Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - GMS Inc. | a2226736zex-23_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS 2

As filed with the Securities and Exchange Commission on January 4, 2016

Registration No. 333-205902

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GMS INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

5030 (Primary Standard Industrial Classification Code Number) |

46-2931287 (I.R.S. Employer Identification No.) |

100 Crescent Centre Parkway, Suite 800

Tucker, Georgia 30084

(800) 392-4619

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

G. Michael Callahan, Jr.

President and Chief Executive Officer

GMS Inc.

100 Crescent Centre Parkway, Suite 800

Tucker, Georgia 30084

(800) 392-4619

(Name, address, including zip code, and telephone number including area code, of agent for service)

| Copies of all communications, including communications sent to agent for service, should be sent to: | ||

Andrew B. Barkan, Esq. Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, New York 10004 (212) 859-8000 |

Peter J. Loughran, Esq. Debevoise & Plimpton LLP 919 Third Avenue New York, New York 10022 (212) 909-6000 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý | Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) |

||

|---|---|---|---|---|

Common Stock, par value $0.01 per share |

$200,000,000 | $23,240 | ||

|

||||

- (1)

- Estimated

solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933.

- (2)

- Includes

the offering price of common stock that may be purchased by the underwriters upon the exercise of their option to purchase additional shares.

- (3)

- The Registrant previously paid $23,240 in connection with a prior filing of this Registration Statement on July 28, 2015.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION. DATED JANUARY 4, 2016

Shares

GMS Inc.

Common Stock

This is an initial public offering of shares of common stock of GMS Inc. We are selling all of the shares to be sold in the offering.

Prior to this offering, there has been no public market for the common stock. The initial public offering price is expected to be between $ and $ per share. We have applied to list our common stock on the New York Stock Exchange under the symbol "GMS".

The underwriters have an option for a period of 30 days to purchase up to a maximum of additional shares of our common stock from us, to cover any over-allotments.

After the completion of this offering, we expect to be a "controlled company" within the meaning of the corporate governance standards of the New York Stock Exchange.

Investing in our common stock involves risk. See "Risk Factors" beginning on page 19 to read about factors you should consider before buying shares of our common stock.

| |

Price to Public |

Underwriting Discounts and Commissions(1) |

Proceeds to GMS Inc. |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | |||||||

| Total | $ | $ | $ | |||||||

- (1)

- We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See "Underwriting."

Delivery of the shares of common stock will be made on or about , 2016.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Barclays | Credit Suisse | |||

RBC Capital Markets |

Baird |

Wells Fargo Securities |

| SunTrust Robinson Humphrey | Raymond James | Stephens Inc. |

The date of this prospectus is , 2016.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us that we have referred to you. Neither we nor the underwriters have authorized anyone to provide you with additional information or information different from that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us that we have referred to you. If anyone provides you with additional, different or inconsistent information, you should not rely on it. Offers to sell, and solicitations of offers to buy, shares of our common stock are being made only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock. Our business and financial condition may have changed since such date.

No action is being taken in any jurisdiction outside the United States to permit a public offering of common stock or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restriction as to this offering and the distribution of this prospectus applicable to those jurisdictions.

This prospectus includes estimates regarding market and industry data that we prepared based on our management's knowledge and experience in the markets in which we operate, together with information obtained from various sources, including publicly available information, industry reports and publications, surveys, our customers, suppliers, trade and business organizations and other contacts in the markets in which we operate.

In presenting this information, we have made certain assumptions that we believe to be reasonable based on such data and other similar sources and on our knowledge of, and our experience to date in, the markets for the products we distribute. Market share data is subject to change and may be limited by the availability of raw data, the voluntary nature of the data gathering process and other limitations

i

inherent in any statistical survey of market shares. In addition, customer preferences are subject to change. Accordingly, you are cautioned not to place undue reliance on such market share data. References herein to our being a leader in a market or product category refer to our belief that we have a leading market share position in each specified market based on volume, for our wallboard market share position, or sales dollars, for our ceilings market share position, unless the context otherwise requires. In addition, unless otherwise stated or the context otherwise requires, the discussions herein regarding (1) the wallboard market are based on the total volume of wallboard produced in U.S. manufacturing facilities, some of which is sold into Canada, and (2) the suspended ceilings systems, or ceilings, market are based on the total sales, in dollars, of ceilings distributed or otherwise sold in North America.

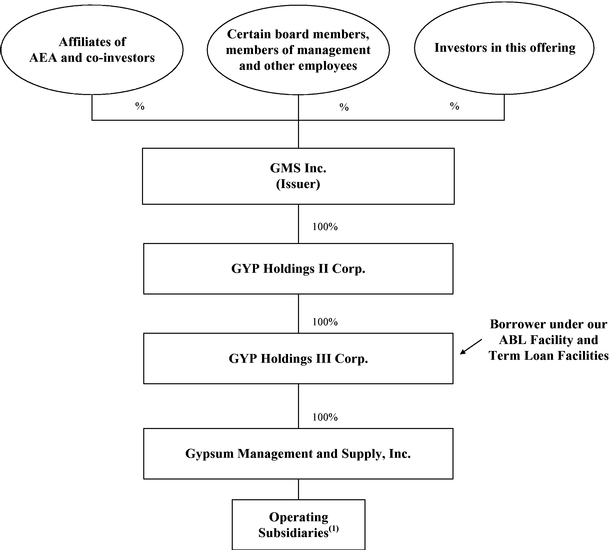

On April 1, 2014, GMS Inc., or the Successor, acquired, through its wholly-owned entities, GYP Holdings II Corp. and GYP Holdings III Corp., all of the capital stock of Gypsum Management and Supply, Inc., or the Predecessor. Successor is majority owned by certain affiliates of AEA Investors LP, which we refer to as "AEA" or our "Sponsor," and certain of our other stockholders. We refer to this acquisition as the "Acquisition."

As a result of the Acquisition and resulting change in control and changes due to the impact of purchase accounting, we are required to present separately the operating results for the Predecessor periods ending on or prior to March 31, 2014 and the Successor periods beginning on or after April 1, 2014. Accordingly, unless otherwise indicated or the context otherwise requires, all references to "the Company," "GMS," "we," "us," "our" and other similar terms mean (1) the Predecessor for periods ending on or prior to March 31, 2014 and (2) the Successor for periods beginning on or after April 1, 2014, in each case together with its consolidated subsidiaries.

Our fiscal year ends on April 30 of each year. References in this prospectus to a fiscal year mean the year in which that fiscal year ends. References in this prospectus to "fiscal 2011" or "FY 2011" relate to the year ended April 30, 2011, references in this prospectus to "fiscal 2012" or "FY 2012" relate to the year ended April 30, 2012, references in this prospectus to "fiscal 2013" or "FY 2013" relate to the year ended April 30, 2013, references in this prospectus to "fiscal 2015" or "FY 2015" relate to the year ended April 30, 2015 and references in this prospectus to "fiscal 2016" relate to the year ending April 30, 2016. References in this prospectus to "full year 2014" or "FY 2014" represent the sum of the results of the eleven month period from May 1, 2013 to March 31, 2014 and the one month period from April 1, 2014 to April 30, 2014.

The audited financial statements included in this prospectus include a black line division to indicate that the Predecessor and Successor reporting entities have applied different bases of accounting and are not comparable. Please note that our discussion of certain financial information for the year ended April 30, 2014, specifically net sales and Adjusted EBITDA, includes data from the Predecessor and Successor periods on a combined basis for the full year 2014. The change in basis resulting from the Acquisition did not impact such financial information and, although this presentation of financial information on a combined basis does not comply with generally accepted accounting principles in the United States, or GAAP, we believe it provides a meaningful method of comparison to the other periods presented in this prospectus. The data is being presented for analytical purposes only. Combined operating results (1) have not been prepared on a pro forma basis as if the Acquisition occurred on the first day of the period, (2) may not reflect the actual results we would have achieved absent the Acquisition and (3) may not be predictive of future results of operations.

ii

Amounts presented in this prospectus in thousands or millions are approximations of the actual amounts in that they have been rounded.

This prospectus includes trademarks and service marks owned by us, including GMSTM, GMS Gypsum Management & Supply, Inc.® and GTS®. This prospectus also contains trademarks, trade names and service marks of other companies, which are the property of their respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, trade names and service marks. We do not intend our use or display of other parties' trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

iii

This summary highlights selected information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all the information that may be important to you. You should read the entire prospectus carefully, especially "Risk Factors" beginning on page 19 of this prospectus and our consolidated financial statements and related notes included elsewhere in this prospectus, before deciding to invest in our common stock.

We are the leading North American distributor of wallboard and suspended ceilings systems. Our product offering of wallboard, suspended ceilings systems, or ceilings, and complementary interior construction products is designed to provide a comprehensive solution for our core customer, the interior contractor who installs these products in commercial and residential buildings.

Since our founding in 1971, we have grown our business from a single location to over 155 branches across 37 states through a combination of both organic growth and acquisitions. Underpinning that growth is our entrepreneurial culture, which both enables us to drive organic growth by delivering outstanding customer service and makes us an attractive acquirer for smaller distributors whose owners are seeking liquidity. Over time, we have increased our market share in the distribution of wallboard and ceilings, which management currently estimates is 11% for wallboard, based on volume produced in the United States and Canada, and 14% for ceilings, based on sales dollars in North America.

We serve as a critical link between our suppliers and our highly fragmented customer base of over 20,000 contractors. Based on wallboard's unique product attributes and delivery requirements, distributing wallboard requires a higher degree of logistics and service expertise than most other building products. Wallboard has a high weight-to-value ratio, is easily damaged, cannot be left outside and often must be delivered to a job site before or after normal business hours. Due to the weight of the product, we are often required to deliver wallboard to the specific room where it will be installed. For example, we can place the precise amount and type of wallboard necessary for a second story room of a new building through the second story window using a specialized truck with an articulating boom loader. To do this effectively, we need to load the truck at the branch so that the precise amount and type of wallboard for each room of the building can be off-loaded by the articulating boom loader in the right sequence. Our sales, dispatch and delivery teams then coordinate an often complicated, customized delivery plan to ensure that our delivery schedule matches the customer's job site schedule, that deliveries are made with regard to the specific challenges of a customer's job site, that no damage occurs to the customer's property and, most importantly, that proper safety procedures are followed at all times. Often this requires us to send an employee to a job site before the delivery is made to document the specific requirements and safety considerations of a particular location. Given the logistical intensity of this process and the premium contractors place on distributors delivering the right product, at the right time, in the right place, we are able to differentiate ourselves based on service and can generate attractive gross profit margins. In addition to executing a logistics-intensive service, for all of our products we facilitate purchasing relationships between suppliers and our highly fragmented customer base by transferring technical product knowledge, educating contractors on proper installation techniques for new products, ensuring local product availability and extending trade credit.

We believe our strategic focus and operating model enable us to differentiate ourselves within our industry. Whereas several of our competitors are part of larger organizations that manufacture or distribute a wide variety of products, we focus on distributing wallboard, ceilings and complementary interior construction products. We believe this focus enables us to provide superior service and product expertise to our customers. In addition, our operating model combines a national platform with a local go-to-market strategy through over 155 branches across the country. We believe this combination enables us to generate economies of scale while maintaining the high service levels, entrepreneurial culture and customer intimacy of a local business. In order to tailor its products and services to meet

1

the needs of its local market, each of our branches operates with a significant amount of autonomy within the parameters of our overall business model. Branch managers are responsible for sales, pricing and staffing activities, and have full operational control of customer service and deliveries. They are compensated in part based on the profit they are able to achieve, which aligns their incentives with our financial goals. We believe our experienced, locally-focused teams, and our ability to develop, motivate and incentivize them, are key to our success. Through our Yard Support Center, which includes over 120 employees at our corporate office in Atlanta, we support our branches with various back office functions including accounting, information technology, or IT, legal, safety, human resources, marketing and risk management. We also use our Yard Support Center to generate purchasing efficiencies and share best practices across our branch network.

We have grown our Company and developed our distinctive culture under strong, consistent leadership. Our senior management team has been with us for an average of 22 years. We have been able to retain top talent and incentivize managers through our entrepreneurial culture and broad-based equity ownership. Prior to this offering, 71 of our employees own approximately 32% of our common stock, including vested options. Together with our strong base of experienced operators, our management team has grown our Company from a single site location to the market leader we are today.

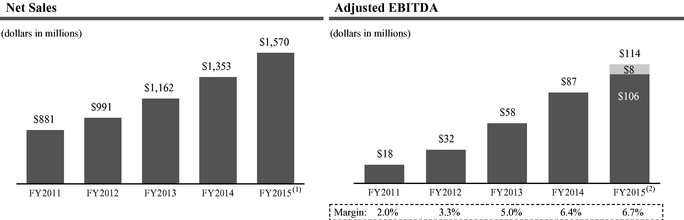

For fiscal 2015, we generated $1.6 billion in net sales, $113.9 million of Adjusted EBITDA and $13.8 million of net loss. For a discussion of our use of Adjusted EBITDA and a reconciliation to net income (loss), please refer to "—Summary Financial and Other Data." Net sales and Adjusted EBITDA grew 16.0% and 30.8%, respectively, in fiscal 2015 as compared to full year 2014. Over the past four years, net sales and Adjusted EBITDA have grown at a compound annual growth rate, or CAGR, of 15.5% and 59.2%, respectively.

- (1)

- Our net sales do not reflect net sales attributable to acquired entities for any period prior to the respective dates

of their acquisition. Entities acquired in FY 2015 generated approximately $82.0 million in net sales in FY 2015 prior to their respective acquisition dates.

- (2)

- Our Adjusted EBITDA for FY 2015 includes approximately $8.1 million from entities acquired in FY 2015 for the period prior to the date of acquisition of such entities, as permitted by the ABL Facility and the Term Loan Facilities. However, Adjusted EBITDA margin, which is calculated as a percentage of net sales, excludes this $8.1 million adjustment for FY 2015 to be consistent with our calculation of net sales for the same period.

2

The table below summarizes our major product categories:

(dollars in millions)

|

Wallboard | Ceilings | Steel Framing | Other Products | ||||

|---|---|---|---|---|---|---|---|---|

Fiscal 2015 Net Sales |

$718.1 | $278.7 | $243.2 | $330.1 | ||||

% of Fiscal 2015 Net Sales |

45.7% |

17.8% |

15.5% |

21.0% |

||||

Description(1) |

• #1 market position

• Used to finish the interior walls and ceilings in residential, commercial and institutional construction projects |

• #1 market position

• Suspended ceiling systems primarily comprised of mineral fiber ceiling tile and grid

• Architectural specialty ceilings systems |

• Steel framing products for interior walls

• Sold into commercial applications, typically as part of a package with wallboard, ceilings and other products |

• Primarily consists of complementary interior construction products, including joint compound, finishing materials, tools and fasteners, safety products and EIFS (exterior insulation and finishing system) |

||||

Products |

• Various types of wallboard including: 1/2 inch standard (residential), 5/8 inch fire-rated (commercial), foil-backed, lead-lined, moisture-resistant, mold-resistant and vinyl-covered

• Tile backer |

• Acoustical ceiling tiles (standard and architectural specialty)

• Clips

• Covered fiberglass

• Ceiling tile grid

• Hangers |

• Beads, clips, furring, hangers, joists, lath, mesh and trim

• Control joint

• Drywall steel

• Flat stock

• Plastering steel

• Structural

• Studs and track |

• Adhesives

• EIFS

• Fasteners

• Insulation

• Joint compound

• Plaster

• Safety equipment

• Tools

• Trims |

||||

Primary End Markets |

• Residential New Construction

• Residential Repair and Remodeling, or R&R

• Commercial New Construction

• Commercial R&R |

• Commercial New Construction

• Commercial R&R |

• Commercial New Construction

• Commercial R&R |

• Commercial New Construction

• Commercial R&R

• Residential New Construction

• Residential R&R |

||||

Key Manufacturers |

• American Gypsum Company, LLC, or American Gypsum

• CertainTeed Corporation, or CertainTeed

• Continental Building Products Inc., or Continental

• Georgia-Pacific Corporation, or Georgia-Pacific

• National Gypsum Company, or National Gypsum

• Pabco Building Products, LLC, or Pabco

• USG Corporation, or USG |

• Armstrong World Industries, Inc., or Armstrong

• CertainTeed

• USG |

• ClarkDietrich Building Systems LLC

• Marino\WARE Industries, Inc.

• Super Stud Building Products, Inc.

• Telling Industries LLC |

• Dryvit Systems, Inc.

• Grabber Construction Products, Inc.

• Johns Manville

• Knauf Gips KG

• PrimeSource Building Products, Inc.

• Stanley Black & Decker, Inc.

• Sto Corp. |

- (1)

- Market position based on management's estimates, and based on volume, for wallboard, and sales dollars, for ceilings.

3

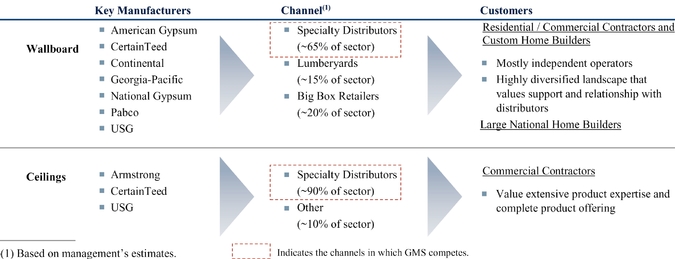

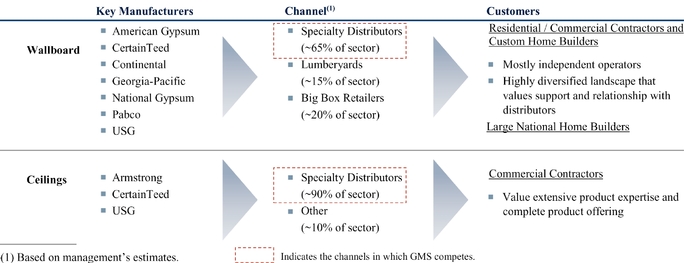

As the U.S. construction market evolved during the second half of the 20th century, contractors began to specialize in specific trades within the construction process, and specialty distributors emerged to supply them. One of these trades was wallboard and ceilings installation, and we, along with other specialty distributors, tailored our product offerings and service capabilities to meet the unique needs of that trade. Today, specialty distributors comprise the preferred distribution channel for wallboard and ceilings in both the commercial and residential construction markets.

We believe the success of the specialty distribution model in wallboard and ceilings is driven by the strong value proposition provided to our customers. Given the logistical complexity of the distribution services we provide, the expertise needed to execute effectively, and the special equipment required, we believe specialty distributors focused on wallboard and ceilings are best suited to meet contractors' needs.

The table below provides an overview of the supply chain in our industry, which illustrates management's estimate of the share of the supply channel that is represented by specialty distributors.

Supply Chain Overview

We estimate the North American market for the distribution of wallboard, ceilings and complementary interior construction products generated approximately $14 billion in sales in 2014. Of that market, we believe approximately $11 billion was served through specialty distributors like GMS, while the remaining approximately $3 billion was served by big box retailers, lumberyards and other channels. Despite continued consolidation among our competitors, we believe the North American specialty distribution industry remains highly fragmented and consists of approximately 400 local or regional participants. Our largest competitors in the North American specialty distribution industry include Allied Building Products (a subsidiary of CRH plc), Foundation Building Materials, L&W Supply (a subsidiary of USG) and Winroc (a subsidiary of Superior Plus). However, we believe smaller, regional or local competitors still comprise more than half of the industry. In contrast, the manufacturers of wallboard and ceilings products are highly consolidated. Since the late 1990s, the number of North American wallboard manufacturers has been reduced from twelve to seven, with the top four manufacturers representing approximately 75% of the wallboard market in 2014. Similarly, management estimates that three ceilings manufacturers accounted for approximately 95% of the ceilings manufactured in North America during 2014.

The main drivers for our products are commercial new construction, commercial repair and remodeling, or R&R, residential new construction and residential R&R. We believe all four end

4

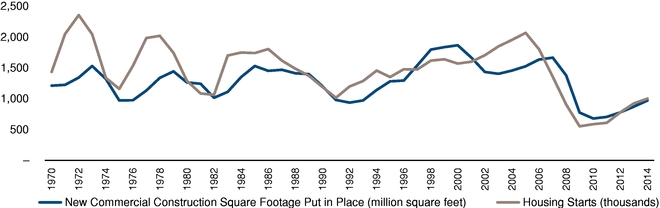

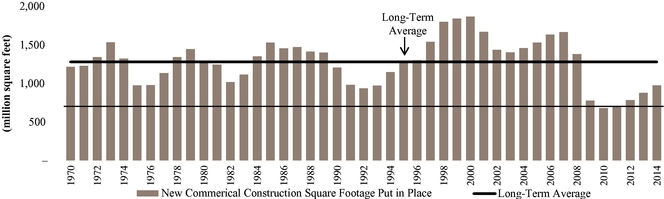

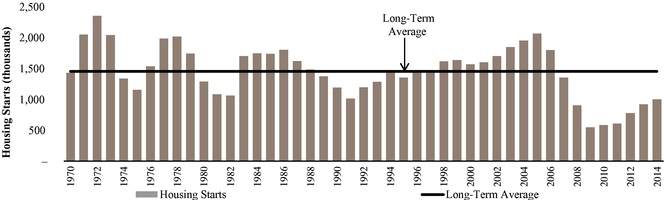

markets have begun an extended period of expansion. From 2011 to 2014, commercial construction square footage put in place has increased 38% and housing starts have increased 65%. Despite this progress, for 2014, commercial construction square footage put in place still would have needed to increase by 31% in order to achieve the historical market average of 1.3 billion square feet annually since 1970, while housing starts would have needed to increase by 45% in order to reach the historical market average of 1.5 million annually since 1970. Demand for our interior building products has historically correlated closely with construction activity, typically trailing housing starts and commercial construction square footage put in place by approximately six to nine months. As commercial and residential new construction activity approaches historical levels, we expect a corresponding increase in demand for the products we distribute.

We believe that the following competitive strengths will drive our future growth:

Entrepreneurial culture. We believe our entrepreneurial, results-driven culture fosters highly dedicated employees who provide our customers with outstanding service that differentiates us from our competition. We empower managers with the independence and authority to make decisions locally. Further, we incentivize employees throughout our Company to generate business and execute it profitably through a compensation program that includes variable compensation and equity ownership. Prior to this offering, 71 of our employees own approximately 32% of our common stock, including vested options. We also believe our entrepreneurial culture, combined with our dedication to developing, training and providing opportunities for all of our employees, helps us attract and retain top talent. Similarly, we believe these characteristics have also positioned us as an attractive acquirer for smaller distributors whose owners are seeking liquidity.

Market leader with significant scale advantages. We are the largest North American specialty distributor of wallboard, ceilings and complementary interior construction products. Our industry is characterized by a large number of smaller, local distributors, which generally lack our level of scale and resources. We believe our leading market position, national reach and differentiated platform provide us significant advantages relative to these competitors, including:

- •

- advantageous purchasing and sourcing, such as exclusive supplier relationships in many markets;

- •

- significant flexibility to efficiently and economically serve a broad range of customers, ranging from local specialty contractors to

large production home builders, across their span of operations; and

- •

- substantial financial and human resources to invest in developing our employees and maintaining our market-leading fleet and infrastructure.

Unwavering focus on relationships and superior service. We aim to be the premier partner of choice for our customers, suppliers and employees as well as smaller distributors whose owners may be seeking liquidity.

- •

- Customers. We believe we offer superior

services and solutions due to our comprehensive product offering, local market knowledge, product expertise and the quality of our service. We deliver products to job sites in a precise, safe and

timely manner with around-the-clock support from our dedicated local teams.

- •

- Suppliers. We provide a trusted professional partnership, resources for investment in growth and differentiated market access through our national reach. As a result, we have become a significant customer for our top suppliers, which enables us to obtain both competitive pricing and access to product in times of tight supply.

5

- •

- Employees. We provide our employees with an

entrepreneurial culture, a safe work environment, attractive compensation, financial incentives and career development opportunities.

- •

- Acquisition candidates. We provide smaller distributors whose owners may be seeking liquidity with the opportunity to continue to operate their business in an entrepreneurial manner while relieving them of the risks and burdens associated with owning a small business. We also offer these owners scale advantages, resources for future growth and an attractive culture and platform for their employees.

Differentiated operating model. We believe the combination of our national scale with our local go-to-market strategy helps to drive our growth and attractive margin profile. Specifically, through our Yard Support Center we are able to benefit from scaled purchasing efficiencies, integrated technology systems and shared best practices across our branch network, while still tailoring our service and product offering to the local preferences of each market. By retaining local brands and substantial autonomy in our branches, we are able to leverage local relationships and generate strong customer loyalty. In addition, we believe the inherent diversity in our model across customers, geographies and end markets offers lower volatility and less cyclicality than less diversified distributors in the building materials industry. We have low customer concentration with our largest customer representing less than 3% of our sales in fiscal 2015; we have geographic diversity with operations in 37 states; and based on certain assumptions by management as to the application of our products and our end markets, we believe that we have a balanced mix of business between the commercial and residential markets as well as between the new construction and R&R markets.

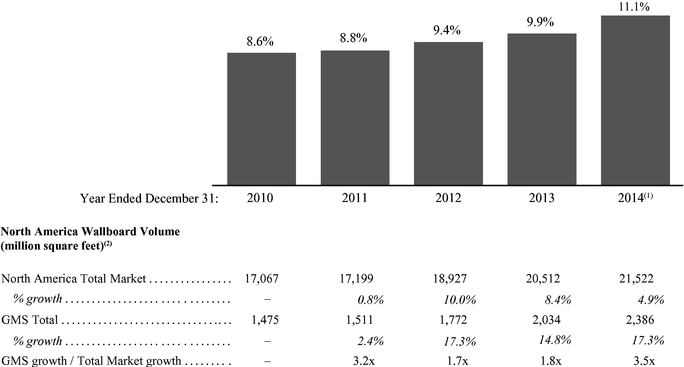

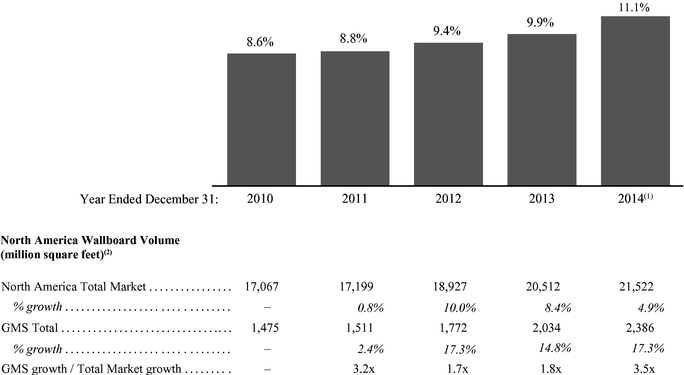

Multi-faceted growth. We have a track record of achieving above-market growth by capturing market share within our existing footprint, opening new branches and making selective acquisitions. Based on market data from the Gypsum Association and management's estimates, our volume growth outpaced the wallboard market by an average of approximately 700 basis points annually from 2010 to 2015, and we have increased our market share by approximately 250 basis points over the same period. We believe our success in capturing market share is due to our differentiated culture, superior customer service, national scale and strong supplier relationships. We also have a successful history of growth through opening new branches in select locations where we have identified opportunities in underserved markets. Since the beginning of 2010, we have opened 25 new branches and we currently expect to open several new branches each year depending on market conditions. The new branches we have opened since 2010 have typically delivered attractive returns on invested capital in these markets within a few years. In addition, we complement our organic growth strategy with tuck-in acquisitions, of which we completed nine, constituting 14 new branches, since the beginning of full year 2014 through October 31, 2015. We believe our success in acquiring smaller distributors has been the result of our highly selective acquisition criteria, our focus on culture, our strategy of maintaining the acquisition's existing brand, when appropriate, to help ensure customer and employee continuity, our experience with integration, our national scale and our competitive position.

6

GMS Wallboard Market Share

Source: Gypsum Association and Company data.

- (1)

- Includes

the wallboard volume from entities acquired in fiscal 2015 assuming that the entities were acquired on January 1,

2014.

- (2)

- Represents the wallboard production volume of U.S. manufacturing facilities, some of which is sold into Canada.

Our objective is to strengthen our competitive position, achieve above-market rates of profitable growth and increase stockholder value through the following key strategies:

Continue to invest in our employees, assets and infrastructure. We believe our above-market growth is driven by the quality of our employees and our ability to continuously develop outstanding talent. Each year, we target graduates from premier universities to enter our training program and spend considerable time and resources training them across all major functions of our operations. In addition to recruiting and training new talent, we have developed an extensive management training program for existing, high potential employees which is focused on developing sales capabilities, financial acumen and operational and safety expertise. While these programs represent a considerable investment, we believe they are critical to supporting our growth strategy by providing managers for new branches and increasing the overall capacity of our management team. Many of our former trainees have been promoted to run branches, regions and even divisions throughout our Company. We also believe the size and growth of our Company provide our employees with superior career opportunities than many of our competitors, which further enables us to recruit and retain top talent. To ensure that we support our employees with the best equipment, systems and infrastructure, we also continue to invest in other key areas of our business. We have a young and well maintained fleet of trucks and delivery equipment and have also made significant investments in our IT infrastructure and continuously improve our IT capabilities.

7

Grow market share within our existing geographic footprint. We expect to continue to capture profitable market share from competitors within our existing geographic footprint. We believe that our dedication to delivering superior customer service and our national scale differentiates us from our competitors. We also continue to provide strong financial incentives, support and technology to maximize the efficiency and effectiveness of our experienced salesforce as they work to provide local market expertise and tailored solutions for our customers. For example, our salesforce will provide our customers with leads on new job activity that helps them grow their businesses. Additionally, we have a strategic initiative to leverage our national capabilities to serve large homebuilders throughout their operations that we believe will increase our penetration of those accounts. We believe this provides a compelling value proposition for our homebuilder customers by ensuring consistent service levels across their footprint.

Accelerate growth by selectively opening new branches and executing acquisitions. We believe that significant opportunities exist to expand our geographic footprint by opening new branches and executing selective, tuck-in acquisitions.

- •

- New branches. Our strategy

for opening new branches is to further penetrate markets that are adjacent to our existing operations. Typically, we have pre-existing customer relationships in these markets but need a new location

to fully capitalize on those relationships. Relative to our size and scale, the capital investment required to open a new facility is usually small, and the new branches we have opened since 2010 have

typically generated attractive returns on invested capital within a few years. We believe our existing infrastructure is capable of supporting a much larger branch network, and we currently expect to

open several new branches each year depending on market conditions.

- •

- Selective acquisitions. We will continue to selectively pursue tuck-in acquisitions and have a dedicated team of professionals to manage the process. Due to the large, highly fragmented nature of our market and our reputation throughout the industry, we believe we have the potential to access a robust acquisition pipeline that will continue to supplement our strong organic growth. We use a rigorous targeting process to identify acquisition candidates that will fit our culture and business model. As a result of our scale, purchasing power and ability to improve operations through implementing best practices, we believe we can achieve substantial synergies and drive earnings accretion from our acquisition strategy. We also believe that our successful track record in acquiring businesses provides a competitive advantage in the evaluation and integration of future acquisitions. We consistently strive to maintain an extensive and active acquisition pipeline and are often evaluating several acquisition opportunities at any given time.

Capitalize on accelerating growth across distinct end markets. We believe the new commercial and residential construction markets have both begun an extended period of expansion. Given the extreme depth of the last recession, despite the growth to date, activity in both markets remains well below average historical levels. As such, we believe both markets will experience an extended, sustained period of growth in the future. In addition, while R&R activity has historically been more stable than new construction activity, we believe the prolonged period of under-investment during the downturn will result in above-average growth in both commercial and residential R&R activity in the near term.

Achieve improved financial performance through operational excellence and operating leverage. Over the past five years, as volumes have recovered and as we have streamlined our operating model, our Adjusted EBITDA margins have improved significantly. Our Yard Support Center continues to drive procurement savings and operational excellence across our branch network. Our operational initiatives include optimizing pricing, improving fleet utilization and maximizing working capital efficiency. As our volumes continue to grow, we expect margins to improve from the inherent operating leverage in our business. In the past, our existing branch network has supported substantially higher volumes per

8

branch. As our end markets continue to recover, we expect to generate higher operating margins on incremental volume as we leverage our fixed costs at our existing branches. Similarly, we have made significant investments in our Yard Support Center over the past few years to prepare for significant growth in our business. As we continue to grow our volumes, we expect to gain operating leverage on that investment in the years ahead.

Subsequent to October 31, 2015, we acquired Badgerland Supply Inc. ("Badgerland"), Hathaway & Sons ("Hathaway") and Gypsum Supply Company Inc. ("GSC") for a total purchase price of approximately $83.5 million. Badgerland, Hathaway and GSC distribute wallboard and related building materials from 15 locations in Wisconsin, Illinois, California, Michigan and Ohio. For the twelve months ended October 31, 2015, the combined companies generated approximately $128.1 million in net sales and the earnings of these entities would have contributed approximately $12.2 million to our Adjusted EBITDA for that period, including operating synergies.

Our business is subject to a number of risks of which you should be aware before deciding to invest in our common stock. The risks are discussed more fully in the "Risk Factors" section of this prospectus immediately following this prospectus summary. These risks include, but are not limited to, the following:

- •

- general economic and financial conditions;

- •

- the state of the commercial and residential construction and R&R markets;

- •

- competitive industry pressures;

- •

- the fluctuation in prices of the products we distribute;

- •

- the consolidation of our industry;

- •

- product shortages and relationships with key suppliers;

- •

- product liability and warranty claims, and other claims related to our business;

- •

- our ability to attract key employees; and

- •

- our current level of indebtedness.

GMS Inc. is a Delaware corporation. Our Predecessor was founded in 1971. Our principal executive office is located at 100 Crescent Centre Parkway, Suite 800, Tucker, Georgia 30084, and our telephone number at that address is (800) 392-4619. We maintain a website on the Internet at www.gms.com. The information contained on, or that can be accessed through, our website is not a part of, and should not be considered as being incorporated by reference into, this prospectus. For a chart illustrating our organizational structure, see "—Organizational Structure."

AEA is one of the most experienced global private investment firms. Founded in 1968, AEA currently manages over $6 billion of capital for an investor group that includes former and current chief executive officers of major multinational corporations, family groups, and institutional investors from around the world. With a staff of approximately 70 investment professionals and offices in New

9

York, Stamford, London, Munich and Shanghai, AEA focuses on investing in companies in the consumer products/retail, industrial products, specialty chemicals and related services sectors.

The chart below summarizes our ownership and corporate structure after giving effect to this offering, assuming no exercise of the underwriters' option to purchase additional shares.

- (1)

- Some of our operating subsidiaries sponsor deferred compensation arrangements that entitle selected employees of those subsidiaries to participate in increases in the adjusted book value of a specified number of shares of common stock of those subsidiaries. Adjusted book value for this purpose generally means the book value of the relevant shares, as increased, or decreased, to reflect those shares' ratable portion of any annual earnings, or losses, of the relevant subsidiary (based on the total number of outstanding shares of the relevant subsidiary). In certain cases, employees participate in these arrangements by holding a minority portion of the common stock of the subsidiary, which stock is generally non-transferrable and subject to mandatory provisions that require the stock to be redeemed at its adjusted book value, subject in certain cases to an agreed upon minimum value, only upon termination of employment. As of October 31, 2015, the total fair value of these liabilities is $26.7 million, of which $1.4 million is the current portion. These amounts are included in current liabilities and liabilities to noncontrolling interest holders on our unaudited condensed consolidated balance sheets. The redemption value of the awards is $30.3 million as of October 31, 2015. We do not expect to grant similar interests in our subsidiaries in the future.

10

Common stock offered by us |

shares. | |

Common stock to be outstanding after this offering |

shares. | |

Option to purchase additional shares |

The underwriters have an option to purchase up to an aggregate of additional shares of common stock from us, to cover any over-allotments. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. | |

Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and commissions and estimated offering expenses, will be approximately $ , assuming the shares are offered at $ per share (the midpoint of the price range set forth on the cover page of this prospectus). We intend to use the net proceeds from this offering to (i) repay approximately $ of indebtedness under the Second Lien Facility and (ii) pay approximately $ of fees and expenses related to this offering, including fees of $ to our Sponsor immediately following this offering. We expect to use any remaining proceeds for general corporate purposes. See "Use of Proceeds." | |

Dividend policy |

We do not expect to pay any dividends on our common stock for the foreseeable future. See "Dividend Policy." | |

Proposed New York Stock Exchange symbol |

"GMS" | |

Directed share program |

The underwriters have reserved for sale, at the initial public offering price, up to shares of the common stock to be offered to our directors, officers and employees. See "Underwriting." | |

Risk factors |

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 19 of this prospectus for a discussion of factors you should carefully consider before investing in our common stock. |

The number of shares of common stock to be outstanding after this offering excludes:

- •

- shares of common stock issuable upon the exercise of options outstanding under our existing equity plan as of

October 31, 2015 at a weighted average exercise price of $ per share; and

- •

- shares of common stock reserved for future issuance under our existing equity plan.

Unless otherwise indicated, all information contained in this prospectus:

- •

- assumes an initial public offering price of $ per share, which is the midpoint of the price range set forth on the

cover page of this prospectus;

- •

- assumes the underwriters' option to purchase additional shares will not be exercised;

- •

- gives effect to a -for- stock split

effected on , 2016; and

- •

- gives effect to our amended and restated certificate of incorporation and our amended and restated bylaws, which will be in effect prior to the consummation of this offering.

11

Summary Financial and Other Data

The summary consolidated financial information of Successor presented below as of October 31, 2015 and for the six months ended October 31, 2015 and 2014 has been derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial information of Successor presented below for the fiscal year ended April 30, 2015, the one month ended April 30, 2014 and as of April 30, 2015 and 2014 has been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial information of Predecessor presented below for the eleven months ended March 31, 2014 and the fiscal year ended April 30, 2013 has been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial information of Predecessor presented below as of April 30, 2013 has been derived from our consolidated financial statements not included in this prospectus. As discussed elsewhere in this prospectus, on April 1, 2014, GMS Inc., or the Successor, acquired, through its wholly-owned entities, GYP Holdings II Corp. and GYP Holdings III Corp., all of the capital stock of Gypsum Management and Supply, Inc., or the Predecessor. Successor is majority owned by certain affiliates of AEA and certain of our other stockholders. We refer to this transaction as the "Acquisition." As a result of the Acquisition and the resulting change in control and changes due to the impact of purchase accounting, we are required to present separately the operating results for the Predecessor periods ending on or prior to March 31, 2014 and the Successor periods beginning on or after April 1, 2014. For a discussion of our Predecessor and Successor periods, see "Basis of Presentation."

The historical data presented below has been derived from financial statements that have been prepared using GAAP. This data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes included elsewhere in this prospectus. The selected operating data has been prepared on an unaudited basis.

12

| |

Successor |

|

Predecessor | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

||||||||||||||||||||

| |

Six Months Ended October 31, 2015 |

Six Months Ended October 31, 2014 |

Fiscal Year Ended April 30, 2015 |

One Month Ended April 30, 2014 |

|

Eleven Months Ended March 31, 2014 |

Fiscal Year Ended April 30, 2013 |

||||||||||||||

| |

|

||||||||||||||||||||

| |

|

||||||||||||||||||||

| |

|

||||||||||||||||||||

| |

(in thousands, except share and per share data) |

||||||||||||||||||||

Statement of Operations Data: |

|||||||||||||||||||||

Net sales |

$ | 910,518 | $ | 807,562 | $ | 1,570,085 | $ | 127,332 | $ | 1,226,008 | $ | 1,161,610 | |||||||||

Cost of sales (exclusive of depreciation and amortization shown separately below) |

625,717 | 566,852 | 1,091,114 | 97,955 | 853,020 | 824,331 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Gross profit |

284,801 | 240,710 | 478,971 | 29,377 | 372,988 | 337,279 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Operating expenses: |

|||||||||||||||||||||

Selling, general and administrative expenses |

224,562 | 195,093 | 396,155 | 46,052 | 352,930 | 295,289 | |||||||||||||||

Depreciation and amortization |

31,327 | 32,655 | 64,165 | 6,336 | 12,253 | 11,627 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Total operating expenses |

255,889 | 227,748 | 460,320 | 52,388 | 365,183 | 306,916 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Operating income (loss) |

28,912 | 12,962 | 18,651 | (23,011 | ) | 7,805 | 30,363 | ||||||||||||||

Other (expense) income: |

|||||||||||||||||||||

Interest expense |

(18,517 | ) | (18,363 | ) | (36,396 | ) | (2,954 | ) | (4,226 | ) | (4,413 | ) | |||||||||

Change in fair value of financial instruments |

— | — | (2,494 | ) | — | — | — | ||||||||||||||

Change in fair value of mandatorily redeemable common shares(1) |

— | — | — | — | (200,004 | ) | (198,212 | ) | |||||||||||||

Other income, net |

919 | 1,076 | 1,916 | 149 | 2,187 | 1,169 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Total other (expense), net |

(17,598 | ) | (17,287 | ) | (36,974 | ) | (2,805 | ) | (202,043 | ) | (201,456 | ) | |||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Income (loss) before tax |

11,314 | (4,325 | ) | (18,323 | ) | (25,816 | ) | (194,238 | ) | (171,093 | ) | ||||||||||

Income tax expense (benefit) |

5,928 | (455 | ) | (4,526 | ) | (6,863 | ) | 6,623 | 11,534 | ||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) |

$ | 5,386 | $ | (3,870 | ) | $ | (13,797 | ) | $ | (18,953 | ) | $ | (200,861 | ) | $ | (182,627 | ) | ||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Weighted average shares outstanding: |

|||||||||||||||||||||

Basic |

3,219,856 | 3,187,354 | 3,194,566 | 3,183,870 | |||||||||||||||||

Diluted |

3,240,389 | 3,187,354 | 3,194,566 | 3,183,870 | |||||||||||||||||

Net income (loss) per share: |

|||||||||||||||||||||

Basic |

$ | 1.67 | $ | (1.21 | ) | $ | (4.32 | ) | $ | (5.95 | ) | ||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Diluted |

$ | 1.66 | $ | (1.21 | ) | $ | (4.32 | ) | $ | (5.95 | ) | ||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

Other Financial Data: |

|||||||||||||||||||||

Adjusted EBITDA(2)(3) |

$ | 68,913 | $ | 64,531 | $ | 113,860 | $ | 8,372 | $ | 78,690 | $ | 57,511 | |||||||||

Adjusted EBITDA margin(2)(3) |

7.6 | % | 7.3 | % | 6.7 | % | 6.6 | % | 6.4 | % | 5.0 | % | |||||||||

13

| |

Successor |

|

Predecessor | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

||||||||||||||

| |

October 31, 2015 |

April 30, 2015 |

April 30, 2014 |

|

April 30, 2013 |

||||||||||

| |

|

||||||||||||||

| |

|

||||||||||||||

| |

(in thousands) |

||||||||||||||

Balance Sheet Data: |

|||||||||||||||

Cash and cash equivalents |

$ | 9,420 | $ | 12,284 | $ | 32,662 | $ | 13,383 | |||||||

Total assets |

1,121,166 | 1,154,576 | 1,122,351 | 494,626 | |||||||||||

Total debt(4) |

563,132 | 556,984 | 538,785 | 115,003 | |||||||||||

Total stockholders' equity (deficit) |

299,891 | 297,472 | 299,434 | (274,846 | ) | ||||||||||

| |

Six Months Ended October 31, 2015 |

Fiscal Year Ended April 30, 2015 |

|||||

|---|---|---|---|---|---|---|---|

| |

(in thousands, except share and per share data) |

||||||

Pro Forma Statement of Operations Data(5): |

|||||||

Pro forma net income(5) |

|||||||

Pro forma weighted average shares outstanding(6) |

|||||||

Basic |

|||||||

Diluted |

|||||||

Pro forma net income per share(5)(6) |

|||||||

Basic |

|||||||

Diluted |

|||||||

| |

Six Months Ended |

Fiscal Year Ended | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

October 31, 2015 |

October 31, 2014 |

April 30, 2015 |

April 30, 2014 |

April 30, 2013 |

|||||||||||

Selected Operating Data: |

||||||||||||||||

Branches (at period end) |

159 | 148 | 156 | 140 | 132 | |||||||||||

Employees (at period end) |

3,246 | 2,827 | 3,088 | 2,621 | 2,405 | |||||||||||

Wallboard volume (million square feet) |

1,381 | 1,191 | 2,328 | 2,088 | 1,850 | |||||||||||

- (1)

- Represents

the change in fair value of mandatorily redeemable common shares of the Predecessor, all of which were acquired by the Company on April 1,

2014 in connection with the Acquisition. These shares had certain redemption features which provided that upon the death or disability of the shareholder or termination of his employment, Predecessor

would be required to purchase these shares at their then current fair values. Pursuant to this provision, these shares were deemed to be mandatorily redeemable and, as such, were required to be

reflected as a liability at their estimated fair values at the end of any reporting period. Changes in fair value are reflected as "Change in fair value of mandatorily redeemable common shares" on our

consolidated statements of operations. Fair value was estimated based on commonly used valuation techniques. For additional details, see Note 10 of our audited consolidated financial statements

included elsewhere in this prospectus.

- (2)

- We report our financial results in accordance with GAAP. However, we present Adjusted EBITDA and Adjusted EBITDA margin, which are not recognized financial measures under GAAP, because we believe they assist investors and analysts in comparing our operating performance across reporting periods on a consistent basis by excluding items that we do not believe are indicative of our core operating performance. Management believes Adjusted EBITDA is helpful in highlighting trends in our operating results, while other measures can differ significantly depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which companies operate and capital investments.

In addition, we utilize Adjusted EBITDA in certain calculations under the ABL Facility and the Term Loan Facilities. The ABL Facility and the Term Loan Facilities permit us to make certain additional adjustments in calculating Consolidated EBITDA, such as projected net cost savings, which are not reflected in the Adjusted EBITDA data presented in this prospectus. We may in the future reflect such permitted adjustments in our calculations of Adjusted EBITDA. See "Description of Certain Indebtedness—Senior Credit Facilities."

You are encouraged to evaluate each adjustment and the reasons we consider it appropriate for supplemental analysis. In addition, in evaluating Adjusted EBITDA, you should be aware that in the future, we may incur expenses similar to the adjustments in the presentation of Adjusted EBITDA. Our presentation of Adjusted EBITDA should not be construed as

14

an inference that our future results will be unaffected by unusual or non-recurring items. In addition, Adjusted EBITDA may not be comparable to similarly titled measures used by other companies in our industry or across different industries.

- •

- Adjusted EBITDA and Adjusted EBITDA margin do not reflect every expenditure, future

requirements for capital expenditures or contractual commitments;

- •

- Adjusted EBITDA does not reflect changes in our working capital needs;

- •

- Adjusted EBITDA does not reflect the significant interest expense, or the amounts necessary to

service interest or principal payments, on our outstanding debt;

- •

- Adjusted EBITDA does not reflect income tax expense and, because the payment of taxes is part

of our operations, tax expense is a necessary element of our costs and ability to operate;

- •

- although depreciation and amortization are eliminated in the calculation of Adjusted EBITDA,

the assets being depreciated and amortized will often have to be replaced in the future, and Adjusted EBITDA does not reflect any costs of such replacements;

- •

- non-cash compensation is and will remain a key element of our overall long-term incentive

compensation package, although we exclude it as an expense when evaluating our ongoing operating performance for a particular period;

and

- •

- Adjusted EBITDA does not reflect the impact of earnings or charges resulting from matters we

consider not to be indicative of our ongoing operations.

We also include information concerning Adjusted EBITDA margin, which is calculated as Adjusted EBITDA divided by net sales. We present Adjusted EBITDA margin because it is used by management as a performance measure to judge the level of Adjusted EBITDA that is generated from net sales.

Adjusted EBITDA and Adjusted EBITDA margin have their limitations as analytical tools and you should not consider them in isolation, or as a substitute for analysis of our results as reported under GAAP. Some of these limitations include:

- We compensate for these limitations by relying primarily on our GAAP results and using Adjusted EBITDA and Adjusted EBITDA margin only as supplemental information.

15

The following is a reconciliation of our net income (loss) to Adjusted EBITDA:

| |

Successor |

|

Predecessor | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

||||||||||||||||||||

| |

Six Months Ended October 31, 2015 |

Six Months Ended October 31, 2014 |

Fiscal Year Ended April 30, 2015 |

One Month Ended April 30, 2014 |

|

Eleven Months Ended March 31, 2014 |

Fiscal Year Ended April 30, 2013 |

||||||||||||||

| |

|

||||||||||||||||||||

| |

|

||||||||||||||||||||

| |

|

||||||||||||||||||||

| |

(in thousands) |

||||||||||||||||||||

Net income (loss) |

$ | 5,386 | $ | (3,870 | ) | $ | (13,797 | ) | $ | (18,953 | ) | $ | (200,861 | ) | $ | (182,627 | ) | ||||

Interest expense |

18,517 | 18,363 | 36,396 | 2,954 | 4,226 | 4,413 | |||||||||||||||

Change in fair value of mandatorily redeemable shares |

— | — | — | — | 200,004 | 198,212 | |||||||||||||||

Interest income |

(438 | ) | (549 | ) | (1,010 | ) | (76 | ) | (846 | ) | (798 | ) | |||||||||

Income tax expense (benefit) |

5,928 | (455 | ) | (4,526 | ) | (6,863 | ) | 6,623 | 11,534 | ||||||||||||

Depreciation expense |

13,738 | 17,381 | 32,208 | 3,818 | 12,224 | 11,665 | |||||||||||||||

Amortization expense |

17,589 | 15,274 | 31,957 | 2,518 | 38 | 72 | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

EBITDA |

$ | 60,720 | $ | 46,144 | $ | 81,228 | $ | (16,602 | ) | $ | 21,408 | $ | 42,471 | ||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Executive compensation(a) |

$ | — | $ | — | $ | — | $ | 20 | $ | 2,427 | $ | 13,420 | |||||||||

Stock appreciation rights expense(b) |

1,286 | 1,114 | 2,268 | 80 | 1,288 | 1,061 | |||||||||||||||

Redeemable noncontrolling interests(c) |

1,005 | 907 | 1,859 | 71 | 2,957 | 2,195 | |||||||||||||||

Equity-based compensation(d) |

1,361 | 3,450 | 6,455 | 1 | 27 | 82 | |||||||||||||||

Acquisition related costs(e) |

— | 837 | 837 | 16,155 | 51,809 | 230 | |||||||||||||||

Severance, other costs related to discontinued operations and closed branches and certain other costs(f) |

1,381 | 163 | 413 | — | — | (30 | ) | ||||||||||||||

Transaction costs (acquisitions and other)(g) |

1,755 | 119 | 1,891 | — | — | — | |||||||||||||||

Loss (gain) on disposal of assets |

280 | 527 | 1,089 | 170 | (1,034 | ) | (2,231 | ) | |||||||||||||

Management fee to related party(h) |

1,125 | 1,125 | 2,250 | 188 | — | — | |||||||||||||||

Effects of fair value adjustments to inventory(i) |

— | 4,486 | 5,012 | 8,289 | — | — | |||||||||||||||

Interest rate swap and cap mark-to-market(j) |

— | — | 2,494 | — | (192 | ) | 313 | ||||||||||||||

Contributions from acquisitions(k) |

— | 5,659 | 8,064 | — | — | — | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | |

Adjusted EBITDA |

$ | 68,913 | $ | 64,531 | $ | 113,860 | $ | 8,372 | $ | 78,690 | $ | 57,511 | |||||||||

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

- (a)

- Represents

compensation paid to certain executives who were majority owners prior to the Acquisition. Following the Acquisition, these executives'

compensation agreements were amended, and going forward we do not anticipate additional adjustments.

- (b)

- Represents

non-cash compensation expenses related to stock appreciation rights agreements. For additional details regarding stock appreciation rights, refer

to "Management's Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies—Subsidiary Equity-Based Deferred Compensation

Arrangements."

- (c)

- Represents

non-cash compensation expense related to changes in the redemption values of noncontrolling interests. For additional details regarding

redeemable noncontrolling interests of our subsidiaries, refer to "Management's Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting

Policies—Subsidiary Equity-Based Deferred Compensation Arrangements."

- (d)

- Represents

non-cash equity-based compensation expense related to stock options.

- (e)

- Represents non-recurring expenses related specifically to the Acquisition, including fees to financial advisors, accountants, attorneys and other professionals as well as costs related to the retirement of corporate stock appreciation rights. Also included are one-time bonuses paid to certain employees in connection with the Acquisition.

16

- (f)

- Represents

severance expenses, other costs related to discontinued operations and closed branches and certain other costs permitted in calculations under

the ABL Facility and the Term Loan Facilities.

- (g)

- Represents

one-time costs related to this offering and acquisitions (other than the Acquisition) paid to third party advisors.

- (h)

- Represents

management fees paid by us to our Sponsor. After this offering, our Sponsor will no longer receive management fees from us.

- (i)

- Represents

the non-cash cost of sales impact of purchase accounting adjustments to increase inventory to its estimated fair value, primarily related to the

Acquisition.

- (j)

- Represents

the mark-to-market adjustments for certain financial instruments.

- (k)

- Represents earnings of acquired entities from the beginning of the period presented to the date of such acquisition, as well as certain purchasing synergies and cost savings, as defined in and permitted by the ABL Facility and the Term Loan Facilities. Contributions from acquisitions are only reflected for fiscal 2015 and the six months ended October 31, 2014.

- (3)

- Our

Adjusted EBITDA for fiscal 2015 and the six months ended October 31, 2014 includes approximately $8.1 million and $5.7 million, respectively,

from entities acquired in fiscal 2015 and the six months ended October 31, 2014 for the period prior to the date of acquisition of such entities, as defined in and permitted by the ABL Facility

and the Term Loan Facilities. However, Adjusted EBITDA margin, which is calculated as a percentage of net sales, excludes these $8.1 million and $5.7 million adjustments for fiscal 2015 and the

six months ended October 31, 2014, respectively, to be consistent with our calculation of net sales for the same period.

- (4)

- Includes

long-term debt and capital lease obligations.

- (5)

- Pro

forma to give effect to the following transactions as if they had occurred as of the beginning of the periods presented: (i) this offering,

(ii) the repayment of $ million of indebtedness under the Second Lien Facility from the proceeds of this offering as described in "Use of Proceeds" and (iii) each

of the related adjustments mentioned below.

- Adjustments

to net income (loss) for the six months ended October 31, 2015 and the fiscal year ended April 30, 2015 reflect

(i) a $ and $ , respectively, decrease in interest expense (see the reconciliation of historical

interest expense to pro forma interest expense below),

(ii) a $ and $ , respectively, increase in income tax expense due to higher income before taxes

relating to our pro forma net income and (iii) the removal

of $ and $ , respectively, of our Sponsor's management fees. Pro forma net income for the six months ended

October 31, 2015 and the fiscal year ended

April 30, 2015 does not give effect to the payment of fees to our Sponsor of $ .

- The following is a reconciliation of historical net (loss) to pro forma net income for the six months ended October 31, 2015 and the fiscal year ended April 30, 2015:

| (in thousands) |

Six Months Ended October 31, 2015 |

Fiscal Year Ended April 30, 2015 |

|||||

|---|---|---|---|---|---|---|---|

Net income (loss) |

$ | $ | |||||

Decrease in interest expense(a) |

|||||||

Increase in income tax expense(b) |

|||||||

Removal of management fee(c) |

|||||||

| | | | | | | | |

Pro forma net income (loss) |

$ | $ | |||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

- (a)

- See

the reconciliation of historical interest expense to pro forma interest expense below.

- (b)

- Reflects

an increase of $ and $ , respectively, in income tax expense for the six months ended October 31, 2015

and the

fiscal year ended April 30, 2015 for the related tax effects of the pro forma adjustments. The tax impact is based upon an increase of pro forma income before taxes of $ and

$

, respectively, and a statutory tax rate of % and %, respectively.

- (c)

- Reflects the removal of $ and $ , respectively, of our Sponsor's management fees for the six months ended October 31, 2015 and the fiscal year ended April 30, 2015. In connection with this offering, the management agreement will be terminated. See "Certain Relationships and Related Party Transactions."

17

The following is a reconciliation of historical interest expense to pro forma interest expense for the six months ended October 31, 2015 and the fiscal year ended April 30, 2015.

| (in thousands) |

Six Months Ended October 31, 2015 |

Fiscal Year Ended April 30, 2015 |

|||||

|---|---|---|---|---|---|---|---|

Interest expense |

$ | $ | |||||

Decrease resulting from use of proceeds of this offering(a) |

|||||||

| | | | | | | | |

Pro forma interest expense |

$ | $ | |||||

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

- (a)

- Assumes repayment of $ million of indebtedness under the Second Lien Facility, which bears interest at a rate of 7.75% per annum, from the proceeds of this offering, as if it had occurred as of the beginning of the periods presented.

- (6)

- Gives effect to (i) the -for- stock split effected on , 2016 and (ii) the shares of our common stock to be issued by us in this offering. Pro forma basic net income per share consists of pro forma net income divided by the pro forma basic weighted average common shares outstanding. Pro forma diluted net income per share consists of pro forma net income divided by the pro forma diluted weighted average common shares outstanding.

18

Investing in our common stock involves a high degree of risk. You should carefully consider the following factors, as well as other information contained in this prospectus, before deciding to invest in shares of our common stock. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment in our common stock.

Risks Relating to Our Business and Industry

Our business is affected by general business, financial market and economic conditions, which could adversely affect our results of operations.

Our business and results of operations are significantly affected by general business, financial market and economic conditions. General business, financial market and economic conditions that could impact the level of activity in the commercial and residential construction and the repair and remodeling markets include, among others, interest rate fluctuations, inflation, unemployment levels, tax rates, capital spending, bankruptcies, volatility in both the debt and equity capital markets, liquidity of the global financial markets, the availability and cost of credit, investor and consumer confidence, global economic growth, local, state and federal government regulation and the strength of regional and local economies in which we operate.

There was a significant decline in economic growth, both in the United States and worldwide, that began in the second half of 2007 and continued through 2011. During this period, the U.S. construction markets we serve experienced unprecedented declines since the post-World War II era. There can be no guarantee that any improvement in these markets will be sustained or continue.

Our sales are in part dependent upon the commercial new construction market and the commercial repair and remodel market.

The recent downturn in the U.S. commercial new construction market was one of the most severe of the last 40 years. Previously, such downturns in the construction industry have typically lasted about 2 to 3 years, resulting in market declines of approximately 20% to 40%, while the recent downturn in the commercial construction market has lasted over 4 years, resulting in a market decline of approximately 60%. According to Dodge Data & Analytics, commercial construction put in place began to recover in 2013 and continued to increase 11% in 2014. However, 2014 levels of new commercial construction square footage put in place, measured by square footage of construction, are still well below the historical market average of 1.3 billion square feet annually since 1970. We cannot predict the duration of the current market conditions or the timing or strength of any future recovery of commercial construction activity in our markets. Continued weakness in the commercial construction market and the commercial R&R market, would have a significant adverse effect on our business, financial condition and operating results. Continued uncertainty about current economic conditions will continue to pose a risk to our business that serves the commercial construction and R&R markets as participants in this industry may postpone spending in response to tighter credit, negative financial news and/or declines in income or asset values, which could have a continued material negative effect on the demand for our products and services.

Our sales are also in part dependent upon the residential new construction market and home repair and remodeling activity.

The distribution of our products, particularly wallboard, to contractors serving the residential market represents a significant portion of our business. Though its cyclicality has historically been somewhat moderated by R&R activity, wallboard demand is highly correlated with housing starts. Housing starts and R&R activity, in turn, are dependent upon a number of factors, including housing demand, housing inventory levels, housing affordability, foreclosure rates, geographical shifts in the

19

population and other changes in demographics, the availability of land, local zoning and permitting processes, the availability of construction financing and the health of the economy and mortgage markets. Unfavorable changes in any of these factors beyond our control could adversely affect consumer spending, result in decreased demand for homes and adversely affect our business.