Attached files

| file | filename |

|---|---|

| EX-5.1 - Mr. Amazing Loans Corp | ex5-1.htm |

| EX-21.1 - Mr. Amazing Loans Corp | ex21-1.htm |

| EX-23.1 - Mr. Amazing Loans Corp | ex23-1.htm |

As filed with the Securities and Exchange Commission January 25, 2016

Registration Statement No. 333-_____________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

IEG Holdings Corporation

(Exact name of registrant as specified in its charter)

| Florida | 6141 | 90-1069184 | ||

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

6160 West Tropicana Ave., Suite E-13

Las Vegas, NV 89103

(702) 227-5626

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Paul Mathieson

Chief Executive Officer

6160 West Tropicana Ave., Suite E-13

Las Vegas, NV 89103

(702) 227-5626

(Name, address and telephone number of agent for service)

With copies to:

Laura Anthony, Esq.

Legal & Compliance, LLC

330 Clematis Street, Suite 217

West Palm Beach, FL 33401

(800) 341-2684

Approximate date of proposed sale to public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on the Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: [ ]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering: [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering: [ ]

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] (Do not check if a smaller reporting company) | Smaller reporting company | [X] |

CALCULATION OF REGISTRATION FEE

| Title of Class of Securities to be Registered | Amount to be Registered | Proposed

Maximum Aggregate Price Per Share (1) | Proposed

Maximum Aggregate Offering Price (1) | Amount of Registration Fee (1) | ||||||||||||

| Common Stock, par value $0.001 per share | 1,000,000 | $ | 5.00 | $ | 5,000,000 | $ | 503.50 | |||||||||

(1) Estimated solely for purposes of calculating the registration fee under Rule 457(a) of the Securities Act of 1933, as amended.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION, DATED JANUARY 25, 2016 |

1,000,000 Shares of Common Stock

![]()

IEG Holdings Corporation is offering 1,000,000 shares of its common stock, par value $0.001 per share, in a direct public offering, without any involvement of underwriters.

Our common stock is quoted on the OTCQB® marketplace under the symbol, “IEGH.” On January 20, 2016, the last reported sale price of our common stock on the OTCQB was $5.00 per share.

The direct public offering price is $5.00 per share of common stock. Should all shares being offered by us hereunder be sold, we would receive an aggregate of $5,000,000.

The total proceeds from this offering will not be escrowed or segregated but will be available to us immediately. There is no minimum number of shares that must be sold by us for the offering to proceed, and we will retain the proceeds from the sale of any of the offered shares. The offering is being conducted on a self-underwritten, best efforts basis, which means our officers and directors will attempt to sell the shares. This prospectus will permit our officers and directors to sell the shares directly to the public, with no commission or other remuneration payable to them for any shares they may sell. For more information, see the section titled “Plan of Distribution” and “Use of Proceeds” herein.

In offering the securities on our behalf, the officers and directors will rely on the safe harbor from broker-dealer registration set out in Rule 3a4-1 under the Securities and Exchange Act of 1934. The shares will be offered at a fixed price of $5.00 per share for a period of 60 days from the effective date of this prospectus, unless the offering is terminated prior to such time or extended by our board of directors for an additional 60 days.

| Per Share | Total | |||||||

| Public offering price | $ | 5.00 | $ | 5,000,000 | ||||

| Offering proceeds to IEG Holdings Corporation before expenses | $ | 5.00 | $ | 5,000,000 | ||||

We are an “emerging growth company,” as such term is defined in Section 2(a)(19) of the Securities Act of 1933, as amended, and we will be subject to reduced public reporting requirements. See “Emerging Growth Company Status.”

Persons effecting transactions in the shares should confirm the registration of these securities under the securities laws of the states in which transactions occur or the existence of applicable exemptions from such registration.

THE SECURITIES BEING OFFERED ARE SPECULATIVE AND INVOLVE A HIGH DEGREE OF RISK. THEY SHOULD BE CONSIDERED ONLY BY PERSONS WHO CAN AFFORD THE LOSS OF THEIR ENTIRE INVESTMENT. SEE “RISK FACTORS” BEGINNING ON PAGE 7 OF THIS PROSPECTUS FOR A DISCUSSION OF INFORMATION THAT SHOULD BE CONSIDERED IN CONNECTION WITH AN INVESTMENT IN OUR SECURITIES.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR PASSED UPON THE ADEQUACY OR ACCURACY OF THIS PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE WILL NOT SELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION HAS BEEN CLEARED OF COMMENTS AND IS DECLARED EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OF SALE IS NOT PERMITTED.

The date of this prospectus is , 2016.

| 1 |

TABLE OF CONTENTS

No dealer, salesperson or other individual has been authorized to give any information or to make any representation other than those contained in this prospectus in connection with the offer made by this prospectus and, if given or made, such information or representations must not be relied upon as having been authorized by us. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which such an offer or solicitation is not authorized or in which the person making such offer or solicitation is not qualified to do so, or to any person to whom it is unlawful to make such offer or solicitation. Neither the delivery of this prospectus nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in our affairs or that information contained herein is correct as of any time subsequent to the date hereof.

For investors outside the United States: We have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves, and observe any restrictions relating to, the offering of the shares of our common stock and the distribution of this prospectus outside the United States.

| 2 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes “forward-looking statements” within the meaning of the federal securities laws that involve risks and uncertainties. Forward-looking statements include statements we make concerning our plans, objectives, goals, strategies, future events, future revenues or performance, capital expenditures, financing needs and other information that is not historical information. Some forward-looking statements appear under the headings “Prospectus Summary,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” When used in this prospectus, the words “estimates,” “expects,” “anticipates,” “projects,” “forecasts,” “plans,” “intends,” “believes,” “foresees,” “seeks,” “likely,” “may,” “might,” “will,” “should,” “goal,” “target” or “intends” and variations of these words or similar expressions (or the negative versions of any such words) are intended to identify forward-looking statements. All forward-looking statements are based upon information available to us on the date of this prospectus.

These forward-looking statements are subject to risks, uncertainties and other factors, many of which are outside of our control, that could cause actual results to differ materially from the results discussed in the forward-looking statements, including, among other things, the matters discussed in this prospectus in the sections captioned “Prospectus Summary,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” Some of the factors that we believe could affect our results include:

| ● | limitations on our ability to continue operations and implement our business plan; |

| ● | our history of operating losses; |

| ● | the timing of and our ability to obtain financing on acceptable terms; |

| ● | the effects of changing economic conditions; |

| ● | the loss of members of the management team or other key personnel; |

| ● | competition from larger, more established companies with greater economic resources than we have; |

| ● | costs and other effects of legal and administrative proceedings, settlements, investigations and claims, which may not be covered by insurance; |

| ● | costs and damages relating to pending and future litigation; |

| ● | the impact of additional legal and regulatory interpretations and rulemaking and our success in taking action to mitigate such impacts; |

| ● | control by our principal equity holders; and |

| ● | the other factors set forth herein, including those set forth under “Risk Factors.” |

There are likely other factors that could cause our actual results to differ materially from the results referred to in the forward-looking statements. All forward-looking statements attributable to us in this prospectus apply only as of the date of this prospectus and are expressly qualified in their entirety by the cautionary statements included in this prospectus. We undertake no obligation to publicly update or revise forward-looking statements to reflect events or circumstances after the date made or to reflect the occurrence of unanticipated events, except as required by law.

We are responsible for the disclosure in this prospectus. However, this prospectus includes industry data that we obtained from internal surveys, market research, publicly available information and industry publications. The market research, publicly available information and industry publications that we use generally state that the information contained therein has been obtained from sources believed to be reliable. The information therein represents the most recently available data from the relevant sources and publications and we believe remains reliable. We did not fund and are not otherwise affiliated with any of the sources cited in this prospectus. Forward-looking information obtained from these sources is subject to the same qualifications and additional uncertainties regarding the other forward-looking statements in this prospectus.

| 3 |

This summary highlights material information concerning our business and this offering. This summary does not contain all of the information that you should consider before making your investment decision. You should carefully read the entire prospectus and the information incorporated by reference into this prospectus, including the information presented under the section entitled “Risk Factors” and the financial data and related notes, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from future results contemplated in the forward-looking statements as a result of factors such as those set forth in “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.” All historical information in this prospectus has been adjusted to reflect the 1-for-6 reverse stock split of our common stock that was effective February 22, 2013 and the 1-for-100 reverse stock split of our common stock that was effective June 17, 2015.

In this prospectus, unless the context indicates otherwise, “IEG Holdings,” the “Company,” “we,” “our,” “ours” or “us” refer to IEG Holdings Corporation, a Florida corporation, and its subsidiaries.

Our Company

We were organized as a Florida corporation on January 21, 1999, under the name Interact Technologies, Inc. (“Interact”). Interact was formed for the purpose of acquiring certain medical technology. On February 18, 1999, we changed our name to Fairhaven Technologies, Inc. (“Fairhaven”). Fairhaven’s business plan continued to involve the acquisition of certain medical technology. By June 1999, Fairhaven abandoned its business plan and had no operations until December 2001. On December 14, 2001, we changed our name to Ideal Accents, Inc. Ideal Accents, Inc. was engaged primarily in the business of accessorizing cars and trucks at the new vehicle dealer level. Ideal Accents, Inc. ceased operations in 2005. Investment Evolution Corporation, our wholly owned subsidiary (“IEC”), commenced operations in 2010 and in February 2013, we changed our name to IEG Holdings Corporation. Since March 2013, we have been engaged in the business of providing unsecured consumer loans ranging from $2,000 - $10,000 and offer loans online under the consumer brand “Mr. Amazing Loans”. Beginning in mid-2015, we changed our loan terms, such that we offer only $5,000 loans over a five-year term. We are headquartered in Las Vegas, Nevada and originate direct consumer loans in the states of Alabama, Arizona, California, Florida, Georgia, Illinois, Kentucky, Louisiana, Missouri, Nevada, New Jersey, New Mexico, Oregon, Pennsylvania, Texas, Utah and Virginia via our website and online distribution network. We are a fully licensed consumer installment loan provider in the 17 states in which we operate and we offer all loans within the prevailing statutory rates.

We have two wholly owned subsidiaries, each of which is described below:

| ● | IEC: Our U.S. operating entity that holds all state licenses, leases, employee contracts and other operating and administrative expenses. | |

| ● | IEC SPV, LLC (“SPV”): A bankruptcy remote special purpose vehicle that holds our U.S. loan receivables. |

In 2005, Paul Mathieson, our Chief Executive Officer and a member of our Board of Directors, founded IEG Holdings Limited (“IEG”) in Sydney, Australia. IEG launched the Amazing Loans business in Australia in 2005 and the Mr. Amazing Loans business in the United States via Investment Evolution Global Corporation (“IEGC”) in 2010. From 2005 until 2012, Mr. Mathieson operated the Amazing Loans business through IEG in Australia. IEG ceased doing business in Australia in 2012. On January 28, 2013, IEGC entered into a stock exchange agreement (the “Stock Exchange Agreement”) among IEGC, its sole stockholder, IEG, and IEG Holdings. Under the terms of the Stock Exchange Agreement, we agreed to acquire a 100% interest in IEGC for 2,724,471 shares of our common stock after giving effect to a 1-for-6 reverse stock split (also adjusted for the 1-for-100 reverse stock split that took effect June 17, 2015). On February 14, 2013, we filed an amendment to our articles of incorporation, as amended, with the Secretary of State of Florida which had the effect of:

| ● | changing our name from Ideal Accents, Inc. to IEG Holdings Corporation, | |

| ● | increasing the number of shares of our authorized common stock to 1,000,000,000, $.001 par value, | |

| ● | creating 50,000,000 shares of “blank-check” preferred stock, and | |

| ● | effecting the Reverse Stock Split pursuant to the terms of the Stock Exchange Agreement. |

FINRA approved the amendment to our articles of incorporation, as amended, on March 11, 2013.

| 4 |

On March 13, 2013, we completed the acquisition of IEGC under the terms of the Stock Exchange Agreement and issued to IEG 2,724,471 shares of our common stock after giving effect to the Reverse Stock Split whereby we acquired a 100% interest in IEGC. The stock exchange agreement between IEGC, IEG and IEG Holdings resulted in a reverse acquisition with a public shell, with IEGC being the accounting acquirer. IEG Holdings issued 908 shares of its common stock to the stockholders of IEG (IEG transferred its ownership in IEGC to its stockholders, which is why the shares were issued to the ultimate stockholders of IEG rather than to IEG itself) for each share of IEGC, in exchange for 100% ownership interest in IEGC. We determined that IEGC was the accounting acquirer because of the following facts and circumstances:

| 1. | After consummation of the transaction, the ultimate stockholders of IEGC own 99.1% of the outstanding shares of IEG Holdings; | |

| 2. | The board of directors of IEG Holdings immediately after the transaction is comprised exclusively of former directors of IEGC; and | |

| 3. | The operations of IEG Holdings immediately after the transaction are those of IEGC. |

In August 2015, IEGC assigned all of its tangible and intangible assets to IEG Holdings and IEGC was dissolved.

On May 1, 2015, we filed articles of amendment to our amended and restated articles of incorporation, as amended, with the Secretary of State of Florida. The amendment was approved by FINRA, and became effective, on June 17, 2015. The articles of amendment effected (i) a 1-for-100 reverse stock split, and (ii) an increase in our authorized capital stock from 2,550,000,000 shares to 3,050,000,000 shares, of which 3,000,000,000 shares are common stock and 50,000,000 are preferred stock. No fractional shares were issued as a result of the reverse stock split. Rather, stockholders of fractional shares received a cash payment at a price equal to the closing price of our common stock as of the date of the reverse stock split.

On September 10, 2015, we filed articles of amendment to our amended and restated articles of incorporation, as amended, with the Secretary of State of Florida. The articles of amendment had the effect of adjusting the conversion ratios of the Series A, Series F, Series G and Series H preferred stock to account for the Company’s offering to existing stockholders of the Corporation commenced August 3, 2015 and removing references to conversion on June 30, 2015 for Series F and Series G preferred stock:

| (i) | Adjusting the conversion ratio of the Series A preferred stock from 4 to 8 shares of common stock for each Series A preferred stock; | |

| (ii) | Adjusting the conversion ratio of the Series F preferred stock from 3,333/10,000 (0.3333) to 6,666/10,000 (0.6666) shares of common stock for each Series F preferred stock; | |

| (iii) | Adjusting the conversion ratio of the Series G preferred stock from 2,000/10,000 (0.2000) to 4,000/10,000 (0.4000) shares of common stock for each Series G preferred stock; and | |

| (iv) | Adjusting the conversion ratio of the Series H preferred stock from 1,333/10,000 (0.1333) to 2,666/10,000 (0.2666) shares of common stock for each Series H preferred stock. |

On December 1, 2015, we filed articles of amendment to our amended and restated articles of incorporation, as amended, with the Secretary of State of Florida. The articles of amendment had the effect of adjusting the conversion ratios of the Series A, Series F, Series G and Series H preferred stock to account for the Company’s offering to existing stockholders of the Corporation commenced December 1, 2015:

| (i) | Adjusting the conversion ratio of the Series A preferred stock from 8 to 16 shares of common stock for each Series A preferred stock; | |

| (ii) | Adjusting the conversion ratio of the Series F preferred stock from 6,666/10,000 (0.6666) to 13,332/10,000 (1.3332) shares of common stock for each Series F preferred stock; | |

| (iii) | Adjusting the conversion ratio of the Series G preferred stock from 4,000/10,000 (0.4000) to 8,000/10,000 (0.8000) shares of common stock for each Series G preferred stock; and | |

| (iv) | Adjusting the conversion ratio of the Series H preferred stock from 2,666/10,000 (0.2666) to 5,332/10,000 (0.5332) shares of common stock for each Series H preferred stock. |

On January 8, 2016, we filed articles of amendment to our amended and restated articles of incorporation, as amended, with the Secretary of State of Florida. The articles of amendment had the effect of adjusting the conversion ratios of the Series A and Series H preferred stock to account for the Company’s offering to existing stockholders of the Corporation commenced January 8, 2016:

| (i) | Adjusting the conversion ratio of the Series A preferred stock from 16 to 32 shares of common stock for each Series A preferred stock; and | |

| (ii) | Adjusting the conversion ratio of the Series H preferred stock from 5,332/10,000 (0.5332) to one share of common stock for each Series H preferred stock. |

| 5 |

On January 14, 2016, we filed a Preliminary Schedule 14C Information Statement with the Securities and Exchange Commission, in connection with the approval of articles of amendment to our amended and restated articles of incorporation, as amended, by our Board of Directors and the holder of a majority of the voting power of the issued and outstanding capital stock of the Company, to, on the Effective Date (as defined below), (i) effect a reverse stock split of the issued and outstanding shares of the common stock, at the ratio of 1-for-100, (ii) immediately after the reverse stock split, effect a forward stock split on a 100-for-1 share basis of the issued and outstanding common stock and reduce the number of authorized shares of common stock from 3,000,000,000 to 200,000,000, and (iii) immediately prior to the reverse stock split, pay in cash to those shareholders holding fewer than 100 shares of common stock, instead of issuing fractional shares, an amount per share equal to the average closing price per share of the common stock on the OTCQB, averaged over a period of 30 consecutive calendar days ending on (and including) the date of the Effective Date, without interest. The articles of amendment will be effective upon their filing with the Secretary of State of Florida which will occur approximately, but not less than, 20 days after the definitive information statement is mailed to the shareholders of the Company (“Effective Date”).

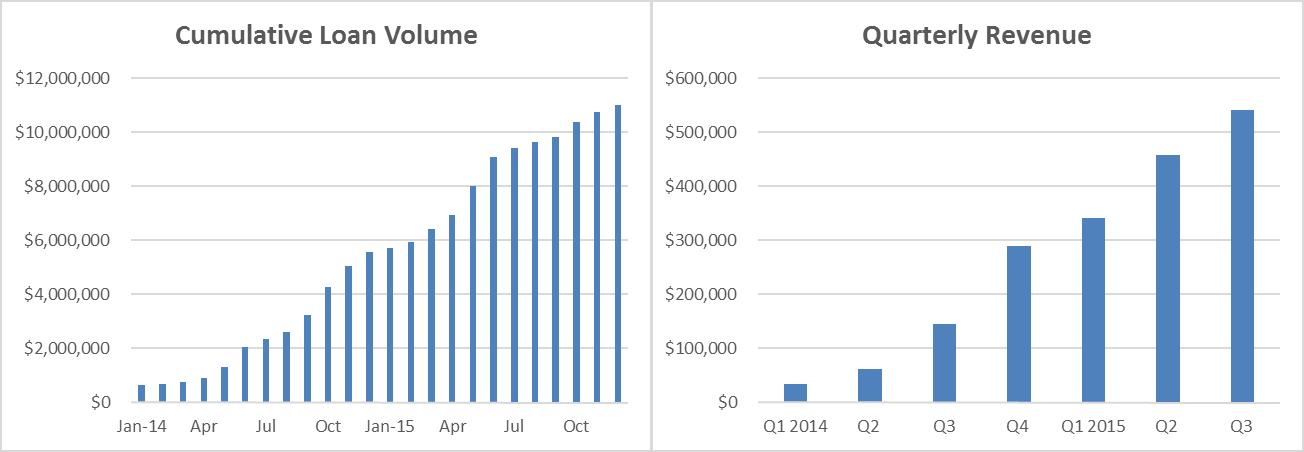

For the fiscal year ended December 31, 2014 and the nine months ended September 30, 2015, we generated revenue of $529,225 and $1,327,329, respectively, and had a net loss of $5,401,754 and $4,239,353, respectively. Our accountants have raised substantial doubt regarding our ability to continue as a going concern. As noted in our consolidated financial statements, we had an accumulated stockholders’ deficit of approximately $14.7 million and recurring losses from operations as of December 31, 2014. See “Risk Factors - Our accountants have raised substantial doubt regarding our ability to continue as a going concern.”

Emerging Growth Company Status

We are an “emerging growth company” as defined in Section 2(a)(19) of the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As such, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. We intend to take advantage of all of these exemptions.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards, and delay compliance with new or revised accounting standards until those standards are applicable to private companies. We have elected to take advantage of the benefits of this extended transition period.

We could be an emerging growth company until the last day of the first fiscal year following the fifth anniversary of our first common equity offering, although circumstances could cause us to lose that status earlier if our annual revenues exceed $1.0 billion, if we issue more than $1.0 billion in non-convertible debt in any three-year period or if we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Company Information

Our principal office is located at 6160 West Tropicana Ave., Suite E-13, Las Vegas, NV 89103 and our phone number is (702) 227-5626. Our corporate website address is www.investmentevolution.com. Information contained on, or accessible through, our website is not a part of, and is not incorporated by reference into, this prospectus.

The Offering

| Issuer | IEG Holdings Corporation | |

| Common stock offered by us | 1,000,000 shares of common stock. | |

| Common stock outstanding before this offering | 28,877,999 shares | |

| Common stock to be outstanding after this offering | 29,877,999 shares | |

| Offering price per share of common stock | $5.00. See “Plan of Distribution.” | |

| Use of proceeds | We expect to receive net proceeds from this offering of approximately $4,429,496, based upon a public offering price of $5.00 per share of common stock, after deducting estimated broker commissions, estimated at $500,000, and estimated offering expenses, estimated at $70,504. We intend to use the net proceeds from this offering to fund new loan originations and for general corporate purposes. See “Use of Proceeds.” | |

| Risk factors | See “Risk Factors” beginning on page 7 of this prospectus for a discussion of some of the factors you should carefully consider before deciding to invest in our common stock. | |

| OTC trading symbol | IEGH |

| 6 |

SUMMARY HISTORICAL FINANCIAL DATA

The following table presents our summary historical financial data for the periods indicated. The summary historical financial data for the years ended December 31, 2014 and 2013 and the balance sheet data as of December 31, 2014 and 2013 are derived from the audited financial statements. The summary historical financial data for the nine months ended September 30, 2015 and 2014 and the balance sheet data as of September 30, 2015 and 2014 are derived from our unaudited financial statements.

Historical results are included for illustrative and informational purposes only and are not necessarily indicative of results we expect in future periods, and results of interim periods are not necessarily indicative of results for the entire year. You should read the following summary financial data in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes appearing elsewhere in this prospectus.

| Year

Ended December 31, | Nine

Months Ended September 30, | |||||||||||||||

| 2014 | 2013 | 2015 | 2014 | |||||||||||||

| (unaudited) | ||||||||||||||||

| Statement of Operations Data | ||||||||||||||||

| Total revenues | $ | 529,225 | $ | 62,949 | $ | 1,327,329 | 239,832 | |||||||||

| Total operating expenses | 5,381,671 | 4,345,539 | 4,984,986 | 4,115,113 | ||||||||||||

| Loss from operations | (4,852,446 | ) | (4,282,590 | ) | (3,657,657 | ) | (3,875,281 | ) | ||||||||

| Total other income (expense) | (549,308 | ) | (195,385 | ) | (581,696 | ) | (433,681 | ) | ||||||||

| Net loss | $ | (5,401,754 | ) | $ | (4,477,975 | ) | $ | (4,239,353 | ) | (4,308,962 | ) | |||||

| Net loss per share, basic and diluted | $ | (0.40 | ) | $ | (0.72 | ) | $ | (0.19 | ) | (0.37 | ) | |||||

| Balance Sheet Data (at period end) | ||||||||||||||||

| Cash and cash equivalents | $ | 433,712 | $ | 281,879 | $ | 1,697,982 | 2,367,308 | |||||||||

| Working capital (1) | 719,602 | (280,786 | ) | $ | 2,759,664 | (2,497,574 | ) | |||||||||

| Total assets | 4,929,120 | 922,140 | 8,654,389 | 5,093,570 | ||||||||||||

| Total liabilities | (2,537,156 | ) | (2,923,596 | ) | 124,080 | 4,143,010 | ||||||||||

| Stockholders’ equity (deficit) | 2,391,964 | (2,001,456 | ) | 8,530,309 | 950,560 | |||||||||||

(1) Working capital represents total current assets less total current liabilities.

Investment in our common stock involves a number of substantial risks. You should not invest in our stock unless you are able to bear the complete loss of your investment. In addition to the risks and investment considerations discussed elsewhere in this prospectus, the following factors should be carefully considered by anyone purchasing the securities offered through this prospectus. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations. If any of the following risks actually occur, our business could be harmed. In such case, the trading price of our common stock could decline and investors could lose all or a part of the money paid to buy our common stock.

| 7 |

Risks Related to Our Business and Industry

If our involvement in a December 11, 2014 article published in the Examiner or any other publicity regarding our company or the offering during the waiting period, including our December 2, 2014 press release, were held to be in violation of federal or state securities laws, we could incur monetary damages, fines or other damages that could have a material adverse effect on our financial condition and prospects.

On December 11, 2014, information about our company was published in an article by the Examiner. Our chief executive officer, Mr. Mathieson, did not participate in an interview with the author of the Examiner article. Rather, the author included certain quotations from Mr. Mathieson that were contained in prior press releases by us and summarized statements previously made by Mr. Mathieson that were contained in a prior article published by the Opportunist Magazine. Prior to its publication, the author of the December 11th article provided Mr. Mathieson a copy of the article.

In addition, we issued a press release on December 2, 2014 in which we referenced, among other things, our intention to file a registration statement on Form S-1 and to list our securities on NASDAQ. The December 2nd press release presented certain statements about our company in isolation and did not disclose many of the related risks and uncertainties described in this prospectus.

If it were determined that the December 11th article, the December 2nd press release or any of our other publicity-related activities constituted a violation of Section 5 of the Securities Act, the SEC and relevant state regulators could impose monetary fines or other sanctions as provided under relevant federal and state securities laws. Such regulators could also require us to make a rescission offer, which is an offer to repurchase the securities, to our stockholders that purchased shares in this offering. This could also give rise to a private right of action to seek a rescission remedy under Section 12(a)(2) of the Securities Act.

We are unable to quantify the extent of any monetary damages that we might incur if monetary fines were imposed, rescission were required or one or more other claims were successful. As of the date of this prospectus, we are not aware of any pending or threatened claims alleging violations of any federal or state securities laws. However, there can be no assurance that any such claim will not be asserted in the future or that the claimant in any such action will not prevail. The possibility that such claims may be asserted in the future will continue until the expiration of the applicable federal and state statutes of limitations, which generally vary from one to three years from the date of sale. If the payment of damages or fines is significant, it could have a material adverse effect on our cash flow, financial condition or prospects.

Our limited operating history and our failure since inception to achieve an operating profit makes our future prospects and financial performance unpredictable, and the current scale of our operations is insufficient to achieve profitability.

We commenced operations in 2010 and as a result, we have a limited operating history upon which a potential investor can evaluate our prospects and the potential value of an investment in our company. In addition, we have not made an operating profit since our incorporation. We remain subject to the risks inherently associated with new business enterprises in general and, more specifically, the risks of a new financial institution and, in particular, a new Internet-based financial institution. Our prospects are subject to the risks and uncertainties frequently encountered by companies in their early stages of development, including the risk that we will not be able to implement our business strategy. The current scale of our operations is insufficient to achieve profitability. If we are unable to implement our business strategy and grow our business, our business will be materially adversely affected.

Historically, we have been dependent on our credit facility.

We have been dependent on our credit facility with BFG Investment Holdings, LLC (“BFG”) to execute on our growth plans and operate our business. Effective July 15, 2015, BFG converted the credit facility from a revolving facility to a term loan, and we paid off the balance of the loan in August 2015. It will be very difficult to find a financing source to replace the revolving credit facility. The loss of our revolving credit facility could have a material adverse effect on our business. As a result of BFG’s conversion of the revolving credit facility to a term loan, monthly principal and interest payments equal to 100% of the consumer loan proceeds were due. We have been able to raise capital through the unregistered sale of shares of preferred stock to fund the increase in our loan book and, as a result, have not drawn down any funds from the credit facility since September 2014. Until we are able to replace the credit facility, we intend to continue to use the proceeds from equity sales to fund our operations.

On August 21, 2015, we, through certain of our wholly owned subsidiaries, paid an aggregate of $1,676,954.22, representing all principal and accrued interest under the Loan and Security Agreement, as amended (the “Loan Agreement”), among BFG and certain of our wholly owned subsidiaries. As a result, there is currently no outstanding balance under the Loan Agreement. However, the Loan Agreement continues in effect and we are subject to a net profit interest under which we are required to pay BFG 20% of the “Net Profit” of its subsidiary, IEC SPV, LLC, until 10 years from the date the loan is repaid in full. Net Profit is defined as the gross revenue less (i) interest paid on the loan, (ii) payments on any other debt incurred as a result of refinancing the loan through a third party, as provided in the Loan Agreement, (iii) any costs, fees or commissions paid on the existing credit facility, and (iv) charge-offs to bad debt resulting from consumer loans. The Net Profit arrangement can be terminated by us upon a payment of $3,000,000 to BFG.

| 8 |

Because our officers and board of directors will make all management decisions, you should only purchase our securities if you are comfortable entrusting our directors to make all decisions.

Our board of directors will have the sole right to make all decisions with respect to our management. Investors will not have an opportunity to evaluate the specific projects that will be financed with future operating income. You should not purchase our securities unless you are willing to entrust all aspects of our management to our officers and directors.

We may not be able to implement our plans for growth successfully, which could adversely affect our future operations.

Since January 1, 2014, the amount we have lent to borrowers (our loan book) has grown 1,772% from $587,000 to $10,989,023 as of December 31, 2015. We expect to continue to grow our loan book and number of customers at an accelerated rate following completion of this offering. Our future success will depend in part on our continued ability to manage our growth. We may not be able to achieve our growth plans, or sustain our historical growth rates or grow at all. Various factors, such as economic conditions, regulatory and legislative considerations and competition, may also impede our ability to expand our market presence. If we are unable to grow as planned, our business and prospects could be adversely affected.

Our inability to manage our growth could harm our business.

We anticipate that our loan book and customer base will continue to grow significantly over time. To manage the expected growth of our operations and personnel, we will be required to, among other things:

| ● | improve existing and implement new transaction processing, operational and financial systems, procedures and controls; | |

| ● | maintain effective credit scoring and underwriting guidelines; and | |

| ● | increase our employee base and train and manage this growing employee base. |

If we are unable to manage growth effectively, our business, prospects, financial condition and results of operations could be adversely affected.

We may need to raise additional capital that may not be available, which could harm our business.

Our growth will require that we generate additional capital either through retained earnings or the issuance of additional debt or equity securities. Additional capital may not be available on terms acceptable to us, if at all. Any equity financings could result in dilution to our stockholders or reduction in the earnings available to our common stockholders. If adequate capital is not available or the terms of such capital are not attractive, we may have to curtail our growth and our business, and our business, prospects, financial condition and results of operations could be adversely affected.

As an online consumer loan company whose principal means of delivering personal loans is the Internet, we are subject to risks particular to that method of delivery.

We are predominantly an online consumer loan company and there are a number of unique factors that Internet-based loan companies face. These include concerns for the security of personal information, the absence of personal relationships between lenders and customers, the absence of loyalty to a conventional hometown branch, customers’ difficulty in understanding and assessing the substance and financial strength of an online loan company, a lack of confidence in the likelihood of success and permanence of online loan companies and many individuals’ unwillingness to trust their personal details and financial future to a relatively new technological medium such as the Internet. As a result, some potential customers may be unwilling to establish a relationship with us.

Conventional “brick and mortar” consumer loan companies, in growing numbers, are offering the option of Internet-based lending to their existing and prospective customers. The public may perceive conventional established loan companies as being safer, more responsive, more comfortable to deal with and more accountable as providers of their lending needs. We may not be able to offer Internet-based lending that has sufficient advantages over the Internet-based lending services and other characteristics of conventional “brick and mortar” consumer loan companies to enable us to compete successfully.

| 9 |

We may not be able to make technological improvements as quickly as some of our competitors, which could harm our ability to compete with our competitors and adversely affect our results of operations, financial condition and liquidity.

Both the Internet and the financial services industry are undergoing rapid technological changes, with frequent introductions of new technology-driven products and services. In addition to improving the ability to serve customers, the effective use of technology increases efficiency and enables financial institutions to reduce costs. Our future success will depend in part upon our ability to address the needs of our customers by using technology to provide products and services that will satisfy customer demands, as well as to create additional efficiencies in our operations. We may not be able to effectively implement new technology-driven products and services or be successful in marketing these products and services to our customers. If we are unable, for technical, legal, financial or other reasons, to adapt in a timely manner to changing market conditions, customer requirements or emerging industry standards, our business, prospects, financial condition and results of operations could be adversely affected.

A significant disruption in our computer systems or a cyber security breach could adversely affect our operations.

We rely extensively on our computer systems to manage our loan origination and other processes. Our systems are subject to damage or interruption from power outages, computer and telecommunications failures, computer viruses, cyber security breaches, vandalism, severe weather conditions, catastrophic events and human error, and our disaster recovery planning cannot account for all eventualities. If our systems are damaged, fail to function properly or otherwise become unavailable, we may incur substantial costs to repair or replace them, and may experience loss of critical data and interruptions or delays in our ability to perform critical functions, which could adversely affect our business and results of operations. Any compromise of our security could also result in a violation of applicable privacy and other laws, significant legal and financial exposure, damage to our reputation, loss or misuse of the information and a loss of confidence in our security measures, which could harm our business.

Our ability to protect the confidential information of our borrowers and investors may be adversely affected by cyber-attacks, computer viruses, physical or electronic break-ins or similar disruptions.

We process certain sensitive data from our borrowers and investors. While we have taken steps to protect confidential information that we receive or have access to, our security measures could be breached. Any accidental or willful security breaches or other unauthorized access to our systems could cause confidential borrower and investor information to be stolen and used for criminal purposes. Security breaches or unauthorized access to confidential information could also expose us to liability related to the loss of the information, time-consuming and expensive litigation and negative publicity. If security measures are breached because of third-party action, employee error, malfeasance or otherwise, or if design flaws in our software are exposed and exploited, our relationships with borrowers and investors could be severely damaged, and we could incur significant liability.

Because techniques used to sabotage or obtain unauthorized access to systems change frequently and generally are not recognized until they are launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. In addition, federal regulators and many federal and state laws and regulations require companies to notify individuals of data security breaches involving their personal data. These mandatory disclosures regarding a security breach are costly to implement and often lead to widespread negative publicity, which may cause borrowers and investors to lose confidence in the effectiveness of our data security measures. Any security breach, whether actual or perceived, would harm our reputation, we could lose borrowers and investors and our business and operations could be adversely affected.

Any significant disruption in service on our platform or in our computer systems, including events beyond our control, could prevent us from processing or posting payments on loans, reduce the attractiveness of our marketplace and result in a loss of borrowers or investors.

In the event of a system outage and physical data loss, our ability to perform our servicing obligations, process applications or make loans available would be materially and adversely affected. The satisfactory performance, reliability and availability of our technology are critical to our operations, customer service, reputation and our ability to attract new and retain existing borrowers and investors.

Any interruptions or delays in our service, whether as a result of third-party error, our error, natural disasters or security breaches, whether accidental or willful, could harm our relationships with our borrowers and investors and our reputation. Additionally, in the event of damage or interruption, our insurance policies may not adequately compensate us for any losses that we may incur. Our disaster recovery plan has not been tested under actual disaster conditions, and we may not have sufficient capacity to recover all data and services in the event of an outage. These factors could prevent us from processing or posting payments on the loans, damage our brand and reputation, divert our employees’ attention, reduce our revenue, subject us to liability and cause borrowers and investors to abandon our marketplace, any of which could adversely affect our business, financial condition and results of operations.

| 10 |

Our unsecured loans generally have delinquency and default rates higher than prime and secured loans, which could result in higher loan losses.

We are in the business of originating unsecured personal loans. As of September 30, 2015, approximately 3.04% of our customers were subprime borrowers at loan origination date, which we define as borrowers having credit scores below 600 on the credit risk scale developed by VantageScore Solutions, LLC. Effective November 2014, we ceased lending to any borrowers with credit scores below 600. As a result, our percentage of subprime borrowers should decrease over the next four years. Unsecured personal loans and subprime loans generally have higher delinquency and default rates than secured loans and prime loans. Subprime borrowers are associated with lower collection rates and are subject to higher loss rates than prime borrowers. Subprime borrowers have historically been, and may in the future become, more likely to be affected, or more severely affected, by adverse macroeconomic conditions, particularly unemployment. If our borrowers default under an unsecured loan, we will bear a risk of loss of principal, which could adversely affect our cash flow from operations. Delinquency interrupts the flow of projected interest income from a loan, and default can ultimately lead to a loss. We attempt to manage these risks with risk-based loan pricing and appropriate management policies. However, we cannot assure you that such management policies will prevent delinquencies or defaults and, if such policies and methods are insufficient to control our delinquency and default risks and do not result in appropriate loan pricing, our business, financial condition, liquidity and results of operations could be harmed. If aspects of our business, including the quality of our borrowers, are significantly affected by economic changes or any other conditions in the future, we cannot be certain that our policies and procedures for underwriting, processing and servicing loans will adequately adapt to such changes. If we fail to adapt to changing economic conditions or other factors, or if such changes affect our borrowers’ capacity to repay their loans, our results of operations, financial condition and liquidity could be materially adversely affected. At September 30, 2015, we had 134 loans considered past due at 31+ days past due, representing 8.24% of the number of loans in our active portfolio. At September 30, 2015 we had 27 loans considered delinquent at 61-90 days past due, representing 1.66% of the loans in our active portfolio. At September 30, 2015, we had 71 loans in default (defined as 91+ days past due) representing 4.36% of the number of loans in our active portfolio. Loans become eligible for legal collection at 60 days past due.

If our estimates of loan receivable losses are not adequate to absorb actual losses, our provision for loan receivable losses would increase, which would adversely affect our results of operations.

We maintain an allowance for loans receivable losses. To estimate the appropriate level of allowance for loan receivable losses, we consider known and relevant internal and external factors that affect loan receivable collectability, including the total amount of loan receivables outstanding, historical loan receivable charge-offs, our current collection patterns, and economic trends. If customer behavior changes as a result of economic conditions and if we are unable to predict how the unemployment rate, housing foreclosures, and general economic uncertainty may affect our allowance for loan receivable losses, our provision may be inadequate. Our allowance for loan receivable losses is an estimate, and if actual loan receivable losses are materially greater than our allowance for loan receivable losses, our financial position, liquidity, and results of operations could be adversely affected.

Our risk management efforts may not be effective.

We could incur substantial losses and our business operations could be disrupted if we are unable to effectively identify, manage, monitor, and mitigate financial risks, such as credit risk, interest rate risk, prepayment risk, liquidity risk, and other market-related risks, as well as operational risks related to our business, assets and liabilities. Our risk management policies, procedures, and techniques, including our scoring methodology, may not be sufficient to identify all of the risks we are exposed to, mitigate the risks we have identified or identify additional risks to which we may become subject in the future.

We face strong competition for customers and may not succeed in implementing our business strategy.

Our business strategy depends on our ability to remain competitive. There is strong competition for customers from personal loan companies and other types of consumer lenders, including those that use the Internet as a medium for lending or as an advertising platform. Our competitors include:

| ● | large, publicly-traded, state-licensed personal loan companies such as SpringLeaf Holdings, and OneMain Financial, a subsidiary of CitiGroup; | |

| ● | peer-to-peer lending companies such as Lending Club and Prosper; | |

| ● | online personal loan companies such as Avant; | |

| ● | “brick and mortar” personal loan companies, including those that have implemented websites to facilitate online lending; and | |

| ● | payday lenders, tribal lenders and other online consumer loan companies. |

| 11 |

Some of these competitors have been in business for a long time and have name recognition and an established customer base. Most of our competitors are larger and have greater financial and personnel resources. In order to compete profitably, we may need to reduce the rates we offer on loans, which may adversely affect our business, prospects, financial condition and results of operations. To remain competitive, we believe we must successfully implement our business strategy. Our success depends on, among other things:

| ● | having a large and increasing number of customers who use our loans for financing needs; |

| ● | our ability to attract, hire and retain key personnel as our business grows; |

| ● | our ability to secure additional capital as needed; |

| ● | our ability to offer products and services with fewer employees than competitors; |

| ● | the satisfaction of our customers with our customer service; |

| ● | ease of use of our websites; and |

| ● | our ability to provide a secure and stable technology platform for providing personal loans that provides us with reliable and effective operational, financial and information systems. |

If we are unable to implement our business strategy, our business, prospects, financial condition and results of operations could be adversely affected.

We depend on third-party service providers for our core operations including online lending and loan servicing, and interruptions in or terminations of their services could materially impair the quality of our services.

We rely substantially upon third-party service providers for our core operations, including online web lending and marketing and vendors that provide systems that automate the servicing of our loan portfolios which allow us to increase the efficiency and accuracy of our operations. These systems include tracking and accounting of our loan portfolio as well as customer relationship management, collections, funds disbursement, security and reporting. This reliance may mean that we will not be able to resolve operational problems internally or on a timely basis, which could lead to customer dissatisfaction or long-term disruption of our operations. If these service arrangements are terminated for any reason without an immediately available substitute arrangement, our operations may be severely interrupted or delayed. If such interruption or delay were to continue for a substantial period of time, our business, prospects, financial condition and results of operations could be adversely affected.

If we lose the services of any of our key management personnel, our business could suffer.

Our future success significantly depends on the continued service and performance of our Chief Executive Officer, Paul Mathieson and our Chief Operating Officer, Carla Cholewinski. Competition for these employees is intense and we may not be able to attract and retain key personnel. We do not maintain any “key man” or other related insurance. The loss of the service of our Chief Executive Officer or our Chief Operating Officer, or the inability to attract additional qualified personnel as needed, could materially harm our business.

We have incurred, and will continue to incur, increased costs as a result of being a public reporting company.

In April 2015, we became a public reporting company. As a public reporting company, we incur significant legal, accounting and other expenses that we did not incur as a non-reporting company, including costs associated with our SEC reporting requirements. We expect that the additional reporting and other obligations imposed on us under the Exchange Act, will increase our legal and financial compliance costs and the costs of our related legal, accounting and administrative activities significantly. Management estimates that compliance with the Exchange Act reporting requirements as a reporting company will cost in excess of $200,000 annually. Given our current financial resources, these additional compliance costs could have a material adverse impact on our financial position and ability to achieve profitable results. These increased costs will require us to divert money that we could otherwise use to expand our business and achieve our strategic objectives.

We operate in a highly competitive market, and we cannot ensure that the competitive pressures we face will not have a material adverse effect on our results of operations, financial condition and liquidity.

The consumer finance industry is highly competitive. Our success depends, in large part, on our ability to originate consumer loan receivables. We compete with other consumer finance companies as well as other types of financial institutions that offer similar products and services in originating loan receivables. Some of these competitors may have greater financial, technical and marketing resources than we possess. Some competitors may also have a lower cost of funds and access to funding sources that may not be available to us. While banks and credit card companies have decreased their lending to non-prime customers in recent years, there is no assurance that such lenders will not resume those lending activities. Further, because of increased regulatory pressure on payday lenders, many of those lenders are starting to make more traditional installment consumer loans in order to reduce regulatory scrutiny of their practices, which could increase competition in markets in which we operate.

| 12 |

Negative publicity could adversely affect our business and operating results.

Negative publicity about our industry or our company, including the quality and reliability of our marketplace, effectiveness of the credit decisioning and scoring models used in the marketplace, changes to our marketplace, our ability to effectively manage and resolve borrower and investor complaints, privacy and security practices, litigation, regulatory activity and the experience of borrowers and investors with our marketplace or services, even if inaccurate, could adversely affect our reputation and the confidence in, and the use of, our marketplace, which could harm our business and operating results. Harm to our reputation can arise from many sources, including employee misconduct, misconduct by our partners, outsourced service providers or other counterparties, failure by us or our partners to meet minimum standards of service and quality, inadequate protection of borrower and investor information and compliance failures and claims.

Our business is subject to extensive regulation in the jurisdictions in which we conduct our business.

Our operations are subject to regulation, supervision and licensing under various federal, state and local statutes, ordinances and regulations. In most states in which we operate, a consumer credit regulatory agency regulates and enforces laws relating to consumer lenders such as us. These rules and regulations generally provide for licensing as a consumer lender, limitations on the amount, duration and charges, including interest rates, for various categories of loans, requirements as to the form and content of finance contracts and other documentation, and restrictions on collection practices and creditors’ rights. In certain states, we are subject to periodic examination by state regulatory authorities. Some states in which we operate do not require special licensing or provide extensive regulation of our business.

We are also subject to extensive federal regulation, including the Truth in Lending Act, the Equal Credit Opportunity Act and the Fair Credit Reporting Act. These laws require us to provide certain disclosures to prospective borrowers and protect against discriminatory lending and leasing practices and unfair credit practices. The principal disclosures required under the Truth in Lending Act include the terms of repayment, the total finance charge and the annual percentage rate charged on each contract or loan. The Equal Credit Opportunity Act prohibits creditors from discriminating against credit applicants on the basis of race, color, religion, national origin, sex, age or marital status. According to Regulation B promulgated under the Equal Credit Opportunity Act, creditors are required to make certain disclosures regarding consumer rights and advise consumers whose credit applications are not approved of the reasons for the rejection. In addition, the credit scoring system used by us must comply with the requirements for such a system as set forth in the Equal Credit Opportunity Act and Regulation B. The Fair Credit Reporting Act requires us to provide certain information to consumers whose credit applications are not approved on the basis of a report obtained from a consumer reporting agency and to respond to consumers who inquire regarding any adverse reporting submitted by us to the consumer reporting agencies. Additionally, we are subject to the Gramm-Leach-Bliley Act, which requires us to maintain the privacy of certain consumer data in our possession and to periodically communicate with consumers on privacy matters. We are also subject to the Servicemembers Civil Relief Act, which requires us, in most circumstances, to reduce the interest rate charged to customers who have subsequently joined, enlisted, been inducted or called to active military duty.

A material failure to comply with applicable laws and regulations could result in regulatory actions, lawsuits and damage to our reputation, which could have a material adverse effect on our results of operations, financial condition and liquidity.

The Consumer Financial Protection Bureau (the “CFPB”) is a new agency, and there continues to be uncertainty as to how the agency’s actions or the actions of any other new agency could impact our business or that of our issuing banks.

The CFPB, which commenced operations in 2011, has broad authority over the business in which we engage. This includes authority to write regulations under federal consumer financial protection laws, such as the Truth in Lending Act and the Equal Credit Opportunity Act, and to enforce those laws against and examine financial institutions for compliance. The CFPB is authorized to prevent “unfair, deceptive or abusive acts or practices” through its regulatory, supervisory and enforcement authority. To assist in its enforcement, the CFPB maintains an online complaint system that allows consumers to log complaints with respect to various consumer finance products, including the loan products we facilitate. This system could inform future CFPB decisions with respect to its regulatory, enforcement or examination focus.

We are subject to the CFPB’s jurisdiction, including its enforcement authority, as a servicer and acquirer of consumer credit. The CFPB may request reports concerning our organization, business conduct, markets and activities. The CFPB may also conduct on-site examinations of our business on a periodic basis if the CFPB were to determine, through its complaint system, that we were engaging in activities that pose risks to consumers.

There continues to be uncertainty as to how the CFPB’s strategies and priorities, including in both its examination and enforcement processes, will impact our businesses and our results of operations going forward. Actions by the CFPB could result in requirements to alter or cease offering affected loan products and services, making them less attractive and restricting our ability to offer them.

Actions by the CFPB or other regulators against us or our competitors that discourage the use of the marketplace model or suggest to consumers the desirability of other loan products or services could result in reputational harm and a loss of borrowers or investors. Our compliance costs and litigation exposure could increase materially if the CFPB or other regulators enact new regulations, change regulations that were previously adopted, modify, through supervision or enforcement, past regulatory guidance, or interpret existing regulations in a manner different or stricter than have been previously interpreted.

| 13 |

Our accountants have raised substantial doubt regarding our ability to continue as a going concern.

As noted in our consolidated financial statements, we had an accumulated stockholders’ deficit of approximately $14.68 million and recurring losses from operations as of December 31, 2014. We intend to fund operations through raising additional capital through debt financing and equity issuances and increased lending activities which may be insufficient to fund our capital expenditures, working capital or other cash requirements for the year ending December 31, 2016. We are continuing to seek additional funds to finance our immediate and long term operations. The successful outcome of future financing activities cannot be determined at this time and there is no assurance that if achieved, we will have sufficient funds to execute our intended business plan or generate positive operating results. These factors, among others, raise substantial doubt about our ability to continue as a going concern. The audit report of Rose, Snyder & Jacobs LLP for the fiscal years ended December 31, 2014 and 2013 contains a paragraph that emphasizes the substantial doubt as to our continuance as a going concern. This means that there is a significant risk that we may not be able to remain operational for an indefinite period of time.

Risks Relating to Our Common Stock and the Offering

Trading on the OTC Markets is volatile and sporadic, which could depress the market price of our common stock and make it difficult for our security holders to resell their common stock.

Our common stock is currently quoted on the OTCQB tier of the OTC Markets. Trading in securities quoted on the OTC Markets is often thin and characterized by wide fluctuations in trading prices, due to many factors, some of which may have little to do with our operations or business prospects. This volatility could depress the market price of our common stock for reasons unrelated to operating performance. Moreover, the OTC Markets is not a stock exchange, and trading of securities on the OTC Markets is often more sporadic than the trading of securities listed on a quotation system like NASDAQ or a stock exchange like the New York Stock Exchange. These factors may result in investors having difficulty reselling any shares of our common stock.

Our common stock price is likely to be highly volatile because of several factors, including a limited public float.

The market price of our common stock has been volatile in the past and the market price of our common stock is likely to be highly volatile in the future. You may not be able to resell shares of our common stock following periods of volatility because of the market’s adverse reaction to volatility.

Other factors that could cause such volatility may include, among other things:

| ● | actual or anticipated fluctuations in our operating results; | |

| ● | the absence of securities analysts covering us and distributing research and recommendations about us; | |

| ● | we may have a low trading volume for a number of reasons, including that a large portion of our stock is closely held; | |

| ● | overall stock market fluctuations; | |

| ● | announcements concerning our business or those of our competitors; | |

| ● | actual or perceived limitations on our ability to raise capital when we require it, and to raise such capital on favorable terms; | |

| ● | conditions or trends in the industry; | |

| ● | litigation; | |

| ● | changes in market valuations of other similar companies; | |

| ● | future sales of common stock; | |

| ● | departure of key personnel or failure to hire key personnel; and | |

| ● | general market conditions. |

Any of these factors could have a significant and adverse impact on the market price of our common stock. In addition, the stock market in general has at times experienced extreme volatility and rapid decline that has often been unrelated or disproportionate to the operating performance of particular companies. These broad market fluctuations may adversely affect the trading price of our common stock, regardless of our actual operating performance.

| 14 |

Our common stock has in the past been a “penny stock” under SEC rules. It may be more difficult to resell securities classified as “penny stock.”

In the past, our common stock was a “penny stock” under applicable SEC rules (generally defined as non-exchange traded stock with a per-share price below $5.00). Unless we maintain a per-share price above $5.00, these rules impose additional sales practice requirements on broker-dealers that recommend the purchase or sale of penny stocks to persons other than those who qualify as “established customers” or “accredited investors.” For example, broker-dealers must determine the appropriateness for non-qualifying persons of investments in penny stocks. Broker-dealers must also provide, prior to a transaction in a penny stock not otherwise exempt from the rules, a standardized risk disclosure document that provides information about penny stocks and the risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, disclose the compensation of the broker-dealer and its salesperson in the transaction, furnish monthly account statements showing the market value of each penny stock held in the customer’s account, provide a special written determination that the penny stock is a suitable investment for the purchaser, and receive the purchaser’s written agreement to the transaction.

Legal remedies available to an investor in “penny stocks” may include the following:

| ● | If a “penny stock” is sold to the investor in violation of the requirements listed above, or other federal or states securities laws, the investor may be able to cancel the purchase and receive a refund of the investment. | |

| ● | If a “penny stock” is sold to the investor in a fraudulent manner, the investor may be able to sue the persons and firms that committed the fraud for damages. |

However, investors who have signed arbitration agreements may have to pursue their claims through arbitration.

These requirements may have the effect of reducing the level of trading activity, if any, in the secondary market for a security that becomes subject to the penny stock rules. The additional burdens imposed upon broker-dealers by such requirements may discourage broker-dealers from effecting transactions in our securities, which could severely limit the market price and liquidity of our securities. These requirements may restrict the ability of broker-dealers to sell our common stock and may affect your ability to resell our common stock.

Many brokerage firms will discourage or refrain from recommending investments in penny stocks. Most institutional investors will not invest in penny stocks. In addition, many individual investors will not invest in penny stocks due, among other reasons, to the increased financial risk generally associated with these investments.

For these reasons, penny stocks may have a limited market and, consequently, limited liquidity. We can give no assurance at what time, if ever, our common stock will not be classified as a “penny stock” in the future.

If we fail to maintain effective internal control over financial reporting, the price of our securities may be adversely affected.

Our internal control over financial reporting may have weaknesses and conditions that could require correction or remediation, the disclosure of which may have an adverse impact on the price of our common stock. We are required to establish and maintain appropriate internal control over financial reporting. Failure to establish those controls, or any failure of those controls once established, could adversely affect our public disclosures regarding our business, prospects, financial condition or results of operations. In addition, management’s assessment of internal control over financial reporting may identify weaknesses and conditions that need to be addressed in our internal control over financial reporting or other matters that may raise concerns for investors. Any actual or perceived weaknesses and conditions that need to be addressed in our internal control over financial reporting or disclosure of management’s assessment of our internal control over financial reporting may have an adverse impact on the price of our common stock.

We are required to comply with certain provisions of Section 404 of the Sarbanes-Oxley Act and if we fail to continue to comply, our business could be harmed and the price of our securities could decline.

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act require an annual assessment of internal control over financial reporting, and for certain issuers an attestation of this assessment by the issuer’s independent registered public accounting firm. The standards that must be met for management to assess the internal control over financial reporting as effective are evolving and complex, and require significant documentation, testing, and possible remediation to meet the detailed standards. We expect to incur significant expenses and to devote resources to Section 404 compliance on an ongoing basis. It is difficult for us to predict how long it will take or costly it will be to complete the assessment of the effectiveness of our internal control over financial reporting for each year and to remediate any deficiencies in our internal control over financial reporting. As a result, we may not be able to complete the assessment and remediation process on a timely basis. In the event that our Chief Executive Officer or Chief Financial Officer determines that our internal control over financial reporting is not effective as defined under Section 404, we cannot predict how regulators will react or how the market prices of our securities will be affected; however, we believe that there is a risk that investor confidence and the market value of our securities may be negatively affected.

| 15 |

Our Chief Executive Officer has, and will continue to have after giving effect to this offering, voting control, which will limit your ability to influence the outcome of important transactions, including a change in control.

As of January 25, 2016, Mr. Mathieson beneficially owns 5,000,000 shares of our common stock and 1,000,000 shares of our Series A preferred stock convertible at any time into 32,000,000 shares of our common stock. Our Series A preferred stock votes together with the common stock on all matters submitted to our stockholders for approval and each share of Series A preferred stock entitles the holder to 1,001 votes per share. In contrast, each share of our common stock has one vote per share. Upon the completion of this offering, Mr. Mathieson, our Chief Executive Officer, will hold approximately 97.6 % of the voting power of our outstanding capital stock. Because of the 1,001-to-1 voting ratio between our Series A preferred stock and our common stock, after the completion of this offering, Mr. Mathieson will continue to control a majority of the combined voting power of our capital stock and therefore be able to control all matters submitted to our stockholders for approval. Mr. Mathieson may have interests that differ from yours and may vote in a way with which you disagree and which may be adverse to your interests. This concentrated voting power may have the effect of delaying, preventing or deterring a change in control of our company, could deprive our stockholders of an opportunity to receive a premium for their capital stock as part of a sale of our company and might ultimately affect the market price of our common stock.

As a board member, Mr. Mathieson owes a fiduciary duty to our stockholders and must act in good faith and in a manner he reasonably believes to be in the best interests of our stockholders. As a stockholder, Mr. Mathieson is entitled to vote his shares in his own interest, which may not always be in the interests of our stockholders generally. For a description of the Series A preferred stock, see the section titled “Description of Securities—Description of Series A Preferred Stock.”

Our management team will have immediate and broad discretion over the use of the net proceeds from this offering and we may use the net proceeds in ways with which you disagree.