Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - TIDEWATER INC | d11579d8k.htm |

Pareto Securities Oil &

Offshore Conference

September 2, 2015

Jeffrey M. Platt Joseph M. Bennett President and CEO Executive Vice President and Chief Investor Relations Officer Exhibit 99.1 |

FORWARD-LOOKING STATEMENTS In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of

1995, the Company notes that certain statements set forth in this presentation

provide other than historical information and are forward looking.

The actual achievement of any forecasted results, or the unfolding

of future economic or business developments in a way anticipated or projected by the Company, involve numerous risks and uncertainties that may cause the Company’s actual

performance to be materially different from that stated or implied in the

forward-looking statement. Among those risks and uncertainties,

many of which are beyond the control of the Company, include,

without limitation, fluctuations in worldwide energy demand and oil and gas prices; fleet additions by competitors and industry overcapacity; changes in capital spending by

customers in the energy industry for offshore exploration, development and

production; changing customer demands for different vessel

specifications, which may make some of our older vessels

technologically obsolete for certain customer projects or in certain markets;

uncertainty of global financial market conditions and difficulty

accessing credit or capital; acts of terrorism and piracy;

significant weather conditions; unsettled political conditions, war, civil unrest

and governmental actions, such as expropriation or enforcement of

customs or other laws that are not well- developed or

consistently enforced, especially in higher political risk countries where we operate; foreign currency fluctuations; labor changes proposed by international conventions; increased

regulatory burdens and oversight; and enforcement of laws related to the

environment, labor and foreign corrupt practices. Readers should

consider all of these risks factors, as well as other information

contained in the Company’s form 10-K’s and 10-Q’s.

TIDEWATER 601

Poydras Street, Suite 1500, New

Orleans, La. 70130 Pareto Securities Oil & Offshore

Conference 2

Phone: 504.568.1010 | Fax: 504.566.4580 Web site address: www.tdw.com Email: connect@tdw.com |

Providing safe, efficient and compliant operations

New fleet comprised of vessels that service all water depths

Geographic diversity

Staying close to our customers

Prompt, proactive cost-cutting initiatives (“control what we

can control”)

Reducing CapEx, and returning capital to shareholders as

operating outlook improves

Maintaining a solid balance sheet (low leverage) and

sufficient liquidity

Experienced management team to lead the way

Tidewater’s Strategy & Focus in a Challenging Market

Pareto Securities Oil & Offshore Conference

3 |

Stop Work Obligation

Safety performance is 25% of mgt. incentive comp

Safe Operations is Priority #1

Pareto Securities Oil & Offshore Conference

4 0.00 0.10 0.20 0.30 0.40 0.50 0.60 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 TOTAL RECORDABLE INCIDENT RATES (per 200,000 Man Hours) TIDEWATER DOW CHEMICAL CHEVRON EXXON/MOBIL Operating safely offshore is like holding a snake by its head. It's a task that can't be turned loose not for a microsecond or an accident will strike without pity. |

Too Many Offshore Rigs, and Activity Levels Drive OSV Demand Pareto Securities Oil & Offshore Conference 5 0 50 100 150 200 250 300 350 400 450 8/04 8/05 8/06 8/07 8/08 8/09 8/10 8/11 8/12 8/13 8/14 8/1 Source: IHS-Petrodata Note: 32 “Other” rigs, along with the Jackups and Floaters, provide a total working rig count of 600 in August 2015. 361 207 Prior peak (summer 2008) Jackups Floaters Rig CIP Jackups 125 Floaters 75 Other 9 209 |

Drivers

of our Business “Peak to Present” Pareto Securities Oil

& Offshore Conference 6

July 2008 (Peak) Jan. 2011 (Trough) August 2015 Working Rigs 603 538 600 Rigs Under Construction 186 118 209 OSV Global Population 2,033 2,599 3,364 OSV’s Under Construction 736 367 398 OSV/Rig Ratio 3.37 4.83 5.60 (4.94 without ~400 old vessels believed not available) Source: IHS-Petrodata and Tidewater |

Tidewater’s Active Fleet

As of June 30, 2015 Pareto Securities Oil & Offshore Conference 7 0 5 10 15 20 25 30 35 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Year Built Deepwater vessels Towing Supply/Supply Other vessels 222 “New” vessels – 7.4 avg yrs 12 “Traditional” vessels – 27.3 avg yrs (only 4 OSVs) |

Vessel

Population by Owner (AHTS and PSVs only) Estimated as of August

2015 Pareto Securities Oil & Offshore Conference

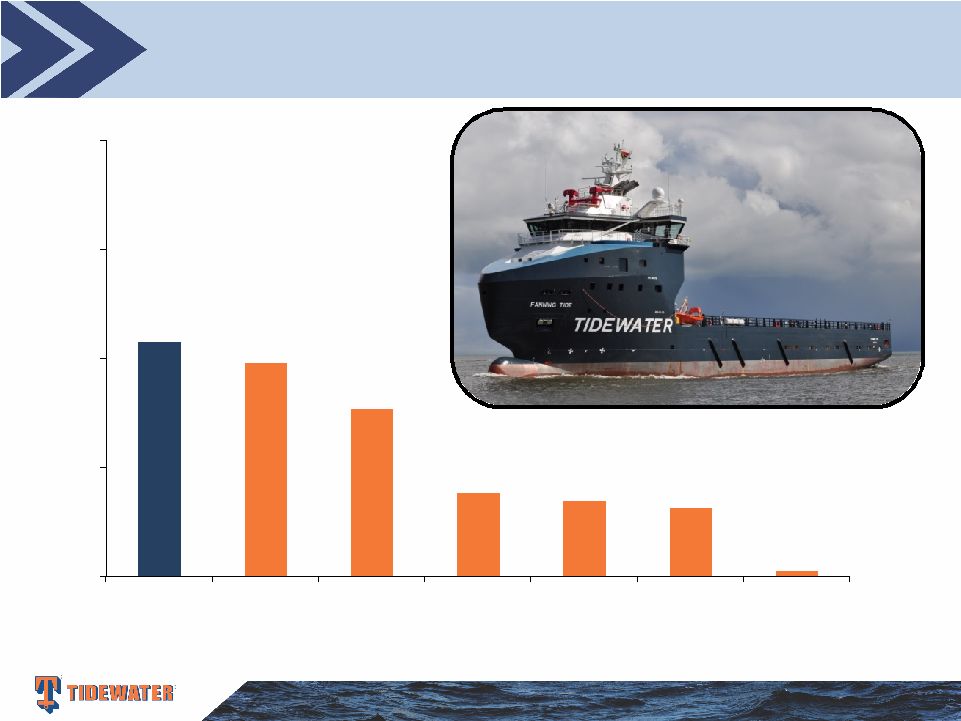

8 215 196 154 77 69 63 5 0 100 200 300 400 Tidewater Competitor #2 Competitor #3 Competitor #4 Competitor # 5 Competitor #1 Avg. All Others (~2,573 total vessels for 400+ owners) Source: IHS-Petrodata and Tidewater |

Geographic Diversity – Vessel Count by Region (Excludes stacked vessels – as of 6/30/15) Pareto Securities Oil & Offshore Conference 9 Americas 65(28%) SS Africa/Europe 103(44%) MENA 44(19%) Asia/Pac 22(9%) 38 additional Tidewater vessels were stacked as of 6/30/15. |

A New

Fleet that Services All Water Depths (Excludes

stacked vessels – as of 6/30/15) Pareto Securities Oil & Offshore Conference 10 New Avg. Traditional Vessels NBV Vessels Deepwater 8 $26.1M 0 Towing Supply 14 $10.8M 0 Other 0 0 0 22 0 New Avg. Traditional Vessels NBV Vessels Deepwater 33 $28.3M 0 Towing Supply 36 $12.6M 1 Other 30 $1.5M 3 99 4 New Avg. Traditional Vessels NBV Vessels Deepwater 36 20.7M 0 Towing Supply 19 $10.4M 2 Other 5 $1.6M 3 60 5 New Avg. Traditional Vessels NBV Vessels Deepwater 13 $17.0M 1 Towing Supply 28 $11.5M 0 Other 0 0 2 41 3 Americas SSAE MENA Asia/Pac Vessel count info is as of 6/30/15, and includes leased vessels. Avg NBV excludes the impact of leased vessels which have no NBV. Average NBV of the 12 Traditional vessels is ~$720,000 each at 6/30/15. |

Staying Close to our Customers – Strong Customer Base Current Revenue Mix Pareto Securities Oil & Offshore Conference 11 Super Majors 34% NOC's 33% Others 33% Approximately 60% of our revenue is derived from drilling support activity and 40% from non-drilling related activity, such as support of production and construction activity Our top 10 customers in Fiscal 2015 (4 Super Majors, 5 NOC’s, and 1 IOC) accounted for 61% of our revenue |

Our

Remaining Construction Backlog Pareto Securities Oil & Offshore

Conference 12

Count Deepwater PSVs 13 Deepwater AHTSs - Towing Supply/Supply 3 Other - Total 16 Vessels Under Construction As of June 30, 2015 Estimated delivery schedule – 10 remaining in FY ’16 and 6 in FY ‘17. CAPX of $154m remaining in

FY ‘16 and $69m in FY ‘17. |

CapEx is Decreasing from Recent High Levels Pareto Securities Oil & Offshore Conference 13 $0 $200 $400 $600 $800 $1,000 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Amounts in Fiscal 2016 and 2017 represent known CAPX on only the 16 vessels under construction as of 6/30/15. Fiscal 2014 is exclusive of Troms acquisition Fiscal Year |

Solid

Balance Sheet and Financial Flexibility Our Financial Position Provides Us

Strategic Optionality Pareto Securities Oil & Offshore

Conference 14

As of June 30, 2015

Cash & Cash Equivalents

$103 million Total Debt $1,544 million Shareholders Equity $2,451 million Net Debt / Net Capitalization 37% Total Debt / Capitalization 39% ~$700 million of available liquidity as of 6/30/15, including $600 million of unused capacity under the company’s revolving credit facility. |

Debt

Maturities and Covenants as of 6/30/15 Maturities Limited for Several

Years Pareto Securities Oil & Offshore Conference

15 Fiscal Year $0 $200 $400 $600 $800 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 Debt Covenants: 1) Debt/Total Capitalization Ratio of not greater than 55% 2) EBITDA/Interest coverage of not less than 3.0X |

Return

Capital to Shareholders Consistent Dividends and Opportunistic Share

Repurchases Pareto Securities Oil & Offshore

Conference 16

$0 $50 $100 $150 $200 $250 $300 $350 $400 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Dividends Share Repurchases (in millions) Fiscal Years ~6.0% Current Dividend Yield During this 16-year period, $659 million of dividends were paid and $757 million of total stock repurchases were made.

|

Tidewater’s Subsea Business

Pareto Securities Oil & Offshore Conference

17 Eight work-class ROVs in current fleet Commercial operations underway with additional opportunities in Americas, SSAE and Asia/Pac ROV capabilities generating potential for OSV pull through |

Tidewater’s Strategy

Pareto Securities Oil & Offshore Conference

18 Continue to improve upon stellar safety and compliance programs Stay close to our customers Monitor industry developments to adjust our playbook accordingly - Pro-active cost reduction initiatives - Maintain/protect liquidity Maintain solid balance sheet and financial flexibility to deal with industry uncertainties and seize opportunities when presented Return capital to shareholders through dividends and opportunistic share repurchases |

ANY QUESTIONS??

Q & A??? Pareto Securities Oil & Offshore Conference 19 |

HOUSTON, TEXAS Tidewater Marine, L.L.C. 6002 Rogerdale Road Suite 600 Houston, Texas 77072-1655 P: +1 713 470 5300 NEW ORLEANS, LOUISIANA Worldwide Headquarters Tidewater Inc. Pan American Life Center 601 Poydras Street, Suite 1500 New Orleans, Louisiana 70130 P: +1 504 568 1010 |

The

Worldwide OSV Fleet (Includes AHTS and PSVs only) Estimated as of August

2015 Pareto Securities Oil & Offshore Conference

21 As of August 2015, there are approximately 400 additional AHTS and PSV’s (~12% of the global fleet) under construction. Some number of these, we believe, will not be completed and delivered. Vessels > 25 years old today Global fleet is estimated at ~3,348 vessels, including ~700 vessels that are 25+ yrs old (21%). Source: ODS-Petrodata and Tidewater |

Fleet

Renewal & Expansion Largely Funded by CFFO Pareto Securities

Oil & Offshore Conference 22

Over a 16-year period, Tidewater has invested ~$5.5 billion in CapEx, and paid out

~$1.4 billion through dividends and share repurchases. Over the same

period, CFFO and proceeds from dispositions were ~$4.3 billion and ~$930

million, respectively. Fiscal Year |

History

of Solid Earnings and Returns on a Through-Cycle Basis Pareto

Securities Oil & Offshore Conference 23

Adjusted Return On Avg. Equity 4.3% 7.2% 12.4% 18.9% 18.3% 19.5% 11.4% 5.0% 4.3% 5.9% 7.0% 6.3%

Adjusted EPS**

$1.03 $1.78 $3.33 $5.94 $6.39 $7.89 $5.20 $2.40 $2.13 $3.03 $3.69 $3.33 $0.00 $2.00 $4.00 $6.00 $8.00 Fiscal 2004 Fiscal 2005 Fiscal 2006 Fiscal 2007 Fiscal 2008 Fiscal 2009 Fiscal 2010 Fiscal 2011 Fiscal 2012 Fiscal 2013 Fiscal 2014 Fiscal 2015 ** EPS in Fiscal 2004 is exclusive of the $.30 per share after tax impairment charge. EPS in Fiscal 2006 is exclusive of the $.74 per share after tax

gain from the sale of six KMAR vessels. EPS in Fiscal 2007 is exclusive of

$.37 per share of after tax gains from the sale of 14 offshore tugs. EPS in Fiscal 2010 is exclusive of $.66 per share Venezuelan provision, a $.70 per share tax benefit related to favorable resolution of tax litigation and a $0.22

per share charge for the proposed settlement with the SEC of the

company’s FCPA matter. EPS in Fiscal 2011 is exclusive of total $0.21 per share charges for settlements with DOJ and Government of Nigeria for FCPA matters, a $0.08 per share charge related to participation in a multi-company U.K.-based pension

plan and a $0.06 per share impairment charge related to certain vessels.

EPS in Fiscal 2012 is exclusive of $0.43 per share goodwill impairment charge. EPS in Fiscal 2014 is exclusive of $0.87 per share goodwill impairment charge. EPS in Fiscal 2015 is exclusive of $4.67 per share of goodwill and other assets impairment

charges. |

Active

Vessel Dayrates & Utilization by Segment

Pareto Securities Oil & Offshore Conference

24 $6,000 $10,000 $14,000 $18,000 $22,000 $26,000 12/11 6/12 12/12 6/13 12/13 6/14 12/14 6/15 Americas Asia/Pac MENA Sub Sah Africa/Eur. 60% 70% 80% 90% 100% 12/11 6/12 12/12 6/13 12/13 6/14 12/14 6/15 Utilization stats exclude stacked vessels. |

New

Vessel Trends by Vessel Type Deepwater PSVs

Pareto Securities Oil & Offshore Conference

25 22 23 24 25 25 25 25 28 29 32 34 38 40 43 44 45 47 49 51 54 55 57 62 66 69 73 75 76 76 77 80 81 86 - 40 80 120 160 200 240 $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 Average Day Rate, Adjusted Average Day Rate, and Average Fleet Size Average Fleet Size Average Day Rate Utilization-Adjusted Average Day Rate Q1 Fiscal 2016 Avg Day Rate: $26,917 Utilization: 72.7% $153 million, or 51%, of Vessel Revenue in Q1 Fiscal 2016 |

New

Vessel Trends by Vessel Type Deepwater AHTS

Pareto Securities Oil & Offshore Conference

26 5 5 5 5 5 5 5 5 6 8 9 9 11 11 11 11 11 11 11 11 11 11 11 11 11 11 12 12 12 12 12 12 12 - 40 80 120 160 200 240 $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 Average Day Rate, Adjusted Average Day Rate, and Average Fleet Size Average Fleet Size Average Day Rate Utilization-Adjusted Average Day Rate Q1 Fiscal 2016 Avg Day Rate: $30,813 Utilization: 59.6% $20 million, or 7%, of Vessel Revenue in Q1 Fiscal 2016 |

New

Vessel Trends by Vessel Type Towing Supply/Supply Vessels

Pareto Securities Oil & Offshore Conference

27 39 40 43 46 47 49 51 54 57 59 61 63 68 78 81 83 85 88 93 99 101 101 102 103 103 103 104 105 105 105 105 104 105 - 50 100 150 200 250 $0 $5,000 $10,000 $15,000 $20,000 $25,000 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 Average Day Rate, Adjusted Average Day Rate, and Average Fleet Size Average Fleet Size Average Day Rate Utilization-Adjusted Average Day Rate Q1 Fiscal 2016 Avg Day Rate: $14,252 Utilization: 74.3% $101 million, or 34%, of Vessel Revenue in Q1 Fiscal 2016 |

Vessel

Revenue and Vessel Operating Margin Fiscal 2008-2016

Pareto Securities Oil & Offshore Conference

28 Note: Vessel operating margin is defined as vessel revenue less vessel operating expenses

Prior peak period (FY2009)

averaged quarterly revenue of

$339M, quarterly operating

margin of $175.6M at 51.8%

$300 million $150 million 50.0% |

Historical Vessel Cash Operating Margins

Pareto Securities Oil & Offshore Conference

29 Vessel Cash Operating Margin ($) Vessel Cash Operating Margin (%) $119 million Vessel Margin in Q1 FY2016 (98% from New Vessels) Q1 FY2016 Vessel Margin: 40% |