Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - AMERIQUEST, INC. | a2226550zex-23_1.htm |

| EX-10.20 - EX-10.20 - AMERIQUEST, INC. | a2226550zex-10_20.htm |

| EX-10.21 - EX-10.21 - AMERIQUEST, INC. | a2226550zex-10_21.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

Index to Consolidated Financial Statements

As filed with the Securities and Exchange Commission January 12, 2016

Registration No. 333-207897

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

to

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

AMERIQUEST, INC.

(Exact name of Registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

7374 (Primary Standard Industrial Classification Code Number) |

47-3684547 (I.R.S. Employer Identification Number) |

AmeriQuest, Inc.

457 Haddonfield Road

Suite 220

Cherry Hill, NJ 08002

(800) 608-0809

(Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices)

Douglas W. Clark

President and Chief Executive Officer

9045 Strada Stell Court

Suite 301

Naples, FL 34109

(800) 608-0809

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||||

Jeffrey D. Saper, Esq. Michael C. Labriola, Esq. Kenisha D. Nicholson, Esq. Wilson Sonsini Goodrich & Rosati, P.C. 1700 K Street NW, Fifth Floor Washington, DC 20006 (202) 973-8800 |

Mark Joyce Executive Vice President and Chief Financial Officer AmeriQuest, Inc. 2651 Warrenville Road Suite 560 Downers Grove, IL 60515 (800) 608-0809 |

Keith Townsend, Esq. Laura Bushnell, Esq. Carrie Ratliff, Esq. King & Spalding LLP 1180 Peachtree Street, N.E. Atlanta, GA 30309 (404) 572-4600 |

||

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered(1) |

Proposed Maximum Aggregate Price Per Share |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) |

||||

|---|---|---|---|---|---|---|---|---|

Common Stock, par value $0.001 per share |

7,076,922 | $13.00 | $91,999,986 | $9,265 | ||||

|

||||||||

- (1)

- Includes

shares the underwriters have the option to purchase to cover over-allotments, if any.

- (2)

- Estimated

solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as

amended.

- (3)

- The Registrant previously paid $7,553 in connection with prior filing of this Registration Statement.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to completion)

Issued January 12, 2016

6,153,846 Shares

This is the initial public offering of common stock of AmeriQuest, Inc. Prior to this offering, no public market has existed for our common stock. We are offering 6,153,846 shares. We currently estimate that the initial public offering price will be between $11.00 and $13.00 per share. We have applied to list our common stock on the NASDAQ Global Market under the symbol "AMQ."

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 12.

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Initial public offering price |

$ | $ | |||||

Underwriting discounts and commissions(1) |

$ | $ | |||||

Proceeds to us, before expenses |

$ | $ | |||||

- (1)

- Please see the section of this prospectus entitled "Underwriting" for additional information regarding underwriter compensation.

The selling stockholders identified in this prospectus have granted the underwriters the right to purchase up to an additional 923,076 shares of common stock at the price to public less underwriting discounts and commissions. The underwriters can exercise this option within 30 days from the date of this prospectus. We will not receive any of the proceeds from any sale of shares by the selling stockholders.

We are an "emerging growth company" as defined under U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements after this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of our common stock to purchasers on or about , 2016.

| RAYMOND JAMES | STEPHENS INC. |

| BAIRD | WILLIAM BLAIR |

The date of this prospectus is , 2016

TABLE OF CONTENTS

Neither we, the selling stockholders nor the underwriters have authorized anyone to provide you with information that is different from that contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the selling stockholders and the underwriters are offering to sell shares of common stock and seeking offers to buy shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date on the front of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2016 (25 days after the date of this prospectus), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

For investors outside the United States: neither we, the selling stockholders nor any of the underwriters have done anything that would permit this offering, or possession or distribution of this prospectus, in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside of the United States.

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes thereto and the information set forth under the sections "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," in each case included in this prospectus. Some of the statements in this prospectus constitute forward-looking statements. See "Cautionary Note Regarding Forward-Looking Statements."

Unless the context requires otherwise, the words "we," "us," "our," "our company" and "our business" refer to AmeriQuest, Inc., a Delaware corporation, and prior to the reorganization described elsewhere in this prospectus summary, AmeriQuest Business Services, Inc., a New Jersey corporation, and in each case, their consolidated subsidiaries.

Overview

We are a growing provider of technology-enabled business-to-business solutions that address the financial process, procurement and asset management needs of businesses. Our solutions are designed to eliminate the inefficiency, expense and lost opportunities caused by traditional paper-based processes, allowing our customers to be competitive. We leverage our deep industry expertise, proprietary technology and customer and supplier relationships to help enterprises and organizations of varying sizes manage complex and dynamic operational and administrative processes that are frequently managed manually and require substantial internal resources. While we originated as a provider of procurement and fleet management solutions for the transportation industry, we have used our technology and the expertise we developed to offer robust financial process automation solutions and more advanced procurement solutions to companies in multiple industries in recent years.

Our financial process automation solutions consist primarily of our cloud-based technology offerings that automate accounts receivable and accounts payable processes for our customers, including e-invoicing, credit and collections management, working capital management and reporting analytics. These solutions are delivered through two products: our accounts receivable automation platform; and our accounts payable automation platform. Our procurement solutions leverage our financial process automation technology to conduct group purchasing, predominantly for goods supporting the transportation industry, enabling companies to optimize their procurement processes from sourcing through payment. Our asset management solutions provide data-driven strategic planning, asset acquisition and disposition, and asset financing and usage alternatives to help businesses, predominantly in the transportation industry, to lower the total cost of capital asset ownership. Our cloud-based solutions are highly scalable and offered in an à la carte format, so that our customers can selectively purchase those solutions that they need. These complementary business solutions enable us to capitalize on our customer and supplier network, cross-selling opportunities and operational scale.

PayStream Advisors, a third-party research and consulting firm, estimates that business-to-business trade in the United States was conducted through 16.5 billion invoices distributed among approximately 10 million businesses during 2013. Entities of various sizes incur substantial costs to process and facilitate these business-to-business transactions. Traditionally, these transactions have been paper-based, labor-intensive and error-prone. Moreover, many businesses lack scale, real-time data and specialized personnel for these transactions, all of which can cause operational inefficiencies and excess cost.

We have provided technology-enabled solutions to the transportation sector for nearly twenty years. However, we expanded our focus in recent years, and our financial process automation solutions and our procurement solutions now offer a comprehensive suite of technology-enabled services to

1

purchasers and suppliers in other sectors, including the manufacturing, retail, energy, higher education and media industries. During the year ended December 31, 2014, we serviced over 2,250 customers varying by size and industry, including Daimler Trucks North America, LLC, or Daimler, the University of Florida, Dot Transportation, Inc. and Cardinal Logistics Management Corporation. We processed $12.2 billion in transaction volume and 9.2 million transactions through our financial process automation and procurement solutions for our customers and their transaction partners during the year ended December 31, 2014.

We have experienced substantial growth as we have expanded into new sectors. Our total revenue was $57.6 million, $67.4 million and $84.8 million during the years ended December 31, 2012, 2013 and 2014, respectively, a compound annual growth rate, or CAGR, of 21.4% over those periods. Our net income was $0.6 million, $4.6 million and $6.8 million during the years ended December 31, 2012, 2013 and 2014, respectively. Our adjusted EBITDA(1) was $12.6 million, $21.6 million and $25.9 million during the years ended December 31, 2012, 2013 and 2014, respectively, representing a CAGR of 43.3% over those periods. Our total revenue was $63.9 million and $65.2 million, our net income was $4.6 million and $4.2 million and our adjusted EBITDA was $18.3 million and $21.0 million during the nine months ended September 30, 2014 and 2015, respectively.

Industry background and trends

We believe a significant market opportunity exists for technology-enabled business-to-business solutions that assist enterprises with their financial process, procurement and asset management needs. These traditional processes are often poorly managed or controlled within a business, resulting in several common challenges:

Traditional, manual business-to-business processes are often expensive and error-prone. Ardent Partners recently estimated that "best-in-class" corporations experience invoice exceptions at less than half the rate experienced by other businesses. These best-in-class businesses are characterized by a high level of standardized accounts payable processes, automated approval routing and straight-through invoice processing. Ardent Partners estimates that these best-in-class businesses process accounts payable invoices at over 86% lower cost and over 78% faster than other businesses.

Achieving the benefits of scale is difficult even for large organizations. Many suppliers provide improved pricing with greater purchasing volume. Businesses that lack sufficient purchasing volume for certain goods and services may receive inferior pricing as compared to competitors, notwithstanding that procurement spending may be a relatively large and material element of their business.

Traditional finance and procurement overhead is often fixed. Finance and procurement personnel costs are typically fixed and not easily scaled to respond to fast-changing business conditions. Businesses need more staff during periods of growth and fewer staff during slowdowns. In addition, manual staffing is inherently difficult to size, even at its most effective, in smaller organizations. Businesses are also reluctant to invest in qualified and experienced administrative and operations personnel due to unpredictable market conditions.

Multi-party business transactions are complex. The average U.S. business annually transacts with hundreds of counterparties, including customers, partners, and suppliers, creating complex multi-

- (1)

- Adjusted EBITDA is a financial measure that is not calculated in accordance with U.S. generally accepted accounting principles, or GAAP. A reconciliation of this non-GAAP measure to the most directly comparable GAAP measure along with a summary of the definition and its material limitations are included at "Selected Consolidated Financial Data—Other key financial metrics—Adjusted EBITDA."

2

party transactions. These participants frequently operate without a common system to communicate in an automated and paperless environment, often relying on several different types of electronic data interchange, or EDI, systems and data formats, which also increases the complexity of transactions.

Increased need for real-time visibility and effective internal controls. Businesses are operating in an increasingly fast-paced, complex and global environment. Enabling fast and accurate decision-making with real-time and reliable information is critical to the long-term success of most organizations. Beyond the business incentive, many businesses are also subject to increasing demands on their internal controls structure imposed by increased regulations.

Managing working capital efficiently can be challenging. Many companies have the opportunity to enhance stockholder value by managing working capital more efficiently but are encumbered by a number of internal challenges. Aberdeen Group estimates that comprehensive accounts payable automation solutions increase a business's early payment discount savings by up to 340 basis points as compared to businesses without a centralized, automated accounts payable system. At the same time, many suppliers lack the resources to efficiently manage the large number of customers that they service.

Legacy business-to-business systems lack modern architecture and desired user experience. Users expect immediate and secure access to their enterprises' critical business information, but many business-to-business applications do not offer an optimized user experience, availability on personal mobile devices and ease-of-deployment.

Our solutions

Our solutions are designed to leverage our industry experience and investments in technology to address common challenges for businesses of various sizes and across a variety of industries.

Financial process automation solutions

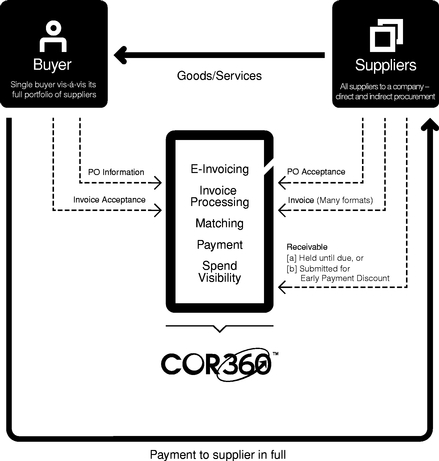

Our cloud-based financial process automation solutions address key participants in the business-to-business community, including manufacturers, suppliers, dealers, distributors, trading partners and end customers. We enable companies to streamline, automate and manage transaction processes including e-invoicing, accounts payable, accounts receivable, collections, order management, credit risk management, reporting and payments. Our financial process automation solutions provide the following key benefits:

Automation of manual, labor-intensive processes. By transforming manual, paper-based purchase order and invoice processes to automated and electronic processes, our solutions help companies eliminate unnecessary overhead and error risk related to these tasks.

Seamless integration. Our cloud-based financial process automation and procurement solutions utilize our proprietary transaction engine technology to enable fast connections among trading partners by turning every trading transaction into standardized data that is transmitted real-time into the relevant system.

Increased visibility and reporting capabilities. Customers benefit from end-to-end visibility into transaction processes, which enables them to maintain visibility of and collaboration among buyers and sellers and to automate entire accounts receivable and accounts payable departments without compromising business requirements.

Access to channel finance and credit and collections management. Our accounts receivable financial process automation solutions provide channel finance to a closed community of purchasers that

3

vary by size and industry, allowing suppliers to reduce and often minimize their credit exposure to significant segments of their customer base.

Cloud-based delivery with enhanced user experience. Our financial process automation solutions utilize a cloud-based Business-Process-as-a-Service, or BPaaS, delivery model and provide a modern and intuitive user interface.

Deep domain and best practices expertise. Our financial process automation solutions are supported by our long history in financial process management.

Procurement solutions

Our procurement solutions enable organizations to realize the benefits of volume-based, electronic procurement by identifying and establishing contracts with suppliers, aggregating the collective purchasing power of all participating customers and promoting process efficiencies of electronic transactions. Our procurement solutions provide the following key benefits:

High-volume purchasing power. We aggregate the purchasing power of our customers to provide pricing comparable to that available to high-volume purchasers, allowing our customers to more effectively compete.

Enhanced access to supplier network and purchasers. Our purchasers gain access to more than 5,000 dealers and distributors for over 135 suppliers currently using our solution. At the same time, we assume credit responsibility for customers purchasing through our system and guarantee timely payment to suppliers, allowing suppliers to reach more customers.

Strategic procurement expertise. Our supply management team has deep expertise in strategic sourcing, contract and price negotiation, supplier selection and supplier relationship management.

Seamless integration. Our cloud-based procurement solutions are delivered entirely using our proprietary transaction engine, the same interface platform that supports our cloud-based financial process automation solutions, which enables fast and standardized communication among participants.

Enhanced user experience. Our customers and suppliers input and process their transactions through our financial process automation platform, allowing purchasers the benefit of a comprehensive buyer's guide, workflow improvement tools and automated spending analysis in addition to our procurement pricing benefits. Purchaser and supplier user experiences are designed to be intuitive and accessible to novice users with minimal training.

Asset management solutions

Our asset management solutions provide data-driven strategic planning, asset acquisition and disposition strategies, and asset financing and asset utilization alternatives, all of which are designed to lower the total cost of capital asset ownership. Although these solutions are presently focused on the transportation industry, we believe they have application across a variety of industries with similar needs. Our solutions provide the following key benefits:

Data-driven asset management strategy. Utilizing our proprietary technology platform and deep transportation industry expertise, we can provide businesses with analyses of their current asset usage and suggest alternative strategies, allowing our customers to gain operational leverage by lowering the total cost of ownership of capital equipment.

4

Lower asset acquisition costs and optimum resale gains. When capital equipment is identified and specified properly by an acquirer, and is part of an overall asset lifecycle strategy, companies benefit from lower asset acquisition costs, and can also dispose of their assets at the optimal time to ensure maximum residual value.

Deep domain expertise in asset management and regulatory compliance. Our established relationships with some of the country's largest lenders allow us to provide advice and access strategic financing for our customers for the full lifecycle of capital assets. Our asset management experts also have deep knowledge of asset regulations and mandates.

Our strengths

We believe that we are well positioned to benefit from the transformations occurring in the business-to-business transaction market, including the growing trend toward enterprise-wide automation. Our key competitive strengths include:

End-to-end solution suite. Our flexible, menu-driven approach allows companies to select individual services from our solutions in order to maximize value and impact. Our financial process automation solutions address the full procure-to-pay cycle and the full order-to-cash sales cycle. Our procurement and asset management solutions assist in managing the procurement and full capital asset purchase and use cycle needs of our customers.

Highly scalable, proprietary technology. Our proprietary financial process automation and procurement solutions are delivered via a cloud-based BPaaS model. Our infrastructure has the flexibility to support significant growth in transaction volume from new and existing customers. As an example, since December 31, 2012, our financial process automation and procurement solutions transaction volume has increased from $3.4 billion to $12.2 billion, or 259%, and the number of transactions has increased from 2.7 million to 9.2 million, or 241%, without the need for substantial capital expenditures or significant changes to our technology infrastructure to support the increased demands on our solutions.

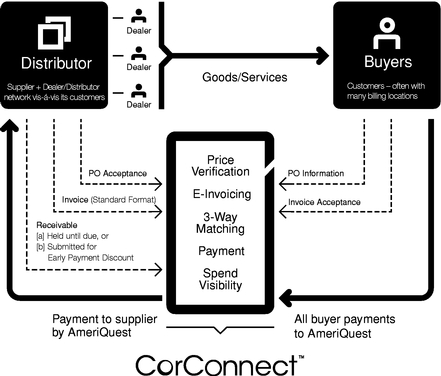

Powerful network effect. Our proprietary CorConnect solution is a closed-loop private commerce network that connects an entire purchasing cycle ecosystem—suppliers, dealers, distributors, vendors and purchasers. As our networks of purchasers and suppliers grow, they become more powerful and mutually reinforcing, increasing the value and desirability of participation in our solutions.

Strong customer retention. We focus extensively on assisting our customers to maximize their benefit from our solutions, and we frequently engage with our customers to continue to improve our offerings to meet their needs. As an illustration, 96% of our top 100 financial process automation and procurement solutions customers in 2012 made purchases from us in the nine month period ended September 30, 2015. We determined our top 100 financial process automation and procurement solutions customers based on our customers' overall gross transaction volume in dollars in 2012.

Deep domain expertise. We have deep domain experience and are an established leader in the transportation industry. In 2014, approximately a third of North America's 100 largest private trucking fleets utilized us for one or more of our financial process automation, procurement or asset management solutions.

Highly visible business model. Our transaction-based model with volume minimums for our financial process automation solutions and consistency of customer transaction levels year-over-year for our procurement solutions provide strong visibility of future revenue, enhancing our ability to effectively manage our business.

5

Our growth strategy

Our key strategic initiatives include:

Selectively expand into new markets. We intend to continue to selectively expand into new markets in which we can leverage our domain expertise, particularly in industries lagging in the adoption of paperless solutions for processes such as procurement and billing.

Further penetrate our existing markets. We will continue to invest in sales and marketing to increase our profile within the transportation industry, while also increasing our emphasis on customer acquisition opportunities in adjacent industries, such as manufacturing and industrials.

Capitalize on cross-selling opportunities. As of December 31, 2014, only 9% of our customers purchased more than one of our solutions during the fiscal year then ended, which we believe provides a substantial sales opportunity within our existing base of more than 2,250 customers. As we expand our product capabilities to include additional features, we expect our customers will perceive and derive even greater value from our platform and expand their use in the future.

Leverage our technology offerings. We intend to enhance our collaboration with our customers and continue to build functionality to address their needs and requirements. The investment in our software solutions, expansion of our procurement capabilities and development of new applications, features and functionality should allow us to expand our addressable market across other verticals.

Selectively pursue acquisitions. We may pursue acquisitions of businesses, technologies and solutions that are complementary to our existing offerings. We may also pursue acquisitions that allow us to expand into new industries or geographies where we do not currently have a significant presence.

Risks affecting us

Investing in our common stock involves risk. You should carefully consider all the information in this prospectus prior to investing in our common stock. These risks are discussed more fully in the section entitled "Risk Factors" immediately following this prospectus summary. These risks and uncertainties include, but are not limited to, the following:

- •

- our failure to adequately assess and monitor the credit risks of our customers;

- •

- our dependence on a small number of customer relationships, such as with Daimler;

- •

- a loss of or decrease in sales from key customers or supplier relationships;

- •

- long and unpredictable sales cycles that require significant employee time and financial resources;

- •

- our inability to effectively expand the reach of our existing products to new customers and new markets and sustain recent growth

rates;

- •

- our inability to compete effectively; and

- •

- declines in general economic conditions, and in particular, demand for products and services offered through our procurement solutions.

Corporate information and reorganization

We were originally organized in 1996 as a New Jersey corporation. In September 2015, we effected a corporate reorganization. Pursuant to this reorganization, AmeriQuest, Inc., a Delaware corporation formed in April 2015, acquired all of the outstanding shares of capital stock of AmeriQuest Business

6

Services, Inc., or ABI, in a share exchange. Following such reorganization, ABI became a wholly owned subsidiary of AmeriQuest, Inc., the issuer in this offering.

Our principal executive offices are located at 457 Haddonfield Road, Suite 220, Cherry Hill, NJ 08002, and our telephone number is (800) 608-0809. You can access our website at www.ameriquestcorp.com. Information contained on our website is not part of this prospectus and is not incorporated in this prospectus by reference.

We have registered the AMERIQUEST, AMERIQUEST TRANSPORTATION SERVICES, COR360 and ONECONNECT trademarks in the U.S. in certain classes of goods and services applicable to our business. We have several other trademarks, service marks and pending applications relating to our solutions, including for CORCONNECT and CORCENTRIC. Solely for convenience, trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names. This prospectus may also contain trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners.

7

Common stock offered by us |

6,153,846 shares | |

Common stock to be outstanding after this offering |

19,043,814 shares |

|

Underwriters' option |

The underwriters have been granted a 30-day option to purchase up to an additional 923,076 shares, all of which will be sold by the selling stockholders named herein. |

|

Use of proceeds |

We estimate that the net proceeds to us from the sale of our common stock in this offering will be approximately $63.6 million, based on an assumed initial public offering price of $12.00 per share, which is the midpoint of the price range listed on the cover page of this prospectus, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

|

|

The principal purposes of this offering are to create a public market for our common stock and to facilitate our future access to the public capital markets, as well as to obtain additional capital. We may use a portion of the proceeds from this offering for future acquisitions of complementary businesses, technologies or other assets, although we do not currently have any plans for any acquisitions. In addition, if we do not apply some or all of the proceeds towards acquisitions, we may use some of the remaining net proceeds from this offering to reduce the outstanding indebtedness under the long-term promissory notes issued in connection with purchase of equipment for certain of our asset management leasing operations, and we may use the remainder of the net proceeds from this offering for working capital and general corporate purposes, which may include investing in our sales and marketing and product enhancement efforts. We will not receive any proceeds from the shares sold by selling stockholders, if any. See "Use of Proceeds." |

|

Directed share program |

At our request, the underwriters have reserved up to 5.0% of the shares of common stock offered by this prospectus for sale, at the initial public offering price, to our directors, officers, employees and business associates, including certain of our customers, suppliers and other persons with which we have an existing business relationship. If these persons purchase shares, this will reduce the number of shares available for sale to the public. |

|

Risk factors |

See "Risk Factors" and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in shares of our common stock. |

|

Proposed NASDAQ Global Market symbol |

"AMQ" |

8

The number of shares of our common stock that will be outstanding after this offering is based on 12,889,968 shares of our common stock outstanding as of September 30, 2015. This number excludes:

- •

- 4,005,000 shares of common stock issuable upon exercise of options outstanding at a weighted-average exercise price of $2.21 per share

under our Equity and Incentive Plan as of September 30, 2015, which plan will terminate as to new awards following this offering;

- •

- an additional 403,628 shares of our common stock reserved for future issuance under our Equity and Incentive Plan as of

September 30, 2015, which plan will terminate as to new awards following this offering;

- •

- an additional 1,462,020 shares of our common stock reserved for future issuance under our 2011 Director Stock Purchase Plan and 2011

Employee Stock Purchase Plan as of September 30, 2015, which plans will terminate as to new awards following this offering;

- •

- an additional 2,933,332 shares of our common stock to be reserved for future issuance under our 2015 Equity Incentive Plan following

this offering; and

- •

- an additional 266,668 shares of our common stock to be reserved for future issuance under our 2015 Employee Stock Purchase Plan following this offering.

Except as otherwise indicated herein, all information in this prospectus, including the number of shares that will be outstanding after this offering, assumes or gives effect to:

- •

- a 4-for-1 forward stock split effective January 12, 2016; and

- •

- no exercise of options outstanding as of September 30, 2015.

9

SUMMARY CONSOLIDATED FINANCIAL DATA

In the following tables, we provide our summary consolidated financial data. We have derived the summary consolidated statements of income for the years ended December 31, 2012, 2013 and 2014 from our audited consolidated financial statements appearing elsewhere in this prospectus. We have derived the summary consolidated statement of income for the nine months ended September 30, 2014 and 2015 and balance sheet data as of September 30, 2015 from our unaudited consolidated interim financial statements appearing elsewhere in this prospectus. The unaudited consolidated financial data for the nine months ended September 30, 2014 and 2015 and as of September 30, 2015 includes all adjustments, consisting only of normal recurring accruals that are necessary in the opinion of our management for a fair presentation of our financial position and results of operations for these periods. Our historical results are not necessarily indicative of the results to be expected in the future.

When you read this summary consolidated financial data, it is important that you read it together with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and in conjunction with the consolidated financial statements, related notes, and other financial information included elsewhere in this prospectus.

Consolidated statements of income

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2012 | 2013 | 2014 | 2014 | 2015 | |||||||||||

| |

(In thousands, except share and per share amounts) |

|||||||||||||||

Revenue: |

||||||||||||||||

Financial process automation solutions |

$ | 8,440 | $ | 18,914 | $ | 24,073 | $ | 17,876 | $ | 21,073 | ||||||

Procurement solutions |

10,021 | 10,391 | 12,071 | 9,254 | 8,852 | |||||||||||

Asset management solutions |

39,093 | 38,079 | 48,652 | 36,729 | 35,230 | |||||||||||

| | | | | | | | | | | | | | | | | |

Total revenue |

57,554 | 67,384 | 84,796 | 63,859 | 65,155 | |||||||||||

Direct costs of revenue (excluding depreciation and amortization shown separately below): |

||||||||||||||||

Financial process automation solutions |

3,918 | 7,518 | 8,291 | 6,247 | 7,105 | |||||||||||

Procurement solutions |

928 | 1,124 | 1,200 | 788 | 874 | |||||||||||

Asset management solutions |

22,384 | 18,199 | 26,783 | 21,599 | 19,239 | |||||||||||

| | | | | | | | | | | | | | | | | |

Total direct costs of revenue |

27,230 | 26,841 | 36,274 | 28,634 | 27,218 | |||||||||||

Operating expenses: |

||||||||||||||||

Sales and marketing |

11,497 | 12,491 | 15,100 | 11,149 | 12,106 | |||||||||||

General and administrative |

6,345 | 6,784 | 7,902 | 6,063 | 5,638 | |||||||||||

Depreciation and amortization |

10,341 | 10,191 | 10,622 | 7,750 | 9,434 | |||||||||||

Other income |

— | — | — | — | (463 | ) | ||||||||||

| | | | | | | | | | | | | | | | | |

Total operating expenses |

28,183 | 29,466 | 33,624 | 24,962 | 26,715 | |||||||||||

| | | | | | | | | | | | | | | | | |

Operating income |

2,141 | 11,077 | 14,898 | 10,263 | 11,222 | |||||||||||

Interest expense |

(1,280 | ) | (3,239 | ) | (3,296 | ) | (2,499 | ) | (2,435 | ) | ||||||

Interest income |

68 | 80 | 110 | 86 | 106 | |||||||||||

Foreign exchange gain (loss), net |

43 | (382 | ) | (639 | ) | (384 | ) | (1,035 | ) | |||||||

| | | | | | | | | | | | | | | | | |

Income before income taxes |

972 | 7,536 | 11,073 | 7,466 | 7,858 | |||||||||||

Provision for income taxes |

344 | 2,893 | 4,245 | 2,853 | 3,622 | |||||||||||

| | | | | | | | | | | | | | | | | |

Net income |

$ | 628 | $ | 4,643 | $ | 6,828 | $ | 4,613 | $ | 4,236 | ||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

Net income per common share: |

||||||||||||||||

Basic |

$ | 0.05 | $ | 0.37 | $ | 0.54 | $ | 0.37 | $ | 0.34 | ||||||

Diluted |

$ | 0.05 | $ | 0.36 | $ | 0.52 | $ | 0.35 | $ | 0.32 | ||||||

Pro forma diluted |

$ | 0.49 | $ | 0.29 | ||||||||||||

Weighted average common shares outstanding: |

||||||||||||||||

Basic |

12,511,328 | 12,406,060 | 12,578,160 | 12,568,956 | 12,635,924 | |||||||||||

Diluted |

13,016,692 | 12,954,940 | 13,132,868 | 13,119,856 | 13,203,104 | |||||||||||

Pro forma diluted |

13,910,464 | 14,517,663 | ||||||||||||||

10

Consolidated balance sheet data

The following table presents summary consolidated balance sheet data as of September 30, 2015:

- •

- on an actual basis without any adjustments to reflect subsequent or anticipated events;

- •

- on a pro forma basis reflecting (i) the vesting of shares of restricted common stock upon the consummation of this offering,

(ii) the recognition of stock-based compensation expense in connection with the vesting of options to purchase up to 3,600,000 shares of common stock for which performance conditions will be

satisfied upon the effectiveness of this offering (see note 13 to our consolidated financial statements contained elsewhere in this prospectus) and (iii) the reclassification of our redeemable

common stock to stockholders' equity in connection with the termination of our shareholders' agreement effective upon the completion of this offering; and

- •

- on a pro forma as adjusted basis further reflecting the receipt by us of the net proceeds from the sale of 6,153,846 shares of common stock in this offering at an assumed initial public offering price of $12.00 per share, the midpoint of the price range set forth on the cover of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us, and the application of proceeds from the offering as described in "Use of Proceeds" as if each had occurred on September 30, 2015.

The unaudited pro forma and pro forma as adjusted consolidated financial data is presented for informational purposes only and does not purport to represent what our consolidated results of operations or financial position actually would have been had the transactions reflected occurred on the date indicated or to project our financial condition as of any future date or results of operations for any future period.

| |

As of September 30, 2015 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Actual | Pro Forma | Pro Forma As Adjusted |

|||||||

| |

(In thousands) |

|||||||||

Cash and cash equivalents |

$ | 32,767 | $ | 32,767 | $ | 99,111 | ||||

Total current assets |

192,753 | 194,619 | 260,963 | |||||||

Total assets |

255,432 | 257,297 | 319,873 | |||||||

Total current liabilities |

126,913 | 126,913 | 125,912 | |||||||

Total non-current liabilities |

93,499 | 93,499 | 93,499 | |||||||

Total redeemable common stock |

8,344 | — | — | |||||||

Stockholders' equity |

26,676 | 36,885 | 100,462 | |||||||

Other key financial metrics

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2012 | 2013 | 2014 | 2014 | 2015 | |||||||||||

| |

(In thousands) |

|||||||||||||||

Adjusted revenue |

$ | 42,330 | $ | 53,281 | $ | 62,359 | $ | 45,459 | $ | 49,548 | ||||||

Adjusted EBITDA |

12,612 | 21,579 | 25,880 | $ | 18,279 | $ | 20,968 | |||||||||

Adjusted revenue and adjusted EBITDA are each financial measures not calculated in accordance with accounting principles generally accepted in the United States, or GAAP. A reconciliation of these non-GAAP measures to the most directly comparable GAAP-based measures along with a summary of the definition and material limitations of each measure are included in the section titled "Selected Consolidated Financial Data—Other key financial metrics."

11

This offering involves a high degree of risk. In addition to the other information contained in this prospectus, prospective investors should carefully consider the following risks before investing in our common stock. If any of the following risks actually occur, our business, operating results and financial condition could be materially adversely affected. As a result, the trading price of our common stock could decline, and you may lose all or part of your investment in our common stock. The risks discussed below also include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements. See "Cautionary Note Regarding Forward-looking Statements" in this prospectus.

Risks Related to Our Business

If we fail to adequately assess and monitor the credit risks of our customers, our business and operating results could be harmed.

In connection with our financial process automation and procurement solutions, we often take on credit and collections risk associated with the transaction. As such, if our customers do not tender payment for their orders, we are still obligated to pay the supplier. As of September 30, 2015, the largest outstanding account receivable from a customer was $19.2 million, which represents 12.9% of our total accounts receivable. Conversely, if a supplier fails to deliver on a purchase order, we are often obligated to refund the customer for the entire amount of the transaction. While we use analytics to manage our credit risk, we cannot eliminate the credit risk from our customers, many of which are small to medium-sized businesses. The methods that we employ to screen potential customers and establish appropriate credit limits cannot eliminate all potential credit risks and may not always prevent us from approving customer applications that are fraudulently completed. In addition, changes in our industry may result in periodic changes in credit policies, such as expected increases in customer credit limits, which may further increase our exposure to additional credit losses. We may also fail to detect changes to the credit risk of customers, including our financial process automation solutions customers, over time. If we fail to adequately manage our credit risks, our business and operating results may be materially adversely affected.

A limited number of relationships are responsible for a significant portion of our revenue and cash flow. A decrease in sales to these customers could materially harm our business and operating results.

To date, a substantial portion of our business has been dependent on a limited group of relationships. For example, our largest relationship, Daimler Trucks North America LLC, or Daimler, uses our CorConnect product to manage billing and support services for its over 700 parts dealers. Transactions between Daimler's parts dealer network and their customers were 47.7% and 49.6% of our financial process automation solutions revenue and 13.5% and 16.1% of our total revenue during the year ended December 31, 2014 and the nine months ended September 30, 2015, respectively. As a result, there may be significant variability in our results if our relationship with this group of suppliers were to change or be lost completely. Additionally, most of our customers may generally terminate their respective agreements with us in each case for cause upon written notice of certain uncured material breaches of contract by us, upon the bankruptcy or insolvency of the other party or under certain other circumstances.

We expect that a limited number of customers and relationships will continue to account for a substantial portion of our revenue in future periods. A decrease in sales to these customers or a loss of one or more could harm our results of operations and financial condition.

12

Our recent growth rates may not be sustainable or indicative of our future growth.

We have substantially expanded our overall business, customer base, employee headcount and operations in recent periods. We increased our total number of full-time employees from 130 employees as of December 31, 2011 to 227 employees as of September 30, 2015. Our expansion has placed, and our expected future growth will continue to place, a significant strain on our managerial, customer operations, research and development, sales and marketing, administrative, financial and other resources. We anticipate further growth in headcount will be required to address increases in our solution offerings and continued expansion. Our success will depend in part upon the ability of our management team to manage this growth effectively. To do so, we must continue to recruit, hire, train, manage and integrate a significant number of qualified managers and employees in specialized roles within our company, including in technology, sales and marketing. If our new employees perform poorly, or if we are unsuccessful in recruiting, hiring, training, managing and integrating these new employees, or retaining these or our existing employees, our business and results of operations may suffer.

In addition, to manage the expected growth of our headcount and operations, we will need to continue to improve our operational, financial, management and information technology infrastructure. Our anticipated additional headcount and capital investments will increase our costs, which will make it more difficult for us to address any future revenue shortfalls by reducing expenses in the short term. If we are unable to manage our growth successfully, our business and results of operations will be harmed. Moreover, our historical growth rates may not be indicative of future growth.

If we fail to execute our growth strategy, which largely depends on our ability to grow our financial process automation solutions, our business could suffer.

One of the key means of achieving our growth strategy will be through growth in our financial process automation solutions. During the year ended December 31, 2014, revenue generated from our financial process automation solutions was 28.4% of our revenue, up from 14.7% and 28.1% during the years ended December 31, 2012 and 2013, respectively. This increase in relative revenue was the result of 68.9% CAGR in revenue growth for these solutions alone over those years. Additionally, during the nine months ended September 30, 2015, our financial process automation solutions revenue increased $3.2 million to $21.1 million or 17.9% as compared to the nine months ended September 30, 2014. Although we expect this area to account for a significant amount of our revenue growth for the foreseeable future, we may be unable to grow this aspect of our business as rapidly as we expect or maintain the current rate of growth in this area that we have recently experienced. For example, the recent growth in our financial process automation solutions revenue was largely driven by transactions between Daimler's parts dealers and their customers. Revenues attributable to Daimler's parts dealers represented 47.7% and 49.6% of our financial process automation solutions revenue during the year ended December 31, 2014 and the nine months ended September 30, 2015, respectively, but was not a material relationship prior to 2013. We believe our growth strategy for our financial process automation solutions will depend on our ability to acquire additional customer networks.

We buy and sell commercial trucks and trailers, and there is no guarantee that our activities will be profitable.

While we typically act as a broker for sellers of capital equipment, in certain circumstances, we may purchase the asset outright from a customer, make necessary repairs or improvements and subsequently sell the asset. As such, we are exposed to price movements in the market for trucks and trailers. Moreover, we may have to spend money to repair or improve the asset, and there is no guarantee that we can recover such investments upon resale or earn a profit on our activities. While we have not generally carried more than $2.5 million of assets held for sale at a given time during prior years (with an average monthly carrying value of $0.8 million during the last three fiscal years) nor held assets in inventory for longer than 120 days, if there is a downturn in the market for capital equipment,

13

particularly commercial trucks and trailers, or if we make an unusually large purchase of assets which we are unable to sell quickly, we may be forced to hold our assets longer than anticipated or sell such assets at a loss.

Our sales cycles, particularly for our financial process automation solutions, can be lengthy and unpredictable and require significant employee time and financial resources.

Sales cycles for our solutions, particularly our financial process automation solutions, tend to be long and unpredictable. Even after we have convinced prospective customers of the need for, and value of, our products and solutions, our customers frequently have extensive budgeting, procurement and approval processes that can slow down the sales process by months or even years. Customers may choose, and many historically have chosen, to follow industry trends rather than be early adopters of new products or solutions, which can extend the lead time for or prevent acceptance of more recently introduced products or solutions such as ours. The implementation and deployment of our solutions can also be unpredictable due to contract negotiations and challenges with implementation. Furthermore, the implementation and deployment of new products and solutions may require troubleshooting, which requires additional time and resources from us and our customers. These delays may lengthen our sales cycles.

Our average sales cycle for financial process automation contracts sold in 2014 was approximately seven months. Our average sales cycle for our asset management solutions often varies because it frequently depends upon our customers' asset needs. By contrast, the average sales cycle for our procurement solutions was approximately two to three months. The extended sales process of our financial process automation solutions, in particular, requires our senior management and our sales and marketing and customer services personnel to dedicate significant time to sales, and to use significant financial resources without any assurance of success or recovery of our related expenses.

Our lengthy and often unpredictable sales cycle also makes it difficult to forecast the timing and volume of new financial process automation customer implementations and future financial process automation agreements, which, in turn, may make forecasting our future financial process automation results of operations challenging. In the event that we publicly disclose any forecasts of our future results of operations or other forward-looking metrics, and those forecasts ultimately prove to be inaccurate, the value of our common stock could significantly decline.

We are exposed to the credit risk of our asset financing customers, which could adversely affect our business and operating results.

We provide lease financing for independent contractors that fulfill carriage contracts on behalf of a sponsor organization. While the sponsor organizations remit weekly lease payments directly to us, we are subject to payment risk in our leasing activities resulting from defaults in payment or performance by the sponsor organization and the independent contractors and credit risk from the independent contractors. Moreover, we provide short-term lending arrangements that allow a customer to purchase a capital asset while awaiting final funding from a third-party lender. We are subject to payment and credit risk in our lending activities resulting from defaults in payment by the borrower, as well as the risk that the third-party lender fails to deliver final funding.

A decline in general economic conditions, and in particular, a decline in demand for products and services offered through our procurement solutions, would adversely affect our business and operating results.

Our operating results are materially affected by conditions in the economy generally and in the industries that we serve. We generate revenue based primarily on the volume of transactions we process. Our transaction volume is correlated with the amount of business activity in the United States. Downturns in the economy are generally characterized by reduced commercial activity and,

14

consequently, reduced purchasing of products and services by businesses. Further, economic conditions also may impact the ability of our customers or partners to pay for services they have purchased. As a result, if economic conditions deteriorate, our reserve for credit losses and write-offs of accounts receivable could increase.

We have identified a material weakness in our internal control over financial reporting. Although we expect to make every effort to address this material weakness, we may find that we are unable to improve our internal control over financial reporting, which could make it difficult to maintain an effective system of internal control over financial reporting, reduce the reliability of our financial reporting, harm investor confidence in our company and affect the value of our common stock.

We will be required, pursuant to Section 404 of the Sarbanes-Oxley Act to furnish a report by management on, among other things, the effectiveness of our internal control over financial reporting in the second annual report we file with the SEC. This assessment will need to include disclosure of any material weaknesses identified by our management in our internal control over financial reporting, as well as a statement that our independent registered public accounting firm has issued an opinion on our internal control over financial reporting. However, our auditors will not be required to formally attest to the effectiveness of our internal control over financial reporting pursuant to Section 404 until we are no longer an "emerging growth company" as defined in the JOBS Act if we take advantage of the exemptions available to us through the JOBS Act. At such time as our auditors are required to formally attest to our internal control over financial reporting, they may issue a report that is adverse in the event they are not satisfied with the level at which our controls are documented, designed or operating.

We are in the very early stages of the costly and challenging process of compiling the system and processing documentation necessary to perform the evaluation needed to comply with Section 404.

In connection with the preparation of our consolidated financial statements for the years ended December 31, 2013 and 2014, we and our independent registered public accounting firm identified a material weakness in the design and operation of our internal control over financial reporting. The material weakness relates to the classification of leased assets on our consolidated balance sheet, consolidated income statement and consolidated statement of cash flows. As a result, we restated our 2012 and 2013 financial statements to correct the misclassification in conjunction with the 2013 and 2014 audits. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of a company's annual or interim financial statements will not be prevented or detected on a timely basis.

We are currently in the process of remediating the material weakness and are taking numerous steps that we believe will address the underlying causes of the material weakness, primarily through the hiring of additional financial reporting personnel with technical accounting and financial reporting experience and the enhancing of our internal review procedures during the financial statement close process. If we fail to effectively remediate deficiencies in our control environment or are unable to implement and maintain effective internal control over financial reporting and disclosure controls to meet the demands that will be placed upon us as a public company, including the requirements of Section 404 of the Sarbanes-Oxley Act, we may be unable to accurately report our financial results, or report them within the timeframes required by the SEC.

Even if we are able to report our financial statements accurately and in a timely manner, if we do not make all necessary improvements to address the material weakness, continued disclosure of a material weakness will be required in future filings with the SEC, which could cause our reputation to be harmed and our stock price to decline.

We may not be able to remediate this or any future material weaknesses, or to complete our evaluation, testing and any required remediation in a timely fashion. During the evaluation and testing

15

process, if we identify one or more material weaknesses in our internal control over financial reporting, we will be unable to assert that our internal controls are effective. If we are unable to assert that our internal control over financial reporting is effective, or if our auditors are unable to express an opinion on the effectiveness of our internal controls when they are required to issue such opinion, investors could lose confidence in the accuracy and completeness of our financial reports, which could harm our stock price.

We operate in a competitive business environment, and if we are unable to compete effectively, our business and operating results would be adversely affected.

The market for our products and services is highly competitive, and competition could intensify in the future. Our competitors vary in size and in the scope and breadth of the products and services they offer. We may experience competitive disadvantages from time to time as potential customers prioritize or value competitive factors differently. As a result, a specific offering of our products and service features, networks and pricing may serve as a competitive advantage with respect to one customer and a disadvantage for another based on the customer's individual preferences.

Some of our competitors have longer operating histories, greater brand name recognition, larger customer bases, more extensive customer relationships and greater financial and technical resources. In addition, our larger competitors also have greater resources to promote and sell their products and services and to pursue acquisitions. As a result, they may be able to adapt more quickly to new or emerging technologies and changing opportunities, standards or customer requirements.

Future mergers or consolidations among competitors, or acquisitions of our competitors by large companies may present competitive challenges to our business. The resulting combined entities could be at a competitive advantage if their products and service features are effectively integrated and bundled into more diverse and attractive sales packages. Overall, increased competition in our markets could result in intensified pricing pressure, reduced profit margins, increased sales and marketing expenses and a failure to increase, or a loss of, market share. We may not be able to maintain or improve our competitive position against our current or future competitors, which could adversely affect our business and operating results.

If our efforts to attract new customers are not successful, our revenue growth will be adversely affected, and the new customers we do attract may not generate revenue comparable to our current or historical customers.

There is no guarantee that we can sustain the customer acquisition rates that we have experienced in recent periods. Our ability to attract new customers will depend in large part on the success of our sales and marketing efforts, which may not be successful. Our prospective customers may not be familiar with our solutions, or may have traditionally used other products and services. Our prospective customers may develop their own solutions or purchase competitive product offerings. Additionally, we seek to attract larger customer networks that may have entrenched solutions already. All of these efforts require substantial time and expense. It may be difficult to identify, engage and market to customers, and many of our customers typically require input from one or more internal levels of approval. This requires us to spend substantial time and effort assisting potential customers in evaluating our solution including providing demonstrations. If our prospective customers do not perceive our solution to be of sufficiently high value and quality, we may not be able to attract new customers and our business, operating results and financial condition would be adversely affected. Additionally, even if we are successful in attracting new customers, such new customers may not generate comparable revenue relative to our current or historical customers, which could materially adversely affect our operating results and our growth.

16

We may undertake future acquisitions, which may divert our management's attention and result in unexpected operating difficulties, increased costs and dilution to our stockholders. We also may never realize the anticipated benefits of the acquisitions.

We have acquired several businesses in past years, and we may continue to acquire businesses, technologies, services and products in the future. The acquisition and integration of each business involves a number of risks and may result in unforeseen operating difficulties and expenditures in assimilating or integrating the businesses, technologies, products, personnel or operations of the acquired business. Furthermore, among other risks, future acquisitions may:

- •

- increase the difficulty of satisfying our obligations under our debt facilities;

- •

- involve our entry into geographic or business markets in which we have little or no prior experience;

- •

- fail to result in the addition of new customers for us;

- •

- result in a delay or reduction of sales for both us and the business we acquire; and

- •

- disrupt our ongoing business, divert our resources and require significant management attention that would otherwise be available for ongoing development of our current business.

To complete a future acquisition, we may determine that it is necessary to use a substantial amount of our cash or engage in equity or debt financing. We can make no assurances that the anticipated benefits of any acquisition, such as operating improvements or anticipated cost savings, would be realized or that we would not be exposed to unexpected liabilities in connection with any acquisition.

Further, an acquisition may negatively affect our operating results because it may require us to incur charges and substantial debt or other liabilities, may cause adverse tax consequences, substantial depreciation and amortization or deferred compensation charges, may require the amortization, write-down or impairment of amounts related to deferred compensation, goodwill and other intangible assets, or may not generate sufficient financial return to offset acquisition costs.

Our procurement solutions strategy is in part dependent upon our ability to deliver products and services at competitive or discounted prices. This strategy may not be successful, which could have a material adverse effect on our business and results of operations.

In addition to receiving fees and rebates from our suppliers, we receive fees from purchasers that are based on a product margin that varies by procurement program. In order to maintain and develop new relationships with purchasers in our procurement solutions, we look for ways to reduce the prices that they pay for products and services. However, success in serving such purchasers by reducing the prices they pay suppliers for products and services reduces the fees that we receive for processing such transactions. Moreover, since our fees are based on a product margin, we are exposed to commodity price changes. For example, if the price of tires declines, then the amount that we earn on a fixed number of tire purchases would correspondingly decline.

In order to maintain or increase our revenues and margins while implementing these strategies, we would have to increase sales volumes of existing products and services or introduce and sell new products and services in amounts sufficient to compensate for the reduced revenue effect of price reductions. If our competitors in these lines of business similarly reduce or obtain lower prices for their procurement purchasers, we may face further challenges. A failure to successfully implement our price reduction strategy could have a material adverse effect on our business, financial condition and results of operations.

17

Our procurement solutions, which rely on suppliers to provide discounts on aggregated purchases, compete with those suppliers' efforts to sell directly to customers. As a result, suppliers may limit or terminate their participation in our procurement solutions if the prices that they receive for products purchased through our solutions become too low.

Suppliers participate in our procurement solutions by offering discounts on aggregated purchases. However, suppliers also sell directly to customers outside of our procurement solutions program, typically at higher prices. Thus, our suppliers have an incentive to limit sales through our procurement solutions program if they can make the same sales outside of our program at higher prices.

In some cases, suppliers must approve each customer before it is allowed to participate in our procurement solutions program. Similarly, some suppliers impose size limitations on which customers may participate in our procurement solutions program. If suppliers do not authorize new customers to participate in our procurement program, or increase the requirements under which new customers may join, our business and operating results may be harmed.

We rely on fees and rebates that we receive from our procurement solutions suppliers. The failure to maintain contracts with these procurement solutions suppliers could adversely affect our business, financial condition and results of operations.

We rely heavily on our relationships with our procurement solutions suppliers, which provide products and services to our procurement solutions purchasers at reduced prices. These suppliers pay us rebates calculated either as a percentage of the transaction value under specific preferred procurement programs or as a pre-determined fee per transaction or item. Our contracts with these suppliers may be terminated upon zero to sixty days' notice. Supplier commitment to our procurement solutions has been, and will continue to be, a crucial element of our business model. There can be no assurances that our relationships with our suppliers will continue on existing terms or at all. A termination of any relationship or agreement with a supplier would result in the loss of fees and rebates pursuant to our arrangement with that supplier, which could adversely affect our business, financial condition and results of operations. Moreover, since some suppliers pay us rebates calculated as a percentage of the transaction value, we are exposed to commodity price changes. For example, if the price of tires declines, then the amount that we earn on a fixed number of tire sales would correspondingly decline.

If we cannot demonstrate to our procurement solutions suppliers the ability to increase their market share or access to purchasers through our procurement solutions or other products and services, we may lose negotiating leverage with our contracted suppliers which may result in our inability to maintain our agreements with purchasers or win new business. In addition, if we lose a relationship with a supplier, we may not be able to negotiate similar arrangements for our procurement solutions purchasers with other suppliers on the same terms and conditions or at all, which could damage our reputation with our procurement purchasers and, in turn, have a material adverse effect on our business, financial condition and results of operations.

If we fail to respond to evolving technological changes, our products and solutions could become obsolete or less competitive.

The markets in which we compete are highly competitive and are often characterized by new and rapidly evolving technologies, techniques, standards, regulations, customer requirements and frequent product introductions. We must anticipate and respond to the technological advances offered by our competitors and the requirements of our customers and partners, in order to maintain and improve upon our competitive position. Accordingly, our results of operations depend upon, among other things, our ability to develop and introduce new products and solutions, as well as our ability to improve existing products. The process of developing new technologies and products is complex, and we must

18

continue to invest significant resources in research and development in order to develop new products and to enhance our existing products and services.

Our ability to develop new features and enhance our products will depend on our ability to anticipate industry evolution, practices and standards and to continue to enhance existing solutions. In addition, the success of any enhancement or new feature depends on several factors, including the timely completion, introduction and market acceptance of the enhancement or feature. Any new solutions we develop or acquire might not be introduced in a timely or cost-effective manner and might not achieve the broad market acceptance necessary to generate significant revenue. If any of our competitors implements new technologies before we are able to implement them or better anticipates the innovation and integration opportunities in related industries, those competitors may be able to provide more effective or cheaper solutions than ours. If we are unable to develop enhancements to, and new features for, our existing products or if we are unable to develop new products that keep pace with technological developments or industry standards, our business could be harmed.

If the market for our cloud-based delivery model develops more slowly than we expect, our growth may slow or stall, and our business, operating results, and financial condition could be adversely affected.

Use of cloud-based applications for financial process automation and procurement is at an early stage within our industry. We are currently focusing on transaction processing, data analytics and other technology opportunities and our success will depend to a substantial extent on the willingness of potential new customers, large and small, to increase their use of our cloud-based products. Many companies have invested substantial personnel and financial resources to integrate established enterprise software into their businesses and therefore may be reluctant or unwilling to switch to our services. Furthermore, some companies may be reluctant or unwilling to use our services, because they have concerns regarding the risks associated with the security and reliability of, among other things, the technology delivery model associated with these services. If companies do not perceive the benefits of our services, then the market for these services may not expand as much or develop as quickly as we expect, either of which would significantly adversely affect our business, financial condition and results of operations.

Failure to adequately expand our direct sales force will impede our growth.

We will need to continue to expand and optimize our sales infrastructure in order to grow our customer base and our business. We plan to continue to expand our direct sales force. Competition for such qualified sales personnel is intense. We cannot be certain of our ability to identify, hire and retain adequately qualified sales personnel. Identifying and recruiting qualified personnel and training them requires significant time, expense and attention. It can take several months before our sales representatives are fully trained and productive. Our business may be adversely affected if our efforts to expand and train our direct sales force do not generate a corresponding increase in revenue. In particular, if we are unable to hire, develop and retain talented sales personnel, or if new direct sales personnel are unable to achieve desired productivity levels in a reasonable period of time, we may not be able to realize the expected benefits to revenue from this investment.

Our future success also depends in part on our ability to sell additional features or enhanced elements of our applications to our current customers. This may require increasingly costly sales efforts that are targeted at senior management. If these efforts are not successful, our business may suffer.

Our debt obligations, or our incurrence of additional debt obligations, could limit our flexibility in managing our business and could materially and adversely affect our financial performance.

As of September 30, 2015, we had approximately $87.3 million of long-term indebtedness (including current portion) outstanding. In addition, we are permitted under our credit agreement to

19