Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - OLIN Corp | form8-k.htm |

Exhibit 99.1

Credit Suisse Basic Materials Conference September 16, 2015

Forward-Looking Statements This communication includes forward-looking statements. These statements relate to analyses and other information that are based on management’s beliefs, certain assumptions made by management, forecasts of future results, and current expectations, estimates and projections about the markets and economy in which Olin Corporation (“Olin”) and The Dow Chemical Company’s (“TDCC”) chlorine products business operate. These statements may include statements regarding the proposed combination of TDCC’s chlorine products business with Olin in a “Reverse Morris Trust” transaction, the expected timetable for completing the transaction, benefits and synergies of the transaction, future opportunities for the combined company and products and any other statements regarding Olin’s and TDCC’s chlorine products businesses’ future operations, anticipated business levels, future earnings, planned activities, anticipated growth, market opportunities, strategies and competition. The statements contained in this communication that are not statements of historical fact may include forward-looking statements that involve a number of risks and uncertainties. We have used the words “anticipate,” “intend,” “may,” “expect,” “believe,” “plan,” “estimate,” “will,” and variations of such words and similar expressions in this communication to identify such forward-looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions, which are difficult to predict and many of which are beyond our control. Therefore, actual outcomes and results may differ materially from those matters expressed or implied in such forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to: factors relating to the satisfaction of the conditions to the proposed transaction, including regulatory approvals; the parties’ ability to meet expectations regarding the timing, completion and accounting and tax treatments of the proposed transaction; the possibility that Olin may be unable to achieve expected synergies and operating efficiencies in connection with the transaction within the expected time-frames or at all; the integration of the TDCC’s chlorine products business being more difficult, time-consuming or costly than expected; the effect of any changes resulting from the proposed transaction in customer, supplier and other business relationships; general market perception of the proposed transaction; exposure to lawsuits and contingencies associated with TDCC’s chlorine products business; the ability to attract and retain key personnel; prevailing market conditions; changes in economic and financial conditions of Olin and TDCC’s chlorine products business; uncertainties and matters beyond the control of management; and the other risks detailed in Olin’s Form 10-K for the fiscal year ended December 31, 2014 and Olin’s Form 10-Q for the fiscal quarter ended June 30, 2015. These risks, as well as other risks associated with Olin, TDCC’s chlorine products business and the proposed transaction are also more fully discussed in the prospectus included in the registration statement on Form S-4 filed with the Securities and Exchange Commission (the “SEC”) by Olin, and declared effective by the SEC, on September 2, 2015. The forward-looking statements should be considered in light of these factors. In addition, other risks and uncertainties not presently known to Olin or that Olin considers immaterial could affect the accuracy of our forward-looking statements. The reader is cautioned not to rely unduly on these forward-looking statements. Olin and TDCC undertake no obligation to update publicly any forward-looking statements, whether as a result of future events, new information or otherwise.

SEC Disclosure Rules Important Notices and Additional Information In connection with the proposed combination of Olin with the chlorine products business of The Dow Chemical Company (“TDCC”), Blue Cube Spinco Inc. (“Splitco”) has filed with the Securities and Exchange Commission (the “SEC”), and the SEC declared effective on September 2, 2015, a registration statement on Form S-4 and Form S-1 containing a prospectus and Olin has filed with the SEC, and the SEC declared effective on September 2, 2015, a registration statement on Form S-4 containing a prospectus. INVESTORS AND SECURITYHOLDERS ARE ADVISED TO READ THE REGISTRATION STATEMENTS/PROSPECTUSES AS WELL AS ANY OTHER RELEVANT DOCUMENTS, BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT OLIN, TDCC, SPLITCO AND THE PROPOSED TRANSACTION. Investors and securityholders may obtain a free copy of the registration statements/prospectuses and other documents filed by Olin, TDCC and Splitco with the SEC at the SEC’s website at http://www.sec.gov. Free copies of these documents and each of the companies’ other filings with the SEC, may also be obtained from the respective companies by directing a request to Olin at Olin Corporation, ATTN: Investor Relations, 190 Carondelet Plaza, Suite 1530, Clayton, Missouri 63105 or TDCC or Splitco at The Dow Chemical Company, 2030 Dow Center, Midland, Michigan 48674, ATTN: Investor Relations, as applicable. This communication shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

The “New Olin” HighlightsTransformative transaction to acquire Dow’s Chlorine Products (“DCP”) nearing completion “New Olin” will have unmatched scale, vertical integration and product diversity Experienced management team on board to drive integration and achieve synergy targets ($200 MM/yr. - $300 MM/yr. EBITDA) Best in class cost position and participation strategy focused on asset utilization expected to drive more stable earnings and cash generation

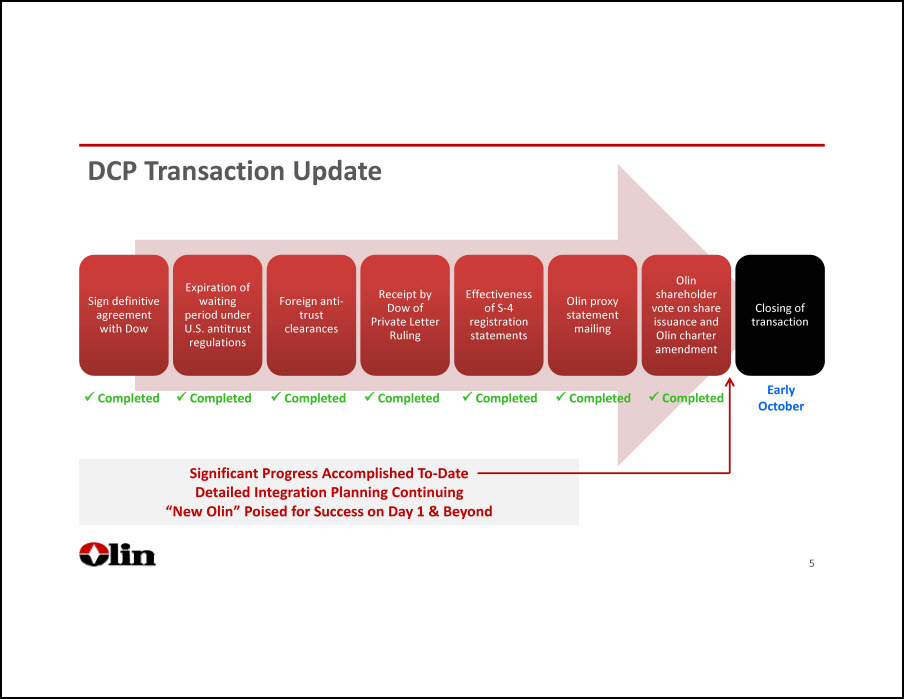

DCP Transaction Update Sign definitive agreement with Dow Expiration of waiting period under U.S. antitrust regulations Foreign anti-trust clearances Receipt by Dow of Private Letter Ruling Effectiveness of S-4 registration statements Olin proxy statement mailing Olin shareholder vote on share issuance and Olin charter amendment Closing of transaction Completed Completed Completed Completed Completed Completed Completed Significant Progress Accomplished To-Date Detailed Integration Planning Continuing “New Olin” Poised for Success on Day 1 & Beyond Early October

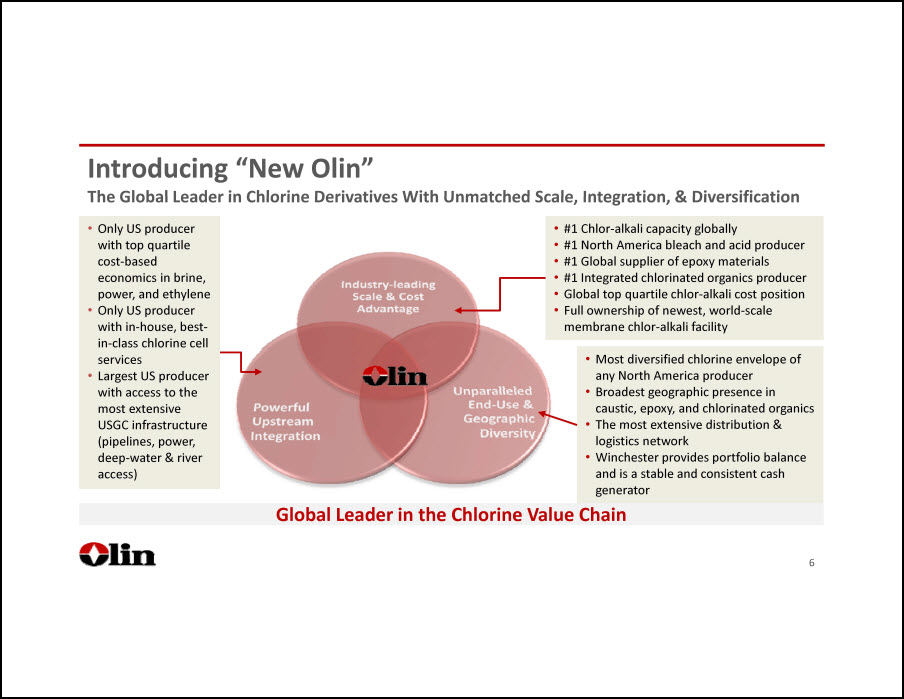

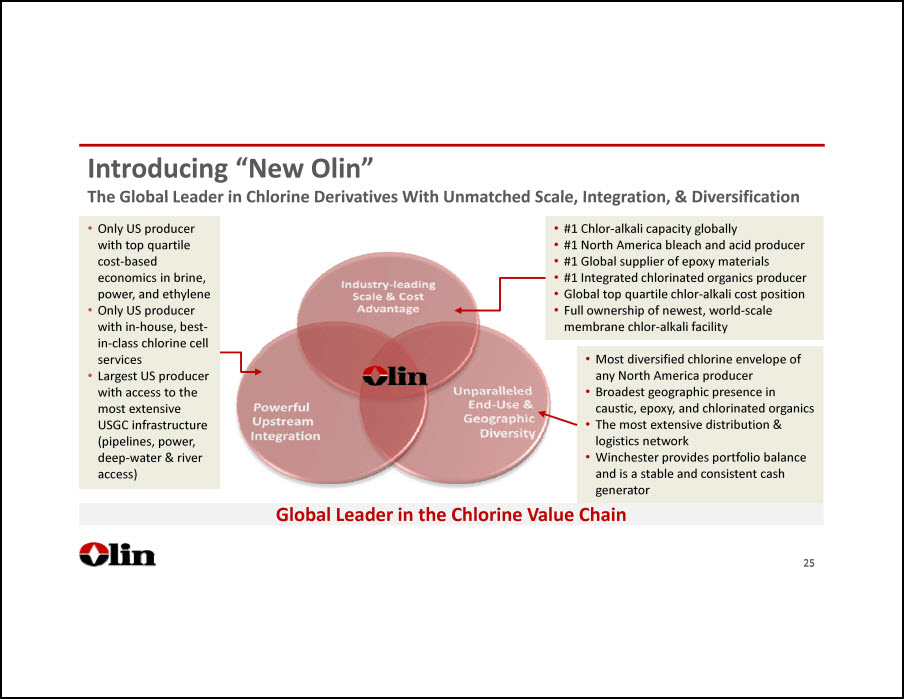

Introducing “New Olin” The Global Leader in Chlorine Derivatives With Unmatched Scale, Integration, & Diversification #1 Chlor-alkali capacity globally #1 North America bleach and acid producer #1 Global supplier of epoxy materials #1 Integrated chlorinated organics producer Global top quartile chlor-alkali cost position Full ownership of newest, world-scale membrane chlor-alkali facility Only US producer with top quartile cost-based economics in brine, power, and ethylene Only US producer with in-house, best-in-class chlorine cell services Largest US producer with access to the most extensive USGC infrastructure (pipelines, power, deep-water & river access) Most diversified chlorine envelope of any North America producer Broadest geographic presence in caustic, epoxy, and chlorinated organics The most extensive distribution & logistics network Winchester provides portfolio balance and is a stable and consistent cash generator Global Leader in the Chlorine Value Chain Industry-leading Scale & Cost Advantage Powerful Upstream Integration Unparalleled End-Use & Geographic Diversity

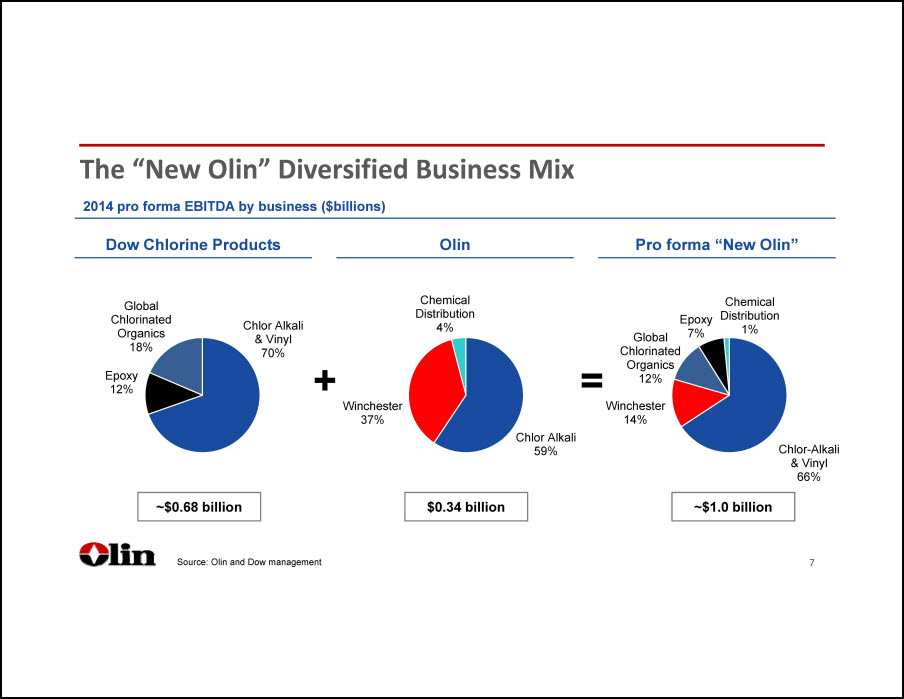

The “New Olin” Diversified Business Mix 2014 pro forma EBITDA by business ($billions) Dow Chlorine Products Epoxy 12% Global Chlorinated Organics 18% Chlor Alkali & Vinyl 70% + Olin Chemical Distribution 4% Winchester 37% Chlor Alkali 59% = Pro forma "New Olin" Winchester 14% Global Chlorinated Organics 12% Epoxy 7% Chemical Distribution 1% Chlor-Alkali & Vinyl 66% ~$0.68 billion $0.34 billion ~$1.0 billion Source: Olin and Dow management

"New Olin" Management Team Additions Olin management team complemented by key DCP personnel Pat Dawson President Epoxy Over 30 years of Dow experience Clive Grannum President Chlorinated Organics 25 years of chemical industry experience combined with Rohm & Haas and Dow John Sampson Vice President Manufacturing & Engineering Over 30 years of Dow experience Jim Varilek President Chlor Alkali Vinyl Over 30 years of Dow experience Key direct reports in Chlor Alkali Vinyl, Chlorinated Organics and Epoxy have also agreed to join Olin Provides “New Olin” with increased management depth and industry expertise

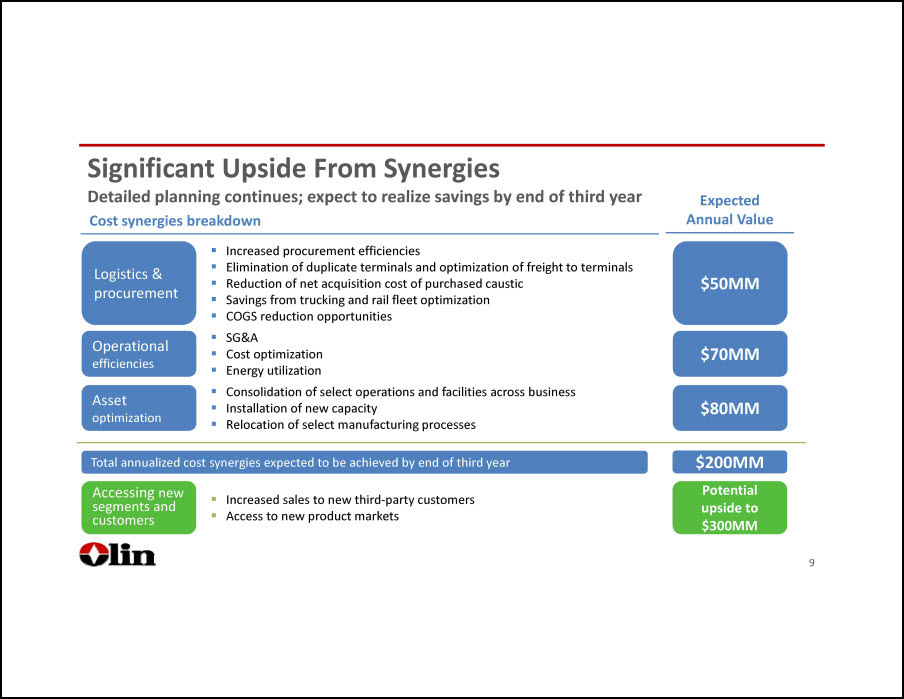

Significant Upside From Synergies Detailed planning continues; expect to realize savings by end of third year Cost synergies breakdown Expected Annual Value Logistics & procurement Increased procurement efficiencies Elimination of duplicate terminals and optimization of freight to terminals Reduction of net acquisition cost of purchased caustic Savings from trucking and rail fleet optimization COGS reduction opportunities $50MM Operational efficiencies SG&A Cost optimization Energy utilization $70MM Asset optimization Consolidation of select operations and facilities across business Installation of new capacity Relocation of select manufacturing processes $80MM Total annualized cost synergies expected to be achieved by end of third year $200MM Accessing new segments and customers Increased sales to new third-party customers Access to new product markets Potential upside to $300MM

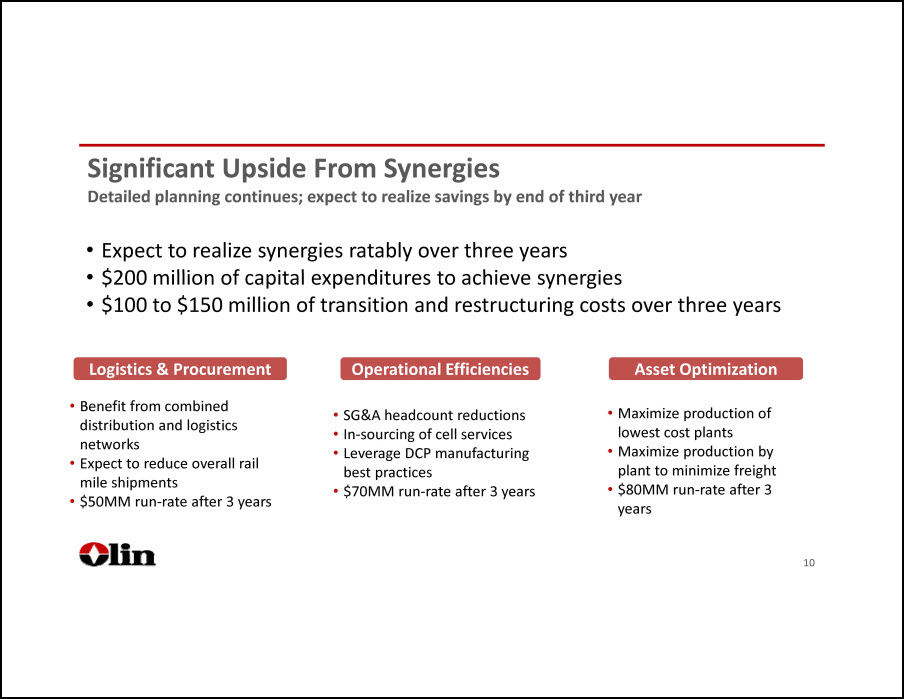

Significant Upside From Synergies Detailed planning continues; expect to realize savings by end of third year Logistics & Procurement Benefit from combined distribution and logistics networks Expect to reduce overall rail mile shipments $50MM run-rate after 3 years Operational Efficiencies SG&A headcount reductions In-sourcing of cell services Leverage DCP manufacturing best practices $70MM run-rate after 3 years Asset Optimization Maximize production of lowest cost plants Maximize production by plant to minimize freight $80MM run-rate after 3 years Expect to realize synergies ratably over three years $200 million of capital expenditures to achieve synergies $100 to $150 million of transition and restructuring costs over three years

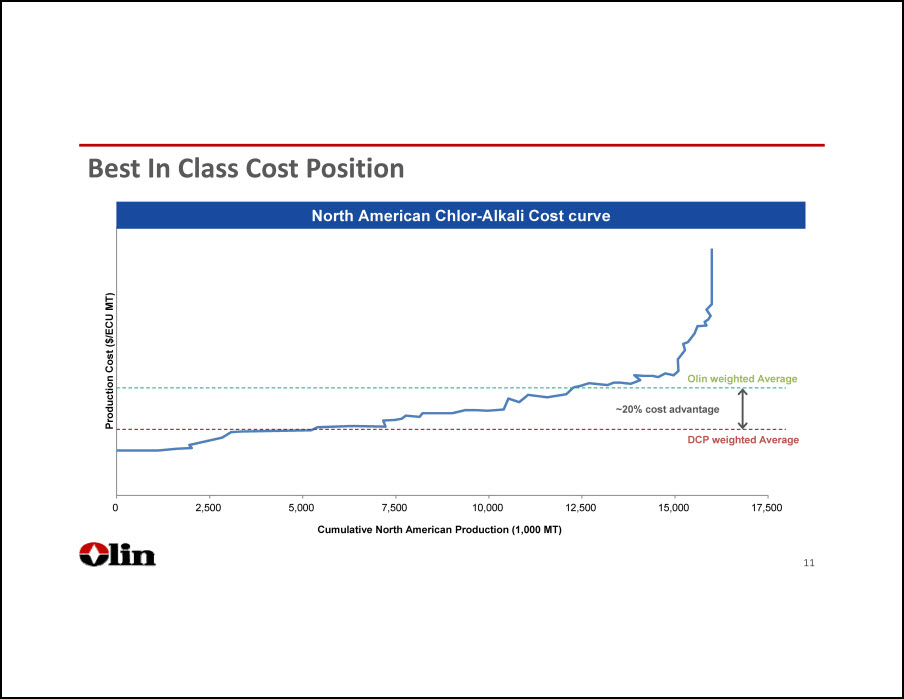

Best In Class Cost Position DCP weighted Average Olin weighted Average ~20% cost advantage North American Chlor-Alkali Cost curve Cumulative North America Production (1,000 MT) Production Cost ($/ECU MT)

Success Factors Go Beyond Assets, Feedstocks, and Markets Olin experience and customer intimacy + DCP scale, manufacturing excellence and derivatives experience = Winning combination Olin and DCP share compatible corporate cultures “New Olin” will retain a strong customer and partner in Dow via two-way product and service contracts

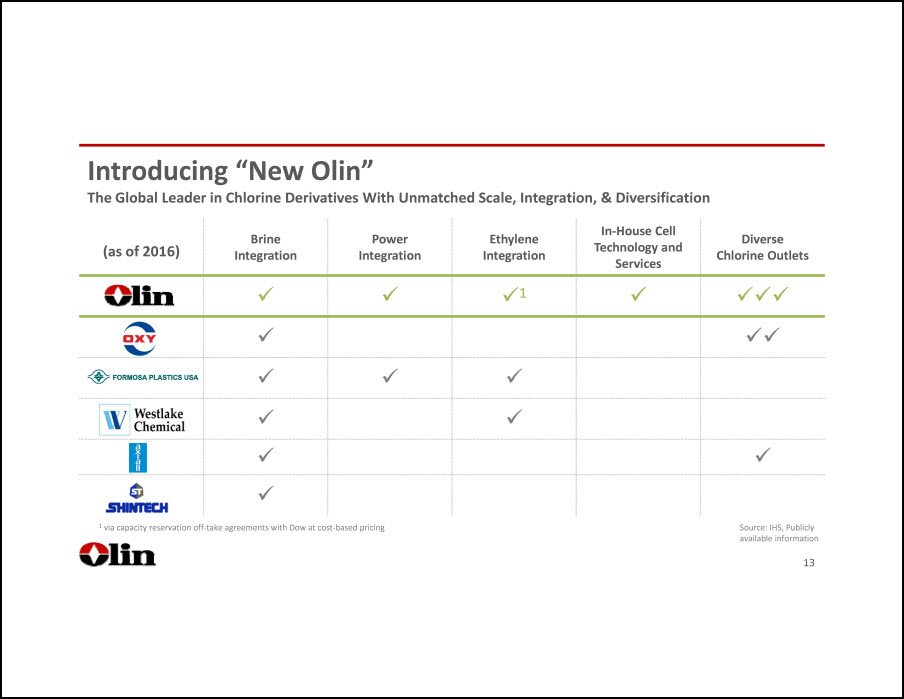

Introducing “New Olin” The Global Leader in Chlorine Derivatives With Unmatched Scale, Integration, & Diversification (as of 2016) Brine Integration Power Integration Ethylene Integration In-House Cell Technology and Services Diverse Chlorine Outlets 1 via capacity reservation off-take agreements with Dow at cost-based pricing Source: IHS, Publicly available information

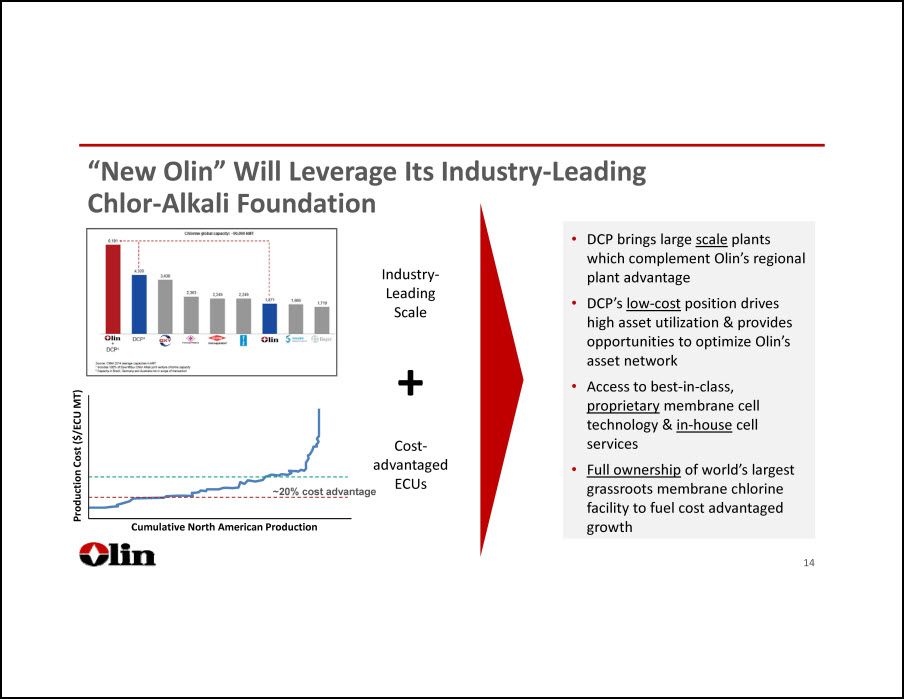

“New Olin” Will Leverage Its Industry-Leading Chlor-Alkali Foundation Industry-Leading Scale + Cost-advantaged ECUs DCP brings large scale plants which complement Olin’s regional plant advantage DCP’s low-cost position drives high asset utilization & provides opportunities to optimize Olin’s asset network Access to best-in-class, proprietary membrane cell technology & in-house cell services Full ownership of world’s largest grassroots membrane chlorine facility to fuel cost advantaged growth Cumulative North American Production ~20% cost advantage Production Cost ($/ECU MT)

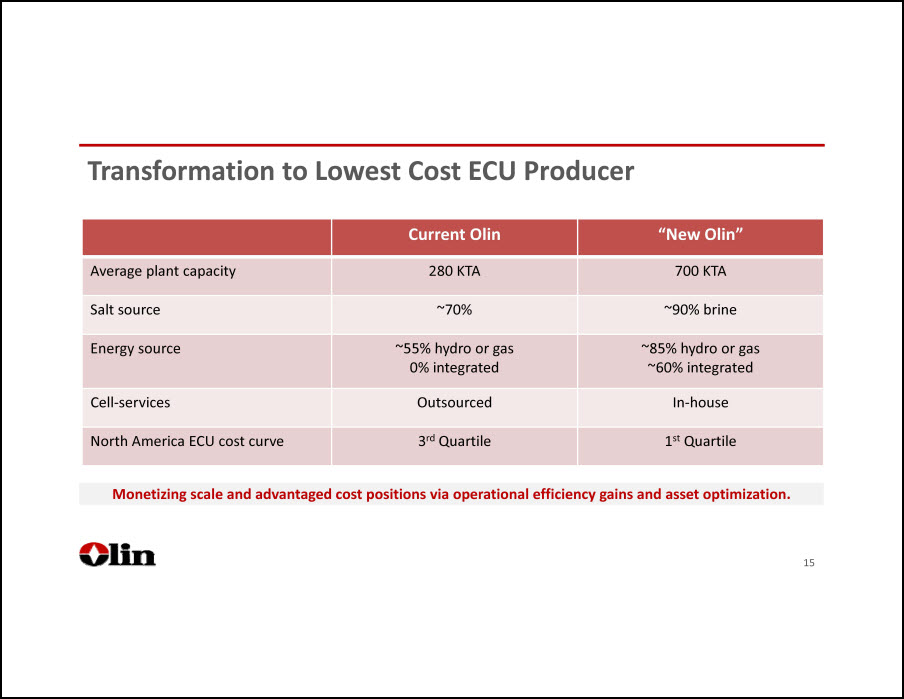

Transformation to Lowest Cost ECU Producer Current Olin “New Olin” Average plant capacity 280 KTA 700 KTA Salt source ~70% ~90% brine Energy source ~55% hydro or gas 0% integrated ~85% hydro or gas ~60% integrated Cell-services Outsourced In-house North America ECU cost curve 3rd Quartile 1st Quartile Monetizing scale and advantaged cost positions via operational efficiency gains and asset optimization.

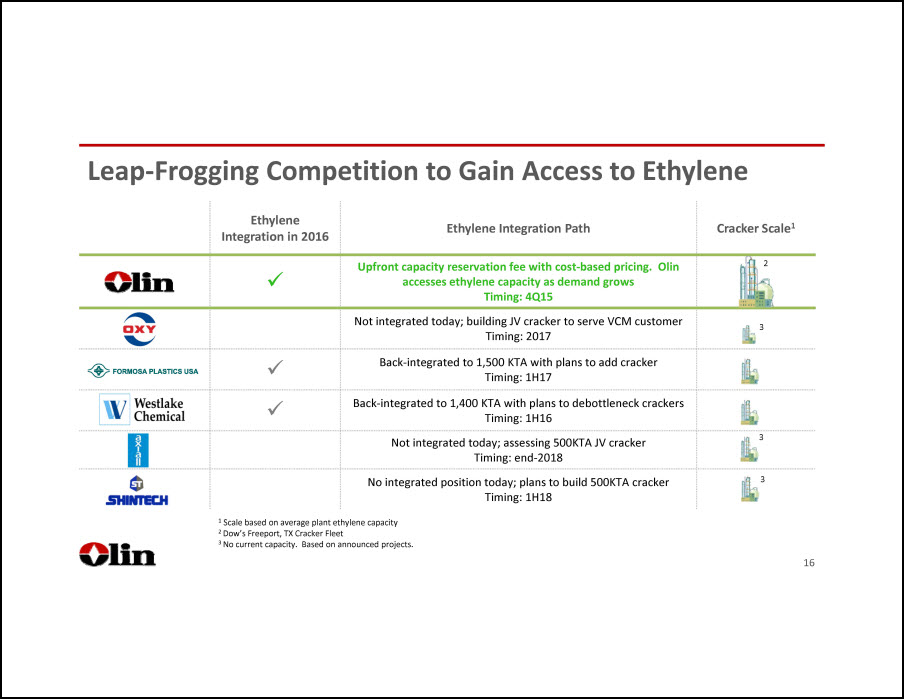

Leap-Frogging Competition to Gain Access to Ethylene Ethylene Integration in 2016 Ethylene Integration Path Cracker Scale1 Upfront capacity reservation fee with cost-based pricing. Olin accesses ethylene capacity as demand grows Timing: 4Q15 Not integrated today; building JV cracker to serve VCM customer Timing: 2017 Back-integrated to 1,500 KTA with plans to add cracker Timing: 1H17 Back-integrated to 1,400 KTA with plans to debottleneck crackers Timing: 1H16 Not integrated today; assessing 500KTA JV cracker Timing: end-2018 No integrated position today; plans to build 500KTA cracker Timing: 1H18 Leap-Frogging Competition to Gain Access to Ethylene 1 Scale based on average plant ethylene capacity 2 Dow’s Freeport, TX Cracker Fleet 3 No current capacity. Based on announced projects. 2 3 3 3

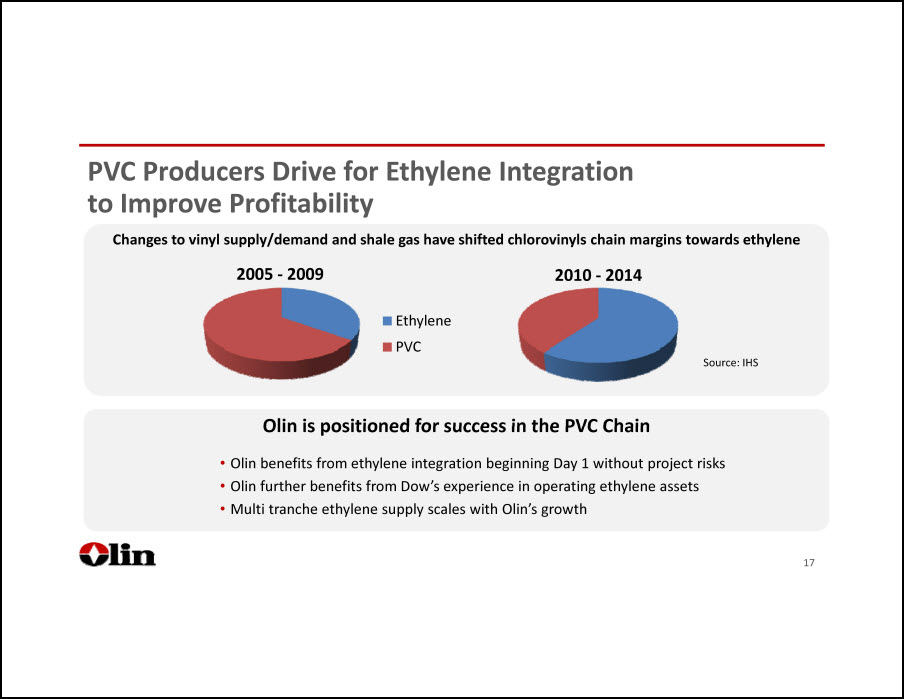

PVC Producers Drive for Ethylene Integration to Improve Profitability Changes to vinyl supply/demand and shale gas have shifted chlorovinyls chain margins towards ethylene Olin is positioned for success in the PVC Chain Source: IHS Olin benefits from ethylene integration beginning Day 1 without project risks Olin further benefits from Dow’s experience in operating ethylene assets Multi tranche ethylene supply scales with Olin’s growth 2005 - 2009 Ethylene PVC 2010 - 2014

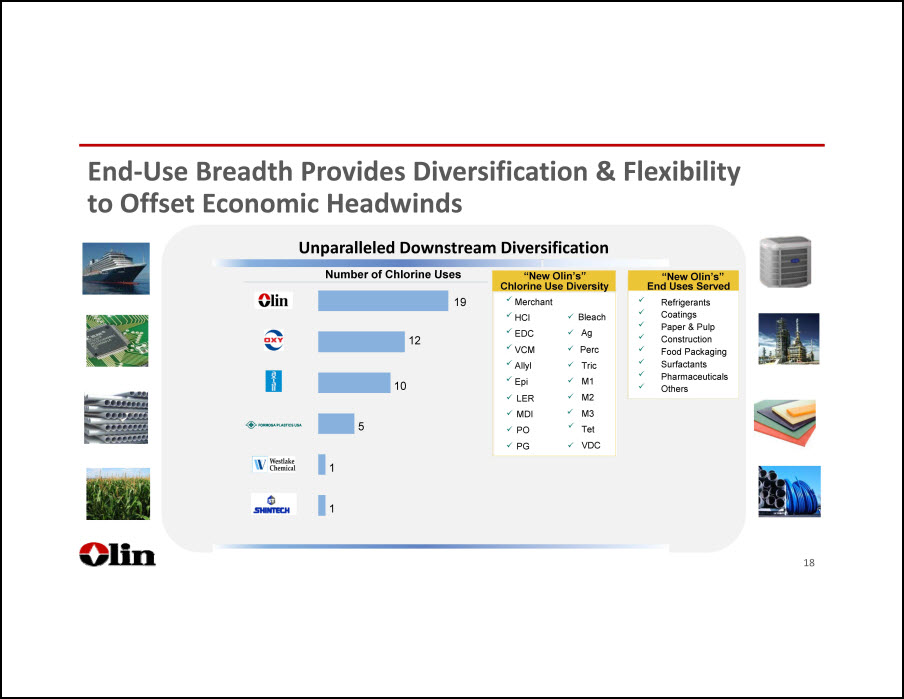

End-Use Breadth Provides Diversification & Flexibility to Offset Economic Headwinds Unparalleled Downstream Diversification

Number of Chlorine Uses 19 12 10 5 1 1 "New Olin's" Chlorine Use Diversity Merchant HCI EDC VCM Allyl Epi LER MDI PO PG Bleach Ag Perc Tric M1 M2 M3 Tet VDC "New Olin's" End Uses Served Refrigerants Coatings Paper & Pulp Construction Food Packaging Surfactants Pharmaceuticals Other

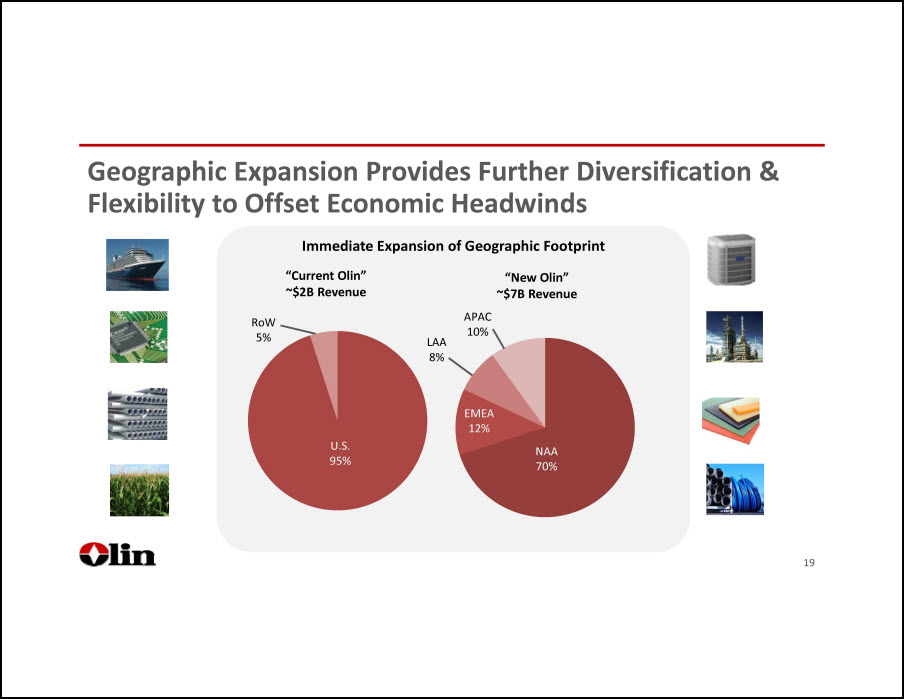

Geographic Expansion Provides Further Diversification & Flexibility to Offset Economic Headwinds Immediate Expansion of Geographic Footprint “Current Olin” ~$2B Revenue “New Olin” ~$7B Revenue U.S.95% RoW5% NAA70% EMEA12% LAA8% APAC10%

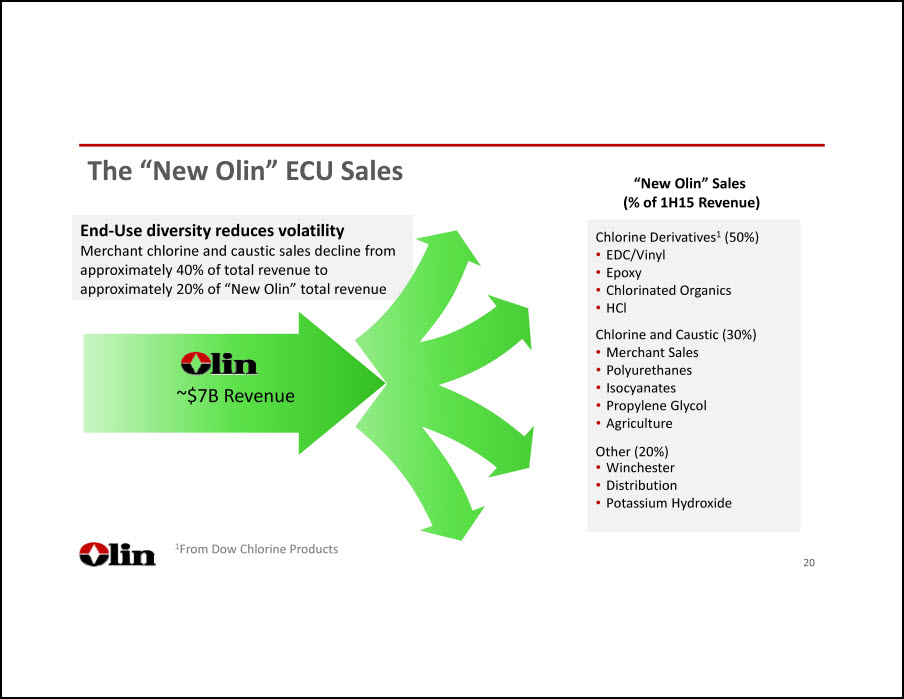

The “New Olin” ECU Sales Olin ~$7B Revenue “New Olin” Sales (% of 1H15 Revenue) End-Use diversity reduces volatility Merchant chlorine and caustic sales decline from approximately 40% of total revenue to approximately 20% of “New Olin” total revenue Chlorine Derivatives1 (50%) EDC/Vinyl Epoxy Chlorinated Organics HCl Chlorine and Caustic (30%) Merchant Sales Polyurethanes Isocyanates Propylene Glycol Agriculture Other (20%) Winchester Distribution Potassium Hydroxide 1From Dow Chlorine Products

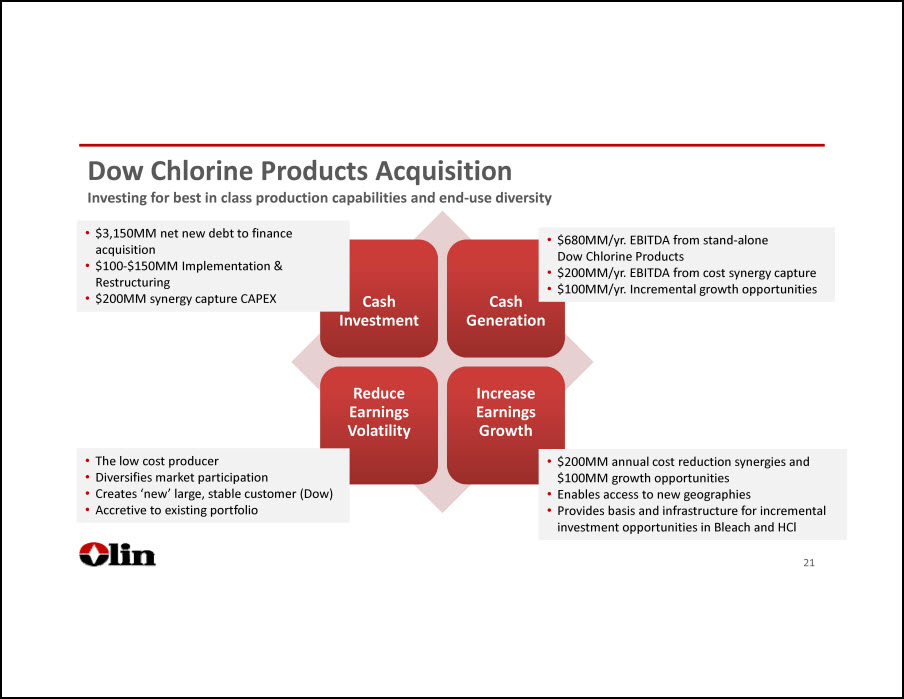

Dow Chlorine Products Acquisition Investing for best in class production capabilities and end-use diversity $3,150MM net new debt to finance acquisition $100-$150MM Implementation & Restructuring $200MM synergy capture CAPEX $680MM/yr. EBITDA from stand-alone Dow Chlorine Products $200MM/yr. EBITDA from cost synergy capture $100MM/yr. Incremental growth opportunities $200MM annual cost reduction synergies and $100MM growth opportunities Enables access to new geographies Provides basis and infrastructure for incremental investment opportunities in Bleach and HCl The low cost producer Diversifies market participation Creates ‘new’ large, stable customer (Dow) Accretive to existing portfolio

Winchester EBITDA & Cash Flows Support “New Olin” Profit improvement through growth and cost reduction reduces cyclicality Growth in shooting sports has increased installed customer base 49% growth in new shooters from 2009 to 2014 2/3rds are in the 18 to 34 age group and 50% are female Growth has been concentrated in handguns Centerfire relocation cost reduction program expected to yield $40 million of annual savings beginning in 2017 Cost savings in 2015 are expected to be $35 million Between 2006 and 2014, Winchester’s EBITDA has grown at a 25% compounded annual growth rate

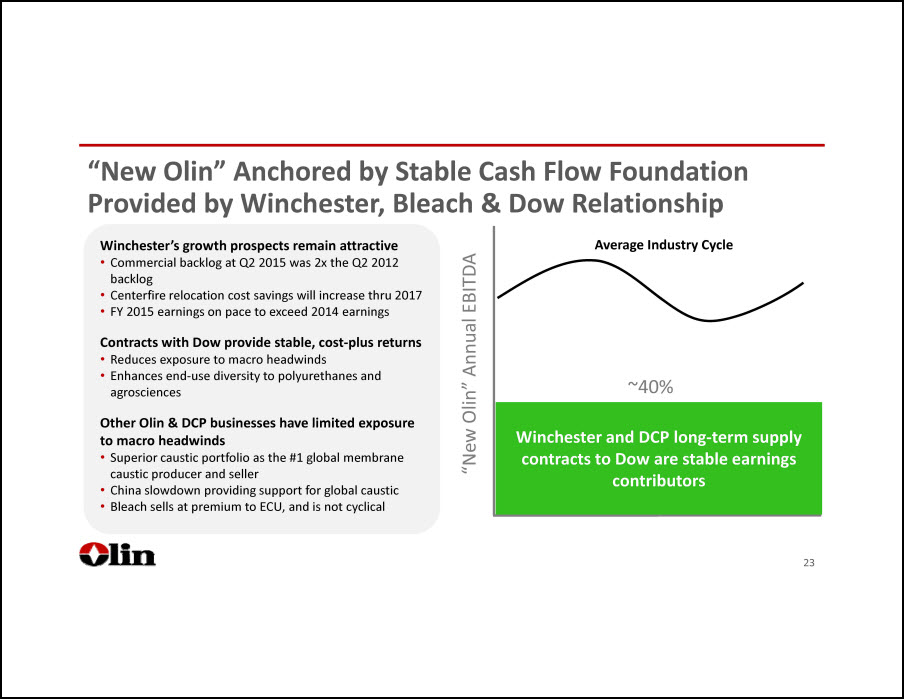

“New Olin” Anchored by Stable Cash Flow Foundation Provided by Winchester, Bleach & Dow Relationship Winchester’s growth prospects remain attractive Commercial backlog at Q2 2015 was 2x the Q2 2012 backlog Centerfire relocation cost savings will increase thru 2017 FY 2015 earnings on pace to exceed 2014 earnings Contracts with Dow provide stable, cost-plus returns Reduces exposure to macro headwinds Enhances end-use diversity to polyurethanes and agrosciences Other Olin & DCP businesses have limited exposure to macro headwinds Superior caustic portfolio as the #1 global membrane caustic producer and seller China slowdown providing support for global caustic Bleach sells at premium to ECU, and is not cyclical Winchester and DCP long-term supply contracts to Dow are stable earnings contributors ~40% “New Olin” Annual EBITDA Average Industry Cycle

Financial Priorities Moving Forward Maintain capital structure that provides financial flexibility to invest for organic growth and reward shareholders Ample cash generation to satisfy: Capital expenditures for maintenance, growth opportunities and synergy attainment Working capital fluctuations Debt reduction Shareholder remuneration 355 consecutive quarterly common dividends paid

Introducing “New Olin” The Global Leader in Chlorine Derivatives With Unmatched Scale, Integration, & Diversification #1 Chlor-alkali capacity globally #1 North America bleach and acid producer #1 Global supplier of epoxy materials #1 Integrated chlorinated organics producer Global top quartile chlor-alkali cost position Full ownership of newest, world-scale membrane chlor-alkali facility Only US producer with top quartile cost-based economics in brine, power, and ethylene Only US producer with in-house, best-in-class chlorine cell services Largest US producer with access to the most extensive USGC infrastructure (pipelines, power, deep-water & river access) Most diversified chlorine envelope of any North America producer Broadest geographic presence in caustic, epoxy, and chlorinated organics The most extensive distribution & logistics network Winchester provides portfolio balance and is a stable and consistent cash generator Global Leader in the Chlorine Value Chain Industry-Leading Scale & Cost Advantage Powerful Upstream Integration Unparalleled End-Use & Geographic Diversity