Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - GEOSPACE TECHNOLOGIES CORP | geos-ex231_25.htm |

| EX-32.1 - EX-32.1 - GEOSPACE TECHNOLOGIES CORP | geos-ex321_28.htm |

| EX-31.1 - EX-31.1 - GEOSPACE TECHNOLOGIES CORP | geos-ex311_30.htm |

| EX-23.2 - EX-23.2 - GEOSPACE TECHNOLOGIES CORP | geos-ex232_26.htm |

| EX-32.2 - EX-32.2 - GEOSPACE TECHNOLOGIES CORP | geos-ex322_29.htm |

| EX-21.1 - EX-21.1 - GEOSPACE TECHNOLOGIES CORP | geos-ex211_24.htm |

| EX-31.2 - EX-31.2 - GEOSPACE TECHNOLOGIES CORP | geos-ex312_27.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

x |

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the Fiscal Year Ended September 30, 2015 OR |

|

¨ |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission file number 001-13601

GEOSPACE TECHNOLOGIES CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

|

Texas |

|

76-0447780 |

|

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

7007 Pinemont Drive

Houston, Texas 77040-6601

(Address of Principal Executive Offices)

(713) 986-4444

(Registrant’s telephone number, including area code)

Securities Registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock |

|

The NASDAQ Global Market |

Securities Registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨ |

Accelerated filer x |

Non-accelerated filer ¨ |

Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

There were 13,147,916 shares of the Registrant’s Common Stock outstanding as of the close of business on October 31, 2015. As of March 31, 2015, the aggregate market value of the Registrant’s Common Stock held by non-affiliates was approximately $211 million (based upon the closing price of $16.51 on March 31, 2015, as reported by The NASDAQ Global Market).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the Registrant’s 2016 Annual Meeting of Stockholders are incorporated by reference into Part III of this report.

Item 1. Business

Business Overview

Geospace Technologies Corporation reincorporated as a Texas corporation effective April 16, 2015. We originally incorporated as a Delaware corporation on September 27, 1994. Unless otherwise specified, the discussion in this Annual Report on Form 10-K refers to Geospace Technologies Corporation and its subsidiaries. We design and manufacture instruments and equipment used in the oil and gas industry to acquire seismic data in order to locate, characterize and monitor hydrocarbon producing reservoirs. We also design and manufacture non-seismic products, including industrial products, offshore cables, thermal printing equipment and film. We report and categorize our customers and products into two different segments: Seismic and Non-Seismic.

We have engaged in the seismic instrument and equipment business since 1980 and market our products primarily to the oil and gas industry. Demand for our products has been, and will likely continue to be, vulnerable to downturns in the economy and the oil and gas industry in general. For more information, please refer to the risks discussed under the heading “Risk Factors”.

Products and Product Development

Seismic Products

Our seismic business segment accounts for the majority of our revenue. Geoscientists use seismic data primarily in connection with the exploration, development and production of oil and gas reserves to map potential and known hydrocarbon bearing formations and the geologic structures that surround them. Our seismic product lines currently consist of land and marine nodal data acquisition systems, permanent land and seabed reservoir monitoring products and services, geophones and geophone strings, hydrophones, leader wire, connectors, telemetry cables, marine streamer retrieval and steering devices and various other products. Our seismic products are compatible with most major competitive seismic data acquisition systems currently in use. We believe that our seismic products are among the most technologically advanced instruments and equipment available for seismic data acquisition.

Traditional Products

An energy source and a data recording system are combined to acquire seismic data. We provide many of the components of seismic data recording systems, including geophones, hydrophones, multi-component sensors, leader wire, geophone strings, connectors, seismic telemetry cables and other seismic related products. On land, our customers use geophones, leader wire, cables and connectors to receive and measure seismic reflections resulting from an energy source into data recording units, which store the seismic information for subsequent processing and analysis. In the marine environment, large ocean-going vessels tow long seismic cables known as “streamers” containing hydrophones which are used to detect pressure changes. Hydrophones transmit electrical impulses back to the vessel’s data recording unit where the seismic data is stored for subsequent processing and analysis. Our marine seismic products help steer streamers while being towed and help recover streamers if they become disconnected from the vessel.

Our seismic sensor, cable and connector products are compatible with most major competitive seismic data acquisition systems currently in use. Sales result primarily from seismic contractors purchasing our products as components of new seismic data acquisition systems or to repair and replace components of seismic data acquisition systems already in use.

Our products used in marine seismic data acquisition include our marine seismic streamer retrieval devices (“SRDs”). Occasionally, streamer cables are severed and become disconnected from the vessel as a result of obstacles, inclement weather, vessel traffic or human error. Our SRDs, which are attached to the streamer cables, contain air bags which are designed to inflate automatically at a given water depth, bringing the severed streamer cables to the surface. These SRDs save the seismic contractors significant time and money compared to the alternative of losing the streamer cable. We also produce seismic streamer steering devices, or “birds,” which are fin-like devices that attach to the streamer cable. These birds help maintain the streamer cable at a certain desired depth as it is being towed through the water.

Our wholly-owned subsidiary in the Russian Federation manufactures international standard geophones, sensors, seismic leader wire, seismic telemetry cables and related seismic products for customers in the Russian Federation and other international seismic

1

marketplaces. We have a branch office in Colombia that primarily rents seismic equipment to our customers in the South American market. Operating in foreign locations involves certain risks as discussed under the heading “Risk Factors – Our Foreign Subsidiaries and Foreign Marketing Efforts Face Additional Risks and Difficulties” in this Annual Report on Form 10-K.

Wireless Products

We have developed a land-based wireless (or nodal) seismic data acquisition system called the GSX. Each GSX station operates independently and therefore can be deployed in virtually unlimited channel configurations. Rather than utilizing interconnecting cables as required by most traditional land data acquisition systems, each GSX station operates as an independent data collection system. As a result, our GSX system requires less maintenance, which we believe allows our customers to operate more effectively and efficiently because of its reduced environmental impact, lower weight and ease of operation. Our GSX system is designed into configurations ranging from one to four channels per station. Since its introduction in 2008 and through September 30, 2015, we have sold 331,000 GSX channels and we have 130,000 GSX channels in our rental fleet. We do not expect to expand our GSX rental fleet in the foreseeable future.

We have also developed a marine-based wireless seismic data acquisition system called the OBX. Similar to our GSX land-based wireless system, the marine OBX system can be deployed in virtually unlimited channel configurations and does not require interconnecting cables between each station. Our deep water versions of the OBX system can be deployed in depths of up to 3,450 meters. Through September 30, 2015, we have sold 450 OBX stations and we have 4,400 OBX stations in our rental fleet. We expect to make additional investments in our OBX rental fleet in fiscal year 2016 as a result of a recent agreement executed with an international seismic contractor.

Reservoir Products

Seismic surveys repeated over selected time intervals show dynamic changes within the reservoir and can be used to monitor the effects of oil and gas production. In this regard, we have developed permanently installed high-definition reservoir monitoring systems for land and ocean-bottom applications in producing oil and gas fields. We also produce a retrievable version of our ocean-bottom system for use on fields where permanently installed systems are not appropriate or economical. Utilizing these tools, producers can enhance the recovery of oil and gas deposits over the life of a reservoir.

Our high-definition reservoir monitoring products include the HDSeis™ product line and a suite of borehole and reservoir monitoring products and services. Our HDSeis™ system is a high-definition seismic data acquisition system with flexible architecture that allows it to be configured as a borehole seismic system or as a subsurface system for both land and marine reservoir-monitoring projects. The scalable architecture of the HDSeis™ system enables custom designed system configuration for applications ranging from low-channel engineering and environmental-scale surveys requiring a minimum number of recording channels to high-channel surveys required to efficiently conduct permanent reservoir imaging and monitoring. Modular architecture allows virtually unlimited channel expansion. In addition, multi-system synchronization features make the HDSeis™ system well suited for multi-well or multi-site acquisition, simultaneous surface and downhole acquisition and continuous reservoir monitoring projects.

Reservoir monitoring requires special purpose or custom designed systems in which portability becomes less critical and functional reliability assumes greater importance. This reliability factor helps assure successful operations in inaccessible locations over a considerable period of time. Additionally, reservoirs located in deep water or harsh environments require special instrumentation and new techniques to maximize recovery. Reservoir monitoring also requires high-bandwidth, high-resolution seismic data for engineering project planning and reservoir management. We believe our HDSeis™ System and tools, designed for cost-effective deployment and lifetime performance, will make borehole and seabed seismic acquisition a cost-effective and reliable process for the challenges of reservoir monitoring. Our multi-component seismic product developments include an omni-directional geophone for use in reservoir monitoring, a compact marine three-component or four-component gimbaled sensor and special-purpose connectors, connector arrays and cases.

In November 2012, we received an order from Statoil (the “Statoil Order”) for $171.7 million, including amendments, to instrument two reservoirs in the North Sea. During the fiscal years ended September 30, 2013 and 2014, we recognized revenue of $109.6 million and $62.1 million, respectively, from the Statoil Order using the percentage of completion revenue recognition method.

2

During the fiscal year ended September 30, 2014, we also delivered a $5.0 million permanent land reservoir monitoring system for use in Saudi Arabia and a $4.4 million system to enlarge BP’s existing Valhall field system. We did not deliver nor did we receive orders for any permanent reservoir monitoring systems during fiscal year 2015.

In addition, we produce seismic borehole acquisition systems which employ a fiber optic augmented wireline capable of very high data transmission rates. These systems are used for several reservoir monitoring applications, including an application pioneered by us allowing operators and service companies to monitor and measure the results of fracturing operations.

Non-Seismic Products

Our non-seismic businesses leverage upon our existing manufacturing facilities and engineering capabilities. We have found that many of our seismic products, with little or no modification, have direct application to industries beyond those involved in oil and gas exploration and development. For example, our customers utilize our borehole tools to monitor subsurface carbon dioxide injections and for mine safety applications.

Our non-seismic products include thermal imaging products targeted at the commercial graphics industry as well as various industrial products. Our industrial products include (i) sensors and tools for vibration monitoring, mine safety application and earthquake detection, (ii) cables for power and communication for the offshore oil and gas and offshore construction industries, and (iii) water meter cables and other specialty industrial cable and connector products.

Business Strategy

Our long-term business strategy is focused on continued investment in research and development, expansion of our manufacturing and engineering capacity, expansion of our seismic equipment rental business, selective acquisitions, reinvestment of profits and minimizing debt obligations.

|

|

· |

Continue Investment in Research and Development – Historically, our growth has been driven through our internal development of new products targeted at the seismic industry. In past years, our seismic product innovations included the introduction of borehole seismology tools, seabed permanent reservoir monitoring systems and wireless data acquisition systems. These innovative technologies are the result of our continuous investment in research and development initiatives, even during difficult industry cycles when we experience a significant decline in customer demand for our products. We believe our past growth is a direct result of this strategy and we intend to continue such research and development investments. |

|

|

· |

Attract and Retain Engineering Staff – Our engineering staff has been key to our success, we intend to continue our tradition of retaining and attracting engineering staff and providing appropriate compensation and benefits. |

|

|

· |

Expand Manufacturing and Engineering Capacity to Accommodate Future Growth – Our new product innovations have led to significant revenue growth in previous years. Since our initial public offering in 1997 and through fiscal year 2015, we have expanded our manufacturing, warehousing, engineering and office space from 99,000 square feet to 648,000 square feet. Early in fiscal year 2013, we received a large order from Statoil to design and manufacture two seabed permanent reservoir monitoring systems. This order required substantially all of our manufacturing capacity and capabilities for a period of approximately 18 months, requiring us to outsource many of our routine manufacturing activities and to turn away potential customer orders for other products. Furthermore, we had no spare manufacturing capacity to accommodate any other large order for a permanent reservoir monitoring system, should one have occurred. We believe we are the world leader in the design and manufacture of these systems. As such, we expect to receive future orders for large-scale reservoir monitoring systems which may exceed the magnitude of the Statoil Order, although the timing and frequency of such orders, if any, is unknown. We are currently experiencing depressed industry conditions as a result of lower crude oil prices and their impact upon capital spending in the oil and gas industry worldwide. The resulting significant decline in seismic product orders and, in particular, the lack of any orders for permanent reservoir monitoring systems, have required us to defer our plans to expand our manufacturing and engineering facilities until product demand, including demand for large permanent reservoir monitoring systems, and factory capacity utilization return to levels comparable to those we experienced during fiscal year 2013. |

3

|

|

· |

Expand our Seismic Equipment Rental Business – We have offered seismic equipment to our customers on a rental basis for many years, originally through our subsidiary in Canada. Following our introduction of new wireless data acquisition technology in 2008, we began offering our newly introduced GSX systems for rent in 2009, and at that time we initiated a rental fleet of 2,000 GSX channels. At the conclusion of fiscal year 2015, our rental fleet contained 130,000 GSX channels which are warehoused in North America, South America and Europe. Many current owners of our GSX channels were initially introduced to the product through a rental. We believe this rental strategy has contributed to the sale of 331,000 GSX channels since its introduction in 2008. We have also expanded this rental strategy to our marine OBX wireless system. At the conclusion of fiscal year 2015, our rental fleet contained 4,400 OBX stations. While demand has declined substantially for the rental of our GSX equipment due to the significant underutilization of customer-owned land data acquisition systems, we expect our OBX rental revenue to increase in fiscal year 2016 as a result of a recent agreement executed with an international seismic contractor. We plan to meet this demand by adding additional OBX stations to our rental fleet. We believe our rental business creates opportunities for us to demonstrate the qualities and benefits of new products like the GSX and OBX to potential customers without requiring the customer to make a large upfront capital investment. As a result, we will continue adding new product technologies to our rental fleet to meet customer demand. |

|

|

· |

Selectively Pursue Acquisitions of Businesses with Technological and Engineering Overlap – The seismic industry periodically experiences volatile business cycles requiring us to rapidly increase and decrease our business activities to meet the industry’s demand for our products. The seismic industry generally offers equipment manufacturers like us limited visibility into new orders creating challenges for us to manage our manufacturing capacity, workforce and working capital. While our primary growth initiative is to expand our seismic product offerings, we may also seek out other non-seismic business opportunities which complement our existing products, engineering and manufacturing capabilities, and company-wide culture. While we routinely evaluate both seismic and non-seismic business acquisition opportunities, we may direct these efforts toward non-seismic businesses in order to diversify our revenue base and expose us to different markets with different business cycles. |

|

|

· |

Reinvest Profits and Minimize Debt Obligations – Our growth over the years has resulted from the reinvestment of our cash profits back into engineering projects, plant additions, rental fleet development and expansion, small niche acquisitions and working capital expansion. While we are not opposed to moderate amounts of short-term debt during favorable business cycles, we choose to minimize our exposure to long-term debt obligations which, in our view, restrict our ability to operate during periodic difficult business cycles in the seismic industry similar to the current business environment. We believe this strategy has allowed us to achieve higher revenue and profit growth than our peers, many of whom have significant long-term debt burdens. We also believe that the value of our common shares outstanding will be best served in the long-term by reinvesting our cash profits back into the business. In this regard, we do not anticipate paying any cash dividends in the foreseeable future, nor do we expect to initiate a buy-back program to repurchase our common stock. |

Segment and Geographic Information

We report and categorize our sales and products into two business segments: Seismic and Non-Seismic. Our Seismic product lines currently include land and marine wireless data acquisition systems, seabed permanent reservoir monitoring systems and services, geophones and geophone strings, hydrophones, leader wire, connectors, telemetry cables, marine streamer retrieval and steering devices and various other products. Our Non-Seismic product lines include thermal imaging and industrial products. Frequently, we have a minor amount of Seismic product sales to our Non-Seismic customers. For a discussion of financial information by segment and geographic area, see Note 19 to the consolidated financial statements contained in this Annual Report on Form 10-K.

Competition

Seismic Products

We are one of the world’s largest designers and manufacturers of seismic related products. The principal competitors for many of our traditional seismic products are Sercel (a division of CGG), ION Geophysical (“ION”), INOVA (a joint venture formed in 2009 between ION and Bureau of Geophysical Prospecting, a subsidiary of China National Petroleum Company) and Steward Cable (a

4

division of Amphenol Corporation). Furthermore, entities in China affiliated with Sercel as well as other Chinese manufacturers produce low-cost geophones meeting current industry standards. Geophones are generally price sensitive, so the ability to manufacture these products at a low cost is essential to maintain market share. We believe our primary competitor in the manufacture of our marine products is Sercel.

The primary competitors for our land wireless data acquisition systems are Sercel, Fairfield Industries, INOVA Wireless Seismic and numerous smaller entities. We believe the primary competitors for our marine nodal data acquisition systems are marine seismic data acquisition service providers like Fairfield Industries, Seabed Geosolutions (a joint venture formed between Fugro and CGG), and Magseis ASA, each of whom utilizes their own proprietary nodal technology. For land and marine wireless data acquisition systems, while price is an important factor in a customer’s decision to purchase the product, we believe customers also place a high value on a product’s historical performance and the ongoing engineering and field support provided by the product’s manufacturer.

Our primary competitors for rental of our traditional and wireless seismic equipment are Mitcham Industries, Inc. and Seismic Equipment Solutions.

Our primary competitors for our seabed permanent reservoir monitoring systems are Alcatel-Lucent and Petroleum Geo-Services ASA. We believe our primary competitors for high-definition borehole seismic data acquisition systems are Avalon Sciences Ltd and Sercel. A product’s historical performance, field support and engineering capabilities are important factors for receiving orders for our seismic reservoir products.

The principal keys for success in the seismic instruments and equipment market are technological superiority, product durability, reliability, and customer support. Price and product delivery are always important considerations for our customers. In general, most customers prefer to standardize data acquisition systems, geophones and hydrophones, particularly if they are used by seismic companies that have multiple crews which are able to support each other. This standardization makes it difficult for competitive manufacturers to gain market share from other manufacturers with existing customer relationships.

As mentioned above, a key factor for seismic instruments and equipment manufacturers is durability under harsh field conditions. Seismic instruments and equipment must meet not only rigorous technical specifications regarding signal integrity and sensitivity, but must also be extremely rugged and durable to withstand the rigors of field use, often in harsh environments.

Non-Seismic Products

There are numerous competitors and competitive technologies for our thermal imaging products including other thermal device manufacturers and manufacturers of direct-to-screen and inkjet solutions similar to those offered by Hewlett Packard. Our non-seismic industrial products face competition from numerous domestic and international specialty product manufacturers.

Suppliers

We purchase raw materials from a variety of suppliers located in various countries. We typically have multiple suppliers for our critical materials.

We produce our own brand of dry thermal film internally. We also purchase a substantial quantity of dry thermal film manufactured by Agfa-Gevaert N.V. In addition, we manufacture variants of our marine wireless products using a timing device manufactured by Microsemi Corporation. For a discussion of the risks related to our reliance on these suppliers, see “Risk Factors – We Rely on Key Suppliers for Certain Components Used in Our Products.”

We do not currently experience any significant difficulties in obtaining raw materials from our suppliers for the production of our seismic or non-seismic products.

5

Product Manufacturing and Assembly

Our manufacturing and product assembly operations consist of machining, molding or cabling the necessary component parts, configuring these parts along with components received from various vendors and assembling a final product. We manufacture seismic equipment to the specifications of our customers. For example, we can armor cables for applications such as deep water uses. We assemble geophone strings and seismic telemetry cables based on a number of customer choices such as length, gauge, tolerance and color of molded parts. With regard to dry thermal film, we mix and react various chemicals to formulate a reactive layer that is then coated onto a clear polyester film. Upon completion of our manufacturing and assembly operations, we test our final products to the functional and, in the case of seismic equipment, environmental extremes of product specifications and inspect the products for quality assurance. Consistent with industry practice, we normally manufacture and ship our products based on customer orders and, therefore, typically do not maintain significant inventories of finished goods held for sale, although we do stock significant amounts of finished good sub-assemblies in anticipation of future customer orders.

Markets and Customers

Our principal customers for our traditional and wireless seismic products are seismic contractors and, to a lesser extent, major independent and government-owned oil and gas companies that either operate their own seismic crews or specify seismic instrument and equipment preferences to contractors. For our deep water permanent reservoir monitoring products, our customers are generally large international oil and gas companies that operate long-term offshore oil and gas producing properties. Our thermal imaging customers primarily consist of direct users of our equipment as well as specialized resellers that focus on the newsprint, silkscreen and corrugated box printing industries. Our industrial product customers consist of specialty manufacturers, research institutions and industrial product distributors. No customer comprised 10% of our revenue during fiscal year 2015. Revenue recognition for the Statoil Order comprised 26.2% and 36.5% of our revenue for fiscal years 2014 and 2013, respectively. The following table describes our sales by customer type (in thousands):

|

|

YEAR ENDED SEPTEMBER 30, |

|

|||||||||

|

|

2015 |

|

|

2014 |

|

|

2013 |

|

|||

|

Traditional seismic exploration product revenue |

$ |

30,083 |

|

|

$ |

52,001 |

|

|

$ |

49,782 |

|

|

Wireless seismic exploration product revenue |

|

25,070 |

|

|

|

78,636 |

|

|

|

87,316 |

|

|

Seismic reservoir product revenue |

|

5,412 |

|

|

|

84,309 |

|

|

|

138,103 |

|

|

Non-seismic product revenue |

|

23,758 |

|

|

|

21,420 |

|

|

|

24,578 |

|

|

Other |

|

544 |

|

|

|

546 |

|

|

|

828 |

|

|

|

$ |

84,867 |

|

|

$ |

236,912 |

|

|

$ |

300,607 |

|

Intellectual Property

We seek to protect our intellectual property by means of patents, trademarks, trade secrets and other measures. Although we do not consider any single patent essential to our success, we consider our patents regarding our marine seismic cable retrieval devices to be of particular value to us. These patents are scheduled to expire in 2022. At this time we are not able to predict the effect of the patent expiration. We also hold patents on geophones, micro-geophones and seismic data acquisition and have pending applications on related technology. We protect our proprietary rights to our technology through a variety of methods, including confidentiality agreements and proprietary information agreements with suppliers, employees, consultants and others who may have access to proprietary information.

Research and Development

We expect to incur significant future research and development expenditures aimed at the development of additional seismic and non-seismic products. We have incurred company-sponsored research and development expenses of $14.7 million, $16.5 million and $14.7 million during the fiscal years ended September 30, 2015, 2014 and 2013, respectively.

6

Employees

As of September 30, 2015, we employed 978 people predominantly on a full-time basis, of which 659 were employed in the United States, 277 in the Russian Federation and the remainder in the United Kingdom, Canada, China and Colombia. Our employees in the Russian Federation belong to a national union for machine manufacturers. Our remaining employees are not unionized. We have never experienced a work stoppage and consider our relationship with our employees to be satisfactory.

Financial Information by Segment and Geographic Area

For a discussion of financial information by segment and geographic area, see Note 19 to the consolidated financial statements contained in this Annual Report on Form 10-K. For a description of risks attendant to our foreign operations, please see “Risk Factors - Our Foreign Subsidiaries and Foreign Marketing Efforts Face Additional Risks and Difficulties.”

Available Information

We file annual, quarterly and special reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). Our SEC filings are available to the public over the internet at the SEC’s website at www.sec.gov. You may also read and copy any document we file at the SEC’s public reference room at 100 F Street, NE, Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for further information on their public reference room. Our SEC filings are also available to the public on our website at www.geospace.com. Please note that information contained on our website, whether currently posted or posted in the future, is not a part of this Annual Report on Form 10-K or the documents incorporated by reference in this Annual Report on Form 10-K.

Item 1A. Risk Factors

Risk Factors

Commodity Price Levels May Affect Demand for Our Products, Which Has and Could Continue to Materially and Adversely Affect our Results of Operations and Liquidity

Demand for many of our products and the profitability of our operations depend primarily on the level of worldwide oil and gas exploration activity. Prevailing oil and gas prices, with an emphasis on crude oil prices, and market expectations regarding potential changes in such prices significantly affect the level of worldwide oil and gas exploration activity. During periods of improved energy commodity prices, the capital spending budgets of oil and natural gas operators tend to expand, which results in increased demand for our products. Conversely, in periods when these energy commodity prices deteriorate, such as is occurring in 2015, capital spending budgets of oil and natural gas operators tend to contract and the demand for our products generally weakens. Historically, the markets for oil and gas have been volatile and are subject to wide fluctuation in response to changes in the supply of and demand for oil and gas, market uncertainty and a variety of additional factors that are beyond our control. These factors include the level of consumer demand, supplies of oil and natural gas, regional and international economic conditions, weather conditions, domestic and foreign governmental regulations (including those related to climate change), price and availability of alternative fuels, political conditions, instability and hostilities in the Middle East and other significant oil-producing regions, increases and decreases in the supply of oil and gas, the effect of worldwide energy conservation measures and the ability of OPEC to set and maintain production levels and prices of foreign imports.

Slow economic recovery in the United States, uncertainty in the European markets and slowing economic growth in growing economies like those in China and India could lead to a decline in demand for crude oil and natural gas. Further slowdowns in economic activity would likely reduce worldwide demand for energy and result in an extended period of lower crude oil and natural gas prices. Any material changes in oil and gas prices or other market trends that adversely impact seismic exploration activity would likely affect the demand for our products and could materially and adversely affect our results of operations and liquidity.

Generally, as exists at present, imbalances in the supply and demand for oil and gas will ordinarily affect oil and gas prices and in such circumstances our company will be adversely affected as now with world supplies exceeding demand.

7

Our New Products Require a Substantial Investment by Us in Research and Development Expense and May Not Achieve Market Acceptance

Our outlook and assumptions are based on various macro-economic factors and internal assessments, and actual market conditions could vary materially from those assumed. In recent years, we have incurred significant expenditures to fund our research and development efforts, and we intend to continue those expenditures in the future. However, research and development is by its nature speculative, and we cannot assure you that these expenditures will result in the development of new products or services or that any new products and services we have developed recently or may develop in the future will be commercially marketable or profitable to us. In particular, we have incurred substantial expenditures to develop our land and marine wireless nodal seismic data acquisition systems, as well as other seismic products for permanent reservoir monitoring applications. In addition, we try to use some of our capabilities, particularly our cable manufacturing capabilities, to supply products to new markets. Further, we have incurred substantial expense and expended significant effort to develop our thermal solutions products. We cannot assure you that we will realize our expectations regarding acceptance of and revenue generated by our new products and services in existing or new markets.

The Short Term Nature of Our Order Backlog and Delayed or Canceled Customer Orders May Cause Us to Experience Fluctuations in Quarterly Results of Operations

Historically, the rate of new orders for our products has varied substantially from quarter to quarter. Moreover, we typically operate, and expect to continue operating, on the basis of orders in-hand for our products before we commence substantial manufacturing “runs.” The short-term nature of our order backlog for most products generally does not allow us to predict with any accuracy demand for our products more than approximately three months in advance. Thus, our ability to replenish orders and the completion of orders, particularly large orders for deep water permanent reservoir monitoring projects, can significantly impact our operating results and cash flow for any quarter, and results of operations for any one quarter may not be indicative of results of operations for future quarters.

Additionally, customers can delay or even cancel orders and rental contracts before delivery. For larger orders, we attempt to negotiate for a non-refundable deposit or cancellation penalties depending on our relationship with the customer. However, such deposits or penalties, even when obtained, may not fully compensate us for our inventory investment and forgone profits if the order is ultimately cancelled.

These periodic fluctuations in our operating results and the impact of any order delays/cancellations could adversely affect our stock price.

Our Credit Risk Could Increase and We May Incur Bad Debt Write-Offs if Our Customers Face Difficult Economic Circumstances

We believe that our allowance for bad debts is adequate in light of known circumstances. However, we cannot assure you that additional amounts attributable to uncollectible receivables and bad debt write-offs will not have a material adverse effect on our future results of operations. Many of our seismic customers are not well capitalized and as a result cannot always pay our invoices when due. We have in the past incurred write-offs in our accounts receivable due to customer credit problems. We have found it necessary from time to time to extend trade credit, including promissory notes, to long-term customers and others where some risks of non-payment exist. With the recent decline in oil prices and a decline in seismic activities around the world, some of our customers may experience significant liquidity difficulties, which increase those credit risks. An increase in the level of bad debts and any deterioration in our credit risk could adversely affect the price of our stock. In addition, we rent equipment to our customers which utilize such equipment in various countries around the world. If our rental customers experience financial difficulties, it could be difficult or impossible to retrieve our rental equipment from foreign countries.

8

Our Industry is Characterized by Rapid Technological Development and Product Obsolescence, Which May Affect Our Ability to Provide Product Enhancements or New Products on a Timely and Cost Effective Basis

Our instruments and equipment are constantly undergoing rapid technological improvement. Our future success depends on our ability to continue to:

|

|

· |

improve our existing product lines, |

|

|

· |

address the increasingly sophisticated needs of our customers, |

|

|

· |

maintain a reputation for technological leadership, |

|

|

· |

maintain market acceptance of our products, |

|

|

· |

anticipate changes in technology and industry standards, |

|

|

· |

respond to technological developments on a timely basis and |

|

|

· |

develop new markets for our products and capabilities. |

Current competitors or new market entrants may develop new technologies, products or standards that could render our products obsolete. We cannot assure you that we will be successful in developing and marketing, on a timely and cost effective basis, product enhancements or new products that respond to technological developments, that are accepted in the marketplace or that comply with new industry standards. Additionally, in anticipation of customer product orders, from time to time we acquire substantial quantities of inventories, which if not sold or integrated into products within a reasonable period of time, could become obsolete. In such case, we would be required to impair the value of such inventories on our balance sheet.

We Operate in Highly Competitive Markets and Our Competitors May Be Able to Provide Newer or Better Products Than We Are Able

The markets for most of our products are highly competitive. Many of our existing and potential competitors have substantially greater marketing, financial and technical resources than we do. Some competitors currently offer a broader range of instruments and equipment for sale than we do and may offer financing arrangements to customers on terms that we may not be able to match. In addition, new competitors may enter the market and competition could intensify. As to our non-seismic thermal solutions products, we compete with other printing solutions, including inkjet and laser printing technologies, many of which are provided by large companies with significant resources.

We cannot assure you that sales of our products will continue at current volumes or prices if current competitors or new market entrants introduce new products with better features, performance, price or other characteristics than our products. Competitive pressures or other factors may also result in significant price competition that could have a material adverse effect on our results of operations.

The Limited Market for Our Seismic Products Can Affect Our Revenue in the Seismic Business Segment

In our seismic business segment, we generally market our traditional and wireless products to seismic service contractors. We estimate that, based on published industry sources, fewer than 50 seismic contracting companies are currently operating worldwide (excluding those operating in the Russian Federation and the former Soviet Union, India, the People’s Republic of China and certain Eastern European countries, where seismic data acquisition activity is difficult to verify). We estimate that fewer than 20 seismic contractors are engaged in marine seismic exploration. Due to these market factors, a relatively small number of customers, some of whom are experiencing financial difficulties, account for most of our sales. From time to time, these seismic contractors have sought to vertically integrate and acquire our competitors, which has influenced their supplier decisions before and after such transactions. In addition, consolidation among our customers may further concentrate our business to a limited number of customers and expose us to increased risks related to dependence on a small number of customers. The loss of a small number of these customers could materially and adversely impact sales of our seismic products. We market our seabed permanent reservoir monitoring systems products to large oil and gas companies. Since this product’s introduction in 2002, we have received system orders from three offshore oil and gas operators including BP, Shell and Statoil, which have accounted for a significant portion of our revenue in fiscal year 2014 and prior

9

fiscal years. We did not deliver nor have we received orders for any permanent reservoir monitoring systems during fiscal year 2015 which caused a significant decline in our fiscal year 2015 revenue and profits from our seismic reservoir product segment.

We Cannot Be Certain of the Effectiveness of Patent Protection on Our Products

We hold and from time to time apply for certain patents relating to some of our seismic products. We also own several patents which relate to the development of dry thermal film. We cannot assure you that our patents will prove enforceable or free of challenge, that any patents will be issued for which we have applied or that competitors will not develop functionally similar technology outside the protection of any patents we have or may obtain.

Our Foreign Subsidiaries and Foreign Marketing Efforts Are Subject to Additional Political, Economic, Legal and Other Uncertainties Not Generally Associated with Domestic Operations

Based on customer billing data, sales to customers outside the United States accounted for approximately 40% of our sales during fiscal year 2015; however, we believe the percentage of sales outside the United States is much higher since many of our products are first delivered to a domestic location and ultimately shipped to a foreign location. We again expect sales outside of the United States to represent a substantial portion of our sales for fiscal year 2016 and subsequent years.

Foreign sales are subject to special risks inherent in doing business outside of the United States, including the risk of war, terrorist activities, civil disturbances, embargo and government activities, shifting foreign attitudes about conducting business activities with the United States, restrictions of the movement and exchange of funds, inhibitions of our ability to collect accounts receivable, international sanctions, expropriation and nationalization of our assets or those of our customers, currency fluctuations, devaluations and conversion restrictions, confiscatory taxation or other adverse tax policies and governmental actions that may result in the deprivation of our contractual rights, all of which may disrupt markets or our operations.

A portion of our manufacturing is conducted through our subsidiary Geospace Technologies Eurasia, which is based in the Russian Federation. Our business could be directly affected by political and economic conditions in the Russian Federation, including the current geopolitical instability involving the Russian Federation and Ukraine. In regards to Ukraine, sanctions levied by the United States government preclude the export of seismic equipment to the Russian Federation if it will be used directly or indirectly in Russia’s energy sector for exploration or production in (i) deepwater (greater than 500 feet), (ii) Arctic offshore or (iii) shale projects in Russia that have the potential to produce oil or gas. Furthermore, if an exporter is unable to determine whether its seismic equipment will be used in such projects, the export is prohibited. In fiscal year 2015, we imported $2.9 million of products from Geospace Technologies Eurasia for resale elsewhere in the world. If imports of these products from the Russian Federation are restricted by government regulation, we may be forced to find other sources for these products at potentially higher costs. Boycotts, protests, unfavorable regulations, additional governmental sanctions and other actions in the region could also adversely affect our ability to operate profitably. Delays in obtaining governmental approvals can affect our ability to timely deliver our products pursuant to contractual obligations, which could result in us being liable to our customers for damages. The risk of doing business in the Russian Federation and other economically or politically volatile areas could adversely affect our operations and earnings.

Foreign sales are also generally subject to the risk of compliance with additional laws, including tariff regulations and import and export restrictions. International sales of our products containing hydrophones require prior U.S. government approval in the form of an export license, which may be withheld by the U.S. government based upon factors which we cannot predict.

We may experience difficulties in connection with future foreign sales. Additionally, due to foreign laws and restrictions, should we experience substantial growth in certain foreign markets, for example in the Russian Federation, we may not be able to transfer cash balances to the United States to assist with debt servicing or other obligations.

10

Our Global Operations Expose Us to Risks Associated with Conducting Business Internationally, Including Failure to Comply with U.S. Laws Which Apply to International Operations, Such as the Foreign Corrupt Practices Act and US Export Control Laws, as well as the Laws of Other Countries

We have offices in Colombia, Canada, China, the Russian Federation and the United Kingdom, in addition to our offices in the United States. In additional to the risks noted above that are inherent in conducting business internationally, we are also liable for compliance with international and U.S. laws and regulations that apply to our international operations. These laws and regulations include data privacy requirements, labor relations laws, tax laws, anti-competition regulations, import and trade restrictions, export control laws, U.S. laws such as the Foreign Corrupt Practices Act and similar laws in other countries which also prohibit certain payments to governmental officials or certain payments or remunerations to customers. Many of our products are subject to U.S. export law restrictions that limit the destinations and types of customers to which our products may be sold, or require an export license in connection with sales outside the United States. Given the high level of complexity of these laws, there is a risk that some provisions may be inadvertently or intentionally breached, for example through fraudulent or negligent behavior of individual employees, our failure to comply with certain formal documentation requirements or otherwise. Additionally, we may be held liable for actions taken by our local dealers and partners. Violations of these laws and regulations could result in fines, criminal sanctions against us, our officers or our employees, and prohibitions on the conduct of our business. Any such violations could include prohibitions on our ability to offer our products in one or more countries and could materially damage our reputation, our brand, our international expansion efforts, our ability to attract and retain employees, our business and our operating results.

Our Strategy of Leasing Seismic Products Exposes Us to Additional Risks Relating to Equipment Recovery, Lease Renewals, Technological Obsolescence and Impairment of Assets

Our rental fleet of seismic equipment represents a significant portion of our assets and accounts for a growing portion of our revenue. Equipment leased by our customers is frequently located in foreign countries where retrieval of the equipment after the termination of the lease is difficult or impossible if the customer does not return the equipment. The costs associated with retrieving this equipment or the loss of equipment that is not retrieved could be significant and could adversely affect our operations and earnings.

The advancement of seismic technology having a significant competitive advantage over the equipment in our rental fleet could have an adverse effect on our ability to profitably lease and/or sell this equipment. Significant improvements in technology may also require us to recognize an asset impairment charge to our rental fleet investment and to invest significant sums to upgrade or replace our rental fleet with newer equipment demanded by our customers. In addition, rental contracts may not be renewed for equipment in our rental fleet, whether or not it has become obsolete. Significant technology improvements by our competitors could have an adverse effect on our results of operations and earnings.

Our equipment leasing business has high fixed costs, which primarily consist of depreciation expenses. In periods of declining rental revenue, these fixed costs generally do not decline. As a result, any significant decline in rental revenue caused by reduced demand could adversely affect our results of operations.

Cybersecurity Breaches and Other Disruptions of our Information Technology Network and Systems Could Adversely Affect our Business

We rely on information technology networks and systems, some of which are owned and operated by third parties, to process, transmit and store electronic information. In particular, we depend on our information technology infrastructure for a variety of functions, including worldwide financial reporting, inventory management, procurement, invoicing and email communications. Any of these systems may be susceptible to outages due to fire, floods, power loss, telecommunications failures, terrorist attacks and similar events. Despite the implementation of network security measures, our systems and those of third parties on which we rely may also be vulnerable to computer viruses, break-ins, malware and similar disruptions. Malware, if surreptitiously installed on our systems and not timely detected and removed, could collect and disclose sensitive information relating to our customers, employees or others, exposing us to legal liability and causing us to suffer reputational damage. It could also lead to disruptions in critical systems or the corruption or destruction of critical data. If we are unable to prevent such outages and breaches, these events could damage our reputation and lead to financial losses from remedial actions, loss of business or potential liability.

11

Because We Have No Plans to Pay Any Dividends for the Foreseeable Future, Investors Must Look Solely to Stock Appreciation for a Return on Their Investment in Us

We have not paid cash dividends on our common stock since our incorporation and do not anticipate paying any cash dividends in the foreseeable future. We currently intend to retain any future earnings to support our operations and growth. Any payment of cash dividends in the future will be dependent on the amount of funds legally available, our financial condition, capital requirements and other factors that our Board of Directors may deem relevant. Accordingly, investors must rely on sales of their common stock after price appreciation, which may never occur, as the only way to realize any future gains on their investment.

Unfavorable Currency Exchange Rate Fluctuations Could Adversely Affect Our Results of Operations

Substantially all of our third-party sales from the United States are made in U.S. dollars, though from time to time we may make sales in foreign currencies including intercompany sales. As a result, we may be subject to foreign currency fluctuations on our sales. The reporting currency for our financial statements is the U.S. dollar. However, the assets, liabilities, revenue and costs of our Russian, Canadian, United Kingdom, Chinese and Colombian subsidiaries are denominated in currencies other than U.S. dollars. To prepare our consolidated financial statements, we must translate those assets, liabilities, revenue and expenses into U.S. dollars at then-applicable exchange rates. Consequently, increases and decreases in the value of the U.S. dollar versus these other currencies will affect the amount of these items in our consolidated financial statements, even if their value has not changed in their original currency. These translations could result in significant changes to our results of operations from period to period. For the fiscal year ended September 30, 2015, approximately 10.6% of our consolidated revenue related to the operations of our foreign subsidiaries.

We Have a Relatively Small Public Float, and Our Stock Price May be Volatile

At September 30, 2015, we have approximately 12.8 million shares outstanding held by non-affiliates. This small float results in a relatively illiquid market for our common stock. Our daily trading volume for the year ended September 30, 2015 averaged approximately 267,000 shares. Our small float and daily trading volumes have in the past caused, and may in the future result in, significant volatility in our stock price.

We Rely on Key Suppliers for Certain Components Used in Our Products

While we currently manufacture dry thermal film, we also purchase a large quantity of dry thermal film from a European manufacturer through its distributor. Except for the film produced by us and sold to us by this manufacturer/distributor, we know of no other source for dry thermal film that performs well in our thermal imaging equipment. If we are unable to economically manufacture dry thermal film internally or the European manufacturer/distributor we rely on were to discontinue producing dry thermal film, were to become unwilling to contract with us on competitive terms or were unable to supply dry thermal film in sufficient quantities to meet our requirements, our ability to compete in the thermal imaging marketplace could be impaired, which could adversely affect our financial performance.

Certain models of our marine wireless products require a timing device we purchase from a United States manufacturer. We currently do not possess the ability to manufacture this component and have no other source for this device. If this manufacturer were to discontinue its production of this timing device, were to become unwilling to contract with us on competitive terms or were unable to supply the component in sufficient quantities to meet our requirements, our ability to compete in the marine wireless marketplace could be impaired, which could adversely affect our financial performance.

Our Success Depends Upon a Limited Number of Key Personnel

Our success depends on attracting and retaining highly skilled professionals. A number of our employees are highly skilled engineers and other professionals. In addition, our success depends to a significant extent upon the abilities and efforts of the members of our senior management team. If we fail to continue to attract and retain such professionals, our ability to compete in the industry could be adversely affected.

12

A General Downturn in the Economy in Future Periods May Adversely Affect Our Business

Slow economic recovery in the United States, uncertainty in the European markets and slowing growth in China and India and any other economic slowdown in future periods, could adversely affect our business in ways that we cannot predict. During times of economic slowdown, our customers may reduce their capital expenditures and defer or cancel pending projects and product orders. Such developments occur even among customers that are not experiencing financial difficulties. Any economic downturn may adversely affect the demand for oil and gas generally or cause volatility in oil and gas commodity prices and, therefore, adversely affect the demand for delivery of our products to the oil and gas industry. It could also adversely affect the demand for consumer products, which could in turn adversely affect our thermal solutions business. To the extent these factors adversely affect other seismic companies in the industry, there could be an oversupply of products and services and downward pressure on pricing for seismic products and services, which could adversely affect us. Additionally, bankruptcies or financial difficulties among our customers could reduce our cash flows and adversely impact our liquidity and profitability. See “The Limited Market for Our Seismic Products Can Affect Our Revenues in the Seismic Business,” above.

We Have a Minimal Disaster Recovery Program at our Houston Facilities

Due to its proximity to the Texas Gulf Coast, our facilities in Houston, Texas are annually subject to the threat of hurricanes, and the aftermath that follows. Hurricanes may cause, among other types of damage, the loss of electrical power for extended periods of time. If we lost electrical power at our Pinemont facility, or if a fire or other natural disaster occurred, we would be unable to continue our manufacturing operations during the power outage because we do not own a generator or any other back-up power source large enough to provide for our manufacturing power consumption needs. Additionally, we do not have an alternative manufacturing or operating location in the United States. Therefore, a significant disruption in our manufacturing operations could materially and adversely affect our business operations during an extended period of a power outage, fire or other natural disaster. We have a back-up generator to provide power for our information technology operations. We store our back-up data offsite and we replicate our mission critical data to an alternative cloud-based data center on a real-time basis. In the event of a major service interruption in our data center, we believe we would be able to activate our mission critical applications within less than 24 hours.

Our Credit Agreement Imposes Restrictions on Our Business

We and several of our subsidiaries are parties to a credit agreement with a bank. Amounts available for borrowing under the credit agreement are determined by a borrowing base, which is determined based upon certain of our assets. The credit agreement limits the incurrence of additional indebtedness, requires the maintenance of a single financial ratio that compares certain of our and our U.S. subsidiaries’ assets to certain of our liabilities, restricts our and our U.S. subsidiaries’ ability to pay cash dividends and contains other covenants customary in agreements of this type. Our ability to comply with these restrictions may be affected by events beyond our control, including, but not limited to, prevailing economic, financial and industry conditions and continuing declines in our sales of products. The breach of any of these covenants or restrictions, as well as any failure to make a payment of interest or principal when due, could result in a default under the credit agreement. Such a default would permit our lender to declare any amounts borrowed from it to be due and payable, together with accrued and unpaid interest, and the ability to borrow under the credit agreement could be terminated. If we are unable to repay any debts owed to our lender, the lender could proceed against the collateral securing that debt. While we intend to seek alternative sources of cash in such a situation, there is no guarantee that any alternative cash source would be available or would be available on terms favorable to us.

Reliance on Third Party Subcontractors Could Adversely Affect our Results of Operations and Reputation

We may rely on subcontractors to complete certain projects. The quality and timing of production and services by our subcontractors is not totally under our control. Reliance on subcontractors gives us less control over a project and exposes us to significant risks, including late delivery, substandard quality and high costs. The failure of our subcontractors to deliver quality products or services in a timely manner could adversely affect our profitability and reputation.

The High Fixed Costs of our Operations Could Adversely Affect our Results of Operations.

We have a high fixed cost structure primarily consisting of (i) depreciation expenses associated with our rental equipment and (ii) fixed manufacturing costs including salaries and benefits, taxes, insurance, maintenance, depreciation and other fixed

13

manufacturing costs. In regards to our rental equipment, large declines in the demand for rental equipment could result in substantial operating losses due to the on-going nature of rental equipment depreciation expense. Concerning our product manufacturing costs, in periods of low product demand our fixed costs generally do not decline or may decline only in modest increments. Therefore lower demand for our rental equipment and manufactured products could adversely affect our results of operations.

Our Long-Lived Assets May be Subject to Impairment.

We periodically assess our long-lived assets for impairment. Significant sustained future decreases in oil and natural gas prices may require us to write down the value of these assets if future cash flows anticipated to be generated from the related assets fall below the asset’s net book value. If we are forced to write down the value of our long-lived assets, these noncash asset impairments could adversely affect our results of operations.

Our Use of Percentage-of-Completion Method of Accounting Could Result in Volatility in our Results of Operations

We recognize revenue and profits from larger orders like the Statoil Order using the percentage-of-completion method of accounting. Although we currently have no orders in hand that will require us to utilize the percentage-of-completion method of accounting, we anticipate that such contracts will again occur in the future although we can give no assurances in this regard. This accounting method requires us to estimate contract costs and the profitability of our long-term contracts. While such estimates may be reasonably reliable when made, these estimates can change as a result of uncertainties associated with these types of contracts. Accordingly, we review the contract price and cost estimates periodically as our manufacturing efforts progress, and the cumulative impact of any periodic revisions to the contract price or cost estimates will be reflected in the period in which these changes become known, including, to the extent required, the recognition of losses at the time such losses are known and estimable, and such losses could be material. In addition, change orders can increase (sometimes substantially) the future scope and cost of a job. Therefore, change order awards (although frequently beneficial in the long-term) can have the short-term effect of reducing the contract’s percentage-of-completion and, thus, the revenue and profits that otherwise would be recognized to date.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

As of September 30, 2015, our operations included the following locations:

|

Location |

|

Owned/Leased |

|

Approximate Square Footage/Acreage |

|

Use |

|

Segment |

|

Houston, Texas |

|

Owned |

|

387,000 |

|

See Note 1 below |

|

Seismic and non-seismic |

|

Houston, Texas |

|

Owned |

|

77,000 |

|

See Note 2 below |

|

Corporate |

|

Houston, Texas |

|

Owned |

|

30,000 |

|

See Note 3 below |

|

Seismic |

|

Houston, Texas |

|

Owned |

|

17.3 acres |

|

See Note 4 below |

|

Seismic |

|

Houston, Texas |

|

Leased |

|

38,000 |

|

See Note 5 below |

|

Seismic |

|

Ufa, Bashkortostan, Russia |

|

Owned |

|

120,000 |

|

Manufacturing, sales and service |

|

Seismic |

|

Calgary, Alberta, Canada |

|

Owned |

|

45,000 |

|

Manufacturing, sales and service |

|

Seismic and non-seismic |

|

Luton, Bedfordshire, England |

|

Owned |

|

8,000 |

|

Sales and service |

|

Non-seismic |

|

Beijing, China |

|

Leased |

|

1,000 |

|

Sales and service |

|

Seismic |

|

Bogotá, Colombia |

|

Owned |

|

19,000 |

|

Sales and service |

|

Seismic |

While we believe that our facilities are adequate for our immediate needs, we are currently evaluating plans for the expansion of our Houston manufacturing and engineering facilities.

|

|

(1) |

This property is located at 7007 Pinemont Drive in Houston, Texas (the “Pinemont Facility”). The Pinemont Facility contains substantially all manufacturing activities and all engineering, selling, marketing and administrative activities for us in the United States. The Pinemont Facility also serves as our international corporate headquarters. |

14

|

|

(2) |

This property is located at 7334 N. Gessner in Houston, Texas. The property previously contained a manufacturing operation and certain support functions. The property is currently leased to a tenant under a lease agreement which expires in July 2020. |

|

|

(3) |

This property is located at 6410 Langfield Road in Houston, Texas. This facility provides additional warehousing and testing capacity for our manufacturing operations. |

|

|

(4) |

This property is located adjacent to the Pinemont Facility. It is currently being used as additional parking for the Pinemont Facility and legacy structures are being used to support our manufacturing and warehousing operations. Future expansion plans, if pursued, are expected to more fully utilize this property. |

|

|

(5) |

This property is located at 6855 Wynnwood, Houston, Texas. This property is used to assemble products and to warehouse inventories. The lease term for this facility expires on March 31, 2016 and there are no plans to extend the lease for this property. Our activities at this facility are expected to be moved to the Pinemont Facility. |

Item 3. Legal Proceedings

We are involved in various pending or potential legal actions in the ordinary course of our business. Management is unable to predict the ultimate outcome of these actions, because of the inherent uncertainty of litigation. However, management believes that the most probable, ultimate resolution of these matters will not have a material adverse effect on our consolidated financial position, results of operations or cash flows.

Item 4. Mine Safety Disclosures

None.

15

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

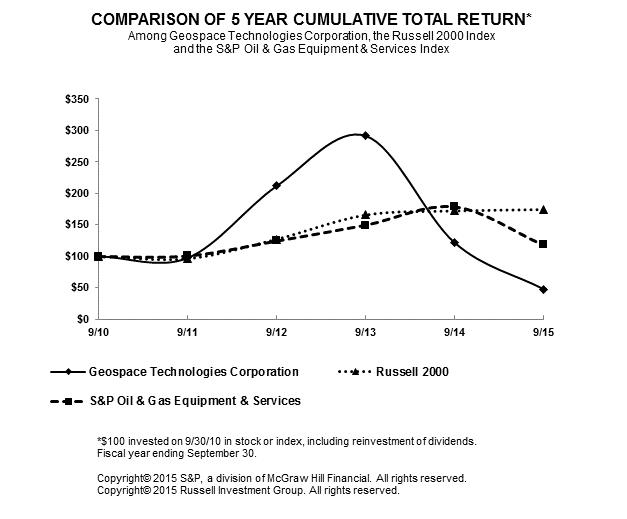

Stock Performance Graph

The following graph compares the performance of the Company’s common stock with the performance of the Russell 2000 index and the Standard & Poor’s Oil & Gas Equipment and Services index as of each of the dates indicated.

The graph assumes $100 invested on September 30, 2010 (a) in the Company’s common stock, (b) in the stocks comprising the Russell 2000 index on that day and (c) in the stocks comprising the Standard & Poor’s Oil & Gas Equipment and Services index on that day. Reinvestment of all dividends on stocks comprising the two indices is assumed. The foregoing graphs are based on historical data and are not necessarily indicative of future performance. These graphs shall not be deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulations 14A or 14C under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or to the liabilities of Section 18 of the Exchange Act.

Holders of Record

Our common stock is traded on The NASDAQ Global Market under the symbol “GEOS”. On October 31, 2015, there were approximately 74 holders of record of our common stock, and the closing price per share on such date was $15.36 as quoted by The NASDAQ Global Market.

16

Market Information for Common Stock

The following table shows the high and low per share sales prices for our common stock reported on The NASDAQ Global Market.

|

|

Low |

|

|

High |

|

||

|

Year Ended September 30, 2015: |

|

|

|

|

|

||

|

Fourth Quarter |

$ |

13.44 |

|

|

$ |

23.45 |

|

|

Third Quarter |

|

15.59 |

|

|

|

26.75 |

|

|

Second Quarter |

|

14.95 |

|

|

|

28.88 |

|

|

First Quarter |

|

24.07 |

|

|

|

35.32 |

|

|

|

|

|

|

|

|

|

|

|

Year Ended September 30, 2014: |

|

|

|

|

|

||

|

Fourth Quarter |

$ |

34.01 |

|

|

$ |

55.50 |

|

|

Third Quarter |

|

41.63 |

|

|

|

66.84 |

|

|

Second Quarter |

|

60.70 |

|

|

|

94.82 |

|

|

First Quarter |

|

79.60 |

|

|

|

107.93 |

|

Dividends

Since our initial public offering in 1997, we have not paid dividends, and we do not intend to pay cash dividends on our common stock in the foreseeable future. We presently intend to retain our earnings for use in our business, with any future decision to pay cash dividends dependent upon our growth, profitability, financial condition and other factors our Board of Directors may deem relevant. Our existing credit agreement also has covenants that materially limit our ability to pay dividends. For a discussion of our credit agreement, see the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources” contained in this Annual Report on Form 10-K.

Securities Authorized for Issuance under Equity Compensation Plans

The following equity plan information is provided as of September 30, 2015:

Equity Compensation Plan Information

|

Plan Category |

|

Number of Securities to be Issued upon Exercise of Outstanding Options, Warrants and Rights (a) |

|

|

Weighted-average Exercise Price of Outstanding Options, Warrants and Rights (b) |

|

|

Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans (Excluding Securities Reflected in Column (a)) (c) |

|

||

|

Equity Compensation Plans Approved by Security Holders |

|

89,700 |

|

|

$ |

17.27 |

|

|

|

1,476,000 |

|

During fiscal year 2015, we issued a total of 3,000 restricted shares of common stock to our directors. The weighted average grant date fair value of the shares issued was $19.13 per share. The restrictions on the shares issued lapse in four equal annual installments commencing on the first anniversary date of the issuance. The issuances were exempt from registration pursuant to Section 4(a)(2) under the Securities Act of 1933, as amended.

Recent Sales of Unregistered Securities and Use of Proceeds

None.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

None.

17

Item 6. Selected Consolidated Financial Data

The following table sets forth certain selected historical financial data on a consolidated basis. We have derived the selected consolidated financial information as of September 30, 2015 and 2014 and for fiscal years 2015, 2014 and 2013 from our audited consolidated financial statements appearing elsewhere in this Annual Report on Form 10-K. We have derived the selected consolidated financial information as of September 30, 2013, 2012 and 2011 and for fiscal years 2012 and 2011 from audited consolidated information not included herein. The selected consolidated financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in item 7 and our consolidated financial statements appearing elsewhere in this Annual Report on Form 10-K.

|

|

|

Year Ended September 30, |

|

|||||||||||||||||

|

|

|

2015 |

|

|

2014 |

|

|

2013 |

|

|

2012 |

|

|

2011 |

|

|||||

|

|

|

(in thousands, except share and per share amounts) |

|

|||||||||||||||||

|

Statement of Operations Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

|

$ |

84,867 |

|

|

$ |

236,912 |

|

|

$ |

300,607 |

|

|

$ |

191,664 |

|

|

$ |

172,970 |

|

|

Cost of revenue |

|

|

96,067 |

|

|

|

140,453 |

|

|

|

160,846 |

|

|

|

109,600 |

|

|

|

98,857 |

|

|

Gross profit (loss) |

|

|

(11,200 |

) |

|

|

96,459 |

|

|

|

139,761 |

|

|

|

82,064 |

|

|

|

74,113 |

|

|

Operating expenses: |

|

|

|

|

|

|

|