Attached files

| file | filename |

|---|---|

| EX-3.2 - EX-3.2 - DULUTH HOLDINGS INC. | d70652dex32.htm |

| EX-1.1 - EX-1.1 - DULUTH HOLDINGS INC. | d70652dex11.htm |

| EX-3.1 - EX-3.1 - DULUTH HOLDINGS INC. | d70652dex31.htm |

| EX-23.2 - EX-23.2 - DULUTH HOLDINGS INC. | d70652dex232.htm |

| EX-5.1 - EX-5.1 - DULUTH HOLDINGS INC. | d70652dex51.htm |

Table of Contents

Registration No. 333-207300

As filed with the Securities and Exchange Commission on November 9, 2015

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2 TO

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

Duluth Holdings Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Wisconsin | 5611 | 39-1564801 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

P.O. Box 409

170 Countryside Drive

Belleville, Wisconsin 53508-0409

(608) 424-1544

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Stephen L. Schlecht

Executive Chairman

P.O. Box 409

170 Countryside Drive

Belleville, Wisconsin 53508-0409

(608) 424-1544

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

| Dennis F. Connolly, Esq. Godfrey & Kahn, S.C. 780 North Water Street Milwaukee, Wisconsin 53202 (414) 273-3500 |

Christopher D. Lueking, Esq. Latham & Watkins LLP 330 North Wabash Avenue, Suite 2800 Chicago, Illinois 60611 (312) 876-7700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional shares for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

¨ | Accelerated filer | ¨ | |||||||

| Non-accelerated filer |

x | Smaller reporting company | ¨ | |||||||

| (Do not check if a smaller reporting company) |

||||||||||

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities To Be Registered |

Amount to be Registered(1)(2) |

Proposed Maximum Offering Price Per Share |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(3) | ||||

| Class B Common Stock, no par value per share |

7,666,667 | $16.00 | $122,666,672 | $12,352.53 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated pursuant to Rule 457(a) of the Securities Act of 1933, as amended. |

| (2) | Includes 1,000,000 additional shares of common stock that the underwriters have the option to purchase. |

| (3) | The registrant previously paid $11,580.50 in connection with the initial filing of this Registration Statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY—SUBJECT TO COMPLETION—DATED NOVEMBER 9, 2015

PROSPECTUS

6,666,667 Shares

Duluth Holdings Inc.

Class B Common Stock

Duluth Holdings Inc. is offering 6,666,667 shares of Class B common stock. This is our initial public offering and no public market currently exists for our Class B common stock. We anticipate the initial public offering price to be between $14.00 and $16.00 per share.

Duluth Holdings Inc. has two classes of authorized common stock: Class A common stock and Class B common stock. The rights of holders of Class A common stock and Class B common stock are identical, except for voting and conversion rights. Each share of Class A common stock is entitled to ten votes per share and is convertible at any time into one share of Class B common stock. Each share of Class B common stock is entitled to one vote per share. Outstanding shares of Class A common stock will represent approximately 10.8% of our outstanding capital stock immediately following the completion of this offering.

We have applied to have our Class B common stock listed on the NASDAQ Global Select Market under the symbol “DLTH.”

Following this offering, we will be a “controlled company” under the corporate governance rules for NASDAQ-listed companies, and our board of directors has determined not to have an independent nominating function and instead to have the full board of directors be directly responsible for nominating members of our board.

We are an “emerging growth company” as defined under federal securities laws and are subject to reduced public company reporting requirements. Investing in our Class B common stock involves a high degree of risk. See “Risk Factors” beginning on page 13 of this prospectus.

| Per Share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

(1) See “Underwriting (Conflicts of Interest)” for a description of the compensation payable to the underwriters.

We have granted the underwriters an option for a period of 30 days to purchase up to an additional 1,000,000 shares of our Class B common stock at the initial public offering price after deducting underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of Class B common stock to purchasers on or about , 2015.

| William Blair | Baird | Raymond James | BMO Capital Markets |

, 2015

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 13 | ||||

| 35 | ||||

| 37 | ||||

| 38 | ||||

| 39 | ||||

| 41 | ||||

| 43 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

45 | |||

| 62 | ||||

| 74 | ||||

| 80 | ||||

| 89 | ||||

| 92 | ||||

| 94 | ||||

| 100 | ||||

| Material U.S Federal Income Tax Consequences to Non-U.S. Holders |

102 | |||

| 106 | ||||

| 114 | ||||

| 114 | ||||

| 114 | ||||

| Index to Consolidated Financial Statements of Duluth Holdings Inc. |

F-1 | |||

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by us or on our behalf or to which we have referred you. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. We are offering to sell, and seeking offers to buy, shares of our Class B common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is complete and accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our Class B common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: we have not, and the underwriters have not, done anything that would permit this offering, or possession or distribution of this prospectus, in any jurisdiction where action for that purpose is required, other than in the United States. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about, and to observe, any restrictions as to this offering and the distribution of this prospectus applicable to those jurisdictions.

Trademarks, Trade Names and Service Marks

We use various trademarks, trade names and service marks in our business including without limitation Duluth Trading Co.®, Duluth Trading Company®, Alaskan Hardgear®, Armachillo®, Ballroom®, Buck Naked™, Bucket Master®, Cab Commander®, Crouch Gusset®, Dry on the Fly®, Duluthflex®, Fire Hose®, Longtail T®, No Polo Shirt® and Wild Boar Mocs®. For convenience, we may not include the ® or ™ symbols, but such omission is not meant to indicate that we would not protect our intellectual property rights to the fullest extent allowed by law. Any other trademarks, trade names or service marks referred to in this registration statement are the property of their respective owners.

Table of Contents

Industry and Market Data

This prospectus includes industry and market data that we obtained from industry sources, third-party studies, including market analyses and reports prepared for us by Information Resources, Inc., or IRI, and internal company surveys. Industry sources generally state that the information contained therein has been obtained from sources believed to be reliable. Although we are responsible for all of the disclosure contained in this prospectus and we believe the industry and market data to be reliable as of the date of this prospectus, this information could prove to be inaccurate.

Basis of Presentation

Effective February 2013, we changed our fiscal year end from December 31 to the Sunday nearest to January 31. Accordingly, references in this prospectus to fiscal 2014 and 2013 refer to years ended February 1, 2015 and February 2, 2014, respectively. Certain differences in numbers in the tables and text throughout this prospectus may exist due to rounding.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our Class B common stock. Before you decide to invest in our Class B common stock, you should read this entire prospectus carefully, including our financial statements and the related notes thereto and the matters discussed in the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained elsewhere in this prospectus. Unless we state otherwise or the context otherwise requires, references in this prospectus to “we,” “our,” “us,” “Duluth Trading” and “the Company” refer to Duluth Holdings Inc. and its subsidiary on a consolidated basis.

Our Company

Duluth Trading is a rapidly growing lifestyle brand of men’s and women’s casual wear, workwear and accessories sold exclusively through our own channels. We offer a comprehensive line of innovative, durable and functional products, such as our Longtail T® shirts, Buck Naked™ underwear and Fire Hose® work pants, which reflect our position as the Modern, Self-Reliant American Lifestyle brand. Our brand has a heritage in workwear that transcends tradesmen and appeals to a broad demographic of men and women for everyday and on-the-job use. Approximately 88% of our fiscal 2014 net sales consisted of proprietary products sold under our Duluth Trading brand name. We believe the foundation of our success is our culture of “poking average in the eye” by seeing things for what they could be and should be and finding a way to make them exactly that, and we like to do it all with a big, toothy grin. Our brand is defined by: solution-based products manufactured with high quality craftsmanship, humorous and distinctive marketing and an outstanding customer experience.

Our design process reflects a “there’s gotta be a better way” attitude, resulting in differentiated products with enhanced features and enduring styles that go beyond short-lived fashion trends. We strive to make shopping for our products fun by using attention-grabbing advertisements that serve to reinforce our brand identity. We also use storytelling to differentiate our products in the marketplace and create emotional connections with our customers. We provide our customers with a unique and entertaining experience across all channels through our content-rich website, catalogs and “store like no other” retail environment. We treat our customers like next-door neighbors, as exemplified by our exceptional customer service and unconditional “No Bull Guarantee” on all purchases. To protect the integrity of the Duluth Trading brand, we offer our products exclusively through our omnichannel distribution network, consisting of our website, catalogs and retail stores. This model creates multiple touch points with our customers and enables us to control both the expression of our Duluth Trading brand and the pricing of our products. Our distribution strategy eliminates the need to sell through third-party retailers, allowing us to focus on our core competencies of product development, storytelling and serving customers.

Duluth Trading was founded in 1989 when two brothers in the home construction industry were tired of dragging tools from job to job using discarded five-gallon drywall compound buckets. The two brothers were never satisfied with the status quo and believed “there’s gotta be a better way.” So they invented the Bucket Boss®—a ruggedly durable canvas tool organizer that fits around a drywall bucket and transformed the way construction workers organized their tools. Capitalizing on their initial success, these brothers launched a catalog that later became known as Duluth Trading Company. Under the initial philosophy of “Job Tough, Job Smart,” this catalog was dedicated to improving and expanding on existing methods of tool storage, organization and transport. In December 2000, GEMPLER’S Inc., an agricultural and horticultural supply catalog business founded and owned by Stephen L. Schlecht, acquired Duluth Trading and brought the two mail order companies together. Both catalogs had customers who worked outside and embraced the spirit of hands-on, self-reliant Americans. In February 2003, the GEMPLER’S catalog business was sold to W.W. Grainger (NYSE:GWW) and proceeds from that sale have been used to fund the growth of Duluth Trading. With that transaction, GEMPLER’S, Inc. changed its corporate name to Duluth Holdings Inc.

1

Table of Contents

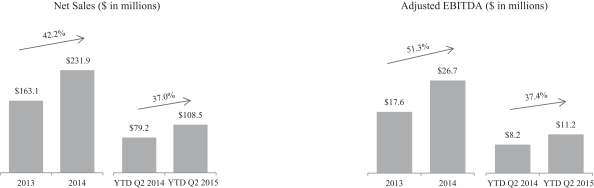

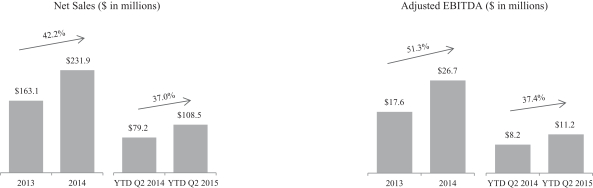

From what began as an idea aimed at those working in the building trades, Duluth Trading has become a widely recognized brand and proprietary line of innovative and functional apparel and gear. We have created strong brand awareness, built a loyal customer base and generated robust net sales momentum. We have done so by sticking to our roots of “there’s gotta be a better way” and through our relentless focus on providing our customers with quality, functional products. We have established a strong track record of growth and profitability as demonstrated by our net sales and operating income compound annual growth rates, or CAGRs, between calendar 2009 and fiscal 2014 of 28% and 51%, respectively. We believe that the foregoing attributes have enabled us to deliver strong financial results, as evidenced by:

| • | net sales have increased year-over-year for 22 consecutive quarters through August 2, 2015; |

| • | net sales in fiscal 2014 increased by 42.2% over the prior year to $231.9 million and net sales in the first six months of fiscal 2015 increased by 37.0% over the first six months of the prior year to $108.5 million; |

| • | Adjusted EBITDA in fiscal 2014 increased by 51.3% over the prior year to $26.7 million and Adjusted EBITDA in the first six months of fiscal 2015 increased 37.4% over the first six months of the prior year to $11.2 million; and |

| • | our retail stores have achieved an average payback of less than two years. |

See “Summary Consolidated Financial and Other Data—Non-U.S. GAAP Financial Measures” for a reconciliation of our net income to Adjusted EBITDA, a non-U.S. GAAP financial measure. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for our definition of Adjusted EBITDA.

What Makes Us Different

We believe the following strengths differentiate us and provide a foundation for future growth:

Differentiated, Everyday Lifestyle Brand

Our understanding of the Modern, Self-Reliant American Lifestyle enables us to create personal connections with our customers, who lead a hands-on lifestyle, value a job well-done and are often outdoors for work and hobbies. The workwear heritage of our products is the foundation of our authentic and differentiated brand. We communicate our brand values and product performance nationally through multiple mediums, including television, catalogs, digital advertising and sponsored events. We believe these marketing efforts make our brand synonymous with this lifestyle, validate our authenticity and establish us as a trusted provider of durable and functional casual wear and workwear.

2

Table of Contents

Solution-Based Design

Our products solve the problems our customers experience with commonly available apparel and gear. We generate new product ideas in part by proactively seeking input from our customers, including our trades panels, which are comprised of select groups located across the United States with expertise in various fields. Our trades panels test our products in intense conditions and offer suggestions for new and improved features. We believe that our focus on thoughtful product design and commitment to quality, such as “triple stitching the extra stitch” and “doubling down on extra durable fabric,” keeps our existing customers engaged while also attracting new customers to our brand. And we do it all because there are a whole lotta legs, torsos, feet and crotches out there counting on us.

Humorous and Distinctive Marketing

We make shopping for our products fun by using attention-grabbing advertisements that are humorous, irreverent and quirky. Our national advertising campaigns that feature characters such as our Giant Angry Beaver, Buck Naked Guy and Grab-Happy Grizzly continue to increase our brand awareness and drive customers to our brand. We use storytelling to differentiate our products in the marketplace and create emotional connections with our customers. For example, we inspire our female customers by featuring women of “grit and substance” whose professions range from ranching to horse training to dog sled racing to landscape design. We believe our approach to marketing gives our products a distinct identity, enhances our brand and helps us stand out in the market.

Outstanding and Engaging Customer Experience

An important principle that shapes the Duluth Trading brand is our commitment to treat our customers like next-door neighbors by providing a shopping experience that is fun, inviting and hassle-free. We are dedicated to delivering outstanding customer service by standing behind all purchases with our unconditional “No Bull Guarantee.” Our content-rich, user-friendly website is designed to provide an enjoyable, informative and efficient shopping experience. Our call center is open 24 hours a day, seven days a week and is staffed with friendly, knowledgeable representatives dedicated to making every customer experience positive. Our retail stores are designed to bring our brand to life by creating a unique and entertaining experience with engaging sales associates and a compelling and complete assortment of our products. We believe these elements help promote customer loyalty and drive repeat purchases.

Attractive, Loyal Customer Base

The quality and consistency of our product offering attracts a broad demographic of men and women who lead the Modern, Self-Reliant American Lifestyle. According to an internal company survey, 87% of our customers identified themselves as working outside of the building trades. Our average customer is a long-standing homeowner with an annual household income of over $75,000. Based on these characteristics, we believe our customers have a high level of disposable income and are attracted by the high quality craftsmanship and enhanced features of our products. We enjoy a high level of brand satisfaction as evidenced by our Net Promoter Score of approximately 70% and the fact that 76% of our customers would recommend Duluth Trading to a friend or colleague, according to IRI. In addition, we currently have over 200,000 online product reviews, over 90% of which are four or five star ratings.

Omnichannel Presence with Complete Distribution Control

We sell our products exclusively through our direct and retail channels, giving us complete control of the presentation of our brand and the relationships with our customers. This strategy allows us to present our brand in a consistent manner, including marketing, pricing and product presentation. It also enables us to reduce

3

Table of Contents

logistical complexities and costs because we are not subject to timing, delivery and quantity requirements set by third-party retailers. We believe this approach to distribution is a significant advantage for our brand, allowing us to deliver feature rich, superior quality products at competitive prices.

| • | Direct Segment. We have an established direct platform that reaches customers nationwide through our website and catalogs, which together comprised approximately 90% of our fiscal 2014 net sales. Based on our internal research and our fiscal 2014 net sales, the concentration of our direct nationwide customer base was generally aligned with the geographic concentration of the U.S. population, and our top three markets during fiscal 2014 were California, Texas and New York, in that order. Our duluthtrading.com website serves as a storefront to our entire product collection, and approximately 78% of our fiscal 2014 net sales in the direct segment were transacted online. Our catalog business is an important part of our heritage, and approximately 22% of our fiscal 2014 net sales in the direct segment were transacted via our call center. Our catalogs also serve as a tangible vehicle for our authentic and humorous storytelling and often drive customers who wish to further interact with our brand to visit our website and retail stores. |

| • | Retail Segment. In 2010, we opened our first retail store and have since expanded our retail presence, operating seven retail stores and two outlet stores as of November 2015. Retail sales represented approximately 10% of our fiscal 2014 net sales, and we expect retail sales to represent an increasing percentage of our net sales over time. Our retail stores allow us to reach customers who prefer to shop in a brick and mortar setting and give new and existing consumers the opportunity to touch and feel our innovative products. |

Seasoned Management Team Driving an Impassioned Culture

Our senior management team has extensive experience across a broad range of key disciplines. With an average of approximately 30 years of experience in their respective functional areas, our management team has been instrumental in driving results and in developing a robust and scalable infrastructure to support our continued growth. Our senior management team embraces the Modern, Self-Reliant American Lifestyle and has fostered a culture committed to “outthink, outsmart and outcraft average,” which is shared by employees throughout our organization. Our strong company culture and spirited corporate personality are exemplified by the long tenure of our team members with us. We believe the strength of our senior management team, supported by our dedicated board of directors and passionate employees, is a key driver of our success and positions us well to execute our long-term growth strategy.

Our Growth Strategies

Our goal is to expand the reach of the Duluth Trading brand, using strategies that will further drive growth and profitability:

| • | Building Brand Awareness to Continue Customer Acquisition. We are a rapidly growing lifestyle brand, have built strong brand awareness and have successfully acquired customers over the past five years. As a relatively young brand, we believe that we have a significant opportunity to build even greater brand awareness. According to IRI, once we bring customers to our brand, they are more satisfied with Duluth Trading than any other brand in our competitive set. We intend to leverage our unique and compelling marketing strategy, retail expansion and continued catalog prospecting to capture potential new customers. |

| • | Accelerating Retail Expansion. IRI has validated that our customers’ purchasing decisions are heavily influenced by the availability of our retail stores. We believe that our customers’ desire to shop in stores, combined with the number of potential markets for our stores and the compelling unit |

4

Table of Contents

| economics of our existing retail stores, provide us with a significant opportunity to grow our U.S. retail presence. We have identified markets with the potential for approximately 100 U.S. store locations that feature high concentrations of existing Duluth Trading customers and potential customers that fit our brand demographics. Our existing retail stores have been highly profitable in both metropolitan and rural locations across multiple markets and have achieved an average payback of less than two years. We plan to continue building our organization and investing in software systems and operational infrastructure to support the growth in our retail segment. Based on our experience to date, we believe the combination of our direct and retail channels in an individual geographic market substantially increases the net sales and customer acquisition potential in that market. |

| • | Selectively Broadening Assortments in Certain Men’s Product Categories. We intend to continue to expand our men’s business by selectively broadening our assortment in certain product categories that exhibit high potential and resonate with the lifestyle of our men’s customers, such as outerwear and footwear. Through product introductions that expand seasonality and occasions for wear, we believe we can grow our share of closet with existing and new men’s customers. |

| • | Growing Our Women’s Business. Since launching in 2005, our women’s business has grown significantly to represent approximately 19% of our net sales in fiscal 2014 and has achieved a 55% CAGR from fiscal 2012 to fiscal 2014. According to IRI, women have lower awareness of our brand but report high levels of satisfaction with Duluth Trading once they have tried our products. We expect that our women’s business will continue to represent an increasing portion of our overall business going forward and intend to grow it through acquiring new customers, by broadening our women’s product assortment and by leveraging all of our marketing channels, including national television and digital advertising, our catalogs and retail stores. |

Market Opportunity

We operate in the U.S. apparel, footwear and accessories market, primarily in the everyday casual wear and workwear categories. According to IRI, the total market, including men’s, women’s and children’s apparel, footwear and accessories (such as jewelry, bags and small leather goods), is estimated to be $334 billion in 2015. Within this industry, apparel is expected to account for approximately 65% of sales, footwear is expected to account for approximately 19% of sales and accessories is expected to account for approximately 16% of sales. IRI expects total U.S. apparel dollar sales to continue to grow at 2% to 4% annually. We believe that we are well-positioned to capture an increasing share of this attractive market by continuing to execute on our growth strategies of building customer awareness, accelerating our retail store expansion, selectively broadening our assortment in certain men’s product categories and growing our women’s business.

Recent Developments

We expect total net sales to be between $55.0 million and $55.5 million in the three months ended November 1, 2015 compared to $42.6 million in the three months ended November 2, 2014. We expect net sales for our direct segment to be between $46.3 million and $46.6 million and net sales for our retail segment to be between $8.7 million and $8.9 million in the three months ended November 1, 2015 compared to $36.7 million and $5.9 million in the three months ended November 2, 2014, respectively.

We expect our gross margin rate to be up slightly in the three months ended November 1, 2015 compared to the three months ended November 2, 2014.

5

Table of Contents

We expect our selling, general and administrative expense in the three months ended November 1, 2015 to be higher than the three months ended November 2, 2014 on an absolute basis and relative to net sales due primarily to additional expenses incurred in the implementation of our warehouse management systems and third party logistics (3PL) infrastructure to support the continuing growth of our business.

We expect our adjusted EBITDA in the three months ended November 1, 2015 to be lower than the three months ended November 2, 2014, primarily due to increased expenses as discussed above.

We intend to issue a press release reporting our results of operations for the third quarter of 2015 by mid-to-late December.

Summary Risk Factors

Our ability to implement our business strategy is subject to numerous risks and uncertainties. You should carefully consider all of the information set forth in this prospectus and, in particular, the information under the heading “Risk Factors,” prior to making an investment in our Class B common stock. These risks include, among others, the following:

| • | We may fail to offer products that customers want to purchase. |

| • | We may not be able to maintain and enhance our brand image. |

| • | We may not be able to effectively execute our growth strategies, including growing our retail presence. |

| • | Our marketing strategy of associating our Duluth Trading brand with the Modern, Self-Reliant American Lifestyle may not be successful with future customers. |

| • | Our business may be subject to system interruptions or performance failures in our technology infrastructure, which could impair customer access to our sites. |

| • | We rely on our key suppliers and/or third-party service providers, and any interruptions in our supply chain could impair our ability to service our customers. |

| • | The dual class structure of our common stock and the existing ownership of capital stock by our executive officers, directors and their affiliates have the effect of concentrating voting control with our executive officers, directors and their affiliates for the foreseeable future. |

| • | Following this offering, our Executive Chairman will own shares representing a majority of the voting power of our outstanding capital stock. |

Our Corporate Information

Our principal executive office is located at 170 Countryside Drive, Belleville, Wisconsin 53508, and our telephone number is (608) 424-1544. Our website address is www.duluthtrading.com. Our website and the information contained on, or that can be accessed through, our website will not be deemed to be incorporated by reference in, and are not considered part of, this prospectus. You should not rely on any such information in making your decision whether to purchase our shares of Class B common stock.

6

Table of Contents

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in gross revenue during our last fiscal year, we qualify as an “emerging growth company” as defined under the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of reduced regulatory and reporting requirements that are otherwise generally applicable to public companies. As an emerging growth company:

| • | we may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this prospectus; |

| • | we are exempt from the requirement to obtain an audit of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act; |

| • | we are permitted to provide less extensive disclosure about our executive compensation arrangements; and |

| • | we are not required to hold non-binding advisory votes on executive compensation or golden parachute arrangements. |

We remain an emerging growth company and may continue to take advantage of these provisions until the earliest to occur of: (i) the last day of our fiscal year following the fifth anniversary of this offering, which anniversary will occur on the last day of fiscal 2020; (ii) the date on which we are deemed to be a “large accelerated filer” (which means (a) the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter, (b) we have filed at least one annual report on Form 10-K, and (c) we have been subject to the reporting requirements of the Securities Exchange Act of 1934, as amended, or the Exchange Act, for at least twelve months); (iii) the last day of our fiscal year during which our annual gross revenue exceeds $1.0 billion; and (iv) the date on which we issue more than $1.0 billion of non-convertible debt during the previous three-year period.

The JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. Thus, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected not to avail ourselves of this extended transition period.

7

Table of Contents

The Offering

| Issuer in this offering |

Duluth Holdings Inc. |

| Class B common stock to be offered by us |

6,666,667 shares (or 7,666,667 shares of Class B common stock if the underwriters’ option to purchase additional shares is exercised in full) |

| Class B common stock to be outstanding immediately following this offering |

27,928,411 shares (or 28,928,411 shares of Class B common stock if the underwriters’ option to purchase additional shares is exercised in full) |

| Class A common stock to be outstanding immediately following this offering |

3,364,200 shares |

| Use of Proceeds |

We estimate that the net proceeds to us from this offering will be approximately $91.1 million, or approximately $105.1 million if the underwriters exercise in full their option to purchase additional shares, assuming an initial public offering price of $15.00 per share, the midpoint of the price range set forth on the cover of this prospectus, and after deducting estimated underwriting discounts and offering expenses. |

We intend to make a final “S” corporation distribution to shareholders who were shareholders immediately prior to this offering in an amount equal to 100% of our cumulative undistributed taxable income prior to our conversion to a “C” corporation, determined using a pro-rata allocation method for 2015 (unless otherwise required by law), which we currently estimate to be $51.1 million. We intend to use a portion of the net proceeds from this offering to repay borrowings under a short-term note which we intend to fund part of this final distribution and may use a portion of the net proceeds from this offering to fund the balance of this final distribution. We estimate net proceeds in excess of the final “S” corporation distribution to be approximately $40.0, and we intend to use such proceeds to fund growth initiatives and for other general corporate purposes, including funding new retail store expansion and infrastructure expenditures. See “Use of Proceeds.”

| Voting Rights |

The rights of holders of Class A common stock and Class B common stock are identical, except for voting and conversion rights. Each share of Class A common stock is entitled to ten votes per share, and each share of Class B common stock is entitled to one vote per share. Following completion of this offering, each share of Class A common stock may be converted into one share of Class B common stock at the option of its holder and will be automatically converted into one share of Class B common stock upon transfer, subject to certain exceptions. See “Description of Capital Stock.” |

| Dividend Policy |

We do not anticipate paying dividends on our Class B common stock for the foreseeable future. See “Dividend Policy.” |

8

Table of Contents

| Conflicts of Interest |

A portion of the net proceeds from this offering will be used to repay borrowings under a short-term note. Because BMO Capital Markets Corp. is an underwriter in this offering and an affiliate of BMO Capital Markets Corp. is a lender under the short-term note and will receive 5% or more of the net proceeds from the sale of our Class B common stock in this offering, BMO Capital Markets Corp. is deemed to have a “conflict of interest” under Rule 5121 (“Rule 5121”) of the Financial Industry Regulatory Authority, Inc. (“FINRA”). As a result, this offering will be conducted in accordance with FINRA Rule 5121. Pursuant to that rule, the appointment of a “qualified independent underwriter” is not required in connection with this offering as the members primarily responsible for managing the public offering do not have a conflict of interest, are not affiliates of any member that has a conflict of interest and meet the requirements of paragraph (f)(12)(E) of FINRA Rule 5121. See “Use of Proceeds” and “Underwriting (Conflicts of Interest).” |

| Risk Factors |

You should read the “Risk Factors” section of this prospectus for a discussion of factors to carefully consider before deciding to invest in our Class B common stock. |

| Proposed NASDAQ Global Select Market Symbol |

“DLTH” |

| Directed Share Program |

At our request, the underwriters have reserved up to 333,333 shares of our Class B common stock, or approximately 5.0% of the shares being offered by this prospectus, for sale at the initial public offering price to our directors, officers, certain employees and other parties with a connection to the Company. Any reserved shares not purchased will be offered by the underwriters to the general public on the same terms as the other shares. See “Underwriting (Conflicts of Interest).” |

The number of shares of Class B common stock to be outstanding after this offering is based on 21,261,744 shares of Class B common stock outstanding as of August 2, 2015 (after giving effect to the conversion of 261,660 shares of Class A common stock into Class B common stock after August 2, 2015) and excludes 1,564,631 shares of Class B common stock reserved for issuance under the 2015 Equity Incentive Plan of Duluth Holdings Inc., or the 2015 Equity Incentive Plan, assuming no exercise of the underwriters’ option to purchase additional shares.

In addition, except when otherwise indicated, information in this prospectus reflects or assumes:

| • | completion of the 3,738-for-one stock split of our Class A common stock and Class B common stock, effective on November 4, 2015; |

| • | completion of our conversion from an “S” corporation to a “C” corporation for income tax purposes; |

| • | no exercise by the underwriters of their option to purchase additional shares of Class B common stock; and |

| • | no purchases by our directors, officers, certain employees and other parties with a connection to the Company, who have indicated an interest in purchasing shares of Class B common stock in this offering at the initial public offering price, in an amount which we do not currently expect will exceed $5 million. See “Principal Shareholders” and “Underwriting (Conflicts of Interest).” |

9

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables present summary consolidated financial and other data as of and for the periods indicated, and certain unaudited pro forma information to reflect our conversion from an “S” corporation to a “C” corporation for income tax purposes. The summary consolidated statements of operations data for the fiscal years ended February 2, 2014, February 1, 2015 and the summary consolidated balance sheet data as of February 2, 2014 and February 1, 2015 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated statements of operations data for the six months ended August 3, 2014 and August 2, 2015 and the summary consolidated balance sheet data as of August 2, 2015 are derived from our unaudited financial statements included elsewhere in this prospectus. The historical results presented below are not necessarily indicative of the results to be expected for any future period. You should read this summary consolidated financial and other data in conjunction with the consolidated financial statements and accompanying notes and the information under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” appearing elsewhere in this prospectus.

| Fiscal Year Ended(1) | Six Months Ended (unaudited) |

|||||||||||||||

| February 2, 2014 |

February 1, 2015 |

August 3, 2014 |

August 2, 2015 |

|||||||||||||

| (in thousands, except per share data) | ||||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||

| Direct |

$ | 152,896 | $ | 208,909 | $ | 71,840 | $ | 94,698 | ||||||||

| Retail |

10,193 | 22,958 | 7,330 | 13,786 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net sales |

163,089 | 231,867 | 79,170 | 108,484 | ||||||||||||

| Cost of goods sold(2) |

71,088 | 100,877 | 33,417 | 45,359 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

92,001 | 130,990 | 45,753 | 63,125 | ||||||||||||

| Selling, general and administrative expenses |

75,786 | 106,964 | 38,846 | 54,616 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

16,215 | 24,026 | 6,907 | 8,509 | ||||||||||||

| Interest expense |

248 | 341 | 127 | 112 | ||||||||||||

| Other income (expense), net |

86 | 422 | 75 | 75 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income taxes |

16,053 | 24,107 | 6,855 | 8,472 | ||||||||||||

| Income tax expense |

— | — | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

16,053 | 24,107 | 6,855 | 8,472 | ||||||||||||

| Less: Net income attributable to noncontrolling interest |

537 | 460 | 101 | 82 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income attributable to controlling interest |

$ | 15,516 | $ | 23,647 | $ | 6,754 | $ | 8,390 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Pro forma net income information (unaudited):(3) |

||||||||||||||||

| Income before provision for income taxes |

$ | 15,516 | $ | 23,647 | $ | 6,754 | $ | 8,390 | ||||||||

| Pro forma provision for income taxes |

6,206 | 9,459 | 2,702 | 3,356 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Pro forma net income |

$ | 9,310 | $ | 14,188 | $ | 4,052 | $ | 5,034 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Per share data: |

||||||||||||||||

| Basic net income per share attributable to controlling interest (Class A and Class B) |

$ | 0.66 | $ | 0.99 | $ | 0.28 | $ | 0.35 | ||||||||

| Diluted net income per share attributable to controlling interest (Class A and Class B) |

0.65 | 0.99 | 0.28 | 0.35 | ||||||||||||

| Pro forma basic net income per share attributable to controlling interest (Class A and Class B) |

$ | 0.39 | $ | 0.60 | $ | 0.17 | $ | 0.21 | ||||||||

| Pro forma diluted net income per share attributable to controlling interest (Class A and Class B) |

0.39 | 0.59 | 0.17 | 0.21 | ||||||||||||

10

Table of Contents

| Actual February 1, 2015 |

Actual August 2, 2015 |

Pro Forma August 2, 2015(4) |

Pro Forma As Adjusted August 2, 2015(5) |

|||||||||||||

| (in thousands) | ||||||||||||||||

| Consolidated Balance Sheet Data (unaudited): |

||||||||||||||||

| Cash |

$ | 7,881 | $ | 366 | $ | 366 | $ | 45,211 | ||||||||

| Working capital |

25,714 | 28,683 | 28,683 | 68,728 | ||||||||||||

| Total assets |

70,949 | 74,402 | 74,402 | 119,247 | ||||||||||||

| Total debt, including current portion |

5,684 | 12,654 | 12,654 | 12,654 | ||||||||||||

| Additional paid in capital |

— | — | 34,500 | 74,545 | ||||||||||||

| Retained earnings |

36,025 | 34,500 | — | — | ||||||||||||

| Shareholders’ equity |

38,262 | 37,505 | 37,505 | 77,550 | ||||||||||||

| Fiscal Year Ended | Six Months Ended | |||||||||||||||

| February 2, 2014 | February 1, 2015 | August 3, 2014 | August 2, 2015 | |||||||||||||

| (in thousands, except store data) | ||||||||||||||||

| Operating Data (unaudited): |

||||||||||||||||

| Number of Stores(6) |

4 | 6 | 4 | 7 | ||||||||||||

| Capital expenditures |

$ | 3,952 | $ | 5,269 | $ | 2,715 | $ | 3,841 | ||||||||

| EBITDA |

$ | 17,548 | $ | 26,269 | $ | 7,805 | $ | 9,758 | ||||||||

| Adjusted EBITDA |

$ | 17,624 | $ | 26,661 | $ | 8,155 | $ | 11,205 | ||||||||

(1) Effective February 2013, we changed our fiscal year end from December 31 to the Sunday nearest to January 31.

(2) Includes the direct cost of purchased merchandise; inventory shrinkage; inventory adjustments due to obsolescence, including excess and slow-moving inventory and lower of cost or market reserves; inbound freight; and freight from our distribution centers to our retail stores.

(3) The unaudited pro forma net income information for all years and periods presented gives effect to an adjustment for income tax expense on the income attributable to controlling interest as if we had been a “C” corporation at an assumed combined federal, state and local effective income tax rate, which approximates our statutory income tax rate, of 40%. No pro forma income tax expense was calculated on the income attributable to noncontrolling interest because this entity will not convert to a “C” corporation.

(4) This column gives effect to the final distribution relating to the termination of our “S” corporation status equal to 100% of our cumulative undistributed taxable income from the date of our formation through August 2, 2015, equal to $34.5 million. This assumes a distribution to the shareholders followed by a contribution to capital of the corporation.

(5) This column gives effect to (i) the sale by us of 6,666,667 shares of our Class B common stock in this offering assuming an initial public offering price of $15.00 per share, the midpoint of the filing range set forth on the cover page of this prospectus, after deducting the underwriting discounts and commissions and estimated offering expenses payable by us and (ii) the application of the estimated proceeds from this offering as described under “Use of Proceeds.”

(6) Includes one outlet store.

Non-U.S. GAAP Financial Measures

We report our financial results in accordance with U.S. generally accepted accounting principles, or U.S. GAAP. To supplement this information, we also use non-U.S. GAAP financial measures in this prospectus, including EBITDA and Adjusted EBITDA. EBITDA is calculated as net income before interest expense, income tax expense, and depreciation and amortization expenses. Adjusted EBITDA is calculated as EBITDA further adjusted for non-cash stock based compensation expense and a payment for a portion of the grantees’ tax liabilities associated with a grant of restricted stock awards. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for our definition of Adjusted EBITDA.

11

Table of Contents

The following table represents reconciliations of net income to EBITDA and EBITDA to Adjusted EBITDA for the periods indicated below:

| Fiscal Year Ended | Six Months Ended | |||||||||||||||

| February 2, 2014 | February 1, 2015 | August 3, 2014 | August 2, 2015 | |||||||||||||

| (in thousands) | ||||||||||||||||

| Net income |

$ | 16,053 | $ | 24,107 | $ | 6,855 | $ | 8,472 | ||||||||

| Depreciation and amortization |

1,247 | 1,821 | 823 | 1,174 | ||||||||||||

| Interest expense |

248 | 341 | 127 | 112 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| EBITDA |

17,548 | 26,269 | 7,805 | 9,758 | ||||||||||||

| Non-cash stock based compensation expense |

76 | 74 | 32 | 332 | ||||||||||||

| Payment for a portion of the grantees’ tax liabilities associated with a grant of restricted stock awards |

— | 318 | 318 | 1,115 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 17,624 | $ | 26,661 | $ | 8,155 | $ | 11,205 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

12

Table of Contents

Investing in our Class B common stock involves a high degree of risk. Before you invest, you should carefully consider the following risks, as well as general economic and business risks and all of the other information contained in this prospectus. Any of the following risks could have a material adverse effect on our business, operating results and financial condition and cause the trading price of our Class B common stock to decline, which could cause you to lose all or part of your investment.

Risks Related to Our Business

If we fail to offer products that customers want to purchase, our business and results of operations could be adversely affected.

Our products must satisfy the desires of customers, whose preferences change over time. In order to be successful, we must design, obtain and offer to customers innovative and high-quality products on a continuous and timely basis. Failure to effectively respond to customer needs and preferences, or convey a compelling brand image or price-to-value equation to customers may result in lower net sales and gross profit margins.

Our success depends in part on management’s ability to effectively anticipate or identify customer needs and preferences and respond quickly with marketable product offerings in advance of the actual time of sale to the customer. Even if we are successful in anticipating or identifying our customers’ needs and preferences, we must continue to develop and introduce innovative, high-quality products and product features in response to changing consumer demand.

Factors that could affect our ability to accurately forecast consumer demand for our products include:

| • | a failure in our solution-based design process to accurately identify the problems our customers are experiencing with commonly available apparel and gear or a lack of customer acceptance of new products or product features we design; |

| • | customer unwillingness to attribute premium value to our new products or product features we design relative to the commonly available apparel and gear they were intended to replace; |

| • | new, well-received product introductions by competitors; |

| • | weak economic conditions or consumer confidence, which reduce demand for our products; and |

| • | terrorism, civil unrest or acts of war, or the threat thereof, which adversely affect consumer confidence and spending and/or interrupt production and distribution of products and raw materials. |

There can be no assurance that we will be able to successfully anticipate or identify our customers’ needs and preferences and design products and product features in response. As a result, we may not successfully manage inventory levels to meet our future order requirements. If we fail to accurately forecast consumer demand, we may experience excess inventory levels or a shortage of product required to meet the demand. Inventory levels in excess of consumer demand may result in inventory write-downs and the sale of excess inventory at discounted prices, which could have an adverse effect on the image and reputation of our brand and negatively impact profitability. On the other hand, if we underestimate demand for our products, our third-party manufacturers may not be able to produce sufficient quantities of our products to meet consumer requirements, and this could result in delays in the shipment of products and lost revenue, as well as damage to the image and reputation of our brand and our relationship with our customers. These risks could have a material adverse effect on our brand as well as our results of operations and financial condition.

13

Table of Contents

Our business depends on our ability to maintain a strong brand. We may not be able to maintain and enhance the Duluth Trading brand if we receive unfavorable complaints, negative publicity or otherwise fail to live up to consumers’ expectations, which could materially adversely affect our business, results of operations and growth prospects.

We currently offer a differentiated brand to our customers defined by solution-based products manufactured with high quality craftsmanship, humorous and distinctive marketing, and an outstanding customer experience. Maintaining and enhancing the Duluth Trading brand is critical to expanding our base of customers. If we fail to maintain our brand, or if we incur excessive expenses in this effort, our business, operating results and financial condition may be materially adversely affected. We anticipate that, as we raise our profile nationally and attract an increasing amount of competition, maintaining and enhancing our brand may become increasingly difficult and expensive and may require us to make substantial additional investments in areas such as marketing, store operations, merchandising, technology and personnel.

Customer complaints or negative reactions to, or unfavorable publicity about, our product quality or product features, our storytelling or irreverent advertising, the shopping experience on our website or in our retail stores, product delivery times, customer data handling and security practices or customer support, especially on blogs, social media, other third-party websites and our website, could rapidly and severely diminish consumer use of our website and catalogs, visits to our retail stores and consumer confidence in us and result in harm to our brand. Furthermore, these factors could cause our customers to no longer feel a personal connection with the Duluth Trading brand, which could result in the loss of customers and materially adversely affect our business, results of operations and growth prospects.

Our marketing strategy of associating our brand and products with the Modern, Self-Reliant American Lifestyle may not be successful with future customers.

We have been successful in marketing our products by associating our brand and products with a heritage of workwear and the Modern, Self-Reliant American Lifestyle. To sustain long-term growth, we must continue to be successful in promoting our products to customers who identify with this lifestyle. If our customer base declines through natural attrition and is not replaced by new customers due to, for example, a lack of personal identification with this lifestyle, our net sales could decline, which could adversely affect our business, results of operations and financial condition.

Our net sales and profits depend on the level of consumer spending for apparel, footwear and accessories, which is sensitive to general economic conditions and other factors. An economic recession or a decline in consumer spending could have a material adverse effect on our business and results of operations.

The apparel, footwear and accessories industry has historically been subject to cyclical variations and is particularly affected by adverse trends in the general economy. The success of our business depends on consumer spending. There are a number of factors that influence consumer spending, including actual and perceived economic conditions, disposable consumer income, interest rates, consumer credit availability, unemployment, stock market performance, extreme weather conditions, energy prices and tax rates in the national, regional and local markets where we sell our products. A decline in actual or perceived economic conditions or other factors could negatively impact the level of consumer spending and have a material adverse impact on our business and results of operations.

Retail store expansion could adversely affect the operating results of our retail channel and reduce the revenue of our direct channel.

As we increase the number of our retail stores, our stores may become more highly concentrated in the geographic regions we serve. As a result, the number of customers and related net sales at individual stores may decline and the payback period may be increased. In addition, as we open more retail stores, and if our competitors open stores with similar formats, our retail store format may become less unique and may be less

14

Table of Contents

attractive to customers as a shopping destination. If either of these events occurs, the operating results of our retail channel could be materially adversely affected. The growth in the number of our retail stores may also draw customers away from our website and catalogs, which could materially adversely affect net sales from our direct channel.

If we cannot successfully implement future retail store expansion, our growth and profitability could be adversely impacted.

After the completion of this offering, we plan to open new retail stores. Our ability to open new retail stores in a timely manner and operate them profitably depends on a number of factors, many of which are beyond our control, including:

| • | our ability to manage the financial and operational aspects of our retail growth strategy, including making appropriate investments in our software systems, information technology and operational infrastructure; |

| • | our ability to identify suitable locations, including our ability to gather and assess demographic and marketing data to accurately determine consumer demand for our products in the locations we select; |

| • | our ability to negotiate favorable lease agreements; |

| • | our ability to properly assess the profitability and payback period of potential new retail store locations; |

| • | the availability of financing on favorable terms; |

| • | our ability to secure required governmental permits and approvals; |

| • | our ability to hire and train skilled store operating personnel, especially management personnel; |

| • | the availability of construction materials and labor and the absence of significant construction delays or cost overruns; |

| • | our ability to provide a satisfactory mix of merchandise that is responsive to the needs of our customers living in the areas where new retail stores are built; |

| • | our ability to establish a supplier and distribution network able to supply new retail stores with inventory in a timely manner; |

| • | our competitors building or leasing stores near our retail stores or in locations we have identified as targets for a new retail store; |

| • | consumer demand for our products, which drives traffic to our retail stores; and |

| • | general economic and business conditions affecting consumer confidence and spending and the overall strength of our business. |

We may not be able to grow the number of our retail stores, accelerate the rate of new store openings, achieve the net sales growth and payback periods historically achieved by our retail stores or maintain consistent levels of profitability in our retail stores, particularly as we expand into markets now served by other apparel chains, outdoor specialty stores, apparel catalog businesses and online apparel businesses. In addition, the substantial management time and resources which our retail store expansion strategy requires may result in disruption to our existing business operations which may decrease our profitability.

We may face risks and new challenges associated with our geographic expansion.

Our retail stores as of November 2015 are concentrated in the Midwest. As we expand our retail store locations, we may face new challenges that are different from those we currently encounter. Our expansion into new geographic markets could result in increased competitive, merchandising, distribution and other challenges. We may encounter difficulties in attracting customers in our new retail locations due to a lack of customer familiarity with our brand, our lack of familiarity with local customer preferences, competition with new

15

Table of Contents

competitors or with existing competitors with a large, established market presence and seasonal differences in the market. Our ability to expand successfully into other geographic markets will depend on acceptance of our retail store experience by customers in those markets, including our ability to design our stores in a manner that resonates locally and to offer the correct product assortment to appeal to consumers in such markets. There can be no assurance that any newly opened stores will be received as well as, or achieve net sales or profitability levels consistent with, our projected targets or be comparable to those of our existing stores in the time periods estimated by us, or at all. If our stores fail to achieve, or are unable to sustain, acceptable net sales and profitability levels, our business, results of operations and growth prospects may be materially adversely affected.

Furthermore, our retail stores may be located in regions that will be far from our Belleville, Wisconsin headquarters and will require additional management time and attention. Failure to properly supervise the operation and maintain the consistency of the customer experience in those retail stores could result in loss of customers and potentially harm future net sales prospects.

We may be unable to keep existing retail store locations or open new retail locations in desirable places, which could materially adversely affect our sales and profitability.

We may be unable to keep existing retail locations or open new retail locations in desirable places in the future. We compete with other retailers and businesses for suitable retail locations. Local land use, local zoning issues, environmental regulations and other regulations may affect our ability to find suitable retail locations and also influence the cost of leasing or buying them. We also may have difficulty negotiating real estate leases for new stores, renewing real estate leases for existing stores or negotiating purchase agreements for new sites on acceptable terms. In addition, construction, environmental, zoning and real estate delays may negatively affect retail location openings and increase costs and capital expenditures. If we are unable to keep up our existing retail store locations or open new retail store locations in desirable places and on favorable terms, our net sales and profits could be materially adversely affected.

The success of our direct channel depends on customers’ use of our digital platform, including our website, and response to catalogs and digital marketing; if our overall marketing strategies, including our maintenance of a robust customer list, is not successful, our business and results of operations could be materially adversely affected.

The level of customer traffic and volume of customer purchases through our direct channel, which accounted for approximately 90% of our net sales in fiscal 2014, is substantially dependent on our ability to provide a content-rich and user-friendly website, widely distributed and informative catalogs, a fun, easy and hassle-free customer experience and reliable delivery of our products. If we are unable to maintain and increase customers’ use of our e-commerce platform, including our website, which accounted for 78% of our direct channel net sales in fiscal 2014, and the volume of purchases decline, our business and results of operations could be adversely affected.

Customer response to our catalogs and digital marketing is substantially dependent on merchandise assortment, merchandise availability and creative presentation, as well as the selection of customers to whom our catalogs are sent and to whom our digital marketing is directed, changes in mailing strategies and the size of our mailings. Our maintenance of a robust customer list, which we believe includes desirable demographic characteristics for the products we offer, has also been a key component of our overall strategy. If the performance of our website, catalogs and email declines, or if our overall marketing strategy is not successful, our business and results of operations could be adversely affected.

16

Table of Contents

Dependence on our e-commerce sales channel subjects us to numerous risks that could have a material adverse effect on our business, financial condition and results of operations.

Sales through our e-commerce business accounted for 70% of our total net sales in fiscal 2014. Our results of operations and financial condition are dependent on maintaining our e-commerce business and expanding our e-commerce business is an important part of our growth strategy. Dependence on our e-commerce business and its continued growth subjects us to certain risks, including:

| • | diversion of traffic from our stores; |

| • | liability for online content; |

| • | the need to keep pace with rapid technological change; |

| • | government regulation of the Internet, including taxation; and |

| • | risks related to the computer systems that operate our website and related support systems, including computer viruses, systems failure or inadequacy, electronic break-ins and similar disruptions. |

Our failure to successfully respond to these risks and uncertainties could reduce our e-commerce sales, increase our costs, diminish our growth prospects, and damage our brand, which could negatively impact our business, financial condition and results of operations.

Competitive pricing pressures with respect to shipping our products to our customers may harm our business and results of operations.

Given the size of our direct segment net sales relative to our total net sales, shipping and handling revenue has had a significant impact on our gross profit and gross profit margin. Historically, this revenue has partially offset our shipping and handling expense included in selling, general and administrative expenses. Online and omnichannel retailers are increasing their focus on delivery services, with customers increasingly seeking faster, guaranteed delivery times and low-price or free shipping. To remain competitive, we may be required to offer discounted, free or other more competitive shipping options to our customers, which may result in declines in our shipping and handling revenue and increased shipping and handling expense. Declines in shipping and handling revenues may have a material adverse effect on our gross profit and gross profit margin, as well as our Adjusted EBITDA to the extent there are not commensurate declines, or if there are increases, in our shipping and handling expense.

We are subject to payment-related risks.

We accept payments using a variety of methods, including credit cards, debit cards, gift cards and physical bank checks. For existing and future payment methods we offer to our customers, we may become subject to additional regulations and compliance requirements (including obligations to implement enhanced authentication processes that could result in increased costs and reduce the ease of use of certain payment methods), as well as fraud. For certain payment methods, including credit and debit cards, we pay interchange and other fees, which may increase over time, raising our operating costs and lowering profitability. We rely on third-party service providers for payment processing services, including the processing of credit and debit cards. In each case, it could disrupt our business if these third-party service providers become unwilling or unable to provide these services to us. We are also subject to payment card association operating rules, including data security rules, certification requirements and rules governing electronic funds transfers, which could change or be reinterpreted to make it difficult or impossible for us to comply. If we fail to comply with these rules or requirements, or if our data security systems are breached or compromised, we may be liable for card issuing banks’ costs, subject to fines and higher transaction fees and/or lose our ability to accept credit and debit card payments from our customers and process electronic funds transfers or facilitate other types of payments, and our business and operating results could be adversely affected.

17

Table of Contents

We rely on third-party service providers, such as UPS and the United States Postal Service, or USPS, to deliver products purchased through our direct channel to our customers and our business could be negatively impacted by disruptions in the operations of these third-party service providers.

Relying on third-party service providers puts us at risk from disruptions in their operations, such as employee strikes, inclement weather and their inability to meet our shipping demands. If we are forced to use other delivery service providers, our costs could increase and we may be unable to meet shipment deadlines. Moreover, we may be unable to obtain terms as favorable as those received from the transportation providers we currently use, which would further increase our costs. In addition, if our products are not delivered to our customers on time, our customers may cancel their orders or we may lose business from these customers in the future. These factors may negatively impact our financial condition and results of operations.

Increases in postage, paper and printing costs could adversely affect the costs of producing and distributing our catalogs and promotional mailings, which could have an adverse effect on our business and results of operations.

Catalog mailings are a key aspect of our business and increases in costs relating to postage, paper and printing would increase the cost of our catalog mailings and could reduce our profitability to the extent that we are unable to offset such increases by raising prices, by implementing more efficient printing, mailing, delivery and order fulfillment systems or by using alternative direct-mail formats.

We currently use the USPS for distribution of substantially all of our catalogs and are therefore vulnerable to postal rate increases. The current economic and legislative environments may lead to further rate increases or a discontinuation of the discounts for bulk mailings and sorting by zip code and carrier routes, which we currently leverage for cost savings.

Paper for catalogs and promotional mailings is a vital resource in the success of our business. The market price for paper has fluctuated significantly in the past and may continue to fluctuate in the future. In addition, the continued consolidation or closings of production facilities in the United States may have an impact on future pricing and supply availability of catalog paper. We do not have multi-year fixed-price contracts for the supply of paper and are not guaranteed access to, or reasonable prices for, the amounts required for the operation of our business over the long term.

We also depend upon external vendors to print and mail our catalogs. The limited number of printers capable of handling such needs subjects us to risks if any printer fails to perform under our agreement. Most of our catalog-related costs are incurred prior to mailing, and we are not able to adjust the costs of a particular catalog mailing to reflect the actual subsequent performance of the catalog.

If we fail to acquire new customers, or fail to do so in a cost-effective manner, we may not be able to increase net revenue or profit per active customer.

Our success depends on our ability to acquire customers in a cost-effective manner. In order to expand our customer base, we must appeal to and acquire customers who identify with the Duluth Trading brand. We have made significant investments related to customer acquisition and expect to continue to spend significant amounts to acquire additional customers. For example, we have recently expanded our national television advertising campaigns. Such campaigns are expensive and may not result in the cost-effective acquisition of customers. Furthermore, as our brand becomes more widely known in the market, future marketing campaigns may not result in the acquisition of new customers at the same rate as past campaigns.

We believe that many of our new customers originate from word-of-mouth and other non-paid referrals from existing customers. Therefore, we must ensure that our existing customers remain loyal in order for us to continue receiving those referrals. If our efforts to satisfy our existing customers are not successful, we may not be able to acquire sufficient numbers of new customers through word-of-mouth and other non-paid referrals so as to continue to grow our business in a cost-effective manner, and we may be required to incur significantly higher marketing expenses in order to acquire new customers.

18

Table of Contents

We also use other paid and non-paid advertising. Our paid advertising includes search engine marketing, display advertising and paid social media. Our non-paid advertising efforts include search engine optimization, non-paid social media and email. We obtain a significant amount of traffic via search engines and, therefore, rely on search engines such as Google, Yahoo! and Bing. Search engines frequently update and change the logic that determines the placement and display of results of a user’s search, such that the purchased or algorithmic placement of links to our sites can be negatively affected. Moreover, a search engine could, for competitive or other purposes, alter its search algorithms or results, causing our sites to place lower in search query results. A major search engine could change its algorithms in a manner that negatively affects our paid or non-paid search ranking, and competitive dynamics could impact the effectiveness of search engine marketing or search engine optimization. We also obtain a significant amount of traffic via social networking websites or other channels used by our current and prospective customers. As e-commerce and social networking continue to rapidly evolve, we must continue to establish relationships with these channels and may be unable to develop or maintain these relationships on acceptable terms. Additionally, digital advertising costs may continue to rise and as our usage of these channels expands, such costs may impact our ability to acquire new customers in a cost-effective manner. If the level of usage of these channels by our customer base does not grow as expected, we may suffer a decline in customer growth or net sales. A significant decrease in the level of usage or customer growth would have a material adverse effect on our business, financial condition and operating results.