | |||||||||

Noncontrolling interests | |||||||||||||||

Earnings from continuing operations attributable to noncontrolling interests, gross of tax | (13,258 | ) | (13,258 | ) | — | — | — | ||||||||

Loss from discontinued operations attributable to noncontrolling interests | 16,962 | 16,962 | — | — | — | ||||||||||

3,704 | 3,704 | — | — | — | |||||||||||

Net earnings attributable to Forest City Realty Trust, Inc. | $ | 496,042 | $ | — | $ | — | $ | — | $ | 496,042 | |||||

12

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Statement of Operations – Three Months Ended December 31, 2014 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Plus Discontinued Operations | Pro-Rata Consolidation (Non-GAAP) | |||||||||||

(in thousands) | |||||||||||||||

Revenues | |||||||||||||||

Rental | $ | 135,947 | $ | 5,098 | $ | 74,568 | $ | — | $ | 205,417 | |||||

Tenant recoveries | 28,889 | 1,784 | 16,017 | — | 43,122 | ||||||||||

Service and management fees | 14,469 | 228 | 2,049 | — | 16,290 | ||||||||||

Parking and other | 15,493 | (442 | ) | 5,590 | — | 21,525 | |||||||||

Arena | — | — | — | 17,497 | 17,497 | ||||||||||

Land sales | 17,735 | 1,574 | 149 | — | 16,310 | ||||||||||

Subsidized Senior Housing | — | — | 12,005 | — | 12,005 | ||||||||||

Military Housing | 7,875 | — | 1,384 | — | 9,259 | ||||||||||

Total revenues | 220,408 | 8,242 | 111,762 | 17,497 | 341,425 | ||||||||||

Expenses | |||||||||||||||

Property operating and management | 101,044 | 4,494 | 26,903 | — | 123,453 | ||||||||||

Real estate taxes | 19,192 | 971 | 9,015 | — | 27,236 | ||||||||||

Ground rent | 2,922 | 88 | 3,656 | — | 6,490 | ||||||||||

Arena operating | — | — | — | 11,690 | 11,690 | ||||||||||

Cost of land sales | 6,376 | 404 | — | — | 5,972 | ||||||||||

Subsidized Senior Housing operating | — | — | 7,880 | — | 7,880 | ||||||||||

Military Housing operating | 1,265 | — | 770 | — | 2,035 | ||||||||||

Corporate general and administrative | 10,036 | — | — | — | 10,036 | ||||||||||

REIT conversion and reorganization costs | 5,697 | — | — | — | 5,697 | ||||||||||

146,532 | 5,957 | 48,224 | 11,690 | 200,489 | |||||||||||

Depreciation and amortization | 52,328 | 1,600 | 24,419 | 4,985 | 80,132 | ||||||||||

Write-offs of abandoned development projects and demolition costs | 266 | — | — | — | 266 | ||||||||||

Impairment of real estate | 146,300 | 261 | 3,124 | — | 149,163 | ||||||||||

Total expenses | 345,426 | 7,818 | 75,767 | 16,675 | 430,050 | ||||||||||

Operating income (loss) | (125,018 | ) | 424 | 35,995 | 822 | (88,625 | ) | ||||||||

Interest and other income | 8,806 | 2,180 | 590 | — | 7,216 | ||||||||||

Net loss on disposition of partial interest in development project | (708 | ) | — | — | — | (708 | ) | ||||||||

Net gain on disposition of full or partial interests in rental properties | 30,894 | — | 2,346 | — | 33,240 | ||||||||||

Net gain on change in control of interests | 227,901 | — | — | — | 227,901 | ||||||||||

Interest expense | (45,360 | ) | (1,494 | ) | (28,432 | ) | (4,834 | ) | (77,132 | ) | |||||

Amortization of mortgage procurement costs | (2,066 | ) | (74 | ) | (820 | ) | (165 | ) | (2,977 | ) | |||||

Loss on extinguishment of debt | (252 | ) | (11 | ) | (3,759 | ) | — | (4,000 | ) | ||||||

Earnings (loss) before income taxes | 94,197 | 1,025 | 5,920 | (4,177 | ) | 94,915 | |||||||||

Income tax expense (benefit) | |||||||||||||||

Current | (2,625 | ) | — | — | (81 | ) | (2,706 | ) | |||||||

Deferred | 30,746 | — | — | (1,855 | ) | 28,891 | |||||||||

28,121 | — | — | (1,936 | ) | 26,185 | ||||||||||

Earnings (loss) from unconsolidated entities, gross of tax | 7,185 | (16 | ) | (5,920 | ) | (820 | ) | 461 | |||||||

Earnings (loss) from continuing operations | 73,261 | 1,009 | — | (3,061 | ) | 69,191 | |||||||||

Discontinued operations, net of tax | |||||||||||||||

Operating loss from rental properties | (6,264 | ) | (3,706 | ) | — | 2,558 | — | ||||||||

Equity in earnings (loss) | (503 | ) | — | — | 503 | — | |||||||||

(6,767 | ) | (3,706 | ) | — | 3,061 | — | |||||||||

Net earnings (loss) | 66,494 | (2,697 | ) | — | — | 69,191 | |||||||||

Noncontrolling interests | |||||||||||||||

Earnings from continuing operations attributable to noncontrolling interests, gross of tax | (1,009 | ) | (1,009 | ) | — | — | — | ||||||||

Loss from discontinued operations attributable to noncontrolling interests | 3,706 | 3,706 | — | — | — | ||||||||||

2,697 | 2,697 | — | — | — | |||||||||||

Net earnings attributable to Forest City Realty Trust, Inc. | $ | 69,191 | $ | — | $ | — | $ | — | $ | 69,191 | |||||

13

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Consolidated Statement of Operations – Year Ended December 31, 2014 (Unaudited)

Full Consolidation (GAAP) | Less Noncontrolling Interest | Plus Unconsolidated Investments at Pro-Rata | Plus Discontinued Operations | Pro-Rata Consolidation (Non-GAAP) | |||||||||||

(in thousands) | |||||||||||||||

Revenues | |||||||||||||||

Rental | $ | 526,966 | $ | 16,189 | $ | 284,597 | $ | 4,015 | $ | 799,389 | |||||

Tenant recoveries | 118,035 | 7,018 | 71,547 | 1,377 | 183,941 | ||||||||||

Service and management fees | 50,522 | 323 | 7,456 | — | 57,655 | ||||||||||

Parking and other | 53,765 | 358 | 22,232 | 36 | 75,675 | ||||||||||

Arena | — | — | — | 64,045 | 64,045 | ||||||||||

Land sales | 68,102 | 6,548 | 2,837 | 1,601 | 65,992 | ||||||||||

Subsidized Senior Housing | — | — | 47,077 | — | 47,077 | ||||||||||

Military Housing | 31,967 | 1,358 | 5,605 | — | 36,214 | ||||||||||

Total revenues | 849,357 | 31,794 | 441,351 | 71,074 | 1,329,988 | ||||||||||

Expenses | |||||||||||||||

Property operating and management | 384,119 | 10,612 | 110,130 | 2,539 | 486,176 | ||||||||||

Real estate taxes | 78,637 | 3,375 | 36,871 | (667 | ) | 111,466 | |||||||||

Ground rent | 9,387 | 358 | 13,686 | — | 22,715 | ||||||||||

Arena operating | — | — | — | 42,284 | 42,284 | ||||||||||

Cost of land sales | 23,457 | 1,928 | 990 | 1,142 | 23,661 | ||||||||||

Subsidized Senior Housing operating | — | — | 30,822 | — | 30,822 | ||||||||||

Military Housing operating | 11,481 | 1,311 | 3,071 | — | 13,241 | ||||||||||

Corporate general and administrative | 45,419 | — | — | — | 45,419 | ||||||||||

REIT conversion and reorganization costs | 5,697 | — | — | — | 5,697 | ||||||||||

558,197 | 17,584 | 195,570 | 45,298 | 781,481 | |||||||||||

Depreciation and amortization | 196,167 | 4,828 | 88,923 | 20,948 | 301,210 | ||||||||||

Write-offs of abandoned development projects and demolition costs | 1,655 | — | — | — | 1,655 | ||||||||||

Impairment of real estate | 277,095 | 261 | 3,124 | — | 279,958 | ||||||||||

Total expenses | 1,033,114 | 22,673 | 287,617 | 66,246 | 1,364,304 | ||||||||||

Operating income (loss) | (183,757 | ) | 9,121 | 153,734 | 4,828 | (34,316 | ) | ||||||||

Interest and other income | 42,780 | 3,681 | 883 | — | 39,982 | ||||||||||

Net loss on disposition of partial interest in development project | (20,298 | ) | (3,379 | ) | — | — | (16,919 | ) | |||||||

Net gain on disposition of full or partial interests in rental properties | 30,281 | 27 | 52,421 | 28,042 | 110,717 | ||||||||||

Net gain on change in control of interests | 230,660 | — | — | — | 230,660 | ||||||||||

Interest expense | (194,176 | ) | (5,649 | ) | (110,195 | ) | (24,647 | ) | (323,369 | ) | |||||

Amortization of mortgage procurement costs | (7,797 | ) | (211 | ) | (3,217 | ) | (286 | ) | (11,089 | ) | |||||

Loss on extinguishment of debt | (1,179 | ) | (48 | ) | (3,743 | ) | (448 | ) | (5,322 | ) | |||||

Earnings (loss) before income taxes | (103,486 | ) | 3,542 | 89,883 | 7,489 | (9,656 | ) | ||||||||

Income tax expense (benefit) | |||||||||||||||

Current | 12,515 | — | — | (2,554 | ) | 9,961 | |||||||||

Deferred | (21,670 | ) | — | — | 6,595 | (15,075 | ) | ||||||||

(9,155 | ) | — | — | 4,041 | (5,114 | ) | |||||||||

Earnings (loss) from unconsolidated entities, gross of tax | 90,089 | 78 | (89,883 | ) | (3,181 | ) | (3,053 | ) | |||||||

Earnings (loss) from continuing operations | (4,242 | ) | 3,620 | — | 267 | (7,595 | ) | ||||||||

Discontinued operations, net of tax | |||||||||||||||

Operating loss from rental properties | (29,686 | ) | (17,103 | ) | — | 12,583 | — | ||||||||

Gain on disposition of rental properties | 14,856 | 58 | — | (14,798 | ) | — | |||||||||

Equity in earnings (loss) | (1,948 | ) | — | — | 1,948 | — | |||||||||

(16,778 | ) | (17,045 | ) | — | (267 | ) | — | ||||||||

Net loss | (21,020 | ) | (13,425 | ) | — | — | (7,595 | ) | |||||||

Noncontrolling interests | |||||||||||||||

Earnings from continuing operations attributable to noncontrolling interests, gross of tax | (3,620 | ) | (3,620 | ) | — | — | — | ||||||||

Loss from discontinued operations attributable to noncontrolling interests | 17,045 | 17,045 | — | — | — | ||||||||||

13,425 | 13,425 | — | — | — | |||||||||||

Net loss attributable to Forest City Realty Trust, Inc. | $ | (7,595 | ) | $ | — | $ | — | $ | — | $ | (7,595 | ) | |||

14

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Net Asset Value Components – December 31, 2015

The following represents components of our business relevant to calculate Net Asset Value (“NAV”), a non-GAAP measure. There is no directly comparable GAAP financial measure to NAV. We consider NAV to be a useful supplemental measure which assists both management and investors to estimate the fair value of our Company. The calculation of NAV involves significant estimates and can be calculated using various methods. Each individual investor must determine the specific methodology, assumptions and estimates to use to arrive at an estimated NAV of the Company.

The components of NAV do not consider the potential changes in rental and fee income streams or development platform. The components include non-GAAP financial measures, such as NOI and information related to our rental properties business prepared using the pro-rata consolidation method. Although these measures are not presented in accordance with GAAP, investors can use these non-GAAP measures as supplementary information to evaluate our business. The non-GAAP measures presented are not intended to be performance measures that should be regarded as alternatives to, or more meaningful than, our GAAP measures.

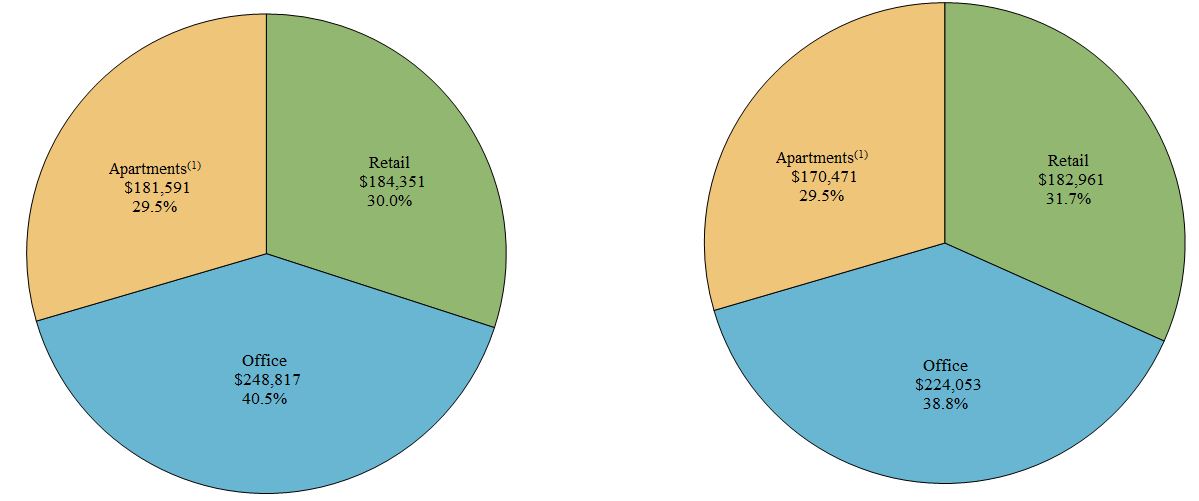

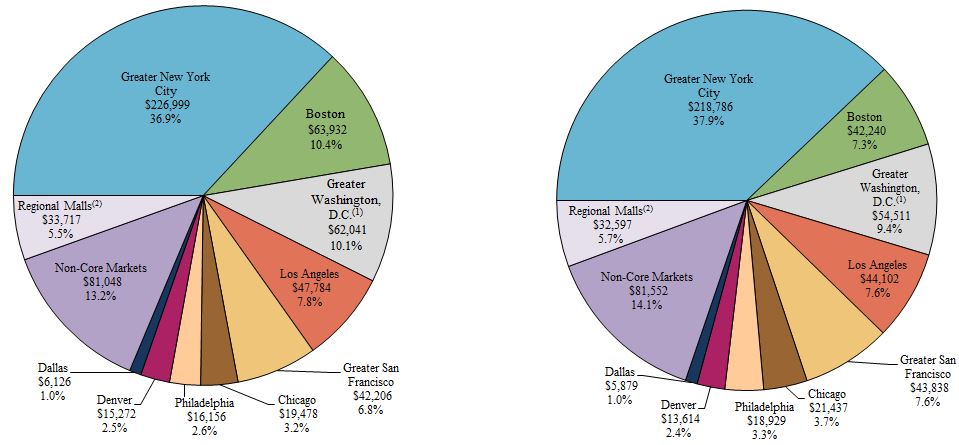

Net Asset Value Components - December 31, 2015 | |||||||||||||||||||

Completed Rental Properties | |||||||||||||||||||

Q4 2015 | Net Stabilized | Stabilized | Annualized | Nonrecourse | |||||||||||||||

(Dollars in millions at pro-rata) | NOI (1) | Adjustments (2) | NOI | Stabilized NOI (3) | Debt (4) | ||||||||||||||

Commercial Real Estate | A | B | =A+B | ||||||||||||||||

Retail | |||||||||||||||||||

Regional Malls | $ | 33.5 | $ | (3.2 | ) | $ | 30.3 | $ | 121.2 | $ | (1,184.7 | ) | |||||||

Specialty Retail Centers | 14.1 | 0.6 | 14.7 | 58.8 | (516.4 | ) | |||||||||||||

Subtotal Retail | $ | 47.6 | $ | (2.6 | ) | $ | 45.0 | $ | 180.0 | $ | (1,701.1 | ) | |||||||

Office | |||||||||||||||||||

Life Science | $ | 22.3 | $ | 0.4 | $ | 22.7 | $ | 90.8 | $ | (604.2 | ) | ||||||||

New York | 35.1 | 1.2 | 36.3 | 145.2 | (1,068.0 | ) | |||||||||||||

Central Business District | 4.5 | (0.2 | ) | 4.3 | 17.2 | (57.3 | ) | ||||||||||||

Suburban/Other | 3.8 | — | 3.8 | 15.2 | (102.4 | ) | |||||||||||||

Subtotal Office | $ | 65.7 | $ | 1.4 | $ | 67.1 | $ | 268.4 | $ | (1,831.9 | ) | ||||||||

Arena | $ | 8.5 | $ | (8.5 | ) | $ | — | $ | — | $ | — | ||||||||

Residential Real Estate | |||||||||||||||||||

Apartments, Core Markets | $ | 31.0 | $ | 3.0 | $ | 34.0 | $ | 136.0 | $ | (1,372.3 | ) | ||||||||

Apartments, Non-Core Markets (5) | 10.2 | 0.9 | 11.1 | 44.4 | (348.5 | ) | |||||||||||||

Subsidized Senior Housing | 4.7 | (0.3 | ) | 4.4 | 17.8 | (139.2 | ) | ||||||||||||

Military Housing | 7.0 | (2.7 | ) | 4.3 | 17.0 | (28.5 | ) | ||||||||||||

Subtotal Residential | $ | 52.9 | $ | 0.9 | $ | 53.8 | $ | 215.2 | $ | (1,888.5 | ) | ||||||||

Subtotal | $ | 174.7 | $ | (8.8 | ) | $ | 165.9 | $ | 663.6 | $ | (5,421.5 | ) | |||||||

Other | (12.3 | ) | 3.5 | (8.8 | ) | (35.0 | ) | — | |||||||||||

Grand Total | $ | 162.4 | $ | (5.3 | ) | $ | 157.1 | $ | 628.6 | $ | (5,421.5 | ) | |||||||

Development Pipeline | Book Value (4) | ||||||||||||||||||

Projects under construction | $ | 527.2 | $ | (111.0 | ) | ||||||||||||||

Projects under development | $ | 509.0 | $ | (185.7 | ) | ||||||||||||||

Land inventory | $ | 72.9 | $ | (8.6 | ) | ||||||||||||||

Other Tangible Assets | |||||||||||||||||||

Cash and equivalents | $ | 309.9 | |||||||||||||||||

Restricted cash | $ | 273.6 | |||||||||||||||||

Notes and accounts receivable, net (6) | $ | 423.1 | |||||||||||||||||

Net investments and advances to unconsolidated entities | $ | 106.8 | |||||||||||||||||

Prepaid expenses and other deferred costs, net | $ | 119.2 | |||||||||||||||||

Net proceeds from assets held for sale and Westchester's Ridge Hill (7) | $ | 506.7 | |||||||||||||||||

Recourse Debt and Other Liabilities | |||||||||||||||||||

Revolving credit facility | $ | — | |||||||||||||||||

Convertible senior debt | $ | (271.0 | ) | ||||||||||||||||

Less: convertible debt | $ | 271.0 | |||||||||||||||||

Construction payables | $ | (142.8 | ) | ||||||||||||||||

Operating accounts payable and accrued expenses (8) | $ | (752.7 | ) | ||||||||||||||||

Share Data (in millions) | |||||||||||||||||||

Diluted weighted average number of shares for the three months ended December 31, 2015 | 273.6 | ||||||||||||||||||

15

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Net Asset Value Components – December 31, 2015 (continued)

(1) | Q4 2015 NOI is reconciled to NOI at full consolidation by Product Group for the three months ended December 31, 2015 in the Supplemental Operating Information section of this supplemental package. |

(2) | The net stabilized adjustments column represents net adjustments assumed to arrive at an estimated annualized stabilized NOI for properties currently in initial lease-up periods, net of the removal of partial period NOI for recently sold properties. The following properties are currently in their initial lease-up periods: |

Cost at 100% | Cost at Pro-Rata Share | Lease Commitment % as of | |||||

Property | February 16, 2016 | ||||||

(in millions) | |||||||

Apartments: | |||||||

Winchester Lofts (Non-Core Market) | $ | 62.8 | $ | 62.8 | 92% | ||

Aster Town Center North (Core Market) | $ | 23.4 | $ | 21.1 | 43% | ||

a) | NOI for the apartments in the above table is reflected at 5% of the pro-rata cost. This assumption does not reflect our anticipated NOI, but rather is used in order to establish a hypothetical basis for an estimated valuation of leased-up properties. |

b) | On January 29, 2016, through our investment in Nets Sports and Entertainment, LLC sold our 55% ownership interest in the Arena and 20% ownership interest in the Nets, collectively (the “Disposal Group”), to Onexim Sports and Entertainment Holdings USA, Inc. As a result, we removed partial period NOI for the Arena. |

In addition, we include stabilization adjustments to the Q4 2015 NOI as follows:

c) | On January 29, 2016, we closed on the creation of a joint venture with QIC, in which QIC acquired 51% of our equity ownership of Westchester’s Ridge Hill. Due to the ongoing lease up at Westchester’s Ridge Hill (Regional Mall), we have included a stabilization adjustment to the Q4 2015 NOI to arrive at our 2016 estimate of annualized stabilized NOI following the disposition of our partial interest. |

d) | Due to quarterly fluctuations in our regional malls, primarily due to seasonality, we have included a stabilization adjustment of $1.5 million to reduce Q4 2015 NOI. |

e) | Due to a temporary decline in occupancy at 88 Sidney Street (Life Science), we have included a stabilization adjustment to the Q4 2015 NOI to arrive at our estimate of stabilized NOI. |

f) | Due to planned renovations at Ballston Quarter (Regional Mall), we have included a stabilization adjustment to the Q4 2015 NOI to arrive at our estimate of stabilized NOI. |

g) | Due to quarterly fluctuations of NOI as a result of distribution restrictions from our limited-distribution subsidized senior housing properties, we have included a stabilization adjustment to the Q4 2015 NOI to arrive at our estimate of stabilized NOI. Our updated estimate of stabilized NOI is based on the 2015 annual NOI of $17.8 million. |

h) | At the conclusion of the initial development period at each of our military housing communities, we estimate the ongoing property and asset management fees, net of operating expenses, to be $17.0 million. |

i) | Other excludes participation payments of $1.0 million and certain variable development and operating overhead. |

The net stabilized adjustments are not comparable to any GAAP measure and therefore do not have a reconciliation to the nearest comparable GAAP measure.

(3) | Pro-rata annualized stabilized NOI is calculated by taking the Q4 2015 stabilized NOI times a multiple of four. |

(4) | Amounts are derived from the respective pro-rata balance sheet line item as of December 31, 2015 and are reconciled to their GAAP equivalents in the Selected Financial Information section of this supplemental package. Due to the disposition of our partial interest in Westchester’s Ridge Hill to QIC, we have removed nonrecourse debt of $169.4 million attributable to this property. Assets and liabilities held for sale for the Disposal Group are excluded from each pro-rata balance sheet line item. |

(5) | Includes NOI of $0.4 million ($1.6 million annualized) and nonrecourse debt of $10.4 million related to 3 consolidated properties included in a master purchase and sale agreement for the sale of 47 (44 unconsolidated investments, included in “Subsidized Senior Housing” and 3 consolidated properties, included in “Apartments, Non-Core Markets”) federally assisted housing apartment communities. |

(6) | Includes $159.7 million of straight-line rent receivable (net of $10.8 million of allowance for doubtful accounts). |

16

Forest City Realty Trust, Inc. and Subsidiaries

Selected Financial Information

Net Asset Value Components – December 31, 2015 (continued)

(7) | Subsequent to December 31, 2015, we sold our ownership interest in the Arena, the Nets and a development opportunity, comprised of land at 625 Fulton Avenue, in Brooklyn, New York. These represent assets and liabilities held for sale on our consolidated balance sheet. Net proceeds from assets held for sale and the partial disposition in Westchester’s Ridge Hill to QIC are as follows: |

Net Proceeds | Note Receivable Maturity Date | |||

(in millions) | ||||

Arena: | ||||

Net Cash Proceeds | $ | 54.0 | ||

Note Receivable | 92.6 | January 29, 2019 | ||

146.6 | ||||

625 Fulton Avenue - Land: | ||||

Net Cash Proceeds | 94.0 | |||

Note Receivable | 58.0 | April 12, 2016 | ||

152.0 | ||||

Nets - Note Receivable | 125.1 | January 29, 2021 | ||

Westchester’s Ridge Hill - Net Cash Proceeds | 83.0 | |||

$ | 506.7 | |||

(8) | Includes $60.4 million of straight-line rent payable. |

Net Asset Value Components - Stabilized NOI - Q3 2015 vs. Q4 2015

The following represents the quarterly change in stabilized NOI used to estimate NAV, as a result of recent property openings, acquisitions or sales, as well as other portfolio changes. GAAP reconciliations for beginning period can be found in prior supplemental packages furnished with the SEC and are available on our website at www.forestcity.net.

Net Asset Value Components - Stabilized NOI | |||||||||||||||||||||||

Stabilized Adjustments | |||||||||||||||||||||||

Q3 2015 | Property | Property | Property | Portfolio | Q4 2015 | ||||||||||||||||||

(Dollars in millions at pro-rata) | Stabilized NOI | Openings | Acquisitions | Sales | NOI Changes | Stabilized NOI | |||||||||||||||||

Commercial Real Estate | |||||||||||||||||||||||

Retail | |||||||||||||||||||||||

Regional Malls | $ | 35.1 | $ | — | $ | — | $ | (5.6 | ) | $ | 0.8 | $ | 30.3 | ||||||||||

Specialty Retail Centers | 14.3 | — | — | — | 0.4 | 14.7 | |||||||||||||||||

Subtotal Retail | $ | 49.4 | $ | — | $ | — | $ | (5.6 | ) | $ | 1.2 | $ | 45.0 | ||||||||||

Office | |||||||||||||||||||||||

Life Science | $ | 23.1 | $ | — | $ | — | $ | — | $ | (0.4 | ) | $ | 22.7 | ||||||||||

New York | 35.4 | — | — | — | 0.9 | 36.3 | |||||||||||||||||

Central Business District | 4.0 | — | — | — | 0.3 | 4.3 | |||||||||||||||||

Suburban/Other | 3.6 | — | — | — | 0.2 | 3.8 | |||||||||||||||||

Subtotal Office | $ | 66.1 | $ | — | $ | — | $ | — | $ | 1.0 | $ | 67.1 | |||||||||||

Arena | $ | 7.6 | $ | — | $ | — | $ | (7.6 | ) | $ | — | $ | — | ||||||||||

Residential Real Estate | |||||||||||||||||||||||

Apartments, Core Markets | $ | 33.9 | $ | 0.3 | $ | — | $ | — | $ | (0.2 | ) | $ | 34.0 | ||||||||||

Apartments, Non-Core Markets | 11.6 | — | — | — | (0.5 | ) | 11.1 | ||||||||||||||||

Subsidized Senior Housing | 4.1 | — | — | — | 0.3 | 4.4 | |||||||||||||||||

Military Housing | 4.3 | — | — | — | — | 4.3 | |||||||||||||||||

Subtotal Residential | $ | 53.9 | $ | 0.3 | $ | — | $ | — | $ | (0.4 | ) | $ | 53.8 | ||||||||||

Subtotal | $ | 177.0 | $ | 0.3 | $ | — | $ | (13.2 | ) | $ | 1.8 | $ | 165.9 | ||||||||||

Other | (8.8 | ) | — | — | — | — | (8.8 | ) | |||||||||||||||

Grand Total | $ | 168.2 | $ | 0.3 | $ | — | $ | (13.2 | ) | $ | 1.8 | $ | 157.1 | ||||||||||

17

(THIS PAGE INTENTIONALLY LEFT BLANK)

18

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Operating Information

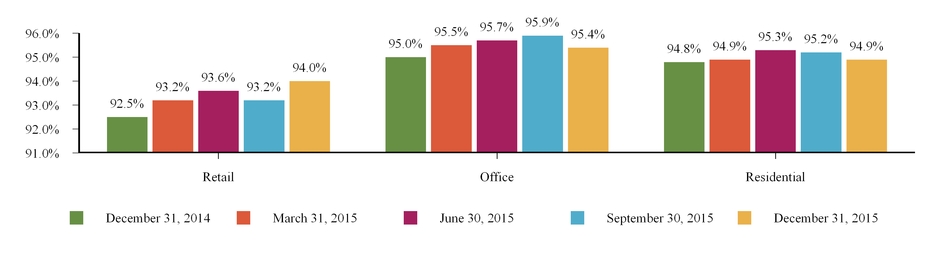

Occupancy Data

Retail and office occupancy data represents leased occupancy at the end of the quarter. Leased occupancy percentage is calculated by dividing the sum of the total tenant occupied space under the lease and vacant space under lease by gross leasable area (“GLA”). Occupancy data includes leases with original terms of one year or less.

Leased Occupancy | ||

As of December 31, | ||

Retail | 2015 | 2014 |

Comparable | 94.0% | 92.5% |

Total | 93.7% | 92.3% |

Office | ||

Comparable | 95.4% | 94.9% |

Total | 94.4% | 94.4% |

Residential occupancy data represents economic occupancy, which is calculated by dividing the period-to-date gross potential rent less vacancy by gross potential rent. Residential occupancy data excludes military and limited-distribution subsidized senior housing units.

Economic Occupancy | ||

Years Ended December 31, | ||

Residential | 2015 | 2014 |

Comparable | 94.9% | 94.9% |

Total | 93.7% | 92.2% |

The graph below provides comparable leased and economic occupancy data as reported in previous quarters. Prior period amounts may differ from above since the properties qualifying as comparable change from period to period.

Comparable Occupancy Percentage Trend

19

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Operating Information

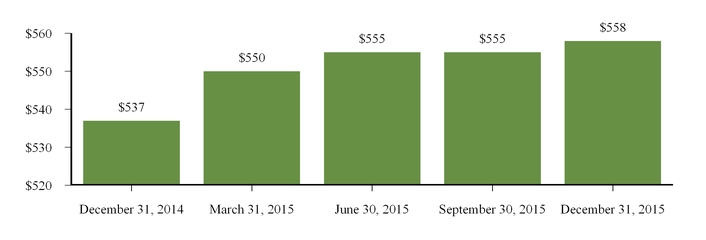

Retail Sales Data

The following provides retail sales data for small shop inline tenants at our regional malls. We believe this data allows investors to better understand the productivity of our small shop inline tenants.

The graph below represents regional mall sales for tenants that were open and operating for the duration of each rolling 12-month period presented. Those tenants that have begun and/or ceased operations in the rolling 12-month periods shown are not included.

FCE Regional Mall Sales per Square Foot (1)

Rolling 12-month basis for periods presented

(1) | All sales data is derived from schedules provided by our tenants and is not subject to the same internal control and verification procedures applied to other data supplied in this supplemental package. |

20

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Operating Information

Leasing Summary

Retail Centers

The following tables represent those new leases and GLA signed and rent per square foot (“SF”) on the same space in which there was a former tenant and existing tenant renewals.

Regional Malls

Quarter | Number of Leases Signed | GLA Signed | Contractual Rent Per SF (1) | Expired Rent Per SF (1) | Cash Basis % Change over Prior Rent | ||||||||||||

Q1 2015 | 34 | 169,951 | $ | 46.51 | $ | 36.92 | 26.0 | % | |||||||||

Q2 2015 | 21 | 48,967 | $ | 63.79 | $ | 49.62 | 28.6 | % | |||||||||

Q3 2015 | 38 | 174,228 | $ | 46.82 | $ | 37.55 | 24.7 | % | |||||||||

Q4 2015 | 23 | 81,251 | $ | 51.34 | $ | 39.91 | 28.6 | % | |||||||||

Total | 116 | 474,397 | $ | 49.23 | $ | 38.98 | 26.3 | % | |||||||||

Specialty Retail Centers

Quarter | Number of Leases Signed | GLA Signed | Contractual Rent Per SF (1) | Expired Rent Per SF (1) | Cash Basis % Change over Prior Rent | ||||||||||||

Q1 2015 | 11 | 40,421 | $ | 34.55 | $ | 35.41 | (2.4 | )% | |||||||||

Q2 2015 | 7 | 42,562 | $ | 31.74 | $ | 29.95 | 6.0 | % | |||||||||

Q3 2015 | 3 | 45,814 | $ | 36.81 | $ | 33.78 | 9.0 | % | |||||||||

Q4 2015 | 2 | 2,334 | $ | 39.61 | $ | 27.51 | 44.0 | % | |||||||||

Total | 23 | 131,131 | $ | 34.52 | $ | 32.92 | 4.9 | % | |||||||||

Office Buildings

The following table represents those new leases and GLA signed on the same space in which there was a former tenant and existing tenant renewals along with all other new leases signed within the rolling 12-month period.

Same-Space Leases | Other New Leases | ||||||||||||||||||||||

Quarter | Number of Leases Signed | GLA Signed | Contractual Rent Per SF (1) | Expired Rent Per SF (1) | Cash Basis % Change over Prior Rent | Number of Leases Signed | GLA Signed | Contractual Rent Per SF (1) | Total GLA Signed | ||||||||||||||

Q1 2015 | 18 | 75,460 | $ | 22.49 | $ | 21.40 | 5.1 | % | 2 | 8,196 | $ | 21.94 | 83,656 | ||||||||||

Q2 2015 | 24 | 223,312 | $ | 33.34 | $ | 31.82 | 4.8 | % | 4 | 4,696 | $ | 20.89 | 228,008 | ||||||||||

Q3 2015 | 12 | 168,622 | $ | 69.08 | $ | 68.50 | 0.8 | % | 2 | 5,582 | $ | 17.18 | 174,204 | ||||||||||

Q4 2015 | 25 | 156,299 | $ | 19.90 | $ | 19.85 | 0.3 | % | 5 | 6,023 | $ | 17.28 | 162,322 | ||||||||||

Total | 79 | 623,693 | $ | 38.32 | $ | 37.48 | 2.2 | % | 13 | 24,497 | $ | 19.51 | 648,190 | ||||||||||

(1) | Retail and Office contractual rent per square foot includes base rent and fixed additional charges for common area maintenance and real estate taxes as of rental commencement. Retail contractual rent per square foot also includes fixed additional marketing/promotional charges. For all expiring leases, contractual rent per square foot includes any applicable escalations. |

21

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Operating Information

Apartment Communities

The following tables present leasing information of our apartment communities. Prior period amounts may differ from data as reported in previous quarters since the properties that qualify as comparable change from period to period.

Quarterly Comparison

Monthly Average Residential Rental Rates (2) | Economic Residential Occupancy | |||||||||||||||||

Comparable Apartment | Leasable Units | Three Months Ended December 31, | Three Months Ended December 31, | |||||||||||||||

Communities (1) | at Pro-Rata % (3) | 2015 | 2014 | % Change | 2015 | 2014 | % Change | |||||||||||

Core Markets | 8,170 | $ | 1,931 | $ | 1,859 | 3.9 | % | 95.1 | % | 95.5 | % | (0.4 | )% | |||||

Non-Core Markets | 7,529 | $ | 921 | $ | 890 | 3.5 | % | 91.4 | % | 94.0 | % | (2.6 | )% | |||||

Total Comparable Apartments | 15,699 | $ | 1,446 | $ | 1,394 | 3.7 | % | 94.0 | % | 95.1 | % | (1.1 | )% | |||||

Year-to-Date Comparison

Monthly Average Residential Rental Rates (2) | Economic Residential Occupancy | |||||||||||||||||

Comparable Apartment | Leasable Units | Years Ended December 31, | Years Ended December 31, | |||||||||||||||

Communities (1) | at Pro-Rata % (3) | 2015 | 2014 | % Change | 2015 | 2014 | % Change | |||||||||||

Core Markets | 7,967 | $ | 1,912 | $ | 1,852 | 3.2 | % | 95.5 | % | 95.5 | % | — | ||||||

Non-Core Markets | 7,401 | $ | 897 | $ | 873 | 2.7 | % | 93.4 | % | 93.4 | % | — | ||||||

Total Comparable Apartments | 15,368 | $ | 1,423 | $ | 1,380 | 3.1 | % | 94.9 | % | 94.9 | % | — | ||||||

Sequential Comparison

Monthly Average Residential Rental Rates (2) | Economic Residential Occupancy | |||||||||||||||||

Three Months Ended | Three Months Ended | |||||||||||||||||

Comparable Apartment | Leasable Units | December 31, | September 30, | December 31, | September 30, | |||||||||||||

Communities (1) | at Pro-Rata % (3) | 2015 | 2015 | % Change | 2015 | 2015 | % Change | |||||||||||

Core Markets | 8,924 | $ | 1,958 | $ | 1,935 | 1.2 | % | 94.7 | % | 95.6 | % | (0.9 | )% | |||||

Non-Core Markets | 8,549 | $ | 932 | $ | 928 | 0.4 | % | 91.9 | % | 93.9 | % | (2.0 | )% | |||||

Total Comparable Apartments | 17,473 | $ | 1,456 | $ | 1,443 | 0.9 | % | 93.9 | % | 95.0 | % | (1.1 | )% | |||||

(1) | Includes stabilized apartment communities completely opened and operated in the periods presented. These apartment communities include units leased at affordable apartment rates which provide a discount from average market rental rates. For the three months ended December 31, 2015, 17.1% of leasable units in core markets and 4.2% of leasable units in non-core markets were affordable housing units. Excludes all military and limited-distribution subsidized senior housing units. |

(2) | Represents gross potential rent less concessions. |

(3) | Leasable units at pro-rata represent our share of comparable leasable units at the apartment community. |

22

(THIS PAGE INTENTIONALLY LEFT BLANK)

23

Forest City Realty Trust, Inc. and Subsidiaries

Supplemental Operating Information

Comparable NOI - Pro-Rata

Three Months Ended | Year Ended | ||||

December 31, 2015 | December 31, 2015 | ||||

Retail | 4.2 | % | 5.1 | % | |

Office | 7.6 | % | 4.9 | % | |

Apartments | 5.6 | % | 4.7 | % | |

Total | 5.9 | % | 4.9 | % | |

The tables below provide the percentage change of Comparable NOI as reported in previous quarters. GAAP reconciliations for previous periods can be found in prior supplemental packages furnished with the SEC and are available on our website at www.forestcity.net.

Quarterly Historical Trends | Annual Historical Trends | |||||||||||||||||||||||||

Three Months Ended | Year Ended | Year Ended | 11 Months Ended | |||||||||||||||||||||||