Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - Hospitality Investors Trust, Inc. | v425465_8k.htm |

Exhibit 99.1

THIS IS NEITHER AN OFFER TO SELL NOR A SOLICITATION OF AN OFFER TO BUY THE SECURITIES DESCRIBED HEREIN . AN OFFERING IS MADE ONLY BY PROSPECTUS . THIS LITERATURE MUST BE PRECEDED OR ACCOMPANIED BY A CURRENT PROSPECTUS . AS SUCH, A COPY OF THE CURRENT PROSPECTUS MUST BE MADE AVAILABLE TO YOU IN CONNECTION WITH THIS OFFERING AND SHOULD BE READ IN ORDER TO UNDERSTAND FULLY ALL OF THE IMPLICATIONS AND RISKS OF THIS OFFERING . No offering is made except by a prospectus filed with the Department of Law of the State of New York . Neither the Attorney - General of the State of New York nor any other state or federal regulator has passed on or endorsed the merits of this offering or these securities or confirmed the adequacy or accuracy of the prospectus . Any representation to the contrary is unlawful . All information contained in this material is qualified in its entirety by the terms of the current prospectus . The achievement of any goals is not guaranteed . An investment should only be made after a careful review of the prospectus . Publicly Registered Non - Traded Real Estate Investment Trust

American Realty Capital Hospitality Trust, Inc. 2 IMPORTANT INFORMATION REGARDING THE OFFERING Risk Factors Investing in our common stock involves a high degree of risk . You should purchase these securities only if you can afford a complete loss of your investment . See the section entitled “Risk Factors” in the prospectus for a discussion of the risks which should be considered in connection with your investment in our common stock . Forward - Looking Statements This presentation may contain forward - looking statements . You can identify forward - looking statements by the use of forward looking terminology such as “believes,” “expects,” “may,” “will,” “would,” “could,” “should,” “seeks,” “intends,” “plans,” “projects,” “estimates,” “anticipates,” “predicts,” or “potential” or the negative of these words and phrases or similar words or phrases . Please review the end of this presentation and the fund’s prospectus for a more complete list of risk factors, as well as a discussion of forward - looking statements and other offering details.

American Realty Capital Hospitality Trust, Inc. 3 ▪ Hospitality Trust, Inc. owns select - service and full - service hotels: ▪ Affiliated with premium national brands such as Hilton, Marriott and Hyatt ▪ Operated by experienced management companies ▪ Located in strong U.S. markets with diverse demand generators ▪ Well - maintained , with minimum deferred maintenance or capital required ▪ Lead market with superior rates, occupancies and cash flows ▪ Purchased at a discount to replacement cost Capital Preservation Capital Appreciation Monthly Cash Distributions Hospitality Trust seeks to provide: INVESTMENT THESIS

Hotels Keys % NOI Summary by Brand 63 8,088 48.7% 51 5,592 40.0% 16 1,953 9.4% 2 224 1.1% 1 236 0.5% Independent 2 252 0.4% Total 134 16,345 100.0% Hotels Keys % NOI Top 5 Flags 46 5,609 30.7% 20 2,436 18.0% 17 1,573 13.8% 10 1,402 12.0% 15 1,953 9.4% Top 5 MSAs Hotels Keys % NOI Miami / W. Palm 7 780 6.5% Chicago 5 763 5.0% Phoenix 2 292 4.0% Orlando 3 610 3.6% San Diego 3 377 3.0% Portfolio Composition Geography (134 Hotels, 32 States) Top Hotels by State American Realty Capital Hospitality Trust, Inc. 4 CURRENT PORTFOLIO SNAPSHOT 22 12 11 9 6 6 5 5 FL TX TN GA KY IL MI LA

American Realty Capital Hospitality Trust, Inc. 5 STRONG FINANCIAL POSITION ($ in millions) 2015 Distribution Coverage Q1'15 Q2'15 Q3'15 MFFO $4.6 $19.2 $15.7 Distributions Paid $4.6 $7.8 $11.1 Distribution Coverage - Quarterly 100% 244% 141% Distribution Coverage - YTD 100% 191% 167% (1) Assumes 30 - day LIBOR of 20 bps applied to floating rate debt 2015E Financial Summary Current Capital Structure Hotels 134 $ Effective Rate (1) Keys 16,345 Purchase Price of Assets $2,115.5 States 32 Price Per Key ($000) $129.4 Occupancy 75.7% Mortgage Debt $1,181.4 3.94% ADR $118.04 Term Loan $122.8 3.95% RevPAR $89.31 Total Debt $1,304.2 3.94% RevPAR Growth 6.8% Cash $76.6 Total Revenues $555.9 Net Debt $1,227.6 Hotel EBITDA $180.7 Preferred Equity $312.9 7.50% Int. Coverage: Debt 3.5x Net Debt + Preferred Equity $1,540.5 Int. Coverage: Debt + Pref 2.4x Net Debt / Purchase Price 58.0% Net Debt + Preferred / Purchase Price 72.8%

American Realty Capital Hospitality Trust, Inc. 6 POSITIVE LODGING FUNDAMENTALS 0.6% 0.8% 0.9% 2.1% 2.5% 1.9% Luxury Upper Upscale Upscale Upper Midscale Midscale Economy U.S . Industry Performance 2015 (3) Record U.S. Performance (2) Demand - Supply Delta, YTD September 2015 (1) 2015 Lodging Demand Drivers Focus Chain Scales Outperforming Industry 2014: ▪ 2014 Room revenue of $133 billion: All - time annual record ▪ 2014 RevPAR growth of 8.3%: 97% of all submarkets achieved positive RevPAR growth in 2014 YTD 2015: ▪ Highest room demand, occupancy, ADR and RevPAR ever in 1H15 ▪ Strong occupancy ( 65.4%) and room demand growth (3.4%) through YTD September ▪ TTM September U.S. hotel room revenues of $141 billion ▪ RevPAR growth of 7.2% through YTD September ▪ Hotel values expected to increase 7% in 2015 and again in 2016 Record Increase in Household Net Worth (4) +$20T (29%) since 2012 Consumer Spending Growth (5) PCE rose 2.2% in 2Q15, the fastest since 2012 Strong Airline Fundamentals (6) 2Q15 profits of $5.0bn 2015E: 80% rise in net income Continued Manufacturing Sector Expansion (7) 34 consecutive months of expansion through October Occupancy Growth Exceeding Expectations (8) 65.8% in 2015E; highest level since 1981 Strong GDP Growth (5) 2Q15 growth of 3.9% 1.2% 2.9% 1.7% 5.1% 6.8% 1.0% 3.0% 2.0% 4.7% 6.7% Supply Demand Occupancy ADR RevPAR 2015E YTD September 2015 Source: (1) Smith Travel Research, Q3’15 ( 2) Smith Travel Research, Q3’15 (3) PFK Hospitality Research, LLC, Smith Travel Research, Q2/Q3’15 (4) Federal Reserve Bank of St. Louis, Goldman Sachs Investment Research (5) U.S. Department of Commerce (6) International Air Transport Association, Dallas Morning News (7) Institute for Supply Management (8) PKF Hospitality Research

American Realty Capital Hospitality Trust, Inc. 7 KEY INITIATIVES ▪ We intend to fund our remaining acquisition pipeline with transitional capital in the form of mezzanine financing or preferred equity ▪ Pipeline represents 32 hotels totaling a purchase price of $541.2 million ▪ Consists of six remaining acquisition tranches scheduled to close over the next five months from Summit Hotel Properties (16 hotels), Noble Investment Group (11 hotels) and Wheelock Street Capital (5 hotels) ▪ Explore deleveraging strategies ▪ Utilization of property free cash flow ▪ Potential sale of select assets ▪ New equity partner ▪ Establish NAV ▪ Expected Q1 2016

American Realty Capital Hospitality Trust, Inc. 8 ARC Hospitality Trust, Inc. is led by seasoned professionals with extensive institutional experience in the real estate and hospitality business. Edward T. Hoganson Chief Financial Officer ARC Hospitality Trust, Inc. Jonathan P. Mehlman President & Chief Executive Officer ARC Hospitality Trust, Inc. EXPERIENCED MANAGEMENT TEAM Paul Hughes Senior Vice President & Counsel ARC Hospitality Trust, Inc. James A. Carroll CEO, Property Manager Crestline Hotels & Resorts, LLC Aaron Deyerle Controller ARC Hospitality Trust, Inc.

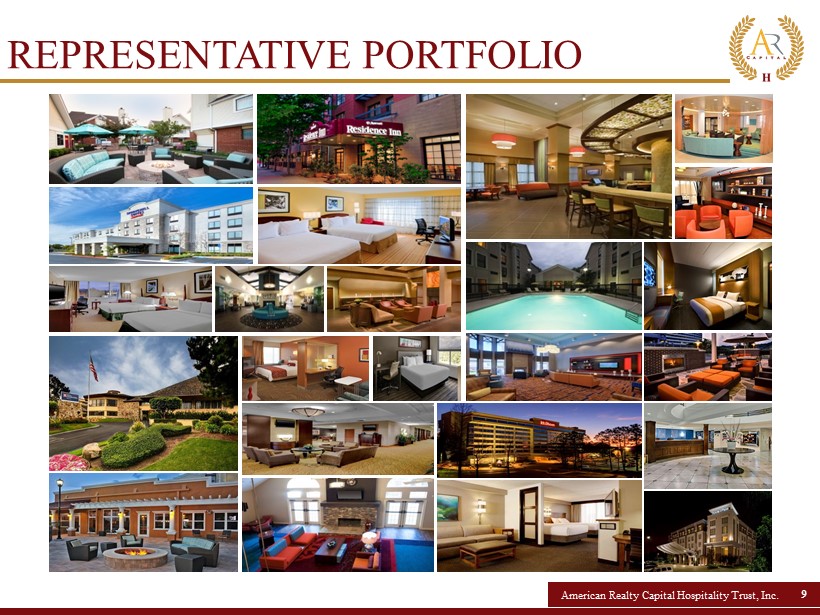

American Realty Capital Hospitality Trust, Inc. 9 REPRESENTATIVE PORTFOLIO

American Realty Capital Hospitality Trust, Inc. 10 Investing in our common stock involves a high degree of risk . You should purchase these securities only if you can afford a complete loss of your investment . See ‘‘Risk Factors’’ beginning on page 31 of the prospectus for a discussion of the risks that should be considered in connection with your investment in our common stock, including : • We intend to use substantial available proceeds from this offering to reduce our borrowings, including borrowings made in connection with the acquisition of a portfolio of 116 hotel assets, or the Grace Portfolio, by approximately $ 500 million, which may limit our ability to pay distributions from offering proceeds or acquire additional properties for some time . • Since our inception, all of our distributions have been paid from offering proceeds . Distributions paid from sources other than our cash flows from operations, particularly from proceeds of this offering, will result in us having fewer funds available to reduce our borrowings as intended and acquire additional properties and may adversely affect our ability to fund future distributions . • There is no guarantee that distributions will be paid or that you will receive any return on your investment . We expect that future distributions will be paid from our cash flows from operations following the acquisition of the Grace Portfolio, but there can be no assurance we will be able to generate sufficient cash flow from operations to maintain current cash distributions or increase distributions over time . • Because we are dependent upon our advisor, our property manager, our sub - property manager and their affiliates to conduct our operations, any adverse changes in the financial condition of these entities or our relationship with these entities could hinder our operating performance and the return on your investment . • No public market currently exists, or may ever exist, for shares of our common stock and our shares are, and may continue to be, illiquid . Our share repurchase program may be the only way to dispose of your shares, but there are a number of limitations placed on such repurchases . See ‘‘Share Repurchase Program . ’’ RISK FACTORS

American Realty Capital Hospitality Trust, Inc. 11 • Market conditions and other factors could cause us to delay our liquidity event beyond the sixth anniversary of the termination of the primary offering . We also cannot assure you that we will be able to achieve a liquidity event . • We established the initial offering price on an arbitrary basis ; as a result, the actual value of your investment may be substantially less than what you pay . • There are substantial conflicts among the interests of our investors, our interests and the interests of our advisor, property manager, our sub - property manager, our sponsor, our dealer manager and our and their respective affiliates, which could result in decisions that are not in the best interests of our stockholders . • Because our dealer manager is owned by an entity under common control with the parent of our sponsor, you will not have the benefit of an independent due diligence review of us, which is customarily performed in underwritten offerings . • We may change our investment objectives and strategies without stockholder consent . • We are obligated to pay fees to our advisor, which could be substantial and may result in our advisor recommending riskier investments . • We are obligated to pay the special limited partner a subordinated distribution upon termination of the advisory agreement, which may be substantial and therefore may discourage us from terminating the advisor . • We incurred substantial additional indebtedness to consummate the acquisition of the Grace Portfolio, or the Grace Acquisition, which could hinder our ability to pay distributions to our stockholders or could decrease the value of your investment if income on, or the value of, the property securing the debt falls . • Our failure to qualify or remain qualified as a REIT would result in higher taxes, may adversely affect our operations, would reduce the amount of income available for distribution and would limit our ability to pay distributions to our stockholders . • Commencing with the NAV pricing date, the offering price for shares in our primary offering and pursuant to our DRIP, as well as the repurchase price for our shares, will be based on NAV, which may not accurately reflect the value of our assets . • There are limitations on ownership and transferability of our shares . Please see ‘‘Description of Securities — Restrictions on Ownership and Transfer . ’’ RISK FACTORS

American Realty Capital Hospitality Trust, Inc. 12 MFFO DISCLOSURE This presentation contains modified funds from operations (“MFFO”), a non - GAAP measure which the Investment Program Association (“IPA”) has recommended as a supplemental measure for publicly registered, non - listed REITs. We believe MFFO is reflective of the ongoing operating performance of publicly registered, non - listed REITs by adjusting for those costs that are more reflective of acquisitions and investment activity, along with other items the IPA believes are not indicative of the ongoing operating performance of a publicly registered, non - listed REIT, such as straight - lining of rents as required by GAAP. We believe that MFFO can provide, on a going - forward basis, an indication of the sustainability (that is, the capacity to continue to be maintained) of our operating performance after the period in which we are acquiring properties and once our portfolio is stabilized. MFFO is not equivalent to our net income or loss as determined under GAAP. Not all publicly registered, non - listed REITs calculate MFFO the same way. Accordingly, comparisons with other non - listed REITs may not be meaningful. Furthermore, MFFO is not indicative of cash flow available to fund cash needs and should not be considered as an alternative to net income (loss) or income (loss) from continuing operations as determined under GAAP as an indication of our performance, as an alternative to cash flows from operations, as an indication of our liquidity, or indicative of funds available to fund our cash needs including our ability to make distributions to our stockholders. MFFO should be reviewed in conjunction with other GAAP measurements and should not be construed to be more relevant or accurate than the current GAAP methodology. Please refer to our filings with the SEC, including our most recent Quarterly Report on Form 10 - Q, for a reconciliation of our calculation of MFFO to our net income or loss as determined under GAAP.

American Realty Capital Hospitality Trust, Inc. archospitalityreit.com ▪ For account information, including balances and the status of submitted paperwork, please call us at (844) 276 - 1077 ▪ Financial Advisors may view client accounts, statements and tax forms at www.dstvision.com ▪ Shareholders may access their accounts at www.americanrealtycap.com