Attached files

| file | filename |

|---|---|

| 8-K - FIRST BANCORP. 8-K - FIRST BANCORP /PR/ | a51269231.htm |

| EX-99.1 - EXHIBIT 99.1 - FIRST BANCORP /PR/ | a51269231ex99_1.htm |

|

Exhibit 99.2 |

Financial Results FYE 2015

& 4Q 2015

2 Forward-Looking

Statements This presentation contains “forward-looking statements”

concerning First BanCorp’s (the “Corporation”) future economic

performance. The words or phrases “would be,” “will allow,” “intends

to,” “will likely result,” “are expected to,” “expect,” “anticipate,”

“look forward,” “should,” “believes” and similar expressions are meant

to identify “forward-looking statements” within the meaning of Section

27A of the Private Securities Litigation Reform Act of 1995, and are

subject to the safe harbor created by such section. The Corporation

wishes to caution readers not to place undue reliance on any such

“forward-looking statements,” which speak only as of the date made, and

to advise readers that various factors, including, but not limited to,

uncertainty about whether the Corporation and FirstBank Puerto Rico

(“FirstBank” or “the Bank”) will be able to fully comply with the

written agreement dated June 3, 2010 that the Corporation entered into

with the Federal Reserve Bank of New York (the “FED”) and the order

dated June 2, 2010 (the “Order”)that FirstBank entered into with the

FDIC and the Office of the Commissioner of Financial Institutions of

Puerto Rico that, among other things, require FirstBank to maintain

certain capital levels and reduce its special mention, classified,

delinquent and non-performing assets; the risk of being subject to

possible additional regulatory actions; uncertainty as to the

availability of certain funding sources, such as retail brokered CDs;

the Corporation’s reliance on brokered CDs and its ability to obtain, on

a periodic basis, approval from the FDIC to issue brokered CDs to fund

operations and provide liquidity in accordance with the terms of the

Order; the risk of not being able to fulfill the Corporation’s cash

obligations or resume paying dividends to the Corporation’s stockholders

in the future due to the Corporation’s inability to receive approval

from the FED to receive dividends from FirstBank or FirstBank’s failure

to generate sufficient cash flow to make a dividend payment to the

Corporation; the strength or weakness of the real estate markets and of

the consumer and commercial credit sectors and their impact on the

credit quality of the Corporation’s loans and other assets, including

the Corporation’s construction and commercial real estate loan

portfolios, which have contributed and may continue to contribute to,

among other things, the high levels of non-performing assets,

charge-offs and the provision expense and may subject the Corporation to

further risk from loan defaults and foreclosures; adverse changes in

general economic conditions in the United States and in Puerto Rico,

including the interest rate scenario, market liquidity, housing

absorption rates, real estate prices and disruptions in the U.S. capital

markets, which may reduce interest margins, impact funding sources and

affect demand for all of the Corporation’s products and services and the

value of the Corporation’s assets; an adverse change in the

Corporation’s ability to attract new clients and retain existing ones; a

decrease in demand for the Corporation’s products and services and lower

revenues and earnings because of the continued recession in Puerto Rico

and the current fiscal problems and budget deficit of the Puerto Rico

government; uncertainty about regulatory and legislative changes for

financial services companies in Puerto Rico, the United States and the

U.S. and British Virgin Islands, which could affect the Corporation’s

financial performance and could cause the Corporation’s actual results

for future periods to differ materially from prior results and

anticipated or projected results; uncertainty about the effectiveness of

the various actions undertaken to stimulate the United States economy

and stabilize the United States’ financial markets, and the impact such

actions may have on the Corporation’s business, financial condition and

results of operations; changes in the fiscal and monetary policies and

regulations of the federal government, including those determined by the

Federal Reserve System, the FDIC, government-sponsored housing agencies

and regulators in Puerto Rico and the U.S. and British Virgin Islands;

the risk of possible failure or circumvention of controls and procedures

and the risk that the Corporation’s risk management policies may not be

adequate; the risk that the FDIC may further increase the deposit

insurance premium and/or require special assessments to replenish its

insurance fund, causing an additional increase in the Corporation’s

non-interest expense; risks of not being able to recover the assets

pledged to Lehman Brothers Special Financing, Inc.; the impact on the

Corporation’s results of operations and financial condition associated

with acquisitions and dispositions; a need to recognize additional

impairments on financial instruments or goodwill relating to

acquisitions; risks that downgrades in the credit ratings of the

Corporation’s long-term senior debt will adversely affect the

Corporation’s ability to access necessary external funds; the impact of

the Dodd-Frank Wall Street Reform and Consumer Protection Act on the

Corporation’s businesses, business practices and cost of operations; and

general competitive factors and industry consolidation. The Corporation

does not undertake, and specifically disclaims any obligation, to update

any “forward-looking statements” to reflect occurrences or unanticipated

events or circumstances after the date of such statements except as

required by the federal securities laws. Investors should refer to the

Corporation’s Annual Report on Form 10-K for the year ended December 31,

2013 for a discussion of such factors and certain risks and

uncertainties to which the Corporation is subject.

Agenda Fiscal Year & Fourth

Quarter 2015 Highlights Aurelio Alemán, President & Chief Executive

Officer Fiscal Year & Fourth Quarter 2015 Results of Operations Orlando

Berges, Executive Vice President & Chief Financial Officer Questions &

Answers 3

Fiscal Year 2015 & Fourth

Quarter Results Key Highlights 4

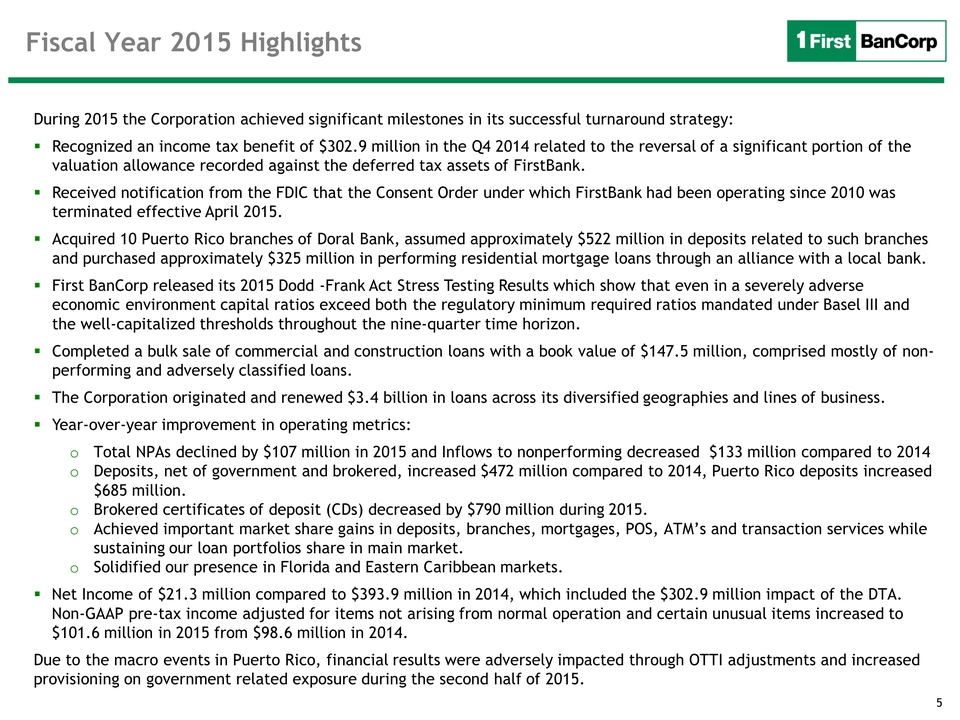

Fiscal Year 2015 Highlights

During 2015 the Corporation achieved significant milestones in its

successful turnaround strategy: Recognized an income tax benefit of

$302.9 million in the Q4 2014 related to the reversal of a significant

portion of the valuation allowance recorded against the deferred tax

assets of FirstBank. Received notification from the FDIC that the

Consent Order under which FirstBank had been operating since 2010 was

terminated effective April 2015. Acquired 10 Puerto Rico branches of

Doral Bank, assumed approximately $522 million in deposits related to

such branches and purchased approximately $325 million in performing

residential mortgage loans through an alliance with a local bank. First

BanCorp released its 2015 Dodd -Frank Act Stress Testing Results which

show that even in a severely adverse economic environment capital ratios

exceed both the regulatory minimum required ratios mandated under Basel

III and the well-capitalized thresholds throughout the nine-quarter time

horizon. Completed a bulk sale of commercial and construction loans with

a book value of $147.5 million, comprised mostly of non-performing and

adversely classified loans. The Corporation originated and renewed $3.4

billion in loans across its diversified geographies and lines of

business. Year-over-year improvement in operating metrics: Total NPAs

declined by $107 million in 2015 and Inflows to nonperforming decreased

$133 million compared to 2014 Deposits, net of government and brokered,

increased $472 million compared to 2014, Puerto Rico deposits increased

$685 million. Brokered certificates of deposit (CDs) decreased by $790

million during 2015. Achieved important market share gains in deposits,

branches, mortgages, POS, ATM’s and transaction services while

sustaining our loan portfolios share in main market. Solidified our

presence in Florida and Eastern Caribbean markets. Net Income of $21.3

million compared to $393.9 million in 2014, which included the $302.9

million impact of the DTA. Non-GAAP pre-tax income adjusted for items

not arising from normal operation and certain unusual items increased to

$101.6 million in 2015 from $98.6 million in 2014. Due to the macro

events in Puerto Rico, financial results were adversely impacted through

OTTI adjustments and increased provisioning on government related

exposure during the second half of 2015. 5

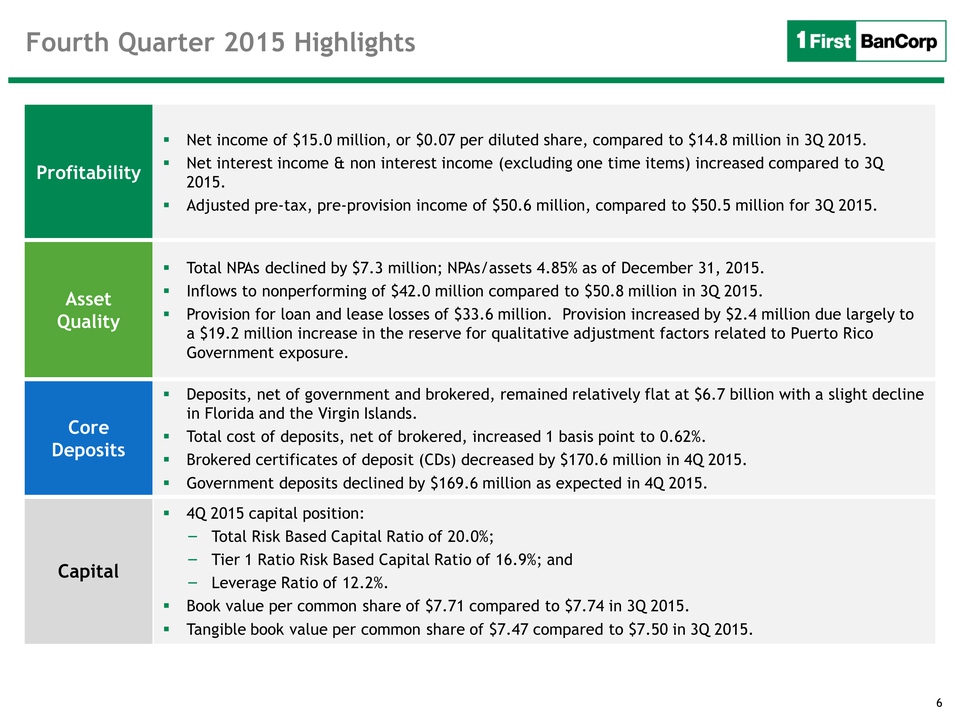

6 Profitability RNet income

of $15.0 million, or $0.07 per diluted share, compared to $14.8 million

in 3Q 2015. Net interest income & non interest income (excluding one

time items) increased compared to 3Q 2015. Adjusted pre-tax,

pre-provision income of $50.6 million, compared to $50.5 million for 3Q

2015. Asset Quality Total NPAs declined by $7.3 million; NPAs/assets

4.85% as of December 31, 2015. Inflows to nonperforming of $42.0 million

compared to $50.8 million in 3Q 2015. Provision for loan and lease

losses of $33.6 million. Provision increased by $2.4 million due largely

to a $19.2 million increase in the reserve for qualitative adjustment

factors related to Puerto Rico Government exposure. Core Deposits

Deposits, net of government and brokered, remained relatively flat at

$6.7 billion with a slight decline in Florida and the Virgin Islands.

Total cost of deposits, net of brokered, increased 1 basis point to

0.62%. Brokered certificates of deposit (CDs) decreased by $170.6

million in 4Q 2015. Government deposits declined by $169.6 million as

expected in 4Q 2015. Capital 4Q 2015 capital position: Total Risk Based

Capital Ratio of 20.0%; Tier 1 Ratio Risk Based Capital Ratio of 16.9%;

and Leverage Ratio of 12.2%. Book value per common share of $7.71

compared to $7.74 in 3Q 2015. Tangible book value per common share of

$7.47 compared to $7.50 in 3Q 2015.

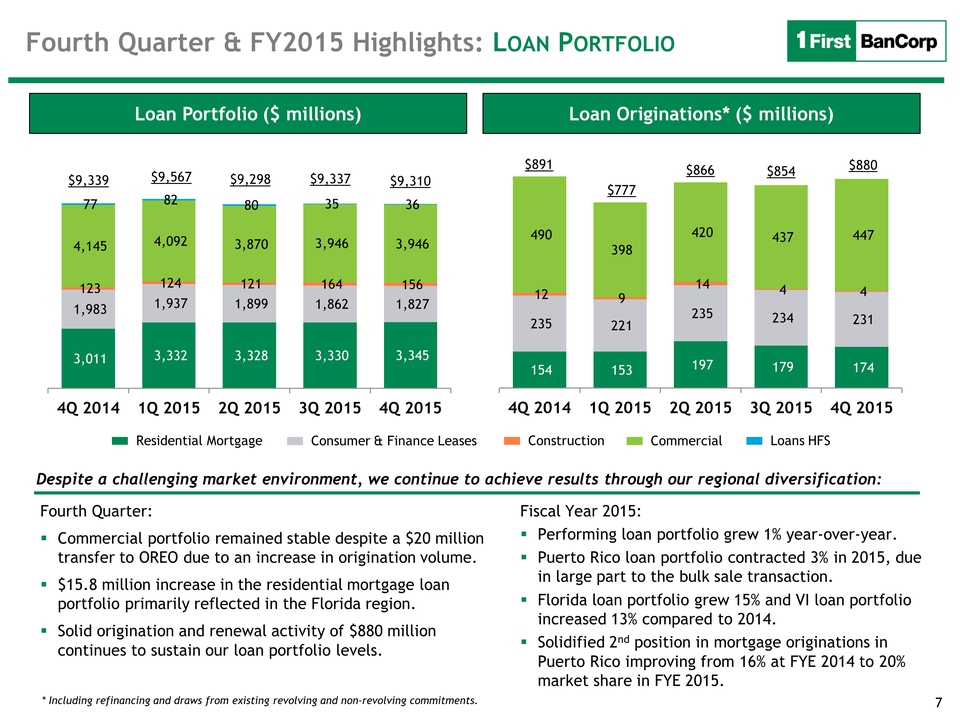

7 Loan Originations* ($

millions) Loan Portfolio ($ millions) 3,011 3,332 3,328 3,330 3,345

1,983 1,937 1,899 1,862 1,827 123 124 121 164 156 4,145 4,092 3,870

3,946 3,946 77 82 80 35 36 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015$9,339

$9,567 154 153 197 179 174 235 221 235 234 231 12 9 14 4 4 490 398 420

437 447 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015 $880 $891 $777

Residential Mortgage Consumer & Finance Leases Construction Commercial

Loans HFS Fourth Quarter: Commercial portfolio remained stable despite a

$20 million transfer to OREO due to an increase in origination volume.

$15.8 million increase in the residential mortgage loan portfolio

primarily reflected in the Florida region. Solid origination and renewal

activity of $880 million continues to sustain our loan portfolio levels.

Fiscal Year 2015: Performing loan portfolio grew 1% year-over-year.

Puerto Rico loan portfolio contracted 3% in 2015, due in large part to

the bulk sale transaction. Florida loan portfolio grew 15% and VI loan

portfolio increased 13% compared to 2014. Solidified 2nd position in

mortgage originations in Puerto Rico improving from 16% at FYE 2014 to

20% market share in FYE 2015. Despite a challenging market environment,

we continue to achieve results through our regional diversification: *

Including refinancing and draws from existing revolving and

non-revolving commitments. Fourth Quarter & FY2015 Highlights: LOAN

PORTFOLIO $9,298 $866 $9,337 $854 $9,310

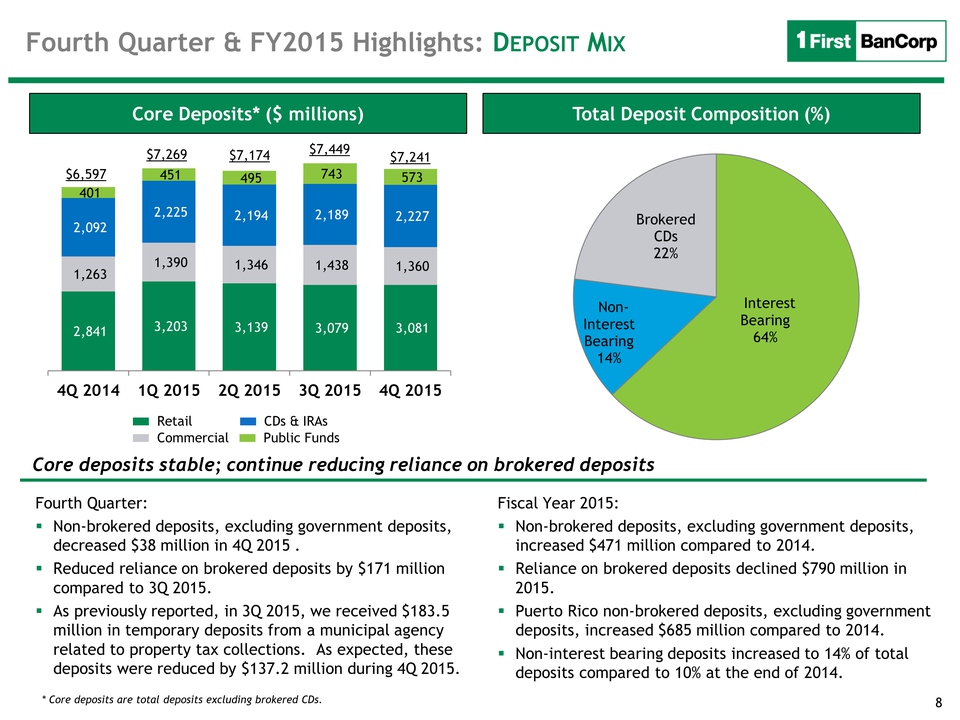

8 Total Deposit Composition

(%) Core Deposits* ($ millions) 2,841 3,203 3,139 3,079 3,081 1,263

1,390 1,346 1,438 1,360 2,092 2,225 2,194 2,189 2,227 401 451 495 743

573 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015 * Core deposits are total

deposits excluding brokered CDs. $6,597 $7,269 Interest Bearing 64%

Non-Interest Bearing 14% Brokered CDs 22% Fourth Quarter: Non-brokered

deposits, excluding government deposits, decreased $38 million in 4Q

2015 . Reduced reliance on brokered deposits by $171 million compared to

3Q 2015. As previously reported, in 3Q 2015, we received $183.5 million

in temporary deposits from a municipal agency related to property tax

collections. As expected, these deposits were reduced by $137.2 million

during 4Q 2015. Core deposits stable; continue reducing reliance on

brokered deposits Fourth Quarter & FY2015 Highlights: DEPOSIT MIX Retail

Commercial CDs & IRAs Public Funds $7,174 $7,449 $7,241 Fiscal Year

2015: Non-brokered deposits, excluding government deposits, increased

$471 million compared to 2014. Reliance on brokered deposits declined

$790 million in 2015. Puerto Rico non-brokered deposits, excluding

government deposits, increased $685 million compared to 2014.

Non-interest bearing deposits increased to 14% of total deposits

compared to 10% at the end of 2014.

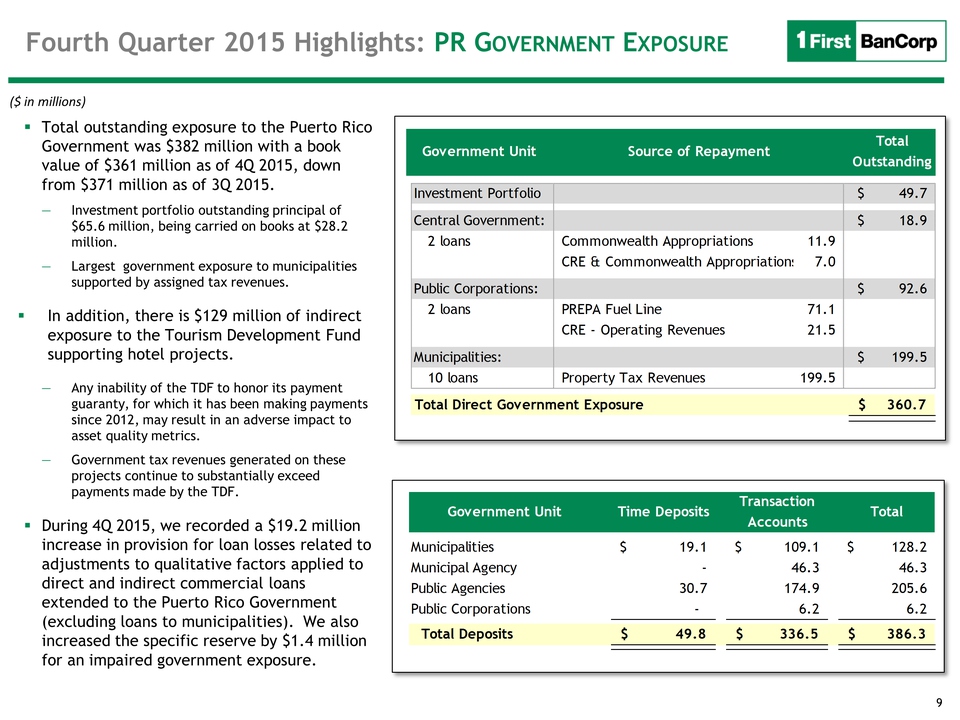

9 Fourth Quarter 2015

Highlights: PR GOVERNMENT EXPOSURE Total outstanding exposure to the

Puerto Rico Government was $382 million with a book value of $361

million as of 4Q 2015, down from $371 million as of 3Q 2015. Investment

portfolio outstanding principal of $65.6 million, being carried on books

at $28.2 million. Largest government exposure to municipalities

supported by assigned tax revenues. In addition, there is $129 million

of indirect exposure to the Tourism Development Fund supporting hotel

projects. Any inability of the TDF to honor its payment guaranty, for

which it has been making payments since 2012, may result in an adverse

impact to asset quality metrics. Government tax revenues generated on

these projects continue to substantially exceed payments made by the

TDF. During 4Q 2015, we recorded a $19.2 million increase in provision

for loan losses related to adjustments to qualitative factors applied to

direct and indirect commercial loans extended to the Puerto Rico

Government (excluding loans to municipalities). We also increased the

specific reserve by $1.4 million for an impaired government exposure. ($

in millions) Investment Portfolio49.7$ Central Government:18.9$ 2

loans11.97.0Public Corporations:92.6$ 2 loans71.1CRE - Operating

Revenues21.5Municipalities:199.5$ 10 loans199.5Total Direct Government

Exposure360.7$ Government UnitSource of RepaymentTotal

OutstandingProperty Tax RevenuesCommonwealth AppropriationsCRE &

Commonwealth AppropriationsPREPA Fuel LineGovernment UnitTime

DepositsTransaction AccountsTotalMunicipalities19.1$ 109.1$ 128.2$

Municipal Agency- 46.3 46.3 Public Agencies30.7 174.9 205.6 Public

Corporations- 6.2 6.2 Total Deposits49.8$ 336.5$ 386.3

10 Fourth Quarter

ResultsResults of Operations

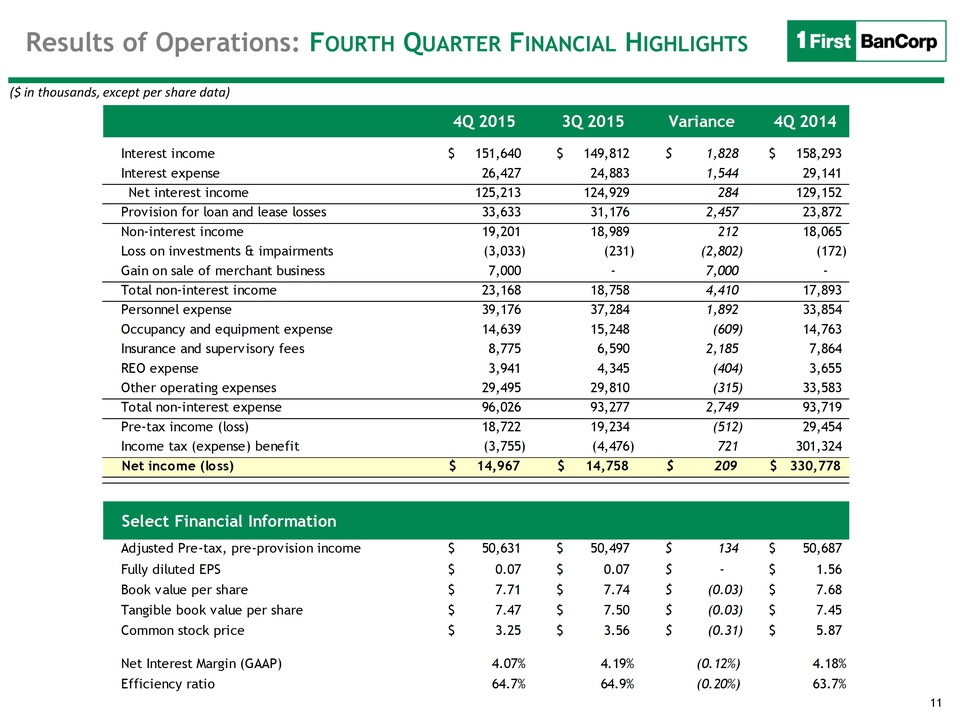

11 Results of Operations:

FOURTH QUARTER FINANCIAL HIGHLIGHTS ($ in thousands, except per share

data) Select Financial Information 4Q 20153Q 2015Variance4Q 2014Interest

income151,640$ 149,812$ 1,828$ 158,293$ Interest expense26,427 24,883

1,544 29,141 Net interest income125,213 124,929 284 129,152 Provision

for loan and lease losses33,633 31,176 2,457 23,872 Non-interest

income19,201 18,989 212 18,065 Loss on investments & impairments(3,033)

(231) (2,802) (172) Gain on sale of merchant business7,000 - 7,000 -

Total non-interest income23,168 18,758 4,410 17,893 Personnel

expense39,176 37,284 1,892 33,854 Occupancy and equipment expense14,639

15,248 (609) 14,763 Insurance and supervisory fees8,775 6,590 2,185

7,864 REO expense3,941 4,345 (404) 3,655 Other operating expenses29,495

29,810 (315) 33,583 Total non-interest expense96,026 93,277 2,749 93,719

Pre-tax income (loss)18,722 19,234 (512) 29,454 Income tax (expense)

benefit(3,755) (4,476) 721 301,324 Net income (loss)14,967$ 14,758$ 209$

330,778$ Select Financial InformationAdjusted Pre-tax, pre-provision

income50,631$ 50,497$ 134$ 50,687$ Fully diluted EPS0.07$ 0.07$ -$ 1.56$

Book value per share7.71$ 7.74$ (0.03)$ 7.68$ Tangible book value per

share7.47$ 7.50$ (0.03)$ 7.45$ Common stock price3.25$ 3.56$ (0.31)$

5.87$ Net Interest Margin (GAAP)4.07%4.19%(0.12%)4.18%Efficiency

ratio64.7%64.9%(0.20%)63.7%

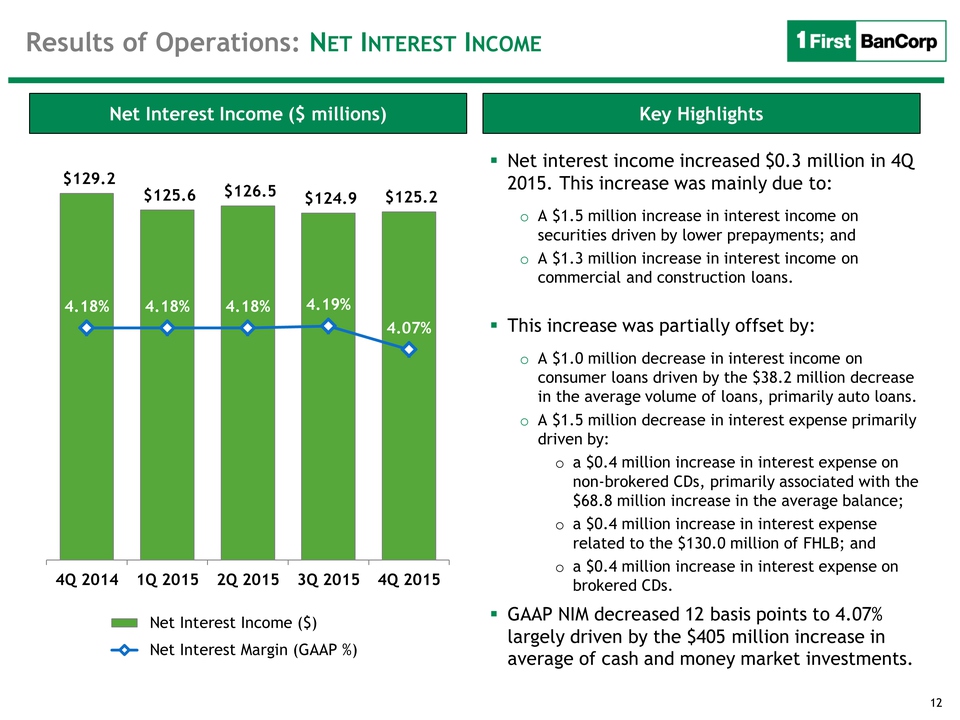

12 Key Highlights Net

Interest Income ($ millions) $129.2 $125.6 $126.5 $124.9 $125.2 4.18%

4.18% 4.18% 4.19% 4.07% 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015 Net

Interest Income ($) Net Interest Margin (GAAP %) Net interest income

increased $0.3 million in 4Q 2015. This increase was mainly due to: oA

$1.5 million increase in interest income on securities driven by lower

prepayments; and oA $1.3 million increase in interest income on

commercial and construction loans. This increase was partially offset

by: oA $1.0 million decrease in interest income on consumer loans driven

by the $38.2 million decrease in the average volume of loans, primarily

auto loans. oA $1.5 million decrease in interest expense primarily

driven by: oa $0.4 million increase in interest expense on non-brokered

CDs, primarily associated with the $68.8 million increase in the average

balance; oa $0.4 million increase in interest expense related to the

$130.0 million of FHLB; and oa $0.4 million increase in interest expense

on brokered CDs. GAAP NIM decreased 12 basis points to 4.07% largely

driven by the $405 million increase in average of cash and money market

investments. Results of Operations: NET INTEREST INCOME

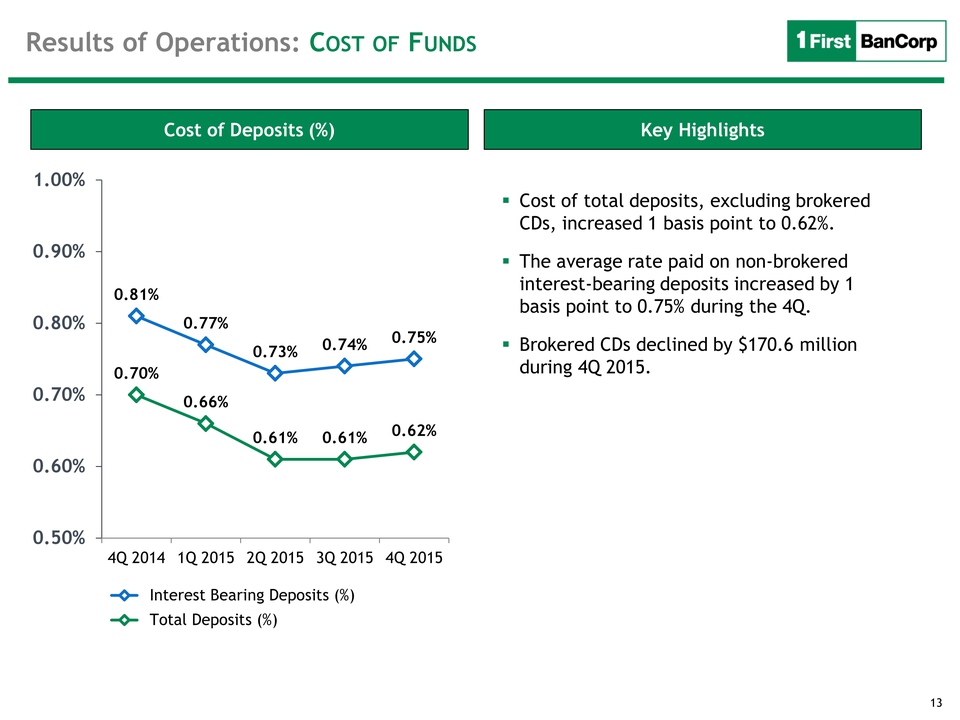

13 Key Highlights Cost of

Deposits (%) 0.81% 0.77% 0.73% 0.74% 0.75% 0.70% 0.66% 0.61% 0.61% 0.62%

0.50% 0.60% 0.70% 0.80% 0.90% 1.00% 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q

2015 Interest Bearing Deposits (%) Total Deposits (%) Cost of total

deposits, excluding brokered CDs, increased 1 basis point to 0.62%. The

average rate paid on non-brokered interest-bearing deposits increased by

1 basis point to 0.75% during the 4Q. Brokered CDs declined by $170.6

million during 4Q 2015. Results of Operations: COST OF FUNDS

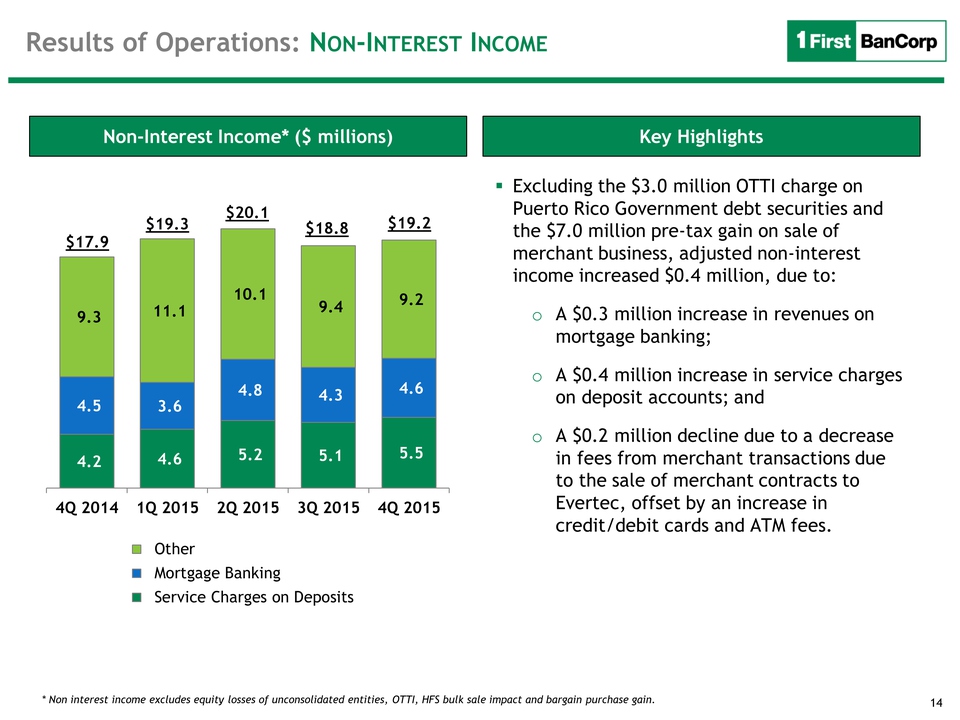

14 Key Highlights

Non-Interest Income* ($ millions) 4.2 4.6 5.2 5.1 5.5 4.5 3.6 4.8 4.3

4.6 9.3 11.1 10.1 9.4 9.2 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015 Other

Mortgage Banking Service Charges on Deposits* Non interest income

excludes equity losses of unconsolidated entities, OTTI, HFS bulk sale

impact and bargain purchase gain. Excluding the $3.0 million OTTI charge

on Puerto Rico Government debt securities and the $7.0 million pre-tax

gain on sale of merchant business, adjusted non-interest income

increased $0.4 million, due to: oA $0.3 million increase in revenues on

mortgage banking; oA $0.4 million increase in service charges on deposit

accounts; and oA $0.2 million decline due to a decrease in fees from

merchant transactions due to the sale of merchant contracts to Evertec,

offset by an increase in credit/debit cards and ATM fees. $19.2 $17.9

$19.3 Results of Operations: NON-INTEREST INCOME $20.1 $18.8

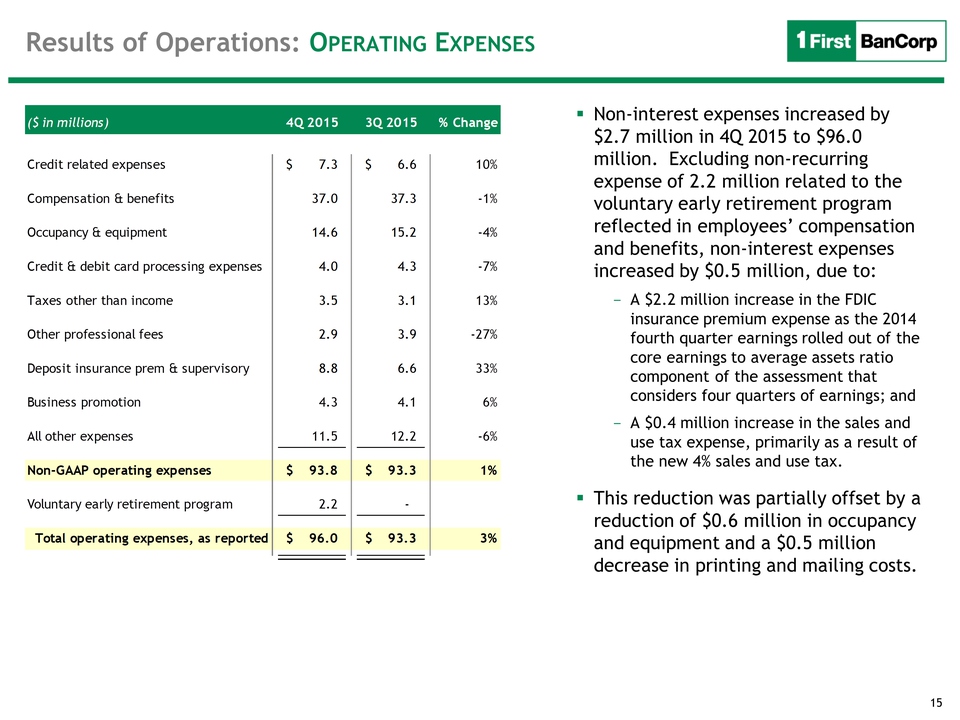

15 Results of Operations:

OPERATING EXPENSES Non-interest expenses increased by $2.7 million in 4Q

2015 to $96.0 million. Excluding non-recurring expense of 2.2 million

related to the voluntary early retirement program reflected in

employees’ compensation and benefits, non-interest expenses increased by

$0.5 million, due to: A $2.2 million increase in the FDIC insurance

premium expense as the 2014 fourth quarter earnings rolled out of the

core earnings to average assets ratio component of the assessment that

considers four quarters of earnings; and A $0.4 million increase in the

sales and use tax expense, primarily as a result of the new 4% sales and

use tax. This reduction was partially offset by a reduction of $0.6

million in occupancy and equipment and a $0.5 million decrease in

printing and mailing costs. ($ in millions)4Q 20153Q 2015% ChangeCredit

related expenses7.3$ 6.6$ 10%Compensation & benefits37.0 37.3

-1%Occupancy & equipment14.6 15.2 -4%Credit & debit card processing

expenses4.0 4.3 -7%Taxes other than income3.5 3.1 13%Other professional

fees2.9 3.9 -27%Deposit insurance prem & supervisory8.8 6.6 33%Business

promotion4.3 4.1 6%All other expenses11.5 12.2 -6%Non-GAAP operating

expenses93.8$ 93.3$ 1%Voluntary early retirement program 2.2 - Total

operating expenses, as reported96.0$ 93.3$ 3%

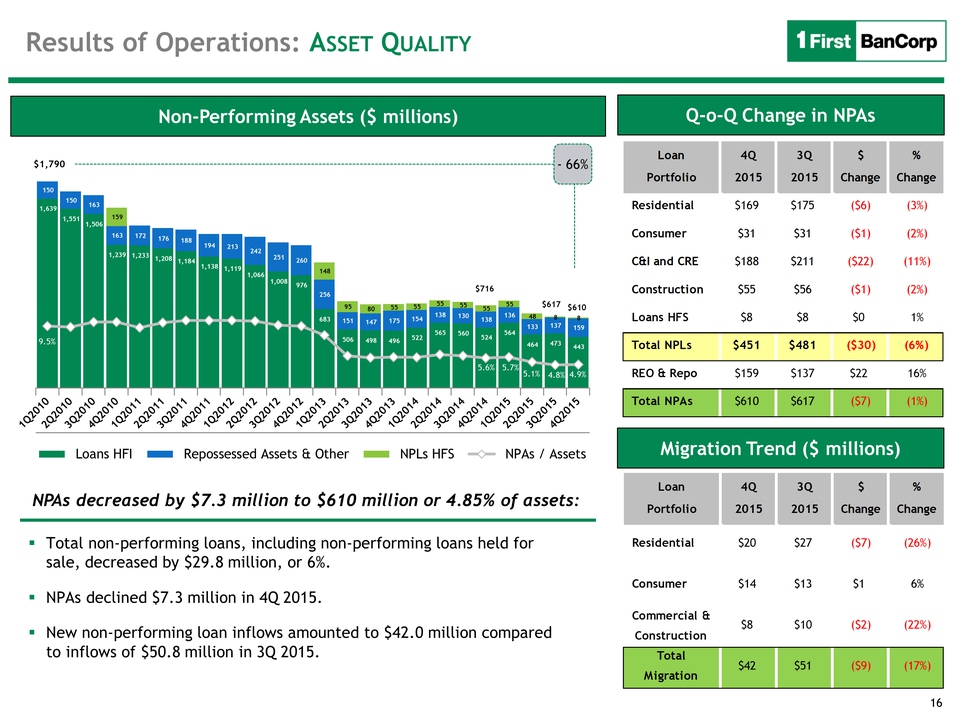

16 Non-Performing Assets ($

millions) Total non-performing loans, including non-performing loans

held for sale, decreased by $29.8 million, or 6%. NPAs declined $7.3

million in 4Q 2015. New non-performing loan inflows amounted to $42.0

million compared to inflows of $50.8 million in 3Q 2015. NPAs decreased

by $7.3 million to $610 million or 4.85% of assets: Results of

Operations: ASSET QUALITY Q-o-Q Change in NPAs Migration Trend ($

millions) 1,639 1,551 1,506 1,239 1,233 1,208 1,184 1,138 1,119 1,066

1,008 976 683 506 498 496 522 565 560 524 564 464 473 443 150 150 163

163 172 176 188 194 213 242 251 260 256 151 147 175 154 138 130 138 136

133 137 159 159 148 95 80 55 55 55 55 55 55 48 8 8 9.5% 5.6% 5.7% 5.1%

4.8% 4.9% Loans HFI Repossessed Assets & Other NPLs HFS NPAs /

Assets$1,790 $610 $716 $617 - 66% Loan4 Q3Q$% Portfolio 20152015Change

ChangeResidential $169$175($6)(3%) Consumer $31 $31($1)(2%)C&I and

CRE$188 $211 ($22)(11%) Construction $55$56($1)(2%) Loans

HFS$8$8$01%Total NPLs$451$481($30)(6%)REO & Repo$159$137$2216%Total

NPAs$610$617($7)(1%)Loan4Q3Q$%Portfolio20152015ChangeChangeResidential$20$27($7)(26%)Consumer$14$13$16%$8$10($2)(22%)$42$51($9)(17%)

Commercial & Construction Total Migration

17 Key Highlights Net

Charge-Offs ($ millions) 7 5 3 5 5 19 16 11 14 12 2 8 62 5 5 4Q 2014 1Q

2015 2Q 2015 3Q 2015 4Q 2015 Residential Consumer Commercial

Construction$22 Total net charge-offs for 3Q 2015 were $22 million, or

0.95% of average loans, compared to $24 million in 3Q 2015. Allowance

coverage ratio of 2.60% as of December 31, 2015 compared to 2.46% as of

September 30, 2015. The ratio of the allowance to NPLs held for

investment was 54.36% as of December 31, 2015 compared to 48.44% as of

September30, 2015. $27 $29 Commercial NPLs (Includes HFS) *Net Carrying

Amount = % of unpaid principal balance net of reserves and accumulated

charge-offs. Results of Operations: NET CHARGE-OFFS $79 $24 ProductBook

ValueAccum. Charge-offsReservesNet Carrying Amount

*C&I$137.1$32.6$16.571.1%Const.62.8 89.5 0.9 40.6%CRE51.3 23.7 3.8

63.4%Total$251.2$145.8$21.257.9%

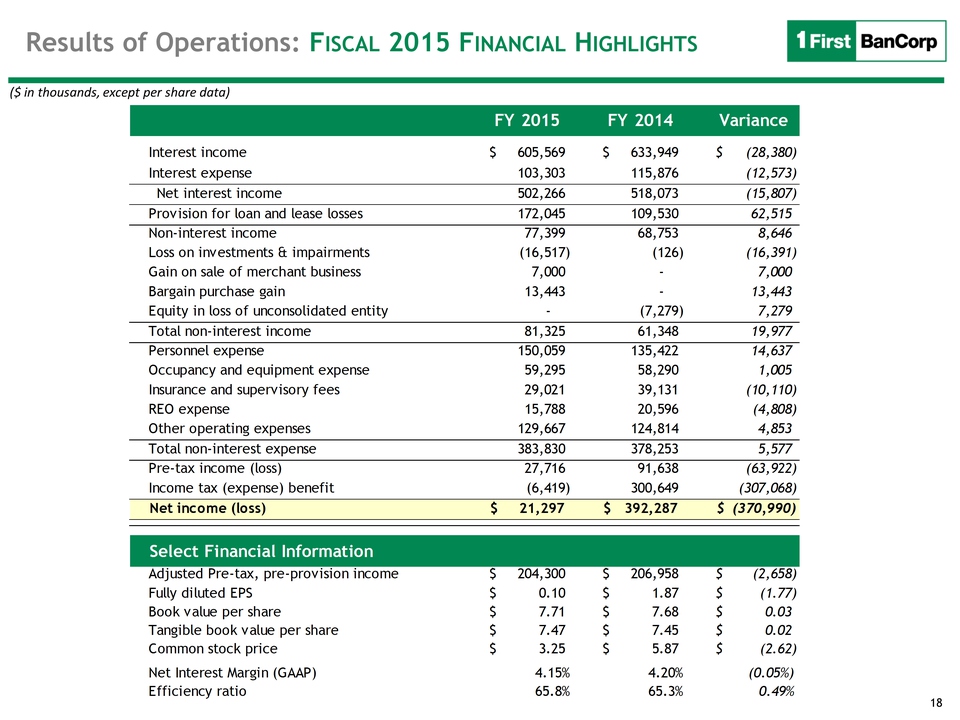

18 Results of Operations:

FISCAL 2015 FINANCIAL HIGHLIGHTS ($ in thousands, except per share data)

Select Financial Information FY 2015FY 2014VarianceInterest

income605,569$ 633,949$ (28,380)$ Interest expense103,303 115,876

(12,573) Net interest income502,266 518,073 (15,807) Provision for loan

and lease losses172,045 109,530 62,515 Non-interest income77,399 68,753

8,646 Loss on investments & impairments(16,517) (126) (16,391) Gain on

sale of merchant business7,000 - 7,000 Bargain purchase gain13,443 -

13,443 Equity in loss of unconsolidated entity- (7,279) 7,279 Total

non-interest income81,325 61,348 19,977 Personnel expense150,059 135,422

14,637 Occupancy and equipment expense59,295 58,290 1,005 Insurance and

supervisory fees29,021 39,131 (10,110) REO expense15,788 20,596 (4,808)

Other operating expenses129,667 124,814 4,853 Total non-interest

expense383,830 378,253 5,577 Pre-tax income (loss)27,716 91,638 (63,922)

Income tax (expense) benefit(6,419) 300,649 (307,068) Net income

(loss)21,297$ 392,287$ (370,990)$ Select Financial InformationAdjusted

Pre-tax, pre-provision income204,300$ 206,958$ (2,658)$ Fully diluted

EPS0.10$ 1.87$ (1.77)$ Book value per share7.71$ 7.68$ 0.03$ Tangible

book value per share7.47$ 7.45$ 0.02$ Common stock price3.25$ 5.87$

(2.62)$ Net Interest Margin (GAAP)4.15%4.20%(0.05%)Efficiency

ratio65.8%65.3%0.49%

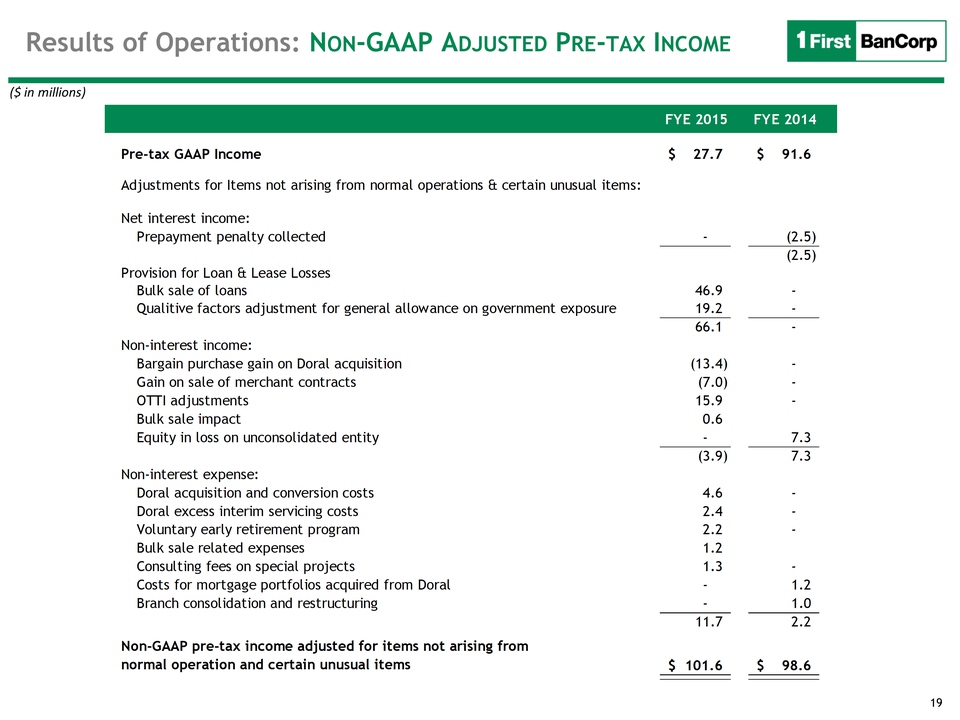

19 ($ in millions) Select

Financial Information Results of Operations: NON-GAAP ADJUSTED PRE-TAX

INCOME FYE 2015FYE 2014Pre-tax GAAP Income27.7$ 91.6$ Adjustments for

Items not arising from normal operations & certain unusual items:Net

interest income: Prepayment penalty collected- (2.5) (2.5) Provision for

Loan & Lease Losses Bulk sale of loans46.9 - Qualitive factors

adjustment for general allowance on government exposure19.2 - 66.1 -

Non-interest income: Bargain purchase gain on Doral acquisition(13.4) -

Gain on sale of merchant contracts(7.0) - OTTI adjustments15.9 - Bulk

sale impact0.6 Equity in loss on unconsolidated entity- 7.3 (3.9) 7.3

Non-interest expense: Doral acquisition and conversion costs4.6 - Doral

excess interim servicing costs2.4 - Voluntary early retirement

program2.2 - Bulk sale related expenses1.2 Consulting fees on special

projects1.3 - Costs for mortgage portfolios acquired from Doral- 1.2

Branch consolidation and restructuring- 1.0 11.7 2.2 Non-GAAP pre-tax

income adjusted for items not arising from normal operation and certain

unusual items101.6$ 98.6$

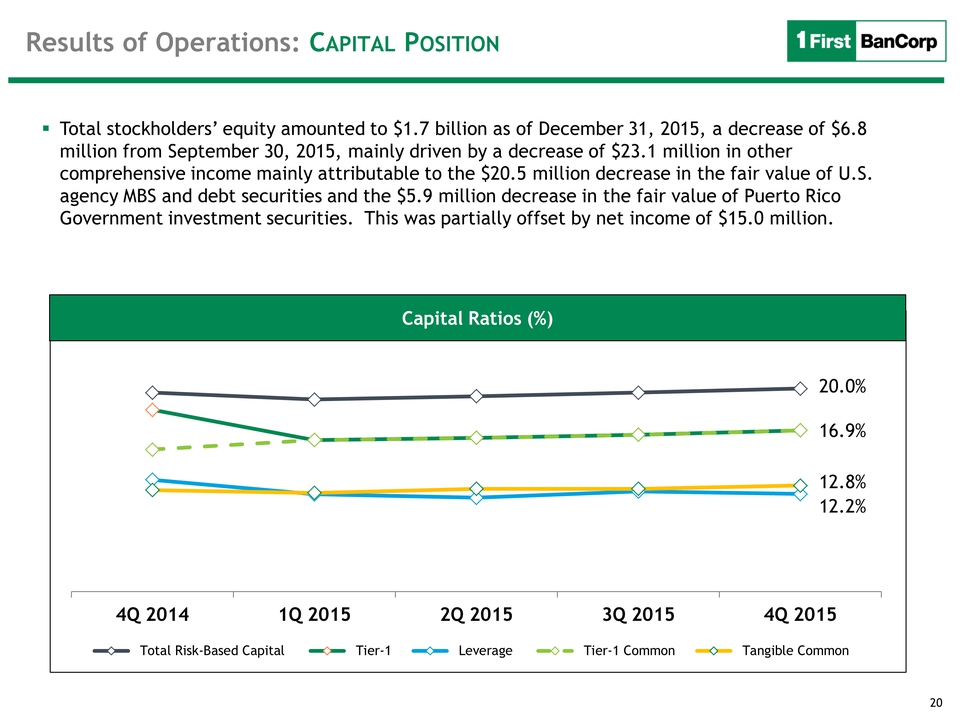

20 Results of Operations:

CAPITAL POSITION Capital Ratios (%) Total stockholders’ equity amounted

to $1.7 billion as of December 31, 2015, a decrease of $6.8 million from

September 30, 2015, mainly driven by a decrease of $23.1 million in

other comprehensive income mainly attributable to the $20.5 million

decrease in the fair value of U.S. agency MBS and debt securities and

the $5.9 million decrease in the fair value of Puerto Rico Government

investment securities. This was partially offset by net income of $15.0

million. Capital Ratios (%) 20.0% 12.2% 16.9% 12.8% 4Q 2014 1Q 2015 2Q

2015 3Q 2015 4Q 2015 Total Risk-Based Capital Tier-1 Leverage Tier-1

Common Tangible Common

21 Fiscal Year 2015 &

Fourth Quarter Results Q & A

22 Fourth Quarter Results

exhibits

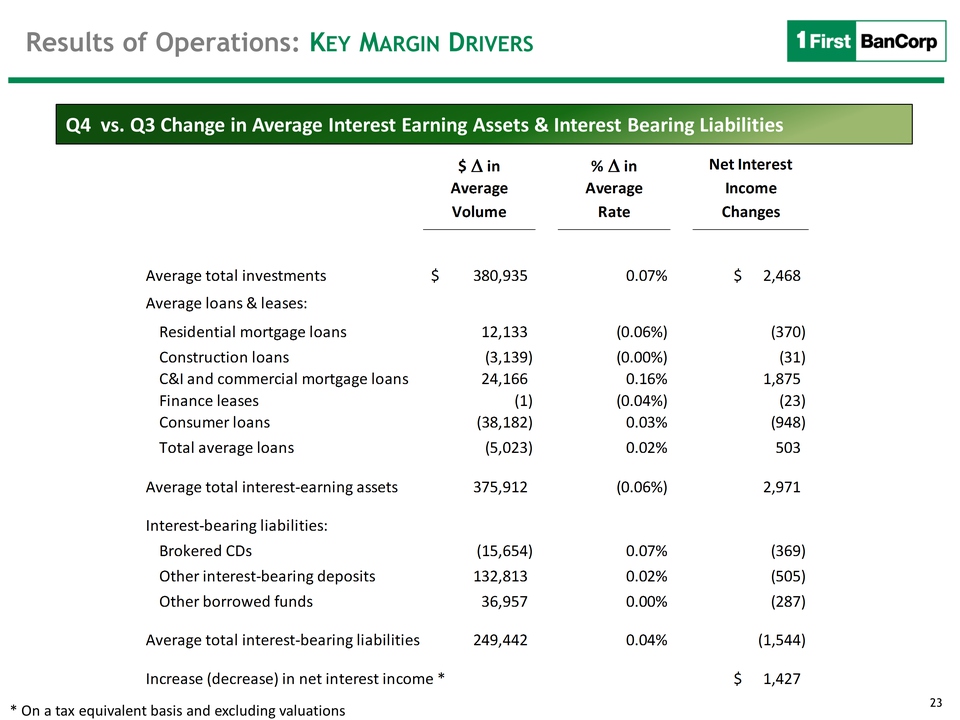

23 Results of Operations:

KEY MARGIN DRIVERS Q4 vs. Q3 Change in Average Interest Earning Assets &

Interest Bearing Liabilities * On a tax equivalent basis and excluding

valuations $ Δ in % Δ in AverageAverageVolumeRateAverage total

investments380,935$ 0.07%2,468$ Average loans & leases:Residential

mortgage loans12,133 (0.06%)(370) Construction loans(3,139) (0.00%)(31)

C&I and commercial mortgage loans24,166 0.16%1,875 Finance leases(1)

(0.04%)(23) Consumer loans(38,182) 0.03%(948) Total average loans(5,023)

0.02%503 Average total interest-earning assets375,912 (0.06%)2,971

Interest-bearing liabilities:Brokered CDs(15,654) 0.07%(369) Other

interest-bearing deposits132,813 0.02%(505) Other borrowed funds36,957

0.00%(287) Average total interest-bearing liabilities249,442

0.04%(1,544) Increase (decrease) in net interest income *1,427$ Net

InterestIncomeChangesExhibits

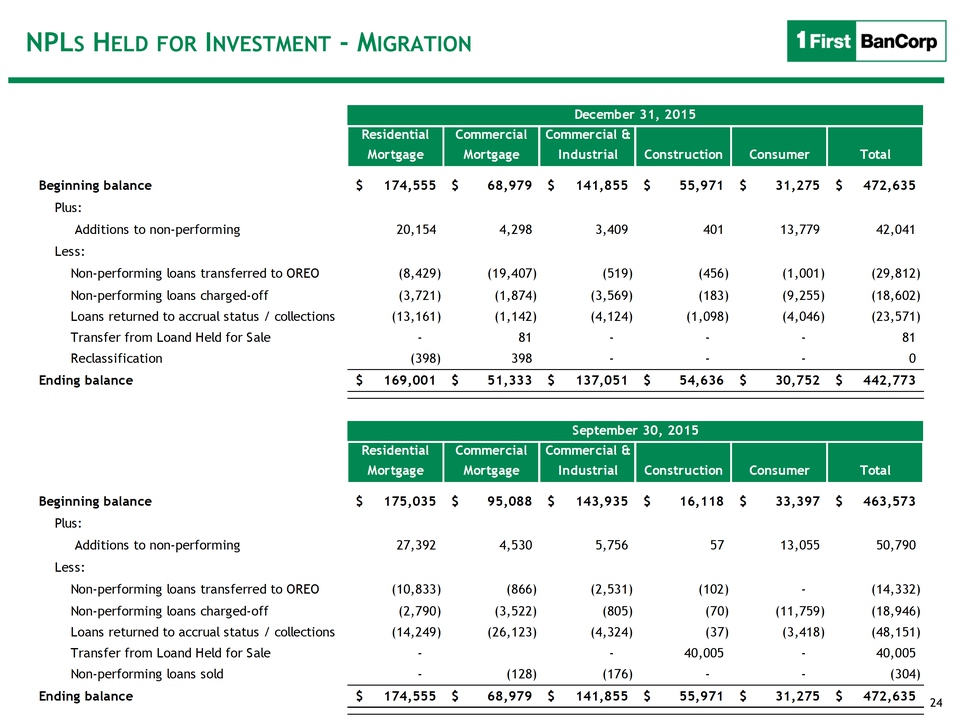

24 NPLS HELD FOR INVESTMENT

- MIGRATION Residential MortgageCommercial MortgageCommercial &

IndustrialConstructionConsumerTotalBeginning balance174,555$ 68,979$

141,855$ 55,971$ 31,275$ 472,635$ Plus: Additions to

non-performing20,154 4,298 3,409 401 13,779 42,041 Less: Non-performing

loans transferred to OREO(8,429) (19,407) (519) (456) (1,001) (29,812)

Non-performing loans charged-off(3,721) (1,874) (3,569) (183) (9,255)

(18,602) Loans returned to accrual status / collections(13,161) (1,142)

(4,124) (1,098) (4,046) (23,571) Transfer from Loand Held for Sale- 81 -

- - 81 Reclassification(398) 398 - - - 0 Ending balance169,001$ 51,333$

137,051$ 54,636$ 30,752$ 442,773$ Residential MortgageCommercial

MortgageCommercial & IndustrialConstructionConsumerTotalBeginning

balance175,035$ 95,088$ 143,935$ 16,118$ 33,397$ 463,573$ Plus:

Additions to non-performing27,392 4,530 5,756 57 13,055 50,790 Less:

Non-performing loans transferred to OREO(10,833) (866) (2,531) (102) -

(14,332) Non-performing loans charged-off(2,790) (3,522) (805) (70)

(11,759) (18,946) Loans returned to accrual status / collections(14,249)

(26,123) (4,324) (37) (3,418) (48,151) Transfer from Loand Held for

Sale- - 40,005 - 40,005 Non-performing loans sold- (128) (176) - - (304)

Ending balance174,555$ 68,979$ 141,855$ 55,971$ 31,275$ 472,635$

December 31, 2015September 30, 2015

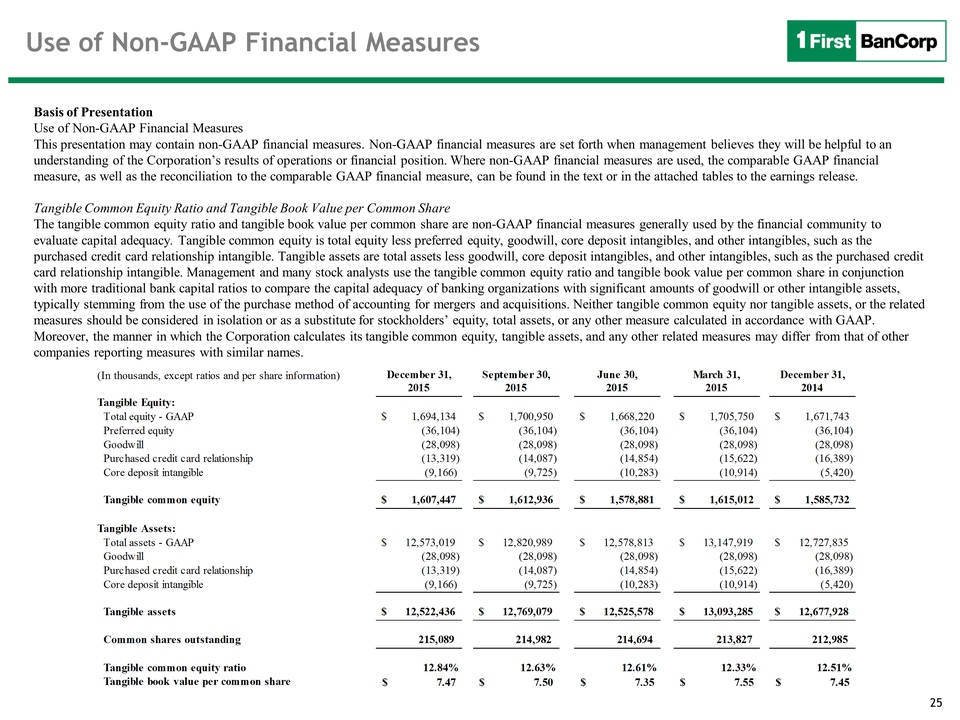

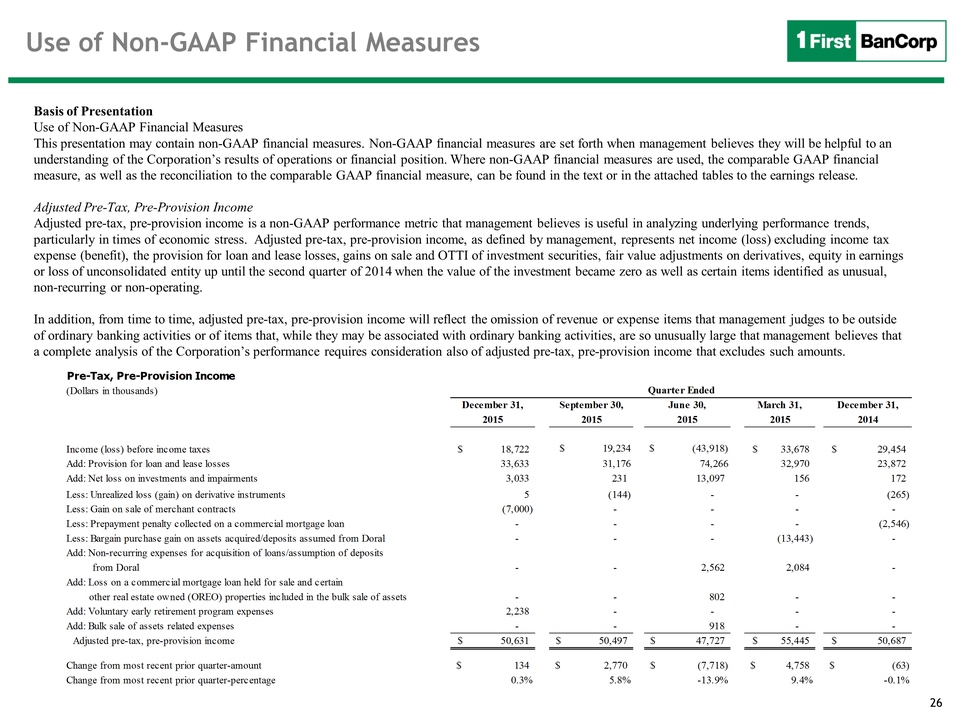

25 Use of Non-GAAP

Financial Measures Basis of Presentation Use of Non-GAAP Financial

Measures This presentation may contain non-GAAP financial measures.

Non-GAAP financial measures are set forth when management believes they

will be helpful to an understanding of the Corporation’s results of

operations or financial position. Where non-GAAP financial measures are

used, the comparable GAAP financial measure, as well as the

reconciliation to the comparable GAAP financial measure, can be found in

the text or in the attached tables to the earnings release. Tangible

Common Equity Ratio and Tangible Book Value per Common Share The

tangible common equity ratio and tangible book value per common share

are non-GAAP financial measures generally used by the financial

community to evaluate capital adequacy. Tangible common equity is total

equity less preferred equity, goodwill, core deposit intangibles, and

other intangibles, such as the purchased credit card relationship

intangible. Tangible assets are total assets less goodwill, core deposit

intangibles, and other intangibles, such as the purchased credit card

relationship intangible. Management and many stock analysts use the

tangible common equity ratio and tangible book value per common share in

conjunction with more traditional bank capital ratios to compare the

capital adequacy of banking organizations with significant amounts of

goodwill or other intangible assets, typically stemming from the use of

the purchase method of accounting for mergers and acquisitions. Neither

tangible common equity nor tangible assets, or the related measures

should be considered in isolation or as a substitute for stockholders’

equity, total assets, or any other measure calculated in accordance with

GAAP. Moreover, the manner in which the Corporation calculates its

tangible common equity, tangible assets, and any other related measures

may differ from that of other companies reporting measures with similar

names. (In thousands, except ratios and per share information)December

31,September 30,June 30,March 31,December 31,20152015201520152014Total

equity - GAAP $ 1,694,134 $ 1,700,950 $ 1,668,220 $ 1,705,750 $

1,671,743 Preferred equity (36,104)(36,104)(36,104)(36,104)

(36,104)Goodwill (28,098)(28,098)(28,098)(28,098)(28,098) Purchased

credit card relationship (13,319) (14,087) (14,854) (15,622)

(16,389)Core deposit intangible (9,166) (9,725)(10,283)(10,914)

(5,420)Tangible common equity $ 1,607,447 $ 1,612,936 $ 1,578,881 $

1,615,012 $ 1,585,732 Total assets - GAAP $ 12,573,019 $ 12,820,989 $

12,578,813 $ 13,147,919 $ 12,727,835

Goodwill(28,098)(28,098)(28,098)(28,098)(28,098)Purchased credit card

relationship (13,319) (14,087) (14,854) (15,622) (16,389)Core deposit

intangible (9,166) (9,725)(10,283) (10,914)(5,420)Tangible assets $

12,522,436 $ 12,769,079 $ 12,525,578 $ 13,093,285 $ 12,677,928 Common

shares outstanding 215,089 214,982 214,694 213,827 212,985 Tangible

common equity ratio12.84%12.63%12.61%12.33%12.51%Tangible book value per

common share7.47$ 7.50$ 7.35$ 7.55$ 7.45$ Tangible Equity:Tangible

Assets:

26 Use of Non-GAAP

Financial Measures Basis of Presentation Use of Non-GAAP Financial

Measures This presentation may contain non-GAAP financial measures.

Non-GAAP financial measures are set forth when management believes they

will be helpful to an understanding of the Corporation’s results of

operations or financial position. Where non-GAAP financial measures are

used, the comparable GAAP financial measure, as well as the

reconciliation to the comparable GAAP financial measure, can be found in

the text or in the attached tables to the earnings release. Adjusted

Pre-Tax, Pre-Provision Income Adjusted pre-tax, pre-provision income is

a non-GAAP performance metric that management believes is useful in

analyzing underlying performance trends, particularly in times of

economic stress. Adjusted pre-tax, pre-provision income, as defined by

management, represents net income (loss) excluding income tax expense

(benefit), the provision for loan and lease losses, gains on sale and

OTTI of investment securities, fair value adjustments on derivatives,

equity in earnings or loss of unconsolidated entity up until the second

quarter of 2014 when the value of the investment became zero as well as

certain items identified as unusual, non-recurring or non-operating. In

addition, from time to time, adjusted pre-tax, pre-provision income will

reflect the omission of revenue or expense items that management judges

to be outside of ordinary banking activities or of items that, while

they may be associated with ordinary banking activities, are so

unusually large that management believes that a complete analysis of the

Corporation’s performance requires consideration also of adjusted

pre-tax, pre-provision income that excludes such amounts. Pre-Tax,

Pre-Provision Income(Dollars in thousands)December 31,September 30,June

30,March 31,December 31,20152015201520152014Income (loss) before income

taxes 18,722$ $ 19,234 $ (43,918)33,678$ 29,454$ Add: Provision for loan

and lease losses33,633 31,17674,26632,970 23,872 Add: Net loss on

investments and impairments3,033 231 13,097 156 172 Less: Unrealized

loss (gain) on derivative instruments 5 (144) - - (265) Less: Gain on

sale of merchant contracts(7,000) - - - - Less: Prepayment penalty

collected on a commercial mortgage loan - - - - (2,546) Less: Bargain

purchase gain on assets acquired/deposits assumed from Doral - - -

(13,443) - Add: Non-recurring expenses for acquisition of

loans/assumption of deposits from Doral- - 2,562 2,084 - Add: Loss on a

commercial mortgage loan held for sale and certain other real estate

owned (OREO) properties included in the bulk sale of assets - - 802 - -

Add: Voluntary early retirement program expenses2,238 - - - - Add: Bulk

sale of assets related expenses- - 918 - - Adjusted pre-tax,

pre-provision income50,631$ 50,497$ 47,727$ 55,445$ 50,687$ Change from

most recent prior quarter-amount134$ 2,770$ (7,718)$ 4,758$ (63)$ Change

from most recent prior quarter-percentage0.3%5.8%-13.9%9.4%-0.1%Quarter

Ended