Attached files

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2015

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 0-3279

KIMBALL INTERNATIONAL, INC. | ||

(Exact name of registrant as specified in its charter) | ||

Indiana | 35-0514506 | |

(State or other jurisdiction of | (I.R.S. Employer Identification No.) | |

incorporation or organization) | ||

1600 Royal Street, Jasper, Indiana | 47549-1001 | |

(Address of principal executive offices) | (Zip Code) | |

(812) 482-1600 | ||

Registrant's telephone number, including area code | ||

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each Class | Name of each exchange on which registered | |

Class B Common Stock, par value $0.05 per share | The NASDAQ Stock Market LLC | |

Securities registered pursuant to Section 12(g) of the Act: | ||

Class A Common Stock, par value $0.05 per share | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. Large accelerated filer o Accelerated filer x Non-accelerated filer o Smaller reporting company o (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x |

Class A Common Stock is not publicly traded and, therefore, no market value is available, but it is convertible on a one-for-one basis for Class B Common Stock. The aggregate market value of the Class B Common Stock held by non-affiliates, as of December 31, 2014 (the last business day of the Registrant's most recently completed second fiscal quarter) was $340.0 million, based on 98.5% of Class B Common Stock held by non-affiliates.

The number of shares outstanding of the Registrant's common stock as of August 17, 2015 was:

Class A Common Stock - 336,657 shares

Class B Common Stock - 37,219,426 shares

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the Annual Meeting of Share Owners to be held on October 20, 2015, are incorporated by reference into Part III.

KIMBALL INTERNATIONAL, INC.

FORM 10-K INDEX

Page No. | ||

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

2

PART I

Forward-Looking Statements

This document contains certain forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These are statements made by management, using their best business judgment based upon facts known at the time of the statements or reasonable estimates, about future results, plans, or future performance and business of the Company. Such statements involve risk and uncertainty, and their ultimate validity is affected by a number of factors, both specific and general. They should not be construed as a guarantee that such results or events will, in fact, occur or be realized as actual results may differ materially from those expressed in these forward-looking statements. The statements may be identified by the use of words such as “believes,” “anticipates,” “expects,” “intends,” “plans,” “projects,” “estimates,” “forecasts,” “seeks,” “likely,” “future,” “may,” “might,” “should,” “would,” “will,” and similar expressions. It is not possible to foresee or identify all factors that could cause actual results to differ from expected or historical results. We make no commitment to update these factors or to revise any forward-looking statements for events or circumstances occurring after the statement is issued, except as required in current and quarterly periodic reports filed with the Securities and Exchange Commission (“SEC”) or otherwise by law.

The risk factors discussed in Item 1A - Risk Factors of this report could cause our results to differ materially from those expressed in forward-looking statements. There may be other risks and uncertainties that we are unable to predict at this time or that we currently do not expect to have a material adverse effect on our business. Any such risks could cause our results to differ materially from those expressed in forward-looking statements.

At any time when we make forward-looking statements, we desire to take advantage of the “safe harbor” which is afforded such statements under the Private Securities Litigation Reform Act of 1995 where factors could cause actual results to differ materially from forward-looking statements.

Item 1 - Business

As used herein, the terms “Company,” “Kimball,” “we,” “us,” or “our” refer to Kimball International, Inc., the Registrant, and its subsidiaries. Reference to a year relates to a fiscal year, ended June 30 of the year indicated, rather than a calendar year unless the context indicates otherwise. Additionally, references to the first, second, third, and fourth quarters refer to those respective quarters of the fiscal year indicated.

Spin-Off of Kimball Electronics reported as Discontinued Operations

On October 31, 2014 (“Distribution Date”), we completed the spin-off of our Electronic Manufacturing Services (“EMS”) segment by distributing the related shares of Kimball Electronics, Inc. (“Kimball Electronics”), on a pro rata basis, to the Company's Share Owners of record as of October 22, 2014 (“the Record Date”). On the Distribution Date, each of the Company's Share Owners received three shares of Kimball Electronics for every four shares of the Company held by such Share Owner on the Record Date. After the Distribution Date, the Company does not beneficially own any Kimball Electronics shares and Kimball Electronics is an independent publicly traded company. Kimball International, Inc. trades on the NASDAQ under the ticker symbol “KBAL” and Kimball Electronics, Inc. trades on the NASDAQ under the ticker symbol “KE”.

In connection with the spin-off of Kimball Electronics, the Company and Kimball Electronics entered into several agreements covering administrative and tax matters to provide or obtain services on a transitional basis, as needed, for varying periods after the spin-off, including a separation and distribution agreement, a tax matters agreement, an employee matters agreement, and a transition services agreement. The administrative agreements cover various services such as information technology, human resources, taxation, and finance. The Company expects all transition services to be substantially complete within one year after the spin-off. The Company has retained all liabilities for U.S. federal, state, and local income taxes on income prior to the spin-off, as well as certain non-income taxes attributable to Kimball Electronics’ business. Kimball Electronics generally will be liable for all other taxes attributable to its business. In connection with the spin-off, the Company has adjusted its employee stock compensation awards and separated its retirement and post-employment benefit plans. The agreements listed above have been incorporated by reference as exhibits to this Annual Report on Form 10-K. The above summary of the agreements is qualified in its entirety by reference to the full text of the applicable agreements.

On October 30, 2014, holders of a sufficient number of shares of Class A common stock converted such shares into Class B common stock such that the number of outstanding shares of Class A common stock is, after such conversions, less than 15% of the total number of issued and outstanding shares of both Class A common stock and Class B common stock. Pursuant to the Company’s Amended and Restated Articles of Incorporation if at any time the number of shares of Class A common stock issued and outstanding is less than 15% of the total number of issued and outstanding shares of both Class A common stock and Class B common stock, then all of the rights, preferences, limitations and restrictions relating to Class B common stock shall

3

become the same as the rights, preferences, limitations and restrictions of Class A common stock, without any further action of or by its Share Owners, and all distinctions between Class A common stock and Class B common stock shall be eliminated so that all shares of Class B common stock are equal to shares of Class A common stock with respect to all matters, including without limitation, dividend payments and voting rights. The elimination of such distinctions, which occurred on October 30, 2014, is referred to as the “stock unification.” As a result of the stock unification, Class A common stock and Class B common stock now vote as a single class (except as otherwise required by applicable law) on all matters submitted to a vote of the Company’s Share Owners. We have filed to deregister the shares of Class A Common Stock under the Exchange Act. It is expected that deregistration will become effective in September 2015. Deregistration will not affect the rights of Share Owners who choose to continue to hold their Class A shares. See Note 2 - Spin-Off Transaction of Notes to Consolidated Financial Statements for more information on the spin-off of our EMS segment.

The following disclosures within this Part I, have been recast to describe the continuing operations of Kimball International, Inc. after the spin-off.

Overview

Kimball was incorporated in Indiana in 1939. Our corporate headquarters is located at 1600 Royal Street, Jasper, Indiana.

Kimball is a leading manufacturer of design driven, technology savvy, high quality furnishings sold under the Company’s family of brands: National, Kimball Office, and Kimball Hospitality. Our diverse portfolio provides solutions for the workplace, learning, healing, and hospitality environments. Customers can access our products globally through a variety of distribution channels. Recognized with a reputation for excellence as a trustworthy company and recognized with the Great Place to Work® designation, Kimball International is committed to a high performance culture with a foundation of sound ethics, continuous improvement, and social responsibility.

Kimball has been in the furniture business since 1950. Our core markets include furniture sold under the Kimball Office, National, and Kimball Hospitality brand names. Throughout all of the brands, the Company offers unlimited possibilities for creating functional environments that convey just the right image for each unique setting as furniture solutions are tailored to the end user's needs and demands. The workplace model is evolving to optimize human interaction, and Kimball Office and National provide furniture solutions which create spaces where people can connect. Our rich wood heritage and craftsmanship remain, while new products and mixed materials integrate into our product portfolio, satisfying the marketplace's need for multi-functional, open accommodations throughout all industries. Our furniture solutions are used in open floor plan areas, conference rooms, training rooms, private offices, lobby/reception areas, and dining/lounge areas with a vast mix of wood, metal, laminate, paint, and fabric options. Products include modern and classic desks, credenzas, seating, tables, collaborative workstations, contemporary cubicle systems, filing and storage units, and accessories. In addition, the Company introduced several new products designed specifically for the growing healthcare market. In the hospitality industry, Kimball Hospitality works with designers to create furniture which extends the unique ambiance of a property into guest rooms and public spaces by providing furniture solutions for hotel properties and mixed use developments. Products include, but are not limited to, headboards, desks, tables, dressers, entertainment centers, chests, wall panels, upholstered seating, task seating, cabinets, and vanities with a broad mix of wood, metal, stone, laminate, finish, and fabric options. The Company also has a trucking fleet and customer fulfillment centers to facilitate prompt delivery of products. Certain logistics services, such as backhauls, are sold on a contract basis, but the sales level is immaterial.

Production currently occurs in Company-owned or leased facilities located in the United States. In the United States, we have manufacturing facilities and showrooms in ten states and the District of Columbia. Financial information by geographic area for each of the three years in the period ended June 30, 2015 is included in Note 15 - Geographic Area Information of Notes to Consolidated Financial Statements and is incorporated herein by reference.

Recent Business Changes

Capacity Utilization Restructuring Plan

In November 2014, we announced a capacity utilization restructuring plan which includes the consolidation of our metal fabrication production from an operation located in Post Falls, Idaho, into existing production facilities in Indiana, and the reduction of our Company plane fleet from two jets to one.

Key factors in the decision to consolidate the Post Falls operation into the Indiana facilities include the improvement of customer delivery, supply chain dynamics, and transportation costs. The transfer of work involves the start-up of metal fabrication capabilities in a Company-owned facility, along with the transfer of certain assembly operations into two additional Company-owned facilities, all located in southern Indiana. The manufacturing capacity realignment will be carefully managed to mitigate customer disruptions. The consolidation activities began immediately after the announcement in November 2014,

4

and we are actively marketing for sale the Post Falls, Idaho facility. We anticipate pre-tax savings of approximately $5 million per year after the plan is fully implemented which is expected to occur by September 2016.

The reduction of our plane fleet from two jets to one reduces our cost structure while aligning the plane fleet size with our needs following the spin-off of Kimball Electronics. Previously, one of our jets was used primarily for the successful strategy of transporting customers to visit our showrooms, offices, research and development center, and manufacturing locations, while the remaining jet was used primarily for management travel. The plane used primarily for management travel was sold in the third quarter of fiscal year 2015, and as a result, we began realizing the expected annual pre-tax savings of $0.8 million. In regards to the remaining jet, we believe that our location in rural Jasper, Indiana and the location of our manufacturing locations in small towns away from major metropolitan areas necessitates the need for the remaining jet to efficiently transport customers.

Other Recent Business Changes

Production within our existing facilities was expanded in fiscal years 2015 and 2013 to manufacture select hospitality furniture products domestically, improving our ability to meet customer requests for shorter lead times.

A production facility in Virginia was opened during fiscal year 2011 to manufacture upholstered seating, headboards, and other products for the Company's custom, program, and catalog offerings for hospitality guest rooms and public spaces.

Seasonality

The impact of seasonality on our sales revenue includes lower sales in the third quarter of our fiscal year due to the buying season of the government and lower sales of hospitality furniture during times of high hotel occupancy such as the summer months.

Locations

The Company's products as of June 30, 2015 were primarily produced at eleven plants: seven located in Indiana, two in Kentucky, and one each in Idaho and Virginia. In addition, select finished goods are purchased from external sources. The Company continually assesses manufacturing capacity and adjusts such capacity as necessary.

In addition, a facility in Indiana houses an education center for dealer and employee training, a research and development center (American Association for Laboratory Accreditation certified), and a product showroom. Furniture showrooms are maintained in eight additional cities in the United States. Office space is leased in Dongguan, Guangdong, China and Ho Chi Minh City, Vietnam to facilitate sourcing of select finished goods and components from the Asia Pacific Region.

Marketing Channels

Our furniture is marketed by sales representatives to end users, office furniture dealers, wholesalers, brokers, designers, purchasing companies, and catalog houses throughout North America and on an international basis.

We categorize our sales by the following vertical markets:

Education - Whether K-12, higher education, vocational training or any other learning institution, we understand that furniture for education needs to enhance learning and social environments. We offer quality, stylish solutions that we believe will make students and faculty more productive and comfortable.

Finance - Banking and financial offices require affordable, functional, and stylish environments. Our versatile and flexible furnishings offer sophisticated styles for reception areas, employee work spaces, executive offices, and boardrooms.

Government - We supply office furniture including desks, tables, seating, bookcases and filing and storage units for federal, state, and local government offices. We hold a GSA Multiple Award Schedule with General Services Administration Federal Supply Service. We also partner with multiple general purchasing organizations which assist public agencies such as state and local governments with office furniture purchases.

Healthcare - We offer products to value-conscious healthcare customers, including hospitals, clinics, physician office buildings, long-term care facilities, and assisted living facilities throughout the country.

Hospitality - We offer a complete package of product and service support to the hospitality industry. We partner with the most recognized hotel brands to meet their specific requirements for properties throughout the world.

Commercial - The largest portion of our business is in the commercial market. We are a full-facility provider offering products for a variety of office applications including: private office, open plan, lobby-lounge, conferencing, dining, and everything in between.

5

A table showing our net sales by end market vertical is included in Part II, Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations.

Major Competitive Factors

Our products are sold in the office furniture and hospitality furniture industries. These industries have similar major competitive factors which include price in relation to quality and appearance, the utility of the product, supplier lead time, reliability of on-time delivery, sustainability, and the ability to respond to requests for special and non-standard products. We offer payment terms similar to industry standards and in unique circumstances may grant alternate payment terms.

Certain industries are more price sensitive than others, but all expect on-time, damage-free delivery. The Company maintains sufficient finished goods inventories to be able to offer prompt shipment of most of our own lines of hospitality furniture. In addition to the many options available on our standard furniture products, custom furniture is produced to customer specifications and shipping timelines on a project basis. Many of our office furniture products are shipped through our delivery system, which we believe offers the ability to reduce damage to product, enhance scheduling flexibility, and improve the capability for on-time deliveries.

Competitors

There are numerous furniture manufacturers competing within the marketplace, with a significant number of competitors offering similar products.

Our competition includes furniture manufacturers such as Steelcase Inc., Herman Miller, Inc., Knoll, Inc., HNI Corporation, and several other privately-owned furniture manufacturers.

Working Capital

The Company does not believe that it or the industry in general, has any special practices or special conditions affecting working capital items that are significant for understanding our furniture business. The Company does receive advance payments from customers on select furniture projects primarily in the hospitality industry.

Raw Material Availability

Certain components used in the production of furniture are manufactured internally and are generally readily available, as are other raw materials used in the production of wood and non-wood furniture. Certain fabricated seating components and wood frame assemblies as well as finished furniture products, which are generally readily available, are sourced on a global scale in an effort to provide quality products at the lowest total cost.

Order Backlog

The aggregate sales price of products pursuant to worldwide open orders, which may be canceled by the customer, was as follows:

(Amounts in Millions) | June 30, 2015 | June 30, 2014 | |||||

Order Backlog of Continuing Operations | $ | 111.9 | $ | 97.2 | |||

Substantially all of the open orders as of June 30, 2015 are expected to be filled within the next fiscal year. Open orders may not be indicative of future sales trends.

Research and Development

Research and development activities include the development of manufacturing processes, engineering and testing procedures, major process improvements, new product development and product redesign, information technology initiatives, and wood related technologies.

Research and development costs were approximately:

Year Ended June 30 | |||||

(Amounts in Millions) | 2015 | 2014 | 2013 | ||

Research and Development Costs of Continuing Operations | $7 | $7 | $6 | ||

6

Intellectual Property

We own the Kimball (registered trademark) trademark and we own the following trademarks which we believe are significant to the Company:

Registered Trademarks: Acquaint, Beo, Bingo, Boyd, Cetra, Definition, Dock, Eloquence, Epicenter, Footprint, Fringe, Hum. Minds at Work, IntegraClear, Interworks, Jiminy, Mix-It, National, National. Furniture with Personality, Perks, Pura, Staccato, Traxx, WaveWorks, Xsite

Trademarks: Aurora, Fold, Jewel, Lavoro, Mio, Myriad, Priority, Swift, Villa, Wish, Bloom (pending), Canopy (pending), Epic (pending), Essay (pending), Flip (pending), Kimball Health (pending), Kore (pending), Pairings (pending), Whimsy (pending), Xsede (pending)

We also own patents for the following products which we believe are significant to the Company:

Patents: Acquaint, Aurora, Davari, Epic, Exhibit, Fluent, Mix-It, Priority, Swift, Villa, Wish, Xsite, Xsede (pending)

We also own other patents and trademarks and have certain other trademark and patent applications pending, which in our opinion are not significant to our business. Patents expire at various times depending on the patent's date of issuance.

Environment and Energy Matters

Our operations are subject to various federal, state, local, and foreign laws and regulations with respect to environmental matters. We believe that we are in substantial compliance with present laws and regulations and that there are no material liabilities related to such items.

We are dedicated to excellence, leadership, and stewardship in matters of protecting the environment and communities in which we have operations. Reinforcing our commitment to the environment, seven of our showrooms and two non-manufacturing locations were designed under the guidelines of the U.S. Green Building Council's LEED (Leadership in Energy and Environmental Design) for Commercial Interiors program. One manufacturing facility was designed under the LEED Operations and Maintenance program guidelines. We believe that continued compliance with foreign, federal, state, and local laws and regulations which have been enacted relating to the protection of the environment will not have a material effect on our capital expenditures, earnings, or competitive position. We believe capital expenditures for environmental control equipment during the two fiscal years ending June 30, 2017, will not represent a material portion of total capital expenditures during those years.

Our manufacturing operations require the use of natural gas and electricity. Federal and state regulations may control the allocation of fuels available to us, but to date we have experienced no interruption of production due to such regulations. In our wood furniture manufacturing plants a portion of energy requirements are satisfied internally by the use of our own scrap wood produced during the manufacturing of product.

Employees

June 30 2015 | June 30 2014 | ||||

United States | 2,828 | 2,783 | |||

Foreign Countries | 66 | 61 | |||

Total Employees of Continuing Operations | 2,894 | 2,844 | |||

Our U.S. operations and foreign sites are not subject to collective bargaining arrangements. We believe that our employee relations are good.

Available Information

The Company makes available free of charge through its website, http://www.ir.kimball.com, its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. All reports the Company files with the SEC are also available via the SEC website, http://www.sec.gov, or may be read and copied at the SEC Public Reference Room located at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The Company's Internet website and the information contained therein or incorporated therein are not intended to be incorporated into this Annual Report on Form 10-K.

7

Item 1A - Risk Factors

The following important risk factors, among others, could affect future results and events, causing results and events to differ materially from those expressed or implied in forward-looking statements made in this report and presented elsewhere by management from time to time. Such factors, among others, may have a material adverse effect on our business, financial condition, and results of operations and should be carefully considered. Additional risks and uncertainties that we do not currently know about, we currently believe are immaterial or we have not predicted may also affect our business, financial condition, or results of operations. Because of these and other factors, past performance should not be considered an indication of future performance.

We may not realize the potential benefits that we expect to achieve subsequent to the spin-off of our EMS segment into a new independent publicly traded company. The spin-off was completed on October 31, 2014, but spin-off related matters will likely continue to require time and attention of our management for the first half of fiscal year 2016. We may not realize the anticipated benefits from the spin-off as quickly as expected or at all. Any such difficulties or distractions could adversely affect our financial position, results of operations, or cash flows.

If the distribution or certain internal transactions undertaken relating to the spin-off do not qualify as tax-free transactions, the Company, its Share Owners as of the distribution date, and Kimball Electronics could be subject to substantial tax liabilities. On October 10, 2014 the Company received a favorable written tax ruling from the Internal Revenue Service (“IRS”) that the Company’s stock unification in connection with the spin-off will not cause the Company to recognize income or gain as a result of the unification. In addition, the Company has also received an opinion of Squire Patton Boggs (US) LLP to the effect that the distribution satisfies the requirements to qualify as a tax-free transaction (except for cash received in lieu of fractional shares) for U.S. federal income tax purposes to the Company, the Company’s Share Owners and Kimball Electronics under Section 355 of the Internal Revenue Code of 1986, as amended (the “Code”).

The tax ruling and the tax opinion rely on the accuracy of certain factual representations and assumptions provided by the Company and Kimball Electronics in connection with obtaining the tax ruling and tax opinion, including with respect to post-spin-off operations and conduct of the parties. If these factual representations and assumptions are inaccurate or incomplete in any material respect, we will not be able to rely on the tax ruling and/or the tax opinion.

Furthermore, the tax opinion will not be binding on the IRS or the courts. Accordingly, the IRS or the courts may reach conclusions with respect to the spin-off that are different from the conclusions reached in the tax opinion. If, notwithstanding our receipt of the tax opinion, the spin-off is determined to be taxable, then (i) the Company would be subject to tax as if it sold the Kimball Electronics common stock in a taxable sale for its fair market value; and (ii) each Share Owner who received Kimball Electronics common stock would be treated as receiving a distribution of property in an amount equal to the fair market value of the Kimball Electronics common stock that would generally result in varied tax liabilities for each Share Owner depending on the facts and circumstances.

Even if the spin-off does qualify as a tax-free transaction for U.S. federal income tax purposes, the distribution will be taxable to the Company (but not to the Company’s Share Owners) pursuant to Section 355(e) of the Code if there are one or more acquisitions (including issuances) of the stock of either the Company or Kimball Electronics, representing 50% or more, measured by vote or value, of the then-outstanding stock of either the Company or Kimball Electronics and the acquisition or acquisitions are deemed to be part of a plan or series of related transactions that include the distribution. Any acquisition of our common stock within two years before or after the distribution (with exceptions, including public trading by less-than-5% Share Owners and certain compensatory stock issuances) generally will be presumed to be part of such a plan unless that presumption is rebutted. The resulting tax liability may have a material adverse effect on our business, financial condition, results of operations and cash flows.

We entered into a Tax Matters Agreement with Kimball Electronics that governs the respective rights, responsibilities and obligations of us and Kimball Electronics after the spin-off with respect to tax liabilities and benefits, tax attributes, tax contests and other tax sharing regarding U.S. federal, state, local and foreign income taxes, other tax matters and related tax returns. The Tax Matters Agreement also provides special rules for allocating tax liabilities in the event that the spin-off or certain internal transactions undertaken in anticipation of the spin-off do not qualify as tax-free transactions. Though valid as between us and Kimball Electronics, the Tax Matters Agreement will not be binding on the IRS.

Pursuant to the Tax Matters Agreement, (i) we have agreed (a) not to enter into any transaction that could cause any portion of the spin-off to be taxable to Kimball Electronics, including under Section 355(e) of the Code; (b) to indemnify Kimball Electronics for any tax liabilities resulting from such transactions entered into by us; and (ii) Kimball Electronics has agreed to indemnify us for any tax liabilities resulting from such transactions entered into by Kimball Electronics. In addition, under U.S. Treasury regulations, each member of the Company’s consolidated group at the time of the spin-off (including Kimball Electronics) would be jointly and severally liable for the resulting U.S. federal income tax liability if all or a portion of the spin-off does not or certain internal transactions undertaken in anticipation of the spin-off do not qualify as tax-free transactions. These obligations may discourage, delay or prevent a change of control of our Company.

8

If Kimball Electronics were to default in its obligation to us to pay taxes under the Tax Matters Agreement, we could be legally liable under applicable tax law for such liabilities and required to make additional tax payments. Accordingly, under certain circumstances, we may be obligated to pay amounts in excess of our agreed-upon share of tax liabilities. To the extent we are responsible for any liability under the Tax Matters Agreement, there could be a material adverse impact on our business, financial condition, results or operations and cash flows.

Uncertain macroeconomic and industry conditions could adversely impact demand for our products and adversely affect operating results. Market demand for our products, which impacts revenues and gross profit, is influenced by a variety of economic and industry factors such as:

• | weakness in the global financial markets; |

• | volatility and the cyclical nature of worldwide economic conditions; |

• | global consumer confidence; |

• | general corporate profitability of the end markets to which we sell; |

• | credit availability to the end markets to which we sell; |

• | white-collar unemployment rates; |

• | commercial property vacancy rates; |

• | new office construction and refurbishment rates; |

• | deficit status of many governmental entities which may result in declining purchases of office furniture; |

• | new hotel and casino construction and refurbishment rates. |

We must make decisions based on order volumes in order to achieve efficiency in manufacturing capacities. These decisions include determining what level of additional business to accept, production schedules, component procurement commitments, and personnel requirements, among various other considerations. We must constantly monitor the changing economic landscape and may modify our strategic direction based upon the changing business environment. If we do not react quickly enough to the changes in market or economic conditions, it could result in lost customers, decreased market share, and increased operating costs.

We may be exposed to the credit risk of our customers who are adversely affected by weakness in market conditions. Weakness in market conditions may drive an elevated risk of potential bankruptcy of customers resulting in a greater risk of uncollectible outstanding accounts receivable. Accordingly, we intensely monitor our receivables and related credit risks. The realization of these risks could have a negative impact on our profitability.

Reduction of purchases by or the loss of a significant number of customers could reduce revenues and profitability. Significant declines in the level of purchases by customers or the loss of a significant number of customers, could have a material adverse effect on our business. A reduction of government spending could also have an adverse impact on our sales levels. We can provide no assurance that we will be able to fully replace any lost sales, which could have an adverse effect on our financial position, results of operations, or cash flows.

We operate in a highly competitive environment and may not be able to compete successfully. The office and hospitality furniture industries are competitive due to numerous global manufacturers competing in the marketplace. In times of reduced demand for office furniture, large competitors may apply more pressure to their aligned distribution to sell their products exclusively which could lead to reduced opportunities for our products. While we work toward reducing costs to respond to pricing pressures, if we cannot achieve the proportionate reductions in costs, profit margins may suffer. In addition, as end markets dictate, we are continually assessing excess capacity and developing plans to better utilize manufacturing operations.

We may be unable to purchase a sufficient amount of materials, parts, and components for use in our products at a competitive price, in a timely manner, or at all. We depend on suppliers globally to provide timely delivery of materials, parts, and components for use in our products. We monitor the financial stability of suppliers when feasible as the loss of a significant supplier could have an adverse impact on our operations. Certain finished products and components we purchase are primarily manufactured in select regions of the world and issues in those regions could cause manufacturing delays. In addition, delays can occur related to the transport of products and components via container ships, which load and unload through various U.S. ports which sometimes experience congestion. Maintaining strong relationships with key suppliers is essential. Price increases of commodity components could have an adverse impact on our profitability if we cannot offset such increases with other cost reductions or by price increases to customers. Materials we utilize are generally available, but future availability is unknown and could impact our ability to meet customer order requirements. If suppliers fail to meet commitments to us in terms of price, delivery, or quality, it could interrupt our operations and negatively impact our ability to meet commitments to customers.

Our operating results could be adversely affected by increases in the cost of fuel and other energy sources. The cost of energy is a critical component of freight expense and the cost of operating manufacturing facilities. Increases in the cost of energy could reduce our profitability.

9

We are subject to manufacturing inefficiencies due to the transfer of production and other factors. At times we may experience labor or other manufacturing inefficiencies due to factors such as new product introductions, transfers of production among our manufacturing facilities, a sudden decline in sales, a new operating system, or turnover in personnel. Manufacturing inefficiencies could have an adverse impact on our financial position, results of operations, or cash flows.

A change in our sales mix among various products could have a negative impact on the gross profit margin. Changes in product sales mix could negatively impact our gross margin as margins of different products vary. We strive to improve the margins of all products, but certain products have lower margins in order to price the product competitively. An increase in the proportion of sales of products with lower margins could have an adverse impact on our financial position, results of operations, or cash flows.

Our restructuring efforts may not be successful. We continually evaluate our manufacturing capabilities and capacities in relation to current and anticipated market conditions. A critical component of our restructuring initiatives is the transfer of production among facilities which may result in some manufacturing inefficiencies and excess working capital during the transition period. The successful execution of restructuring initiatives is dependent on various factors and may not be accomplished as quickly or effectively as anticipated.

We will face risks commonly encountered with growth through acquisitions. Our sales growth plans may occur through both organic growth and acquisitions. Acquisitions involve many risks, including:

• | difficulties in identifying suitable acquisition candidates and in negotiating and consummating acquisitions on terms attractive to us; |

• | difficulties in the assimilation of the operations of the acquired company; |

• | the diversion of resources, including diverting management's attention from our current operations; |

• | risks of entering new geographic or product markets in which we have limited or no direct prior experience; |

• | the potential loss of key customers of the acquired company; |

• | the potential loss of key employees of the acquired company; |

• | the potential incurrence of indebtedness to fund the acquisition; |

• | the potential issuance of common stock for some or all of the purchase price, which could dilute ownership interests of our current Share Owners; |

• | the acquired business not achieving anticipated revenues, earnings, cash flow, or market share; |

• | excess capacity; |

• | the assumption of undisclosed liabilities; and |

• | dilution of earnings. |

If efforts to introduce new products are not successful, this could limit sales growth or cause sales to decline. We regularly introduce new products to keep pace with workplace trends and evolving regulatory and industry requirements, including environmental, health, and safety standards such as sustainability and ergonomic considerations, and similar standards for the workplace and for product performance. Shifts in workforce demographics, working styles, and technology may impact the types of office furniture products purchased by our customers as smaller and more collaborative workstations gain popularity. The introduction of new products requires the coordination of the design, manufacturing, and marketing of such products. The design and engineering required for certain new products can take an extended period of time, and further time may be required to achieve customer acceptance. Accordingly, the launch of any particular product may be delayed or may be less successful than we originally anticipated. Difficulties or delays in introducing new products or lack of customer acceptance of new products could limit sales growth or cause sales to decline.

If customers do not perceive our products and services to be innovative and of high quality, our brand and name recognition and reputation could suffer. We believe that establishing and maintaining good brand and name recognition and a good reputation is critical to our business. Promotion and enhancement of our name and brands will depend on the effectiveness of marketing and advertising efforts and on successfully providing innovative and high quality products and superior services. If customers do not perceive our products and services to be innovative and of high quality, our reputation, brand and name recognition could suffer, which could have a material adverse effect on our business.

A loss of independent manufacturing representatives, dealers, or other sales channels could lead to a decline in sales. Our office furniture is marketed primarily through Company salespersons to end users, office furniture dealers, wholesalers, rental companies, and catalog houses. Our hospitality furniture is marketed to end users using independent manufacturing representatives. A significant loss within any of these sales channels could result in a sales decline and thus have an adverse impact on our financial position, results of operations, or cash flows.

Failure to effectively manage working capital may adversely affect our cash flow from operations. We closely monitor inventory and receivable efficiencies and continuously strive to improve these measures of working capital, but customer

10

financial difficulties, cancellation or delay of customer orders, transfers of production among our manufacturing facilities, or manufacturing delays could adversely affect our cash flow from operations.

We may not be able to achieve maximum utilization of our manufacturing capacity. Fluctuations and deferrals of customer orders may have a material adverse effect on our ability to utilize our fixed capacity and thus negatively impact our operating margins.

We could incur losses due to asset impairment. As business conditions change, we must continually evaluate and work toward the optimum asset base. It is possible that certain assets such as, but not limited to, facilities, equipment, or intangible assets, could be impaired at some point in the future depending on changing business conditions. Such impairment could have an adverse impact on our financial position and results of operations.

Fluctuations in our effective tax rate could have a significant impact on our financial position, results of operations, or cash flows. We are subject to income taxes as well as non-income based taxes, mainly in the United States. Judgment is required in determining the worldwide provision for income taxes, other tax liabilities, interest, and penalties. Future events could change management's assessment. We operate within multiple taxing jurisdictions and are subject to tax audits in these jurisdictions. These audits can involve complex issues, which may require an extended period of time to resolve. We have also made assumptions about the realization of deferred tax assets. Changes in these assumptions could result in a valuation allowance for these assets. Final determination of tax audits or tax disputes may be different from what is currently reflected by our income tax provisions and accruals.

A failure to comply with the financial covenants under the Company's $30 million credit facility could adversely impact the Company. Our credit facility requires the Company to comply with certain financial covenants. We believe the most significant covenants under this credit facility are the adjusted leverage ratio and the fixed charge coverage ratio. More detail on these financial covenants is discussed in Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations. As of June 30, 2015, we had no short-term borrowings under this credit facility and had total cash and cash equivalents of $34.7 million. In the future, a default on the financial covenants under our credit facility could cause an increase in the borrowing rates or could make it more difficult for us to secure future financing which could adversely affect the financial condition of the Company.

Our business may be harmed due to failure to successfully implement information technology solutions or a lack of reasonable safeguards to maintain data security. Our business depends on effective information technology systems which also are intended to minimize the risk of a security breach or cybersecurity threat, including the misappropriation of assets or other sensitive information, or data corruption which could cause operational disruption. Information systems require an ongoing commitment of significant resources to maintain and enhance existing systems and develop new systems in order to keep pace with changes in information processing technology and evolving industry standards. Implementation delays, poor execution, or a breach of information technology systems could disrupt our operations, damage our reputation, or increase costs related to the mitigation of, response to, or litigation arising from any such issue.

Failure to protect our intellectual property could undermine our competitive position. We attempt to protect our intellectual property rights, both in the United States and in foreign countries, through a combination of patent, trademark, copyright, and trade secret laws, as well as licensing agreements and third-party non-disclosure and assignment agreements. Because of the differences in foreign laws concerning proprietary rights, our intellectual property rights do not generally receive the same degree of protection in foreign countries as they do in the United States, and therefore in some parts of the world, we have limited protections, if any, for our intellectual property. Competing effectively depends, to a significant extent, on maintaining the proprietary nature of our intellectual property. The degree of protection offered by the claims of the various patents and trademarks may not be broad enough to provide significant proprietary protection or competitive advantages to the Company, and patents or trademarks may not be issued on pending or contemplated applications. In addition, not all of our products are covered by patents. It is also possible that our patents and trademarks may be challenged, invalidated, canceled, narrowed, or circumvented.

We may be sued by third parties for alleged infringement of their intellectual property rights and incur substantial litigation or other costs. We could be notified of a claim regarding intellectual property rights which could lead us to spend time and money to defend or address the claim. Even if the claim is without merit, it could result in substantial costs and diversion of resources.

Our insurance may not adequately protect us from liabilities related to product defects. We maintain product liability and other insurance coverage that we believe to be generally in accordance with industry practices, but our insurance coverage does not extend to field visits to repair, retrofit or replace defective products, or to product recalls. As a result, our insurance coverage may not be adequate to protect us fully against substantial claims and costs that may arise from liabilities related to product defects, particularly if we have a large number of defective products that we must repair, retrofit, replace, or recall.

11

We are subject to extensive environmental regulation and significant potential environmental liabilities. Our past and present operation and ownership of manufacturing plants and real property are subject to extensive and changing federal, state, local, and foreign environmental laws and regulations, including those relating to discharges in air, water, and land, the handling and disposal of solid and hazardous waste, and the remediation of contamination associated with releases of hazardous substances. In addition, the increased prevalence of global climate issues may result in new regulations that may negatively impact us. We cannot predict what environmental legislation or regulations will be enacted in the future, how existing or future laws or regulations will be administered or interpreted or what environmental conditions may be found to exist. Compliance with more stringent laws or regulations, or stricter interpretation of existing laws, may require additional expenditures, some of which could be material. In addition, any investigations or remedial efforts relating to environmental matters could involve material costs or otherwise result in material liabilities.

Our success will continue to depend to a significant extent on our key personnel. We depend significantly on our executive officers and other key personnel. The unexpected loss of the services of any of our executive officers or other key personnel would have an adverse effect on us.

Our failure to retain the existing management team, maintain our engineering, technical, and manufacturing process expertise, or continue to attract qualified personnel could adversely affect our business. Our success is dependent on keeping pace with technological advancements and adapting services to provide manufacturing capabilities which meet customers' changing needs. In addition, we must retain our qualified engineering and technical personnel and successfully anticipate and respond to technological changes in a cost effective and timely manner. Our culture and guiding principles focus on continuous training, motivating, and development of employees, and we strive to attract, motivate, and retain qualified personnel. Failure to retain and attract qualified personnel could adversely affect our business.

Turnover in personnel could cause manufacturing inefficiencies. The demand for manufacturing labor in certain geographic areas makes retaining experienced production employees difficult. Turnover could result in additional training and inefficiencies that could impact our operating results.

Natural disasters or other catastrophic events may impact our production schedules and, in turn, negatively impact profitability. Natural disasters or other catastrophic events, including severe weather, terrorist attacks, power interruptions, and fires, could disrupt operations and likewise our ability to produce or deliver products. Our manufacturing operations require significant amounts of energy, including natural gas and oil, and governmental regulations may control the allocation of such fuels. Employees are an integral part of our business and events such as a pandemic could reduce the availability of employees reporting for work. In the event we experience a temporary or permanent interruption in our ability to produce or deliver product, revenues could be reduced, and business could be materially adversely affected. In addition, catastrophic events, or the threat thereof, can adversely affect U.S. and world economies, and could result in delayed or lost sales of our products. In addition, any continuing disruption in our computer system could adversely affect the ability to receive and process customer orders, manufacture products, and ship products on a timely basis, and could adversely affect relations with customers, potentially resulting in reduction in orders from customers or loss of customers. We maintain insurance to help protect us from costs relating to some of these matters, but such may not be sufficient or paid in a timely manner to us in the event of such an interruption.

Imposition of government regulations may significantly increase our operating costs in the United States and abroad. Legislative and regulatory reforms by the U.S. federal and foreign governments could significantly impact our profitability by burdening us with forced cost choices that cannot be recovered by increased pricing. For example:

• | We import a portion of our wooden furniture products and are thus subject to an antidumping tariff on wooden bedroom furniture supplied from China. The tariffs are subject to review and could result in retroactive and prospective tariff rate increases which could have an adverse impact on our financial condition, results of operations, or cash flows. |

• | Foreign regulations are increasing in many areas such as data privacy, hazardous waste disposal, labor relations and employment practices. Compliance with these regulations could have an adverse impact on our financial condition, results of operations, or cash flows. |

Provisions of the Dodd-Frank Act relating to “Conflict Minerals” may increase our costs and reduce our sales levels. The Dodd-Frank Wall Street Reform and Consumer Protection Act contains provisions to improve transparency and accountability concerning the supply of certain minerals originating from the Democratic Republic of Congo (“DRC”) and adjoining countries that are believed to benefit armed groups. As a result, the SEC has adopted due diligence, disclosure, and reporting requirements for companies which manufacture products that include components containing such minerals, regardless of whether the minerals are actually mined in the DRC or adjoining countries. We have determined that certain of our products contain such specified minerals, and we have developed a process to comply with the SEC regulations. Such

12

regulations could decrease the availability and increase the prices of components used in our products, particularly if we choose (or are required by our customers) to source such components from different suppliers than we use now. In addition, as our supply chain is complex and the process to comply with the SEC rules is cumbersome, the ongoing compliance process is both time-consuming and costly. We may face reduced sales if we are unable to timely verify the origins of minerals contained in the components included in our products.

The value of our common stock may experience substantial fluctuations for reasons over which we may have little control. The value of common stock could fluctuate substantially based on a variety of factors, including, among others:

• | actual or anticipated fluctuations in operating results; |

• | announcements concerning our Company, competitors, or industry; |

• | overall volatility of the stock market; |

• | changes in the financial estimates of securities analysts or investors regarding our Company, the industry, or competitors; and |

• | general market or economic conditions. |

Furthermore, stock prices for many companies fluctuate widely for reasons that may be unrelated to their operating results. These fluctuations, coupled with changes in results of operations and general economic, political, and market conditions, may adversely affect the value of our Company's common stock.

Item 1B - Unresolved Staff Comments

None.

Item 2 - Properties

The location and number of our major manufacturing, warehousing, and service facilities, including our executive and administrative offices, as of June 30, 2015, are as follows:

Number of Facilities | ||

North America | ||

Idaho | 1 | |

Indiana | 16 | |

Kentucky | 2 | |

Virginia | 1 | |

Asia | ||

China | 1 | |

Vietnam | 1 | |

Total Facilities | 22 | |

The listed facilities occupy approximately 3,770,000 square feet in aggregate, of which approximately 3,653,000 square feet are owned and 117,000 square feet are leased.

Generally, properties are utilized at normal capacity levels on a multiple shift basis. At times, certain facilities utilize a reduced second or third shift. Due to sales fluctuations, not all facilities were utilized at normal capacity during fiscal year 2015. We continually assess our capacity needs and evaluate our operations to optimize our service levels by geographic region.

Significant loss of income resulting from a facility catastrophe would be partially offset by business interruption insurance coverage.

Operating leases for all facilities and related land, including twelve leased office furniture showroom facilities which are not included in the tables above, total 204,000 square feet and expire from fiscal year 2016 to 2026 with many of the leases subject to renewal options. The leased showroom facilities are in six states and the District of Columbia. See Note 5 - Commitments and Contingent Liabilities of Notes to Consolidated Financial Statements for additional information concerning leases.

We own approximately 400 acres of land which includes land where various facilities reside, including approximately 155 acres of land in the Kimball Industrial Park, Jasper, Indiana (a site for certain production and other facilities, and for possible future expansions).

13

Item 3 - Legal Proceedings

We and our subsidiaries are not parties to any pending legal proceedings, other than ordinary routine litigation incidental to the business. The outcome of current routine pending litigation, individually and in the aggregate, is not expected to have a material adverse impact.

Item 4 - Mine Safety Disclosures

Not applicable.

Executive Officers of the Registrant

Our executive officers as of August 26, 2015 are as follows:

(Age as of August 26, 2015)

Name | Age | Office and Area of Responsibility | Executive Officer Since Calendar Year | |||

Robert F. Schneider | 54 | Chairman of the Board, Chief Executive Officer | 1992 | |||

Donald W. Van Winkle | 54 | President, Chief Operating Officer | 2010 | |||

Michelle R. Schroeder | 50 | Vice President, Chief Financial Officer | 2003 | |||

Kevin D. McCoy | 44 | Vice President; President, National Office Furniture | 2014 | |||

Michael S. Wagner | 43 | Vice President; President, Kimball Office | 2014 | |||

R. Gregory Kincer | 57 | Vice President, Corporate Development | 2014 | |||

Julia E. Heitz Cassidy | 50 | Vice President, General Counsel and Secretary | 2014 | |||

Lonnie P. Nicholson | 51 | Vice President, Chief Administrative Officer | 2014 | |||

Executive officers are elected annually by the Board of Directors.

Mr. Schneider was appointed Chairman of the Board, Chief Executive Officer in November 2014 and was appointed to our Board of Directors in February 2014. He led the Kimball Hospitality subsidiary in 2013 and 2014, and was Executive Vice President, Chief Financial Officer (“CFO”) from July 1997 to November 2014. He has been with the Company for 27 years in various financial and executive positions. As leader of Kimball Hospitality, he oversaw the business as it returned to profitability in fiscal year 2014. He was also responsible for strategic planning, SEC reporting, finance, capital structure, insurance, tax, internal audit, and treasury services as CFO of your Company.

Mr. Van Winkle was appointed President, Chief Operating Officer in November 2014. He previously served as Executive Vice President, President — Furniture Group since March 2014. He also served as Vice President, President — Office Furniture Group from February 2010 until November 2013 when he was appointed Executive Vice President, President — Office Furniture Group. He had previously served as Vice President, General Manager of National Office Furniture from October 2003 until February 2010, and prior to that served as Vice President, Chief Finance and Administrative Officer for the Furniture Brands Group as well as other key finance roles within our Furniture business since joining the Company in January 1991.

Ms. Schroeder was appointed Vice President, CFO in November 2014. She previously served as Vice President and Chief Accounting Officer, a position she assumed in May 2009. She was appointed to Vice President in December 2004, served as Corporate Controller from August 2002 until May 2009, and prior to that served as Assistant Corporate Controller and Director of Financial Analysis. As CFO, Ms. Schroeder has responsibility for the accounting, internal audit, investor relations, tax and treasury functions, as well as setting financial strategy and policies for the Company.

Mr. McCoy was appointed President, National Office Furniture in November 2014 and was also appointed to Vice President, Kimball International, Inc. in February 2015. Previously, he served as Vice President, General Manager of National Office Furniture, a position he assumed in 2010. He joined Kimball in 1996 and spent nine years with National and Kimball Office, building a solid background in both front line and management sales experience. He became Vice President of Sales for National Office Furniture in 2005 with responsibility for the field sales organization, distribution strategy and execution, and the achievement of National’s profitable growth goals.

Mr. Wagner was appointed President, Kimball Office in November 2014 and was also appointed to Vice President, Kimball International, Inc. in February 2015. He previously served as Vice President, General Manager of Kimball Office. Since joining Kimball in October 2013, Mr. Wagner has led the extensive sales growth and aggressive cost reductions at Kimball Office. Prior to joining Kimball, he most recently served as Senior Vice President of Sales and Marketing with OFS Brands (an office

14

furniture manufacturing company) since 2004. His career spans over 20 years of experience in the office furniture industry with leadership positions in sales, sales management, marketing, and strategic planning.

Mr. Kincer was appointed Vice President, Corporate Development in November 2014. Since 2006, he served as Vice President, Business Development, Treasurer with responsibility for global treasury operations managing Company-wide liquidity, commercial banking relationships, corporate debt facilities, foreign exchange risk, and insurance programs as well as the evaluation of acquisition opportunities. He also served in various finance and leadership roles of progressing responsibility since joining the Company in 1994.

Ms. Heitz Cassidy was appointed Vice President, General Counsel and Secretary in November 2014. She provides strategic-thinking leadership, advice and counsel to the Company’s executive management as well as oversees the Company’s legal functions, and as Corporate Secretary, assists the Board of Directors. She previously served as Deputy General Counsel since August 2009, with responsibility for handling all day-to-day legal activities of the Company and was appointed to Vice President in October 2013. She joined Kimball in 1996 as an associate corporate counsel and has held positions of increasing responsibility within the legal department during her career.

Mr. Nicholson was appointed Vice President, Chief Administrative Officer in February 2015. He also served as Vice President, Chief Information Officer from January 2014 until March 2015. Throughout 2013 he served as Director, Business Analytics and then Vice President, Business Analytics, with oversight of strategic application of data analysis, social media and mobile computing in support of the Company's growth of information management into more predictive analysis in order to build greater responsiveness to customer needs and improvement of operational decision making. He also served as Director of Organizational Development from November 2011 until January 2013, and Director of Employee Engagement from November 2008 until November 2011 following other roles of advancing responsibility in the areas of application development, systems analysis, process reengineering, lean/continuous improvement and enterprise resource planning (“ERP”) since joining the Company in 1986.

15

PART II

Item 5 - Market for Registrant's Common Equity, Related Share Owner Matters and Issuer Purchases of Equity Securities

Market Prices

The Company's Class B Common Stock trades on the NASDAQ Global Select Market of The NASDAQ Stock Market LLC under the symbol: KBAL. High and low sales prices by quarter for the last two fiscal years as quoted by the NASDAQ system were as follows:

2015 | 2014 | ||||||||||||||

High | Low | High | Low | ||||||||||||

First Quarter | $ | 17.95 | $ | 14.15 | $ | 12.00 | $ | 9.61 | |||||||

Second Quarter | $ | 15.39 | $ | 10.20 | |||||||||||

Second Quarter — Prior to Spin-Off | $ | 18.70 | $ | 14.56 | |||||||||||

Second Quarter — After Spin-Off | $ | 13.85 | $ | 8.38 | |||||||||||

Third Quarter | $ | 10.75 | $ | 8.51 | $ | 20.10 | $ | 13.60 | |||||||

Fourth Quarter | $ | 12.83 | $ | 10.01 | $ | 18.97 | $ | 15.35 | |||||||

On October 31, 2014 (“Distribution Date”), we completed the spin-off of our EMS segment by distributing the related shares of Kimball Electronics, Inc., on a pro rata basis, to the Company's Share Owners of record as of October 22, 2014 (“the Record Date”). On the Distribution Date, each of the Company's Share Owners received three shares of Kimball Electronics for every four shares of the Company held by such Share Owner on the Record Date. After the Distribution Date, the Company does not beneficially own any Kimball Electronics shares and Kimball Electronics is an independent publicly traded company. Kimball International, Inc. trades on the NASDAQ under the ticker symbol “KBAL” and Kimball Electronics, Inc. trades on the NASDAQ under the ticker symbol “KE”. Prior to the Distribution Date, the Company's Class B Common Stock traded under the symbol: KBALB. On the Distribution Date, the closing price of our Class B Common Stock was $17.98 per share. After the Distribution Date, on a 30-day volume weighted average price basis to eliminate the impact of stock price volatility immediately after Distribution Date, the average price of our Common Stock was $9.89 per share and the average price of Kimball Electronics common stock was $10.32 per share, which equates to a split-adjusted price of $7.74.

There is no established public trading market for the Company's Class A Common Stock. However, Class A shares are convertible on a one-for-one basis to Class B shares.

Dividends

As a result of the stock unification which occurred on October 30, 2014 as described in Note 10 - Common Stock, Class A Common Stock and Class B Common Stock now vote as a single class on all matters submitted to a vote of the Company’s Share Owners. Prior to the October 30, 2014 stock unification, on a fiscal year basis, shares of Class B Common Stock were entitled to $0.02 per share dividend more than the annual dividends paid on Class A Common Stock, provided that dividends were paid on the Company's Class A Common Stock.

Dividends declared totaled $7.7 million and $7.5 million for fiscal years 2015 and 2014, respectively. Included in the fiscal year 2015 figure are dividends computed and accrued on unvested restricted share units. Dividends on these restricted share units accumulate and, when the restricted share units vest, are paid in shares of Common Stock, with the number of shares determined based on the closing price of our Common Stock on the vesting date. Dividends per share declared by quarter for fiscal year 2015 compared to fiscal year 2014 were as follows:

2015 | 2014 | ||||||||||||||

Class A | Class B | Class A | Class B | ||||||||||||

First Quarter | $ | 0.045 | $ | 0.05 | $ | 0.045 | $ | 0.05 | |||||||

Second Quarter | 0.05 | 0.05 | 0.045 | 0.05 | |||||||||||

Third Quarter | 0.05 | 0.05 | 0.045 | 0.05 | |||||||||||

Fourth Quarter | 0.05 | 0.05 | 0.045 | 0.05 | |||||||||||

Total Dividends | $ | 0.195 | $ | 0.20 | $ | 0.180 | $ | 0.20 | |||||||

During the first quarter of fiscal year 2016, a quarterly dividend of $0.055 per share was declared for all outstanding shares of common stock payable October 15, 2015 to Share Owners of record on September 25, 2015. This dividend is a 10% increase over the previous quarter dividend.

16

Share Owners

On August 17, 2015, the Company's Class A Common Stock was owned by 124 Share Owners of record, and the Company's Class B Common Stock was owned by 1,436 Share Owners of record, of which 63 also owned Class A Common Stock.

Securities Authorized for Issuance Under Equity Compensation Plans

The information required by this item concerning securities authorized for issuance under equity compensation plans is incorporated by reference to Item 12 - Security Ownership of Certain Beneficial Owners and Management and Related Share Owner Matters of Part III.

Issuer Purchases of Equity Securities

A share repurchase program authorized by the Board of Directors was announced on October 16, 2007. The program allows for the repurchase of up to two million shares of common stock and will remain in effect until all shares authorized have been repurchased. At June 30, 2015, 1.0 million shares remained available under the repurchase program.

During fiscal 2015, we repurchased 1.0 million shares of our common stock. The following table presents a summary of share repurchases made by the Company during the fourth quarter of fiscal year 2015:

Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||

Month #1 (April 1 - April 30, 2015) | — | $ | — | — | 1,684,090 | |||||||

Month #2 (May 1 - May 31, 2015) | 254,893 | $ | 12.08 | 254,893 | 1,429,197 | |||||||

Month #3 (June 1 - June 30, 2015) | 420,114 | $ | 12.23 | 420,114 | 1,009,083 | |||||||

Total | 675,007 | $ | 12.18 | 675,007 | ||||||||

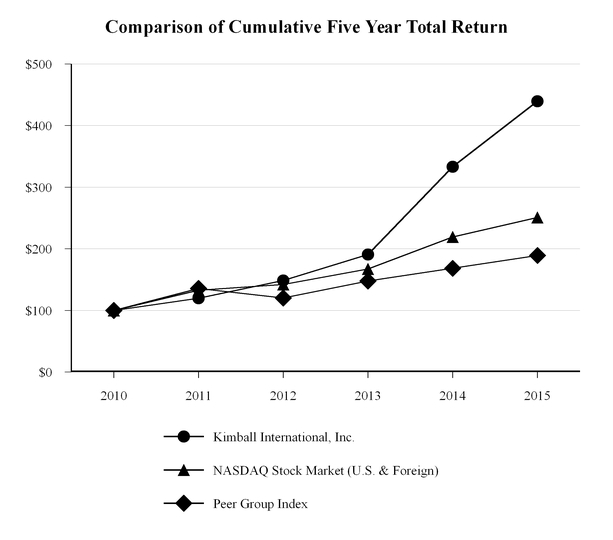

Performance Graph

The following performance graph is not deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C under the Exchange Act or to the liabilities of Section 18 of the Exchange Act and will not be deemed to be incorporated by reference into any filing under the Securities Act or the Exchange Act, except to the extent we specifically incorporate it by reference into such a filing.

The graph below compares the cumulative total return to Share Owners of our common stock from June 30, 2010 through June 30, 2015, the last business day in the respective fiscal years, to the cumulative total return of the NASDAQ Stock Market (U.S. and Foreign) and a peer group index for the same period of time.

The spin-off of Kimball Electronics is reflected as an increase in the total cumulative return to Share Owners as a result of each Share Owner receiving a distribution of three shares of Kimball Electronics for every four shares of the Company. The increase in the total cumulative return was calculated based on the value of Kimball Electronics stock, using a 30-day volume weighted average price calculation to eliminate the impact of stock price volatility immediately after the October 31, 2014 spin-off date.

Due to the diversity of our operations prior to the spin-off date, we are not aware of any public companies that are directly comparable. Therefore, the peer group index is comprised of publicly traded companies in both the furniture industry and in our former EMS segment, as follows:

Furniture peers: HNI Corporation, Knoll, Inc., Steelcase Inc., Herman Miller, Inc.

EMS peers (applicable through the October 31, 2014 spin-off): Benchmark Electronics, Inc., Jabil Circuit, Inc., Plexus Corp.

In order to reflect the segment allocation of Kimball International, Inc. prior to the October 31, 2014 spin-off date, a market capitalization-weighted index was first computed for each peer group, then a composite peer group index was calculated based on each segment's proportion of net sales to total consolidated sales for fiscal years 2010 through 2014 and for fiscal year 2015 through the October 31, 2014 spin-off date. After the spin-off date, only the Furniture peer companies were used in the capitalization-weighted peer group index. The public companies included in the peer groups have a larger revenue base than each of our business segments.

17

The graph assumes $100 is invested in our common stock and each of the two indexes at the closing market quotations on June 30, 2010, and that dividends and the Kimball Electronics spin-off stock distribution are reinvested. The performances shown on the graph are not necessarily indicative of future price performance.

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |||||||||||||

Kimball International, Inc. | $ | 100.00 | $ | 119.89 | $ | 148.50 | $ | 190.85 | $ | 333.13 | $ | 439.63 | ||||||

NASDAQ Stock Market (U.S. & Foreign) | $ | 100.00 | $ | 132.73 | $ | 142.01 | $ | 167.01 | $ | 219.06 | $ | 250.68 | ||||||

Peer Group Index | $ | 100.00 | $ | 135.39 | $ | 119.99 | $ | 147.78 | $ | 168.23 | $ | 188.99 | ||||||

18

Item 6 - Selected Financial Data

This information should be read in conjunction with Item 8 - Financial Statements and Supplementary Data and Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations.

Year Ended June 30 | |||||||||||||||||||

(Amounts in Thousands, Except for Per Share Data) | 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||

Net Sales | $ | 600,868 | $ | 543,817 | $ | 500,005 | $ | 525,310 | $ | 481,178 | |||||||||

Income (Loss) from Continuing Operations | $ | 11,143 | $ | 3,419 | $ | (6,616 | ) | $ | 1,749 | $ | (3,180 | ) | |||||||

Earnings (Loss) Per Share from Continuing Operations: | |||||||||||||||||||

Basic: | |||||||||||||||||||

Class A | $ | 0.25 | $ | 0.07 | $ | (0.20 | ) | $ | 0.03 | $ | (0.10 | ) | |||||||

Class B | $ | 0.29 | $ | 0.09 | $ | (0.17 | ) | $ | 0.05 | $ | (0.08 | ) | |||||||

Diluted: | |||||||||||||||||||

Class A | $ | 0.25 | $ | 0.07 | $ | (0.20 | ) | $ | 0.03 | $ | (0.10 | ) | |||||||

Class B | $ | 0.29 | $ | 0.09 | $ | (0.17 | ) | $ | 0.05 | $ | (0.08 | ) | |||||||

Total Assets | $ | 266,129 | $ | 722,146 | $ | 644,519 | $ | 595,516 | $ | 626,312 | |||||||||

Long-Term Debt, Less Current Maturities | $ | 241 | $ | 268 | $ | 294 | $ | 273 | $ | 286 | |||||||||

Cash Dividends Per Share: | |||||||||||||||||||

Class A | $ | 0.195 | $ | 0.18 | $ | 0.18 | $ | 0.18 | $ | 0.18 | |||||||||

Class B | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | $ | 0.20 | |||||||||

The preceding table excludes all income statement activity of the discontinued operations. The balance sheet data in the preceding table includes the EMS segment for fiscal years prior to 2015.

Fiscal year 2015 income from continuing operations included $3.2 million ($0.08 per diluted share) of after-tax restructuring expenses and $3.2 million ($0.08 per diluted share) of after-tax expense related to the spin-off.

Fiscal year 2014 income from continuing operations included an after-tax gain of $1.1 million ($0.03 per diluted share) for the sale of an idle Furniture segment manufacturing facility and land located in Jasper, Indiana, after-tax impairment of $0.7 million ($0.02 per diluted share) for an aircraft which was subsequently sold, and $1.4 million ($0.04 per diluted share) of after-tax expense related to the spin-off.