Attached files

| file | filename |

|---|---|

| EX-21.1 - EXHIBIT 21.1 - Columbia Pipeline Group, Inc. | cpgx-20151231xex211.htm |

| EX-32.1 - EXHIBIT 32.1 - Columbia Pipeline Group, Inc. | cpgx-20151231xex321.htm |

| EX-32.2 - EXHIBIT 32.2 - Columbia Pipeline Group, Inc. | cpgx-20151231xex322.htm |

| EX-12.1 - EXHIBIT 12.1 - Columbia Pipeline Group, Inc. | cpgx-20151231xex121.htm |

| EX-31.1 - EXHIBIT 31.1 - Columbia Pipeline Group, Inc. | cpgx-20151231xex311.htm |

| EX-23.1 - EXHIBIT 23.1 - Columbia Pipeline Group, Inc. | cpgx-20151231xex231.htm |

| EX-31.2 - EXHIBIT 31.2 - Columbia Pipeline Group, Inc. | cpgx-20151231xex312.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) | ||

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-36838

Columbia Pipeline Group, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 47-1982552 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

5151 San Felipe St., Suite 2500 Houston, Texas | 77056 | |

(Address of principal executive offices) | (Zip Code) | |

(713) 386-3701

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |||

Common stock, par value $0.01 | New York Stock Exchange | |||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12-b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | |

Non-accelerated filer ¨ | Smaller reporting company ¨ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

As of June 30, 2015, there was no public market for the registrant's common stock.

There were 399,841,350 shares of Common Stock, $0.01 Par Value outstanding as of February 10, 2016.

Documents Incorporated by Reference

Part III of this report incorporates by reference specific portions of the Registrant’s Notice of Annual Meeting and Proxy Statement relating to the Annual Meeting of Stockholders to be held on May 10, 2016.

CONTENTS

Page No. | ||

Items 1 and 2. | ||

Item 1A. | ||

Item 1B. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

2

DEFINED TERMS The following is a list of frequently used abbreviations or acronyms that are found in this report: | |

Affiliates and Subsidiaries of Columbia Pipeline Group, Inc. | |

CEG | Columbia Energy Group |

CEVCO | Columbia Energy Ventures, LLC |

CNS Microwave | CNS Microwave, LLC |

Columbia Gas Transmission | Columbia Gas Transmission, LLC |

Columbia Gulf | Columbia Gulf Transmission, LLC |

Columbia Midstream | Columbia Midstream Group, LLC |

Columbia OpCo | CPG OpCo LP |

Columbia Remainder Corporation | Columbia Remainder Corporation |

CPGSC | Columbia Pipeline Group Services Company |

CPP GP LLC | CPP GP LLC |

CPPL | Columbia Pipeline Partners LP |

Crossroads | Crossroads Pipeline Company |

Hardy Storage | Hardy Storage Company, LLC |

Millennium Pipeline | Millennium Pipeline Company, L.L.C. |

OpCo GP | CPG OpCo GP LLC |

Pennant | Pennant Midstream, LLC |

Abbreviations and Definitions | |

Adjusted EBITDA | A supplemental non-GAAP financial measure defined by us as net income before interest expense, income taxes, and depreciation and amortization, plus distributions of earnings received from equity investees and one-time transaction costs, less equity earnings in unconsolidated affiliates and other, net. |

AFUDC | Allowance for funds used during construction, is the method prescribed by the FERC for inclusion in our tariff rates as reimbursement for the cost of financing construction projects with investor capital and borrowed funds until a project is placed into operation |

AOC | Administrative Order by Consent |

AOCI | Accumulated Other Comprehensive Income (Loss) |

ASC | Accounting Standards Codification |

ASU | Accounting Standards Update |

Btu | British Thermal Unit |

CAA | Clean Air Act |

CCRM | Capital Cost Recovery Mechanism |

condensate | A natural gas liquid with a low vapor pressure, mainly composed of propane, butane, pentane and heavier hydrocarbon functions |

DOT | Department of Transportation |

Dth/d | Dekatherms per day |

EIA | U.S. Energy Information Administration |

end-user markets | The ultimate users and consumers of transported energy products |

EPA | United States Environmental Protection Agency |

EPS | Earnings per share |

FASB | Financial Accounting Standards Board |

FERC | Federal Energy Regulatory Commission |

3

DEFINED TERMS (continued) | |

GAAP | Generally Accepted Accounting Principles |

Hilcorp | Hilcorp Energy Company |

HP | Horsepower |

IPO | Initial public offering of Columbia Pipeline Partners LP, which was completed on February 11, 2015 |

LDC | Local distribution companies are involved in the delivery of natural gas to consumers within a specific geographic area |

LNG | Natural gas that has been cooled to minus 161 degrees Celsius for transportation, typically by ship. The cooling process reduces the volume of natural gas by 600 times |

MMBtu | One million British Thermal Units |

MMDth | One million Dekatherms |

MMDth/d | One million Dekatherms per day |

NAAQS | National Ambient Air Quality Standards |

NGA | Natural Gas Act of 1938 |

NGL | Hydrocarbons in natural gas that are separated from the natural gas as liquids through the process of absorption, condensation, adsorption or other methods in natural gas processing or cycling plants. Generally such liquids consist of propane and heavier hydrocarbons and are commonly referred to as lease condensate, natural gasoline and liquefied petroleum gases. Natural gas liquids include natural gas plant liquids (primarily ethane, propane, butane and isobutane) and lease condensate (primarily pentanes produced from natural gas at lease separators and field facilities) |

NiSource | NiSource Inc. |

NiSource Corporate Services | NiSource Corporate Services Company |

NiSource Finance | NiSource Finance Corp. |

OCI | Other Comprehensive Income (Loss) |

park and loan services | Those services pursuant to which customers receive the right for a fee to store natural gas in (park), or borrow gas from (loan), our facilities on a contractual basis |

PHMSA | Pipeline and Hazardous Materials Safety Administration |

Piedmont | Piedmont Natural Gas Company, Inc. |

play | A proven geological formation that contains commercial amounts of hydrocarbons |

ppb | parts per billion |

reservoir | A porous and permeable underground formation containing an individual and separate natural accumulation of producible hydrocarbons (crude oil and/or natural gas) which is confined by impermeable rock or water barriers and is characterized by a single natural pressure system |

shale gas | Natural gas produced from organic (black) shale formations |

Tcf | One trillion cubic feet |

throughput | The volume of natural gas transported or passing through a pipeline, plant, terminal or other facility during a particular period |

Williams Partners | Williams Partners L.P. |

4

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Some of the information in this report may contain forward-looking statements. Forward-looking statements give our current expectations, contain projections of results of operations or of financial condition, or forecasts of future events. Words such as “may,” “assume,” “forecast,” “position,” “predict,” “strategy,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,” “project,” “budget,” “potential,” or “continue,” and similar expressions are used to identify forward-looking statements. They can be affected by assumptions used or by known or unknown risks or uncertainties. Consequently, no forward-looking statements can be guaranteed. When considering these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this report. Actual results may vary materially. You are cautioned not to place undue reliance on any forward-looking statements. You should also understand that it is not possible to predict or identify all such factors and should not consider the following list to be a complete statement of all potential risks and uncertainties. Factors that could cause our actual results to differ materially from the results contemplated by such forward-looking statements include:

• | changes in general economic conditions; |

• | competitive conditions in our industry; |

• | actions taken by third-party operators, processors and transporters; |

• | the demand for natural gas storage and transportation services; |

• | our ability to successfully implement our business plan; |

• | our ability to complete internal growth projects on time and on budget; |

• | the price and availability of debt and equity financing; |

• | the availability and price of natural gas to the consumer compared to the price of alternative and competing fuels; |

• | competition from the same and alternative energy sources; |

• | energy efficiency and technology trends; |

• | operating hazards and other risks incidental to transporting, storing and gathering natural gas; |

• | natural disasters, weather-related delays, casualty losses and other matters beyond our control; |

• | interest rates; |

• | labor relations; |

• | large customer defaults; |

• | changes in the availability and cost of capital; |

• | changes in tax status; |

• | the effects of existing and future laws and governmental regulations; |

• | the effects of future litigation; and |

• | certain factors discussed elsewhere in this report. |

Other factors described herein, as well as factors that are unknown or unpredictable, could also have a material adverse effect on future results. Please see Item 1A “Risk Factors.” Except as required by applicable securities laws, we do not intend to update these forward-looking statements and information.

5

PART I

ITEMS 1 AND 2. BUSINESS AND PROPERTIES

Unless the context otherwise requires, references in this Annual Report on Form 10-K (this "Form 10-K") to “we,” “us,” “our,” the “Company” and “CPG” refer to Columbia Pipeline Group, Inc., a Delaware corporation, and its consolidated subsidiaries including CEG and CPPL.

Organizational History

We are a growth-oriented Delaware corporation formed by NiSource on September 26, 2014 to own, operate and develop a portfolio of pipelines, storage and related midstream assets. On July 1, 2015, NiSource distributed, pursuant to an effective registration statement on Form 10, 317.6 million shares, one share of CPG common stock for every one share of NiSource common stock held by NiSource stockholders on the record date. As of July 1, 2015, CPG is an independent, publicly traded company, and NiSource does not retain any ownership interest in CPG (the "Separation"). CPG's common stock began trading "regular-way" under the ticker symbol "CPGX" on the NYSE on July 2, 2015.

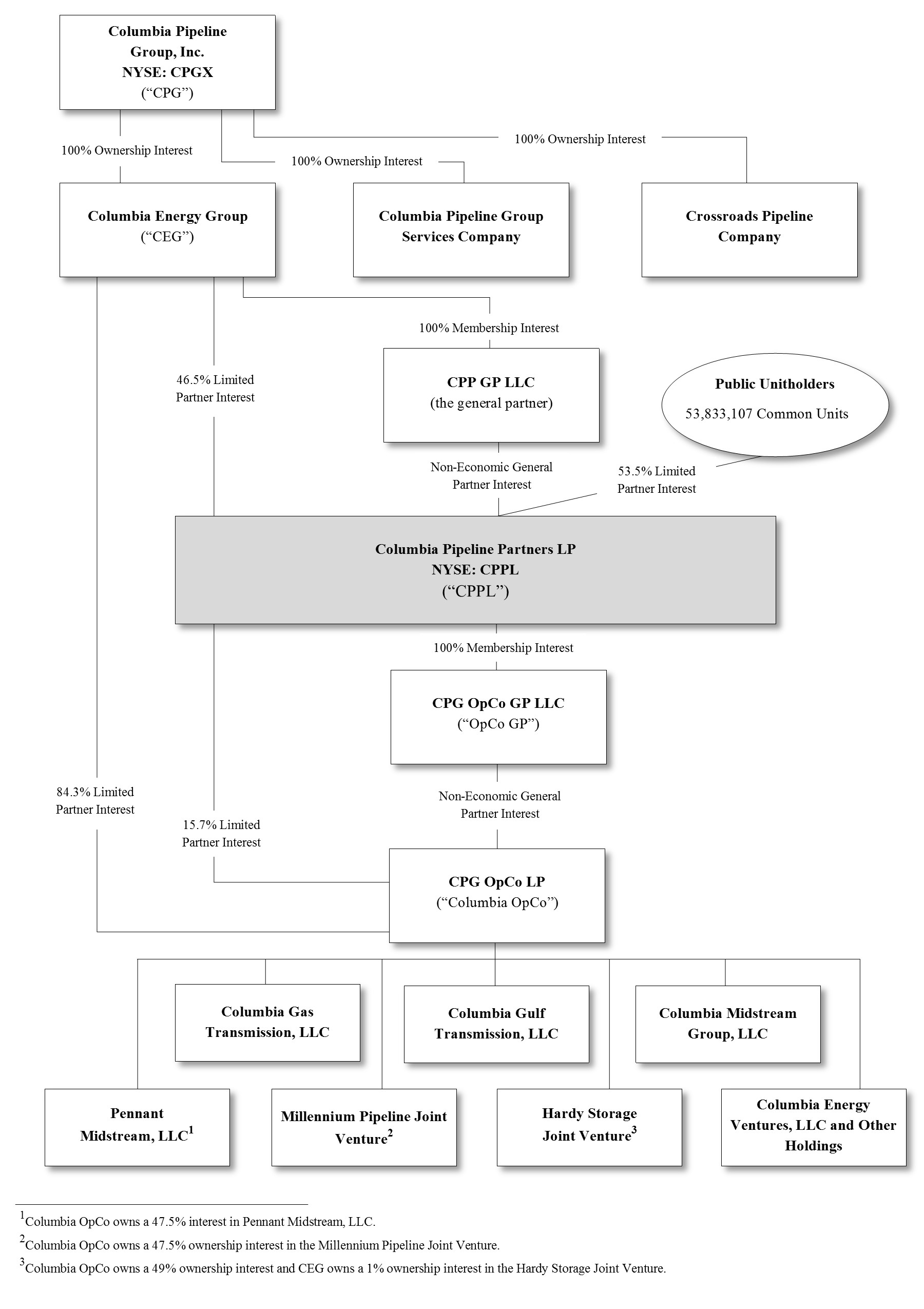

We own approximately 15,000 miles of strategically located interstate gas pipelines extending from New York to the Gulf of Mexico and one of the nation’s largest underground natural gas storage systems, with approximately 300 MMDth of working gas capacity, as well as related gathering and processing assets. For the year ended December 31, 2015, 94.6% of our revenue, excluding revenues generated from cost recovery under certain regulatory tracker mechanisms, which we refer to as “tracker-related revenues,” was generated under firm revenue contracts. As of December 31, 2015, these contracts had a weighted average remaining contract life of 4.8 years. We own these assets through Columbia OpCo, a partnership between our wholly owned subsidiary CEG and CPPL.

Through our wholly owned subsidiary CEG, we own the general partner of CPPL, all of CPPL’s incentive distribution rights and all of CPPL’s subordinated units, which, in the aggregate, represent a 46.5% limited partner interest in CPPL. CPPL completed its initial public offering on February 11, 2015, selling 53.5% of its limited partner interests.

6

The following is a simplified diagram of our ownership structure, including key operating subsidiaries immediately following the Separation:

7

Business Segment

Our operations comprise one reportable segment containing our portfolio of pipelines, storage and related midstream assets. Please see Note 23, “Segments of Business” in Item 8, Financial Statements and Supplementary Data for further discussion regarding our segment.

Description of Businesses and Properties

Interstate Pipeline and Storage Assets. We own the FERC-regulated natural gas transportation and storage assets described below.

Columbia Gas Transmission. Columbia Gas Transmission owns and operates a FERC-regulated interstate natural gas transportation pipeline and storage system, which has historically largely operated as a means to transport gas from the Gulf Coast, via Columbia Gulf, from various pipeline interconnects, and from production areas in the Appalachia region to markets in the midwest, Atlantic, and northeast regions. As Marcellus and Utica shale gas production has grown, Columbia Gas Transmission’s operations and assets also have grown due to the increased production within the pipeline’s operating area. As the market continues to evolve, Columbia Gas Transmission is in various phases of execution and construction on a multitude of growth projects to help move the growing production of gas out of the Marcellus and Utica shale plays and into on-system markets in the northeast and mid-Atlantic markets as well as off-system markets in the Gulf Coast.

Columbia Gas Transmission’s pipeline system consists of 11,272 miles of natural gas transmission pipeline. It has a transportation capacity of approximately 10 MMDth/d, transports an average of approximately 4.0 MMDth/d and serves communities in Delaware, Kentucky, Maryland, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Virginia and West Virginia. Columbia Gas Transmission owns and leases approximately 819,500 acres of underground storage, 3,432 storage wells, which includes 35 storage fields in four states with approximately 627.5 MMDth in total operational capacity, with approximately 290 MMDth of working gas capacity.

Columbia Gulf. The Columbia Gulf pipeline system is a FERC-regulated interstate natural gas transportation pipeline system, which consists of 3,341 miles of natural gas transmission pipeline. The system offers shippers access to two actively traded market hubs—the Columbia Gulf Mainline Pool and the Columbia Gulf Onshore Pool. In addition, Columbia Gulf interconnects with the Henry Hub in South Louisiana and the Columbia Gas Transmission Pool near Leach, Kentucky. Through its interstate and intrastate pipeline interconnections, Columbia Gulf provides upstream supply to serve growing markets in the mid-Atlantic, midwest, Florida and southeast. Columbia Gulf also has a project underway that will connect its system with the Cameron LNG export facility. In addition, Columbia Gulf recently reconfigured its system so that it can reverse flow on one of its three pipelines. Flows on the other two pipelines will be reversed as part of expansion projects that are underway.

Millennium Pipeline Joint Venture. We own a 47.5% ownership interest in Millennium Pipeline, which transports an average of 1.1 MMDth/d of natural gas primarily sourced from the Marcellus shale to markets across southern New York and the lower Hudson Valley, as well as to the New York City market through its pipeline interconnections. Millennium Pipeline has access to the Northeast Pennsylvania Marcellus shale natural gas supply and is pursuing growth opportunities to expand its system. The Millennium Pipeline system consists of approximately 253 miles of natural gas transmission pipeline and three compressor stations with over 43,000 horsepower of installed capacity. Columbia Gas Transmission acts as operator of Millennium Pipeline, and DTE Millennium Company and National Grid Millennium LLC each own an equal remaining share of Millennium Pipeline.

Hardy Storage Joint Venture. We own a 50% ownership interest in Hardy Storage, which owns an underground natural gas storage field in Hardy and Hampshire counties in West Virginia. Columbia Gas Transmission serves as operator of Hardy Storage. Hardy Storage has a working storage capacity of approximately 12 MMDth and the ability to deliver 176,000 Dth/d. A third party, Piedmont Natural Gas Company, Inc., owns the remaining 50% ownership interest in Hardy Storage.

Gathering, Processing and Other Assets. Through our ownership interests in Columbia OpCo, we own the gathering, processing and other assets described below.

Columbia Midstream. Columbia Midstream provides natural gas producer services including gathering, treating, conditioning, processing, compression and liquids handling in the Appalachian Basin. Columbia Midstream owns approximately 123 miles of natural gas gathering pipeline and one compressor station with 6,800 horsepower of installed capacity and also owns a 47.5% ownership interest in Pennant, which owns approximately 49 miles of natural gas gathering pipeline infrastructure, a cryogenic processing plant and a 36 mile NGL pipeline. Columbia Midstream supports the growing production in the Utica and Marcellus resource plays.

8

CEVCO. CEVCO manages Columbia OpCo’s mineral rights positions in the Marcellus and Utica shale areas. CEVCO owns production rights to approximately 460,000 acres and has sub-leased the production rights in three storage fields and has also contributed its production rights in one other field. CEVCO has entered into multiple transactions to develop its minerals position and as a result receives revenue through working interests and/or royalty interests.

Business Strategy

Our principal business objective is to utilize our existing geographic advantages, flexible capital structure, management strength and diverse customer base to substantially increase our fee-generating long-term assets, positioning us to pay dividends to our stockholders and increase such payments over time. We expect to achieve this objective through the following business strategies:

Capitalize on organic expansion opportunities. Our assets are strategically located within proximity to growing production from the Marcellus and Utica shale areas and growing demand centers, providing us with substantial organic expansion opportunities. We expect the revenues generated from our businesses will increase as we execute on our significant portfolio of organic growth opportunities, which include the growth projects listed here-in. We intend to leverage our management team’s expertise in constructing, developing and optimizing our assets in order to increase and diversify our customer base, increase natural gas supply on our system and maximize volume throughput.

Permit CPPL to further invest in organic growth projects. We expect Columbia OpCo to issue a significant amount of new limited partner interests over the next several years to fund our organic growth opportunities, and we expect that CPPL will exercise its preemptive right to purchase these newly issued equity interests to the extent financing is available. CPPL also has a right of first offer with respect to acquiring CEG’s retained 84.3% limited partner interest in Columbia OpCo if CEG decides to sell such interest. We do not expect to sell CEG’s retained limited partner interest in Columbia OpCo in the near term.

Maintain and grow stable cash flows supported by long-term, fee-based contracts. We will continue to pursue opportunities to increase the fee-based component of our contract portfolio to minimize our direct commodity price exposure. We will focus on obtaining additional long-term firm commitments from customers, which may include reservation-based charges, volume commitments and acreage dedications. Substantially all of the organic growth projects that we expect to complete are supported by long-term service contracts and binding precedent agreements.

Target a conservative and flexible capital structure. We intend to target credit metrics consistent with the profile of investment-grade midstream energy companies. Furthermore, we intend to maintain a balanced capital structure while financing the capital required to (i) contribute substantially all of the capital required to finance our organic expansion projects and (ii) pursue potential third-party acquisitions.

Current System Expansion Opportunities

The unique location and capabilities of our pipeline assets place us in a strategically advantageous position to continue to capitalize on expected growth in production from the Marcellus and Utica shales. To that end, we have recently placed into service or are currently pursuing the following significant expansion projects:

• | Chesapeake LNG. This approximately $28 million project was placed into service in the second quarter of 2015 and replaced 120,000 Dth/d of existing LNG peak shaving facilities nearing the end of their useful lives. |

• | Big Pine Expansion. We are investing approximately $75 million to extend the Big Pine pipeline and add compression facilities that will add incremental capacity. The project will support Marcellus shale production in western Pennsylvania. The project piping was placed into service in the third quarter of 2015 and we expect the compression to be placed into service in the second quarter of 2016. |

• | East Side Expansion. This project provides access for production from the Marcellus shale to northeastern and mid-Atlantic markets. The approximately $295 million project added 312,000 Dth/d of capacity and was placed into service in the fourth quarter of 2015. |

• | Washington County Gathering. A producer has contracted with us to build an approximately 20 mile gas gathering system in southwestern Pennsylvania. The initial project went into service during the third quarter of 2015 and we expect to invest approximately $120 million through 2018. |

9

• | Kentucky Power Plant Project. We expect to invest approximately $25 million to construct 2.7 miles of 16-inch pipeline and other facilities to a power plant near Columbia Gas Transmission’s Line P. This project will provide up to 72,000 Dth/d of new firm service and is expected to be placed into service in the second quarter of 2016. |

• | Gibraltar Pipeline Project. We expect to invest approximately $270 million to construct an approximately 1 MMDth/d dry gas header pipeline in southwest Pennsylvania. We expect this to be the first of multiple phases with a projected initial in-service date in the fourth quarter of 2016. |

• | Utica Access Project. We expect to invest approximately $50 million to construct 4.7 miles of 24-inch pipeline to provide 205,000 Dth/d of new firm transportation to provide Utica production access to liquid trading points on Columbia Gas Transmission's system. This project is expected to be placed into service in the fourth quarter of 2016. |

• | Leach XPress. This project will provide approximately 1.5 MMDth/d of capacity from the Marcellus and Utica production regions to the Leach compressor station located on the Columbia Gulf system, TCO Pool, and other markets on the Columbia Gas Transmission system. We expect the project, which involves an estimated investment of approximately $1.4 billion, to be placed into service in the fourth quarter of 2017. |

• | Rayne XPress. This project will transport approximately 1 MMDth/d of southwest Marcellus and Utica production from the Leach, Kentucky interconnect with Columbia Gas Transmission towards the Rayne compressor station in southern Louisiana to reach various Gulf Coast markets. We expect the project, which involves an estimated investment of approximately $380 million, to be placed into service in the fourth quarter of 2017. |

• | Millennium Lateral. We intend to invest approximately $20 million through our ownership stake in Millennium Pipeline to construct approximately 8 miles of 16-inch pipeline to a new power plant situated near Wawayanda, New York. This project will provide up to 127,000 Dth/d of new firm capacity and is expected to be placed into service in the second quarter of 2017. |

• | Cameron Access Project. This project, which involves an investment of approximately $310 million, will provide 800,000 Dth/d of transportation capacity on the Columbia Gulf system to the Cameron LNG export terminal in Louisiana. We expect the project to be placed into service in the first quarter of 2018. |

• | WB XPress. This project, which involves an investment of approximately $850 million, will expand Columbia Gas Transmission's WB system in order to transport approximately 1.3 MMDth/d of Marcellus production to pipeline interconnects and East Coast markets, including access to the Cove Point LNG terminal. We expect this project to be placed into service in the fourth quarter of 2018. |

• | Mountaineer XPress. This approximately $2.0 billion project will provide new takeaway capacity for Marcellus and Utica production. The project will provide up to 2.7 MMDth/d of firm transportation capacity on the Columbia Gas Transmission system. We expect this project to be placed into service in the fourth quarter of 2018. |

• | Gulf XPress. This project will provide 860,000 Dth/d of firm transportation capacity for Marcellus and Utica production on the Columbia Gulf system. This project involves an investment of approximately $0.7 billion and is expected to be placed into service in the fourth quarter of 2018. |

• | Millennium Eastern System Upgrade. We intend to invest approximately $130 million through our ownership stake in Millennium Pipeline to expand eastward flow capacity by 237,500 Dth/d to Ramapo and other nearby points on the system. We expect this project to be placed into service in the fourth quarter of 2018. |

In 2013, the FERC approved the modernization settlement entered into by Columbia Gas Transmission and its customers that provides recovery and return on an investment of up to $1.5 billion over a five-year period to modernize its system to improve system integrity and enhance service reliability and flexibility. The modernization program includes, among other things, replacement of aging pipeline and compressor facilities, enhancements to system inspection capabilities and improvements in control systems. Columbia Gas Transmission placed approximately $319 million in modernization investments into service during 2015. In January 2016, the FERC approved Columbia Gas Transmission's third annual filing for recovery under this program. In December 2015, Columbia Gas Transmission filed an extension of this settlement and has requested FERC’s approval of the customer agreement by March 31, 2016. This extension will allow Columbia Gas Transmission to invest an additional $1.1 billion

10

over an additional three-year period through 2020. This agreement also expands the scope of facility investments covered by the program.

Regulatory Matters

Pipeline Safety and Maintenance. Our pipelines used for gathering and transporting natural gas and NGLs are subject to regulation by the PHMSA of the DOT pursuant to the Natural Gas Pipeline Safety Act of 1968 (“NGPSA”), with respect to natural gas and the Hazardous Liquids Pipeline Safety Act of 1979, as amended (“HLPSA”), with respect to NGLs. Both the NGPSA and the HLPSA were amended by the Pipeline Safety Improvement Act of 2002 (“PSI Act”) and the Pipeline Inspection, Protection, Enforcement and Safety Act of 2006 (“PIPES Act”). Pursuant to these acts, PHMSA has promulgated regulations governing, among other things, pipeline wall thicknesses, design pressures, maximum operating pressures, pipeline patrols and leak surveys, minimum depth requirements, and emergency procedures, as well as other matters intended to ensure adequate protection for the public and to prevent accidents and failures. Additionally, PHMSA has promulgated regulations requiring pipeline operators to develop and implement integrity management programs for certain gas and hazardous liquid pipelines that, in the event of a pipeline leak or rupture, could affect “high consequence areas,” where a release could have the most significant adverse consequences, including high population areas, certain drinking water sources and unusually sensitive ecological areas. We believe that our pipeline operations are in material compliance with applicable NGPSA and HLPSA requirements; however, due to the possibility of new or amended laws and regulations or reinterpretation of existing laws and regulations, future compliance with the NGPSA and HLPSA could result in increased costs.

Moreover, new legislation or regulations adopted by PHMSA may impose more stringent requirements applicable to integrity management programs and other pipeline safety aspects of our operations, which could cause us to incur increased capital costs, operational delays and costs of operation. For example, the Pipeline Safety, Regulatory Certainty and Job Creation Act of 2011 (the “2011 Pipeline Safety Act”), which authorized funding for federal pipeline safety programs through 2015, directed the Secretary of Transportation to undertake a number of reviews, studies and reports, some of which could result in more stringent safety controls or inspections or additional natural gas and hazardous liquids pipeline safety rulemaking. Among other things, the 2011 Pipeline Safety Act directed the Secretary of Transportation to promulgate regulations relating to expanded integrity management requirements, automatic or remote-controlled valve use, excess flow valve use, leak detection system installation, pipeline material strength testing, and operator verification of records confirming the maximum allowable pressure of certain interstate gas transmissions pipelines. The 2011 Pipeline Safety Act also increases the maximum penalty for violation of pipeline safety regulations from $100,000 to $200,000 per violation per day of violation and from $1.0 million to $2.0 million for a related series of violations. Although a number of the mandates imposed under the 2011 Act have yet to be acted upon by PHMSA, those mandates continue to have the potential to cause owners and operators of pipeline facilities to incur significant capital expenditures and/or operating costs in the future. Legislation that would reauthorize federal pipeline safety programs through 2019, referred to as Securing America’s Future Energy: Protecting Infrastructure of Pipelines and Enhancing Safety ("SAFE PIPES"), was approved by the Senate Commerce Committee in December 2015 and will be considered by the U.S. Senate. Among other things, the SAFE PIPES legislation would require PHMSA to conduct an assessment of its inspection process and integrity management programs for natural gas and hazardous liquid pipelines and likely would require PHMSA to pursue those mandates under the 2011 Pipeline Safety Act that have not yet been acted upon. More recently, in February 2016, PHMSA issued an advisory bulletin for natural gas storage facility operators. The bulletin recommends that operators review operations to identify the potential for leaks and failures caused by corrosion, chemical or mechanical damage, or other material deficiencies in piping, tubing, casing, valves, and other associated facilities. The bulletin further advises operators to review storage facility locations and operations of shut-off and isolation systems, and review and update emergency plans as necessary. Finally, the advisory directs compliance with state regulations governing the permitting, drilling, completion, and operation of storage wells, and recommends the voluntary implementation of certain industry-recognized recommended practices for natural gas storage facilities. PHMSA indicated when it issued the advisory bulletin that additional regulations related to safety standards for natural gas storage facilities are likely forthcoming. At this time, we cannot predict the impact of any future regulatory actions in this area.

In addition, while states are largely preempted by federal law from regulating pipeline safety for interstate lines, several are certified by PHMSA to assume responsibility for enforcing federal intrastate pipeline regulations and inspection of intrastate pipelines. In practice, because states can adopt stricter standards for intrastate pipelines than those imposed by the federal government for interstate lines, states vary considerably in their authority and capacity to address pipeline safety. We do not anticipate any significant difficulty or material cost in complying with applicable intrastate pipeline safety laws and regulations in 2016. Our pipelines have operations and maintenance plans designed to keep the facilities in compliance with pipeline safety requirements. We, or the entities in which we own an interest, inspect our pipelines regularly in material compliance with applicable state and federal maintenance requirements. Nonetheless, the adoption of new or amended regulations by states in which we operate that result in more stringent

11

or costly pipeline integrity management or safety standards could have a significant adverse effect on us and similarly situated midstream operators.

For additional information regarding pipeline safety risk, see "Risk Factors" under Item 1A of this Form 10-K.

Environmental and Occupational Safety and Health. Our pipeline, storage and related midstream operations are subject to stringent and complex federal, state and local laws and regulations governing occupational safety and health, the discharge of materials into the environment and environmental protection. The more significant of these existing environmental and occupational safety and health laws and regulations, as amended from time to time, include the following:

• | The Federal CAA and comparable state laws, which restrict the emission of air pollutants from many sources and imposes various pre-construction, monitoring, reporting requirements, and provides authority for adopting climate change regulatory initiatives. Our natural gas transmission and storage assets are considered potential sources of air emissions subject to permitting obligations for existing, modified or new sources of air emissions and compliance with which could result in potential delays in the development of projects and in the incurrence of capital expenditures for air pollution control equipment or other air emissions-related issues. |

• | The Federal Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”) and comparable state laws, which impose liability on generators, transporters, and arrangers of hazardous substances at sites where hazardous substance releases have occurred. Under CERCLA, responsible parties, including current and past owners or operators of a site where a hazardous substance release occurred and entities who disposed or arranged for the disposal of a hazardous substance released at the site may be held liable for the costs of cleaning up the hazardous substances released, for damages to natural resources and for the costs of certain health studies. We generate materials in the course of our operations that may be regulated as hazardous substances. |

• | The Federal Resource Conservation and Recovery Act (“RCRA”) and comparable state statutes, which govern the generation, treatment, storage, transport, and disposal of solid wastes, including hazardous wastes. In the course of our operations, we generate some amounts of ordinary industrial wastes that may be regulated as hazardous wastes. |

• | The U.S. Federal Water Pollution Control Act, also known as the federal Clean Water Act (“CWA”), and analogous state laws that regulate discharges of pollutants from facilities to state and federal waters, and establishes the extent to which waterways are subject to federal jurisdiction and rulemaking as protected waters of the United States. Among other things, the CWA may require permits for facilities that discharge wastewaters or dredge and fill material into regulated waters, including wetlands; spill prevention, control and countermeasure plans requiring appropriate berms to help prevent contamination of regulated waters in the event of a hydrocarbon release; and individual permits or coverage under general permits for discharges of stormwater runoff from certain types of facilities. |

• | The U.S. Oil Pollution Act of 1990 (“OPA”), which amends the CWA and subjects certain owners and operators, including owners and operators of pipelines and other onshore facilities, to liability for removal costs and damages arising from an oil spill in waters of the United States. |

• | The Toxic Substances Control Act and any comparable state laws, which require that polychlorinated biphenyl (“PCB”) contaminated materials be managed in accordance with a comprehensive regulatory regime. We are currently remediating PCBs at certain gas transmission facilities where PCBs were released into the environment. |

• | The U.S. Occupational Safety and Health Act (“OSHA”) and analogous state laws, which establish workplace standards for the protection of the health and safety of employees, including the implementation of hazard communications programs designed to inform employees about hazardous substances in the workplace, potential harmful effects of these substances, and appropriate control measures. |

• | The Endangered Species Act and comparable state statutes, which restrict activities that may affect federally identified endangered and threatened species or their habitats through the implementation of operating restrictions or a temporary, seasonal, or permanent ban in affected areas. Any expansion projects pursued by us must take into consideration the adverse impact of such projects on protected species and habitats. |

12

• | The National Environmental Policy Act, which requires federal agencies to consider potential environmental effects in their decisions, including site approvals. Many of our capital projects require federal agency review, and therefore the environmental effects of proposed projects are a factor in determining whether we will be authorized to complete those projects. |

These laws and regulations, as well as state counterparts, generally restrict the level of pollutants emitted to ambient air, discharges to surface water, and disposals or other releases to surface and below-ground soils and ground water. Failure to comply with these laws and regulations may result in the assessment of sanctions, including administrative, civil, and criminal penalties; the imposition of investigatory, remedial, and corrective action obligations or the incurrence of capital expenditures; the occurrence of delays in the development of projects; and the issuance of injunctions restricting or prohibiting some or all of our activities in a particular area. See Risk Factors under Item 1A of this Form 10-K for further discussion on hydraulic fracturing, climate change, and regulations relating to environmental protection. The ultimate financial impact arising from environmental laws and regulations is neither clearly known nor determinable as new standards, such as air emission standards and water quality standards, continue to evolve.

We have made and will continue to make operating and capital expenditures, some of which may be material, to comply with environmental and occupational safety and health laws and regulations. These are necessary business costs in our operations and in the pipeline transportation and storage industry. Although we are not fully insured against all environmental and occupational safety and health risks, and our insurance does not cover any penalties or fines that may be issued by a governmental authority, we maintain insurance coverage that we believe is sufficient based on our assessment of insurable risks and consistent with insurance coverage held by other similarly situated industry participants. Nevertheless, it is possible that other developments, such as stricter and more comprehensive environmental and occupational safety and health laws and regulations, as well as claims for damages to property or persons resulting from our operations, could result in substantial costs and liabilities, including administrative, civil, and criminal penalties. We believe that we are in material compliance with existing environmental and occupational safety and health regulations. Further, we believe that the cost of maintaining compliance with these existing laws and regulations will not have a material adverse effect on our business, financial condition, results of operations, or cash flows, but new or more stringently applied existing laws and regulations could increase the cost of doing business, and such increases could be material.

Regulatory Compliance. Regulation of natural gas transportation by the FERC and other federal and state regulatory agencies, including DOT has a significant impact on our business.

Our interstate natural gas transportation and storage system operations are regulated by the FERC under the NGA and the Natural Gas Policy Act of 1978 (“NGPA”), and the FERC’s regulations under those statutes. The FERC regulatory policies govern the rates and services that each FERC-regulated pipeline is permitted to charge customers for interstate transportation and storage of natural gas. The FERC’s policy permits our interstate pipeline companies to include an income tax allowance in the cost of service-based rates of a pipeline organized as a tax pass through partnership entity to reflect actual or potential income tax liability on public utility income, if we prove that the ultimate owners of our partnership interests have an actual or potential income tax liability on such income. In addition, the FERC also regulates the construction of U.S. interstate natural gas pipelines and storage facilities, including the extension, enlargement and abandonment of facilities. Failure to comply with the NGA, the NGPA and the other federal laws and regulations governing our operations and business activities can result in the imposition of administrative, civil and criminal remedies. The FERC may propose and implement new rules and regulations which may affect the business, financial condition and results of operations of our interstate natural gas transmission and storage companies.

Pursuant to Section 1(b) of the NGA, our natural gas gathering facilities are exempt from the jurisdiction of the FERC under the NGA. The distinction between FERC-regulated transmission services and federally unregulated gathering services has been the subject of substantial litigation, and the FERC currently determines whether facilities are gathering facilities on a case-by-case basis, so the classification and regulation of our gathering facilities may be subject to change based on future determinations by the FERC, the courts or Congress. State regulation of gathering facilities generally includes various safety, environmental and, in some circumstances, nondiscriminatory take requirements and complaint-based rate regulation. We cannot predict what effect, if any, a change in the regulation of our gathering facilities might have on our operations, but the industry could be required to incur additional capital expenditures and increased costs depending on future legislative and regulatory changes.

Our operations are also impacted by new regulations, which have increased the time that it takes to obtain required construction permits. Additionally, increased regulation of natural gas producers in our areas of operations, including regulation associated with hydraulic fracturing, could reduce regional supply of natural gas and therefore throughput on our assets.

13

Competition. Our pipeline systems compete primarily with other interstate and intrastate pipelines. Pipelines typically compete with each other based on location, capacity, price and reliability.

Competition for natural gas gathering is primarily based on rates, customer commitment levels, timing, performance, commercial terms, reliability, services levels, location of gathering systems, reputation and fuel efficiencies. Our principal competitors for low and high pressure gathering systems include numerous independent gas gatherers and integrated energy companies, who have plans to build gathering facilities to move volumes to interstate pipelines. Some of our competitors have capital resources and control supplies of natural gas greater than we do.

Seasonality

Natural gas demand for heating is impacted by weather, which in turn influences the value of transportation and storage. Peak demand for natural gas typically occurs during the winter months, however, because a high percentage of our revenues are derived from firm capacity reservation fees under long-term contracts, our transportation and storage revenues are not generally seasonal in nature. Operating revenues for 2015 were approximately 25% in the first quarter, 24% in the second quarter, 24% in the third quarter, and 27% in the fourth quarter.

Customers and Contracts

Our customer mix for natural gas transportation services includes LDCs, municipal utilities, direct industrial users, electric power generators, marketers, producers and LNG exporters. We provide a significant portion of our transportation and storage services through firm contracts and derive a small portion of our revenues through interruptible service contracts. Transportation and storage services are generally provided under firm agreements where customers reserve capacity in pipelines and storage facilities. The vast majority of these agreements provide for fixed reservation charges that are paid monthly regardless of the actual volumes transported on the pipelines or injected or withdrawn from our storage facilities, plus a small variable component that is based on volumes transported, injected or withdrawn, which is intended to recover variable costs. We also provide interruptible transportation and storage services where customers can use capacity if it is available at the time of the request. Interruptible revenues depend on the amount of volumes transported or stored and the associated market rates for this interruptible service. Columbia Gas of Ohio, an affiliated party prior to the Separation, accounted for approximately 13% of our total operating revenues for the year ended December 31, 2015. No other customer accounted for greater than 10% of total operating revenue. Please see Note 25, “Concentration of Credit Risk” in Item 8, Financial Statements and Supplementary Data for further discussion.

Our customers for our midstream operations consist of natural gas producers with whom we primarily have long-term, fee-based gas gathering agreements, with terms ranging from 10 to 15 years typically with minimum volume commitments.

Employees

As of December 31, 2015, we had approximately 1,968 active employees. Of these 1,968 employees, 258 are covered by collective bargaining agreements, 224 of which expire in 2016.

Additional Information

We were formed on September 26, 2014 as a Delaware corporation. Our principal executive offices are located at 5151 San Felipe St., Suite 2500, Houston, Texas 77056, and our telephone number is 713-386-3701. We electronically file various reports with the Securities and Exchange Commission (“SEC”), including annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to such reports. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site that contains reports and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. Additionally, information about us, including our reports filed with the SEC, is available through our website at http://www.columbiapipelinegroup.com. These reports are accessible at no charge through our website and are made available as soon as reasonably practicable after such material is filed with or furnished to the SEC. Our website and the information contained on that site, or connected to that site, are not incorporated by reference into this report.

14

RISK FACTORS

Our business, results of operations, cash flows and financial condition are subject to a number of risks and uncertainties. You should carefully consider the risks and uncertainties described below, together with all of the other information in this Form 10-K. The risks and uncertainties we face are not limited to those described below. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also materially adversely affect our business, results of operations, cash flows and financial condition. This Form 10-K also contains forward-looking statements that involve risks and uncertainties. You should carefully read the section entitled “Cautionary Note Concerning Forward-Looking Statements” on page 5 of this Form 10-K.

If any of the following risks were to occur, our business, financial condition, results of operations, cash flows and cash available for the payment of dividends could be materially adversely affected. In that case, we might not be able to pay dividends to our stockholders, the trading price of our common stock could materially decline and you could lose all or part of your investment.

We may not have sufficient cash from operations following the establishment of cash reserves and payment of costs and expenses to enable us to pay dividends to our stockholders.

The amount of cash we generate from our operations will fluctuate based on, among other things:

• | the rates we charge for our transmission, storage and gathering services; |

• | the level of firm transmission and storage capacity sold and volumes of natural gas we transport, store and gather for our customers; |

• | regional, domestic and foreign supply and perceptions of supply of natural gas; the level of demand and perceptions of demand in our end-use markets; and actual and anticipated future prices of natural gas and other commodities (and the volatility thereof), which may impact our ability to renew and replace firm transmission and storage agreements; |

• | legislative or regulatory action affecting the demand for natural gas, the supply of natural gas, the rates we can charge, how we contract for services, our existing contracts, operating costs and operating flexibility; |

• | the imposition of requirements by state agencies that materially reduce the demand of our customers, such as LDCs and power generators, for our pipeline services; |

• | the commodity price of natural gas, which could reduce the quantities of natural gas available for transport; |

• | the creditworthiness of our customers, particularly in light of recent declines in commodity prices; |

• | the level of our operating and maintenance and general and administrative costs; |

• | the level of capital expenditures we incur to maintain our assets; |

• | regulatory and economic limitations on the development of LNG export terminals in the Gulf Coast region; |

• | successful development of LNG export terminals in the eastern or northeastern United States, which could reduce the need for natural gas to be transported on the Columbia Gulf pipeline system; |

• | changes in insurance markets and the level, types and costs of coverage available, and the financial ability of our insurers to meet their obligations; |

• | changes in, or new, statutes, regulations or governmental policies by federal, state and local authorities with respect to protection of the environment; |

• | changes in accounting rules and/or tax laws or their interpretations; |

• | nonperformance or force majeure by, or disputes with or changes in contract terms with, major customers, suppliers, dealers, distributors or other business partners; and |

• | changes in, or new, statutes, regulations, governmental policies and taxes, or their interpretations. |

15

In addition, the actual amount of cash we will have available for the payment of dividends will depend on other factors, including:

• | the level and timing of capital expenditures we make; |

• | construction costs; |

• | fluctuations in our working capital needs; |

• | our ability to borrow funds and access capital markets; |

• | our debt service requirements and other liabilities; |

• | restrictions contained in our existing or future debt agreements, including our credit facilities; and |

• | the cash distribution policy of CPPL. |

Expansion projects that are expected to be accretive may nevertheless reduce our cash from operations on a per share of common stock basis.

Even if we complete expansion projects that we believe will be accretive, these expansion projects may nevertheless reduce our cash from operations on a per share of common stock basis. Any expansion project involves potential risks, including, among other things:

• | service interruptions or increased downtime associated with our projects, including the reversal of Columbia Gulf’s pipelines; |

• | a decrease in our liquidity as a result of our using a significant portion of our available cash or borrowing capacity to finance the project or acquisition; |

• | an inability to complete expansion projects on schedule or within the budgeted cost due to the unavailability of required construction personnel or materials, accidents, weather conditions or an inability to obtain necessary permits, among other factors; |

• | the assumption of unknown liabilities when making acquisitions for which we are not indemnified or for which our indemnity is inadequate; |

• | the diversion of our management’s attention from other business concerns; |

• | mistaken assumptions about the overall costs of equity or debt, demand for our services, supply volumes, reserves, revenues and costs, including synergies and potential growth; |

• | an inability to successfully integrate acquired assets or the businesses we build; |

• | an inability to receive cash flows from a newly built asset until it is operational; and |

• | unforeseen difficulties operating in new product areas or new geographic areas. |

If any expansion projects or acquisitions we ultimately complete are not accretive to our distributable cash flow per share of common stock, our ability to pay dividends to our stockholders may be reduced.

The amount of cash we have available for the payment of dividends to our stockholders depends primarily on our cash flow and not solely on profitability, which may prevent us from paying dividends even during periods when we record net income.

The amount of cash we have available for the payment of dividends depends primarily upon our cash flow, including cash flow from reserves and working capital or other borrowings, and not solely on profitability, which will be affected by non-cash items. As a result, we may pay cash dividends during periods when we record net losses for financial accounting purposes and may be unable to pay cash dividends during periods even when we record net income.

16

CPPL may not have sufficient cash from operations to pay the minimum quarterly distribution to us on our subordinated units following the establishment of cash reserves and payment of costs and expenses and payment of the minimum quarterly distribution on its common units.

CPPL may not have sufficient cash from operations each quarter to pay the minimum quarterly distribution of $0.1675 per unit, or $0.67 per unit per year. The amount of cash CPPL can distribute on its units principally depends upon the amount of cash it generates from its operations, which will fluctuate based on, among other things:

• | the rates Columbia OpCo charges for its transmission, storage and gathering services; |

• | the level of firm transmission and storage capacity sold and volumes of natural gas Columbia OpCo transports, stores and gathers for its customers; |

• | regional, domestic and foreign supply and perceptions of supply of natural gas; the level of demand and perceptions of demand in Columbia OpCo’s end-use markets; and actual and anticipated future prices of natural gas and other commodities (and the volatility thereof), which may impact Columbia OpCo’s ability to renew and replace firm transmission and storage agreements; |

• | legislative or regulatory action affecting the demand for natural gas, the supply of natural gas, the rates Columbia OpCo can charge, how Columbia OpCo contracts for services, Columbia OpCo’s existing contracts, operating costs and operating flexibility; |

• | the imposition of requirements by state agencies that materially reduce the demand of Columbia OpCo’s customers, such as LDCs and power generators, for its pipeline services; |

• | the commodity price of natural gas, which could reduce the quantities of natural gas available for transport; |

• | the creditworthiness of Columbia OpCo’s customers, particularly in light of recent declines in commodity prices; |

• | the level of Columbia OpCo’s operating and maintenance and general and administrative costs; |

• | the level of capital expenditures Columbia OpCo incurs to maintain its assets; |

• | regulatory and economic limitations on the development of LNG export terminals in the Gulf Coast region; |

• | successful development of LNG export terminals in the eastern or northeastern United States, which could reduce the need for natural gas to be transported on the Columbia Gulf pipeline system; |

• | changes in insurance markets and the level, types and costs of coverage available, and the financial ability of Columbia OpCo's insurers to meet their obligations; |

• | changes in, or new, statutes, regulations or governmental policies by federal, state and local authorities with respect to protection of the environment; |

• | changes in accounting rules and/or tax laws or their interpretations; |

• | nonperformance or force majeure by, or disputes with or changes in contract terms with, major customers, suppliers, dealers, distributors or other business partners; and |

• | changes in, or new, statutes, regulations, governmental policies and taxes, or their interpretations. |

In addition, the actual amount of cash CPPL will have available for distribution will depend on other factors, including:

• | the level and timing of capital expenditures CPPL or Columbia OpCo makes; |

• | construction costs; |

• | fluctuations in CPPL’s or Columbia OpCo’s working capital needs; |

• | CPPL’s or Columbia OpCo’s ability to borrow funds and access capital markets; |

17

• | CPPL’s or Columbia OpCo’s debt service requirements and other liabilities; |

• | restrictions contained in CPPL’s or Columbia OpCo’s existing or future debt agreements; and |

• | the amount of cash reserves established by CPPL’s general partner. |

As a result of these factors, the amount of cash CPPL distributes in any quarter to us may fluctuate significantly from quarter to quarter and may be significantly less than the minimum quarterly distribution amount that we expect to receive.

We and our affiliates, including the general partner of CPPL, may have conflicts of interest with CPPL.

Conflicts may arise in the future between the interests of CPG and our affiliates, including the general partner of CPPL, and CPPL. The partnership agreement of CPPL permits the board of directors of the general partner of CPPL to form a conflicts committee of independent directors and to submit to that committee matters that the board believes may involve conflicts of interest. There can be no assurance that the conflicts committee will resolve any conflict of interest in our favor.

We depend on certain key customers for a significant portion of our revenues and to anchor our portfolio of growth projects. The loss of key customers could have a material adverse effect on our business, results of operations, financial condition, growth plans and ability to pay dividends to our stockholders.

We are subject to risks of loss resulting from nonperformance by our customers. We depend on certain key customers for a significant portion of our revenues. In addition, we are making significant capital expenditures to expand our existing assets and construct new energy infrastructure based on long-term contracts with customers, including natural gas producers who may be adversely impacted by sustained low commodity prices. Our credit procedures and policies and credit support arrangements may not be adequate to fully eliminate customer credit risk. Further, we may not be able to effectively remarket capacity related to nonperforming customers. The deterioration in the creditworthiness of our customers or the failure of our customers to meet their contractual obligations could have a material adverse effect on our business, results of operations, financial condition, growth plans and ability to pay dividends to our stockholders.

The expansion of our existing assets and construction of new assets is subject to regulatory, environmental, political, legal and economic risks, which could adversely affect our results of operations and financial condition, and reduce our cash from operations on a per share of common stock basis.

One of the ways we intend to grow our business is through the expansion of our existing assets and construction of new energy infrastructure assets. The construction of additions or modifications to our existing pipelines, and the construction of other new energy infrastructure assets, involve numerous regulatory, environmental, political and legal uncertainties beyond our control and will require the expenditure of significant capital that we may be unable to raise. If we undertake these projects they may not be completed on schedule, at the budgeted cost or at all. Moreover, our revenues may not increase immediately upon the expenditure of funds on a particular project. For instance, if we expand a new pipeline, the construction may occur over an extended period of time, and we will not receive any material increases in revenues from such project until the project is completed. We may also construct facilities to capture anticipated future growth in production or demand in regions such as the Marcellus and Utica shale production areas, which may not materialize or where contracts are later cancelled.

Since we are not engaged in the exploration for and development of natural gas reserves, we do not possess reserve expertise and we often do not have access to third-party estimates of potential reserves in an area prior to constructing facilities in such area. To the extent we rely on estimates of future production in our decision to acquire or construct additions to our systems, such estimates may prove to be inaccurate because there are numerous uncertainties inherent in estimating quantities of future production. As a result, new pipelines may not be able to attract enough throughput to achieve our expected investment return, which could adversely affect our results of operations and financial condition. The construction of new pipelines may also require us to obtain new rights-of-way, and it may become more expensive for us to obtain these new rights-of-way or to renew existing rights-of-way. If the cost of renewing or obtaining new rights-of-way increases, our cash flows could be adversely affected.

Certain of our internal growth projects may require regulatory approval from federal and state authorities prior to construction, including any extensions from or additions to our transmission and storage system. The approval process for storage and transportation projects located in the Northeast has become increasingly challenging, due in part to state and local concerns related to unregulated exploration and production and gathering activities in new production areas, including the Marcellus shale area. Such authorization may not be granted or, if granted, such authorization may include burdensome or expensive conditions.

18

A substantial portion of our organic growth projects are supported by binding precedent agreements that are subject to certain conditions, which, if not satisfied, would permit the customer to opt out of the agreement.

A substantial portion of our estimated capital costs for organic growth projects are supported by a combination of (i) service agreements, which are long-term legally binding obligations that secure our revenue streams, and (ii) binding precedent agreements, which are subject to certain conditions to their effectiveness, which, if not satisfied, would enable either us or the customer to terminate the agreement. These conditions include, among others, the receipt of governmental approvals and the achievement of certain in-service dates. If the conditions in a precedent agreement are not satisfied and the customer elects to terminate the agreement, the underlying project and the related revenue streams could be at risk, which could have a material adverse effect on our financial condition, results of operations and our ability to pay dividends to our stockholders.

Any significant decrease in production of natural gas in our areas of operation could adversely affect our business and operating results and reduce our cash available for the payment of dividends to our stockholders.

Our business is dependent on the continued availability of natural gas production and reserves in our areas of operation. Low prices for natural gas or regulatory limitations could adversely affect development of additional reserves and production that is accessible by our pipeline and storage assets. Production from existing wells and natural gas supply basins with access to our systems will naturally decline over time. The amount of natural gas reserves underlying these wells may also be less than anticipated, and the rate at which production from these reserves declines may be greater than anticipated. Additionally, the competition for natural gas supplies to serve other markets could reduce the amount of natural gas supply for our customers or lower natural gas prices could cause producers to determine in the future that drilling activities in areas outside of our current areas of operation are strategically more attractive to them. For example, in response to historically low natural gas prices, a number of large natural gas producers have announced their intention to re-evaluate and/or reduce their drilling programs in certain areas. A reduction in the natural gas volumes supplied by producers could result in reduced throughput on our systems and adversely impact our ability to grow our operations and increase the payment of dividends to our stockholders. Accordingly, to maintain or increase the contracted capacity or the volume of natural gas transported, stored and gathered on our systems and cash flows associated therewith, our customers must continually obtain adequate supplies of natural gas.

The primary factors affecting our ability to obtain sources of natural gas include (i) the level of successful drilling activity near our systems and (ii) our ability to compete for volumes from successful new wells. We have no control over the level of drilling activity in our areas of operation, the amount of reserves associated with wells connected to our gathering system or the rate at which production from a well declines. In addition, we have no control over producers or their drilling or production decisions, which are affected by, among other things, the availability and cost of capital, prevailing and projected energy prices, demand for hydrocarbons, levels of reserves, geological considerations, environmental or other governmental regulations, the availability of drilling permits, the availability of drilling rigs, and other production and development costs.

Fluctuations in energy prices can also greatly affect the development of new natural gas reserves. In general terms, the prices of natural gas, oil and other hydrocarbon products fluctuate in response to changes in supply and demand, market uncertainty and a variety of additional factors that are beyond our control. These factors include worldwide economic conditions; weather conditions and seasonal trends; the levels of domestic production and consumer demand; the availability of imported LNG; the ability to export LNG; the availability of transportation systems with adequate capacity; the volatility and uncertainty of regional pricing differentials and premiums; the price and availability of alternative fuels; the effect of energy conservation measures; the nature and extent of governmental regulation and taxation; and the anticipated future prices of natural gas, LNG and other commodities. Declines in natural gas prices could have a negative impact on exploration, development and production activity and, if sustained, could lead to a material decrease in such activity. Sustained reductions in exploration or production activity in our areas of operation would lead to reduced utilization of our systems. Because of these factors, even if new natural gas reserves are known to exist in areas served by our assets, producers may choose not to develop those reserves.

We receive cash from royalty payments on our mineral rights positions through our working interests and overriding royalty interests. We are not the operator of the wells from which we receive royalty payments, and therefore, we are not able to control the timing of exploration or development efforts, or associated costs.

Through our subsidiary, CEVCO, we own production rights to approximately 460,000 acres in the Marcellus and Utica shale areas and have subleased the production rights in three storage fields and have also contributed our production rights in one other field. We do not currently operate any of these properties and do not have plans to develop the capacity to operate any of our properties. As owner of both non-operating working interests and overriding royalty interests, we are dependent on contract operators to develop our properties. Our ability to achieve targeted returns on capital in drilling or acquisition activities and to achieve production

19

growth rates will be materially affected by decisions made by our contract operators over which we have little or no control. Such decisions include:

• | the timing and amount of capital expenditures; |

• | the timing of initiating the drilling and recompleting of wells; |

• | the extent of operating costs; |

• | selection of technology and drilling and completion methods; and |

• | the rate of production of reserves, if any. |

If the royalty payments we receive from our sublessees are reduced, our ability to pay dividends to our stockholders could be adversely affected.

Our revenues from CEVCO royalty interests will decrease if production on our subleased production rights declines, which would reduce the amount of cash we have available for the payment of dividends to our stockholders.

The amount of the royalty payments we receive on our subleased production rights depends in part on the amount of production on our properties. In addition, the royalty payments vary with the natural gas liquids and oil content of the production. For example, “dry gas” wells produce mainly natural gas, or methane, as opposed to “wet gas” wells, which produce methane along with other byproducts such as ethane, which may result in additional revenue streams from such production. During 2015 and 2014, natural gas prices remained relatively low, as well as a decrease in oil and natural gas liquids prices, leading some producers to announce significant reductions to their drilling plans. A significant reduction in the level of production on our properties could adversely affect on our ability to pay dividends to our stockholders.

Our operations are subject to environmental laws and regulations that may expose us to significant costs and liabilities and changes in these laws could have a material adverse effect on our results of operations.

Our natural gas transportation activities are subject to stringent and complex federal, state and local environmental laws and regulations. As with the industry generally, compliance with current and anticipated environmental laws and regulations increases our overall cost of business, including our capital costs to construct, maintain and upgrade pipelines and other facilities. For instance, we may be required to obtain and maintain permits and other approvals issued by various federal, state and local governmental authorities; monitor for, limit or prevent releases of materials from our operations in accordance with these permits and approvals; install pollution control equipment or replace aging pipelines and other facilities; limit or prohibit construction activities in sensitive areas such as wetlands, wilderness or urban areas or areas inhabited by endangered or threatened species; and incur potentially substantial new obligations or liabilities for any pollution or contamination that may result from our operations. Under a September 15, 1999 FERC order approving an April 5, 1999 settlement, Columbia Gas Transmission remediates polychlorinated biphenyls (“PCBs”) at specific gas transmission facilities pursuant to a 1995 Administrative Order on Consent (subsequently modified in 1996 and 2007) (“AOC”) and recovers a portion of those costs in rates. Columbia Gas Transmission’s ability to recover these costs ceased on January 31, 2015. As of December 31, 2015, Columbia Gas Transmission had remaining liabilities of $1.8 million to cover costs associated with PCB remediation related to this AOC.

Moreover, new, modified or stricter environmental laws, regulations or enforcement policies could be implemented that significantly increase our or our customer’s compliance costs, pollution mitigation costs, or the cost of any remediation of environmental contamination that may become necessary, and these costs could be material. For example, in October 2015, the U.S. Environmental Protection Agency (“EPA”) issued a final rule under the federal Clean Air Act (“CAA”), lowering the National Ambient Air Quality Standard (“NAAQS”) for ground-level ozone to 70 parts per billion for the 8-hour primary and secondary ozone standards. The EPA is required to make attainment and non-attainment designations for specific geographic locations under the revised standards by October 1, 2017 and, depending on the severity of the ozone present, non-attainment areas will have until between 2020 and 2037 to meet the health standard. With EPA lowering the ground-level ozone standard, states may be required to implement more stringent regulations, which could apply to our or our customers’ operations. Compliance with this final rule could, among other things, require installation of new emission controls, result in longer permitting timelines, and significantly increase capital expenditures and operating costs. In another example, the EPA released a final rule in May 2015 that attempted to clarify federal jurisdiction under the Clean Water Act (“CWA”) over waters of the United States, but a number of legal challenges to this rule are pending, and implementation of the rule has been stayed nationwide. To the extent the rule expands the scope of the CWA’s jurisdiction, we could face increased costs and delays with respect to obtaining permits for dredge and fill activities in wetland

20