Attached files

| file | filename |

|---|---|

| 8-K - 8-K - OneMain Holdings, Inc. | shi-20150930xearningsrelea.htm |

Exhibit 99.1

SPRINGLEAF REPORTS THIRD QUARTER 2015 RESULTS

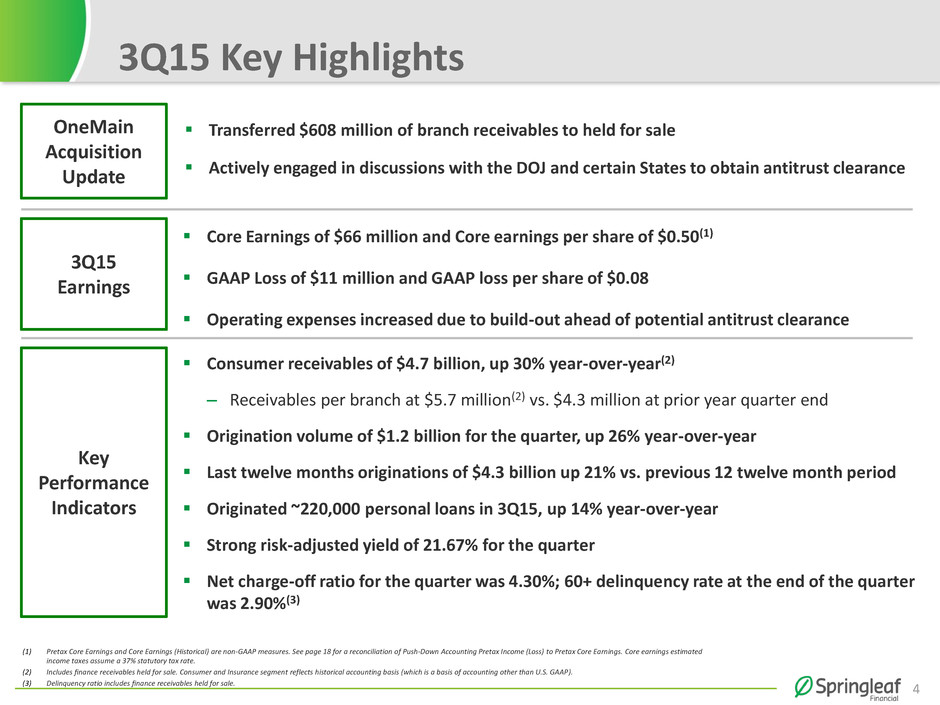

Evansville, IN, November 9, 2015 - Springleaf Holdings, Inc. (NYSE: LEAF) today reported a GAAP basis net loss of $11 million, or $0.08 per diluted share for the third quarter of 2015, compared with net income of $427 million or $3.70 per diluted share in the third quarter of 2014, which included a pretax gain of $641 million on the sale of real estate assets.

Core earnings (a non-GAAP measure) in consumer operations for the quarter were $66 million, a 3% increase from $64 million in the prior year quarter, and core earnings per diluted share (a non-GAAP measure) were $0.50 for the third quarter versus $0.55 in the prior year quarter.1,2 Weighted average diluted shares outstanding increased to 134.5 million for the third quarter of 2015 from 115.3 million for the prior year quarter as a result of the company’s issuance of 19.4 million common shares on May 4, 2015.

Third Quarter Highlights

• | Consumer net finance receivables reached $4.7 billion at September 30, 2015, an increase of $1.1 billion, or 30% from September 30, 2014, and up 9% from June 30, 2015. The $4.7 billion at September 30, 2015 included $825 million of direct auto loan receivables.3 |

• | Consumer net finance receivables per branch were $5.7 million3 at September 30, 2015, up 31% from $4.3 million at September 30, 2014, and up 9% from $5.2 million at June 30, 2015. |

• | Yield for our Consumer segment in the quarter was 25.97%, down 105 basis points from the third quarter of 2014. Risk-adjusted yield, representing yield less net charge-off rate, for our Consumer segment in the quarter was 21.67%, down 67 basis points from the third quarter of 2014. |

• | The company originated $1.2 billion of total consumer loans in the third quarter of 2015, including $278 million of direct auto loan originations, up $194 million from the third quarter of 2014. |

Jay Levine, President and CEO of Springleaf said, “Our results this quarter continue to demonstrate our ability to generate significant growth in total receivables and receivables per branch, both of which were up over 30% from last year’s quarter. Growing receivables per branch continues to be a key strategy for us because of the positive operating leverage provided by our largely fixed cost branch network. Consumer receivables per branch reached $5.7 million3, up from $4.3 million one year ago and from $5.2 million at June 30, 2015, reflecting our continued success with direct auto lending. Also contributing to our strong performance this quarter was the meaningful improvement in our net charge-off ratio from last year’s third quarter and the second quarter of this year.”

1 Excludes the impact of charges related to fair value adjustments on debt and earnings attributable to non-controlling interests.

2 Core Earnings income taxes assume 37% statutory tax rate.

3 3Q 2015 includes finance receivables held for sale.

1

Core Consumer Operations: (Reported on a historical accounting basis, which is a non-GAAP measure. Refer to the reconciliation of non-GAAP to comparable GAAP measures on page 10.)

Consumer and Insurance

Consumer and Insurance pretax income was $77 million in the third quarter of 2015, up 22% from $63 million in the third quarter of 2014, versus $76 million in the second quarter of 2015.4

Consumer net finance receivables reached $4.7 billion at September 30, 2015, an increase of 30% from September 30, 2014 and up 9% from June 30, 2015, driven by improved targeting and scoring algorithms which enhanced the quality of new customer leads, incremental internet customer acquisition, and continued strong growth in direct auto lending.5 Driven by these same factors, Consumer net finance receivables per branch continued to grow, reaching $5.7 million at September 30, 2015, up from $4.3 million at September 30, 2014 and $5.2 million at June 30, 2015.5

Net interest income was $250 million in the quarter, up 28% from the prior year quarter and 7% from the prior quarter. Yield in the current quarter was 25.97%, down 105 basis points from the prior year quarter, and 53 basis points from the second quarter of 2015, reflecting the impact of the successful roll-out of the company’s direct-to-consumer auto loan product. Risk adjusted yield was 21.67% in the third quarter of 2015, down 67 basis points from the third quarter of 2014 as the decline in yield more than offset the year-over-year improvement in net charge-offs. Risk adjusted yield grew 3 basis points from the second quarter of 2015.

The annualized net charge-off ratio was 4.30% in the third quarter of 2015, versus 4.68% in the prior year quarter and 4.86% in the prior quarter.

The annualized gross charge-off ratio was 5.19% in the third quarter of 2015, down 27 basis points from the prior year quarter, and down 65 basis points from the second quarter of 2015. Recovery ratio was 89 basis points in the quarter, versus 78 basis points in the prior year quarter and 98 basis points in the second quarter of 2015.

The 60+ delinquency ratio was 2.90% at quarter end, versus 2.55% at prior year quarter end and 2.39% at prior quarter end.6

Acquisitions and Servicing

The Acquisitions and Servicing segment contributed $28 million to the company’s consolidated pretax income in the quarter. The entire Acquisitions and Servicing segment, which includes non-controlling interests, generated pretax income of $59 million in the quarter7, with net interest income of $92 million and a yield of 26.50%. Net finance receivables at quarter-end were $1.7 billion, down from $2.1 billion at September 30, 2014, and down from $1.8 billion at June 30, 2015. The principal balance of the

4 Consumer and Insurance segment reflects historical accounting basis (which is a basis of accounting other than U.S. GAAP).

5 3Q15 includes finance receivables held for sale.

6 Delinquency ratio includes loans held for sale.

7 Includes the impact of earnings attributable to non-controlling interests.

2

portfolio was $2.2 billion at quarter-end versus $2.7 billion at September 30, 2014 and $2.3 billion at June 30, 2015.

The annualized net charge-off ratio improved to 4.39% in the quarter, versus 5.31% in the prior year quarter and 5.07% in the prior quarter.

The annualized gross charge-off ratio was 5.05% in the quarter, down 78 basis points from the prior year quarter and down 70 basis points from the second quarter 2015. Recoveries continued to improve in the quarter at 66 basis points versus 52 basis points in the prior year quarter.

The 60+ delinquency ratio for the Acquisitions and Servicing segment was 4.06% at the end of the quarter, a decrease of 105 basis points from the prior year quarter end, and up 31 basis points from the prior quarter end.

Non-Core Portfolio: (Reported on a historical accounting basis, which is a non-GAAP measure.)

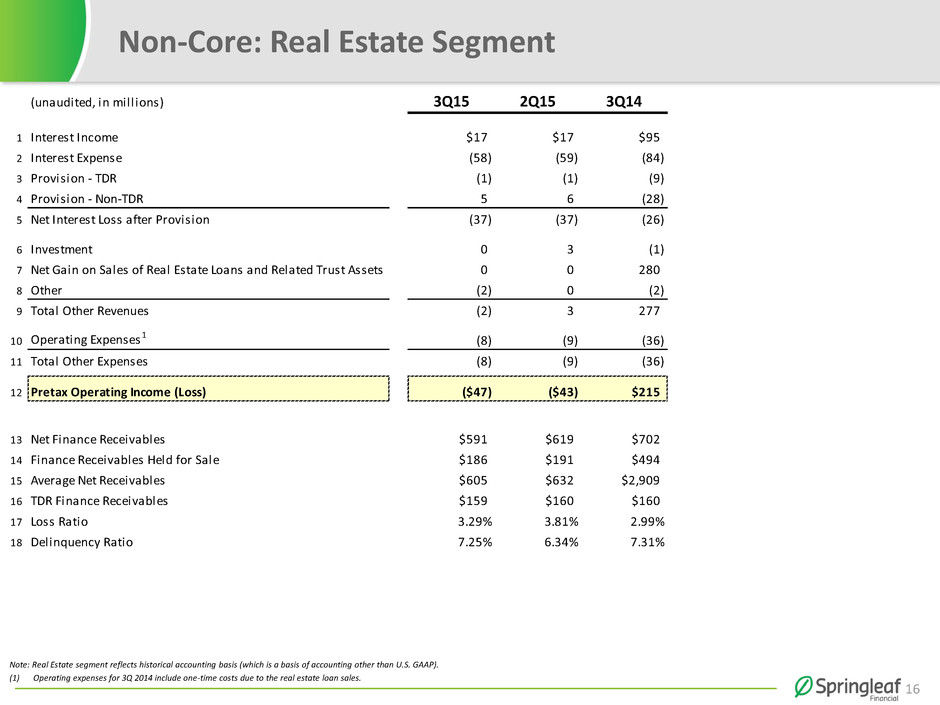

Legacy Real Estate and Other Non-Core

The Non-Core Portfolio (consisting of legacy real estate loans) generated a pretax loss of $47 million in the quarter. The loss resulted primarily from the reduction in interest earning assets attributable to real estate sales completed in 2014. The sale proceeds, which have been allocated to the Non-Core portfolio, are expected to be used to fund the purchase of OneMain Financial Holdings, LLC (“OneMain”) and/or for general corporate purposes. At closing, the majority of the debt allocated to the Non-Core Portfolio will be re-allocated to the Core Consumer segment. The real estate portfolio was $0.8 billion at quarter end, down from $1.2 billion at the prior year quarter end.8

The Other Non-Core activities generated a pretax loss of $16 million9 in the quarter.

Liquidity and Capital Resources

As of September 30, 2015, the company had $4.9 billion of cash and highly liquid investment securities. The company had total outstanding debt of $9.6 billion at quarter-end, in a variety of debt instruments.

On May 4, 2015, the company issued approximately 19.4 million shares of common stock for net proceeds of approximately $976 million.10 The proceeds may be used to fund the acquisition of OneMain and/or for general corporate purposes, which may include debt repurchases and repayments, capital expenditures and other possible acquisitions.

8 Includes both held for investment and held for sale finance receivables.

9 Excludes one-time costs of $14 million.

10 Approximate total after deducting offering-related expenses totaling $24 million.

3

2015 Guidance

The company has established 2015 guidance ranges for certain metrics related to its Core Consumer Operations as follows:

3Q15 YTD A1 | 2015E Guidance | |

Consumer Net Finance Receivables at Period End2 | $4.65bn | $4.85bn - $4.95bn |

Consumer Yield | 26.43% | 26.00% - 26.25% |

Consumer Net Charge-off Ratio | 4.90% | 5.00% - 5.25% |

Consumer Risk-Adjusted Yield3 | 21.53% | 20.75% - 21.25% |

Acquisitions & Servicing Pretax Income4 | $95mm | $115mm - $125mm |

1. | Net Finance Receivables represents data as of September 30, 2015 and includes finance receivables held for sale. All other metrics represent data for the nine months ended September 30, 2015. |

2. | Net Finance Receivables includes finance receivables held for sale. |

3. | Risk Adjusted Yield = Yield less Net Charge-off Ratio. |

4. | Excludes impact of earnings attributable to non-controlling interests. |

OneMain Acquisition

The company has been in discussions with the Department of Justice and certain states to obtain antitrust clearance to consummate the proposed acquisition of OneMain. On September 30, 2015, the company transferred $608 million of personal loans from held for investment to held for sale.

Use of Non-GAAP Measures

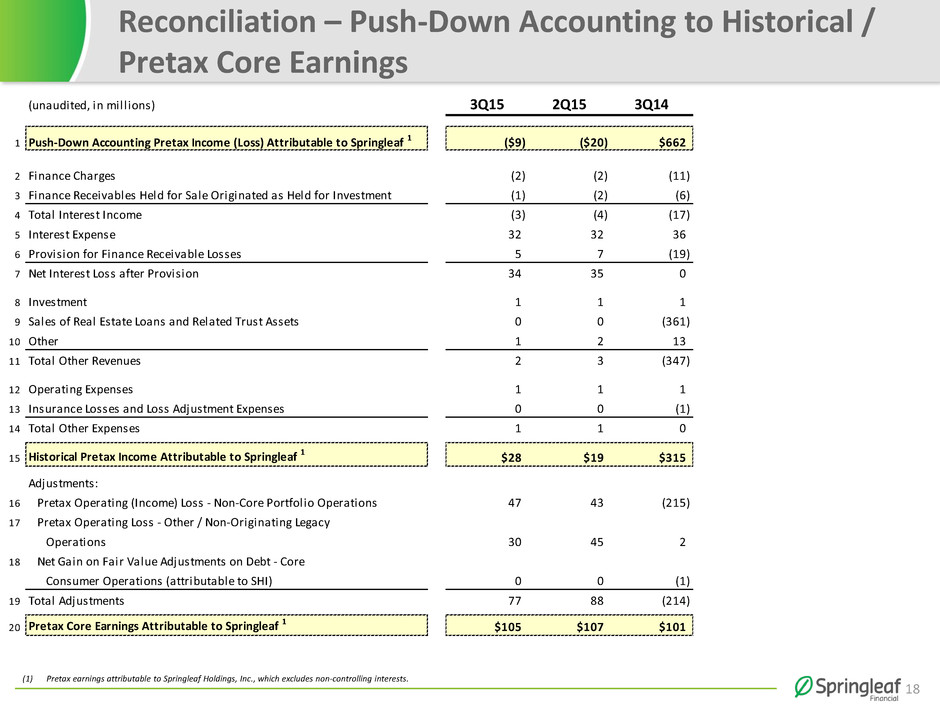

We report the operating results of our Core Consumer Operations, Non-Core Portfolio and Other Non-Core using the same accounting basis that we employed prior to 2010 when we were acquired by Fortress (“Fortress Acquisition”), which we refer to as “historical accounting basis,” to provide a consistent basis for both management and other interested third parties to better understand our operating results. The historical accounting basis, which is a basis of accounting other than accounting principles generally accepted in the United State of America (“U.S. GAAP”), also provides better comparability of the operating results of these segments to our competitors and other companies in the financial services industry. The historical accounting basis is not applicable to Acquisitions and Servicing since this segment resulted from the purchase of the SpringCastle Portfolio on April 1, 2013 and therefore, was not affected by the Fortress Acquisition.

Pretax Core Earnings is a key performance measure used by management in evaluating the performance of our Core Consumer Operations. Pretax Core Earnings represents our income (loss) before provision for (benefit from) income taxes on a historical accounting basis and excludes results of operations from our Non-Core Portfolio (legacy real estate loans) and other non-originating legacy operations, gains (losses) resulting from accelerated long-term debt repayment and repurchases of long-term debt related to Core Consumer Operations (attributable to Springleaf), gains (losses) on fair value adjustments on debt

4

related to Core Consumer Operations (attributable to Springleaf), and results of operations attributable to non-controlling interests. Pretax Core Earnings provides us with a key measure of our Core Consumer Operations’ performance as it assists us in comparing its performance on a consistent basis. Management believes Pretax Core Earnings is useful in assessing the profitability of our core business and uses Pretax Core Earnings in evaluating our operating performance. Pretax Core Earnings is a non-GAAP measure and should be considered in addition to, but not as a substitute for or superior to, operating income, net income, operating cash flow, and other measures of financial performance prepared in accordance with U.S. GAAP.

Conference Call & Webcast Information

Springleaf management will host a conference call and webcast to discuss our third quarter 2015 results and other general matters at 5:00 pm Eastern on Monday, November 9, 2015. Both the call and webcast are open to the general public. The general public is invited to listen to the call by dialing 877-330-3668 (U.S. domestic), or 678-304-6859 (international), conference ID 53834701, or via a live audio webcast through the Investor Relations section of the website. For those unable to listen to the live broadcast, a replay will be available on our website or by dialing 800-585-8367 (U.S. domestic), or 404-537-3406, conference ID 53834701, beginning approximately two hours after the event. The replay of the conference call will be available through November 23, 2015. An investor presentation will be available on the Investor Relations page of Springleaf’s website at www.springleaf.com prior to the start of the conference call.

Forward-Looking Statements

This presentation contains “forward-looking statements” within the meaning of the U.S. federal securities laws. Forward-looking statements include, without limitation, statements concerning plans, objectives, goals, projections, strategies, future events or performance, our 2015 guidance ranges and underlying assumptions and other statements, which are not statements of historical facts. Statements preceded by, followed by or that otherwise include the words “anticipate,” “appears,” “believe,” “foresee,” “intend,” “should,” “expect,” “estimate,” “project,” “plan,” “may,” “could,” “will,” “are likely” and similar expressions are intended to identify forward-looking statements. These statements involve predictions of our future financial condition, performance, plans and strategies, and are thus dependent on a number of factors including, without limitation, assumptions and data that may be imprecise or incorrect. Specific factors that may impact performance or other predictions of future actions include, but are not limited to: various risks relating to the OneMain acquisition, including in respect of the satisfaction of closing conditions to the OneMain acquisition that are materially adverse to the business, financial condition or results of operations of the combined company; resolution of any potential concerns expressed to us by the Department of Justice and certain state Attorneys General with respect to the OneMain acquisition; unanticipated difficulties financing the purchase price of the OneMain acquisition; unanticipated expenditures relating to the OneMain acquisition; uncertainties as to the timing of the closing of the OneMain acquisition; litigation relating to the OneMain acquisition; the impact of the OneMain acquisition on each company’s relationships with employees and third parties;

5

the inability to obtain, or delays in obtaining, cost savings and synergies from the OneMain acquisition and risks associated with the integration of the companies; changes in general economic conditions, including the interest rate environment and the financial markets; levels of unemployment and personal bankruptcies; shifts in residential real estate values; natural or accidental events such as earthquakes, hurricanes, tornadoes, fires, or floods; war, acts of terrorism, riots, civil disruption, pandemics, or other events disrupting business or commerce; changes in the rate at which we can collect or potentially sell our finance receivables portfolio; our ability to successfully realize the benefits of the SpringCastle Portfolio and the OneMain acquisition if completed; the effectiveness of our credit risk scoring models; changes in our ability to attract and retain employees or key executives; changes in the competitive environment in which we operate; shifts in collateral values, delinquencies, or credit losses; changes in federal, state and local laws, regulations, or regulatory policies and practices; potential liability relating to real estate and personal loans which we have sold or may sell in the future, or relating to securitized loans; the effect of future sales of our remaining portfolio of real estate loans and the transfer of servicing of these loans; the costs and effects of any litigation or governmental inquiries or investigations; our continued ability to access the capital markets or the sufficiency of our current sources of funds to satisfy our cash flow requirements; our ability to comply with our debt covenants; our ability to generate sufficient cash to service all of our indebtedness; the potential for downgrade of our debt by rating agencies; our substantial indebtedness, which could prevent us from meeting our obligations under our debt instruments and limit our ability to react to changes in the economy, or our ability to incur additional borrowings; the impacts of our securitizations and borrowings; our ability to maintain sufficient capital levels in our regulated and unregulated subsidiaries; changes in accounting standards or tax policies and practices and the application of such new policies and practices to the manner in which we conduct business; the material weakness that we have identified in our internal control over financial reporting; and other risks described in the “Risk Factors” section of the Company’s Form 10‐K filed with the SEC on March 16, 2015 and in the Company’s other filings with the SEC, including the Company’s Form 10-Q for the period ended March 31, 2015. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. We caution you not to place undue reliance on these forward-looking statements that speak only as of the date they were made. We do not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of this presentation or to reflect the occurrence of unanticipated events. You should not rely on forward-looking statements as the sole basis upon which to make any investment decision.

6

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(dollars in millions except earnings (loss) per share) | Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2015 | 2014 | 2015 | 2014 | |||||||||||||

Interest income: | ||||||||||||||||

Finance charges | $ | 424 | $ | 436 | $ | 1,234 | $ | 1,514 | ||||||||

Finance receivables held for sale originated as held for investment | 4 | 48 | 13 | 55 | ||||||||||||

Total interest income | 428 | 484 | 1,247 | 1,569 | ||||||||||||

Interest expense | 171 | 180 | 500 | 577 | ||||||||||||

Net interest income | 257 | 304 | 747 | 992 | ||||||||||||

Provision for finance receivable losses | 82 | 103 | 249 | 379 | ||||||||||||

Net interest income after provision for finance receivable losses | 175 | 201 | 498 | 613 | ||||||||||||

Other revenues: | ||||||||||||||||

Insurance | 40 | 44 | 116 | 125 | ||||||||||||

Investment | 11 | 12 | 44 | 32 | ||||||||||||

Net loss on repurchases and repayments of debt | — | — | — | (7 | ) | |||||||||||

Net gain (loss) on fair value adjustments on debt | — | 1 | — | (15 | ) | |||||||||||

Net gain on sales of real estate loans and related trust assets | — | 641 | — | 731 | ||||||||||||

Other | — | (12 | ) | (2 | ) | (7 | ) | |||||||||

Total other revenues | 51 | 686 | 158 | 859 | ||||||||||||

Other expenses: | ||||||||||||||||

Operating expenses: | ||||||||||||||||

Salaries and benefits | 100 | 95 | 305 | 279 | ||||||||||||

Other operating expenses | 87 | 75 | 227 | 193 | ||||||||||||

Insurance losses and loss adjustment expenses | 17 | 20 | 53 | 57 | ||||||||||||

Total other expenses | 204 | 190 | 585 | 529 | ||||||||||||

Income before provision for income taxes | 22 | 697 | 71 | 943 | ||||||||||||

Provision for income taxes | 2 | 235 | 1 | 310 | ||||||||||||

Net income | 20 | 462 | 70 | 633 | ||||||||||||

Net income attributable to non-controlling interests | 31 | 35 | 93 | 82 | ||||||||||||

Net income (loss) attributable to Springleaf Holdings, Inc. | $ | (11 | ) | $ | 427 | $ | (23 | ) | $ | 551 | ||||||

Share Data: | ||||||||||||||||

Weighted average number of shares outstanding: | ||||||||||||||||

Basic | 134,452,763 | 114,788,439 | 125,701,635 | 114,788,439 | ||||||||||||

Diluted | 134,452,763 | 115,316,314 | 125,701,635 | 115,212,398 | ||||||||||||

Earnings (loss) per share: | ||||||||||||||||

Basic | $ | (0.08 | ) | $ | 3.72 | $ | (0.18 | ) | $ | 4.80 | ||||||

Diluted | $ | (0.08 | ) | $ | 3.70 | $ | (0.18 | ) | $ | 4.79 | ||||||

7

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(dollars in millions except par value amount) | September 30, 2015 | December 31, 2014 | ||||||

Assets | ||||||||

Cash and cash equivalents | $ | 3,865 | $ | 879 | ||||

Investment securities | 1,742 | 2,935 | ||||||

Net finance receivables: | ||||||||

Personal loans | 4,061 | 3,831 | ||||||

SpringCastle Portfolio | 1,667 | 1,979 | ||||||

Real estate loans | 547 | 625 | ||||||

Retail sales finance | 27 | 48 | ||||||

Net finance receivables | 6,302 | 6,483 | ||||||

Allowance for finance receivable losses | (193 | ) | (176 | ) | ||||

Net finance receivables, less allowance for finance receivable losses | 6,109 | 6,307 | ||||||

Finance receivables held for sale | 797 | 205 | ||||||

Restricted cash and cash equivalents | 270 | 218 | ||||||

Other assets | 501 | 485 | ||||||

Total assets | $ | 13,284 | $ | 11,029 | ||||

Liabilities and Shareholders’ Equity | ||||||||

Long-term debt | $ | 9,555 | $ | 8,356 | ||||

Insurance claims and policyholder liabilities | 467 | 446 | ||||||

Deferred and accrued taxes | 139 | 152 | ||||||

Other liabilities | 294 | 238 | ||||||

Total liabilities | 10,455 | 9,192 | ||||||

Shareholders’ equity: | ||||||||

Common stock | 1 | 1 | ||||||

Additional paid-in capital | 1,524 | 529 | ||||||

Accumulated other comprehensive income (loss) | (11 | ) | 3 | |||||

Retained earnings | 1,469 | 1,492 | ||||||

Springleaf Holdings, Inc. shareholders’ equity | 2,983 | 2,025 | ||||||

Non-controlling interests | (154 | ) | (188 | ) | ||||

Total shareholders’ equity | 2,829 | 1,837 | ||||||

Total liabilities and shareholders’ equity | $ | 13,284 | $ | 11,029 | ||||

8

CORE KEY METRICS

(dollars in millions) | Three Months Ended September 30, | At or for the Nine Months Ended September 30, | ||||||||||||||

2015 | 2014 | 2015 | 2014 | |||||||||||||

Consumer and Insurance | ||||||||||||||||

Finance receivables held for investment: | ||||||||||||||||

Net finance receivables | $ | 4,044 | $ | 3,578 | ||||||||||||

Number of accounts | 870,877 | 894,182 | ||||||||||||||

TDR finance receivables | $ | 27 | $ | 18 | ||||||||||||

Allowance for finance receivable losses - TDR | $ | 7 | $ | 1 | ||||||||||||

Provision for finance receivable losses - TDR | $ | 4 | $ | 1 | $ | 14 | $ | 1 | ||||||||

Average net receivables | $ | 4,476 | $ | 3,481 | $ | 4,130 | $ | 3,295 | ||||||||

Yield | 25.97 | % | 27.02 | % | 26.43 | % | 27.00 | % | ||||||||

Gross charge-off ratio | 5.19 | % | 5.46 | % | 5.79 | % | 5.60 | % | ||||||||

Recovery ratio | (0.89 | )% | (0.78 | )% | (0.89 | )% | (0.67 | )% | ||||||||

Charge-off ratio | 4.30 | % | 4.68 | % | 4.90 | % | 4.93 | % | ||||||||

Delinquency ratio | 3.31 | % | 2.55 | % | ||||||||||||

Origination volume | $ | 1,167 | $ | 925 | $ | 3,227 | $ | 2,595 | ||||||||

Number of accounts originated | 219,613 | 193,288 | 600,323 | 566,032 | ||||||||||||

Finance receivables held for sale: | ||||||||||||||||

Net finance receivables | $ | 608 | $ | — | ||||||||||||

Number of accounts | 144,392 | — | ||||||||||||||

TDR finance receivables | $ | 2 | $ | — | ||||||||||||

Acquisitions and Servicing | ||||||||||||||||

Net finance receivables | $ | 1,667 | $ | 2,083 | ||||||||||||

Number of accounts | 242,660 | 291,153 | ||||||||||||||

TDR finance receivables | $ | 12 | $ | 8 | ||||||||||||

Allowance for finance receivable losses - TDR | $ | 4 | $ | 2 | ||||||||||||

Provision for finance receivable losses - TDR | $ | 1 | $ | 2 | $ | 2 | $ | 2 | ||||||||

Average net receivables | $ | 1,714 | $ | 2,142 | $ | 1,818 | $ | 2,279 | ||||||||

Yield | 26.50 | % | 24.26 | % | 26.58 | % | 24.28 | % | ||||||||

Net charge-off ratio | 4.39 | % | 5.31 | % | 4.98 | % | 7.09 | % | ||||||||

Delinquency ratio | 4.06 | % | 5.11 | % | ||||||||||||

9

RECONCILIATION OF PGAAP AND HISTORICAL INCOME (NON-GAAP)

(dollars in millions) | Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2015 | 2014 | 2015 | 2014 | |||||||||||||

Income before provision for income taxes - push-down accounting basis | $ | 22 | $ | 697 | $ | 71 | $ | 943 | ||||||||

Interest income adjustments | (3 | ) | (17 | ) | (10 | ) | (88 | ) | ||||||||

Interest expense adjustments | 32 | 36 | 94 | 100 | ||||||||||||

Provision for finance receivable losses adjustments | 5 | (19 | ) | 14 | (17 | ) | ||||||||||

Repurchases and repayments of long-term debt adjustments | — | — | — | (4 | ) | |||||||||||

Fair value adjustments on debt | — | — | — | 8 | ||||||||||||

Sales of finance receivables held for sale originated as held for investment adjustments | — | (361 | ) | — | (536 | ) | ||||||||||

Amortization of other intangible assets | 2 | 1 | 4 | 3 | ||||||||||||

Other | 1 | 13 | 7 | 15 | ||||||||||||

Income before provision for income taxes - historical accounting basis | $ | 59 | $ | 350 | $ | 180 | $ | 424 | ||||||||

PRETAX CORE EARNINGS (NON-GAAP) RECONCILIATION

(dollars in millions) | Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2015 | 2014 | 2015 | 2014 | |||||||||||||

Income before provision for income taxes - historical accounting basis | $ | 59 | $ | 350 | $ | 180 | $ | 424 | ||||||||

Adjustments: | ||||||||||||||||

Pretax operating (income) loss - Non-Core Portfolio Operations | 47 | (215 | ) | 138 | (87 | ) | ||||||||||

Pretax operating loss - Other/non-originating legacy operations | 30 | 2 | 88 | 12 | ||||||||||||

Net loss from accelerated repayment/repurchase of debt - Core Consumer Operations (attributable to SHI) | — | — | — | 1 | ||||||||||||

Net (gain) loss on fair value adjustments on debt - Core Consumer Operations (attributable to SHI) | — | (1 | ) | — | 7 | |||||||||||

Pretax operating income attributable to non-controlling interests | (31 | ) | (35 | ) | (93 | ) | (82 | ) | ||||||||

Pretax core earnings | $ | 105 | $ | 101 | $ | 313 | $ | 275 | ||||||||

Springleaf Holdings, Inc.

Contact:

Craig Streem, 812-468-5752

craig.streem@springleaf.com

Source: Springleaf Holdings, Inc.

10