Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT - Shimmick Construction Company, Inc. | fs12015a2ex23i_shimmick.htm |

| EX-10.4 - COMMERCIAL SECURITY AGREEMENT - Shimmick Construction Company, Inc. | fs12015a2ex10iv_shimmick.htm |

| EX-23.4 - CONSENT - Shimmick Construction Company, Inc. | fs12015a2ex23iv_shimmick.htm |

| EX-23.2 - CONSENT - Shimmick Construction Company, Inc. | fs12015a2ex23ii_shimmick.htm |

| EX-10.3 - BUSINESS LOAN AGREEMENT - Shimmick Construction Company, Inc. | fs12015a2ex10iii_shimmick.htm |

As filed with the Securities and Exchange Commission on December 2, 2015.

Registration No. 333-207782

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________

Amendment

No. 2 to

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

___________________

SHIMMICK CONSTRUCTION COMPANY,

INC.

(Exact name of registrant as

specified in its charter)

|

California |

|

1600 |

|

94-3107390 |

|

(State or other jurisdiction of incorporation or organization) |

|

(Primary Standard Industrial Classification Code Number) |

|

(I.R.S. Employer |

8201 Edgewater Drive, Suite

202

Oakland, CA

94621

(510)

777-5000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Paul Cocotis, Chief Executive Officer

Shimmick Construction

Company, Inc.

8201 Edgewater Drive,

Suite 202

Oakland, CA

94621

(510)

777-5000

(Name, address, including zip code, and telephone number, including

area code, of agent for service)

___________________

Copies to:

|

Paul Lucido |

|

Jonathan H. Talcott

|

___________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

|

¨ |

|

Accelerated filer |

|

¨ |

|

Non-accelerated filer |

|

R |

|

Smaller reporting company |

|

¨ |

|

(Do not check if a smaller reporting company) |

||||||

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We and the selling shareholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we and the selling shareholders are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS |

|

SUBJECT TO COMPLETION |

|

DATED DECEMBER 2, 2015 |

[•] Shares

Common Stock

Shimmick Construction Company, Inc. is offering [•] shares of its common stock and the selling shareholders are offering [•] shares of common stock. We will not receive any proceeds from the sale of shares by the selling shareholders. We anticipate that the initial public offering price will be between $[•] and $[•] per share.

This is our initial public offering, and prior to this offering, there has been no public market for our common stock. We have applied to list our common stock on the Nasdaq Global Market under the symbol “SCCI.”

We are an “emerging growth company” under the federal securities laws and will be subject to reduced public company reporting requirements.

Investing in our common stock involves a high degree of risk. Please read “Risk Factors” beginning on page 11 of this prospectus for a discussion of some of the risks you should consider before investing.

|

|

|

Per Share |

|

Total |

|

Public offering price |

|

$ |

|

$ |

|

Underwriting discounts and commissions(1) |

|

$ |

|

$ |

|

Proceeds, before expenses, to us |

|

$ |

|

$ |

|

Proceeds, before expenses, to the selling shareholders |

|

$ |

|

$ |

____________

(1) The underwriters will receive compensation in addition to the underwriting discounts and commissions. See “Underwriting.”

We and the selling shareholders have granted the underwriters an option, exercisable within 30 days of the date of this prospectus, to purchase a maximum of [•] additional shares of our common stock from us and the selling shareholders at the initial public offering price, less the underwriting discounts and commissions, to cover over-allotments of shares, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of our common stock to purchasers against payment on or about [•], 2015.

FBR

The date of this prospectus is [•], 2015.

TABLE OF CONTENTS

|

PROSPECTUS SUMMARY |

|

1 |

|

RISK FACTORS |

|

11 |

|

CAUTIONARY STATEMENT CONCERNING FORWARD LOOKING STATEMENTS |

|

27 |

|

MARKET AND INDUSTRY DATA |

|

28 |

|

TRADEMARKS, SERVICE MARKS AND TRADE NAMES |

|

28 |

|

USE OF PROCEEDS |

|

29 |

|

DIVIDENDS AND DIVIDEND POLICY |

|

29 |

|

CAPITALIZATION |

|

30 |

|

DILUTION |

|

31 |

|

SELECTED CONSOLIDATED FINANCIAL DATA |

|

33 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND |

|

35 |

|

BUSINESS |

|

50 |

|

MANAGEMENT |

|

66 |

|

PRINCIPAL AND SELLING SHAREHOLDERS |

|

75 |

|

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS |

|

76 |

|

DESCRIPTION OF CAPITAL STOCK |

|

77 |

|

SHARES ELIGIBLE FOR FUTURE SALE |

|

80 |

|

UNDERWRITING |

|

82 |

|

U.S. FEDERAL INCOME TAX CONSIDERATIONS FOR NON-U.S. HOLDERS |

|

87 |

|

LEGAL MATTERS |

|

90 |

|

EXPERTS |

|

90 |

|

WHERE YOU CAN FIND MORE INFORMATION |

|

90 |

|

INDEX TO FINANCIAL INFORMATION |

|

F-1 |

_________________________

You should rely only on the information contained or incorporated by reference in this prospectus and in any free writing prospectus that we have authorized for use in connection with this offering. Neither we nor the underwriters nor the selling shareholders have authorized any other person to provide you with additional or different information. If anyone provides you with different or inconsistent information, you should not rely on it. Neither we nor the underwriters nor the selling shareholders are making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should assume that the information in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

i

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that is important to you or that you should consider before investing in our common stock. You should carefully read the entire prospectus, including the risk factors, financial data, and financial statements included herein, before making a decision about whether to invest in our common stock. Unless the context requires otherwise or we specifically indicate otherwise, the information in this prospectus assumes that the underwriters do not exercise their over-allotment option. As used in this prospectus, unless the context otherwise requires or indicates, the terms “Shimmick,” “our company,” “we,” “our,” “ours,” and “us” refer to Shimmick Construction Company, Inc. and its subsidiaries.

Overview of Our Business

Our Company

We are a leading heavy civil construction company offering general construction, construction management, and design-build services to federal, state, and local public agencies and private customers in California and the Western United States. We possess the in-house capabilities necessary to self-perform nearly all aspects of heavy civil construction — structural, foundations, utilities, mechanical, and electrical — which enables us to compete for large, technical projects and differentiates us from many of our competitors. Since our present executive team assumed leadership in 2001, we and our joint venture partners have been awarded over $5 billion worth of complex critical public infrastructure projects, including bridges, water/wastewater treatment facilities, dams, transit & rail, highways & roadways, ports, and airports. The portion of these projects allocable to us was over $3.4 billion. Since 2001, we have achieved a revenue compound annual growth rate (CAGR) of approximately 19%. Prior to this offering, our growth has been predominantly funded by retained earnings. Several long-term trends in our geographic markets, including population growth and the deterioration of existing infrastructure, have resulted in a renewed focus on infrastructure development and funding in California and the Western states. As a result of our growth and this renewed focus, the number and size of contracts in our bidding pipeline has significantly increased. While the competitive environment is impacted by a number of factors outside of our control, such as the general business climate and the amount of contracts being offered, we and our joint venture partners have a project pipeline of approximately $12 billion, of which we and our joint venture partners are actively engaged in bidding approximately $4 billion as outlined in the table below. The portion of such amounts allocable to us is approximately $8.3 billion and $2.2 billion, respectively. We believe that we are ideally positioned to benefit from increased investment now and in the future.

|

Project |

|

Type of Work |

|

Status |

|

Estimated |

|

Near-Term Bid Project A |

|

Water |

|

Bid date in December 2015 |

|

$ 250 |

|

Near-Term Bid Project B |

|

Roads and Bridges |

|

Bid date in January 2016 |

|

$ 120 |

|

Near-Term Bid Project C |

|

Water |

|

Bid date in January 2016 |

|

$ 450 |

|

Near-Term Bid Project D |

|

Transit |

|

Bid date in February 2016 |

|

$ 650 |

|

Other Near-Term Bids |

|

Various |

|

Bid dates between November 2015 and February 2016 |

|

$ 183 |

|

In Process Bid Project A |

|

Design/Build Rail |

|

Best and final offer due Spring 2016 |

|

$ 750 |

|

In Process Bid Project B |

|

Construction Manager / General Contractor |

|

Request for qualifications submitted |

|

$ 250 |

|

Other In Process Bids |

|

Various |

|

Various |

|

$ 138 |

|

Prequalified Project A |

|

Water |

|

Prequalified |

|

$ 85 |

|

Prequalified Project B |

|

Roads and Bridges |

|

Prequalified |

|

$ 1,200 |

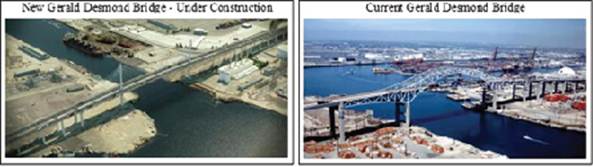

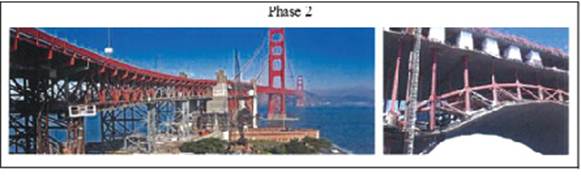

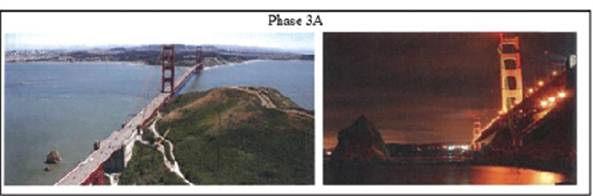

We have worked on many high-profile projects involving critical heavy infrastructure. Notable ongoing or recently-completed projects include the $245 million seismic and wind retrofit of the Golden Gate Bridge, the $140 million raising of the San Vicente Dam to improve water availability in the San Diego region, the $779 million replacement of the Gerald Desmond Bridge linking the Long Beach Terminal Island and the Long Beach Freeway, the $629 million expansion of the Los Angeles County Metropolitan Transportation Authority (LA MTA) Metro Gold Line to connect East Los Angeles to downtown, and the $772 million extension of the Bay Area Rapid Transit

1

(BART) rail commuter system south from Fremont to San Jose. In light of our many successful projects, we are widely acknowledged by a prominent trade publication, Engineering News-Record (ENR), as a leader in our field. Over the last five years, ENR’s national rankings by revenue have listed us as high as #3 in Dams & Reservoirs, #4 in Drinking Water Treatment, #9 in Water Supply, #11 in Marine and Port Facilities, #12 in Bridges, and #14 in Mass Transit. These rankings are a testament to the depth and breadth of our capabilities.

We primarily compete for new customer contracts independently, seeking to win and successfully complete new jobs as the general contractor. Given our in-house capabilities across the heavy civil construction specialties, we typically expect to self-perform the majority of the specified project elements on contracts where we are the general contractor, often achieving an 80% self-performance rate. For certain project elements that do not align with our in-house expertise or that require more commoditized capabilities — such as fencing of work areas or black asphalt paving of roads and highways — we may engage subcontractors to complete such discrete tasks. In heavy civil construction, contracts are principally awarded on a fixed-price basis, and we earn and recognize revenue on the percentage of completion method, based upon the proportion of units of production completed relative to the total estimated units of production for each item of work on a project.

Within the heavy civil construction industry, we have observed a trend toward larger and more complex infrastructure projects. Since our founding in 1990, our growth has been fueled by the increasing scale and scope of these projects, and we and our joint venture partners have successfully won and performed work on contracts with values ranging up to $800 million. With the proceeds of this offering, we believe that we will have the financial flexibility to pursue an increasing share of these large contracts. Our contracts pose a number of risks to us as outlined in “Risk Factors,” including risks associated with variances from the contract, such as cost, scope, or timing overruns for which we may not be entitled to reimbursement or additional compensation. For the largest projects, responsibilities and risk are typically shared among multiple contractors, and we believe that we will benefit from our history of partnering with other industry leaders, including AECOM, Alstom SA, Balfour Beatty plc, Black & Veatch Corporation, Dragados S.A., Granite Construction Incorporated, Obayashi Corporation, PCL Construction, Skanska AB, and Tutor Perini Corporation. We have similarly strong relationships with top design firms, including AECOM, Arup Group Limited, Jacobs Engineering Group Inc., Parsons Corporation and Parsons Brinckerhoff Group, Inc. Each of our joint ventures is formed to complete a specific contract jointly controlled by the joint venture partners. The financial benefits and risks of the joint venture are allocated based on each partner’s equity stake in the venture. As the market continues to move towards larger and more complex projects, we are well-positioned to accelerate our growth.

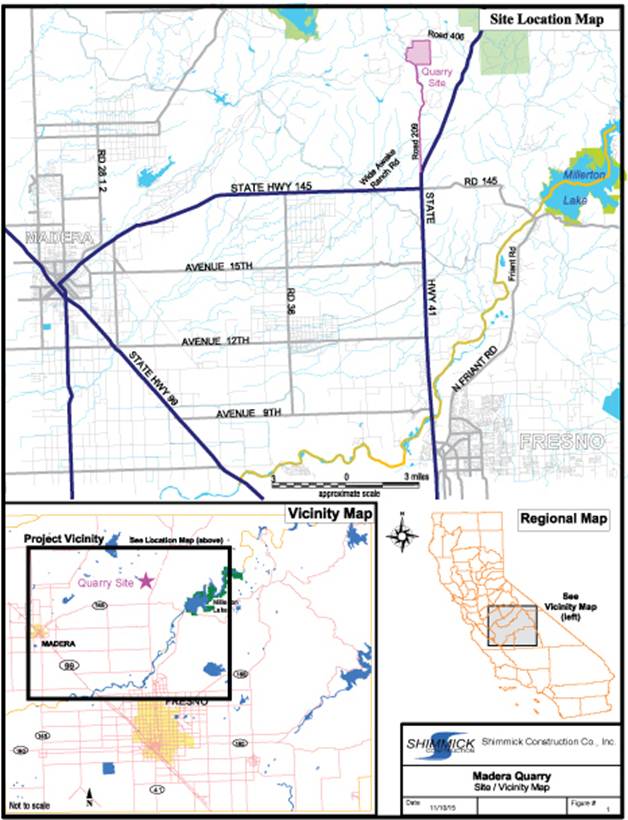

In addition to our heavy civil construction business, we own and operate a premium hard rock quarry in Madera, California with an estimated overall capacity of 62 million tons of reserves. The quarry currently has an annual permit capacity of approximately 900,000 tons through 2060 to support concrete and asphalt production. Assuming a value of $0.75/ton, we estimate these permitted granite reserves to have a value of approximately $30.8 million. The quarry sits on approximately 1,000 acres of real property near Fresno, one of California’s fastest growing communities.

For the nine months ended September 30, 2015, our revenues, net income attributable to Shimmick Construction Company, Inc. and EBITDA attributable to Shimmick Construction Company, Inc., or “Company EBITDA,” were $360.6 million, $7.4 million and $16.0 million, respectively, representing 64%, 7% and 24% increases over the same period in 2014. During the twelve months ended December 31, 2014 our revenues, net income attributable to Shimmick Construction Company, Inc. and Company EBITDA were $319.6 million, $9.1 million and $17.9 million, respectively, as compared to $285.9 million, $1.1 million and $9.0 million for the prior year. As of September 30, 2015, our total contract backlog stood at $618 million, which we expect to earn primarily in the two years ending September 30, 2017.

Our Markets

Throughout our history, we have primarily focused on the California market and have structured our operations geographically with locations in Oakland and Irvine to support our customers. We believe that we have an intimate knowledge of California markets and long-standing relationships with significant customers, including the California Department of Transportation (Caltrans), the LA MTA, BART, the Santa Clara Valley Transportation Authority (VTA), the Orange County Sanitation District (OCSD), the Metropolitan Water District of California (MWD), the Port of Long Beach, the Port of Los Angeles, the City of San Francisco, and the City and county of Los Angeles, among many others. In addition to our California focus, we have selectively pursued contracts in other Western states. We believe that these markets are important to our growth strategy, as infrastructure funding in these states continues to increase. We are licensed as a civil contractor and possess other specialty licenses to operate in

2

California, Oregon, Washington, Nevada, Arizona, Hawaii, Alaska, and Texas. We are currently working on projects in Washington as well as preparing multiple bids on projects in Hawaii.

California’s infrastructure — much of it built in the 1950s and 1960s — has deteriorated over the last several decades. The American Society of Civil Engineers (ASCE) estimates that $45.0 billion and $29.9 billion are needed to maintain and upgrade California’s drinking water and wastewater systems, respectively, over the next 20 years. From a transportation perspective, the ASCE rates 34% of California’s roads as poor or mediocre in quality and categorizes 2,769 bridges as structurally deficient. Population growth in California and in the Western United States has put further stress on degrading infrastructure, necessitating restoration and new-build infrastructure projects throughout the region. In addition, California’s historic and ongoing drought has necessitated a significant upgrade in the state’s water infrastructure, particularly as population continues to grow. We believe the financial crisis of 2007 to 2009 further delayed necessary investment in critical infrastructure, but recently important steps have been taken at the national, state, and local levels to appropriate funding and accelerate these types of projects.

On December 1, 2015, Congressional negotiators agreed on an approximately $300 billion transportation bill to invest in the nation’s highways and infrastructure over the next five years. The Fixing America’s Surface Transportation (FAST) Act would represent the first transportation funding legislation to last longer than two years since 2005. Specifically, the FAST Act plans to spend approximately $255 billion and $48 billion on highway infrastructure and transit projects, respectively, and would be funded through the reauthorization of gas tax revenue and offsets from other areas of the federal budget. In California, Governor Brown recently proposed a 2015 infrastructure funding plan which calls for $57 billion in state funding over the next five years. In addition, the LA MTA publicly announced its intention to spend $8.5 billion in Southern California over the next ten years to develop new rail projects, add carpool lanes, and fund Metrolink capital improvement projects. Finally, the 2014 passage of Proposition 1 in California provides for a $7.5 billion water bond, demonstrating the state population’s heightened awareness of water scarcity. Although our concentration in California may result in our financial results being significantly impacted by factors such as local climate, business and economic conditions, and government budget restrictions, we believe that California will remain an attractive market and that we are positioned to benefit from the growing wave of infrastructure spending being appropriated at the federal, state, and local levels.

Competitive Strengths

We believe that our competitive strengths in the heavy civil construction industry include the following:

Long and Successful Track Record of Infrastructure Construction. Through our 26 years of experience, we have developed efficient processes and controls that allow us to provide high-quality contracting services for bridges, water/wastewater treatment facilities, dams, transit & rail, highways & roadways, ports, and airports. Our expertise, coupled with strong underlying market dynamics, has helped us become a market leader in California. Customers increasingly require that bidders for heavy civil infrastructure projects have a strong history of contract performance, which we believe positions us well to compete for the anticipated wave of new projects in coming years.

Experienced Executive Team with Significant Ownership. Each member of our senior leadership team has over 25 years of industry experience, and our Chief Executive Officer, President, Executive Vice Presidents, and Chief Financial Officer have worked together for over 15 years. Since our present management team assumed leadership in 2001, revenues and equity have both grown at a CAGR of 19%. Additionally, senior executives have significant ownership in the business and will own [•]% after the consummation of this offering.

Self-Performance of Contracts. We have self-performance capabilities in virtually all aspects of heavy civil construction. In particular, we believe that our in-house foundations, mechanical, and electrical capabilities set us apart from heavy civil contractors of our size. Our ability to self-perform makes us more competitive in the bid process, as we are able to confidently estimate the cost of each job package given our expertise and track record. These capabilities allow us to bid for more technically challenging projects, which are generally less competitive. In addition, our focus on self-performance allows us to capture profit margin that otherwise would be shared with subcontractors.

Consistent History of Managing Construction Projects and Contract Risk. Our long and successful track record in our markets provides us with an understanding of the various risks of infrastructure construction. We provide services predominantly pursuant to “fixed price” contracts, which, if properly managed, allow for better profit margin opportunities than “cost plus” contracts. We monitor and manage risk throughout a contract’s duration, including the bid process, pre-construction planning activities, and construction. Our project managers lead our estimating processes, and our senior management reviews all bid proposals prior to submission, thereby increasing

3

accountability and an understanding of the financial and operating risks and opportunities of our contracts. We maintain a database of prior contract proposals and records from completed projects, such as raw material requirements and costs, labor requirements and costs, and equipment needs, enabling us to rely on our institutional knowledge when estimating project costs in developing new proposals.

Long-Term Relationships with Customers and Partners. Since our first major contract win with the City of San Francisco in 1990, we have developed strong relationships with the major California infrastructure owners, including Caltrans, LA MTA, BART, the VTA, the Port of Long Beach, the Port of Los Angeles, the City of San Francisco and the City and county of Los Angeles. In addition, we have formed joint venture relationships with many of the most prominent construction companies, including AECOM, Alstom SA, Balfour Beatty plc, Black & Veatch Corporation, Dragados S.A., Granite Construction Incorporated, Obayashi Corporation, PCL Construction, Skanska AB, and Tutor Perini Corporation, in order to compete for and win some of our largest contracts. These relationships have enabled us to achieve the rapid growth we have experienced since our founding and we believe they will facilitate continued growth in the future.

Entrepreneurial Culture with a Commitment to Talent Development. Consistent with our corporate motto “building the people and projects that improve America’s infrastructure,” our senior management team has instilled in our culture an emphasis on the professional development of each employee. We recruit many of our new employees from a network of approximately 25 college campuses, where we seek to identify candidates with a desire to develop as construction and engineering professionals and who have key intangible qualities in addition to academic credentials. We believe that our entrepreneurial culture and complex projects provide unique opportunities for our employees to grow within our organization. We also encourage our employees to take proactive steps to advance their development, which we believe has resulted in a larger percentage of our employees achieving the Professional Engineer designation relative to our competitors.

Growth Strategy

We have implemented the following strategies in order to drive growth in our business and, ultimately, to enhance shareholder value:

Continue to Grow in our California Markets. We operate in every major California market, including San Francisco, San Jose, the Central Valley, Los Angeles, Orange County, San Diego, and the Inland Empire. These markets are experiencing strong growth in infrastructure spending caused by factors such as growing populations, the need for new water resources, increased federally-funded highway construction, enhanced port and airport activity, and the installation of public transit systems. We will continue our efforts to increase our market share in these core markets. In addition, we will look to grow opportunistically into markets that we see as a natural expansion of our current operations, including power generation and industrial.

Develop Well-Resourced Teams to Bid Large Projects. As a result of deteriorating infrastructure as well as historical delays to project funding, we have observed that the size of projects we are evaluating and bidding continues to grow. In the past, we have bid and won large projects where our specialized capabilities aligned with the customer’s needs. Examples of such larger projects include the replacement of the Gerald Desmond Bridge, the Silicon Valley BART extension, the Eastside Light Rail Transit system, and the wind and seismic retrofit of the Golden Gate Bridge. We believe that the proceeds from this offering will give us the financial flexibility to pursue more large projects. By giving our bid teams both the human and financial resources necessary to evaluate and prudently compete for these large contracts, we believe that we will win an increasing share of these projects while maintaining favorable margins. As of September 30, 2015, we and our joint venture partners were actively engaged in bidding four opportunities with contract values between approximately $450 million and $1.2 billion.

Expand into Attractive New Geographies. Although we have traditionally focused on our core California markets, we have selectively sought projects in other Western states. We actively consider projects in other geographic markets, and we evaluate opportunities based on factors such as market size and growth dynamics, competition, the availability of qualified employees and compatibility of unique local requirements with our own expertise. We have been selective in our out-of-state bids to date, and are currently working on projects in Washington as well as preparing multiple bids on projects in Hawaii.

Independently Brand our Electrical and Foundation Businesses. We believe that our electrical and foundation capabilities are among the very best in our industry and are differentiators when we compete for complex, multi-faceted contracts. ENR estimates the national electrical and excavation & foundation markets to be $30 billion

4

and $4.5 billion, respectively, with the potential for substantial growth in the future. By independently branding these operations, we believe that we will continue to support our heavy civil work while pursuing increased subcontracting work to create additional revenue streams. For example, there is a large subcontracting market for electrical and foundations outside heavy civil construction, such as building construction.

Vertically Integrate Aggregates through Madera Quarry Operations. We recently opened our premium hard rock quarry in Madera, California. Our quarry operations can support concrete and asphalt production with an initial permitted annual capacity of 900,000 tons of high quality granite aggregate. The quarry is strategically located near Fresno, which is one of California’s fastest growing communities and where our aggregates can be used in new residential construction. In addition, we believe that our production of aggregates will give us an advantage in bidding heavy civil contracts, particularly in roadwork. In the future, we plan to build asphalt facilities to work in conjunction with our quarry. This plan will allow us to market hot mixed asphalt concrete to the local market as well as give us an advantage with respect to future paving jobs that we self-perform in the region surrounding the quarry.

Strategically Pursue Acquisitions. After completion of this offering, we expect to periodically evaluate strategic acquisition opportunities that would enable us to enhance our capabilities, pursue complementary markets or enter new geographies where we do not have an existing track record. Although we are not engaged in negotiations and have no firm agreements for any material acquisitions at this time, we will evaluate acquisition opportunities as they may arise, in order to identify opportunities that would accelerate our growth.

Selling Shareholders

The selling shareholders are officers, directors and employees of ours, including Paul Cocotis, our Chief Executive Officer and Chairman of the Board, Paul Camaur, our President, Jeffrey Lessman and Christian Fassari, each an Executive Vice President of ours, and Scott Fairgrieve, our Chief Financial Officer, Assistant Secretary and Treasurer. Many of our officers, directors and employees are shareholders and are selling a pro rata portion of their shares in this offering. For more information on the selling shareholders, including the selling shareholders’ beneficial ownership of our common stock before and after the offering, see “Principal and Selling Shareholders” beginning on page 75. Immediately following the completion of the offering, our officers and directors will own approximately [•]% of our stock ([•]% if the underwriters exercise their over-allotment option in full).

Risks Affecting Us

Investing in our common stock involves risks. For a discussion of these risks and other considerations that could negatively affect us, including risks related to this offering and our common stock, see “Risk Factors” and “Cautionary Statement Concerning Forward-Looking Statements.” These risks include, among others:

• If we are unable to accurately estimate the overall risks, requirements or costs when we bid on or negotiate a contract that is ultimately awarded to us, we may achieve a lower than anticipated profit or incur a loss on the contract.

• Economic downturns or reductions in government funding of infrastructure projects could reduce our revenues and profits and have a material adverse effect on our results of operations.

• We operate primarily in California and adverse changes to the economy and business environment in the state has had an adverse effect on, and could continue to adversely affect, our operations, which could lead to lower revenues and reduced profitability.

• Our ability to successfully win bids in a highly competitive marketplace.

• The cancellation of significant contracts or our disqualification from bidding for new contracts could reduce our revenues and profits and have a material adverse effect on our results of operations.

• Government contracts generally have strict regulatory requirements and government contractors are subject to suspension or debarment from government contracting.

• Our failure to meet schedule or performance requirements of our contracts could adversely affect us.

• Timing of the award and performance of new contracts could have an adverse effect on our operating results and cash flow.

• Our participation in construction joint ventures exposes us to liability and/or harm to our reputation for failures of our partners.

5

• An inability to obtain bonding could limit the aggregate dollar amount of contracts that we are able to pursue.

• The percentage-of-completion method of accounting for contract revenues involved significant estimates which may result in material adjustments, which could result in a charge against our earnings.

• Our contract backlog is subject to unexpected adjustments and cancellations and could be an uncertain indicator of our future earnings.

Corporate Information

Our principal executive offices are located at 8201 Edgewater Drive, Suite 202, Oakland, CA 94621, and our telephone number is (510) 777-5000. Our corporate website address is www.shimmick.com. The information contained on, or accessible from, our corporate website is not part of this prospectus and you should not consider information contained on our website to be a part of this prospectus or in deciding whether to purchase our common stock.

Certain Corporate Matters

In connection with this offering, we will convert to a subchapter C corporation. As a result of this conversion, we will record a tax provision (estimated to be in excess of $5 million) to recognize deferred taxes. In addition, prior to the effective date of the registration statement of which this prospectus is a part, we will file an amendment to our articles of incorporation, which will effect, among other things, a [•]-for-1 stock split with respect to our common stock. Furthermore, upon completion of this offering, we will terminate the buy/sell agreements to which each of our shareholders is a party. The buy/sell agreements provide for mandatory redemption of the shares of common stock held by our shareholders (each of whom is an officer, director or employee of ours) upon cessation of their service to us. Because we determined that our common stock is presently mandatorily redeemable in accordance with U.S. generally accepted accounting principles, or “GAAP,” the carrying value of our shares of common stock and the related retained earnings are treated as a long-term liability on our financial statements. Once the buy/sell agreements have been terminated upon completion of this offering, all of the presently outstanding common stock will be treated as shareholders’ equity under GAAP.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenues during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012, or the “JOBS Act.” An emerging growth company may take advantage of specified reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company:

• we may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this prospectus;

• we are exempt from the requirement to obtain an attestation and report from our auditors on the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002, or the “Sarbanes-Oxley Act”;

• we are permitted to provide less extensive disclosure about our executive compensation arrangements;

• we are not required to give our shareholders non-binding advisory votes on executive compensation or golden parachute arrangements; and

• we may elect to use an extended transition period for complying with new or revised accounting standards that may be issued by the Financial Accounting Standards Board or the Securities and Exchange Commission, or the “SEC.”

We have irrevocably elected to take advantage of the extended transition period for new or revised accounting standards. This means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can delay adoption of the standard until it applies to private companies.

We may take advantage of these provisions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenues, have more than $700 million in market value of our common stock held by non-affiliates or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced reporting and other requirements.

6

The Offering

|

Common stock offered by us |

|

[•] shares ([•] shares if the underwriters exercise the over-allotment option in full). |

Common stock offered by the selling shareholders |

|

|

|

|

|

|

|

Common stock to be outstanding after the offering |

|

|

|

|

|

|

Common stock beneficially owned by the selling shareholders after the offering |

|

|

|

|

|

|

|

Use of proceeds |

|

We estimate that the net proceeds to us from this offering, after deducting the underwriters’ discounts and commissions and our estimated offering expenses, will be approximately $[•] million. We intend to use the net proceeds from this offering for working capital and other general corporate purposes. We will not receive any proceeds from the sale of common stock by the selling shareholders. |

|

|

|

|

Over-allotment option |

|

We and the selling shareholders have granted the underwriters a 30-day option to purchase a maximum of [•] additional shares of our common stock from us and the selling shareholders at the initial public offering price, less the underwriting discounts and commissions, to cover over-allotments, if any. |

|

|

|

|

|

Risk factors |

|

You should consider carefully all of the information set forth in this prospectus and, in particular, the specific factors set forth under “Risk Factors” on page 11, before deciding whether to invest in our common stock. |

|

|

|

|

|

Dividend policy |

|

After the consummation of this offering, we do not anticipate that we will declare or pay regular dividends on our common stock in the foreseeable future, as we generally intend to invest any future earnings in the development and growth of our business. |

|

|

|

|

|

Proposed Nasdaq Global Market symbol for our common stock |

|

|

Except as otherwise indicated, all information in this prospectus:

• gives effect to the filing of an amendment to our articles of incorporation, effecting a [•]-for-1 stock split with respect to our common stock, which will occur prior to the effective date of the registration statement of which this prospectus is a part;

• gives effect to the filing of our amended and restated articles of incorporation and adoption of our amended and restated bylaws, which will occur prior to the effective date of the registration statement of which this prospectus is a part;

• excludes 1,668 shares issuable in connection with bonuses earned in 2014 upon achievement of certain vesting conditions; and

• excludes [•] shares reserved for issuance pursuant to our Incentive Plan adopted in November 2015, or the “Incentive Plan.”

7

Summary Selected Consolidated Financial Data

The following table sets forth summary selected consolidated financial information as of the dates and for the periods represented, as well as (a) certain pro forma information that gives effect to the termination of the redemption rights of the holders of our common stock subject to mandatory redemption upon the closing of this offering and will give effect to the proposed stock split, once the stock split ratio has been determined, and (b) certain pro forma as adjusted information that gives further effect to the sale by us of [•] shares of common stock in this offering at an assumed initial public offering price of $[•] per share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us.

The financial data as of and for the years ended December 31, 2013 and 2014 have been derived from our audited consolidated financial statements and notes thereto included elsewhere in this prospectus. The financial data for the nine months ended September 30, 2014 and 2015 have been derived from our unaudited condensed consolidated financial statements and notes thereto included elsewhere in this prospectus. We have prepared the unaudited consolidated financial information set forth below on the same basis as our audited consolidated financial statements and have included all adjustments, consisting of only normal recurring adjustments, that we consider necessary for a fair presentation of our financial position and operating results for such periods. Our historical results are not necessarily indicative of the results to be expected in any future period, and our interim results are not necessarily indicative of the results to be expected for the full fiscal year.

The data presented below should be read in conjunction with, and are qualified in their entirety by reference to, “Capitalization,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus. Amounts are in thousands, except share and per share data.

|

|

|

Years Ended December 31, |

|

Nine Months Ended September 30, |

||||||||||||

|

|

|

2013 |

|

2014 |

|

2014 |

|

2015 |

||||||||

|

|

|

|

|

|

|

(Unaudited) |

||||||||||

|

Contract revenues |

|

$ |

285,893 |

|

|

$ |

319,629 |

|

|

$ |

219,594 |

|

|

$ |

360,551 |

|

|

Cost of contract revenues |

|

|

279,942 |

|

|

|

293,409 |

|

|

|

200,058 |

|

|

|

332,733 |

|

|

|

|

5,951 |

|

|

|

26,220 |

|

|

|

19,536 |

|

|

|

27,818 |

|

|

|

General and administrative expenses(1) |

|

|

10,387 |

|

|

|

15,424 |

|

|

|

11,077 |

|

|

|

16,090 |

|

|

Income (loss) from operations |

|

|

(4,436 |

) |

|

|

10,796 |

|

|

|

8,459 |

|

|

|

11,728 |

|

|

Equity (loss) in net earnings of affiliates |

|

|

82 |

|

|

|

(188 |

) |

|

|

(34 |

) |

|

|

(160 |

) |

|

Other income (expense), net |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1,101 |

) |

|

|

(1,424 |

) |

|

|

(999 |

) |

|

|

(898 |

) |

|

|

|

|

616 |

|

|

|

(76 |

) |

|

|

(336 |

) |

|

|

90 |

|

|

|

|

|

(485 |

) |

|

|

(1,500 |

) |

|

|

(1,335 |

) |

|

|

(808 |

) |

|

|

Net income (loss)(2) |

|

|

(4,839 |

) |

|

|

9,108 |

|

|

|

7,090 |

|

|

|

10,760 |

|

|

Less/add: Net loss (income) attributable to noncontrolling interests |

|

|

5,899 |

|

|

|

16 |

|

|

|

(157 |

) |

|

|

(3,340 |

) |

|

|

$ |

1,060 |

|

|

$ |

9,124 |

|

|

$ |

6,933 |

|

|

$ |

7,420 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EBITDA attributable to Shimmick Construction Company, Inc. – unaudited(4) |

|

$ |

9,037 |

|

|

$ |

17,901 |

|

|

$ |

12,899 |

|

|

$ |

16,009 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pro forma net income per share attributable to Shimmick Construction Company, Inc. – unaudited(3): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

81.68 |

|

|

$ |

61.55 |

|

|

$ |

55.63 |

|

|

|

|

|

|

|

|

$ |

74.93 |

|

|

$ |

56.47 |

|

|

$ |

51.17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pro forma weighted average shares of common stock – unaudited(3): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

82,898 |

|

|

|

82,885 |

|

|

|

83,008 |

|

|

|

|

|

|

|

|

|

90,369 |

|

|

|

90,340 |

|

|

|

90,242 |

|

|

8

|

|

|

|

|

|

|

As of September 30, 2015 |

||||||||

|

|

|

As of December 31, 2013 |

|

As of December 31, 2014 |

|

Actual |

|

Pro Forma(5) |

|

Pro Forma As Adjusted(6)(7) |

||||

|

Consolidated Balance Sheet Data: |

|

|

|

|

|

|

|

(unaudited) |

|

|

||||

|

Cash and cash equivalents |

|

$ |

34,730 |

|

$ |

40,248 |

|

$ |

31,636 |

|

$ |

31,636 |

|

|

|

Working capital |

|

|

37,248 |

|

|

43,578 |

|

|

49,941 |

|

|

49,941 |

|

|

|

Total assets |

|

|

215,422 |

|

|

236,046 |

|

|

260,991 |

|

|

260,991 |

|

|

|

Long-term debt, net of current portion |

|

|

32,924 |

|

|

24,115 |

|

|

26,640 |

|

|

26,640 |

|

|

|

Shimmick Construction Company, Inc. shares

subject to mandatory |

|

|

57,191 |

|

|

63,063 |

|

|

68,632 |

|

|

— |

|

|

|

Shimmick Construction Company, Inc. shareholders’ equity |

|

|

— |

|

|

— |

|

|

— |

|

|

68,632 |

|

|

____________

(1) Includes stock-based compensation expense of $804,000 and $2.2 million recorded in the year ended December 31, 2014 and the nine months ended September 30, 2015, respectively. See Notes 13 and 14 to our consolidated financial statements for a discussion of stock-based compensation expense recorded.

(2) The Company has elected S Corporation status under which income and losses from the Company are included in the personal income tax returns of the shareholders. Consequently, the Company’s operating results do not include a material provision for income taxes. Upon its initial public offering, the Company intends to change its federal income tax status from S Corporation to C Corporation. In connection therewith, its statutory tax rate (U.S. federal and state taxes, net of federal benefit) will increase from 1.5% to approximately 40%. See Note 1 to our consolidated financial statements.

(3) See Note 16 to our consolidated financial statements for an explanation of the method used to calculate our pro forma basic and diluted net income per share attributable to Shimmick Construction Company, Inc. and the pro forma weighted-average number of shares used in the computation of the pro forma per share amounts.

(4) The term EBITDA is not defined under GAAP. We believe, however, that Company EBITDA is meaningful to our investors to enhance their understanding of our financial performance. We understand that EBITDA is frequently used by securities analysts, investors and other interested parties as a measure of financial performance and to compare our performance with the performance of other companies that report EBITDA. Our calculation of Company EBITDA however, may not be comparable to similarly titled measures reported by other companies. When assessing our operating performance, investors and others should not consider this data in isolation or as a substitute for net income calculated in accordance with GAAP. Further, the results presented by Company EBITDA cannot be achieved without incurring the costs that the measure excludes. As used in this prospectus, Company EBITDA is defined as net income attributable to Shimmick Construction Company, Inc. plus depreciation and amortization expense, stock-based compensation expense, operating lease expense on construction equipment, interest expense and taxes and other costs. The following table reconciles net income attributable to Shimmick Construction Company, Inc. (the closest GAAP financial measure) to Company EBITDA for the periods presented in this table and elsewhere in this prospectus.

|

Amounts in thousands |

|

Years Ended December 31, |

|

Nine Months Ended September 30, |

||||||||

|

|

|

2013 |

|

2014 |

|

2014 |

|

2015 |

||||

|

|

|

|

|

|

|

(unaudited) |

||||||

|

Net income attributable to Shimmick Construction Company, Inc. |

|

$ |

1,060 |

|

$ |

9,124 |

|

$ |

6,933 |

|

$ |

7,420 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjustments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5,991 |

|

|

5,208 |

|

|

3,901 |

|

|

2,989 |

|

|

|

|

— |

|

|

804 |

|

|

240 |

|

|

2,162 |

|

|

|

|

15 |

|

|

680 |

|

|

319 |

|

|

2,202 |

|

|

|

|

1,957 |

|

|

2,085 |

|

|

1,506 |

|

|

1,222 |

|

|

|

|

14 |

|

|

— |

|

|

— |

|

|

14 |

|

|

EBITDA attributable to Shimmick Construction Company, Inc. |

|

$ |

9,037 |

|

$ |

17,901 |

|

$ |

12,899 |

|

$ |

16,009 |

(5) The pro forma column reflects the termination of the redemption rights of the holders of the common stock subject to mandatory redemption upon the closing of this offering and will reflect the proposed stock split, once the stock split ratio has been determined.

9

(6) The pro forma as adjusted column further reflects the receipt of $[•] million in net proceeds from our sale of shares of common stock in this offering at an assumed initial public offering price of $[•] per share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us.

(7) Each $1.00 increase or decrease in the assumed initial public offering price of $[•] per share would increase or decrease, respectively, the amount of cash and cash equivalents, working capital, total assets and total shareholders’ (deficit) equity by $[•] million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We may also increase or decrease the number of shares we are offering. An increase or decrease of 1,000,000 in the number of shares we are offering would increase or decrease, respectively, the amount of cash and cash equivalents, working capital, total assets and total pro forma shareholders’ equity by approximately $[•] million, assuming the assumed initial public offering price per share, as set forth on the cover page of this prospectus, remains the same after deducting underwriting discounts and commissions. The pro forma as adjusted information is illustrative only, and we will adjust this information based on the actual initial public offering price and other terms of this offering determined at pricing.

10

RISK FACTORS

An investment in our common stock involves risks. You should carefully consider each of the following risks and all of the information set forth in this prospectus before deciding to invest in our common stock. The risks and uncertainties described below are not the only ones we face. If any of the following risks and uncertainties develops into actual events, our business, financial condition, results of operations and cash flows could be materially adversely affected. In that case, the price of our common stock could decline and you may lose all or part of your investment.

Risks Related to Our Business and Industry

If we are unable to accurately estimate the overall risks, requirements or costs when we bid on or negotiate a contract that is ultimately awarded to us, we may achieve a lower than anticipated profit or incur a loss on the contract.

The majority of our revenues and backlog are derived from fixed unit price contracts and lump sum contracts. Fixed unit price contracts require us to provide materials and services at a fixed unit price based on approved quantities irrespective of our actual per unit costs. Lump sum contracts require that the total amount of work be performed for a single price irrespective of our actual per unit costs. We realize a profit on our contracts only if we accurately estimate our costs and then successfully control actual costs and avoid cost overruns, and our revenues exceed actual costs. If our cost estimates for a contract are inaccurate, or if we do not execute the contract within our cost estimates, then cost overruns may cause us to incur losses or cause the contract not to be as profitable as we expected. The final results under these types of contracts could negatively affect our cash flow, earnings and financial position.

The costs incurred and gross profit realized on our contracts can vary, sometimes substantially, from our original projections due to a variety of factors, including, but not limited to:

• on site conditions that differ from those assumed in the original bid or contract;

• failure to include required materials or work in a bid, or the failure to estimate properly the quantities or costs needed to complete a lump sum contract;

• contract or project modifications creating unanticipated costs not covered by change orders;

• failure by our suppliers, subcontractors, designers, engineers, joint venture partners or customers to perform their obligations;

• delays in quickly identifying and taking measures to address issues which arise during contract execution;

• changes in availability, proximity and costs of materials, including steel, concrete, aggregates and other construction materials, as well as fuel and lubricants for our equipment;

• claims or demands from third parties for alleged damages arising from the design, construction or use and operation of a project of which our work is part;

• difficulties in obtaining required governmental permits or approvals;

• availability and skill level of workers in the geographic location of a project;

• citations issued by any governmental authority, including the Occupational Safety and Health Administration;

• unexpected labor conditions or work stoppages;

• changes in applicable laws and regulations;

• delays caused by weather conditions;

• fraud, theft or other improper activities by our suppliers, subcontractors, designers, engineers, joint venture partners or customers or our own personnel; and

• mechanical problems with our machinery or equipment.

11

Many of our contracts with public sector customers contain provisions that purport to shift some or all of the above risks from the customer to us, even in cases where the customer is partly at fault. Our experience has often been that public sector customers have been willing to negotiate equitable adjustments in the contract compensation or completion time provisions if unexpected circumstances arise. However, public sector customers may seek to impose contractual risk-shifting provisions more aggressively, which could increase risks and adversely affect our cash flow, earnings and financial position.

Economic downturns or reductions in government funding of infrastructure projects could reduce our revenues and profits and have a material adverse effect on our results of operations.

Our business is highly dependent on the amount and timing of infrastructure work funded by various governmental entities, which, in turn, depends on the overall condition of the economy, the need for new or replacement infrastructure, the priorities placed on various projects funded by governmental entities and federal, state or local government spending levels. Spending on infrastructure could decline for numerous reasons, including decreased revenues received by state and local governments for spending on such projects, including federal funding. The most recent recession caused a nationwide decline in home sales and an increase in foreclosures, which correspondingly resulted in decreases in property taxes and some other local taxes, which are among the sources of funding for municipal road, bridge and water infrastructure construction. State spending on highway and other projects can be adversely affected by decreases or delays in, or uncertainties regarding, federal highway funding, which could adversely affect us. Construction companies in the heavy civil market are reliant upon contracts with state transportation departments for a significant portion of their revenues.

See “Business — Our Markets” beginning on page 51 for a more detailed discussion of our markets and their funding sources.

We operate primarily in California and adverse changes to the economy and business environment in the state has had an adverse effect on, and could continue to adversely affect, our operations, which could lead to lower revenues and reduced profitability.

Because of our geographic concentration in California, we are susceptible to fluctuations in our business caused by adverse economic or other conditions in the state, including natural or other disasters. The stagnant or depressed economy in California has in the past adversely affected, and could continue to adversely effect, our business and results of operations as well as the availability of state and local government funding.

We work in a highly competitive marketplace.

In the past, a majority of the contracts on which we bid were awarded through a competitive bid process, with awards generally being made to the lowest bidder, but sometimes recognizing other factors, such as shorter contract schedules or prior experience with the customer. For our design-build and other alternative methods of delivering projects, reputation, marketing efforts, quality of design and minimizing public inconvenience are also significant factors considered in awarding contracts, in addition to cost. Within our markets, we compete with many international, national, regional and local construction firms. Some of these competitors have achieved greater market penetration than we have in the markets in which we compete, and some may have greater financial and other resources than we do. In addition, there are a number of international and national companies in our industry that are larger than we are and that, if they so desire, could establish a presence in our markets and compete with us for contracts.

The cancellation of significant contracts or our disqualification from bidding for new contracts could reduce our revenues and profits and have a material adverse effect on our results of operations.

Contracts that we enter into with governmental entities can usually be canceled at any time by them with payment only for the work already completed. In addition, we could be prohibited from bidding on certain governmental contracts if we fail to maintain qualifications required by those entities. A cancellation of an unfinished contract or our debarment from the bidding process could cause our equipment and work crews to be idled for a significant period of time until other comparable work becomes available, which could have a material adverse effect on our business and results of operations.

12

Government contracts generally have strict regulatory requirements.

A majority of our total revenues in 2014 was derived from contracts funded by federal, state and local government agencies and authorities. Government contracts are subject to specific procurement regulations, contract provisions and a variety of socioeconomic requirements relating to their formation, administration, performance and accounting and often include express or implied certifications of compliance. Claims for civil or criminal fraud may be brought for violations of regulations, requirements or statutes. We may also be subject to qui tam (“whistle blower”) litigation brought by private individuals on behalf of the government under the False Claims Act, which could include claims for up to treble damages. Further, if we fail to comply with any of the regulations, requirements or statutes or if we have a substantial number of accumulated Occupational Safety and Health Administration, Mine Safety and Health Administration or other workplace safety violations, our existing government contracts could be terminated and we could be suspended from government contracting or subcontracting, including federally funded projects at the state level. Should one or more of these events occur, it could have a material adverse effect on our financial position, results of operations, cash flows and liquidity.

Government contractors are subject to suspension or debarment from government contracting.

Our substantial dependence on government contracts exposes us to a variety of risks that differ from those associated with private sector contracts. Various statutes to which our operations are subject, including the Davis-Bacon Act (which regulates wages and benefits), the Walsh-Healy Act (which prescribes a minimum wage and regulates overtime and working conditions), Executive Order 11246 (which establishes equal employment opportunity and affirmative action requirements) and the Drug-Free Workplace Act, provide for mandatory suspension and/or debarment of contractors in certain circumstances involving statutory violations. In addition, the Federal Acquisition Regulation and various state statutes provide for discretionary suspension and/or debarment in certain circumstances that might call into question a contractor’s willingness or ability to act responsibly, including as a result of being convicted of, or being found civilly liable for, fraud or a criminal offense in connection with obtaining, attempting to obtain or performing a public contract or subcontract. The scope and duration of any suspension or debarment may vary depending upon the facts and the statutory or regulatory grounds for debarment and could have a material adverse effect on our financial position, results of operations, cash flows and liquidity.

Our success depends upon the continuing contributions of certain key personnel, each of whom would be difficult to replace. If we were to lose the benefit of the experience, efforts and abilities of one or more of these individuals, our operating results could suffer.

Our continuing success depends on the performance of our management team. We cannot guarantee the continued employment of any of our key executives who may choose to leave our company for any number of reasons, such as other business opportunities, differing views on our strategic direction or other reasons. We rely on the experience, efforts and abilities of these individuals, each of whom would be difficult to replace. We intend to enter into employment agreements with our key executives prior to the completion of this offering; however, the employment agreements will not guarantee their continued service to us.

Our success depends on attracting and retaining qualified personnel, joint venture partners and subcontractors in a competitive environment.

The success of our business is dependent on our ability to attract, develop and retain qualified personnel, joint venture partners, advisors and subcontractors. Changes in general or local economic conditions and the resulting impact on the labor market and on our joint venture partners may make it difficult to attract or retain qualified individuals in the geographic areas where we perform our work. If we are unable to provide competitive compensation packages, high-quality training programs and attractive work environments or to establish and maintain successful partnerships, our ability to profitably execute our work could be adversely impacted.

We rely heavily on immigrant labor. We have taken steps that we believe are sufficient and appropriate to ensure compliance with immigration laws. However, we cannot provide assurance that we have identified, or will identify in the future, all illegal immigrants who work for us. Our failure to identify illegal immigrants who work for us may result in fines or other penalties being imposed upon us, which could have a material adverse effect on our operations, results of operations and financial condition.

13

Our failure to meet schedule or performance requirements of our contracts could adversely affect us.

In most cases, our contracts require completion by a scheduled acceptance date. Failure to meet any such schedule could result in additional costs, penalties or liquidated damages being assessed against us, and these could exceed projected profit margins on the contract. Performance problems on existing and future contracts could cause actual results of operations to differ materially from those anticipated by us and could cause us to suffer damage to our reputation within the industry and among our customers.

Adverse weather conditions may cause delays, which could slow completion of our contracts and negatively affect our revenues and cash flow.

Because all of our construction projects are built outdoors, work on our contracts is subject to unpredictable weather conditions. While weather has historically had a minimal impact on our operation due to the concentration of our work in California, where the climate is generally temperate, weather could have an increasingly frequent or severe effect on our operation if general climatic changes occur or if we expand into other geographic regions that tend to experience more extreme weather conditions. Lengthy periods of wet or cold winter weather could interrupt construction, and this could lead to under-utilization of crews and equipment, resulting in less efficient rates of overhead recovery. Extreme heat could prevent us from performing certain types of operations. Changes in weather conditions could cause delays and otherwise significantly affect our project costs. While revenues might be recovered following a period of bad weather, it would generally be impossible to recover the cost of inefficiencies, and significant periods of bad weather typically would reduce profitability of affected contracts both in the current period and during the future life of affected contracts. Such reductions in contract profitability would negatively affect our results of operations.

Timing of the award and performance of new contracts could have an adverse effect on our operating results and cash flow.

A substantial portion of our revenues and earnings is generated from large-scale project awards. The timing of project awards is unpredictable and outside of our control. Awards, including expansions of existing projects, often involve complex and lengthy negotiations and competitive bidding processes. These processes can be impacted by a wide variety of factors including a customer’s decision to not proceed with the development of a project, governmental approvals, financing contingencies, commodity prices, environmental conditions and overall market and economic conditions. We may not win contracts that we have bid upon due to price, a customer’s perception of our ability to perform and/or perceived technology advantages held by others. Many of our competitors may be more inclined to take greater or unusual risks or terms and conditions in a contract that we might not deem acceptable. Because a significant portion of our revenues is generated from large projects, our results of operations can fluctuate quarterly and annually depending on whether and when large project awards occur and the commencement and progress of work under large contracts already awarded. As a result, we are subject to the risk of losing new awards to competitors or the risk that revenue may not be derived from awarded projects as quickly as anticipated.

The uncertainty of the timing of contract awards may also present difficulties in matching the size of our equipment fleet and work crews with contract needs. In some cases, we may maintain and bear the cost of more equipment and ready work crews than are currently required, in anticipation of future needs for existing contracts or expected future contracts. If a contract is delayed or an expected contract award is not received, we would incur costs that could have a material adverse effect on our anticipated profit.

In addition, the timing of the revenues, earnings and cash flows from our contracts can be delayed by a number of factors, including adverse weather conditions, such as prolonged or intense periods of rain, snow, storms or flooding; delays in receiving material and equipment from suppliers and services from subcontractors; and changes in the scope of work to be performed. Such delays, if they occur, could have adverse effects on our operating results for current and future periods until the affected contracts are completed.

Our participation in construction joint ventures exposes us to liability and/or harm to our reputation for failures of our partners.

As part of our business, we are a party to joint venture arrangements, pursuant to which we typically jointly bid on and execute particular projects with other companies in the construction industry. Success on these joint projects depends upon managing the risks discussed in the various risks described in these “Risk Factors” and on whether our joint venture partners satisfy their contractual obligations.

14

We and our joint venture partners are generally jointly and severally liable for all liabilities and obligations of our joint ventures. If a joint venture partner fails to perform or is financially unable to bear its portion of required capital contributions or other obligations, including liabilities stemming from lawsuits, we could be required to make additional investments, provide additional services or pay more than our proportionate share of a liability to make up for our partner’s shortfall. Furthermore, if we are unable to adequately address our partner’s performance issues, the customer may terminate the project, which could result in legal liability to us, harm to our reputation and reduction to our profit on a project.

In connection with acquisitions, certain counterparties to joint venture arrangements, which may include our historical direct competitors, may not desire to continue such arrangements with us and may terminate the joint venture arrangements or not enter into new arrangements. Any termination of a joint venture arrangement could cause us to reduce our backlog and could materially and adversely affect our business, results of operations and financial condition.

An inability to obtain bonding could limit the aggregate dollar amount of contracts that we are able to pursue.

As is customary in the construction business, we are required to provide surety bonds to our customers to secure our performance under construction contracts. Our ability to obtain surety bonds primarily depends upon our capitalization, working capital, past performance, management expertise and reputation and certain external factors, including the overall capacity of the surety market. Surety companies consider such factors in relationship to the amount of our backlog and their underwriting standards, which may change from time to time. Events that adversely affect the insurance and bonding markets generally may result in bonding becoming more difficult to obtain in the future, or being available only at a significantly greater cost. Our inability to obtain adequate bonding would limit the amount that we can bid on new contracts and could have a material adverse effect on our future revenues and business prospects.

We may be unable to identify and contract with qualified Disadvantaged Business Enterprise (“DBE”) contractors to perform as subcontractors.