Attached files

| file | filename |

|---|---|

| EX-23 - EX-23.1 - BIOCEPT INC | bioc-ex231_23.htm |

| EX-5 - EX-5.1 - BIOCEPT INC | bioc-ex51_117.htm |

As filed with the Securities and Exchange Commission on December 21, 2015

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Biocept, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

8071 |

80-0943522 |

|

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

5810 Nancy Ridge Drive

San Diego, CA 92121

(858) 320-8200

(Address, including zip code, and telephone number, including

area code, of registrant’s principal executive offices)

Michael W. Nall

Chief Executive Officer and President

Biocept, Inc.

5810 Nancy Ridge Drive

San Diego, CA 92121

(858) 320-8200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

Frederick T. Muto Charles J. Bair Cooley LLP 4401 Eastgate Mall San Diego, CA 92121 (858) 550-6142 |

Mark G. Foletta Chief Financial Officer Biocept, Inc. 5810 Nancy Ridge Drive San Diego, CA 92121 (858) 320-8200 |

Martin P. Dunn, Esq. Morrison & Foerster LLP 2000 Pennsylvania Avenue, NW, Suite 6000 Washington, DC 20006 (202) 778-1611 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 under the Securities Exchange Act of 1934. (Check one):

|

Large Accelerated Filer o |

Accelerated Filer o |

Non-accelerated Filer o |

Smaller Reporting Company x |

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered |

|

Amount to be |

|

|

Proposed Maximum Offering Price Per |

|

|

Proposed Maximum |

|

|

Amount of |

|

Shares of common stock, $0.0001 par value per share |

|

3,774,122 (1) |

|

|

$1.45 (2) |

|

|

$5,472,477 |

|

|

$551 |

|

(1) |

Represents 790,000 shares of common stock currently outstanding and 2,984,122 shares of common stock that are issuable pursuant to a common stock purchase agreement with the selling stockholder named herein. Pursuant to Rule 416(a) of the Securities Act of 1933, as amended, this Registration Statement also covers any additional shares of common stock which may become issuable to prevent dilution from stock splits, stock dividends and similar events. |

|

(2) |

Pursuant to Rule 457(c) of the Securities Act of 1933, as amended, calculated on the basis of the average and low prices per share of the registrant’s common stock reported on The NASDAQ Capital Market on December 18, 2015. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholder may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and the selling stockholder is not soliciting offers to buy these securities, in any state where the offer or sale of these securities is not permitted.

PROSPECTUS, SUBJECT TO COMPLETION, DATED DECEMBER 21, 2015

3,774,122 Shares

Common Stock

This prospectus relates to the sale of up to 3,774,122 shares of our common stock by Aspire Capital Fund, LLC. Aspire Capital is also referred to in this prospectus as the selling stockholder. The prices at which the selling stockholder may sell the shares will be determined by the prevailing market price for the shares or in negotiated transactions. We will not receive proceeds from the sale of the shares by the selling stockholder. However, we may receive proceeds of up to $15 million from the sale of our common stock to the selling stockholder, pursuant to a common stock purchase agreement entered into with the selling stockholder on December 21, 2015, once the registration statement, of which this prospectus is a part, is declared effective.

The selling stockholder is an “underwriter” within the meaning of the Securities Act of 1933, as amended. We will pay the expenses of registering these shares, but all selling and other expenses incurred by the selling stockholder will be paid by the selling stockholder.

Our common stock is listed on The NASDAQ Capital Market under the ticker symbol “BIOC.” On December 21, 2015, the last reported sale price per share of our common stock was $1.48 per share.

You should read this prospectus, together with additional information described under the headings “Incorporation of Certain Information by Reference” and “Where You Can Find More Information,” carefully before you invest in any of our securities.

Investing in our securities involves a high degree of risk. See “Risk Factors” on page 6 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is .

|

|

1 |

|

|

|

2 |

|

|

|

6 |

|

|

|

31 |

|

|

|

32 |

|

|

|

36 |

|

|

|

37 |

|

|

|

39 |

|

|

|

39 |

|

|

|

39 |

|

|

|

40 |

We incorporate by reference important information into this prospectus. You may obtain the information incorporated by reference without charge by following the instructions under “Where You Can Find More Information.” You should carefully read this prospectus as well as additional information described under “Incorporation of Certain Information by Reference,” before deciding to invest in our common shares. All references in this prospectus to “Biocept,” “the Company,” “we,” “us” or “our” mean Biocept, Inc., unless we state otherwise or the context otherwise requires.

We are responsible for the information contained in this prospectus. We have not authorized anyone to provide you with different information, and we take no responsibility for any other information others may give you. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

We use in this prospectus our BIOCEPT logo, for which a United States trademark application has been filed, our mark CEE, which is a registered United States trademark, and our marks OncoCEE-BR, OncoCEE-LU, CEE-Selector, CEE-Cap, CEE-Enhanced, CEE-Sure, OncoCEE-GA, OncoCEE-PR, OncoCEE-ME, OncoCEE-CR and OncoCEE, which in the United States are unregistered trademarks. This prospectus also includes trademarks, tradenames and service marks that are the property of other organizations. Solely for convenience, trademarks and tradenames referred to in this prospectus appear (after the first usage) without the ® and ™ symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or that the applicable owner will not assert its rights, to these trademarks and tradenames.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. All statements other than statements of historical facts contained in this prospectus, including statements regarding our future results of operations and financial position, business strategy, prospective products, product approvals, timing and likelihood of success, plans and objectives of management for future operations, and future results of current and anticipated products are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this prospectus are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this prospectus and are subject to a number of risks, uncertainties and assumptions described in this prospectus and the documents that we incorporate by reference herein and have been filed as exhibits to the registration statement of which this prospectus is a part. Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified and some of which are beyond our control, you should not rely on these forward-looking statements as predictions of future events. The events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. Moreover, we operate in an evolving environment. New risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise. The forward-looking statements contained in this prospectus are excluded from the safe harbor protection provided by the Private Securities Litigation Reform Act of 1995 and Section 27A of the Securities Act.

This prospectus also contains estimates and other statistical data made by independent parties and by us relating to market size and growth and other data about our industry. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. In addition, projections, assumptions and estimates of our future performance and the future performance of the markets in which we operate are necessarily subject to a high degree of uncertainty and risk.

-1-

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, especially the “Risk Factors” section of this prospectus before making an investment decision.

Our Company

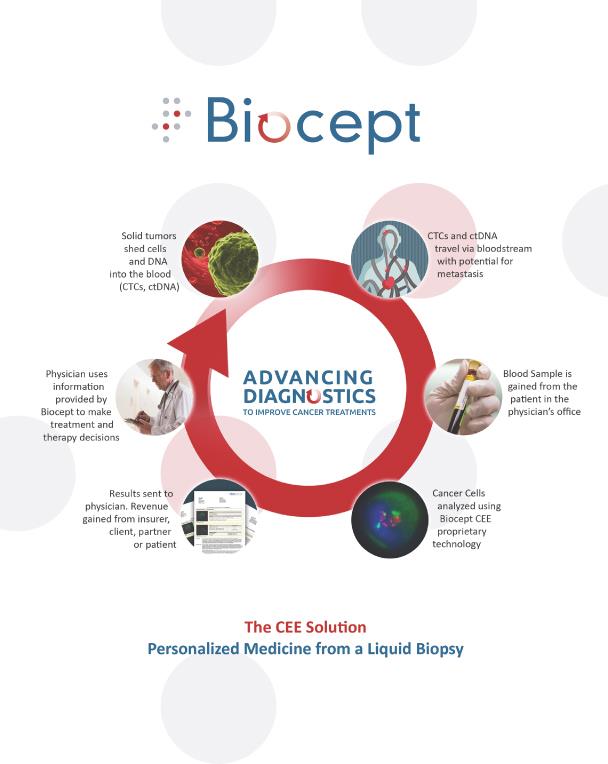

We are an early-stage molecular oncology diagnostics company that develops and commercializes proprietary circulating tumor cell (“CTC”) and circulating tumor DNA (“ctDNA”) assays utilizing a standard blood sample, or “liquid biopsy.” Our current blood-based molecular cancer diagnostics provide, and our planned future diagnostics would provide, information to oncologists and other physicians that enable them to select appropriate personalized treatment for their patients based on better, timelier and more-detailed data on the characteristics of their patients’ tumors.

Our current molecular cancer diagnostics and our planned future diagnostics utilize our CEE technology for the enumeration and analysis of CTCs, and our Target-SelectorTM technology for the detection and analysis of ctDNA from plasma, each performed on a standard blood sample. The CEE technology is an internally developed and patented, microfluidics-based CTC capture and analysis platform, with enabling features that change how CTC testing can be used by clinicians by providing real-time biomarker monitoring from a standard blood sample. The Target-Selector technology enables mutation detection with enhanced sensitivity and specificity and is applicable to nucleic acid from CTCs or other sample types, such as blood plasma from ctDNA. We believe the Target-Selector technology could someday be used as a stand-alone test for molecular biomarker screening and monitoring.

At our corporate headquarters facility located in San Diego, California, we operate a clinical laboratory that is certified under the Clinical Laboratory Improvement Amendments of 1988 (“CLIA”) and accredited by the College of American Pathologists (“CAP”). We manufacture our CEE microfluidic channels, related equipment and certain reagents to perform our current assays and our planned future assays at this facility. CLIA certification is required before any clinical laboratory, including ours, may perform testing on human specimens for the purpose of obtaining information for the diagnosis, prevention, or treatment of disease or the assessment of health. The assays we offer and intend to offer are classified as laboratory developed tests under CLIA regulations.

Risks That We Face

An investment in our common stock involves a high degree of risk. You should carefully consider the risks summarized below. The risks are discussed more fully in the “Risk Factors” section of this prospectus immediately following this prospectus summary. These risks include, but are not limited to, the following:

|

|

· |

we are an early-stage company with a history of substantial net losses. We have never been profitable and we have an accumulated deficit of approximately $150.6 million (as of September 30, 2015); |

|

|

· |

we expect to incur net losses in the future, and we may never achieve sustained profitability; |

|

|

· |

our business depends upon our ability to introduce additional tests and increase sales of our cancer diagnostic test; |

|

|

· |

our business depends on executing on our sales and marketing strategy for our cancer diagnostic tests and gaining acceptance of our current tests and future tests in the market; |

|

|

· |

our business depends on our ability to continually develop new cancer diagnostic tests and enhance our current tests and future tests; |

|

|

· |

our business depends on being able to obtain coverage and adequate reimbursement from governmental and other third-party payors for tests and services; |

|

|

· |

our business depends on satisfying any applicable United States (including FDA) and international regulatory requirements with respect to tests and services; and many of these requirements are new and still evolving; |

|

|

· |

our business depends on our ability to effectively compete with other diagnostic tests, methods and services that now exist or may hereafter be developed; |

|

|

· |

we depend on our senior management and in August 2013 we hired a new chief executive officer; |

-2-

|

|

· |

we depend on our ability to attract and retain scientists, clinicians and sales personnel with extensive experience in oncology, who are in short supply; and |

|

|

· |

we need to obtain or maintain patents or other appropriate protection for the intellectual property utilized in our current and planned tests and services, and we must avoid infringement of third-party intellectual property. |

Company Information

We maintain our principal executive offices at 5810 Nancy Ridge Drive, San Diego, California 92121. Our telephone number is (858) 320-8200 and our website address is www.biocept.com. The information contained in, or that can be accessed through, our website is not incorporated into and is not part of this prospectus. We were incorporated in California on May 12, 1997 and reincorporated as a Delaware corporation on July 30, 2013.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act, or JOBS Act, enacted in April 2012. An “emerging growth company” may take advantage of reduced reporting requirements that are otherwise applicable to public companies. These provisions include, but are not limited to:

|

|

· |

being permitted to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this prospectus; |

|

|

· |

not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act; |

|

|

· |

reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements; and |

|

|

· |

exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

We may take advantage of these provisions until December 31, 2019. However, if certain events occur prior to December 31, 2019, including if we become a “large accelerated filer,” our annual gross revenues exceed $1.0 billion or we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company before such date.

We have elected to take advantage of certain of the reduced disclosure obligations and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than the information you might receive from other public reporting companies in which you hold equity interests.

-3-

|

Common stock being offered by the selling stockholder |

3,774,122 shares |

|

|

|

|

Common stock outstanding |

18,880,054 (as of December 17, 2015) |

|

|

|

|

Use of proceeds |

The selling stockholder will receive all of the proceeds from the sale of the shares offered for sale by it under this prospectus. We will not receive proceeds from the sale of the shares by the selling stockholder. However, we may receive up to $15 million in proceeds from the sale of our common stock to the selling stockholder under the common stock purchase agreement described below. Any proceeds from the selling stockholder that we receive under the purchase agreement are expected be used for working capital and general corporate purposes. |

|

|

|

|

NASDAQ Capital Market Symbol |

BIOC |

|

|

|

|

Risk Factors |

Investing in our securities involves a high degree of risk. You should carefully review and consider the “Risk Factors” section of this prospectus for a discussion of factors to consider before deciding to invest in shares of our common stock. |

On December 21, 2015, we entered into a common stock purchase agreement (referred to in this prospectus as the “Purchase Agreement”), with Aspire Capital Fund, LLC, an Illinois limited liability company (referred to in this prospectus as “Aspire Capital” or the “selling stockholder”), which provides that, upon the terms and subject to the conditions and limitations set forth therein, Aspire Capital is committed to purchase up to an aggregate of $15 million of our shares of common stock over the approximately 30-month term of the Purchase Agreement. In consideration for entering into the Purchase Agreement, concurrently with the execution of the Purchase Agreement, we issued to Aspire Capital 165,000 shares of our common stock as a commitment fee (referred to in this prospectus as the “Commitment Shares”). Upon execution of the Purchase Agreement, the Company agreed to sell to Aspire Capital 625,000 shares of common stock at $1.60 per share for proceeds of $1,000,000 (referred to in this prospectus as the “Initial Purchase Shares”). Concurrently with entering into the Purchase Agreement, we also entered into a registration rights agreement with Aspire Capital (referred to in this prospectus as the “Registration Rights Agreement”), in which we agreed to file one or more registration statements, including the registration statement of which this prospectus is a part, as permissible and necessary to register under the Securities Act of 1933, as amended, or the Securities Act, the sale of the shares of our common stock that have been and may be issued to Aspire Capital under the Purchase Agreement.

As of December 17, 2015, there were 18,880,054 shares of our common stock outstanding (16,480,183 shares held by non-affiliates) excluding the 3,774,122 shares offered that have been issued or may be issuable to Aspire Capital pursuant to the Purchase Agreement. If all of such 3,774,122 shares of our common stock offered hereby were issued and outstanding as of the date hereof, such shares would represent 19.99% of the total common stock outstanding or 22.90% of the non-affiliate shares of common stock outstanding as of the date hereof. The number of shares of our common stock ultimately offered for sale by Aspire Capital is dependent upon the number of shares purchased by Aspire Capital under the Purchase Agreement.

Pursuant to the Purchase Agreement and the Registration Rights Agreement, we are registering 3,774,122 shares of our common stock under the Securities Act, which includes the Commitment Shares and the Initial Purchase Shares that have already been issued to Aspire Capital and 2,984,122 shares of common stock which we may issue to Aspire Capital after this registration statement is declared effective under the Securities Act, such shares together with the Initial Purchase Shares. All 3,774,122 shares of common stock are being offered pursuant to this prospectus.

After the Securities and Exchange Commission has declared effective the registration statement of which this prospectus is a part, on any trading day on which the closing sale price of our common stock exceeds $0.50, we have the right, in our sole discretion, to present Aspire Capital with a purchase notice (each, a “Purchase Notice”), directing Aspire Capital (as principal) to purchase up to 100,000 shares of our common stock per trading day, up to $15 million of our common stock in the aggregate at a per share price (the “Purchase Price”) calculated by reference to the prevailing market price of our common stock (as more specifically described below).

In addition, on any date on which we submit a Purchase Notice for 100,000 shares to Aspire Capital and the closing sale price of our stock is equal to or greater than $0.50 per share of Common Stock , we also have the right, in our sole discretion, to present Aspire Capital with a volume-weighted average price purchase notice (each, a “VWAP Purchase Notice”) directing Aspire Capital to purchase an amount of stock equal to up to 30% of the aggregate shares of the Company’s common stock traded on the Nasdaq

-4-

Capital Market on the next trading day (the “VWAP Purchase Date”), subject to a maximum number of shares we may determine (the “VWAP Purchase Share Volume Maximum”) and a minimum trading price (the “VWAP Minimum Price Threshold”) (as more specifically described below). The purchase price per Purchase Share pursuant to such VWAP Purchase Notice (the “VWAP Purchase Price”) is calculated by reference to the prevailing market price of our common stock (as more specifically described below).

The Purchase Agreement provides that the Company and Aspire Capital shall not effect any sales under the Purchase Agreement on any purchase date where the closing sale price of our common stock is less than $0.50 per share (the “Floor Price”). This Floor Price and the respective prices and share numbers in the preceding paragraphs shall be appropriately adjusted for any reorganization, recapitalization, non-cash dividend, stock split, reverse stock split or other similar transaction. There are no trading volume requirements or restrictions under the Purchase Agreement, and we will control the timing and amount of any sales of our common stock to Aspire Capital. Aspire Capital has no right to require any sales by us, but is obligated to make purchases from us as we direct in accordance with the Purchase Agreement. There are no limitations on use of proceeds, financial or business covenants, restrictions on future fundings, rights of first refusal, participation rights, penalties or liquidated damages in the Purchase Agreement. Aspire Capital may not assign its rights or obligations under the Purchase Agreement. The Purchase Agreement may be terminated by us at any time, at our discretion, without any penalty or cost to us.

-5-

You should carefully consider the following information about risks, together with the other information contained in this prospectus, before making an investment in our common stock. If any of the circumstances or events described below actually arises or occurs, our business, results of operations, cash flows and financial condition could be harmed. In any such case, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to Our Financial Condition and Capital Requirements

We are an early-stage company with a history of net losses; we expect to incur net losses in the future, and we may never achieve sustained profitability.

We have historically incurred substantial net losses, including net losses of $9.2 million and $15.9 million for the years ended December 31, 2013 and 2014, respectively, and we have never been profitable. At December 31, 2014, our accumulated deficit was approximately $138.3 million. Before 2008, we were pursuing a business plan relating to fetal genetic disorders and other fields, all of which were unrelated to cancer diagnostics. The portion of our accumulated deficit that relates to the period from inception through December 31, 2007 is approximately $66.5 million.

We expect our losses to continue as a result of costs relating to our lab operations as well as increased sales and marketing costs and ongoing research and development expenses. These losses have had, and will continue to have, an adverse effect on our working capital, total assets and stockholders’ equity. Because of the numerous risks and uncertainties associated with our commercialization efforts, we are unable to predict when we will become profitable, and we may never become profitable. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. Our inability to achieve and then maintain profitability would negatively affect our business, financial condition, results of operations and cash flows. Our chief executive officer Michael W. Nall, who joined us in August 2013, has not previously been the chief executive officer of a public or private company, and therefore his lack of experience may result in some of his time being spent acclimating to his new position and responsibilities. A lack of significant experience in being the chief executive officer of a public company could have an adverse effect on his ability to quickly respond to problems or effectively manage issues surrounding the operation of a public company.

We need to raise additional capital to continue as a going concern.

We expect to continue to incur losses for the foreseeable future and will have to raise additional capital to fund our planned operations and to meet our long-term business objectives. As a result, there is substantial doubt about our ability to continue as a going concern unless we are able to successfully raise additional capital. Until we can generate significant cash from operations, including assay revenues, we expect to continue to fund our operations with the proceeds from offerings of our equity securities or debt, or transactions involving product development, technology licensing or collaboration. We can provide no assurances that any sources of a sufficient amount of financing will be available to us on favorable terms, if at all. Failure to raise additional capital in sufficient amounts would significantly impact our ability to continue as a going concern. The actual amount of funds that we will need and the timing of any such investment will be determined by many factors, some of which are beyond our control.

Risks Relating to Our Business and Strategy

If we are unable to increase sales of our OncoCEE diagnostic tests or successfully develop and commercialize other tests, our revenues will be insufficient for us to achieve profitability.

We currently derive substantially all of our revenues from sales of cancer diagnostic tests. We recently began offering our OncoCEE cancer tests through our CLIA-certified, CAP accredited, and state-licensed laboratory. We are in varying stages of research and development for other cancer diagnostic tests that we may offer. If we are unable to increase sales of our OncoCEE-BR for breast cancer, OncoCEE-LU for NSCLC and OncoCEE-GA for gastric cancer diagnostic test or successfully develop and commercialize other cancer diagnostic tests, we will not produce sufficient revenues to become profitable.

If we are unable to execute our sales and marketing strategy for cancer diagnostic tests and are unable to gain acceptance in the market, we may be unable to generate sufficient revenue to sustain our business.

We are an early-stage company and have engaged in only limited sales and marketing activities for the OncoCEE-BR for breast cancer, OncoCEE-LU for NSCLC and OncoCEE-GA for gastric cancer diagnostic tests we offer through our CLIA-certified, CAP accredited, and state-licensed laboratory. To date, we have received very limited revenue.

Although we believe that our current tests and our planned diagnostic tests represent a promising commercial opportunity, our tests may never gain significant acceptance in the marketplace and therefore may never generate substantial revenue or profits for

-6-

us. We will need to establish a market for our cancer diagnostic tests and build that market through physician education, awareness programs and the publication of clinical trial results. Gaining acceptance in medical communities requires, among other things, publication in leading peer-reviewed journals of results from studies using our current tests and/or our planned cancer tests. The process of publication in leading medical journals is subject to a peer review process and peer reviewers may not consider the results of our studies sufficiently novel or worthy of publication. Failure to have our studies published in peer-reviewed journals would limit the adoption of our current tests and our planned tests.

Our ability to successfully market the cancer diagnostic tests that we may develop will depend on numerous factors, including:

|

· |

conducting clinical utility studies of such tests in collaboration with key thought leaders to demonstrate their use and value in important medical decisions such as treatment selection; |

|

· |

whether our current or future partners, vigorously support our offerings; |

|

· |

the success of our sales force; |

|

· |

whether healthcare providers believe such diagnostic tests provide clinical utility; |

|

· |

whether the medical community accepts that such diagnostic tests are sufficiently sensitive and specific to be meaningful in patient care and treatment decisions; and |

|

· |

whether private health insurers, government health programs and other third-party payors will cover such cancer diagnostic tests and, if so, whether they will adequately reimburse us. |

Failure to achieve widespread market acceptance of our current tests and our planned cancer diagnostic tests would materially harm our business, financial condition and results of operations.

If we cannot develop tests to keep pace with rapid advances in technology, medicine and science, our operating results and competitive position could be harmed.

In recent years, there have been numerous advances in technologies relating to the diagnosis and treatment of cancer. Several new cancer drugs have been approved, and a number of new drugs in clinical development may increase patient survival time. There have also been advances in methods used to identify patients likely to benefit from these drugs based on analysis of biomarkers. We must continuously develop new cancer diagnostic tests and enhance any existing tests to keep pace with evolving standards of care. Our current tests and our planned tests could become obsolete unless we continually innovate and expand them to demonstrate benefit in the diagnosis, monitoring or prognosis of patients with cancer. New cancer therapies typically have only a few years of clinical data associated with them, which limits our ability to develop cancer diagnostic tests based on, for example, biomarker analysis related to the appearance or development of resistance to those therapies. If we cannot adequately demonstrate the applicability of our current tests and our planned tests to new treatments, by incorporating important biomarker analysis, sales of our tests could decline, which would have a material adverse effect on our business, financial condition and results of operations.

If our current tests and our planned tests do not continue to perform as expected, our operating results, reputation and business will suffer.

Our success depends on the market’s confidence that we can continue to provide reliable, high-quality diagnostic results. We believe that our customers are likely to be particularly sensitive to test defects and errors. As a result, the failure of our current or planned tests to perform as expected would significantly impair our reputation and the public image of our cancer tests, and we may be subject to legal claims arising from any defects or errors.

If our sole laboratory facility becomes damaged or inoperable, or we are required to vacate the facility, our ability to sell and provide cancer diagnostic tests and pursue our research and development efforts may be jeopardized.

We currently derive our revenues from our OncoCEE-BR for breast cancer, OncoCEE-LU for NSCLC and OncoCEE-GA for gastric cancer diagnostic tests conducted in our CLIA-certified, CAP accredited, and state-licensed laboratory. We do not have any clinical reference laboratory facilities other than our facility in San Diego, California. Our facilities and equipment could be harmed or rendered inoperable by natural or man-made disasters, including fire, earthquake, flooding and power outages, which may render it difficult or impossible for us to perform our diagnostic tests for some period of time. The inability to perform our current tests and our planned tests or the backlog of tests that could develop if our facility is inoperable for even a short period of time may result in the loss of customers or harm to our reputation or relationships with scientific or clinical collaborators, and we may be unable to regain those

-7-

customers or repair our reputation in the future. Furthermore, our facilities and the equipment we use to perform our research and development work could be costly and time-consuming to repair or replace.

The San Diego area has recently experienced serious fires and power outages, and is considered to lie in an area with earthquake risk.

Additionally, a key component of our research and development process involves using biological samples as the basis for our diagnostic test development. In some cases, these samples are difficult to obtain. If the parts of our laboratory facility where we store these biological samples were damaged or compromised, our ability to pursue our research and development projects, as well as our reputation, could be jeopardized. We carry insurance for damage to our property and the disruption of our business, but this insurance may not be sufficient to cover all of our potential losses and may not continue to be available to us on acceptable terms, if at all.

Further, if our CLIA-certified, CAP accredited, and state-licensed laboratory became inoperable we may not be able to license or transfer our technology to another facility with the necessary qualifications, including state licensure and CLIA certification, under the scope of which our current tests and our planned cancer diagnostic tests could be performed. Even if we find a facility with such qualifications to perform our tests, it may not be available to us on commercially reasonable terms.

If we cannot compete successfully with our competitors, we may be unable to increase or sustain our revenues or achieve and sustain profitability.

Our principal competition comes from mainstream diagnostic methods, used by pathologists and oncologists and other physicians for many years, which focus on tumor tissue analysis. It may be difficult to change the methods or behavior of oncologists and other physicians to incorporate our CTC and ctDNA testing, including molecular diagnostic testing, in their practices in conjunction with or instead of tissue biopsies and analysis. In addition, companies offering capital equipment and kits or reagents to local pathology laboratories represent another source of potential competition. These kits are used directly by the pathologist, which can facilitate adoption. We plan to focus our marketing and sales efforts on medical oncologists rather than pathologists.

We also face competition from companies that offer products or are conducting research to develop products for CTC or ctDNA testing in various cancers. In particular, Janssen Diagnostics, LLC markets its CellSearch® test and Atossa Genetics markets its ArgusCYTE® test, which are competitive to our tests for CTC enumeration and HER2 analysis. CTC and ctDNA testing is a new area of science and we cannot predict what tests others will develop that may compete with or provide results similar or superior to the results we are able to achieve with the tests we develop. In addition to Janssen Diagnostics and Atossa Genetics, our competitors also include public companies such as Alere (Adnagen) and Illumina as well as many private companies, including Apocell, EPIC Sciences, Clearbridge Biomedics, Cynvenio Biosystems, Fluxion Biosciences, Guardant Health, RareCells and Silicon Biosystems. Many of these groups, in addition to operating research and development laboratories, are establishing CLIA-certified testing laboratories while others are focused on selling equipment and reagents. Our sales and distribution agreements are non-exclusive and our partners could enter into agreements with competitors.

We expect that pharmaceutical and biopharmaceutical companies will increasingly focus attention and resources on the personalized cancer diagnostic sector as the potential and prevalence of molecularly targeted oncology therapies approved by the FDA along with companion diagnostics increases. For example, the FDA has recently approved two such agents—Xalkori® from Pfizer Inc. along with its companion anaplastic lymphoma kinase FISH test from Abbott Laboratories, Inc., Zelboraf® from Daiichi-Sankyo/Genentech/Roche along with its companion B-raf kinase V600 mutation test from Roche Molecular Systems, Inc. and Tafinlar® from GlaxoSmithKline along with its companion B-raf kinase V600 mutation test from bioMerieux. These recent FDA approvals are only the second, third and fourth instances of simultaneous approvals of a drug and companion diagnostic, the first being the 2010 approval of Genentech’s Herceptin® for HER2 positive breast cancer along with the HercepTest from partner Dako A/S. Our competitors may invent and commercialize technology platforms or tests that compete with ours.

There are a number of companies which are focused on the oncology diagnostic market, such as Biodesix, Caris, Clarient, Foundation Medicine, Neogenomics, Response Genetics, Agendia, Genomic Health, and Genoptix, who while not currently offering CTC or ctDNA tests are selling to the medical oncologists and pathologists and could develop or offer CTC or ctDNA tests. Large laboratory services companies, such as Sonic USA, Quest and LabCorp, provide more generalized cancer diagnostic testing.

Additionally, projects related to cancer diagnostics and particularly genomics have received increased government funding, both in the United States and internationally. As more information regarding cancer genomics becomes available to the public, we anticipate that more products aimed at identifying targeted treatment options will be developed and that these products may compete with ours. In addition, competitors may develop their own versions of our current or planned tests in countries where we did not apply

-8-

for patents or where our patents have not issued and compete with us in those countries, including encouraging the use of their test by physicians or patients in other countries.

Some of our present and potential competitors have widespread brand recognition and substantially greater financial and technical resources and development, production and marketing capabilities than we do. Others may develop lower-priced, less complex tests that payors, pathologists and oncologists and other physicians could view as functionally equivalent to our current or planned tests, which could force us to lower the list price of our tests and impact our operating margins and our ability to achieve and maintain profitability. In addition, technological innovations that result in the creation of enhanced diagnostic tools that are more sensitive or specific than ours may enable other clinical laboratories, hospitals, physicians or medical providers to provide specialized diagnostic tests similar to ours in a more patient-friendly, efficient or cost-effective manner than is currently possible. If we cannot compete successfully against current or future competitors, we may be unable to increase or create market acceptance and sales of our current or planned tests, which could prevent us from increasing or sustaining our revenues or achieving or sustaining profitability.

We expect to continue to incur significant expenses to develop and market cancer diagnostic tests, which could make it difficult for us to achieve and sustain profitability.

In recent years, we have incurred significant costs in connection with the development of cancer diagnostic tests. For the year ended December 31, 2013, our research and development expenses were $3.1 million and our sales and marketing expenses were $0.1 million. For the year ended December 31, 2014, our research and development expenses were $4.5 million and our sales and marketing expenses were $2.1 million. We expect our expenses to continue to increase for the foreseeable future as we conduct studies of our current tests and our planned cancer diagnostic tests, establish a sales and marketing organization, drive adoption of and reimbursement for our diagnostic tests and develop new tests. As a result, we need to generate significant revenues in order to achieve sustained profitability.

If oncologists and other physicians decide not to order our OncoCEE cancer diagnostic tests or our future cancer diagnostic tests, we may be unable to generate sufficient revenue to sustain our business.

To generate demand for our current tests and our planned cancer diagnostic tests, we will need to educate oncologists, pathologists, and other health care professionals on the clinical utility, benefits and value of the tests we provide through published papers, presentations at scientific conferences, educational programs and one-on-one education sessions by members of our sales force. In addition, we need to assure oncologists and other physicians of our ability to obtain and maintain coverage and adequate from third-party payors. We need to hire additional commercial, scientific, technical and other personnel to support this process. Unless an adequate number of medical practitioners order our current tests and our planned tests, we will likely be unable to create demand in sufficient volume for us to achieve sustained profitability.

Clinical utility studies are important in demonstrating to both customers and payors a test’s clinical relevance and value. If we are unable to identify collaborators willing to work with us to conduct clinical utility studies, or the results of those studies do not demonstrate that a test provides clinically meaningful information and value, commercial adoption of such test may be slow, which would negatively impact our business.

Clinical utility studies show when and how to use a clinical test, and describe the particular clinical situations or settings in which it can be applied and the expected results. Clinical utility studies also show the impact of the test results on patient care and management. Clinical utility studies are typically performed with collaborating oncologists or other physicians at medical centers and hospitals, analogous to a clinical trial, and generally result in peer-reviewed publications. Sales and marketing representatives use these publications to demonstrate to customers how to use a clinical test, as well as why they should use it. These publications are also used with payors to obtain coverage for a test, helping to assure there is appropriate reimbursement.

Our OncoCEE-BR test is currently part of a clinical utility study led by investigators at the Dana-Farber Cancer Institute. We will need to conduct additional studies for this test, as well as other CTC and ctDNA tests we plan to introduce, to increase test adoption in the marketplace and obtain coverage and adequate reimbursement. Should we not be able to perform these studies, or should their results not provide clinically meaningful data and value for oncologists and other physicians, adoption of our tests could be impaired and we may not be able to obtain coverage and adequate reimbursement for them.

We are undergoing a management transition.

Until August 26, 2013, David F. Hale, our Chairman, served as our principal executive officer. On that date, Michael W. Nall began his employment with us as our Chief Executive Officer and President, with David F. Hale remaining employed as our Executive Chairman until February 10, 2014. Mr. Hale currently serves as non-Executive Chairman of our Board of Directors. We intend to recruit and hire other senior executives, including our recent hiring of Mark Foletta as our interim Chief Financial Officer. Such a

-9-

management transition subjects us to a number of risks, including risks pertaining to coordination of responsibilities and tasks, creation of new management systems and processes, differences in management style, effects on corporate culture, and the need for transfer of historical knowledge. In addition, Mr. Nall has not previously been the chief executive officer of a public or private company, and therefore his lack of experience may result in some of his time being spent acclimating to his new position and responsibilities. A lack of significant experience in being the chief executive officer of a public company could have an adverse effect on his ability to quickly respond to problems or effectively manage issues surrounding the operation of a public company.

The loss of key members of our executive management team could adversely affect our business.

Our success in implementing our business strategy depends largely on the skills, experience and performance of key members of our executive management team and others in key management positions, including Michael W. Nall, our Chief Executive Officer and President, Lyle J. Arnold, Ph.D., our Senior Vice-President of Research & Development and Chief Scientific Officer, and Veena M. Singh, M.D., our Senior Vice President and Senior Medical Director, Mark G. Foletta, our Chief Financial Officer and Raaj Trivedi, Vice President, Commercial Operations. The collective efforts of each of these persons and others working with them as a team are critical to us as we continue to develop our technologies, tests and research and development and sales programs. As a result of the difficulty in locating qualified new management, the loss or incapacity of existing members of our executive management team could adversely affect our operations. If we were to lose one or more of these key employees, we could experience difficulties in finding qualified successors, competing effectively, developing our technologies and implementing our business strategy. Our Chief Executive Officer and President, Chief Financial Officer, Chief Scientific Officer, Vice President, Commercial Operations and Senior Medical Director have employment agreements, however, the existence of an employment agreement does not guarantee retention of members of our executive management team and we may not be able to retain those individuals for the duration of or beyond the end of their respective terms. We do not maintain “key person” life insurance on any of our employees.

In addition, we rely on collaborators, consultants and advisors, including scientific and clinical advisors, to assist us in formulating our research and development and commercialization strategy. Our collaborators, consultants and advisors are generally employed by employers other than us and may have commitments under agreements with other entities that may limit their availability to us.

The loss of a key employee, the failure of a key employee to perform in his or her current position or our inability to attract and retain skilled employees could result in our inability to continue to grow our business or to implement our business strategy.

There is a scarcity of experienced professionals in our industry. If we are not able to retain and recruit personnel with the requisite technical skills, we may be unable to successfully execute our business strategy.

The specialized nature of our industry results in an inherent scarcity of experienced personnel in the field. Our future success depends upon our ability to attract and retain highly skilled personnel, including scientific, technical, commercial, business, regulatory and administrative personnel, necessary to support our anticipated growth, develop our business and perform certain contractual obligations. Given the scarcity of professionals with the scientific knowledge that we require and the competition for qualified personnel among life science businesses, we may not succeed in attracting or retaining the personnel we require to continue and grow our operations.

Our failure to continue to attract, hire and retain a sufficient number of qualified sales professionals would hamper our ability to increase demand for our cancer diagnostic test, to expand geographically and to successfully commercialize any other tests or products we may develop.

To succeed in selling our diagnostic tests and any other tests or products that we are able to develop, we must expand our sales force in the United States and/or internationally by recruiting additional sales representatives with extensive experience in oncology and established relationships with medical oncologists, surgeons, oncology nurses, pathologists and other hospital personnel. To achieve our marketing and sales goals, we will need to continue to build our sales and commercial infrastructure, with which to date we have had limited experience. Sales professionals with the necessary technical and business qualifications are in high demand, and there is a risk that we may be unable to attract, hire and retain the number of sales professionals with the right qualifications, scientific backgrounds and relationships with decision-makers at potential customers needed to achieve our sales goals. We expect to face competition from other companies in our industry, some of whom are much larger than us and who can pay greater compensation and benefits than we can, in seeking to attract and retain qualified sales and marketing employees. If we are unable to hire and retain qualified sales and marketing personnel, our business will suffer.

-10-

Our dependence on commercialization partners for sales of tests could limit our success in realizing revenue growth.

We intend to grow our business through the use of commercialization partners for the sales, marketing and commercialization of our current tests and our planned future tests, and to do so we must enter into agreements with these partners to sell, market or commercialize our tests. These agreements may contain exclusivity provisions and generally cannot be terminated without cause during the term of the agreement. We may need to attract additional partners to expand the markets in which we sell tests. These partners may not commit the necessary resources to market and sell our cancer diagnostics tests to the level of our expectations, and we may be unable to locate suitable alternatives should we terminate our agreement with such partners or if such partners terminate their agreement with us.

Any relationships we form with commercialization partners are subject to change over time. For example, over 75% of our revenue in 2012 was generated through our arrangement with Clarient, but Clarient is no longer marketing the OncoCEE-BR test as actively as before. In May 2013, we amended our commercialization agreement with Clarient such that Clarient is no longer the exclusive marketer of the OncoCEE-BR test. In 2013 and 2014, only 10% and 6%, respectively, of our revenues were generated through our arrangement with Clarient, and we expect that in the future the percentage of our revenue which is generated through our arrangement with Clarient will diminish further. If we cannot replace any diminution in revenues we receive through Clarient, our results will be weakened.

If current or future commercialization partners do not perform adequately, or we are unable to locate commercialization partners, we may not realize revenue growth.

We depend on third parties for the supply of blood samples and other biological materials that we use in our research and development efforts. If the costs of such samples and materials increase or our third party suppliers terminate their relationship with us, our business may be materially harmed.

We have relationships with suppliers and institutions that provide us with blood samples and other biological materials that we use in developing and validating our current tests and our planned future tests. If one or more suppliers terminate their relationship with us or are unable to meet our requirements for samples, we will need to identify other third parties to provide us with blood samples and biological materials, which could result in a delay in our research and development activities and negatively affect our business. In addition, as we grow, our research and academic institution collaborators may seek additional financial contributions from us, which may negatively affect our results of operations.

We currently rely on third-party suppliers for critical materials needed to perform our current tests and our planned future tests and any problems experienced by them could result in a delay or interruption of their supply to us.

We currently purchase raw materials for our microfluidic channels and testing reagents under purchase orders and do not have long-term contracts with most of the suppliers of these materials. If suppliers were to delay or stop producing our materials or reagents, or if the prices they charge us were to increase significantly, or if they elected not to sell to us, we would need to identify other suppliers. We could experience delays in manufacturing the microfluidic channels or performing tests while finding another acceptable supplier, which could impact our results of operations. The changes could also result in increased costs associated with qualifying the new materials or reagents and in increased operating costs. Further, any prolonged disruption in a supplier’s operations could have a significant negative impact on our ability to perform cancer diagnostic tests in a timely manner.

Some of the components used in our current or planned products are currently sole-source, and substitutes for these components might not be able to be obtained easily or may require substantial design or manufacturing modifications. Any significant problem experienced by one of our sole source suppliers may result in a delay or interruption in the supply of components to us until that supplier cures the problem or an alternative source of the component is located and qualified. Any delay or interruption would likely lead to a delay or interruption in our manufacturing operations. The inclusion of substitute components must meet our product specifications and could require us to qualify the new supplier with the appropriate government regulatory authorities.

If we were sued for product liability or professional liability, we could face substantial liabilities that exceed our resources.

The marketing, sale and use of our current tests and our planned future diagnostic tests could lead to the filing of product liability claims against us if someone alleges that our tests failed to perform as designed. We may also be subject to liability for errors in the test results we provide to physicians or for a misunderstanding of, or inappropriate reliance upon, the information we provide. A product liability or professional liability claim could result in substantial damages and be costly and time-consuming for us to defend.

Although we believe that our existing product and professional liability insurance is adequate, our insurance may not fully protect us from the financial impact of defending against product liability or professional liability claims. Any product liability or

-11-

professional liability claim brought against us, with or without merit, could increase our insurance rates or prevent us from securing insurance coverage in the future. Additionally, any product liability lawsuit could damage our reputation, result in the recall of tests, or cause current partners to terminate existing agreements and potential partners to seek other partners, any of which could impact our results of operations.

If we use biological and hazardous materials in a manner that causes injury, we could be liable for damages.

Our activities currently require the controlled use of potentially harmful biological materials and chemicals. We cannot eliminate the risk of accidental contamination or injury to employees or third parties from the use, storage, handling or disposal of these materials. In the event of contamination or injury, we could be held liable for any resulting damages, and any liability could exceed our resources or any applicable insurance coverage we may have. Additionally, we are subject to, on an ongoing basis, federal, state and local laws and regulations governing the use, storage, handling and disposal of these materials and specified waste products. The cost of compliance with these laws and regulations may become significant and could have a material adverse effect on our financial condition, results of operations and cash flows. In the event of an accident or if we otherwise fail to comply with applicable regulations, we could lose our permits or approvals or be held liable for damages or penalized with fines.

We may acquire other businesses or form joint ventures or make investments in other companies or technologies that could harm our operating results, dilute our stockholders’ ownership, increase our debt or cause us to incur significant expense.

As part of our business strategy, we may pursue acquisitions of businesses and assets. We also may pursue strategic alliances and joint ventures that leverage our core technology and industry experience to expand our offerings or distribution. We have no experience with acquiring other companies and limited experience with forming strategic alliances and joint ventures. We may not be able to find suitable partners or acquisition candidates, and we may not be able to complete such transactions on favorable terms, if at all. If we make any acquisitions, we may not be able to integrate these acquisitions successfully into our existing business, and we could assume unknown or contingent liabilities. Any future acquisitions also could result in significant write-offs or the incurrence of debt and contingent liabilities, any of which could have a material adverse effect on our financial condition, results of operations and cash flows. Integration of an acquired company also may disrupt ongoing operations and require management resources that would otherwise focus on developing our existing business. We may experience losses related to investments in other companies, which could have a material negative effect on our results of operations. We may not identify or complete these transactions in a timely manner, on a cost-effective basis, or at all, and we may not realize the anticipated benefits of any acquisition, technology license, strategic alliance or joint venture.

To finance any acquisitions or joint ventures, we may choose to issue shares of our common stock as consideration, which would dilute the ownership of our stockholders. If the price of our common stock is low or volatile, we may not be able to acquire other companies or fund a joint venture project using our stock as consideration. Alternatively, it may be necessary for us to raise additional funds for acquisitions through public or private financings. Additional funds may not be available on terms that are favorable to us, or at all.

If we cannot support demand for our current tests and our planned future diagnostic tests, including successfully managing the evolution of our technology and manufacturing platforms, our business could suffer.

As our test volume grows, we will need to increase our testing capacity, implement automation, increase our scale and related processing, customer service, billing, collection and systems process improvements and expand our internal quality assurance program and technology to support testing on a larger scale. We will also need additional clinical laboratory scientists and other scientific and technical personnel to process these additional tests. Any increases in scale, related improvements and quality assurance may not be successfully implemented and appropriate personnel may not be available. As additional tests are commercialized, we may need to bring new equipment on line, implement new systems, technology, controls and procedures and hire personnel with different qualifications. Failure to implement necessary procedures or to hire the necessary personnel could result in a higher cost of processing or an inability to meet market demand. We cannot assure you that we will be able to perform tests on a timely basis at a level consistent with demand, that our efforts to scale our commercial operations will not negatively affect the quality of our test results or that we will respond successfully to the growing complexity of our testing operations. If we encounter difficulty meeting market demand or quality standards for our current tests and our planned future tests, our reputation could be harmed and our future prospects and business could suffer, which may have a material adverse effect on our financial condition, results of operations and cash flows.

We may encounter manufacturing problems or delays that could result in lost revenue.

We currently manufacture our proprietary microfluidic channels at our San Diego facility and intend to continue to do so. We believe we currently have adequate manufacturing capacity for our microfluidic channels. If demand for our current tests and our planned future tests increases significantly, we will need to either expand our manufacturing capabilities or outsource to other

-12-

manufacturers. If we or third party manufacturers engaged by us fail to manufacture and deliver our microfluidic channels or certain reagents in a timely manner, our relationships with our customers could be seriously harmed. We cannot assure you that manufacturing or quality control problems will not arise as we attempt to increase the production of our microfluidic channels or reagents or that we can increase our manufacturing capabilities and maintain quality control in a timely manner or at commercially reasonable costs. If we cannot manufacture our microfluidic channels consistently on a timely basis because of these or other factors, it could have a significant negative impact on our ability to perform tests and generate revenues.

International expansion of our business would expose us to business, regulatory, political, operational, financial and economic risks associated with doing business outside of the United States.

Our business strategy contemplates possible international expansion, including partnering with academic and commercial testing laboratories, and introducing OncoCEE technology outside the United States as part of CE-marked IVD test kits and/or testing systems utilizing our CEE and/or CEE-Selector technologies. Doing business internationally involves a number of risks, including:

|

· |

multiple, conflicting and changing laws and regulations such as tax laws, export and import restrictions, employment laws, regulatory requirements and other governmental approvals, permits and licenses; |

|

· |

failure by us or our distributors to obtain regulatory approvals for the sale or use of our current tests and our planned future tests in various countries; |

|

· |

difficulties in managing foreign operations; |

|

· |

complexities associated with managing government payor systems, multiple payor-reimbursement regimes or self-pay systems; |

|

· |

logistics and regulations associated with shipping blood samples, including infrastructure conditions and transportation delays; |

|

· |

limits on our ability to penetrate international markets if our current tests and our planned future diagnostic tests cannot be processed by an appropriately qualified local laboratory; |

|

· |

financial risks, such as longer payment cycles, difficulty enforcing contracts and collecting accounts receivable and exposure to foreign currency exchange rate fluctuations; |

|

· |

reduced protection for intellectual property rights, or lack of them in certain jurisdictions, forcing more reliance on our trade secrets, if available; |

|

· |

natural disasters, political and economic instability, including wars, terrorism and political unrest, outbreak of disease, boycotts, curtailment of trade and other business restrictions; |

|

· |

failure to comply with the Foreign Corrupt Practices Act, including its books and records provisions and its anti-bribery provisions, by maintaining accurate information and control over sales activities and distributors’ activities; and |

|

· |

Any of these risks, if encountered, could significantly harm our future international expansion and operations and, consequently, have a material adverse effect on our financial condition, results of operations and cash flows. |

General economic or business conditions may have a negative impact on our business.

Continuing concerns over United States health care reform legislation and energy costs, geopolitical issues, the availability and cost of credit and government stimulus programs in the United States and other countries have contributed to increased volatility and diminished expectations for the global economy. These factors, combined with low business and consumer confidence and high unemployment, precipitated an economic slowdown and recession. If the economic climate does not improve, or it deteriorates, our business, including our access to patient samples and the addressable market for diagnostic tests that we may successfully develop, as well as the financial condition of our suppliers and our third-party payors, could be adversely affected, resulting in a negative impact on our business, financial condition and results of operations.

Intrusions into our computer systems could result in compromise of confidential information.

Despite the implementation of security measures, our technology or systems that we interface with, including the Internet and related systems, may be vulnerable to physical break-ins, hackers, improper employee or contractor access, computer viruses, programming errors, or similar problems. Any of these might result in confidential medical, business or other information of other persons or of ourselves being revealed to unauthorized persons.

-13-

There are a number of state, federal and international laws protecting the privacy and security of health information and personal data. As part of the American Recovery and Reinvestment Act of 2009, or ARRA, Congress amended the privacy and security provisions of the Health Insurance Portability and Accountability Act, or HIPAA. HIPAA imposes limitations on the use and disclosure of an individual’s healthcare information by healthcare providers, healthcare clearinghouses, and health insurance plans, collectively referred to as covered entities, and also grants individuals rights with respect to their health information. HIPAA also imposes compliance obligations and corresponding penalties for non-compliance on individuals and entities that provide services to healthcare providers and other covered entities, collectively referred to as business associates. ARRA also made significant increases in the penalties for improper use or disclosure of an individual’s health information under HIPAA and extended enforcement authority to state attorneys general. As amended by ARRA and subsequently by the final omnibus rule adopted in 2013, or Final Omnibus Rule, HIPAA also imposes notification requirements on covered entities in the event that certain health information has been inappropriately accessed or disclosed: notification requirements to individuals, federal regulators, and in some cases, notification to local and national media. Notification is not required under HIPAA if the health information that is improperly used or disclosed is deemed secured in accordance with encryption or other standards developed by the U.S. Department of Health and Human Services, or HHS. Most states have laws requiring notification of affected individuals and/or state regulators in the event of a breach of personal information, which is a broader class of information than the health information protected by HIPAA. Many state laws impose significant data security requirements, such as encryption or mandatory contractual terms to ensure ongoing protection of personal information. Activities outside of the United States implicate local and national data protection standards, impose additional compliance requirements and generate additional risks of enforcement for non-compliance. We may be required to expend significant capital and other resources to ensure ongoing compliance with applicable privacy and data security laws, to protect against security breaches and hackers or to alleviate problems caused by such breaches.

We depend on our information technology and telecommunications systems, and any failure of these systems could harm our business.

We depend on information technology and telecommunications systems for significant aspects of our operations. In addition, our third-party billing and collections provider depends upon telecommunications and data systems provided by outside vendors and information we provide on a regular basis. These information technology and telecommunications systems support a variety of functions, including test processing, sample tracking, quality control, customer service and support, billing and reimbursement, research and development activities and our general and administrative activities. Information technology and telecommunications systems are vulnerable to damage from a variety of sources, including telecommunications or network failures, malicious human acts and natural disasters. Moreover, despite network security and back-up measures, some of our servers are potentially vulnerable to physical or electronic break-ins, computer viruses and similar disruptive problems. Despite the precautionary measures we have taken to prevent unanticipated problems that could affect our information technology and telecommunications systems, failures or significant downtime of our information technology or telecommunications systems or those used by our third-party service providers could prevent us from processing tests, providing test results to oncologists, pathologists, billing payors, processing reimbursement appeals, handling patient or physician inquiries, conducting research and development activities and managing the administrative aspects of our business. Any disruption or loss of information technology or telecommunications systems on which critical aspects of our operations depend could have an adverse effect on our business.

Regulatory Risks Relating to Our Business

Healthcare policy changes, including recently enacted legislation reforming the U.S. health care system, may have a material adverse effect on our financial condition, results of operations and cash flows.

The Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act, or collectively the ACA, enacted in March 2010, makes a number of substantial changes in the way health care is financed by both governmental and private insurers. Among other things, the ACA:

|

· |

Mandates a reduction in payments for clinical laboratory services paid under the Medicare Clinical Laboratory Fee Schedule, or CLFS, annual Consumer Price Index update of 1.75% for the years 2011 through 2015. In addition, a multifactor productivity adjustment is made to the fee schedule payment amount, which could further reduce payment rates. These changes in payments may apply to some or all of the tests we furnish to Medicare beneficiaries. |

|

· |

Establishes an Independent Payment Advisory Board to reduce the per capita rate of growth in Medicare spending if spending exceeds a target growth rate. The Independent Payment Advisory Board has broad discretion to propose policies, which may have a negative impact on payment rates for services, including clinical laboratory services, beginning in 2016, and for hospital services beginning in 2020. |

-14-

|

diagnostic test or to our products that are in development; nevertheless, this could change in the future if either the FDA or the Internal Revenue Service, which regulates the payment of this excise tax, changes its position. |

Although some of these provisions may negatively impact payment rates for clinical laboratory tests, the ACA also extends coverage to over 30 million previously uninsured people, which may result in an increase in the demand for our current tests and our planned future cancer diagnostic tests. The mandatory purchase of insurance has been strenuously opposed by a number of state governors, resulting in lawsuits challenging the constitutionality of certain provisions of the ACA. In 2012, the Supreme Court upheld the constitutionality of the ACA, with the exception of certain provisions dealing with the expansion of Medicaid coverage under the law.