Attached files

| file | filename |

|---|---|

| 8-K - 8-K - SunCoke Energy Partners, L.P. | d120633d8k.htm |

| EX-99.3 - EX-99.3 - SunCoke Energy Partners, L.P. | d120633dex993.htm |

| EX-99.1 - EX-99.1 - SunCoke Energy Partners, L.P. | d120633dex991.htm |

Exhibit 99.2

SunCoke Energy Partners, L.P. Q4 2015 Earnings Conference Call January 28, 2016

Forward-Looking Statements This slide presentation should be reviewed in conjunction with the Fourth Quarter 2015 earnings release of SunCoke Energy Partners, L.P. (SXCP) and conference call held on January 28, 2016 at 10:00 a.m. ET. Some of the information included in this presentation constitutes “forward-looking statements.” All statements in this presentation that express opinions, expectations, beliefs, plans, objectives, assumptions or projections with respect to anticipated future performance of SunCoke Energy, Inc. (SXC) or SXCP, in contrast with statements of historical facts, are forward-looking statements. Such forward-looking statements are based on management’s beliefs and assumptions and on information currently available. Forward-looking statements include information concerning possible or assumed future results of operations, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance improvements, the effects of competition and the effects of future legislation or regulations. Forward-looking statements include all statements that are not historical facts and may be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “anticipate,” “estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions. Although management believes that its plans, intentions and expectations reflected in or suggested by the forward-looking statements made in this presentation are reasonable, no assurance can be given that these plans, intentions or expectations will be achieved when anticipated or at all. Moreover, such statements are subject to a number of assumptions, risks and uncertainties. Many of these risks are beyond the control of SXC and SXCP, and may cause actual results to differ materially from those implied or expressed by the forward-looking statements. Each of SXC and SXCP has included in its filings with the Securities and Exchange Commission cautionary language identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement. For more information concerning these factors, see the Securities and Exchange Commission filings of SXC and SXCP. All forward-looking statements included in this presentation are expressly qualified in their entirety by such cautionary statements. Although forward-looking statements are based on current beliefs and expectations, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date hereof. SXC and SXCP do not have any intention or obligation to update publicly any forward-looking statement (or its associated cautionary language) whether as a result of new information or future events or after the date of this presentation, except as required by applicable law. This presentation includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. Reconciliations of non-GAAP financial measures to GAAP financial measures are provided in the Appendix at the end of the presentation. Investors are urged to consider carefully the comparable GAAP measures and the reconciliations to those measures provided in the Appendix. SXCP Q4 2015 Earnings Call 1

2015 Overview Achieved solid safety, environmental and operating performance across coke & coal logistics fleet Achieved 33% DCF growth primarily through Convent Marine Terminal (“CMT”) and Granite City acquisitions Delivered FY 2015 Adj. EBITDA attributable to SXCP of ~$192M(1) and DCF of ~$117M(1), above revised guidance(2) When excluding benefit of CMT and Granite City 23% dropdown, delivered FY ‘15 results within original guidance Returned ~$56M to public unitholders in 2015 through distributions and unit repurchases and began de-levering by repurchasing ~$48M debt during Q4 (1) For a definition and reconciliation of Adjusted EBITDA attributable to SXCP and Distributable Cash Flow, please see appendix. (2) Revised guidance provided October 2015, which included an estimated $20M contribution from Convent SXCP Q4 2015 Earnings Call 2

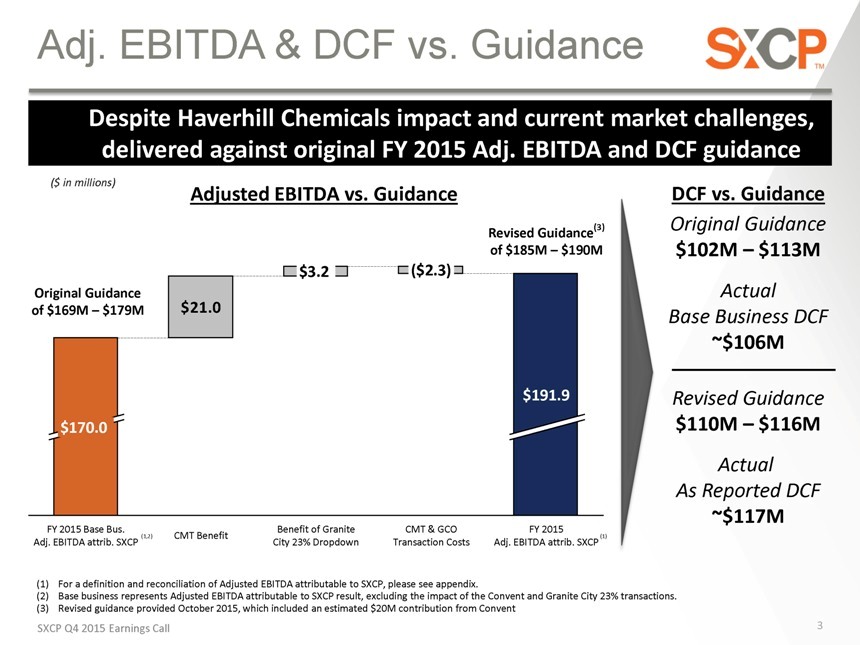

Adj. EBITDA & DCF vs. Guidance Despite Haverhill Chemicals impact and current market challenges, delivered against original FY 2015 Adj. EBITDA and DCF guidance ($ in millions) Adjusted EBITDA vs. Guidance Revised Guidance(3) of $185M – $190M $3.2 ($2.3) Original Guidance of $169M – $179M $21.0 $191.9 $170.0 FY 2015 Base Bus. (1,2) Benefit of Granite CMT & GCO FY 2015 (1) CMT Benefit Adj. EBITDA attrib. SXCP City 23% Dropdown Transaction Costs Adj. EBITDA attrib. SXCP DCF vs. Guidance Original Guidance $102M – $113M Actual Base Business DCF ~$106M Revised Guidance $110M – $116M Actual As Reported DCF ~$117M (1) For a definition and reconciliation of Adjusted EBITDA attributable to SXCP, please see appendix. (2) Base business represents Adjusted EBITDA attributable to SXCP result, excluding the impact of the Convent and Granite City 23% transactions. (3) Revised guidance provided October 2015, which included an estimated $20M contribution from Convent SXCP Q4 2015 Earnings Call 3

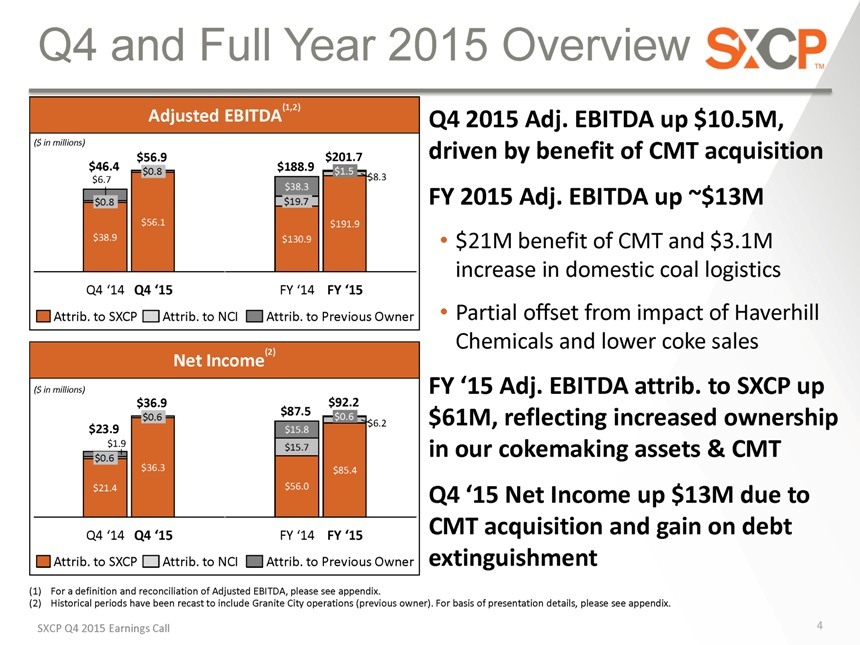

Q4 and Full Year 2015 Overview Adjusted EBITDA(1,2) ($ in millions) $56.9 $201.7 $46.4 $0.8 $188.9 $1.5 $6.7 $8.3 $38.3 $0.8 $19.7 $56.1 $191.9 $38.9 $130.9 Q4 ‘14 Q4 ‘15 FY ‘14 FY ‘15 Attrib. to SXCP Attrib. to NCI Attrib. to Previous Owner Net Income(2) ($ in millions) $36.9 $92.2 $0.6 $87.5 $0.6 $23.9 $15.8 $6.2 $1.9 $15.7 $0.6 $36.3 $85.4 $21.4 $56.0 Q4 ‘14 Q4 ‘15 FY ‘14 FY ‘15 Attrib. to SXCP Attrib. to NCI Attrib. to Previous Owner Q4 2015 Adj. EBITDA up $10.5M, driven by benefit of CMT acquisition FY 2015 Adj. EBITDA up ~$13M • $21M benefit of CMT and $3.1M increase in domestic coal logistics • Partial offset from impact of Haverhill Chemicals and lower coke sales FY ‘15 Adj. EBITDA attrib. to SXCP up $61M, reflecting increased ownership in our cokemaking assets & CMT Q4 ‘15 Net Income up $13M due to CMT acquisition and gain on debt extinguishment (1) For a definition and reconciliation of Adjusted EBITDA, please see appendix. (2) Historical periods have been recast to include Granite City operations (previous owner). For basis of presentation details, please see appendix. SXCP Q4 2015 Earnings Call 4

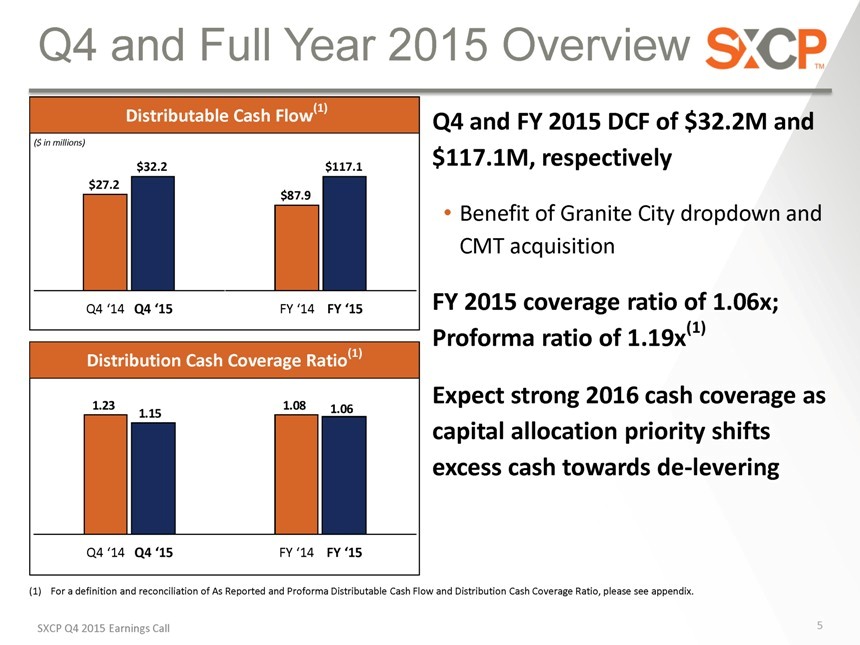

Q4 and Full Year 2015 Overview Distributable Cash Flow(1) ($ in millions) $32.2 $117.1 $27.2 $87.9 Q4 ‘14 Q4 ‘15 FY ‘14 FY ‘15 Distribution Cash Coverage Ratio(1) 1.23 1.15 1.08 1.06 Q4 ‘14 Q4 ‘15 FY ‘14 FY ‘15 Q4 and FY 2015 DCF of $32.2M and $117.1M, respectively • Benefit of Granite City dropdown and CMT acquisition FY 2015 coverage ratio of 1.06x; Proforma ratio of 1.19x(1) Expect strong 2016 cash coverage as capital allocation priority shifts excess cash towards de-levering (1) For a definition and reconciliation of As Reported and Proforma Distributable Cash Flow and Distribution Cash Coverage Ratio, please see appendix. SXCP Q4 2015 Earnings Call 5

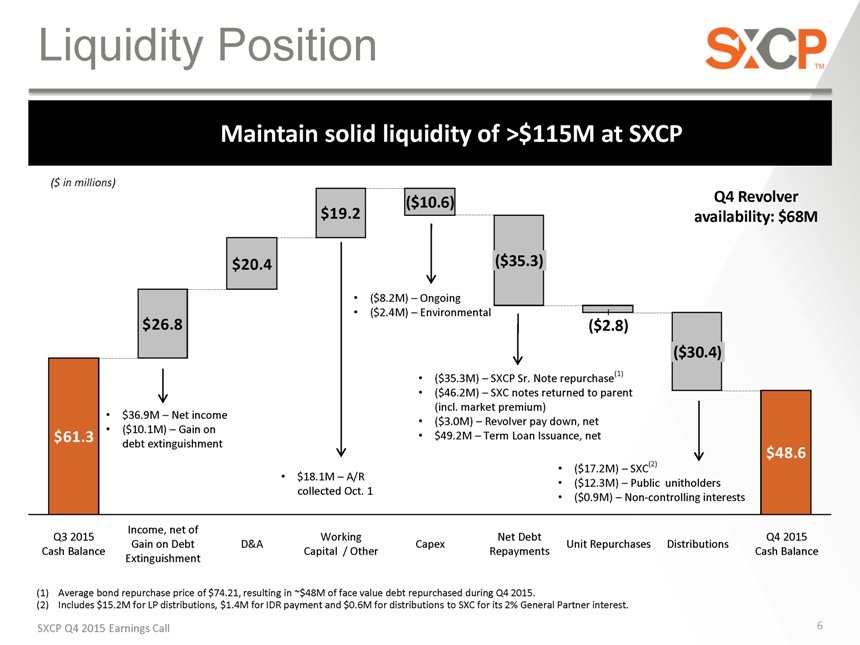

Liquidity Position Maintain solid liquidity of >$115M at SXCP ($ in millions) ($10.6) Q4 Revolver $19.2 availability: $68M $20.4 ($35.3) • ($8.2M) – Ongoing • ($2.4M) – Environmental $26.8 ($2.8) ($30.4) • ($35.3M) – SXCP Sr. Note repurchase(1) • ($46.2M) – SXC notes returned to parent (incl. market premium) • $36.9M – Net income • ($3.0M) – Revolver pay down, net $ 61.3 • ($10.1M) – Gain on • $49.2M – Term Loan Issuance, net debt extinguishment $48.6 • ($17.2M) – SXC(2) • $18.1M – A/R • ($12.3M) – Public unitholders collected Oct. 1 • ($0.9M) – Non-controlling interests Income, net of Q3 2015 Working Net Debt Q4 2015 Gain on Debt D&A Capex Unit Repurchases Distributions Cash Balance Capital / Other Repayments Cash Balance Extinguishment (1) Average bond repurchase price of $74.21, resulting in ~$48M of face value debt repurchased during Q4 2015. (2) Includes $15.2M for LP distributions, $1.4M for IDR payment and $0.6M for distributions to SXC for its 2% General Partner interest. SXCP Q4 2015 Earnings Call 6

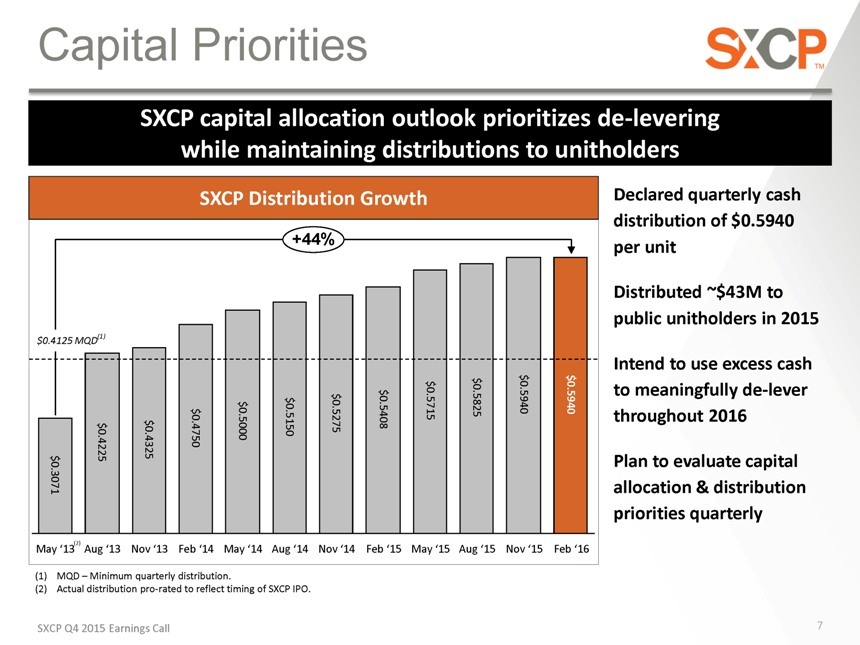

Capital Priorities SXCP capital allocation outlook prioritizes de-levering while maintaining distributions to unitholders SXCP Distribution Growth +44% $0.4125 MQD(1) $ $ $ $ 0 0 0 $ 0 . $ . $ 0 . 0 $ 0 . $ 0 . 0 . 5715 5825 5940 5940 $ . $ 0 . 0 . 4750 5000 5150 5275 5408 $ 4225 4325 0 . 3071 May ‘13(2) Aug ‘13 Nov ‘13 Feb ‘14 May ‘14 Aug ‘14 Nov ‘14 Feb ‘15 May ‘15 Aug ‘15 Nov ‘15 Feb ‘16 Declared quarterly cash distribution of $0.5940 per unit Distributed ~$43M to public unitholders in 2015 Intend to use excess cash to meaningfully de-lever throughout 2016 Plan to evaluate capital allocation & distribution priorities quarterly (1) MQD – Minimum quarterly distribution. (2) Actual distribution pro-rated to reflect timing of SXCP IPO. SXCP Q4 2015 Earnings Call 7

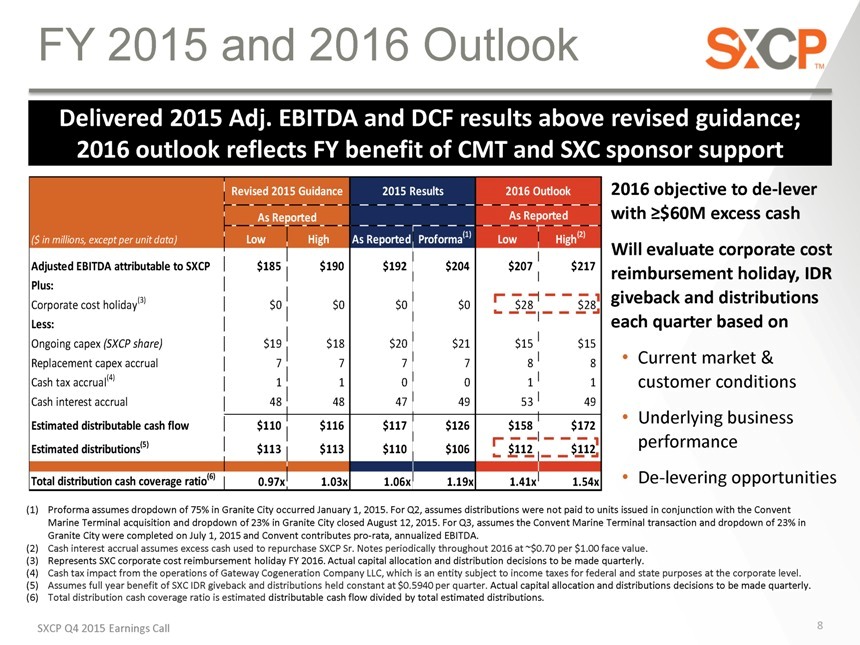

FY 2015 and 2016 Outlook Delivered 2015 Adj. EBITDA and DCF results above revised guidance; 2016 outlook reflects FY benefit of CMT and SXC sponsor support Revised 2015 Guidance 2015 Results 2016 Outlook As Reported As Reported ($ in millions, except per unit data) Low High As Reported Proforma(1) Low High(2) Adjusted EBITDA attributable to SXCP $185 $190 $192 $204 $207 $217 Plus: Corporate cost holiday(3) $0 $0 $0 $0 $28 $28 Less: Ongoing capex (SXCP share) $19 $18 $20 $21 $15 $15 Replacement capex accrual 7 7 7 7 8 8 Cash tax accrual(4) 1 1 0 0 1 1 Cash interest accrual 48 48 47 49 53 49 Estimated distributable cash flow $110 $116 $117 $126 $158 $172 Estimated distributions(5) $113 $113 $110 $106 $112 $112 Total distribution cash coverage ratio(6) 0.97x 1.03x 1.06x 1.19x 1.41x 1.54x 2016 objective to de-lever with $60M excess cash Will evaluate corporate cost reimbursement holiday, IDR giveback and distributions each quarter based on • Current market & customer conditions • Underlying business performance • De-levering opportunities (1) Proforma assumes dropdown of 75% in Granite City occurred January 1, 2015. For Q2, assumes distributions were not paid to units issued in conjunction with the Convent Marine Terminal acquisition and dropdown of 23% in Granite City closed August 12, 2015. For Q3, assumes the Convent Marine Terminal transaction and dropdown of 23% in Granite City were completed on July 1, 2015 and Convent contributes pro-rata, annualized EBITDA. (2) Cash interest accrual assumes excess cash used to repurchase SXCP Sr. Notes periodically throughout 2016 at ~$0.70 per $1.00 face value. (3) Represents SXC corporate cost reimbursement holiday FY 2016. Actual capital allocation and distribution decisions to be made quarterly. (4) Cash tax impact from the operations of Gateway Cogeneration Company LLC, which is an entity subject to income taxes for federal and state purposes at the corporate level. (5) Assumes full year benefit of SXC IDR giveback and distributions held constant at $0.5940 per quarter. Actual capital allocation and distributions decisions to be made quarterly. (6) Total distribution cash coverage ratio is estimated distributable cash flow divided by total estimated distributions. SXCP Q4 2015 Earnings Call 8

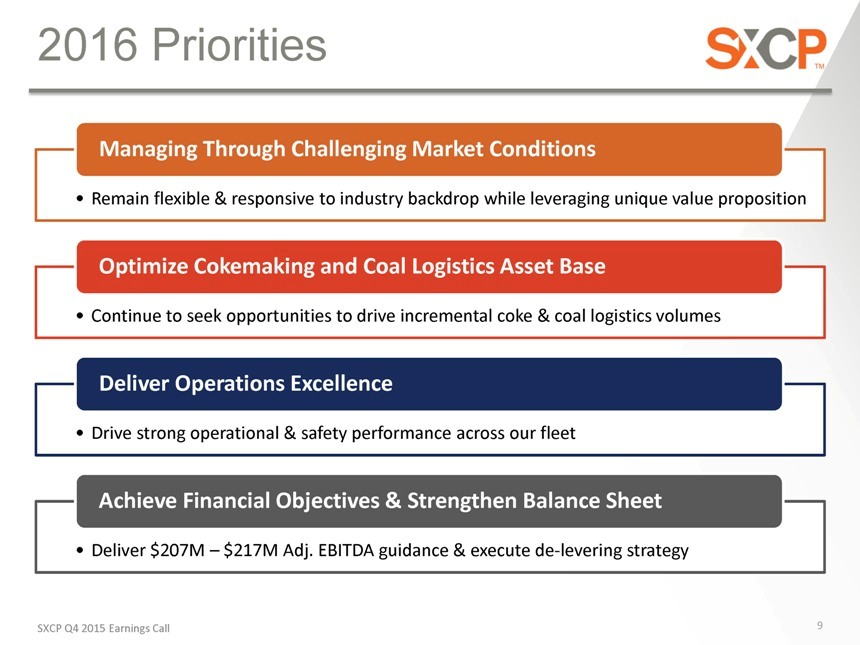

2016 Priorities Managing Through Challenging Market Conditions • Remain flexible & responsive to industry backdrop while leveraging unique value proposition Optimize Cokemaking and Coal Logistics Asset Base • Continue to seek opportunities to drive incremental coke & coal logistics volumes Deliver Operations Excellence • Drive strong operational & safety performance across our fleet Achieve Financial Objectives & Strengthen Balance Sheet • Deliver $207M – $217M Adj. EBITDA guidance & execute de-levering strategy SXCP Q4 2015 Earnings Call 9

QUESTIONS SXCP Q4 2015 Earnings Call 10

Investor Relations 630-824-1987 www.suncoke.com

APPENDIX SXCP Q4 2015 Earnings Call 12

Basis of Presentation & Definitions BASIS OF PRESENTATION • On January 13, 2015, we acquired a 75 percent interest in the Granite City cokemaking operation from SXC. Because this was a transfer between entities under common control, all historical financial results of Granite City prior to the dropdown have been included in our financial results. On August 12, 2015, we acquired an additional 23 percent interest in the Granite City cokemaking facility. Net income attributable to SunCoke Energy Partners, L.P./Previous Owner includes 100 percent of Granite City net income prior to dropdown, 75 percent after the January dropdown and 98 percent after dropdown in August. Net income attributable to Previous Owner includes 100% of Granite City net income prior to the dropdown on January 13, 2015. DEFINITIONS • Adjusted EBITDA represents earnings before interest, taxes, depreciation and amortization adjusted for sales discounts, and Coal Logistics deferred revenue. Prior to the expiration of our nonconventional fuel tax credits in 2013, Adjusted EBITDA included an add-back of sales discounts related to the sharing of these credits with our customers. Any adjustments to these amounts subsequent to 2013 have been included in Adjusted EBITDA. Coal Logistics deferred revenue adjusts for differences between the timing of recognition of take-or-pay shortfalls into revenue for GAAP purposes versus the timing of payments from our customers. This adjustment aligns Adjusted EBITDA more closely with cash flow. Adjusted EBITDA does not represent and should not be considered an alternative to net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance and liquidity of the Partnership’s net assets and its ability to incur and service debt, fund capital expenditures and make distributions. Adjusted EBITDA provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance and liquidity. EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, and they should not be considered an alternative to net income, operating cash flow or any other measure of financial performance presented in accordance with GAAP. • EBITDA represents earnings before interest, taxes, depreciation and amortization. • Adjusted EBITDA attributable to SXC/SXCP represents Adjusted EBITDA less Adjusted EBITDA attributable to noncontrolling interests. • Adjusted EBITDA/Ton represents Adjusted EBITDA divided by tons sold/handled. SXCP Q4 2015 Earnings Call 13

Basis of Presentation & Definitions • Distributable Cash Flow equals Adjusted EBITDA less net cash paid for interest expense, ongoing capital expenditures, accruals for replacement capital expenditures, and cash distributions to noncontrolling interests; plus amounts received under the Omnibus Agreement and acquisition expenses deemed to be Expansion Capital under our Partnership Agreement. Distributable Cash Flow is a non-GAAP supplemental financial measure that management and external users of SXCP’s financial statements, such as industry analysts, investors, lenders and rating agencies use to assess: • SXCP’s operating performance as compared to other publicly traded partnerships, without regard to historical cost basis; • the ability of SXCP’s assets to generate sufficient cash flow to make distributions to SXCP’s unitholders; • SXCP’s ability to incur and service debt and fund capital expenditures; and • the viability of acquisitions and other capital expenditure projects and the returns on investment of various investment opportunities. We believe that Distributable Cash Flow provides useful information to investors in assessing SXCP’s financial condition and results of operations. Distributable Cash Flow should not be considered an alternative to net income, operating income, cash flows from operating activities, or any other measure of financial performance or liquidity presented in accordance with generally accepted accounting principles (GAAP). Distributable Cash Flow has important limitations as an analytical tool because it excludes some, but not all, items that affect net income and net cash provided by operating activities and used in investing activities. Additionally, because Distributable Cash Flow may be defined differently by other companies in the industry, our definition of Distributable Cash Flow may not be comparable to similarly titled measures of other companies, thereby diminishing its utility. • Ongoing capital expenditures (“capex”) are capital expenditures made to maintain the existing operating capacity of our assets and/or to extend their useful lives. Ongoing capex also includes new equipment that improves the efficiency, reliability or effectiveness of existing assets. Ongoing capex does not include normal repairs and maintenance, which are expensed as incurred, or significant capital expenditures. For purposes of calculating distributable cash flow, the portion of ongoing capex attributable to SXCP is used. • Replacement capital expenditures (“capex”) represents an annual accrual necessary to fund SXCP’s share of the estimated costs to replace or rebuild our facilities at the end of their working lives. This accrual is estimated based on the average quarterly anticipated replacement capital that we expect to incur over the long term to replace our major capital assets at the end of their working lives. The replacement capex accrual estimate will be subject to review and prospective change by SXCP’s general partner at least annually and whenever an event occurs that causes a material adjustment of replacement capex, provided such change is approved by our conflicts committee. SXCP Q4 2015 Earnings Call 14

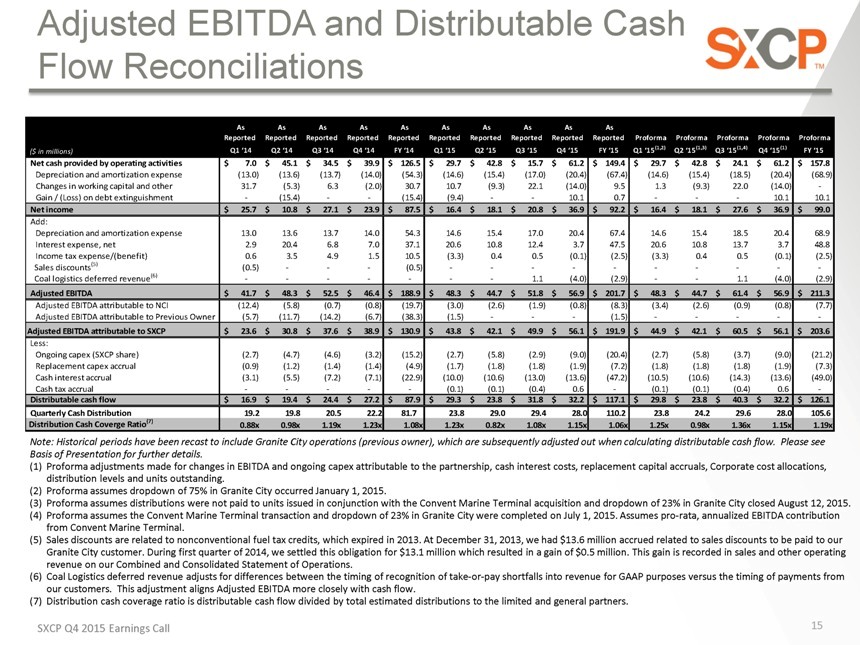

Adjusted EBITDA and Distributable Cash Flow Reconciliations As As As As As As As As As As Reported Reported Reported Reported Reported Reported Reported Reported Reported Reported Proforma Proforma Proforma Proforma Proforma ($ in millions) Q1 ‘14 Q2 ‘14 Q3 ‘14 Q4 ‘14 FY ‘14 Q1 ‘15 Q2 ‘15 Q3 ‘15 Q4 ‘15 FY ‘15 Q1 ‘15(1,2) Q2 ‘15(1,3) Q3 ‘15(1,4) Q4 ‘15(1) FY ‘15 Net cash provided by operating activities $ 7.0 $ 45.1 $ 34.5 $ 39.9 $ 126.5 $ 29.7 $ 42.8 $ 15.7 $ 61.2 $ 149.4 $ 29.7 $ 42.8 $ 24.1 $ 61.2 $ 157.8 Depreciation and amortization expense (13.0) (13.6) (13.7) (14.0) (54.3) (14.6) (15.4) (17.0) (20.4) (67.4) (14.6) (15.4) (18.5) (20.4) (68.9) Changes in working capital and other 31.7 (5.3) 6.3 (2.0) 30.7 10.7 (9.3) 22.1 (14.0) 9.5 1.3 (9.3) 22.0 (14.0) —Gain / (Loss) on debt extinguishment —(15.4) —— (15.4) (9.4) —— 10.1 0.7 ——— 10.1 10.1 Net income $ 25.7 $ 10.8 $ 27.1 $ 23.9 $ 87.5 $ 16.4 $ 18.1 $ 20.8 $ 36.9 $ 92.2 $ 16.4 $ 18.1 $ 27.6 $ 36.9 $ 99.0 Add: Depreciation and amortization expense 13.0 13.6 13.7 14.0 54.3 14.6 15.4 17.0 20.4 67.4 14.6 15.4 18.5 20.4 68.9 Interest expense, net 2.9 20.4 6.8 7.0 37.1 20.6 10.8 12.4 3.7 47.5 20.6 10.8 13.7 3.7 48.8 Income tax expense/(benefit) 0.6 3.5 4.9 1.5 10.5 (3.3) 0.4 0.5 (0.1) (2.5) (3.3) 0.4 0.5 (0.1) (2.5) Sales discounts(5) (0.5) ——— (0.5) ——————————Coal logistics deferred revenue(6) ——————— 1.1 (4.0) (2.9) —— 1.1 (4.0) (2.9) Adjusted EBITDA $ 41.7 $ 48.3 $ 52.5 $ 46.4 $ 188.9 $ 48.3 $ 44.7 $ 51.8 $ 56.9 $ 201.7 $ 48.3 $ 44.7 $ 61.4 $ 56.9 $ 211.3 Adjusted EBITDA attributable to NCI (12.4) (5.8) (0.7) (0.8) (19.7) (3.0) (2.6) (1.9) (0.8) (8.3) (3.4) (2.6) (0.9) (0.8) (7.7) Adjusted EBITDA attributable to Previous Owner (5.7) (11.7) (14.2) (6.7) (38.3) (1.5) ——— (1.5) —————Adjusted EBITDA attributable to SXCP $ 23.6 $ 30.8 $ 37.6 $ 38.9 $ 130.9 $ 43.8 $ 42.1 $ 49.9 $ 56.1 $ 191.9 $ 44.9 $ 42.1 $ 60.5 $ 56.1 $ 203.6 Less: Ongoing capex (SXCP share) (2.7) (4.7) (4.6) (3.2) (15.2) (2.7) (5.8) (2.9) (9.0) (20.4) (2.7) (5.8) (3.7) (9.0) (21.2) Replacement capex accrual (0.9) (1.2) (1.4) (1.4) (4.9) (1.7) (1.8) (1.8) (1.9) (7.2) (1.8) (1.8) (1.8) (1.9) (7.3) Cash interest accrual (3.1) (5.5) (7.2) (7.1) (22.9) (10.0) (10.6) (13.0) (13.6) (47.2) (10.5) (10.6) (14.3) (13.6) (49.0) Cash tax accrual ————— (0.1) (0.1) (0.4) 0.6 — (0.1) (0.1) (0.4) 0.6 —Distributable cash flow $ 16.9 $ 19.4 $ 24.4 $ 27.2 $ 87.9 $ 29.3 $ 23.8 $ 31.8 $ 32.2 $ 117.1 $ 29.8 $ 23.8 $ 40.3 $ 32.2 $ 126.1 Quarterly Cash Distribution 19.2 19.8 20.5 22.2 81.7 23.8 29.0 29.4 28.0 110.2 23.8 24.2 29.6 28.0 105.6 Distribution Cash Coverge Ratio(7) 0.88x 0.98x 1.19x 1.23x 1.08x 1.23x 0.82x 1.08x 1.15x 1.06x 1.25x 0.98x 1.36x 1.15x 1.19x Note: Historical periods have been recast to include Granite City operations (previous owner), which are subsequently adjusted out when calculating distributable cash flow. Please see Basis of Presentation for further details. (1) Proforma adjustments made for changes in EBITDA and ongoing capex attributable to the partnership, cash interest costs, replacement capital accruals, Corporate cost allocations, distribution levels and units outstanding. (2) Proforma assumes dropdown of 75% in Granite City occurred January 1, 2015. (3) Proforma assumes distributions were not paid to units issued in conjunction with the Convent Marine Terminal acquisition and dropdown of 23% in Granite City closed August 12, 2015. (4) Proforma assumes the Convent Marine Terminal transaction and dropdown of 23% in Granite City were completed on July 1, 2015. Assumes pro-rata, annualized EBITDA contribution from Convent Marine Terminal. (5) Sales discounts are related to nonconventional fuel tax credits, which expired in 2013. At December 31, 2013, we had $13.6 million accrued related to sales discounts to be paid to our Granite City customer. During first quarter of 2014, we settled this obligation for $13.1 million which resulted in a gain of $0.5 million. This gain is recorded in sales and other operating revenue on our Combined and Consolidated Statement of Operations. (6) Coal Logistics deferred revenue adjusts for differences between the timing of recognition of take-or-pay shortfalls into revenue for GAAP purposes versus the timing of payments from our customers. This adjustment aligns Adjusted EBITDA more closely with cash flow. (7) Distribution cash coverage ratio is distributable cash flow divided by total estimated distributions to the limited and general partners. SXCP Q4 2015 Earnings Call 15

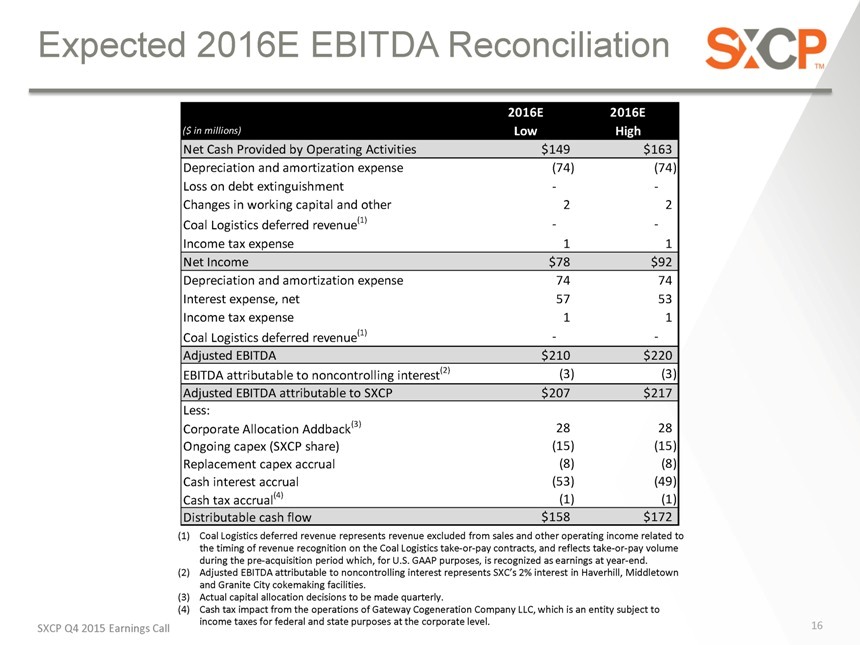

Expected 2016E EBITDA Reconciliation 2016E 2016E ($ in millions) Low High Net Cash Provided by Operating Activities $149 $163 Depreciation and amortization expense (74) (74) Loss on debt extinguishment — Changes in working capital and other 2 2 Coal Logistics deferred revenue(1) — Income tax expense 1 1 Net Income $78 $92 Depreciation and amortization expense 74 74 Interest expense, net 57 53 Income tax expense 1 1 Coal Logistics deferred revenue(1) — Adjusted EBITDA $210 $220 EBITDA attributable to noncontrolling interest(2) (3) (3) Adjusted EBITDA attributable to SXCP $207 $217 Less: Corporate Allocation Addback(3) 28 28 Ongoing capex (SXCP share) (15) (15) Replacement capex accrual (8) (8) Cash interest accrual (53) (49) Cash tax accrual(4) (1) (1) Distributable cash flow $158 $172 (1) Coal Logistics deferred revenue represents revenue excluded from sales and other operating income related to the timing of revenue recognition on the Coal Logistics take-or-pay contracts, and reflects take-or-pay volume during the pre-acquisition period which, for U.S. GAAP purposes, is recognized as earnings at year-end. (2) Adjusted EBITDA attributable to noncontrolling interest represents SXC’s 2% interest in Haverhill, Middletown and Granite City cokemaking facilities. (3) Actual capital allocation decisions to be made quarterly. (4) Cash tax impact from the operations of Gateway Cogeneration Company LLC, which is an entity subject to income taxes for federal and state purposes at the corporate level. SXCP Q4 2015 Earnings Call 16

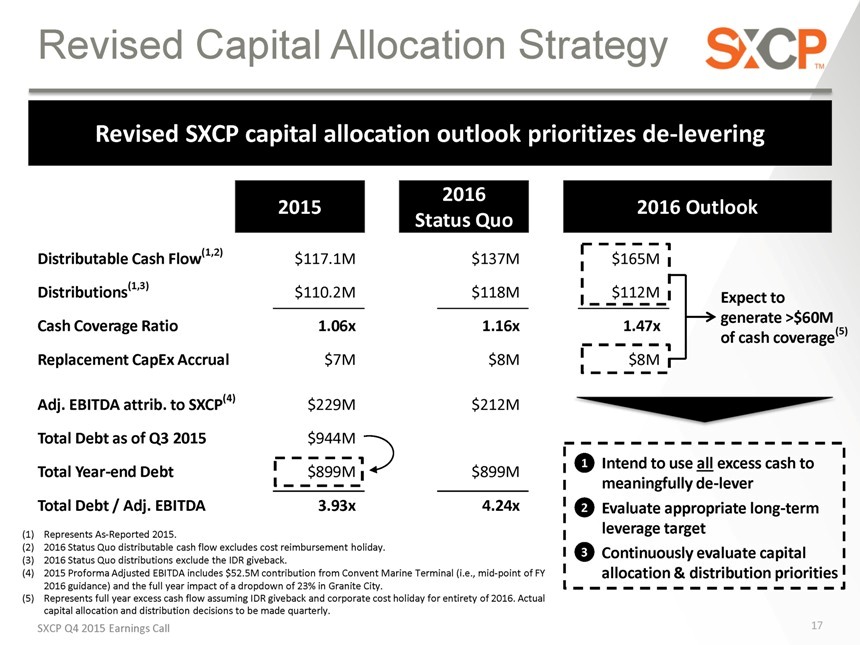

Revised Capital Allocation Strategy Revised SXCP capital allocation outlook prioritizes de-levering 2015 2016 Status Quo Distributable Cash Flow(1,2) $117.1M $137M Distributions(1,3) $110.2M $118M Cash Coverage Ratio 1.06x 1.16x Replacement CapEx Accrual $7M $8M Adj. EBITDA attrib. to SXCP(4) $229M $212M Total Debt as of Q3 2015 $944M Total Year-end Debt $899M $899M Total Debt / Adj. EBITDA 3.93x 4.24x 2016 Outlook $165M $112M Expect to generate >$60M 1.47x (5) of cash coverage $8M 1 Intend to use all excess cash to meaningfully de-lever 2 Evaluate appropriate long-term leverage target 3 Continuously evaluate capital allocation & distribution priorities (1) Represents As-Reported 2015. (2) 2016 Status Quo distributable cash flow excludes cost reimbursement holiday. (3) 2016 Status Quo distributions exclude the IDR giveback. (4) 2015 Proforma Adjusted EBITDA includes $52.5M contribution from Convent Marine Terminal (i.e., mid-point of FY 2016 guidance) and the full year impact of a dropdown of 23% in Granite City. (5) Represents full year excess cash flow assuming IDR giveback and corporate cost holiday for entirety of 2016. Actual capital allocation and distribution decisions to be made quarterly. SXCP Q4 2015 Earnings Call 17

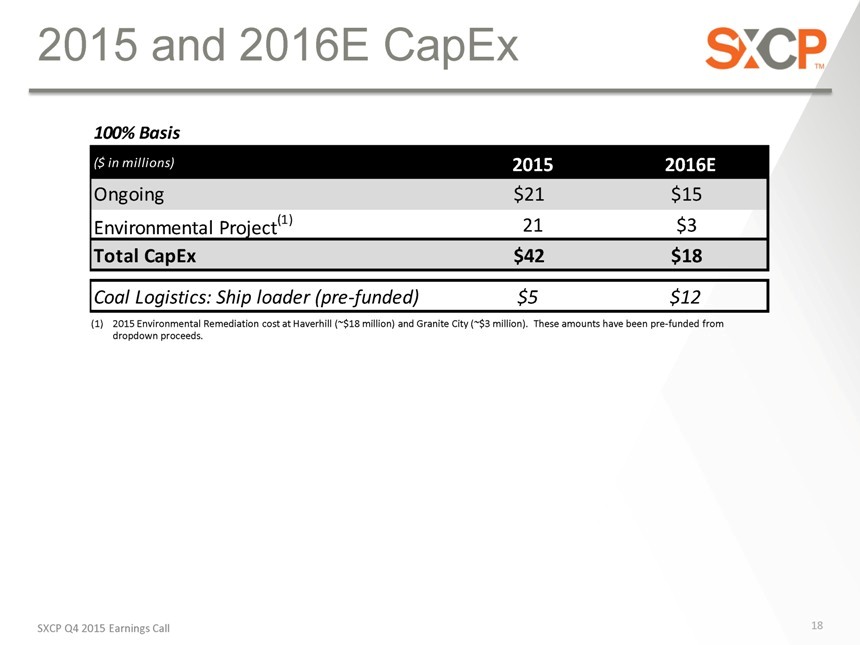

2015 and 2016E CapEx 100% Basis ($ in millions) 2015 2016E Ongoing $21 $15 Environmental Project(1) 21 $3 Total CapEx $42 $18 Coal Logistics: Ship loader (pre-funded) $5 $12 (1) 2015 Environmental Remediation cost at Haverhill (~$18 million) and Granite City (~$3 million). These amounts have been pre-funded from dropdown proceeds. SXCP Q4 2015 Earnings Call 18