Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CITIZENS FINANCIAL GROUP INC/RI | d50192d8k.htm |

| EX-99.1 - EX-99.1 - CITIZENS FINANCIAL GROUP INC/RI | d50192dex991.htm |

| EX-99.3 - EX-99.3 - CITIZENS FINANCIAL GROUP INC/RI | d50192dex993.htm |

3Q15 Financial Results

October 23, 2015

Exhibit 99.2 |

Forward-looking statements

1 This document contains forward-looking statements within the Private Securities Litigation Reform Act of 1995. Any statement that does not describe historical or current facts is a forward-looking statement. These statements often include the words “believes,” “expects,” “anticipates,” “estimates,” “intends,” “plans,” “goals,” “targets,” “initiatives,” “potentially,” “probably,” “projects,” “outlook” or similar expressions or future conditional verbs such as “may,” “will,” “should,” “would,” and “could.” Forward-looking statements are based upon the current beliefs and expectations of management, and on information currently available to management. Our statements speak as of the date hereof, and we do not assume any obligation to update these statements or to update the reasons why actual results could differ from those contained in such statements in light of new information or future events. We caution you, therefore, against relying on any of these forward-looking statements. They are neither statements of historical fact nor guarantees or assurances of future performance. While there is no assurance that any list of risks and uncertainties or risk factors is complete, important factors that could cause actual results to differ materially from those in the forward-looking statements include the following, without limitation: negative economic conditions that adversely affect the general economy, housing prices, the job market, consumer confidence and spending habits which may affect, among other things, the level of nonperforming assets, charge-offs and provision expense; the rate of growth in the economy and employment levels, as well as general business and economic conditions; our ability to implement our strategic plan, including the cost savings and efficiency components, and achieve our indicative performance targets; our ability to remedy regulatory deficiencies and meet supervisory requirements and expectations; liabilities and business restrictions resulting from litigation and regulatory investigations; our capital and liquidity requirements (including under regulatory capital standards, such as the Basel III capital standards) and our ability to generate capital internally or raise capital on favorable terms; the effect of the current low interest rate environment or changes in interest rates on our net interest income, net interest margin and our mortgage originations, mortgage servicing rights and mortgages held for sale; changes in interest rates and market liquidity, as well as the magnitude of such changes, which may reduce interest margins, impact funding sources and affect the ability to originate and distribute financial products in the primary and secondary markets; the effect of changes in the level of checking or savings account deposits on our funding costs and net interest margin; financial services reform and other current, pending or future legislation or regulation that could have a negative effect on our revenue and businesses, including the Dodd- Frank Act and other legislation and regulation relating to bank products and services; a failure in or breach of our operational or security systems or infrastructure, or those of our third party vendors or other service providers, including as a result of cyber attacks; management’s ability to identify and manage these and other risks; and any failure by us to successfully replicate or replace certain functions, systems and infrastructure provided by The Royal Bank of Scotland Group plc (RBS). In addition to the above factors, we also caution that the amount and timing of any future common stock dividends or share repurchases will depend on our financial condition, earnings, cash needs, regulatory constraints, capital requirements (including requirements of our subsidiaries), and any other factors that our board of directors deems relevant in making such a determination. Therefore, there can be no assurance that we will pay any dividends to holders of our common stock, or as to the amount of any such dividends. In addition, the timing and manner of the sale of RBS’s remaining ownership of our common stock remains uncertain, and we have no control over the manner in which RBS may seek to divest such remaining shares. Any such sale would impact the price of our shares of common stock. More information about factors that could cause actual results to differ materially from those described in the forward-looking statements can be found under “Risk Factors” in Part I, Item 1A in our Annual Report on Form 10-K for the year ended December 31, 2014, filed with the United States Securities and Exchange Commission on March 3, 2015. Note: Percentage changes, per share amounts, and ratios presented in this document are calculated using whole dollars. |

3Q15 highlights 2 1) Adjusted results are non-GAAP items. Where there is a reference to an “Adjusted” result in a paragraph, all measures which follow that “Adjusted” result are also “Adjusted” and exclude restructuring charges and special items as applicable. See important information on use of Non-GAAP items in the Appendix. There were no restructuring charges or special items recorded in third quarter 2015. Improving profitability and returns Diluted EPS of $0.40 compares with Adjusted diluted EPS 1 of $0.40 in 2Q15 and $0.36 in 3Q14 Solid operating leverage of 3% YoY, 1% sequential quarter NIM improvement to 2.76% in 3Q15 from 2.72% in 2Q15 Strong capital, liquidity, and funding Excellent credit quality and progress on risk management Continued progress on strategic growth and efficiency initiatives Robust capital levels with a Common Equity Tier 1 Ratio of 11.8% Tangible book value per share growth of 2% in 3Q15 Average deposits increased $9.3 billion, or 10% vs 3Q14; loan-to-deposit ratio of 96%

In early August executed $250 million subordinated-debt offering and share

repurchase – in connection

with July sell-down, RBS ownership ~20.9%

Continued strong credit quality with nonperforming loans down 2% from 2Q15 and

4% from 3Q14 Net charge-off ratio of 0.31% compared with

0.33% in 2Q15 and 0.38% in 3Q14 Allowance for loan and lease

losses of 1.23% of total loans and leases stable with 2Q15

Allowance coverage of NPLs 116% vs. 114% in 2Q15 and 111% in 3Q14

Generated 8% YoY average loan growth, with strength in commercial, auto,

student and mortgage —

YoY average loan growth of $7.1 billion, with $4.0 billion in commercial, $2.4

billion in auto, and a net $786 million across other

portfolios Consumer initiatives –

2% HH growth YoY, continued progress in student and organic auto originations,

business bankers up 39 YoY

Commercial initiatives –

Strong loan growth across major businesses with CRE loans up 17%

YoY; Treasury Solutions fees up 7% YoY.

Continued focus on expense discipline -

Noninterest expense up 1% from Adjusted 3Q14

1 despite continued investments in technology, growth initiatives and regulatory programs

— On track to deliver targeted $200 million end of 2016 savings goal Making progress on new initiatives designed to enhance performance |

Financial summary –

GAAP 3 1) Non-GAAP item. See important information on use of Non-GAAP items in the Appendix.

2) Includes held for sale. 3) Return on average tangible common equity. 4) Return on average total tangible assets. 5) Full-time equivalent employees. Highlights Linked quarter: GAAP net income up $30 million driven by a $25 million after-tax decrease in restructuring charges and special items — 3Q15 reflects $7 million preferred dividend, payable semi-annually NII up $16 million, reflecting 1% average loan growth and an additional day Noninterest income down $7 million largely reflecting a reduction in mortgage banking and capital markets fees from relatively strong 2Q15 levels Noninterest expense down $43 million, driven by a $40 million decrease in restructuring charges and special items Provision expense stable with prior quarter Prior year quarter: Net income increased $31 million driven by a $13 million after-tax decrease in restructuring charges and special items NII up $36 million, as average loans grew 8% — 5% average earning asset growth Noninterest income up $12 million, led by an increase in other income and broad growth across most other categories Noninterest expense down 1% Provision for credit losses of $76 million was stable with prior year levels 3Q15 change from $s in millions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Net interest income 856 $ 840 $ 820 $ 16 $ 2 % 36 $ 4 % Noninterest income 353 360 341 (7) (2) 12 4 Total revenue 1,209 1,200 1,161 9 1 48 4 Noninterest expense 798 841 810 (43) (5) (12) (1) Pre-provision profit 411 359 351 52 14 60 17 Provision for credit losses 76 77 77 (1) (1) (1) (1) Income before income tax expense 335 282 274 53 19 61 22 Income tax expense 115 92 85 23 25 30 35 Net income 220 $ 190 $ 189 $ 30 $ 16 % 31 $ 16 % Preferred dividends 7 $ — $ — $ 7 $ NM 7 $ NM Net income available to common stockholders 213 $ 190 $ 189 $ 23 $ 12 % 24 $ 13 % $s in billions Average interest earning assets 123.0 $ 123.2 $ 117.2 $ (0.2) $ — % 5.8 $ 5 % Average deposits 2 101.0 $ 98.5 $ 91.7 $ 2.5 $ 2 % 9.3 $ 10 % Key metrics Net interest margin 2.76 % 2.72 % 2.77 % 4 bps (1) bps Loan-to-deposit ratio (period-end) 2 96.1 % 96.6 % 97.3 % (58) bps (126) bps ROTCE 1,3 6.6 % 5.9 % 5.8 % 70 bps 79 bps ROTA 1,4 0.7 % 0.6 % 0.6 % 9 bps 7 bps Efficiency ratio 1 66 % 70 % 70 % (400) bps (382) bps FTEs 5 17,817 17,903 17,852 (86) — % (35) — % Per common share Diluted earnings 0.40 $ 0.35 $ 0.34 $ 0.05 $ 14 % 0.06 $ 18 % Tangible book value 1 24.52 $ 24.03 $ 23.04 $ 0.49 $ 2 % 1.48 $ 6 % Average diluted shares outstanding (in millions) 533.4 539.9 560.2 (6.5) (1) % (26.8) (5) % |

Restructuring charges and special items

4 GAAP results included restructuring charges and special items related to enhancing efficiencies and improving processes across the organization and separation from The Royal Bank of Scotland Group plc (“RBS”). 1) These are non-GAAP financial measures. Please see Non-GAAP Reconciliation Tables in the Appendix for an explanation of our use of

non-GAAP financial measures and their reconciliation to GAAP.

Restructuring charges and special items

1 3Q15 change from ($s in millions, except per share data) 3Q15 2Q15 3Q14 2Q15 3Q14 Pre-tax total noninterest expense restructuring charges and special items — 40 21 (40) (21) After-tax total noninterest expense restructuring charges and special items — 25 13 (25) (13) Pre-tax restructuring charges and special items — (40) (21) 40 21 After-tax restructuring charges and special items — (25) (13) 25 13 Diluted EPS impact — $ (0.05) $ (0.02) $ 0.05 $ 0.02 $ |

Adjusted financial summary -

excluding restructuring charges and special items

1 5 1) Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and special items associated with Chicago Divestiture,

efficiency and effectiveness programs and separation from RBS. See

important information on use of Non-GAAP items in the Appendix.

2) Includes held for sale. 3) Adjusted return on average tangible common equity. 4) Adjusted return on average total tangible assets. 5) Full-time equivalent employees. Highlights 3Q15 vs. adjusted 2Q15: Net income increased $5 million from Adjusted 2Q15 as the benefit of revenue growth and lower expense was partially offset by an increase in the effective tax rate Total revenue up $9 million — NII up $16 million as 1% average loan growth, an additional day in the quarter, and improving investment portfolio and loan yields were muted by modestly higher deposit costs — Noninterest income down $7 million with other income and service charge and fee growth more than offset by a reduction in mortgage banking and capital markets fees from relatively robust 2Q levels — Adjusted noninterest expense down slightly reflecting continued cost discipline Efficiency ratio improved 68 basis points Provision expense stable with prior quarter Tangible book value per share of $24.52 up 2% 3Q15 vs. adjusted 3Q14: Net income up 9% from Adjusted 3Q14 reflecting impact of positive operating leverage Total revenue up $48 million — NII up 4% with 5% average earning asset growth muted by lower yields — Noninterest income up 4% Noninterest expense up 1% — Efficiency ratio improved by ~200 bps Adjusted diluted EPS up 11% 3Q15 change from $s in millions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Net interest income 856 $ 840 $ 820 $ 16 $ 2 % 36 $ 4 % Noninterest income 353 360 341 (7) (2) 12 4 Total revenue 1,209 1,200 1,161 9 1 48 4 Adjusted noninterest expense 1 798 801 789 (3) — 9 1 Adjusted pre-provision profit 1 411 399 372 12 3 39 10 Provision for credit losses 76 77 77 (1) (1) (1) (1) Adjusted pretax income 1 335 322 295 13 4 40 14 Adjusted income tax expense 1 115 107 93 8 7 22 24 Adjusted net income 220 $ 215 $ 202 $ 5 $ 2 % 18 $ 9 % Preferred dividends 7 $ — $ — $ 7 $ NM 7 $ NM Adjusted net income available to common stockholders 1 213 $ 215 $ 202 $ (2) $ (1) % 11 $ 5 % $s in billions Average interest earning assets 123.0 $ 123.2 $ 117.2 $ (0.2) $ — % 5.8 $ 5 % Average deposits 2 101.0 $ 98.5 $ 91.7 $ 2.5 $ 2 % 9.3 $ 10 % Key metrics Net interest margin 2.76 % 2.72 % 2.77 % 4 bps (1) bps Loan-to-deposit ratio (period-end) 2 96.1 % 96.6 % 97.3 % (58) bps (126) bps Adjusted ROTCE 1,3 6.6 % 6.7 % 6.2 % (7) bps 38 bps Adjusted ROTA 1,4 0.7 % 0.7 % 0.7 % 1 bps 2 bps Adjusted efficiency ratio 1 66 % 67 % 68 % (68) bps (200) bps FTEs 5 17,817 17,903 17,852 (86) — % (35) — % Per common share Adjusted diluted EPS 1 0.40 $ 0.40 $ 0.36 $ — $ — % 0.04 $ 11 % Tangible book value 1 24.52 $ 24.03 $ 23.04 $ 0.49 $ 2 % 1.48 $ 6 % Average diluted shares outstanding (in millions) 533.4 539.9 560.2 (6.5) (1) % (26.8) (5) % |

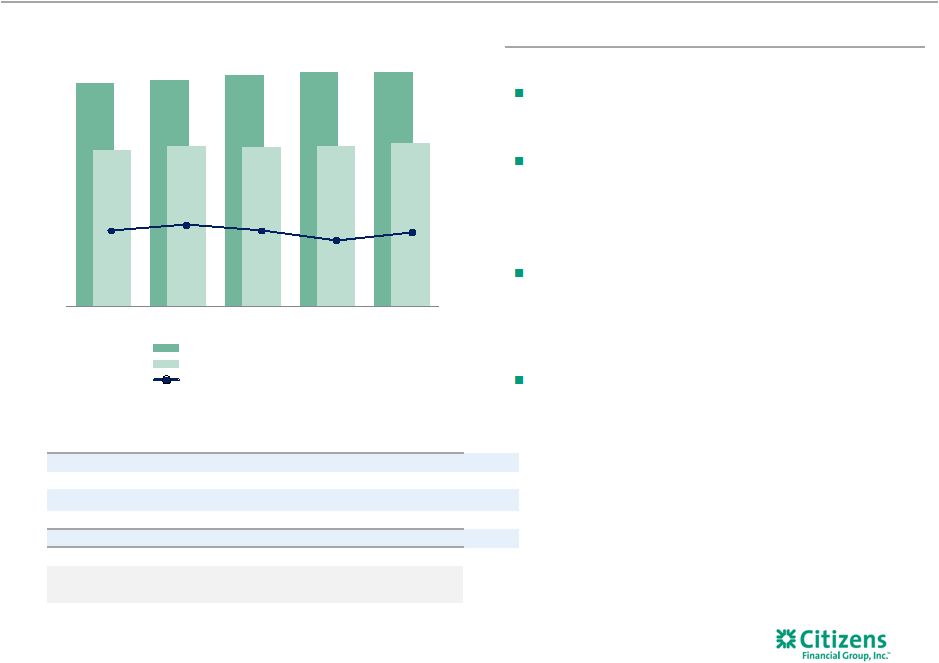

$117B $119B $121B $123B $123B $820 $840 $836 $840 $856 3Q14 4Q14 1Q15 2Q15 3Q15 2.77% 2.80% 2.77% 2.72% 2.76% Net interest income 6 Highlights Net interest income $s in millions, except earning assets Average interest-earning assets Average interest earning assets Net interest income Net interest margin 1) Includes Interest-bearing cash and due from banks and deposits in banks.

Linked quarter:

NII up $16 million, or 2%

— Reflects $1.2 billion increase in average loans and leases and an additional day in the quarter NIM improved 4 bps to 2.76% — Benefitting from initiatives to improve loan yields and mix and to improve balance sheet efficiency Prior year quarter: NII up $36 million, or 4% — 8% average loan growth, and reduction in pay-fixed swap costs, partially offset by continued pressure from the persistent low-rate environment and higher deposit costs NIM relatively stable despite continuing impact of the low- rate environment $s in billions 3Q14 4Q14 1Q15 2Q15 3Q15 Retail loans $48.5 $49.8 $50.4 $50.9 $51.6 Commercial loans 41.2 42.3 43.5 44.7 45.2 Investments and cash 1 27.3 26.5 27.1 27.1 25.8 Loans held for sale 0.2 0.2 0.3 0.5 0.5 Total interest-earning assets $117.2 $118.7 $121.3 $123.2 $123.0 Loan Yields 3.33% 3.34% 3.34% 3.30% 3.32% Cost of funds 0.45% 0.49% 0.50% 0.52% 0.54% |

2.72% 2.76% 0.03% 0.01% 0.01% (0.01%) 2Q15 NIM% Reduction in cash/securities Investment portfolio yields Loan yields Deposit costs 3Q15 NIM% 2.77% 2.76% 0.05% 0.04% (0.01%) (0.06%) (0.03%) 3Q14 NIM% Reduction in cash/securities Investment portfolio yields/ pay-fixed swap run off Loan yields Deposit costs Borrowing costs 3Q15 NIM% Net interest margin NIM walk 3Q14 to 3Q15 NIM walk 2Q15 to 3Q15 7 |

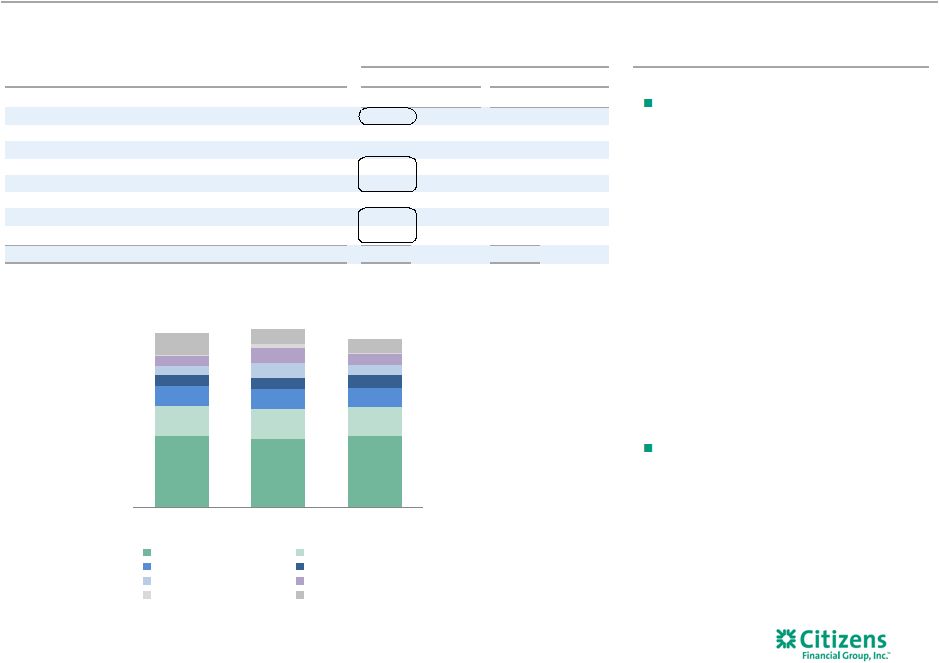

$353 $360 $341 3Q15 2Q15 3Q14 Service charges and fees Card fees Trust and inv services FX & trade finance fees Mortgage banking fees Capital markets fee income Securities gains (losses) Other income Noninterest income Linked quarter: Noninterest income down $7 million as growth in other income and service charges and fees was more than offset by reductions in mortgage banking and capital markets fees from relatively robust 2Q levels as well as lower securities gains — Mortgage banking fees down $12 million driven by an $8 million decrease in MSR valuation as well as lower origination volume and sale gains — Other income up $15 million given an $8 million branch real estate gain — Securities gains decreased $7 million Prior year quarter: Noninterest income up $12 million, or 4% — Growth in other income, card fees, trust & investment services fees and service charges and fees — More muted results in mortgage banking, capital markets and FX & trade finance fees 8 Highlights 1) Other income includes bank owned life insurance and other income. $s in millions 1 3Q15 change from 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Service charges and fees 145 $ 139 $ 144 $ 6 $ 4 % 1 $ 1 % Card fees 60 60 58 — — 2 3 Trust & investment services fees 41 41 39 — — 2 5 Mortgage banking fees 18 30 21 (12) (40) (3) (14) Capital markets fees 21 30 22 (9) (30) (1) (5) FX & trade finance fees 22 22 26 — — (4) (15) Securities gains, net 2 9 2 (7) (78) — — Other income 1 44 29 29 15 52 15 52 Noninterest income 353 $ 360 $ 341 $ (7) $ (2) % 12 $ 4 % |

$798 $801 $789 66% 67% 68% 3Q15 2Q15 3Q14 Adjusted salary and benefits Adjusted occupancy & equip Adjusted all other Adjusted efficiency ratio Adjusted noninterest expense – excluding restructuring charges and special items 1 3Q15 vs. Adjusted 2Q15: Noninterest expense down slightly relative to Adjusted 2Q15 levels, reflecting continued strong cost discipline — Reduction in equipment expense, other expense, and amortization of software was partially offset by an increase in outside services from unusually low second quarter levels — FTEs down 86 reflecting continuing focus on efficiency 3Q15 vs. Adjusted 3Q14: Noninterest expense increased $9 million from Adjusted 3Q14 levels — Lower salaries and benefits and amortization of software was more than offset by an increase in other expense, equipment expense and outside services — FTEs relatively stable as efficiency initiatives more than offset net investments to drive growth and enhance operational effectiveness, including increased regulatory-driven staffing requirements 9 Highlights 1) Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and special items associated with Chicago Divestiture,

efficiency and effectiveness programs and separation from RBS. See

important information on use of Non-GAAP items in the Appendix.

. 1 1 Full-time equivalents (FTEs) 17,817 17,903 17,852 1 3Q15 change from $s in millions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Adjusted salaries and benefits 1 404 $ 405 $ 409 $ (1) $ — % (5) $ (1) % Adjusted occupancy 1 75 75 75 — — — — Adjusted equipment expense 1 62 65 58 (3) (5) 4 7 Adjusted outside services 1 89 83 87 6 7 2 2 Adjusted amortization of software 1 35 37 38 (2) (5) (3) (8) Adjusted other expense 1 133 136 122 (3) (2) 11 9 Adjusted noninterest expense 1 798 $ 801 $ 789 $ (3) $ — % 9 $ 1 % Restructuring charges and special items — 40 21 (40) (100) (21) (100) Total noninterest expense 798 $ 841 $ 810 $ (43) $ (5) % (12) $ (1) % |

7% 30% 10% 16% 11% 5% 21% 51% 39% 10% Consolidated average balance sheet Linked quarter: Total earning assets stable with prior quarter — Commercial loans up $478 million driven by strength in Commercial Real Estate, Franchise Finance and Corporate Finance — Retail loans up $707 million driven by growth in auto, mortgage, and student Total deposits increased 2% — Growth focused on commercial relationships and consumer money market Prior year quarter: Total earning assets up 5% — Retail loans up 7% driven by growth in auto, mortgage and student — Commercial loans up 10% driven by growth in Commercial Real Estate, Industry Verticals, Corporate Finance, Franchise Finance, and Mid-Corporate Total deposits up $9.3 billion, or 10%, reflecting strength in money-market, term deposits and checking with interest Borrowed funds down $3.0 billion as reductions in FHLB advances and repos were partially offset by sub-debt issuances tied to our capital exchange transactions, as well as senior debt borrowings to enhance LCR 10 Highlights $123.0 billion Interest-earning assets $113.0 billion Deposits/borrowed funds Total Retail 42% Total Commercial 37% Note: Loan portfolio trends reflect non-core portfolio impact not included in segment results on pages 11 & 12.

1) Low-cost core deposits include demand, checking with interest, and regular savings.

CRE Other Commercial Residential mortgage Total home equity Automobile Other Retail Investments and interest-bearing deposits Retail / Personal Commercial/ Municipal/ Wholesale Borrowed funds 3Q15 change from $s in billions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Investments and interest bearing deposits 25.8 $ 27.1 $ 27.3 $ (1.4) $ (5) % (1.6) $ (6) % Total commercial loans 45.2 44.7 41.2 0.5 1 4.0 10 Total retail loans 51.6 50.9 48.5 0.7 1 3.2 7 Total loans and leases 96.8 95.6 89.7 1.2 1 7.1 8 Loans held for sale 0.5 0.5 0.2 — — 0.3 NM Total interest-earning assets 123.0 123.2 117.2 (0.2) — 5.8 5 Total noninterest-earning assets 12.1 12.3 11.5 (0.2) (2) 0.6 5 Total assets 135.1 $ 135.5 $ 128.7 $ (0.4) $ — 6.4 $ 5 Low-cost core deposits 1 51.7 51.1 48.7 0.7 1 3.0 6 Money market deposits 36.5 34.9 32.4 1.6 5 4.2 13 Term deposits 12.7 12.6 10.6 0.2 1 2.1 20 Total deposits 101.0 $ 98.5 $ 91.7 $ 2.5 $ 2 9.3 $ 10 Total borrowed funds 12.0 14.8 15.0 (2.8) (19) (3.0) (20) Total liabilities 115.6 $ 115.9 $ 109.3 $ (0.3) $ — 6.3 $ 6 Total stockholders' equity 19.5 19.6 19.4 (0.1) (1) 0.1 — Total liabilities and equity 135.1 $ 135.5 $ 128.7 $ (0.4) $ — % 6.4 $ 5 % |

Yields 3.67% 3.68% 3.72% 3.68% 3.69% $9.9 $10.6 $10.9 $11.1 $11.6 $19.1 $18.8 $18.4 $18.0 $17.6 $11.4 $12.4 $12.9 $13.5 $13.8 $1.6 $1.8 $2.3 $2.7 $3.2 $3.0 $3.0 $3.1 $3.1 $3.0 $2.7 $2.6 $2.5 $2.3 $2.4 $47.7B $49.2B $50.1B $50.7B $51.6B 3Q14 4Q14 1Q15 2Q15 3Q15 Mortgage Home Equity Auto Student Business Banking Other Consumer Banking average loans and leases 11 1) Other includes Credit Card, RV, Marine, Other. Average loans and leases $s in billions 1 Linked quarter: Average loans increased $863 million, or 2% Consumer loan yields up 1 basis point reflecting continued improvement in mix Prior year quarter: Average loans up $3.9 billion largely as growth of $2.4 billion in auto, $1.7 billion in mortgages and $1.6 billion in student was partially offset by $1.5 billion lower home equity outstandings Loan yields up modestly despite the continued pressure from the low-rate environment Recent developments: Mortgage originations of $1.6 billion in 3Q15, up $38 million QoQ and $543 million YoY Originated ~$60 million of new installment credit loans Highlights |

Yields 2.61% 2.62% 2.57% 2.56% 2.57% $5.9 $6.0 $6.2 $6.4 $6.2 $2.1 $2.5 $2.9 $3.0 $3.0 $2.7 $2.8 $2.9 $3.1 $3.2 $11.8 $11.7 $12.0 $12.2 $12.0 $6.1 $6.3 $6.1 $6.1 $6.1 $7.0 $7.2 $7.4 $7.7 $8.2 $2.2 $2.4 $2.6 $2.8 $3.1 $37.8B $38.9B $40.1B $41.3B $41.8B 3Q14 4Q14 1Q15 2Q15 3Q15 Mid-Corporate Industry Verticals Franchise Finance Middle Market Asset Finance Commercial Real Estate Other Commercial Banking average loans and leases Linked quarter: Average loans up $524 million, or 1%, with solid growth in CRE and Franchise Finance Loan yields remained relatively stable despite the continued effect of the low-rate environment Prior year quarter: Average loans up $4.1 billion on strength in Commercial Real Estate, Industry Verticals, Mid- Corporate, Franchise Finance and Corporate Finance Loan yields down 4 bps largely reflecting the pronounced effect of the continued low-rate environment in 2015 12 1) Other includes Business Capital, Govt & Professional Banking, Corporate Finance & Global Markets, Treasury Solutions, Corporate and Commercial Banking Admin. $s in billions 1 Highlights Average loans and leases |

$40.1 $40.9 $41.7 $43.0 $44.6 $25.8 $26.3 $25.8 $26.4 $26.8 $15.2 $15.7 $16.0 $16.6 $16.9 $10.6 $11.9 $12.2 $12.6 $12.7 $6.3 $5.1 $4.6 $4.4 $2.9 $6.7 $6.1 $7.0 $6.5 $5.1 $2.0 $2.8 $3.9 $3.9 $4.1 $106.7B $108.8B $111.2B $113.3B $113.0B 3Q14 4Q14 1Q15 2Q15 3Q15 Money market & savings DDA Checking with interest Term & time deposits Total fed funds & repo Short-term borrowed funds Total long-term borrowings Average funding and cost of funds Linked quarter: Average interest-bearing deposits increased $2.1 billion, or 3%, with particular strength in money market — Total deposit costs of 0.25% increased 1 bp, as the pace of growth slowed reflecting enhanced pricing strategies DDA up $335 million, interest checking up $373 million, money market & savings up $1.6 billion, and term deposits up $154 million Continued progress in repositioning liabilities structure to better align with peers Prior year quarter: Average interest-bearing deposits increased $8.4 billion, or 13%, on strength across all categories — Total deposit cost of funds increased 7 bps 13 Highlights Average interest-bearing liabilities and DDA $s in billions Deposit cost of funds 0.18% 0.20% 0.22% 0.24% 0.25% Total cost of funds 0.45% 0.49% 0.50% 0.52% 0.54% |

Summary of progress on strategic initiatives

14 Initiative 3Q15 Status Commentary Reenergize household growth 3Q15 household growth of 2% and deposits up 7% from 3Q14. New customer cross-sell rate

increased to 3.26 vs. 3.05 in 3Q14.

Expand mortgage sales force

LOs up 81, or 22%, and origination volume up 53% from 3Q14.

Continued competitive pressure around attracting and retaining LOs with strong

conforming orientation.

Grow Auto 3Q15 organic origination yields of 3.51%, up 41 bps from 3Q14. Grow Student Continued strong new refi product originations of $262 million in 3Q15. Expand Business Banking Relationship managers up 13 from 2Q15 and 39 since 3Q14. Pricing improvements gaining

traction with portfolio yields up 6 bps vs. 3Q14.

Expand Wealth sales force

Added 42 wealth managers and 151 licensed bankers over the past year; wealth

managers relatively flat with 2Q15.

Build out Mid-Corp & verticals

Mid-Corp and specialty vertical average loans up from 3Q14 by 6% and 42%,

respectively. Continue development of

Capital Markets

Fee income declined 5% from 3Q14 given weaker market conditions while market

share improved in traditional middle market &

sponsor-led deals. Build out Treasury Solutions

Fees up 7% in the quarter compared to 3Q14 with strong contributions from cash management and commercial card. Grow Franchise Finance Strong portfolio growth with average balances up 21% from 3Q14. Core: Middle Market Average loans up 2% YoY, with origination yields in 3Q15 expanding 33bps compared to 3Q14,

reflecting improved pricing discipline.

Core: CRE CRE average loans up 17% to $8.2 billion from 3Q14. Core: Asset Finance Portfolio balances flat compared to 3Q14. New business initiatives targeting areas with

attractive risk/return metrics underway to mitigate reduced RBS

referrals. Top I

On-track to largely complete $200 million in cost savings ideas by

YE15. Top II

Starting to see benefits from pricing and operations transformation initiatives. Revenue enhancement initiatives building momentum, but are earlier in evolution. Balance Sheet Optimization Initiatives in flight to focus balance sheet on most productive assets and lower deposit costs.

Recent efforts have begun to arrest NIM decline.

|

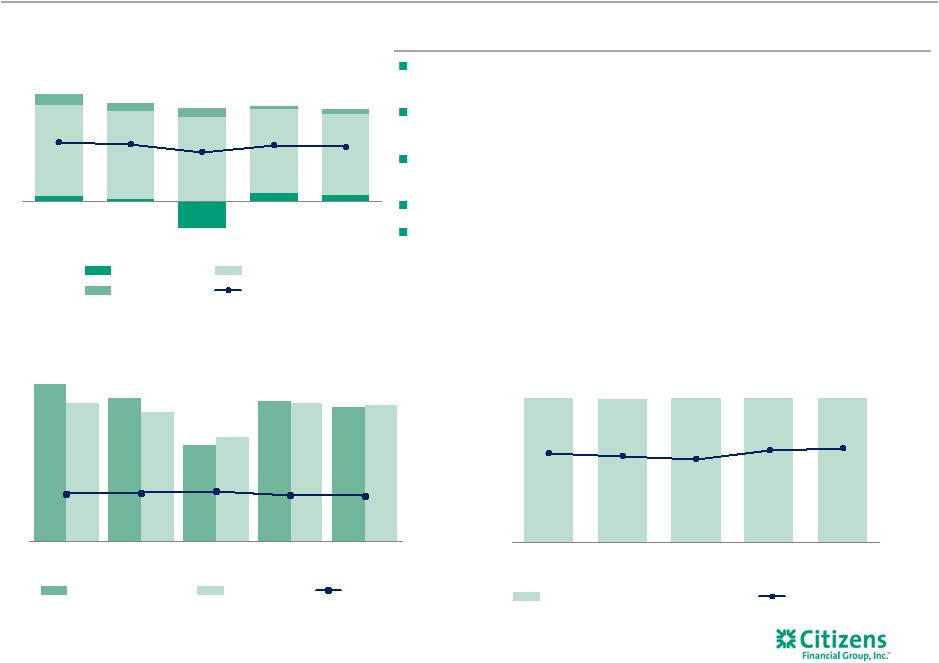

Overall credit quality remains strong. NPLs declined by $16 million or

2% QoQ

and 4% YoY Net charge-offs were $75 million, or 0.31% of average loans and leases

compared with 0.33% in 2Q15 and 0.38% in 3Q14

Provision for credit losses of $76 million in third quarter 2015 remained

stable with second quarter 2015

Allowance as a % of total loans and leases was stable, 1.23% vs. 1.24% in

2Q15 NPLs to total loans improved to 1.06% vs. 1.09% in

2Q15 —

Allowance coverage for NPLs increased to 116% vs. 114% in 2Q15

$4 $2 ($22) $7 $5 $75 $72 $69 $68 $66 $9 $6 $7 $3 $4 $88 $80 $54 $78 $75 0.38% 0.35% 0.23% 0.33% 0.31% 3Q14 4Q14 1Q15 2Q15 3Q15 Commercial Retail SBO Net c/o ratio $88 $80 $54 $78 $75 $77 $72 $58 $77 $76 $1.1B $1.1B $1.1B $1.1B $1.0B 3Q14 4Q14 1Q15 2Q15 3Q15 Net charge-offs Provision NPLs $1,201 $1,195 $1,202 $1,201 $1,201 111% 109% 106% 114% 116% 3Q14 4Q14 1Q15 2Q15 3Q15 Allowance for loan and lease losses Coverage Ratio Strong credit quality trends continue 15 Highlights Net charge-offs (recoveries) Provision for credit losses, charge-offs, NPLs Allowance for loan and lease losses $s in millions 1 for credit losses 1) Allowance for loan and lease losses to nonperforming loans and leases. |

16.1% 15.8% 15.5% 15.3% 15.4% 12.9% 12.4% 12.2% 11.8% 11.8% 3Q14 4Q14 1Q15 2Q15 3Q15 Total capital ratio Common equity tier 1 ratio 97% 98% 96% 97% 96% 3Q14 4Q14 1Q15 2Q15 3Q15 as of $s in billions (period-end) 3Q14 4Q14 1Q15 2Q15 3Q15 Basel I/III transitional basis 1,2 Basel I Basel III Common equity tier 1 capital 13.3 $ 13.2 $ 13.4 $ 13.3 $ 13.2 $ Risk-weighted assets 103.2 $ 106.0 $ 109.8 $ 112.1 $ 112.3 $ Common equity tier 1 ratio 12.9 % 12.4 % 12.2 % 11.8 % 11.8 % Total capital ratio 16.1 % 15.8 % 15.5 % 15.3 % 15.4 % Basel III fully phased-in 1,3 Common equity tier 1 ratio 12.5% 12.1% 12.1% 11.8% 11.7% Basel III minimum for CET1 ratio 2015 2016 2017 2018 2019 Basel III minimum plus phased-in capital conservation buffer 4.5 % 5.1 % 5.8 % 6.4 % 7.0 % Capital and liquidity remain strong 16 Highlights 1) Current reporting period regulatory capital ratios are preliminary. 2) Periods prior to 1Q15 reported on a Basel I basis. Basel III ratios assume that certain definitions impacting qualifying Basel III capital

will phase in through 2018. Ratios also reflect the required US

Standardized methodology for calculating RWAs, effective January 1, 2015.

3)

Prior to Basel III becoming effective January 1, 2015 this was a Non-GAAP financial measure. See important information on use of Non-GAAP items in the Appendix. 4) Based on the September 2014 release of the U.S. version of the Liquidity Coverage Ratio (LCR). Note that as a modified LCR company,

CFG’s formal compliance requirement of 90% does not begin

until January 2016.

5) Period-end Includes held for sale. Loan-to-deposit ratio 5 Capital ratio trend 1,2 1,2 Capital levels remain above regional peers 3Q15 Basel III common equity tier 1 ratio (transitional basis) down approximately 7 basis points from 2Q15 — Net income: ~20 bps increase — RWA growth: ~2 bps decrease — Share repurchase: ~22 bps decrease — Dividends & other: ~3 bps decrease LDR remained relatively stable at 96% Already meet initial LCR requirement 4 |

4Q15 outlook 17 4Q15 expectations vs. 3Q15 Net interest income, net interest margin Operating leverage, efficiency ratio Credit trends and costs Average loan growth rate of ~1.5% Net interest margin broadly stable Positive operating leverage expected to continue; anticipate fee income growth

Modest expense growth reflecting higher depreciation & software

amortization, seasonality Expect stable asset quality

trends Provision expense expected to increase given build

associated with loan growth Capital, liquidity

and funding Quarter-end Basel III common equity Tier 1 ratio ~11.7% Loan-to-deposit ratio 97-98% |

Key messages 18 Continue to execute well on our broad agenda — Good clean quarter with positive operating leverage, rebound in NIM — Delivering for all stakeholders — Adding top talent to executive team New initiatives tracking to expectations Asset sensitivity continues to be stable Asset quality, capital ratios, and liquidity position remain strong |

Appendix 19 ******************************************* |

$372 $411 3Q14 3Q15 $90.7 $97.4 3Q14 3Q15 0.66% 0.68% 3Q14 3Q15 $202 $220 $0.36 $0.40 3Q14 3Q15 6.2% 6.6% 3Q14 3Q15 Quarter over quarter results 20 Adjusted pre-provision profit 1 $s in millions Adjusted return on average tangible assets 1 Adjusted net income 1 $s in millions 1) Adjusted results are non-GAAP items and exclude the effect of net restructuring charges and special items associated with Chicago

Divestiture, efficiency and effectiveness programs and separation

from RBS. See important information on use of Non-GAAP items in the Appendix. 2) Excludes loans held for sale. Adjusted return on average tangible common equity 1 38 bps 2 bps 9% 10% Period-end loans 2 $s in billions Period-end deposits $s in billions 7% 11% Adjusted Diluted EPS 1 $101.9 9% $93.5 3Q14 3Q15 |

$399 $411 2Q15 3Q15 11.8% 11.8% 2Q15 3Q15 0.67% 0.68% 2Q15 3Q15 $215 $220 $0.40 $0.40 2Q15 3Q15 10.4% 10.4% 2Q15 3Q15 6.7% 6.6% 2Q15 3Q15 Linked quarter results 21 Adjusted pre-provision profit 1 $s in millions Adjusted return on average tangible assets 1 Adjusted net income 1 $s in millions Adjusted return on average tangible common equity 1 Tier 1 leverage ratio 2 7 bps 1 bps unchanged 2% 3% 1) Adjusted results are non-GAAP items and exclude the effect of net restructuring charges and special items associated with Chicago

Divestiture, efficiency and effectiveness programs and separation

from RBS. See important information on use of Non-GAAP items in the Appendix. 2) Current reporting period regulatory capital ratios are preliminary. unchanged Adjusted Diluted EPS 1 Basel III common equity tier 1 capital ratio 2 unchanged |

Consumer Banking segment

22 1) Non-GAAP item. Adjusted results exclude the effect of net restructuring charges and special items associated with Chicago Divestiture,

efficiency and effectiveness programs and separation from RBS. See

important information on use of Non-GAAP items in the Appendix.

2) Includes held for sale. 3) Operating segments are allocated capital on a risk-adjusted basis considering economic and regulatory capital requirements. We approximate that regulatory capital is equivalent to a sustainable target level for Tier 1 common equity and then allocate that approximation to the segments based on economic capital. Highlights Linked quarter: Net income up $2 million, or 3% Net interest income up $12 million, driven by loan growth and one additional day in the quarter, partially offset by higher deposit costs — Average loans up 2% and average deposits up 1% Noninterest income up $5 million as growth in other income, service charges and fees, and trust & investment services fees was partially offset by lower mortgage banking fees — Results include $8 million branch real estate sale gain — Mortgage banking fees down $12 million driven by an $8 million decrease in mortgage servicing rights valuation; originations up 2% Noninterest expense increased $10 million reflecting increased outside services and salary and benefits expense tied to growth initiatives Prior year quarter: Net income up $14 million, or 26% Total revenue up $33 million on strong loan growth and momentum in mortgage, household growth and wealth — Average loans up $4.0 billion and average deposits up $4.9 million Noninterest expense increased $14 million, as higher advertising and our continued investment in the business to drive further growth was partially offset by our focus on improving efficiency 3Q15 change from $s in millions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Net interest income 556 $ 544 $ 532 $ 12 $ 2 % 24 $ 5 % Noninterest income 235 230 226 5 2 9 4 Total revenue 791 774 758 17 2 33 4 Noninterest expense 623 613 609 10 2 14 2 Pre-provision profit 168 161 149 7 4 19 13 Provision for credit losses 64 60 66 4 7 (2) (3) Income before income tax expense 104 101 83 3 3 21 25 Income tax expense 36 35 29 1 3 7 24 Net income 68 $ 66 $ 54 $ 2 $ 3 % 14 $ 26 % Average balances $s in billions Total loans and leases 51.9 $ 51.0 $ 47.8 $ 0.9 $ 2 % 4.0 $ 8 % Total deposits 70.5 $ 70.0 $ 65.6 $ 0.6 $ 1 % 4.9 $ 7 % Mortgage Banking metrics Originations 1,561 $ 1,523 $ 1,018 $ 38 $ 2 % 543 $ 53 % Origination Pipeline 2,152 1,897 973 255 13 % 1,179 121 % Gain on sale of secondary originations 1.80% 2.18% 1.69% (38) bps 11 bps Performance metrics ROTCE 1,3 5.7% 5.7% 4.6% 1 bps 110 bps Efficiency ratio 1 79% 79% 80% (53) bps (170) bps |

Commercial Banking segment

23 1) Non-GAAP item. See important information on use of Non-GAAP items in the Appendix.

2) Includes held for sale. 3) Operating segments are allocated capital on a risk-adjusted basis considering economic and regulatory capital requirements. We

approximate that regulatory capital is equivalent to a sustainable

target level for Tier 1 common equity and then allocate that approximation to the segments based on economic capital. Linked quarter: Commercial Banking net income increased $10 million Total revenue up $5 million, net interest income up $13 million on an average 1% increase in loans and 8% increase in deposits — Strength in Commercial Real Estate, Franchise Finance, Corporate Finance — Average deposits up $1.9 billion, or 8% Noninterest income decreased $8 million due to a decrease in capital markets fees from strong second quarter levels Noninterest expense decreased $6 million, or 3%, largely reflecting lower regulatory costs and equipment expense, partially offset by increased outside services and insurance costs Prior year quarter: Net income increased $6 million, as 4% revenue growth was partially offset by increased noninterest expense and a $3 million increase in provision for credit losses. Net interest income up $29 million on an average

$4.2 billion increase in loans and $3.6 billion increase in

deposits Noninterest income down $4 million as strength in service charges and other fees, card fees, and interest rate products was offset by a reduction in foreign exchange and trade finance fees, capital market fees and leasing income Noninterest expense up $13 million driven by increased regulatory costs, salaries and benefits tied to growth initiatives and outside services expense Highlights 3Q15 change from $s in millions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Net interest income 299 $ 286 $ 270 $ 13 $ 5 % 29 $ 11 % Noninterest income 100 108 104 (8) (7) (4) (4) Total revenue 399 394 374 5 1 25 7 Noninterest expense 175 181 162 (6) (3) 13 8 Pre-provision profit 224 213 212 11 5 12 6 Provision for credit losses 3 7 — (4) (57) 3 — Income before income tax expense 221 206 212 15 7 9 4 Income tax expense 76 71 73 5 7 3 4 Net income 145 $ 135 $ 139 $ 10 $ 7 % 6 $ 4 % Average balances $s in billions Total loans and leases 2 42.0 $ 41.5 $ 37.8 $ 0.5 $ 1 % 4.2 $ 11 % Total deposits 24.6 $ 22.7 $ 21.0 $ 1.9 $ 8 % 3.6 $ 17 % Performance metrics ROTCE 1,3 12.2% 11.7% 13.1% 55 bps (86) bps Efficiency ratio 1 44% 46% 43% (232) bps 40 bps |

3Q15 change from

$s in millions 3Q15 2Q15 3Q14 2Q15 3Q14 $ % $ % Net interest income 1 $ 10 $ 18 $ (9) $ (90) % (17) $ (94) % Noninterest income 18 22 11 (4) (18) 7 64 Total revenue 19 32 29 (13) (41) (10) (34) Noninterest expense — 47 39 (47) (100) (39) (100) Pre-provision profit (loss) 19 (15) (10) 34 227 29 290 Provision for credit losses 9 10 11 (1) (10) (2) (18) Income (loss) before income tax expense (benefit) 10 (25) (21) 35 140 31 148 Income tax expense (benefit) 3 (14) (17) 17 121 20 118 Net income (loss) 7 $ (11) $ (4) $ 18 $ 164 % 11 $ 275 % Average balances $s in billions Total loans and leases 3.4 $ 3.6 $ 4.2 $ (0.2) $ (6) % (0.9) $ (20) % Total deposits 5.9 $ 5.9 $ 5.1 $ — $ — % 0.8 $ 15 % Other 24 1) Includes held for sale. Linked quarter: Other recorded net income up $18 million, as lower total revenue was more than offset by a $40 million decrease in restructuring charges and special items Net interest income decreased $9 million, driven by lower non-core balances Noninterest income decreased $4 million, reflecting lower securities gains Noninterest expense down $47 million, driven by a decrease in restructuring charges and special items Provision for credit losses decreased $1 million — Reflects a $1 million reserve build versus a $1 million release in the prior quarter Prior year quarter: Net income up $11 million, as lower total revenue was more than offset by lower expenses and restructuring charges and special items Net interest income decreased $17 million, as lower swap costs were offset by an increase in wholesale funding costs and lower non-core loans Noninterest income up $7 million, reflecting the effect of and accounting change related to the low-income housing portfolio, offset by income tax expense Noninterest expense down $39 million given lower restructuring charges and special items, and lower incentives Provision for credit losses decreased $2 million — Reflects a $12 million decrease in non-core charge-offs Highlights |

Restructuring charges and special items

25 GAAP results included restructuring charges and special items related to enhancing efficiencies and improving processes across the organization and separation from the Royal Bank of Scotland Group plc (“RBS”). 1) These are non-GAAP financial measures. Please see Non-GAAP Reconciliation Tables in the Appendix for an explanation of our use of

non-GAAP financial measures and their reconciliation to GAAP.

as of and for the three months ended

Restructuring charges and special items

1 ($s in millions, except per share data) pre-tax after-tax pre-tax after-tax pre-tax after-tax Noninterest expense restructuring charges and special items: Salaries and employee benefits — — 6 4 (6) (4) Outside services — — 16 10 (16) (10) Occupancy — — 15 9 (15) (9) Equipment expense — — — — — — Other operating expense — — 3 2 (3) (2) Total noninterest expense restructuring charges and special items — $ — $ 40 $ 25 $ (40) $ (25) $ Net restructuring charges and special items — $ — $ (40) $ (25) $ 40 $ 25 $ Diluted EPS impact — $ (0.05) $ 0.05 $ September 30, 2015 June 30, 2015 increase/decrease |

Loan Reconciliation

26 Average balances $s in millions 1) Primarily Treasury Solutions (Credit cards). 2) Primarily Business Banking. 3Q15 change from 3Q15 2Q15 3Q14 Consumer Banking Segment 47,848 $ 49,351 $ 50,260 $ 51,024 $ 51,886 $ 862 $ 2 % 4,038 $ 8 % Add: Non-core loans 2,932 2,801 2,667 2,517 2,358 (159) (6) (574) (20) Retail loans in Commercial Banking (1) 134 145 143 161 160 (1) (1) 26 19 Other 737 681 629 586 540 (46) (8) (197) (27) Less: Commercial loans in Consumer Banking (2) 3,022 3,017 3,056 3,096 3,045 (51) (2) 23 1 LHFS 170 179 197 282 282 — — 112 66 Total Retail loans 48,459 $ 49,782 $ 50,446 $ 50,910 $ 51,617 $ 707 $ 1 3,158 $ 7 % Commercial Banking Segment 37,787 $ 38,926 $ 40,241 $ 41,467 $ 41,993 $ 526 $ 1 % 4,206 $ 11 % Add: Commercial loans in Consumer Banking (2) 3,022 3,017 3,056 3,096 3,045 (51) (2) 23 1 Non-core loans 353 309 266 230 202 (28) (12) (151) (43) CRA 171 182 198 212 241 29 14 70 41 Other 25 28 24 23 27 4 17 2 8 Less: Retail loans in Commercial Banking (1) 134 145 143 161 160 (1) (1) 26 19 LHFS 33 54 136 171 174 3 2 141 427 Total Commercial loans 41,191 $ 42,263 $ 43,506 $ 44,696 $ 45,174 $ 478 $ 1 3,983 $ 10 % 3Q14 4Q14 1Q15 2Q15 |

$3.2B $3.0B $2.9B $2.7B $2.5B 3Q14 4Q14 1Q15 2Q15 3Q15 Retail Commercial SBO Non-core home equity portfolio serviced by others (SBO) 1 SBO balances by FICO 2 SBO balances by LTV Top 5 SBO balances by state 1 Non-core period-end loans SBO balances by product SBO Lien Position 1st Lien 2nd Lien < 70 80-89 70-79 90-99 100-119 120+ < 620 620-679 680-719 720-759 760+ HE Loan HELOC 27 $s in millions 1 A portion of the serviced by others portfolio is serviced by CFG. 2 FICO scores updated quarterly. |

Non-GAAP Financial Measures

28 This document contains non-GAAP financial measures. The table below presents reconciliations of certain non-GAAP measures. These reconciliations exclude restructuring charges and/or special items, which are usually included, where applicable, in the financial results presented in accordance with GAAP. Restructuring charges and special items include expenses related to our efforts to improve processes and enhance efficiencies, as well as rebranding, separation from RBS and regulatory expenses. The non-GAAP measures set forth below include “total revenue”, “noninterest income”, “ noninterest expense”, “pre-provision profit”, “income before income tax expense (benefit)”, “income tax expense (benefit)”, “net income”, “net income available to common stockholders”, “salaries and employee benefits”, “outside services”, “occupancy”, “equipment expense”, “amortization of software”, “other operating expense”, “net income per average common share”, “return of average common equity” and “return on average total assets”. In addition, we present computations for "tangible book value per common share", “return on average tangible common equity”, “return on average total tangible assets” and “efficiency ratio” as part of our non-GAAP measures. Additionally, "pro forma Basel III fully phased-in common equity tier 1 capital" computations for periods prior to first quarter 2015 are presented as part of our non-GAAP measures. We believe these non-GAAP measures provide useful information to investors because these are among the measures used by our management team to evaluate our operating performance and make day-to-day operating decisions. In addition, we believe restructuring charges and special items in any period do not reflect the operational performance of the business in that period and, accordingly, it is useful to consider these line items with and without restructuring charges and special items. We believe this presentation also increases comparability of period-to-period results. We also consider pro forma capital ratios defined by banking regulators but not effective at each period end to be non-GAAP financial measures. Since analysts and banking regulators may assess our capital adequacy using these pro forma ratios, we believe they are useful to provide investors the ability to assess our capital adequacy on the same basis. Other companies may use similarly titled non-GAAP financial measures that are calculated differently from the way we calculate such measures. Accordingly, our non-GAAP financial measures may not be comparable to similar measures used by other companies. We caution investors not to place undue reliance on such non-GAAP measures, but instead to consider them with the most directly comparable GAAP measure. Non-GAAP financial measures have limitations as analytical tools, and should not be considered in isolation, or as a substitute for our results as reported under GAAP. |

Non-GAAP Reconciliation Table

29 (Excluding restructuring charges and special items) $s in millions, except per share data 3Q15 2Q15 1Q15 4Q14 3Q14 2015 2014 Noninterest income, excluding special items: Noninterest income (GAAP) A $353 $360 $347 $339 $341 $1,060 $1,339 Less: Special items - Chicago gain — — — — — — 288 Noninterest income, excluding special items (non-GAAP) B $353 $360 $347 $339 $341 $1,060 $1,051 Total revenue, excluding special items: Total revenue (GAAP) C $1,209 $1,200 $1,183 $1,179 $1,161 $3,592 $3,800 Less: Special items - Chicago gain — — — — — — 288 Total revenue, excluding special items (non-GAAP) D $1,209 $1,200 $1,183 $1,179 $1,161 $3,592 $3,512 Noninterest expense, excluding restructuring charges and special items: Noninterest expense (GAAP) E $798 $841 $810 $824 $810 $2,449 $2,568 Less: Restructuring charges and special items MM — 40 10 33 21 50 136 Noninterest expense, excluding restructuring charges and special items (non-GAAP)

F $798 $801 $800 $791 $789 $2,399 $2,432 Net income, excluding restructuring charges and special items: Net income (GAAP) G $220 $190 $209 $197 $189 $619 $668 Add: Restructuring charges and special items, net of income tax expense (benefit)

— 25 6 20 13 31 (95) Net income, excluding restructuring charges and special items (non-GAAP)

H $220 $215 $215 $217 $202 $650 $573 Net income available to common stockholders (GAAP), excluding restructuring charges and special

items Net income available to common stockholders (GAAP) I $213 $190 $209 $197 $189 $612 $668 Add: Restructuring charges and special items, net of income tax expense (benefit)

— 25 6 20 13 31 (95) Net income available to common stockholders, excluding restructuring charges and special items

(non-GAAP) J $213 $215 $215 $217 $202 $643 $573 Return on average common equity, excluding restructuring charges and special items:

Average common equity (GAAP)

K $19,261 $19,391 $19,407 $19,209 $19,411 $19,352 $19,463 Return on average common equity, excluding restructuring charges and special items (non-GAAP)

J/K 4.40% 4.45 % 4.49 % 4.48 % 4.14 % 4.45 % 3.94 % Return on average tangible common equity and return on average tangible common equity,

excluding restructuring charges and special items:

Average common equity (GAAP)

L $19,261 $19,391 $19,407 $19,209 $19,411 $19,352 $19,463 Less: Average goodwill (GAAP) 6,876 6,876 6,876 6,876 6,876 6,876 6,876 Less: Average other intangibles (GAAP) 4 5 5 6 6 5 7 Add: Average deferred tax liabilities related to goodwill (GAAP) 453 437 422 403 384 438 368 Average tangible common equity (non-GAAP) M $12,834 $12,947 $12,948 $12,730 $12,913 $12,909 $12,948 Return on average tangible common equity (non-GAAP) I/M 6.60 % 5.90 % 6.53 % 6.12 % 5.81 % 6.34 % 6.90 % Return on average tangible common equity, excluding restructuring charges and special items

(non-GAAP) J/M 6.60 % 6.67 % 6.73 % 6.76 % 6.22 % 6.67 % 5.92 % Return on average total assets, excluding restructuring charges and special items:

Average total assets (GAAP)

N $135,103 $135,521 $133,325 $130,671 $128,691 $134,655 $126,598 Return on average total assets, excluding restructuring charges and special items (non-GAAP)

H/N 0.65 % 0.64 % 0.65 % 0.66 % 0.62 % 0.65 % 0.61 % Return on average total tangible assets and return on average total tangible assets, excluding

restructuring charges and special items:

Average total assets (GAAP)

N $135,103 $135,521 $133,325 $130,671 $128,691 $134,655 $126,598 Less: Average goodwill (GAAP) 6,876 6,876 6,876 6,876 6,876 6,876 6,876 Less: Average other intangibles (GAAP) 4 5 5 6 6 5 7 Add: Average deferred tax liabilities related to goodwill (GAAP) 453 437 422 403 384 438 368 Average tangible assets (non-GAAP) O $128,676 $129,077 $126,866 $124,192 $122,193 $128,212 $120,083 Return on average total tangible assets (non-GAAP) G/O 0.68 % 0.59 % 0.67 % 0.63 % 0.61 % 0.65 % 0.74 % Return on average total tangible assets, excluding restructuring charges and special items (non-

GAAP) H/O 0.68 % 0.67 % 0.69 % 0.69 % 0.66 % 0.68 % 0.64 % FOR THE NINE MONTHS ENDED SEPTEMBER 30 QUARTERLY TRENDS |

Non-GAAP Reconciliation Table

30 (Excluding restructuring charges and special items) $s in millions, except per share data 3Q15 2Q15 1Q15 4Q14 3Q14 2015 2014 Efficiency ratio and efficiency ratio, excluding restructuring charges and special items:

Net interest income (GAAP)

$856 $840 $836 $840 $820 $2,532 $2,461 Add: Noninterest income (GAAP) 353 360 347 339 341 1,060 1,339 Total revenue (GAAP) C $1,209 $1,200 $1,183 $1,179 $1,161 $3,592 $3,800 Efficiency ratio (non-GAAP) E/C 66.02 % 70.02 % 68.49 % 69.88 % 69.84 % 68.17 % 67.58 % Efficiency ratio, excluding restructuring charges and special items (non-GAAP)

F/D 66.02 % 66.70% 67.65 % 67.11 % 68.02 % 66.78 % 69.23 % Tangible book value per common share: Common shares - at end of period (GAAP) P 527,636,510 537,149,717 547,490,812 545,884,519 559,998,324 527,636,510 559,998,324 Stockholders' equity (GAAP) $19,353 $19,339 $19,564 $19,268 $19,383 $19,353 $19,383 Less: Goodwill (GAAP) 6,876 6,876 6,876 6,876 6,876 6,876 6,876 Less: Other intangible assets (GAAP) 3 4 5 6 6 3 6 Add: Deferred tax liabilities related to goodwill (GAAP) 465 450 434 420 399 465 399 Tangible common equity (non-GAAP) Q $12,939 $12,909 $13,117 $12,806 $12,900 $12,939 $12,900 Tangible book value per common share (non-GAAP) Q/P $24.52 $24.03 $23.96 $23.46 $23.04 $24.52 $23.04 Net income per average common share - basic and diluted, excluding restructuring charges and

special items: Average common shares outstanding - basic (GAAP) R 530,985,255 537,729,248 546,291,363 546,810,009 559,998,324 538,279,222 559,998,324 Average common shares outstanding - diluted (GAAP) S 533,398,158 539,909,366 549,798,717 550,676,298 560,243,747 540,926,361 560,081,031 Net income available to common stockholders (GAAP) I $213 $190 $209 $197 $189 $612 $668 Net income per average common share - basic (GAAP) I/R 0.40 0.35 0.38 0.36 0.34 1.14 1.19 Net income per average common share - diluted (GAAP) I/S 0.40 0.35 0.38 0.36 0.34 1.13 1.19 Net income available to common stockholders, excluding restructuring charges and special items

(non-GAAP) J 213 215 215 217 202 643 573 Net income per average common share - basic, excluding restructuring charges and special items

(non-GAAP) J/R 0.40 0.40 0.39 0.40 0.36 1.20 1.02 Net income per average common share - diluted, excluding restructuring charges and special

items (non-GAAP)

J/S 0.40 0.40 0.39 0.39 0.36 1.19 1.02 Pro forma Basel III fully phased-in common equity tier 1 capital ratio¹:

Common equity tier 1 (regulatory)

$13,200 $13,270 $13,360 $13,173 $13,330 Less: Change in DTA and other threshold deductions (GAAP) 2 3 3 (6) (5) Pro forma Basel III fully phased-in common equity tier 1 (non-GAAP)

T $13,198 $13,267 $13,357 $13,179 $13,335 Risk-weighted assets (regulatory general risk weight approach) $112,277 $112,131 $109,786 $105,964 $103,207 Add: Net change in credit and other risk-weighted assets (regulatory)

243 247 242 2,882 3,207 Basel III standardized approach risk-weighted assets (non-GAAP) U $112,520 $112,378 $110,028 $108,846 $106,414 Pro forma Basel III fully phased-in common equity tier 1 capital ratio

(non-GAAP)¹

T/U 11.7% 11.8% 12.1% 12.1% 12.5% Salaries and employee benefits, excluding restructuring charges and special items:

Salaries and employee benefits (GAAP)

V $404 $411 $419 $397 $409 $1,234 $1,281 Less: Restructuring charges and special items — 6 (1) 1 — 5 43 Salaries and employee benefits, excluding restructuring charges and special items (non-GAAP)

W $404 $405 $420 $396 $409 $1,229 $1,238 FOR THE NINE MONTHS ENDED SEPTEMBER 30 QUARTERLY TRENDS 1 Periods prior to 1Q15 reported on a Basel I basis. Basel III ratios assume certain definitions impacting qualifying Basel III

capital, which otherwise will phase in through 2018, are fully phased-in. Ratios also reflect the required US Standardized methodology for calculating RWAs, effective January 1, 2015. |

Non-GAAP Reconciliation Table

31 (Excluding restructuring charges and special items) $s in millions, except per share data 3Q15 2Q15 1Q15 4Q14 3Q14 2015 2014 Outside services, excluding restructuring charges and special items: Outside services (GAAP) X $89 $99 $79 $106 $106 $267 $314 Less: Restructuring charges and special items — 16 8 18 19 24 60 Outside services, excluding restructuring charges and special items (non-GAAP)

Y $89 $83 $71 $88 $87 $243 $254 Occupancy, excluding restructuring charges and special items: Occupancy (GAAP) X $75 $90 $80 $81 $77 $245 $245 Less: Restructuring charges and special items — 15 2 5 2 17 11 Occupancy, excluding restructuring charges and special items (non-GAAP)

AA $75 $75 $78 $76 $75 $228 $234 Equipment expense, excluding restructuring charges and special items: Equipment expense (GAAP) BB $62 $65 $63 $63 $58 $190 $187 Less: Restructuring charges and special items — — 1 1 — 1 3 Equipment expense, excluding restructuring charges and special items (non-GAAP)

CC $62 $65 $62 $62 $58 $189 $184 Amortization of software, excluding restructuring charges and special items:

Amortization of software

DD $35 $37 $36 $43 $38 $108 $102 Less: Restructuring charges and special items — — — 6 — — — Amortization of software, excluding restructuring charges and special items (non-GAAP)

EE $35 $37 $36 $37 $38 $108 $102 Other operating expense, excluding restructuring charges and special items:

Other operating expense (GAAP)

FF $133 $139 $133 $134 $122 $405 $439 Less: Restructuring charges and special items — 3 — 2 — 3 19 Other operating expense, excluding restructuring charges and special items (non-GAAP)

GG $133 $136 $133 $132 $122 $402 $420 Pre-provision profit, excluding restructuring charges and special items:

Total revenue, excluding restructuring charges and special items

(non-GAAP) D

$1,209 $1,200 $1,183 $1,179 $1,161 $3,592 $3,512 Less: Noninterest expense, excluding restructuring charges and special items (non-GAAP)

F 798 801 800 791 789 2,399 2,432 Pre-provision profit, excluding restructuring charges and special items (non-GAAP)

HH $411 $399 $383 $388 $372 $1,193 $1,080 Income before income tax expense (benefit), excluding restructuring charges and special items:

Income before income tax expense (GAAP)

II $335 $282 $315 $283 $274 $932 $985 Less: Income before income tax expense (benefit) related to restructuring charges and special

items (GAAP) — (40) (10) (33) (21) (50) 152 Income before income tax expense, excluding restructuring charges and special items (non-GAAP)

JJ $335 $322 $325 $316 $295 $982 $833 Income tax expense, excluding restructuring charges and special items: Income tax expense (GAAP) KK $115 $92 $106 $86 $85 $313 $317 Less: Income tax (benefit) related to restructuring charges and special items (GAAP)

— (15) (4) (13) (8) (19) 57 Income tax expense, excluding restructuring charges and special items (non-GAAP)

LL $115 $107 $110 $99 $93 $332 $260 Restructuring charges and special expense items include: Restructuring charges $0 $25 $1 $10 $1 $26 $104 Special items 0 15 9 23 20 24 32 Restructuring charges and special expense items MM $0 $40 $10 $33 $21 $50 $136 3Q15 2Q15 1Q15 4Q14 3Q14 % Change % Change Operating leverage, excluding restructuring charges and special items: Total revenue, excluding restructuring charges and special items (non-GAAP)

D $1,209 $1,200 $1,161 0.8% 4.1% Less: Noninterest expense, excluding restructuring charges and special items (non-GAAP)

F $798 $801 $789 (0.4)% 1.1% Operating leverage, excluding restructuring charges and special items: (non-GAAP)

NN 1.1% 3.0% QUARTERLY TRENDS 3Q15 v 2Q15 FOR THE NINE MONTHS ENDED SEPTEMBER 30 QUARTERLY TRENDS 3Q15 v 3Q14 |

Non-GAAP Reconciliation Table

32 Non-GAAP Reconciliation - Segments $s in millions Consumer Banking Commercial Banking Other Consolidated Consumer Banking Commercial Banking Other Consolidated Consumer Banking Commercial Banking Other Consolidated Net income (loss) (GAAP) A 68 145 7 220 66 135 (11) 190 61 147 1 209 Less: Preferred stock dividends — — 7 7 — — — — — — — — Net income available to common stockholders B $68 $145 $— $213 $66 $135 ($11) $190 $61 $147 $1 $209 Return on average tangible common equity Average common equity (GAAP) C $4,791 $4,722 $9,748 $19,261 $4,681 $4,625 $10,085 $19,391 $4,649 $4,526 $10,232 $19,407 Less: Average goodwill (GAAP) — — 6,876 6,876 — — 6,876 6,876 — — 6,876 6,876 Average other intangibles (GAAP) — — 4 4 — — 5 5 — — 5 5 Add: Average deferred tax liabilities related to goodwill (GAAP) — — 453 453 — — 437 437 — — 422 422 Average tangible common equity (non-GAAP) D $4,791 $4,722 $3,321 $12,834 $4,681 $4,625 $3,641 $12,947 $4,649 $4,526 $3,773 $12,948 Return on average tangible common equity (non-GAAP) B/D 5.67 % 12.24% NM 6.60 % 5.66 % 11.69% NM 5.90 % 5.30 % 13.15% NM 6.53 % Return on average total tangible assets Average total assets (GAAP) E $53,206 $43,113 $38,784 $135,103 $52,489 $42,617 $40,415 $135,521 $51,602 $41,606 $40,117 $133,325 Less: Average goodwill (GAAP) — — 6,876 6,876 — — 6,876 6,876 — — 6,876 6,876 Average other intangibles (GAAP) — — 4 4 — — 5 5 — — 5 5 Add: Average deferred tax liabilities related to goodwill (GAAP) — — 453 453 — — 437 437 — — 422 422 Average tangible assets (non-GAAP) F $53,206 $43,113 $32,357 $128,676 $52,489 $42,617 $33,971 $129,077 $51,602 $41,606 $33,658 $126,866 Return on average total tangible assets (non-GAAP) A/F 0.51% 1.34% NM 0.68 % 0.51% 1.27% NM 0.59 % 0.48 % 1.43% NM 0.67 % Efficiency ratio Noninterest expense (GAAP) G $623 $175 $— $798 $613 $181 $47 $841 $596 $173 $41 $810 Net interest income (GAAP) 556 299 1 856 544 286 10 840 533 276 27 836 Noninterest income (GAAP) 235 100 18 353 230 108 22 360 219 100 28 347 Total revenue H $791 $399 $19 $1,209 $774 $394 $32 $1,200 $752 $376 $55 $1,183 Efficiency ratio (non-GAAP) G/H 78.72 % 43.75 % NM 66.02 % 79.25 % 46.07 % NM 70.02 % 79.25 % 46.01% NM 68.49 % Consumer Banking Commercial Banking Other Consolidated Consumer Banking Commercial Banking Other Consolidated Net income (loss) (GAAP) A $52 $140 $5 $197 $54 $139 ($4) $189 Less: Preferred stock dividends — — — — — — — — Net income available to common stockholders B $52 $140 $5 $197 $54 $139 ($4) $189 Return on average tangible common equity Average common equity (GAAP) C $4,756 $4,334 $10,119 $19,209 $4,685 $4,205 $10,521 $19,411 Less: Average goodwill (GAAP) — — 6,876 6,876 — — 6,876 6,876 Average other intangibles (GAAP) — — 6 6 — — 6 6 Add: Average deferred tax liabilities related to goodwill (GAAP) — — 403 403 — — 384 384 Average tangible common equity (non-GAAP) D $4,756 $4,334 $3,640 $12,730 $4,685 $4,205 $4,023 $12,913 Return on average tangible common equity (non-GAAP) B/D 4.30 % 12.76% NM 6.12% 4.57 % 13.10% NM 5.81% Return on average total tangible assets Average total assets (GAAP) E $50,546 $40,061 $40,064 $130,671 $49,012 $38,854 $40,825 $128,691 Less: Average goodwill (GAAP) — — 6,876 6,876 — — 6,876 6,876 Average other intangibles (GAAP) — — 6 6 — — 6 6 Add: Average deferred tax liabilities related to goodwill (GAAP) — — 403 403 — — 384 384 Average tangible assets (non-GAAP) F $50,546 $40,061 $33,585 $124,192 $49,012 $38,854 $34,327 $122,193 Return on average total tangible assets (non-GAAP) A/F 0.40 % 1.38% NM 0.63 % 0.44 % 1.42% NM 0.61% Efficiency ratio Noninterest expense (GAAP) G $611 $180 $33 $824 $609 $162 $39 $810 Net interest income (GAAP) 536 283 21 840 532 270 18 820 Noninterest income (GAAP) 218 111 10 339 226 104 11 341 Total revenue H $754 $394 $31 $1,179 $758 $374 $29 $1,161 Efficiency ratio (non-GAAP) G/H 81.09% 45.48 % NM 69.88 % 80.42 % 43.35 % NM 69.84 % THREE MONTHS ENDED MAR 31, 2015 2015 2015 2014 2014 THREE MONTHS ENDED SEPT 30, THREE MONTHS ENDED JUNE 30, THREE MONTHS ENDED DEC 31, THREE MONTHS ENDED SEPT 30, |

Non-GAAP Reconciliation Table

33 Non-GAAP Reconciliation - Segments $s in millions Consumer Banking Commercial Banking Other Consolidated Consumer Banking Commercial Banking Other Consolidated Net income (loss) (GAAP) A $195 $427 ($3) $619 $130 $421 $117 $668 Less: Preferred stock dividends — — 7 7 — — — — Net income available to common stockholders B $195 $427 ($10) $612 $130 $421 $117 $668 Return on average tangible common equity Average common equity (GAAP) C $4,708 $4,625 $10,019 $19,352 $4,635 $4,120 $10,708 $19,463 Less: Average goodwill (GAAP) — — 6,876 6,876 — — 6,876 6,876 Average other intangibles (GAAP) — — 5 5 — — 7 7 Add: Average deferred tax liabilities related to goodwill (GAAP) — — 438 438 — — 368 368 Average tangible common equity (non-GAAP) D $4,708 $4,625 $3,576 $12,909 $4,635 $4,120 $4,193 $12,948 Return on average tangible common equity (non-GAAP) B/D 5.55% 12.35% NM 6.34 % 3.76 % 13.67 % NM 6.90 % Return on average total tangible assets Average total assets (GAAP) E $52,438 $42,451 $39,766 $134,655 $48,398 $37,951 $40,249 $126,598 Less: Average goodwill (GAAP) — — 6,876 6,876 — — 6,876 6,876 Average other intangibles (GAAP) — — 5 5 — — 7 7 Add: Average deferred tax liabilities related to goodwill (GAAP) — — 438 438 — — 368 368 Average tangible assets (non-GAAP) F $52,438 $42,451 $33,323 $128,212 $48,398 $37,951 $33,734 $120,083 Return on average total tangible assets (non-GAAP) A/F 0.50% 1.35 % NM 0.65 % 0.36 % 1.48 % NM 0.74 % Efficiency ratio Noninterest expense (GAAP) G $1,832 $529 $88 $2,449 $1,902 $472 $194 $2,568 Net interest income (GAAP) 1,633 861 38 2,532 1,615 790 56 2,461 Noninterest income (GAAP) 684 308 68 1,060 681 318 340 1,339 Total revenue H $2,317 $1,169 $106 $3,592 $2,296 $1,108 $396 $3,800 Efficiency ratio (non-GAAP) G/H 79.07% 45.26% NM 68.17 % 82.82% 42.62 % NM 67.58% FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2015 2014 |

34 * * * * * * * * * * ******************** |